Functional Forms for Tractable Economic Models

and the Cost Structure of International Trade††thanks: This paper replaces its previous working versions

“Pass-Through and Demand Forms”/“A Tractable Approach to Pass-Through Patterns”/“The Average-Marginal Relationship and Tractable Equilibrium Forms”.

We are grateful to many colleagues and seminar participants

for helpful comments. We appreciate the research assistance of Konstantin

Egorov, Eric Guan, Franklin Liu, Eva Lyubich, Yali Miao, Daichi Ueda,

Ryo Takahashi, Huan Wang, and Xichao Wang. This research was funded by the Kauffman

Foundation, the Becker Friedman Institute for Research in Economics,

the Japan Science and Technology Agency and the Japan Society for

the Promotion of Science to which we are grateful. We are particularly

indebted to Jeremy Bulow for detailed discussion and for inspiring

this work and to James Heckman for advice on relevant theorems in

duration analysis and nonparametric estimation. All errors are our

own.

Abstract

We present functional forms allowing a broader range of analytic solutions to common economic equilibrium problems. These can increase the realism of pen-and-paper solutions or speed large-scale numerical solutions as computational subroutines. We use the latter approach to build a tractable heterogeneous firm model of international trade accommodating economies of scale in export and diseconomies of scale in production, providing a natural, unified solution to several puzzles concerning trade costs. We briefly highlight applications in a range of other fields. Our method of generating analytic solutions is a discrete approximation to a logarithmically modified Laplace transform of equilibrium conditions.

1 Introduction

Analytic solutions have played a major role in many fields of economics. They are useful both as closed-form, pencil-and-paper solutions to applied theory models, and as components (subroutines) of larger models, making them more computationally tractable.111This later type of use is particularly important in the closely allied computationally-intensive field of Bayesian statistics where closed-form tractable priors are typically used to approximate otherwise computationally intractable probability models. In this paper, we substantially expand the class of known analytic solutions to a broad class of standard economic models. We then illustrate the application of these ideas to a computationally-intensive model of international trade that helps resolve a long-standing puzzle about trade costs by allowing more realistic functional forms of such costs.222In this main, computationally intensive application we find that analytic characterization of the solutions of sub-problems in larger-scale models is particularly useful in conjunction with analytic-differentiation software, graphics processing units (GPUs), and related optimization algorithms. GPU computing has witnessed dramatic developments over the last few years, which our work benefitted from.

We observe that most frequently used functional forms that lead to analytic solutions in economics, namely linear and constant-elasticity functions, share a convenient property: They preserve functional forms under transformations that we refer to as “average-marginal transformations”. That is, the functional form of the average value of the function is the same as that of its derivative. Formally, we say that a functional form class is preserved by average-marginal transformations if for any function the class also contains any linear combination of and .333A simple economic interpretation would be to identify with the price of a good sold by a monopolist, i.e. with the average revenue the firm receives per unit sold, in which case is the marginal revenue. The name of the transformation is chosen to be consistent with this and similar examples. The Bulow-Pfleiderer demand class (Bulow and Pfleiderer, 1983) discussed later is also invariant under average-marginal transformations. We then find all functions that have such property.

Within this class, we identify functional forms that have a given level of “algebraic tractability”, a property we define. These are linear combinations of power functions satisfying certain conditions. When used to represent demand and cost curves they lead to economic optimization conditions that may be transformed to polynomial equations of a degree smaller than 5. These, in turn, may be solved explicitly by the method of radicals. This substantially generalizes the simple analytic solutions that economists are familiar with in the case of constant marginal cost and either linear or constant-elasticity demand. Even beyond degree 5, precise solutions to such polynomial equations are available at minimal cost in standard mathematical software.

We show that elements of functional form classes preserved by average-marginal transformations also have advantageous properties when applied to aggregation over heterogeneous firms in monopolistically competitive models: They lead to closed-form aggregation integrals under very flexible assumptions. This means that a problem with a continuum of heterogeneous firms may be reduced to a set of explicit equations at the macroeconomic level.

In our method, the existence of closed-form solutions to optimization conditions sometimes requires parameter restrictions involving parameters both from the supply side and the demand side. These restrictions may or may not be approximately satisfied in a particular market. If they are not satisfied, one may be tempted to conclude that our method is not applicable. Most likely this is the reason why economists have not found (or have not attempted to find) the kind of solutions we discuss in our paper.

We explain, however, that the range of applicability of our method is larger than it may seem at first sight as this issue does not pose a large problem. Even if the parameter restrictions are not satisfied, analytic solutions at other parameter values may be used to construct an interpolation that covers parameter values of interest. In this way one can extend the usefulness of our analytic method. Another way is to realize that a given demand or cost function may be approximated by functions that satisfy our restrictions, in which case the restrictions are satisfied by choice.444Yet way of extending the usefulness of the solutions is to use Taylor series expansions around them, which may be useful for certain types of models.

While our approach is useful in many fields of economics, as we illustrate, the main application we focus on in this paper belongs to the field of international trade. Analytic tractability has been important for international trade to the extent that almost all models assumed constant marginal costs of both production and logistics/shipping. Under such assumptions trade models are much more straightforward to solve. Yet, as we discuss in detail, these assumptions contrast with models of cost used by the logistics managers that economists are presumably attempting to describe. As we show, our functional forms preserve analytical tractability while allowing the realism of matching such models.

Our primary application in this paper shows how such more realistic models of cost can help resolve the trade cost puzzle in a model of world trade flows with heterogeneous firms.555Even though we do need considerable computational power to fit our model to the data, without the tractability of our functional forms the computations would be significantly harder and we would not have attempted to obtain a calibration of world trade flows that we discuss below. Standard models of international trade attribute the observed rapid falloff of trade flows with distance to trade costs that increase dramatically with distance. But we have no reason to believe that such dramatic distance dependence of trade costs exists in the real world. Container shipping charges depend on distance only modestly, and in any case, represent only a tiny fraction of the value of the transported goods. A similar statement holds for the so-called iceberg trade costs, i.e., the damage of goods during transportation: We know goods typically do not get damaged during transport, and if they do, the damage probability is unlikely to strongly increase with the distance a shipping container traveled over the ocean. While trade costs may be sizeable, they are much more likely to be associated with shipment preparation and coordination or with loading and unloading, rather than with the distance traveled over the ocean. For this reason, the rapid falloff of trade with distance represents a puzzle from the point of view of standard models of international trade.666This puzzle in various forms has been discussed by many authors; see Disdier and Head (2008) for an overview and Head and Mayer (2013) for an in-depth discussion of the problem.

Our model resolves this puzzle in a very natural way. Firms find it costly to produce larger quantities due to increasing marginal costs of production. At the same time, they find it beneficial to concentrate their exports to a few destinations due to economies of scale in shipping. With this cost structure, even a small cost advantage of a particular destination will be enough to make the firm export there instead of other destinations. If trade costs are slightly smaller for closer destinations, this cost advantage will lead to substantially larger trade flows at smaller distances and substantially smaller trade flows at larger distances.

The model also resolves a puzzle related to firm entry into export markets. Although it is not as widely discussed as the trade cost puzzle, it is a clear empirical regularity that models with constant marginal costs cannot address in a natural way. In the data, one can often see two similar firms, say, from China, one exporting to, say, Portugal and not to Greece and the other exporting to Greece and not to Portugal. To reconcile such patterns with the assumption of constant marginal cost of production, standard international trade models introduce stochastic cost shocks specific to each firm-destination pair. These cost shocks have to be dramatically large. For the second firm they need to offset the entire profit the first firm makes from its exports to Portugal. In the absence of any real-world phenomenon that could lead to cost shocks of this kind, this represents a puzzle.777We discuss alternative mechanisms in Section 4.

Our model explains this puzzle in a straightforward way. With increasing marginal costs of production and economies of scale in shipping, firms need to solve a combinatorially difficult problem of choosing export destinations.888In economics there are many combinatorially difficult problems, and we expect our methods to be useful there. Different approximate solutions of this choice problem can lead to different sets of export destinations, even if the maximized profits are almost the same. One approximately optimal set of export destinations may include Portugal, while another one may include Greece.

We solve the model using an iterative method involving an outer loop and an inner loop. The outer loop requires an evaluation of firms’ profit functions for many discrete choices of export destinations. Our functional forms bring a tractability advantage that makes these evaluations fast. In the inner loop, we solve for a general equilibrium of the world economy keeping the discrete choices fixed. There using our functional forms is helpful because it allows for an analytic calculation of derivatives that are needed for accelerated gradient descent algorithms.

Separately, we develop many other applications of the proposed functional forms. For the model of outsourcing decisions in a sequential supply chain constructed by Antràs and Chor (2013), we reformulate the theory to simplify the analysis and use this new formulation to apply our functional forms. This allows us to show that for more realistic demand functions, outsourcing occurs at both the early (viz. raw materials) and late (viz. final commercial sales) stages of production, while intermediate stages are performed in-house, corresponding to common observation of outsourcing patterns. For a model of labor bargaining by Stole and Zwiebel (1996a, b), we tractably generalize the closed-form solutions that have been found for linear or constant-elasticity demand and show that for realistic demand patterns the employment effects of bargaining have interesting and intuitive cyclical patterns. We also discuss applications to imperfectly competitive supply chains, two-sided platforms, selection markets, auctions, and, extensively, monopolistic competition.

Finally, we show that our method may be thought of as a discrete approximation to a logarithmically modified Laplace transform. It may also be thought of as a sieve method of non-parametric econometrics. In addition, the transformed variables reveal economic properties of demand functions that would appear accidental otherwise.

The next section provides a quick illustration of our functional forms with a focus on modeling demand under income inequality. Section 3 presents our main theoretical results. Section 4 focuses on modeling world trade. Section 5 discusses other applications. Section 6 develops the theory connecting our tractable functions to a logarithmically modified Laplace transform. The paper also includes an appendix and supplementary material.

2 Example: Replacing Constant-Elasticity Demand

2.1 Constant-elasticity demand and its flexible replacement

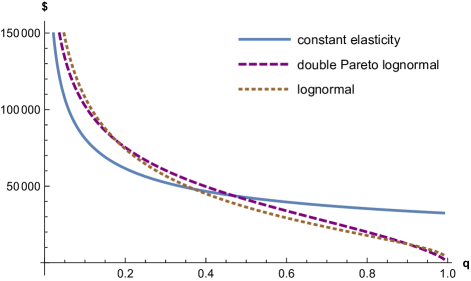

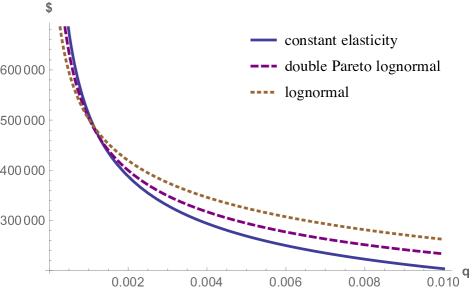

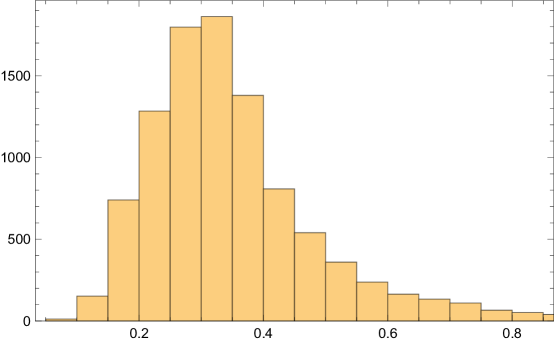

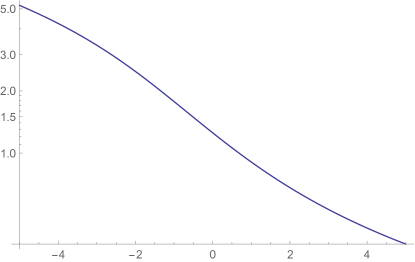

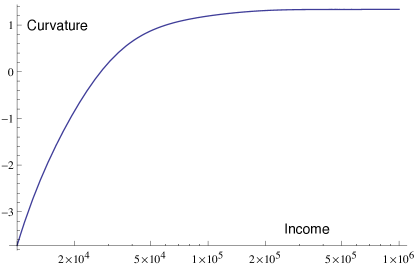

The most canonical and widely-used demand form in economic analysis is the constant-elasticity specification, corresponding to inverse demand . It is frequently used because of its analytic tractability. Historically, it appeared in the economic literature because in discrete-choice settings it is plausible that product’s valuations follow the income distribution and the income distribution was believed to be approximately Pareto, i.e., power-law.999In cases where each individual can consume at most one unit of an indivisible product, the inverse demand function equals the reversed quantile function of the distribution of valuations (willingness to pay), up to constant rescaling. The reversed income quantile function here refers to the function that maps a given quantile measured starting at the top of the income distribution to the corresponding valuation level. Note also that, of course, we do not wish to say that the most important property of constant-elasticity demand lies in the context in which it first appeared. We are merely using this example as an illustration of our approach to demand functions. Modern data of income, however, led to different conclusions on the shape of the income distribution.101010The origin of constant-elasticity demand historically appears to be the argument by Say (1819) that willingness to pay for a typical discrete-choice product is likely to be proportional to income, and thus that the distribution of the willingness to pay should have the same shape as the income distribution. (Say’s assumption is likely to be approximately correct for example for products that save a fixed amount of time to the owner, independently of their wealth.) Since early probate measurements of top incomes exhibited power laws (i.e., Pareto distributions) (Garnier, 1796; Say, 1828), by extrapolation Dupuit (1844) and Mill (1848) suggested that demand would have a constant elasticity. This observation appears to be the origin of the modern focus on constant elasticity demand form (Ekelund and Hébert, 1999; Lloyd, 2001). However evidence on broader income distributions that became available in the 20th century as the tax base expanded (Piketty, 2014) shows that, beyond the top incomes that were visible in 19th century data, the income distribution is roughly lognormal through the mid-range and thus has a probability density function that is bell-shaped, rather than power-law. Distributions that accurately match income distributions throughout their full range (Reed and Jorgensen, 2004; Toda, 2012, 2017) have a similar bell shape but incorporate the Pareto tail measured in the 19th century data.

In this section we discuss another demand form that is also highly analytically tractable but has more flexibility. This flexibility allows us to get a much better match to the income distribution.111111Similarly, this flexibility could allow us to get a better match to a distribution of valuations in cases where it differs from the exact income distribution. As an illustration, we show that our proposed demand form leads to substantially different policy implications than the constant-elasticity form in the socially important case of bias of innovative technical progress.

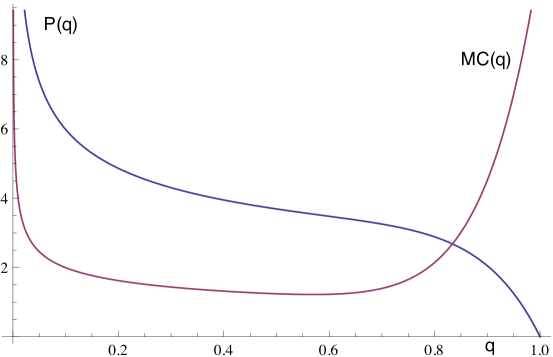

Consider the task of representing the empirical income distribution using a corresponding demand function. Constant-elasticity demand fails this purpose, as illustrated in Figure 1. This is because the income distribution is not Pareto but approximately double Pareto lognormal (Reed and Jorgensen, 2004; Toda, 2012, 2017). Working with the double Pareto lognormal distribution (or with the more loosely fitting lognormal distribution) in economic models would be quite difficult.121212See Footnote 14. To overcome this difficulty, we propose a functional form that allows for the same basic shape, but leads to calculations almost as easy as for the constant-elasticity form:

| (1) |

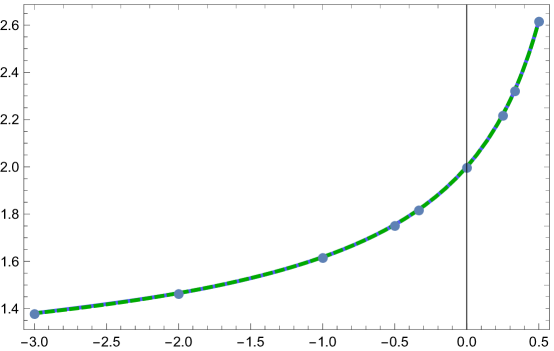

A set of parameter values that matches the income distribution (for the US in 2012) very well is . We obtained these values by a generalized-method-of-moments fit and rounding the results. The match is illustrated in Figure 2.

2.2 Bias in technological progress

As a simple, illustrative application, we discuss the case of bias in technological progress described in Kremer and Snyder (2015, 2017). First, we do that for the case of constant-elasticity demand and explain why it is highly tractable. Then we turn to our proposed demand form in Equation 1 and show that it preserves a high degree of tractability that constant-elasticity demand has.

When the private sector decides which products to develop, it chooses profit-making products, not necessarily those products that create the greatest social value. This bias in technological progress depends on the discrepancy between private and social gains. Kremer and Snyder (2015, 2017) consider the fraction of the social gains from creating a new product that may be appropriated by a monopolist131313Budish, Roin and Williams (2015) studied this problem recently in a different context. , referred to as the appropriability ratio, and show that the maximal fraction of potential surplus that may be lost due to imperfect appropriability is equal to one minus this appropriability ratio. They compare different demand functions since they lead to different bias in research and development, but always assume no costs. Here we assume a fixed demand function and consider biases at different levels of marginal production cost. We walk quite didactically through the process of solving the model in order to illustrate the source of the tractability of the constant-elasticity form and why it carries over to our proposed generalized form but not to the lognormal distribution form. We then follow Kremer and Snyder (2017)’s argument that a sensible demand function is one matching the world income distribution and use this as motivation for using our form to study the impact of cost on the appropriability ratio, which is very different under our form than under constant elasticity.

Consider a monopolist with a constant marginal cost and constant-elasticity (inverse) demand . Her marginal revenue is . Under the constant elasticity form, , which has the same form as , just a different multiplicative constant out front. For this reason, the marginal revenue has the same form as well: . The monopolist optimally equates it to the marginal cost, so the optimal quantity may be determined by solving the linear equation with , yielding . From this it follows by substitution that the firm’s absolute markup is , where PS stands for the producer surplus. Furthermore, the average consumer surplus also has the same form as , differing only by a multiplicative constant:

Evaluated at the optimal quantity, the average consumer surplus is . The appropriability ratio, i.e., the ratio of producer surplus and the total surplus, may be evaluated as , which is a constant independent of cost. Thus all products have precisely the same appropriability ratio, and cost is irrelevant to the bias of investments in research and development.

If we tried to investigate this problem in a tractable way for more general demand functions that have been used in the economic literature, we could use the Bulow-Pfleiderer demand introduced in the next section, which includes both constant-elasticity and linear demand as special cases. However, we would again find that the cost has no impact on the bias of technical progress.

If instead, we tried to investigate the implications of demand curves corresponding to other distributions of product valuations, such as the lognormal distribution or the double-Pareto lognormal distribution (which fits the income distribution), we would quickly find that such investigation cannot be carried out analytically.141414For a lognormal distribution with mean and standard deviation of the exponent, the inverse demand is , where is the standard normal cumulative distribution function and where we normalized maximum demand to 1. There is no analytic solution to the monopolist’s optimization condition because the following expression is too complicated: . The more realistic double-Pareto lognormal distribution leads to even more complicated expressions. Clearly, if demand functions of this kind were used inside larger models, the absence of analytic tractability could quickly become a significant obstacle.

Here we show that working with the demand form in Equation 1 is much easier and elegant and leads to substantive economic results. Its marginal form has the same functional form as itself:

If we introduce the notation

the monopolist’s first-order condition is just the quadratic equation

This leads to the closed-form solution

The per-unit consumer and producer surplus again take the same functional form:

The appropriability ratio is then

where the last equality was obtained by substituting for the marginal cost from the first-order condition. Substituting the parameter values we specified right after Equation 1 gives

This equals for (when the product serves a tiny fraction of the population) and monotonically increases in q to for (when most of the population is served). This suggests a bias towards cheap, mass-market products and away from expensive products that mostly cater to the rich; of course, all this analysis is based, like Kremer and Snyder’s, on aggregate surplus and might well reverse if distributional concerns were incorporated.

While we focused here on biases from the appropriability ratio, it can be shown (in closed-form) that many other aspects of standard intellectual property policy differ substantially under our form from the results under the constant pass-through class. For example, under our form the ratio of consumer surplus to monopoly deadweight loss is much greater (usually by several times) than under the Bulow-Pfleiderer class so that patents are more desirable and optimal patent protection is greater than under the standard forms. Similarly allowing pharmaceutical producers to price discriminate often increases deadweight loss under the standard forms (Aguirre et al., 2010), while it is always beneficial under our form. Thus the standard forms are substantively misleading on a number of issues and the added complexity of using our form is minimal.

3 Central Results

In the previous section we focused on a particular functional form derived from our theory, a particular calibration target (the US income distribution) and a particular application. However, our approach applies much more broadly. We characterize all functional forms that have the useful property of the form above: namely that, in the language of demand curves, linear combinations of marginal revenue and inverse demand take the same form as inverse demand itself. Within these we then identify functional forms that lead to closed-form solutions utilizing power functions and the method of radicals.

3.1 Form preservation under the average-marginal transformation

Let us denote by the average of an economic variable that depends on , where a baseline interpretation of is a quantity of a good. The marginal variable is then . We now formally define what it means for these two variables to have the same functional form, as we alluded to in the previous section.

Definition 1.

(Form Preservation) We say that a functional form class is form-preserving under average-marginal transformations if for any function , the class also contains any linear combination of and . In other words, . In economic terms, we interpret as the average of the variable , such as revenue or cost, and as its marginal counterpart. This definition thus states that any linear combination of the average and marginal variables belong to the defined class of functions.151515Note that any form-preserving class is also form-preserving under multiple applications of operators of this type.

Obviously, if is taken to be a sufficiently large (e.g. infinite-dimensional) class of functions it may be form-preserving in a fairly mechanical way. For example, if it is the set of all analytic functions with the domain for some then we know that is also analytic and has at least as large a domain. This observation is not very useful for the purposes of tractability because the set of all analytic functions with this domain contains many that, as we discussed in the previous section, are not tractable using standard analytic and computational methods.

Thus we will naturally wish to consider smaller classes. It is, therefore, useful to identify the most general set of finite-dimensional functional form classes that are form-preserving under the average-marginal transformations . Before stating the characterization theorem, let us briefly clarify what we mean by the dimensionality of a functional form class. For example, a functional form class , where and are continuously varying real numbers is two-dimensional, while with continuously varying real , , and is three-dimensional.161616While this intuitive description is sufficient for practical purposes, more formally we say that an -dimensional functional form class is a subset of a space of functions (of a scalar, continuous variable) that is homeomorphic to an -dimensional manifold, possibly with a boundary. Such manifold, with or without a boundary, is often referred to as the moduli space.

Theorem 1.

(Characterization of Form-Preserving Functions) Any real finite-dimensional functional form class with domain (or an open subinterval of it) that is form-preserving under average-marginal transformations must be a set of linear combinations of

where , , and are fixed sets of real numbers and . If we exclude functions oscillating as , only the functions in the first row are allowed. In that case the most general form is the set of linear combinations of

The proof is provided in Appendix A.

3.2 Tractability

We now provide a specific formal definition of “tractability” that allows us to characterize the class of form-preserving functional forms that have various levels of such tractability. While the term tractability is constantly invoked in economics papers to justify various “simplifying” assumptions, it is almost never defined formally.171717Of course, in other contexts the word “tractability” may have other meanings that are also useful. We specify below what we mean by “tractability” in this paper.

A potential reason for this is that there is no standard, clear definition within applied mathematics of the notion of tractability of the solution of mathematical equations. The theory of polynomial equations establishes that generic polynomial equations of degree at most four have solutions in terms of “the method of radicals” (roots of different orders) and that generic polynomial equations of higher degree have no such solutions, according to the Abel–Ruffini theorem. But this theory does not imply that one could not extend the list of “closed-form” functions by adding some other functions (other than roots) to provide solutions to higher order polynomials. In practice, polynomial equations of any reasonably low order (say less than a hundred) can be solved extremely rapidly by standard mathematical software (Kubler et al., 2014).181818Of course, the notion of “tractability” and “closed-form solutions” is subjective to some extent. Equations whose solutions may be expressed in terms of functions that are familiar enough are often said to have closed-form solutions. That does not imply, however, that such notion is meaningless. Familiar functions are easier to work with for researchers thanks to existing intuition, as well as thanks to their implementation in symbolic or numerical software. In this paper we made definite choices to resolve the terminological ambiguity.

For this reason, we use a specific definition of tractability, which we call algebraic tractability, that is very simplistic: an equation is algebraically tractable at some level if it can be solved using power functions and a solution to a polynomial equation of degree no greater than . While this definition eliminates many other functions with known solutions, it does a good job capturing existing forms that are widely considered tractable while allowing an extension to richer forms in a pragmatic manner given the ease with which polynomial equations can be solved both analytically and computationally (Kubler and Schmedders, 2010).

An important feature of the (non-oscillating) class of functional forms in Theorem 1 is that if we include terms with powers of logarithms we must also include all terms with powers of logarithms below this. That is, if the class includes linear combinations of and it must also include linear combinations , , and . With a small number of (explicitly enumerable) exceptions, classes of functional forms like this can rarely be solved in closed-form because of the combination of power and logarithmic terms.191919The most notable exception is the case when only a single power of is used which can be divided out of the equation to yield a polynomial in . While this class is of some interest, we do not focus on it here because it has the unappealing property that if one wishes to include a constant term (which is often desirable as we discuss below) one is limited to a small number of powers of logarithms and all other parameters are set. There are other specific exceptions and exploring the use of these is an interesting direction for future research, but none offers the flexibility afforded by power functions that we focus on below. This is likely why they have formed the basis of so much prior work. We thus see the logarithm-based forms instead as limits of the power forms that are worth including but not focusing on.

On the other hand, the even-simpler class of sums of power functions nests all frequently-used tractable forms in the economic literature, namely constant-elasticity demand combined with constant marginal cost, linear demand combined with linear marginal cost as in Farrell and Shapiro (1990), and the “constant pass-through” demand of Bulow and Pfleiderer (1983) (henceforth BP) with constant marginal cost.202020In this section, for expositional purposes, we discuss tractability from the point of view of monopoly problems. But it is worth noting that tractability considerations would be exactly the same for Cournot oligopoly and very similar in the many applications we discuss in this paper.,212121The BP demand, defined below, gives constant pass-through rate of specific taxes to monopolist’s prices only in the case of a constant marginal cost. For this reason, we prefer to use the term Bulow-Pfleiderer (BP) demand, instead of the frequently used term “constant pass-through demand”.As a result, we focus on functional form classes composed of linear combinations of power functions .222222There are a few cases not nested in the forms of Theorem 1 for which the firm’s first-order condition may be solved. Hyperbolic demand curves used by Simonovska (2015) are one of them. Cases where the solution is in terms of the Lambert W function are the exponential utility function of Behrens and Murata (2007, 2012) and single-product versions of the Almost Ideal Demand System and of translog demand.

The BP demand corresponds to for some real constants , and , not necessarily all positive. In a monopolist’s first-order condition, constant marginal cost enters in the same way as . In this sense, constant marginal cost is compatible with this demand side specification. (Similarly, linear marginal cost would be fully compatible with the demand side in the special case of , i.e., linear demand.)

Using the BP demand form with constant marginal cost leads both to tractability and to an important substantive implication: the constancy of the pass-through rate of the constant marginal cost to price. However, it is clearly possible to preserve the former property without the latter. For example, consider inverse demand and average cost of the form and .232323Mrázová and Neary (2014) studied the properties such bi-power form applied to inverse demand functions in combination with constant marginal cost. Their goal was not to obtain closed-form solutions. Then the monopolist’s first-order condition gives

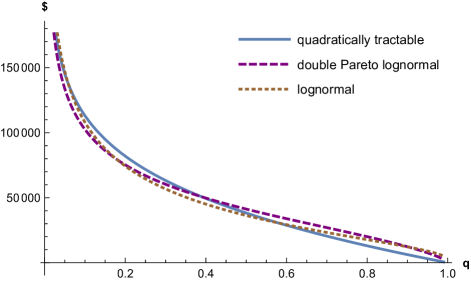

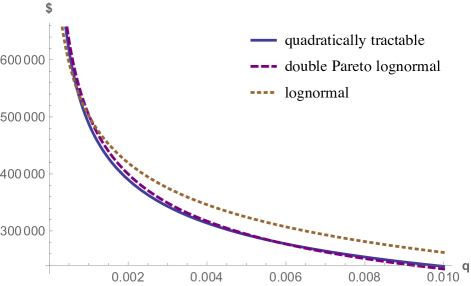

This more general form thus still leads to a closed-form solution but offers substantially more flexibility. For example, it can accommodate simultaneously U-shaped cost curves and demand curves generated by a bell-shaped valuation distribution (in the sense of discrete choice). Figure 3 provides an example. A disadvantage of this form, however, is that it does not include a constant term. A constant term would have been useful for studying the pass-through rate and similar comparative statics. Another disadvantage is the absence of an explicit expression for the direct demand

It is thus useful to look beyond systems that lead to a linear equation (after a substitution using a power function). Quadratic, cubic and quartic equations also yield closed-form solutions by the method of radicals. Furthermore, polynomials of higher, but still small, order can be solved extremely quickly by most mathematical software without resorting to numerical search. For this reason, we define tractability in terms of the degree of polynomial solution a form admits.

Definition 2.

(Tractability) We say that an economic problem involving a scalar is algebraically tractable at level if a definite power of is the solution of a polynomial equation of order . For short we often refer to this simply as “tractability” and use adverbial forms for low (e.g. linearly or quadratically tractable). By classical results of the theory of polynomial equations, only for can such an equation be explicitly solved by the method of radicals and thus we refer to economic problems that are algebraically tractable at level as analytically tractable.

We now characterize the set of functional forms from the power class that are tractable at level for any positive integer . A very naive conjecture based on the above discussion is that this is simply the set of forms that can be written as the sum of powers. To see why this is wrong, consider the equation

This does not admit a quadratic solution, but can be solved cubically by defining , transforming the equation into

While the quadratic solution fails here, the cubic succeeds, because the gap between the power of the first and second term () is not equal to that between the second and third term (); instead it is twice the second gap, implying that there is a “missing” term in the equation. On the other hand, the equation

is quadratically tractable because the gap between the first and second powers equals that between the second and third. More broadly the number of such evenly-spaced powers sufficient to represent the class determines its level of tractability.

Theorem 2.

(Closed-Form Solutions) A functional form class composed of all linear combinations of a finite set of powers of is algebraically tractable at level for generic linear coefficients if and only if the powers included are for some fixed real numbers and and some fixed set of integers for a fixed integer . More informally, a class of sum of power laws is tractable at level if it consists of at most evenly-spaced powers of .

| Form | Tractability properties | Flexibility | Special cases | Historical notes | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Linear | Constant | Farrell and Shapiro (1990) | ||||||||||

|

|

|

|

||||||||||

| Linearly tractable |

|

BP |

|

||||||||||

|

|

BP | This paper | ||||||||||

|

|

BP |

|

One example of applying this theorem was given in the previous section: our tractable form involves 3 evenly spaced power laws and thus is quadratically tractable. Table 1 summarizes a rich set of other possibilities covered by this theorem. The demand side of some of these has appeared in previous literature as we cite in the paper, though only in the case of Farrell and Shapiro (1990) are we aware of authors harnessing the accompanying cost-side flexibility.

3.3 Aggregation over heterogeneous firms

Models of international trade involving firm heterogeneity frequently use the framework of Melitz (2003) or Melitz and Ottaviano (2008), which assume respectively constant elasticity and linear demand. While these forms clearly play a role in the tractability of those models, the models are not always explicitly solvable even under these forms. Instead, the key properties these allow is that the firms’ optimization problems may be solved explicitly and that aggregation integrals over heterogeneous firms may be expressed in closed form, assuming Pareto-distributed firm productivity.

We present a theorem that shows that substantial generalizations of these models can still lead to closed-form aggregation. We defer a full model set-up to Supplementary Material I.7.5, but it may be thought of simply as the Melitz (2003) model with relaxed functional form assumptions on the shape of demand, supply, and firm productivity distributions.

Theorem 3.

(Aggregation) Suppose that the utility structure implies an inverse demand curve and that firms have marginal cost functions , where is an idiosyncratic parameter influencing the firm’s productivity, distributed according to a cumulative distribution function . Assume that , , , and are linear combinations of powers of their arguments, with the second order condition for the firm’s profit maximization satisfied. Furthermore, suppose that the powers are such that and the difference between marginal revenue and are both of the form with common , but possibly differing and polynomials . Then the aggregation integrals for the firms’ revenue, cost, and profit may be performed explicitly. The resulting expressions may contain special functions, namely the standard hypergeometric function, the standard Appell function, or more generally Lauricella functions, and in the case of high-order polynomials (higher-order tractable specifications), increasingly high-degree polynomial root functions.

While this result is closely related to our general theory and our other applications (in particular, because this aggregation is possible when the relevant variables have our proposed forms), there are also a few differences worth noting. First, aggregation is still possible when the heterogeneous component of marginal cost is “shifted” (in the exponent space) by a uniform multiplicative power factor relative to . This corresponds to the “possibly differing ” in the statement of the theorem. Second, our results here are about aggregation, not solution, and the resulting functions are not, therefore, solutions to polynomial equations but rather various functions that may be exotic to some economists, but are widely used in mathematics and related applied fields. Finally, as the complexity of the forms rises, it is the complexity of these functions that rises.

Closed-form aggregation is useful for at least three reasons. First of all, in the simplest cases the resulting aggregation integrals are just polynomial functions, which means that at the aggregate level the economic equations are relatively simple. Second, when the aggregation integrals lead to commonly used special functions, these are likely to be implemented in numerical software of the researcher’s choice. The researcher gets a fast and numerically reliable implementation of these functions and their derivatives without spending time on approximation methods. Third, it is possible to take advantage of the properties of these functions that have been studied in the mathematical literature.

3.4 Interpolation between solutions

We have discussed how to obtain closed-form solutions in economic modeling. We used linear combinations of power function and imposed conditions on their exponents. It is natural to ask what happens if these conditions are not satisfied. Suppose we have a computationally intensive model whose numerical solutions rely on closed-form solutions to its sub-problems. If we relax our assumptions on the exponents we just mentioned, the sub-problems will not be solvable in closed form and obtaining numerical solutions to the full problem may require an excessive amount of time. Here we would like to point out that in this case we have another way to proceed: we can solve the full problem at special loci where the conditions on exponents are satisfied, and then interpolate between the resulting solutions.

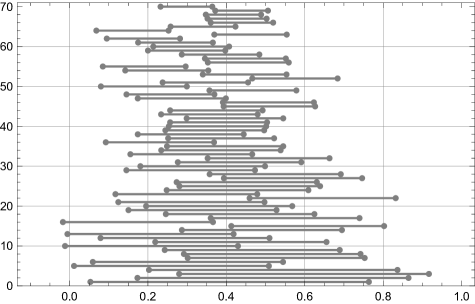

Let us illustrate this approach with a toy example that is not computationally intensive. Consider a monopolistic firm with marginal revenue , and marginal cost , . After the substitution , the firm’s first-order condition becomes , with . This equation admits closed-form solutions by the method of radicals for , ,,,1,2,3,4. The second-order condition is satisfied only for , so we restrict our attention to the first 9 values. For illustration, consider the simple goal of finding numerical values of for between these points. Instead of solving the first-order conditions by usual numerical methods, we may interpolate between the closed-form solutions, say, using cubic splines. Figure 4 shows the result of such interpolation, as well as the true solutions to the first-order condition, for . The agreement is extremely good, with average absolute value of relative deviations equal to 0.00013 and maximum absolute value of relative deviations equal to 0.00056.242424The corresponding values for Mathematica’s Hermite polynomial interpolation were 0.00069 and 0.0021.

If variables of interest in large scale, computationally intensive problems are similarly well behaved, then clearly the interpolation method could save remarkable amounts of computation time and research budgets. There are other ways to extend the usefulness of the closed-form solutions to other parameter values. For example, it may be possible to perform a Taylor expansion around a given closed-form solution. Such approach may also be combined with the interpolation method.

More broadly, one can view our approach to economic modeling as resembling pragmatic approaches in Bayesian Statistics. In that literature, it is usually impossible to compute the posterior probability distribution associated with most prior distributions given the observed, often large, data set. It is therefore common to approximate the prior by one selected from a class of prior distributions which are known to update to another prior within that class in closed form as this minimizes the computational requirements of updating. In a similar manner, our tractable equilibrium forms may approximate arbitrary cost and demand curves, while allowing solutions in closed-form which allow nesting inside of computationally intensive models.

In the next two sections we explore concrete applications of our approach to closed-form solutions in economics. We will return to more theoretical matters in Section 6.

4 World Trade

4.1 Overview

In this section we present a large-scale empirical application of our analytic approach to flexible functional forms in economics: a model of world trade with a realistic cost structure for heterogeneous firms.

International trade researchers almost always postulated constant marginal costs. Firms were assumed to have a constant marginal cost of production. They were also assumed to face constant marginal costs of trade, either in the “iceberg” form (i.e., damage of goods as they are transported) or in a per-unit form. Both of these assumptions are unrealistic. When we depart from them, we find an interpretation of world trade flows that is dramatically different from the conventional view. The model’s parameters and predictions take realistic values, which resolves empirical puzzles in the international trade literature.

Our model describes a world with multiple countries, with a general setup analogous to Melitz (2003). Our two important modifications are as follows. First, in addition to the usual iceberg cost, we allow for a specific cost of trade that varies non-linearly with the traded quantity. Second, production is subject to increasing marginal cost, designed to capture the difficulty of scaling the firm, e.g. due to internal agency problems. After discussing computational considerations and, separately, the two economic cost effects, we return to the setup of the main model in Subsection 4.6.

4.2 Computational considerations

In applied fields of economics, such as the study of international trade, researchers can quickly reach the limits of what is computationally feasible because of the number of economic agents and the high dimensionality of their choice sets (or state spaces). In our case, we study trade flows between many countries involving heterogeneous firms, each of which is facing a combinatorially difficult decision problem. With powerful hardware, software, and efficient algorithms, we were able to get a model fit for given parameter values in about a month and at a non-trivial cost. We were utilizing our analytic solutions to sub-problems, without which the computation would be substantially longer and more costly.

Our functional forms help us in two ways: First, to evaluate firms’ sales decisions conditional on the level of their marginal cost of production and export entry decisions, we just need to evaluate closed-form solutions. This is crucial for being able to quickly evaluate a large number of alternative sales patterns a firm may consider, and to find some of the best ones. Second, conditional of all firms’ export entry decisions, we can solve for the resulting general equilibrium of world trade by accelerated gradient descent algorithms, the Adam algorithm in our case. For this algorithm to be useful, we need to be able to calculate gradients of candidate solutions’ loss functions (error functions) analytically. Because of the scale of the problem, we do not perform the gradient calculation by hand. Instead, we rely on automatic analytic differentiation software, namely the neural-network optimization package of PyTorch, which allows us to run all computations in a highly parallel fashion on graphics processing units (GPUs).252525PyTorch is an open source software framework developed by Facebook primarily for deep learning in artificial neural networks. Its first version was released in 2017.

4.3 Firm-level economies of scale in shipping: a generalized Economic Order Quantity model

Most models of international trade assume that the costs of trade are of the “iceberg” type: a fraction of all goods transported is assumed to be destroyed in transit. It seems implausible that most of true trade costs would scale with trade volume and value in this manner.262626Tariffs would depend on value in the same way as iceberg trade costs, although the details of their impact would be different, as goods are not destroyed and governments collect tariff revenue. That said, most trade costs modeled as iceberg trade costs in the literature are not supposed to represent tariffs and we will not focus on tariffs in this paper, although, of course, they may be incorporated in our model. A certain fraction of international trade papers, e.g. Melitz and Ottaviano (2008), allow for constant marginal per unit costs of trade.272727Per-unit costs of trade seem more realistic than costs of trade proportional to the goods’ value, as documented by, e.g., Hummels and Skiba (2004). Note that this reference did not allow for non-linearity of trade costs. However, the adoption of standardized shipping containers has made such constant marginal per-unit costs of transportation extremely low relative to the trade costs necessary to explain the rates of global trade flows.

We work with the assumption that most important trade costs come from coordination (shipment preparation) costs and inventory costs, which is why the logistics literature focuses on them. These costs depend on the frequency of shipping. If a firm ships too infrequently, it will face large costs associated with idle inventory. If it ships too frequently, shipment preparation costs will add up to a large number. Knowing this trade-off, the firm will choose an optimal frequency of shipping that balances these two effects. The resulting effective cost of trade then exhibits economies of scale: a firm wishing to ship only a small quantity on average per unit of time will find shipping to be costly per unit of quantity.

To gain empirical insight into the scale economies of international trade, we estimate a model of optimal shipping frequency using monthly international shipment data. Our approach generalizes the classic Economic Order Quantity model of Ford W. Harris, which is widely taught in operations management courses in business schools and applied by logistics planning managers in corporations.282828Despite not appearing in the international trade literature, the Economic Order Quantity (EOQ) model (Harris, 1913) is perhaps the most classical model of trade costs in the operations research literature and is regularly taught to business students as a method of optimizing their inventory decisions; see e.g. Cárdenas-Barrón et al. (2014) for highlights of its importance. Judging from the absence of citations, the academic international trade community is largely unaware of Harris’ publication. When fixed costs per shipment are included in international trade models, they are incorporated in theoretical models with different structures. Those models are similar in spirit, but do not strictly speaking contain the EOQ model or its generalizations (Kropf and Sauré, 2014; Hornok and Koren, 2015a). These papers provide very useful insights into shipment frequency issues, and so does the purely empirical paper Hornok and Koren (2015b). Note also that economies of scale in shipping were studied by Anderson et al. (2014) and Forslid and Okubo (2016), but those approaches were not based on shipping frequency and in the former case involved external (i.e., not within-firm) economies of scale. Consider a firm that produces a single good in one country and wishes to ship to a different country quantity per year, on average. The firm faces a tradeoff between inventory costs and coordination costs associated with frequent shipping. The average annual inventory cost is linearly proportional to and to the time a typical unit of the good needs to remain in storage. If the size of each shipment is , then , in turn, is linearly proportional to , implying , for some constant . The coordination cost of each shipment is proportional to its size: , [0,1). (In addition, we could assume an additional term proportional to , but this would not affect the optimal choice of for given .) The resulting average annual coordination cost is . Minimizing the sum of the inventory cost and the coordination cost leads to the optimal choice , the minimized value , and the optimal frequency of shipping equal to

This result implies that we can infer the coordination cost exponent by examining the relationship between the average annual quantity shipped and the frequency of shipping. If we regress the logarithm of shipping frequency on the logarithm of average annual quantity , the resulting slope coefficient should equal . The model predicts that this coefficient always lies between 0 and 1/2, since [0,1).

Our simple model of shipping frequency choice nests two important extreme cases. The original Economic Order Quantity model, in which the cost per shipment is fixed, corresponds to and , implying effective cost of trade (here inventory and coordination) proportional to . The other extreme case has and and corresponds to effective cost of trade linearly proportional to , i.e., constant marginal cost of trade, as assumed in almost all of the international trade literature.

To estimate and to test the prediction that (0,1/2], we used a dataset on monthly shipments from China to Japan during years 2000-2006. We focus on firms in one narrowly-defined product category.292929We selected firms by requiring that they specialize in one product category (one 8-digit HS code). The exporting firm had to be active for more than two years to be included in our estimation sample. We selected industries that included at least 10 firms meeting these criteria, in order to work with industries that allow for a precise estimate of . We were also careful to take into account potential effects of seasonality, which could affect our estimates. We constructed a measure of seasonal variations of exports for individual industries. Our estimates of did not differ almost at all between industries with larger and smaller seasonality. We discuss more details in Appendix B. Our point estimate of (averaged across industries) is 0.39 with a 95 confidence interval of [0.36,0.42].303030The confidence interval corresponds to a simple statistical model in which for different industries is drawn from a normal distribution. We can thus clearly reject the null hypothesis that and , which would correspond to trade costs being linearly proportional to quantity shipped, as assumed in the vast majority of the international trade literature. We can also reject the original EOQ model, which would correspond to and . We see, however, that the original EOQ model is closer to reality than the linear proportionality assumption.

In our main trade model, we round the resulting value for from 0.39 to 0.4. This estimate implies that increasing quantity by 10 reduces (the variable component of) the marginal cost of trade by 4. We refer to the effective cost of trade as “cost of shipping”, remembering that it arises from per-shipment coordination costs and from inventory costs with optimally chosen shipping frequency. In the rest of this section, we use the notation for what was here, and set .

4.4 Export quantity determination

For clarity of exposition, let us now consider the problem of export quantity determination for a firm that faces trade costs found in the previous subsection. Similar ingredients will appear also in our main model described in Subsection 4.6.

A firm considers exporting to one foreign country. If it delivers quantity there, it will receive revenue , for which we choose the form , where and . The elasticity of demand is consistent with the typical range in the trade literature. The firm faces an iceberg trade cost factor , meaning that it needs to send in order for to arrive. The shipping requires units of labor, which translates into a cost . We choose , with , in agreement with the previous subsection. In this illustrative example, we assume constant marginal cost MC.

The second derivative of the profit function is , so the profit function is convex for and concave for . To identify the maximum, we just need to find potential local maxima in the second region and to check whether they are larger than zero. This is because at the profit is zero, and as it goes to .

The firm’s first-order condition is

We recognize that the function of on the left-hand side is one of our proposed tractable functional forms. We can, therefore, solve the first-order condition in closed-form, in this case using the quadratic formula. If there is no real solution and the firm will choose not to export. If , the solution that lies in the region equals

Plugging this position of the local maximum into the profit function gives

The first two factors are positive, and the last one is positive if and only if . If this condition is satisfied, the firm will export the quantity satisfying the first-order condition, otherwise, it will export zero.313131If exporting leads to zero profit just like not exporting, we specify that the firm chooses not to export. Thus for any level of marginal cost, the quantity chosen by the firm may be written compactly as

where the second factor represents an indicator function. We see that the functional form allowed for a very simple and straightforward analysis. We also see that exporting may not be profitable even if there is no fixed cost of exporting. This implies that such model with constant elasticity of demand can generate an export cutoff without fixed costs of exporting.

In our main model described in Subsection 4.6, which no longer assumes that the marginal cost of production is constant, we still benefit from the closed-form characterization of the solution to the first-order condition in terms of the level of marginal production cost. This is both for the evaluation of the solution and for taking derivatives of the solution, as needed by gradient descent algorithms. Of course, the degree of the benefit grows in proportion to the number of potential export destinations.

4.5 Increasing marginal cost of production

Economies of scale, modeled using fixed costs of production, are present in most models of firms in the international trade literature. By contrast, diseconomies of scale almost never appear in that literature. Yet there are many reasons to believe that increasing marginal costs of production are similarly important in shaping firms’ behavior. This is presumably why introductory economics classes frequently illustrate increasing marginal cost schedules. Beyond short-to-medium term capacity constraints and adjustment costs usually discussed in such courses, even in the longer term if a company decides to scale up its production an order of magnitude, it needs to introduce an additional layer of management hierarchy, which brings with it non-trivial agency problems. In a large organization incentives are diluted, and maintaining motivation, discipline, and output quality becomes harder.323232The restaurant industry is an obvious example: few people would associate chain restaurants with outstanding culinary experience. Another fairly obvious example is the automobile industry: there are many automakers in the world, each having a relatively small market share, very stable over time, even though cars produced by different automakers are highly substitutable from costumers’ perspective. With constant marginal costs of production this would require a remarkably small dispersion of marginal costs across firms, which is especially hard to rationalize given the large observed fluctuations of currency exchange rates. Also, the increasing nature of marginal costs of production was one of the reasons why socialist economies were unsuccessful: state-controlled monopolies avoid duplication of effort in product design and other fixed costs of production, yet they suffer from severe agency problems that private sector competition can mitigate. Although here we emphasize increasing marginal costs of production in the long term, they are also interesting at short time scales; see Almunia, Antràs, Lopez-Rodriguez and Morales (2018) and references therein. Of course, managers of firms are intuitively aware of these problems, at least to some extent, and take them to account when shaping the structure of the firm.

Issues of this kind are the subject of interest to vast literature within organizational economics, which includes Williamson (1967), Calvo and Wellisz (1978), and Tirole (1986).333333Oliver E. Williamson’s Nobel lecture (Williamson (2009)) provides an excellent, compact discussion of the many things that may go wrong in a large organization. For a related discussion, see Tirole (1988).

Estimating how much marginal costs increase with production volume is non-trivial since both economies and diseconomies of scale play a role in firm behavior. Our model provides a unique opportunity to obtain such estimates by matching firm-level multi-destination export data with world trade model solutions.

4.6 Model setup

Apart from the cost structure of the firms, our model is closely analogous to Melitz (2003), which many readers are familiar with. For this reason, we keep the description of the modeling setup succinct.

The world consists of countries, indexed by . In each country, different varieties of a differentiated good are produced by monopolistically competitive heterogeneous single-product firms using a single factor of production, for simplicity referred to as labor.

Consider a firm located in country and identified by an index . In order to produce a quantity , the firm needs to pay a variable cost of , where is the competitive wage the firm’s country and is a positive constant that depends on the firm. Importantly, the constant determines how quickly marginal costs increase when any firm decides to scale up production; it is the elasticity of the marginal cost of production with respect to quantity. In addition to the variable cost, there is a fixed cost of operation and a fixed cost of exporting to a destination country , expressed in units of domestic labor.343434In general, we can allow for country-dependence of these costs: and . We chose to make them country-independent for simplicity, not for tractability or computational feasibility reasons.

Entry into the industry is unrestricted, but involves a sunk cost of entry , again in units of domestic labor. Only after the entry cost has been paid does the firm learn its variable cost parameter , drawn from a distribution with cumulative distribution function . When the value of is revealed, the firm decides whether or not to exit the industry, and if it does not exit, whether to export to any of the other countries. In addition to endogenous exit, with a probability of per period the firm is exogenously forced to exit (starting from the end of the first period).

Trade costs have two components. The first corresponds to standard iceberg trade costs: in order of one unit of the good to arrive in the destination country , units need to be shipped.353535Including also per-unit trade costs would not affect the computational feasibility of the model. The second component requires using an amount of labor given by , where we set to be consistent with the empirical value, as in Subsection 4.4.363636The cost is associated with coordination/shipment preparation tasks and with inventory costs. Its form is motivated by the empirical results of Subsection 4.3.

Consumers in each country have a CES utility function that depends on the quantity of each variety consumed. As in Subsection 4.4, we set the elasticity of substitution equal to 5, which is consistent with the typical range in the existing empirical literature of about 4 to 8. This exact choice is motivated by analytic tractability. Each country has an endowment of labor , which is supplied at a country-specific competitive wage rate mentioned above.

The revenue a firm can earn by selling a quantity in a given market is , where . The factor is endogenously determined and depends on the price index and the consumption expenditures in the destination country.

The firm may choose to exit the industry (to save on the fixed cost ) or to operate and sell its product in a number of countries, earning a non-negative profit per period of operation. In expectation, an entrant needs to break even: , which determines the equilibrium measure of firms in each country.373737The model has no explicit discounting of future utility, but plays a role similar to a discount rate. Similarly, labor markets in each country need to clear, which means that the total labor demanded by firms at wage needs to equal the labor endowment . If we impose balanced budget conditions, consumers’ expenditures equal their wage earnings, as firms earn zero ex-ante profits.383838In our empirical setting we allow for budget imbalances that reflects similar imbalances in the data.

4.7 The exporting firm’s problem

Let us discuss the nature of the exporting firm’s problem. Increasing marginal costs will limit the scale of the firm’s production. Since trade is subject to decreasing marginal costs, the firm will concentrate its exports into a limited number of countries. The overall production level of firm as well as export market entry decisions are endogenous. For now let us consider the relation between of export quantities and , conditional on having paid fixed costs of exporting to a number of countries.

The first-order condition for choosing the quantity that should reach a foreign market equates the marginal revenue and the comprehensive marginal cost that depends on the overall production level :

in analogy with Subsection 4.4. The solution for given is:

If the marginal cost of production exceeds /(), the first-order condition cannot be satisfied. For domestic sales we assume and , so the optimal quantity sold domestically is simply .

The total quantity produced should equal the total of quantity sold domestically and sent abroad: , with given by the formula above. This represents one equation for one unknown: . Each root of this equation

represents a candidate optimum for the firm.393939Mathematically, the firm’s choice of

destinations in order to maximize profit is a submodular function maximization. This is because serving an additional set of markets is less

attractive if the initial set of markets is larger:

for and . Here denotes the optimal profit a firm can earn if it serves a set of markets . If instead our problem was supermodular

function maximization, it would be algorithmically easy. International trade papers such as Antràs et al. (2017) take advantage

of supermodular function maximization being straightforward. The profit-maximizing choice(s) of destinations

may then be found by evaluating total profits at these candidate optima. For a small number of countries this is simple, but for large the

problem becomes combinatorially difficult.404040For an in-depth discussion of combinatorial

discrete choice problems in economics, see Eckert and Arkolakis (2017). The method that Eckert and Arkolakis

propose would be useful for us if the number of countries we consider were substantially smaller. This is because the method reduces the exponent

of an exponentially difficult problem, but does not change its exponential nature; submodular function maximization is NP-hard in general. For this reason, when we solve the model for a large number of countries, we use approximate algorithms instead of an exhaustive

search.414141We should clarify that even conditional on having made export fixed-cost payments,

the number of candidate optima is still combinatorially large. This is because for some destinations it may be impossible to satisfy the FOC and

in those cases we allow the firm to export zero amount there. To avoid this difficulty, when we consider candidate optima, we restrict attention

to those that satisfy a particular ordering condition, without loss of generality. We rank export destinations by the level of (constant) marginal

cost that would make them a profitable destination, in descending order. Then we require that if a firm exports a positive amount to a given destination,

it also exports to all preceding destinations. Imposing this condition is without loss of generality because if a firm decides to export zero amount

to a destination, it should not have paid the associated fixed cost of exporting in the first place.

4.8 Solution strategy

We solve the model using an iterative algorithm that has an outer loop and an inner loop.424242Due to its combinatorial nature, the exact version of our model is computationally extremely difficult. It may seem natural to try to obtain approximate solutions by first fixing aggregate variables in the model, solving for firm decisions given these aggregates, and then updating the aggregate variables based on the firms’ behavior. We attempted to do that, but could not get results within a reasonable amount of time and budget. This is because for any values of aggregates, we needed to solve separate discrete choice problems by many firms, which requires a lot of time. For this reason, we used a different nesting of loops: we moved all discrete choice decisions into an outer loop of an iterative algorithm, and given these discrete choices, we solved for all continuous variables in an inner loop. In the outer loop firms decide whether or not they pay fixed costs of operation and fixed costs of exporting and commit to their decision. In the inner loop, we then solve for the general equilibrium of the world economy given these fixed-cost decisions.

Finding this general equilibrium without the tractable functional forms is computationally difficult since a multi-level nested iteration is very time-consuming. However, thanks to the analytic nature of our model, we were able to obtain the general equilibrium much faster using accelerated gradient descent in a space parametrized by quantities , wages , measures of firms , price-index related variables , and country-level expenditures . We used the Adam optimizer of Kingma and Ba (2014), as implemented in PyTorch, a neural network optimization software for GPU computing.434343We tried several accelerated and non-accelerated gradient descent algorithms. Adam performed the best. The gradients are computed analytically by automatic differentiation (autograd, in this case) and backpropagation.444444Our model, as detailed in the next subsection, had more than 20,000 variables and described 2 million potential trade flows. Newton’s method would not be feasible here, given that the Hessian of the loss function would have 400 million entries, although light-weight second order methods, such as L-BFGS, could potentially be useful. They would again benefit from the analytic nature of our model. For an overview of optimization algorithms, see the excellent book by Goodfellow, Bengio and Courville (2016).454545Given firms’ sunk cost decisions, we need to solve for the general equilibrium of the world economy, i.e., we need to solve for wages, price indexes, and the measure of firms of each type in each country, as well as for production levels of each firm. What makes our calculation fast is the fact that we have explicit formulas for quantities sent to individual destinations conditional on the firm’s marginal cost, and that these formulas and their derivatives may be evaluated extremely fast.

Given a solution to the general equilibrium problem, we then let firms reconsider their fixed cost payments. For numerical stability, we do not update at once the fixed cost payment decisions of all firms. Instead, for each productivity level in a country we introduce versions (copies) of firms, which can differ by their fixed cost commitments. Updating fixed-cost commitments then proceeds in cohorts. In one iteration of the outer loop, version 1 firms will be able to reconsider the fixed cost payment. In the second iteration, version 2 firms will do so, etc. Keeping different versions of firms comes at a computational cost, of course, but we found this necessary.

Finding the best fixed cost decision is a combinatorially difficult problem. Given that there are potential export destinations, this leads to possibilities for the exports. With , this is more than . To obtain an approximate optimum, we use Algorithm 2 of Buchbinder et al. (2015), which is stochastic in nature. We consider 9 (random) runs of that algorithm, and if the best of them is better than the firm’s previous fixed cost decision, we update it. After the update, we again solve for a new general equilibrium involving continuous variables.

4.9 Fitting the model

We work with countries. This choice is motivated by data availability and parameter fit considerations: For a substantially larger number of countries, the trade data would be too noisy and unreliable. For a substantially smaller number, it would be impossible to read off the elasticity of the marginal production cost from the firms’ export pattern using our method.

The labor endowment in the model is interpreted as an efficiency-adjusted number of units of a single production factor, which in practice would include labor, capital, and the related productivity. This effective labor endowment and the trade cost prefactors are recovered by fitting the model to data on country GDP and world trade flows for the year 2006, as described below.

To match the typical empirical firm size distribution, which we take as Pareto distribution with Pareto index , we choose the firm size distribution to be another Pareto distribution with Pareto index .464646The value of 1.05 for the Pareto index of the firm size distribution has empirical support in Aoyama et al. (2010), at least for the advanced economies studied there. In our open-economy model, there is no simple closed-form expression for the firm size (revenue) as a function of firm productivity. For this reason we use a formula that would hold exactly for closed economies, as well as in the absence of trade costs for the world. Simple algebra shows that the required value of the productivity Pareto index is and we use this value. The calibration results in a good match for the firm size distribution of Chinese exporters (both for all firms and for single-HSID firms, as these have the same empirical shape). Given this encouraging result, we have not explored other specifications for the productivity distribution. The productivity distribution is the same for every country in the model; any real-world overall firm productivity differences across countries are represented by adjustments to the countries’ effective labor endowments.

For computational purposes we discretize the productivity distribution to discrete values, each representing the same probability mass.474747Initially, we tried , but such crude discretization led to numerical errors that were too large. Also note that even though for simplicity we sometimes refer to the probability masses as “firms”, they really represent collections of firms in monopolistic competition, not a few discrete firms in an oligopoly model.

In addition, we need to specify (the flow value of) the costs of entry, fixed costs of production, export market entry costs, as well as iceberg trade costs. We make these choices as simple as possible, independent of the country or country pair. Their values are given in Table 2. The flow value of the cost of entry is set to one half of the fixed cost of operation. The fixed cost of exporting is set to be negligible. The iceberg trade cost is non-zero but small enough to be consistent with prices firms in practice pay for insurance or as tariffs. In general, the parameters are chosen to reflect a long-term interpretation of the model, with timescales of many years.484848We do not attempt to model high-frequency phenomena in international trade (except that shipping frequency considerations provide a micro-foundation for our trade costs). For studying month-to-month or year-to-years changes, it would not be appropriate to assume that the sunk fixed cost of exporting is fairly negligible.

| 100 | 20 | 10 | multiple values | ||||

| 5 | 0.8 | 0.6 | 1.05 | ||||

| 0.05 | 0.1 | 1.05 |

We use importer-reported data on international trade flows for the year 2006 from the UN Comtrade database. We select 100 countries/economies with the largest GDP, as reported by the IMF in its World Economic Outlook database, subject to trade and GDP data availability. We adjust the countries’ GDP for tradability using the United Nations’ gross value added database; see Appendix C.

4.10 Elasticity of the marginal cost of production

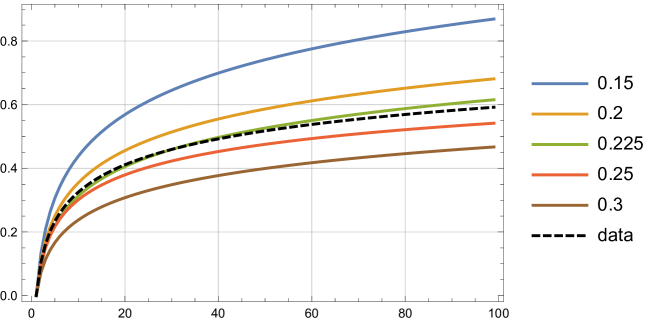

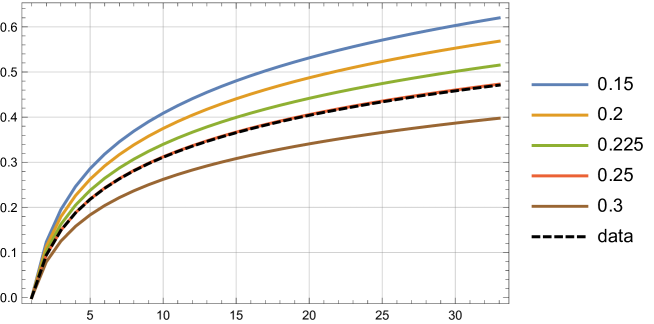

We solve for the model fit for different values of the parameter , the quantity-elasticity of the marginal cost of production. Then we compare the resulting pattern of firm trade with that of Chinese firm-level export data for 2006 in order to find what value of leads to a good agreement.

We obtained fits to the data on world trade flows and adjusted GDP levels for values of ranging from 0.15 to 0.3; see Figure 5. In each case, we computed power-law best-fit curves that describe the dependence of the median size of Chinese firms that export to a destination as a function of the popularity rank of that export destination.494949More precisely, we use the generalized method of moments to fit functions of the form . The popularity is computed as the fraction of Chinese firms in the data that choose to export to the given destination. We also computed such best-fit curve for the data. The results are intuitive: For smaller , the difference between the median (log) size of firms exporting to unpopular destinations and to popular destinations is larger because in this case the most productive firms will dominate world trade, and if a less productive firm decides to export at all, it will choose a few of the popular destinations.