Exploring the Vickrey-Clarke-Groves Mechanism for Electricity Markets

Abstract

Control reserves are power generation or consumption entities that ensure balance of supply and demand of electricity in real-time. In many countries, they are operated through a market mechanism in which entities provide bids. The system operator determines the accepted bids based on an optimization algorithm. We develop the Vickrey-Clarke-Groves (VCG) mechanism for these electricity markets. We show that all advantages of the VCG mechanism including incentive compatibility of the equilibria and efficiency of the outcome can be guaranteed in these markets. Furthermore, we derive conditions to ensure collusion and shill bidding are not profitable. Our results are verified with numerical examples.

keywords:

Electrical networks, game theory, optimization, control reserves.1 Introduction

The liberalization of electricity markets leads to opportunities and challenges for ensuring stability and efficiency of the power grid. For a stable grid, the supply and demand of electricity at all times need to be balanced. This instantaneous balance is reflected in the grid frequency. Whereas scheduling (yearly, day-ahead) is based on forecast supply and demand of power, the control reserves (also referred to as ancillary services) provide additional controllability to balance supply and demand of power in real-time. With increasing volatile renewable sources of energy, the need for control reserves also has increased. This motivates analysis and design of optimization algorithms and market mechanisms that procure these reserves.

The objective of this paper is a game theoretic exploration of an alternative market mechanism for the control reserves with potential improvements. To further discuss this, we briefly discuss relevant features of the existing market mechanism. Control reserves are categorized as primary, secondary, and tertiary. Primary reserves balance frequency deviations in timescale of seconds. Secondary reserves balance the deviations on a timescale of seconds to minutes not resolved by primary control. Tertiary reserves restore secondary reserves and typically act 15 minutes after a disturbance to frequency. The secondary and tertiary control reserves in several countries are procured in a market. In the Swiss market for example, the auction mechanism implemented by the Transmission System Operator (TSO) minimizes the cost of procurement of required amounts of power, given bids (Abbaspourtorbati and Zima, 2016).

In a pay-as-bid mechanism, since payments to winners are equal to their bid prices, a rational player may over-bid to ensure profit. As an alternative to pay-as-bid, we explore the Vickrey Clarke Groves (VCG) mechanism. This is one of the most prominent auction mechanisms. The first analysis of the VCG mechanism was carried out by (Vickrey, 1961) for the sale of a single item. This work was subsequently generalized to multiple items by (Clarke, 1971) and (Groves, 1973).

It has been shown that the VCG mechanism is the only mechanism that possesses efficiency and incentive compatibility. Efficiency implies that goods are exchanged between buyers and sellers in a way that creates maximal social value. Incentive compatibility means that it is optimal for each participant to bid their true value. Variants of the VCG mechanism have been successfully deployed generating billions of dollars in Spectrum auctions, for instance, in the 2012 UK spectrum auction (Cramton, 2013; Day and Cramton, 2012) and in advertising, for instance, by Facebook111https://developers.facebook.com/docs/marketing-api/pacing (Varian and Harris, 2014). For further discussion on the VCG mechanism and its application to real auctions we recommend (Milgrom, 2004; Klemperer, 2004).

Investigation must be performed before applying the VCG mechanism. As outlined in the paper of Ausubel and Milgrom (Ausubel et al., 2006), coalitions of participants can influence the auction in order to obtain higher collective profit. These peculiarities occur when the outcome of the auction is not in the core. The core is a solution concept in coalition game theory where prices are distributed so that there is no incentive for participants to leave the coalition (Osborne and Rubinstein, 1994). This has recently motivated the study and application of VCG auctions where the outcome is projected to the core (Cramton, 2013; Abhishek and Hajek, 2012).

The electricity market can be thought of as a reverse auction. In contrast to an auction with multiple goods, in an electricity market, each participant can bid for continuum values of power. Furthermore, to clear this market, certain constraints, such as balance of supply and demand and network constraints need to be guaranteed. Due to the differences between an electricity market and an auction mechanism for multiple items (such as spectrum or adverts), there are conceptual and theoretical advances in VCG mechanism that need to be analyzed.

In this paper, we apply the VCG mechanism to control reserve markets and provide a mathematically rigorous analysis of it. We show that efficiency and incentive compatibility of the VCG mechanism will hold even in the case of stochastic markets, see Theorem 1. On the other hand, we provide examples where shill bidding might occur. The remainder of the paper develops ways to resolve this issue. In particular, building upon a series of results based on coalitional game theory, in Theorem 4 we show how a simple pay-off monotonicity condition removes incentives for shill bidding and other collusions. The proofs developed significantly simplify the arguments of Ausubel and Milgrom (Ausubel et al., 2006).

The paper is organized as follows. In Section 2 we introduce the VCG mechanism for control reserve markets, analyzing its positive and negative aspects. Throughout Section 3 we investigate conditions that can mitigate these problems making the mechanism competitive. We conclude with specific simulations based on data available from Swissgrid (the Swiss TSO) showing the applicability of VCG mechanism to the Swiss ancillary service market.

2 Electricity auction market setup

We briefly describe the control reserve market of Switzerland. The formulation and results derived are generalizable to alternative markets, with similar features as will be discussed. The Swiss system operator (TSO), Swissgrid, procures secondary and tertiary reserves in its reserves markets. These consist of a weekly market where secondary reserves are procured and daily markets where both secondary and tertiary reserves are procured. Each market participant submits a bid that consists of a price per unit of power (CHF/MW, swiss franc per megawatt) and a volume of power which it can supply (MW). Offers are indivisible and thus, must be accepted entirely or rejected. Moreover, conditional offers are accepted. This means that a participant can offer a set of bids, of which only one can be accepted. If an offer is accepted, the participant is paid for its availability irrespective of whether these reserves are deployed (an additional payment is made in case of deployment). This availability payment, under the current swiss reserve market, is pay-as-bid. An extensive description of the Swiss Ancillary market is given in (Abbaspourtorbati and Zima, 2016).

We abstract the control reserve market summarized above as follows. Let denote the set of auction participants and . Let be all the bids placed by participant , where is the vector of power supplies offered (MW) and are their corresponding requested costs (or prices). Here is the number of bids from participant . Let be the set of all bids and . Given a set , a mechanism defines which bids are accepted with a choice function, and a payment to each participant, payment rule . The utility of participant is hence

| (1) |

where is participant ’s true cost of providing the offered power and is the binary vector indicating his accepted bids.

The transmission system operator’s objective function is

The variable selects the accepted bids, can be any additional variables entering the TSO’s optimization and is a general function. In most electricity market, the objective is to minimize the cost of procurement subject to some constraints:

| (2a) | |||

| (2b) | |||

The above constraints correspond to procurement of the required amounts of power, e.g. in the Swiss reserve markets accepted reserves must have a deficit probability of less than 0.2%. We let be the feasible values of for this optimization. The optimization defines a general class of models, where the cost function is affine in and the prices of bids do not enter the constraints.

2.1 The pay-as-bid mechanism

In the current pay-as-bid mechanism we recognize:

It follows that each participant’s utility is . As such, rational participants would bid more than their true values to make profit. Consequently, under pay-as-bid, the TSO attempts to minimize inflated bids rather than true costs. Thus, pay-as-bid cannot guarantee power reserves are procured cost effectively.

2.2 The VCG mechanism

The VCG mechanism is characterized with the same choice function as the pay-as-bid mechanism but a different payment rule.

Definition 1

The Vickrey-Clarke-Groves (VCG) choice function and payment rule are defined as:

where denotes the vector of bids placed by all participants excluding . The function must be carefully chosen to make the mechanism meaningful. Namely, we require that payments go from the TSO to power plants, positive transfers, and that power plants will not face negative utilities participating to such auctions, individual rationality. A particular choice of is the Clarke pivot-rule, which minimizes the procurement cost given all bids excluding ’s:

A set of bids is a dominant-strategy Nash equilibrium if for each participant ,

Moreover, a dominant-strategy equilibrium is incentive compatible if where is the true cost of power , as given in (1). That is, each participant finds it more profitable to bid truthfully , rather than any other vector , regardless of other participants’ bids. Hence, all the bidding strategies are dominated by strategy .

The following theorem summarizes the contributions of (Vickrey, 1961), (Clarke, 1971) and (Groves, 1973) in designing the VCG mechanism. In our proof, we are mindful of the slightly non-standard setting of the electrical markets: that auctions are “reverse-auctions”, i.e. with a single buyer and many sellers, and that constraints in the optimization problem may be non-standard.

Theorem 1

Given the clearing model of (2).

-

a)

The energy procurement auction under VCG choice function and payment rule is a Dominant-Strategy Incentive-Compatible (D.S.I.C) mechanism.

-

b)

The VCG outcomes are efficient, that is, the sum of all the utilities is maximized.

-

c)

The Clarke pivot rule ensures positive transfers and individual rationality.

a) We distinguish between the participant placing a generic bid and biding truthfully . For , substituting the VCG choice function and payment rule with as in (2):

where the term in brackets is the cost of but evaluated at . For , however, . Note that

We then have because is a feasible suboptimal allocation for the available bids .

b) Let denote the utility gained by the TSO, that is, . By Definition (1) and incentive compatibility, . We then have: . Hence, , which is maximized by the clearing model (2).

c) This can be easily verified substituting :

| (3) |

In summary, all producers have incentive to reveal their true values for price of power in a VCG market. Thus, it becomes easier for entities to enter the auction, without spending resources in computing optimal bidding strategies. This can help in achieving market liberalization objectives. Moreover, from the above theorem it follows that the winners of the auctions are the producers with the lowest true values. This is because participants bid truthfully and the VCG choice function minimizes the cost of the accepted bids.

Note that the result above are very general. We do not need to assume any particular form for the term and the constraints . Furthermore, using the exact same approach in the proof, we can state the exact same theorem for the case in which the participants provide continuous bid curves: , where . The difference is only in notation; we use for the optimal bid accepted from player instead of the binary variables .

So, there are persuasive arguments for considering VCG market for control reserves. However, there are potential disadvantages that must be eliminated.

Example 1

Suppose the TSO has to procure 800 MW from PowerPlant1, , who bids CHF for 800 MW, and PowerPlant2, , who bids CHF for 800 MW. Under the VCG mechanism, PowerPlant1 wins the auction receiving a payment of CHF. Suppose now that power plants and entered the auction each bidding 0 CHF for 200 MW. Clearly, the new entrants become winners and each of them would receive a VCG payment of CHF.

This example shows that: (a) producers with very low prices (in this case 0 CHF) could receive very high payments; (b) collusion or shill bidding can increase participants’ profits. In fact, and could be a group of losers who jointly lowered their bids to win the auction, or they could represent multiple identities of the same losing participant (i.e. a power plant with true value greater than 40’000 CHF for 800 MW). Entering the auction with four shills, however, this participant would have received a payment of 440’000 CHF.

Our goal is now to derive conditions that make VCG outcomes competitive and prevent shill bidding or collusion.

3 Solution approach for VCG market

In coalition game theory, the core is the set of allocations of goods that cannot be improved upon by the formation of coalitions. (Ausubel et al., 2006) identify conditions for a VCG outcome to lie in the core. Following their analysis we derive conditions for core outcomes in our setting and provide new simpler proofs relevant to our problem formulation that show that shill bidding and collusion can be eliminated from certain class of electricity markets under the VCG mechanism.

Given a game where is the set of participants, let denote the coalitional value function

This function provides the optimal objective function, for any subset of participants that includes the TSO. Here, is the cost the TSO incurs for the VCG outcome with participants . That is, is the solution to optimization (2) with for all , and with additional constraints that for all . Clearly for since increasing participation reduces costs. We thus let represent the coalition game associated with the auction.

Definition 2

The is defined as follows

The core is thus the set of all the feasible outcomes, coming from an efficient mechanism (first equality above), that are unblocked by any coalition (the inequality). We say that an outcome is competitive if it lies in the core; that is, there is no incentive for forming coalitions. In the previous example, the outcome was not competitive because it was blocked by coalition . PowerPlant1 was offering only 40’000 CHF for the total amount of 800 MW. It will be also shown in Theorem 4 that core outcomes eliminate any incentives for collusions and shill bidding.

3.1 Ensuring core payments

Since core outcome is a competitive outcome, we investigate under which conditions the outcomes of the VCG mechanism applied to the control reserve market will be in the core. Note that there are constraints that define a core outcome. Our first Lemma provides an equivalent characterization of the core with significantly lower number of constraints.

Lemma 1

Given a VCG auction , let be its outcome and the corresponding winners. Assuming participants revealed their true values, if and only if, ,

| (4) |

Core constraints with are immediately satisfied as (individual rationality, Theorem 1c). Now, is unblocked by any (since is the outcome with participants). Thus, . Moreover, fixing , the dominant constraints are those corresponding to minimal , in particular, when (this being maximal set with not taking part in the coalition ). Finally recall from (3) that, under the VCG mechanism, . \qed The following definition and theorem act over subsets of participants. Here, we imagine that there is a set of potential participants and, for each subset of , we consider whether the outcome of the auction with L participants lies in the core.

Definition 3

Participant displays payoff monotonicity if ,

| (5) |

Theorem 2

The outcome of the VCG auction lies in the core for all if and only if payoff monotonicity holds for each participant in .

To prove that payoff monotonicity is sufficient for to lie in the core, we prove that (4) holds. Let . Considering , we notice that:

since displays payoff monotonicity over ; we also have since displays payoff monotonicity over . We can continue with the same considerations up to since displays payoff monotonicity over . Therefore, . This same argument holds for any subset of participants and . Thus (4) holds and so, by Lemma 1, the VCG outcome belongs to the core.

To prove that payoff monotonicity is also necessary for outcomes to lie in the core, suppose that does not display payoff monotonicity. Then, there exist sets , where (5) does not hold. We may chose for some . To see this, take and with , then, since payoff monotonicity does not hold,

| (6) | |||

The strict inequality above must hold for one of the summands . So we may consider sets that differ by one participant, say . Let and be the minimal such sets. By minimality, for . Further, after rearranging the above inequality we see that . That is both participant and are winners of the VCG auction with participants (instead of ). Then, considering Lemma 1 for the auction with , and , we have: . Thus (4) does not hold since the outcome is blocked by coalition .\qed Whether a VCG outcome is competitive hence depends on a particular property of the optimal cost . Namely, has to make (5) hold for each . Note that a similar result was proven in (Ausubel et al., 2006), for a sale auction of a finite number of objects, without any constraints. Our result generalizes this to markets with continuous goods and arbitrary social planner objectives of the form (2).

3.2 Single stage electricity procurement auction

The class of auctions cleared by (2) is very general and suitable for mechanisms with multiple stages of decisions. We will see, in fact, how the two-stages Swiss clearing model described in (Abbaspourtorbati and Zima, 2016) can be abstracted as in (2). But first, we start considering simpler auctions, characterized by single-stage decisions. More specifically, energy procurement auctions where the TSO has to procure a fixed amount of MW, subject to conditional offer constraints. Hence, we consider auctions cleared by:

| (7a) | ||||

| s.t. | ||||

| Note that the last constraint above ensures that each bidder can only have one offer accepted. We further suppose that the power offered by participants is equally spaced by some increment , which is a divisor of and is chosen by the TSO: | ||||

| each bids on power offers , . | (7b) | |||

The model above is a simple clearing model within class (2). We can now derive conditions on participants’ bids to ensure pay-off monotonicity, condition (5), is satisfied. Thus, we derive conditions under which the outcome of auctions cleared by (7a), (7b) would lie in the core.

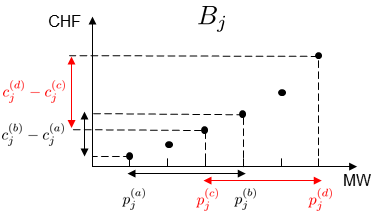

Theorem 3

In words, marginally increasing cost condition (8) implies core outcomes, and thus eliminates incentives for collusions. Condition (8) is visualized in Figure 1.

To prove that condition (8) is sufficient for payoff monotonicity, the following Lemma is needed.

Lemma 2

In the following proofs we apply the notation that if is the accepted power allocation from bidder , then is the associated cost bid from . If the accepted allocation is zero, we define . {pf} The proof follows by contradiction. That is, we will show that when is such that , for some then can be modified to provide a lower cost allocation, , for participants (thus contradicting optimality of ). First, we notice that since bids are equally spaced by MW (7b) and satisfy condition (8), it is never optimal to accept more than MW ().

Now, assume is such that , for some . In order to procure exactly MW, some participants’ accepted MWs must decrease, that is, the set is non-empty. Consider a feasible allocation for the auction with participants where units of power are procured and

So, is constructed from by transferring units of power from participants in to participants in . In doing so, the inequality can be maintained:

The above inequality holds because when summing over , ’s sums to and ’s sums to .

Since is optimal for participants and is not:

| (9) |

where we used as a short-hand-notation for the cost corresponding to choosing bids.

Now, we use (8) to replace the summations over in (9). In particular, define so that

Note that is feasible since and have the same sum over (and thus cancel) and is feasible. Further, since , by condition (8):

| (10) |

Adding (10) to both side of (9) (and canceling ) gives

which contradicts the optimality of . \qed A consequence of the above Lemma is that given the optimal allocation to procure MW, for any lower amount of MWs (while being multiple of ) to be procured, the total MWs accepted from each participant never increases. Now, we are ready to prove Theorem 3.

We prove that under condition (8), inequality (5) holds for each , for any with being a generic new entered participant. Since is a generic set and can be any new participant, this is sufficient to prove that the payoffs are monotonic over all the possible couple of sets (the generalization to arbitrary sets can then be achieved by the interpolating sums, as was done in (6)). We adopt the same notation used in Lemma 2 and we identify with the set of winners.

For each we have by definition . Thus , (since the optimal solution is unchanged when is removed from S). By Lemma 2, and so also. Thus, payoff monotonicity holds for : for . This says that a loser of the auction cannot become a winner as more participants enter.

For each winning participant, , recall that . Adopting the same notation of Lemma 2, we can indicate it as:

where are the optimal amounts to be accepted from , when exits the auction. By Lemma 2, in fact, . Similarly, after participant enters the auction, . That is,

where are the amounts accepted from when exits the new auction. By Lemma 2, we again have .

Notice that so far we applied Lemma 2 to justify the increase of the accepted amounts, first, from each and now from , due to the exit of from the auctions. We can apply Lemma 2 again and affirm that , and in particular , because of the entrance of .

We now find suitable lower and upper bounds to ensure inequality . First, note that , where are the cheapest allocation to procure MW among . By Lemma 2 we have , since ’s sum to (due to ), and ’s sum to . Moreover, since (7b) holds and every satisfies (8), ’s are such that , because exactly MW are purchased. Using the above suboptimal allocation, we have a lower bound for :

| (11) |

Defining now we must have and , since the right hand side is a feasible cost to procure MW among the participants . Indeed, and . Hence, we have:

| (12) |

Moreover, since ’s satisfy (8), we have:

| (13) |

The above holds because , and . In particular, are the amounts accepted to procure MW among , while are to procure the same MWs among . Then, combining (12) , (13) and (11), we finally obtain \qed

Condition (8) on every participant’s bids hence is sufficient to ensure that our VCG procurement auctions will always have core outcomes. While we do not show here that the condition is necessary, we illustrate that there are certainly auctions where condition (8) is violated and for which payoff monotonicity does not hold.

Example 2

Consider Example 1 where power plants and placed just one bid for 800 MW hence violating condition (7b). It is easy to see that the payoffs of each of the four winners are not monotonic. In fact, if just one of them (e.g. ) was participating, he would receive no payment; when ,, enter the auction, however, he becomes a winner hence making positive profit. Suppose now that and bid accordingly to (7b), but the bids have a decreasing marginal cost: , . In this case, when participates alone, he receives a VCG payment of CHF; when ,, enter the auction, however, he receives CHF.

As previously anticipated, we are now able to prove that the condition derived also makes collusions and shill bidding unprofitable. Therefore, the participants are better off with their dominant strategies, which is truthful bidding. Although the result is well-known in literature (Milgrom, 2004),(Ausubel et al., 2006) and motivates the choice of the core as a competitive standard, we can now prove it using the tools developed so far for the problem at hand.

Theorem 4

(i) Let be a set of colluders who would lose the auction when bidding their true values , while bidding they become winners. Defining and , the VCG payment that each player in receives is

where the first equality comes from definition of VCG payment, the first inequality comes from the fact that since displays payoff monotonicity and because, when decrease their bids, less MWs are being accepted from (Lemma 2) and is bidding with increasing marginal cost. The last equality comes from the fact that originally was a group of non-winners. Then, , is bounded by the payment that would receive when he is the only one lowering its bid. By Theorem 1.a he will not face any benefit in doing so.

(ii) We denote with multiple identities of the same participant . Since every participant bids accordingly to (8), the outcome is guaranteed to lie in the core. Hence, by Lemma 1 and substituting , we have:

where is the cost when , or equivalently , is removed from the auction. Therefore, the total payment that would receive is bounded by the one he would receive bidding as a single participant. Making use of shills, hence, is not profitable. \qed

To confirm the previous theoretical results, we come back to Example 1, where the TSO had to procure a fixed amount of 800 MW. That is a simple auction cleared by (7a). Suppose that now power plants and bid according to (7b) (with = 200 MW) and condition (8). The available bids are now: , , .

The winners of the auction are still power plants ,,, but now the VCG payments that they receive is CHF . The total cost incurred by the TSO is much lower than before and no coalition of players now blocks the outcome. If ,, and were multiple identities of the same losing participant (i.e. a power plant with true value greater than 40’000 CHF for 800 MW), shill bidding would become unprofitable (as expected). If, moreover, they were losing participants who jointly lowered their bids, the payments of 8’000 CHF surely made at least one of them to have negative profit.

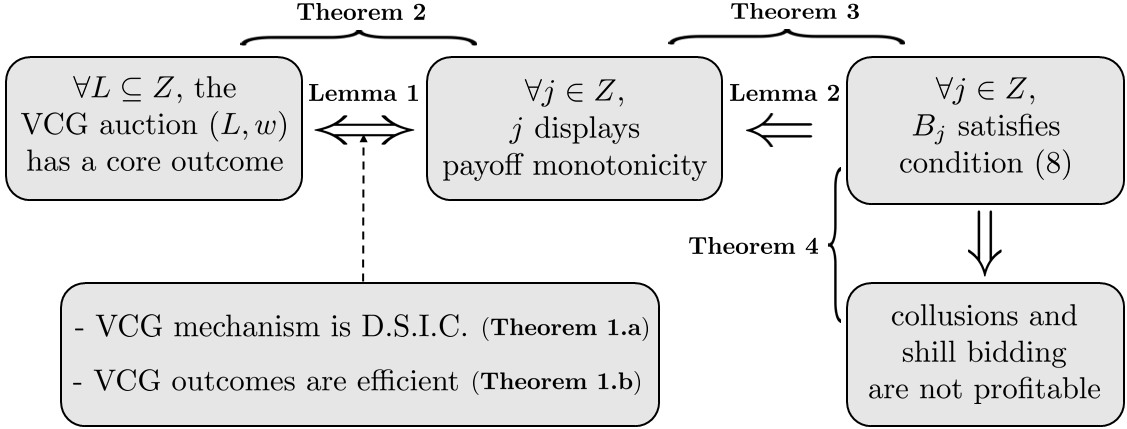

The diagram in Fig. 2 summarizes and links the concepts we developed so far. Notice that Lemma 2, Theorem 3 and Theorem 4 are specific for the class of auctions (7).

3.3 Application to two-stage stochastic market

As we anticipated, the Swiss reserve market as described in (Abbaspourtorbati and Zima, 2016) can be modeled abstractly according to the optimization problem (2). There are two stages of decision variables corresponding to weekly () and daily () bids. Weekly bids are available at the instance of optimization, whereas daily bids are unknown. A number of stochastic scenarios corresponding to likely possibilities of daily bids based on their past values is used in the optimization (). The cost function corresponds to the cost of weekly bids and the expected cost of daily bids. Thus, the cost can be written as . The choice function determines the accepted weekly bids.

The function captures three types of constraints: (a) those corresponding to procurement of certain amount of tertiary reserves; (b) probabilistic constraints, which ensure that with sufficiently high probabilities, the supply and demand of power is balanced; (c) those corresponding to conditional bids. Constraint (b) links the daily and weekly variables. Constraints (a) and (c) correspond to those present in the optimization formulation (7a).

It follows from the analysis of Section 2, that the VCG mechanism applied to the two-stage stochastic market is an incentive compatible dominant strategy mechanism with socially efficient outcome. Due to coupling of the two stage decision variables, the analysis of the core payment is significantly more difficult. In particular, the result derived in Theorem 3 do not readily apply. The amount of procured MWs is not anymore fixed and thus (7b) is not well defined. Selecting infinitely small (forcing participants to provide continuous bid curves) and linearizing the probabilistic constraints (b), however, we could show that under condition (8) this clearing model follows the same regularity property of Lemma 2. Whether this makes all the participants display payoff monotonicity is a subject of our current study. Nevertheless, in the numerical example section, we evaluate the performance of the VCG mechanism and compare it to the pay-as-bid mechanism.

4 Simulations and Analysis

The following simulations are based on the bids placed in the 46th Swiss weekly procurement auction of 2014, where 21 power plants bid for secondary reserves, 25 for tertiary positive and 21 for tertiary negative reserves. Note that the secondary reserves are symmetric, that is, participants need to provide same amount of positive and negative power. Tertiary reserves are on the other hand asymmetric. Thus, participants bid for tertiary negative , and tertiary positive . As in (Abbaspourtorbati and Zima, 2016), probabilistic scenarios for future daily auctions are assumed. The amount of daily reserves is based on the data of the previous week. Three scenarios are considered corresponding to nominal, high (20% higher) and low prices (20% lower) compared to the previous week.

The corresponding outcome of the pay-as-bid mechanism and the VCG mechanism is shown in Table 1. Note that in reality, in a repeated bidding process, the VCG mechanism would lead to different bidding behaviors, which we have not modeled here.

| SRL | TRL- | TRL+ | |

|---|---|---|---|

| Procured MWs | 409 MW | 114 MW | 100 MW |

| Sum of pay-as-bid payments | 2,29 million CHF | ||

| Sum of VCG payments | 2,53 million CHF | ||

Recall that in a pay-as-bid mechanism, a rational participant will overbid to ensure positive profit. Unfortunately, it is hard to know the true values of the bids for each participant. So, it is hard to have an accurate comparison between the VCG and pay-as-bid based on past data. We now scale all the bid prices down by 90%, assuming that those were participants’ true values and hence the bids that they would have placed under the VCG mechanism. The outcome of both mechanisms is shown in Table 2.

| SRL | TRL- | TRL+ | |

|---|---|---|---|

| Procured MWs | 409 MW | 114 MW | 100 MW |

| Sum of pay-as-bid payments | 2,06 million CHF | ||

| Sum of VCG payments | 2,28 million CHF | ||

All the results are proportional (as it could be expected) and the sum of VCG payments is lower than the sum of pay-as-bid payments we had in the first scenario. This means that assuming such scaled bids were participants’ true values, the VCG mechanism would have led to a lower procurement cost than the implemented pay-as-bid mechanism. Hence, the VCG mechanism, apart from leading to a dominant strategy equilibrium with an efficient allocation, would have been beneficial also in terms of costs, for this particular case study based on the past data.

This does not happen in generic VCG auctions. In particular, the cost incurred by the auctioneer in a VCG auction is usually higher than the cost under a pay-as-bid mechanism, considering the same set of bids. To see this, recall that the VCG payments are . These payments measure the benefit that each participant brings to the auction. When the VCG payments are computed through the two-stage stochastic optimization algorithm of (Abbaspourtorbati and Zima, 2016) we observed that the costs are not significantly different from the pay-as-bid mechanism. Intuitively, the two-stage market softens the benefit that every participant brings to the weekly auction: his accepted bids can always be replaced by amounts of MWs allocated to the future. In fact, the amounts of MWs bought in the weekly auction are not fixed and they are flexible depending on the future daily bids available in that week.

To confirm the intuition above, we now assume that we had perfect information about the future daily auctions. As such, we run a deterministic auction assuming that the TSO already knew that the optimal amounts to be purchased were 409 MW for SRL , 114 MW for TRL- and 100 MW for TRL+ as predicted in Table 1 . Given fixed MWs to be procured, the auction is cleared by the simplified model (7a). In this case, naturally, we have the same winners of the auction as the previous case for both VCG and pay-as-bid mechanism. The VCG payments however are significantly higher than the pay-as-bid payments. The results are shown in Table 3.

| SRL | TRL- | TRL+ | |

|---|---|---|---|

| Procured MWs | 409 MW | 114 MW | 100 MW |

| Sum of pay-as-bid payments | 2,06 million CHF | ||

| Sum of VCG payments | 7,97 million CHF | ||

The result can be explained as follows. When a winner is removed from the auction (to compute the term ) the amounts of MWs to be accepted among the other participants originally were subject to flexibility due to two stage decision variables and lack of a fixed total amount for each type of reserve SRL, TRL-, TRL+. If these total reserves are fixed for each type, the benefit that every participant brings to the Swiss weekly auction is much higher, and this results in higher VCG payments.

The mixed integer optimization problems were solved with GUROBI, on a quad-core computer with processing speed 1.7 GHz and memory 4 Gb. The first two simulations had a computation time of 9 min, with an average of 17 s for each optimal cost . The last simulation took 7 min, with an average of 14 s for each .

5 Conclusion

We developed a VCG market mechanism for electricity markets, motivated by the set-up of the control reserves (ancillary services) market. We showed that the mechanism results in an incentive compatible dominant strategy Nash equilibrium. Furthermore, this mechanism is socially efficient. Through examples, we showed that shill bidding can occur. We thus, derived conditions under which a deterministic procurement mechanism can guarantee no shill bidding and thus competitive outcomes. These findings, both theoretical and empirical, act to support the application of VCG mechanism for the electricity markets under consideration. By removing incentives for collusion and by providing a simple truthful mechanism, we expect that the implementation simplifies the biding process, increases markets efficiency and encourages participation from increasing number of entities. We verified our results based on market data available from Swissgrid. Future work consists of deriving conditions under which Theorem 4 could be extended to the stochastic market.

We thank Farzaneh Abbaspour and Marek Zima from Swissgrid for helpful discussions.

References

- Abbaspourtorbati and Zima (2016) Abbaspourtorbati, F. and Zima, M. (2016). The swiss reserve market: Stochastic programming in practice. IEEE Transactions on Power Systems, 31(2), 1188–1194.

- Abhishek and Hajek (2012) Abhishek, V. and Hajek, B. (2012). On the incentive to deviate in core selecting combinatorial auctions. In Proceedings of the 24th International Teletraffic Congress, 37. International Teletraffic Congress.

- Ausubel et al. (2006) Ausubel, L.M., Milgrom, P., et al. (2006). The lovely but lonely Vickrey auction. Combinatorial auctions, 17, 22–26.

- Clarke (1971) Clarke, E.H. (1971). Multipart pricing of public goods. Public choice, 11(1), 17–33.

- Cramton (2013) Cramton, P. (2013). Spectrum auction design. Review of Industrial Organization, 42(2), 161–190.

- Day and Cramton (2012) Day, R.W. and Cramton, P. (2012). Quadratic core-selecting payment rules for combinatorial auctions. Operations Research, 60(3), 588–603.

- Groves (1973) Groves, T. (1973). Incentives in teams. Econometrica: Journal of the Econometric Society, 617–631.

- Klemperer (2004) Klemperer, P. (2004). Auctions: theory and practice. Available at SSRN 491563.

- Milgrom (2004) Milgrom, P.R. (2004). Putting auction theory to work. Cambridge University Press.

- Osborne and Rubinstein (1994) Osborne, M. and Rubinstein, A. (1994). A Course in Game Theory. MIT Press. URL https://books.google.co.uk/books?id=5ntdaYX4LPkC.

- Varian and Harris (2014) Varian, H.R. and Harris, C. (2014). The VCG auction in theory and practice. The American Economic Review, 104(5), 442–445.

- Vickrey (1961) Vickrey, W. (1961). Counterspeculation, auctions, and competitive sealed tenders. The Journal of finance, 16(1), 8–37.