Afonso S. Bandeira, Asad Lodhia, and Philippe Rigollet

NYU, Courant Institute of Mathematical Sciences: bandeira@cims.nyu.eduMIT, Department of Mathematics: lodhia@math.mit.eduMIT, Department of Mathematics: rigollet@math.mit.edu

Abstract

We prove that Kendall’s Rank correlation matrix converges to the Marčenko

Pastur law, under the assumption that observations are i.i.d random vectors

with components that are independent and absolutely continuous with respect to the Lebesgue

measure. This is the first result on the empirical spectral distribution of a multivariate -statistic.

1 Introduction

Estimating the association between two random variables is a central statistical problem. As such many methods have been proposed, most notably Pearson’s correlation coefficient. While this measure of association is well suited to the Gaussian case, it may be inaccurate in other cases. This observation has led statisticians to consider other measures of associations such as Spearman’s and Kendall’s that can be proved to be more robust to heavy-tailed distributions (see, e.g., [LHY+12]).

In a multivariate setting, covariance and correlation matrices are preponderant tools to understand the interaction between variables. They are also used as building blocks for more sophisticated statistical questions such as principal component analysis or graphical models.

The past decade has witnessed an unprecedented and fertile interaction between random matrix theory and high-dimensional statistics (see [PA14] for a recent survey). Indeed, in high-dimensional settings, traditional asymptotics where the sample size tends to infinity fail to capture a delicate interaction between sample size and dimension and random matrix theory has allowed statisticians and practitioners alike to gain valuable insight on a variety of multivariate problems.

The terminology “Wishart matrices” is often, though sometimes abusively, used to refer to random matrices of the form , where is an random matrix with independent rows (throughout this paper we restrict our attention to real random matrices). The simplest example arises where has i.i.d standard Gaussian entries but the main characteristics are shared by a much wider class of random matrices. This universality phenomenon manifests itself in various aspects of the limit distribution, and in particular in the limiting behavior of the empirical spectral distribution of the matrix. Let be a Wishart matrix and denote by its eigenvalues; then the empirical spectral distribution of is the distribution on defined as the following mixture of Dirac point masses at the s:

Assuming that the entries of are independent, centered and of unit variance, it can be shown that converges weakly to the Marčenko-Pastur distribution under weak moment conditions (see [EKYY12] for the weakest condition).

While this development alone has led to important statistical advances, it fails to capture more refined notions of correlations, notably more robust ones involving ranks and therefore dependent observations. A first step in this direction was made by [YK86], where the matrix is assumed to have independent rows with isotropic distribution. More recently, this result was extended in [BZ08, O’R12] and covers for example the case of Spearman’s matrix that is based on ranks, which is also a Wishart matrix of the form .

The main contribution of this paper is to derive the limiting distribution of Kendall’s matrix, a cousin of Spearman’s matrix but which is not of the Wishart type but rather a matrix whose entries are -statistics. Kendall’s matrix is a very popular surrogate for correlation matrices but an understanding the fluctuations of its eigenvalues is still missing. Interestingly, Marčenko-Pastur results have been used as heuristics, without justification, precisely for Kendall’s in the context of certain financial applications [CCL+15].

As it turns out, the limiting distribution of is not exactly Marčenko-Pastur, but rather an affine transformation of it. Our main theorem below gives the precise form of this transformation.

Theorem 1.

Let , be independent

random vectors in whose components are independent

random variables that have a density with respect to the Lebesgue

measure on . Then as and the empirical

spectral distribution of converges in probability to

where is distributed according to the standard Marčenko-Pastur law with parameter

(see Theorem 4 for the appropriate definition).

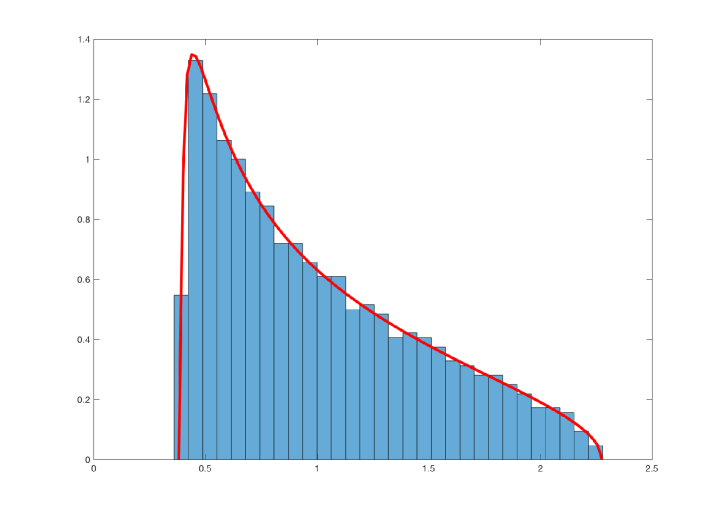

Figure 1 illustrates numerically the result of Theorem 1.

Figure 1: Histogram of the eigenvalues the Kendall matrix for . The superimposed red line is the probability density function , where is distributed according to the standard Marčenko-Pastur law with parameter .

Notation: For any integer we write . We denote by the identity matrix of . For a vector , we denote by it’s th coordinate. For any matrix , we denote by the diagonal matrix with the same diagonal elements as and any real number , we define . In other words, the operator replaces each diagonal element of a matrix by the value .

We denote the sign function with convention that . We define the Frobenius norm of a matrix as . Finally, we define to be the uniform distribution on the interval .

2 Kendall’s Tau

The (univariate) Kendall statistic [Ess24, Lin25, Lin29, Ken38] is defined as follows. Let be independent samples of a pair of real-valued random variables. Then the (empirical) Kendall between and is defined as

The statistic takes values in and it is not hard to see that it can be expressed as

Where a pair is said to be concordant if and have the same sign and discordant otherwise.

It is known that the Kendall statistic is asymptotically Gaussian (see, e.g., [Ken38]). Specifically, if and are independent, then as ,

(1)

This property has been central to construct independence tests between two random variables and (see, e.g, [KG90]).

Kendall’s stastistic can be extended to the multivariate case. Let , be independent copies of a random vector , with independent coordinates . The (empirical) Kendall matrix of is defined to be the matrix whose entries are given by

(2)

Note that the can be written as the sum of rank-one random matrices:

(3)

where the function is taken entrywise.

It is easy to see that for all . Together with (1), it implies that the matrix

is such that and as . This suggests that if the empirical spectral distribution of converges to a Marčenko-Pastur distribution, it should be a standard Marčenko-Pastur distribution. This heuristic argument supports the affine transformation arising in Theorem 1. However, the matrix is not Wishart and the Marčenko-Pastur limit distribution does not follow from standard arguments. Nevertheless, Kendall’s is a -statistic which are known to satisfy the weakest form of universality, namely a Central Limit Theorem under general conditions [Hoe48, dlPG99]. In this paper, we show that in the case of the Kendall matrix, this universality phenomenon extends to the empirical spectral distribution.

Akin to most asymptotic results on -statistics, we utilize a variant of Hoeffding’s (a.k.a. Efron-Stein, a.k.a ANOVA) decomposition [Hoe48]:

(4)

where

It is easy to check that each of the vectors in the right-hand side of (4) are centered and are orthogonal to each other with respect to the inner product where . These random vectors can be expressed conveniently thanks to the following Lemma.

Lemma 2.

For , let denote the cumulative distribution function of .

Fix and let is a random vector with th coordinate given by . Then

Proof.

For any , observe that since the components of have a density, then so that

The observation that follows from the fact that .

∎

Next, note that, the coordinates of each are mutually independent so that and

(7)

where . Theorem 4 implies as and , the empirical spectral distribution of

converges in probability to , where is distributed according to the standard Marčenko-Pastur law with parameter . Moreover,

for some constant independent of . By Lemma 5, the normalized Frobenius norm bounds the Lévy distance between spectral measures. An application of Lemma 5, together with (6), triangle inequality and the above bounds yields the following result.

Proposition 3.

As and , the empirical spectral distribution of

converges in probability to the law of , where is distributed according to the standard Marčenko-Pastur law with parameter .

Let denote the empirical spectral distribution of . Using Lemma 5 once more, we show that the Lévy distance between and converges to zero. This implies Theorem 1 by Proposition 3. To that end, observe that by (5) and triangle inequality:

(8)

To show that (8) goes to zero, we notice that the collection of matrices satisfies

(9)

To see this, expand

(10)

and notice that each expectation is zero unless by Tower property and Lemma 2. Note that when , the expression (10) is bounded by for some . The equation (9) also holds for the collection of matrices and we also have by a similar argument.

Therefore the right side of (8) is bounded by:

for some constant , which vanishes as . This concludes the proof of Theorem 1.

Acknowledgements: The authors would like to thank Alice Guionnet for helpful comments and discussions. A. S. B. was supported by Grant NSF-DMS-1541100. Part of this work was done while A. S. B. was with the Department of Mathematics at MIT. A. L. was supported by Grant NSF-MS-1307704. P. R was supported by Grants NSF-DMS-1541099, NSF-DMS-1541100 and DARPA-BAA-16-46 and a grant from the MIT NEC Corporation.

Appendix A The standard Marčenko-Pastur law

We include here the definition of the standard Marčenko-Pastur law and a bound on the distance between empirical spectral distributions of two matrices.

Theorem 4(Marčenko-Pastur law [BS10, Theorem 3.6]).

Let be independent copies of a random vector such that

Suppose that and define ,

and . Then the empirical spectral distribution of the

matrix

converges almost surely to the standard Marčenko-Pastur law which has density:

Let and be two normal

matrices, with empirical spectral distributions and . Then

where is the Lévy distance between

the distribution functions and .

References

[BS10]

Z. Bai and J. W. Silverstein.

Spectral analysis of large dimensional random matrices.

Springer Series in Statistics. Springer, New York, second edition,

2010.

[BZ08]

Z. Bai and W. Zhou.

Large sample covariance matrices without independence structures in

columns.

Statist. Sinica, 18(2):425–442, 2008.

[CCL+15]

F. Crénin, D. Cressey, S. Lavaud, J. Xu, and P. Clauss.

Random matrix theory applied to correlations in operational risk.

Journal of Operational Risk, 10(4):45–71, December 2015.

[dlPG99]

V. H. de la Peña and E. Giné.

Decoupling.

Probability and its Applications (New York). Springer-Verlag, New

York, 1999.

[EKYY12]

L. Erdős, A. Knowles, H.-T. Yau, and J. Yin.

Spectral statistics of Erdős-Rényi Graphs II:

Eigenvalue spacing and the extreme eigenvalues.

Comm. Math. Phys., 314(3):587–640, 2012.

[Ess24]

F. Esscher.

On a method of determining correlation from the ranks of the

variates.

Scandinavian Actuarial Journal, 1924(1):201–219, 1924.

[Hoe48]

W. Hoeffding.

A class of statistics with asymptotically normal distribution.

Ann. Math. Statistics, 19:293–325, 1948.

[Ken38]

M. G. Kendall.

A new measure of rank correlation.

Biometrika, 30(1/2):81–93, 1938.

[KG90]

M. Kendall and J. D. Gibbons.

Rank correlation methods.

A Charles Griffin Title. Edward Arnold, London, fifth edition, 1990.

[LHY+12]

H. Liu, F. Han, M. Yuan, J. Lafferty, and L. Wasserman.

High-dimensional semiparametric Gaussian copula graphical models.

Ann. Statist., 40(4):2293–2326, 2012.

[Lin25]

J. W. Lindeberg.

Über die korrelation.

Den VI skandinaviske Matematikerkongres i København, pages

437–446, 1925.

[Lin29]

J. Lindeberg.

Some remarks on the mean error of the percentage of correlation.

Nordic Statistical Journal, 1:137–141, 1929.

[O’R12]

S. O’Rourke.

A note on the Marchenko-Pastur law for a class of random matrices

with dependent entries.

Electron. Commun. Probab., 17:no. 28, 13, 2012.

[PA14]

D. Paul and A. Aue.

Random matrix theory in statistics: a review.

J. Statist. Plann. Inference, 150:1–29, 2014.

[YK86]

Y. Q. Yin and P. R. Krishnaiah.

Limit theorems for the eigenvalues of product of large-dimensional

random matrices when the underlying distribution is isotropic.

Teor. Veroyatnost. i Primenen., 31(2):394–398, 1986.