A Contract Design Approach for Phantom Demand Response

Abstract

We design an optimal contract between a demand response aggregator (DRA) and power grid customers for incentive-based demand response. We consider a setting in which the customers are asked to reduce their electricity consumption by the DRA and they are compensated for this demand curtailment. However, given that the DRA must supply every customer with as much power as she desires, a strategic customer can temporarily increase her base load in order to report a larger reduction as part of the demand response event. The DRA wishes to incentivize the customers both to make costly effort to reduce load and to not falsify the reported load reduction. We model this problem as a contract design problem and present a solution. The proposed contract consists of two parts: a part that depends on (the possibly inflated) load reduction as measured by the DRA and another that provides a share of the profit that accrues to the DRA through the demand response event to the customers. Since this profit accrues due to the total load reduction because of the actions taken by all the customers, the interaction among the customers also needs to be carefully included in the contract design. The contract design and its properties are presented and illustrated through examples.

I Introduction

Demand Response (DR), in which a utility company or an aggregator motivates customers to curtail their power usage, has now become an acceptable method in situations where high peaks in demand occur, transmission congestion increases, or some power plants are not available to generate enough power [2, 3, 4, 5]. Per the Federal Energy Regulatory Commission (FERC), demand response is the change in electric usage by end-use customers from their normal consumption patterns in response to changes in the price of electricity or any other incentive [6].

In general, DR programs may be divided into two main categories: Price Based Programs (PBP) and Incentive Based Programs (IBP). PBPs refer to schemes in which the electricity price varies as a function of variables such as the time of usage or the total demand, with the expectation that the consumers will adjust their demand in response to such a price profile. On the other hand, IBPs offer a constant price for power to every user; however, customers are offered a reward if they reduce their demand when the utility company desires. Classically, these incentives were proposed to be constant and based only on customer participation in the program; however, market-based incentives that offer a reward that varies with the amount of load reduction that a customer achieves have also been proposed. There exists a rich literature for IBPs (e.g, see [7, 8, 9, 10] and the references therein) studying the design of suitable incentives with aims such as social welfare maximization, minimization of electricity generation and delivery costs, and reducing renewable energy supply uncertainty for demand response.

In this paper, we consider an incentive based program for demand response where the customers are rewarded financially by a demand response aggregator (which role can also be filled by a utility company) for their load reduction during DR events. When called upon to reduce their loads, each customer puts in some effort to achieve a true value of load reduction. The effort is costly to the customers since it causes them discomfort. Further, the amount of effort expended is private knowledge for each customer. Incentivizing customers to put in effort in this setting is the problem of moral hazard [11, Chapter 4]. Following the rich literature back to Holmstrom [12], as a means to incentivize the customer to put in ample effort in the presence of moral hazard, the demand response aggregator (DRA) must pay each customer proportional to the effort that the customer puts in. However, by taking advantage of the fact that the DRA must supply as much power as the customer desires and by anticipating the demand response call, a strategic customer can artificially inflate her base load before an expected DR event. In other words, the true amount of load reduction is also private knowledge for the customer. By artificially inflating the base load, for the same nominal load reduction, the customer can report more measured load reduction and gain more financial reward from the DRA [13, 14]. This implies that the problem of adverse selection [11, Chapter 3] is also present.

That such strategic behavior by customers to exploit IBPs is not idle speculation has been pointed out multiple times [14], [15]. In 2013, it was revealed that the Federal Energy Regulatory Commission issued large civil penalties to customers for exactly this sort of strategic behavior [16]. For instance, Enerwise paid a civil penalty of $780,000 for wrongly claiming on the behalf of its client, the Maryland Stadium Authority (MSA), that it reduced the baseline electricity usage in 2009 and 2010 at Camden Yards. It may also be pointed out that the possibility of behavior in which “phantom DR occurs through inflated baseline” to obtain “payments for fictitious reductions” was pointed out in a related but different context by California ISO in its opinion on FERC order 745 [17]. To avoid this phantom demand response, a payment structure to incentivize a rational customer to provide maximal effort and low (or no) misreporting is needed.

While there is much literature that uses competitive game theory in smart grids particularly for solutions based on concepts such as pricing (e.g., [18], [19] and the references therein), much of this literature assumes the users to be truthful and non-anticipatory. While this is often a good assumption in cases where users are price taking and either unable or unwilling to transmit false information, it can lead to overly optimistic results in the framework discussed above. We consider anticipatory and strategic customers that maximize their own profit by predicting the impact of their actions and possibly falsifying any information they transmit.

Of more interest to our setting is the literature on contract design for DR with information asymmetry and strategic behavior. For instance, [13] proposed a DR contract that avoids inefficiencies in the presence of a strategic sensor; however, the possibility of baseline inflation was not considered. [20] proposed a DR market to maximize the social welfare; however, the baseline consumption levels were assumed to be known. The works closest to ours in this stream are [21] and [22]. [21] considered a two-stage game for DR. Assuming knowledge of the utility function of the consumer, the authors proposed using a linear penalty function for the deviation of the usage level from the reported baseline to induce users to report their true baselines, while at the same time adjusting the electricity price appropriately to realize the desired load reduction. [22] designed a two-stage mechanism to induce truth telling by the customer irrespective of the utility function of the DRA. The proposed mechanism relied on assuming a linear utility function for the customers, a deterministic baseline and a low probability of occurrence of the DR event. Unlike these works, we design a contract which maximizes the utility function of the DRA (which includes the payment to the customer) and a more general utility function for the customer that includes falsification and effort costs, as well as constraints of individual rationality.

In economics, contract design with either moral hazard or adverse selection alone has a vast literature (for a summary, see, e.g., [23, Chapter 14B] and [23, Chapter 14C]). In the problem we consider, moral hazard followed by adverse selection arises. This combination is much less discussed in the literature and is significantly more difficult since incentives to solve moral hazard (for instance, through payments that are an increasing function of the reported effort) may, in fact, exacerbate the problem of adverse selection by incentivizing larger falsification of the reported effort. A notable exception is [11, Chapter 7] which considers a specific buyer-seller framework with two hidden actions and two hidden pieces of information. In this stream, the closest works to our setup are [24, 25] who study the problem of incentivizing a single manager (a single customer in our framework) by the owner of a firm (the DRA in our framework) and propose a contract by assuming accurate revelation of the private information of the manager to the owner in long run. Our formulation includes the more general case of multiple customers with the DRA obtaining non-accurate knowledge of the load reduction by the customers even in the long run.

The chief contribution of this paper is the design of a contract to maximize the utility function of the DRA while incentivizing rational customers to expend costly effort to reduce their load. The contract addresses the issue of moral hazard followed by adverse selection that is enabled by the fact that knowledge of the effort put in as well as that of the true load savings realized are both private to the customers. The contract that we propose consists of two parts: one part that pays the customer based on the (possibly falsified) reported load reduction, and another that provides a share of the profit that accrues to the DRA through the demand response event to the customer. One interesting result is that the optimal contract may lead to both under-reporting and over-reporting of load reduction by the customer depending on the true load reduction realized by the customer. In other words, if a strategic customer wishes to maximize her profit, she may sometimes decrease her base load before the DR event to under-report her power reduction as a part of DR event. We also show that the DRA can realize any arbitrary demand reduction by contracting with an appropriate number of customers.

The rest of the paper is organized as follows. In Section II, the problem statement is presented. In Section III, we propose a contract structure for the DR problem. Next, in Section IV, we derive the optimal strategy chosen by DRA and the customers in response, discuss the interactions among customers, and study several extensions of the problem. In Section V, numerical examples are provided to illustrate the results. Section VI concludes the paper and presents some avenues for future work.

Notation

(which is often simplified to when the meaning is clear from the context) denotes the probability distribution function (pdf) of random variable given the event . A Gaussian distribution is denoted by where is the mean and is the standard deviation. For two functions and , denotes the convolution between and . specifies that the expectation of function is taken with respect to the random variable ; when is clear from the context, we abbreviate the notation to . Given variables , the set defining their collection is denoted by , or sometimes simply by .

II Problem Statement

During a DR event, the DRA calls on the customers to decrease their power consumption. A contract that pays the customers merely for the act of reducing the load will not incentivize the customers to exert the maximal effort for reducing the load by as much amount as possible. To solve this problem, the DRA may offer a contract that makes the payment to the customer proportional to the load reduction. However, with such a contract, a strategic customer will try to anticipate the DR event and increase her base load, i.e., the load before the demand response event began. This pre-increase allows the customer to reduce the load during the DR event by a larger amount than would have been possible in the absence of such an increase; thus, receiving a larger payment even though the DRA accrues the benefit of only a smaller true load reduction. The central problem considered in this paper is to design a contract that is free from both these problems.

Remark 1.

It is worth pointing out that the falsification of the load reduction claimed by the customer may happen even though the load at the customer is being monitored constantly and accurately. Further, the DRA can not find the ‘true’ base load by considering the load used by a customer at some arbitrary time before the DR event. For one, this simply shifts the problem of customer manipulation of the load to an earlier time. Second, some of the increase in the base load may be due to true shifts in customer need due to, e.g., increased temperature.

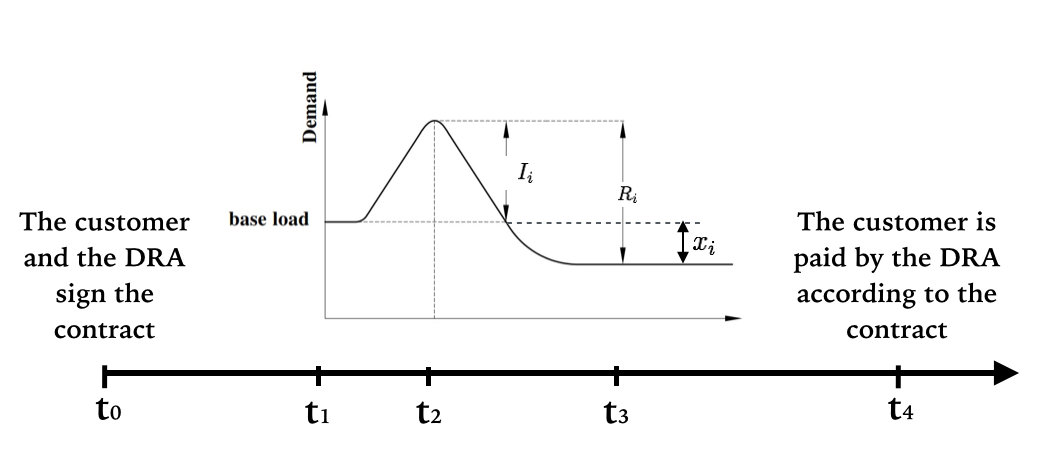

II-A Timeline

Consider customers denoted by that are contracted with a DRA. We refer to the timeline shown in Figure 1 to explain the sequence of events. At time , strategic customers anticipate that a DR event is likely to begin at time . Accordingly, at this time, each customer calculates the effort she is willing to put in for the load reduction during the DR event. We assume that this effort costs the customer . Further, this effort leads to a reduction in the load by an amount that can depend on local conditions that are private knowledge for the -th customer. For instance, a factory might be able to induce a large load reduction with a small effort based on its assembly line requirements given the orders it has to fulfill. The DRA is assumed to know the probability density function according to which is realized, while the customer knows the local conditions and can calculate the value of that will be realized. After this calculation, each customer at time may increase (or decrease) the load by an amount in anticipation of the DR event.

Assumption 1.

The random variables describing the load reductions are conditionally independent given the actions taken by all the customers, so that

Assumption 2.

At time , the DR event begins and the DRA calls on the customers to decrease their loads. Each customer now makes the predetermined effort leading to a reduction of her load by . The DR event ends at with each customer having reported that she decreased the load by an amount . Note that the true reduction in the load for the -th customer is , while the false report111We wish to emphasize again that the load at the customer is being accurately monitored at all times. is .

We also show the times and in the timeline in Figure 1. At time (much before ), the contract specifying the payment structure is signed between the DRA and the customers. We assume that is sufficiently early, so that at , the customers too do not know the local conditions and must consider their expected utility according to the probability density functions (or, equivalently, ). At time , at least a part of the payment as specified by the contract to the customers is paid by the DRA to incentivize them to participate in the DR event. The time is sufficiently close to the DR event, so that the realized value of is not known at time to the DRA. The contract may specify that the rest of the payment is done at some later time , when the DRA may have more knowledge of the true value of .

II-B Utility Functions

The effort cost suffered by the -th customer for an effort is given by a function that is known to all the customers and the DRA. Further, for a true reduction , if the customer manipulates her base load and reports the reduction to be she suffers a falsification cost . This can model, e.g., any extra payment by the customer for boosting her consumption as she manipulated the load prior to the DR event. For simplicity, we assume that where . Thus, with a payment , the utility of the -th customer is given by

The utility of the DRA is given by its net profit, which is the difference of the gross profit that occurs due to the load reduction by the customers and the payments made to the customers as part of the contract. For simplicity, we assume that the gross profit made due to reduction of load is equal to ; more complicated cases can be easily considered. With a total payment , the utility of the DRA is given by

II-C Problem Formulation

We assume that the customers and the DRA are rational and risk neutral, so that they seek to maximize the expected value of their utility functions. The problem we consider in this paper is for the DRA to design a contract that maximizes its own utility when rational customers choose actions and reports to optimize their own utility functions. Denote by the set of random variables describing the actual load reductions generated by the customers, i.e, and by the set . Further, denote by the set of random variables describing the load reductions of all customers except , i.e, and by the set . Thus, the optimization problem to be solved by DRA is given by

As stated in problem , we impose two constraints on the contract.

Individual rationality

We assume that the DRA can not force customers to participate in the load reduction program due to political or social reasons. Instead, the contract should be individually rational so that a rational customer chooses to participate. We impose this constraint in the form of ex ante individual rationality. This constraint requires that no customer chooses to walk away from the contract at time before she knows either her own load saving or the savings of the other customers; thus,

Incentive compatibility

Incentive Compatibility is a standard constraint imposed in mechanism design which is used to limit the space of the contracts we need to optimize over (see, e.g., [26]). Specifically, this constraint implies that the utility of the consumers does not increase if they calculate their report based on any arbitrary quantity other than the true value of their load reduction . Further, this constraint also implies that without loss of generality, a customer with private information of load reduction would always prefer the payment over the alternatives for any .

We make the following further assumptions:

Assumption 3.

-

(i)

(Deterministic Policies) The customers choose effort according to deterministic policies. Stochastic policies would imply additional stochasticity in that we do not consider in this paper.

-

(ii)

(Communication Structure) Individual customers cannot communicate with each other, so that the load reduction claimed by the -th customer as well as the true profit and hidden action for this customer are not known to the other customers. The DRA does not have access to and till possibly at a much later time

-

(iii)

(Public Knowledge of Functional Forms) The functional forms of , , the probability distribution functions , the weights , and the contracts offered are known to all the customers and the DRA.

We now proceed to present our solution to the problem .

III Structure of the Proposed Contract

In this section, we present a contract as a solution of the problem . To this end, we begin by discussing why some intuitive contracts may fail.

III-A Some Intuitive Contracts

For simplicity, in this section, we restrict our attention to the scenario when only one customer is present. For notational ease, when , we drop the subscript referring to the -th customer.

Example 1.

Consider a contract that provides a constant payment to the customer for decreasing her load. Then, the utility function of the customer is given by:

where is the unit step function. In this case, the customer seeking to maximize her utility, will choose (i.e., no action) but (i.e., minimal load reduction reported irrespective of true value of ), independently of the value of . The utility function of the DRA is given by

Thus, if zero action leads to zero true load reduction, the DRA ends up making a payment in spite of not achieving any load reduction. Thus, this contract is unsuitable for the DRA.

The contract proposed in Example fails because it does not account for the fact that the amount of effort is known only to the customer and not the DRA. Since the effort is costly, this generates the problem of moral hazard [11, Chapter 4]. To induce a positive load reduction in spite of the presence of moral hazard, the contract must make at least part of the payment proportional to the amount of the load reduction. Otherwise, as discussed above, a rational customer will not choose any non-zero effort.

Example 2.

Consider a contract in which the DRA provides an incentive to the customer in response to the reported reduction at time . Then, the utility function of the customer is given by:

while the utility function of the DRA is given by

Especially if is small, this contract would result in the customer choosing and misreporting a large to maximize . Once again, the contract will be unsuitable for the DRA.

The reason the contract in Example fails is that the DRA does not have access to the true load reduction at when it has to make at least part of the payment. This creates the problem of adverse selection [11, Chapter 3]. If the DRA relies on the reported value for the payment, this creates an incentive for the customer to misreport as high as possible to gain maximal payment (modulo the falsification cost).

Remark 2.

If the problem is one that displays only one of moral hazard or adverse selection, optimal contracts can be designed using standard methods from the literature. However, such contracts are unsuitable for the problem since we face the problem of moral hazard followed by adverse selection.

We conclude this discussion with the following result.

Lemma 1.

Assume that the DRA has accurate knowledge of the true load reduction at time .

-

•

The level of effort by the -th customer which maximizes the utility of the DRA is given by

-

•

The DRA can ensure that the effort is expended by the each customer by offering a contract that specifies payments of the form

(2)

Proof.

See Appendix. ∎

Next, we propose a contract structure for the problem using a two-part payment structure.

III-B Proposed Contract Structure

The contract that the DRA offers to the customers should at once incentivize them to put in costly effort and to report the load reduction truthfully. We propose a contract in which the payment to the -th customer is given by a pair of the form , where

-

•

is a bonus which is rewarded to the -th customer at after the customer reports load reduction , and

-

•

is the share of its own gross profit that the DRA realizes due to the demand reduction by the customers and pays back to the -th customer at a much later time .

Note that the payment of the share supposes that the DRA knows the profit it obtains as a result of the load reductions by the customers at time . We first consider the case when this profit is known to the DRA perfectly. We then extend the results to the case when the gross profit can only be estimated (possibly with some error) in Section IV-D2.

The proposed contract results in the payment function for the -th customer as given by

| (3) |

Further, the utility function of the customer can be written as

| (4) |

while the utility function for the DRA is given by

| (5) |

By invoking the revelation principle [11], without loss of optimality, we restrict attention to direct mechanisms (where ) that are incentive compatible. Further, to emphasize the dependence of the utilities on the bonus function and the share, we will sometimes write as and as

Finally, to ensure that the problem is non-trivial with this contract, we will impose the following further constraints on the problem.

Assumption 4.

The DRA does not provide all the profit back to the customers, i.e., .

Assumption 5.

The bonus is always positive, i.e., . will imply that the DRA can fine the customers which we disallow in keeping with the individual rationality constraints. We will also assume that is twice differentiable and concave in and further that is designed such that is concave in , where is the optimal report by the -th customer as a function of her load reduction.

IV Design of the Contract

In this section, we solve for the optimal contract by solving the problem . We begin by exploring the design space in terms of identifying the properties that any contract should satisfy.

IV-A An Impossibility Result

The first question that arises is if we can design any contract that incentivize the consumers not to misreport and set for all . While naive applications of the revelation principle may suggest that such contracts are not only possible, but that limiting our consideration to such contracts is without loss of generality, this is not the case if the revelation principle is interpreted properly in our context. Note that the if a contract that ensures were possible, Lemma 1 states that the optimal efforts as desired by the DRA are given by .

Theorem 1.

Proof.

See Appendix. ∎

IV-B Contract Design

We now design the payment schemes for the contract to solve problem . We solve problem in three steps:

-

1.

First, we characterize what the optimal value of the load reduction claimed by each customer would be for a given contract . Thus, we find the optimal value of , as the solution of the problem

(6) -

2.

Then, for this value , we calculate the optimal effort exerted by the customers, i.e., we solve the problem

(7) -

3.

Finally, having characterized the response of the customers, we optimize the parameters of the proposed contract for the DRA. Thus, we solve

(8)

when the customers exert the efforts and report reductions . We continue with the following result on the first step.

Theorem 2.

Consider the optimization problem . The optimal choice of the reported load reduction obtained as a solution to the problem (6) is given by the solution to the following equation

| (9) |

Proof.

See Appendix. ∎

This result characterizes the optimal reporting by the customer. We note the following interesting feature.

Corollary 1.

With the payment scheme in problem , if is a decreasing (respectively increasing) in , then the customer underreports (respectively overreports) her true load reduction.

Proof.

The proof follows directly from (9). ∎

Remark 3.

Since may be a decreasing and an increasing function for different values of , the optimal contract may induce both under-reporting and over-reporting of the load reduction by the customer. In other words, for some values of the true load reduction, it is possible that a strategic customer may decrease her base load before the DR event and under-report her power reduction to maximize her profit.

Next, we characterize the optimal effort by solving the problem (7).

Theorem 3.

Consider the optimization problem . The optimal choice of the effort is obtained as the solution of the equation

| (10) |

where is as specified in Theorem 2.

Proof.

See Appendix. ∎

Finally, having characterized the response of the customers, the third step is to optimize the parameters of the proposed contract by solving (8).

Theorem 4.

Proof.

Proof follows directly from (8). ∎

IV-C Example Contracts

Notice that equations (9)-(12) do not constrain the choices of the contract terms or the resulting actions of the customers to be unique. We now make more assumptions on the problem and provide some example contracts that result. We consider two scenarios:

-

•

Unspecified load reduction: In the first scenario, we consider the case when the DRA is interested in the overall load reduction from all the customers to be as large as possible. In this case, we propose a bonus function of the form for every customer with , where is a specified constant.

-

•

Specified load reduction: In the second case, we assume that the DRA wishes the overall load reduction to be equal to a given value . In this case, the customers are in competition with each other for the load reduction they provide and the consequent payment they obtain. Thus, we must consider the bonus function to customer to be a function of not only her own report , but also the reports from other customers. Following the classical Cournot game [27], we propose a bonus function of the form , where is a designer-specified parameter that depends on .

IV-C1 Unspecified load reduction

We begin with the case when the bonus function is of the form for all customers. In this case, there is no competition among the customers. Our first result says that we can simplify the incentive compatibility constraint.

Lemma 1.

Consider the problem such that , the bonus function does not depend on and is further of the form . If the proposed contract structure in (3) is incentive compatible, then it holds that

In particular for the contract , these conditions reduce to

Proof.

See Appendix. ∎

Remark 4.

The result implies that an incentive compatible contract will associate higher load reduction with a higher report .

With this result, we can restate the problem to be solved by the DRA as

The following result summarizes the optimal contract and the resulting actions under it for the problem .

Theorem 5.

Consider the problem posed above.

-

•

The optimal contract obtained as a solution to the problem is specified by the relations

-

•

In response to this optimal contract, every customer over-reports her true load reduction as . Further, the customer exerts the effort

Proof.

See Appendix. ∎

Remark 5.

Note that the constraint that implies the condition

IV-C2 Specified load reduction

We now consider the case when . Once again, we can simplify the incentive compatibility constraint according to the following result.

Lemma 2.

Consider the problem with a bonus function for the -th customer that depends on the report submitted by the -th customer and the sum of the reports submitted by all other customers. If the proposed contract is incentive compatible, then it holds that

In particular for the contract , these conditions reduce to

| (13) | |||

Proof.

See Appendix. ∎

We can now restate the problem to be solved by the DRA as follows.

Since the bonus paid to -th customer is a function not only of , but also of the reports from the other customers, the customers compete against each other to gain the maximum compensation possible. Thus, the optimal strategies of the players become interdependent. We analyze this interdependence in the usual Nash Equilibrium sense. For the following result, we make the simplification that all the parameters ’s and ’s are constants with and , .

We first present the following initial result.

Theorem 6.

Consider the problem . Define the variables

There is a unique Nash Equilibrium among the users and the DRA as given by the following:

-

(i)

The DRA selects the contract as

(14) (15) -

(ii)

The customers exert the optimal effort and report as

(16) (17) where

This equilibrium always exists.

Proof.

See Appendix. ∎

Remark 6.

To obtain the conditions for , we can substitute (14) in (15) to obtain

Note that the denominator evaluates to

Thus, the condition for is refined to the choice of , and which satisfy

The condition implies that as the desired load reduction increases, the number of customers that the DRA contracts with must increase as well.

Remark 7.

Note that the optimal level of the effort expended by the -th customer is an increasing function of both the assigned share and the total amount of desired load reduction , which is intuitively specifying.

IV-D Extensions

Although the above development was done with some specific assumptions, the contracts can be generalized to remove many of these assumptions. We provide some examples below. For notational ease, we consider the case when and drop the subscript referring to the -th customer. Further, we assume that the parameter and the bonus function is given by

IV-D1 Realization error with non-zero mean

The effort by the customer is assumed to lead to the realization of load reduction . As specified by Assumption 2, in the development so far, we assumed that the realization error is a random variable with mean zero. If, instead, the error has mean , then the following result summarizes the optimal contract.

Proposition 1.

Consider the problem for and mean of the realization error.

-

•

The optimal contract is given by

-

•

The optimal effort and the report by the customer are given by

Proof.

The proof follows in a straight-forward manner along the lines of that of Theorem 6. ∎

Remark 8.

Note that the optimal reporting function does not depend on . Further, as increases (resp. decreases),

-

•

the expected load saving for the same contract increases (resp. decreases),

-

•

the optimal effort exerted by customer is lower (resp. higher),

-

•

the optimal value of the share provided by DRA to the customer will increase (resp. decrease).

IV-D2 Inexact knowledge of the true load reduction

So far, we assumed that at , the DRA has an accurate knowledge of the true load reduction due to the customer. In practice, it may only be able to estimate this reduction by, e.g., large scale data analysis on all similar customers on that day or historical behavioral of the same customer. Let the DRA observe a noisy estimate of the load reduction at , where denotes the estimation error. We assume that this error in independent of and has mean . In this case, the share of the profit assigned to the customer changes to . In other words, the utility functions of the customer and the DRA from (4) and (5) alter to

| (18) | ||||

| (19) |

We have the following result that can be proved along the lines of Theorem 6.

Proposition 2.

Remark 9.

Note that the optimal reporting function and the optimal effort do not depend on . Further, as increases (resp. decreases), the optimal value of the share provided by DRA to the customer decreases (resp. increases).

V illustration and discussion

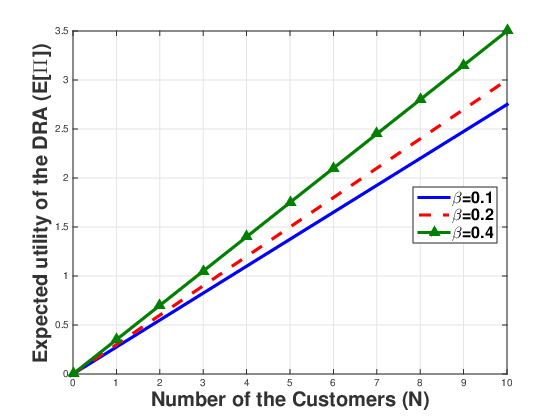

We now present some illustrative numerical examples. We first consider the unspecified load reduction scenario. We set and assume that , . Figure 2 presents the expected utility of the DRA with the optimal contract as presented in Theorem 5 for various values of as we vary the number of the customers that the DRA contracts with. As shown in this figure, for a fixed value of , the expected utility of the DRA increases linearly with the number of customers. This is intuitively specifying since as specified by Theorem 5, for a fixed , the effort invested by each customer for the optimal contract is a constant independent of or . Further, we observe that for a fixed , as increases, the expected utility of the DRA increases. In other words, for the same expected load reduction, the DRA needs to pay less to the customers. Note that satisfying the condition for precludes the choice of an arbitrarily large by the DRA.

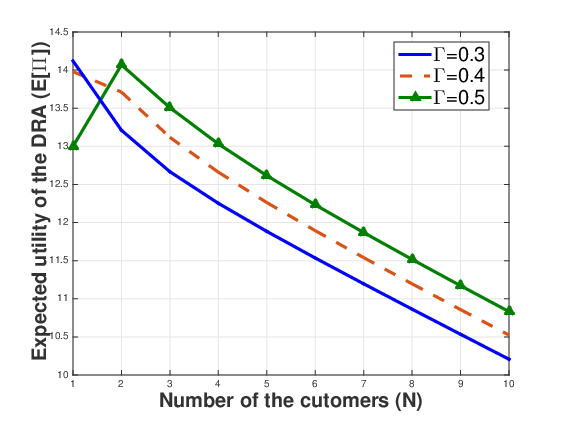

Next, we consider the specified load reduction scenario. We set . Figure 3(a) shows how the expected utility of the DRA varies as a function of the number of customers contracted by the DRA for various value of the total expected load reduction that the DRA desires. We can observe that for a small number of customers, the expected utility of the DRA is a decreasing function of while for large enough , it is an increasing function of . Intuitively, if the number of customers that the DRA has contracted with is too small, it must pay too high a compensation for realizing the desired load reduction. In fact, as the expected load reduction that it wishes increases, the expected utility of the DRA may become negative unless the number of customers is also increased. Once a sufficient number of customers have been contracted with, the total payment once again decreases with the number of customers. Once again, this does not imply that the number of customers can be increased arbitrarily given the constraints of and individual rationality for the customers. Viewed alternatively, for the same number of customers, the total expected load reduction is bounded by these constraints.

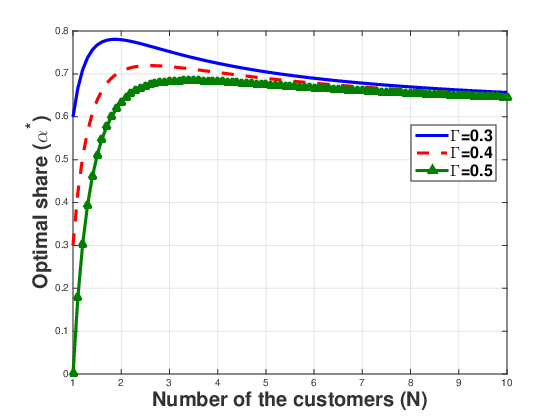

For the same setting, the optimal value of the share assigned to the customer as a function of the number of customers for various value of is illustrated in Figure 3(b). The plot indicates that the optimal value of the share assigned to the customer by the DRA is always positive as desired. Further, it is a decreasing function of the expected load reduction desired by the DRA. This plot illustrates that the constraint imposes an upper bound on the accepted value of . For a given value of , the variation of the optimal share is non-intuitive, although it should be noted that for a large enough number of customers, the share converges to the same value.

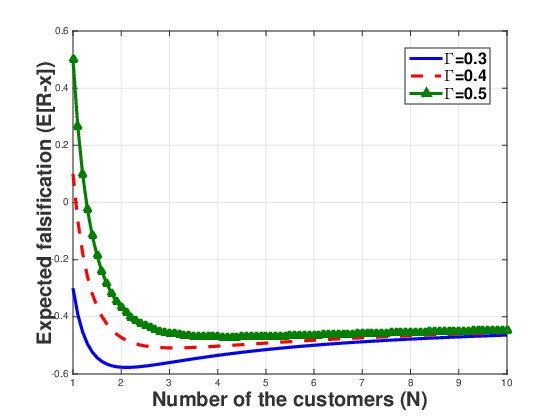

Figure 3(c) displays the expected value of the falsification by each customer as a function of the number of customers for various value of . Figure 3(c) implies that the expected value of the falsification decreases when the DRA chooses a larger ; in fact, it becomes negative for a high enough . The negative falsification is interesting since it implies that the customer under-reports her load reduction. Note that a larger value of can be interpreted as a higher expected utility of the DRA. Thus, as the expected utility of the DRA increases, the customers under-report their true load reduction since they can gain more compensation through their shares.

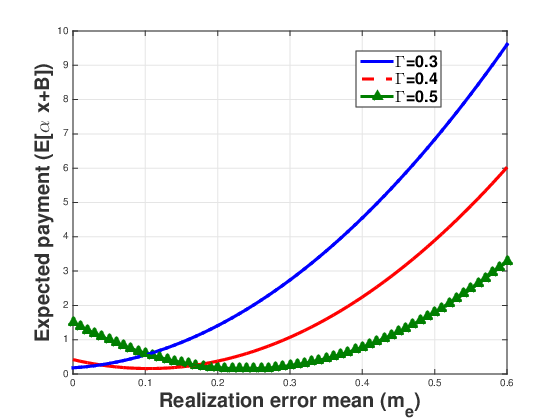

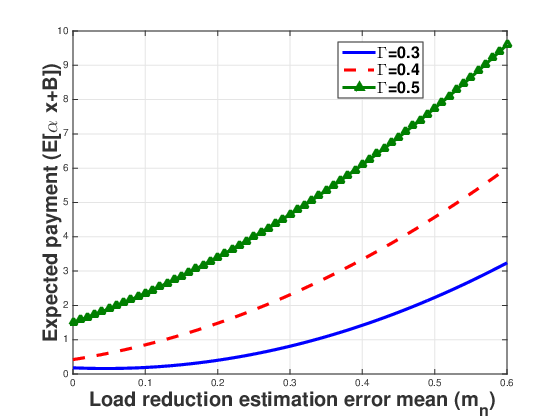

Finally, we illustrate the impact of the realization error and the estimation error . We consider a single customer and set . Figure 4(a) plots the expected payment by the DRA as a function of . As can be seen, the pattern of variation is quite complex. For a large enough , the expected load reduction by the customer is large. Thus, the payment through the shares dominates and the expected payment also increases. Figure 4(b) plots the expected payment by the DRA as a function of . The figure illustrates that as the mean of the error with which the DRA estimates the true load reduction increases, it increases the compensation it provides to the customer. In addition, as the DRA wishes to realize a larger value of , the expected value of the compensation also becomes larger. This is expected since a higher value of implies that the DRA observes a higher load reduction compared to the one realized in practice; consequently, it rewards the customer more based on its own observation.

VI Conclusion and future directions

In this paper, we designed an optimal contract between a demand response aggregator (DRA) and power grid customers for incentive-based demand response. We considered a setting in which the DRA asks the customers to reduce their electricity consumption and compensates them for this demand curtailment. However, given that the DRA must supply every customer with as much power as she desires, a strategic customer can temporarily increase her base load to report a larger reduction as part of the demand response event. The DRA wishes to incentivize the customers both to make costly effort to reduce load and to not falsify the reported load reduction. We modeled this problem as a contract design problem and presented a solution. The proposed contract consists of a part that depends on (the possibly inflated) load reduction as measured by the DRA and another that provides a share of the profit that accrues to the DRA through the demand response event to the customers. The contract design, its properties, and the interactions of the customers under the contract were discussed and illustrated.

The paper opens many directions for future work. We can consider the dynamic case when the customers need to be incentivized to participate in demand response repeatedly. Particularly interesting is the case when the customers also gain a signal about the total load reductions on a particular day and can alter their strategies accordingly. Another problem that should be considered is when the DRA is able to observe only the sum of the profit due to the effort by multiple customers and thus the payment cannot be based on individual efforts of each customer. This may lead to the problem of ‘free-riding’ in which some customers seek payment in spite of not putting in any effort, by relying on the efforts of other customers.

Appendix A

Proof of Lemma 1

Proof.

If the DRA has accurate knowledge of the true load reduction at time the utility of the DRA is given by and that of the -th customer is given by . Thus, for any effort exerted by the customer, the payment would solve the problem (notice, in particular, that the individual rationality constraints will be satisfied with this payment). Substituting this payment in the utility of the DRA, we see that the level of effort by the -th customer which maximizes the expected utility of the DRA is given by

Further, with this effort, the expected utility of the DRA is given by

where we have used Assumption 2. However, this payment can be implemented only if the DRA could observe . We show that even if is unobservable for the DRA, and it can only observe at time , it can incentivize the customer to exert the same effort and realize the maximal utility for itself. To this end, consider the payment specified by

With this payment, the expected utility of the -th customer can be written as

Given the definition of , it is easy to see that the customer chooses to maximize her expected utility. Further, the expected utility of the DRA is given by

Thus, the expected utility of the DRA is maximized with this choice of the payment. ∎

Proof of Theorem 1

Proof.

We prove by contradiction. Suppose that there exists a bonus function and an allocation which simultaneously satisfies two conditions: (i) it incentivizes each customer to choose the strategy , and (ii) it incentivizes each customer to choose .

By , the utility of the -th customer is maximized if she reports . Since the portion of payment does not depend on we can write

| (20) | ||||

| (21) |

(20) implies that

or, in turn, that

Since this equation should hold for all , we must have for some constant . In other words, the DRA provides a fixed compensation to the customer irrespective of what she reports. Further, with truthful reporting, Lemma 1 implies that the payment

| (22) |

maximizes the utility of the DRA while ensuring choice of the desired action by the customers. The fact that and that the payment is given by (22) implies that the following conditions must be met

However, this allocation violates Assumptions 4 and 5. Thus, our supposition is wrong and there does not exist a payment function that simultaneously guarantees and ∎

Proof of Theorem 2

Proof.

Proof of Theorem 3

Proof.

The effort is chosen to maximize the utility of the customer given that the optimal report is calculated as given in the equation (9). Thus,

where we have used Assumption 2. For optimality, we set

This condition yields

| (23) |

Using Theorem 2, we can write this condition as

Finally, given the concavity of in , we note that is a maximizer.

∎

Proof of Lemma 1

Proof.

(4) implies that the utility of the -th customer, , depends on the parameter through the report and the bonus . For an incentive compatible contract, the utility of the -th customer is maximized when she chooses to calculate her report (and consequently receive the bonus) based on . Envelop theorem thus implies that the optimal choice of the parameter should satisfy

| (24) |

We note that

Thus, (24) yields

To evaluate the second order condition, we start with the first order incentive compatibility condition as

and differentiate both sides with respect to to obtain

The second-order condition for the optimal choice of implies that

Thus, we can write

In particular, for the contract , it is straightforward to see that these conditions reduce to

∎

Proof of Theorem 5

Proof.

First, the optimal load reduction is specified by Theorem 2. Thus, according to (9), the optimal report is specified as

Using this report, we can calculate the optimal effort exerted by the customer using Theorem 3. Thus, from (10), we have

The optimal contract can now be specified using Theorem 4. First, (11) implies the relation

| (25) |

On the other hand, (12) implies the relation

| (26) |

From (25) and (26), we solve Finally, it is straight-forward to check that the optimal contract satisfies all the constraints in the problem. ∎

Proof of Lemma 2

Proof.

With the proposed bonus function, the utility of customer depends on the true load reduction by the other customers since is a function of , where , . Since Assumption 3 states that customer does not have access to the load savings by other customers at the time of generating the report and obtaining the consequent bonus, the contract is incentive compatible if the expected utility of customer (with expectation taken with respect to ) is maximized if the customer calculates the report based on her true load saving . Now, following the proof of Lemma 1, we can obtain that necessary and sufficient conditions for incentive compatibility as

| (27) | ||||

In particular, for the contract , it is straightforward to see that these conditions reduce to

∎

Proof of Theorem 6

Proof.

We first prove that the contract structure and the effort and the report specified in the theorem statement specifies a Nash equilibrium and then show that the equilibrium is unique and it always exists. To this end, we start by identifying the optimal report as specified by Theorem 2 with the specified bonus function and the assumption .

Proof of (17): We have

| (28) |

where we have used the fact that according to Assumption 3, is a function of only and is not a function of We take the expectation of both sides of (28) with respect to to obtain

| (29) | ||||

| (30) |

Proof of (16): The optimal choice of effort is specified by Theorem 3. With the given bonus function and the assumptions and we obtain

Using the first derivative condition to evaluate the optimal choice of we set

| (32) |

We evaluate the terms on the left hand side as follows.

| (33) | |||

| (34) | |||

| (35) |

where (33) follows from Assumption 1 and the fact that the report is not dependent on for all , (34) follows from (17) and (31), (35) follows from Assumption 2 and straight-forward algebraic manipulation. Similar manipulation yields

| (36) |

Substituting (35) and (36) in (32) and solving for yields

| (37) | ||||

| (38) |

Summing (38) times for we obtain

Substituting in (38) finally yields (16). The second derivative condition implies that is indeed a maximizer.

Proof of (15): Given (16) and Assumption 2, we have that the overall load reduction

A simple realignment yields (15).

Proof of (14): Given (15), the optimal share is specified by (8). With the specified bonus function, we have

| (39) |

From (28) and (30), we can write

| (40) |

where , , and . Substituting (40) in (39), we obtain

| (41) |

The first order derivative condition implies that is given by the equation

which yields

Proof of optimality of the contract: and have been chosen to satisfy (8) and the constraint on the total load reduction. It is easy to verify that the individual rationality and incentive compatibility constraints are met. Thus, the contract is optimal in the sense of solving Problem . That the Nash equilibrium always exists and is unique is clear from the above derivation of the contract and the optimal actions and reports.

∎

References

- [1] D. G. Dobakhshari and V. Gupta, “Optimal contract design for incentive-based demand response,” in Proceedings of the American Control Conference (ACC), 2016.

- [2] A. C. Tellidou and A. G. Bakirtzis, “Agent-based analysis of capacity withholding and tacit collusion in electricity markets,” Power Systems, IEEE Transactions on, vol. 22, no. 4, pp. 1735–1742, 2007.

- [3] J. S. Vardakas, N. Zorba, and C. V. Verikoukis, “A survey on demand response programs in smart grids: Pricing methods and optimization algorithms,” Communications Surveys & Tutorials, IEEE, vol. 17, no. 1, pp. 152–178, 2015.

- [4] R. Deng, Z. Yang, M.-Y. Chow, and J. Chen, “A survey on demand response in smart grids: Mathematical models and approaches,” IEEE Transactions on Industrial Informatics, vol. 11, no. 3, pp. 570–582, 2015.

- [5] M. H. Albadi and E. El-Saadany, “Demand response in electricity markets: An overview,” in IEEE Power Engineering Society general meeting, vol. 2007, 2007, pp. 1–5.

- [6] V. M. Balijepalli, V. Pradhan, S. Khaparde, and R. Shereef, “Review of demand response under smart grid paradigm,” in Innovative Smart Grid Technologies-India (ISGT India), 2011 IEEE PES. IEEE, 2011, pp. 236–243.

- [7] A.-H. Mohsenian-Rad, V. W. Wong, J. Jatskevich, and R. Schober, “Optimal and autonomous incentive-based energy consumption scheduling algorithm for smart grid,” in Innovative Smart Grid Technologies (ISGT), 2010. IEEE, 2010, pp. 1–6.

- [8] P. Samadi, A.-H. Mohsenian-Rad, R. Schober, V. W. Wong, and J. Jatskevich, “Optimal real-time pricing algorithm based on utility maximization for smart grid,” in Smart Grid Communications (SmartGridComm), 2010 First IEEE International Conference on. IEEE, 2010, pp. 415–420.

- [9] A. J. Roscoe and G. Ault, “Supporting high penetrations of renewable generation via implementation of real-time electricity pricing and demand response,” IET Renewable Power Generation, vol. 4, no. 4, pp. 369–382, 2010.

- [10] Q. Wang, M. Liu, and R. Jain, “Dynamic pricing of power in smart-grid networks,” in Decision and Control (CDC), 2012 IEEE 51st Annual Conference on. IEEE, 2012, pp. 1099–1104.

- [11] J.-J. Laffont and D. Martimort, The theory of incentives: the principal-agent model. Princeton university press, 2009.

- [12] B. Hölmstrom, “Moral hazard and observability,” The Bell journal of economics, pp. 74–91, 1979.

- [13] H.-p. Chao, “Price-responsive demand management for a smart grid world,” The Electricity Journal, vol. 23, no. 1, pp. 7–20, 2010.

- [14] H.-p. Chao and M. DePillis, “Incentive effects of paying demand response in wholesale electricity markets,” Journal of Regulatory Economics, vol. 43, no. 3, pp. 265–283, 2013.

- [15] F. A. Wolak, “Residential customer response to real-time pricing: The Anaheim critical peak pricing experiment,” Center for the Study of Energy Markets, 2007.

- [16] J. Pierobon, Two FERC settlements illustrate attempts to ‘game’ demand response programs, 2013, http://www.theenergyfix.com/2013/07/25/two-ferc-settlements-illustrate-attempts-to-game-demand-response-programs/.

- [17] J. Bushnell, S. M. Harvey, B. F. Hobbs, and S. Stoft, “Final opinion on economic issues raised by FERC order 745, “Demand response compensation in organized wholesale energy markets”,” June 2011, available at http://www.caiso.com/2b97/2b97a0bb6ef70.pdf.

- [18] W. Saad, Z. Han, H. V. Poor, and T. Basar, “Game-theoretic methods for the smart grid: An overview of microgrid systems, demand-side management, and smart grid communications,” IEEE Signal Processing Magazine, vol. 29, no. 5, pp. 86–105, 2012.

- [19] Z. M. Fadlullah, Y. Nozaki, A. Takeuchi, and N. Kato, “A survey of game theoretic approaches in smart grid,” in Wireless Communications and Signal Processing (WCSP), 2011 International Conference on. IEEE, 2011, pp. 1–4.

- [20] D. T. Nguyen, M. Negnevitsky, and M. de Groot, “Market-based demand response scheduling in a deregulated environment,” IEEE Transactions on Smart Grid, vol. 4, no. 4, pp. 1948–1956, 2013.

- [21] Y. Chen, W. S. Lin, F. Han, Y.-H. Yang, Z. Safar, and K. R. Liu, “A cheat-proof game theoretic demand response scheme for smart grids,” in 2012 IEEE International Conference on Communications (ICC). IEEE, 2012, pp. 3362–3366.

- [22] D. Prabhakar, D. Kalathil, K. Poolla, and P. Varaiya, “Mechanism design for self-reporting baselines in demand response,” in Proceedings of the American Control Conference, 2016.

- [23] A. Mas-Colell, M. D. Whinston, J. R. Green et al., Microeconomic theory. Oxford university press New York, 1995, vol. 1.

- [24] K. J. Crocker and T. Gresik, “Optimal compensation with earnings manipulation: Managerial ownership and retention,” mimeo, Tech. Rep., 2010.

- [25] K. J. Crocker and J. Slemrod, “The economics of earnings manipulation and managerial compensation,” The RAND Journal of Economics, vol. 38, no. 3, pp. 698–713, 2007.

- [26] R. B. Myerson, “Incentive compatibility and the bargaining problem,” Econometrica: Journal of the Econometric Society, pp. 61–73, 1979.

- [27] R. Amir, “Cournot oligopoly and the theory of supermodular games,” Games and Economic Behavior, vol. 15, no. 2, pp. 132–148, 1996.

| Donya Ghavidel-Dobhakhshari received her B.S. degree in Electrical Engineering at Iran University of Science and Technology, Tehran, Iran, 2014, and her M.S. degree in Electrical Engineering from the University of Notre Dame, Notre Dame, IN, USA, in 2016, where she is currently pursuing the Ph.D. degree in Electrical Engineering. Her research interests lie in game theory, mechanism design, and their applications to power systems and networks. |

| Vijay Gupta Vijay Gupta is a Professor in the Department of Electrical Engineering at the University of Notre Dame, having joined the faculty in January 2008. He received his B. Tech degree at Indian Institute of Technology, Delhi, and his M.S. and Ph.D. at California Institute of Technology, all in Electrical Engineering. Prior to joining Notre Dame, he also served as a research associate in the Institute for Systems Research at the University of Maryland, College Park. He received the 2013 Donald P. Eckman Award from the American Automatic Control Council and a 2009 National Science Foundation (NSF) CAREER Award. His research and teaching interests are broadly at the interface of communication, control, distributed computation, and human decision making. |