Maximum A Posteriori Learning in Demand Competition Games

Abstract

We consider an inventory competition game between two firms. The question we address is this: If players do not know the opponent’s action and opponent’s utility function can they learn to play the Nash policy in a repeated game by observing their own sales? In this work it is proven that by means of Maximum A Posteriori (MAP) estimation, players can learn the Nash policy. It is proven that players’ actions and beliefs do converge to the Nash equilibrium.

I INTRODUCTION

Assume two players are engaged in a strategic learning process in which they play a one-stage game repeatedly. In a one-stage game, at the beginning of every stage players order inventory levels by incurring ordering costs, and then a random demand occurs. If a player meets the demand she/he collects revenues. If a player has extra inventory levels at the end of the stage, she/he will incur holding costs. A proportion of any unmet demand will switch to another player. In this game the objective of every player is to make ordering decisions so as to maximize her/his own expected revenue.

We consider a scenario in which every player is informed of her/his own utility function but does not know the opponent’s utility function. Each player knows both her/his own local demand distribution and the opponent’s local demand distribution, but she/he cannot observe the current and past actions of the opponent. Players observe their own sales and remember their own previous sales. Players’ sales contain information about the opponent’s action. Each player constructs a belief about the opponent’s strategy set such that includes opponent’s Nash policy; i.e., player () assumes that the opponent plays a threshold policy with a uniform distribution over . A player’s belief is a conditional probability density function over the opponent’s strategies given the previous sales. At every stage of the repeated game, players observe their own sales and then update their beliefs about their opponent’s strategy set. At every stage of the repeated game, every player has a belief about the opponent’s strategy set. At every stage of the repeated game, players compute the Maximum A Posteriori (MAP) estimation of their belief and play their best response to that strategy.

The studies most related to this work are [1]-[5]. Authors in and address the competitive inventory game. Various authors have argued the convergence to Nash equilibrium in games with a finite strategy set (see and ).

I-A Notation

I-B One-Stage Game

Consider two players without initial inventory levels. Each player brings his inventory level to , where , by incurring the total ordering cost , where is the variable ordering cost per unit. Then each player receives the random demand from the customers for whom player is the first choice. If the demand is unmet by player , i.e., , then a fixed proportion of this unmet demand switches to player . Therefore, the total demand faced by player becomes

in which . We will suppress the dependence of on when there is no possibility of confusion. Subsequently, player collects the revenues and incurs the holding cost where is the unit revenue and is the unit holding cost. As a result, player ’s utility function is given as

where the expectation is taken with respect to and

We denote the game characterized by the utility functions given above and the strategy sets as .

I-C Repeated Games

Player’s utility function, given actions , is

the expectation is over local demands and , in which

In repeated games, players try to maximize their own utility function given their belief about their opponent’s strategy. Assume the information vectors and beliefs at stage are given. The learning process at stage is given below:

-

1.

Players choose optimal actions , given their belief about the opponent’s action:

-

2.

Demands occur, and players observe their own sales:

where and are defined as random outcomes respectively for local demands and at stage with density functions and .

-

3.

Players update their information vectors:

-

4.

Players update their beliefs about the distribution of the opponent’s strategy:

The learning process at stage is similar to stage . In this work it will be shown that where is the Nash equilibrium:

in which

II Discrete Learning Model

At the first stage there is no sales history, and the information vector is given as . supposes that plays a threshold policy with a uniform distribution on , therefore the initial belief is the continuous density function for . It is noticeable that . To make the model discrete, for example, let step size be . ’s discrete belief about the distribution of ’s strategy at stage is , where and , stands for the probability that ’s strategy will be , given . It is noticeable that .

At the first stage, ’s initial discrete belief about ’s action, , is , in which

At the first stage, players choose the optimal actions given their belief about the distribution of the opponent’s strategy. Then demands occur, and players observe their own sales and update their belief about the distribution of the opponent’s strategy based on Bayes’s rule.

At the second stage, the information vector is , and ’s discrete belief about opponent’s action is , where

From (1),

From (2) and (3),

,

.

Discrete local demands are

for ,

for .

It is noticeable that

,

,

,

where is defined as

,

,

.

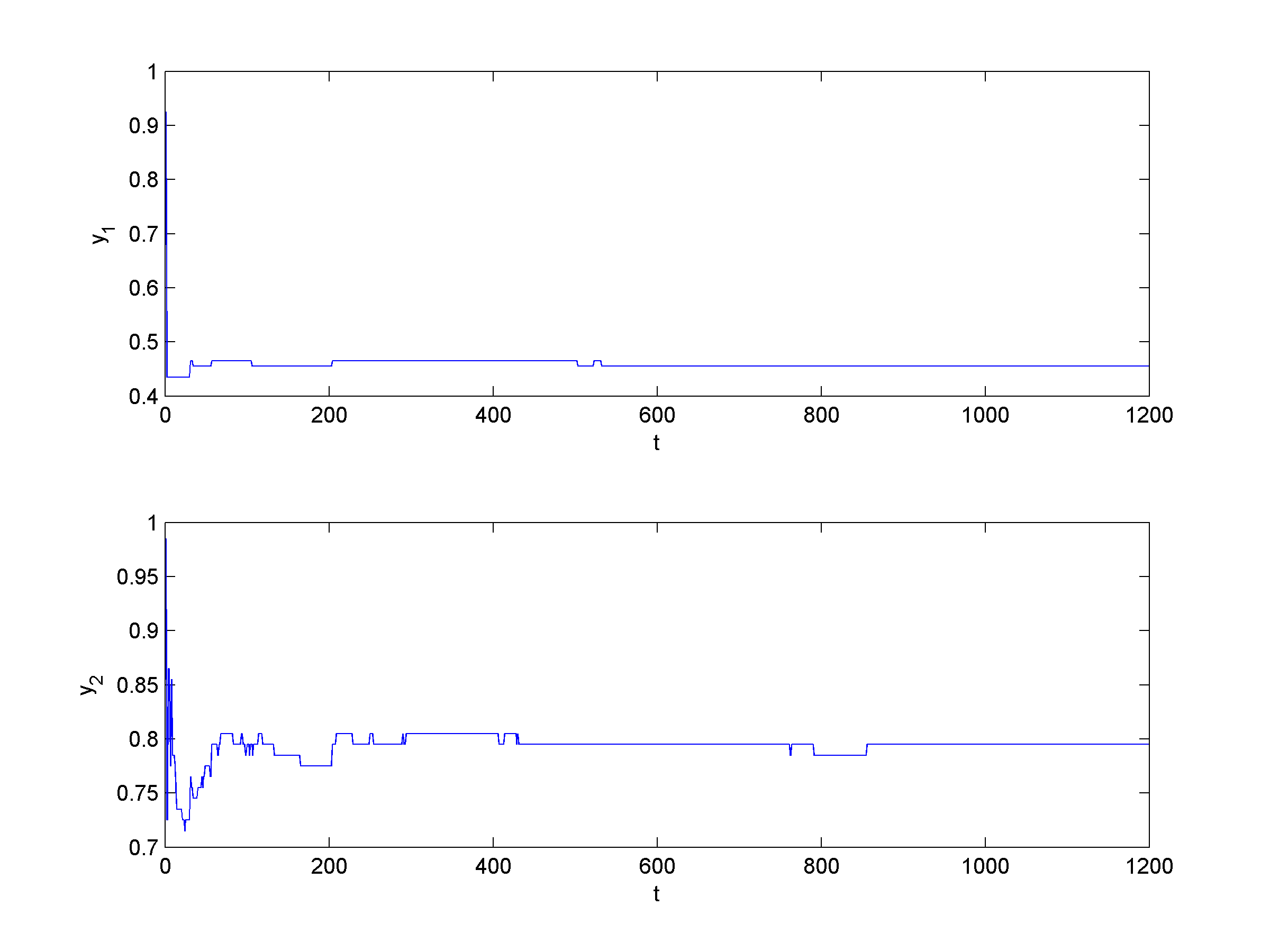

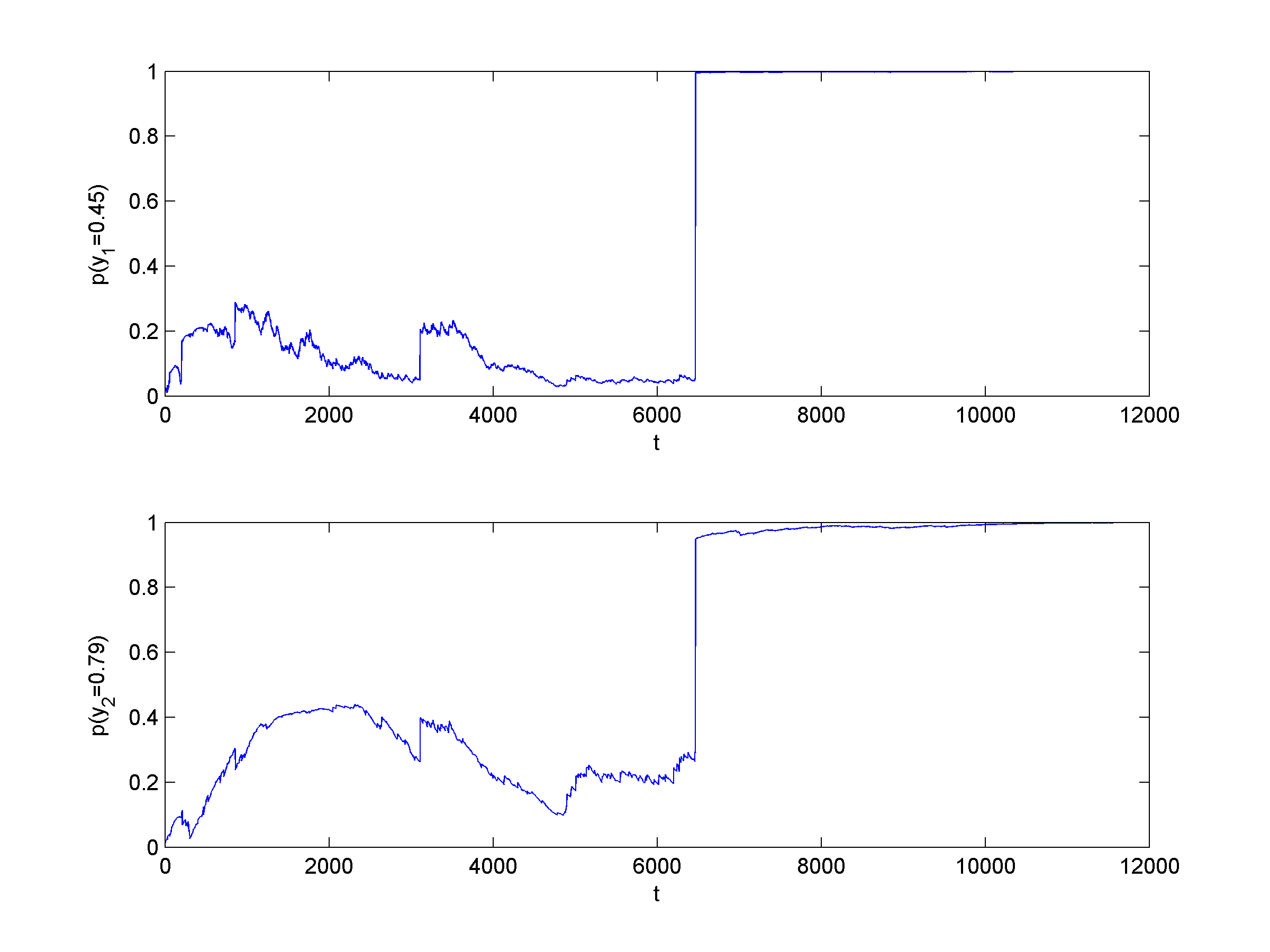

Example 1: Consider the case , , , , and for , . To make the model discrete, let step size be . In figures 1 and 2, it is shown that by means of MAP estimation players’ actions and beliefs converge to the Nash equilibrium .

III Convergence to the Nash Equilibrium

At the first stage, believes that will choose a policy in the interval with density function , and similarly, believes that will choose a policy in the interval with density function . Proposition 1 means that there exists an interval such that will not play any policy in .

Proposition 1: For at least one of the players, without loss of generality for , there exists an interval or or , such that for . This means that will never play any policy in . Proof is given in the Appendix.

It is noticeable that the set can always be found unless and .

Proposition 2 means that if there exists an interval such that does not choose any policy in then will eventually figure out that .

Proposition 2: If there exists an interval , without loss of generality , such that for , then for any given ,

Proof is given in the Appendix.

Theorem: Players’ actions in the demand competition game will converge to the Nash equilibrium, , by MAP.

Proof: At the first stage, believes that will choose a policy in the interval with density function , and similarly, believes that will choose a policy in the interval with density function .

Without loss of generality, assume

Here the worst-case is considered, in which

According to Proposition 2, for the given there exists an such that ,

According to Proposition 2, for the given there exists an such that

Let define,

According to Proposition 2, for , and

; therefore,

It is evident that and . According to Proposition 1, without loss of generality, assume

According to Proposition 2, for the given there exists an such that ,

According to Proposition 2, for the given there exists an such that ,

Let define,

According to Proposition 2, for , and

; therefore,

According to Proposition 1, without loss of generality, assume

Because and because according to Proposition 2, for the given there exists an such that , where

Because and because according to Proposition 2, for the given there exists an such that , where

Let define,

It is easy to check that and

.

Similarly, a sequence can be found such that

and

Let

because of the uniqueness of the Nash equilibrium, . For the given there exists an such that for , ; hence for , and .

In summary, by using Proposition 1 and 2 an infinite sequence of sets, can be found such that , in which

-

1.

,

-

2.

-

3.

and

Therefore convergence to the Nash equilibrium follows.

IV CONCLUSIONS

This work introduce a two-player competitive game in which players do not know the opponent’s utility function and the opponent’s action. It is shown that players can learn the Nash equilibrium by engaging in a strategic learning process in which they play a one-shot game repeatedly. Players construct a belief about their opponent’s strategy set and play their best response to the Maximium A Posteriori (MAP) of their beliefs. In every stage players observe their own sales and update their beliefs about their opponent’s strategy set. It is proven that players’ beliefs and actions will converge to the Nash equilibrium. Future work can be done that would investigate the case in which players do not know their opponent’s local demand distribution.

V Appendix

V-A Proof of Proposition 1

According to [1]-[5] the Nash equilibrium is unique. It can be claimed that 2) and 3) cannot be satisfied simultaneously unless . Similarly, 1) and 4) cannot be satisfied simultaneously unless .

-

1.

-

2.

-

3.

-

4.

Suppose 2) and 3) are satisfied, since best response functions are nonincreasing (Proposition 1 part 2b); therefore,

the odd-numbered inequalities result from 2) and the even-numbered inequalities result from 3). From Proposition 1 part 4) it is evident that (5) contradicts the uniqueness of the Nash equilibrium unless because the initial assumption was that .

Similarly, suppose 1) and 4) are satisfied, then

the odd-numbered inequalities result from 1) and the even-numbered inequalities result from 4). It is evident that (6) contradicts the uniqueness of the Nash equilibrium unless , because the initial assumption was that .

It is assumed, without loss of generality, that . Because the best response functions are nonincreasing (Proposition 1), it follows that

Therefore, .

The case and can be proved in the same manner.

V-B Proof of Proposition 3

It is easy to check that

Lemma: For every

,

where the conditional expectation is taken with respect to given .

Proof:

in which .

It is evident that , unless ; therefore,

and by taking sum over

From [8] (page 418)

therefore

and let be , then

References

- [1] A. Zeinalzadeh, A. Alptekinoglu, and G. Arslan, On Existence of equilibrium in inventory competition with fixed order costs, submitted, Operations Research Letters, August 5, 2015.

- [2] A. Zeinalzadeh, Learning in inventory competition games, University of Hawaii at Manoa, May 2013.

- [3] A. Zeinalzadeh, A. Alptekinoglu and G. Arslan, Inventory competition under fixed order costs, INFORMS MSOM (Manufacturing and Service Operations Management) Annual Conference, Technion, Haifa, Israel, June 28-29, 2010.

- [4] A. Zeinalzadeh, A. Alptekinoglu, and G. Arslan, Learning in infinite-horizon inventory competition with total demand observations, Proceedings of the American Control Conference, Montreal Canada, June 27-29, 2012, pp. 1382-1387.

- [5] A. Zeinalzadeh, A. Alptekinoglu, and G. Arslan, Distribution-Free learning in inventory competition, presented at the 4th World Congress of the Game Theory Society, July 22-26, 2012, Istanbul, Turkey.

- [6] Ferguson, Thomas Shelburne, A course in large sample theory, 1929.

- [7] Parlar, M. Game theoretic analysis of the substitutable product inventory problem with random demands. Naval Research Logistics, 35, 1988, pp 397-409.

- [8] Netessine, S. Rudi, N. Centralized and Competitive Inventory Models with Demand Substitution Operations Research, March 1, 51(2), 2003, pp 329-335.

- [9] Netessine, S., Rudi, N., and Wang, Y. Inventory competition and incentives to back-order. IIE Transactions, 38(11), 2006, pp 883-902.

- [10] Nachbar, J.H., Prediction, optimization, and learning in games. Econometrica 65, 1997, pp 275-309.

- [11] Nachbar, J.H., Bayesian learning in repeated games of incomplete information. Social Choice and Welfare 18, 2001, pp 303-326.

- [12] Kalai, E., Lehrer, E., Rational learning leads to Nash equilibrium. Econometrica 61, 1993, pp 1019-1045.

- [13] E. Parzen, Modern probability theory and its application. John Wiley and Sons, New York, 1960.