Low rank approximate solutions to large-scale differential matrix Riccati equations

Abstract

In the present paper, we consider large-scale continuous-time differential matrix Riccati equations. To the authors’ knowledge, the two main approaches proposed in the litterature are based on a splitting scheme or on a Rosenbrock / Backward Differentiation Formula (BDF) methods. The approach we propose is based on the reduction of the problem dimension prior to integration. We project the initial problem onto an extended block Krylov subspace and obtain a low-dimensional differential matrix Riccati equation. The latter matrix differential problem is then solved by a Backward Differentiation Formula (BDF) method and the obtained solution is used to reconstruct an approximate solution of the original problem. This process is repeated, increasing the dimension of the projection subspace until achieving a chosen accuracy. We give some theoretical results and a simple expression of the residual allowing the implementation of a stop test in order to limit the dimension of the projection space. Some numerical experiments will be given.

keywords:

Extended block Krylov, Low rank approximation, Differential matrix Riccati equations.1 Introduction

In this paper, we consider the continuous-time differential matrix Riccati equation (DRE in short) on the time interval of the form

| (1) |

where is some given low-rank matrix, is the unknown matrix function,

is assumed to be large, sparse and nonsingular, and . The matrices and are assumed to have full rank with .

Differential Riccati equations play a fundamental role in many areas such as control,

filter design theory, model reduction problems, differential

equations and robust control problems [1, 23, 24]. Differential matrix Riccati equations are also involved in game theory, wave propagation and scattering theory such as boundray value problems; see [1, 10]. In the last decades, some numerical methods have been proposed for approximating solutions of large scale algebraic Riccati equations [6, 18, 19, 20, 26].

Generally, the matrices , and are obtained from the

discretization of operators defined on infinite dimensional

subspaces. Moreover, the matrix is generally sparse, banded

and very large. For such problems, only a few attempts have been made to solve Equation (1), see [7] for instance.

In the present paper, we propose a projection method onto Krylov subspaces. The idea is to project the initial differential Riccati equation onto an extended block Krylov subspace of small dimension, solve the obtained low dimensional differential matrix equation and get approximate solutions to the initial differential matrix equations.

An expression of the solution of equation (1) is avalaible under some assumptions on the coefficient matrices , and , see [2] for more details. This result can be stated as follows.

Theorem 1

Assuming that is stabilizable and is observable and provided that , the differential Riccati equation (1) admits a unique solution given by

| (2) |

where is the positive definite solution of the ARE,

| (3) |

and is the positive definite solution of the Lyapunov equation

Unfortunately, the formula (2) is not suitable for large scale problems as it requires the computation of a matrix exponential, of an inverse matrix and various products of matrices.

The paper is organized as follows: In Section 2, we give some basic facts about the differential Riccati equation and the underlying finite-horizon LQR problem associated to a dynamical system and its cost function . In Section 3, we recall the extended block Arnoldi algorithm with some usefull classical algebraic properties. Section 4 is devoted to the BDF integration method that allows one to solve numerically differential Riccati equations. In Section 5, we introduce a new approach for the numerical resolution of a differential Riccati equation, based on a projection onto a sequence of block extended Krylov subspaces. The initial differential Riccati equation is projected onto such a subspace to get a low dimensional differential Riccati equation that is solved by the BDF method. We give some theoretical results on the norm of the residual and on the error. The projection finite horizon LQR problem is studied in Section 6. In the last section, we give some numerical experiments and also comparisons with different approaches.

Throughout this paper, we use the following notations: The 2-norm of matrices will be denoted by . . Finally, and will denote the identity of size and the zero matrix of size , respectively.

2 The finite-horizon LQR problem

The Linear Quadratic Regulator (LQR) problem is a well known design technique in the theory of optimal control. The system dynamics are described by a set of linear differential equations and the cost function is a quadratic function.

A linear quadratic regulator (LQR) problem can be described as follows. Let be the state vector of dimension , the control vector

and the output vector of length . We consider the following LQR problem with finite time-horizon (the continuous case ) [1, 13, 24, 27]:

For each initial state , find the optimal cost such that:

| (4) |

under the dynamic constrains

| (5) |

In addition, when a minimum exists, find an optimal input control which achieves this minimum, that is

| (6) |

where the optimal state and the corresponding output satisfy (5).

Assuming that the pair is stabilizable (i.e. there exists a matrix

such that is stable) and the pair is detectable (i.e.,

stabilizable), the optimal input minimizing the functional can be determined through a feedback operator such

that the feedback law is given by , where and

is the unique solution to the following differential Riccati equation

| (7) |

In addition, the optimal state trajectory satisfies and can also be expressed as

The optimal cost is given by the following quadratic function of the initial state ; (see [13])

| (8) |

We notice that if we set and , then

Then we recover the solution to the differential Riccati equation (1) and

For a thorough study on the existence and uniqueness of the solution of the DRE (1), see [1, 5, 13].

These results are summarized in the following theorem; (see [13])

Theorem 2

Assume that the pair is stabilizable and the pair is detectable. Then, the differential matrix Riccati equation (1) has a unique positive solution on and for any initial state , the optimal cost of is given by

where the optimal control is given by

and the optimal trajectory is determined by

Remark 1

For the infinite horizon case, the optimal cost is given by

where is the unique postitive and stabilizing solution of the algebraic Riccati equation

and the optimal feedback is given by .

Remark 2

For the discrete case, LQR finite-horizon problem is described as follows

| (9) |

under the discrete-dynamic constrains

| (10) |

The optimal control is given by

and is computed by solving the following discrete-time algebraic Riccati equation

When tends to infinity, we obtain the infinite-horizon discrete-time LQR and under some assumptions, is the unique positive definite solution to the discrete time algebraic Riccati equation (DARE)

In this paper, we consider only the continuous case which needs the development of efficient numerical methods that allow approximate solutions to the related large-scale differential Riccati matrix equation (1) .

3 The extended block Arnoldi algorithm

We first recall the extended block Arnoldi process applied to the pair where is nonsingular and . The projection subspace of which is considered in this paper was introduced in [16, 26].

Note that the subspace is a sum of two block Krylov subspaces

where .

The following algorithm allows us to compute an orthonormal basis of the extended Krylov subspace . This basis contains information on both and . Let be some fixed integer which limits the dimension of the constructed basis. Therefore The extended block Arnoldi process is described as follows:

-

1.

an matrix, an matrix and an integer.

-

2.

Compute the QR decomposition of , i.e., ;

Set ; -

3.

For

-

4.

Set : first columns of and : second columns of

-

5.

; .

-

6.

Orthogonalize w.r.t to get , i.e.,

For

;

;

Endfor -

7.

Compute the QR decomposition of , i.e., .

-

8.

Endfor .

Since the above algorithm implicitly involves a Gram-Schmidt process, the computed block vectors , have their columns mutually orthogonal provided none of the upper triangular matrices are rank deficient.

Hence, after steps, Algorithm 1 builds an orthonormal basis of the Krylov subspace

and a block upper Hessenberg matrix whose non zeros blocks are the . Note that each submatrix () is of order .

Let be the

restriction of the matrix to the extended Krylov subspace , i.e., . It is shown in [26] that is

also block upper Hessenberg with blocks.

Moreover, a recursion is derived to compute from without requiring matrix-vector products with . For

more details about the computation of from , we

refer to [26]. We note that for large problems, the

inverse of the matrix is not computed explicitly. Indeed, in many applications, the nonsingular matrix

is sparse and structured, allowing an effortless decomposition in order to compute the block . It is also possible to use iterative solvers with preconditioners to solve

linear systems with . However, when these linear systems are

not solved accurately, the theoretical properties of the extended

block Arnoldi process are no longer valid. The next identities will be of use in the sequel

Let , and suppose that steps of Algorithm 1 have been run, then we have

| (11) | |||||

| (12) |

where is the block of and is the matrix of the last columns of the identity matrix .

4 The BDF method for solving DREs

In this section, we recall some general facts about the well known BDF method which is a common choice for solving DREs. In the literature, to our knowledge, the integration methods (Rosenbrock, BDF) are directly applied to equation (1), [3, 7, 15]. At each timestep , the approximate of the , where is the solution to (1) is then computed solving an algebraic Riccati equation (ARE) [7]. We consider the general DRE (1) and apply the -step BDF method. At each iteration of the BDF method, the approximation of is given by the implicit relation

| (13) |

where is the step size, and are the coefficients of the BDF method as listed in Table 2 and is given by

| 1 | 1 | 1 | ||

|---|---|---|---|---|

| 2 | 2/3 | 4/3 | -1/3 | |

| 3 | 6/11 | 18/11 | -9/11 | 2/11 |

The approximate solves the following matrix equation

which can be written as the following continuous-time algebraic Riccati equation

| (14) |

Where, assuming that at each timestep, can be approximated as a product of low rank factors , , with (in practice, the matrices are never computed, as we will explain in a remark after Algorithm 2), the coefficients matrices are given by

These Riccati equations can be solved applying direct methods based on Schur decomposition, or based on generalized eigenvalues of the Hamiltonian in the small dimensional cases ([4, 28, 24]) or matrix sign function methods ([9, 21, 25]). When the dimension of the problem is large, this approach would be too demanding in terms of computation time and memory. In this case, iterative methods, as Krylov subspaces, Newton-type ([4, 6, 12, 22, 23, 17]) or ADI-type appear to be a standard choice, see ([8, 18, 19, 20]) for more details.

4.1 The BDF+Newton+EBA method

As explained in the previous subsection, at each time step , the approximation of is computed solving the large-scale ARE (14) which can be expressed as the nonlinear equation

| (15) |

where is the matrix-valued function defined by

| (16) |

where

, , , and

In the small dimensional case, direct methods, as Bartel Stewart algorithm is a usual choice for solving the symmetric Riccati equation (15). For large-scale problems, a common strategy consists in applying the inexact Newton-Kleinman’s method combined with an iterative method for the numerical resolution of the large-scale Lyapunov equations arising at each internal iteration of the Newton’s algorithm, or a block Krylov projection method directly applied to (15).

Omitting to mention the index in in our notations, we define a sequence of approximates to as follows:

-

1.

Set

-

2.

Build the sequence defined by

(17)

where the Fréchet derivative of at is given by

| (18) |

A straightforward calculation proves that is the solution to the Lyapunov equation

| (19) |

Assuming that all the ’s involved in can be approximated as products of low-rank factors, ie , we numerically solve (19) applying the Extended-Block-Arnoldi (EBA) method introduced in [18, 26]. As mentioned in [7], in order to avoid using complex arithmetics, the constant term of member of (19) can be splitted into two terms, separating the positive ’s from the negative ones. This yields a pair of Lyapunov equations and that have to be numerically solved at each Newton’s iteration. Then, the solution to (19) is obtained by substracting the solutions of and .

In the numerical examples, we will refer to this method as BDF-Newton-EBA and we will compare its performances against the ”reverse” method introduced in the next section.

5 Projecting and solving the low dimensional DRE

In this section, we propose a new approach to obtain low rank approximate solution to the differential Riccati equation (1). Instead of applying the integration scheme to the original problem (1), we first reduce the dimension of the problem by projection.

Let us apply, under the assumption that the matrix is nonsingular, the Extended Block Arnoldi (EBA) algorithm to the pair , generating the matrices and as described in section 2. For the sake of simplicity, we omit to mention the time variable in the formulae. Let be the desired approximate solution to (1) given as

| (20) |

satisfying the Galerkin orthogonality condition

| (21) |

where is the residual associated to the approximation . Then, from (20) and (21), we obtain the low dimensional differential Riccati equation

| (22) |

with , , where is the matrix of the first columns of the identity matrix and is the matrix obtained from the QR decomposition

| (23) |

At each timestep and for a given Extended Block Krylov projection subspace, applying a BDF() integration scheme, we have to solve a small dimensional continuous algebraic Riccati equation derived from (22) as explained in Section 3. This can be done by performing a direct method and we assume that it has a unique symmetric positive semidefinite and stabilizing solution . Nevertheless, the computations of and become increasingly expensive as gets larger. In order to stop the EBA iterations, it is desirable to be able to test if , where is some chosen tolerance, without having to compute extra matrix products involving the matrix . The next result gives an expression of the residual norm of which does not require the explicit calculation of the approximate . A factored form will be computed only when the desired accuracy is achieved. This approach will be denoted as Extended Block Arnoldi-BDF() method in the sequel.

Theorem 3

Let be the approximation obtained at step by the Extended Block Arnoldi-BDF() method and solves the low-dimensional differential Riccati equation (22), Then the residual satisfies

| (24) |

where is the matrix corresponding to the last rows of .

Proof 1

The result of Theorem 3 is important in practice, it allows us to stop the iteration when convergence is achieved without computing the approximate solution at each iteration. In our experiments, this test on the residual is performed at the final timestep. We summarize the steps of our method in the following algorithm

-

1.

Input , a tolerance , an integer and timestep . Set .

-

2.

Compute as low-rank products (*)

-

3.

For

-

4.

Compute an orthonormal basis of

-

5.

Set , and ,

-

6.

Apply BDF() to the projected DRE

-

7.

once is computed, if , then

-

8.

Endfor

-

9.

(whithout computing the product (**)

Let us give some important remarks on the preceding algorithm:

-

1.

In order to initialize the BDF() integration scheme, the approximates ,…, are computed by lower-order integration schemes. In our tests, we chose and was computed as a product of low-rank factors () by the Implicit Euler method BDF().

-

2.

During the integration process, as explained in Section 3, the constant term is updated at each timestep , taking into account the low-rank factor of the approximate factorization . This factorization does not require the computation of as it is obtained by performing a truncated single value decomposition of the small dimensional matrix. Consider the singular value decomposition of the matrix where is the diagonal matrix of the singular values of sorted in decreasing order. Let be the matrix of the first columns of corresponding to the singular values of magnitude greater than some tolerance . We obtain the truncated singular value decomposition where . Setting , it follows that

The following result shows that the approximation is an exact solution of a perturbed differential Riccati equation.

Theorem 4

Proof 2

Theorem 5

Let be the exact solution of (1) and let be the approximate solution obtained at step . The error satisfies the following equation

| (27) |

where is the residual given by

Proof 3

The result is easily obtained by subtracting the residual equation from the initial DRE (1).

6 The projected LQR problem

In this section, we consider the finite horizon LQR problem (9) and show how the extended block Arnoldi method can be used to give approximate costs to (9). At step of the extended block Arnoldi algorithm, let us consider the projected low order dynamical system obtained by projecting the original dynamical system (9) onto the extended block Krylov subspace :

| (28) |

where , and . Notice that for small values of the iteration number , is an approximation of the original large state .

Proposition 1

Assume at step that is stabilizable and that is detectable and consider the low dimension LQR problem with finite time-horizon:

Minimize

| (29) |

under the dynamic constrains (28). Then, the unique optimal feedback minimizing the cost function (29) is given by

where and is the unique stabilizing solution of (22).

The proof can be easily derived from the fact that is obtained from the projected Riccati equation (22) and also from the fact that the dynamical system (28) is obtained from a Galerkin projection of (10) onto the same extended block Krylov subspace.

The optimal projected state satisfies which can also be expressed as

and the optimal cost is given the following quadratic function of the initial state

| (30) | |||||

| (31) |

since where is the obtained approximate solution to (1). This shows clearly that the reduced optimal cost is an approximation of the initial minimal cost.

As already stated, the vector is an approximation of the original state vector . The corresponding feedback law is determined by where is the approximate solution to the differential matrix Riccati equation (7). Then

Now, using the fact that , it follows that

where .

Remark 3

It was shown in [13] that, assuming the pair to be stabilizable, is an increasing and symmetric positive set of matrices satisfying the differential Riccati equation (1) and that there exists a finite positive scalar such that for any initial state , we have

for every initial vector which shows that for all . Therefore, converges to a symmetric and positive matrix as : satisfying the following algebraic Riccati equation (see [13])

and is the only positive and stabilizing solution to this algebraic Riccati equation.

7 Numerical examples

In this section, in order to assess the interest of projecting the original equation before proceeding to the time integration, we compared the results given by the following approaches :

-

1.

EBA-BDF() method, as described in Section 5 (Algorithm 2) of the present paper.

-

2.

BDF()-Newton-EBA: as described in Section 4.1.

We also gave an example in which we compare our strategy to the Low-Rank Second-Order Splitting method (LRSOS for short) introduced by Stillfjord [27] and to the BDF-LR-ADI method introduced by Benner and Mena [7].

In the first three examples, the number of steps for the BDF() integration scheme was set to .

All the experiments were performed on a laptop with an Intel Core i7 processor and 8GB of RAM. The algorithms were coded in Matlab R2014b.

Example 1. The matrix was obtained from the 5-point discretization of the operators

on the unit square with homogeneous Dirichlet boundary conditions. The number of inner grid points in each direction is and the dimension of the matrix was . Here we set , , , , and . The entries of the matrices and were random values uniformly distributed on and the number of columns in and was set to . The initial condition was choosen as a low rank product , where was randomly generated.

We applied our approach combining a projection onto the Extended Block Krylov subspaces followed by a BDF integration scheme to small to medium size problems, with a tolerance of for the stop test on the residual. In our tests, we used a 2-step BDF scheme with a constant timestep . The first approximate was computed by the Implicit Euler scheme and the Extended Block Krylov method for Riccati equation, see [18] for more details.

To our knowledge, there is no available exact solution of large scale matrix Riccati differential equations in the literature. In order to check if our approaches produce reliable results, we began comparing our results to the one given by Matlab’s ode23s solver which is designed for stiff differential equations. This was done by vectorizing our DRE, stacking the columns of one on top of each other. This method, based on Rosenbrock integration scheme, is not suited to large-scale problems. The memory limitation of our computer allowed us a maximum size of for the matrix for the ode23s method.

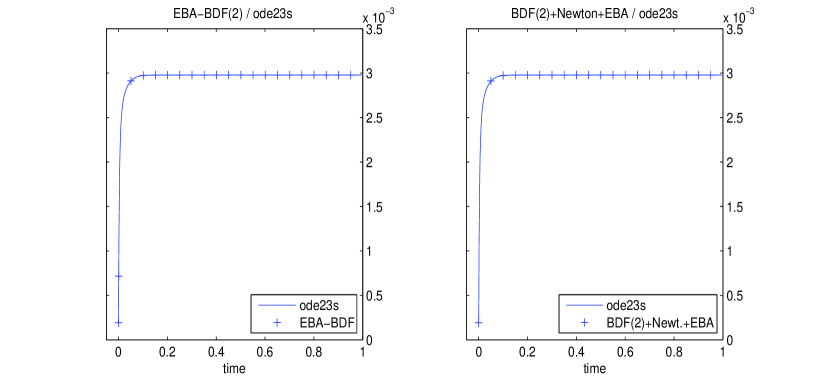

In Figure 1, we compared the component of the solution obtained by the methods tested in this section, to the solution provided by the ode23s method from matlab, on the time interval , for and a constant timestep .

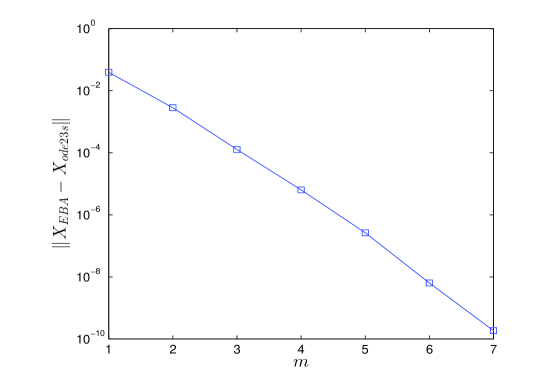

We observe that all the methods give similar results in terms of accuracy. Figure 2 features the norm of the difference , where is the solution obtained by the EBA-BDF method, at time versus the number of iterations of the Extended Arnoldi process. It shows that the two approximate solutions are very close for a moderate size of the projection space (). The ode23s solver took 510 seconds whereas our method gave an approximate solution in seconds.

In Table 2, we give the obtained runtimes in seconds, for the resolution of Equation (1) for , with a timestep . The figures illustrate that as the dimension of the problem gets larger, it is preferable to reduce the dimension of the problem prior to integration.

| size() | ode23s | EBA+BDF(2) | BDF(2)+Newton-EBA |

|---|---|---|---|

Example 2. In this example, we considered the same problem as in the previous example for medium to large dimensions. We kept the same settings as in Example 1, on the time interval . For all the tests, we applied the EBA+BDF(2) method and the timestep was set to . In Table 3, we reported the runtimes, residual norms and the number of the Extended Arnoldi iterations for various sizes of .

| size() | Runtime (s) | Residual norms | Number of iterations () |

|---|---|---|---|

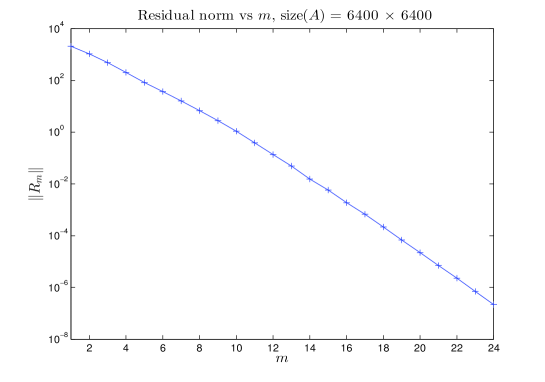

The next figure shows the norm of the residual versus the number of Extended Block Arnoldi iterations for the case.

As expected, Figure 3 shows that the accuracy improves as increases.

Example 3 This example was taken from [7] and comes from the autonomous linear-quadratic optimal control problem of one dimensional heat flow

Using a standard finite element approach based on the first order B-splines, we obtain the following ordinary differential equation

| (34) |

where the matrices and are given by:

Using the semi-implicit Euler method, we get the following discrete dynamical system

We set and . The entries of the matrix and the matrix were random values uniformly distributed on . We chose the initial condition as , where . In our experiments we used , and .

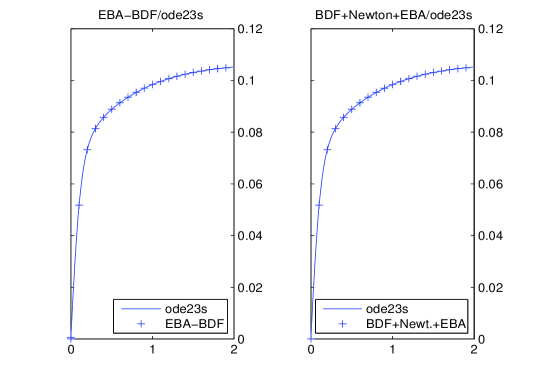

In Figure 4, we plotted the first component over the time interval of the approximate solutions obtained by the EBA-BDF(2), the BDF(2)-Newton-EBA methods and the ode23s solver. It again illustrates the similarity of the results in term of accuracy.

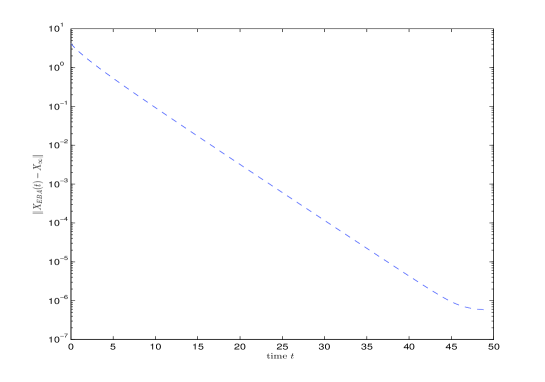

Figure 5 illustrates the remark of Proposition 1 in Section 6, claiming that under certain conditions, we have , where is the only positive and stabilizing solution to the ARE: . In order to do so, we plotted the norm of the difference in function of the time parameter on a relatively large time scale (), for an initial value , where is the matrix computed by the EBA-BDF(2) method. In this example, we have .

Table 4 reports on the computational times, residual norms and number of Krylov iteration, for various sizes of the coefficient matrices on the time interval . We only reported the results given for the EBA-BDF(2) method which clearly outperfoms the BDF(2)-Newton EBA method in terms of computational time. For instance, in the case where case, the BDF-Newton EBA method required seconds and more than seconds for .

| size() | Runtime (s) | Residual norms | number of iterations () |

|---|---|---|---|

Example 4 In this last example, we applied the EBA-BDF(1) method to the well-known problem Optimal Cooling of Steel Profiles. The matrices were extracted from the IMTEK collection 111https://portal.uni-freiburg.de/imteksimulation/downloads/benchmark. We compared the EBA-BDF(1) method to the splitting method LRSOP (in its Strang splitting variant) [27] and the BDF(1)-LR-ADI method [7], for sizes and , on the time interval . The initial value was choosen as , with . The code for the LRSOP method contains paralell loops which used 4 threads on our machine for this test. The BDF(1)-LR-ADI consists in applying the BDF(1) integration scheme to the original DRE (1). As for the BDF(p) Newton-EBA method presented in Section 4.1, it implies the numerical resolution of a potentially large-scale algebraic Riccati equation for each timestep. This resolution was performed via a the LR-ADI method, available in the M.E.S.S Package 222http://www.mpi-magdeburg.mpg.de/projects/mess/. For the LRSOS and BDF(1)-LR-ADI, the tolerance for column compression strategies were set to . The timestep was set to and the tolerance for the Arnoldi stop test was set to for the EBA-BDF(1) method and the projected equations were numerically solved by a dense solver (care from matlab) every 3 extended Arnoldi iterations.

| size | EBA-BDF(1) | LRSOS | BDF(1)-LR-ADI | LRSOS vs EBA-BDF(1) | EBA-BDF(1) vs BDF(1)-LR-ADI |

|---|---|---|---|---|---|

| s | s | s | |||

| s | s | s |

In Table 5, we listed the obtained runtimes and the relative errors , where denotes LRSOP or BDF(1)-LR-ADI, at final time . For the EBA-BDF(1), the number of Arnoldi iterations and the residual norms were , for and , for . This example shows that our method EBA-BDF is interesting in terms of execution time.

8 Conclusion

In this article, we have proposed a strategy consisting in projecting a large-scale differential problem onto a sequence of extended block Krylov subspaces and solving the projected matrix differential equation by a BDF integration scheme. The main purpose of this work was to show that projecting the original problem before integration gives encouraging results. In the case where the matrix is not invertible (or ill-conditioned), which is out of the scope of this paper, one could contemplate the use of the block-Arnoldi algorithm instead of the extended-block-Arnoldi method. We gave some theoretical results such as a simple expression of the residual which does not require the computation of products of large matrices and compared our approach experimentally to the common approach for which the integration scheme is directly applied to the large-scale original problem. Our experiments have shown that projecting before performing the time integration is interesting in terms of computational time.

Acknowledgements We would like to thank Dr. Tony Stillfjord for providing us with the codes of the low-rank second-order splitting (LRSOP) method and for his insightfull comments.

References

- [1] H. Abou-Kandil, G. Freiling, V. Ionescu, G. Jank, Matrix Riccati Equations in Control and Sytems Theory, in Systems & Control Foundations & Applications, Birkhauser, (2003).

- [2] B.D.O. Anderson, J.B. Moore, Linear Optimal Control, Prentice-Hall, Englewood Cliffs, NJ, (1971).

- [3] E. Arias, V. Hernández, J.J. Ibáñez and J. Peinado, A fixed point-based BDF method for solving differential Riccati equations, Appl. Math. and Comp., (188):1319–1333, (2007).

- [4] W.F. Arnold III, A.J. Laub, Generalized eigenproblem algorithms and software for algebraic Riccati equations, Pro., (72):1746–1754, (1984).

- [5] K. J. Astrm, Introduction to stochastic control theory. New York:Academic Press, 1970.

- [6] P. Benner, R. Byers, An exact line search method for solving generalized continous algebraic Riccati equations, IEEE Trans. Automat. Control, 43, (1):101–107, (1998).

- [7] P. Benner, H. Mena,BDF methods for large-scale differential Riccati equations,Proceedings of Mathematical Theory of Network and Systems (MTNS 2004), (2004).

- [8] A. Bouhamidi, M. Hached, K. Jbilou A Preconditioned Block Arnoldi Method for Large Scale Lyapunov and Algebraic Riccati Equations, Journal of Global Optimization, volume 65, 1, 19–23, (2016)

- [9] R. Byers, Solving the algebraic Riccati equation with the matrix sign function, Linear Alg. Appl., 85:267–279, (1987).

- [10] G. Caviglia, A. Morro, Riccati equations for wave propagation in planary-stratified solids, Eur. J. Mech. A/Solids, 19:721–741, (2000).

- [11] J.L. Casti, Linear Dynamical Systems, Mathematics in Science and Engineering, Academic Press, (1987).

- [12] J.P. Chehab, M. Raydan, Inexact Newton’s method with inner implicit preconditioning of algebraic Riccati equations, Comp. App. Math., 1–15, (2015), doi:10.1007/s40314-05-0274-8.

- [13] M. J. Corless and A. E. Frazho, Linear systems and control - An operator perspective, Pure and Applied Mathematics. Marcel Dekker, New York-Basel, 2003.

- [14] B.N. Datta, Numerical Methods for Linear Control Systems Design and Analysis, Elsevier Academic Press, (2003).

- [15] L. Dieci, Numerical Integration of the Differential Riccati Equation and Some Related Issues , SIAM J. NUMER. ANAL., Vol. 29, No. 3, pp. 781-815, (1992).

- [16] V. Druskin, L. Knizhnerman, Extended Krylov subspaces: approximation of the matrix square root and related functions, SIAM J. Matrix Anal. Appl., 19(3):755–771, (1998).

- [17] A.C.H. Guo, P. Lancaster, Analysis and modification of Newton’s method for algebraic Riccati equations, Math. Comp., 67:1089–1105, (1998).

- [18] M. Heyouni, K. Jbilou, An Extended Block Arnoldi algorithm for Large-Scale Solutions of the Continuous-Time Algebraic Riccati Equation, Electronic Transactions on Numerical Analysis, Volume 33, 53–62, (2009).

- [19] K. Jbilou, Block Krylov subspace methods for large continuous-time algebraic Riccati equations, Num. Alg., (34):339–353, (2003).

- [20] K. Jbilou, An Arnoldi based algorithm for large algebraic Riccati equations, Applied Mathematics Letters, (19):437–444, (2006).

- [21] C.S. Kenny, A.J. Laub, P. Papadopoulos, Matrix sign function algorithms for Riccati equations, In Proceedings of IMA Conference on Control: Modelling, Computation, Information, IEEE Computer Society Press, p:1–10, Southend-On-Sea, (1992).

- [22] D.L. Kleinman, On an iterative technique for Riccati equation computations, IEEC Trans. Autom. Contr., (13):114–115, (1968).

- [23] P. Lancaster, L. Rodman, The Algebraic Riccati Equations, Clarendon Press, Oxford, 1995.

- [24] V. Mehrmann, The autonomous Linear Quadratic Control Problem, theory and Numerical Solution, Number in Lecture Notes in Control and Information Sciences, Springer-Verlag, Heidelberg, (1991).

- [25] D.J. Roberts, Linear model reduction and solution of the algebraic Riccati equation by use of the sign function, Internt. J. Control, 32:677–687, (1998).

- [26] V. Simoncini, A new iterative method for solving large-scale Lyapunov matrix equations, SIAM J. Sci. Comp., 29(3):1268–1288, (2007).

- [27] T. Stillfjord, Low-rank second-order splitting of large-scale differential Riccati equations, IEEE Trans. Automat. Control 60(10), 2791–2796 (2015).

- [28] P. Van Dooren, A generalized eigenvalue approach for solving Riccati equations, SIAM J. Sci. Stat. Comput., 2:121–135, (1981).