Simple Mechanisms for Subadditive Buyers via Duality

Yang Cai

Department of Computer Science

Yale University

yang.cai@yale.edu

Mingfei Zhao

School of Computer Science

McGill University

mingfei.zhao@mail.mcgill.ca

Abstract

We provide simple and approximately revenue-optimal mechanisms in the multi-item multi-bidder settings. We unify and improve all previous results, as well as generalize the results to broader cases. In particular, we prove that the better of the following two simple, deterministic and Dominant Strategy Incentive Compatible mechanisms, a sequential posted price mechanism or an anonymous sequential posted price mechanism with entry fee, achieves a constant fraction of the optimal revenue among all randomized, Bayesian Incentive Compatible mechanisms, when buyers’ valuations are XOS over independent items. If the buyers’ valuations are subadditive over independent items, the approximation factor degrades to , where is the number of items. We obtain our results by first extending the Cai-Devanur-Weinberg duality framework

to derive an effective benchmark of the optimal revenue for subadditive bidders, and then analyzing this upper bound with new techniques.

1 Introduction

In Mechanism Design, we aim to design a mechanism/system such that a group of strategic participants, who are only interested in optimizing their own utilities, are incentivized to choose actions that also help achieve the designer’s objective. Clearly, the quality of the solution with respect to the designer’s objective is crucial. However, perhaps one should also pay equal attention to another criterion of a mechanism, that is, its simplicity. When facing a complicated mechanism, participants may be confused by the rules and thus unable to optimize their actions and react in unpredictable ways instead. This may lead to undesirable outcomes and poor performance of the mechanism. An ideal mechanism would be optimal and simple. However, such cases of simple mechanisms being optimal only exist in single-item auctions, with the seminal examples of auctions by Vickrey [45] and Myerson [38], while none has been discovered in broader settings. Indeed, we now know that even in fairly simple settings the optimal mechanisms suffer many undesirable properties including randomization, non-monotonicity, and others [40, 44, 39, 32, 33, 4, 18, 19]. To move forward, one has to compromise – either settle with optimal but somewhat complex mechanisms or turn to simple but approximately optimal solutions.

Recently, there has been extensive research effort focusing on the latter approach, that is, studying the performance of simple mechanisms through the lens of approximation. In particular, a central problem on this front is how to design simple and approximately revenue-optimal mechanisms in multi-item settings. For instance, when bidders have unit-demand valuations, we know sequential posted price mechanisms approximates the optimal revenue due to a line of work initiated by Chawla et al. [13, 14, 16, 10]. When buyers have additive valuations, we know that either selling the items separately or running a VCG mechanism with per bidder entry fee approximates the optimal revenue due to a series of work initiated by Hart and Nisan [31, 11, 36, 1, 46, 10]. Recently, Chawla and Miller [17] generalized the two lines of work described above to matroid rank functions111Here is a hierarchy of the valuation functions. additive & unit-demand matroid rank constrained additive & submodular

XOS subadditive. A function is constrained additive if it is additive up to some downward closed feasibility constraints. The class of submodular functions is neither a superset nor a subset of the class of constrained additive functions. See Definition 2 for the formal definition. . They show that a simple mechanism, the sequential two-part tariff mechanism, suffices to extract a constant fraction of the optimal revenue. For subadditive valuations beyond matroid rank functions, we only know how to handle a single buyer [41]222All results mentioned above assume that the buyers’ valuation distributions are over independent items. For additive and unit-demand valuations, this means a bidder’s values for the items are independent. The definition is generalized to subadditive valuations by Rubinstein and Weinberg [41]. See Definition 1.. It is a major open problem to extend this result to multiple subadditive buyers.

In this paper, we unify and strengthen all the results mentioned above via an extension of the duality framework proposed by Cai et al. [10]. Moreover, we show that even when there are multiple buyers with XOS valuation functions, there exists a simple, deterministic and Dominant Strategy Incentive Compatible (DSIC) mechanism that achieves a constant fraction of the optimal Bayesian Incentive Compatible (BIC) revenue333A mechanism is Bayesian Incentive Compatible (BIC) if it is in every bidder’s interest to tell the truth, assuming that all other bidders’ reported their values. A mechanism is Dominant Strategy Incentive Compatible (DSIC) if it is in every bidder’s interest to tell the truth no matter what reports the other bidders make.. For subadditive valuations, our approximation ratio degrades to .

Informal Theorem 1.

There exists a simple, deterministic and DSIC mechanism that achieves a constant fraction of the optimal BIC revenue in multi-item settings, when the buyers’ valuation distributions are XOS over independent items. When the buyers’ valuation distributions are subadditive over independent items, our mechanism achieves at least of the optimal BIC revenue, where is the number of items.

The original paper by Cai et al. [10] provided a unified treatment for additive and unit-demand valuations. However, it is inadequate to provide an analyzable benchmark for even a single subadditive bidder. In this paper, we show how to extend their duality framework to accommodate general subadditive valuations. Using this extended framework, we substantially improve the approximation ratios for many of the settings discussed above, and in the meantime generalize the results to broader cases. See Table 1 for the comparison between the best ratios reported in the literature and the new ratios obtained in this work.

* The result is implied by another result for a more general setting.

Table 1: Comparison of approximation ratios between previous and current work.

Our mechanism is either a rationed sequential posted price mechanism (RSPM) or an anonymous sequential posted price with entry fee mechanism (ASPE). In an RSPM, there is a price for buyer if she wants to buy item , and she is allowed to purchase at most one item. We visit the buyers in some arbitrary order and the buyer takes her favorite item among the available items given the item prices for her. Here we allow personalized prices, that is, could be different from if . In an ASPE, every buyer faces the same collection of item prices . Again, we visit the buyers in some arbitrary order. For each buyer, we show her the available items and the associated price for each item. Then we ask her to pay the entry fee to enter the mechanism, which may depend on what items are still available and the identity of the buyer. If the buyer accepts the entry fee, she can proceed to purchase any item at the given prices; if she rejects the entry fee, then she will leave the mechanism without receiving anything. Given the entry fee and item prices, the decision making for the buyer is straightforward, as she only accepts the entry fee when the surplus for winning her favorite bundle is larger than the entry fee. Therefore, both RSPM and ASPE are DSIC and ex-post Individually Rational (ex-post IR).

1.1 Our Contributions

To obtain the new generalizations, we provide important extensions to the duality framework in [10], as well as novel analytic techniques and new simple mechanisms.

1. Accommodating subadditive valuations: the original duality framework in [10] already unified the additive case and unit-demand case by providing an approximately tight upper bound for the optimal revenue using a single dual solution. A trivial upper bound for the revenue is the social welfare, which may be arbitrarily bad in the worst case. The duality based upper bound in [10] improves this trivial upper bound, the social welfare, by substituting the value of each buyer’s favorite item with the corresponding Myerson’s virtual value. However, the substitution is viable only when the following condition holds – the buyer’s marginal gain for adding an item solely depends on her value for that item (assuming it’s feasible to add that item444WLOG, we can reduce any constrained additive valuation to an additive valuation with a feasibility constraint (see Definition 2)), but not the set of items she has already received. This applies to valuations that are additive, unit-demand and more generally constrained additive, but breaks under more general valuation functions, e.g., submodular, XOS or subadditive valuations. As a consequence, the original dual solution from [10] fails to provide a nice upper bound for more general valuations. To overcome this difficulty, we take a different approach. Instead of directly studying the dual of the original problem, we first relax the valuations and argue that the optimal revenue of the relaxed valuation is comparable to the original one. Then, since we choose the relaxation in a particular way, by applying a dual solution similar to the one in [10] to the relaxed valuation, we recover an upper bound of the optimal revenue for the relaxed valuation resembling the appealing format of the one in [10]. Combining these two steps, we obtain an upper bound for subadditive valuations that is easy to analyze. Indeed, we use our new upper bound to improve the approximation ratio for a single subadditive buyer from [41] to . See Section 5.1 for more details.

2. An adaptive dual: our second major change to the framework is that we choose the dual in an adaptive manner. In [10], a dual solution is chosen up front inducing a virtual value function , then the corresponding optimal virtual welfare is used as a benchmark for the optimal revenue. Finally, it is shown that the revenue of some simple mechanism is within a constant factor of the optimal virtual welfare. Unfortunately, when the valuations are beyond additive and unit-demand, the optimal virtual welfare for this particular choice of virtual value function becomes extremely complex and hard to analyze. Indeed, it is already challenging to bound when the buyers’ valuations are -demand. In this paper, we take a more flexible approach. For any particular allocation rule , we tailor a special dual based on in a fashion that is inspired by Chawla and Miller’s ex-ante relaxation [17]. Therefore, the induced virtual valuation also depends on . By duality, we can show that the optimal revenue obtainable by is still upper bounded by the virtual welfare with respect to under allocation rule . Since the virtual valuation is designed specifically for allocation , the induced virtual welfare is much easier to analyze. Indeed, we manage to prove that for any allocation the induced virtual welfare is within a constant factor of the revenue of some simple mechanism, when bidders have XOS valuations. See Section 5.2 and 5.3 for more details.

3. A novel analysis and new mechanism: with the two contributions above, we manage to derive an upper bound of the optimal revenue similar to the one in [10] but for subadditive bidders. The third major contribution of this paper is a novel approach to analyzing this upper bound. The analysis in [10] essentially breaks the upper bound into three different terms– Single, Tail and Core, and bound them separately. All three terms are relatively simple to bound for additive and unit-demand buyers, but for more general settings the Core becomes much more challenging to handle. Indeed, the analysis in [10] was insufficient to tackle the Core even when the buyers have -demand valuations555The class of -demand valuations is a generalization of unit-demand valuations, where the buyer’s value is additive up to items.– a very special case of matroid rank valuations, which itself is a special case of XOS or subadditive valuations. Rubinstein and Weinberg [41] showed how to approximate the Core for a single subadditive bidder using grand bundling, but their approach does not apply to multiple bidders. Yao [46] showed how to approximate the Core for multiple additive bidders using a VCG with per bidder entry fee mechanism, but again it is unclear how his approach can be extended to multiple k-demand bidders. A recent paper by Chawla and Miller [17] finally broke the barrier of analyzing the Core for multiple -demand buyers. They showed how to bound the Core for matroid rank valuations using a sequential posted price mechanism by applying the online contention resolution scheme (OCRS) developed by Feldman et al. [26]. The connection with OCRS is an elegant observation, and one might hope the same technique applies to more general valuations. Unfortunately, OCRS is only known to exist for special cases of downward closed constraints, and as we show in Section 7.2.1, the approach by Chawla and Miller cannot yield any constant factor approximation for general constrained additive valuations.

We take an entirely different approach to bound the Core. Here we provide some intuition behind our mechanism and analysis. The Core is essentially the optimal social welfare induced by some truncated valuation , and our goal is to design a mechanism that extracts a constant fraction of the welfare as revenue. Let be any sequential posted price mechanism. A key observation is that when bidder ’s valuation is subadditive over independent items, her utility in , which is the largest surplus she can achieve from the unsold items, is also subadditive over independent items. If we can argue that her utility function is -Lipschitz (Definition 6) with some small , Talagrand’s concentration inequality [43, 42] allows us to set an entry fee for the bidder so that we can extract a constant fraction of her utility just through the entry fee. If we modify by introducing an entry fee for every bidder, according to Talagrand’s concentration inequality, the new mechanism should intuitively have revenue that is a constant fraction of the social welfare obtained by 666’s welfare is simply its revenue plus the sum of utilities of the bidders, and can extract some extra revenue from the entry fee, which is a constant fraction of the total utility from the bidders.. Therefore, if there exists a sequential posted price mechanism that achieves a constant fraction of the optimal social welfare under the truncated valuation , the modified mechanism can obtain a constant fraction of Core as revenue. Surprisingly, when the bidders have XOS valuations, Feldman et al. [25] showed that there exists an anonymous sequential posted price mechanism that always obtains at least half of the optimal social welfare. Hence, an anonymous sequential posted price with per bidder entry fee mechanism should approximate the Core well, and this is exactly the intuition behind our ASPE mechanism.

To turn the intuition into a theorem, there are two technical difficulties that we need to address: (i) the Lipschitz constants of the bidders’ utility functions turn out to be too large (ii) we deliberately neglected the difference in bidders’ behavior under and in hope to keep our discussion in the previous paragraph intuitive. However, due to the entry fee, bidders may end up purchasing completely different items under and , so it is not straightforward to see how one can relate the revenue of to the welfare obtained by . See Section 7.2.1 for a more detailed discussion on how we overcome these two difficulties.

1.2 Related Work

In recent years, we have witnessed several breakthroughs in designing (approximately) optimal mechanisms in multi-dimensional settings. The black-box reduction by Cai et al. [6, 7, 8, 9] shows that we can reduce any Bayesian mechanism design problem to a similar algorithm design problem via convex optimization. Through their reduction, it is proved that all optimal mechanisms can be characterized as a distribution of virtual welfare maximizers, where the virtual valuations are computed by an LP. Although this characterization provides important insights about the structure of the optimal mechanism, the optimal allocation rule is unavoidably randomized and might still be complex as the virtual valuations are only a solution of an LP.

Another line of work considers the “Simple vs. Optimal” auction design problem. For instance, a sequence of results [13, 14, 15, 16] show that sequential posted price mechanism can achieve of the optimal revenue, whenever the buyers have unit-demand valuations over independent items. Another series of results [31, 11, 36, 1, 46] show that the better of selling the items separately and running the VCG mechanism with per bidder entry fee achieves of the optimal revenue, whenever the buyers’ valuations are additive over independent items. Cai et al. [10] unified the two lines of results and improved the approximation ratios to for the additive case and for the unit-demand case using their duality framework.

Some recent works have shown that simple mechanisms can approximate the optimal revenue even when buyers have more sophisticated valuations. For instance, Chawla and Miller [17] showed that the sequential two-part tariff mechanism can approximate the optimal revenue when buyers have matroid rank valuation functions over independent items. Their mechanism requires every buyer to pay an entry fee up front, and then run a sequential posted price mechanism on buyers who have accepted the entry fee. Our ASPE is similar to their mechanism, but with two major differences: (i) since buyers are asked to pay the entry fee before the seller visits them, the buyers have to make their decisions based on the expected utility (assuming every other buyer behaves truthfully) they can receive. Hence, the mechanism is only guaranteed to be BIC and interim IR. While in our mechanism, the buyers can see what items are still available before paying the entry fee, therefore the decision making is straightforward and the ASPE is DSIC and ex-post IR; (ii) the item prices in the ASPE are anonymous, while in the sequential two-part tariff mechanism, personalized prices are allowed. For valuations beyond matroid rank functions, Rubinstein and Weinberg [41] showed that for a single buyer whose valuation is subadditive over independent items, either grand bundling or selling the items separately achieves at least of the optimal revenue.

The Cai-Devanur-Weinberg duality framework [10] has been applied to other intriguing Mechanism Design problems. For example, Eden et al. showed that the better of selling separately and bundling together gets an -approximation for a single bidder with “complementarity- valuations over independent items” [24]. The same authors also proved a Bulow-Klemperer result for regular i.i.d. and constrained additive bidders [23]. Liu and Psomas provided a Bulow-Klemperer result for dynamic auctions [37]. Finally, Brustle et al. [5] extended the duality framework to two-sided markets and used it to design simple mechanisms for approximating the Gains from Trade.

Strong duality frameworks have recently been developed for one additive buyer [18, 20, 27, 28, 29]. These frameworks show that the dual problem of revenue maximization can be viewed as an optimal transport/bipartite matching problem. Hartline and Haghpanah provided an alternative duality framework in [30]. They showed that if certain paths exist, these paths provide a witness of the optimality of a certain Myerson-type mechanism, but these paths are not guaranteed to exist in general. Similar to the Cai-Devanur-Weinberg framework, Carroll [12] independently made use of a partial Lagrangian over incentive constraints. These duality frameworks have been successfully provide conditions under which a certain type of mechanism is optimal when there is a single unit-demand or additive bidder. However, none of these frameworks succeeds in yielding any approximately optimal results in multi-buyer settings.

2 Preliminaries

We focus on revenue maximization in the combinatorial auction with independent bidders and heterogenous items. Each bidder has a valuation that is subadditive over independent items (see Definition 1). We denote bidder ’s type as , where is bidder ’s private information about item . For each , , we assume is drawn independently from the distribution . Let be the distribution of bidder ’s type and be the distribution of the type profile. We use (or ) and (or ) to denote the support and density function of (or ). For notational convenience, we let to be the types of all bidders except and (or to be the types of the first (or ) bidders. Similarly, we define ,

and for the corresponding distributions, support sets and density functions. When bidder ’s type is , her valuation for a set of items is denoted by .

Definition 1.

[41]

For every bidder , whose type is drawn from a product distribution , her distribution of valuation function is subadditive over independent items if:

•

- has no externalities, i.e., for each and , only depends on , formally, for any such that for all , .

•

- is monotone, i.e., for all and , .

•

- is subadditive, i.e., for all and , .

We use to denote , as it only depends on . When is XOS (or constrained additive) for all and , we say is XOS (or constrained additive) over independent items.

We first formally define various valuation classes.

Definition 2.

We define several classes of valuations formally. Let be the type and be the value for bundle .

•

Constrained Additive:, where is a downward closed set system over the items specifying the feasible bundles. In particular, when , the valuation is an additive function; when , the valuation is a unit-demand function; when is a matroid, the valuation is a matroid-rank function. An equivalent way to represent any constrained additive valuations is to view the function as additive but the bidder is only allowed to receive bundles that are feasible, i.e., bundles in . To ease notations, we interpret as an -dimensional vector such that .

•

XOS/Fractionally Subadditive:, where is some finite number and is an additive function for any .

•

Subadditive: for any .

The following are a few examples of various valuation distributions which are over independent items (Definition 1):

XOS/Fractionally Subadditive: encodes all the possible values associated with item , and .

Given and , we use to denote the expected revenue of a BIC mechanism . Throughout the paper, we use the following notations for the simple mechanisms we consider.

Single-Bidder Mechanisms:

- denotes the optimal expected revenue achievable by any posted price mechanism that only allows the buyer to purchase at most one item, and we use SRev for short if there is no confusion777The mechanism is slightly different from selling separately, as we only allow the buyer to purchase at most one item..

- denotes the optimal expected revenue achievable by selling a grand bundle and we use BRev for short if there is no confusion.

Multi-Bidder Mechanisms:

- denotes the optimal expected revenue achievable by selling the items via an RSPM to the bidders, and we use PostRev for short when there is no confusion.

- denotes the optimal expected revenue achievable by selling the items via an ASPE to the bidders, and we use APostEnRev for short when there is no confusion.

Single-Dimensional Copies Setting: In the analysis for unit-demand bidders in [14, 10], the optimal revenue is upper bounded by the optimal revenue in the single-dimensional copies setting defined in [14]. We use the same technique. We construct agents, where agent has value of being served with , and we are only allow to use matchings, that is, for each at most one agent is served and for each at most one agent is served888This is exactly the copies setting used in [14], if every bidder is unit-demand and has value with type . Notice that this unit-demand multi-dimensional setting is equivalent as adding an extra constraint, each buyer can purchase at most one item, to the original setting with subadditive bidders.. Notice that this is a single-dimensional setting, as each agent’s type is specified by a single number. Let be the optimal BIC revenue in this copies setting.

Continuous vs. Discrete Distributions: We explicitly assume that the input distributions are discrete. Nevertheless, it is known that every can be discretized into such that the optimal revenue for and are within of each other [10]. So our results also apply to continuous distributions.

2.1 Our Mechanisms

In this section, we introduce a class of mechanisms called Sequential Posted Price with Entry Fee. For each bidder , the mechanism first determines a posted price for each item and an entry fee function for each bidder that maps the set of available items to a real value entry fee. The seller visits the bidders sequentially in some arbitrary order. For simplicity, we assume the bidders are visited in the lexicographical order. When bidder is visited, let be the set of items that are still available. Clearly, this set only depends on the types of bidders who are visited before . The mechanism shows the set to bidder and asks her for an entry fee . If she accepts the entry fee, she can enter the mechanism and take her favorite bundle by paying .

If there exist multiple bundles with the same maximum surplus, the bidder can break ties arbitrarily. Sometimes, there is a feasibility constraint on what items a buyer can purchase. In particular, if we say the mechanism is rationed, then , i.e., a buyer can purchase at most one item. Formally, the favorite bundle is defined as follows:

.

0: is the price for bidder to purchase item and is bidder ’s entry fee function.

1:

2:fordo

3: Show bidder the set of available items , and define entry fee as .

4:if Bidder pays the entry fee then

5: receives her favorite bundle , paying .

6: .

7:else

8: gets nothing and pays .

9:endif

10:endfor

Algorithm 1Sequential Posted Price with Entry Fee Mechanism

See Algorithm 1 for the formal specification of the above mechanism. Notice that before the bidder decides whether to pay the entry fee, she is aware of the set which contains all available items. Thus, she can compute her favorite bundle and the corresponding utility if she chooses to enter the mechanism. She can then compare that utility with the entry fee and accept the entry fee if the former is greater than the latter. The mechanism described above is therefore deterministic and DSIC. Throughout this paper, we focus on the following two special cases of this class of mechanisms:

-Rationed Sequential Posted Price Mechanism (RSPM): Every buyer can purchase at most one item and the mechanism always charges entry fee, i.e., and for all and .

-Anonymous Sequential Posted Price with Entry Fee Mechanism (ASPE): The mechanism uses anonymous posted prices, i.e., for any item and bidders , but may charge positive and personalized entry fee. Also, any buyer can purchase any bundle available once she has paid the entry fee, i.e., .

3 Paper Organization

In this section, we provide the roadmap to our paper. In Section 4, we review the Duality framework of [10].

In Section 5, we derive an upper bound of the optimal revenue for subadditive bidders by combining the duality framework with our new techniques, i.e. valuation relaxation and adaptive dual variables. Our main result in this section, Theorem 2, shows that the revenue can be upper bounded by two terms – Non-Favorite and Single defined in Lemma 4.

In Section 6, we use the single bidder case to familiarize the readers with some basic ideas and techniques used to bound Single and Non-Favorite. The main result of this section, Theorem 3, shows that the optimal revenue for a single subadditive bidder is upper bounded by and .

Section 7 contains the main result of this paper. We show how to upper bound the optimal revenue for XOS (or subadditive) bidders with a constant number of (or ) PostRev (the optimal revenue obtainable by an RSPM) and APostEnRev ((the optimal revenue obtainable by an ASPE). In particular, Single can be upper bounded by the optimal revenue in the copies setting which is again upper bounded by . We further decompose Non-Favorite into two terms Tail and Core, and show how to bound Tail in Section 7.1 and how to bound Core in Section 7.2.

4 Duality

The focus of [10] was on additive and unit-demand valuations and their respective dual was derived from an LP that is only meaningful for constrained additive valuations. In order to tackle general valuations, we need to apply the duality framework to an LP that is meaningful for general valuations. Instead of using the “implicit forms” LP from [9, 10], we choose a slightly different and more intuitive LP formulation (see Figure 1). For all bidders and types , we use as the interim price paid by bidder and as the interim probability of receiving the exact bundle . To ease the notation, we use a special type to represent the choice of not participating in the mechanism. More specifically, for any and . Now a Bayesian IR (BIR) constraint is simply another BIC constraint: for any type , bidder will not want to lie to type . We let .

Following the recipe provided by [10], we take the partial Lagrangian dual of the LP in Figure 1 by lagrangifying the BIC constraints. Let be the Lagrange multiplier associated with the BIC constraint that if bidder ’s true type is she will not prefer to lie to type

(see Figure 2 and Definition 3). As shown in [10], the dual solution has finite value if and only if the dual variables form a valid flow for every bidder . The reason is that the payments are unconstrained variables, therefore the corresponding coefficients must be in order for the dual solution to have finite value. It turns out when all these coefficients are , the dual variables can be interpreted as a flow described in Lemma 1. We refer the readers to [10] for a complete proof. From now on, we only consider that corresponds to a flow.

Variables:•, for all bidders and types , denoting the expected price paid by bidder when reporting type over the randomness of the mechanism and the other bidders’ types.•, for all bidders , all bundles of items , and types , denoting the probability that bidder receives exactly the bundle when reporting type over the randomness of the mechanism and the other bidders’ types.Constraints:•, for all bidders , and types , guaranteeing that the reduced form mechanism is BIC and Bayesian IR.•, guaranteeing is feasible.Objective:•, the expected revenue.

Figure 1: A Linear Program (LP) for Revenue Optimization.

Definition 3.

Let be the partial Lagrangian defined as follows:

(1)

(2)

Variables:• for all , the Lagrangian multipliers for Bayesian IC and IR constraints.

Constraints:• for all , guaranteeing that the Lagrangian multipliers are non-negative.Objective:•.

Figure 2: Partial Lagrangian of the Revenue Maximization LP.

A set of feasible duals is useful if . is useful iff for each bidder , forms a valid flow, i.e., iff the following satisfies flow conservation at all nodes except the source and the sink:

1. Nodes: A super source and a super sink , along with a node for every type .

2. An edge from to with flow , for all .

3. An edge from to with flow for all , and (including the sink).

Definition 4(Virtual Value Function).

For each flow , we define a corresponding virtual value function , such that for every bidder , every type and every set ,

The proof of Theorem 1 is essentially the same as in [10]. We include it in Appendix B for completeness.

For any flow and any BIC mechanism , the revenue of is the virtual welfare of w.r.t. the virtual valuation corresponding to .

Let be the optimal dual variables and be the revenue optimal BIC mechanism, then the expected virtual welfare with respect to (induced by ) under equals to the expected revenue of .

5 Canonical Flow and Properties of the Virtual Valuations

In this section, we present a canonical way of setting the dual variables/flow that induces our benchmarks. A recap of the flow for additive valuations and the appealing properties of the corresponding virtual valuation functions can be found in Appendix C. We refer readers to that Section for more intuition about the flow.

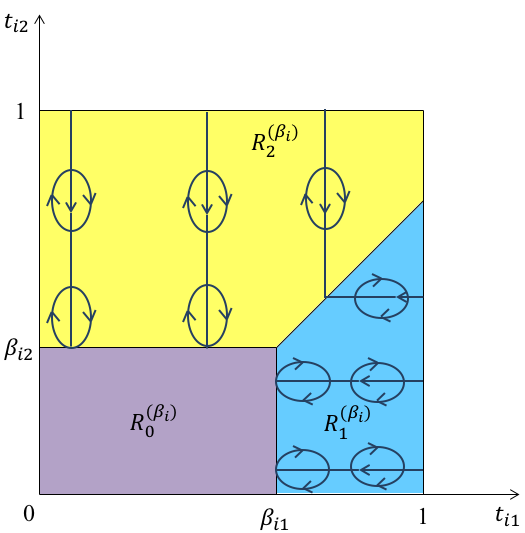

Although any flow can provide a finite upper bound of the optimal revenue, we focus on a particular class of flows, in which every flow is parametrized by a set of parameters . Based on , we partition the type set of each buyer into regions: (i) contains all types such that for all . (ii) contains all types such that and is the smallest index in . Intuitively, if we view as the price of item for bidder , then contains all types in that cannot afford any item, and any with contains all types in whose “favorite” item is . We first provide a Partial Specification of the flow :

1. For every type in region , the flow goes directly to (the super sink).

2. For all , any flow entering is from (the super source) and any flow leaving is to .

3. For all and in (), only if and only differ in the -th coordinate.

For additive valuations and any type , the contribution to the virtual value function from any type is either if , or if , only differs on the -th coordinate and . In either case, the contribution does not depend on for any . This is the key property that allows [10] to choose a flow such that the value of the favorite item is replaced by the corresponding Myerson’s ironed virtual value in the virtual value function . Unfortunately, this property no longer holds for subadditive valuations. When and , the contribution heavily depends on of all the other item . All we can conclude is that the contribution lies in the range 999 is subadditive and monotone for every type , therefore and ., but this is not sufficient for us to convert the value of item into the corresponding Myerson’s ironed virtual value.

5.1 Valuation Relaxation

This is the first major barrier for extending the duality framework to accommodate subadditive valuations. We overcome it by considering a relaxation of the valuation functions. More specifically, for any , we construct another function for every buyer such that: (i) for any , is subadditive and monotone, and for every bundle the new value is no smaller than the original value ; (ii) for any BIC mechanism with respect to the original valuations, there exists another mechanism that is BIC with respect to the new valuations and its revenue is comparable to the revenue of ; (iii) for the new valuations , there exists a flow whose induced virtual value functions have properties similar to those in the additive case.

Property (ii) implies that the optimal revenue with respect to can serve as a proxy for the original optimal revenue. Moreover, due to Theorem 1, the optimal revenue for is upper bounded by the partial Lagrangian dual with respect to , which has an appealing format similar to the additive case by property (iii). Thus, we obtain a benchmark for subadditive bidders that resembles the benchmark for additive bidders in [10].

Definition 5(Relaxed Valuation).

Given , for any buyer , define , if the “favorite” item is in , i.e., . Otherwise, define .

In the next Lemma, we show that for any BIC mechanism for , there exists a BIC mechanism for such that its revenue is comparable to the revenue of (property (ii)). Moreover, the ex-ante probability for any buyer to receive any item in is no greater than in (property (i)). We will see later that this is an important property for our analysis. The proof of Lemma 2 is similar to the -BIC to BIC reduction in [34, 2, 21] and can be found in Appendix H.

Lemma 2.

For any and any BIC mechanism for subadditive valuation with for all , there exists a BIC mechanism for valuations with for all , such that

(i), for all and ,

(ii)

(or ) is the revenue of the mechanism (or ) while the buyers’ types are drawn from and buyer ’s valuation is (or ). (or ) is the probability of buyer receiving exactly bundle when her reported type is in mechanism (or ).

5.2 Virtual Valuation for the Relaxed Valuation

For any , based on the same partition of the type sets as in the beginning of Section 5, we construct a flow that respects the partial specification, such that the corresponding virtual valuation function for has the same appealing properties as in the additive case.

For the relaxed valuation, as is only positive for types , that only differ in the -th coordinate, the contribution from item to the virtual valuation solely depends on and but not for any other item

. Notice that this property does not hold for the original valuation, and it is the main reason why we choose the relaxed valuation as in Definition 5. Moreover, we can choose carefully so that the virtual valuation of has the following format:

Lemma 3.

Let be the distribution of when is drawn from . For any , there exists a flow such that the corresponding virtual value function of valuation satisfies the following properties:

1. For any , .

2. For any , , where is the Myerson’s ironed virtual value for with respect to .

The proof of Lemma 3 is postponed to Appendix D.

Next, we use the virtual welfare of the allocation to bound the revenue of .

Lemma 4.

For any ,

where . Non-Favorite denotes the sum of the first two terms. Single denotes the last term.

Proof.

The Lemma follows easily from the properties in Lemma 3 and Theorem 1.

∎

Proof of Theorem 2:

First, let’s look at the value of . When for some and , because . For the other cases, . Therefore,

Our statement follows from combining Lemma 2, Lemma 4 with the inequality above.

5.3 Upper Bound for the Revenue of Subadditive Buyers

In Section 5.1, we have argued that for any , there exists a mechanism such that its revenue with respect to the relaxed valuation is comparable to the revenue of with respect to the original valuation. In Section 5.2, we have shown for any how to choose a flow to obtain an upper bound for and also an upper bound for . Now we specify our choice of .

In [10], the authors fixed a particular , and shown that under any allocation rule, the corresponding benchmark can be bounded by the sum of the revenue of a few simple mechanisms. However, for valuations beyond additive and unit-demand, the benchmark becomes much more challenging to analyze101010Indeed, the difficulties already arise for valuations as simple as -demand. A bidder’s valuation is -demand if her valuation is additive subject to a uniform matroid with rank .. We adopt an alternative and more flexible approach to obtain a new upper bound. Instead of fixing a single for all mechanisms, we customize a different for every different mechanism . Next, we relax the valuation and design the flow based on the chosen as specified in Section 5.1 and 5.2.

Then we upper bound the revenue of with the benchmark in Theorem 2 and argue that for any mechanism , the corresponding benchmark can be upper bounded by the sum of the revenue of a few simple mechanisms. As we allow , in other words the flow , to depend on the mechanism, our new approach may provide a better upper bound. As it turns out, our new upper bound is indeed easier to analyze.

Lemma 5 specifies the two properties of our that play the most crucial roles in our analysis. We construct such a in the proof of Lemma 5, however the construction is not necessarily unique and any satisfying these two properties suffices. Note that our construction heavily relies on property (i) of Lemma 2.

Lemma 5.

For any constant and any mechanism , there exists a such that: for the mechanism constructed in Lemma 2 according to , any and ,

(i);

(ii), where .

Before proving Lemma 5, we provide some intuition behind the two required properties.

Property (i) is used to guarantee that if item ’s price for bidder is higher than for all and in an RSPM, for any item and any bidder , is still available with probability at least when is visited. As for any bidder to purchase item , must be greater than her price for item . By the union bound, the probability that there exists such a bidder is upper bounded by the LHS of property (i), and therefore is at most . With this guarantee, we can easily show that the RSPM achieves good revenue (Lemma 17). Property (ii) states that the ex-ante probability for bidder to receive an item in is not much bigger than the probability that bidder ’s value is larger than item . This is crucial for proving our key Lemma 24, in which we argue that two different valuations provide comparable welfare under the same allocation rule . With Lemma 24, we can show that the ASPE obtains good revenue.

Proof of Lemma 5:

When there is only one buyer, we can simply set every to be and both conditions are satisfied.

When there are multiple players, we let

where . Clearly, when the distribution of is continuous, then

(3)

and therefore for any ,

So the first condition is satisfied. The second condition holds because by the first property in Lemma 2, .

When the distribution for is discrete, it is possible that Equation 3 does not hold, but this is essentially a tie breaking issue and not hard to fix. Let be an extremely small constant that is smaller than for any , any and any . Let be a random variable uniformly distributed on , and think of it as a random rebate that the seller gives to bidder when she purchases item . Now we modify the definition of as

Both of the two properties in Lemma 5 hold if we replace with . The only change we need to make in the mechanism is to actually give the bidders as the corresponding rebate. Since we can choose to be arbitrarily small, the sum of the rebate is also arbitrarily small. For the simplicity of the presentation, we will omit and in the rest of the paper. The random rebate indeed makes our mechanism randomized(according to the random variable ). However, the randomized mechanism is a uniform distribution of deterministic DSIC mechanisms (after determining all ), and the expected revenue of the randomized mechanism is simply the average revenue of all these deterministic mechanisms. Therefore, there must be one realization of the rebates such that the corresponding deterministic mechanism has revenue above the expectation, i.e., the expected revenue of the randomized one. Thus if the randomized mechanism is proved to achieve some approximation ratio, there must exist a deterministic one that achieves the same ratio. The deterministic mechanism will use a fixed value as the rebate.

Similarly, the same issue about discrete distributions arises when we define some other crucial parameters later, e.g., in the Definition of , and . We can resolve all of them together using the trick (adding a random rebate) described above, and we will not include a detailed proof for those cases.

6 Warm Up: Single Bidder

To warm up, we first study the case where there is a single subadditive buyer and show how to improve the approximation ratio from to . Since there is only one buyer, we will drop the subscript in the notations. As specified in Section 5.3, we use a that satisfies both properties in Lemma 5. For a single buyer, we can simply set to be for all . We use in the following proof to denote the corresponding terms in Theorem 2 for . Notice . Theorem 3 shows that the optimal revenue is within a constant factor of the better of selling separately and grand bundling.

Theorem 3.

For a single buyer whose valuation distribution is subadditive over independent items,

for any BIC mechanism .

Recall that the revenue for mechanism is upper bounded by (Theorem 2). We first upper bound by . Since is a feasible allocation in the original setting, with is a feasible allocation in the copies setting, and therefore is the Myerson Virtual Welfare of a certain allocation in the copies setting, which is upper bounded by . By [14], is at most .

Lemma 6.

For any BIC mechanism ,

For , we first bound it by the social welfare from all non-favorite items. Then we decompose the latter into two terms and , and bound them separately. For every , define , . Here the threshold is chosen as

(4)

Since is subadditive for all , we have for every , . We decompose based on the inequality above. Proof of Lemma 7 can be found in Appendix E.

Lemma 7.

Using the definition of and SRev, we can upper bound with a similar argument as in [10].

Lemma 8.

For any BIC mechanism , .

Proof.

Since , for each type consider the mechanism that posts the same price for each item but only allows the buyer to purchase at most one. Notice if there exists such that , the mechanism is guaranteed to sell one item obtaining revenue . Thus, the revenue obtained by this mechanism

is at least . By definition, this is no more than SRev.

(5)

The last equality is because by the definition of ,

.111111This clearly holds if is drawn from a continuous distribution. When is drawn from a discrete distribution, see the proof of Lemma 5 for a simple fix.

∎

The is upper bounded by where

. We argue that is drawn from a distribution that is subadditive over independent items and is -Lipschitz (see Definition 6). Using a concentration bound by Schechtman [42], we show is upper bounded by the median of random variable and , which are upper bounded by BRev and SRev respectively.

Lemma 9.

For any BIC mechanism , .

Recall that

(6)

We will bound with a concentration inequality from [42]. It requires the following definition:

Definition 6.

A function is -Lipschitz if for any type , and set ,

where is the symmetric difference between and .

Define a new valuation function for the bidder as , for all and . Then is Lipschitz, and when is drawn from the product distribution , remains to be a valuation drawn from a distribution that is subadditive over independent items. See Appendix E for the proof of Lemma 10 and Lemma 11.

Lemma 10.

For all , satisfies monotonicity, subadditivity and no externalities defined in Definition 1.

Lemma 11.

is Lipschitz.

Next, we apply the following concentration inequality to derive Corollary 1, which is useful to analyze the .

Lemma 12.

[42]

Let with be a function drawn from a distribution that is subadditive over independent items of ground set . If is -Lipschitz, then for all ,

Corollary 1.

Let with be a function drawn from a distribution that is subadditive over independent items of ground set . If is -Lipschitz, then if we let be the median of the value of the grand bundle , i.e. ,

Proof.

Let be . If we apply Lemma 12 to the case where is the median and , we have

With the inequality above, we can upper bound the expected value of .

Proof of Lemma 9:

Let be the median of when is sampled from distribution . Now consider the mechanism that sells the grand bundle with price . Notice that the bidder’s valuation for the grand bundle is . Thus with probability at least , the bidder purchases the bundle. Thus, .

It remains to argue that the Lipchitz constant can be upper bounded using SRev. Notice that by AM-GM Inequality,

Consider the mechanism that posts price for each item but only allow the buyer to purchase one item. Then with probability at least , the mechanism sells one item obtaining expected revenue . Thus . Inequality (7) becomes

(8)

Proof of Theorem 3:

Since (Lemma 6) and (Lemma 8 and 9), according to Theorem 2.

7 Multiple Bidders

In this section, we prove our main result – simple mechanisms can approximate the optimal BIC revenue even when there are multiple XOS/subadditive bidders. First, we need the definition of supporting prices.

Here is a sketch of the proof for Theorem 4. We show how to upper bound in Lemma 13. Then, we decompose into and in Lemma 14. We show how to construct a simple mechanism to approximate in Section 7.1 and how to approximate in Section 7.2.

Analysis of :

Lemma 13.

For any mechanism ,

Proof.

We construct a new mechanism in the copies setting based on . Whenever allocates item to buyer and , serves the agent . Since there is at most one that belongs to, serves at most one agent for each of buyer . Hence, is feasible in the copies setting, and is the expected Myerson’s ironed virtual welfare of . Since every agent’s value is drawn independently, the optimal revenue in the copies setting is the same as the maximum Myerson’s ironed virtual welfare in the same setting. Therefore, is no less than .

As showed in [14, 35], a simple posted-price mechanism with the constraint that every buyer can only purchase one item, i.e., an RSPM, achieves revenue at least in the original setting. Hence, .

∎

Core-Tail Decomposition of : we decompose into two terms and 121212In [10], Non-Favorite is decomposed into four different terms Under, Over, Core and Tail. We essentially merge the first three terms into in our decomposition.. First, we need the following definition.

Definition 8.

For every buyer , let For every , let and .

Since is subadditive for all and , we have . The term can be decomposed into and based on the inequality above. The complete proof of Lemma 14 can be found in Appendix F.

Lemma 14.

7.1 Analyzing in the Multi-Bidder Case

In this section we show how to bound with the revenue of an RSPM.

Lemma 15.

For any BIC mechanism , .

We first fix a few notations. Let

, and . We show in the following Lemma that is an upper bound of .

Lemma 16.

For any BIC mechanism ,

Proof.

In the second inequality, the first term is because , so

The second term is because for any such that ,

∎

Next, we argue that can be approximated by an RSPM. Indeed, we prove a stronger lemma, which is also useful for analyzing .

Lemma 17.

Let be a collection of non-negative numbers, such that for any buyer

then

Proof.

Consider a RSPM that sells item to buyer at price . The mechanism

visits the buyers in some arbitrary order. Notice that when it is buyer ’s turn, she purchases exactly item and pays if all of the following three conditions hold: (i) is still available, (ii) and (iii) . The second condition means buyer can afford item . The third condition means she cannot afford any other item . Therefore, buyer ’s purchases exactly item .

Now let us compute the probability that all three conditions hold. Since every buyer’s valuation is subadditive over the items, item is purchased by someone else only if there exists a buyer who has . Because for all , by the union bound, the event described above happens with probability at most , which is less than by property (i) of Lemma 5. Therefore, condition (i) holds with probability at least . Clearly, condition (ii) holds with probability . Finally, condition (iii) holds with at least probability , because according to our assumption of the s, the probability that there exists any item such that is no more than . Since the three conditions are independent, buyer purchases exactly item with probability at least . So the expected revenue of this mechanism is at least .

∎

Proof of Lemma 15:

Since , it satisfies the assumption in Lemma 17 due to the choice of . Therefore,

(9)

Our statement follows from the above inequality and Lemma 16.

We have done the analysis for . Before starting the analysis for , we show that is within a constant factor of . This Lemma is useful for bounding .

Lemma 18.

For all , and .

Proof.

By the definition of ,

The last inequality is because when ,

is at least . As , by Inequality (9),

.

∎

7.2 Analyzing in the Multi-Bidder Case

In this section we upper bound . Recall that

We can view it as the welfare of another valuation function under allocation where . In other words, we “truncate” the function at some threshold, i.e., only evaluate the items whose value on its own is less than that threshold. The new function still satisfies monotonicity, subadditivity and no externalities.

We first compare existing methods for analyzing the Core with our approach before jumping into the proofs.

7.2.1 Comparison between the Existing Methods and Our Approach

As all results in the literature [14, 46, 10, 17] only study special cases of constrained additive valuations, we restrict our attention to constrained additive valuations in the comparison, but our approach also applies to XOS and subadditive valuations.

We compare our approach to the state of the art result by Chawla and Miller [17]. They separate into two parts: (i) the welfare obtained from values below , and (ii) the welfare obtained from values between and 131313In particular, if bidder is awarded a bundle that is feasible for her, the contribution for the first part is and the contribution to the second part is .

It is not hard to show that the latter can be upper bounded by the revenue of a sequential posted price with per bidder entry fee mechanism.

Due to their choice of (similar to the second property of Lemma 5), the former is upper bounded by .

It turns out when every bidder’s feasibility constraint is a matroid, one can use the OCRS from [26] to design a sequential posted price mechanism to approximate this expression.

However, as we show in Example 2, could be times larger than the optimal social welfare when the bidders have general downward closed feasibility constraints.

Hence, such approach cannot yield any constant factor approximation for general constrained additive valuations.

As explained in the intro, we take an entirely different approach. We first construct the posted prices for our ASPE (Definition 9), Feldman et al. [25] showed that the anonymous posted price mechanism with these prices achieves welfare . If all bidders have valuations that are subadditive over independent items, for any bidder and any set of available items , ’s surplus for under valuation () is also subadditive over independent items. According to Talagrand’s concentration inequality, the surplus concentrates and its expectation is upper bounded by its median and its Lipschitz constant . One can extract at least half of the median by setting the median of the surplus as the entry fee. How about the Lipschitz constant ? Unfortunately, could be as large as , which is too large to be bounded.

Here is how we overcome this difficulty. Instead of considering , we construct a new valuation that is always dominated by the true valuation . We consider the social welfare induced by under and define it as . In Section 7.2.2, we show that is not too far away from , so it suffices to approximate (Lemma 24). But why is easier to approximate? The reason is two-fold. (i) For any bidder and any set of available items , bidder ’s surplus for under (defined as in Definition 12, which is ), is not only subadditive over independent items, but also has a small Lipschitz constant (Lemma 25). Indeed, these Lipschitz constants are so small that and can be upper bounded by PostRev (Lemma 22). (ii) If we set the entry fee of our ASPE to be the median of when is drawn from , using a proof inspired by Feldman et al. [25], we can show that our ASPE’s revenue collected from the posted prices plus the expected surplus of the bidders (over the randomness of all bidders’ types) approximates (implied by Lemma 26). Again by Talagrand’s concentration inequality, we can bound bidder ’s expected surplus by our entry fee and (Lemma 28). As is always smaller than the true valuation , thus for any type of bidder and any available items , the surplus for under must be larger than , and the entry fee is accepted with probability at least . Putting everything together, we demonstrate that we can approximate with an ASPE or an RSPM (Lemma 29).

7.2.2 Construction of

We first show that if for any and there is a set of -supporting prices for , then there is a set of -supporting prices for .

Lemma 19.

If for any type and any set , there exists a set of -supporting prices for , then for any and there also exists a set of -supporting prices for . In particular, if and otherwise. Moreover, for all , , and .

Proof.

It suffices to verify that satisfies the two properties of -supporting prices.

For any , . Therefore,

The last equality is because for . Also, we have

Thus, defined above is a set of -supporting prices for . Next, we argue that for all , , . If , , by definition . Otherwise if , then , by the first property of -supporting prices, .

∎

Next, we define the prices of our ASPE.

Definition 9.

We define a price for each item as follows,

where are the -supporting prices of and set for any bidder and type .

can be upper bounded by . The proof follows from the definition of -supporting prices (Definition 7) and the definition of (Definition 9).

Lemma 20.

.

Proof.

∎

In the following definitions, we define which is the welfare of another function under the same allocation .

Definition 10.

Let

and define to be .

Definition 11.

For every buyer and type , let ,

and

for any set . Moreover, let

In the next two Lemmas, we prove some useful properties of . In particular, we argue that can be upper bounded by (Lemma 22).

Lemma 21.

Proof.

According to the definition of , for every buyer , , and . Our statement follows directly from Lemma 17. ∎

In the following two Lemmas, we compare with . The proof of Lemma 23 is postponed to Appendix F.

Lemma 23.

For every buyer , type , satisfies monotonicity, subadditivity and no externalities. Furthermore, for every set and every subset of ,

Lemma 24.

Let

Then,

Proof.

From the definition of , it is easy to see that for every . So we only need to argue that .

(10)

This first inequality is because is non-zero only when , and the difference is upper bounded by when and upper bounded by when .

We first bound .

(11)

The set in the first inequality is defined in Definition 10. The second inequality is due to property (ii) in Lemma 5. The third inequality is due to Definition 10 and the last inequality is due to Lemma 21.

Next, we bound .

(12)

The last inequality is due to Lemma 18. Combining Inequality (10), (11) and (12), we have proved our claim.

∎

By Lemma 20, . Hence, Lemma 24 shows that to approximate , it suffices to approximate . Indeed, we will use as an proxy for in our analysis of the ASPE.

7.2.3 Design and Analysis of Our ASPE

Consider the sequential post-price mechanism with anonymous posted price for item . We visit the buyers in the alphabetical order141414We can visit the buyers in an arbitrary order. We use the the alphabetical order here just to ease the notations in the proof. and charge every bidder an entry fee. We define the entry fee here.

Definition 12(Entry Fee).

For any bidder , any type and any set , let

For any type profile and any bidder , let the entry fee for bidder be

where and is the set of items that are not purchased by the first buyers in the ASPE, when buyer ’s valuation is for all . Notice that even though the seller does not know , she can compute the entry fee , as she observes after visiting the first bidders.

In Lemma 25, we show that is the Lipschitz constant for and the proof is postponed to Appendix F. Moreover, is upper bounded by due to Lemma 22.

Lemma 25.

For any , the function is -Lipschitz. Moreover, for any type , satisfies monotonicity, subadditivity and no externalities.

The following Lemma is crucial for our proof. We show that in expectation over all type profiles, we can lower bound of the sum of for all bidders. In particular, this lower bound plus our ASPE’s revenue from the posted prices already approximates . The proof is inspired by Feldman et al. [25]. Note that is a lower bound of the real surplus of buyer for set . We choose to analyze the sum of because has a small Lipschitz constant, which allows us to approximate with buyer ’s entry fee and .

Lemma 26.

For all , let (Definition 9) be the price for item and every bidder’s entry fee be described as in Definition 12. For every type profile , let be the set of items sold in the corresponding ASPE when buyer ’s valuation is . Then

Proof.

are fresh samples drawn from . The first inequality is because the function is monotone in set for any and type . We use to denote . If we let be the set of items that are in and satisfy that , then due to the definition of and Lemma 23. This inequality is exactly the second inequality above. The next equality is because only depends on the types of bidders other than . The second last inequality is because for all and , as the LHS is the probability that the item is not sold after the seller has visited the first bidders and the RHS is the probability that the item remains unsold till the end of the mechanism. Now, observe that for any according to the definition in Lemma 24. Therefore,

∎

Since entry fee in the ASPE for every bidder as the median of her utility over the available items under . Clearly, bidders accept the entry fee with probability at least , as their true utilities (under ) are always higher than their utilities under . Combining the concentration property of the utility under and Lemma 26, we can argue that the total revenue from our ASPE is comparable to , and therefore is comparable to .

Lemma 27.

For all and , bidder accepts with probability at least when is drawn from . Moreover,

Proof.

For any bidder , type and any set , define bidder ’s utility as Clearly, for any type and set . For any , as long as , buyer accepts the entry fee. Since is the median of , with probability at least when is drawn from . So the revenue from entry fee is at least

For any and , by Lemma 25 and Corollary 1, we are able to derive a lower bound for , as shown in Lemma 28.

Lemma 28.

For all and ,

Proof.

It directly follows from Lemma 25 and Corollary 1. For any and , let be the ground set . Therefore, with is a function drawn from a distribution that is subadditive over independent items. Since, is -Lipschitz and

,

∎

Back to the proof of Lemma 27. According to Lemma 28, the revenue from the entry fee is at least

, which is equal to

.

Combining Lemma 22 and Lemma 26, we can further show that the revenue from the entry fee is at least . Since the revenue from the posted prices is exactly , the total revenue of the ASPE is at least

∎

Combining everything together, we have the main result of Section 7.2.

Now, we have upper bounded , and using the sum of the revenue of simple mechanisms (RSPM and ASPE). Combining these bounds, we complete the proof of Theorem 4.

Proof of Theorem 4:

The proof follows from combining Theorem 2, Lemma 13, 14, 15 and 29.

7.2.4 Bad Example for Chawla and Miller’s Approach

Let bidders be constrained additive and be bidder feasibility constraint. We use to denote the feasibility polytope of bidder . Let be a collection of probabilities that satisfy for all item and . Let . The analysis by Chawla and Miller [17] needs to upper bound using the revenue of some BIC mechanism. When is a matroid for every bidder , this expression can be upper bounded by the revenue of a sequential posted price mechanism constructed using OCRS from [26]. Here we show that if the bidders have general downward closed feasibility constraints, this expression is gigantic. More specifically, we prove that even when there is only one bidder, the expression could be times larger than the optimal social welfare.

Consider the following example.

Example 2.

The seller is selling items to a single bidder. The bidder’s value for each item is drawn i.i.d. from distribution , which is the equal revenue distribution truncated at , i.e.,

Items are divided into disjoint sets , each with size . The bidder is additive subject to feasibility constraint .

Lemma 30.

Let be the feasibility polytope for the bidder in Example 2. Let be the optimal social welfare. Then for any constant , there exists such that for sufficiently large ,

Proof.

For any , consider the following feasible allocation rule: w.p. , don’t allocate anything, and w.p. , give the buyer one of the sets uniformly at random. The corresponding ex-ante probability vector satisfies . Thus . Since , for all . We have . We use to denote the random variable of the bidder’s value for set . It is not hard to see that .

Lemma 31.

For any ,

Proof.

Let be random variable with cdf . Notice , , and .

For every , by the Bernstein concentration inequality, for any ,

Choose , we have

∎

By the union bound, . Therefore, .

∎

8 Open Questions

The main open question following our results is:

•

Open Question:Can we design simple and approximately revenue-optimal mechanisms for multiple buyers with valuations that are subadditive over independent items?

A large fraction of the proof in this work already applies to subadditive valuations. More specifically, our upper bound for the optimal revenue from Theorem 2 holds for all subadditive valuations, and we have used it to obtain a constant factor approximation for a single subadditive buyer and a -approximation for multiple subadditive buyers. Our analysis for the term Single and Tail also applies to subadditive valuations.

The only component that does not extend to subadditive valuations is the analysis of the Core. We heavily used a convenient property of XOS functions, namely, the existence of -supporting prices [22, 3]. Unfortunately, general subadditive functions only permit -supporting prices, which is why our approximation ratio degrades to for subadditive valuations. Our analysis of the Core makes use of the supporting prices in two places: (i) the definition of the proxy core and its comparison to in Section 7.2.2; (ii) lower bounding the revenue of ASPE. For (ii), our proof is inspired by Feldman et al. [25], who showed that there exists a sequential posted-price mechanism that is an -approximation to the optimal social welfare for bidders with XOS valuations. Their proof also makes heavy use of the supporting prices, and the approximation ratio degrades to for subadditive valuations. To resolve the open question above, it is worthwhile to first consider generalizing the result of [25]. In particular,

•

Open Question:Can sequential posted-price mechanisms obtain a constant fraction of the optimal social welfare when bidders have subadditive valuations?

An astute reader may have noticed that the approximation results in this paper are only existential. Luckily, the only nonconstructive part of our argument is finding the right , which is essentially the same as finding the ex-ante allocation probabilities of the optimal or an approximately optimal mechanism. In Appendix G, we show how to find the right when the bidders are symmetric, but the asymmetric case remains open.

•

Open Question:Can we design a polynomial time algorithm to compute these simple and approximately optimal mechanisms for constrained additive and XOS valuations?

Appendix

Appendix A Improved Analysis for Constrained Additive Valuation

In this section, we show that for constrained additive bidders, we do not need to relax the valuations, as applying directly the flow in Section 5 already gives an upper bound with the right format. So we can take to simply be . In particular, we can derive the following improved upper bound for using essentially the same proof as in Section 5.

Theorem 5.

If for any bidder any type , is a constrained additive valuation, then for any mechanism and any ,

Combining the same upper bounds we obtained for

and and the improved upper bound in Theorem 5, we can improve the approximation ratio when the bidder(s) have constrained additive valuations.

Theorem 6.

For a single buyer whose valuation is constrained additive,

for any BIC mechanism .

Theorem 7.

For multiple buyers whose valuations are constrained additive,

(13)

for any BIC mechanism . In particular, if we set to be , then

Proof of Theorem 1:

When is useful, we can simplify function by removing the term associated with and replacing with . After the simplification, we have

which is exactly the virtual welfare of with respect to . Now, we only need to prove that is greater than the revenue of . Let us think of using Expression (1). Since is a BIC mechanism,

for any , and . Also, all the dual variables are nonnegative. Therefore, it is clear that is at least as large as the revenue of .

When is the optimal dual variable, by strong duality, we know equals to the revenue of . But we also know that is at least as large as the revenue of , therefore maximizes the virtual welfare.

Appendix C Recap: Flow for Additive Valuations

When the valuations are additive, we simply view as bidder ’s value for receiving item . Although there are many possible ways to define a flow, we focus on a class of simple ones. Every flow in this class is parametrized by a set of parameters . Based on , we first partition the type space for each bidder into regions:

•

contains all types such that for all .

•

contains all types such that and is the smallest index in .

We use essentially the same flow as in [10]. Here we provide a partial specification and state some desirable properties of the flow. See Figure 4 for an example with items and [10] for a complete description of the flow.

Partial Specification of the flow :1.For every type in region , the flow goes directly to (the super sink).2.For all , any flow entering is from (the super source) and any flow leaving is to .3.For all and in (), only if and only differ in the -th coordinate.

Figure 3: Partial Specification of the flow .Figure 4: An example of for additive bidders with two items.

Lemma 32([10]161616Note that this Lemma is a special case of Lemma 3 in [10] when the valuations are additive. ).

For any , there exists a flow such that the corresponding virtual value function satisfies the following properties:

•

For any , .

•

For any , ,

where is Myerson’s ironed virtual value function for .

The properties above are crucial for showing the approximation results for simple mechanisms in [10]. One of the key challenges in approximating the optimal revenue is how to provide a tight upper bound. A trivial upper bound is the social welfare, which may be arbitrarily bad in the worst case. By plugging the virtual value functions in Lemma 32 into the partial Lagrangian, we obtain a new upper bound that replaces the value of the buyer’s favorite item with the corresponding Myerson’s ironed virtual value. As demonstrated in [10], this new upper bound is at most times larger than the optimal revenue when the buyers are additive, and its appealing structure allows the authors to compare the revenue of simple mechanisms to it. In Section 5, we identify some difficulties in directly applying this flow to subadditive valuations. Then we show how to overcome these difficulties by relaxing the subadditive valuations and obtain a similar upper bound.

For any flow that respects the partial specification in Figure 3, the corresponding virtual valuation function of for any buyer is:

•

, if .

•

, otherwise.

Proof of Lemma 33:

The proof follows the definitions of the virtual valuation function (Definition 4) and relaxed valuation (Definition 5). We use to denote bidder ’s information for all items except item . If and , . Since only when and , . Therefore,

If and or , then . If , there is no flow entering except from the source, so clearly . If , then for any that only differs from in the -th coordinate, we have , because . Hence, .

Let . According to Lemma 33, it suffices to prove that for any , any , .

Claim 1.

For any type , if we only allow flow from type to , where for all and , and the flow equals fraction of the total in flow to , then there exists a flow such that

where is the Myerson virtual value for with respect to .

Proof.

As the flow only goes from and , where and only differs in the -th coordinate, and

. If is a type with the largest value in , then there is no flow coming into it except the one from the source, so . For every other value of , the in flow is exactly

This is because each type of the form with is also in . So of all flow that enters these types will be passed down to (and possibly further, before going to the sink), and the total amount of flow entering all of these types from the source is exactly . Therefore, . Whenever there is no more type with smaller value, we push all the flow to the sink.

∎

If is regular, this completes our proof. When is not regular, we can iron the virtual value function in the same way as in [10]. Basically, for two types that only differ in the -th coordinate, if but , add a loop between and with a proper weight to make .

Lemma 34.

[10]

For any and , there exists a flow such that for any , .

Appendix E Analysis for the Single-Bidder Case

Proof of lemma 7:

In Non-Favorite, since , the corresponding term is simply . Notice is a monotone valuation for every ,

Recall that for all and , . We will replace above with . First, the contribution from is upper bounded by the .

The inequality comes from the monotonicity of and the fact that for every only stays in one region .

Next, we upper bound the contribution from by the .

Proof of Lemma 10:

We argue the three properties one by one.

•

Monotonicity: For all and , . Since is monotone,

Thus, is monotone.

•

Subadditivity: For all and , notice , we have

•

No externalities: For any , , and any such that for all , to prove , it is enough to show . Since for any , if and only if .

Proof of Lemma 11:

For any , and set , define set . Since has no externalities, . Therefore,

The second last inequality is because both and are subadditive and for any item () the single-item valuation () is less than .

Appendix F Missing Proofs for the Multi-Bidder Case

Proof of Lemma 14:

We replace every in with

. Let the contribution from be the first term and the contribution from be the second term.

The inequality comes from the Monotonicity of by replacing with .

For the second term, notice that when , . It can be rewritten as:

Lemma 35.

Let be a set of nonnegative numbers. For any buyer , any type , let , and let

for any set . Then for any bidder , any type , , satisfies monotonicity, subadditivity and no externalities.

Proof of Lemma 35:

We will argue these three properties one by one.

•

Monotonicity: For all and , since is monotone,

Thus is monotone.

•

Subadditivity: For all and , . Since is subadditive, we have

•

No externalities: For any , , and any such that for all , to prove , it suffices to show . Since , for any item , if and only if .

Proof of Lemma 23:

By Lemma 35 and Definition 11, satisfies monotonicity, subadditivity and no externalities.

Since ,

for all , we have . Therefore, .

Proof of Lemma 25:

We first prove that is -Lipschitz. For any and set , let . Recall that . This means that for every , must be less than , because otherwise . Therefore, for all . Since is subadditive, . So by the optimality of , it must be that for all . Similarly, we can show that for every , .

Now let set , if .

Similarly, if , . Thus, is -Lipschitz as

Monotonicity follows directly from the definition of . Next, we argue subadditivity. For all , let , , . Since is a subadditive valuation,

Finally, we argue that has no externalities. Consider a set , and types such that for all . For any , since has no externalities, . Thus, .

Appendix G Efficient Approximation for Symmetric Bidders

In this section, we sketch how to compute the RSPM and ASPE to approximate the optimal revenue in polynomial time for symmetric bidders171717Bidders are symmetric if for any two bidders and , we have and for all .. For any given BIC mechanism , one can follow our proof to construct in polynomial time an RSPM and an ASPE such that the better of the two achieves a constant fraction of ’s revenue. We will describe the construction of the RSPM and the ASPE separately in this section. The difficulty of applying the method described above to construct the desired simple mechanisms is that we need to know an (approximately) revenue-maximizing mechanism . We will show how to circumvent this difficulty when the bidders are symmetric.

Indeed, we can directly construct an RSPM that approximates the PostRev. As we have restricted the buyers to purchase at most one item in an RSPM, the PostRev is upper bounded by the optimal revenue of the unit-demand setting where buyer has value for item when her type is . By [10], we know that the optimal revenue in this unit-demand setting is upper bounded by , so one can simply use the RSPM constructed in [14] to extract revenue at least . Note that the construction is independent of .