2 Notation and Preliminaries

This section introduces notation and background

used throughout the paper. A generic

separable Hilbert space is denoted by ℍ ℍ \mathbb{H} < . , . > ℍ <.,.>_{\mathbb{H}} ∥ . ∥ ℍ \|.\|_{\mathbb{H}} ℍ ℍ \mathbb{H}

The

Hilbert space ℋ = L 2 ( [ 0 , 1 ] ) ℋ superscript 𝐿 2 0 1 \mathcal{H}=L^{2}\left(\left[0,1\right]\right) T 𝑇 T ℋ T superscript ℋ 𝑇 \mathcal{H}^{T}

⟨ f , g ⟩ ℋ = ∫ 0 1 f ( s ) g ¯ ( s ) 𝑑 s , f , g ∈ ℋ formulae-sequence subscript 𝑓 𝑔

ℋ superscript subscript 0 1 𝑓 𝑠 ¯ 𝑔 𝑠 differential-d 𝑠 𝑓

𝑔 ℋ \left\langle f,g\right\rangle_{\mathcal{H}}=\int_{0}^{1}f\left(s\right)\overline{g}\left(s\right)ds,\text{ \ \ \ }f,g\in\mathcal{H}

and

⟨ ( f 1 ⋯ f T ) ′ , ( g 1 ⋯ g T ) ′ ⟩ ℋ T = ∑ j = 1 T ⟨ f j , g j ⟩ ℋ , f j , g j ∈ ℋ , formulae-sequence subscript superscript subscript 𝑓 1 ⋯ subscript 𝑓 𝑇 ′ superscript subscript 𝑔 1 ⋯ subscript 𝑔 𝑇 ′

superscript ℋ 𝑇 superscript subscript 𝑗 1 𝑇 subscript subscript 𝑓 𝑗 subscript 𝑔 𝑗

ℋ subscript 𝑓 𝑗

subscript 𝑔 𝑗 ℋ \left\langle\left(\begin{array}[]{ccc}f_{1}&\cdots&f_{T}\end{array}\right)^{{}^{\prime}},\left(\begin{array}[]{ccc}g_{1}&\cdots&g_{T}\end{array}\right)^{{}^{\prime}}\right\rangle_{\mathcal{H}^{T}}=\sum_{j=1}^{T}\left\langle f_{j},g_{j}\right\rangle_{\mathcal{H}},\text{\ \ \ \ }f_{j},g_{j}\in\mathcal{H},

respectively. An operator Ψ Ψ \Psi ℍ ℍ \mathbb{H} ℂ p superscript ℂ 𝑝 \mathbb{C}^{p} Ψ 1 , … , Ψ p subscript Ψ 1 … subscript Ψ 𝑝

\Psi_{1},\ldots,\Psi_{p} ℍ ℍ \mathbb{H}

(2.1) Ψ ( h ) = ( ⟨ h , Ψ 1 ⟩ ℍ , … , ⟨ h , Ψ p ⟩ ℍ ) ′ , ∀ h ∈ ℍ . formulae-sequence Ψ ℎ superscript subscript ℎ subscript Ψ 1

ℍ … subscript ℎ subscript Ψ 𝑝

ℍ ′ for-all ℎ ℍ \Psi\left(h\right)=\left(\left\langle h,\Psi_{1}\right\rangle_{\mathbb{H}},\ldots,\left\langle h,\Psi_{p}\right\rangle_{\mathbb{H}}\right)^{{}^{\prime}},\text{ \ \ \ }\forall\ h\in\mathbb{H}.

An operator Υ Υ \Upsilon ℂ p superscript ℂ 𝑝 \mathbb{C}^{p} ℍ ℍ \mathbb{H} Υ 1 , … , Υ p subscript Υ 1 … subscript Υ 𝑝

\Upsilon_{1},\ldots,\Upsilon_{p} ℍ ℍ \mathbb{H}

Υ ( y ) = Υ ( ( y 1 , … , y p ) ′ ) = ∑ m = 1 p y m Υ m , ∀ y ∈ ℂ p . formulae-sequence Υ 𝑦 Υ superscript subscript 𝑦 1 … subscript 𝑦 𝑝 ′ superscript subscript 𝑚 1 𝑝 subscript 𝑦 𝑚 subscript Υ 𝑚 for-all 𝑦 superscript ℂ 𝑝 \Upsilon\left(y\right)=\Upsilon\left(\left(y_{1},\ldots,y_{p}\right)^{{}^{\prime}}\right)=\sum_{m=1}^{p}y_{m}\Upsilon_{m},\text{ \ \ \ }\forall\ y\in\mathbb{C}^{p}.

For any two elements f 𝑓 f g 𝑔 g ℍ ℍ \mathbb{H} f ⊗ g tensor-product 𝑓 𝑔 f\otimes g

f ⊗ g : ℍ ⟶ ℍ , f ⊗ g : h ⟼ ⟨ h , g ⟩ ℍ f . : tensor-product 𝑓 𝑔 ⟶ ℍ ℍ tensor-product 𝑓 𝑔

: ⟼ ℎ subscript ℎ 𝑔

ℍ 𝑓 f\otimes g:\mathbb{H\longrightarrow H},\ \ \ f\otimes g:h\longmapsto\left\langle h,g\right\rangle_{\mathbb{H}}f.

We use ∥ . ∥ ℒ \left\|.\right\|_{\mathcal{L}} ∥ . ∥ 𝒩 \left\|.\right\|_{\mathcal{N}} ∥ . ∥ 𝒮 \left\|.\right\|_{\mathcal{S}} [2012 ] ,

Section 13.5.

In the following L 2 ( ℍ , ( − π , π ] ) superscript 𝐿 2 ℍ 𝜋 𝜋 L^{2}\left(\mathbb{H},\left(-\pi,\pi\right]\right) ℍ ℍ \mathbb{H} ( − π , π ] 𝜋 𝜋 \left(-\pi,\pi\right] ( Ω , 𝒜 , ℙ ) Ω 𝒜 ℙ \left(\Omega,\mathcal{A},\mathbb{P}\right) ( − π , π ] 𝜋 𝜋 \left(-\pi,\pi\right] L 2 ( ℍ , Ω ) superscript 𝐿 2 ℍ Ω L^{2}\left(\mathbb{H},\Omega\right) X , Y ∈ L 2 ( ℍ , Ω ) 𝑋 𝑌

superscript 𝐿 2 ℍ Ω X,Y\in L^{2}\left(\mathbb{H},\Omega\right) Cov ( X , Y ) Cov 𝑋 𝑌 \mathrm{Cov}\left(X,Y\right)

Cov ( X , Y ) Cov 𝑋 𝑌 \displaystyle\mathrm{Cov}\left(X,Y\right) = \displaystyle= E [ ( X − E X ) ⊗ ( Y − E Y ) ] : ℍ ⟶ ℍ , : 𝐸 delimited-[] tensor-product 𝑋 𝐸 𝑋 𝑌 𝐸 𝑌 ⟶ ℍ ℍ \displaystyle E\left[\left(X-EX\right)\otimes\left(Y-EY\right)\right]:\mathbb{H\longrightarrow H},

Cov ( X , Y ) Cov 𝑋 𝑌 \displaystyle\mathrm{Cov}\left(X,Y\right) : : \displaystyle: h ⟼ E [ ⟨ h , ( Y − E Y ) ⟩ ℍ ( X − E X ) ] . ⟼ ℎ 𝐸 delimited-[] subscript ℎ 𝑌 𝐸 𝑌

ℍ 𝑋 𝐸 𝑋 \displaystyle h\longmapsto E\left[\left\langle h,\left(Y-EY\right)\right\rangle_{\mathbb{H}}\left(X-EX\right)\right].

Definition 2.1

Let X = { X t , t ∈ ℤ } 𝑋 subscript 𝑋 𝑡 𝑡

ℤ X=\left\{X_{t},t\in\mathbb{Z}\right\} ℍ ℍ \mathbb{H} E ‖ X t ‖ 2 < ∞ 𝐸 superscript norm subscript 𝑋 𝑡 2 E\|X_{t}\|^{2}<\infty X 𝑋 X T 𝑇 T

E X t 𝐸 subscript 𝑋 𝑡 \displaystyle EX_{t} = \displaystyle= E X t + T , ∀ t ∈ ℤ , 𝐸 subscript 𝑋 𝑡 𝑇 for-all 𝑡

ℤ \displaystyle EX_{t+T},\text{ \ \ }\forall\ t\in\mathbb{Z},

Cov ( X t , X s ) Cov subscript 𝑋 𝑡 subscript 𝑋 𝑠 \displaystyle\mathrm{Cov}\left(X_{t},X_{s}\right) = \displaystyle= Cov ( X t + T , X s + T ) , ∀ t , s ∈ ℤ . Cov subscript 𝑋 𝑡 𝑇 subscript 𝑋 𝑠 𝑇 for-all 𝑡 𝑠

ℤ \displaystyle\mathrm{Cov}\left(X_{t+T},X_{s+T}\right),\text{\ \ \ }\forall\ t,s\in\mathbb{Z}.

The smallest such T 𝑇 T X 𝑋 X T 𝑇 T T 𝑇 T T = 1 𝑇 1 T=1

For a T 𝑇 T X 𝑋 X h ℎ h

C h , ( j , j ′ ) X = Cov ( X T h + j , X j ′ ) , h ∈ ℤ and j , j ′ = 0 , 1 , … , T − 1 . formulae-sequence superscript subscript 𝐶 ℎ 𝑗 superscript 𝑗 ′

𝑋 Cov subscript 𝑋 𝑇 ℎ 𝑗 subscript 𝑋 superscript 𝑗 ′ formulae-sequence ℎ ℤ and 𝑗 superscript 𝑗 ′ 0 1 … 𝑇 1

C_{h,\left(j,j^{\prime}\right)}^{X}=\mathrm{Cov}\left(X_{Th+j},X_{j^{\prime}}\right),\text{ \ \ \ }h\in\mathbb{Z}\text{ and }j,j^{\prime}=0,1,\ldots,T-1.

It is easy to verify that the condition

(2.2) ∑ h ∈ ℤ ‖ C h , ( j , j ′ ) X ‖ 𝒮 < ∞ , j , j ′ = 0 , 1 , … , T − 1 , formulae-sequence subscript ℎ ℤ subscript norm superscript subscript 𝐶 ℎ 𝑗 superscript 𝑗 ′

𝑋 𝒮 𝑗

superscript 𝑗 ′ 0 1 … 𝑇 1

\sum_{h\in\mathbb{Z}}\left\|C_{h,\left(j,j^{\prime}\right)}^{X}\right\|_{\mathcal{S}}<\infty,\text{ \ \ \ }j,j^{{}^{\prime}}=0,1,\ldots,T-1,

implies that for each θ 𝜃 \theta { 1 2 π ∑ h = − n n C h , ( j , j ′ ) X e − i h θ : n ∈ ℤ + } conditional-set 1 2 𝜋 superscript subscript ℎ 𝑛 𝑛 superscript subscript 𝐶 ℎ 𝑗 superscript 𝑗 ′

𝑋 superscript 𝑒 𝑖 ℎ 𝜃 𝑛 subscript ℤ \left\{\frac{1}{2\pi}\sum_{h=\mathbb{-}n}^{n}C_{h,\left(j,j^{\prime}\right)}^{X}e^{-ih\theta}:n\in\mathbb{Z}_{+}\right\} ℍ ℍ \mathbb{H}

(2.3) ℱ θ , ( j , j ′ ) X = 1 2 π ∑ h ∈ ℤ C h , ( j , j ′ ) X e − i h θ , j , j ′ = 0 , … , T − 1 . formulae-sequence superscript subscript ℱ 𝜃 𝑗 superscript 𝑗 ′

𝑋 1 2 𝜋 subscript ℎ ℤ superscript subscript 𝐶 ℎ 𝑗 superscript 𝑗 ′

𝑋 superscript 𝑒 𝑖 ℎ 𝜃 𝑗

superscript 𝑗 ′ 0 … 𝑇 1

\mathcal{F}_{\theta,\left(j,j^{\prime}\right)}^{X}=\frac{1}{2\pi}\sum_{h\in\mathbb{Z}}C_{h,\left(j,j^{\prime}\right)}^{X}e^{-ih\theta},\text{ \ \ \ }j,j^{\prime}=0,\ldots,T-1.

Definition 2.2

A sequence { Ψ l , l ∈ ℤ } subscript Ψ 𝑙 𝑙

ℤ \left\{\Psi_{l},l\in\mathbb{Z}\right\} ℍ 1 subscript ℍ 1 \mathbb{H}_{1} ℍ 2 subscript ℍ 2 \mathbb{H}_{2}

(2.4) ∑ l ∈ ℤ ‖ Ψ l ‖ ℒ < ∞ , subscript 𝑙 ℤ subscript norm subscript Ψ 𝑙 ℒ \sum_{l\in\mathbb{Z}}\left\|\Psi_{l}\right\|_{\mathcal{L}}<\infty,

is called a filter. A T 𝑇 T { { Ψ l t , l ∈ ℤ } , t ∈ ℤ } superscript subscript Ψ 𝑙 𝑡 𝑙

ℤ 𝑡

ℤ \left\{\left\{\Psi_{l}^{t},l\in\mathbb{Z}\right\},t\in\mathbb{Z}\right\} T 𝑇 T t 𝑡 t Ψ l t = Ψ l t + T superscript subscript Ψ 𝑙 𝑡 superscript subscript Ψ 𝑙 𝑡 𝑇 \Psi_{l}^{t}=\Psi_{l}^{t+T} t 𝑡 t l 𝑙 l

(2.5) ∑ t = 0 T − 1 ∑ l ∈ ℤ ‖ Ψ l t ‖ ℒ < ∞ . superscript subscript 𝑡 0 𝑇 1 subscript 𝑙 ℤ subscript norm superscript subscript Ψ 𝑙 𝑡 ℒ \sum_{t=0}^{T-1}\sum_{l\in\mathbb{Z}}\left\|\Psi_{l}^{t}\right\|_{\mathcal{L}}<\infty.

Related to the filter { Ψ l , l ∈ ℤ } subscript Ψ 𝑙 𝑙

ℤ \left\{\Psi_{l},l\in\mathbb{Z}\right\} Ψ ( B ) Ψ 𝐵 \Psi\left(B\right) ( ℍ 1 ) ℤ superscript subscript ℍ 1 ℤ \left(\mathbb{H}_{1}\right)^{\mathbb{Z}} ( ℍ 2 ) ℤ superscript subscript ℍ 2 ℤ \left(\mathbb{H}_{2}\right)^{\mathbb{Z}}

Ψ ( B ) = ∑ l ∈ ℤ Ψ l B l , Ψ 𝐵 subscript 𝑙 ℤ subscript Ψ 𝑙 superscript 𝐵 𝑙 \Psi\left(B\right)=\sum_{l\in\mathbb{Z}}\Psi_{l}B^{l},

where B 𝐵 B { X t , t ∈ ℤ } subscript 𝑋 𝑡 𝑡

ℤ \left\{X_{t},t\in\mathbb{Z}\right\} ℍ 1 subscript ℍ 1 \mathbb{H}_{1} Ψ ( B ) Ψ 𝐵 \Psi\left(B\right) ℍ 2 subscript ℍ 2 \mathbb{H}_{2}

( Ψ ( B ) ( X ) ) t = ∑ l ∈ ℤ Ψ l ( X t − l ) . subscript Ψ 𝐵 𝑋 𝑡 subscript 𝑙 ℤ subscript Ψ 𝑙 subscript 𝑋 𝑡 𝑙 \left(\Psi\left(B\right)\left(X\right)\right)_{t}=\sum_{l\in\mathbb{Z}}\Psi_{l}\left(X_{t-l}\right).

For a p × p 𝑝 𝑝 p\times p 𝐀 𝐀 \mathbf{A} a q , r subscript 𝑎 𝑞 𝑟

a_{q,r} q 𝑞 q r 𝑟 r t = k T + d 𝑡 𝑘 𝑇 𝑑 t=kT+d k 𝑘 k t ≡ 𝑇 d 𝑡 𝑇 𝑑 t\overset{T}{\equiv}d

3 Principal component analysis of periodically correlated

functional time series

Before proceeding with the definitions and statements of

properties of the principal component analysis

for PC-FTS’s, we provide a brief introduction, focusing on the ideas and

omitting mathematical assumptions. Suppose { X t } subscript 𝑋 𝑡 \left\{X_{t}\right\} ℋ ℋ \mathcal{H}

(3.1) X t ( u ) = ∑ m = 1 ∞ ξ t m v m ( u ) , E ξ t m 2 = λ m , formulae-sequence subscript 𝑋 𝑡 𝑢 superscript subscript 𝑚 1 subscript 𝜉 𝑡 𝑚 subscript 𝑣 𝑚 𝑢 𝐸 superscript subscript 𝜉 𝑡 𝑚 2 subscript 𝜆 𝑚 X_{t}(u)=\sum_{m=1}^{\infty}\xi_{tm}v_{m}(u),\ \ \ E\xi_{tm}^{2}=\lambda_{m},

where the v m subscript 𝑣 𝑚 v_{m}

static FPC’s in [2015 ] ). The

orthonormal functions v m subscript 𝑣 𝑚 v_{m} ξ t m subscript 𝜉 𝑡 𝑚 \xi_{tm} dynamic FPC’s are not defined as one function for

every “frequency” level m 𝑚 m 3.1

(3.2) X t ( u ) = ∑ m = 1 ∞ ∑ l ∈ ℤ Y m , t + l ϕ m l ( u ) . subscript 𝑋 𝑡 𝑢 superscript subscript 𝑚 1 subscript 𝑙 ℤ subscript 𝑌 𝑚 𝑡 𝑙

subscript italic-ϕ 𝑚 𝑙 𝑢 X_{t}(u)=\sum_{m=1}^{\infty}\sum_{l\in{\mathbb{Z}}}Y_{m,t+l}\phi_{ml}(u).

A single function v m subscript 𝑣 𝑚 v_{m} { ϕ m l , l ∈ ℤ } subscript italic-ϕ 𝑚 𝑙 𝑙

ℤ \left\{\phi_{ml},l\in{\mathbb{Z}}\right\} m 𝑚 m Y m t = ∑ l ∈ ℤ ⟨ X t − l , ϕ m l ⟩ subscript 𝑌 𝑚 𝑡 subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 subscript italic-ϕ 𝑚 𝑙

Y_{mt}=\sum_{l\in{\mathbb{Z}}}\left\langle X_{t-l},\phi_{ml}\right\rangle λ m subscript 𝜆 𝑚 \lambda_{m}

ν m := E ‖ ∑ l ∈ ℤ Y m , t + l ϕ m l ‖ 2 , assign subscript 𝜈 𝑚 𝐸 superscript norm subscript 𝑙 ℤ subscript 𝑌 𝑚 𝑡 𝑙

subscript italic-ϕ 𝑚 𝑙 2 \nu_{m}:=E\left\|\sum_{l\in{\mathbb{Z}}}Y_{m,t+l}\phi_{ml}\right\|^{2},

and we have the decomposition of variance E ‖ X t ‖ 2 = ∑ m = 1 ∞ ν m 𝐸 superscript norm subscript 𝑋 𝑡 2 superscript subscript 𝑚 1 subscript 𝜈 𝑚 E\left\|X_{t}\right\|^{2}=\sum_{m=1}^{\infty}\nu_{m} All results stated in this section are proven in

Section 6

In order to define the dynamic functional principal components in our

setting, we first establish conditions for the existence of a filtered

(output) process of a T 𝑇 T T 𝑇 T X = { X t , t ∈ ℤ } 𝑋 subscript 𝑋 𝑡 𝑡

ℤ X=\left\{X_{t},t\in\mathbb{Z}\right\} T 𝑇 T { { Ψ l t , l ∈ ℤ } , t ∈ ℤ } superscript subscript Ψ 𝑙 𝑡 𝑙

ℤ 𝑡

ℤ \left\{\left\{\Psi_{l}^{t},l\in\mathbb{Z}\right\},t\in\mathbb{Z}\right\} 𝐘 = { 𝐘 t , t ∈ ℤ } 𝐘 subscript 𝐘 𝑡 𝑡

ℤ \mathbf{Y}=\left\{\mathbf{Y}_{t},t\in\mathbb{Z}\right\} ℂ p superscript ℂ 𝑝 \mathbb{C}^{p}

Theorem 3.1

Let X = { X t , t ∈ ℤ } 𝑋 subscript 𝑋 𝑡 𝑡

ℤ X=\left\{X_{t},t\in\mathbb{Z}\right\} ℋ ℋ \mathcal{H} T 𝑇 T { { Ψ l t , l ∈ ℤ } , t ∈ ℤ } superscript subscript Ψ 𝑙 𝑡 𝑙

ℤ 𝑡

ℤ \left\{\left\{\Psi_{l}^{t},l\in\mathbb{Z}\right\},t\in\mathbb{Z}\right\} T 𝑇 T ℋ ℋ \mathcal{H} ℂ p superscript ℂ 𝑝 \mathbb{C}^{p} Ψ l , m t , m = 1 , … , p formulae-sequence superscript subscript Ψ 𝑙 𝑚

𝑡 𝑚

1 … 𝑝

\Psi_{l,m}^{t},m=1,\ldots,p ℋ ℋ \mathcal{H} 2.1 2.5 t 𝑡 t ∑ l ∈ ℤ Ψ l t ( X ( t − l ) ) subscript 𝑙 ℤ superscript subscript Ψ 𝑙 𝑡 subscript 𝑋 𝑡 𝑙 \sum_{l\in\mathbb{Z}}\Psi_{l}^{t}\left(X_{\left(t-l\right)}\right) 𝐘 t subscript 𝐘 𝑡 \mathbf{Y}_{t}

If, in addition,

(3.3) ∑ t = 0 T − 1 ∑ l ∈ ℤ ‖ Ψ l t ‖ 𝒮 < ∞ , superscript subscript 𝑡 0 𝑇 1 subscript 𝑙 ℤ subscript norm superscript subscript Ψ 𝑙 𝑡 𝒮 \sum_{t=0}^{T-1}\sum_{l\in\mathbb{Z}}\left\|\Psi_{l}^{t}\right\|_{\mathcal{S}}<\infty,

then 𝐘 = { 𝐘 t , t ∈ ℤ } 𝐘 subscript 𝐘 𝑡 𝑡

ℤ \mathbf{Y}=\left\{\mathbf{Y}_{t},t\in\mathbb{Z}\right\} T 𝑇 T p × p 𝑝 𝑝 p\times p ℱ θ , ( d , f ) 𝐘 superscript subscript ℱ 𝜃 𝑑 𝑓

𝐘 \mathcal{F}_{\theta,\left(d,f\right)}^{\mathbf{Y}} d , f = 0 , … , T − 1 , formulae-sequence 𝑑 𝑓

0 … 𝑇 1

d,f=0,\ldots,T-1,

ℱ θ , ( d , f ) 𝐘 superscript subscript ℱ 𝜃 𝑑 𝑓

𝐘 \displaystyle\mathcal{F}_{\theta,\left(d,f\right)}^{\mathbf{Y}}

= [ ⟨ ( ℱ θ , ( 0 , 0 ) X ⋯ ℱ θ , ( 0 , T − 1 ) X ⋮ ⋱ ⋮ ℱ θ , ( T − 1 , 0 ) X ⋯ ℱ θ , ( T − 1 , T − 1 ) X ) ( Ψ θ , d , r d ⋮ Ψ θ , d − T + 1 , r d ) , ( Ψ θ , f , q f ⋮ Ψ θ , f − T + 1 , q f ) ⟩ ℋ T ] q , r = 1 , … , p absent subscript delimited-[] subscript superscript subscript ℱ 𝜃 0 0

𝑋 ⋯ superscript subscript ℱ 𝜃 0 𝑇 1

𝑋 ⋮ ⋱ ⋮ superscript subscript ℱ 𝜃 𝑇 1 0

𝑋 ⋯ superscript subscript ℱ 𝜃 𝑇 1 𝑇 1

𝑋 superscript subscript Ψ 𝜃 𝑑 𝑟

𝑑 ⋮ superscript subscript Ψ 𝜃 𝑑 𝑇 1 𝑟

𝑑 superscript subscript Ψ 𝜃 𝑓 𝑞

𝑓 ⋮ superscript subscript Ψ 𝜃 𝑓 𝑇 1 𝑞

𝑓

superscript ℋ 𝑇 formulae-sequence 𝑞 𝑟

1 … 𝑝

\displaystyle\ \ =\left[\left\langle\left(\begin{array}[]{ccc}\mathcal{F}_{\theta,\left(0,0\right)}^{X}&\cdots&\mathcal{F}_{\theta,\left(0,T-1\right)}^{X}\\

\vdots&\ddots&\vdots\\

\mathcal{F}_{\theta,\left(T-1,0\right)}^{X}&\cdots&\mathcal{F}_{\theta,\left(T-1,T-1\right)}^{X}\end{array}\right)\left(\begin{array}[]{c}\Psi_{\theta,d,r}^{d}\\

\vdots\\

\Psi_{\theta,d-T+1,r}^{d}\end{array}\right),\left(\begin{array}[]{c}\Psi_{\theta,f,q}^{f}\\

\vdots\\

\Psi_{\theta,f-T+1,q}^{f}\end{array}\right)\right\rangle_{\mathcal{H}^{T}}\right]_{q,r=1,\ldots,p}

where Ψ θ , d , q d = ∑ l ∈ ℤ Ψ T l + d , q d e i l θ , … , Ψ θ , d − T + 1 , q d = ∑ l ∈ ℤ Ψ T l + d − T + 1 , q d e i l θ , f , d = 0 , … , T − 1 formulae-sequence superscript subscript Ψ 𝜃 𝑑 𝑞

𝑑 subscript 𝑙 ℤ superscript subscript Ψ 𝑇 𝑙 𝑑 𝑞

𝑑 superscript 𝑒 𝑖 𝑙 𝜃 …

formulae-sequence superscript subscript Ψ 𝜃 𝑑 𝑇 1 𝑞

𝑑 subscript 𝑙 ℤ superscript subscript Ψ 𝑇 𝑙 𝑑 𝑇 1 𝑞

𝑑 superscript 𝑒 𝑖 𝑙 𝜃 𝑓

𝑑 0 … 𝑇 1

\Psi_{\theta,d,q}^{d}=\sum_{l\in\mathbb{Z}}\Psi_{Tl+d,q}^{d}e^{il\theta},\ldots,\Psi_{\theta,d-T+1,q}^{d}=\sum_{l\in\mathbb{Z}}\Psi_{Tl+d-T+1,q}^{d}e^{il\theta},f,d=0,\ldots,T-1

To illustrate the spectral density structure of the output process, we

consider T = 2 𝑇 2 T=2

ℱ θ , ( 0 , 0 ) 𝐘 = [ ⟨ ( ℱ θ , ( 0 , 0 ) X ℱ θ , ( 0 , 1 ) X ℱ θ , ( 1 , 0 ) X ℱ θ , ( 1 , 1 ) X ) ( Ψ θ , 0 , r 0 Ψ θ , − 1 , r 0 ) , ( Ψ θ , 0 , q 0 Ψ θ , − 1 , q 0 ) ⟩ ℋ 2 ] q , r = 1 , … , p , superscript subscript ℱ 𝜃 0 0

𝐘 subscript delimited-[] subscript superscript subscript ℱ 𝜃 0 0

𝑋 superscript subscript ℱ 𝜃 0 1

𝑋 superscript subscript ℱ 𝜃 1 0

𝑋 superscript subscript ℱ 𝜃 1 1

𝑋 superscript subscript Ψ 𝜃 0 𝑟

0 superscript subscript Ψ 𝜃 1 𝑟

0 superscript subscript Ψ 𝜃 0 𝑞

0 superscript subscript Ψ 𝜃 1 𝑞

0

superscript ℋ 2 formulae-sequence 𝑞 𝑟

1 … 𝑝

\mathcal{F}_{\theta,\left(0,0\right)}^{\mathbf{Y}}=\left[\left\langle\left(\begin{array}[]{cc}\mathcal{F}_{\theta,\left(0,0\right)}^{X}&\mathcal{F}_{\theta,\left(0,1\right)}^{X}\\

\mathcal{F}_{\theta,\left(1,0\right)}^{X}&\mathcal{F}_{\theta,\left(1,1\right)}^{X}\end{array}\right)\left(\begin{array}[]{c}\Psi_{\theta,0,r}^{0}\\

\Psi_{\theta,-1,r}^{0}\end{array}\right),\left(\begin{array}[]{c}\Psi_{\theta,0,q}^{0}\\

\Psi_{\theta,-1,q}^{0}\end{array}\right)\right\rangle_{\mathcal{H}^{2}}\right]_{q,r=1,\ldots,p},

ℱ θ , ( 1 , 0 ) 𝐘 = [ ⟨ ( ℱ θ , ( 0 , 0 ) X ℱ θ , ( 0 , 1 ) X ℱ θ , ( 1 , 0 ) X ℱ θ , ( 1 , 1 ) X ) ( Ψ θ , 1 , r 1 Ψ θ , 0 , r 1 ) , ( Ψ θ , 0 , q 0 Ψ θ , − 1 , q 0 ) ⟩ ℋ 2 ] q , r = 1 , … , p , superscript subscript ℱ 𝜃 1 0

𝐘 subscript delimited-[] subscript superscript subscript ℱ 𝜃 0 0

𝑋 superscript subscript ℱ 𝜃 0 1

𝑋 superscript subscript ℱ 𝜃 1 0

𝑋 superscript subscript ℱ 𝜃 1 1

𝑋 superscript subscript Ψ 𝜃 1 𝑟

1 superscript subscript Ψ 𝜃 0 𝑟

1 superscript subscript Ψ 𝜃 0 𝑞

0 superscript subscript Ψ 𝜃 1 𝑞

0

superscript ℋ 2 formulae-sequence 𝑞 𝑟

1 … 𝑝

\mathcal{F}_{\theta,\left(1,0\right)}^{\mathbf{Y}}=\left[\left\langle\left(\begin{array}[]{cc}\mathcal{F}_{\theta,\left(0,0\right)}^{X}&\mathcal{F}_{\theta,\left(0,1\right)}^{X}\\

\mathcal{F}_{\theta,\left(1,0\right)}^{X}&\mathcal{F}_{\theta,\left(1,1\right)}^{X}\end{array}\right)\left(\begin{array}[]{c}\Psi_{\theta,1,r}^{1}\\

\Psi_{\theta,0,r}^{1}\end{array}\right),\left(\begin{array}[]{c}\Psi_{\theta,0,q}^{0}\\

\Psi_{\theta,-1,q}^{0}\end{array}\right)\right\rangle_{\mathcal{H}^{2}}\right]_{q,r=1,\ldots,p},

ℱ θ , ( 0 , 1 ) 𝐘 = [ ⟨ ( ℱ θ , ( 0 , 0 ) X ℱ θ , ( 0 , 1 ) X ℱ θ , ( 1 , 0 ) X ℱ θ , ( 1 , 1 ) X ) ( Ψ θ , 0 , r 0 Ψ θ , − 1 , r 0 ) , ( Ψ θ , 1 , q 1 Ψ θ , 0 , q 1 ) ⟩ ℋ 2 ] q , r = 1 , … , p , superscript subscript ℱ 𝜃 0 1

𝐘 subscript delimited-[] subscript superscript subscript ℱ 𝜃 0 0

𝑋 superscript subscript ℱ 𝜃 0 1

𝑋 superscript subscript ℱ 𝜃 1 0

𝑋 superscript subscript ℱ 𝜃 1 1

𝑋 superscript subscript Ψ 𝜃 0 𝑟

0 superscript subscript Ψ 𝜃 1 𝑟

0 superscript subscript Ψ 𝜃 1 𝑞

1 superscript subscript Ψ 𝜃 0 𝑞

1

superscript ℋ 2 formulae-sequence 𝑞 𝑟

1 … 𝑝

\mathcal{F}_{\theta,\left(0,1\right)}^{\mathbf{Y}}=\left[\left\langle\left(\begin{array}[]{cc}\mathcal{F}_{\theta,\left(0,0\right)}^{X}&\mathcal{F}_{\theta,\left(0,1\right)}^{X}\\

\mathcal{F}_{\theta,\left(1,0\right)}^{X}&\mathcal{F}_{\theta,\left(1,1\right)}^{X}\end{array}\right)\left(\begin{array}[]{c}\Psi_{\theta,0,r}^{0}\\

\Psi_{\theta,-1,r}^{0}\end{array}\right),\left(\begin{array}[]{c}\Psi_{\theta,1,q}^{1}\\

\Psi_{\theta,0,q}^{1}\end{array}\right)\right\rangle_{\mathcal{H}^{2}}\right]_{q,r=1,\ldots,p},

ℱ θ , ( 1 , 1 ) 𝐘 = [ ⟨ ( ℱ θ , ( 0 , 0 ) X ℱ θ , ( 0 , 1 ) X ℱ θ , ( 1 , 0 ) X ℱ θ , ( 1 , 1 ) X ) ( Ψ θ , 1 , r 1 Ψ θ , 0 , r 1 ) , ( Ψ θ , 1 , q 1 Ψ θ , 0 , q 1 ) ⟩ ℋ 2 ] q , r = 1 , … , p , superscript subscript ℱ 𝜃 1 1

𝐘 subscript delimited-[] subscript superscript subscript ℱ 𝜃 0 0

𝑋 superscript subscript ℱ 𝜃 0 1

𝑋 superscript subscript ℱ 𝜃 1 0

𝑋 superscript subscript ℱ 𝜃 1 1

𝑋 superscript subscript Ψ 𝜃 1 𝑟

1 superscript subscript Ψ 𝜃 0 𝑟

1 superscript subscript Ψ 𝜃 1 𝑞

1 superscript subscript Ψ 𝜃 0 𝑞

1

superscript ℋ 2 formulae-sequence 𝑞 𝑟

1 … 𝑝

\mathcal{F}_{\theta,\left(1,1\right)}^{\mathbf{Y}}=\left[\left\langle\left(\begin{array}[]{cc}\mathcal{F}_{\theta,\left(0,0\right)}^{X}&\mathcal{F}_{\theta,\left(0,1\right)}^{X}\\

\mathcal{F}_{\theta,\left(1,0\right)}^{X}&\mathcal{F}_{\theta,\left(1,1\right)}^{X}\end{array}\right)\left(\begin{array}[]{c}\Psi_{\theta,1,r}^{1}\\

\Psi_{\theta,0,r}^{1}\end{array}\right),\left(\begin{array}[]{c}\Psi_{\theta,1,q}^{1}\\

\Psi_{\theta,0,q}^{1}\end{array}\right)\right\rangle_{\mathcal{H}^{2}}\right]_{q,r=1,\ldots,p},

where Ψ θ , 0 , q 0 := ∑ l ∈ ℤ Ψ 2 l , q 0 e i l θ assign superscript subscript Ψ 𝜃 0 𝑞

0 subscript 𝑙 ℤ superscript subscript Ψ 2 𝑙 𝑞

0 superscript 𝑒 𝑖 𝑙 𝜃 \Psi_{\theta,0,q}^{0}:=\sum_{l\in\mathbb{Z}}\Psi_{2l,q}^{0}e^{il\theta} Ψ θ , − 1 , q 0 := ∑ l ∈ ℤ Ψ 2 l − 1 , q 0 e i l θ assign superscript subscript Ψ 𝜃 1 𝑞

0 subscript 𝑙 ℤ superscript subscript Ψ 2 𝑙 1 𝑞

0 superscript 𝑒 𝑖 𝑙 𝜃 \Psi_{\theta,-1,q}^{0}:=\sum_{l\in\mathbb{Z}}\Psi_{2l-1,q}^{0}e^{il\theta} Ψ θ , 0 , q 1 := ∑ l ∈ ℤ Ψ 2 l , q 1 e i l θ assign superscript subscript Ψ 𝜃 0 𝑞

1 subscript 𝑙 ℤ superscript subscript Ψ 2 𝑙 𝑞

1 superscript 𝑒 𝑖 𝑙 𝜃 \Psi_{\theta,0,q}^{1}:=\sum_{l\in\mathbb{Z}}\Psi_{2l,q}^{1}e^{il\theta} Ψ θ , 1 , q 1 := ∑ l ∈ ℤ Ψ 2 l + 1 , q 1 e i l θ assign superscript subscript Ψ 𝜃 1 𝑞

1 subscript 𝑙 ℤ superscript subscript Ψ 2 𝑙 1 𝑞

1 superscript 𝑒 𝑖 𝑙 𝜃 \Psi_{\theta,1,q}^{1}:=\sum_{l\in\mathbb{Z}}\Psi_{2l+1,q}^{1}e^{il\theta}

We emphasize that (2.5 𝐘 𝐘 \mathbf{Y} 3.3 [2015 ] , page 327, discuss

this issue in the case of stationary input and output

processes. In the remainder of the paper, we assume (3.3

The operator matrix ( ℱ θ , ( d , f ) X ) 0 ≤ d , f ≤ T − 1 subscript superscript subscript ℱ 𝜃 𝑑 𝑓

𝑋 formulae-sequence 0 𝑑 𝑓 𝑇 1 \left(\mathcal{F}_{\theta,\left(d,f\right)}^{X}\right)_{0\leq d,f\leq T-1} 3.1 ℋ T superscript ℋ 𝑇 \mathcal{H}^{T} ℋ T superscript ℋ 𝑇 \mathcal{H}^{T}

(3.4) ( ℱ θ , ( d , f ) X ) 0 ≤ d , f ≤ T − 1 = ∑ m ≥ 1 λ θ , m φ θ , m ⊗ φ θ , m , subscript superscript subscript ℱ 𝜃 𝑑 𝑓

𝑋 formulae-sequence 0 𝑑 𝑓 𝑇 1 subscript 𝑚 1 tensor-product subscript 𝜆 𝜃 𝑚

subscript 𝜑 𝜃 𝑚

subscript 𝜑 𝜃 𝑚

\left(\mathcal{F}_{\theta,\left(d,f\right)}^{X}\right)_{0\leq d,f\leq T-1}=\sum_{m\geq 1}\lambda_{\theta,m}\varphi_{\theta,m}\otimes\varphi_{\theta,m},

where λ θ , 1 ≥ λ θ , 2 ≥ ⋯ ≥ 0 subscript 𝜆 𝜃 1

subscript 𝜆 𝜃 2

⋯ 0 \lambda_{\theta,1}\geq\lambda_{\theta,2}\geq\cdots\geq 0 { φ θ , m } m ≥ 1 subscript subscript 𝜑 𝜃 𝑚

𝑚 1 \left\{\varphi_{\theta,m}\right\}_{m\geq 1} ℋ T superscript ℋ 𝑇 \mathcal{H}^{T} ( Ψ θ , d , q d ⋯ Ψ θ , d − T + 1 , q d ) ′ superscript superscript subscript Ψ 𝜃 𝑑 𝑞

𝑑 ⋯ superscript subscript Ψ 𝜃 𝑑 𝑇 1 𝑞

𝑑 ′ \left(\begin{array}[]{ccc}\Psi_{\theta,d,q}^{d}&\cdots&\Psi_{\theta,d-T+1,q}^{d}\end{array}\right)^{\prime} φ θ , d p + q subscript 𝜑 𝜃 𝑑 𝑝 𝑞

\varphi_{\theta,dp+q} 𝐘 = { 𝐘 t , t ∈ ℤ } 𝐘 subscript 𝐘 𝑡 𝑡

ℤ \mathbf{Y}=\left\{\mathbf{Y}_{t},t\in\mathbb{Z}\right\} X 𝑋 X

Definition 3.1

Let X = { X t , t ∈ ℤ } 𝑋 subscript 𝑋 𝑡 𝑡

ℤ X=\left\{X_{t},t\in\mathbb{Z}\right\} ℋ ℋ \mathcal{H} T 𝑇 T 2.2 { Φ l , m d , d = 0 , … , T − 1 , m = 1 , … p , l ∈ ℤ } formulae-sequence superscript subscript Φ 𝑙 𝑚

𝑑 𝑑

0 … 𝑇 1 𝑚

1 … 𝑝 𝑙

ℤ \left\{\Phi_{l,m}^{d},d=0,\ldots,T-1,m=1,\ldots p,l\in\mathbb{Z}\right\} ℋ ℋ \mathcal{H}

(3.5) 1 2 π ∫ − π π φ θ , d p + m e − i l θ 𝑑 θ = ( Φ l T + d , m d ⋮ Φ l T + d − T + 1 , m d ) , m = 1 , … , p , d = 0 , … , T − 1 formulae-sequence 1 2 𝜋 superscript subscript 𝜋 𝜋 subscript 𝜑 𝜃 𝑑 𝑝 𝑚

superscript 𝑒 𝑖 𝑙 𝜃 differential-d 𝜃 superscript subscript Φ 𝑙 𝑇 𝑑 𝑚

𝑑 ⋮ superscript subscript Φ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑 formulae-sequence 𝑚 1 … 𝑝

𝑑 0 … 𝑇 1

\dfrac{1}{2\pi}\int_{-\pi}^{\pi}\varphi_{\theta,dp+m}e^{-il\theta}d\theta=\left(\begin{array}[]{c}\Phi_{lT+d,m}^{d}\\

\vdots\\

\Phi_{lT+d-T+1,m}^{d}\end{array}\right),\text{\ \ \ \ }m=1,\ldots,p,\text{\ }d=0,\ldots,T-1

for each l 𝑙 l ℤ ℤ \mathbb{Z}

(3.6) φ θ , d p + m = ( Φ θ , d , m d ⋮ Φ θ , d − T + 1 , m d ) , m = 1 , … , p , d = 0 , … , T − 1 , formulae-sequence subscript 𝜑 𝜃 𝑑 𝑝 𝑚

superscript subscript Φ 𝜃 𝑑 𝑚

𝑑 ⋮ superscript subscript Φ 𝜃 𝑑 𝑇 1 𝑚

𝑑 formulae-sequence 𝑚 1 … 𝑝

𝑑 0 … 𝑇 1

\varphi_{\theta,dp+m}=\left(\begin{array}[]{c}\Phi_{\theta,d,m}^{d}\\

\vdots\\

\Phi_{\theta,d-T+1,m}^{d}\end{array}\right),\text{\ \ \ \ }m=1,\ldots,p,\text{\ }d=0,\ldots,T-1,

for each θ 𝜃 \theta ( − π , π ] 𝜋 𝜋 \left(-\pi,\pi\right]

{ Φ l , m d , l ∈ ℤ } , d = 0 , … , T − 1 , formulae-sequence superscript subscript Φ 𝑙 𝑚

𝑑 𝑙

ℤ 𝑑

0 … 𝑇 1

\left\{\Phi_{l,m}^{d},l\in\mathbb{Z}\right\},\text{\ \ \ \ }d=0,\ldots,T-1,

is said to be the ( d , m ) 𝑑 𝑚 (d,m) X 𝑋 X

Y t , m subscript 𝑌 𝑡 𝑚

\displaystyle Y_{t,m} = \displaystyle= ∑ l ∈ ℤ ⟨ X ( t − l ) , Φ l , m d ⟩ subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 superscript subscript Φ 𝑙 𝑚

𝑑

\displaystyle\sum_{l\in\mathbb{Z}}\left\langle X_{\left(t-l\right)},\Phi_{l,m}^{d}\right\rangle

= \displaystyle= ∑ l ∈ ℤ ⟨ X ( t − l T − d ) , Φ l T + d , m d ⟩ + ∑ l ∈ ℤ ⟨ X ( t − l T − d + 1 ) , Φ l T + d − 1 , m d ⟩ subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 𝑇 𝑑 superscript subscript Φ 𝑙 𝑇 𝑑 𝑚

𝑑

subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 𝑇 𝑑 1 superscript subscript Φ 𝑙 𝑇 𝑑 1 𝑚

𝑑

\displaystyle\sum_{l\in\mathbb{Z}}\left\langle X_{\left(t-lT-d\right)},\Phi_{lT+d,m}^{d}\right\rangle+\sum_{l\in\mathbb{Z}}\left\langle X_{\left(t-lT-d+1\right)},\Phi_{lT+d-1,m}^{d}\right\rangle

+ ⋯ + ∑ l ∈ ℤ ⟨ X ( t − l T − d + T − 1 ) , Φ l T + d − T + 1 , m d ⟩ , m = 1 , … p , t ≡ 𝑇 d formulae-sequence ⋯ subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 𝑇 𝑑 𝑇 1 superscript subscript Φ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑

𝑚

1 … 𝑝 𝑡 𝑇 𝑑

\displaystyle+\cdots+\sum_{l\in\mathbb{Z}}\left\langle X_{\left(t-lT-d+T-1\right)},\Phi_{lT+d-T+1,m}^{d}\right\rangle,\text{\ \ \ \ }m=1,\ldots p,\text{\ }t\overset{T}{\equiv}d

will be called the ( t , m ) 𝑡 𝑚 (t,m) X 𝑋 X

For illustration, in case of T = 2 𝑇 2 T=2 m = 1 , … , p 𝑚 1 … 𝑝

m=1,\ldots,p

(3.8) 1 2 π ∫ − π π φ θ , m e − i l θ 𝑑 θ = ( Φ 2 l , m 0 Φ 2 l − 1 , m 0 ) and 1 2 π ∫ − π π φ θ , p + m e − i l θ 𝑑 θ = ( Φ 2 l + 1 , m 1 Φ 2 l , m 1 ) , 1 2 𝜋 superscript subscript 𝜋 𝜋 subscript 𝜑 𝜃 𝑚

superscript 𝑒 𝑖 𝑙 𝜃 differential-d 𝜃 superscript subscript Φ 2 𝑙 𝑚

0 superscript subscript Φ 2 𝑙 1 𝑚

0 and 1 2 𝜋 superscript subscript 𝜋 𝜋 subscript 𝜑 𝜃 𝑝 𝑚

superscript 𝑒 𝑖 𝑙 𝜃 differential-d 𝜃 superscript subscript Φ 2 𝑙 1 𝑚

1 superscript subscript Φ 2 𝑙 𝑚

1 \dfrac{1}{2\pi}\int_{-\pi}^{\pi}\varphi_{\theta,m}e^{-il\theta}d\theta=\left(\begin{array}[]{c}\Phi_{2l,m}^{0}\\

\Phi_{2l-1,m}^{0}\end{array}\right)\text{\ }\mathrm{and}\text{ }\dfrac{1}{2\pi}\int_{-\pi}^{\pi}\varphi_{\theta,p+m}e^{-il\theta}d\theta=\left(\begin{array}[]{c}\Phi_{2l+1,m}^{1}\\

\Phi_{2l,m}^{1}\end{array}\right),

for each l 𝑙 l ℤ ℤ \mathbb{Z}

φ θ , m = ( Φ θ , 0 , m 0 Φ θ , − 1 , m 0 ) and φ θ , p + m = ( Φ θ , 1 , m 1 Φ θ , 0 , m 1 ) , θ ∈ ( − π , π ] . formulae-sequence subscript 𝜑 𝜃 𝑚

superscript subscript Φ 𝜃 0 𝑚

0 superscript subscript Φ 𝜃 1 𝑚

0 and subscript 𝜑 𝜃 𝑝 𝑚

superscript subscript Φ 𝜃 1 𝑚

1 superscript subscript Φ 𝜃 0 𝑚

1 𝜃 𝜋 𝜋 \varphi_{\theta,m}=\left(\begin{array}[]{c}\Phi_{\theta,0,m}^{0}\\

\Phi_{\theta,-1,m}^{0}\end{array}\right)\text{\ }\mathrm{and}\text{ }\varphi_{\theta,p+m}=\left(\begin{array}[]{c}\Phi_{\theta,1,m}^{1}\\

\Phi_{\theta,0,m}^{1}\end{array}\right),\ \ \ \theta\in\left(-\pi,\pi\right].

The filters { Φ l , m d , l ∈ ℤ } superscript subscript Φ 𝑙 𝑚

𝑑 𝑙

ℤ \left\{\Phi_{l,m}^{d},l\in\mathbb{Z}\right\} d = 0 , 1 𝑑 0 1

d=0,1

The following proposition lists some useful properties of the

p 𝑝 p { 𝐘 t = ( Y t , 1 , … , Y t , p ) ′ , t ∈ ℤ } formulae-sequence subscript 𝐘 𝑡 superscript subscript 𝑌 𝑡 1

… subscript 𝑌 𝑡 𝑝

′ 𝑡 ℤ \left\{\mathbf{Y}_{t}=(Y_{t,1},\ldots,Y_{t,p})^{\prime},\ t\in\mathbb{Z}\right\} 3.1

Proposition 3.1

Let X = { X t , t ∈ ℤ } 𝑋 subscript 𝑋 𝑡 𝑡

ℤ X=\left\{X_{t},t\in\mathbb{Z}\right\} ℋ ℋ \mathcal{H} T 𝑇 T 2.2

(a)

the eigenfunctions φ m ( θ ) subscript 𝜑 𝑚 𝜃 \varphi_{m}\left(\theta\right) are Hermitian i.e. φ − θ , m = φ ¯ θ , m subscript 𝜑 𝜃 𝑚

subscript ¯ 𝜑 𝜃 𝑚

\varphi_{-\theta,m}=\overline{\varphi}_{\theta,m} and the DFPC scores Y t , m subscript 𝑌 𝑡 𝑚

Y_{t,m} are real-valued provided that X 𝑋 X

is real-valued;

(b)

for each ( t , m ) 𝑡 𝑚 (t,m) , the series ( 3.1 )

is mean-square convergent, has mean zero:

(3.9) E Y t , m = 0 , 𝐸 subscript 𝑌 𝑡 𝑚

0 EY_{t,m}=0,

and satisfies for t ≡ 𝑇 d 𝑡 𝑇 𝑑 t\overset{T}{\equiv}d ,

(3.10) E ‖ Y t , m ‖ 2 𝐸 superscript norm subscript 𝑌 𝑡 𝑚

2 \displaystyle E\left\|Y_{t,m}\right\|^{2} = ∑ j 1 , j 2 = 0 T − 1 ∑ k , l ∈ ℤ ⟨ C k − l , ( j 1 , j 2 ) X ( Φ k T + d − j 2 , m d ) , Φ l T + d − j 1 , m d ⟩ ℋ ; absent superscript subscript subscript 𝑗 1 subscript 𝑗 2

0 𝑇 1 subscript 𝑘 𝑙

ℤ subscript superscript subscript 𝐶 𝑘 𝑙 subscript 𝑗 1 subscript 𝑗 2

𝑋 superscript subscript Φ 𝑘 𝑇 𝑑 subscript 𝑗 2 𝑚

𝑑 superscript subscript Φ 𝑙 𝑇 𝑑 subscript 𝑗 1 𝑚

𝑑

ℋ \displaystyle=\sum\limits_{j_{1},j_{2}=0}^{T-1}\sum\limits_{k,l\in\mathbb{Z}}\left\langle C_{k-l,(j_{1},j_{2})}^{X}\left(\Phi_{kT+d-j_{2},m}^{d}\right),\Phi_{lT+d-j_{1},m}^{d}\right\rangle_{\mathcal{H}};

(c)

for any t 𝑡 t and s 𝑠 s , the DFPC scores Y t , m subscript 𝑌 𝑡 𝑚

Y_{t,m} and

Y s , m ′ subscript 𝑌 𝑠 superscript 𝑚 ′

Y_{s,m^{\prime}} are uncorrelated if s − t 𝑠 𝑡 s-t is not a multiple of T 𝑇 T or m ≠ m ′ 𝑚 superscript 𝑚 ′ m\neq m^{\prime} . In other words

C h , ( j 1 , j 2 ) 𝐘 = 0 superscript subscript 𝐶 ℎ subscript 𝑗 1 subscript 𝑗 2

𝐘 0 C_{h,\left(j_{1},j_{2}\right)}^{\mathbf{Y}}=0 for j 1 ≠ j 2 subscript 𝑗 1 subscript 𝑗 2 j_{1}\neq j_{2} and C h , ( j , j ) 𝐘 superscript subscript 𝐶 ℎ 𝑗 𝑗

𝐘 C_{h,(j,j)}^{\mathbf{Y}} are diagonal matrices for all

h ℎ h ;

(d)

the long-run covariance matrix of the filtered process { 𝐘 t , t ∈ ℤ } subscript 𝐘 𝑡 𝑡

ℤ \left\{\mathbf{Y}_{t},t\in\mathbb{Z}\right\} satisfies the following limiting equality

lim n → ∞ 1 n Var ( 𝐘 1 + ⋯ + 𝐘 n ) = 2 π T ∑ d = 0 T − 1 diag ( λ 0 , d p + 1 , … , λ 0 , d p + p ) . subscript → 𝑛 1 𝑛 Var subscript 𝐘 1 ⋯ subscript 𝐘 𝑛 2 𝜋 𝑇 superscript subscript 𝑑 0 𝑇 1 diag subscript 𝜆 0 𝑑 𝑝 1

… subscript 𝜆 0 𝑑 𝑝 𝑝

\lim_{n\rightarrow\infty}\frac{1}{n}\mathrm{Var}\left(\mathbf{Y}_{1}+\cdots+\mathbf{Y}_{n}\right)=\dfrac{2\pi}{T}\sum_{d=0}^{T-1}\mathrm{diag}\left(\lambda_{0,dp+1},\ldots,\lambda_{0,dp+p}\right).

For illustration, if T = 2 𝑇 2 T=2

E ‖ Y t , m ‖ 2 𝐸 superscript norm subscript 𝑌 𝑡 𝑚

2 \displaystyle E\left\|Y_{t,m}\right\|^{2} = \displaystyle= ∑ k ∈ ℤ ∑ l ∈ ℤ ⟨ C k − l , ( 0 , 0 ) X ( Φ 2 k , m 0 ) , Φ 2 l , m 0 ⟩ ℋ subscript 𝑘 ℤ subscript 𝑙 ℤ subscript superscript subscript 𝐶 𝑘 𝑙 0 0

𝑋 superscript subscript Φ 2 𝑘 𝑚

0 superscript subscript Φ 2 𝑙 𝑚

0

ℋ \displaystyle\sum_{k\in\mathbb{Z}}\sum_{l\in\mathbb{Z}}\left\langle C_{k-l,(0,0)}^{X}\left(\Phi_{2k,m}^{0}\right),\Phi_{2l,m}^{0}\right\rangle_{\mathcal{H}}

+ ∑ k ∈ ℤ ∑ l ∈ ℤ ⟨ C k − l , ( 0 , 1 ) X ( Φ 2 k − 1 , m 0 ) , Φ 2 l , m 0 ⟩ ℋ subscript 𝑘 ℤ subscript 𝑙 ℤ subscript superscript subscript 𝐶 𝑘 𝑙 0 1

𝑋 superscript subscript Φ 2 𝑘 1 𝑚

0 superscript subscript Φ 2 𝑙 𝑚

0

ℋ \displaystyle+\sum_{k\in\mathbb{Z}}\sum_{l\in\mathbb{Z}}\left\langle C_{k-l,(0,1)}^{X}\left(\Phi_{2k-1,m}^{0}\right),\Phi_{2l,m}^{0}\right\rangle_{\mathcal{H}}

+ ∑ k ∈ ℤ ∑ l ∈ ℤ ⟨ C k − l , ( 1 , 0 ) X ( Φ 2 k , m 0 ) , Φ 2 l − 1 , m 0 ⟩ ℋ subscript 𝑘 ℤ subscript 𝑙 ℤ subscript superscript subscript 𝐶 𝑘 𝑙 1 0

𝑋 superscript subscript Φ 2 𝑘 𝑚

0 superscript subscript Φ 2 𝑙 1 𝑚

0

ℋ \displaystyle+\sum_{k\in\mathbb{Z}}\sum_{l\in\mathbb{Z}}\left\langle C_{k-l,(1,0)}^{X}\left(\Phi_{2k,m}^{0}\right),\Phi_{2l-1,m}^{0}\right\rangle_{\mathcal{H}}

+ ∑ k ∈ ℤ ∑ l ∈ ℤ ⟨ C k − l , ( 1 , 1 ) X ( Φ 2 k − 1 , m 0 ) , Φ 2 l − 1 , m 0 ⟩ ℋ , t ≡ 2 0 subscript 𝑘 ℤ subscript 𝑙 ℤ subscript superscript subscript 𝐶 𝑘 𝑙 1 1

𝑋 superscript subscript Φ 2 𝑘 1 𝑚

0 superscript subscript Φ 2 𝑙 1 𝑚

0

ℋ 𝑡 2 0

\displaystyle+\sum_{k\in\mathbb{Z}}\sum_{l\in\mathbb{Z}}\left\langle C_{k-l,(1,1)}^{X}\left(\Phi_{2k-1,m}^{0}\right),\Phi_{2l-1,m}^{0}\right\rangle_{\mathcal{H}},\text{ \ \ \ \ }t\overset{2}{\equiv}0

and

E ‖ Y t , m ‖ 2 𝐸 superscript norm subscript 𝑌 𝑡 𝑚

2 \displaystyle E\left\|Y_{t,m}\right\|^{2} = \displaystyle= ∑ k ∈ ℤ ∑ l ∈ ℤ ⟨ C k − l , ( 1 , 1 ) X ( Φ 2 k , m 1 ) , Φ 2 l , m 1 ⟩ ℋ subscript 𝑘 ℤ subscript 𝑙 ℤ subscript superscript subscript 𝐶 𝑘 𝑙 1 1

𝑋 superscript subscript Φ 2 𝑘 𝑚

1 superscript subscript Φ 2 𝑙 𝑚

1

ℋ \displaystyle\sum_{k\in\mathbb{Z}}\sum_{l\in\mathbb{Z}}\left\langle C_{k-l,(1,1)}^{X}\left(\Phi_{2k,m}^{1}\right),\Phi_{2l,m}^{1}\right\rangle_{\mathcal{H}}

+ ∑ k ∈ ℤ ∑ l ∈ ℤ ⟨ C k − l , ( 1 , 0 ) X ( Φ 2 k + 1 , m 1 ) , Φ 2 l , m 1 ⟩ ℋ subscript 𝑘 ℤ subscript 𝑙 ℤ subscript superscript subscript 𝐶 𝑘 𝑙 1 0

𝑋 superscript subscript Φ 2 𝑘 1 𝑚

1 superscript subscript Φ 2 𝑙 𝑚

1

ℋ \displaystyle+\sum_{k\in\mathbb{Z}}\sum_{l\in\mathbb{Z}}\left\langle C_{k-l,(1,0)}^{X}\left(\Phi_{2k+1,m}^{1}\right),\Phi_{2l,m}^{1}\right\rangle_{\mathcal{H}}

+ ∑ k ∈ ℤ ∑ l ∈ ℤ ⟨ C k − l , ( 0 , 1 ) X ( Φ 2 k , m 1 ) , Φ 2 l + 1 , m 1 ⟩ ℋ subscript 𝑘 ℤ subscript 𝑙 ℤ subscript superscript subscript 𝐶 𝑘 𝑙 0 1

𝑋 superscript subscript Φ 2 𝑘 𝑚

1 superscript subscript Φ 2 𝑙 1 𝑚

1

ℋ \displaystyle+\sum_{k\in\mathbb{Z}}\sum_{l\in\mathbb{Z}}\left\langle C_{k-l,(0,1)}^{X}\left(\Phi_{2k,m}^{1}\right),\Phi_{2l+1,m}^{1}\right\rangle_{\mathcal{H}}

+ ∑ k ∈ ℤ ∑ l ∈ ℤ ⟨ C k − l , ( 0 , 0 ) X ( Φ 2 k + 1 , m 1 ) , Φ 2 l + 1 , m 1 ⟩ ℋ , t ≡ 2 1 . subscript 𝑘 ℤ subscript 𝑙 ℤ subscript superscript subscript 𝐶 𝑘 𝑙 0 0

𝑋 superscript subscript Φ 2 𝑘 1 𝑚

1 superscript subscript Φ 2 𝑙 1 𝑚

1

ℋ 𝑡 2 1

\displaystyle+\sum_{k\in\mathbb{Z}}\sum_{l\in\mathbb{Z}}\left\langle C_{k-l,(0,0)}^{X}\left(\Phi_{2k+1,m}^{1}\right),\Phi_{2l+1,m}^{1}\right\rangle_{\mathcal{H}},\text{ \ \ \ \ }t\overset{2}{\equiv}1.

The long-run covariance matrix is given by

lim n → ∞ 1 n Var ( 𝐘 1 + ⋯ + 𝐘 n ) = 2 π 2 [ diag ( λ 0 , 1 , … , λ 0 , p ) + diag ( λ 0 , p + 1 , … , λ 0 , 2 p ) ] . subscript → 𝑛 1 𝑛 Var subscript 𝐘 1 ⋯ subscript 𝐘 𝑛 2 𝜋 2 delimited-[] diag subscript 𝜆 0 1

… subscript 𝜆 0 𝑝

diag subscript 𝜆 0 𝑝 1

… subscript 𝜆 0 2 𝑝

\lim_{n\rightarrow\infty}\frac{1}{n}\mathrm{Var}\left(\mathbf{Y}_{1}+\cdots+\mathbf{Y}_{n}\right)=\dfrac{2\pi}{2}\left[\mathrm{diag}\left(\lambda_{0,1},\ldots,\lambda_{0,p}\right)+\mathrm{\ diag}\left(\lambda_{0,p+1},\ldots,\lambda_{0,2p}\right)\right].

The following theorem provides a formula for reconstructing the original ℋ ℋ \mathcal{H} X 𝑋 X { Y t , m , t ∈ ℤ , m ≥ 1 } formulae-sequence subscript 𝑌 𝑡 𝑚

𝑡

ℤ 𝑚 1 \left\{Y_{t,m},t\in\mathbb{Z},m\geq 1\right\}

Theorem 3.2

(Inversion Formula) Let X = { X t , t ∈ ℤ } 𝑋 subscript 𝑋 𝑡 𝑡

ℤ X=\left\{X_{t},t\in\mathbb{Z}\right\} ℋ ℋ \mathcal{H} T 𝑇 T { Y t , m , t ∈ ℤ , m ≥ 1 } formulae-sequence subscript 𝑌 𝑡 𝑚

𝑡

ℤ 𝑚 1 \left\{Y_{t,m},t\in\mathbb{Z},m\geq 1\right\} t 𝑡 t m 𝑚 m X t , m subscript 𝑋 𝑡 𝑚

X_{t,m}

X t , m subscript 𝑋 𝑡 𝑚

\displaystyle X_{t,m} : : \displaystyle: = ∑ l ∈ ℤ Y t + l T − d , m Φ l T − d , m 0 + ∑ l ∈ ℤ Y t + l T − d + 1 , m Φ l T − d + 1 , m 1 absent subscript 𝑙 ℤ subscript 𝑌 𝑡 𝑙 𝑇 𝑑 𝑚

superscript subscript Φ 𝑙 𝑇 𝑑 𝑚

0 subscript 𝑙 ℤ subscript 𝑌 𝑡 𝑙 𝑇 𝑑 1 𝑚

superscript subscript Φ 𝑙 𝑇 𝑑 1 𝑚

1 \displaystyle=\sum_{l\in\mathbb{Z}}Y_{t+lT-d,m}\Phi_{lT-d,m}^{0}+\sum_{l\in\mathbb{Z}}Y_{t+lT-d+1,m}\Phi_{lT-d+1,m}^{1}

+ ⋯ + ∑ l ∈ ℤ Y t + l T − d + T − 1 , m Φ l T − d + T − 1 , m T − 1 , t ≡ 𝑇 d ⋯ subscript 𝑙 ℤ subscript 𝑌 𝑡 𝑙 𝑇 𝑑 𝑇 1 𝑚

superscript subscript Φ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑇 1 𝑡 𝑇 𝑑

\displaystyle+\cdots+\sum_{l\in\mathbb{Z}}Y_{t+lT-d+T-1,m}\Phi_{lT-d+T-1,m}^{T-1},\text{\ \ \ \ }t\overset{T}{\equiv}d

Then,

X t subscript 𝑋 𝑡 \displaystyle X_{t} = \displaystyle= ∑ m ≥ 1 X t , m , t ≡ 𝑇 d , subscript 𝑚 1 subscript 𝑋 𝑡 𝑚

𝑡 𝑇 𝑑

\displaystyle\sum_{m\geq 1}X_{t,m},\text{\ \ \ \ }t\overset{T}{\equiv}d,

where the convergence holds in mean square provided that

(3.13) ∑ d = 0 T − 1 ∑ l ∈ ℤ ‖ Φ l , m d ‖ ℋ < ∞ . superscript subscript 𝑑 0 𝑇 1 subscript 𝑙 ℤ subscript norm superscript subscript Φ 𝑙 𝑚

𝑑 ℋ \sum_{d=0}^{T-1}\sum_{l\in\mathbb{Z}}\left\|\Phi_{l,m}^{d}\right\|_{\mathcal{H}}<\infty.

If T = 2 𝑇 2 T=2

X t , m := ∑ l ∈ ℤ Y t + 2 l , m Φ 2 l , m 0 + ∑ l ∈ ℤ Y t + 2 l + 1 , m Φ 2 l + 1 , m 1 , t ≡ 2 0 assign subscript 𝑋 𝑡 𝑚

subscript 𝑙 ℤ subscript 𝑌 𝑡 2 𝑙 𝑚

superscript subscript Φ 2 𝑙 𝑚

0 subscript 𝑙 ℤ subscript 𝑌 𝑡 2 𝑙 1 𝑚

superscript subscript Φ 2 𝑙 1 𝑚

1 𝑡 2 0

X_{t,m}:=\sum_{l\in\mathbb{Z}}Y_{t+2l,m}\Phi_{2l,m}^{0}+\sum_{l\in\mathbb{\ \ Z}}Y_{t+2l+1,m}\Phi_{2l+1,m}^{1},\text{\ \ \ \ }t\overset{2}{\equiv}0

X t , m := ∑ l ∈ ℤ Y t + 2 l − 1 , m Φ 2 l − 1 , m 0 + ∑ l ∈ ℤ Y t + 2 l , m Φ 2 l , m 1 , t ≡ 2 1 . assign subscript 𝑋 𝑡 𝑚

subscript 𝑙 ℤ subscript 𝑌 𝑡 2 𝑙 1 𝑚

superscript subscript Φ 2 𝑙 1 𝑚

0 subscript 𝑙 ℤ subscript 𝑌 𝑡 2 𝑙 𝑚

superscript subscript Φ 2 𝑙 𝑚

1 𝑡 2 1

X_{t,m}:=\sum_{l\in\mathbb{\ Z}}Y_{t+2l-1,m}\Phi_{2l-1,m}^{0}+\sum_{l\in\mathbb{Z}}Y_{t+2l,m}\Phi_{2l,m}^{1},\text{\ \ \ \ }t\overset{2}{\equiv}1.

The following theorem establishes an optimality property of the above DFPC

filter based on a mean square distance criterion.

Theorem 3.3

(Optimality) Let

X = { X t , t ∈ ℤ } 𝑋 subscript 𝑋 𝑡 𝑡

ℤ X=\left\{X_{t},t\in\mathbb{Z}\right\} ℋ ℋ \mathcal{H} T 𝑇 T { X t , m , t ∈ ℤ , m ≥ 1 } formulae-sequence subscript 𝑋 𝑡 𝑚

𝑡

ℤ 𝑚 1 \left\{X_{t,m},t\in\mathbb{Z},m\geq 1\right\} 3.2

For arbitrary ℋ ℋ \mathcal{H}

{ Ψ l , m t , t = 0 , … , T − 1 , m ≥ 1 , l ∈ ℤ } and { Υ l , m t , t = 0 , … , T − 1 , m ≥ 1 , l ∈ ℤ } \left\{\Psi_{l,m}^{t},t=0,\ldots,T-1,m\geq 1,l\in\mathbb{Z}\right\}\ \ {\rm and}\ \ \left\{\Upsilon_{l,m}^{t},t=0,\ldots,T-1,m\geq 1,l\in\mathbb{Z}\right\}

with ∑ t = 0 T − 1 ∑ l ∈ ℤ ‖ Ψ l , m t ‖ < ∞ superscript subscript 𝑡 0 𝑇 1 subscript 𝑙 ℤ norm superscript subscript Ψ 𝑙 𝑚

𝑡 \sum_{t=0}^{T-1}\sum_{l\in\mathbb{Z}}\left\|\Psi_{l,m}^{t}\right\|<\infty ∑ t = 0 T − 1 ∑ l ∈ ℤ ‖ Υ l , m t ‖ < ∞ superscript subscript 𝑡 0 𝑇 1 subscript 𝑙 ℤ norm superscript subscript Υ 𝑙 𝑚

𝑡 \sum_{t=0}^{T-1}\sum_{l\in\mathbb{Z}}\left\|\Upsilon_{l,m}^{t}\right\|<\infty m 𝑚 m

Y ~ t , m subscript ~ 𝑌 𝑡 𝑚

\displaystyle\widetilde{Y}_{t,m} = \displaystyle= ∑ l ∈ ℤ ⟨ X ( t − l ) , Ψ l , m d ⟩ subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 superscript subscript Ψ 𝑙 𝑚

𝑑

\displaystyle\sum_{l\in\mathbb{Z}}\left\langle X_{\left(t-l\right)},\Psi_{l,m}^{d}\right\rangle

= \displaystyle= ∑ l ∈ ℤ ⟨ X ( t − l T − d ) , Ψ l T + d , m d ⟩ + ∑ l ∈ ℤ ⟨ X ( t − l T − d + 1 ) , Ψ l T + d − 1 , m d ⟩ subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 𝑇 𝑑 superscript subscript Ψ 𝑙 𝑇 𝑑 𝑚

𝑑

subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 𝑇 𝑑 1 superscript subscript Ψ 𝑙 𝑇 𝑑 1 𝑚

𝑑

\displaystyle\sum_{l\in\mathbb{Z}}\left\langle X_{\left(t-lT-d\right)},\Psi_{lT+d,m}^{d}\right\rangle+\sum_{l\in\mathbb{Z}}\left\langle X_{\left(t-lT-d+1\right)},\Psi_{lT+d-1,m}^{d}\right\rangle

+ ⋯ + ∑ l ∈ ℤ ⟨ X ( t − l T − d + T − 1 ) , Ψ l T + d − T + 1 , m d ⟩ , t ≡ 𝑇 d ⋯ subscript 𝑙 ℤ subscript 𝑋 𝑡 𝑙 𝑇 𝑑 𝑇 1 superscript subscript Ψ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑

𝑡 𝑇 𝑑

\displaystyle+\cdots+\sum_{l\in\mathbb{Z}}\left\langle X_{\left(t-lT-d+T-1\right)},\Psi_{lT+d-T+1,m}^{d}\right\rangle,\text{\ \ \ \ }t\overset{T}{\equiv}d

and

X ~ t , m subscript ~ 𝑋 𝑡 𝑚

\displaystyle\widetilde{X}_{t,m} = \displaystyle= ∑ l ∈ ℤ Y ~ t + l T − d , m Υ l T − d , m 0 + ∑ l ∈ ℤ Y ~ t + l T − d + 1 , m Υ l T − d + 1 , m 1 subscript 𝑙 ℤ subscript ~ 𝑌 𝑡 𝑙 𝑇 𝑑 𝑚

superscript subscript Υ 𝑙 𝑇 𝑑 𝑚

0 subscript 𝑙 ℤ subscript ~ 𝑌 𝑡 𝑙 𝑇 𝑑 1 𝑚

superscript subscript Υ 𝑙 𝑇 𝑑 1 𝑚

1 \displaystyle\sum_{l\in\mathbb{Z}}\widetilde{Y}_{t+lT-d,m}\Upsilon_{lT-d,m}^{0}+\sum_{l\in\mathbb{Z}}\widetilde{Y}_{t+lT-d+1,m}\Upsilon_{lT-d+1,m}^{1}

+ ⋯ + ∑ l ∈ ℤ Y ~ t + l T − d + T − 1 , m Υ l T − d + T − 1 , m T − 1 , t ≡ 𝑇 d ⋯ subscript 𝑙 ℤ subscript ~ 𝑌 𝑡 𝑙 𝑇 𝑑 𝑇 1 𝑚

superscript subscript Υ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑇 1 𝑡 𝑇 𝑑

\displaystyle+\cdots+\sum_{l\in\mathbb{Z}}\widetilde{Y}_{t+lT-d+T-1,m}\Upsilon_{lT-d+T-1,m}^{T-1},\text{\ \ \ \ }t\overset{T}{\equiv}d

Then, the following inequality

holds for each t ∈ ℤ 𝑡 ℤ t\in\mathbb{Z} p ≥ 1 𝑝 1 p\geq 1

E ‖ X T t − ∑ m = 1 p X T t , m ‖ 2 + ⋯ + E ‖ X T t + T − 1 − ∑ m = 1 p X T t + T − 1 , m ‖ 2 𝐸 superscript norm subscript 𝑋 𝑇 𝑡 superscript subscript 𝑚 1 𝑝 subscript 𝑋 𝑇 𝑡 𝑚

2 ⋯ 𝐸 superscript norm subscript 𝑋 𝑇 𝑡 𝑇 1 superscript subscript 𝑚 1 𝑝 subscript 𝑋 𝑇 𝑡 𝑇 1 𝑚

2 \displaystyle E\left\|X_{Tt}-\sum_{m=1}^{p}X_{Tt,m}\right\|^{2}+\cdots+E\left\|X_{Tt+T-1}-\sum_{m=1}^{p}X_{Tt+T-1,m}\right\|^{2}

= \displaystyle= ∑ m > p ∫ − π π λ m ( θ ) 𝑑 θ subscript 𝑚 𝑝 superscript subscript 𝜋 𝜋 subscript 𝜆 𝑚 𝜃 differential-d 𝜃 \displaystyle\sum_{m>p}\int_{-\pi}^{\pi}\lambda_{m}\left(\theta\right)d\theta

≤ \displaystyle\leq E ‖ X T t − ∑ m = 1 p X ~ T t , m ‖ 2 + ⋯ + E ‖ X T t + T − 1 − ∑ m = 1 p X ~ T t + T − 1 , m ‖ 2 . 𝐸 superscript norm subscript 𝑋 𝑇 𝑡 superscript subscript 𝑚 1 𝑝 subscript ~ 𝑋 𝑇 𝑡 𝑚

2 ⋯ 𝐸 superscript norm subscript 𝑋 𝑇 𝑡 𝑇 1 superscript subscript 𝑚 1 𝑝 subscript ~ 𝑋 𝑇 𝑡 𝑇 1 𝑚

2 \displaystyle E\left\|X_{Tt}-\sum_{m=1}^{p}\widetilde{X}_{Tt,m}\right\|^{2}+\cdots+E\left\|X_{Tt+T-1}-\sum_{m=1}^{p}\widetilde{X}_{Tt+T-1,m}\right\|^{2}.

In practice, the scores Y t , m subscript 𝑌 𝑡 𝑚

Y_{t,m}

(3.14) Y ^ t , m subscript ^ 𝑌 𝑡 𝑚

\displaystyle\widehat{Y}_{t,m} = ∑ l = − L T + d − T + 1 L T + d ⟨ X t − l , Φ ^ l , m d ⟩ absent superscript subscript 𝑙 𝐿 𝑇 𝑑 𝑇 1 𝐿 𝑇 𝑑 subscript 𝑋 𝑡 𝑙 superscript subscript ^ Φ 𝑙 𝑚

𝑑

\displaystyle=\sum_{l=-LT+d-T+1}^{LT+d}\left\langle X_{t-l},\widehat{\Phi}_{l,m}^{d}\right\rangle

= ∑ l = − L L ⟨ X t − l T − d , Φ ^ l T + d , m d ⟩ + ⋯ absent superscript subscript 𝑙 𝐿 𝐿 subscript 𝑋 𝑡 𝑙 𝑇 𝑑 superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑚

𝑑

⋯ \displaystyle=\sum_{l=-L}^{L}\left\langle X_{t-lT-d},\widehat{\Phi}_{lT+d,m}^{d}\right\rangle+\cdots

+ ∑ l = − L L ⟨ X t − l T − d + T − 1 , Φ ^ l T + d − T + 1 , m d ⟩ , t ≡ 𝑇 d , superscript subscript 𝑙 𝐿 𝐿 subscript 𝑋 𝑡 𝑙 𝑇 𝑑 𝑇 1 superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑

𝑡 𝑇 𝑑

\displaystyle\ \ +\sum_{l=-L}^{L}\left\langle X_{t-lT-d+T-1},\widehat{\Phi}_{lT+d-T+1,m}^{d}\right\rangle,\text{\ }t\overset{T}{\equiv}d,

in which Φ ^ l , m d superscript subscript ^ Φ 𝑙 𝑚

𝑑 \widehat{\Phi}_{l,m}^{d} ℱ ^ θ , ( q , r ) X superscript subscript ^ ℱ 𝜃 𝑞 𝑟

𝑋 \widehat{\mathcal{F}}_{\theta,\left(q,r\right)}^{X} L 𝐿 L n 𝑛 n L 𝐿 L 4 5

We conclude this section by showing that under mild assumptions, E | Y ^ t , m − Y t , m | → 0 → 𝐸 subscript ^ 𝑌 𝑡 𝑚

subscript 𝑌 𝑡 𝑚

0 E\left|\widehat{Y}_{t,m}-Y_{t,m}\right|\to 0 3.4 3.1

Condition 3.1

The estimator ℱ ^ θ , ( q , r ) X superscript subscript ^ ℱ 𝜃 𝑞 𝑟

𝑋 \widehat{\mathcal{F}}_{\theta,\left(q,r\right)}^{X}

∫ − π π E ‖ ℱ θ , ( q , r ) X − ℱ ^ θ , ( q , r ) X ‖ 𝒮 2 ⟶ 0 , as n → 0 ; q , r = 0 , … , T − 1 . formulae-sequence ⟶ superscript subscript 𝜋 𝜋 𝐸 superscript subscript norm superscript subscript ℱ 𝜃 𝑞 𝑟

𝑋 superscript subscript ^ ℱ 𝜃 𝑞 𝑟

𝑋 𝒮 2 0 formulae-sequence → as 𝑛 0 𝑞

𝑟 0 … 𝑇 1

\int_{-\pi}^{\pi}E\left\|\mathcal{F}_{\theta,\left(q,r\right)}^{X}-\widehat{\mathcal{F}}_{\theta,\left(q,r\right)}^{X}\right\|_{\mathcal{S}}^{2}\longrightarrow 0,\text{ {as }}n\to 0;\text{\ \ \ \ }q,r=0,\ldots,T-1.

Condition 3.2

Let λ θ , m subscript 𝜆 𝜃 𝑚

\lambda_{\theta,m} 3.4 α θ , 1 := λ θ , 1 − λ θ , 2 assign subscript 𝛼 𝜃 1

subscript 𝜆 𝜃 1

subscript 𝜆 𝜃 2

\alpha_{\theta,1}:=\lambda_{\theta,1}-\lambda_{\theta,2} α θ , m := min { λ θ , m − 1 − λ θ , m , λ θ , m − λ θ , m + 1 } assign subscript 𝛼 𝜃 𝑚

subscript 𝜆 𝜃 𝑚 1

subscript 𝜆 𝜃 𝑚

subscript 𝜆 𝜃 𝑚

subscript 𝜆 𝜃 𝑚 1

\alpha_{\theta,m}:=\min\left\{\lambda_{\theta,m-1}-\lambda_{\theta,m},\lambda_{\theta,m}-\lambda_{\theta,m+1}\right\} m > 1 𝑚 1 m>1 m 𝑚 m { α θ , m : θ ∈ ( − π , π ] } conditional-set subscript 𝛼 𝜃 𝑚

𝜃 𝜋 𝜋 \left\{\alpha_{\theta,m}:\theta\in\left(-\pi,\pi\right]\right\}

Condition 3.2 θ ∈ ( − π , π ] 𝜃 𝜋 𝜋 \theta\in\left(-\pi,\pi\right] m 𝑚 m

Condition 3.3

Let φ θ , m subscript 𝜑 𝜃 𝑚

\varphi_{\theta,m} 3.4 ω 𝜔 \omega ℋ T superscript ℋ 𝑇 \mathcal{H}^{T} φ θ , m subscript 𝜑 𝜃 𝑚

\varphi_{\theta,m} ⟨ φ θ , m , ω ⟩ ℋ T ∈ ( 0 , ∞ ) subscript subscript 𝜑 𝜃 𝑚

𝜔

superscript ℋ 𝑇 0 \left\langle\varphi_{\theta,m},\omega\right\rangle_{\mathcal{H}^{T}}\in\left(0,\infty\right) ⟨ φ θ , m , ω ⟩ ℋ T ≠ 0 subscript subscript 𝜑 𝜃 𝑚

𝜔

superscript ℋ 𝑇 0 \left\langle\varphi_{\theta,m},\omega\right\rangle_{\mathcal{H}^{T}}\neq 0 ℒ e b { θ : ⟨ φ θ , m , ω ⟩ ℋ T = 0 } = 0 ℒ 𝑒 𝑏 conditional-set 𝜃 subscript subscript 𝜑 𝜃 𝑚

𝜔

superscript ℋ 𝑇 0 0 \mathcal{L}eb\left\{\theta:\left\langle\varphi_{\theta,m},\omega\right\rangle_{\mathcal{H}^{T}}=0\right\}=0 ℒ e b ℒ 𝑒 𝑏 \mathcal{L}eb ℝ ℝ \mathbb{R} ( − π , π ] 𝜋 𝜋 \left(-\pi,\pi\right]

Under Condition 3.3 φ θ , m subscript 𝜑 𝜃 𝑚

\varphi_{\theta,m}

Theorem 3.4

If Conditions

3.1 3.3 L = L ( n ) 𝐿 𝐿 𝑛 L=L(n) E | Y ^ t , m − Y t , m | → 0 → 𝐸 subscript ^ 𝑌 𝑡 𝑚

subscript 𝑌 𝑡 𝑚

0 E\left|\widehat{Y}_{t,m}-Y_{t,m}\right|\to 0 n → ∞ → 𝑛 n\to\infty

4 Numerical implementation

The theory presented in Section 3 R package, pcdpca, which

allows to preform all procedures described in this paper. In particular,

it is used to perform the analysis and simulations in Section 5

We use linearly independent basis functions { B 1 , B 2 , … , B K } subscript 𝐵 1 subscript 𝐵 2 … subscript 𝐵 𝐾 \left\{B_{1},B_{2},\ldots,B_{K}\right\} x ( u ) = ∑ j = 1 K c j B j ( u ) 𝑥 𝑢 superscript subscript 𝑗 1 𝐾 subscript 𝑐 𝑗 subscript 𝐵 𝑗 𝑢 x\left(u\right)=\sum_{j=1}^{K}c_{j}B_{j}\left(u\right) [2009 ] or Chapter 1 of

[2017 ] . We thus work in a finite

dimensional space ℋ K = sp { B 1 , B 2 , … , B K } subscript ℋ 𝐾 sp subscript 𝐵 1 subscript 𝐵 2 … subscript 𝐵 𝐾 \mathcal{H}_{K}=\mathrm{sp}\left\{B_{1},B_{2},\ldots,B_{K}\right\} A : ℋ K → ℋ K : 𝐴 → subscript ℋ 𝐾 subscript ℋ 𝐾 A:\mathcal{H}_{K}\rightarrow\mathcal{H}_{K} K × K 𝐾 𝐾 K\times K 𝔄 𝔄 \mathfrak{A} A ( x ) = 𝑩 ′ 𝔄 𝐜 , 𝐴 𝑥 superscript 𝑩 ′ 𝔄 𝐜 A(x)=\boldsymbol{B}^{\prime}\mathfrak{A}\mathbf{c}, 𝑩 = ( B 1 , B 2 , … , B K ) ′ 𝑩 superscript subscript 𝐵 1 subscript 𝐵 2 … subscript 𝐵 𝐾 ′ \boldsymbol{B}=\left(B_{1},B_{2},\ldots,B_{K}\right)^{\prime} 𝐜 = ( c 1 , c 2 , … , c K ) ′ 𝐜 superscript subscript 𝑐 1 subscript 𝑐 2 … subscript 𝑐 𝐾 ′ \mathbf{c}=\left(c_{1},c_{2},\ldots,c_{K}\right)^{\prime} 𝐌 B subscript 𝐌 𝐵 \mathbf{M}_{B} K × K 𝐾 𝐾 K\times K ( ⟨ B q , B r ⟩ ) q , r = 0 , … , K subscript subscript 𝐵 𝑞 subscript 𝐵 𝑟

formulae-sequence 𝑞 𝑟

0 … 𝐾

\left(\left\langle B_{q},B_{r}\right\rangle\right)_{q,r=0,\ldots,K} X t = 𝑩 ′ 𝐜 t subscript 𝑋 𝑡 superscript 𝑩 ′ subscript 𝐜 𝑡 X_{t}=\boldsymbol{B}^{\prime}\mathbf{c}_{t}

𝐁 T ′ := ( ( B 1 0 ⋮ 0 ) , … , ( B K 0 ⋮ 0 ) , … , ( 0 ⋮ 0 B 1 ) , … , ( 0 ⋮ 0 B K ) ) = ( 𝐛 1 ′ , 𝐛 2 ′ , … , 𝐛 T ′ ) . assign superscript subscript 𝐁 𝑇 ′ subscript 𝐵 1 0 ⋮ 0 … subscript 𝐵 𝐾 0 ⋮ 0 … 0 ⋮ 0 subscript 𝐵 1 … 0 ⋮ 0 subscript 𝐵 𝐾 superscript subscript 𝐛 1 ′ superscript subscript 𝐛 2 ′ … superscript subscript 𝐛 𝑇 ′ \mathbf{B}_{T}^{\prime}:=\left(\left(\begin{array}[]{c}B_{1}\\

0\\

\vdots\\

0\end{array}\right),\ldots,\left(\begin{array}[]{c}B_{K}\\

0\\

\vdots\\

0\end{array}\right),\ldots,\left(\begin{array}[]{c}0\\

\vdots\\

0\\

B_{1}\end{array}\right),\ldots,\left(\begin{array}[]{c}0\\

\vdots\\

0\\

B_{K}\end{array}\right)\right)=\left(\mathbf{b}_{1}^{\prime},\mathbf{b}_{2}^{{}^{\prime}},\ldots,\mathbf{b}_{T}^{\prime}\right).

Next, define the matrix

(4.1) 𝔉 θ X ¯ = ( ℱ θ , ( 0 , 0 ) 𝐜 ⋯ ℱ θ , ( 0 , T − 1 ) 𝐜 ⋮ ⋱ ⋮ ℱ θ , ( T − 1 , 0 ) 𝐜 ⋯ ℱ θ , ( T − 1 , T − 1 ) 𝐜 ) ( 𝐌 B ′ 0 ⋱ 0 𝐌 B ′ ) superscript subscript 𝔉 𝜃 ¯ 𝑋 superscript subscript ℱ 𝜃 0 0

𝐜 ⋯ superscript subscript ℱ 𝜃 0 𝑇 1

𝐜 ⋮ ⋱ ⋮ superscript subscript ℱ 𝜃 𝑇 1 0

𝐜 ⋯ superscript subscript ℱ 𝜃 𝑇 1 𝑇 1

𝐜 superscript subscript 𝐌 𝐵 ′ missing-subexpression 0 missing-subexpression ⋱ missing-subexpression 0 missing-subexpression superscript subscript 𝐌 𝐵 ′ \mathfrak{F}_{\theta}^{\underline{X}}=\left(\begin{array}[]{ccc}\mathcal{F}_{\theta,\left(0,0\right)}^{\mathbf{c}}&\cdots&\mathcal{F}_{\theta,\left(0,T-1\right)}^{\mathbf{c}}\\

\vdots&\ddots&\vdots\\

\mathcal{F}_{\theta,\left(T-1,0\right)}^{\mathbf{c}}&\cdots&\mathcal{F}_{\theta,\left(T-1,T-1\right)}^{\mathbf{c}}\end{array}\right)\left(\begin{array}[]{ccc}\mathbf{M}_{B}^{\prime}&&0\\

&\ddots&\\

0&&\mathbf{M}_{B}^{\prime}\end{array}\right)

as the matrix corresponding to the operator ℱ θ X ¯ superscript subscript ℱ 𝜃 ¯ 𝑋 \mathcal{F}_{\theta}^{\underline{X}} ℋ K T superscript subscript ℋ 𝐾 𝑇 \mathcal{H}_{K}^{T} ℱ θ , ( q , r ) 𝐜 superscript subscript ℱ 𝜃 𝑞 𝑟

𝐜 \mathcal{F}_{\theta,\left(q,r\right)}^{\mathbf{c}} 𝐜 = { 𝐜 t , t ∈ ℤ } 𝐜 subscript 𝐜 𝑡 𝑡

ℤ \mathbf{c}=\left\{\mathbf{c}_{t},t\in\mathbb{Z}\right\} 2.3

If λ θ , m subscript 𝜆 𝜃 𝑚

\lambda_{\theta,m} φ θ , m := ( φ θ , m , 1 ′ , … , φ θ , m , T ′ ) ′ assign subscript 𝜑 𝜃 𝑚

superscript superscript subscript 𝜑 𝜃 𝑚 1

′ … superscript subscript 𝜑 𝜃 𝑚 𝑇

′ ′ \mathbf{\varphi}_{\theta,m}:=\left(\mathbf{\varphi}_{\theta,m,1}^{\prime},\ldots,\mathbf{\ \varphi}_{\theta,m,T}^{\prime}\right)^{\prime} m 𝑚 m T K × T K 𝑇 𝐾 𝑇 𝐾 TK\times TK 𝔉 θ X ¯ superscript subscript 𝔉 𝜃 ¯ 𝑋 \mathfrak{F}_{\theta}^{\underline{X}} λ θ , m subscript 𝜆 𝜃 𝑚

\lambda_{\theta,m}

𝐁 T ′ φ θ , m = ( 𝐛 1 ′ , 𝐛 2 ′ , … , 𝐛 T ′ ) ( φ θ , m , 1 ′ , … , φ θ , m , T ′ ) ′ = ( 𝑩 ′ φ θ , m , 1 , … , 𝑩 ′ φ θ , m , T ) ′ superscript subscript 𝐁 𝑇 ′ subscript 𝜑 𝜃 𝑚

superscript subscript 𝐛 1 ′ superscript subscript 𝐛 2 ′ … superscript subscript 𝐛 𝑇 ′ superscript superscript subscript 𝜑 𝜃 𝑚 1

′ … superscript subscript 𝜑 𝜃 𝑚 𝑇

′ ′ superscript superscript 𝑩 ′ subscript 𝜑 𝜃 𝑚 1

… superscript 𝑩 ′ subscript 𝜑 𝜃 𝑚 𝑇

′ \mathbf{B}_{T}^{\prime}\mathbf{\varphi}_{\theta,m}=\left(\mathbf{b}_{1}^{\prime},\mathbf{b}_{2}^{\prime},\ldots,\mathbf{b}_{T}^{\prime}\right)\left(\mathbf{\varphi}_{\theta,m,1}^{\prime},\ldots,\mathbf{\varphi}_{\theta,m,T}^{\prime}\right)^{\prime}=\left(\boldsymbol{B}^{\prime}\mathbf{\varphi}_{\theta,m,1},\ldots,\boldsymbol{B}^{\prime}\mathbf{\varphi}_{\theta,m,T}\right)^{\prime}

are the m 𝑚 m ℱ θ X ¯ superscript subscript ℱ 𝜃 ¯ 𝑋 \mathcal{F}_{\theta}^{\underline{X}} C h , ( q , r ) 𝐜 superscript subscript 𝐶 ℎ 𝑞 𝑟

𝐜 C_{h,\left(q,r\right)}^{\mathbf{c}} ℱ θ , ( q , r ) 𝐜 superscript subscript ℱ 𝜃 𝑞 𝑟

𝐜 \mathcal{F}_{\theta,\left(q,r\right)}^{\mathbf{c}} q , r = 0 , … , T − 1 formulae-sequence 𝑞 𝑟

0 … 𝑇 1

q,r=0,\ldots,T-1 θ ∈ ( − π , π ] 𝜃 𝜋 𝜋 \theta\in\left(-\pi,\pi\right]

C ^ h , ( q , r ) 𝐜 = T n ∑ j ∈ ℤ 𝐜 q + T j 𝐜 r + T j − T h ′ I { 1 ≤ q + T j ≤ n } I { 1 ≤ r + T j − T h ≤ n } , h ≥ 0 , formulae-sequence superscript subscript ^ 𝐶 ℎ 𝑞 𝑟

𝐜 𝑇 𝑛 subscript 𝑗 ℤ subscript 𝐜 𝑞 𝑇 𝑗 superscript subscript 𝐜 𝑟 𝑇 𝑗 𝑇 ℎ ′ 𝐼 1 𝑞 𝑇 𝑗 𝑛 𝐼 1 𝑟 𝑇 𝑗 𝑇 ℎ 𝑛 ℎ 0 \widehat{C}_{h,\left(q,r\right)}^{\mathbf{c}}=\frac{T}{n}\sum_{j\in\mathbb{Z}}\mathbf{c}_{q+Tj}\mathbf{c}_{r+Tj-Th}^{\prime}I\left\{1\leq q+Tj\leq n\right\}I\left\{1\leq r+Tj-Th\leq n\right\},\text{ \ \ \ }h\geq 0,

( C ^ ¯ − h , ( q , r ) 𝐜 ) ′ = C ^ h , ( q , r ) 𝐜 , h < 0 , formulae-sequence superscript superscript subscript ¯ ^ 𝐶 ℎ 𝑞 𝑟

𝐜 ′ superscript subscript ^ 𝐶 ℎ 𝑞 𝑟

𝐜 ℎ 0 \left(\overline{\widehat{C}}_{-h,\left(q,r\right)}^{\mathbf{c}}\right)^{\prime}=\widehat{C}_{h,\left(q,r\right)}^{\mathbf{c}},\text{ \ \ \ }h<0,

and

(4.2) ℱ ^ θ , ( q , r ) 𝐜 = 1 2 π ∑ | h | ≤ q ( n ) w ( h q ( n ) ) C ^ h , ( q , r ) 𝐜 e − i h θ , superscript subscript ^ ℱ 𝜃 𝑞 𝑟

𝐜 1 2 𝜋 subscript ℎ 𝑞 𝑛 𝑤 ℎ 𝑞 𝑛 superscript subscript ^ 𝐶 ℎ 𝑞 𝑟

𝐜 superscript 𝑒 𝑖 ℎ 𝜃 \widehat{\mathcal{F}}_{\theta,\left(q,r\right)}^{\mathbf{c}}=\frac{1}{2\pi}\sum_{\left|h\right|\leq q(n)}w\left(\frac{h}{q(n)}\right)\widehat{C}_{h,\left(q,r\right)}^{\mathbf{c}}e^{-ih\theta},

where w 𝑤 w q ( n ) ⟶ ∞ ⟶ 𝑞 𝑛 q(n)\longrightarrow\infty q ( n ) n ⟶ 0 ⟶ 𝑞 𝑛 𝑛 0 \frac{q(n)}{n}\longrightarrow 0 4.2 4.1 consistent estimator 𝔉 ^ θ X ¯ superscript subscript ^ 𝔉 𝜃 ¯ 𝑋 \widehat{\mathfrak{F}}_{\theta}^{\underline{X}} λ ^ θ , m subscript ^ 𝜆 𝜃 𝑚

\widehat{\lambda}_{\theta,m} φ ^ θ , m := ( φ ^ θ , m , 1 ′ , … , φ ^ θ , m , T ′ ) ′ assign subscript ^ 𝜑 𝜃 𝑚

superscript superscript subscript ^ 𝜑 𝜃 𝑚 1

′ … superscript subscript ^ 𝜑 𝜃 𝑚 𝑇

′ ′ \widehat{\mathbf{\varphi}}_{\theta,m}:=\left(\widehat{\mathbf{\varphi}}_{\theta,m,1}^{\prime},\ldots,\widehat{\mathbf{\ \varphi}}_{\theta,m,T}^{\prime}\right)^{\prime} m ≥ 1 𝑚 1 m\geq 1

𝐁 T ′ φ ^ θ , m superscript subscript 𝐁 𝑇 ′ subscript ^ 𝜑 𝜃 𝑚

\displaystyle\mathbf{B}_{T}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,m} = \displaystyle= ( 𝐛 1 ′ , … , 𝐛 T ′ ) ( φ ^ θ , m , 1 ⋮ φ ^ θ , m , T ) = ( 𝑩 ′ φ ^ θ , m , 1 ⋮ 𝑩 ′ φ ^ θ , m , T ) = ( φ ^ θ , m , 1 ⋮ φ ^ θ , m , T ) = φ ^ θ , m superscript subscript 𝐛 1 ′ … superscript subscript 𝐛 𝑇 ′ subscript ^ 𝜑 𝜃 𝑚 1

⋮ subscript ^ 𝜑 𝜃 𝑚 𝑇

superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑚 1

⋮ superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑚 𝑇

subscript ^ 𝜑 𝜃 𝑚 1

⋮ subscript ^ 𝜑 𝜃 𝑚 𝑇

subscript ^ 𝜑 𝜃 𝑚

\displaystyle\left(\mathbf{b}_{1}^{\prime},\ldots,\mathbf{b}_{T}^{\prime}\right)\left(\begin{array}[]{c}\widehat{\mathbf{\varphi}}_{\theta,m,1}\\

\vdots\\

\widehat{\mathbf{\varphi}}_{\theta,m,T}\end{array}\right)=\left(\begin{array}[]{c}\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,m,1}\\

\vdots\\

\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,m,T}\end{array}\right)=\left(\begin{array}[]{c}\widehat{\varphi}_{\theta,m,1}\\

\vdots\\

\widehat{\varphi}_{\theta,m,T}\end{array}\right)=\widehat{\varphi}_{\theta,m}

to get estimators φ ^ θ , m subscript ^ 𝜑 𝜃 𝑚

\widehat{\varphi}_{\theta,m}

( 𝑩 ′ φ ^ θ , d p + m , 1 ⋮ 𝑩 ′ φ ^ θ , d p + m , T ) = ( Φ ^ θ , d , m d ⋮ Φ ^ θ , d − T + 1 , m d ) , superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑑 𝑝 𝑚 1

⋮ superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑑 𝑝 𝑚 𝑇

superscript subscript ^ Φ 𝜃 𝑑 𝑚

𝑑 ⋮ superscript subscript ^ Φ 𝜃 𝑑 𝑇 1 𝑚

𝑑 \left(\begin{array}[]{c}\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,dp+m,1}\\

\vdots\\

\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,dp+m,T}\end{array}\right)=\left(\begin{array}[]{c}\widehat{\Phi}_{\theta,d,m}^{d}\\

\vdots\\

\widehat{\Phi}_{\theta,d-T+1,m}^{d}\end{array}\right),

or equivalently

(4.4) ( 𝑩 ′ 𝚽 ^ l T + d , m d ⋮ 𝑩 ′ 𝚽 ^ l T + d − T + 1 , m d ) := 1 2 π ∫ − π π ( 𝑩 ′ φ ^ θ , d p + m , 1 ⋮ 𝑩 ′ φ ^ θ , d p + m , T ) e − i l θ 𝑑 θ = ( Φ ^ l T + d , m d ⋮ Φ ^ l T + d − T + 1 , m d ) , assign superscript 𝑩 ′ superscript subscript ^ 𝚽 𝑙 𝑇 𝑑 𝑚

𝑑 ⋮ superscript 𝑩 ′ superscript subscript ^ 𝚽 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑 1 2 𝜋 superscript subscript 𝜋 𝜋 superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑑 𝑝 𝑚 1

⋮ superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑑 𝑝 𝑚 𝑇

superscript 𝑒 𝑖 𝑙 𝜃 differential-d 𝜃 superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑚

𝑑 ⋮ superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑 \left(\begin{array}[]{c}\boldsymbol{B}^{\prime}\widehat{\mathbf{\Phi}}_{lT+d,m}^{d}\\

\vdots\\

\boldsymbol{B}^{\prime}\widehat{\mathbf{\Phi}}_{lT+d-T+1,m}^{d}\end{array}\right):=\dfrac{1}{2\pi}\int_{-\pi}^{\pi}\left(\begin{array}[]{c}\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,dp+m,1}\\

\vdots\\

\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,dp+m,T}\end{array}\right)e^{-il\theta}d\theta=\left(\begin{array}[]{c}\widehat{\Phi}_{lT+d,m}^{d}\\

\vdots\\

\widehat{\Phi}_{lT+d-T+1,m}^{d}\end{array}\right),

for d = 0 , … , T − 1 𝑑 0 … 𝑇 1

d=0,\ldots,T-1 m = 1 , … , p 𝑚 1 … 𝑝

m=1,\ldots,p Φ ^ l , m d superscript subscript ^ Φ 𝑙 𝑚

𝑑 \widehat{\Phi}_{l,m}^{d}

Y ^ t , m subscript ^ 𝑌 𝑡 𝑚

\displaystyle\widehat{Y}_{t,m} = \displaystyle= ∑ l = − L T + d − T + 1 L T + d ⟨ X t − l , Φ ^ l , m d ⟩ superscript subscript 𝑙 𝐿 𝑇 𝑑 𝑇 1 𝐿 𝑇 𝑑 subscript 𝑋 𝑡 𝑙 superscript subscript ^ Φ 𝑙 𝑚

𝑑

\displaystyle\sum_{l=-LT+d-T+1}^{LT+d}\left\langle X_{t-l},\widehat{\Phi}_{l,m}^{d}\right\rangle

= \displaystyle= ∑ l = − L L ⟨ X t − l T − d , Φ ^ l T + d , m d ⟩ + ⋯ + ∑ l = − L L ⟨ X t − l T − d + T − 1 , Φ ^ l T + d − T + 1 , m d ⟩ superscript subscript 𝑙 𝐿 𝐿 subscript 𝑋 𝑡 𝑙 𝑇 𝑑 superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑚

𝑑

⋯ superscript subscript 𝑙 𝐿 𝐿 subscript 𝑋 𝑡 𝑙 𝑇 𝑑 𝑇 1 superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑

\displaystyle\sum_{l=-L}^{L}\left\langle X_{t-lT-d},\widehat{\Phi}_{lT+d,m}^{d}\right\rangle+\cdots+\sum_{l=-L}^{L}\left\langle X_{t-lT-d+T-1},\widehat{\Phi}_{lT+d-T+1,m}^{d}\right\rangle

= \displaystyle= ∑ l = − L L 𝐜 ( t − l T − d ) ′ 𝐌 B 𝚽 ^ ¯ l T + d , m d + … + ∑ l = − L L 𝐜 ( t − l T − d + T − 1 ) ′ 𝐌 B 𝚽 ^ ¯ l T + d − T + 1 , m d , t ≡ 𝑇 d , superscript subscript 𝑙 𝐿 𝐿 superscript subscript 𝐜 𝑡 𝑙 𝑇 𝑑 ′ subscript 𝐌 𝐵 superscript subscript ¯ ^ 𝚽 𝑙 𝑇 𝑑 𝑚

𝑑 … superscript subscript 𝑙 𝐿 𝐿 superscript subscript 𝐜 𝑡 𝑙 𝑇 𝑑 𝑇 1 ′ subscript 𝐌 𝐵 superscript subscript ¯ ^ 𝚽 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑 𝑡 𝑇 𝑑

\displaystyle\sum_{l=-L}^{L}\mathbf{c}_{\left(t-lT-d\right)}^{\prime}\mathbf{M}_{B}\overline{\widehat{\mathbf{\Phi}}}_{lT+d,m}^{d}+\ldots+\sum_{l=-L}^{L}\mathbf{c}_{\left(t-lT-d+T-1\right)}^{\prime}\mathbf{M}_{B}\overline{\widehat{\mathbf{\Phi}}}_{lT+d-T+1,m}^{d},\text{\ }t\overset{T}{\equiv}d,

where L 𝐿 L

∑ l = − L L ( ‖ Φ ^ l T + d , m d ‖ ℋ 2 + ⋯ + ‖ Φ ^ l T + d − T + 1 , m d ‖ ℋ 2 ) ≥ 1 − ε superscript subscript 𝑙 𝐿 𝐿 superscript subscript norm superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑚

𝑑 ℋ 2 ⋯ superscript subscript norm superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑑 ℋ 2 1 𝜀 \sum_{l=-L}^{L}\left(\left\|\widehat{\Phi}_{lT+d,m}^{d}\right\|_{\mathcal{H}}^{2}+\cdots+\left\|\widehat{\Phi}_{lT+d-T+1,m}^{d}\right\|_{\mathcal{H}}^{2}\right)\geq 1-\varepsilon

for some d 𝑑 d and small ε > 0 𝜀 0 \varepsilon>0 X t subscript 𝑋 𝑡 X_{t}

X ^ t = ∑ m = 1 p ∑ l = − L L Y ^ t + l T − d , m Φ ^ l T − d , m 0 + … + ∑ m = 1 p ∑ l = − L L Y ^ t + l T − d + T − 1 , m Φ ^ l T − d + T − 1 , m T − 1 , t ≡ 𝑇 d . subscript ^ 𝑋 𝑡 superscript subscript 𝑚 1 𝑝 superscript subscript 𝑙 𝐿 𝐿 subscript ^ 𝑌 𝑡 𝑙 𝑇 𝑑 𝑚

superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑚

0 … superscript subscript 𝑚 1 𝑝 superscript subscript 𝑙 𝐿 𝐿 subscript ^ 𝑌 𝑡 𝑙 𝑇 𝑑 𝑇 1 𝑚

superscript subscript ^ Φ 𝑙 𝑇 𝑑 𝑇 1 𝑚

𝑇 1 𝑡 𝑇 𝑑

\widehat{X}_{t}=\sum_{m=1}^{p}\sum_{l=-L}^{L}\widehat{Y}_{t+lT-d,m}\widehat{\Phi}_{lT-d,m}^{0}+\ldots+\sum_{m=1}^{p}\sum_{l=-L}^{L}\widehat{Y}_{t+lT-d+T-1,m}\widehat{\Phi}_{lT-d+T-1,m}^{T-1},\text{ \ \ \ }t\overset{T}{\equiv}d.

For illustration, set T = 2 𝑇 2 T=2

𝐁 T ′ = ( ( B 1 0 ) , … , ( B K 0 ) , ( 0 B 1 ) , … , ( 0 B K ) ) = ( 𝐛 1 ′ , 𝐛 2 ′ ) superscript subscript 𝐁 𝑇 ′ subscript 𝐵 1 0 … subscript 𝐵 𝐾 0 0 subscript 𝐵 1 … 0 subscript 𝐵 𝐾 superscript subscript 𝐛 1 ′ superscript subscript 𝐛 2 ′ \mathbf{B}_{T}^{\prime}=\left(\left(\begin{array}[]{c}B_{1}\\

0\end{array}\right),\ldots,\left(\begin{array}[]{c}B_{K}\\

0\end{array}\right),\left(\begin{array}[]{c}0\\

B_{1}\end{array}\right),\ldots,\left(\begin{array}[]{c}0\\

B_{K}\end{array}\right)\right)=\left(\mathbf{b}_{1}^{\prime},\mathbf{b}_{2}^{{}^{\prime}}\right)

as a vector of linearly independent elements in ℋ 2 superscript ℋ 2 \mathcal{H}^{2}

(4.5) 𝔉 θ X ¯ = ( ℱ θ , ( 0 , 0 ) 𝐜 ℱ θ , ( 0 , 1 ) 𝐜 ℱ θ , ( 1 , 0 ) 𝐜 ℱ θ , ( 1 , 1 ) 𝐜 ) ( 𝐌 B ′ 0 0 𝐌 B ′ ) superscript subscript 𝔉 𝜃 ¯ 𝑋 superscript subscript ℱ 𝜃 0 0

𝐜 superscript subscript ℱ 𝜃 0 1

𝐜 superscript subscript ℱ 𝜃 1 0

𝐜 superscript subscript ℱ 𝜃 1 1

𝐜 superscript subscript 𝐌 𝐵 ′ 0 0 superscript subscript 𝐌 𝐵 ′ \mathfrak{F}_{\theta}^{\underline{X}}=\left(\begin{array}[]{cc}\mathcal{F}_{\theta,\left(0,0\right)}^{\mathbf{c}}&\mathcal{\ F}_{\theta,\left(0,1\right)}^{\mathbf{c}}\\

\mathcal{F}_{\theta,\left(1,0\right)}^{\mathbf{c}}&\mathcal{\ F}_{\theta,\left(1,1\right)}^{\mathbf{c}}\end{array}\right)\left(\begin{array}[]{cc}\mathbf{M}_{B}^{\prime}&0\\

0&\mathbf{M}_{B}^{\prime}\end{array}\right)

corresponds to the operator ℱ θ X ¯ superscript subscript ℱ 𝜃 ¯ 𝑋 \mathcal{F}_{\theta}^{\underline{X}} ℋ K 2 superscript subscript ℋ 𝐾 2 \mathcal{H}_{K}^{2} q , r = 0 , 1 formulae-sequence 𝑞 𝑟

0 1 q,r=0,1

C ^ h , ( q , r ) 𝐜 = 2 n ∑ j ∈ ℤ 𝐜 q + 2 j 𝐜 r + 2 j − 2 h ′ I { 1 ≤ q + 2 j ≤ n } I { 1 ≤ r + 2 j − 2 h ≤ n } , h ≥ 0 , formulae-sequence superscript subscript ^ 𝐶 ℎ 𝑞 𝑟

𝐜 2 𝑛 subscript 𝑗 ℤ subscript 𝐜 𝑞 2 𝑗 superscript subscript 𝐜 𝑟 2 𝑗 2 ℎ ′ 𝐼 1 𝑞 2 𝑗 𝑛 𝐼 1 𝑟 2 𝑗 2 ℎ 𝑛 ℎ 0 \widehat{C}_{h,\left(q,r\right)}^{\mathbf{c}}=\frac{2}{n}\sum_{j\in\mathbb{Z}}\mathbf{c}_{q+2j}\mathbf{c}_{r+2j-2h}^{\prime}I\left\{1\leq q+2j\leq n\right\}I\left\{1\leq r+2j-2h\leq n\right\},\text{ \ \ \ }h\geq 0,

Estimators of the PC-DFPC filter coefficient Φ l , m d superscript subscript Φ 𝑙 𝑚

𝑑 \Phi_{l,m}^{d} Y t , m subscript 𝑌 𝑡 𝑚

Y_{t,m}

( 𝑩 ′ 𝚽 ^ 2 l , m 0 𝑩 ′ 𝚽 ^ 2 l − 1 , m 0 ) superscript 𝑩 ′ superscript subscript ^ 𝚽 2 𝑙 𝑚

0 superscript 𝑩 ′ superscript subscript ^ 𝚽 2 𝑙 1 𝑚

0 \displaystyle\left(\begin{array}[]{c}\boldsymbol{B}^{\prime}\widehat{\mathbf{\Phi}}_{2l,m}^{0}\\

\boldsymbol{B}^{\prime}\widehat{\mathbf{\Phi}}_{2l-1,m}^{0}\end{array}\right) : : \displaystyle: = 1 2 π ∫ − π π ( 𝑩 ′ φ ^ θ , m , 1 𝑩 ′ φ ^ θ , m , 2 ) e − i l θ 𝑑 θ = ( Φ ^ 2 l , m 0 Φ ^ 2 l − 1 , m 0 ) absent 1 2 𝜋 superscript subscript 𝜋 𝜋 superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑚 1

superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑚 2

superscript 𝑒 𝑖 𝑙 𝜃 differential-d 𝜃 superscript subscript ^ Φ 2 𝑙 𝑚

0 superscript subscript ^ Φ 2 𝑙 1 𝑚

0 \displaystyle=\dfrac{1}{2\pi}\int_{-\pi}^{\pi}\left(\begin{array}[]{c}\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,m,1}\\

\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,m,2}\end{array}\right)e^{-il\theta}d\theta=\left(\begin{array}[]{c}\widehat{\Phi}_{2l,m}^{0}\\

\widehat{\Phi}_{2l-1,m}^{0}\end{array}\right)

( 𝑩 ′ 𝚽 ^ 2 l , m + p 1 𝑩 𝚽 ^ 2 l − 1 , m + p 1 ) superscript 𝑩 ′ superscript subscript ^ 𝚽 2 𝑙 𝑚 𝑝

1 𝑩 superscript subscript ^ 𝚽 2 𝑙 1 𝑚 𝑝

1 \displaystyle\left(\begin{array}[]{c}\boldsymbol{B}^{\prime}\widehat{\mathbf{\Phi}}_{2l,m+p}^{1}\\

\boldsymbol{B}\widehat{\mathbf{\Phi}}_{2l-1,m+p}^{1}\end{array}\right) : : \displaystyle: = 1 2 π ∫ − π π ( 𝑩 ′ φ ^ θ , m + p , 1 𝑩 ′ φ ^ θ , m + p , 2 ) e − i l θ 𝑑 θ = ( Φ ^ 2 l + 1 , m 1 Φ ^ 2 l , m 1 ) , m = 1 , … , p . formulae-sequence absent 1 2 𝜋 superscript subscript 𝜋 𝜋 superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑚 𝑝 1

superscript 𝑩 ′ subscript ^ 𝜑 𝜃 𝑚 𝑝 2

superscript 𝑒 𝑖 𝑙 𝜃 differential-d 𝜃 superscript subscript ^ Φ 2 𝑙 1 𝑚

1 superscript subscript ^ Φ 2 𝑙 𝑚

1 𝑚 1 … 𝑝

\displaystyle=\dfrac{1}{2\pi}\int_{-\pi}^{\pi}\left(\begin{array}[]{c}\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,m+p,1}\\

\boldsymbol{B}^{\prime}\widehat{\mathbf{\varphi}}_{\theta,m+p,2}\end{array}\right)e^{-il\theta}d\theta=\left(\begin{array}[]{c}\widehat{\Phi}_{2l+1,m}^{1}\\

\widehat{\Phi}_{2l,m}^{1}\end{array}\right),\text{ \ \ \ }m=1,\ldots,p.

Y ^ t , m subscript ^ 𝑌 𝑡 𝑚

\displaystyle\widehat{Y}_{t,m} = \displaystyle= ∑ l = − 2 L − 1 2 L ⟨ X ( t − l ) , Φ ^ l , m 0 ⟩ superscript subscript 𝑙 2 𝐿 1 2 𝐿 subscript 𝑋 𝑡 𝑙 superscript subscript ^ Φ 𝑙 𝑚

0

\displaystyle\sum_{l=-2L-1}^{2L}\left\langle X_{\left(t-l\right)},\widehat{\Phi}_{l,m}^{0}\right\rangle

= \displaystyle= ∑ l = − L L 𝐜 ( t − 2 l ) ′ 𝐌 B 𝚽 ^ ¯ 2 l , m 0 + ∑ l = − L L 𝐜 ( t − 2 l + 1 ) ′ 𝐌 B 𝚽 ^ ¯ 2 l − 1 , m 0 , t ≡ 2 0 , superscript subscript 𝑙 𝐿 𝐿 superscript subscript 𝐜 𝑡 2 𝑙 ′ subscript 𝐌 𝐵 superscript subscript ¯ ^ 𝚽 2 𝑙 𝑚

0 superscript subscript 𝑙 𝐿 𝐿 superscript subscript 𝐜 𝑡 2 𝑙 1 ′ subscript 𝐌 𝐵 superscript subscript ¯ ^ 𝚽 2 𝑙 1 𝑚

0 𝑡 2 0

\displaystyle\sum_{l=-L}^{L}\mathbf{c}_{\left(t-2l\right)}^{\prime}\mathbf{M}_{B}\overline{\widehat{\mathbf{\Phi}}}_{2l,m}^{0}+\sum_{l=-L}^{L}\mathbf{c}_{\left(t-2l+1\right)}^{\prime}\mathbf{M}_{B}\overline{\widehat{\mathbf{\Phi}}}_{2l-1,m}^{0},\text{ \ \ \ }t\overset{2}{\equiv}0,

Y ^ t , m subscript ^ 𝑌 𝑡 𝑚

\displaystyle\widehat{Y}_{t,m} = \displaystyle= ∑ l = − 2 L 2 L + 1 ⟨ X ( t − l ) , Φ ^ l , m 1 ⟩ superscript subscript 𝑙 2 𝐿 2 𝐿 1 subscript 𝑋 𝑡 𝑙 superscript subscript ^ Φ 𝑙 𝑚

1

\displaystyle\sum_{l=-2L}^{2L+1}\left\langle X_{\left(t-l\right)},\widehat{\Phi}_{l,m}^{1}\right\rangle

= \displaystyle= ∑ l = − L L 𝐜 ( t − 2 l ) ′ 𝐌 B 𝚽 ^ ¯ 2 l , m 1 + ∑ l = − L L 𝐜 ( t − 2 l − 1 ) ′ 𝐌 B 𝚽 ^ ¯ 2 l + 1 , m 1 , t ≡ 2 1 . superscript subscript 𝑙 𝐿 𝐿 superscript subscript 𝐜 𝑡 2 𝑙 ′ subscript 𝐌 𝐵 superscript subscript ¯ ^ 𝚽 2 𝑙 𝑚

1 superscript subscript 𝑙 𝐿 𝐿 superscript subscript 𝐜 𝑡 2 𝑙 1 ′ subscript 𝐌 𝐵 superscript subscript ¯ ^ 𝚽 2 𝑙 1 𝑚

1 𝑡 2 1

\displaystyle\sum_{l=-L}^{L}\mathbf{c}_{\left(t-2l\right)}^{\prime}\mathbf{M}_{B}\overline{\widehat{\mathbf{\Phi}}}_{2l,m}^{1}+\sum_{l=-L}^{L}\mathbf{c}_{\left(t-2l-1\right)}^{\prime}\mathbf{M}_{B}\overline{\widehat{\mathbf{\Phi}}}_{2l+1,m}^{1},\text{ \ \ \ }t\overset{2}{\equiv}1.

Hence,

X ^ t = ∑ m = 1 p ∑ l = − L L Y ^ t + 2 l , m Φ ^ 2 l , m 0 + ∑ m = 1 p ∑ l = − L L Y ^ t + 2 l + 1 , m Φ ^ 2 l + 1 , m 1 , t ≡ 2 0 , subscript ^ 𝑋 𝑡 superscript subscript 𝑚 1 𝑝 superscript subscript 𝑙 𝐿 𝐿 subscript ^ 𝑌 𝑡 2 𝑙 𝑚

superscript subscript ^ Φ 2 𝑙 𝑚

0 superscript subscript 𝑚 1 𝑝 superscript subscript 𝑙 𝐿 𝐿 subscript ^ 𝑌 𝑡 2 𝑙 1 𝑚

superscript subscript ^ Φ 2 𝑙 1 𝑚

1 𝑡 2 0

\widehat{X}_{t}=\sum_{m=1}^{p}\sum_{l=-L}^{L}\widehat{Y}_{t+2l,m}\widehat{\Phi}_{2l,m}^{0}+\sum_{m=1}^{p}\sum_{l=-L}^{L}\widehat{Y}_{t+2l+1,m}\widehat{\Phi}_{2l+1,m}^{1},\text{ \ \ \ }t\overset{2}{\equiv}0,

X ^ t = ∑ m = 1 p ∑ l = − L L Y ^ t + 2 l , m Φ ^ 2 l , m 1 + ∑ m = 1 p ∑ l = − L L Y ^ t + 2 l − 1 , m Φ ^ 2 l − 1 , m 0 , t ≡ 2 1 . subscript ^ 𝑋 𝑡 superscript subscript 𝑚 1 𝑝 superscript subscript 𝑙 𝐿 𝐿 subscript ^ 𝑌 𝑡 2 𝑙 𝑚

superscript subscript ^ Φ 2 𝑙 𝑚

1 superscript subscript 𝑚 1 𝑝 superscript subscript 𝑙 𝐿 𝐿 subscript ^ 𝑌 𝑡 2 𝑙 1 𝑚

superscript subscript ^ Φ 2 𝑙 1 𝑚

0 𝑡 2 1

\widehat{X}_{t}=\sum_{m=1}^{p}\sum_{l=-L}^{L}\widehat{Y}_{t+2l,m}\widehat{\Phi}_{2l,m}^{1}+\sum_{m=1}^{p}\sum_{l=-L}^{L}\widehat{Y}_{t+2l-1,m}\widehat{\Phi}_{2l-1,m}^{0},\text{ \ \ \ }t\overset{2}{\equiv}1.

5 Application to particulate pollution data and a simulation

study

To illustrate the advantages of PC-DFPCA relative the (stationary)

DFPCA which may arise in certain settings, we further explore the

dataset analyzed in [2015 ] . The

dataset contains intraday measurements of pollution in Graz, Austria

between October 1, 2010 and March 31, 2011. Observations were sampled

every 30 30 30 10 μ m 10 𝜇 𝑚 10\mu m [2015 ] , we employ exactly the same

preprocessing procedure, including square-root transformation, removal

of the mean weakly pattern and outliers. Note that the removal of the

mean weakly pattern does not affect periodic covariances between

weekdays and therefore they can be exploited using the PC-DFPCA

procedure applied with the period T = 7 𝑇 7 T=7 175 175 175 15 15 15 { X t : 1 ≤ t ≤ 175 } conditional-set subscript 𝑋 𝑡 1 𝑡 175 \{X_{t}:1\leq t\leq 175\}

For FPCA and DFPCA we use the same procedure as

[2015 ] using the implementation

published by those researchers as the R package freqdom.

To implement the PC-DFPCA, some modifications are needed. Regarding

the metaparameters q 𝑞 q L 𝐿 L [2015 ] advise choosing q ∼ n similar-to 𝑞 𝑛 q\sim\sqrt{n} L 𝐿 L ∑ − L ≤ i ≤ L ‖ Φ m , l d ‖ 2 ∼ 1 similar-to subscript 𝐿 𝑖 𝐿 superscript norm subscript superscript Φ 𝑑 𝑚 𝑙

2 1 \sum_{-L\leq i\leq L}\|\Phi^{d}_{m,l}\|^{2}\sim 1 n / T 𝑛 𝑇 n/T q 𝑞 q T 𝑇 \sqrt{T} q = 4 𝑞 4 q=4 L = 3 𝐿 3 L=3 10 10 10 [2015 ] ), as it

now relates to weeks not days and we do not expect dependence beyond

3 3 3

As a measure of fit, we use the Normalized Mean Squared Error

(NMSE) defined as

𝙽𝙼𝚂𝙴 = ∑ t = 1 n ‖ X t − X t ^ ‖ 2 / ∑ t = 1 n ‖ X t ‖ 2 , 𝙽𝙼𝚂𝙴 superscript subscript 𝑡 1 𝑛 superscript norm subscript 𝑋 𝑡 ^ subscript 𝑋 𝑡 2 superscript subscript 𝑡 1 𝑛 superscript norm subscript 𝑋 𝑡 2 \verb|NMSE|=\sum_{t=1}^{n}\|X_{t}-\hat{X_{t}}\|^{2}/\sum_{t=1}^{n}\|X_{t}\|^{2},

where the X t ^ ^ subscript 𝑋 𝑡 \hat{X_{t}} 𝙽𝙼𝚂𝙴 ⋅ 100 % ⋅ 𝙽𝙼𝚂𝙴 percent 100 \verb|NMSE|\cdot 100\% percentage of variance explained .

For the sake of comparison and discussion, we focus only on the first

principal component, which already explains 73 % percent 73 73\% 80 % percent 80 80\% 88 % percent 88 88\% 1

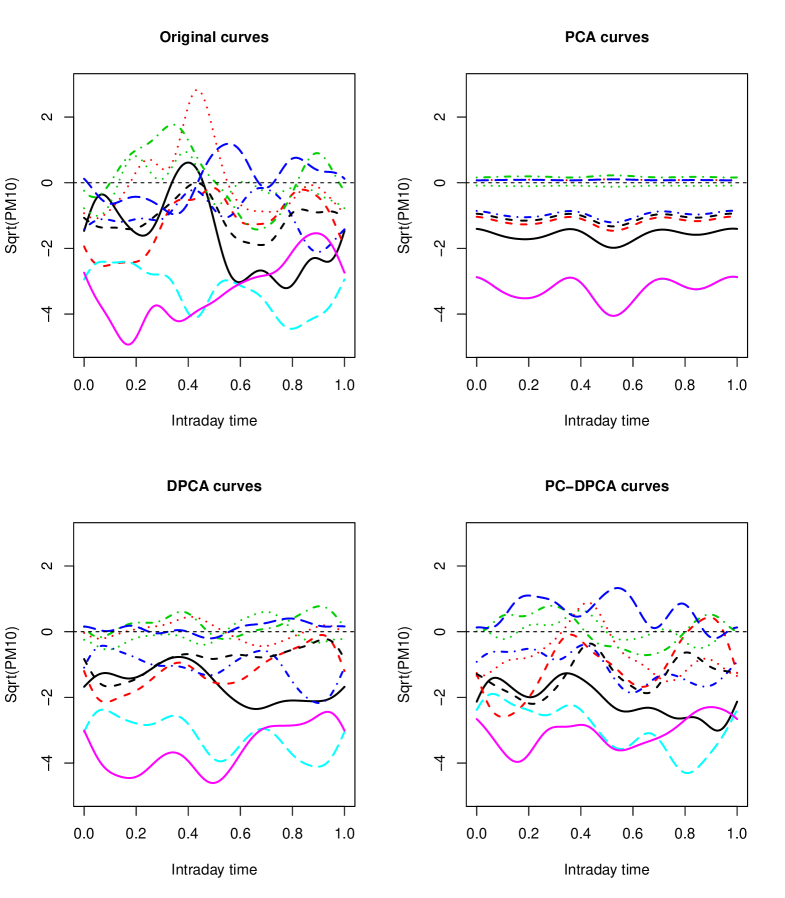

Figure 1: Ten successive intraday observations of

PM10 data (top-left), the corresponding functional PCA curves

reconstructed from the first principal component (top-right), dynamic

functional principal component curves (bottom-left) and

periodically-correlated dynamic principal components (bottom-right).

Colors and types of curves match the same observations among plots.

[2015 ] observed that, for this

particular dataset, the sequences of scores of the DFPC’s

and the static FPC’s were almost

identical. This is no longer the case if the PC-DFPC’s are used.

Figure 2

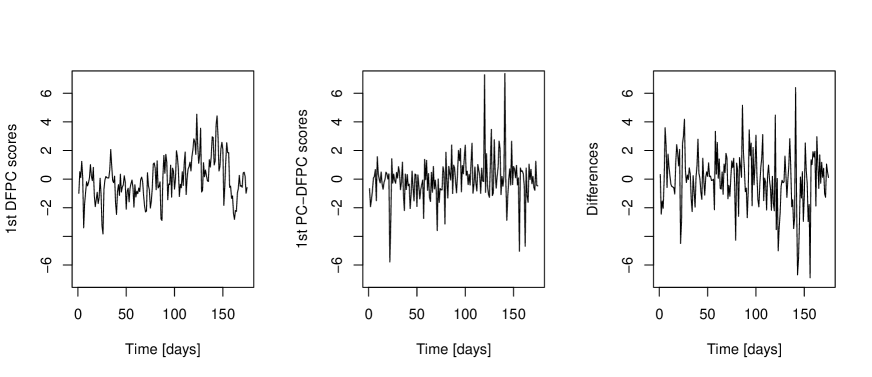

Figure 2: The first dynamic principal component scores (left), the first periodically correlated dynamic principal component scores (middle) and differences between the two series (right).

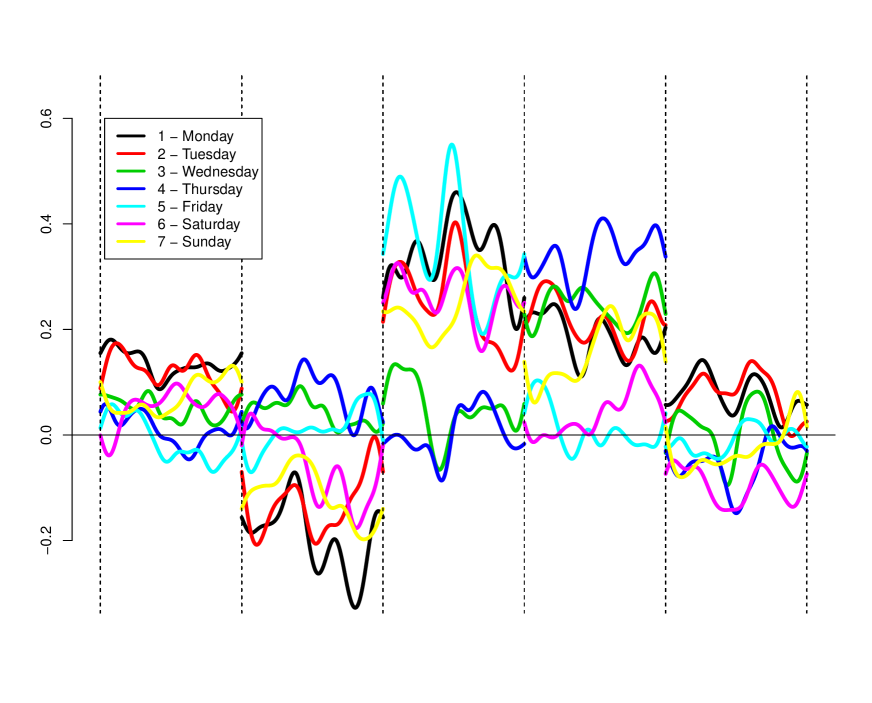

The estimated PC-DFPCA filters are very high dimensional as can be seen in

Figure 3 L = 3 𝐿 3 L=3 T = 7 𝑇 7 T=7 p = 15 𝑝 15 p=15 ( 2 L + 1 ) T 2 p 2 = 735 2 𝐿 1 superscript 𝑇 2 superscript 𝑝 2 735 (2L~{}+~{}1)T^{2}p^{2}~{}=~{}735

Figure 3: Filters of the first principal component

for d = 0 𝑑 0 d=0 m = 1 , 2 , … , 7 𝑚 1 2 … 7

m=1,2,...,7 Φ − 2 , m d , Φ − 1 , m d , … , Φ 2 , m d subscript superscript Φ 𝑑 2 𝑚

subscript superscript Φ 𝑑 1 𝑚

… subscript superscript Φ 𝑑 2 𝑚

\Phi^{d}_{-2,m},\Phi^{d}_{-1,m},...,\Phi^{d}_{2,m}

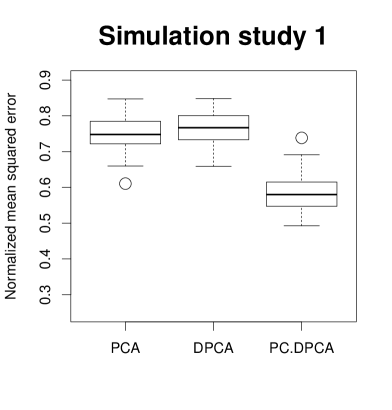

To further analyze the properties of the PC-DFPCA filter, we design

two simulation studies, with two distinct periodically correlated

functional time series. In the first study we set p = 7 𝑝 7 p=7 T = 3 𝑇 3 T=3 n = 300 𝑛 300 n=300 𝐚 i , 𝐛 i ∼ 𝒩 ( 0 , diag ( exp ( − 2 ⋅ 1 p ) , exp ( − 2 ⋅ 2 p ) , … , exp ( − 2 ⋅ p p ) ) ) similar-to subscript 𝐚 𝑖 subscript 𝐛 𝑖

𝒩 0 diag ⋅ 2 1 𝑝 ⋅ 2 2 𝑝 … ⋅ 2 𝑝 𝑝 \mathbf{a}_{i},\mathbf{b}_{i}\sim\mathcal{N}(0,\operatorname{diag}(\exp(-2\cdot\frac{1}{p}),\exp(-2\cdot\frac{2}{p}),...,\exp(-2\cdot\frac{p}{p}))) i ∈ { 1 , 2 , … , 100 } 𝑖 1 2 … 100 i~{}\in~{}\{1,2,...,100\} 0 0

𝐜 T i + 1 = 𝐚 i , 𝐜 T i + 2 = 𝐛 i and 𝐜 T i + 3 = 2 𝐚 i − 𝐛 i for i ∈ { 1 , 2 , … , 100 } . formulae-sequence subscript 𝐜 𝑇 𝑖 1 subscript 𝐚 𝑖 subscript 𝐜 𝑇 𝑖 2 subscript 𝐛 𝑖 and subscript 𝐜 𝑇 𝑖 3 2 subscript 𝐚 𝑖 subscript 𝐛 𝑖 for 𝑖 1 2 … 100 \mathbf{c}_{Ti+1}=\mathbf{a}_{i},\mathbf{c}_{Ti+2}=\mathbf{b}_{i}\text{ and }\mathbf{c}_{Ti+3}=2\mathbf{a}_{i}-\mathbf{b}_{i}\text{ for }i\in\{1,2,...,100\}.

We divide the set

of { 𝐜 t : t ∈ { 1 , 2 , … , 300 } } conditional-set subscript 𝐜 𝑡 𝑡 1 2 … 300 \{\mathbf{c}_{t}:t\in\{1,2,...,300\}\} 150 150 150 150 150 150 L = 2 𝐿 2 L=2 q = 3 𝑞 3 q=3 100 100 100 4 0.59 ( sd = 0.05 ) 0.59 sd 0.05 0.59\ (\operatorname{sd}=0.05) 0.76 ( sd = 0.04 ) 0.76 sd 0.04 0.76\ (\operatorname{sd}=0.04) 0.74 ( sd = 0.04 ) 0.74 sd 0.04 0.74\ (\operatorname{sd}=0.04)

In the second simulation scenario, we sampled a functional periodically

correlated autoregressive process. We set p = 7 𝑝 7 p=7 T = 2 𝑇 2 T=2 n = 1000 𝑛 1000 n=1000

ε i ∼ 𝒩 ( 0 , Σ ) similar-to subscript 𝜀 𝑖 𝒩 0 Σ \varepsilon_{i}\sim\mathcal{N}(0,\Sigma)

with

Σ = diag ( exp ( − 2 ⋅ 1 / p , exp ( − 2 ⋅ 2 / p ) , … , exp ( − 2 ⋅ p / p ) ) ) Σ diag ⋅ 2 1 𝑝 ⋅ 2 2 𝑝 … ⋅ 2 𝑝 𝑝 \Sigma=\operatorname{diag}(\exp(-2\cdot 1/p,\exp(-2\cdot 2/p),...,\exp(-2\cdot p/p)))

for i ∈ { 1 , 2 , … , n } 𝑖 1 2 … 𝑛 i\in\{1,2,...,n\} P i , j = [ δ k , l ] 1 ≤ k , l ≤ p subscript 𝑃 𝑖 𝑗

subscript delimited-[] subscript 𝛿 𝑘 𝑙

formulae-sequence 1 𝑘 𝑙 𝑝 P_{i,j}=[\delta_{k,l}]_{1\leq k,l\leq p} Ψ i , j = 0.9 ⋅ P i , j / ‖ P i , j ‖ subscript Ψ 𝑖 𝑗

⋅ 0.9 subscript 𝑃 𝑖 𝑗

norm subscript 𝑃 𝑖 𝑗

\Psi_{i,j}=0.9\cdot P_{i,j}/\|P_{i,j}\| i , j ∈ { 0 , 1 } 𝑖 𝑗

0 1 i,j\in\{0,1\} δ k , l ∼ 𝒩 ( 0 , exp ( − 2 ⋅ l p ) ) similar-to subscript 𝛿 𝑘 𝑙

𝒩 0 ⋅ 2 𝑙 𝑝 \delta_{k,l}\sim\mathcal{N}(0,\exp(-2\cdot\frac{l}{p})) 𝐜 t subscript 𝐜 𝑡 \mathbf{c}_{t}

𝐜 t = [ 0 , 0 , … , 0 ] ′ for t ≤ 0 subscript 𝐜 𝑡 superscript 0 0 … 0

′ for 𝑡 0 \mathbf{c}_{t}=[0,0,...,0]^{\prime}\text{ for }t\leq 0

and for d ∈ { 0 , 1 } 𝑑 0 1 d\in\{0,1\} 1 ≤ t ≤ n 1 𝑡 𝑛 1\leq t\leq n

𝐜 t = Ψ d , 0 𝐜 t − 1 + Ψ d , 1 𝐜 t − 2 + ε t for t ≡ 2 d . subscript 𝐜 𝑡 subscript Ψ 𝑑 0

subscript 𝐜 𝑡 1 subscript Ψ 𝑑 1

subscript 𝐜 𝑡 2 subscript 𝜀 𝑡 for 𝑡 superscript 2 𝑑 \mathbf{c}_{t}=\Psi_{d,0}\mathbf{c}_{t-1}+\Psi_{d,1}\mathbf{c}_{t-2}+\varepsilon_{t}\text{ for }t\stackrel{{\scriptstyle 2}}{{\equiv}}d.

As in the first simulation, we repeat the

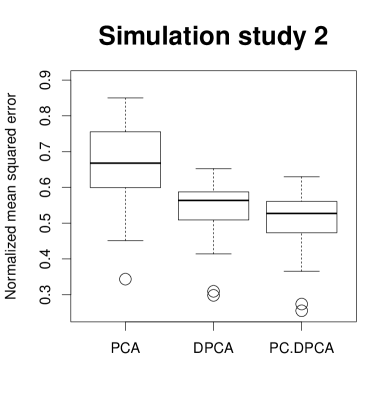

experiment 100 100 100 4 0.51 ( sd = 0.07 ) 0.51 sd 0.07 0.51\ (\operatorname{sd}=0.07) 0.55 ( sd = 0.07 ) 0.55 sd 0.07 0.55\ (\operatorname{sd}=0.07) 0.67 ( sd = 0.1 ) 0.67 sd 0.1 0.67\ (\operatorname{sd}=0.1)

Figure 4: Results of two simulation studies. We

repeat every simulation 100 times and report distribution of NMSE

from these repetitions. PC-DFPCA outperforms the two other methods

in both setups.

6 Proofs of the results of Section 3

To explain the essence and technique of the proofs, we

consider the special case of T = 2 𝑇 2 T=2 T 𝑇 T

Proof of Theorem 3.1 : To

establish the mean

square convergence of the series ∑ l ∈ ℤ Ψ l t ( X ( t − l ) ) subscript 𝑙 ℤ superscript subscript Ψ 𝑙 𝑡 subscript 𝑋 𝑡 𝑙 \sum_{l\in\mathbb{Z}}\Psi_{l}^{t}\left(X_{\left(t-l\right)}\right) S n , t subscript 𝑆 𝑛 𝑡

S_{n,t} S n , t = ∑ − n ≤ l ≤ n Ψ l t ( X ( t − l ) ) subscript 𝑆 𝑛 𝑡

subscript 𝑛 𝑙 𝑛 superscript subscript Ψ 𝑙 𝑡 subscript 𝑋 𝑡 𝑙 S_{n,t}=\sum_{-n\leq l\leq n}\Psi_{l}^{t}\left(X_{\left(t-l\right)}\right) n 𝑛 n m < n 𝑚 𝑛 m<n

(6.1) E ‖ S n , t − S m , t ‖ ℂ p 2 𝐸 superscript subscript norm subscript 𝑆 𝑛 𝑡

subscript 𝑆 𝑚 𝑡

superscript ℂ 𝑝 2 \displaystyle E\left\|S_{n,t}-S_{m,t}\right\|_{\mathbb{C}^{p}}^{2} = \displaystyle= ∑ m < | l | , | k | ≤ n E ⟨ Ψ l t ( X ( t − l ) ) , Ψ k t ( X ( t − k ) ) ⟩ ℂ p subscript formulae-sequence 𝑚 𝑙 𝑘 𝑛 𝐸 subscript superscript subscript Ψ 𝑙 𝑡 subscript 𝑋 𝑡 𝑙 superscript subscript Ψ 𝑘 𝑡 subscript 𝑋 𝑡 𝑘

superscript ℂ 𝑝 \displaystyle\sum_{m<\left|l\right|,\left|k\right|\leq n}E\left\langle\Psi_{l}^{t}\left(X_{\left(t-l\right)}\right),\Psi_{k}^{t}\left(X_{\left(t-k\right)}\right)\right\rangle_{\mathbb{C}^{p}}

≤ \displaystyle\leq ∑ m < | l | , | k | ≤ n E ( ‖ Ψ l t ( X ( t − l ) ) ‖ ℂ p ‖ Ψ k t ( X ( t − k ) ) ‖ ℂ p ) subscript formulae-sequence 𝑚 𝑙 𝑘 𝑛 𝐸 subscript norm superscript subscript Ψ 𝑙 𝑡 subscript 𝑋 𝑡 𝑙 superscript ℂ 𝑝 subscript norm superscript subscript Ψ 𝑘 𝑡 subscript 𝑋 𝑡 𝑘 superscript ℂ 𝑝 \displaystyle\sum_{m<\left|l\right|,\left|k\right|\leq n}E\left(\left\|\Psi_{l}^{t}\left(X_{\left(t-l\right)}\right)\right\|_{\mathbb{C}^{p}}\left\|\Psi_{k}^{t}\left(X_{\left(t-k\right)}\right)\right\|_{\mathbb{C}^{p}}\right)

≤ \displaystyle\leq ∑ m < | l | , | k | ≤ n ‖ Ψ l t ‖ ℒ ‖ Ψ k t ‖ ℒ E ( ‖ X ( t − l ) ‖ ‖ X ( t − k ) ‖ ) subscript formulae-sequence 𝑚 𝑙 𝑘 𝑛 subscript norm superscript subscript Ψ 𝑙 𝑡 ℒ subscript norm superscript subscript Ψ 𝑘 𝑡 ℒ 𝐸 norm subscript 𝑋 𝑡 𝑙 norm subscript 𝑋 𝑡 𝑘 \displaystyle\sum_{m<\left|l\right|,\left|k\right|\leq n}\left\|\Psi_{l}^{t}\right\|_{\mathcal{L}}\left\|\Psi_{k}^{t}\right\|_{\mathcal{L}}E\left(\left\|X_{\left(t-l\right)}\right\|\left\|X_{\left(t-k\right)}\right\|\right)

≤ \displaystyle\leq ∑ m < | l | , | k | ≤ n ‖ Ψ l t ‖ ℒ ‖ Ψ k t ‖ ℒ ( E ‖ X ( t − l ) ‖ 2 E ‖ X ( t − k ) ‖ 2 ) 1 2 subscript formulae-sequence 𝑚 𝑙 𝑘 𝑛 subscript norm superscript subscript Ψ 𝑙 𝑡 ℒ subscript norm superscript subscript Ψ 𝑘 𝑡 ℒ superscript 𝐸 superscript norm subscript 𝑋 𝑡 𝑙 2 𝐸 superscript norm subscript 𝑋 𝑡 𝑘 2 1 2 \displaystyle\sum_{m<\left|l\right|,\left|k\right|\leq n}\left\|\Psi_{l}^{t}\right\|_{\mathcal{L}}\left\|\Psi_{k}^{t}\right\|_{\mathcal{L}}\left(E\left\|X_{\left(t-l\right)}\right\|^{2}E\left\|X_{\left(t-k\right)}\right\|^{2}\right)^{\frac{1}{2}}

≤ \displaystyle\leq M ∑ | l | > m ∑ | k | > m ‖ Ψ l t ‖ ℒ ‖ Ψ k t ‖ ℒ for some M ∈ ℝ + 𝑀 subscript 𝑙 𝑚 subscript 𝑘 𝑚 subscript norm superscript subscript Ψ 𝑙 𝑡 ℒ subscript norm superscript subscript Ψ 𝑘 𝑡 ℒ for some 𝑀 superscript ℝ \displaystyle M\sum_{\left|l\right|>m}\sum_{\left|k\right|>m}\left\|\Psi_{l}^{t}\right\|_{\mathcal{L}}\left\|\Psi_{k}^{t}\right\|_{\mathcal{L}}\text{ \ \ \ }\mathrm{for}\text{ }\mathrm{some}\text{ }M\in\mathbb{R}^{+}

≤ \displaystyle\leq M ( ∑ | l | > m ‖ Ψ l t ‖ ℒ ) 2 . 𝑀 superscript subscript 𝑙 𝑚 subscript norm superscript subscript Ψ 𝑙 𝑡 ℒ 2 \displaystyle M\left(\sum_{\left|l\right|>m}\left\|\Psi_{l}^{t}\right\|_{\mathcal{L}}\right)^{2}.

Summability condition (2.5 6.1 n 𝑛 n m 𝑚 m { S n , t , n ∈ ℤ + } subscript 𝑆 𝑛 𝑡

𝑛

superscript ℤ \left\{S_{n,t},n\in\mathbb{Z}^{+}\right\} L 2 ( ℂ p , Ω ) superscript 𝐿 2 superscript ℂ 𝑝 Ω L^{2}\left(\mathbb{C}^{p},\Omega\right) t 𝑡 t 𝐘 𝐘 \mathbf{Y} t 𝑡 t i.e. ,

𝐘 t subscript 𝐘 𝑡 \displaystyle\mathbf{Y}_{t} = \displaystyle= ∑ l ∈ ℤ Ψ l 0 ( X ( t − l ) ) subscript 𝑙 ℤ superscript subscript Ψ 𝑙 0 subscript 𝑋 𝑡 𝑙 \displaystyle\sum_{l\in\mathbb{Z}}\Psi_{l}^{0}\left(X_{\left(t-l\right)}\right)

= \displaystyle= ∑ l ∈ ℤ Ψ 2 l 0 ( X ( t − 2 l ) ) + ∑ l ∈ ℤ Ψ 2 l − 1 0 ( X ( t − 2 l + 1 ) ) , t ≡ 2 0 subscript 𝑙 ℤ superscript subscript Ψ 2 𝑙 0 subscript 𝑋 𝑡 2 𝑙 subscript 𝑙 ℤ superscript subscript Ψ 2 𝑙 1 0 subscript 𝑋 𝑡 2 𝑙 1 𝑡 2 0

\displaystyle\sum_{l\in\mathbb{Z}}\Psi_{2l}^{0}\left(X_{\left(t-2l\right)}\right)+\sum_{l\in\mathbb{Z}}\Psi_{2l-1}^{0}\left(X_{\left(t-2l+1\right)}\right),\text{\ \ \ \ }t\overset{2}{\equiv}0

𝐘 t subscript 𝐘 𝑡 \displaystyle\mathbf{Y}_{t} = \displaystyle= ∑ l ∈ ℤ Ψ l 1 ( X ( t − l ) ) subscript 𝑙 ℤ superscript subscript Ψ 𝑙 1 subscript 𝑋 𝑡 𝑙 \displaystyle\sum_{l\in\mathbb{Z}}\Psi_{l}^{1}\left(X_{\left(t-l\right)}\right)

= \displaystyle= ∑ l ∈ ℤ Ψ 2 l 1 ( X ( t − 2 l ) ) + ∑ l ∈ ℤ Ψ 2 l + 1 1 ( X ( t − 2 l − 1 ) ) , t ≡ 2 1 , subscript 𝑙 ℤ superscript subscript Ψ 2 𝑙 1 subscript 𝑋 𝑡 2 𝑙 subscript 𝑙 ℤ superscript subscript Ψ 2 𝑙 1 1 subscript 𝑋 𝑡 2 𝑙 1 𝑡 2 1

\displaystyle\sum_{l\in\mathbb{Z}}\Psi_{2l}^{1}\left(X_{\left(t-2l\right)}\right)+\sum_{l\in\mathbb{Z}}\Psi_{2l+1}^{1}\left(X_{\left(t-2l-1\right)}\right),\text{\ \ \ \ }t\overset{2}{\equiv}1,

for each h ∈ ℤ ℎ ℤ h\in\mathbb{Z}

Cov ( 𝐘 2 h , 𝐘 0 ) Cov subscript 𝐘 2 ℎ subscript 𝐘 0 \displaystyle\mathrm{Cov}\left(\mathbf{Y}_{2h},\mathbf{Y}_{0}\right) = \displaystyle= lim n → ∞ ∑ | k | ≤ n ∑ | l | ≤ n Cov ( Ψ k 0 ( X ( 2 h − k ) ) , Ψ l 0 ( X ( 0 − l ) ) ) subscript → 𝑛 subscript 𝑘 𝑛 subscript 𝑙 𝑛 Cov superscript subscript Ψ 𝑘 0 subscript 𝑋 2 ℎ 𝑘 superscript subscript Ψ 𝑙 0 subscript 𝑋 0 𝑙 \displaystyle\lim_{n\rightarrow\infty}\sum_{\left|k\right|\leq n}\sum_{\left|l\right|\leq n}\mathrm{Cov}\left(\Psi_{k}^{0}\left(X_{\left(2h-k\right)}\right),\Psi_{l}^{0}\left(X_{\left(0-l\right)}\right)\right)