On structure, family and parameter estimation of hierarchical Archimedean copulas∗111∗This work has been submitted to Journal of Statistical Computation and Simulation.

Abstract

Research on structure determination and parameter estimation of hierarchical Archimedean copulas (HACs) has so far mostly focused on the case in which all appearing Archimedean copulas belong to the same Archimedean family. The present work addresses this issue and proposes a new approach for estimating HACs that involve different Archimedean families. It is based on employing goodness-of-fit test statistics directly into HAC estimation. The approach is summarized in a simple algorithm, its theoretical justification is given and its applicability is illustrated by several experiments, which include estimation of HACs involving up to five different Archimedean families.

keywords:

hierarchical Archimedean copula; copula estimation; structure determination; goodness-of-fit1 Introduction

Copulas, i.e., multivariate distribution functions with standard uniform univariate margins, establish a connection between general joint distribution functions (d.f.s) and their univariate margins through Sklar’s Theorem; see [1]. A popular class of copulas are Archimedean copulas (ACs) [2, p. 109] or their asymmetric generalization, hierarchical Archimedean copulas (HACs); note that HACs are also called nested Archimedean copulas, see, e.g., [3, p. 87]. For a motivation addressing the advantages of hierarchical over exchangeable Archimedean copulas in applications, see, e.g., [4]. HACs are popular due to their flexibility but conveniently limited number of parameters. Fast sampling methods have already been proposed for them, see, e.g., [5, 6], whereas efficient methods for their estimation are still a matter of research, see, e.g., [7, 8, 9, 10], which concern both structure determination and parameter estimation of HACs. This research is largely restricted to the most commonly used HACs that are constructed by nesting of a single one-parametric family of Archimedean copulas. In what follows, we call a HAC consisting of ACs of the same family a homogeneous HAC, otherwise, a heterogeneous HAC. Although the above-mentioned papers briefly mention the possibility of heterogeneous HACs estimation, they are focused mainly on the case of homogeneous HACs and all reported experiments involve only homogeneous HACs. From this point of view, estimation of heterogeneous HACs is still an open task and our work is an attempt that addresses this challenging case in detail. Note that the generalization of homogeneous HACs to heterogeneous HACs brings several advantages, such as the possibility of having bivariate margins from different Archimedean copula families rather than only having different parameters but belonging to the same parametric Archimedean family. This is of interest when modeling pairwise tail dependence, see [11], but also when Archimedean families are restricted in their range concerning concordance (e.g., the family of Ali-Mikhail-Haq only allows for Kendall’s tau in ).

In this work, we propose a new approach to estimating heterogeneous HACs, which is based on extending a homogeneous HAC estimation approach by involving goodness-of-fit test statistics directly into the estimation. Whereas such an extension is rather simple and straightforward, assuring that a resulting estimate satisfies the sufficient nesting condition, which guarantees that a proper copula results, is a substantially more complex problem compared to its counterpart for the homogeneous case. However, we provide an algorithm in pseudo-code and its theoretical justification represented by Theorem 6.8, which shows that under weak conditions, the algorithm returns a function satisfying the sufficient nesting condition. Those weak conditions are additionally addressed by Theorems 6.10 and 6.13, which explicitly present two general scenarios under which the algorithm guarantees to satisfy the sufficient nesting condition. We also show that the proposed extension to the heterogeneous case is not restricted to a specific homogenous HAC estimation approach and by application to another homogeneous estimator, we can easily construct an alternative heterogeneous HAC estimator, i.e., we actually introduce a whole new framework of HAC estimators.

Complementary to this theoretical part, the validity of the proposed approach is illustrated by experiments on simulated data which involve heterogeneous HAC models with up to five different parametric families of Archimedean generators. The results of these experiments confirm that the proposed approach is able to properly determine the structure and estimate the parameters of a HAC, as well as properly estimating different parametric families of Archimedean generators of a heterogeneous HAC.

Moreover, this work also contributes to the topic that is frequently called collapsing of HAC structures, which, informally speaking, serves to turning binary HAC structures (binary trees), which often result from estimation processes, to non-binary ones, allowing to access all possible HAC structures. Our contribution it to introduce a novel approach, which, by contrast to the collapsing approaches proposed, e.g., in [7, 12], does not force the user to specify any threshold before a collapsing process begins and lets one to choose an appropriate collapsed HAC after the collapsing process has been finished. Complementary to this approach, an automated heuristic procedure for choosing an appropriate collapsed HAC is proposed, which is again not dependent on any pre-defined threshold. Also, a new re-estimation procedure for re-estimating the parameters of a collapsed HAC is introduced and compared to the approach proposed in [12]. All these contributions are then intensively tested and the obtained results are reported in the experimental part of this work.

This work also addresses a close relationship between an existing HAC structure estimator and the sufficient nesting condition. We show that this structure estimator inherently assures the latter condition, and that such a property is unique among existing structure estimators. This finding is also theoretically justified by Theorem 6.3, which shows that by using the considered structure estimator, a proper homogeneous HAC can be obtained under relatively weak conditions.

As a by-product, two existing approaches for homogeneous HAC estimation are experimentally compared, showing not only their precision in structure and parameter estimation, but also their robustness against misspecification of the underlying families.

This work is structured as follows. Sections 2 and 3 recall the necessary theoretical concepts concerning ACs and HACs, respectively. An AC estimator based on the inversion of Kendall’s tau is recalled in Section 4, and an aggregated goodness-of-fit test statistic is introduced in Section 5. Section 6 represents the theoretical part of this work. In Section 6.1, the new approach to collapsing is addressed, in Section 6.2, the relationship between the existing structure estimator and the sufficient nesting condition is addressed, in Section 6.3, an existing approach to homogeneous HAC estimation is recalled and the findings from Section 6.2 are applied to this estimator, which results in Theorem 6.3. Finally, in Section 6.4, our new approach to heterogeneous HAC estimation is introduced. The proofs of all theorems and lemmas are presented in Appendix. Section 7 describes the design and the results of the performed experiments and Section 8 concludes. Note that a part of the experimental results is included in an attachment.

2 Archimedean Copulas

To construct ACs in arbitrary dimensions, we need the notion of an Archimedean generator and of complete monotonicity.

Definition 2.1.

An Archimedean generator (shortly, generator) is a continuous, non-increasing function , which satisfies and which is strictly decreasing on . We denote the set of all generators by . If satisfies for all , is called completely monotonic (c.m.). Note that denotes the -th derivative of . Finally, we denote the set of all c.m. generators by .

Definition 2.2.

Any -dimensional copula (simply -copula) is an Archimedean copula based on a generator (we denote it -AC), if it admits the form

| (1) |

where is defined by .

Note that if is strictly decreasing, is the ordinary inverse.

Remark 1.

As can be seen from from their definition, ACs are invariant to permutation of their arguments, e.g., for any 2-AC , for all .

A condition sufficient for (1) to be a proper copula in arbitrary dimensions is stated in the following theorem.

Note that in [13], given , the authors present a condition that is both necessary and sufficient for to be a -copula. In this work, we will however build HACs only from ACs based on completely monotonic generators. The reason for it, which is connected to a sufficient condition assuring that a HAC-like function is a proper copula, is addressed in detail in Section 3.

Assuming complete monotonicity of generators implies that ACs are restricted to be models for positively dependent random vectors only, in other words, the pairwise rank correlations of such ACs are non-negative. This follows from the fact that if a generator is c.m., then, according to [14, p. 167], is logarithmically convex. Thus is concave. Defining and considering that is the independence copula, it follows from Theorem 2.3.1 in [15] that is subadditive, which in turn implies that for all , and thus that pairwise rank correlations are non-negative; see Remark 2.3.2 in [15].

In practice, one often works with families of generators (families of ACs). E.g., in [2, p. 116], the reader can find 22 c.m. families parametrized by a real parameter. Generally, a one-parametric family of generators can be represented by a bivariate function such that for all the function is the generator from the considered family with the parameter . This idea is formalized in the following definition.

Definition 2.4.

Let . If is such that

| (2) |

then is called parametric family of Archimedean generators, and is called its parameter range. In order to formalize the relationship describing whether or not a given generator is from a given parametric family, we define a relationship (denoted ) between a generator and a parametric family of Archimedean generators given by

| (3) |

Note that is a bivariate function, hence the term cannot be used.

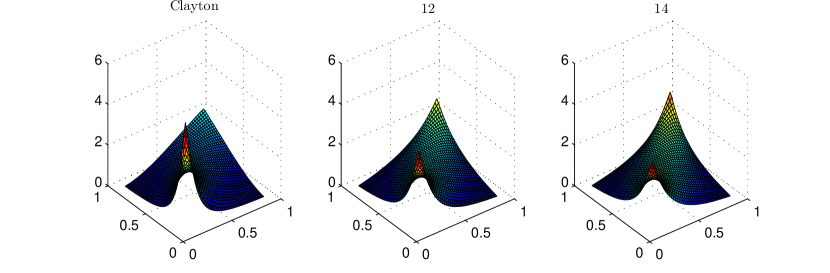

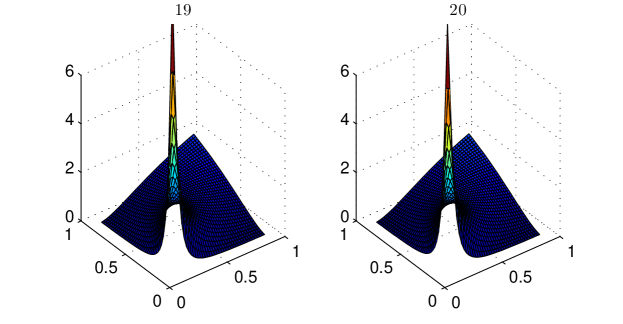

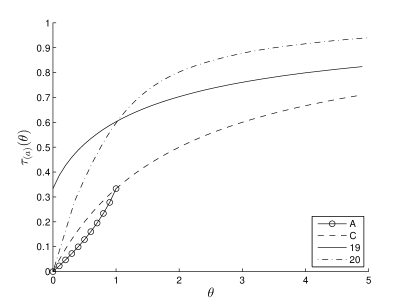

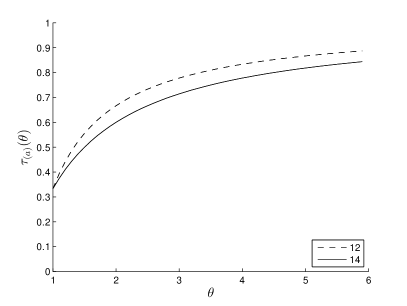

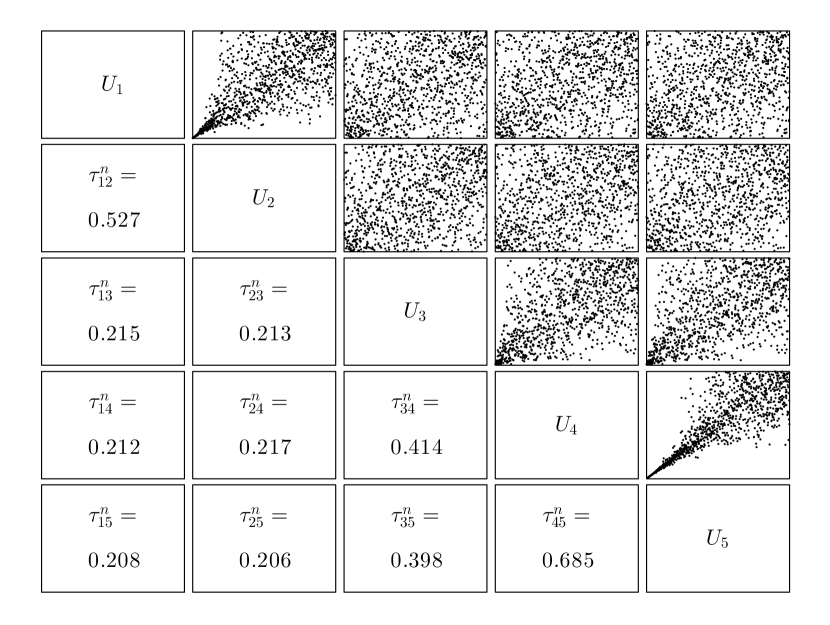

As we will work with several parametric families of Archimedean generators at the same time, we denote each of these families by , where is a unique label (that will be called family label) corresponding to the parametric family of Archimedean generators . Completely monotonic parametric families of Archimedean generators (shortly, families) we use in our work include Ali-Mikhail-Haq ( A) and Clayton ( C); see Table 1. In connection with this fact, we denote {A, C, 12, 14, 19, 20}, where the numbers corresponds to the numbers of AC families presented in [2, p. 116]. The density functions of ACs {A, C, 20} such that Kendall’s tau equals 0.25 are depicted in Figure 1, and the density functions for {C, 12, 14, 19 20} such that Kendall’s tau equals 0.5 are depicted in Figure 2. These density functions illustrate that such ACs differ particularly in the tails. Note that dependence models which can capture tail dependence are of interest particularly in finance, see, e.g., [16].

Remark 2.

If , then is uniquely given by the pair of the label and the parameter , hence, we denote the generator by .

As we work with c.m. generators only, the parameter ranges in Table 1 are hence restricted to the values for which the corresponding ACs are models for a positively dependent random vector. This means that, e.g., for a Clayton generator with , although the function is a copula for , we do not consider such a generator in this work, which is described later in Section 3. Note that this restriction can often be (but not always) solved by appropriately transforming selected input variables (through sign changes, for example) and using the fact that, if and are continuous random variables and denotes the value of Kendall’s tau for the random vector , then . For more details on this approach allowing to model negatively dependent random vectors by HACs based on c.m. generators, see, e.g., the inverting procedure described in Algorithm 4 in [10].

| A | [0, 1) | 0 | 0 | ||

|---|---|---|---|---|---|

| C | 0 | ||||

| 12 | |||||

| 14 | unknown | ||||

| 19 | 1 | 0 | |||

| 20 | 1 | 0 |

3 Hierarchical Archimedean Copulas

A -copula is called hierarchical Archimedean (HAC) if it is an AC with arguments possibly replaced by other HACs [5]; also, see, e.g., [6, 7, 10]. In the last two articles, which address homogenous HAC estimation, the authors use, apart from the HAC definition, various auxiliary concepts addressing necessary properties of HAC structures, e.g., the HAC structures representation through sequences of reordered indices grouped through parentheses. In this work, we extend those articles to heterogeneous HACs. This inevitably involves more notation and we consider introducing it directly in the HAC definition more transparent than introducing it as auxiliary concepts later. Hence, we propose a definition of HACs, which is a slight modification of the one originally proposed in [17], and we explicitly refer to the tree structure through concepts from graph theory. This is mainly motivated by the fact that these concepts will be needed both in the construction of the algorithm for heterogeneous HACs estimation presented in Section 6 and in its theoretical justification represented by Theorem 6.8.

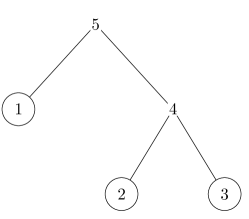

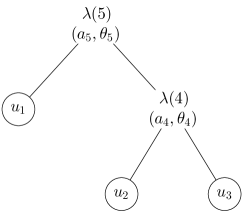

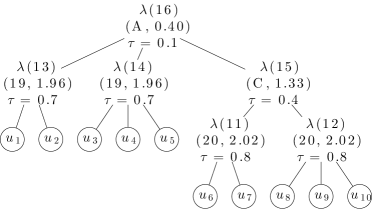

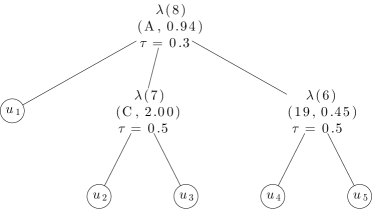

In order to get familiar with this alternative HAC definition, we first illustrate it in an example. Consider a HAC for two generators ; its tree structure is depicted in Figure 3.

In the language of graph theory, an undirected tree is a pair , where is a set of nodes and is a set of pairs of different nodes from . For the representation depicted in Figure 3, we can derive a tree with the same structure such as the one depicted in Figure 3 just by assigning different numbers to all of its nodes. For this tree, we have and . As we can observe, not all nodes correspond to the same objects. More precisely, the leaves correspond to the variables, whereas the non-leaf nodes (we will call them forks) correspond to the ACs (uniquely determined by the corresponding generators) nested in . As each fork corresponds to a generator, we represent this relationship using a labeling denoted , which maps the forks to corresponding generators. In our example, it would be and . Using this notation, turns into and into .

Finally, having the structure and the involved generators encoded in and , respectively, we can for a given , explicitly express the value , which we assign to the node 5 using the values assigned to its children. These values are defined by for for the variables, and, for the generators (or forks), going from the bottom to the top of the structure, and . Clearly, . Now consider that are the children of the node 4 and are the children of the node 5. Using this notation, the (inner) copula values, and are glued together through and , where . For clarity, also note that, e.g., node 2 (or node 3) is not a child of the node 5.

Definition 3.1.

Let be a labeled tree with nodes , edges and rooted in the node . Let the nodes be the leaves of and the nodes , which will be called forks, have at least two children each. In connection with , the following notation will be used:

-

•

For , denote by the set of children of ; thus the cardinality of fulfills for , i.e., being a fork, and for , i.e., for being a leaf.

-

•

For and , the simplified notation

(4) will be used with a further simplification for .

Finally, let be a labeling of forks with c.m. Archimedean generators such that for each , there exists with the following two properties:

-

(i)

;

-

(ii)

.

Then:

-

a)

if the function , defined

(5) is a -copula, it is called hierarchical Archimedean -copula (-HAC) with the (tree) structure and the labeling ;

-

b)

if is binary, then is called binary;

-

c)

given a finite set of family labels such that is a parametric family of Archimedean generators for all , if fulfill

(6) then is called parametric;

-

d)

given that is parametric, if fulfill

(7) then is called -homogeneous, otherwise, is called -heterogeneous.

Remark 3.

1) If is a binary -HAC then the number of forks in the structure (denoted by in Definition 3.1) is . 2) An -parametric is a HAC with generators from the families in . A heterogeneous HAC involves generators from different families, whereas a homogenous HAC from a single family. 3) The vector variable is used only for clarity and notational convenience and is not used in the algorithms below.

Remark 4.

In the rest of our work, especially in Section 6.4.2, given a set and an -parametric function , we use the convention that , where , unless stated otherwise.

If a function is -parametric, we use a graphical representation following from Remark 4 that uniquely determines it. Given two family labels , an example of a -heterogeneous trivariate function is depicted in Figure 3. Clearly, its structure is the one depicted in Figure 3, and the convention stated in Remark 4, i.e., and , is used.

As in the case of ACs, we can ask for necessary and sufficient conditions for the function given by (5) to be a proper copula. As has already been mentioned before, such a condition is not known. However, several sufficient conditions are known. An early one has been proposed in [18], see Theorem 4.4 therein, which is proven for a subclass of HACs called fully nested Archimedean copulas. Its generalization to all HACs, which has been proposed in [19], is recalled in the following theorem.

Theorem 3.2.

Another, weaker sufficient condition has appeared recently in [20]. In this condition, neither nor nor are required to be c.m., but it is sufficient that these three functions are -monotone or ‘less than’ -monotone, where , see [20] for details. Relaxing the requirement of the complete monotonicity allows to construct more HACs then under (9), e.g., [20] provides 151 new 5-HACs in Example 2.4. However, even if the article addresses parametric families of generators in that example, no simplification of the proposed condition in terms of the parameters of the generators similar to, e.g., the fourth column in Table 2, is provided. Without it, -monotonicity has to be directly checked for each pair of parent-child generators, which makes the estimation process at least challenging, especially in high dimensions and under consideration that the condition, by contrary to the complete monotonicity, depends on . Also, no efficient sampling strategies, similar to the ones proposed, e.g., in [5, 6], are known. Without these tools at hand, performing estimation experiments seems to be at least an intricate task. Due to these reasons, we restrict to HACs satisfying the condition (9), which will be called the sufficient nesting condition (s.n.c.).

Observing the s.n.c.s in Table 1, we can see that, for an -homogeneous function , (9) simplifies to

| (10) |

for all . Assuming an -heterogeneous , where , such a simplification of (9) is not possible as the s.n.c.s vary depending on the family combination of a particular pair , which can be seen from the last column in Table 2.

| (A, C) | |||

|---|---|---|---|

| (A, 19) | any | ||

| (A, 20) | |||

| (C, 12) | |||

| (C, 14) | |||

| (C, 19) | |||

| (C, 20) |

Table 2 lists all family combinations of the completely monotone generators of [2, pp. 116–119], which result in proper HACs according to the s.n.c., see [21] or Theorem 4.3.2 in [15] for more details; see also Sections 4.2.3 and 4.3 in [15], which show how so-called general nesting transformations of generators can be used for constructing such family combinations. Hence, we will consider the following family combinations

| (A, A), (C, C), (12, 12), (19, 19), (20, 20), | ||||

| (11) |

Finally, note that all generators compatible with a given generator can be constructed and characterized as in [22].

4 An Archimedean copula estimator based on inversion of Kendall’s tau

Assume i.i.d. random vectors , distributed according to a joint distribution function with continuous margins , and the copula . Now consider that, as is a random sample from , where , one can base estimation of directly on , if the margins are known. In practice, the margins are typically unknown and must be estimated parametrically or non-parametrically. In the following, we will work under unknown margins and thus we consider the pseudo-observations

| (12) |

where denotes the empirical distribution function corresponding to the th margin and denotes the rank of among .

In the following, we refer to

| (13) |

as to the population version of Kendall’s tau. If is a 2-AC and is a twice continuously differentiable generator with for all , Kendall’s tau can be represented as [3, p. 91], [2, p. 163]

| (14) |

For a generator from a family , (14) states a functional relationship between and (denoted by ), which involves at most a one-dimensional integration, e.g., for {19, 20}, or even no integration, e.g., is in a closed form for {A, C, 12, 14}, see Table 3 (the relationship between and for other generators can be found, e.g., in [15]).

| A | |||

|---|---|---|---|

| C | |||

| 12 | |||

| 14 | |||

| 19 | |||

| 20 |

Note that the forms of the functions presented in Table 3 are taken from [15, p. 65] for all considered families except for the family 20, which is introduced here. The graphs of for are depicted in Figure 4.

In connection to (14), using Remark 2.3.2 in [15] and its generalization given by Proposition 2 in [10], it follows that if the function given by (5) satisfies (9), then

| (15) |

where for all . This condition is clearly not equivalent to the s.n.c., e.g., considering the function in Figure 3 with = (A, 0.25) and = (C, 0.5), it satisfies (15) as and but violates (9), see Table 2. However, assuming a homogenous HAC from a family such that the s.n.c. is in the form , see Table 1, (15) combined with relatively weak assumptions turns to the s.n.c., as is shown in the following lemma.

Lemma 4.1.

Let be a tree with leaves and forks, and be a family with the parameter range such that 1) for all , 2) is strictly increasing on , and 3) is equivalent to for all . If

| (16) |

then let be an -homogeneous function given by (5) with the labeling defined for all , and then it holds that (15) implies (10).

The three assumption on in Lemma 4.1 holds for all , see Table 1, but also for many other families, e.g., for the three popular families of Frank, Gumbel and Joe copulas, see Table 2.3 in [15]. With this lemma at hand, one can aim, in homogenous HAC estimation, to assure (15) instead of (10), which is one of the key ideas we use in our approach to homogenous HAC estimation addressed in Section 6.3. Also, assuming a heterogeneous HAC, note that satisfying (15) does not impose, by contrary to (9) (see Tables 1 and 2), any assumptions on the underlying families of the generators but just requires a particular ordering of the strength of the dependence of the generators in the structure. Hence, even if there are not known any additional conditions (like in the homogeneous case) that would turn it into the s.n.c., one can find its particular use also in heterogeneous estimation, as we show in Section 6.4.

As noted in Section 1, some of the considered families cannot model dependencies for all , e.g., for all {A, 12, 14, 19}. This fact illustrated by Figure 4 explicitly addresses the fourth column in Table 3, which shows the ranges of for . It also clarifies the selection of the families in Figures 1 and 2.

If it exists, the inversion of establishes a method-of-moments-like estimator of the parameter given by , based on the sample version of Kendall’s tau

| (17) |

see [23]. Note that we use the notation for notational convenience related to the sample version of Kendall correlation matrix defined in Section 6.1. If has no solution, this estimation method does not lead to an estimator. Unless there is an explicit form for , is computed by numerical root finding [4].

In [4], a comparison of 10 estimators for ACs in precision of estimation of the parameter is provided, which includes Kendall’s tau, Blomqvist’s beta, minimum distance estimators, the maximum-likelihood estimator, a simulated maximum-likelihood estimator, and a maximum-likelihood estimator based on the copula diagonal. There, e.g., in Figure 4, one can observe that the Kendall’s tau-based estimator recalled above (there denoted by ) together with the ML estimator perform well when compared with the remaining estimators. For this reason, these two estimators are considered in this work. Also, in [12], an HAC estimator based on Hoeffding’s is investigated, however, this estimator was clearly outperformed by its analogous based on Kendall’s tau in the ability to estimate the structure of the true copula. Finally, note that for Spearman’s rho, there is no explicit formula analogous to (14) known for ACs [15, p. 62], which makes its application in our context at least challenging.

5 An aggregated goodness-of-fit test statistic

Once we have the parameters estimated, we can ask how well our estimated model fits the data, that is, we can conduct a goodness-of-fit test (GoF test). In this work, we use three GoF tests based on statistics similar to Cramér-von Mises statistics [24]. These are the statistics from [25] denoted by or . In this work, we denote the (empirical copula based) statistic by and the (Rosenblatt’s transformation based) statistic by . Given pseudo-observations (12) and a -copula estimate with parameter(s) , they are given

| (18) |

where is the empirical copula and ,

| (19) |

where , and denotes the distribution function of , and

| (20) |

where , is the -variate independence copula and , where is the Rosenblatt’s transform based .

A large value of such statistics leads to the rejection of , where and is an open subset of . Thus for measuring the fitting quality of copula models, we can, informally, evaluate copula models with lower value of such statistics as ‘better’. All these three test statistics performed well in a large scale simulation study conducted at [25] in the bivariate case. We thus choose them as candidates for our purpose of goodness-of-fit evaluation.

We now introduce an g-aggregated statistic. Note that a slightly different version of this statistic has originally appeared in [10]. We later use such generalized statistics in Section 6.4. The one that follows is used directly in the HAC estimation process, where it is applied at each stage for evaluating which generator from some considered families fits the data best. In contrast, the one proposed in [10] is used for evaluating the fit of a whole HAC estimate after its estimation is done, i.e., the evaluations computed for all generators involved in that HAC are gatherer and aggregated using a -aggregation function, which is defined as follows.

Definition 5.1.

Let either , where and , or . Any function , satisfying 1) for all and 2) is exchangeable (i.e., for all and all permutations of ) is called an -aggregation function.

Examples of, e.g., -aggregation functions are the functions maximum, minimum or average restricted to . Note that this type of aggregation functions is used in Algorithm 3 for the input .

Definition 5.2.

Let , where (a column vector) for all . Also, let be an -aggregation function and be the statistic corresponding to a GoF test, e.g., or , for a 2-AC and a pair . A g-aggregated statistics is defined

| (26) |

where are non-empty disjoint subsets of .

Since the choice of substantially affects results of Algorithm 3 and in turn the results of all experiments reported in Section 7, we now discuss the idea behind this concept in more detail. Given a binary -HAC , let . According to Proposition 3 in [10], it follows that, given leaves , the bivariate margin is distributed according to the 2-AC , where and is the youngest common ancestor (see Definition 9 in [10]) of the leaves and . E.g., for the 3-HAC depicted in Figure 3, since the node 5 is the youngest common ancestor of the pairs (1, 2) and (1, 3), it follows that and . Similarly, as the node 4 is the youngest common ancestor of the pair (2, 3), . Now, assume that we are estimating the generator . Assuming a given family to consider for , we can use some homogeneous HAC estimator, e.g., the one proposed in [10] (and here recalled in Algorithm 2), which provides us with an estimate of its parameter. If we consider heterogeneous HACs and thus can be a member of one of more than one families, we can repeat the homogeneous HAC process for each of the possible families, which results in obtaining a corresponding number of generator estimates from these families. E.g., assume two possible families and , which would result in two parameter estimates and in turn in two generator estimates, denoted by , . To decide which of these two estimates are more appropriate for modeling , we can, e.g., evaluate how well a generator estimate fits the data. For this purpose, we suggest to use the aggregated statistic for this purpose. E.g., assume that and , i.e., . As we know, both and are distributed according to . Thus it is reasonable to evaluate an estimate of on the data that correspond to these two bivariate margins, i.e., on the two pairs of data columns and (note that we use the same idea also for the parameter estimation in Algorithms 2 and 3). This can be done by setting and . Hence, for , we evaluate , i.e., a rank-based Cramér-von Mises statistic is computed for the two bivariate margins and the maximum is returned. Similarly for . As measures a certain type of a distance between the empirical copula corresponding to considered data and a 2-copula model (e.g., ), we choose the estimate with the lower value of the aggregated statistic.

6 Estimation of hierarchical Archimedean copulas

In this section, we propose a new approach to HACs estimation that allows to estimate both homogeneous and heterogeneous HACs. This approach is a generalization of the approach to homogeneous HACs estimation proposed in [10], which was experimentally compared with other state-of-the-art approaches to HACs estimation. This comparison shows that it outperforms the other approaches in terms of the ability to determine the true structure, goodness-of-fit and run-time [10]. In Section 6.3, we first introduce its new version, where one superfluous step from the original version is removed, which can be done due to the findings summarized by Theorem 6.3. Then, we use it as a basis for the generalization to heterogeneous HACs proposed in Section 6.4.

Concerning only the structure estimation, a recent performance study comparing 11 available HAC structure estimators has been reported in [12]. There, the estimator named kt_kagg has shown the best performance in the ability to determine the true structure, as well as the lowest computation times. This estimator merges the estimation approach proposed in [10] with the idea for collapsing tree structures proposed in [7]. Due to this, the estimation process of kt_kagg is divided in two steps. In the first step, a binary tree is obtained using hierarchical agglomerative clustering. In the second step, it is collapsed if necessary, according to some strategy, see Algorithm 1 in [12]. In this work, we also use such a two-step approach. First, we obtain a binary HAC using Algorithm 2 or 3, and then, we use a collapsing strategy inspired in the strategy proposed in [12], which however differs in several of its aspects. This is discussed in Section 6.1.

As our definition of HACs explicitly employs a tree structure , we can directly adopt some necessary concepts from graph theory and denote, for a node , by its parent and by the set of all its ancestor forks. For a fork , denote by the set of all its descendant forks and by the set of all its descendant leafs. For a leaf , define . E.g., given the 3-HAC depicted in Figure 3, , . Also, , and .

6.1 Collapsing a binary structure to a non-binary one

Briefly, all the collapsing strategies proposed in [12] involve a process in which all parent-child pairs of forks that are close enough according to some parent-child distance are found, and each is collapsed into one fork. After a pair is collapsed into a fork, the parameter corresponding to this fork is re-estimated. Due to that, there might appear new parent-child pairs to collapse and thus the process repeats until there is nothing left to collapse. Concerning , the estimator kt_kagg employs a distance given by , where and are the Kendall’s tau corresponding to the generators to collapse. The condition for a threshold then determines whether these two nodes are close enough. However, no suggestions of how to set are provided in [12], which may make such an approach difficult to apply.

To overcome this drawback, we introduce a different approach inspired by the pruning of decision trees proposed in [26], in which we look for and collapse only one parent-child pair corresponding to the minimum according to (below, we refer to this minimum as to the minimal distance), and repeat this process until there is nothing left to collapse, i.e., until a one-node structure is obtained. Note that if the families in a collapsing parent-child pair are different, we assign to the collapsed fork the family of the collapsing parent fork, which we do in an effort to satisfy the s.n.c. Once the collapsing process is finished, we obtain a set of structures with decreasing number of nodes, from which the user can choose, similarly to [26], the most suitable structure according to his/her needs, e.g., according to goodness-of-fit or complexity of the model. This implies that the user is indeed not forced to specify any threshold before performing the collapsing step.

However, in some cases, e.g., if one works with a lot of HAC estimates (see our Section 7), some automatized procedure that estimates the number of forks in an underlying non-binary HAC (which in turn determines which one to choose from the set of structures obtained in the collapsing step) would be desirable. For this purpose, we introduce a procedure based on a simple heuristic, which estimates the number of forks using the minimal distances generated during the collapsing process. Let and be a binary -HAC, i.e., has forks. Let . Collapse to using the approach described in the previous paragraph, i.e., has forks, and store the minimal distance from from in . Repeating this process until we get a -AC , we obtain the series , which we use for the estimation of the number of forks in the true copula. To get this estimate, we simply find the lowest from such that . Note that such an alway exists, which follows from the consideration that some of the steps have to be larger than or equal to the average step . Then is considered to be the estimate of the true copula and thus the estimate of the number of forks in the true copula.

It follows from the construction of the procedure that , i.e., the procedure does not allow for collapsing an HAC into an AC. We thus suggest to always consider and also , where might be preferred if the difference between the lowest and the highest of the forks in is very ‘low’, where ‘low’ has to be determined by the user based on a particular data. Together with these two copulas, we also suggest to consider another one, namely . This follows from our observation that if the true copula is binary, the suggested procedure frequently misses to estimate . Here, might be preferred if the lowest difference between the of a parent and a child in is very ‘large’, where, again, ‘large’ has to be determined by the user based on a particular data. One should thus always consider and these two extremes. However, note that such a consideration can always be done after a collapsing process has been finished, i.e., after some insights to the data have been gained by the user, on the contrary to the procedures suggested in [7, 12].

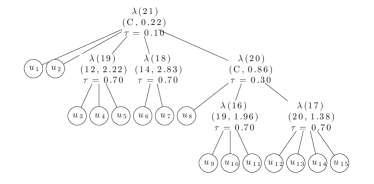

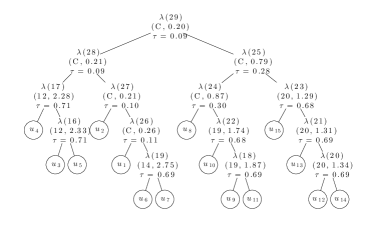

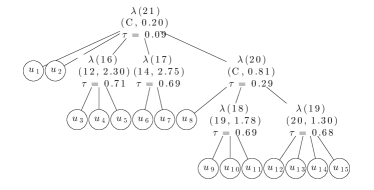

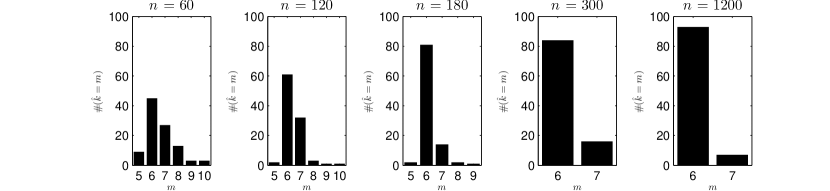

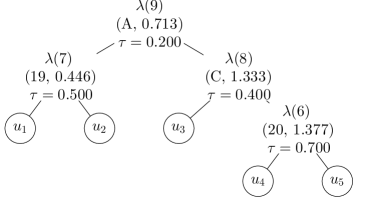

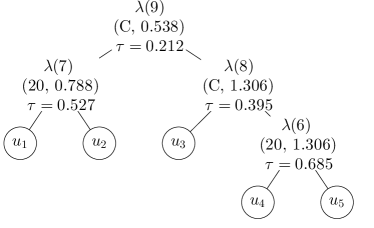

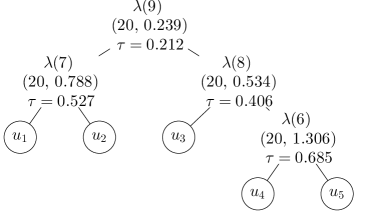

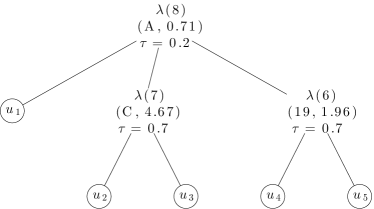

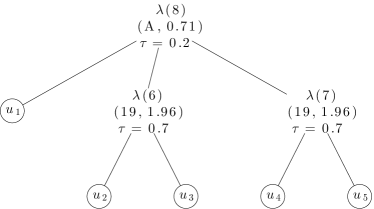

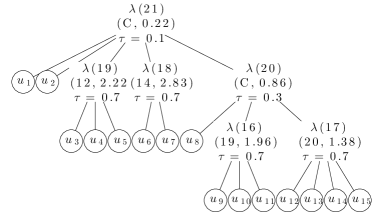

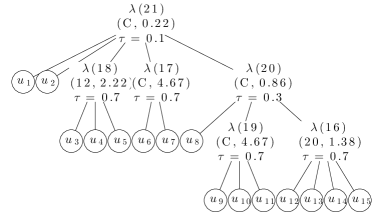

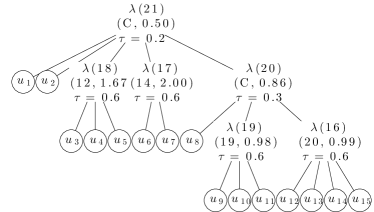

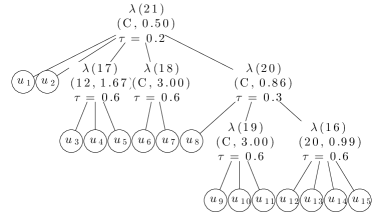

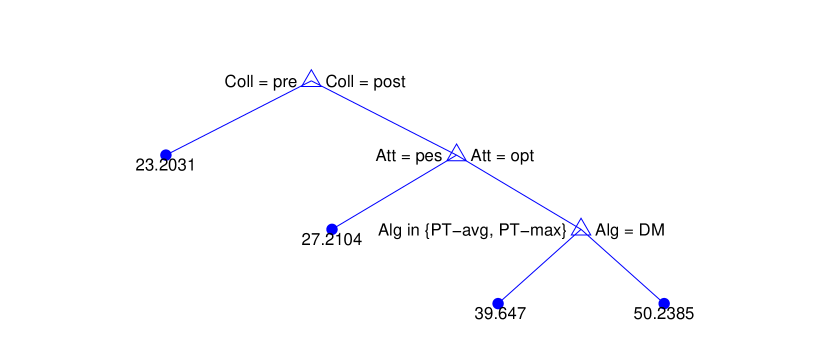

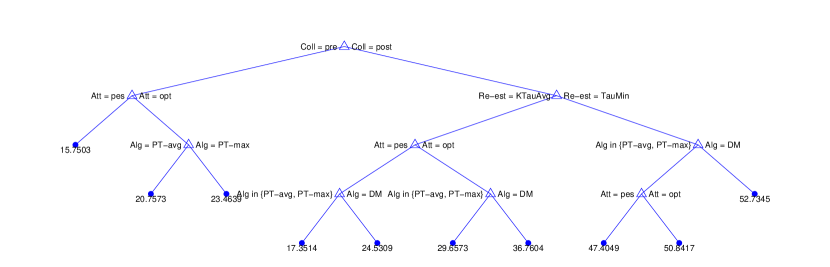

To illustrate our procedure, we generated a sample of observations from the {C, 12, 14, 19, 20}-heterogeneous 15-HAC depicted in Figure 5(a), and, using one of the binary HAC estimation approaches introduced below in Section 6.4, we obtained the binary 15-HAC depicted in Figure 5(b). Then, using the collapsing approach described above, we generated the series depicted in Figure 5(c). Observe the large difference between and . This difference means that the minimal distance is substantially larger when collapsing from to than when collapsing from to . Less formally, when collapsing from to , there might be collapsed forks that are far from each other in the distance and possibly should not be collapsed. Such a statement can be supported by the fact that , and thus the estimate of the number of forks in the model is . The HAC is depicted in Figure 5(d). For deeper insight, we repeat this estimation process 100 times for each (multiplications of 60, which are taken from the experiments described in Section 7) and show the results in the histograms depicted in Figure 6.

Observe that the frequency of = 6 is getting closer to 100 as grows. In Section 7 we show, how successful such an approach is compared to the (unrealistic) assumption that the number of forks in the true copula is known.

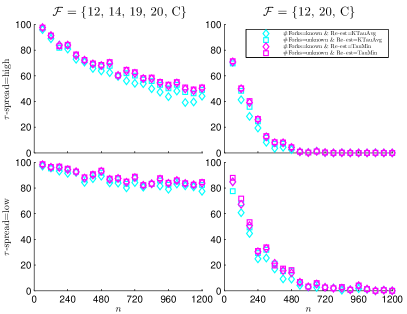

As another improvement, we propose the re-estimation of the parameter of a collapsed fork. The re-estimation process used in kt_kagg is such that the Kendall’s tau corresponding to the collapsed fork is set to , where is the Kendall’s tau corresponding to the collapsing parent fork and corresponds to the Kendall’s tau of the collapsing child fork. If the s.n.c. holds in the collapsing HAC, then , which implies that . On the one hand, such an approach (denoted by TauMin in the following) guarantees the s.n.c. to hold also for the collapsed HAC. On the other hand, it does not take into account the value of the child parameter, which might unnecessarily lead to biasing the collapsed HAC estimate. Hence, in the following paragraph, we introduce a new re-estimation procedure (denoted KTauAvg), which involves all values related to the collapsed node and thus takes into account also the value of the child parameter. These two approaches are compared below in Section 7. Considerations about assuring the s.n.c. for the collapsed HAC while using our collapsing strategy described above are addressed in Section 6.3 (the paragraph containing (34)) and Section 6.4.5.

Denote the sample version of Kendall correlation matrix by , where denotes the sample version of Kendall’s tau between and defined by (17). Let be a fork and be the set of its children. Then the proposed (re-)estimator is given by

| (27) |

where is the family of and is the average function. This estimator is just a generalization of the binary estimator based on Kendall’s tau inversion proposed in [10] to the non-binary case. Note that, given a node with two children, (27) simplifies to the estimator used in Step 1 of Algorithm 2, see Section 6.3. Also note that if the employed values have already been computed, which always happens in our approach as we use them to estimate the HAC structure, the computation time of this estimator is negligible. Let us illustrate the estimator using the 3-HAC depicted in Figure 3. Given a family , assume that and collapse the nodes 4 and 5. Denote the collapsed node by and consider that . Then (27) turns into

6.2 HACs structure estimation

Given an input matrix , Algorithm 1 returns a binary structure estimate and a sequence , where is an estimate of . This algorithm, which is based on the ideas from [27], has been proposed in [10] (see Algorithm 2 therein).

According to our new findings summarized below by Lemma 6.1, it is actually an agglomerative hierarchical clustering (AHC) method [28, p. 414], which is a member of a broad class of AHC methods defined as follows. If denotes a dissimilarity between objects or clusters and and is the dissimilarity between and the combined cluster , then

| (28) |

defines the clustering method for suitable coefficients . Due to notational convenience, we will use the similarity instead of a dissimilarity in the following.

From the point of view of Algorithm 1, objects in AHC refer to leaves and clusters refer to sets of descendant leaves (i.e., to ). Given two clusters or leaves , the similarity (simply denoted by ) between and used in the algorithm is

| (29) |

see Step 2.

Now consider that a dendrogram obtained by an AHC method is a binary tree where the value defined is assigned to each fork in the tree assuming that . Monotonicity of dendrogram means that if is a branch in a dendrogram such that is a leave and is the root, then holds. In other words, if a dendrogram with leaves is monotonic, then

| (30) |

Due to connection of (29) and Step 5, i.e., for all , (30) turns to (15) providing and for all . In other words, if the clustering method based on the dissimilarity produces a monotonic dendrogram, then the output of Algorithm 1 satisfies (15). The next question is clear: Can we somehow assure that an AHC method produces only monotonic dendrograms? Fortunately, there exists a sufficient and necessary condition answering this question.

In [29], it was shown that a hierarchical clustering method given by equation (28) is monotonic, if and only if the following conditions hold:

-

1.

;

-

2.

;

-

3.

.

Lemma 6.1.

Let and be nodes in a binary tree with leaves such that and are disjoint subsets in and there exists a fork satisfying . Let be given by (29). Then

| (31) |

where and .

Observing that coefficients such that and satisfy the conditions on monotonicity implies the following corollary.

6.3 Homogeneous HACs estimation

This section proposes an improved version of the approach for homogeneous HACs estimation introduced in [10]. The new approach summarized by Algorithm 2 is a version of Algorithm 3 proposed in [10] rewritten using our notation and, as will be explained below, one step has been removed.

As mentioned above, Algorithm 3 in [10] includes one more step that serves to guarantee that the resulting estimate is a copula. This step, which is stated as

| (32) |

where and denote the parameters of the children of the fork , would be placed between Step 1 and Step 2 in our new version. Such a step manually forces (10) to be fulfilled, which however might lead to a bias in estimation. Assuming a homogenous HAC from a family with the s.n.c. in the form , see Table 1, such a step is not necessary under relatively weak assumptions as the following theorem reveals.

Theorem 6.3.

Note that in Steps 2 and 5 of Algorithm 1, one can consider also other aggregation functions instead of , e.g., the minimum or maximum. However, according to the experiments reported in [10], setting the aggregation function provides better results than, e.g., for the minimum or maximum. We thus do not provide analogues to Theorem 6.3 for these alternative aggregation functions.

Considering other homogenous estimators available in the literature, analogues to Theorem 6.3 do not exist and thus (15) either must be manually forced or it cannot be assured that the resulting estimate satisfies (10). To illustrate this fact, we now consider the following two estimators:

-

1.

Step 5 of Algorithm 1 together with Step 1 of Algorithm 2 imply that . Another Kendall’s tau based estimator can be constructed just by changing the ordering of the use of and , i.e., by letting . Such an estimator can be found in [30]. In the context of ACs, it is experimentally shown in [4], see Tables 5, 6 and 7 therein, that although this estimator (denoted there by ) has a bias that is similar to the bias of our estimator (denoted there by ), is computationally less efficient than . The following observation that this estimator does not assure that the resulting estimates satisfy (10) can thus be considered as another evidence against choosing this estimator for HAC estimation;

-

2.

The HAC estimator introduced in [7] with an improvement proposed in [9]. In this estimator, we use the maximum likelihood (ML) estimation method for the estimation of at each step . An implementation of this estimator in R can be found in [31] and one of its applications is described in [32]. For a detailed implementation in a pseudo-code (already generalized to the heterogeneous case), see Appendix B.

To quantify how many times an estimator returns an estimate that violates (10), we have done a small experiment, which is described below. According to our observations, the closer the parameters of the parent-child pairs in a HAC model are, the more the considered estimators are prone to violate (10) for a data sampled according to this model. When choosing a HAC model that would be appropriate for this experiment, we went to an extreme and set all its parameters equal, which results in turning this HAC model to an AC. Hence, we generated 1000 times a sample of 100 ( = 100) observations according to the 10-AC from the Clayton family with the parameter (). The first considered estimator violated (15) 7 times and the latter 958 times. Our estimator does not show this problem. Clearly, these results do not imply anything about overall performance of the considered estimators but rather serve for illustrating a desirable property of our estimator that is unique among the considered ones. Also note that other HAC estimators could be created, e.g., by replacing the ML AC estimator in the latter HAC estimator by the inversion of Kendall’s tau or by doing just the opposite in Algorithm 2. However, consider that such HAC estimators would be dependent directly on the pseudo-observations (due to the ML estimation or the diagonal transformation), in contrast to Algorithm 2, which directly depends only on the Kendall correlation matrix. This would imply that they would not admit (28) and thus the s.n.c. would not be guaranteed.

Remark 5.

As , i.e., the family A is unable to model dependencies that correspond to , we set arbitrarily in cases where , where denotes the highest real allowed by the computing system lower than 1. E.g., in MATLAB, would be 1 - 2.2204e-16. A similar approach is used for , i.e., if , we set arbitrarily for = 19, and, if , we set arbitrarily for . Also, as HACs satisfying (9) are unable to model pairwise dependencies such that the corresponding is negative, if , we set arbitrarily for = A, and for {C, 20}.

Clearly, setting the parameter arbitrarily to some value causes a bias. We distinguish two attitudes to cope with this problem:

-

1.

The optimistic attitude, in which we allow, if necessary, to set the parameter to some arbitrary value, accepting that the resulting estimate is biased. This attitude is motivated by the fact that a) the parameter estimation is relatively fast (it is a matter of milliseconds rather than days or weeks) and b) there are instruments available that can measure how well the resulting estimate fits the data, e.g., the GoF statistics recalled in Section 5. Thus, in the case that we have a collection of biased estimates from different families, we can choose the best fitting one using these instruments;

-

2.

The pessimistic attitude, in which, given a family , we stop the estimation process whenever , accepting that the estimation process may not result in any (H)AC at all.

It is important to note that in some cases, even if we set the parameter estimate arbitrarily to some value and thus caused bias, it might happen that the resulting estimate fits the data better than another estimate corresponding to some other family that does not need to be trimmed to some interval. E.g., let . In this case, for the family A, we arbitrarily set to , i.e., . For the family C, such a trimming is not needed and the estimate is provided. But, if the copula underlying the data is more like a copula from the family A, e.g., in tails, GoF might show lower value, i.e., better fit, for the estimate corresponding to the family A despite it is biased. Hence, to avoid omitting such biased estimates that provide better fit, even if they appear rather rarely, we use the optimistic attitude. For more examples in the heterogeneous case, see Section 6.4.6.

Concerning the collapsing procedure we proposed in Section 6.1, we will now show that if (33) holds for the input of Algorithm 2, the construction of this re-estimator inherently assures that the collapsed HAC satisfies the s.n.c. Assume an -homogeneous (possibly non-binary) -HAC with forks, satisfying (10), and denote by the quantity for all . Let be a fork and be the set of its children. Now denote by the fork that is created by collapsing the forks and (without a loss of generality) , i.e., is closer (in ) to than . Assume that , which implies and . Now, rewriting and using (27), it can be observed (similarly to the proof of Lemma 6.1) that (simplifying to

| (34) |

is just a weighted average of and , which in turn implies that as due to the s.n.c. The left hand inequality implies that the s.n.c. for the parent of (which is the same as the parent of ) remains satisfied after collapsing. As is chosen in the way that it is the closest one (in distance) to , it holds that for all . Hence, as , it follows that for all . Thus the s.n.c. remains satisfied also for the children of . Note that under the optimistic attitude, if (33) does not hold for the input of Algorithm 2, we apply the trimming described in Remark 5.

Note that even if the estimation of the parameters depends on the input family , the structure determination is independent on because Algorithm 1 aims to assure (15) instead of (10), which does not involve the families of the underlying generators. As shows Theorem 6.3, such an approach leads to a proper copula for a lot of families. Moreover, as no assumptions on families are necessary, this structure determination approach can be directly used for heterogeneous HAC estimation, which is addressed in the following section. Note that this independence on the underlying families can also be seen in the approach presented in [33] or in the supertree-based approach in [12], which, however, do not cover parameter estimation.

Also, due to this independence, one can consider to collapse an estimated binary structure before (below denoted as pre-collapsing) or after (below denoted as post-collapsing) the parameters are estimated. To clarify, Algorithm 2 corresponds to the latter approach, i.e., a binary HAC (=its structure + its parameters) is first estimated, and then it is collapsed using the approach introduced in Section 6.1. Here, it is important to consider that the parameters are re-estimated, e.g., using (27) if one chooses the KTauAvg re-estimation procedure. In the pre-collapsing approach, one first collapses the structure obtained by Algorithm 1, and then it is passed as an input to Algorithm 2. Here, for the KTauAvg re-estimation procedure, we use an analogoue of (27) given by , where is defined by (27). Hence, given a data sample, two different collapsed HAC estimates can result (one using pre-collapsing and another using post-collapsing), particularly if one consider the attitudes. E.g, assuming the family A and the pessimistic attitude, it can happen that the Kendall’s tau for the root in the binary structure obtained by Algorithm 1 is estimated to be -0.05. Using the post-collapsing approach, this implies that Algorithm 2, as , necessarily ends up without returning any HAC estimate. However, using the pre-collapsing approach, that binary structure is first collapsed, and it is possible that during the re-estimation process, the Kendall’s tau estimate corresponding to the root has changed to 0.05, which a value from , and thus Algorithm 2 does not necessarily ends up without returning any HAC estimate. For this reason, we also consider these two approaches in the experiments described in Section 7.

6.4 Heterogeneous HACs estimation

This section describes, how a HAC that possibly involves generators from different completely monotonic parametric families of Archimedean generators (simply, families) can be estimated. As the structure estimator implemented by Algorithm 1 does not require any assumptions on the families of the underlying generators, we use it as a basis of our new heterogeneous estimator, which is summarized by Algorithm 3 at page 3. Simply speaking, given a set of families , the algorithm returns an -heterogeneous HAC estimate for observations . If , then the algorithm turns into a homogenous estimator. In the rest of this section, we will describe in detail all parts of the algorithm.

Steps 1 and 2 of the algorithm imply that the resulting structure estimate is computed by Algorithm 1. Then, for the parameter estimation, we use the approach from Algorithm 2 (see Step 1 there and Step 5 here) and extend it by involving the aggregated GoF statistics introduced in Definition 5.2. This extension, which is rather straightforward, is described in Section 6.4.1. In Section 6.4.2, we deal with the main problem arising from the extension to heterogeneous HACs, which is how to assure the s.n.c. and in turn that a proper copula results. For this reason, we introduce new concepts that enable assuring the s.n.c. under the optimistic approach, which is justified by Theorem 6.8. Two major cases allowing for up to five different families in a single HAC are then discussed in Sections 6.4.3 and 6.4.4. Finally, in Section 6.4.6, we provide an example illustrating the whole heterogeneous estimation process.

6.4.1 Choosing the appropriate family

Contrary to the homogeneous case, the family of each generator in a heterogeneous estimate can be chosen from a whole set of families. To choose the appropriate family, we evaluate all admissible ones using the GoF test statistic given as an input of Algorithm 3 (inputs 5 and 6) and choose the best fitting one, see also Section 5 for an example. To implement this approach, we added the inner loop (for ), where is related to the s.n.c. and is addressed in detail in Section 6.4.2. In this inner loop, in Step 5, we compute the parameter estimates for all admissible families in the same way as we do for homogenous HACs. Then, having estimated the generators , we select the best fitting one and in turn the best fitting family according to the GoF evaluation of these generators, which is performed in Step 7. Note that Step 6 is closely related to the s.n.c. and is thus described in the following section.

6.4.2 Dealing with the s.n.c.

In homogenous estimation, one can use Theorem 6.3 for a lot of families to deal with the s.n.c., i.e., having a triplet obtained by Algorithm 1, checking (33) to hold assures that a proper copula results, which can be done before Algorithm 2 has been performed.

In the heterogeneous estimation, no analogue to Theorem 6.3 is known, i.e., there is no condition known that would assure that a proper copula results before the estimation process has been started and one have to check the s.n.c. during the estimation process.

In our approach, such a checking process is performed after Step 5. Under the pessimistic attitude (not included in the algorithm as it could be easily derived from the optimistic version described below), if , we remove the family from the set of families admissible for the actual generator. If there is no admissible generator left, the algorithm stops without any result. Under the optimistic attitude, in Step 6, we assure the s.n.c. by forcing that lies in the interval using an auxiliary function defined by

| (35) |

If is an opened or semi-opened interval, e.g., , we first turn it to the closed interval , where is the smallest real allowed by the computing system higher than , and then we use the trim function given by (35).

Even under the optimistic attitude, assuring the s.n.c. is not a trivial task, as can be anticipated from different forms of the s.n.c.s listed in Table 2 or can be seen in the example below Lemma 6.11. However, in Theorem 6.8, we propose specific conditions under which it is assured that a proper copula results before the estimation process has been started, i.e., a situation similar to Theorem 6.3 but taking into consideration that the estimate might be biased. In addition to Theorem 6.8, we will derive explicit forms of these specific conditions for two major cases, in which one is allowed to nest up to 4 or 5 families into a HAC, which are presented in Theorems 6.13 and 6.10, respectively.

As follows from the previous paragraphs, the selection of the interval plays a crucial role in our approach to dealing with the s.n.c. Now, we will introduce several concepts that help to select that, on the one hand, assures the s.n.c. to hold, and, on the other hand, is as wide as possible in order to reduce biasing of the parameter estimates.

Regarding the nature of the parameter constraints following from the s.n.c. and the iterative approach of the estimation process, we introduce a parameter constraint representation which considerably simplifies dealing with different forms of the s.n.c. The idea is to represent the parameter range of a given family by a pair (family label, parameter range), e.g., for the six families from , this representation would be a set with six pairs , (12, ), (14, ), , which is obviously derived from Table 1. The following definition introduces a semigroup that contains such set representations of the parameter ranges.

Definition 6.4.

1) Let , , and . 2) Let be the operation on defined for all by

| (36) |

Then we call the ordered pair the nesting semigroup.

Remark 6.

is a commutative semigroup, i.e., the operation is commutative, associative and the identity element is . This also means that the ordering in which two or more elements of are intersected by is not important. Also note that for all is .

Hence, e.g., assuming and defining , (12, ), (14, ), , it is clear that . Generally, an element from represents generators from different families of generators. However, note that an element from does not necessarily corresponds to a set of generators, i.e., two or more representations can refer to the same generator. E.g., concerning , this follows from the fact that or for all , see Table 1. But, removing the representation of these five generators out of , becomes a representation of a set of generators, see Table 1 again.

Now consider a generator and a set . To decide, whether or not is one of the generators represented by the set , one needs only the pair (and does not need a functional form of ). Based on this observation, a relationship, similar to the relationship introduced in Definition 2.4, is now introduced.

Definition 6.5.

Let , and . Then define the relation by

| (37) |

By convention, is simply denoted by . It follows from the definition that, e.g., (C, 0.5) states that is one of the generators represented by . Similarly, (C, -0.5) states that is not one of the generators represented by

Now, let us have a look at the operation . Assume that we are estimating a {C, 12}-heterogeneous 4-HAC and we have already estimated its structure and two of its generators. E.g., let these two generators be and , which are assigned in the estimation process to be the two children of a generator , which is still unknown, i.e., the values of the pair have not been estimated yet. Such a case corresponds to the one depicted in Figure 7.

The question is, which family-parameter values are admissible in order to the function corresponding to Figure 7 be a copula, i.e., the s.n.c to be satisfied for both parent-child pairs of generators. Considering the pair (, ), according to Tables 1 and 2, if , the s.n.c. to satisfied. Similarly, considering the pair (, ), if , the s.n.c. is satisfied. According to Theorem 3.2, if both conditions are satisfied, i.e., if as well as , then a copula results. To compose these conditions into one, we can use the operation. Observe that . Using Tables 1 and 2 again, we can verify that for all , the s.n.c. for both parent-child pairs is satisfied and thus a proper copula results. Such an approach can be generally used to assure that a proper copula results when a parent (generator) of one or more generators is estimated, which is later shown in connection with Theorem 6.8.

Now, consider two special classes of elements from .

Definition 6.6.

Let . An is called Archimedean, if

| (38) |

Further, an is called -Archimedean, if for all Archimedean holds that

| (39) |

In other words, an Archimedean represents a set of c.m. generators from the families from . An -Archimedean represents the set of all c.m. generators from the families from . E.g., is -Archimedean.

Now, consider again the estimation process related to Figure 7. Having a child generator estimated, e.g., the generator , it would be desirable to have a simple tool that would provide us values of that are admissible in order to the s.n.c. be satisfied without the need of inspecting Tables 1 and 2. E.g., this tool would provide us the set when concerning the child generator . Such a tool in a form of a mapping that relates to the pairs of families from , see (3), is introduced in the following definition.

Definition 6.7.

Let and be -Archimedean. Then the mapping is defined for all by

| (40) |

Hence, given a child generator representation , simply contains representations of all known c.m. generators that can be parents of such that the s.n.c. is satisfied. Clearly, if there appear some other families of c.m. generators that can be parents of such that the s.n.c. is satisfied, a generalization of for these families can be simply done by adding these families to . Returning to the example related to Figure 7, one can easily see, using Tables 1 and 2, that, e.g., or .

Based on these ideas, i.e., using the nesting semigroup , the mapping and the function trim, we are able, for some appropriately selected (its choice is discussed below), to assure that Algorithm 3 always returns a triplet satisfying (9), as states the main theorem of this work.

Theorem 6.8.

In other words, Algorithm 6.8 returns a proper copula provided the condition (41) holds. Note that this condition assures that, given two children (represented by and ) of a parent generator in an estimated HAC, there always exists an admissible pair representing the parent generator such that the s.n.c. holds with its child generators. Without satisfying this condition, it might happen that Algorithm 6.8 stops before the estimation process is finished without any resulting copula, which is discussed in detail in Section 6.4.4.

Theorem 6.8 opens two questions: 1) how to appropriately select for a considered in order to (41) be satisfied? and 2) does there exist some simple, i.e., easy to implement, expression of the range of the mapping ? Both questions can be satisfactorily answered.

Consider the family combinations , i.e., the pairs in Table 2. These pairs can be separated according to the nature of the parameter constraints following from the corresponding s.n.c. shown in the fourth column in Table 2:

-

1.

the class – no constraints on the parameters following from the corresponding s.n.c. ={(A, 19)}.

-

2.

the class – the s.n.c. results in the constraint on the parameter of the parent generator. = {(C, 12), (C, 19)}.

-

3.

the class – the s.n.c. results in the constraint on the parameter of the child generator. = {(A, C), (A, 20)} .

-

4.

the class – the s.n.c. results in the constraint both on the parameter of the parent generator and on the parameter of the child generator. = {(C, 14), (C, 20)}.

Using this classification, we answer the questions stated above for major two cases.

6.4.3 The case

We start with {C, 12, 14, 19, 20}, which contains as subsets all combinations from and .

Lemma 6.9.

Let be -Archimedean. Then the mapping defined by

| (42) |

for all is the mapping given by Definition 6.7 for .

Now we can discuss the appropriate . In the case, we can allow that the appropriate , denote it , is the broadest possible, i.e., is -Archimedean. Explicitly, . This is confirmed by the following theorem.

Theorem 6.10.

Remark 7.

The corresponding version of Theorem 6.10 for any containing a pair combination from or can be proved analogously. Note that such always contains the family C.

6.4.4 The case

Answering the questions is more complicated, if we also involve some family combination from , i.e., if {A, C} or {A, 20} . In this case, it is not possible that the appropriate is -Archimedean. This fact is explained by the following lemma, which generalizes to an arbitrary -HAC the idea of nesting the family combinations {A, C} and {A, 20} in a 3-HAC proposed in Theorem 4.3.2 in [15, p. 118].

Lemma 6.11.

In other words, Lemma 6.11 says that if we want to allow that the family A is involved in the output of Algorithm 3, we have to restrict the parameters of all generators from families C and 20 to be . Otherwise, no copula function satisfying the s.n.c. can be constructed. Study the following example. Assume = {A, C} and two child generators and in the same 4-HAC structure as in the one depicted in Figure 7. Observing that , it follows that there is no admissible choice of the family and the parameter of their parent in order to the s.n.c. be satisfied. Hence, for this choice of , if we want to assure that Algorithm 3 returns a copula, we cannot allow (by setting of the input ) all generators from the -Archimedean set AC and have to set the input to some smaller subset. According to Lemma 6.11, we suggest to choose (as ) the set AC, where . Obviously, setting , we cannot assure that a copula results with the same argument as above in this paragraph. By contrary, setting , we unnecessarily avoid some generators in the estimation process, which in turn could lead to an unnecessarily bias.

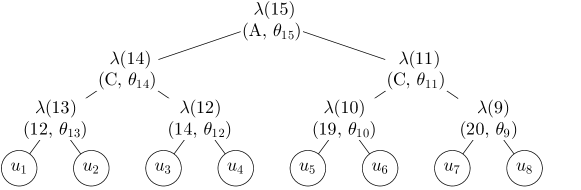

Our next consideration concerns the 8-HAC depicted in Figure 8. It is a -heterogeneous binary 8-HAC that involves family combinations both from and . Now consider the constraints for the parameters following from the s.n.c. As follows from Lemma 6.11, and must be in order to allow for the family A in an output of Algorithm 3. Also, must be due to s.n.c. corresponding to the fact that one of its child is a generator from the family 12, see Table 2. Thus must equal to 1. Next, must be due to the s.n.c. for the combination (C, 14). As and (following the parameter range of the family 14), it implies that . Such a HAC with two parameters restricted to 1 is an extremely constrained model and is rarely feasible in practical applications. Considering other -HACs, that involve all families from , such HACs could be even more constrained, hence, we do not consider them in the following.

We rather consider a smaller subset of , the set {A, C, 19, 20} that contains (as subsets) at least one family combination from each , …, .

Lemma 6.12.

Let be -Archimedean. Then the mapping defined by

| (43) |

for all is the mapping from Definition 6.7 for .

Following the previous considerations, the broadest possible is thus not used in Lemma 6.12, but . The values in bold are the adjustments of the parameter ranges due to the consequences of Lemma 6.11.

Theorem 6.13.

Remark 8.

The corresponding version of Theorem 6.13 for {A, C, 19} containing a pair combination from each , …, can be shown analogously. Also, the corresponding version of Theorem 6.13 for any containing a pair combination from each , …, can be shown analogously as the combination (A, 19) from do not involve any constraints following from the s.n.c. that must be dealt with.

6.4.5 A general strategy, assuring the s.n.c. and pre-collapsing

Finally, we propose a strategy for heterogeneous HACs estimation concerning the and cases:

-

1.

If we want to allow a generator from the family C or 20 to have its parameter value lower than 1, execute the algorithm with and , i.e., then the family A is not allowed in the resulting estimate;

-

2.

If we want to allow the family A in the resulting estimate, execute the algorithm with and ;

-

3.

If we aim to get the best possible fit of the resulting estimate no matter if the family A is involved or not, generate two HAC estimates using both of the previous cases and choose the one that better fits the data using, e.g., some of the GoF test statistics described in Section 5.

Considering the problem of assuring the s.n.c. while collapsing a heterogeneous HACs using our collapsing strategy proposed in Section 6.1, we use an approach that is analogous to what we do in Step 6 of Algorithm 3. I.e., we compute (originally computed in Step 4) by

| (44) |

where are the children of the collapsed node, which assures that the new collapsed fork satisfies the s.n.c with all of its children. Also, for pre-collapsing (see Section 6.3), Step 3 is substituted by , Step 4 is substituted by (44) and the term in Step 7 is substituted by , which is a construction analogous to (27).

6.4.6 An example

Compared to the homogenous HAC estimation, the heterogeneous HAC estimation is significantly more complex partly due to the involvement of GoF testing but mainly due to the need to deal with the s.n.c. for different family combinations. Hence, to clarify the whole heterogeneous estimation process, we illustrate it by the following example.

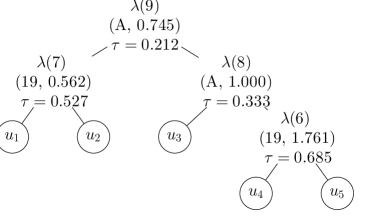

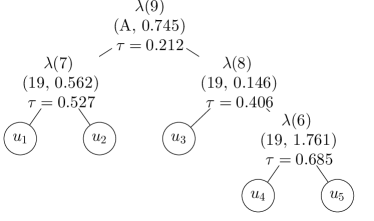

Let and be the {A, C, 19, 20}-heterogeneous binary 5-HAC depicted in Figure 9(b). We sample observations according to using the approach described in [5]. These observations are depicted in Figure 9(a). Now assume that is unknown and we are interested in its estimate based on the data sample.

We set the inputs of Algorithm 3 as follows: , and . We also set to be the maximum function and to be . Recall that the algorithm is constructed under the optimistic attitude.

The Kendall’s correlation matrix computed in Step 1 can be seen in Figure 9(a). In Step 2, Algorithm 1 returns the triplet . This result follows (recall that for all by the definition) from the matrices depicted in Figures 9(a) and 10 corresponding to the loops of Algorithm 1, respectively, and the consideration that Algorithm 1 just joins two leaves or forks corresponding to the maximum in these matrices. Note that in the loop of Algorithm 1, and thus in Step 2 there and in turn . Observe that is the true structure .

Continue with Algorithm 3. Step 3 says that each leave can be assigned to any parent generator from , i.e, generators (but not all of them) from the families A, C, 19 and 20.

Now, start the outer loop with . In Step 3, as , it is . In Step 4, . Thus, , assuming the lexicographical ordering of the families, i.e., = (A, C, 19, 20). As , we compute in Step 5 the estimates for the families {A, C, 19, 20}. As , we should compute for all . But, as , see Table 3, and we assume the optimistic attitude, we artificially set the , similarly to our approach to homogeneous HAC estimation, see Section 6.3. Note that denotes the highest real allowed by the computing system (we used MATLAB for this example) lower than 1. Hence, we get the parameter estimates = (1 - , 4.339, 1.761, 1.306). Due to the fact that all the parameters belong to the corresponding parameter ranges stored in , the values remain unchanged in Step 6. In Step 7, we compute the statistics and get the values (11.732, 3.002, 0.690, 0.355). Note that, assuming , are the observations of . Based on the GoF values, the generator corresponding to the minimal value 0.355 is selected as the best fitting estimated generator. Thus, in Step 8, . In Step 9, as , the parameter constraints for the (still unknown) parent of the fork 6 are computed . The reader can compare this result with the s.n.c.s shown for the child generator from the family 20 in Tables 1 and 2.

Now consider the second loop (). In Step 3, . In Step 4, again, . Thus, , . In Step 5, as , we compute the parameters estimates = (1 - , 2.225, 0.562, 0.788). In Step 6, the trim function applies to and changes it to 1. Recall that this adjustment follows from Lemma 6.11, which says that if one wants to involve the family A in a HAC, it is not possible to have a generator from family 20 with parameter lower than 1. In Step 7, we compute resulting in the values (3.528, 0.656, 0.0527, 1.187) and thus . In Step 8, . In Step 9, , see Tables 1 and 2 to check this result.

In the third and fourth loop, the s.n.c. comes into play more significantly. Consider the third loop (). In Step 3, . In Step 4, as is a fork and not a leaf as in the previous loops, additional constraints following from the s.n.c. come into play. Hence, , . In Step 5, as , we compute the estimates assuming (A, C, 20). Observe that two of the parameters are out of the corresponding parameter ranges, thus in Step 6, we set to trim( and to trim(. Note that under the pessimistic attitude, the estimation process would stop here with no result, as all parameter estimates have been trimmed/biased. In Step 7, we compute the statistic resulting in (0.287, 0.033, 6.331) and thus , i.e., in Step 8. Recall that , i.e., two 2-AC GoF test statistics computed for the bivariate margins and are aggregated by the maximum function. In Step 9, as , the parameter constraints for the parent of the fork 8 are computed as . The reader can compare this result with the s.n.c.s shown in Tables 1 and 2.

Now consider the last loop (). In Step 3, , i.e., both and are forks. Hence, in Step 4, . In Step 5, we compute assuming (A, C) . In Step 6, trimming applies to and thus = trim(. Again, this change relates to Lemma 6.11. In Step 7, the statistic results in (0.030, 0.674) and thus . Recall that are the observations corresponding to the bivariate margins and . In Step 8, := . Step 9 in this loop does not influence the result.

Observe that we have obtained the same families for the same forks as in the model, and that the triplet is satisfying (9), see also Figure 9(c).

Finally, we evaluated the resulting estimate using and we obtained the value 0.032. As a comparison, we used Algorithm 3 to obtain other 4 estimates assuming different settings of the set and attitudes. These estimates are depicted in Figures 11(a), 11(b), 11(c) and 11(d), and the corresponding values of are 0.060, 0.110, 3.248 and 0.037, respectively. As mentioned above, the estimation process for = {A, C, 19, 20} under the pessimistic attitude terminated in the loop without any result. These results show that:

-

1.

Allowing for more families enables for better flexibility and thus for better fit, which follows from the fact that even if the {A, C, 19, 20}-heterogeneous estimate is slightly biased (the generator in the estimate depicted in 9(c)), it can fit the data better than the other estimates with a more restricted choice of families no matter if biased or unbiased;

-

2.

Comparing the values of for the two estimates in Figure 11 obtained under the optimistic attitude with the two estimates depicted in the same figure obtained under the pessimistic attitude, i.e., we observe that the optimistic one for = {C, 19, 20} shows better fit that the pessimistic one but just the opposite for = {A, C, 19}, one should always consider estimates obtained under both of the attitudes as none of the attitudes may assure the better fit.

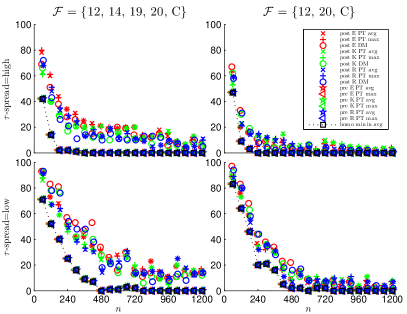

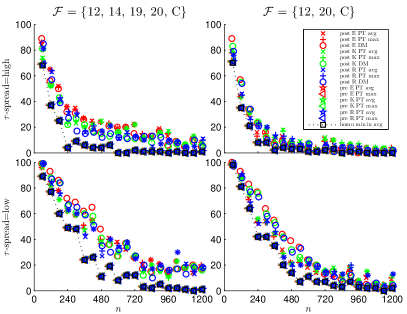

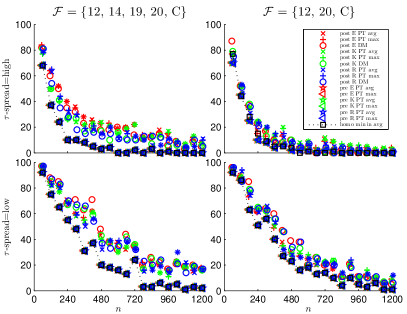

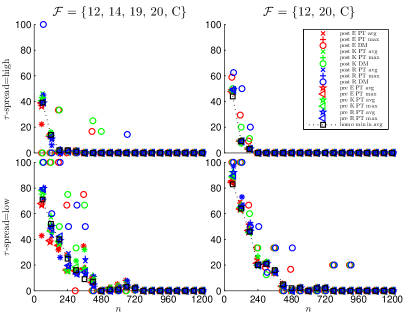

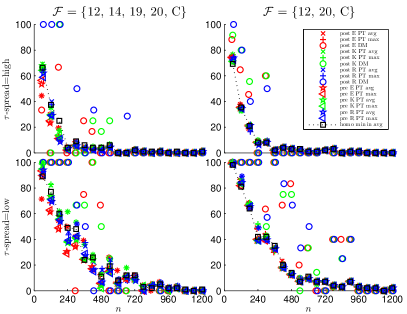

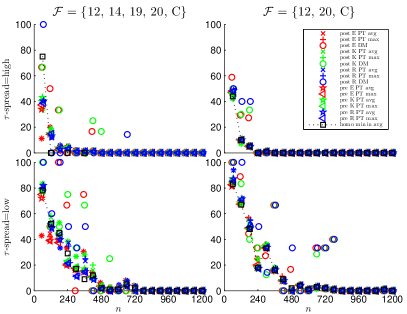

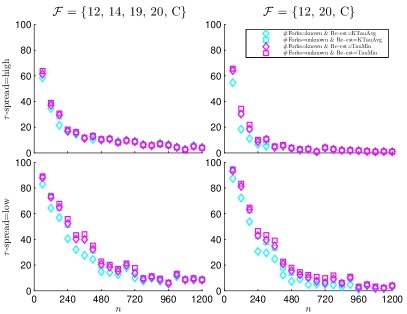

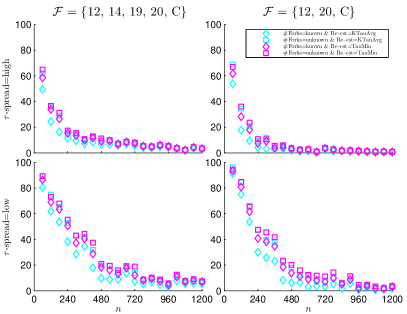

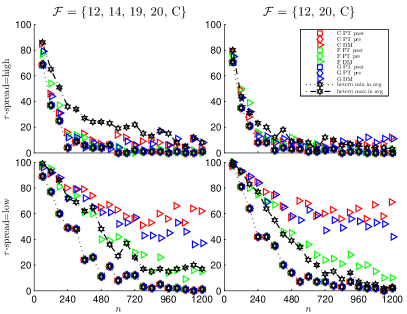

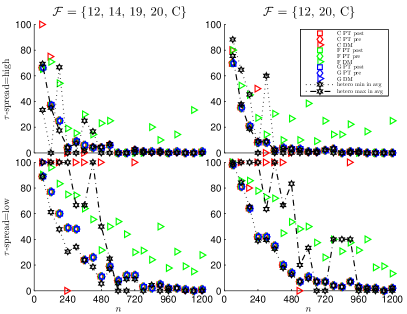

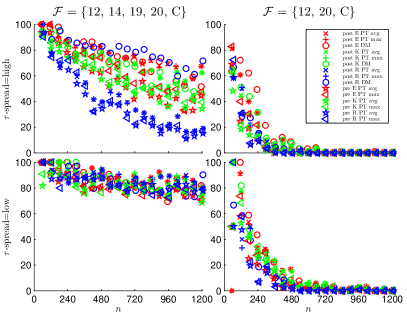

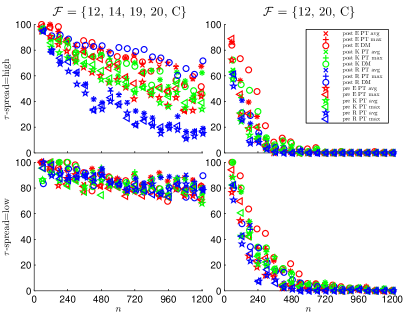

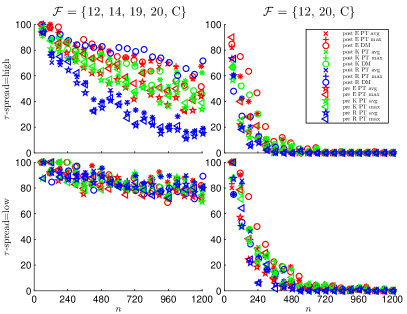

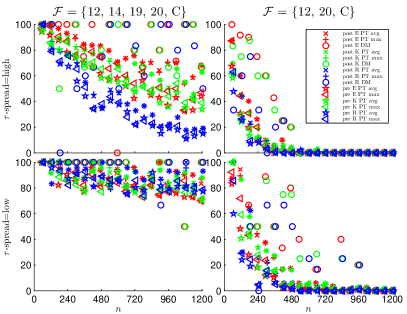

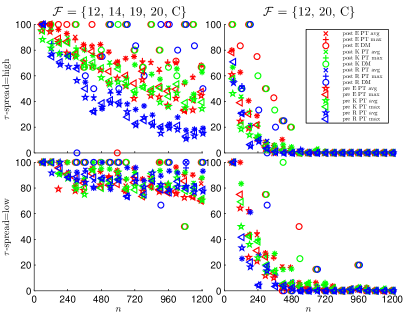

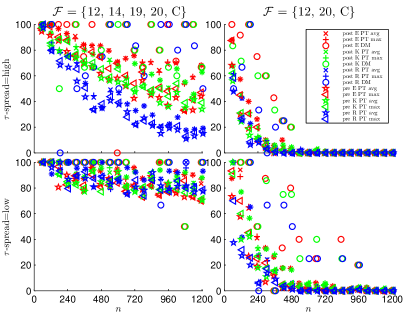

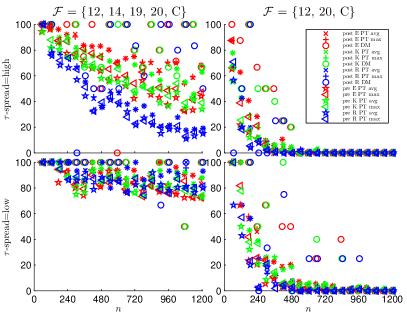

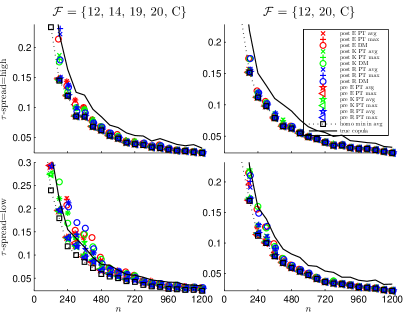

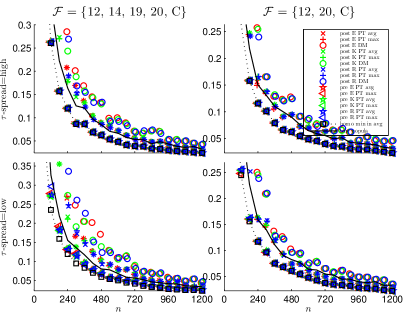

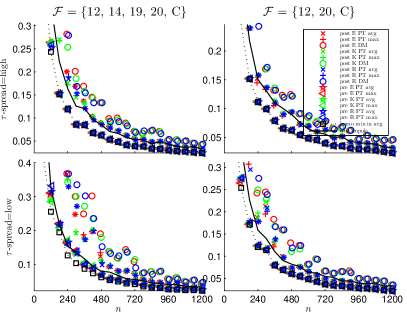

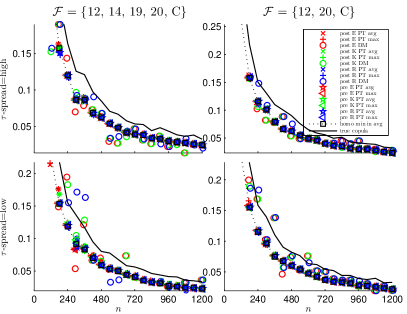

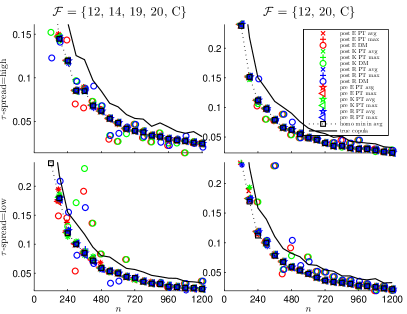

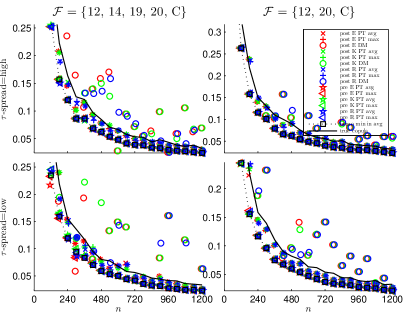

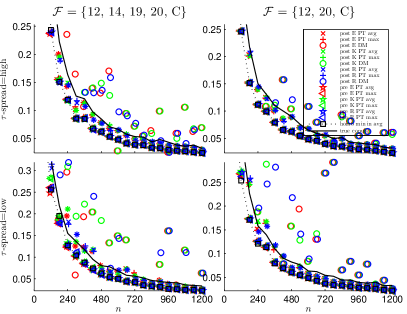

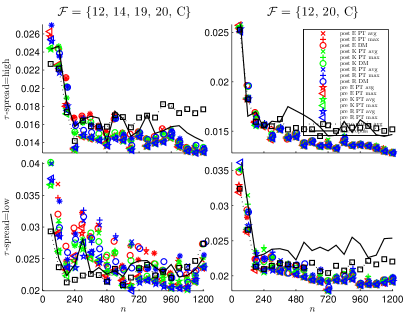

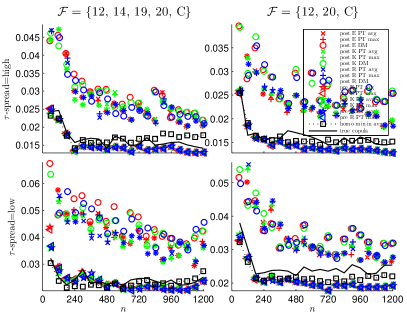

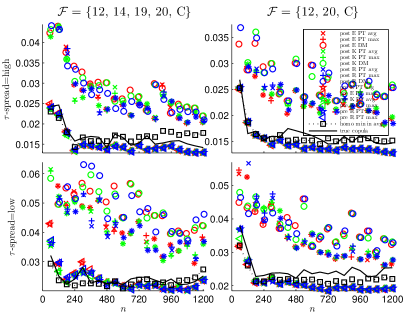

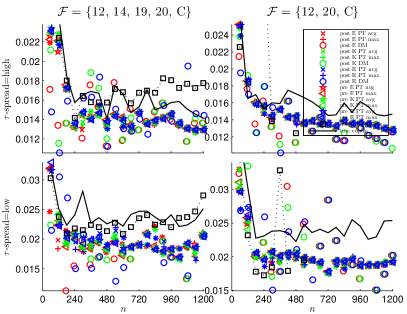

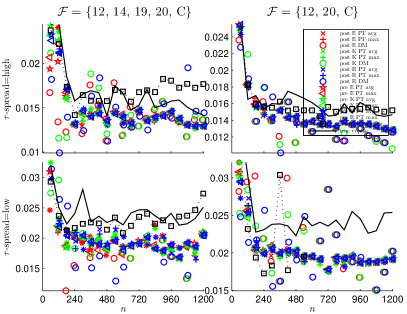

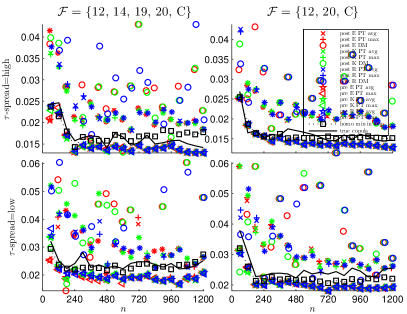

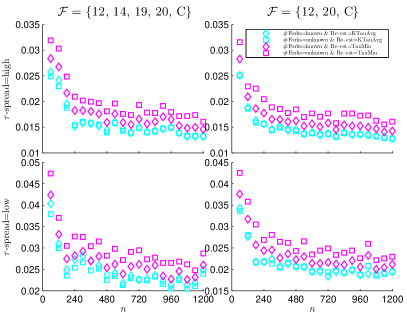

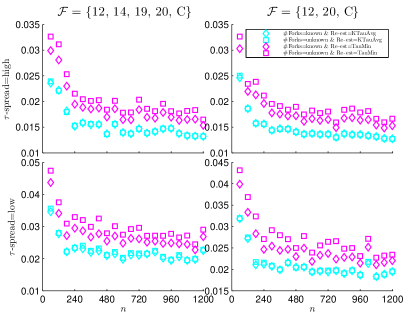

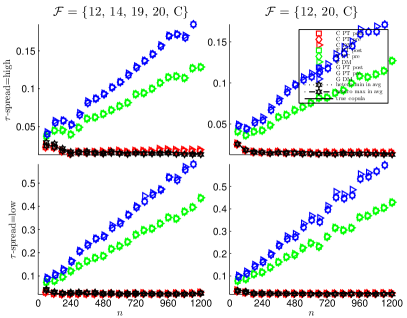

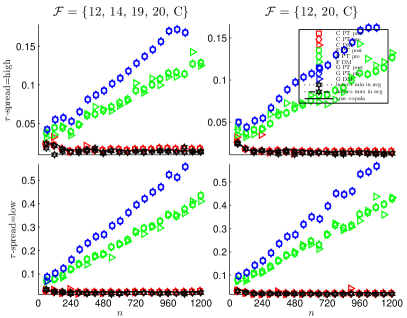

7 Experiments

To show abilities of the proposed approach to heterogeneous HAC estimation represented by Algorithm 3, we perform an experimental study on data simulated from 12 different heterogeneous HACs with dimensions up to and involving up to five parametric families of Archimedean generators in a single HAC. To the best of our knowledge, there does not exist any other implemented methods suitable for heterogeneous HACs estimation. to have at least one heterogeneous estimator to compare, we thus made use of the homogeneous estimator introduced in [7] with an improvement proposed in [9], and generalized it to the heterogeneous case applying the findings reported in Section 6.4. A detailed description of this alternative heterogeneous estimator can be found in Appendix B.

In the rest of this section, several variants of these estimators, generated by different input settings and by using different collapsing approaches, are compared. This comparison concerns success in estimating the structure and the families of the true copula, precision of the estimated parameters and goodness-of-fit. The comparison was implemented and performed in MATLAB.

7.1 Design of the performed experiments