Growth and fluctuation in perturbed nonlinear

Volterra equations

Abstract.

We develop precise bounds on the growth rates and fluctuation sizes of unbounded solutions of deterministic and stochastic nonlinear Volterra equations perturbed by external forces. The equation is sublinear for large values of the state, in the sense that the state–dependence is negligible relative to linear functions. If an appropriate functional of the forcing term has a limit at infinity, the solution of the differential equation behaves asymptotically like the underlying unforced equation when , like the forcing term when , and inherits properties of both the forcing term and underlying differential equation for values of . Our approach carries over in a natural way to stochastic equations with additive noise and we treat the illustrative cases of Brownian and Lévy noise.

1. Introduction

1.1. Problem Overview

We analyse the long–run dynamics of solutions to the scalar Volterra integro-differential equation

| (1.1) |

In particular, we concentrate on the behaviour of unbounded but non-explosive solutions, i.e. but . The nonlinearity is assumed to be sublinear in the state variable in the sense that , guaranteeing global existence of solutions. We draw a distinction between when solutions of (1.1) grow, , and when solutions can be said to fluctuate asymptotically, and . When solutions grow it is natural to ask at what rate they grow and when they fluctuate to ask if the size of these fluctuations can be captured in an appropriate sense; these are the primary goals of this paper.

Nonlinear equations with after effect, such as (1.1), appear naturally in a myriad of diverse applications from models of nuclear reactors to heat flow or even financial management [21, 22]. In the present work, we are especially motivated by economic applications, such as to vintage capital models; in this context the sublinear response of the system represents saturated growth or diminishing returns to scale. This analogy further motivates our study of (1.1) in the presence of random forcing as (1.1) encompasses a broad class of continuous time nonlinear time-series models when is replaced by an appropriate stochastic process [16, 27]. The measure can be thought of as weighting the contributions of capital of different ages to the current growth in the economy, as well as “time-to-build lags” and other delay inducing effects [10]. Hence we assume to be a finite measure so that the influence of older capital becomes negligible as time advances (see [8] for further discussion and motivation with regard to applications). Precisely, is a finite Borel–measure on , i.e.

| (1.2) |

where denotes the -algebra generated by the open sets of . We also define so that and for .

In the framework outlined above, the following is a convenient sufficient condition to guarantee a positive, growing solution to (1.1) (see [8, Theorem 1]):

| (1.3) |

After developing results regarding the qualitative behaviour of solutions to (1.1) we extend our deterministic analysis to consider the asymptotic behaviour of the related stochastic Volterra equation

| (1.4) |

where is a semimartingale. We establish an appropriate existence and uniqueness theorem for equation (1.4) and specialise to the cases of Brownian and Lévy noise in order to prove precise asymptotic results.

Equations (1.1) and (1.4) can both be viewed as perturbations of the underlying Volterra integro-differential equation

| (1.5) |

When is positive and sublinear at infinity, the solution of (1.5) obeys as and grows asymptotically like the solution of the ODE , i.e. the corresponding ODE with the mass of the measure concentrated at zero [8]. It is natural to ask how large the forcing terms in (1.1) and in (1.4) can become while the solutions of (1.1) and of (1.4) continue to grow in the same manner as solutions to . Furthermore, can we identify a new asymptotic regime or growth rate if the forcing terms exceed this critical rate? The main goal of this paper is to identify such critical rates of growth on and , and to determine precise estimates on the growth rate of solutions, or the rate of growth of the partial maxima when solutions fluctuate.

The analysis in our paper [8] deals with growth estimates for the unperturbed version of (1.1) (i.e. ) and can be thought of as demonstrating the asymptotic sharpness of Bihari’s inequality (and related retarded integral inequalities) for a large class of functional differential equations [14, 23]. It is a well-established, but still active, area of work to determine the interplay between the properties of perturbations and fundamental solutions or unperturbed equations. In the context of linear and quasilinear integral equations, the following formulation has proven fruitful: If the perturbation belongs to a function class , and the equation (operator) is stable in an appropriate sense, then the solution also belongs to the class . This phenomenon is referred to as admissibility, and an excellent account by one the most important contributors and initiators of this theory is given in Corduneanu [17]. In the linear case, properties of the fundamental solution and variations of constants formulae are especially helpful in obtaining these admissibility results, but naturally nonlinear equations require entirely different methods.

A central contribution of this paper is to prove results in the spirit of classical linear admissibility theory, exploiting methods more suited to dealing with nonlinear equations in which the state-dependence is sublinear. We give precise estimates on the asymptotic behaviour of solutions whether perturbations are large or small. In doing this, we bear in mind that the great bulk of research focuses on bounded perturbations with different properties or exploits the theory of weighted spaces [19]. In the latter case, (which is our focus here) tends to attract relatively little attention. Our work treats, in a unified manner, large or rapidly fluctuating perturbations which may be either deterministic or stochastic in nature. For many classes of linear differential equations with additive forcing (with or without memory) the asymptotic behaviour of solutions tends to be in one of two regimes. When the perturbation is sufficiently small, the solution tracks that of the unperturbed equation asymptotically; this can even extend to precise quantitative measures, such as Lyapunov exponents, being preserved (see [20, Ch. 10] and the references therein, [33] and Proposition 1 below). The second typical regime is when the perturbation becomes so large that the perturbed solution no longer behaves at all like the fundamental solution and instead the forcing term dominates the dynamics (cf. [4]). The challenge is to characterise precisely the appropriate quantities that are preserved in the case of small perturbations and the critical perturbation size at which the regime shift occurs. There may be interesting dynamics at the critical transition between the small and large perturbative regimes which can sometimes also be characterised; we show that this can be achieved for (1.1), as well as it’s stochastic counterpart (1.4).

There is an extensive literature regarding existence, uniqueness and regularity results for stochastic Volterra equations subject to additive Brownian forcing [11, 13]. More recently, there has been considerable progress in developing stability theory for linear stochastic Volterra equations [2, 3, 26, 36, 38] and stochastic delay differential equations [6, 25, 30, 31], particularly with an instantaneous diffusion term (i.e. delays are confined to the drift term). Moreover, several authors have extended the stability theory to certain classes of nonlinear equations, typically using Lyapunov methods [7, 22, 37, 39]. There has also been some limited exploration of global estimates on solutions in the absence of asymptotic stability for the small noise regime [32, 40]. In contrast, we explicitly explore both the case where the noise term is small relative to the nonlinear drift term in (1.4) and the situation in which the state-independent noise term dominates the dynamics. This is an important first step towards understanding the dynamics of (1.4) with state dependent noise, e.g. where denotes Brownian motion. There are relatively few results in the extant literature concerning the qualitative or asymptotic behaviour of stochastic Volterra equations with non-Brownian noise, although some authors have considered linear equations with quite general noisy driving processes [29]. Hence the combination of nonlinearity, general stochastic noise and memory in (1.4) is especially novel; in particular, we will prove asymptotic results with -stable noise, in which case the solution to (1.4) is a non-Markovian jump process with nonlinear state dependence.

1.2. Outline & Motivation

Much of our analysis flows from the simple matter of integrating (1.1) to obtain the forced Volterra integral equation

| (1.6) |

Since stochastic “differential” equations must be rigorously formulated in integral form, it is perhaps even more natural to treat (1.4) similarly; this leads us to consider

| (1.7) |

Equation (1.6) shows that the solution to (1.1) is a functional of the aggregate behaviour of the forcing term purely through and hence it is natural to formulate asymptotic results in terms of . When studying the asymptotic behaviour of many forced differential systems, hypotheses on the aggregate or average behaviour of the forcing terms are preferable to more restrictive pointwise conditions. When studying stochastic equations pointwise estimates become unrealistically restrictive and it is more natural, perhaps even necessary, to consider average behaviour. In this spirit, Proposition 1 below illustrates how hypotheses on the averaged behaviour of perturbations can be used to classify the behaviour of the elementary perturbed linear ordinary differential equation (ODE) shown in (1.9); the proof is a simple matter of applying the variation of constants formula and integration by parts multiple times (see Section 4 for details). The asymptotic behaviour of the solution to this linear ODE is characterized via the functional

| (1.8) |

quantifies size of the perturbation term. When , the perturbation is small (in some appropriate sense), and the solution to (1.9) is asymptotic to the unperturbed solution in case (i.). On the other hand, when perturbations grow more rapidly than some critical rate, the solution can track the perturbation asymptotically; this is case (iii.) of Proposition 1 when and the solution is asymptotic to the perturbation term as .

Proposition 1.

Consider the nonautonomous linear ordinary differential equation given by

| (1.9) |

Suppose for all and let be defined as in (1.8).

-

(i.)

If , then as .

-

(ii.)

If , then

-

•

implies as ,

-

•

implies and as ,

-

•

implies as .

-

•

-

(iii.)

If , then as .

When the perturbation is precisely at some “critical size”, there is often an intermediate regime where the solution to a perturbed differential system inherits properties of both the unperturbed solution and the perturbation term (cf. [4, Corollary 1]). This regime requires a certain asymptotic balance in the sense that the perturbation term and the unperturbed solution should be of roughly the same order of magnitude. We observe this situation even for the simple linear ordinary differential equation (1.9) in Proposition 1 case (ii.); we prove results of a similar character for (1.1), even for stochastic perturbations.

We now specify our hypotheses on the nonlinearity and outline typical results for the nonlinear Volterra equation (1.1). For solutions of the unperturbed Volterra equation (1.5) to behave similarly to those of the corresponding nonlinear ordinary differential equation with the measure concentrated at zero, i.e.

| (1.10) |

it is important that be sublinear. In previous work we showed that if is asymptotic to a function which is increasing and obeys as (a hypothesis implying sublinearity of ), then the solution to (1.5) obeys

| (1.11) |

where is the function defined by

| (1.12) |

(see [8] for further details). Sublinearity is crucial to this result since, for example, the linear Volterra equation of the form (1.5) does not share the exponential rate of growth of the linear ODE with all of the mass of concentrated at zero (cf. [19, Theorem 7.2.3]). However, the distribution of the measure , as opposed to simply it’s total mass, can impact rates of asymptotic growth when is sublinear in the case where as [5]. We retain the aforementioned hypothesis on and occasionally strengthen it so that decays monotonically to as ; the implications and technical motivations for such hypotheses are discussed in Section 2.

Before stating our main results precisely we give a heuristic argument as to their likely validity. In this discussion we consider the simple (deterministic) case in which both the solution and the perturbation are positive. If the unperturbed equation (1.5) is integrated as above, . In this case, the solution of the integral equation is roughly of order , like the solution to the nonlinear ODE (1.10). This leads to the naive idea that if is of smaller order than (i.e., smaller than ), then on the right–hand side of (1.6) could be absorbed into on the left–hand side, without changing the leading order asymptotic behaviour of . However, if dominates , or is of comparable order, such an outcome is improbable and the asymptotic behaviour of is unlikely to be determined by . Since the asymptotic behaviour of (1.5) is described well by the asymptotic relation as , and is increasing, it is natural to characterise the forcing term as “small” or “large” according as to whether tends to a small or large limit as (if such a limit exists). Hence we define the dimensionless parameter by

| (1.13) |

In some sense is critical; for , is dominated by the solution of (1.5). But for , dominates the solution of (1.5). The cases and are especially decisive; in these cases it is very clear whether the solution of the unperturbed equation or the perturbation dominates. A condition which implies (1.13), and turns out to be very useful in classifying asymptotic behaviour, is

| (1.14) |

If in (1.14), then

so small perturbations give rise to asymptotic behaviour as in (1.5), and the solution dominates the perturbation. If , then

so large perturbations cause the solution to grow at exactly the same rate as , and the solution grows much faster than the original unperturbed Volterra equation. When the perturbation is of a scale comparable to the solution of (1.5), in the sense that ,

| (1.15) |

Examples show that the limits in the first part of (1.15) are not, in general, equal to or . Further investigation for finite and positive leads to better estimates, especially when . The critical character of the case when is demonstrated by the following result: if then

| (1.16) |

This provides sharper estimates for large than the asymptotic bounds given for above and identifies that is of order . We also show by means of examples that when , the limit

can result, so that can only be expected to be exactly of the order of for (see Example 2.14). However, if , it is not necessarily the case that as (see Example 2.13). As , equation (1.16) correctly anticipates that as , which is what pertains when . To generalise the analysis above to stochastic equations, and for notational convenience, we define the following functional for later use:

| (1.17) |

for all functions and such that the above limit is well defined. For deterministic equations we will typically choose in (1.17) but other choices will prove advantageous when considering stochastic perturbations.

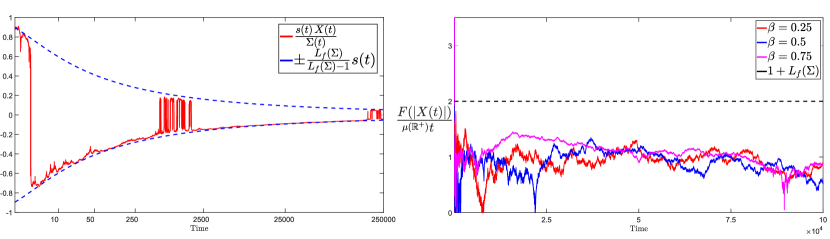

The rest of the paper is organized as follows: in Section 2 we provide the mathematical framework for studying solutions to (1.1), state our main theorems for both growing and fluctuating solutions, and provide examples to illustrate the strengths and limitations of our results. Section 3 contains results for the stochastic Volterra equation (1.7); we first prove a general existence theorem for solutions to (1.7) and then proceed to extend our deterministic results to cover Brownian and -stable Lévy noise. We also present some applications and numerical simulations to illustrate our stochastic results. Section 4 contains the proofs for Section 2 on deterministic Volterra equations and Section 5 contains the proofs for Section 3 on stochastic Volterra equations. The interested reader can find detailed justification of all examples and an outline of the numerical scheme used to produce Figure 1 in Appendix A.

2. Deterministic Volterra Equations

2.1. Mathematical Preliminaries

We briefly recall the relevant existence and uniqueness theory for the deterministic Volterra equation (1.1) in order to keep the presentation self contained.

Definition 2.1.

A function solves the initial value problem (1.1) if it obeys (1.1) almost everywhere on an interval containing zero and is absolutely continuous on that interval. A solution which obeys (1.1) for almost every is called a global solution. A solution which obeys (1.1) for almost every for some is called a local solution.

The following result guarantees the existence of a local solution to (1.1) in the sense of Definition 2.1 [19, Corollary 12.3.2].

Theorem 2.2 (Local Existence Theorem).

We assume throughout that (or stronger hypotheses implying this) and hence will always obey a global linear bound of the form

Therefore solutions to (1.1) are always globally defined in the present framework. Moreover, Gripenberg at al. [19, Theorem 13.5.1] guarantees that solutions to equation (1.1) are unique under the hypotheses of Theorem 2.2 if is locally Lipschitz continuous.

We next define a useful equivalence relation on the space of positive continuous functions; in essence, two functions are equivalent if they have the same leading order asymptotic behaviour.

Definition 2.3.

are asymptotically equivalent if ; written as for short.

implies as and implies that , defined by (1.12), obeys . Hence the following convenient lemma can be proven immediately by asymptotic integration.

Lemma 2.4.

We impose the following sublinearity hypothesis on the nonlinear function :

| (2.2) |

In many cases the following slightly stronger hypothesis is necessary

| (2.3) |

If is an increasing, sublinear function, then but it is still possible that

in the “worst” case. In previous work we provided an example of such a pathological but such nonlinearities are unlikely to arise naturally in applications so condition (2.2) is a relatively mild strengthening of sublinearity in this context [8]. Assuming further that tends to zero monotonically, as in (2.3), one can establish the following lemmata which often prove crucial in the asymptotic analysis of (1.1) and (1.4).

Lemma 2.5.

If (2.3) holds, then obeys

| (2.4) |

The conclusions of Lemma 2.4 are remarkably close to some of the key properties enjoyed by the class of regularly varying functions with unit index, denoted . Namely, implies for all and [15]. The next lemma shows that the auxiliary function from (2.3) preserves asymptotic equivalence (cf. [18, Ch. 3, Problem 2]) and hence , if the limit exists.

Lemma 2.6.

If (2.3) holds, then the function preserves asymptotic equivalence, i.e. if obey , and as , then as .

The connection between the “natural” size hypothesis on , (1.13), and the functional condition, (1.17), is supplied by the following result.

Proposition 2.

Occasionally, we employ the standard Landau “O” and “o” notation. For and in , if for some and sufficiently large, and if as .

2.2. Growth Results

With the requisite preliminaries in hand, we now turn to the computation of explicit growth estimates for solutions to (1.1). Suppose that (1.3) holds so that as , subject to a positive initial condition. Our first result provides an easy to check sufficient condition on which guarantees solutions of (1.1) retain the rate of growth of solutions to the ordinary differential equation (1.10). This sufficient condition is of a different character to conditions involving the functional and expresses more explicitly the idea that the perturbation term, H, should be small relative to the solution of (1.10).

Now we formulate a sufficient condition for to hold in terms of . We also prove that when the solution of (1.1) retains the growth rate of solutions of (1.10) it is of a strictly larger order of magnitude than the perturbation term, H.

Notably, we do not assume that as in Theorem 2.8; this is in the case where . However, if , then . The rationale is as follows in the case , with the case of being similar. By hypothesis for and as is a positive function, is increasing. Therefore, either tends to or to a finite limit. In the former case, as automatically. If, to the contrary, the limit is finite, then tends to a finite positive limit as . But this forces as , a contradiction.

When is nonzero but finite we expect the solution of (1.1) to inherit properties of both the ODE (1.10) and the perturbation term. Our next theorem investigates results of the type (1.11) when ; we show that the growth of solutions to (1.1) is at least as fast as that of solutions to the ODE (1.10) and we prove an upper bound on the growth rate. The resulting upper bound is linear in and this is intuitively appealing as a “larger” should speed up growth. However, this upper estimate on the growth rate is not sharp in general. Without additional hypotheses this upper bound is hard to improve but can be shown to be suboptimal for specific classes of nonlinearity, for example when is regularly varying with less than unit index. We will demonstrate this possible improvement in further work.

Theorem 2.9.

The asymptotic lower bound on the quantity in the result above agrees with Theorem 2.8 as since it correctly predicts that when . In some sense, the case where is special since the perturbation term is approximately the same order of magnitude as the solution to the unperturbed equation (1.5). More precisely, implies that . Furthermore, if preserves asymptotic equivalence (see Lemma 2.6) and , then as where is the leading order behaviour of the solution to (1.5). In many practical cases of interest, such as when for , inherits the asymptotic preserving property from (see [8, Theorem 5]).

When , we can additionally provide upper bounds on the quantity . Moreover, these bounds are sharp in the limit as .

Theorem 2.10.

Albeit under stronger hypotheses, Theorem 2.10 provides more refined conclusions than Theorems 2.11 and 2.12 (see Section 2.3 on fluctuation results). In particular, case establishes bounds which demonstrate that will closely track the asymptotic behaviour of and case establishes that when the forcing term, , is sufficiently large as . Furthermore, when as , is of a strictly larger order of magnitude than the solution of the corresponding ODE (1.10). This result allows us to pick up fluctuations in the solution even when is nonnegative. Even though the solution grows to infinity, it may not do so monotonically and the conclusion of Theorem 2.10 identifies upper and lower rates of growth of the solution ( and respectively) when . When , the fluctuations are entirely determined by .

The main results of this section are all proven by comparison arguments and the careful asymptotic analysis of the resulting differential inequalities. Since we assume positivity of to ensure asymptotic growth of solutions, it is straightforward to show that ; this is proven by a translation argument and appealing to [8, Corollary 2]. The proof of the corresponding upper bound, , is more involved but can be roughly summarized as follows:

-

Step 1:

Use monotonicity and finiteness of the measure to construct the crude upper inequality

(2.9) where includes constants and lower order terms, is a monotone function asymptotic to and we define for .

-

Step 2:

Using hypotheses on the size of the perturbation term, show that is or .

-

Step 3:

Conclude the argument via a variation on Bihari’s inequality.

Results in this section can be restated with positivity assumptions on and replaced by (2.12) below and

| (2.10) |

With this modification one obtains upper bounds on the rate of growth of solutions to (1.1), i.e. results of the type .

2.3. Fluctuation Results

The existence of the limit (even when it takes the value ) is too strong a condition if we hope to apply our deterministic arguments to related equations with stochastic perturbations. We weaken the hypothesis as follows: assume that there exists a function such that

| (2.11) |

As we no longer restrict ourselves to positive solutions, we ask for a degree of symmetry in the problem to simplify the analysis. We ask for “asymptotic oddness” of the nonlinearity in the following sense:

| (2.12) |

We now make hypotheses on , as opposed to . We take , rather than positive and finite since we can always normalise this quantity while keeping the properties of unchanged. Since forces to be eventually increasing, we suppose that is always increasing for ease of exposition but there is strictly no need to make this assumption. Under (2.11) we can permit highly irregular behaviour in as long as we can capture some underlying regularity in the asymptotics of via a well-behaved auxiliary function, . For example, in applications to stochastic equations, could be a stochastic process whose partial maxima are described in terms of a deterministic function; this is the case for classes of processes obeying so-called iterated logarithm laws for instance. The following result illustrates the immediate utility of the hypothesis (2.11) for deterministic equations and furthermore details how this hypothesis carries over to the case when .

Theorem 2.11.

Case of the result above indicates that when the perturbation is of intermediate size, in the sense that , solutions of (1.1) are at most the same order of magnitude as , modulo a multiplier. In case , when the perturbation is so large that , solutions of (1.1) have partial maxima of exactly the same order as those of . This conclusion is strongly hinted at in case of Theorem 2.11 if one lets in that result.

The restriction is crucial to the proof of Theorem 2.10 and cannot be relaxed within the framework of the current argument; we make this comment precise at the relevant moment during the proof itself (see Remark 4.2). In fact, is not a purely technical contrivance but is also essential to the validity of our result. In Example 2.14 we demonstrate that when it is possible to have .

If in (2.11) we can use the following hypothesis and the arguments from Theorem 2.11 to extend the scope of the result above:

| (2.13) |

Theorem 2.12.

In the presence of limited information about the behaviour of , in the sense that (2.13) holds, the result above tells us that the solution of (1.1) is roughly the same order of magnitude as , in the sense that also obeys (2.13), when . When we are still left with a weak conclusion and we are tempted to ask if this is an artifact of the method of proof. Example 2.17 shows that we cannot expect to conclude that in general in this case. However, in attempting to apply this result it is likely that the user would actually seek to refine their choice of in order to obtain a obeying and hence make the stronger conclusion that .

Theorem 2.12 could equally well be stated as follows: implies that

and implies . These two statements are proved independently of one another but we chose to present them as part of a single result as we feel this is the manner in which they would prove most useful in practice; choosing and “close together” can give useful bounds on the size of the solution but using either bound in isolation only gives very crude information (see Example 3.14 for an illustration of this comment).

The results of this section are proven via the usual machinery of comparison and asymptotic analysis but also rely crucially on the construction of a linear differential inequality to achieve sharp results. The key steps in the argument can be understood as follows:

- Step 1:

-

Step 2:

Use (2.3) to derive the linear differential inequality

(2.15) Since we can solve this inequality directly, there is no additional loss of sharpness here.

- Step 3:

-

Step 4:

The upper bounds achieved in Step 3 are recycled and further estimation yields the conclusions shown in the results above.

Essentially the same steps outlined above are successful with random forcing, as we demonstrate below.

2.4. Deterministic Examples

The following examples illustrate both the limitations and sharpness of some of the results outlined above. Consider the Volterra integro-differential equation given by

In the notation of (1.6), and . Hence

| (2.16) |

We construct examples by choosing a solution , up to asymptotic equivalence, and then using (2.16) to figure out how large the perturbation term, , must have been to generate a solution of this size. The calculations relevant to this section can be found in Appendix A. For simplicity we forego any mention of hypotheses of the form (2.11) in this section and concentrate on the special case with positive.

Example 2.13.

The limits in Theorem 2.9 are not always equal to or and furthermore does not in general imply that . If , , then

| (2.17) |

Suppose and take , for all . Thus as . If as , then

Now suppose that so we can choose an advantageous value of . For the purposes of this example it is sufficient to take and . With these choices

and the reader can compare this with the conclusion of Theorem 2.9. Finally, note that

Example 2.14.

If , then

| (2.18) |

This example highlights the potential problems that emerge when one attempts to address the case (resp. ) in the context of Theorem 2.11. In particular, one cannot extend the conclusion of Theorem 2.11 to cover without additional hypotheses because when it is possible to have .

Choose for and let for some . In this case . Furthermore, obeys and by construction . However, we still have

Example 2.15.

Example 2.16.

We present a simple example illustrating the case when the solution to (1.1) is asymptotic to and the functional takes the value . Let .

Example 2.17.

In case of Theorem 2.12 it is possible to have but

when . Hence there is no straightforward improvement of the conclusion of Theorem 2.12 when .

Let with , , and with . This implies that as , where the asymptotics of are given by (2.17), and hence , as required. It is straightforward to verify that .

3. Stochastic Volterra Equations

We now study the pathwise asymptotic behaviour of solutions to (1.4). Our approach is to treat (1.4) as a perturbed version of (1.1) where the forcing term is now stochastic and hence to leverage our deterministic results as much as possible. After proving a strong existence theorem for solutions to (1.4), we use the pathwise asymptotic theory for continuous Brownian martingales and –stable Lévy processes to show that the main results from the previous section are sufficiently general that we can extend them to provide asymptotic estimates on the pathwise growth and fluctuation of solutions. We also explain how our results provide a programme for establishing similar pathwise bounds for broader classes of admissible stochastic noise.

We henceforth work on a given probability space which is complete and has a right continuous filtration. We ask that the nonlinear function obeys the following local Lipschitz condition: for each there exists such that

| (3.1) |

and that obeys a global linear bound of the form

| (3.2) |

where and are positive constants.

In order to leverage the framework of Métivier and Pellaumail [28] we make a slight modification to the formulation of (1.4) and consider the stochastic integral equation

| (3.3) |

By applying Fubini’s Theorem and making a suitable change of variable, (3.3) can be written as

| (3.4) |

where and . This adjustment is necessary for the functional

| (3.5) |

to define a predictable process (measurable with respect to the filtration generated by adapted, left continuous processes) and hence be integrable with respect to general semimartingales (see Protter [34] for details).

In order to define the notion of a strong solution for stochastic equations such as (3.4), we recall some standard terminology from the theory of stochastic processes: a regular process is one which is adapted and has right continuous paths with left hand limits (RCLL). A process is called –null if almost surely the paths are identically zero functions.

Definition 3.1.

A process defined on is said to be a strong solution to equation (3.4) on with initial value if the process

is well–defined on as a regular process and differs from by a –null process.

The solution to (3.4) is unique if for any two processes and obeying Definition 3.1, is a –null process.

Theorem 3.2.

Proof.

This theorem is a natural specialisation of a result of Métivier and Pellaumail [28, Theorem 5]. In order to apply the aforementioned result we must check that the functional from (3.5) and also the constant functional obey the following pair of conditions: firstly for any regular processes (adapted with cadlag paths) and , for each there exists a constant such that

| (3.6) |

for each , and . Secondly, for any regular process there exists such that

| (3.7) |

for each .

When the functional is constant the conditions above are trivially satisfied so suppose now that is given by (3.5) and proceed to verify condition (3.6). Let and be any two regular processes satisfying (resp. ), fix and estimate as follows:

where we have used both (1.2) and (3.1). Now check (3.7); assume is a regular process and fix . The following inequality is a straightforward consequence of (1.2) and (3.2):

where . Thus there exists a unique, strong solution to (3.4), at least locally in time (i.e. we could have with positive probability in Definition 3.1). Moreover, (3.2) can be used to bound the solution to (3.4) below the solution to the corresponding linear equation, which exists for all with probability 1. Hence finite-time blow-up occurs with probability zero and the second part of the claim is proven. ∎

Remark 3.3.

The condition (3.2) will always be satisfied in this section since the hypotheses (2.12) and (2.3) will be imposed throughout. The assumption (1.2) is also present throughout so the only additional hypothesis imposed by Theorem 3.2 is that of local Lipschitz continuity on the nonlinear function (which is only required to guarantee uniqueness of solutions).

We pause now to consider the method by which the results of this section are proven and to illustrate that this presents a framework for generating similar pathwise asymptotic results for a wide range of suitable stochastic forcing terms. Our method of proof relies principally on building appropriate comparison equations so we are not concerned about the pathwise regularity of the solution to (1.4) and hence can treat quite irregular forcing processes.

If denotes the forcing term in (1.4), then our general approach is as follows:

- Step 1:

-

Step 2:

Construct an upper comparison solution (pathwise) in terms of which majorizes the solution to the (1.4); this essentially reduces the stochastic problem to a deterministic one.

-

Step 3:

Conclude the argument using suitable hypotheses on and the results of Section 2.

The steps outlined above also highlight how one can approach the important, and more challenging, case of state-dependent noise, i.e. equations of the form

In particular, hypotheses involving the functional will still allow completion of Step 1, but now the function will involve the process itself. Thus Step 2 will now necessitate further analysis of how this state-dependent perturbation interacts with the drift term .

3.1. Brownian Noise

Throughout this section denotes the unique, strong solution to (3.4),

| (3.8) |

and

Analogous to the deterministic case, we classify the behaviour of solutions to (1.4) according to whether the number is zero, finite or infinite.

The existence and uniqueness of solutions of (1.4) is naturally simpler in the case of Brownian noise. In particular, there is a unique, continuous (strong) solution to (1.4) with Brownian noise if (1.2) holds and the nonlinearity is locally Lipschitz continuous with a global linear bound (see Mao [25, Ch. 5]).

When formulating functional conditions on (1.4) to preserve growth of the type (1.11) it is necessary to distinguish between the cases and . When the martingale term in (1.7), , will tend to an a.s. finite random variable and in this case we clearly expect to retain the growth rate of solutions to (1.10). However, when the martingale term is recurrent on and has large fluctuations of order [35]. Our first result shows that when and , the solution to (1.4) cannot grow faster than that of the ordinary differential equation (1.10).

Our next result mirrors the conclusion of Theorem 3.4 but uses hypotheses on the functional instead of the condition (3.9).

Theorem 3.5.

An interesting special case of Theorem 3.5, which is likely to be important in applications, is when the function is a nonzero constant. In this case, solutions to (1.4) are unbounded with probability one.

Corollary 3.6.

As in the deterministic case when the perturbation is of intermediate or critical magnitude, in the sense that , we expect the solution to inherit characteristics of both the perturbation and the ordinary differential equation (1.10). Our next result demonstrates that this is indeed the case by showing that if the solution to (1.4) grows, then its growth rate is at most the same order of magnitude as the solution to (1.10).

When we show that if the the solution to (1.4) fluctuates, then these fluctuations are at most of order times a multiplier which we can bound in terms of . As in Theorem 2.10 we are unable to extend this argument to for technical reasons which become apparent in the relevant construction. While this bound is practically useful, it appears that it is not sharp in general (see Figure 1, right).

Nonnegativity of the measure no longer plays an important role in the results above; primarily because we are reduced to proving upper bounds on the growth rate of solutions once solutions are no longer necessarily of one sign. For ease of exposition we have left the hypothesis (1.2) in place but it could equally well be replaced by the hypothesis that is a Borel measure with finite total variation norm, i.e. , with the results above unchanged.

Under the hypotheses of Theorem 3.8 we can additionally conclude that

Hence, when , is recurrent on . This leaves open the question of recurrence, or in other words, whether or not the process actually fluctuates, for . In Figure 1 (left) we show simulations of the process in which (a scaled version of) the quantity fluctuates between the quantitative bounds predicted by Theorem 3.8. These numerical experiments further illustrate that our bounds appear to be approximately sharp (at least for some classes of examples).

Finally, when the perturbation term is so large that we expect this exogenous force to dominate the system and this intuition is confirmed by our next result. In particular, we prove that the solution to (1.4) is recurrent on and that its fluctuations are precisely of order .

3.2. Lévy Noise

We now assume that the semimartingale in (1.4) is an –stable Lévy process; the results which follow further emphasize the fact that our methods do not rely on the path continuity of the process in any essential way. For the readers convenience we recall the relevant definitions from the theory of Lévy processes.

Definition 3.10.

If is a Lévy process, it’s characteristic function is given by

where is of the form

| (3.11) |

with , and a measure on satisfying .

is called the characteristic exponent of the process .

The number in (3.11) corresponds to the linear “drift” coefficient of the Lévy process in question, is called the Gaussian coefficient and corresponds to the Brownian or continuous random component; is called the Lévy measure and represents the pure jump part of the process. A Lévy process is uniquely specified by the triple .

Definition 3.11.

For each , a Lévy process with characteristic exponent is called a stable process with index (–stable for short) if for each .

Stable processes are closely related to the class of stable distributions which gain their importance as “attractors” for normalised sums of independent and identically distributed random variables. In particular, a sum of random variables with power law decay in the tails, proportional to , will tend to a stable distribution if and to a normal distribution if . Integrability of the Lévy measure forces us to consider and in this section we also ignore the case since this corresponds to the case of Brownian noise (which was considered in detail in Section 3.1). We tacitly exclude the degenerate case when is a pure drift process and assume for the remainder of this section that

| (3.12) |

Let denote the unique, strong solution to (1.4) throughout.

Our first result is a stochastic analogue of Theorem 2.8 and provides a sufficient condition to retain growth to infinity no faster than the solution of (1.10) in the presence of –stable noise.

Theorem 3.12.

The next results provides a direct stochastic analogue of Theorem 2.12.

3.3. Stochastic Examples

Example 3.14.

To illustrate the practical application of the results in Section 3.1 we present an example with power type nonlinearity and Brownian noise, i.e. . Suppose

, , for some , and is a measure obeying (1.2). In this framework

| (3.13) |

and

Clearly, as and therefore . It is straightforward to show that

for and hence

By Theorem 3.5 we conclude that the unique, strong solution of (1.4) obeys

Similarly, by Theorem 3.9,

where the function is given by (3.13).

Example 3.15.

Let be an –stable process with index and, as in the previous example, suppose we have a power–type nonlinearity given by

Let be a measure obeying (1.2) and suppose the function is given by

By construction, is increasing, positive and satisfies . Furthermore,

If the interval is nonempty, then we can take in the statement of Theorem 3.12 to be with . Hence the solution of (1.4) obeys

This essentially means that if the nonlinearity is sufficiently strong we cannot experience growth in the solution of (1.4) faster than that seen in (1.10) (with positive probability). The restriction is intuitive in the following sense: the smaller is, the more mass there is in the tail of the Lévy measure associated with and hence the partial maxima of will tend to grow faster the smaller the value of ; when is small we require a stronger nonlinearity (larger value of ) to retain the unperturbed growth rate. When we always retain the growth rate of the unperturbed equation.

If we take , then and we can apply Theorem 3.13 to yield

| (3.14) |

where we require to ensure that . Theorem 3.13 also yields

In other words, the solution of (1.4) is with probability one for sufficiently large (in terms of both the noise and nonlinearity). Define the function by

Note that is positive, increasing and obeys . Since we aim to apply Theorem 3.13 we are only interested in the case . It is straightforward to show that

Hence Theorem 3.13 yields

| (3.15) |

and

This example highlights a limitation of Theorem 3.13 (and it’s deterministic counterpart Theorem 2.12). By comparing (3.14) and (3.15) the reader can see that it is not possible to have both and simultaneously in this example; indeed this case is difficult to engineer and only possible in limited circumstances (such as when the nonlinearity is regularly varying with unit index).

4. Proofs of Results for Deterministic Volterra Equations

To improve readability of the proofs, we let in the following sections.

Proof of Proposition 1.

Let for so that

Case (iii.): If , then and as due to positivity. Furthermore, as and asymptotic integration of that limit shows that

Moreover, since is o as , as well. Applying the variation of parameters formula to the linear ODE (1.9) gives

Let and . Now apply integration by parts to show that

| (4.1) |

Note that since . Another application of integration by parts yields

| (4.2) |

implies that and hence there exists such that

Thus

| (4.3) |

Divide by to obtain

and since , it follows that . Thus from (4.3) we have that as and . Combining these limits with (4.1) shows that as .

Case (i.): Suppose so that

Apply integration by parts to (4.1) to obtain

| (4.4) |

Since we have

It is thus clear from (4.4) that

| (4.5) |

where because .

If , then as and hence

as . Now since , it follows that

Use the asymptotic relation between and to show that . Furthermore, since , . Now from (4.1) we have

as claimed.

Finally, if , and as . It follows that and hence that . Thus using a lower estimate from (4.1) shows that

which in turn establishes that . It follows that and hence that . ∎

Proof of Lemma 2.5.

Suppose that . . Thus

| (4.6) |

establishing the first part of (2.4). To prove the second claim estimate as follows

Taking the limsup and using the first claim completes the proof. ∎

Proof of Lemma 2.6.

By hypothesis, for all there exists such that for all

Monotonicity of immediately yields

By Lemma 2.5, and the divergence of , there exists such that for all . Hence Reversing the roles of and in the argument above we have that , or equivalently, , completing the proof. ∎

Proof of Proposition 2.

Define . Then, because is increasing and invertible, and . We begin by considering the case , so

Thus for any there exists such that

Now since is increasing

| (4.7a) | |||

| (4.7b) | |||

for all . From integrating (4.7a) we obtain

for all . If is a positive constant then

With this yields

Thus for

Applying the monotone function to (4.7b), for , we have

Taking limits across the final two sets of inequalities above we obtain

Letting gives the desired result. When we will have

Thus for all . Integrating we obtain

Hence

It follows immediately that . Similarly, when , we have

Integrating by substitution yields Hence

and letting completes the proof that . ∎

Proof of Theorem 2.7.

With defined by (2.1), condition (2.2) and Lemma 2.4 imply as . Therefore, for every , there exists such that

Thus implies or implies . By hypothesis, for every and , there is such that

Define . For , . Now let and . Hence

But since , we also have . Next, because as , there exists such that

Since , there is , so for . If , then

| (4.8) |

where . For , define the function by

By construction for all . Since is differentiable we have

Define

where . Then for or . Choosing guarantees that

Hence

and . From the preceding construction it follows that for all . Hence, from the definition of ,

It follows that and letting shows that

The lower bound is proved similarly and we refer the reader to Theorem 2.8. Since , we will have , as claimed.

We now establish the second part of (2.6), namely that . By hypothesis and the first part of (2.6), for an arbitrary (chosen so small that ), there exists such that

Therefore, for ,

Hence with , and with defined by for and ,

We show momentarily that

| (4.9) |

Using (4.9) yields

Since was chosen arbitrarily, letting yields , as required.

Now we return to the proof of (4.9). Clearly, and therefore there exists such that for all . Let and , then by using the monotonicity of we obtain

Since for , we have for

Letting yields

since as . Finally, as is increasing so

Since was chosen arbitrarily, letting it tend to zero gives the desired bound (4.9). ∎

Proof of Theorem 2.8.

Firstly, with arbitrary, rewrite (1.1) as follows

where . Define for , so

| (4.10) |

Hence

| (4.11) |

Note that . We claim

| (4.12) |

Suppose first that . In this case , but , and (4.12) holds.

Suppose next that . Since as , there is such that for all . By the continuity of and the number given by is well–defined, and in , even in the case when . Therefore, with , we have for all . Since for , the estimate

holds for . Therefore,

| (4.13) |

Since and are positive, tends to some or infinity as . Suppose the former pertains. Then, because , as , contradicting the hypothesis that . Thus, as , and the last quotient on the righthand side of (4.13) is an indeterminate limit as . But by l’Hôpital’s rule, and because ,

To complete the proof of (4.12) note that positivity of implies . Thus . Hence, because as ,

and (4.12) holds.

Equation (4.12) implies that for every there is such that for all . Hence for , . Then for ,

Integrating we obtain

Integrating by substitution with

Letting , we have

From (4.10) we have for and for we have . Hence

Therefore and hence . Letting we have and, since as by Lemma 2.4, this implies

We now proceed to compute the corresponding lower bound. Since , there exists such that , for all , with arbitrary. For

Letting for , it is straightforward to show that

Now define the lower comparison solution

and

Thus for ,

and . Now suppose that for , , but . Then implies and

Therefore

a contradiction. Hence for all . For , and thus by [8, Corollary 2], under (2.2). Hence

Thus

Recall Lemma 2.4 and let to obtain proving the first limit in (2.7).

Proof of Theorem 2.9.

The required lower bound, , can be derived exactly as in Theorem 2.8. For the upper bound, recall the estimate (4.11) from the proof of Theorem 2.8:

where for and .

Remark 4.1.

The stronger hypothesis (2.3) can be used to improve the estimate above . We state this improvement here for convenience. Using the mean value theorem, (2.3) and the first part of Lemma 2.5, estimate as follows:

| (4.14) |

where results from using the Mean Value Theorem. The differential inequality above is now linear in and can be solved explicitly; we will return to this estimate frequently.

Next, since , and

Hence

Thus for . Combine this estimate with (4.11) to obtain

Integrated the inequality above reads

Make the substitution to obtain

Define , so

Now combine equation (4.10) with the inequality above as follows:

for all Thus

and letting yields Recall Lemma 2.4 and let to obtain

Now assume that (2.3) holds and show that . Since is increasing there exists such that for all . Also, for all and owing to the divergence of there exists such that for all . Therefore, by positivity of ,

Then, since for all ,

and it follows immediately that

| (4.15) |

By hypothesis as and consequently

Furthermore, because preserves asymptotic equivalence (see Lemma 2.6 and note that it requires (2.3)),

Hence

Using the facts collected above compute as follows

Similarly, because , . Thus

Returning to (4.15) and using the limit above yields

Finally, let to give the desired conclusion. ∎

Proof of Theorem 2.10 .

Proof of Theorem 2.10 .

The first limit in (2.8) follows from positivity of , which implies

directly from (1.1), and setting in case of Theorem 2.11. The proof of the second limit in (2.8) is straightforward. By hypothesis and Proposition 2,

as . Therefore, for every there is such that for . But positive implies . Thus , or , for all . Hence . Letting gives the second part of (2.8).

∎

Proof of Theorem 2.11 (a.).

The hypotheses (2.12) and (2.3) imply that there exists and such that

| (4.16) |

Now use equation (4.16) to derive the following preliminary upper estimate on the size of the solution:

By L’Hôpital’s rule, and hence . By Proposition 2.4, and since by hypothesis,

| (4.17) |

for any nonnegative constants and . Thus there exists such that for all we have . By (2.11), and the previous estimate, there exists such that for all , . Combining this with our initial estimate we obtain

To ensure our comparison solution majorizes the true solution take , so . Hence

Define the upper comparison solution, , as follows:

| (4.18) |

where and . By construction, for all (this follows immediately via a “time of the first breakdown” argument). Applying the same estimation procedures as in Theorems 2.8 and 2.9 to , and in particular to the quantity , we obtain an estimate analogous to (4.1):

| (4.19) |

where . Note once more that the hypothesis (2.3) is needed to obtain the differential inequality (4.19). Before proceeding further with the line of argument from Theorem 2.9 we need to refine the estimate above. implies that and hence, by Lemma 2.5, . Therefore there exists a such that for all we have . Hence

as implies that there exists such that for all . Taking reciprocals of the previous inequality and apply it to the previous estimate of to obtain

Now let

to obtain the consolidated estimate

| (4.20) |

Let and solve the differential inequality above as follows

Integration yields

Hence

| (4.21) |

In the analysis which is required to show that the second term on the right-hand side of (4.21) is bounded it emerges that the first term on the right-hand side is also bounded so we immediately focus on the second term. Define

and restate (4.21) as

By inspection , so either or . Differentiating we obtain

Hence

| (4.22) |

Therefore, for sufficiently small,

| (4.23) |

Remark 4.2.

Note that the hypothesis implies that is eventually increasing and hence has a limit at infinity. If and , is eventually decreasing and . In this case for all and we will be unable to obtain the required estimates to continue the proof.

From (4.23), by asymptotic integration, the convergence and divergence of and are equivalent. Hence

In both cases

Therefore there exists such that for all . Thus, recalling (4.18),

Hence

Therefore, since for all , . Now let

| (4.24) |

One can compute a definite upper bound on in terms of the problem parameters as follows. Define and estimate as above

| (4.25) |

Using (4.24) there exists a such that

Return to (1.1), take absolute values and apply the estimates above as follows

| (4.26) |

Solving the inequalities above yields . In fact the second quantity is always larger so . ∎

Proof of Theorem 2.11 (b.).

Follow the argument of Theorem 2.11 exactly to equation (4.22), which we recall below.

Now implies . Thus as . Recall equation (4.21)

If , then and as . Thus, when as ,

Alternatively, if , , then

In both cases

Once more we conclude that and hence that . By an argument exactly analogous to that which completes the proof of Theorem 2.11 case we can show that . Now write

| (4.27) |

Because , or . Then, since , taking the limsup and liminf across (4.27) gives or . In both cases . Noting that as yields the second part of the conclusion. ∎

5. Proofs of Results for Stochastic Volterra Equations

Proof of Theorem 3.4.

The proof of this result follows directly from the argument used in the proof of Theorem 3.5 and the law of the iterated logarithm for continuous local martingales. ∎

Proof of Theorem 3.5.

We start by proving part (a), which covers the case when . Let be arbitrary, rewrite (1.4) in integral form and estimate as follows

| (5.1) |

Denote by the a.s. event on which is continuous. We now recall the law of the iterated logarithm for continuous local martingales (see Revuz and Yor [35, Ch. V, Ex. 1.15]) which states that if is a continuous local martingale with , then

where denotes the quadratic variation process of . In our case

and thus implies a.s.

Let be arbitrary. By hypothesis there exists such that

| (5.2) |

Define for . Note that and Proposition 2 imply Therefore, for every there exists such that

| (5.3) |

Similarly, by L’Hôpital’s rule,

Thus, again appealing to L’Hôpital’s rule, and moreover, for any , . Hence for every there exists such that

| (5.4) |

Combining (5.3) and (5.4) yields

Rearrange this inequality, let , and then let to obtain . Thus, by proceeding as above, for every there is such that

| (5.5) |

Since is concave, is convex and Therefore,

Take limits in (5.5) to give

and then let to yield . Therefore, for every there exists such that for Now, let , so

| (5.6) |

On the other hand, because a.s., there exists an almost sure event such that for all

Now let . Thus for all and ,

Using the estimate (5.2) on and the finiteness of we have

| (5.7) |

where .

Now since , we have from (5.6) that for all

| (5.8) |

At this point we note that we are in the same position as in the proof of Theorem 2.7 at equation (4). From here a calculation exactly analogous to that which completes the proof of Theorem 2.7 will yield

To prove part (b), let be arbitrary and rewrite (1.4) in integral form as before and take absolute values to obtain

Let be as before. By the Martingale Convergence Theorem (see Revuz and Yor [35, Ch. V, Prop. 1.8]), if is a continuous local martingale with , then

In our case,

and thus implies that exists and is finite a.s. Therefore, as is a.s. continuous, there exists an almost sure event such that for all

Thus for all and ,

Using the estimate (5.2) on and the finiteness of , we have

Lastly, define and so that

Note that this estimate is in precisely the form of (5). It is easy to show, as above, that obeys an estimate of the form (5.6) for all . Hence for all and for all , the estimate

| (5.9) |

holds. At this point we note that we are in the same position as in the proof of part (a) after (5.8), and exactly analogous calculations yield

∎

Proof of Corollary 3.6.

We first prove that a.s. by showing that cannot be bounded with positive probability. Suppose there exists an event , with positive probability, such that for all on . Now consider the linear SDE

The solution to the SDE above is given by . Furthermore, it can be shown that obeys a.s. and a.s. (see Appleby et al. [1, Theorem 4.1]). Write (1.4) as

Applying the variation of constants formula we obtain

With some simple estimation it follows that, on , , a contradiction. To show that a.s. we check obeys , so we can apply Theorem 3.5. By L’Hôpital’s rule

assuming the limit on the right–hand side exists. In fact

Hence and . ∎

Proof of Theorem 3.7.

Let be arbitrary and follow the line of argument from the proof of Theorem 3.8 to obtain

where . We define the upper comparison solution as in (5.15) by

Now by (5.12) there exists such that

| (5.10) |

Let ; monotonicity yields

Hence there exists such that

| (5.11) |

For , using (5.11), calculate as follows

Integrating the previous inequality we obtain

Hence making the substitution yields

where . Thus

Returning to (5.10) and using the estimate above we obtain, for ,

It immediately follows that

Let and note that by construction for all . Therefore,

as required. ∎

Proof of Theorem 3.8.

By L’Hôpital’s rule, and hence

. Therefore, using Proposition 2,

| (5.12) |

for any nonnegative constants and . Arguing as in the proof of Theorem 3.5, with and defined analogously, we have the initial estimate

where . By (5.12) there is such that for all . Hence

| (5.13) | ||||

| (5.14) |

where . Now define the function for by

| (5.15) |

By construction for all . Let , so

Since is increasing and there exists a such that for all we have

By the Mean Value Theorem there exists such that

| (5.16) |

where the final inequality follows from Lemma 2.5. Once more we exploit the Mean Value Theorem and the first part of Lemma 2.5 as follows

| (5.17) |

Hence (5) becomes

Let

Now apply the argument from the proof of Theorem 2.10 beginning at (4.19). Following this line of argument shows that

Returning to (5.15) this yields

Therefore

Thus

Hence we have that a.s.

Suppose that on an event of positive probability, then there exists such that for all , . Let and estimate as before. For all , we obtain

| (5.18) |

Hence

Therefore, because , on . It follows that there exists such that for all . Consider the stochastic integral equation

For all and ,

This implies that for all and for all . Hence on and similarly on , a contradiction. Hence and

From (5) we obtain the following a.s. estimate

If we have , then we can choose sufficiently small that and monotonicity of and will yield , as before. If , we can estimate via the second part of Lemma 2.5. Suppose , then

and letting we obtain a.s. Therefore

Finally . Thus, a.s. and similarly a.s. ∎

Proof of Theorem 3.9.

We follow closely the line of argument from the proof of Theorem 3.8. First we establish the required analogue of (5.12). , so by Proposition 2 . Hence, for any nonnegative constants and ,

With this result in hand we can proceed with the argument from Theorem 3.8 to obtain

where . Define as in (5.15) and with the same estimation as before Therefore, since ,

Note that a.s for all and let to conclude that

The event on which is shown to have probability zero by exactly the line of argument which concludes the proof of Theorem 3.8. Hence a.s. and for all on an event of probability one. Once more using the notation that we recall the a.s. estimate (5)

Using the monotonicity of , an estimate of the form (5) and the hypothesis that ,

Hence a.s. and the claim (3.10) is proven. Now compute as follows

Taking the liminf, rather than the limsup, in the equation above yields a.s., concluding the proof. ∎

Proof of Theorem 3.12.

Proof of Theorem 3.13.

Suppose that and both satisfy the hypotheses on with and . It follows that

| (5.19) |

Relevant properties of –stable processes can be found in Bertoin [12, Theorem 5, Ch. VIII].

We first deal with the claim that a.s. when . Analogous to the beginning of the proof of Theorem 3.8 use Proposition 2 to show that

for any nonnegative constants and . With the estimate above in hand and the proof proceeds as in that of Theorem 3.8 but we arrive at a slightly different initial upper estimate to that derived in equation (5.13) since we employ (5.19) for the asymptotics of . In this case

| (5.20) |

where . Now we are free to define the comparison solution

| (5.21) |

By following exactly the steps from the proof of Theorem 3.8 we obtain with probability one and hence

| (5.22) |

With the usual notation that write

To finally derive the required bound on estimate using (5.22) (as was done in the proof of Theorem 3.8, for example); conclude by plugging in this estimate above and using (5.19).

The proof is essentially the same when . To show that a.s. proceed as before in applying the argument of Theorem 3.8 but note now that this will give for the comparison solution. The conclusion now follows readily.

It remains to show that a.s. Begin by assuming to the contrary that there exists an event with positive probability on which . We first show that on an event of positive probability; work on and estimate as follows

| (5.23) |

for sufficiently large and (the last inequality uses Lemma 2.5). Divide by and take the limsup across (5); the final term on the right–hand side can be dealt with using the hypothesis , the first two terms are and hence we obtain

Therefore the following holds on an event of positive probability

in contradiction of the fact that a.s. ∎

References

- [1] J. A. Appleby, J. Cheng, and A. Rodkina. Characterisation of the asymptotic behaviour of scalar linear differential equations with respect to a fading stochastic perturbation. Discrete & Contininuous Dynamical Systems Supplement, pages 79–90, 2011.

- [2] J. A. Appleby, S. Devin, and D. W. Reynolds. Mean square convergence of solutions of linear stochastic Volterra equations to non–equilibrium limits. Dynam. Con. Disc. Imp. Sys. Ser A Math Anal. B, 13:515–534, 2005.

- [3] J. A. Appleby, S. Devin, and D. W. Reynolds. Almost sure convergence of solutions of linear stochastic Volterra equations to nonequilibrium limits. Journal of Integral Equations and Applications, pages 405–437, 2007.

- [4] J. A. Appleby and D. D. Patterson. Growth rates of solutions of superlinear ordinary differential equations. Applied Mathematics Letters, 71:30–37, 2017.

- [5] J. A. Appleby and D. D. Patterson. Memory dependent growth in sublinear Volterra differential equations. Journal of Integral Equations and Applications, 29(4):531–584, 2017.

- [6] J. A. Appleby and D. W. Reynolds. Non-exponential stability of scalar stochastic Volterra equations. Statistics & Probability letters, 62(4):335–343, 2003.

- [7] J. A. Appleby and A. Rodkina. Asymptotic stability of polynomial stochastic delay differential equations with damped perturbations. Functional Differential Equations, 12(1–2):35–66, 2004.

- [8] J. A. D. Appleby and D. D. Patterson. Growth rates of sublinear functional and Volterra differential equations. SIAM Journal on Mathematical Analysis, 50(2):2086–2110, 2018.

- [9] C. T. Baker and E. Buckwar. Numerical analysis of explicit one-step methods for stochastic delay differential equations. LMS Journal of Computation and Mathematics, 3:315–335, 2000.

- [10] J. Benhabib and A. Rustichini. Vintage capital, investment, and growth. Journal of Economic theory, 55(2):323–339, 1991.

- [11] M. A. Berger and V. J. Mizel. Volterra equations with Itô integrals — I. The Journal of Integral Equations, pages 187–245, 1980.

- [12] J. Bertoin. Lévy processes, volume 121. Cambridge University Press, 1998.

- [13] A. T. Bharucha-Reid. Random integral equations. Academic press, 1972.

- [14] I. Bihari. A generalization of a lemma of Bellman and its application to uniqueness problems of differential equations. Acta Mathematica Academiae Scientiarum Hungarica, 7(1):81–94, 1956.

- [15] N. H. Bingham, C. M. Goldie, and J. L. Teugels. Regular variation, volume 27. Cambridge University Press, 1989.

- [16] P. J. Brockwell and A. Lindner. Existence and uniqueness of stationary Lévy-driven CARMA processes. Stochastic Process. Appl., 119(8):2660–2681, 2009.

- [17] C. Corduneanu. Integral equations and applications. Cambridge University Press, 1991.

- [18] J. A. Dieudonné. Infinitesimal calculus. Hermann, 1971.

- [19] G. Gripenberg, S.-O. Londen, and O. Staffans. Volterra integral and functional equations, volume 34. Cambridge University Press, 1990.

- [20] P. Hartman. Ordinary Differential Equations. SIAM, 2nd edition edition, 2002.

- [21] V. Kolmanovskii and A. Myshkis. Applied Theory of Functional Differential Equations, volume 85. Springer Science & Business Media, 2012.

- [22] V. Kolmanovskii and A. Myshkis. Introduction to the theory and applications of functional differential equations, volume 463. Springer Science & Business Media, 2013.

- [23] O. Lipovan. Integral inequalities for retarded Volterra equations. Journal of Mathematical Analysis and Applications, 322(1):349–358, 2006.

- [24] X. Mao. Exponential stability of equidistant Euler–Maruyama approximations of stochastic differential delay equations. Journal of Computational and Applied Mathematics, 200(1):297–316, 2007.

- [25] X. Mao. Stochastic Differential Equations and Applications. Horwood Publishing, 2nd edition, 2007.

- [26] X. Mao and M. Riedle. Mean square stability of stochastic Volterra integro-differential equations. Systems & Control Letters, 55(6):459–465, 2006.

- [27] T. Marquardt and R. Stelzer. Multivariate CARMA processes. Stochastic Process and their Applications, 117(1):96–120, 2007.

- [28] M. Métivier and J. Pellaumail. On a stopped Doob’s inequality and general stochastic equations. The Annals of Probability, pages 96–114, 1980.

- [29] S.-E. A. Mohammed and M. K. Scheutzow. Lyapunov exponents of linear stochastic functional differential equations driven by semimartingales. Part I: the multiplicative ergodic theory. In Annales de l’IHP Probabilités et statistiques, volume 32, pages 69–105, 1996.

- [30] S.-E. A. Mohammed and M. K. Scheutzow. The stable manifold theorem for non-linear stochastic systems with memory. I. existence of the semiflow. Journal of Functional Analysis, 205(2):271–305, 2003.

- [31] S.-E. A. Mohammed and M. K. Scheutzow. The stable manifold theorem for non-linear stochastic systems with memory: Ii. the local stable manifold theorem. Journal of Functional Analysis, 206(2):253–306, 2004.

- [32] D. Nualart and C. Rovira. Large deviations for stochastic Volterra equations. Bernoulli, pages 339–355, 2000.

- [33] M. Pituk. The Hartman–Wintner theorem for functional differential equations. Journal of Differential Equations, 155(1):1–16, 1999.

- [34] P. E. Protter. Stochastic integration and differential equation. Stochastic Modeling and Applied Probability, 21, 2004.

- [35] D. Revuz and M. Yor. Continuous martingales and Brownian motion, volume 293. Springer Science & Business Media, 1999.

- [36] D. Reynolds and J. Appleby. Decay rates of solutions of linear stochastic Volterra equations. Electronic Journal of Probability, 13:922–943, 2008.

- [37] L. Shaikhet. Lyapunov functionals and stability of stochastic functional differential equations. Springer Science & Business Media, 2013.

- [38] F. Wu and S. Hu. The LaSalle-type theorem for neutral stochastic functional differential equations with infinite delay. Discrete & Continuous Dynamical Systems-A, 32(3):1065, 2012.

- [39] F. Wu, S. Hu, and C. Huang. Robustness of general decay stability of nonlinear neutral stochastic functional differential equations with infinite delay. Systems & Control Letters, 59(3-4):195–202, 2010.

- [40] X. Zhang. Euler schemes and large deviations for stochastic Volterra equations with singular kernels. Journal of Differential Equations, 244(9):2226–2250, 2008.

Appendix A Examples & Numerical Experiments

Example 2.14.

for , with for some . We first show that which, combined with positivity of , yields .

Similarly,

and it then follows from (2.16) that Thus

| (A.1) |

We make the substitution in the integral term and define . Now estimate as follows

Combining this with (A) we obtain

| (A.2) |

It remains to make an asymptotic estimate of the integral term on the right–hand side of equation (A.2). Expanding yields

Hence and since , , as . Therefore

It is straightforward to show that as and thus

with a positive constant. Combining this with (A.2) yields

Before calculating we note that

Hence, by L’Hôpital’s rule,

Thus and , as claimed. ∎

Example 2.13.

Write

in order to work out the asymptotics of . Firstly,

Next

and hence this term will not affect the asymptotics of . Thus

Now suppose instead that we had

In this case

In order to choose freely in this example we must solve for , for a given . To simplify the calculation choose and , so we must solve , or equivalently, , where . It follows that and since we require select the solution (the so–called golden ratio). This yields . Finally,

∎

Example 2.15.

Suppose and let for , we have

Integrating we obtain

Therefore,

Using the fact that is sub-exponential and increasing we have

Now, from (2.16), we have It follows that . Finally,

∎

Example 2.16.

With , , , we have

Hence

Similarly,

since is sub-exponential and is sublinear. It follows from (2.16) that and hence

by the argument above for the limit of the reciprocal. ∎

Figure 1: Numerical Experiments

To investigate further the results from Section 3 numerically we consider the following test equation

| (A.3) |

Hence throughout this section. Let and rewrite (A.3) as a coupled system as follows

Various authors have shown that an explicit one step Euler–Maruyama discretisation reliably approximates solutions to equations of the type (A.3) in a mean–square sense for both fixed time lags and Volterra equations [9, 24]. In particular, we can have confidence in such a numerical scheme if we assume global Lipschitz and linear growth conditions on both and . Using an Euler–Maruyama discretisation of the coupled form of (A.3) we obtain, for ,

where is a normal random variable with mean zero and variance for each . We take

so that obeys a global linear bound and . We choose

so that and is a free parameter. It is straightforward to show that

In Figure 1 (left) we take , , and plot . The scaled process fluctuates between as it tends to zero a.s. As predicted by Theorem 3.8, the largest values of the scaled process are well approximated by . We also make a nonlinear transformation of the coordinates so that the convergence does not take place too quickly to observe. The co-ordinate transformation is given by with ; this nonlinear transformation is intended to be analogous to a log-log plot, typically used with non-negative data.