Optimal consumption and investment under transaction costs

Abstract.

In this article we consider the Merton problem in a market with a single risky asset and transaction costs. We give a complete solution of the problem up to the solution of a free-boundary problem for a first-order differential equation, and find that the form of the solution (whether the problem is well-posed, whether the problem is well-posed only for large transaction costs, whether the no-transaction wedge lies in the first, second or fourth quadrants) depends only on a quadratic whose co-efficients are functions of the parameters of the problem, and then only through the value and slope of this quadratic at zero, one and the turning point.

We find that for some parameter values and for large transaction costs the location of the boundary at which sales of the risky asset occur is independent of the transaction cost on purchases. We give both a mathematical and financial reason for this phenomena.

Alex Tse: Cambridge Endowment for Research in Finance, Judge Business School, University of Cambridge, Cambridge, CB2 1AG, UK. S.Tse@jbs.cam.ac.uk;

Yeqi Zhu: Credit Suisse, London, UK. (The opinions expressed in the paper are those of the author and not of Credit Suisse.) Yeqi.Zhu@credit-suisse.com

1. Introduction

In this article we consider the problem of maximising expected utility of consumption over the infinite horizon in a financial market consisting of a riskless bond and a single risky asset. Merton [9, 10] considered this problem in a perfect, frictionless market and showed that the optimal strategy is to keep a constant fraction of wealth in the risky asset. Of the possible market frictions, arguably the most significant is transaction costs. This paper adds to the growing literature on optimal consumption/investment problems with proportional transaction costs.

In the Merton setting the market is complete. Constantinides and Magill [3] generalised the problem to the incomplete case by introducing transaction costs. They argued that in the case of a single risky asset following exponential Brownian motion and power utility the scalings of the problem should mean that there is a no-transaction wedge, and the optimal strategy should be to trade in a minimal fashion so as to keep the fraction of wealth in the risky asset within an interval . If the initial portfolio is such that the initial fraction of wealth in the risky asset is outside this interval then the agent makes an instantaneous transaction to bring the fraction of wealth in the risky asset to the closest boundary of . Thereafter, the agent only trades when this fraction is on the boundary of . In space, the interval becomes a no-transaction wedge.

The model and accompanying intuition was formulated precisely by Davis and Norman [4]. They used the language of stochastic control and martingales to give a rigorous description of the problem for power utility. For a certain subset of parameter combinations they gave a full description of the solution, specifying both the optimal consumption, and the optimal investment strategy. The optimal investment strategy involves a process which receives a local-time push at both boundaries of an interval, and these pushes are just sufficient to keep the process within the interval. Davis and Norman [4] reduce the problem to solving a pair of first-order ordinary differential equations (ODEs) subject to value matching conditions at unknown free-boundaries. Their analysis was extended by Shreve and Soner [11] to a larger class of parameter combinations using methodologies from viscosity solutions.

Both [4] and [11] consider the value function and the primal problem. Recently, there have been a trio of papers considering the dual problem and shadow prices. Kallsen and Muhle-Karbe [8] were the first to use the shadow-price approach in this context, but only consider logarithmic utility. Herczegh and Prokaj [6] extend their results to power utility. The most complete treatment of the problem via the shadow-price approach is the paper of Choi et al [1]. Choi et al give a full analysis of the problem, covering all parameter combinations (which involve an appreciating risky asset). They reduce the problem to the solution of a free-boundary problem for a single first-order ODE. There are multiple solutions to this free-boundary problem, and the one that is wanted is the one for which the solution to the free-boundary problem satisfies an integral condition.

In this paper we revisit the problem considered by [4, 11, 1, 6]. The fundamental difference between this paper and Choi et al [1] is that we take the primal approach. We show that the problem of constructing the value function can be transformed into finding the solution of a first-order free-boundary problem, subject to an integral condition, as in Choi et al [1]. The advance relative to [1] is that it is much easier to understand the character of the solutions to our differential equation, when compared to that of Choi et al: for our solution the possible behaviours correspond to the possible shapes of a simple quadratic, whereas in Choi et al it is necessary to consider a phase-diagram in which the behaviours depend on a pair of ellipses and/or hyperbolas. Although the two free-boundary problems must be transformations of each other, our solution leads to a simpler problem. Most especially, we can give a direct interpretation of the free-boundary points as the sale and purchase boundaries of the no-transaction wedge and we can prove comparative statics for these boundaries. In the conclusion we will expand on this remark and give further evidence of the benefits of our approach. Nonetheless, many features of our characterising ODE are to be found in the characterising ODE of [1]; in particular in both cases the ODE has a singular point, and for some parameter combinations, though not all, the solution we want passes through this singular point.

The remainder of this paper is structured as follows. In the next section we formulate the problem and discuss how to express the solution in terms of the solution of a first-order ODE. The Hamilton-Jacobi-Bellman equation is second-order, so the key step is an order-reduction in which we make the solution of the equation the independent variable. (This order reductiion technique has been used before in investment/sale problems by Evans et al [5]. Choi et al [1, Section 3.3] make a similar transformation, and this may be one reason why they make more progress than [6].) In Section 2 we do this in the case where it is never optimal for the agent to have negative cash wealth (equivalently never optimal to borrow against holdings of the risky asset), and hence we can use cash wealth as the denominator of an autonomous univariate process which is the ratio of wealth in the risky asset to cash wealth.

In Section 3 we show how the arguments can be extended to the general case. We can no longer use cash wealth as the denominator in the definition of our autonomous univariate process. Instead we use paper wealth (where paper wealth is defined by assuming liquidation is possible with zero transaction costs) as the denominator and consider as key variable the ratio of wealth in the risky asset to paper wealth. At first sight, it looks as if this makes the order-reduction impossible, but inspired by the results of Section 2 we how the problem may be reduced to the identical free-boundary problem as in that section.

In Section 4 we show how the solution to the free-boundary problem depends on a simple quadratic, the co-efficients of which depend on the parameters of the problem. There are several cases depending only on the values and slopes of this quadratic at zero and one, and on the value of the quadratic at the turning point. We can give exact conditions which determine when the problem is well-posed. This main result is stated and proved in Section 5 and mirrors the main result of Choi et al [1], but our formulation is an improvement in the sense that we cover an extra case and we give an algebraic expression for a quantity that Choi et al can only express as an integral.

In Section 6 we consider how the boundaries of the no-transaction wedge depend on the parameters. Analysis of this type seems to be new, and would be difficult under previous approaches. More especially, we show that if the drift is small, then the no-transaction wedge includes the Merton line, and the no-transaction wedge gets larger as transaction costs increase. However, if the drift increases further, then we may loose both the monotonicity property of the no-transaction wedge, and the property that the Merton line (corresponding to zero transaction costs) lies within the no-transaction region. Remarkably, although in general the locations of both the sale and purchase boundaries depend on the transaction costs on both sale and purchases, in some circumstances the sale boundary is independent of the transaction cost on purchases.

Section 7 concludes. Some results, including those on the solution of the ODE are given in an Appendix.

2. Problem specification and a motivating special case

Let denote the price of a risky asset and suppose is an exponential Brownian motion with drift and volatility ; then where is a Brownian motion. Let denote the consumption rate of the individual and let denote the number of units of the risky asset held by the investor. We assume that is non-negative and progressively measurable and that is of finite variation; in particular where and are increasing, adapted, càdlàg processes with representing purchases and sales of the risky asset respectively.

Suppose cash wealth is right-continuous and evolves according to

| (2.1) |

Here represents the transaction cost paid on purchases and represents the transaction cost paid on sales. We assume , else we are in the case of no transaction costs.

We say that a wealth portfolio is solvent at time if

or equivalently if instantaneous liquidation of the risky position yields a cash wealth which is non-negative. A consumption/investment strategy is solvent from time if the resulting wealth portfolio process is solvent for each . Write for the set of strategies which are solvent from time when .

The objective of the agent is to maximise the discounted expected utility of consumption over the infinite horizon, where the discount factor is and the utility function of the agent is assumed to have constant relative risk aversion with risk aversion co-efficient . The maximisation takes place over the set of consumption/investment strategies which are solvent from time zero. In particular, the goal is to find

| (2.2) |

Since the set-up has a Markovian structure, we expect the value function, optimal consumption and optimal portfolio strategy to be functions of the current wealth portfolio of the agent and of the price of the risky asset. Let be the forward starting value function for the problem so that

| (2.3) |

The goal is to solve for the value function . Note that it is the value of the holdings of the risky asset which is important rather than the price level and quantity individually, and in most circumstances and appear as the product . From the scalings of the problem we expect that we can write

| (2.4) |

where the key variable is the ratio of wealth held in the risky asset to cash wealth.

The intuitive arguments of Constantinides and Magill [3] and the concrete results of Davis and Norman [4] lead us to expect that the no-transaction region will be a wedge. For the purposes of this section we suppose that this wedge is contained in the first quadrant of space. Define by . We expect that the agent trades to keep in the interval where the pair of constants is to be determined. Then for initial values the optimal sale strategy includes an immediate sale to bring the ratio of risky wealth to cash wealth below . Thus, if the initial portfolio is such that then we sell units of the risky asset, where so that

This initial transaction at should not change the value function, and hence for ,

or equivalently for where the constant is given by .

If initial wealth is such that then the optimal strategy includes the immediate purchase of risky asset. We purchase units of where so that

Then for , where .

Let be given by

Then we expect will be a supermartingale in general and a martingale under the optimal strategy. Applying Itô’s formula, and optimising over and we obtain the Hamilton-Jacobi-Bellman equation which is a (second order, semi-linear) differential equation for in the no-transaction region: for

| (2.5) |

Finally, we expect that there will be value matching and second-order smooth fit at the free boundary.

In analysing the problem our first goal is to solve (2.5). The equation can be simplified by setting and . (If then we can construct a parallel argument based on .) Then solves a (second-order, non-linear) autonomous equation (with no -dependence):

| (2.6) |

where and . The order of this equation can be reduced by setting so that . We find that

| (2.7) |

Various further transformations do not reduce the order of the problem, but rather simplify the problem in appearance, and add to our ability to interpret the solution. Set , let be inverse to so that and finally set . Then solves

| (2.8) |

where

| (2.9) |

and and are the quadratic functions

| (2.10) | |||||

| (2.11) |

It will turn out that the different solution regimes can be characterised by the quadratic and more especially, the derivatives of at 0 and 1 and the values of at 1 and at the turning point. To this end let be the location of the turning point, and let be the value of at the turning point.

The advantage of switching to becomes apparent when we consider the solution outside the no-transaction region. For , for to be determined. Then using the same transformations we find and

| (2.12) |

so that , and which is a constant. Similarly, on we have .

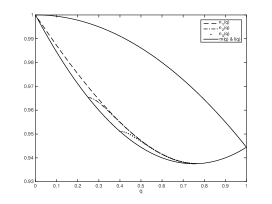

Second order smooth fit of corresponds to first order smooth fit of (and , and ). Hence we are looking for a solution and free boundaries and such that . Thus we require at and . However, the places in space where are exactly the points on the curve . Hence, candidate solutions for the value function can be expressed in terms of solutions to (2.8) with boundary conditions , for boundary points to be determined. Typically, there is a family of solutions to this problem, parameterised by the left-hand-endpoint . Write for the solution to (2.8) started at the point , and let . Clearly the solutions for different cannot cross, and is decreasing in .

To fix ideas, suppose , and . Then the quadratic is -shaped with minimum at and is non-negative everywhere. If then is decreasing at ; it can be shown that any solution started at with lies strictly below the line joining with . With a little more work we can show that for , . Further, since the solutions cannot cross, is decreasing in and is decreasing in . See the first panel of Figure 2.2.

Before describing how to choose the starting point corresponding to a given round-trip transaction cost it is useful to consider how important quantities of the value function and no-transaction region can be inferred immediately from (the correctly chosen) . We have already seen that and . Moreover, from (2.12) at where ,

and similarly . In particular, we can infer the limits of the no-transaction region directly from the solution of the free boundary problem for ; and .

Our objective is to solve the free-boundary problem:

find , , such that is a nonnegative solution of (2.8) with boundary conditions and .

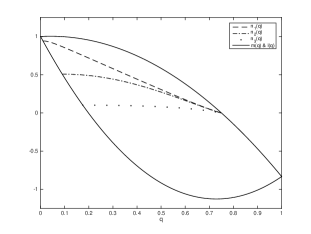

Typically there are many solutions to this problem and each solution corresponds to a different level of transaction costs. See the second panel of Figure 2.2. The above equations provide the key to determining the solution we want. The solution corresponding to the round trip transaction cost must have

| (2.13) |

But so that and then

| (2.14) |

Further,

| (2.15) |

where we use . Hence

| (2.16) |

Define

| (2.17) |

and set . Then, since and we have from the first representation of ,

| (2.18) |

where we use the fact that is decreasing in . Further, we show in Lemma 4 in Section 4 below that and . Hence is well defined on the domain . We set and , and then solves (2.8) and (2.13).

Our results are summarized in the following theorem, which is a special case of a more complete result given in Section 5. At this stage we only have a candidate value function, but the verification argument that the candidate is indeed the value function is standard. Note that the candidate solution is throughout the solvency region.

Theorem 1.

Suppose and .

Let denote the family of solutions to (2.8) with initial values . For any there exists such that , and then the no-transaction wedge is where and .

Set , and . Set and . The value function is given by (2.4) where in the no-transaction region and ; in the sale region , ; and in the purchase region , .

We close this section with a few remarks on the parametrisation of the problem, and on the form of the solution which hold both in the motivating special case of this section, and more generally.

Observe first that the assumption that the process is finite variation can in fact be a conclusion, since if the agent follows a strategy which is not of bounded variation then transaction costs mean that she cannot keep her wealth process admissible. Recall that where is the round-trip transaction cost. As we have seen it is which determines the nature of the solution to the problem, and not the individual transaction costs and . Indeed, if we define via then (2.1) becomes

| (2.19) |

Thus, the problem with proportional transaction costs on both purchases and sales reduces to a problem with transaction cost on purchases only. Conversely, if we set , then we have a problem in which the wealth process satisfies corresponding to a problem with transaction cost on sales only.

We have not included an interest rate term in the specification of the problem. However, the case of a constant interest rate can be reduced to the setting we describe by a simple switch to discounted units for both asset prices and consumption.

The quantities and have been defined as the location of the turning point of and the value of at that point. However, they have a direct interpretation in terms of the solution of the Merton problem with zero transaction costs. In the Merton problem with zero transaction costs the optimal strategy is to invest such that the ratio of wealth in the risky asset to total wealth (ie ) is kept equal to the constant . Moreover, the value function under zero transaction costs is equal to . In our present setting with it is clear that and . Thus, the value function with non-zero transaction costs is bounded above by the value function with zero transaction costs. Recall that in this section we are working under the hypothesis that and then . If we set (with similar definitions for and ) then for ,

and the Merton line lies strictly within the no-transaction wedge. Note that this is not true in general, and there are parameter combinations for which the Merton line lies outside the no-transaction wedge.

3. The general case

In this section we want to develop and expand on the analysis of Section 2, to include all parameter combinations, and not just those for which the the no-transaction region is a wedge in the first quadrant.

One issue with the analysis of the previous section is that for some parameter values it may be that the line lies inside the no-transaction wedge in -space. At , is ill-defined. For this reason in this section we consider an alternative parametrisation in which the key variable is the ratio of wealth in the risky asset to paper wealth, where paper wealth is calculated as the value of the portfolio under an assumption that holdings of the liquid asset can be sold or purchased at zero transaction cost. Note that the solvency requirement implies that paper wealth is non-negative.

Define by . The solvency requirement can be expressed as . Write

| (3.1) |

and consider

| (3.2) |

Applying Itô’s formula we find (subscripts denote space derivatives and denotes a time derivative)

where for

Since is a martingale under the optimal strategy and a super-martingale otherwise, maximising over we find . Since consumption is non-negative we must have that . Further, if then . Hence, if then or equivalently

Similarly, if then

It follows that for we have and for we have . (Alternatively we can derive the form of outside the no-transaction wedge by arguing that the optimal strategy includes an immediate transaction to move the wealth portfolio to the boundary of the no-transaction wedge, as in the previous section.)

Substituting for the optimal consumption we find that in the continuation region, ,

Now we can see the merit of the factor in the definition of : we can divide through (3) by to reduce the problem to one expressed in the dimensionless quantities and . (This completes the parameter reduction; the original parameters , , , , , have been replaced by , , and .)

The parametrisation in terms of allows us to consider problems in which the no-transaction wedge lies outside the first quadrant. However, it has come at some expense: (3) appears considerably more complicated than (2.5) or (2.6). However, inspired by the analysis of Section 2 we can make a transformation in which we recover the same first-order differential equation.

Set and define . (The factor is motivated by the identity whence .) Then away from 0 and 1,

and

| (3.4) |

Moreover,

and on differentiating (3.4) we find for

Then

Also using (3.4) we have

and it follows that

Since consumption must be non-negative this expression must be positive so we can write it as and then

Cancelling factors of and dividing by , Equation (3) becomes

and with ,

Then setting we find

Finally set . Then and

In particular, solves where is as given by (2.9) for all values of (except perhaps at the singular points and ).

Consider now the boundary conditions. For we have . Then and

It follows that ; then . Writing and for we have

Note that can be rewritten as

| (3.5) |

which is valid for or equivalently . A similar analysis gives for where . Thus, the condition of continuity of at the free boundaries is equivalent to , which in turn means that candidate locations of the boundary can be identified with or equivalently .

Note that is equivalent to and that each of these conditions corresponds to the case of leverage (where the agent borrows to finance the position in the risky asset). Similarly is equivalent to . These conditions corresponds to a short position in the risky asset.

From (3.5) at and the similar condition at we have

and hence

| (3.6) |

Following the same steps as in (2.13)-(2.16) we conclude that the solution we want must satisfy

| (3.7) |

Note that if then each of the integrals in (3.6) is over a domain which includes a singularity and hence the integral is not well-defined. But, the integral in (3.7) is well defined since as we shall show and , so that the integrand in (3.7) may be made bounded and continuous at .

The programme for constructing the value function is as before. Construct a family of solutions to parameterised by the initial value . From this family choose the solution for which (3.7) is satisfied and let , and be defined from the resulting . Then the candidate value function can be obtained by integrating over the no-transaction region.

4. Parameter regimes and possible behaviours

We have shown above that the problem of constructing a candidate solution for the value function can be reduced to constructing a solution to a first order ordinary differential equation which starts and ends on a simple curve.

There are many cases to consider, each corresponding to different parameter regimes. However, the key point which we wish to emphasise is that the different cases can be distinguished by considering the behaviour of the function which is a simple quadratic.

We list ten cases. The different cases depend on the signs of the quantities , , , and . Not all of the combinations are possible, and not all lead to different behaviours. (For instance, if then necessarily ; if and , then the behaviour of the solution does not depend on the sign of or the sign of .) In general, we do not analyse in detail the boundary cases, such as (which can be investigated using similar techniques, but would require a separate analysis) or etc (which can be understood as an appropriate limiting case). This is not because these cases are in any way difficult, but rather that it is simple to decide what should happen from the arguments we give below, and they bring no new insights.

Compared with the analysis in Section 2 the new cases bring new phenomena. First, we may find that the problem is ill-posed. Second, the problem may be ill-posed for low transaction costs, but have a finite solution for higher transaction costs. Third, the no-transaction wedge may lie in the second or fourth quadrants of -space, or may intersect both the first and second quadrants. In this case the find an ex-ante remarkable phenomena — the boundary of the no-transaction region at which sales of the risky asset occur does not change as the level of transaction cost on purchases changes. (Ex-post, there is a simple explanation). The phenomena and associated cases are listed in Table 1.

| Location of NT wedge | ||||

| R | 1st Quadrant | 1st & 2nd Quadrant | 4th Quadrant | |

| Unconditionally well-posed | 1AbIIii | 1AbIii | 1Bii | |

| 2AII | 2AI | 2B | ||

| Conditionally well-posed | 1AbIIi | 1AbIi | 1Bi | |

| Unconditionally ill-posed | 1Aa | |||

We distinguish the cases as follows, based on the behaviour of . Call Case 1 and Case 2. Call Case A and Case B. In Case 1A only, call Case a and Case . (Note that in Case 1B, we must have , so the sign of is determined; in Case 2, it turns out that the sign of is not important.) In Cases 1Ab and 2A, call Case I and call Case II. Finally, in Cases 1AbI, 1AbII and 1B call Case i and Case ii.

Table 2 lists all the different cases. Where there is no entry in a cell, it means that the same analysis covers both possible cases for that value. (So, for example, in Case 1Aa, the form of the solution does not depend on the sign of .) Where the entry in the cell is +ve or -ve it means that the sign of the cell is determined by the signs of previous cells in the row. (So, for example, if then necessarily.) It follows from exhaustion that all possible parameter combinations are included in one of the rows, except the boundary cases for which . Note that necessarily , but that any ordering between and these two quantities is possible.

| R | Range of values of | R | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Case 1AbIIii | 1/2 | 1 | 2/3 | ||||||

| Case 1Aa | -ve | 35/2 | 6 | 2/3 | |||||

| Case 1AbIIi | 27/2 | 6 | 2/3 | ||||||

| Case 2AII | +ve | 1 | 1 | 2 | |||||

| Case 1AbIii | 3/2 | 1 | 2/3 | ||||||

| Case 1AbIi | 13/4 | 3/2 | 2/3 | ||||||

| Case 2AI | +ve | 5/2 | 1 | 2 | |||||

| Case 1Bii | -1 | 1 | 2/3 | ||||||

| Case 1Bi | - 3 | 1 | 2/3 | ||||||

| Case 2B | +ve | -1 | 1 | 2 |

The distinction between Cases A and B is that in the former case is a depreciating asset, in the latter case has positive drift. Then in Case A the no-transaction wedge is contained in the upper-half-plane, and in Case B it is a subset of the fourth quadrant.

The distinction between Cases a and b is that in Case a the problem is ill-posed and the value function is infinite. Note that the problem can only be ill-posed if .

The distinction between Cases I and II is that in the former case the solution may pass through the singular point . Then in Case I the no-transaction wedge intersects the second quadrant (and may be a strict subset of the second quadrant) whereas in Case II the no-transaction wedge is contained in the first quadrant. In Case I, for large enough , the value of does not depend on the round-trip transaction cost .

Finally, the distinction between Cases i and ii is that in the latter case the problem has a solution for all transaction costs; in Case i we have and then the problem is ill-posed if the round-trip transaction cost is sufficiently small.

The descriptions of the various cases should be studied in parallel with Figures 4.1—4.9 which provide a pictorial representation of the different cases. Proofs are given in the next section; in this section we describe and characterise the solution in terms of the behaviour of the quadratic .

4.1. Case 1AbIIii: , .

We begin with considering Case 1AbIIii. This is the case we considered in Section 2, and is the simplest case. We have that has a minimum at and .

The following result is completely intuitive given the definitions of and . A proof is given in the Appendix.

Lemma 2.

For all starting points we have . Also .

, and is continuous and strictly increasing.

It follows from the Lemma that is onto and that for any there exists a solution to the free-boundary problem: solves (2.8) subject to , , . Moreover the solution has the additional property that .

Let and let defined on be given by . Both and are well defined by the monotonicity of solutions to (2.8). It follows that however large the transaction costs, the no-transaction wedge is a strict subset of the first quadrant and is such that .

4.2. Case 1Aa: , .

In this case . Let be the roots of (with ) and let be the roots of (with ). Note that . It is clear from the presence of the factor in the numerator of that cannot hit zero before hits zero at . See Figure 4.1. On the other hand on . Thus for any we have . It follows that there is no solution to the free boundary problem. The optimal consumption/investment problem is ill-posed (in the sense that there is a strategy which generates infinite expected discounted utility) for any value for the round-trip transaction cost. (One strategy is at time zero to trade to a cash only position, and thereafter to keep and to consume at the constant rate per unit time.)

Note that in this case we treat both and in the same fashion: the problem is ill-posed in both cases. Thus we do not distinguish between Case I and Case II. On the other hand, if then necessarily . Thus Case ii cannot occur, and we must be in Case i.

4.3. Case 1AbIIi: , .

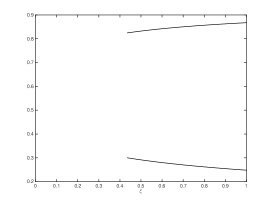

In this case but the turning point of is at and takes a negative value at the turning point. It follows that for these parameter values the problem with zero transaction costs is ill-posed. We argue that the problem remains ill-posed for small transaction costs. However, for large transaction costs the value function is finite. Moreover, we can identify the threshold value of the round-trip transaction cost which lies at the boundary between the two regimes.

Let be the roots of as above. For we can define a family of non-negative solutions to (2.8). Note , and on . Then

| (4.1) |

This integral can be evaluated (see Proposition 13 in the appendix) and we find

where

Then, for the optimal consumption/investment problem with transaction costs is well-posed, but for the problem is ill-posed, and there is a strategy which yields infinite expected utility from consumption. See Figure 4.2.

4.4. Case 2AII: , .

In this case on and is increasing provided and . See Figure 4.3. The condition ensures that has a turning point at . Using the same reasoning as in Lemma 2, as in Case 1AbIIii for we must have . Again as in Case 1AbIIii we can define and and we find . However, unlike for the case , the value of does not matter; since all solutions (with ) are increasing and lie between and , and since , they must intersect before and they must stay positive. The problem cannot be ill-posed if . (Of course, this is clear from the utility function; if then is bounded above and the expected utility from consumption is also bounded above. Conversely a strategy for which , and which involves consuming a constant fraction of wealth per unit time thereafter (so that ) yields a finite lower bound on the value function.)

Recall the final remarks in Section 2 relating to the value function of the zero-transaction cost Merton problem in the case . Now we have that and . Note that in this case the presence of the term in the value function means that increases in (or ) decrease the value function. Hence again the value function is bounded above by the value function with zero transaction costs.

4.5. Case 1AbIii: , .

In this case is positive everywhere, but so that is decreasing on , and for , . See Figure 4.4.

Since the Merton line lies in the second quadrant. For small transaction costs the no-transaction wedge lies in the second quadrant and the agent has a leveraged position in the risky asset, ie borrows to finance the position in the risky asset. This is the case for which we can find a solution with such that . For large transaction costs we have and the no-transaction wedge intersects both quadrants in the upper-half-plane. The threshold between small and large transaction costs is not given as an algebraic function, but is where

| (4.2) |

In the case we find that does not depend on .

Lemma 3.

(i) is well defined. Further and .

(ii) For , and .

(iii) For , . In particular, for , .

Proof.

See appendix. ∎

The intuition behind these results is as follows. Since and is decreasing on , for we have that cannot cross before . Since we have on we must have that passes through the singular point . At this point . A solution for can be constructed beyond , but since solves a first order equation, the solution does not depend in any way on the behaviour of to the left of . Thus, if , does not depend on .

Lemma 4.

is continuous at . Further is strictly decreasing with and

Proof.

See appendix. ∎

Given the function we can define and then is well-defined. We set and and derive the value function in the no-transaction wedge by integrating over the interval .

The following corollary is an immediate consequence of the fact that for , does not depend on .

Corollary 5.

For the no transaction wedge intersects both the first and second quadrants. If the transaction cost on sales is held fixed, then provided the threshold at which sales occur does not depend on the transaction cost on purchases.

Note that for the threshold at which sales occur does depend on the transaction cost on purchases. This is the generic result: in Case II if the problem is well-posed then the locations of both boundaries of the no-transaction wedge depend on the values of both transaction costs.

At first sight Corollary 5 may appear surprising. At a mathematical level, the result is a consequence of the fact that the relevant solution passes through the singular point and on doing so ‘forgets’ its starting point . Hence does not depend on for . Since we find that does not depend on . The financial explanation of this result is fairly simple also. If the no-transaction wedge intersects both quadrants in the upper half plane, then it includes the half-line . If ever , then the agent finances consumption first by borrowing and then when borrowing levels become too great, from sales of the risky asset. But, once cash-wealth is non-positive, the agent will trade in such a way that cash wealth is never positive at any future moment. Thus, once the agent will never again purchase units of risky asset, and the transaction cost on purchases becomes irrelevant. Hence the location of the sell threshold does not depend on . The same arguments show that the value function in the second quadrant does not depend on (for ), although it continues to depend on in the first quadrant.

Note that if then there is no solution of the free-boundary problem (FBP). Instead the solution we want has an endpoint at at which , and is a solution of the initial-value problem (IVP)

find , such that is a nonnegative solution of (2.8) in with boundary conditions and .

4.6. Case 1AbIi: , .

This case combines the novel features of Case 1AbIIi and Case 1AbIii. See Figure 4.5. The value of at the turning point is negative and so for very small transaction costs the problem is ill-posed. For moderate transaction costs the solution is such that the no-transaction wedge lies in the second quadrant. For larger transaction costs the axis lies inside the no-transaction wedge, and then the ratio defining the sales boundary the of no-transaction wedge in the second quadrant does not depend on .

The critical threshold for well-posedness is given by where is given in Corollary 14. The critical threshold above which the no-transaction wedge includes the half-line is not given by an algebraic expression, but instead by where is as given in (4.2).

Note that for , over the domain where both are defined, and hence . Thus .

4.7. Case 2AI: , .

In this case , and as in Case 1AbIii for any we have . See Figure 4.6. Since the problem cannot be ill-posed. For small transaction costs (where small is ) we find that the no transaction wedge lies strictly inside the second quadrant, and the agent always holds negative cash wealth. For the no-transaction region contains the half-line and the value of does not depend on .

4.8. Case 1Bii: , .

Now is a quadratic which is increasing at zero and everywhere positive. See Figure 4.7. We have and so the Merton line lies in the fourth quadrant. We are interested in the behaviour of for . For we have and on , . For let solve (2.8) on the domain and let . It is convenient to rewrite the definition of as

As in Case 1AbIIii, is increasing with and . Setting , is continuous and strictly increasing on with well-defined inverse. Set and . The the solution to the free boundary problem is given by on .

4.9. Case 1Bi: , .

This case combines the features of Cases 1AaIIi and 1Bii. The no-transaction wedge lies in the fourth quadrant, but for sufficiently small transaction costs the problem is ill-posed. See Figure 4.8. The round-trip transaction cost threshold between ill-posed and well-posed problems is given by where is as given in Corollary 14.

4.10. Case 2B: , .

In this case on and on and . The solutions we want are decreasing on , and a solution with exists for each possible round-trip transaction cost. See Figure 4.9.

4.11. Boundary cases

If or equivalently then . It is optimal to sell any initial endowment in the risky asset immediately. Thereafter no further trading is required. Note that in this case the solution to the Merton problem (with no transaction costs) is also to have zero investment in the risky asset since holding the asset brings risk but no return. For this reason it better to sell now rather than later.

If and or equivalently then the problem is ill-posed.

If (and ) or equivalently (and, if , ) then for any value of the transaction cost. The optimal solution to the Merton problem is to invest exclusively in the risky asset and to keep zero cash holdings. Consumption is financed from sales of the risky asset. For the transaction cost problem, if ever cash wealth hits zero, then the investor keeps cash wealth at zero (and finances consumption from sales of the risky asset). But if the agent has a small positive cash wealth, then before selling any risky asset, he first finances consumption from cash wealth. In fact, if there are adverse movements in the price of the risky asset, the agent may also purchase units of risky asset.

If (and ) or equivalently (and ) the problem is ill-posed for zero-transaction costs, but well posed for any positive level of round-trip transaction cost.

5. Verification Lemmas

The main theorem of this paper is the following

Theorem 6.

Recall the formula for in (4.1) and set .

-

(1)

Suppose either

-

(a)

or

-

(b)

and or

-

(c)

, and or

-

(d)

, and .

Then the problem is well-posed.

-

(a)

-

(2)

Suppose either

-

(a)

and or

-

(b)

, and or

-

(c)

, and .

Then the problem is ill-posed.

-

(a)

Proof.

Since the majority of this result is contained in Choi et al [1] we only provide a sketch of the proof. Proofs of well-posedness for subsets of the parameter combinations can also be found in Davis and Norman [4] and Herczegh and Prokaj [6]. The main innovations compared with [1] are that we cover the case and we give an explicit formula for . The other substantial difference is that we take a classical approach via the value function and the Hamilton-Jacobi-Bellman equation, whereas Choi et al construct a solution via the dual problem and the shadow price.

Our contention is that whilst the two approaches are equivalent, ultimately our analysis is simpler, in the sense that the solutions are characterised by the behaviour of a simple quadratic function.

The well-posed case: For the parameter combinations listed as leading to a well-posed problem (excluding for a moment the case where ) we can construct a positive, -solution to the free-boundary problem and thence a function and a candidate value function given by . It remains to prove that this candidate value function is the value function of the optimal consumption/investment problem.

Note that since is we have that the candidate value function is on the solvency region. Hence we can apply Itô’s formula. Set . Then under any admissible strategy and where .

Suppose . Then is a local martingale null at 0. Also and so the local martingale is bounded below by and hence a supermartingale. Then and for any admissible strategy

and by monotone convergence, for any admissible strategy

Hence .

To show the converse, we need to exhibit an admissible strategy for which . Then and we are done. Let be the candidate optimal strategy, with associated wealth process . Then,

and is the singular-control, local time strategy which involves selling/purchasing just enough risky asset to keep in the interval . Define via . Then since includes a factor which decays exponentially over time, it is possible to show that over any horizon , is a martingale and almost surely and in (see [4, 7, 13] for this result). Then, from the martingale property of ,

and letting we conclude

as required.

If the argument that the local martingale is a super-martingale fails, since it is not bounded below. However Davis and Norman [4], see also [7, 13], give an ingenious argument based on taking limits for a family of perturbed utility functions to show that the result holds for also.

If then the same ideas work, except that we construct the value function via which solves the modified problem whereby , . Then . Note there is still smooth fit at , but no second order smooth fit. Hence is discontinuous at but we can still apply Itô’s formula to (3.2). In this case the axis is a boundary to the no-transaction region. Once the agent reaches a leveraged position and cash wealth is negative then cash wealth remains negative for evermore.

The ill-posed case: In this case it is sufficient to exhibit a strategy which yields infinite expected utility. See Choi et al [1] for details. ∎

6. The dependence of the no-transaction wedge on parameters

6.1. Dependence on transaction costs

For most of this paper we have argued that the transaction costs on purchases and on sales only enter the problem through the round-trip transaction cost . Whilst that is true for the construction of (and the locations of the free-boundaries and from which the solution is built), the boundaries of the no-transaction wedge do depend on the individual transaction costs and we have and where

| (6.1) |

and .

Theorem 7.

Suppose all parameters are fixed, except for the transaction costs and . Suppose the problem is well-posed. Then

-

(a)

-

(i)

is non-decreasing in , and is increasing in .

-

(ii)

If and then and does not depend on .

-

(i)

-

(b)

-

(i)

If then the purchase boundary and sale boundary are increasing in and increasing in and the Merton line lies within the no-transaction wedge. We have .

-

(ii)

Suppose or . Then and need not be monotonic in the individual transaction costs, and the Merton line need not lie within the no-transaction wedge. If then and the agent will (at least sometimes) take a leveraged position. If then and the agent will take a short position.

-

(i)

Proof.

(a)(i) Recall the definitions and

From the non-crossing property of the solutions it follows that is decreasing in and that is increasing in , and is decreasing in . The implicit function theorem gives that away from and , and are differentiable.

(a)(ii) This follows from Lemma 3.

(b) We have

and

If then and the sign of both terms is positive, but if then either term may dominate.

Similarly,

and

If then and the sign of both terms is negative, but if then either term may dominate.

Note that solvency requires that . So, when we have and the Merton line lies outside the no transaction wedge. ∎

Of interest is the location of the no-transaction wedge and the relationship between the Merton line and the no-transaction wedge. The key advantage we have over the previous literature ([4, 11]) is that we have decoupled the expressions for the locations of the boundaries of the no-transaction wedge into two parts: we have and given by (6.1) where .

Davis and Norman [4] argue that if (and a further technical condition, Condition B holds) then the no-transaction wedge lies in the first quadrant and contains the Merton line. We saw this in the final comments of Section 2. They also conjecture [4, p704] that if the problem is well-posed and then the no-transaction wedge lies in the second quadrant. As we have seen, if transaction costs are sufficiently large, this need not be the case.

Shreve and Soner [11] give bounds on and . They state in (11.4), (11.5) and (11.6) of [11] that

| (6.2) |

if

| (6.3) |

and if and

| (6.4) |

The bounds (6.2), (6.3) and (6.4) can be seen to follow from our results, sometimes under weaker assumptions.

If (equivalently ) and the problem is well-posed then since is a quadratic and is monotone we must have and so . We conclude that . Then, since ,

| (6.5) | |||||

| (6.6) | |||||

| (6.7) |

Note that from we also have the bound , and the no-transaction wedge lies in the first quadrant.

If (equivalently ) and the problem is well-posed then since we have . Then and (6.5) can be refined to

Shreve and Soner [11, p675] also conjecture that if then and the Merton line lies outside the no-transaction wedge. If then we have and . Then if so that transaction costs on sales are large we have and the Shreve-Soner conjecture is true. However, if transaction costs on sales are small we may find , and the Merton line lies inside the no-transaction wedge. In particular, if then and .

6.2. Dependence on drift

Theorem 8.

Suppose all parameters except the drift are constant and that the problem is well posed. Then both the purchase and sale boundaries of the no-transaction wedge are increasing in the drift in the underlying asset.

Proof.

We want to show that both and are increasing in , which is equivalent to and increasing in . We consider the case ; similar arguments work for .

Fix and let and denote the solutions of and subject to where

Here (respectively ) is the quadratic (respectively ). In general let the and symbols denote solutions defined relative to and . Let .

Let . Then

For and we have and , and we conclude that away from , and cannot cross. Consideration of the cases for , and/or leads to the a similar conclusion.

Suppose first that so that we may restrict attention to . Fix . Then at least until and then it follows both that and , where we make use of and the representation

which we note only depends on through . Since is decreasing in we conclude that and that is increasing in .

In order to consider the sale boundary it is convenient to parameterise solutions of the free boundary problem by the boundary point rather than . Let solve in subject to and let . Then, we have and again we get that solutions are increasing in ; hence is increasing in and is increasing in . It follows that is also increasing in .

Now we relax the assumption that . If , then . For the same proof as given above can be used.

Finally, if then for sufficiently small transaction costs we have , and then by the arguments as above we can conclude that and are monotonic. The only point of delicacy is when transaction costs are larger, when we must consider the case where both and lie below the singular point. Then, for , . Nonetheless, for we have the inequality with strict inequality on , and hence . Note that for large transaction costs.

∎

7. Conclusions

Our goal in this paper was to analyse the Merton problem with transaction costs via the classical approach and the primal problem. We were able to show via judicious transformations that the problem could be reduced to solving a free-boundary problem for a first-order ordinary differential equation. There is a family of solutions to this free boundary problem, and the one we want satisfies an additional integral equation.

Our first main result mirrors the main result of Choi et al [1]. We cover some additional cases (negative drift) but this is not our main contribution. Instead, our main contribution is to demonstrate that the different regimes (determining when the problem is well-posed for all transaction costs, when the problem is well-posed for large transaction costs only, and when the problem is ill-posed; and determining whether the no-transaction region lies in the first, second, fourth or first and second quadrants) depend on the shapes of a quadratic , its values and first derivatives at zero and one, and the value at the turning point. Choi et al [1] also reduce the problem to solving a first order ODE, subject to smooth fit conditions on a free-boundary, and subject to an integral condition. But in their case the points on the free-boundary lie on an ellipse (rather than a quadratic) and the phase-diagram is considerably more complicated.

Following Davis and Norman [4] and Shreve and Soner [11], our approach is via the primal problem rather than the shadow-price approach of [8, 1, 6]. Thus our approach brings different insights to [8, 1, 6]. At one level our results are a re-parametrisation of the results of Choi et al [1] although the derivation is completely different. Nonetheless, this re-parametrisation brings significant simplifications in the analysis. First, as described above we can relate the different cases to the different possible behaviours of a quadratic. Second, in the case where the problem is ill-posed with zero transaction costs, we can give an algebraic expression for the value of the transaction costs at which the problem becomes ill-posed. (Choi et al are only able to give this as an integral involving the roots of a quadratic, see Choi et al [1, Lemma 6.11].) Third, it is immediate from our approach that the integral equation which determines which of the family of candidate solutions of the free-boundary we want has a monotonicity property. In particular, it is immediate from our approach that is strictly decreasing and has an inverse: Choi et al [1, Remark 6.15] are not able to give a corresponding monotonicity argument for their equivalent function. Fourth, we can give a direct interpretation of the free-boundary points of the solution to the first order ODE in terms of the boundaries of the no-transaction wedge. This allows us to identify the solutions of the ODE which pass through the singular point as those which correspond to a no-transaction wedge which includes the half-line . This leads to a further insight which is not present in [1]. Choi et al show a result which is equivalent to the fact that all the solutions of which pass through the singular point at are the same to the right of the singular point, and conclude that the shadow price and value function are independent of the value of transaction costs (provided the level of the transaction cost is above a certain critical value). However, they do not give a financial explanation of this result. In contrast we can give an explanation. We observe that the value function is based on a function which passes through the singularity at if and only if the half-line is inside the no-transaction wedge. If this line is within the no-transaction wedge then under optimal behaviour, since cash wealth only ever increases on the sale boundary, once cash wealth equals zero it is negative at all times thereafter. Hence, since the purchase boundary of the no-transaction region is in the first quadrant, no future purchases of the risky asset will ever take place. It follows that, in the region , the value function (and the location of the sale boundary of the no transaction region) cannot depend on the level of transaction costs on purchases.

Appendix A Proofs

A.1. Proof of Lemma 2

Our goal is to prove Lemma 2 which is contained in the union of the following results. First we show the previously advertised result that for each , lies below the line joining to if and above this line if .

Lemma 9.

Suppose and . Let . Then for , .

Proof.

If then on .

Now suppose . Note that and so that since is a straight line we have the inequality on . Then we have

Hence solutions of (2.8) can only cross from above to below. Hence . ∎

Lemma 10.

Suppose , , , and . Then for , .

Proof.

First note we have and hence .

If then is increasing on and . Then, for , since is decreasing we must have .

So, suppose . Suppose for a contradiction that . Then is decreasing on and . Then and as , . Hence contradicting for close to 1. ∎

If but still (and if , , ) and if is the root of in then the same proof gives that for , .

Lemma 11.

Suppose . Then .

Proof.

We have . Then, at , . If , and then , and . Hence lies below to the right of and . ∎

Lemma 12.

, and is continuous and strictly decreasing.

Proof.

The strict monotonicity of follows from (2.18) and the fact the solutions are monotonic in . Also, is immediate from the fact that . It remains to show that . We prove this in the case and , but the result follows similarly in other cases.

Let be the negative root of where

It is easy to see that and hence . In fact if is differentiable at zero, then by l’Hôpital’s rule, solves

so that has the interpretation of a candidate value for .

Fix with . Then . Let . Then

where is the constant

Since by construction, there exists such that for we have .

For let . If crosses before then it crosses from below and stays above until . Also, for we have by the monotonicity in the second argument of .

Since there exists such that for we have . Then for ,

and for ,

Further, for we have and

Recall that for , . Then, for where we have

But which diverges as .

∎

A.2. The threshold value of transaction costs below which the problem is ill-posed

Proposition 13.

Let and be the quadratics and . Suppose either or or .

Then

Proof.

We have

The result follows on integrating. Note that under the relationships between and given in the statement of the proposition there are no roots of in and each of the four logarithms has a positive argument. ∎

Corollary 14.

Suppose . Then

where are the roots of and are the roots of :

Proof.

We have and and note and . Then with and as in Proposition 13,

| (A.1) |

The result follows using and so that and and so that . ∎

Appendix B Singular point of

Our goal is understand the nature of solutions which pass through the singular point and to prove Lemma 3 and Lemma 4.

We assume that and also if that . Then and . We are interested in the behaviour of as it passes through the singular point .

Let . Then the singular point is now at the origin. We have

| (B.1) | |||||

where

We have and whence and . Note that for sufficiently small we have that is positive and decreasing in the second argument and is positive. Our focus is on proving results about existence and uniqueness of solutions in a neighbourhood of .

For intuition, and following Choi et al [1, Lemma 6.8] consider the initial value ODE

| (B.2) |

where and are positive constants. We look for a solution separately in and . We find that there are multiple solutions for , but a unique solution for .

Fix and define by . Then . Also and hence . The condition forces and then

Thus, the solution is unique for .

Now we look for a solution in . Fix and set . Then . Each value of leads to a solution for which

We can also analyse the behaviour near of solutions to (B.2). We have . Then

Conversely, integrating by parts

In particular,

| (B.3) |

We remark that if and are continuous and positive at , then a small extension of the above argument gives that a solution to (B.2) satisfies .

Now we turn to the solution of the problem

| (B.4) |

We have seen that each member of the family with given by

solves (B.4) for . So, our focus is on the case . Our consideration of (B.2) leads us to expect that there is a unique solution.

Proposition 15.

There exists a unique solution to (B.4) in .

Proof.

Away from standard theory (see for example Walter [12, Chapter II, Section 7]) gives the existence and uniqueness of a solution passing through any point . So, our focus is on solutions near the origin.

For small enough is positive and decreasing in . We work on an interval such that is positive and decreasing in on and is positive and bounded on . Further, we assume that for we have the bounds and . Here where temporarily we assume .

Define . We work with functions defined on . Set and let be the solution to subject to . Then

Now construct a sequence of differentiable functions on where solves subject to . Then

We argue that this family of solutions is increasing in . Clearly on . Suppose inductively that on . Then, since is decreasing in its second argument and for

It follows that as required.

Now we look for an upper bound. Since ,

| (B.5) |

and for

It follows that the function on given by exists and is continuous with . It remains to show that solves (B.4). We have

by monotone convergence. Since the right-hand-side of this expression is continuous differentiable we have that is continuously differentiable and as required.

The only place that we use is to say that there is a positive lower bound for . If , then we can construct a solution not in the strip , but rather until it first leaves the rectangle for some bound , where is chosen so that on . The inequality on gives an upper bound like (B.5) on which again can be used to prove existence of the limit . Setting and we have on . Then restricting attention to we find as required.

Now we consider uniqueness. Let and be solutions which are non-negative on for some . We have that and on . If at some in then since is Lipschitz in away from we have that on and hence on .

So suppose on . We want to show that this leads to a contradiction. Since is increasing in (for small enough ), if we have . Let ; then solves

and which is the desired contradiction. ∎

We can give an asymptotic analysis of the solution to (B.4) in the same spirit as (B.3). Take , then . It follows by the comment after (B.3) that where . Hence . Conversely, using we can conclude where solves . It can be shown that for some constant . Repeating the argument, if solves subject to , then and . Hence . As a byproduct we conclude is well defined at zero and .

Proof of Lemma 3.

(i) This part of the lemma follows from Proposition 15, and the argument above that ..

(ii) Suppose . The case is similar, but sometimes involves reversed inequalities. Since for and it follows that for we have and .

We have . Suppose it is not the case that . Then either there exists , such that or there exists , such that . In the former case

and hence contradicting on . In the latter case

for large enough . Hence, sufficiently close to 1, can only cross the line from above to below, contradicting the existence of a sequence .

(iii) This follows from the uniqueness of solutions to the right of the singular point. ∎

Proof of Lemma 4.

Given the results in Lemma 2 which transfer to this context, all we need to show is that is continuous at . This will follow if and are finite for small positive and where

But , whereas , where we write if for . Hence is finite. Similar expansions hold to the left of 1 and we conclude is finite. ∎

References

- [1] J.H. Choi, M. Sirbu, G. Zitkovic (2013) Shadow prices and well posedness in the problem of optimal investment and consumption with transaction costs. SIAM J. Control and Optimization 51(6) pp. 4419-4449.

- [2] G. M. Constantinides (1986), Capital market equilibrium with transaction costs, The Journal of Political Economy, 94(4), pp. 842-862.

- [3] G. M. Constantinides, M. J. P. Magill (1976), Portfolio selection with transaction costs, Journal of Economic Theory, 13, pp. 264-271.

- [4] M. H. A. Davis, A. Norman (1990), Portfolio selection with transaction costs, Mathematics of Operations Research, 15, pp. 676-713.

- [5] J. D. Evans, V. Henderson, D. Hobson (2008), Optimal timing for an asset sale in an incomplete market Mathematical Finance, 18(4) 545-568.

- [6] A. Herczegh, V. Prokaj (2015) Shadow price in the power utility case. Annals of Applied Probability 25(5) pp. 2671-2707.

- [7] D. Hobson, Y. Zhu (2014), Optimal consumption and sale strategies, ArXiV:1409.3394.

- [8] J. Kallsen, J. Muhle-Karbe (2010) On using shadow prices in portflio optimization with transaction costs. Annals of Applied Probability 20(4) pp. 1341-1358.

- [9] R. C. Merton (1969), Lifetime portfolio selection under uncertainty: the continuous-time case, The Review of Economics and Statistics, 51, pp. 247-257.

- [10] R. C. Merton (1971), Optimum consumption and portfolio rules in a continuous-time model, Journal of Economic Theory, 3(4), pp373-413.

- [11] S. E. Shreve, H. M. Soner (1994), Optimal investment and consumption with transaction costs, Annals of Applied Probability, 4, pp. 609-692.

- [12] W. Walter (1998), Ordinary differential equations Springer, New York. Graduate Texts in Mathematics; 182.

- [13] Y. Zhu. (2015), Investment-consumption model with infinite transaction costs. PhD Thesis, University of Warwick.