Optimal Trade Execution with Instantaneous Price Impact

and Stochastic Resilience111Financial support through the CRC 649 Economic Risk and d-fine GmbH is gratefully acknowledged. We thank Peter Bank, Rüdiger Frey, Nizar Touzi and seminar participants at various institutions for valuable comments and feedback.

Abstract

We study an optimal execution problem in illiquid markets with both instantaneous and persistent price impact and stochastic resilience when only absolutely continuous trading strategies are admissible. In our model the value function can be described by a three-dimensional system of backward stochastic differential equations (BSDE) with a singular terminal condition in one component. We prove existence and uniqueness of a solution to the BSDE system and characterize both the value function and the optimal strategy in terms of the unique solution to the BSDE system. Our existence proof is based on an asymptotic expansion of the BSDE system at the terminal time that allows us to express the system in terms of a equivalent system with finite terminal value but singular driver.

Keywords: stochastic control, multi-dimensional backward stochastic differential equation, portfolio liquidation, singular terminal value

AMS subject classification: 93E20, 60H15, 91G80

1 Introduction and overview

Let . Let be filtered probability space that carries a -dimensional standard Brownian motion . We assume throughout that is the filtration generated by completed by all the null sets and that . We denote by and , respectively, the set of progressively measurable -valued, respectively, continuous processes that are essentially bounded. denotes the set of progressively measurable -valued processes such that , and denotes the subset of all such processes with continuous sample paths such that . All equations and inequalities are to be understood in the -a.s. sense.

In this paper we address the linear-quadratic non-Markovian stochastic control problem

| (1.1) |

subject to

Here, and are positive constants and and are progressively measurable, non-negative and essentially bounded stochastic processes:

The process is called the state process. It is governed by the control . The processes and are uncontrolled. Control problems of the above form arise in models of optimal portfolio liquidation under market impact with stochastic resilience. In such models denotes the number of shares an investor needs to sell at time , denotes the rate at which the stock is traded at time , and the terminal state constraint is the liquidation constraint. The process describes the persistent price impact caused by past trades in a block-shaped limit order book market with constant order book depth as in Obizhaeva and Wang [19]. One interpretation is that the trading rate adds a drift to an underlying fundamental martingale price process. This results in an execution price process of the form

where denotes the underlying fundamental martingale price process. The process describes the rates at which the order book recovers from past trades. The constant describes an additional instantaneous impact factor as in Almgren and Chriss [1]. The first two terms of running cost term in (1.1) capture the expected liquidity cost resulting from the instantaneous and the persistent impact, respectively. The third term can be interpreted as a measure of the market risk associated with an open position. It penalizes slow liquidation. We allow the risk factor to be stochastic.

The majority of the optimal trade execution literature allows for only one of the two possible price impacts. The first approach, initiated by Bertsimas and Lo [6] and Almgren and Chriss [1], describes the price impact as a purely temporary effect that depends only on the present trading rate and does not influence future prices. The impact is typically assumed to be linear in the trading rate, leading to a quadratic cost term of the form .

In our framework, the special case , , , and corresponds to model of Almgren and Chriss [1]. Their model has been extended by many authors. Closest to our work are the papers by Ankirchner et al. [2], Graewe et al. [10], Horst et al. [13], and Kruse and Popier [17]. They all consider non-Markovian liquidation problems with purely temporary price impact where the cost functional is driven by general adapted factor processes and where the HJB equation can be solved in terms of one-dimensional BSDEs or BSPDEs with singular terminal values, depending on the dynamics of the factor processes. A general class of Markovian liquidation problems has been solved in Schied [22] by means of Dawson–Watanabe superprocess. This approach avoids the use of HJB equations and uses instead a probabilistic verification argument based on log-Laplace functionals of superprocesses.

A second approach, initiated by Obizhaeva and Wang [19] assumes that price impact is persistent with the impact of past trades on current prices decaying over time. When impact is persistent one often allows for both absolutely continuous and singular trading strategies. In [19] the authors assumed constant resilience and market depth. Fruth et al. [7] generalized the model to deterministic time-varying market depths and resiliences and obtained a closed form solution by calculus of variation techniques. In the follow up work [8] the authors allowed for stochastic liquidity parameters. They showed the state space divides into a trade and a no-trade region but did not obtain an explicit description of the boundary. Characterization of optimal strategies results in terms of coupled BSDE systems were obtained by Horst and Naujokat [12] for a model of optimal curve following in a two-sided limit order book. An explicit solution of the related free-boundary problem in a model with infinite time horizon and multiplicative price impact has recently been given by Becherer et al. [5].

In this paper we analyze a stochastic control problem arising in models of optimal trade execution with both instantaneous and persistent price impact where only absolutely continuous trading strategies are admissible. Economically, the restriction to absolutely continuous strategies means that the instantaneous impact is the dominating factor. Mathematically, it allows us to formulate the resulting control problem within in a classical, rather than singular stochastic control framework, and to obtain a closed form solution for both, the value function and the optimal trading strategy. Characterizing the value function is typically hard if singular controls are allowed. In fact, when both absolutely continuous and singular controls are admissible as in e.g. [12], one typically only obtains characterization results for optimal controls using maximum principles.

Within our modeling framework, the value function can be represented in terms of the solution to a fully coupled three-dimensional stochastic Riccati equation (BSDE system). For the benchmark case of constant model parameters the stochastic system reduces to a deterministic ODE system. For this case we illustrate how our model can be used to approximate liquidation models with block trades and can, hence, be viewed as a first step towards a unified approach to singular and regular stochastic control problems with singular terminal values.

While uncoupled ODE, respectively, BSDE systems arise in the trade execution models of Gatheral and Schied [9] or Kratz [16], respectively, Ankirchner and Kruse [3], our model seems to be the first that requires the analysis of multi-dimensional BSDE systems. In proving the existence of a unique solution to the BSDE system that describes the value function two challenges need to be overcome. First, the liquidation constraint imposes a singular terminal condition on the first component of the BSDE system. Second, our BSDE system does not satisfy the quasi-monotonicity condition that is necessary for the multi-dimensional comparison principle in [14] to hold. In a one-dimensional setting BS(P)DEs with singular terminal values are well understood and an array of existence of solution results and comparison principles has been obtained in the literature. The majority of the existing results including [2, 10, 13, 17] rely on a finite approximation of the singular terminal value. The (minimal) solution with singular terminal value is then obtained by a monotone limit argument.

We extend the asymptotic expansion approach introduced in Graewe et al. [11] to BSDE systems. The idea is to determine the precise asymptotic behavior of a potential solution to the BSDE system at the terminal time by finding appropriate a priori estimates. The asymptotics of the solution at the terminal time allows us to characterize the solution to the BSDE system with singular terminal value in terms of a BSDE with finite terminal value yet singular driver, for which the existence of a solution in a suitable space can be proved using standard fixed point arguments. Finally, we establish the verification result from which we deduce uniqueness of solutions to the BSDE system as well as a closed-form representation of the optimal trading strategy.

Establishing the a priori estimates for our BSDE system is key for both the proof of existence of a solution and the verification theorem. As pointed out above the BSDE system that characterizes the value does not satisfy the quasi-monotonicity condition of Hu and Peng [14]. In order to overcome this problem we consider the joint dynamics of the BSDE that describes the value function and two additional BSDEs that describe the candidate optimal trading strategy. Using the comparison principle for BSDE systems in [14] we first determine the range of all these processes from which we then deduce the desired deterministic upper bounds for the coefficients of the value function.

The remainder of this paper is structured as follows. The stochastic control problem is formulated in Section 2. The a priori estimates and asymptotic behavior of the solution is established in Section 3. Existence to the HJB equation is proven in Section 4. The verification argument is carried out in Section 5. In Appendix A we recall the multi-dimensional comparison principle for BSDEs and formulate a local -existence result for BSDEs with locally Lipschitz drivers.

Notational convention. Whenever the notation appears we mean that the statement holds for all the when is replaced by , e.g., . Furthermore, for we mean by - that for every there exists such that for all , -a.s.

2 Main result

For any initial state we define by

| (2.1) |

the value function of the stochastic control problem (1.1) with respect to the state dynamics

where only those controls or (trading) strategies belong to the class of admissible controls that satisfy the terminal state constraint

Assumption 2.1.

We assume throughout that the coefficients to the control problem satisfy

Remark 2.2.

Notice that for any (admissible) control as and

We solve the control problem by solving the corresponding stochastic Hamilton-Jacobi-Bellman (HJB) equation. Stochastic HJB equations for non-Markovian control problems were first introduced by Peng [21]. In our model the stochastic HJB equation is given by the first-order stochastic partial differential equation,

| (2.2) |

Definition 2.3.

A pair of random fields is called a classical solution to the above equation if it satisfies the following conditions:

-

•

for each , is continuously differentiable in and ,

-

•

for each , ,

-

•

for each , ,

-

•

for all and it holds that

We prove the existence of a unique classical solution to the equation (2.2) and show that the value function is given by the random field . The linear-quadratic structure of the control problem suggest the ansatz

| (2.3) |

for the solution to the HJB equation. The following lemma shows that this ansatz reduces our HJB equation to the following three-dimensional stochastic Riccati equation:

| (2.4) |

Lemma 2.4.

Proof.

In order to guarantee the uniqueness of a solution to the HJB equation we need to impose a suitable terminal condition. Due to the terminal state constraint we expect the trading rate to tend to infinity for any non-trivial initial position as . We further expect the resulting trading cost to dominate any resilience effect. As a result, we expect that

where denotes the value function corresponding to the control problem with . If , then and

independently of the strategy . Hence,

where is characterized in [2, 11] as the unique solution to the BSDE with singular terminal value

We therefore expect the coefficients of the linear-quadratic ansatz (2.3) to satisfy

| (2.6) |

The next theorem establishes an existence of solutions result for the BSDE system (2.4) when imposed with the singular terminal condition (2.6). The proof is given in Section 4. It is based on a multi-dimensional generalization of the asymptotic expansion approached introduced in [11].

Theorem 2.5.

The next theorem verifies the preceding heuristics; its proof is given in Section 5. In particular, it states that the value function is indeed of the form (2.3). As a result, there exists at most one solution to the BSDE system (2.4) that satisfies (2.6).

Theorem 2.6.

Example 2.7.

In a deterministic benchmark model with a risk neutral investor and constant deterministic resilience the above BSDE system reduces to the following ODE system:

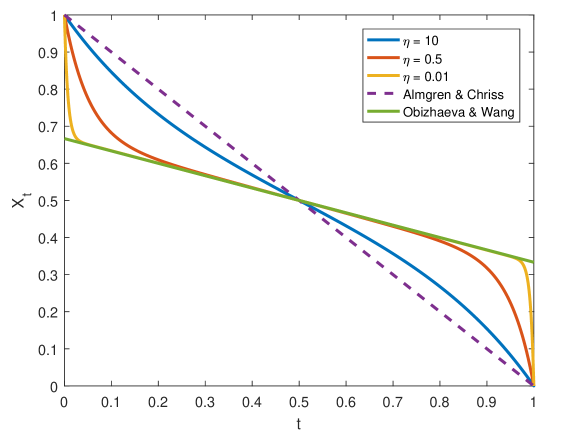

Using the asymptotic expansion introduced in (4.1) the above ODE system can be solved by solving the corresponding ODE system (4.2). That ODE system has finite terminal values yet singular nonlinearity. It can be solved numerically using the MATLAB package bvpsuite [15]. This package is designed for solving ODE systems with regular singular points. The optimal trading strategies for different choices of the instantaneous impact factor and the optimal trading strategies of the benchmark models by Almgren and Chriss [1] and Obizhaeva and Wang [19] are depicted in Figure 1.

As we see, the optimal trading strategy resembles that of the Almgre and Chriss model for large instantaneous impact factors while it resembles that of the Obizhaeva and Wang model with singular controls for small instantaneous impact factors. This suggests that our model can be viewed as a blend of the two extreme cases with only instantaneous, respectively, only persistent market impact.

3 A Priori Estimates

In this section we establish a priori estimates for the BSDE system (2.4). The estimates will be key for both, the proof of the existence of solutions and the verification theorem. Throughout, let

denote any solution to (2.4) that satisfies (2.6). It will be convenient to also consider the processes

that appear in the feedback form (2.5) of the candidate optimal control. The equations for and read:

and

In order to establish the a priori estimates we first determine the range of the processes . The proof of the following lemma uses the multi-dimensional comparison principle for BSDEs, due to Hu and Peng [14] presented in the Appendix.

Lemma 3.1.

It holds that and , -a.e.

Proof.

We first note that together with the -convergence of and as implies and hence .

The nonpositivity of follows from the solution formula for linear BSDEs with essentially bounded coefficients [20, Proposition 5.31]. Indeed, from

we obtain that

| (3.1) |

The non-negativity of follows from similar arguments. In fact,

Even though is singular at , we may apply the solution formula on for all . This yields,

| (3.2) |

The -convergence of to as together with the fact that implies that is essentially bounded below on . Since and are essentially bounded we can apply the dominated convergence theorem to interchange the limit and the expectation in (3.2) when letting in (3.2). As a result, because and because

In order to prove that we need we need to consider their joint dynamics. First, due to the (improper) -convergence of and as there exists a deterministic time such that on . Let us consider the BSDE system for and on :

Since , , and are essentially bounded on we may assume without loss of generality by a standard truncation argument in the -variable that this system is -a.e. uniformly Lipschitz continuous in and . Furthermore, the system is quasi-monotone because . Hence, we may apply the comparison theorem for multi-dimensional BSDEs given in Proposition A.1 in the Appendix with

(up to truncation in ) and terminal conditions and , respectively. As the unique solution to the first BSDE system satisfies , we see that for all . Hence the process is non-negative.

Finally, we conclude from and that . ∎

We are now ready to establish the a priori estimates.

Proposition 3.2.

In terms of the following a priori estimates hold -a.e.:

Proof.

Since we may write the BSDE for in monotone form. That is,

The lower and upper estimate for solve

and

respectively. The preceding equations are time-homogeneous. Thus, for any the processes and still satisfy the respective equations but with singularities at and , respectively. Since is essentially bounded on and in there exits such that on . Because and , we have for all ,

Hence, the classical one-dimensional comparison theorem for BSDEs with monotone drivers [20, Proposition 5.33] yields on . Finally, letting yields on by the continuity of .

In order to establish on one argues similarly. In this case the comparison argument is justified by the inequality

Next, we establish the upper estimate for . Since we may again assume that the BSDE for is monotone, that is

Since we have for all that

| (3.3) |

Let us consider for the deterministic process

Then,

Hence, recalling (3.3), the one-dimensional comparison theorem implies

Since , letting completes the proof.

Finally, to establish the lower estimate for one notices that solves

and is hence a subsolution to the BSDE for . At this point, we already know that the potential singular term in the BSDE for behaves well (being bounded by ) on the entire interval . Hence, no shifting argument at the terminal time is needed in this step and we conclude directly by comparison that . ∎

From the a priori estimates we obtain the asymptotic behavior of our BSDE system at the terminal time as stated in the following corollary. The asymptotic at the terminal time is key to our existence result.

Corollary 3.3.

The following asymptotic behaviors hold in as :

Proof.

The asymptotic behavior of and follows directly from the a priori estimates given above. The asymptotic order of follows from (3.1) and in as . ∎

4 Existence

In this section we prove Theorem 2.5, i.e. the existence of a solution to the BSDE syetem (2.4) that satisfies the singular terminal condition (2.6). Similarly as in [11], our proof of existence is based on the asymptotic behavior established in Corollary 3.3. It suggests the following asymptotic ansatz:

| (4.1) | ||||||

where the asymptotic order of and is raised artificially for similar reasons as in [11, Remark 4.2] to obtain the locally Lipschitz type statement given in Lemma 4.1(ii) below, while the reduced order of unifies the notation and allows us to solve for all three processes in the same weighted -space.

The asymptotic ansatz (4.1) reduces the original system (2.4) to

| (4.2) |

We define such that we have

as a compact notation for (4.2) by identifying and . For specified below, we will establish the existence of a short-time solution to (4.2) in the space

endowed with the norm

Since this means that we are looking for a fixed point in of the operator

Lemma 4.1.

The following holds:

-

(i)

is complete.

-

(ii)

For every there exists a constant (independent of ) such that

Proof.

The spaces and are isometrically isomorphic by identifying with the process in . Hence is complete.

In order to establish the Lipschitz continuity, let be the line segment connecting and . By the mean value theorem we have for , -a.e.,

| (4.3) |

where it is used that the line is contained in , -a.e. But,

from which we see that the supremum in (4.3) is essentially bounded on . ∎

Choosing and appropriately the preceding lemma allows us to use a standard fix-point argument to show that has a unique fix-point. The fix-point is just a local solution to (4.2).

Proposition 4.2.

For sufficient small there exists a short-time solution to (4.2).

Proof.

Let us fix and choose as in Lemma 4.1. For it then holds -a.e.,

This yields, as long as ,

Hence, is an -contraction on . Furthermore, maps onto itself. Indeed, for all it holds -a.e.,

As a result, has a unique fixed point . The process satisfies

By the martingale representation theorem there exits a process such that

Hence, gives the desired short-time solution to (4.2). ∎

We are now ready to prove Theorem 2.5.

Proof of Theorem 2.5.

The short-time solution to (4.2) established by Proposition 4.2 gives in terms of the ansatz (4.1) a short-time solution

to (2.4) that satisfies the singular terminal condition (2.6). In order to see that this short-time solution extends to a global solution in notice first that the system (2.4) satisfies the assumptions of the local -existence results for BSDEs with locally Lipschitz drivers of Lemma A.2 given in the appendix. Hence, the system (2.4) imposed with the essentially bounded terminal value admits an essentially bounded local extension on .

Due to the a priori estimates given in Proposition 3.2 we know that this local extension will stay (recalling ) in the bounded region . When iterating this extension procedure we may therefore choose (cf. the proof of Lemma A.2) step by step the same local Lipschitz constant for the system (2.4), which results in a constant length of the extension interval. Thus, after finitely many steps we obtain a global extension on . ∎

5 Verification

This section devoted to the verification statement of Theorem 2.6. Throughout, let

denote any solution to (2.4) that satisfies (2.6) and recall that the candidate optimal strategy is given in terms of the processes

for which a priori estimates have been established in Section 3. The proof of the admissibility of uses the following iterated integral version of Gronwall’s inequality.

Lemma 5.1 ([4, Corollary 11.1]).

Let , , and be nonnegative continuous functions on with and being nondecreasing, and suppose

where is a nonnegative continuous function on . Then

We are now ready to verify that the candidate optimal control is indeed admissible.

Lemma 5.2.

The feedback control given in (2.5) is admissible.

Proof.

Let us fix an initial state . The dynamics of the state process under the candidate optimal control is given by:

| (5.1) |

Due to the singularity of at the terminal time, it is not clear yet that the solution to (5.1) is well-defined at the terminal time; a priori we only know that .

In order to show that we first apply the variation of constants formula for to get:

and

| (5.2) |

Hence, the process satisfies,

Since , this yields,

By the iterated integral version of Gronwall’s inequality (Lemma 5.1),

| (5.3) | ||||

In view of the a priori upper bounds on and , because the antiderivative of is given by and because ,

Along with (5.3) this shows that is bounded as . Therefore, this time using the a priori lower bound for ,

| (5.4) | ||||

This shows that . It also shows that in as . As it follows that

The boundedness of again implies by (5.2) that . Hence, we conclude

This proves that is indeed admissible. ∎

Lemma 5.3.

For every it holds

Proof.

Recalling , , and , it follows by the dominated convergence theorem,

Furthermore, note that by and Jensen’s inequality,

Hence, by Corollary 3.3,

We are now ready to prove the verification theorem.

Proof of Theorem 2.6.

By a slight abuse of notation we define within this proof the random fields and by the linear-quadratic ansatz (2.3) and verify that this gives indeed the value function of the control problem. For the moment we only know that is a classical solution the HJB equation (2.2).

Let us fix an initial state and admissible control . For we define the stopping time

Since solve the HJB equation, it holds by the Itô-Kunita formula [18, Theorem I.8.1] for all ,

| (5.5) | ||||

The above stochastic integral stopped at is a true martingale. Hence,

| (5.6) |

Since the coefficients of the random field are essentially bounded on , since , and because and , it follows by Hölder’s inequality that

Hence, the dominated convergence theorem applies when letting in (5.6), which yields,

| (5.7) |

Hence, by Lemma 5.3 and again the dominated convergence theorem letting yields,

| (5.8) |

Finally note that since the feedback control attains the infimum in (5.5) it holds equality in (5.6)–(5.8) if ∎

6 Conclusion

In this paper we analyzed a novel stochastic optimal control problem arising in models of optimal trade execution with instantaneous and persistent price impact and stochastic resilience. Assuming that the instantaneous impact factor is constant but allowing for stochastic resilience and market risk we characterized the value function in terms of the unique solution to a three-dimensional stochastic Riccati equation with singular terminal condition in the first component. Our existence of solutions results used an extension of the asymptotic expansion approach introduced in [11] to a multi-dimensional setting. Several open problems remain. First, we cannot guarantee non-negativity of the trading rate. Intuitively, price-triggered round trips should not be beneficial if . Based on our analysis, they can not be ruled out, though. Second, the assumption that and are constant was important to establish the a priori estimates. An extension to more general impact factors, especially a random impact factor is certainly desirable as suggested in [8]. Third, a numerical analysis of a deterministic benchmark model suggests that our model can be viewed as a approximation to a model with both absolutely continuous and singular controls if . While a formal proof of this limit result in a general non-Markovian framework would certainly be desirable it is clearly beyond the scope of the present paper.

Appendix A Appendix

A necessary and sufficient condition under which the comparison theorem holds for multi-dimensional BSDEs has been first given by Hu and Peng [14]. The equivalent quasi-monotonicity condition (iv) below can be found in [24, Theorem 3.1]. The comparison results in [14, 24] are stated under an additional continuity condition on the drivers that is not satisfied in our model. However, the continuity condition is only needed to prove that if a comparison principle holds, then the system is necessarily quasi-monotone. Continuity is not needed for the converse implication. As such, their results are in fact applicable to our framework. Even though, for the reader’s convenience we refer instead to a comparison result for multi-dimensional reflected BSDEs by Wu and Xiao [23] that is formulated explicitly under the weaker regularity assumption (i) given below.

Proposition A.1 ([23, Theorem 3.1]).

Let , , be solutions to the BSDEs

with the drivers , , satisfying

-

(i)

for all and ,

-

(ii)

there exits such that for all and ,

and suppose, in addition,

-

(iii)

,

-

(iv)

for every it holds for all and such that , , , :

Then , .

Below we state a local -existence result for BSDEs with locally Lipschitz drivers not depending on . The result seems well well-known; we give it for completeness. Specifically, we consider the BSDE

| (A.1) |

where we assume that the terminal value

-

•

is essentially bounded and that the driver satisfies

-

•

,

-

•

for every there exists such that for all ,

(A.2)

Lemma A.2.

Under the above assumptions there exits such that there exits on a short-time solution to (A.1).

Proof.

We will show that one may choose , where is the Lipschitz constant given in (A.2) with respect to .

With we define the operator by

Then is a contraction on : For all it holds -a.e.,

Furthermore, maps into itself: For all it holds -a.e.,

Hence, has a unique fixed point in . By the martingale representation theorem, this fixed point gives the desired solution. ∎

References

- [1] R. Almgren and N. Chriss, Optimal execution of portfolio transactions, J. Risk, 3 (2001), pp. 5–39.

- [2] S. Ankirchner, M. Jeanblanc, and T. Kruse, BSDEs with singular terminal condition and control problems with constraints, SIAM J. Control Optim., 52 (2014), pp. 893–913.

- [3] S. Ankirchner and T. Kruse, Optimal position targeting with stochastic linear-quadratic costs, Banach Center Publ., 104 (2015), pp. 9–24.

- [4] D. Bainov and P. Simeonov, Integral Inequalities and Applications, vol. 57 of Mathematics and Its Applications: East European Series, Kluwer, 1992.

- [5] D. Becherer, T. Bilarev, and P. Frentrup, Optimal liquidation under stochastic liquidity. arXiv:1603.06498, Apr. 2017.

- [6] D. Bertsimas and A. W. Lo, Optimal control of execution costs, J. Financ. Markets, 1 (1998), pp. 1–50.

- [7] A. Fruth, T. Schöneborn, and M. Urusov, Optimal trade execution and price manipulation in order books with time-varying liquidity, Math. Finance, 24 (2014), pp. 651–695.

- [8] , Optimal trade execution in order books with stochastic liquidity. Unpublished preprint, http://homepage.alice.de/murusov/papers/fsu-optimal_execution_stochastic.pdf, Sept. 2015.

- [9] J. Gatheral and A. Schied, Optimal trade execution under geometric Brownian motion in the Almgren and Chriss framework, Int. J. Theor. Appl. Finance, 14 (2011), pp. 353–368.

- [10] P. Graewe, U. Horst, and J. Qiu, A non-Markovian liquidation problem and backward SPDEs with singular terminal conditions, SIAM J. Control Optim., 53 (2015), pp. 690–711.

- [11] P. Graewe, U. Horst, and E. Séré, Smooth solutions to portfolio liquidation problems under price-sensitive market impact. To appear in Stochastic Process. Appl., 2017.

- [12] U. Horst and F. Naujokat, When to cross the spread? Trading in two-sided limit order books, SIAM J. Financial Math., 5 (2014), pp. 278–315.

- [13] U. Horst, J. Qiu, and Q. Zhang, A constrained control problem with degenerate coefficients and degenerate backward SPDEs with singular terminal condition, SIAM J. Control Optim., 54 (2016), pp. 946–963.

- [14] Y. Hu and S. Peng, On the comparison theorem for multidimensional BSDEs, C. R. Acad. Sci. Paris, Ser. I, 343 (2006), pp. 135–140.

- [15] G. Kitzhofer, O. Koch, G. Pulverer, C. Simon, and E. Weinmüller, The new MATLAB code bvpsuite for the solution of singular implicit BVPs, J. Numer. Anal. Indust. Appl. Math., 5 (2010), pp. 113–134.

- [16] P. Kratz, An explicit solution of a nonlinear-quadratic constrained stochastic control problem with jumps: Optimal liquidation in dark pools with adverse selection, Math. Oper. Res., 39 (2014), pp. 1198–1220.

- [17] T. Kruse and A. Popier, Minimal supersolutions for BSDEs with singular terminal condition and application to optimal position targeting, Stochastic Process. Appl., 126 (2016), pp. 2554–2592.

- [18] H. Kunita, Stochastic differential equations and stochastic flows of diffeomorphisms, in École d’Été de Probabilités de Saint-Flour XII - 1982, P. L. Hennequin, ed., vol. 1097 of Lecture Notes in Mathematics, Springer, 1984, pp. 143–303.

- [19] A. Obizhaeva and J. Wang, Optimal trading strategy and supply/demand dynamics, Journal of Financial Markets, 15 (2013), pp. 1–31.

- [20] E. Pardoux and A. Răşcanu, Stochastic Differential Equations, Backward SDEs, Partial Differential Equations, vol. 69 of Stochastic Modelling and Applied Probability, Springer, 2014.

- [21] S. Peng, Stochastic Hamiltonian-Jacobi-Bellman equations, SIAM J. Control Optim., 30 (1992), pp. 284–304.

- [22] A. Schied, A control problem with fuel constraint and Dawson–Watanabe superprocesses, Ann. Appl. Probab., 23 (2013), pp. 2472–2499.

- [23] Z. Wu and H. Xiao, Multi-dimensional reflected backward stochastic differential equations and the comparison theorem, Acta Math. Sci. Ser. B Engl. Ed., 30 (2010), pp. 1819–1836.

- [24] Y. Xu, Multidimensional dynamic risk measure via conditional -expectation, Math. Finance, 26 (2016), pp. 638–673.