“Chaos” in energy and commodity markets: a controversial matter

Abstract

We test whether the futures prices of some commodity and energy markets are determined by stochastic rules or exhibit nonlinear deterministic endogenous fluctuations. As for the methodologies, we use the maximal Lyapunov exponents (MLE) and a determinism test, both based on the reconstruction of the phase space. In particular, employing a recent methodology, we estimate a coefficient that describes the determinism rate of the analyzed time series. We find that the underlying system for futures prices shows a reliability level near to while the MLE is positive for all commodity futures series. Thus, the empirical evidence suggests that commodity and energy futures prices are the measured footprint of a nonlinear deterministic, rather than a stochastic, system.

JEL classification: C53; D40; Q02; Q47.

1 Introduction

Over the years, chaos††footnotetext: Keywords: chaos, butterfly effect, commodity futures. theory††footnotetext: 1Dept. of Economics, Roma Tre University, via Silvio D’Amico 77, 00145 Rome, Italy; loretta.mastroeni@uniroma3.it, pierluigi.vellucci@uniroma3.it. has gradually provided a framework to study some interesting properties of time series. An important reason to be interested in chaotic behaviour is that it can potentially identify, among many time series, which of them appear to be actually random. In particular, as for commodity as well as many other markets, evidence on deterministic chaos would have important implications for regulators and short-term trading strategies.

Moreover, if the random walk model is not a proper account of public market behaviour, then the debated Efficient Market Hypothesis, that plays such a basic role in the markets, might be meaningless in this context.

The question is whether such random-looking data are actually random or completely deterministic. If they are completely random, then their behaviour is not predictable anyway; otherwise, it is possible to predict their behaviour over short periods of time (whereas long prediction is impossible, due to the instability of chaotic systems). Hence, this distinction provides the predictability degree of the analyzed system.

The presence of chaos in the time series of commodity and energy markets is a controversial matter: one can take a look at the literature on energy markets, where the evaluations performed over the years show contrasting results, which might be justified, for example, by a misunderstood application of the theoretical aspects of chaos theory.

Chaos theory is linked to Devaney (1989), but in general the literature actually deals with the butterfly effect, which, according to Devaney, is only one of the properties of the definition of chaos.

The butterfly effect entails that, if two initial conditions slightly differ for a quantity , their difference after time will be with , that is, with exponential separation. Small differences in initial conditions (such as those due to rounding errors in numerical computation) yield widely diverging outcomes for such dynamical systems, making long-term prediction impossible in general.

Butterfly effect can be checked by an entropy test (Farmer (1982), Grassberger and Procaccia (1983)) which employs the Kolmogorov entropy (Kolmogorov (1958)) and the maximal Lyapunov exponents (MLE) (Schuster and Just (2006), Ott (2002), Strogatz (2014), Kodba et al. (2004)).

We analyze the nonlinear deterministic structure in some commodity and energy markets by testing for sensitive dependence on initial conditions. Our data set consists of daily prices of commodities (natural gas, heating oil, gold, silver, corn, oats, cocoa, coffee, feeder cattle, lean hogs), considered in two previous papers Benedetto et al. (2015a, 2016) covering several ranges in the period 01.07.1959 - 15.05.2014.

As for the methodologies, we use the Lyapunov Exponents and a determinism test, both based on the reconstruction of the phase space. In particular, we employ a coefficient that describes the determinism rate of the analyzed time series. The coefficient represents, in percentage, the reliability level about the test on the sensitive dependence on initial conditions. The introduction of this reliability level is motivated by the fact that time series generated from stochastic systems might show sensitive dependence on initial conditions (see Tanaka et al. (1996), Ikeguchi and Aihara (1997), Tanaka et al. (1998)). The coefficient has been introduced by Kaplan and Glass (1992), and here it is estimated by employing a recent methodology developed by Kodba et al. (2004).

In our work, the reliability level yields results near to while the MLE is positive for all commodity futures series. This means that they show a considerable contribution of determinism. In this way, we can ensure the presence of butterfly effect (as specified above, one of the properties of a chaotic system, according to Devaney Devaney (1989)) in the commodity futures markets considered in the paper.

This study contributes to an overall picture of the role of chaos in the energy and commodity markets. In particular, we define a working hypothesis that addresses three important features of chaotic signals, namely, the existence of a low-dimensional attractor in the underlying dynamics, the presence of sensitive dependence on initial conditions, and the deterministic behaviour of the system. The methodologies we use suggest that commodity futures prices are the measured footprint of a deterministic, rather than stochastic, system. Determinism analysis suggests that there are several deterministic forces interacting with each other. The presence of a chaotic dynamics could be connected to the existence of several deterministic forces that may result in complex price movements in financial markets. Today, the complexity of financial and commodities markets is very high because world decisions in business, finance and economics are influenced by sociologic, environmental, and geopolitical factors. In this regard, Panas and Ninni Panas and Ninni (2000) write in their still relevant conclusions: “An energy economist who is interested in the dynamic behaviour of the complex system that governs the oil markets needs to know how sensitive the system is to initial conditions, and to achieve this he needs to estimate the Lyapunov exponents”.

Determinism is related to the role of information in the markets that, no doubts, is of paramount importance. Let us think to the stepping formalization proposed by Fama (see e.g. Malkiel and Fama (1970), Fama (1998)). The central issue is whether or not to adopt trading strategies that achieve excess returns relative to the market, based on information contained in the historical data. Currently, the empirical evidence would seem to indicate that markets are often not efficient, even in weak form. The perception of a trend as seemingly stochastic could be due to the lack of knowledge of the information underlying it.

The plan of the paper is as follows. Section 2 provides a brief review of chaos theory results in the field of commodity futures markets. In Section 3 we consider the implications of chaos in commodity futures markets. In Section 4 we describe the dataset and present estimate of three diagnostic tests for deterministic butterfly effect: (i) reconstruction of the phase space, where we estimate the smallest sufficient embedding dimension of the system using the FNN algorithm; (ii) Lyapunov exponents, which measure the divergence rate; (iii) determinism test, to distinguish deterministic behaviour from stochastic one. In Section 5 we discuss and interpret the estimates obtained in Section 4, comparing them with the results found in the literature. Finally, Section 6 is devoted to the conclusions.

2 Brief literature review

The presence of butterfly effect in commodity futures markets is a controversial matter, as can be deduced from the literature reviewed below: some papers claim they have detected the presence of chaos (butterfly effect), while others state the opposite.

Chwee (1998) tests for the presence of butterfly effect using the NYMEX 1-month, 2-month, 3-month, and 6-month daily natural gas settlement prices, from April 1990 to September 1996. The results fail to provide significant evidence of butterfly effect. Serletis and Gogas (1999) test for butterfly effect in seven Mont Belview, Texas hydrocarbon markets, using monthly data from 1985:1 to 1996:12 (for the markets of ethane, propane, normal butane, iso-butane, naptha, crude oil, and natural gas) and find an evidence of butterfly effect.

Panas and Ninni (2000)investigate butterfly effect in daily price data for two major petroleum markets, namely those of Rotterdam and of Mediterranean. The sample consists of the daily prices of different oil products from 4 January 1994 to 7 August 1998, resulting in 1161 observations. All prices were collected from OPEC. The main results obtained by the authors are summarised in their Table 5. They claim to show strong evidence of butterfly effect in a number of oil products considered.

Adrangi et al. (2001) investigate the presence of butterfly effect in crude oil, heating oil, and unleaded gasoline futures prices from the early 1980s. Daily returns data from the nearby contracts are diagnosed by employing correlation dimension test, the BDS test and Kolmogrov entropy. They find strong evidence of non-linear dependence in the data, but it is not consistent with chaos.

The study performed by Panas (2001) analyzes the daily pricing for nonferrous metals (aluminium, copper, lead, tin, nickel and zinc), considering daily closing metal prices over the period from January 1989 to December 2000 (the number of observations is 2987 and the tin series begins in August, 1989) and finding evidence of “deterministic chaos only in the case of tin returns”.

Adrangi and Chatrath (2002) employ daily prices of the nearby (expiring) palladium and platinum futures contracts traded on The Commodity Exchange from November 1983 through March 1995 and January 1975 through June 1995, respectively, focusing their tests on daily returns. They find that the nonlinearity in palladium and platinum is inconsistent with chaotic behaviour.

Chatrath et al. (2002) conduct tests for the presence of low-dimensional chaotic structure in the futures prices of four agricultural commodities: soybean (from 1969 to 1995), corn (from 1969 to 1995), wheat (from 1968 to 1995), cotton (from 1972 to 1995). Even though there is strong evidence of non-linear dependence, this suggests that there is no long-lasting chaotic structure. Moshiri and Foroutan (2006) examine daily crude oil futures prices from 1983 to 2003, listed in NYMEX; their test provides negative evidence of butterfly effect. Matilla-García (2007) studies the butterfly effect nature of three energy futures series — natural gas, unleaded gasoline and light crude oil — finding evidence in futures returns.

Sakai et al. (2007) investigate piglet-pricing data in Japan, considering the monthly data for the real price and population of piglets over 1967 and 1992. An application of Lyapunov spectrum analysis to the data is carried out in order to distinguish deterministic chaos and periodic solutions. Their analysis shows that government intervention might reduce market instability by removing a chaotic market’s long-term unpredictability.

Kyrtsou et al. (2009), analyze five energy products (crude oil, gasoline, heating oil, propane, and natural gas) over the period from 1994 to mid-January 2008. They reject the null hypothesis of butterfly effect behaviour.

Barkoulas et al. (2012) consider a data set which consists of daily oil spot prices covering the period 1.2.1985 - 8.31.2011. They do not find butterfly effect tendencies in the oil market, suggesting that “oil spot prices are the measured footprint of a stochastic rather than a deterministic system” (pp. 585).

3 Concepts and implications of butterfly effect in commodity markets

Several studies show evidence of nonlinearity for various financial time series: Barnett and Serletis (2000), Franses and Van Dijk (2000), Sarantis (2001) and Zhang et al. (2001), among others.

Nonlinear dynamics may be able to explain a large set of time series behaviours. One motivation for this line of research is to determine whether the non-linearities are consistent with chaotic time paths, which have several properties that would be of special interest for commodity market observers (for instance, an apparent stochasticity of time series that could be generated by deterministic systems).

In the literature the interest in whether a prices series is chaotic has been focused on the debate, inter alia, on the worth of the forecasting/technical analysis in the very short run. In fact, a couple of decades ago, several studies showed that this (nonlinear) analysis may provide better results in predicting the price behaviour of many financial instruments. See for instance, among others: Osler and Chang (1995), Clyde and Osler (1997) and references therein. These works are a little dated and deal with financial instruments (not commodities), but are also very interesting since they link the success of technical analysis in the short time and the chaoticness of time series.

Osler and Chang (1995) examine a technical strategy that can be viewed as one of a large class of nonlinear prediction rules potentially deriving from nonlinear versions of structural models such as the monetary models, chaos models, and many others. “Many of these models have been shown to fit the data with some acceptable level of explanatory power within sample, and some appear to be helpful in forecasting conditional exchange rate variances. Nonetheless, out of sample tests of these models indicate that they generally forecast short-term exchange rate changes with little or no greater success than the random-walk model” ( Osler and Chang (1995)). Clyde and Osler (1997) simulate a “chaotic” (we would say “sensitive to initial conditions”) price series and prove that in Head-and-Shoulders trading strategies there is considerable evidence of the fact that technical analysis does work better on nonlinear data than on random data, but the frequency of “hits” (successes) employing the technical trading rule become comparable after just a few trading days (Clyde and Osler (1997) Table IV). Thus, there is evidence that short-term trading could benefit from knowing whether or not the price series are affected by butterfly effect.

Let us try to give a basic motivation in order to explain, from a purely theoretical point of view, the above empirical reasoning. Let us consider the time series and assume that there exists a system such that , , where is the initial condition at the initial time , maps the -dimensional phase space to , and maps to . The function maps an unknown (to the econometrician) dynamics that governs the evolution of the unknown (to the econometrician) state . The econometrician observes . The task is to uncover information about from observations . The time series , which we will assume as the data time series under analysis, has a chaotic explanation if is chaotic. The question is whether it is possible to forecast a chaotic series. Intuitively, the butterfly effect usually does not allow long-term forecasting of chaotic series. If we change slightly the value of the initial point: , the point at discrete time will also be changed (see Fig. 1).

What may happen is that, when time becomes large, the small initial distance grows anyway, and it may grow exponentially fast: , for some . The term represents the uncertainty induced by perturbations. Hence, fixed and , it is bounded if is bounded and so if is as small as possible ( or , for instance): this is the short-term forecasting of chaotic series, which is possible because is amplified at a finite rate . Accordingly, for chaotic time series, if one knows and could measure without error, one could perfectly forecast and, thus, in the short time (let’s say a few days when dealing with daily data).

4 Methodology and dataset

| Commodity contract | Temporal range | Number of points |

|---|---|---|

| Natural gas | 03.04.1990-15.05.2014 | 6.042 |

| Heating oil | 06.03.1979 - 15.05.2014 | 8.825 |

| Gold | 31.12.1974 - 14.05.2014 | 9.884 |

| Silver | 13.06.1963 - 15.05.2014 | 12.758 |

| Corn | 01.07.1959 -15.05.2014 | 13.817 |

| Oats | 01.07.1959 - 15.05.2014 | 13.817 |

| Cocoa | 05.01.1970 - 15.05.2014 | 11.097 |

| Coffee | 17.08.1973 -15.05.2014 | 10.194 |

| Feeder cattle | 06.09.1973- 15.05.2014 | 10.258 |

| Lean hogs | 25.06.1969 - 15.05.2014 | 11.297 |

In this paper we test for sensitive dependence on initial conditions and determinism of the following futures series: two energy series (natural gas, heating oil), two metal series (gold, silver), two grains (corn, oats), two soft commodities (cocoa, coffee) and two other agricultural commodities (feeder cattle, lean hogs) futures from the Chicago Board of Trade (CBOT), Chicago Mercantile Exchange (CME), Inter Continental Exchange (ICE), New York Mercantile Exchange (NYMEX), and its division Commodity Exchange (COMEX). The time series were obtained from http://www.quandl.com. Further information on the data set is provided in the Table 1. The series were already considered in Benedetto et al. (2015a, 2016), where the predictability of commodity market time series is investigated by predicting their entropy (for a surveys on the topic see Benedetto et al. (2015b)).

By way of the following subsections, we explain step by step the methodology of the paper.

4.1 State space reconstruction and the embedding dimension ()

Let the price of commodity at time be denoted by , then returns are measured as . A scalar time series , represents the observations from the markets examined in this paper, which can be used to reconstruct the state space (the so-called “phase space”) Packard et al. (1980). The phase space is defined as the multidimensional space whose axes consist of variables of a dynamical system. The asymptotic behaviour of the dynamical system is related to an attractor, whose dimension will provide a measure of the minimum number of independent variables able to describe the dynamical system. The state space reconstruction is the fundamental step for recovering the properties of the original attractor from a scalar time series. In this respect, it is possible to prove that an attractor, which is topologically equivalent to the scalar time series, can be reconstructed from a dynamical system of variables by using a method of time delay coordinate (Takens (1981), Ruelle (1989)). The reconstructed attractor of the original system is given by the vector sequence

| (1) |

where is an appropriate time delay, is the embedding dimension and index varying on .

Estimation of the smallest sufficient embedding dimension has been performed through the method of the false nearest-neighbours algorithm (Kennel et al. (1992)). Here, the minimum embedding dimension is such that any further increase in the dimension does not significantly increase the distance between any two neighbouring points in the trajectory. If we use the maximum norm, the statistics providing the fraction of false neighbors is Kantz and Schreiber (2004)

| (2) |

where is the threshold on the distance between two neighbouring points, is the Heaviside step function

is the closest neighbour to in dimensions, is the index of the time series element for which we have the minimum , and is a parameter such that we remove from counting all the pairs of points whose initial distance is already large (precisely larger than ). We make use of packages built for the R programming language: timeLag from package “nonlinearTseries”, which gives a criteria for estimating a proper time lag ; false.nearest from package “tseriesChaos”, which performs the method FNN to help deciding the smallest sufficient embedding dimension .

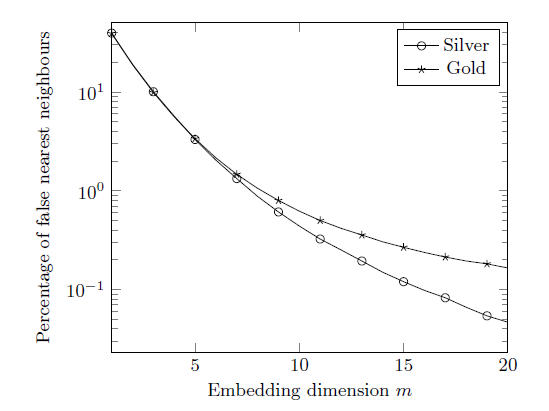

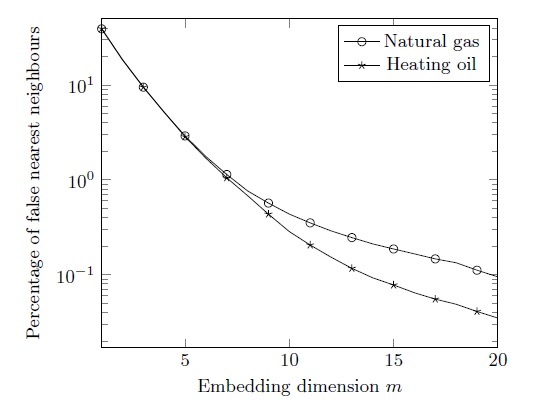

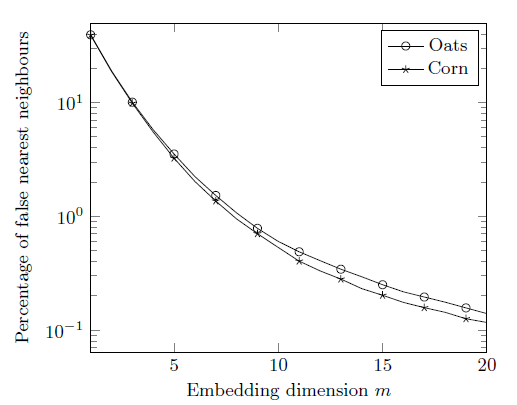

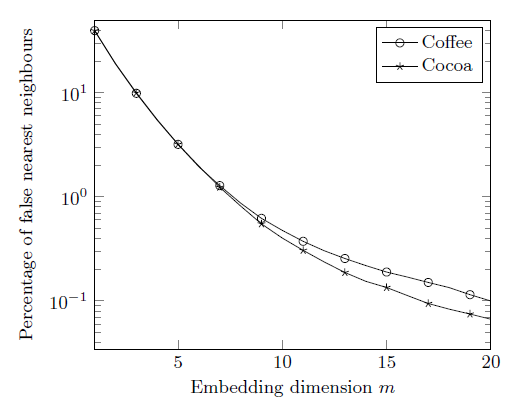

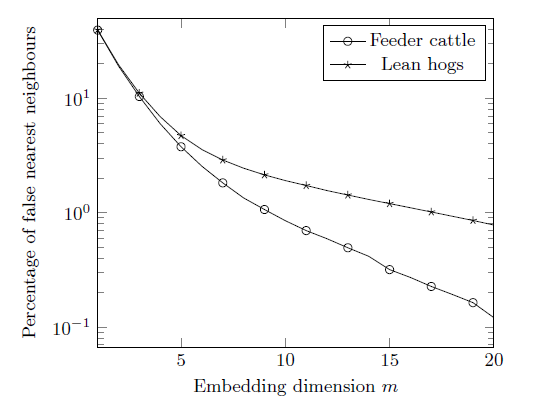

In Figure 2, Figure 3, Figure 4, Figure 5 and Figure 6 we plot the percentage of false nearest neighbours for the commodities considered in the paper, using the datasets described in Table 1. We adopt a logarithmic -scale to make the differences between the curves visible.

If we set a threshold , we use as embedding dimension the minimum value of such that . For the threshold , we get the embedding dimensions reported in Table 2.

| Commodity contract | ||

|---|---|---|

| Natural gas | 1 | 10 |

| Heating oil | 1 | 9 |

| Gold | 1 | 11 |

| Silver | 1 | 10 |

| Corn | 1 | 10 |

| Oats | 1 | 11 |

| Cocoa | 1 | 9 |

| Coffee | 1 | 10 |

| Feeder cattle | 1 | 13 |

| Lean hogs | 1 | 24 |

4.2 Maximal Lyapunov exponent

Measuring for sensitive dependence on initial conditions can be done by a mathematical operation using what are called Lyapunov Exponents. Let and be two points in state space with distance .

Denote by the distance some time ahead between the two trajectories emerging from these points, . Then, the maximal Lyapunov exponent (MLE) is determined by

| (3) |

If is positive, this means an exponential divergence of nearby trajectories, i.e. butterfly effect. Naturally, two trajectories cannot separate farther than the size of the attractor, such that (3) is only valid during times for which remains small. Otherwise, a saturation of the distance occurs and therefore (3) is violated. Due to this fact, a mathematically more rigorous definition will have to involve a first limit such that a second limit can be performed without involving saturation effects. Only in the second limit does the exponent become a well-defined and invariant quantity. For further details see Kantz and Schreiber (2004), Sec. 11.2.

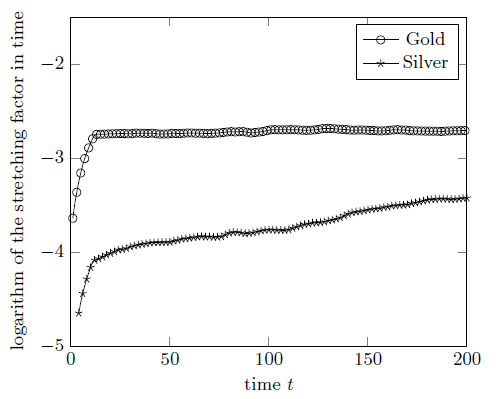

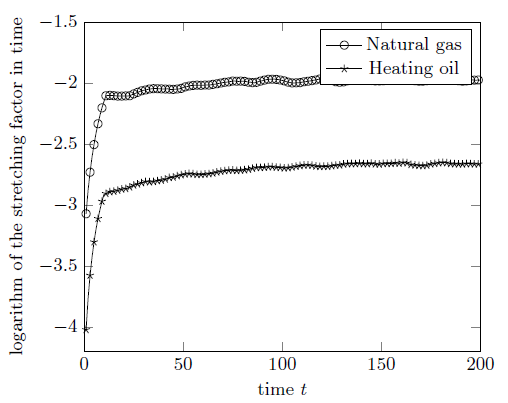

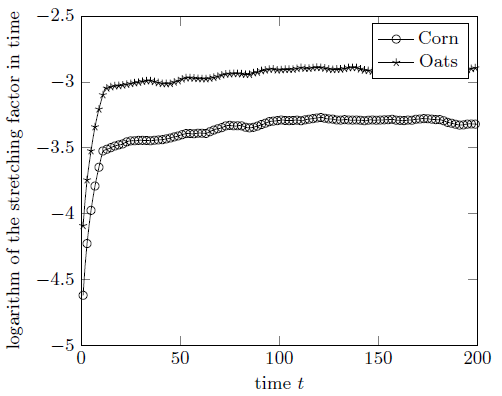

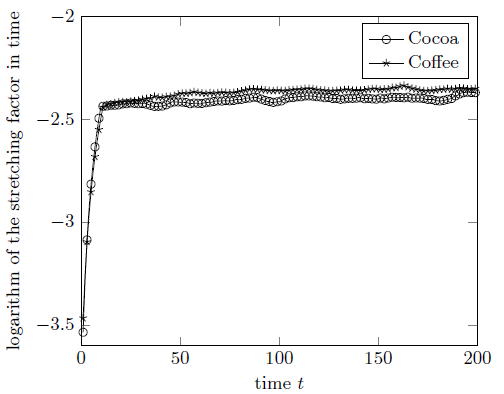

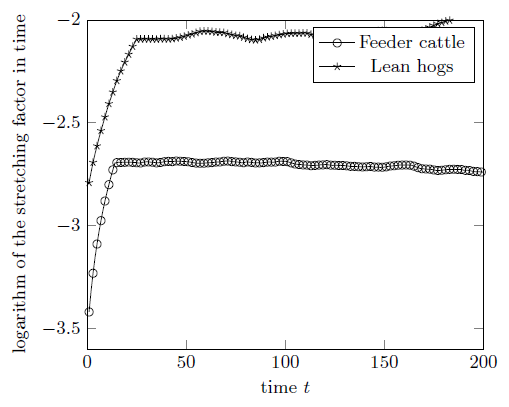

To calculate , we used the routine R lyap_k from package “tseriesChaos”, which performs the algorithm proposed in Rosenstein et al. (1993) (see also Hegger et al. (1999)). Figure 7, Figure 8, Figure 9, Figure 10 and Figure 11 depict the logarithm of the stretching factor in time for the commodities considered in the paper. For the mathematical relationship between Lyapunov exponents and stretching factors see Kantz and Schreiber (2004), p. 204. If for some temporal range the logarithm of the stretching factor exhibits a robust linear increase, its slope is an estimate of (see Kantz and Schreiber (2004), p. 70).

The empirical results obtained for maximal Lyapunov exponent of each commodity are summarised in Table 3.

| Commodity contract | |||

|---|---|---|---|

| Natural gas | 1 | 10 | 0.08548951 |

| Heating oil | 1 | 9 | 0.09728674 |

| Gold | 1 | 11 | 0.07709301 |

| Silver | 1 | 10 | 0.09018312 |

| Corn | 1 | 10 | 0.09386063 |

| Oats | 1 | 11 | 0.08979586 |

| Cocoa | 1 | 9 | 0.09346944 |

| Coffee | 1 | 10 | 0.08772418 |

| Feeder cattle | 1 | 13 | 0.05725445 |

| Lean hogs | 1 | 24 | 0.03637373 |

4.3 Determinism test

Since the commodity futures time series show an irregular random behaviour that often resembles chaos, we test the series in order to verify whether it indeed originates from a deterministic system. For this purpose, we employ the determinism test introduced by Kaplan and Glass (1992), using a package developed in Kodba et al. (2004).

The test is based on the reconstruction of the state space from the observed variable. To construct an approximate vector field of the system, the phase space is covered by equally sized boxes with the same dimension as the reconstructed space. To each box, the average direction of the trajectory through the box during a particular pass is estimated. Each pass of the trajectory through the -th box generates a unit vector, and the approximation for the vector field in the -th box of the phase space is defined as the average vector of all passes. In Kaplan and Glass (1992), is defined as weighted average of with respect to the average displacement per step, , of a random walk. In this way, the determinism coefficient is equal to 1 for a deterministic system, while for a random walk. Then, for the intermediate cases, measures the distance of time series from a deterministic system and from a stochastic process. The idea is to take the determinism coefficient , obtained by Kaplan and Glass’ test, as a measure of the reliability level (in percentage) of the test on sensitive dependence on initial conditions. Actually, it is known that time series generated from stochastic systems also may show positive MLE Tanaka et al. (1996), Ikeguchi and Aihara (1997), Tanaka et al. (1998).

We use a package written in code, which can be downloaded from M. Perc’s Web page 111M. Perc Web Page, http://www.matjazperc.com/ejp/time.html., as described in Kodba et al. (2004).

| Commodity contract | ||

|---|---|---|

| Natural gas | 1 | 0.913584 |

| Heating oil | 1 | 0.881473 |

| Gold | 1 | 0.891292 |

| Silver | 1 | 0.905958 |

| Corn | 1 | 0.904227 |

| Oats | 1 | 0.915515 |

| Cocoa | 1 | 0.808978 |

| Coffee | 1 | 0.904908 |

| Feeder cattle | 1 | 0.904252 |

| Lean hogs | 1 | 0.932926 |

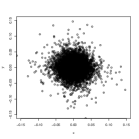

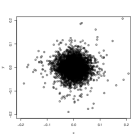

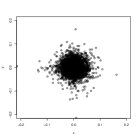

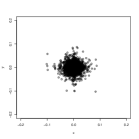

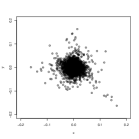

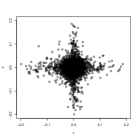

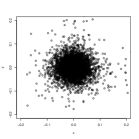

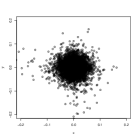

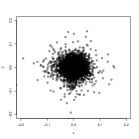

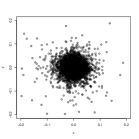

The results of the determinism test for the embedding space presented in Figure 12 and Figure 13 are shown in Table 4. For this calculation the multidimensional embedding space was coarse grained into a grid. In Table 4, is near to for all commodity futures series. So, the deterministic signature is still good enough to be preserved, so that the chaotic appearance of the reconstructed attractor cannot be attributed to stochastic influences.

See Figure 12 and Figure 13. When we look only at the data, we think it were coming out of a black box. If the coming was regular, the graph would be suitably dull: every point would land at the same place. The graph would be a single dot (or almost). But the commodity futures series are, in general, subject to noise and here sensitive to initial conditions (Table 3). As we sayed, it is not a predictable pattern beyond a short time. So instead of the single dot, we will see in Figure 12 and Figure 13 a slightly fuzzy blob. If it were truly random, points would be scattered all over the graph. There would be no relation to be found between one interval and the next. But if a strange attractor were hidden in the data, it might reveal itself as a coalescence of fuzziness into distinguishable structures.

5 A comparison with related results

In this paper we have adopted an approach which can be schematized in the following points: 1) reconstruction of the phase space, where we estimated the smallest sufficient embedding dimension using the FNN algorithm. Moreover, on the basis of the parameters of previous point: 2) we have tested for sensitive dependence on initial conditions using Lyapunov Exponents; 3) we have estimated the determinism coefficient of each time series.

Between the references considered here, the estimation of smallest sufficient embedding dimension is performed by methods for determining it only in Matilla-García (2007), Sakai et al. (2007), Barkoulas et al. (2012). Other references considered arbitrarily varying on a certain range (for example, in Kyrtsou et al. (2009) and in Chwee (1998)), but a similar approach does not allow to select an appropriate value for . In fact, as explained in Packard et al. (1980); Takens (1981); Kennel et al. (1992); Ruelle (1989), the FNN procedure identifies the number of “false nearest neighbors”, points that appear to be nearest neighbours because the embedding space is too small, of every point on the attractor associated with the set , as defined in (1). When the number of false nearest neighbors drops to zero, we have unfolded or embedded the attractor in -dimensional Euclidian space. If we chose , i.e. a dimension less than the appropriate embedding dimension , we are viewing the attractor in too small an embedding space and an estimation of the MLE for an embedding dimension might yield misleading results about the sensitive dependence on initial conditions of the analyzed time series. The same conclusion might occurs in the case . In fact, from a mathematical point of view of the embedding process it does not matter whether one uses the minimum embedding dimension or any , since once the attractor is unfolded, the theory’s work (see Takens (1981)) is done. But, in more relatable terms, working in any dimension larger than the minimum required by the data leads to the problem of contamination by roundoff or instrumental error since this “noise” will affect the additional dimensions of the embedding space where no dynamics is operating Kennel et al. (1992).

Even if the results obtained with the MLE indicate the presence of butterfly effect (Table 3), it is anyway important to compare the reliability of the results obtained about sensitive dependence on initial conditions. As we already said, some stochastic systems may show sensitive dependence on initial conditions (Tanaka et al. (1996), Ikeguchi and Aihara (1997), Tanaka et al. (1998)); thus we propose to assume the results concerning the determinism coefficient as the reliability level (in percentage) of the MLE.

Some papers (Lai (2016), Matilla-García (2007), Panas (2001), Panas and Ninni (2000), Sakai et al. (2007), Serletis and Gogas (1999)) claim to have discovered the evidence of butterfly effect. Lai (2016) uses the BDS test and estimates the correlation dimension employing Grassberger-Procaccia method. Panas and Ninni (2000) and Panas (2001) employ the BDS test and estimate the Kolmogorov entropy, the correlation dimension and the MLE. Serletis and Gogas (1999) work in order to obtain stationary and appropriately filtered data, removing any linear as well as nonlinear stochastic dependence, and then estimate the MLE. Although these studies investigate the presence of both stochastic and determinist components in time series, they do not provide any estimate of the determinism rate existing in the analyzed data. On the other hand, among the cited references, Matilla-García (2007) and Sakai et al. (2007) come closest to the approach followed in this paper. They both build upon a test on determinism of the analyzed time series.

Matilla-García employs a test developed by Kaplan (1994), which introduces a coefficient . The nonzero value of is interpreted as the level of nondeterminism in the data. However, a range is not very specific. For instance, it does not detects the level of determinism in the analyzed time series, it only assesses its order when compared with others.

The work of Sakai et al. (2007) is the only one that uses a deterministic test as we do here. Their deterministic investigation is based on the test developed by Wayland et al. (1993). In this test, the quantity that provides information about the determinism of the time series is the median translation error. If this error is close to 0, then the time series is the result of a deterministic process; if the median translation error is close to 1, then the time series is the result of a stochastic process. In Sakai et al. (2007), the translation error is very close to , which suggests a very high level of determinism in the time series.

The presence of butterfly effect in commodity futures markets is a controversial matter, as can be deduced from the literature reviewed in Section 2: some papers claim they have detected the presence of chaos (butterfly effect), while others state the opposite. Let us now compare our results with those of others, with regards to the futures time series we have presently analyzed.

Kyrtsou et al. (2009) have evaluated natural gas and heating oil, over the period from 1994 to mid-January 2008, showing that Lyapunov exponent estimates are negative. They also show the existence of a structure that is partially deterministic. In our paper, even if we have considered different commodities or different kind of series (futures or spot prices), the futures time series show a considerable contribute of determinism ( near to for all the commodities), which differs from the observation of the partial determinism of the structure enlightened by Kyrtsou et al. (2009). Moreover, in the case of natural gas and heating oil, the MLE that we have detected are positive, while those estimated by Kyrtsou et al. (2009) are negative: these two approaches give different results on Lyapunov exponent. However, we point out that: 1) the approach followed by Kyrtsou et al. (2009) is different from that employed here and, in fact, they test for chaos by applying methods based on neural networks; 2) the time series do not match because they use daily spot prices, provided by www.barchart.com; 3) the sample periods are different, because Kyrtsou et al. (2009) consider the period by 3.1.1994 to 25.1.2008 while we have examined the ranges 06.03.1979 - 15.05.2014 for heating oil and 03.04.1990 - 15.05.2014 for natural gas. A comparison of these two approaches and a new set of measures conducted on the same temporal range could be a useful exercise for next work.

As for heating oil, Adrangi et al. (2001), for observations on the range 1/02/85 - 03/31/95, employ correlation dimension test, the BDS test and Kolmogrov entropy, without finding evidence of butterfly effect.

Matilla-García (2007) uses observations of natural gas futures princes, starting from 04/03/1990 to 10/19/2005. He discovers the positivity of the MLE, wheras for the same energy commodity Chwee (1998), examining observations from April 1990 to September 1996, shows no evidence of butterfly effect from the estimation of the Lyapunov spectra. The results on the positivity of MLE obtained by Matilla-García (2007) are in accordance with ours. This is not surprising, since Matilla-García employs the same method (by Rosenstein et al. (1993)) used here.

As for natural gas Serletis and Gogas (1999) examining monthly data from 1985:2 to 1996:12, “test for positivity of the dominant Lyapunov exponent. Before conducting such a nonlinear analysis, the data were rendered stationary and appropriately filtered, in order to remove any linear as well as nonlinear stochastic dependence”. They find evidence of butterfly effect in all natural gas liquids markets. Differently from their paper, we do not apply any filtering to data.

As for corn, Chatrath, et al. Chatrath et al. (2002) examine data from 11 December 1969 to 30 March 1995. They employ three tests: the correlation dimension, the BDS statistic and a measure of Kolmogorov entropy. These methods reveal that there is no consistent evidence of low dimension chaos in commodity futures prices.

We recall that all the papers cited (Adrangi and Chatrath (2002), Adrangi et al. (2001), Barkoulas et al. (2012), Chatrath et al. (2002), Chwee (1998), Kyrtsou et al. (2009), Lai (2016), Matilla-García (2007), Moshiri and Foroutan (2006), Panas (2001), Panas and Ninni (2000), Sakai et al. (2007), Serletis and Gogas (1999)) investigate the “experimental” definition of chaos. Among them, Lai (2016), Matilla-García (2007), Panas (2001), Panas and Ninni (2000), Sakai et al. (2007), Serletis and Gogas (1999) claim to have discovered the evidence of “chaos” but this term is abused: all the authors cited above investigate the butterfly effect, that is only one of the properties of a chaotic system (see Definition of chaos in Devaney (1989)). It is not a negligible particular. As they rightly say, “the theory is practice”, to mean that the effectiveness of a theory is based on its ability to generate a knowledge of phenomena so accurate as to allow the formulation of reliable forecasts. This also means that an insufficient regard to theoretical aspects might yield results that are not reliable. The contrasting results about the presence of butterfly effect in commodity futures markets may be generated, for example, by this misunderstanding.

For a deeper discussion of the mathematical aspects of the chaos definition we talked about here, see Mastroeni and Vellucci (2016).

6 Conclusions

We have reviewed and analysed the presence of butterfly effect for several commodities markets. In particular, we focused on the following commodity futures series: two energy series (natural gas, heating oil), two metal series (gold, silver), two grains (corn, oats), two soft commodities (cocoa, coffee) and two other agricultural commodities (feeder cattle, lean hogs) futures from the Chicago Board of Trade (CBOT), Chicago Mercantile Exchange (CME), Inter Continental Exchange (ICE), New York Mercantile Exchange (NYMEX), and its division Commodity Exchange (COMEX). The empirical results obtained in the above analysis are summarised in Tables 2, 3, 4.

We used the Lyapunov Exponents and a determinism test, both based on the reconstruction of the phase space. In particular, we employed a coefficient that describes the determinism rate of the analyzed time series. The coefficient represents, in percentage, the reliability level about the test on the sensitive dependence on initial conditions. The introduction of this reliability level is motivated by the fact that time series generated from stochastic systems might show sensitive dependence on initial conditions. The coefficient has been introduced by Kaplan and Glass (1992), and we employ here a recent methodology developed by Kodba et al. (2004).

In our work, the reliability level yields results near to while the MLE is positive for all commodity futures series. This means that the latter show a considerable contribution of determinism. In this way, we can ensure the presence of butterfly effect (that is one of the properties of a chaotic system, according to Devaney (1989)) in the commodity futures markets considered in the paper.

The results of the empirical treatments that we present here are, of course, subject to several interpretations.

The magnitudes of the Lyapunov exponents quantify a system’s dynamics in information theoretical terms. The exponents represent the rate at which the system creates or distorts information (Shaw (1981)). For this purpose, let us consider a unit measuring error in all the commodity futures series, and consider, as an instance, oats and corn commodities since they share the same temporal range of observation. Denote, respectively, with and their MLEs, then the error in the corn series has been amplified times faster than in the oats series.

The role of information in the markets, as we know, is of paramount importance. Let us think of the formalization proposed by Malkiel and Fama (1970), Fama (1998). The central issue is whether or not to adopt trading strategies that achieve excess returns relative to the market, based on information contained in the historical data. Currently, the empirical evidence would seem to indicate that markets are often not efficient, even in weak form. The perception of a trend as seemingly stochastic could be due to the lack of knowledge of the information underlying it.

In other words, for the commodities considered in this paper the empirical analysis suggests that there are several deterministic forces interacting with each other. The presence of a chaotic dynamics could be connected to the existence of several deterministic forces that may result in complex price movements in financial markets. Today, the complexity of financial and commodities markets is very high because world decisions in business, finance and economics are influenced by sociologic, environmental, and geopolitical factors. In this regard, Panas and Ninni Panas and Ninni (2000) write in their conclusions: “An energy economist who is interested in the dynamic behaviour of the complex system that governs the oil markets needs to know how sensitive the system is to initial conditions, and to achieve this he needs to estimate the Lyapunov exponents”.

Thanks to recent methodologies (e.g. package developed by Kodba et al. (2004)), we prove that this is agreeable also in other commodity and energy markets, but it is useful to spell out the conditions under which that is possible. We can add that an economist interested in complex system dynamic behaviour needs to know how deterministic the system is as well as how sensitive it is to initial conditions. That is why he needs to estimate the determinism coefficient and the MLE.

Acknowledgements

The authors thank Prof. Matjaz̆ Perc for the C++ code of the package developed in Kodba et al. (2004).

References

References

- Adrangi and Chatrath (2002) Adrangi, Bahram and Arjun Chatrath (2002), “The dynamics of palladium and platinum prices.” Comput. Econ., 19, 179–195.

- Adrangi et al. (2001) Adrangi, Bahram, Arjun Chatrath, Kanwalroop Kathy Dhanda, and Kambiz Raffiee (2001), “Chaos in oil prices? Evidence from futures markets.” Energ. Econ., 23, 405–425.

- Barkoulas et al. (2012) Barkoulas, John T, Atreya Chakraborty, and Arav Ouandlous (2012), “A metric and topological analysis of determinism in the crude oil spot market.” Energ. Econ., 34, 584–591.

- Barnett and Serletis (2000) Barnett, William A and Apostolos Serletis (2000), “Martingales, nonlinearity, and chaos.” J. Econ. Dyn. Control, 24, 703–724.

- Benedetto et al. (2015a) Benedetto, F, G Giunta, and L Mastroeni (2015a), “A maximum entropy method to assess the predictability of financial and commodity prices.” Digit. Signal Process., 46, 19–31.

- Benedetto et al. (2015b) Benedetto, F, G Giunta, and L Mastroeni (2015b), “Signal processing for financial markets.” In Encyclopedia of Information Science and Technology, Third Edition, 7339–7346, IGI Global.

- Benedetto et al. (2016) Benedetto, F, G Giunta, and L Mastroeni (2016), “On the predictability of energy commodity markets by an entropy-based computational method.” Energ. Econ., 54, 302–312.

- Chatrath et al. (2002) Chatrath, Arjun, Bahram Adrangi, and Kanwalroop Kathy Dhanda (2002), “Are commodity prices chaotic?” Agr. Econ., 27, 123–137.

- Chwee (1998) Chwee, Victor (1998), “Chaos in natural gas futures?” Energy J., 19, 149–164.

- Clyde and Osler (1997) Clyde, William C and Carol L Osler (1997), “Charting: Chaos theory in disguise?” J. Futures Markets, 17, 489–514.

- Devaney (1989) Devaney, Robert L (1989), An introduction to chaotic dynamical systems, volume 13046. Addison-Wesley Reading.

- Fama (1998) Fama, Eugene F. (1998), “Market efficiency, long-term returns, and behavioral finance1.” Journal of Financial Economics, 49, 283 – 306.

- Farmer (1982) Farmer, J Doyne (1982), “Chaotic attractors of an infinite-dimensional dynamical system.” Physica D, 4, 366–393.

- Franses and Van Dijk (2000) Franses, Philip Hans and Dick Van Dijk (2000), Non-linear time series models in empirical finance. Cambridge University Press.

- Grassberger and Procaccia (1983) Grassberger, Peter and Itamar Procaccia (1983), “Estimation of the Kolmogorov entropy from a chaotic signal.” Phys. Rev. A, 28, 2591.

- Hegger et al. (1999) Hegger, Rainer, Holger Kantz, and Thomas Schreiber (1999), “Practical implementation of nonlinear time series methods: The tisean package.” Chaos: An Interdisciplinary Journal of Nonlinear Science, 9, 413–435.

- Ikeguchi and Aihara (1997) Ikeguchi, Tohru and Kazuyuki Aihara (1997), “Lyapunov spectral analysis on random data.” Int. J. Bifurcat. Chaos, 7, 1267–1282.

- Kantz and Schreiber (2004) Kantz, Holger and Thomas Schreiber (2004), Nonlinear time series analysis, volume 7. Cambridge University Press.

- Kaplan (1994) Kaplan, Daniel T. (1994), “Exceptional events as evidence for determinism.” Physica D, 73, 38 – 48.

- Kaplan and Glass (1992) Kaplan, Daniel T and Leon Glass (1992), “Direct test for determinism in a time series.” Phys. Rev. Lett., 68, 427.

- Kennel et al. (1992) Kennel, Matthew B., Reggie Brown, and Henry D. I. Abarbanel (1992), “Determining embedding dimension for phase-space reconstruction using a geometrical construction.” Phys. Rev. A, 45, 3403–3411.

- Kodba et al. (2004) Kodba, Stane, Matjaž Perc, and Marko Marhl (2004), “Detecting chaos from a time series.” Eur. J. Phys., 26, 205.

- Kolmogorov (1958) Kolmogorov, Andrei Nikolaevich (1958), “A new metric invariant of transient dynamical systems and automorphisms in Lebesgue spaces.” In Dokl. Akad. Nauk SSSR (NS), volume 119, 861–864.

- Kyrtsou et al. (2009) Kyrtsou, Catherine, Anastasios G Malliaris, and Apostolos Serletis (2009), “Energy sector pricing: On the role of neglected nonlinearity.” Energ. Econ., 31, 492–502.

- Lai (2016) Lai, Li-Hua (2016), “Dynamic modelling in loss frequency and severity estimated: Evidence from the agricultural rice loss due to typhoons in taiwan.” Agr. Econ., 62, 113–123.

- Malkiel and Fama (1970) Malkiel, Burton G and Eugene F Fama (1970), “Efficient capital markets: A review of theory and empirical work.” The journal of Finance, 25, 383–417.

- Mastroeni and Vellucci (2016) Mastroeni, Loretta and Pierluigi Vellucci (2016), ““Butterfly effect” vs chaos in energy futures markets, working paper n. 209, Department of Economics, Roma Tre University, issn 2279-6916.”

- Matilla-García (2007) Matilla-García, Mariano (2007), “Nonlinear dynamics in energy futures.” Energy J., 28, 7–29.

- Moshiri and Foroutan (2006) Moshiri, Saeed and Faezeh Foroutan (2006), “Forecasting nonlinear crude oil futures prices.” Energy J., 27, 81–95.

- Osler and Chang (1995) Osler, Carol L and PH Chang (1995), “Head and shoulders: Not just a flaky pattern.” FRB of New York staff report.

- Ott (2002) Ott, Edward (2002), Chaos in dynamical systems. Cambridge university press.

- Packard et al. (1980) Packard, Norman H, James P Crutchfield, J Doyne Farmer, and Robert S Shaw (1980), “Geometry from a time series.” Phys. Rev. Lett., 45, 712.

- Panas (2001) Panas, E (2001), “Long memory and chaotic models of prices on the London Metal Exchange.” Resour. Policy, 27, 235–246.

- Panas and Ninni (2000) Panas, Epaminondas and Vassilia Ninni (2000), “Are oil markets chaotic? A non-linear dynamic analysis.” Energ. Econ., 22, 549–568.

- Rosenstein et al. (1993) Rosenstein, Michael T, James J Collins, and Carlo J De Luca (1993), “A practical method for calculating largest Lyapunov exponents from small data sets.” Physica D, 65, 117–134.

- Ruelle (1989) Ruelle, David (1989), Chaotic evolution and strange attractors, volume 1. Cambridge University Press.

- Sakai et al. (2007) Sakai, Kenshi, Shunsuke Managi, Nikolay K Vitanov, and Katsuhiko Demura (2007), “Transition of chaotic motion to a limit cycle by intervention of economic policy: an empirical analysis in agriculture.” Nonlinear dynamics, psychology, and life sciences, 11, 253–265.

- Sarantis (2001) Sarantis, Nicholas (2001), “Nonlinearities, cyclical behaviour and predictability in stock markets: international evidence.” Int. J. Forecasting, 17, 459–482.

- Schuster and Just (2006) Schuster, Heinz Georg and Wolfram Just (2006), Deterministic chaos: an introduction. John Wiley & Sons.

- Serletis and Gogas (1999) Serletis, Apostolos and Periklis Gogas (1999), “The north american natural gas liquids markets are chaotic.” Energy J., 20, 83–103.

- Shaw (1981) Shaw, Robert (1981), “Strange attractors, chaotic behavior, and information flow.” Zeitschrift für Naturforschung A, 36, 80–112.

- Strogatz (2014) Strogatz, Steven H (2014), Nonlinear dynamics and chaos: with applications to physics, biology, chemistry, and engineering. Westview press.

- Takens (1981) Takens, Floris (1981), “Detecting strange attractors in turbulence.” In Dynamical Systems and Turbulence, Warwick 1980, 366–381, Springer.

- Tanaka et al. (1996) Tanaka, Toshiyuki, Kazuyuki Aihara, and Masao Taki (1996), “Lyapunov exponents of random time series.” Phys. Rev. E, 54, 2122.

- Tanaka et al. (1998) Tanaka, Toshiyuki, Kazuyuki Aihara, and Masao Taki (1998), “Analysis of positive Lyapunov exponents from random time series.” Physica D, 111, 42–50.

- Wayland et al. (1993) Wayland, Richard, David Bromley, Douglas Pickett, and Anthony Passamante (1993), “Recognizing determinism in a time series.” Phys. Rev. Lett., 70, 580.

- Zhang et al. (2001) Zhang, Michael Yuanjie, Jeffrey R Russell, and Ruey S Tsay (2001), “A nonlinear autoregressive conditional duration model with applications to financial transaction data.” J. Econometrics, 104, 179–207.