Multiple Time Series Ising Model for Financial Market Simulations

Abstract

In this paper we propose an Ising model which simulates multiple financial time series. Our model introduces the interaction which couples to spins of other systems. Simulations from our model show that time series exhibit the volatility clustering that is often observed in the real financial markets. Furthermore we also find non-zero cross correlations between the volatilities from our model. Thus our model can simulate stock markets where volatilities of stocks are mutually correlated.

1 Introduction

The financial markets are considered to be complex systems where many agents are interacting at different levels and acting rationally or in some cases irrationally. Such financial markets produce a rich structure on time variation of various financial assets and the pronounced properties of asset returns has been classified as the stylized facts, e.g. see [1]. The most prominent property in the stylized facts is that asset returns show fat-tailed distributions that can not be explained by the standard random work model. A possible explanation for the fat-tailed distributions is that the return distributions are viewed as a finite-variance mixture of normal distributions, suggested by Clark[2]. In this view asset returns follow a Gaussian random process with a time-varying volatility. This view, using realized volatility[3, 4] constructed from high-frequency data, has been tested and it is found that the asset returns are consistent with this view[5, 6, 7, 8, 9, 10].

Bornholdt proposed an Ising model designed to simulate financial market as a minimalistic agent based model[11]. The Bornholdt model successfully exhibits several stylized facts such as fat-tailed return distributions and volatility clustering[11, 12, 13, 14]. Variants of the model have also been proposed and they exhibit exponential fat-tail distributions[15] or asymmetric volatility[16]. The view of finite-variance mixture of normal distributions has also been tested for the Bornholdt models and it is shown that returns simulated from the models are consistent with the view of the finite-variance mixture of normal distributions[17, 18].

So far the models studied only dealt with a financial market where a single asset is traded. In the real financial markets various financial assets are traded and they are correlated each other. Measuring correlations between assets is important to investigate stability of financial markets and many studies have been conducted to reveal properties of correlations in financial markets, e.g. [19, 20, 21, 22, 23]. In this study we propose an Ising model that extends the single Bornholdt model to a multiple time series model. Then we perform simulations of our model and show that the model can exhibit correlations between the return volatilities.

2 Multiple Time Series Ising Model

Let us consider a financial market where stocks are traded and assume that each stock is traded by agents on a square lattice. Each agent has a spin and it takes two states corresponding to ”buy” (+1) or ”sell” (-1), where stands for the th agent. The decision of agents are made probabilistically according to a local field. In our model the local field at time is given by

| (1) |

where stands for a summation over the nearest neighbor pairs, denotes the th stock and is the magnetization that shows an imbalance between ”buy” and ”sell” states, given by . is the nearest neighbor coupling and in this study we set . The third term on the right hand side of eq.(1) describes the interaction with other stocks that is not present in the Bornholdt model. More precisely this interaction couples to the magnetization of other stocks and introduce an effect of imitating the states of other stocks. The magnitude of the interaction is given by the interaction parameters that form a matrix having zero diagonal elements, i.e. . As in the Bornholdt model the states of spins are updated according to the following probability.

| (2) | |||||

3 Simulations

In this study we perform simulations for , i.e. we simulate a stock market consisting of two stocks. The simulations are done on square lattices with the periodic boundary condition. We set simulation parameters to . Here we assume symmetric , i.e. , which means that the stocks we consider give the same interaction effect to other stocks each other. Here we make simulations for five values of , . The states of spins are updated randomly according to eq.(2). After discarding the first updates as thermalization we collect data from updates.

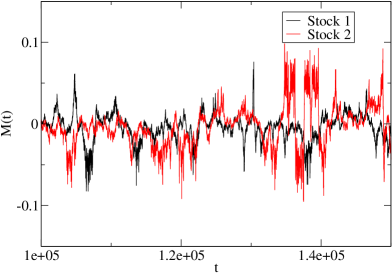

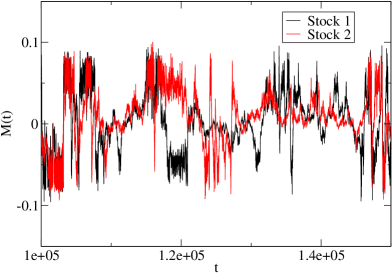

Fig.1 shows the time series of the magnetization for two stocks ( 1 and 2 ) at . Simulating at means that two stocks are independent. On the other hand Fig.2 shows the time series of the magnetization at where the interaction between stocks are present and we find that synchronization occurs between the magnetizations. For other we also see similar synchronization between the magnetizations to a certain extent.

Such synchronization also occurs between the returns defined by as in [13]. The time series of returns at and 0.15 are shown in Figs. 3 and 4 respectively. It is clearly seen that volatility clustering occurs in the return time series. At , however, we see no synchronization between the volatility clusterings. On the other hand some volatility clusterings synchronize at .

To quantify the strength of the synchronization we measure cross correlations between volatilities from the two stocks. The cross correlation between the th and the th volatilities is given by , where and stands for the volatility and its standard deviation of the th stock respectively. Here we define the volatility by the absolute value of return. Table 1 shows the values of cross correlations for various and we find that the cross correlation of volatility increases with .

| 0.0 | 0.05 | 0.07 | 0.10 | 0.15 | |

|---|---|---|---|---|---|

| cross correlation | 0.15 | 0.31 |

4 Conclusion

We have proposed an Ising model which can simulate multiple financial time series and performed simulations of a stock market with two stocks. The interaction parameter in the model tunes the strength of correlations between stocks. We calculated cross correlation between volatilities of the two stocks and found that the cross correlation increases with . Therefore our model serves to simulate stock markets where volatilities of stocks are mutually correlated. Since we have demonstrated the model including only two stocks it may be desirable to further investigate the more realistic model that includes many stocks.

Acknowledgement

Numerical calculations in this work were carried out at the Yukawa Institute Computer Facility and the facilities of the Institute of Statistical Mathematics. This work was supported by JSPS KAKENHI Grant Number 25330047.

References

References

- [1] Cont R 2001 Quantitative Finance 1 223–236

- [2] Clark P K 1973 Econometrica 41 135-155

- [3] Andersen T G and Bollerslev T 1998 International Economic Review 39 885-905

- [4] Andersen T G, Bollerslev T, Diebold F X and Labys P 2001 J. Am. Statist. Assoc.A 96 42-55

- [5] Andersen T G, Bollerslev T, Diebold F X and Labys P 2000 Multinational Finance Journal 4 159–179

- [6] Andersen T G, Bollerslev T, Diebold F X and Ebens H 2001 Journal of Financial Economics 61 43–76

- [7] Andersen T G, Bollerslev T and Dobrev, D 2007 Journal of Econometrics 138 125-180

- [8] Andersen T G, Bollerslev T, Frederiksen P and Nielsen M Ø 2010 Journal of Applied Econometrics 25 233-261

- [9] Takaishi T, Chen TT and Zheng Z 2012 Prog. Theor. Phys. Supplement 194 43-54

- [10] Takaishi T 2012 Procedia - Social and Behavioral Sciences 65 968–973

- [11] Bornholdt S 2001 Int. J. Mod. Phys. C 12 667–674

- [12] Yamano Y 2002 Int. J. Mod. Phys. C 13 89-96

- [13] Kaizoji T, Bornholdt S and Fujiwara Y 2002 Physica A 316 441–452

- [14] Krause S M and Bornholdt S 2011 arXiv:1103.5345

- [15] Takaishi T 2005 Int. J. Mod. Phys. C 16 1311–1317

- [16] Yamamoto R 2010 Physica A 389 1208-214

- [17] Takaishi T 2013 J. Phys.: Conf. Ser. 454 012041

- [18] Takaishi T 2014 JPS Conf. Proc. 019007

- [19] Plerou V, Gopikrishnan P, Rosenow B, Amaral L A N and Stanley H E 1999 Phys. Rev. Lett. 83 1471-1474

- [20] Plerou V, Gopikrishnan P, Rosenow B, Amaral L A N, Guhr T and Stanley H E 2002 Phys. Rev. E 65 066126

- [21] Utsugi A, Ino K and Oshikawa M 2004 Phys. Rev. E 70 026110

- [22] Kim D and Jeong H 2005 Phys. Rev. E 72 046133

- [23] Wang D, Podobnik B, Horvatić D and Stanley H E 2011 Phys. Rev. E 83 046121