Inference for Additive Models in the Presence of Possibly Infinite Dimensional Nuisance Parameters

Abstract

A framework for estimation and hypothesis testing of functional restrictions against general alternatives is proposed. The parameter space is a reproducing kernel Hilbert space (RKHS). The null hypothesis does not necessarily define a parametric model. The test allows us to deal with infinite dimensional nuisance parameters. The methodology is based on a moment equation similar in spirit to the construction of the efficient score in semiparametric statistics. The feasible version of such moment equation requires to consistently estimate projections in the space of RKHS and it is shown that this is possible using the proposed approach. This allows us to derive some tractable asymptotic theory and critical values by fast simulation. Simulation results show that the finite sample performance of the test is consistent with the asymptotics and that ignoring the effect of nuisance parameters highly distorts the size of the tests.

Key Words: Constrained estimation, convergence rates, functional restriction, hypothesis testing, nonlinear model, reproducing kernel Hilbert space.

1 Introduction

Suppose that you are interested in estimating the number of event arrivals in the next one minute, conditioning on a vector of covariates known at the start of the interval. You decide to minimize the negative log-likelihood for Poisson arrivals with conditional intensity for some function . For observation , the negative loglikelihood is proportional to

| (1) |

You suppose that lies in some infinite dimensional space. For example, to avoid the curse of dimensionality, you could choose

| (2) |

where denotes the covariate (the element of the -dimensional covariate ), and the univariate functions are elements in some possibly infinite dimensional space. However, you suppose that is a linear function. You want to test whether linearity with respect to the first variable holds against the alternative of a general additive model. You could also test against the alternative of a general continuous multivariate function, not necessarily additive. This paper addresses practical problems such as the above. The paper is not restricted to this Poisson problem or additive models on real valued variables.

From the example above, we need to (i) estimate , which in this example we chose to be additive with linear under the null; we need to (ii) test this additive restriction, against a more general non-parametric alternative. Under the null, the remaining functions in (2) are not specified. Problem (i) is standard, though the actual numerical estimation can pose problems. Having solved problem (i), solution of problem (ii) requires to test a non-parametric hypothesis (an additive model with linear ) with infinite dimensional nuisance parameters (the remaining unknown functions) against a more general non-parametric alternative. In this paper, we shall call the restriction under the null semi-parametric. This does not necessarily mean that the parameter of interest is finite dimensional, as often the case in the semiparametric literature.

Semiparametric inference requires that the infinite dimensional parameter and the finite dimensional one are orthogonal in the population (e.g., Andrews, 1994, eq.(2.12)). In our Poisson motivating example this is not the case. Even if the restriction is parametric, we do not need to suppose that the parameter value is known under the null. This requires us to modify the test statistic in order to achieve the required orthogonality. Essentially, we project the test statistic on some space that is orthogonal to the infinite dimensional nuisance parameter. This is the procedure involved in the construction of the efficient score in semiparametric statistics. The reader is referred to van der Vaart (1998) for a review of the basic idea. Here, we are concerned with functional restrictions and are able to obtain critical values by fast simulation. In many empirical application, the problem should possibly allow for dependent observations. The extension to dependence is not particularly complicated, but will require us to join together various results in a suitable way.

Throughout, we shall use the framework of reproducing kernel Hilbert spaces. The RKHS setup is heavily used in the derivations of the results. Estimation in these spaces has been studied in depth and is flexible and intuitive from a theoretical point of view. RKHS also allow us to consider multivariate problems in a very natural way. In consequence of these remarks, this paper’s main contribution to the literature is related to testing rather than estimation. Nevertheless, as far as estimation is concerned, we do provide results that are partially new. For example, we establish insights regarding the connection between constrained and penalized estimation together with convergence rates using possibly dependent observations.

Estimation in RKHS can run into computational issues when the sample size is large, as it might be the case in the presence of large data sets. We will address practical computational issues. Estimation of the model can be carried out via a greedy algorithm, possibly imposing LASSO kind of constraints under additivity.

Under the null hypothesis, we can find a representation for the limiting asymptotic distribution which is amenable of fast simulation. In consequence critical values do not need to be generated using resampling procedures. While the discussion of the asymptotic validity of the procedure is involved, the implementation of the test is simple. The Matlab code for greedy estimation, to perform the test, and compute its critical values is available from the URL: <https://github.com/asancetta/ARKHS/>. A set of simulations confirm that the procedure works well, and illustrates the well known fact that nuisance parameters can considerably distort the size of a test if not accounted for using our proposed procedure. The reader can have a preliminary glance at Table 1 in Section 2.1, and Table 2 in Section 6.1 to see this more vividly.

1.1 Relation to the Literature

Estimation in RKHS has been addressed in many places in the literature (see the monographs of Wahba, 1990, and Steinwart and Christmann, 2008). Inference is usually confined to consistency (e.g., Mendelson, 2002, Christmann and Steinwart, 2007), though there are exceptions (Hable, 2012, in the frequentist framework). A common restriction used in the present paper is additivity and estimation in certain subspaces of additive functions. Estimation of additive models has been extensively studied by various authors using different techniques (e.g., Buja et al., 1989, Linton and Nielsen, 1995, Mammen et al., 1999, Meier et al., 2009, Christmann and Hable, 2012). The last reference considers estimation in RKHS which allows for a more general concept of additivity. Here, the assumptions and estimation results are not overall necessarily comparable to existing results. For example, neither independence nor the concept of true model are needed. Moreover, we establish rates of convergence and the link between constrained versus penalized estimation in RKHS. The two are not always equivalent.

The problem of parametric inference in the presence of non-orthogonal nuisance parameters has been addressed by various authors by modification of the score function or equivalent quantities. Belloni et al. (2017) provide general results in the context of high dimensional models. There, the reader can also find the main references in that literature. The asymptotic distribution usually requires the use of the bootstrap in order to compute critical values.

The problem of testing parametric restrictions with finite dimensional nuisance parameter under the null against general nonparametric alternatives is well known (Härdle and Mammen, 1993), and requires the use of the bootstrap in order to derive confidence intervals. Fan et al. (2001) have developed a Generalized Likelihood Ratio test of the null of parametric or nonparameteric additive restrictions versus general nonparametric ones. This is based on a Gaussian error model (or parametric error distribution) for additive regression, and estimation using smoothing kernels. Fan and Jiang (2005) have extended this approach to the nonparametric error distribution. The asymptotic distribution is Chi-square with degrees of freedom equal to some (computable) function of the the data. Chen et al.(2014) considers the framework of sieve estimation and derives a likelihood ratio statistic with asymptotic Chi-square distribution (see also Shen and Shi, 2005).

The approach considered here is complementary to the above references. It allows the parameter space to be a RKHS of smooth functions. Estimation in RKHS is well understood and can cater for many circumstances of interest in applied work. For example, it is possible to view sieve estimation as estimation in RKHS where the feature space defined by the kernel increases with the sample size. The testing procedure is based on a corrected moment condition. Hence, it does not rely on likelihood estimation. The conditions used are elementary, as they just require existence of real valued derivatives of the loss function (in the vein of Christmann and Steinwart, 2007) and mild regularity conditions on the covariance kernel. We also allow for dependent errors. The correction is estimated by either ridge regression, or just ordinary least square using pseudo-inverse.

For moderate sample sizes (e.g. less than 10,000) estimation in RKHS does not pose particular challenges and it is trivial for the regression problem under the square error loss. For large sample sizes, computational aspects in RKHS have received a lot of attention in the literature (e.g., Rasmussen and Williams, 2006, Ch.8, Banerjee et al., 2008, Lázaro-Gredilla et al., 2010).

Here we discuss a greedy algorithm, which is simple to implement (e.g., Jaggi, 2013, Sancetta, 2016) and, apparently, has not been applied to the RKHS estimation framework of this paper.

1.2 Outline

The plan for the paper is as follows. Section 2 reviews some basics of RKHS, defines the problem and model used in the paper, and describes the implementation of the test. Section 3 contains the asymptotic analysis of the estimation problem and the proposed testing procedure in the presence of nuisance parameters. Section 4 provides some additional discussion of the conditions and the asymptotic analysis. Some details related to computational implementation can be found in Section 5. Section 6 concludes with a finite sample analysis via simulations. It also discusses the partial extension to non-smooth loss functions, which exemplify one of the limitations in the framework of the paper. The proofs, and additional results are in the Appendices as supplementary material.

2 The Inference Problem

The explanatory variable takes values in , a compact subset of a separable Banach space (). The most basic example of is . The vector covariate takes values in the Cartesian product , e.g., . The dependent variable takes values in usually . Let and this takes values in . If no dependent variable can be defined (e.g., unsupervised learning, or certain likelihood estimators), . Let be the law of , and use linear functional notation, i.e., for any , . Let , where is the point mass at , implying that is the sample mean of . For , let be the norm (w.r.t. the measure ), e.g., for , , with the obvious modification to norm when .

2.1 Motivation

The problem can be described as follows, though in practice we will need to add extra regularity conditions. Let be a vector space of real valued functions on , equipped with a norm . Consider a loss function . We shall be interested in the case where the second argument is : with . Therefore, to keep notation compact, let . For the special case of the square error loss we would have (). The use of makes it more natural to use linear functional notation. The unknown function of interest is the minimizer of , and it is assumed to be in . We find an estimator where the infimum is over certain functions in . The main goal it to test the restriction that for some subspace of (for example a linear restriction). The restricted estimator in is denoted by . To test the restriction we can look at how close

| (3) |

is to zero for suitable choice of . Throughout, is the partial derivative of with respect to and then evaluated at . The validity of this derivative and other related quantities will be ensured by the regularity conditions we shall impose. The compact notation on the left hand side (l.h.s.) of (3) shall be used throughout the paper. If necessary, the reader can refer to Section A.2.5 in the Appendix (supplementary material) for more explicit expressions when the compact notation is used in the main text. If the restriction held true, we would expect (3) to be mean zero if we used in place of . A test statistic can be constructed from (3) as follows:

| (4) |

where , .

If is finite dimensional, or is orthogonal to the functions (e.g., Andrews, 1994, eq. 2.12), the above display is - to first order - equal in distribution to , under regularity conditions. However, unless the sample size is relatively large, this approximation may not be good. In fact, supposing stochastic equicontinuity and the null that , it can be shown that (e.g., Theorem 3.3.1 in van der Vaart and Wellner, 2000),

The orthogonality condition in Andrews (1994, eq., 2.12) guarantees that the second term on the right hand side (r.h.s.) is zero (Andrews, 1994, eq.2.8, assuming Fréchet differentiability). Hence, we aim to find/construct functions such that the second term on the r.h.s. is zero. In fact this term can severely distort the asymptotic behaviour of .

An example is given in Table 1 which is an excerpt from the simulation results in Section 6.1. Here, the true model is a linear model with 3 variables plus Gaussian noise with signal to noise ratio equal to one. We call this model Lin3. We use a sample of observations with variables. Under the null hypothesis, only the first three variables enter the linear model, against an alternative that all variables enter the true model in an additive nonlinear form. The subspace of these three linear functions is while the full model is . The test functions are restricted to polynomials with no linear term. Details can be found in Section 6.1. The nuisance parameters are the three estimated linear functions, which are low dimensional. It is plausible that the estimation of the three linear functions (i.e. ) should not affect the asymptotic distribution of (4). When the variables are uncorrelated, this is clearly the case as confirmed by the 5% size of the test in Table 1. It does not matter whether we use instruments that are orthogonal to the linear functions or not. However, as soon as the variables become correlated, Table 1 shows that the asymptotic distribution can be distorted. This happens even in such a simple finite dimensional problem. Nevertheless, the test that uses instruments that are made orthogonal to functions in is not affected. The paper will discuss the empirical procedure used to construct such instruments and will study its properties via asymptotic analysis and simulations.

| Lin3 | ||||||

| =100 | =1000 | |||||

| Size | No | No | ||||

| 0 | 1 | 0.05 | 0.03 | 0.06 | 0.05 | 0.05 |

| 0.75 | 1 | 0.05 | 0.02 | 0.05 | 0.03 | 0.05 |

The situation gets really worse with other simulation designs that can be encountered in applications and details are given in Section 6.1. More generally, can be a high dimensional subspace of or even an infinite dimensional one, e.g. the space of additive functions when does not impose this additive restriction. In this case, it is unlikely that functions in are orthogonal to functions in and the distortion due to the nuisance parameters will be larger than what is shown in Table 1.

Here, orthogonal functions are constructed to asympotically satisfy

| (5) |

for any when is inside . The above display will allow us to carry out inferential procedures as in cases previously considered in the literature. The challenge is that the set of such orthogonal functions needs to be estimated. It is not clear before hand that estimation leads to the same asymptotic distribution as if this set were known. We show that this is the case. Suppose that is a set of such estimated orthogonal functions using the method to be spelled out in this paper. The test statistic is

| (6) |

We show that its asymptotic distribution can be easily simulated.

Next, some basics of RKHS are reviewed and some notation is fixed. Restrictions for functions in are discussed and finally the estimation problems is defined.

2.2 Additional Notation and Basic Facts about Reproducing Kernel Hilbert Spaces

Recall that a RKHS on some set is a Hilbert space where the evaluation functionals are bounded. A RKHS of bounded functions is uniquely generated by a centered Gaussian measure with covariance (e.g., Li and Linde, 1999) and is usually called the (reproducing) kernel of . We consider covariance functions with representation

| (7) |

for linearly independent functions and coefficients such that . Here, linear independent means that if there is a sequence of real numbers such that and for all , then for all . The coefficients would be the eigenvalues of (7) if the functions were orthonormal, but this is not implied by the above definition of linear independence. The RKHS is the completion of the set of functions representable as for real valued coefficient such that . Equivalently, , for coefficients in and real valued coefficients satisfying . Moreover, for in (7),

| (8) |

by obvious definition of the coefficients . The change of summation is possible by the aforementioned restrictions on the coefficients and functions . The inner product in is denoted by and satisfies . This implies the reproducing kernel property . Therefore, the square of the RKHS norm is defined in the two following equivalent ways

| (9) |

Throughout, the unit ball of will be denoted by .

The additive RKHS is generated by the Gaussian measure with covariance function , where is a covariance function on (as in (7)) and is the element in . The RKHS of additive functions is denoted by , which is the set of functions as in (2) such that and . For such functions, the inner product is , where - for ease of notation - the individual RKHS are supposed to be the same. However, in some circumstances, it can be necessary to make the distinction between the spaces (see Example 6 in Section 3.3). The norm on is the one induced by the inner product.

Within this scenario, the space restricts functions to be additive, where these additive functions in can be multivariate functions.

Example 1

Suppose that and () (only one additive function, which is multivariate). Let where is the element in , and . Then, the RKHS is dense in the space of continuous bounded functions on (e.g., Christmann and Steinwart, 2007). A (kernel) with such property is called universal.

The framework also covers the case of functional data because is a compact subset of a Banach space (e.g., Bosq, 2000). Most problems of interest where the unknown parameter is a smooth function are covered by the current scenario.

2.3 The Estimation Problem

Estimation will be considered for models in , where is a fixed constant. The goal is to find

| (10) |

i.e. the minimizer with respect to of the loss function .

Example 2

Let so that

By duality, we can also use with sample dependent Lagrange multiplier such that .

For the square error loss the solution is just a ridge regression estimator with (random) ridge parameter . Interest is not restricted to least square problems.

Example 3

Consider the negative log-likelihood where is a duration, and is the hazard function. Then, so that .

Even though the user might consider likelihood estimation, there is no concept of “true model” in this paper. The target is the population estimate

| (11) |

We shall show that this minimizer always exists and is unique under regularity conditions on the loss because is closed.

Theorem 1 in Schölkopf et al. (2001) says that the solution to the penalized problem takes the form for real valued coefficients . Hence, even if the parameter space where the estimator lies is infinite dimensional, is not. This fact will be used without further mention in the matrix implementation of the testing problem.

2.4 The Testing Problem

Inference needs to be conducted on the estimator in (10). To this end, consider inference on functional restrictions possibly allowing not to be fully specified under the null. Within this framework, tests based on the moment equation for suitable test functions are natural (recall (6)). Let be the RKHS with kernel . Suppose that we can write , where is some suitable covariance function. Under the null hypothesis we suppose that ( as in (11)). Under the alternative, . Define

| (12) |

where . This is the estimator under the null hypothesis. For this estimation, we use the kernel . The goal is to consider the quantity in (3) with suitable .

2.4.1 Matrix Implementation

We show how to construct the statistic in (6) using matrix notation. Consider the regression problem under the square error loss: nonlinear least squares. Let be the matrix with entry equal to , the vector with entry equal to . The penalized estimator is the vector . Here, can be chosen such that so that the constraint is satisfied: is in ; here is the entry in and the superscript T is used for transposition. For other problems the solution is still linear, but the coefficients usually do not have a closed form. For the regression problem under the square error loss, if the constraint is binding, the that satisfies the constraint is given by the solution of

where is the eigenvector of and here is the corresponding eigenvalue.

The restricted estimator has the same solution with replaced by which is the matrix with entry . For the square error loss, let be the vector or residuals under the null. (For other problems, is the vector of generalized residuals, i.e. the entry in is .) Under the alternative we have the covariance kernel . Denote by the matrix with entry . Let be the diagonal matrix with diagonal entry equal to . In our case, this entry can be taken to be one, as the second derivative of the square error loss is a constant. However, the next step is the same regardless of the loss function, as we only need to project the functions in onto and consider the orthogonal part. This ensures that the sample version of the orthogonality condition (5) is satisfied. We regress each column of on the columns of . We denote by the column in . We approximately project onto the column space spanned by minimizing the loss function

Here is chosen to go to zero with the sample size (Theorem 3 and Corollary 2). In applications, we may just use a subset of columns from and to avoid notational trivialities, say the first . The solution for all is

and can be verified substituting it in the first order conditions. Let the residual vector from this regression be . In sample, this is orthogonal to the column space of when . We define the instruments by . The test statistic is . Under regularity conditions, if the true parameter lies inside , the vector is asymptotically Gaussian for any and its covariance matrix is consistently estimated by . The distribution of can be simulated from the process , where the random variables are i.i.d. standard normal and the real valued coefficients are eigenvalues of the estimated covariance matrix.

Operational remarks.

-

1.

If is not explicitly given, we can set in the projection step.

-

2.

Instead of we can use a subset of the columns of , e.g. columns. Each column is an instrument.

-

3.

The column of can be replaced by an vector with entry where is an arbitrary element in .

-

4.

To keep the test functions homogeneous, we can set the column of to have entry equal to ; note that satisfies by the reproducing kernel property.

-

5.

When the series expansion (7) for the covariance is known, we can use the elements in the expansion. For example, suppose and are mutually exclusive subsets of the natural numbers such that for . We can directly “project” the elements in onto the linear span of by ridge regression with penalty . For of finite but increasing cardinality, the procedure covers sieve estimators with restricted coefficients. Note that satisfies for .

Additional remarks.

The procedure can be seen as a J-Test where the instruments are given by the ’s. Given that the covariance matrix of the vector can be high dimensional (many instruments for large ) we work directly with the unstandardized statistic. This is common in some high dimensional problems, as it is the case in functional data analysis.

We could replace with . The maximum of correlated Gaussian random variables can be simulated or approximated but it might be operationally challenging (Hartigan, 2014, Theorem 3.4).

The rest of the paper provides details and justification for the estimation and testing procedure. The theoretical justification beyond simple heuristics is technically involved. Section 6.1 (Tables 2 and 3) will show that failing to use the projection procedure discussed in this paper leads to poor results. Additional details can be found in Appendix 2 (supplementary material).

3 Asymptotic Analysis

3.1 Conditions for Basic Analysis

Throughout the paper, means that the l.h.s. is bounded by an absolute constant times the r.h.s..

Condition 1

The set is a RKHS on a compact subset of a separable Banach space , with continuous uniformly bounded kernel admitting an expansion (7), where with exponent and with linearly independent continuous uniformly bounded functions . If each additive component has a different covariance kernel, the condition is meant to apply to each of them individually.

Attention is restricted to loss functions satisfying the following, though generalizations will be considered in Section 6.2. Recall the loss from Section 2.1. Let where . Define for .

Condition 2

The loss is non-negative, twice continuously differentiable for real in an open set containing , and for and . Moreover, for some .

The data are allowed to be weakly dependent, but restricted to uniform regularity.

Condition 3

The sequence () is stationary, with beta mixing coefficient for , where is as in Condition 2.

Remarks on the conditions can be found in Section 4.1.

3.2 Basic Results

This section shows the consistency and some basic convergence in distribution of the estimator. These results can be viewed as a review, except for the fact that we allow for dependent random variables. We also provide details regarding the relation between constrained, and penalized estimators and convergence rates. The usual penalized estimator is defined as

| (13) |

for . As mentioned in Example 2, suitable choice of leads to the constrained estimator. Throughout, will denote the interior of .

Theorem 1

Suppose that Conditions 1, 2, and 3 hold. The population minimizer in (11) is unique up to an equivalence class in .

- 1.

-

2.

Consider (10). We also have that , and if is finite dimensional the r.h.s. is .

-

3.

Consider possibly random such that and in probability. Suppose that there is a finite such that . Then, in probability, and in consequence with probability going to one.

-

4.

If is infinite dimensional, there is a such that , , and in probability, but does not converge to zero in probability.

All the above consistency statements also hold if and in (10) and (13) are approximate minimizers in the sense that the following hold

and

The above result establishes the connection between the constrained estimator in (10) and the penalized estimator in (13). It is worth noting that whether is finite or infinite dimensional, the estimator is equivalent to a penalized estimator with penalty parameter going to zero relatively fast (i.e. does not hold). However, this only ensures uniform consistency and not consistency under the RKHS norm (Point 3 in Theorem 1). For the testing procedure discussed in this paper, we need the estimator to be equivalent to a penalized one with penalty that converges to zero fast enough. This is achieved working with the constrained estimator .

Having established consistency, interest also lies in the distribution of the estimator. We shall only consider the constrained estimator . To ease notation, for any arbitrary, but fixed real valued functions and on define . For suitable and , the quantity will be used as short notation for sums of population covariances. We shall also use the additional condition , where is as in Section 3.1.

Theorem 2

Suppose Conditions 1, 2, and 3 hold. If , then

weakly, where is a mean zero Gaussian process with covariance function

for any .

Now, in addition to the above, also suppose that . If is an asymptotic minimizer such that , and , then,

The second statement in Theorem 2 cannot be established for the penalized estimator with penalty satisfying . The restriction holds for finite dimensional models as long as . When testing restrictions, this is often of interest. However, for infinite dimensional models this is no longer true as the constraint is binding even if . Then, it can be shown that the term has to be replaced with (Lemma 8, in the Appendix). This has implications for testing. Additional remarks can be found in Section 4.2.

3.3 Testing Functional Restrictions

This section considers tests on functional restrictions possibly allowing not to be fully specified under the null. As previously discussed, we write as in Section 2.3. It is not necessary that , but must be a proper subspace of as otherwise there is no restriction to test. Hence, is not necessarily the complement of in . A few examples clarify the framework. We shall make use of the results reviewed in Section 2.2 when constructing the covariance functions and in consequence the restrictions.

3.3.1 Examples

Example 4

Some functional restrictions can also be naturally imposed.

Example 5

Suppose that is an additive space of functions, where each univariate function is an element in the Sobolev Hilbert space of index on , i.e. functions with square integrable weak derivatives. Then, where and where is the covariance function of the -fold integrated Brownian motion (see Section A.2.1, in the supplementary material, or Wahba, 1990, p.7-8, for the details). Consider the subspace that restricts the univariate RKHS for the first covariate to be the set of linear functions, i.e. for real . Then, . Hence we can choose .

In both examples above, is the complement of in . However, we can just consider spaces and to define the model under the null and the space of instruments under the alternative.

Example 6

Suppose is a universal kernel on (see Example 1). We suppose that , while . If is continuous and bounded on , then, . In this case we are testing an additive model against a general nonlinear one.

It is worth noting that Condition 1 restricts the individual covariances in . The same condition is inherited by the individual covariances that comprise (i.e. Condition 1 applies to each individual component of ). In a similar vein, in Example 6, the covariance can be seen as the individual covariance of a multivariate variable and will have to satisfy (7) where the features ’s are functions of the variable . Hence, also Example 6 fits into our framework, though additional notation is required (see Section A.2.1, in the supplementary material for more details).

The examples above can be extended to test more general models.

Example 7

Consider the varying coefficients regression function . The function can be restricted to linear or additive under the null . In the additive case, . In finance, this model can be used to test the conditional Capital Asset Pricing Model and includes the semiparametric model discussed in Connor et al. (2012).

3.3.2 Correction for Nuisance Parameters

Recall that for any and similarly for . Suppose that in (11) lies in the interior of . Then, the moment equation holds for any . This is because, by definition of (11), is orthogonal to all elements in . By linearity, one can restrict attention to (i.e. with ). For such functions , the statistic is normally distributed by Theorem 2. In practice, is rarely known and it is replaced by in (12). The estimator does not need to satisfy for any in under the null. Moreover, the nuisance parameter affects the asymptotic distribution because it affects the asymptotic covariance. From now on, we suppose that the restriction is true, i.e. in (11) lies inside , throughout.

For fixed , let be the penalized population projection operator such that

| (14) |

for any . Let the population projection operator be , i.e. (14) with . We need the following conditions to ensure that we con construct a test statistic that is not affected by the estimator .

Condition 4

Remarks on these conditions can be found in Section 4.1. The following holds.

Theorem 3

Suppose that Condition 4 holds and that is such that . Under the null , we have that

weakly, where the r.h.s. is a mean zero Gaussian process with covariance function

for any .

Theorem 3 says that if we knew the projection (14), we could derive the asymptotic distribution of the moment equation. Additional comments on Theorem 3 are postponed to Section 4.2.

Considerable difficulties arise when the projection is not known. In this case, we need to find a suitable estimator for the projection and construct a test statistic using the moment conditions, whose number does not need to be bounded. Next we show that it is possible to do so as if we knew the true projection operator.

3.3.3 The Test Statistic

For the moment, to avoid distracting technicalities, suppose that the projection and the covariance are known. Then, Theorem 3 suggests the construction of the test statistic for any finite set . Let the cardinality of be , for definiteness. For the sake of clarity in what follows, fix an order on . Define the test statistic

Let be the scaled eigenvalue of the covariance matrix , i.e., , where the eigenvector satisfies if and zero otherwise.

Remark 1

Given that is finite, we can just compute the eigenvalues (in the usual sense) of the matrix with entries , .

Corollary 1

To complete this section, it remains to consider an estimator of the projection and of the covariance function . The population projection operator can be replaced by a sample version

| (15) |

which depends on . To ease notation, write for . By the Representer Theorem, is a linear combination of the finite set of functions , as discussed in Section 2.4.1.

The estimator of at is given by such that

| (16) |

It is not at all obvious that we can effectively use the estimated projection for all , in place of the population one. The following shows that this is the case.

Theorem 4

Note that the condition on can only be satisfied if in Condition 1, , as otherwise the condition on is vacuous.

Let be the distribution of given . Define the function such that . The function might be known under the null. In this case, in (15) can be replaced by , i.e., define the empirical projection as the of

| (18) |

w.r.t. . For example, for the regression problem, using the square error loss, .

Corollary 2

Corollary 2 improves on Theorem 4 as it imposes less restrictions on the exponent and the penalty . Despite the technicalities required to justify the procedure, the implementation shown in Section 2.4.1 is straightforward. In fact evaluated at is the score for the observation and it is the entry in . On the other hand the vector has entry and , for example .

4 Discussion

4.1 Remarks on Conditions

A minimal condition for the coefficients would be with as this is essentially required for for any . Mendelson (2002) derives consistency under this minimal condition in the i.i.d. case, but no convergence rates. Here, the condition is strengthened to , but it is not necessarily so restrictive. The covariance in Example 1 satisfies Condition 1 with exponentially decaying coefficients (e.g. Rasmussen and Williams, 2006, Ch. 4.3.1); the covariance in Example 5 satisfies with (see Ritter et al., 1995, Corollary 2, for this and more general results).

It is not difficult to see that many loss functions (or negative log-likelihoods) of interest satisfy Condition 2 using the fact that (square error loss, logistic, negative log-likelihood of Poisson, etc.). (Recall that was defined just before Condition 2.) Nevertheless, interesting loss functions such as absolute deviation for conditional median estimation do not satisfy Condition 2. The extension to such loss functions requires arguments that are specific to the problem together with additional restrictions to compensate for the lack of smoothness. Some partial extension to the absolute loss will be discuss in Section 6.2.

Condition 3 is standard in the literature. More details and examples can be found in Section A.2.4 in the Appendix.

In Condition 4, the third derivative of the loss function and the strengthening of the moment conditions (Point 1) are used to control the error in the expansion of the moment equation. The moment conditions are slightly stronger than needed. The proofs show that we use the following in various places , , and these can be weakened somehow, but at the cost of introducing dependence on the exponent ( as in Condition 1). The condition is satisfied by various loss functions. For example, the following loss functions have bounded second and third derivative w.r.t. : (regression), (classification), (counting).

Time uncorrelated moment equations in Condition 4 are needed to keep the computations feasible. This condition does not imply that the data are independent. The condition is satisfied in a variety of situations. In the Poisson example given in the introduction this is the case as long as (which implicitly requires being measurable at time ). In general, we still allow for misspecification as long as the conditional expectation is not misspecified.

If the scores at the true parameter are correlated, the estimator of needs to be modified to include additional covariance terms (e.g., Newey-West estimator). Also the projection operator has to be modified such that

This can make the procedure rather involved and it is not discussed further.

It is simple to show that Point 4 in Condition 4 means that for all pairs such that , and for all such that , then (i.e. no perfect correlation when the functions are standardized).

4.2 Remarks on Theorem 2

The asymptotic distribution of the estimator is immediately derived if is finite dimensional.

Example 8

In the infinite dimensional case, Hable (2012) has shown that converges to a Gaussian process whose covariance function would require the solution of some Fredholm equation of the second type. Recall that is as in (13), while we use to denote its population version. The penalty needs to satisfy for some fixed constant . When , we have . Hence, there is no such that . The two estimators are both of interest with different properties. When the penalty does not go to zero the approximation error is non-negligible, e.g. for the square loss the estimator is biased.

Theorem 2 requires . In the finite dimensional case, the distribution of the estimator when lies on the boundary of is not standard (e.g., Geyer, 1994). In consequence the p-values are not easy to find.

4.3 Alternative Constraints

As an alternative to the norm , define the norm . Estimation in is also of interest for variable screening. The following provides some details on the two different constraints.

Lemma 1

Suppose an additive kernel

as in Section 2.2. The

following hold.

1. and

are norms on .

2. We have the inclusion

3. For any , and

are convex sets.

4. Let . If ,

then,

for any , while .

By the inclusion in Lemma 1, all the results derived for also apply to . In this case, we still need to suppose that . Both norms are of interest. When interest lies in variable screening and consistency only, estimation in inherits the properties of the norm (as for LASSO). The estimation algorithms discussed in Section 5 cover estimation in both subsets of .

5 Computational Algorithm

By duality, when and the constraint is the estimator is the usual one obtained from the Representer Theorem (e.g., Steinwart and Christmann, 2008). Estimation in an RKHS poses computational difficulties when the sample size is large. Simplifications are possible when the covariance admits a series expansion as in (7) (e.g., Lázaro-Gredilla et al., 2010).

Estimation for functions in rather than in is even more challenging. Essentially, in the case of the square error loss, estimation in resembles LASSO, while estimation in resembles ridge regression.

A greedy algorithm can be used to solve both problems. In virtue of Lemma 1 and the fact that estimation in has been considered extensively, only estimation in will be address in details. The minor changes required for estimation in will be discussed in Section 5.2.

5.1 Estimation in

Estimation of in is carried out according the following Frank-Wolfe algorithm. Let be the solution to

| (19) |

where , , and , where is the solution to the line search

| (20) |

writing instead of for typographical reasons. Details on how to solve (19) will be given in Section 5.1.1; the line search in (19) is elementary. The algorithm produces functions and coefficients . Note that identifies which of the additive functions will be updated at the iteration.

To map the results of the algorithm into functions with representation in , one uses trivial algebraic manipulations. A simpler variant of the algorithm sets . In this case, the solution at the iteration, takes the particularly simple form (e.g., Sancetta, 2016) and the additive function can be written as .

To avoid cumbersome notation, the dependence on the sample size has been suppressed in the quantities defined in the algorithm. The algorithm can find a solution with arbitrary precision as the number of iterations increases.

Theorem 5

For derived from the above algorithm,

where,

For the sake of clarity, recall that .

5.1.1 Solving for the Additive Functions

The solution to (19) is found by minimizing the Lagrangian

| (21) |

Let be the canonical feature map (Lemma 4.19 in Steinwart and Christmann, 2008); has image in and the superscript is only used to stress that it corresponds to the additive component. The first derivative w.r.t. is , using the fact that , by the reproducing kernel property. Then, the solution is

where is such that . If , set . Explicitly, using the properties of RKHS (see (9))

which is trivially solved for . With this choice of , the constraint is satisfied for all integers , and the algorithm, simply selects such that is minimized. Additional practical computational aspects are discussed in Section A.2.3 in the Appendix (supplementary material).

The above calculations together with Theorem 5 imply the following, which for simplicity, it is stated using the update instead of the line search.

5.2 The Algorithm for Estimation in

When estimation is constrained in , the algorithm has to be modified. Let be the canonical feature map of (do not confuse with in the previous section). Then, (19) is replaced by

and we denote by the solution at the iteration. This solution can be found replacing the minimization of (21) with minimization of . The solution is then where is chosen to satisfy the constraint . No other change in the algorithm is necessary and the details are left to the reader.

Empirical illustration.

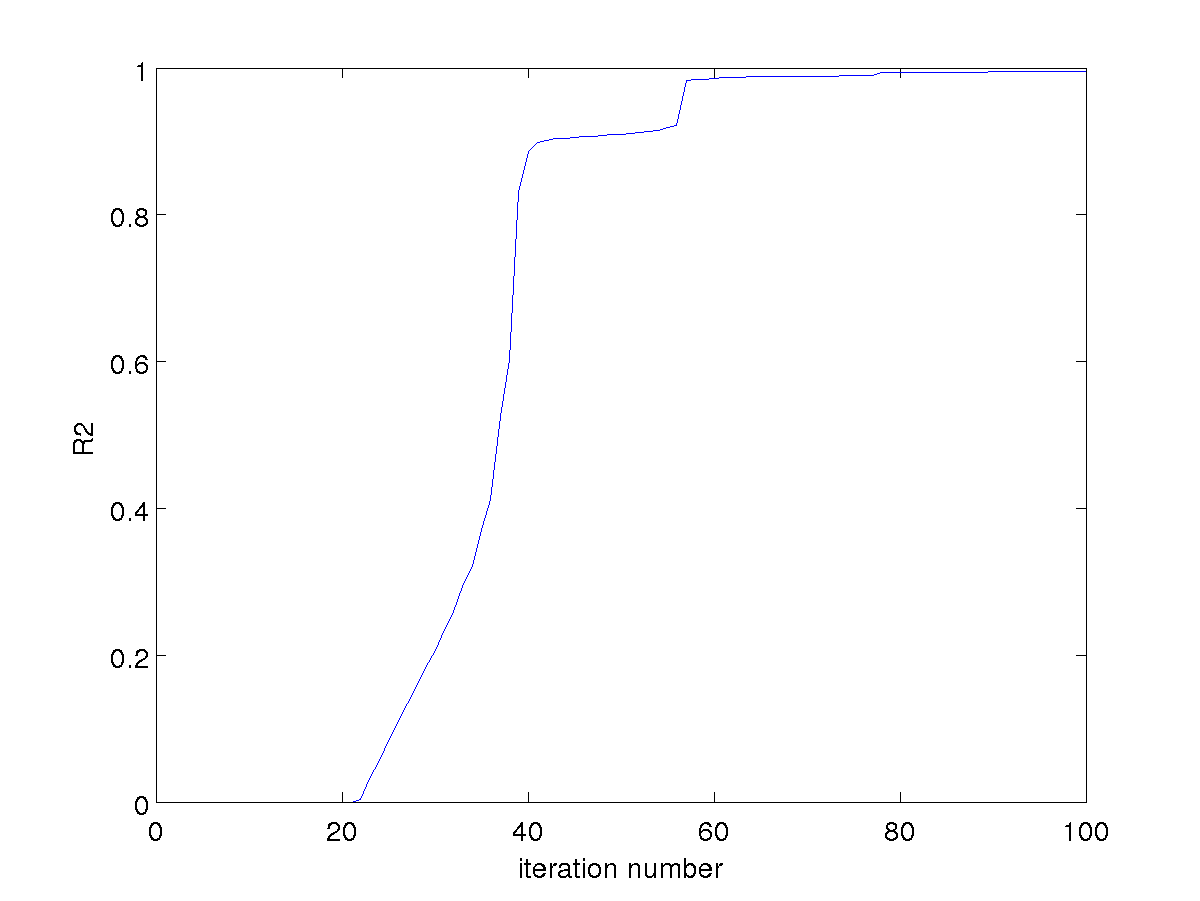

To gauge the rate at which the algorithm converges to a solution, we consider the SARCOS data set (http://www.gaussianprocess.org/gpml/data/), which comprises a test sample of 44484 observations with input variables and a continuous response variable. We standardize the variables by their Euclidean norm, use the square error loss and the Gaussian covariance kernel of Example 1 with and . Hence for this example, the kernel is not additive. Given that the kernel is universal, we shall be able to interpolate the data if is chosen large enough: we choose . The aim is not to find a good statistical estimator, but to evaluate the computational algorithm. Figure 1, plots the as a function of the number of iterations . After approximately iterations, the algorithm starts to fit the data better than a constant, and after about 80-90 iterations the is very close to one. The number of operations per iteration is .

6 Further Remarks

In this last section additional remarks of various nature are included. A simulation example is used to shed further light on the importance of the projection procedure. The paper will conclude with an example on how Condition 2 can be weakened in order to accommodate other loss functions, such as the absolute loss.

6.1 Some Finite Sample Evidence via Simulation Examples

6.1.1 High Dimensional Model

Simulation Design: True Models.

Consider the regression problem where , the number of covariates is , and the sample size is . The covariates are i.i.d. standard Gaussian random variables that are then truncated to the interval . Before truncation, the cross-sectional correlation between and is with , . The error terms are i.i.d. mean zero, Gaussian with variance such that the signal to noise ratio is equal to and . This is equivalent to an of and , i.e. a moderate and low . The following specifications for are used: with (Lin3:); with (LinAll); where the ’s are uniformly distributed in (NonLinear). In NonLinear the first variable enters the model linearly, the forth variable enters it in a nonlinear fashion, while the remaining variables do not enter the model. The choice of random coefficient for NonLinear is along the lines of Friedman (2001) to mitigate the dependence on a specific nonlinear functional form. The number of simulations is 1000.

Estimation Details.

We let be generated by the polynomial additive kernel , where . For such kernel, the true models in the simulation design all lie in a strict subset of . Estimation is carried out in using the algorithm in Section 5 with number of iterations equal to . This should also allow us to assess whether there is a distortion in the test results when the estimator minimizes the objective function on only approximately. The parameter is chosen equal to where is the sample standard deviation of , which is a crude approach to keep simulations manageable. The eigenvalues from the sample covariance were used to simulate the limiting process (see Lemma 17), from which the p-values were derived using simulations.

Hypotheses.

Hypotheses are tested within the framework of Section 3.3. We estimate Lin1, Lin2, Lin3 and LinAll, using the restricted kernel with , i.e., a linear model with 1,2,3 and 10 variables respectively. We also estimate LinPoly using the restricted kernel with as defined in the previous paragraph, i.e., the first variable enters the model linearly, all other functions are unrestricted. In all cases we test against the full unrestricted model with kernel .

Test functions.

We exploit the structure of the covariance kernels. Let the function be such that , . For the Lin1, Lin2, Lin3, LinAll models, we set the test functions as elements in with for model Lin1, and so on. We project on the span of . For LinPoly, we set the test functions as elements in , and project on the span of .

Results.

Table 2 reports the frequency of rejections for a given nominal size of the test. Here, results are for , a signal to noise level , and under the three different true designs: Lin3, LinAll, and NonLin. The column heading “No ” means that no correction was used in estimating the test statistic (i.e. test statistic ignoring the presence of nuisance parameters). The results for the other configurations of sample size, signal to noise ratio and correlation in the variables were similar. The LinPoly model is only estimated when the true model is NonLin. Here, we only report a subset of the tested hypotheses (Lin3 and LinAll, only). The complete set of results is in Section A.3 in the Appendix (supplementary material). Without using the projection adjustment, the size of the test can be highly distorted, as expected. The results reported in Table 2 show that the test (properly constructed using the projection adjustment) has coverage probability relatively close to the nominal one when the null holds, and that the test has a good level of power.

| Size | Lin3 | LinAll | LinPoly | ||||

|---|---|---|---|---|---|---|---|

| No | No | No | |||||

| True model: Lin3 | |||||||

| 0.10 | 0.09 | 0.11 | 0.07 | 0.10 | - | - | |

| 0.05 | 0.05 | 0.05 | 0.04 | 0.06 | - | - | |

| True model: LinAll | |||||||

| 0.10 | 1.00 | 1.00 | 0.49 | 0.08 | - | - | |

| 0.05 | 1.00 | 1.00 | 0.23 | 0.05 | - | - | |

| True model: NonLin | |||||||

| 0.10 | 1.00 | 1.00 | 0.92 | 0.91 | 0.03 | 0.1 | |

| 0.05 | 1.00 | 1.00 | 0.9 | 0.88 | 0.02 | 0.05 | |

6.1.2 Infinite Dimensional Estimation

Simulation Design: True Model.

Consider a bivariate regression model with independent standard normal errors. The regression function is

where the scalar coefficient is chosen so that the signal to noise ratio is and and where . The covariates and the errors together with the other details are as in Section 6.1.1.

Estimation Details and Hypotheses.

We consider two hypotheses. For hypothesis one, (Lin1NonLin) and . This means that we postulate a linear model for the first covariate and a nonlinear for the second. The true model is in , hence this hypothesis allows us to verify the size of a Type I error. For hypothesis two, (LinAll) and . In this case, the true model is not in and this hypothesis allows us to verify the power of the test. All the other details are as in Section 6.1.1.

Test functions.

Let the function be such that , . For Lin1NonLin, and LinAll, the test functions are in . We project on the functions .

Results.

Table 3 reports the frequency of rejections for , a signal to noise level , and . The detailed and complete set of results is in Section A.3 in the Appendix (supplementary material). The results still show a considerable improvement relative to the naive test.

| Lin1NonLin | LinAll | ||||

|---|---|---|---|---|---|

| Size | No | No | |||

| 0.10 | 0.00 | 0.09 | 0.99 | 1.00 | |

| 0.05 | 0.00 | 0.04 | 0.83 | 1.00 | |

| 0.10 | 0.00 | 0.09 | 0.00 | 1.00 | |

| 0.05 | 0.00 | 0.04 | 0.00 | 1.00 | |

| 0.10 | 0.00 | 0.09 | 1.00 | 1.00 | |

| 0.05 | 0.00 | 0.03 | 1.00 | 1.00 | |

| 0.10 | 0.00 | 0.09 | 0.13 | 1.00 | |

| 0.05 | 0.00 | 0.03 | 0.01 | 1.00 | |

6.2 Weakening Condition 2: Partial Extension to the Absolute Loss

Some loss functions are continuous and convex, but they are not differentiable everywhere. An important case is the absolute loss and its variations used for quantile estimation. The following considers an alternative to Condition 2 that can be used in this case. Condition 3 can be weakened, but Condition 1 has to be slightly tightened. The details are stated next, but for simplicity for the absolute loss only. More general losses such as the one used for quantile estimation can be studied in a similar way.

Condition 5

Suppose that , , and that where (the conditional distribution of given ) has a bounded density w.r.t. the Lebesgue measure on , and is the distribution of . Moreover, has derivative w.r.t. which is uniformly bounded for any , and ( as in Section 3.1). The sequence is stationary with summable beta mixing coefficients. Finally, Condition 1 holds with .

The result depends on knowledge of the probability density function of conditioning on . Hence, inference in the presence of nuisance parameters is less feasible within the proposed methodology.

References

- [1] Andrews, D.W.K. (1994) Asymptotics for Semiparametric Econometric Models Via Stochastic Equicontinuity. Econometrica 62, 43-72.

- [2] Banerjee, A., D. Dunson and S. Todkar (2008) Efficient Gaussian Process Regression for Large Data Sets. Biometrika 94, 1-16.

- [3] Belloni, A., V. Chernozhukov, I. Hansen (2017) Program Evaluation and Causal Inference With High-Dimensional Data. Econometrica 85, 233-298.

- [4] Buja, A., T. Hastie and R. Tibshirani (1989) Linear Smoothers and Additive Models (with discussion). Annals of Statistics 17, 453-555.

- [5] Chen, X. and Z. Liao (2014) Sieve M Inference on Irregular Parameters. Journal of Econometrics 182, 70-86.

- [6] Christmann, A. and I. Steinwart (2007) Consistency and Robustness of Kernel-Based Regression in Convex Risk Minimization. Bernoulli 13, 799-719.

- [7] Christmann, A. and R. Hable (2012) Consistency of Support Vector Machines Using Additive Kernels for Additive Models. Computational Statistics and Data Analysis 56, 854-873.

- [8] Connor, G., M. Hagmann and O. Linton (2012) Efficient Semiparametric Estimation of the Fama-French Model and Extensions. Econometrica 80, 713-754.

- [9] Fan, J., C.M. Zhang, and J. Zhang (2001) Generalized Likelihood Ratio Statistics and Wilks Phenomenon. The Annals of Statistics 29, 153-193.

- [10] Fan, J. and J. Jiang (2005) Nonparametric Inferences for Additive Models. Journal of the American Statistical Association 100, 890-907.

- [11] Friedman, J. (2001) Greedy Function Approximation: A Gradient Boosting Machine. Annals of Statistics 29, 1189-1232.

- [12] Geyer, C.J. (1994) On the Asymptotics of Constrained -Estimation. Annals of Statistics 22, 1993-2010.

- [13] Hable, R. (2012) Asymptotic Normality of Support Vector Machine Variants and Other Regularized Kernel Methods. Journal of Multivariate Analysis 106, 92-117.

- [14] Härdle, W. and E. Mammen (1993) Comparing Nonparametric Versus Parametric Regression Fits. Annals of Statistics 21, 1926-1947.

- [15] Hartigan, J.A. (2014) Bounding the Maximum of Dependent Random Variables. Electronic Journal of Statistics 8, 3126-3140.

- [16] Lázaro-Gredilla, M., J. Quiñonero-Candela, C.E. Rasmussen and A.R. Figueiras-Vidal (2010) Sparse Spectrum Gaussian Process Regression. Journal of Machine Learning Research 11, 1865-1881.

- [17] Linton, O.B. and J.P. Nielsen (1995) A Kernel Method of Estimating Structured Nonparametric Regression Based on Marginal Integration.

- [18] Lyons, R.K. (1997) A Simultaneous Trade Model of the Foreign Exchange Hot Potato. Journal of International Economics 42 275-298.

- [19] Mammen, E., O.B. Linton, and J.P. Nielsen (1999) The Existence and Asymptotic Properties of a Backfitting Projection Algorithm under Weak Conditions. Annals of Statistics 27, 1443-1490.

- [20] Meier, L., P. Bühlmann and S. van de Geer (2009). High-Dimensional Additive Modeling. Annals of Statistics 37, 3779-3821.

- [21] Mendelson, S. (2002) Geometric Parameters of Kernel Machines. In: Kivinen J., Sloan R.H. (eds) Computational Learning Theory (COLT). Lecture Notes in Computer Science 2375. Berlin: Springer.

- [22] Rasmussen, C. and C.K.I. Williams (2006) Gaussian Processes of Machine Learning. Cambridge, MA: MIT Press.

- [23] Ritter, K., G.W. Wasilkowski and H. Wozniakowski (1995) Multivariate Integration and Approximation for Random Fields Satisfying Sacks-Ylvisaker Conditions. Annals of Applied Probability 5, 518-540.

- [24] Sancetta A. (2016) Greedy Algorithms for Prediction. Bernoulli 22, 1227-1277.

- [25] Schölkopf, B., R. Herbrich, and A.J. Smola (2001) A Generalized Representer Theorem. In D. Helmbold and B. Williamson (eds.) Neural Networks and Computational Learning Theory 81, 416-426. Berlin: Springer.

- [26] Shen, X. and J. Shi (2005) Sieve Likelihood Ratio Inference on General Parameter Space. Science in China Series A: Mathematics 48, 67-78.

- [27] van der Vaart, A. (1998) Asymptotic Statistics. Cambridge: Cambridge University Press.

- [28] van der Vaart, A. and J.A. Wellner (2000) Weak Convergence and Empirical Processes. New York: Springer.

- [29] Wahba, G. (1990) Spline Models for Observational Data. Philadelphia: SIAM.

Supplementary Material

A.1 Appendix 1: Proofs

Recall that and , . Condition 2 implies Fréchet differentiability of and (w.r.t. ) at in the direction of . It can be shown that these two derivatives are and , respectively. For this purpose, we view as a map from the space of uniformly bounded functions on () to . The details can be derived following the steps in the proof of Lemma 2.21 in Steinwart and Christmann (2008) or the proof of Lemma A.4 in Hable (2012). The application of those proofs to the current scenario, essentially requires that the loss function is differentiable w.r.t. real , and that is uniformly bounded, together with integrability of the quantities , and , as implied by Condition 2. It will also be necessary to take the Fréchet derivative of and conditioning on the sample data. By Condition 2 this will also hold because , and are finite. This will also allow us to apply Taylor’s Theorem in Banach spaces. Following the aforementioned remarks, when the loss function is three times differentiable, we also have that for any , the Fréchet derivative of in the direction of is . These facts will be used throughout the proofs with no further mention. Moreover, throughout, for notational simplicity, we tacitly suppose that so that implies that for any .

A.1.1 Complexity and Gaussian Approximation

The reader can skip this section and refer to it when needed. Recall that the -covering number of a set under the norm (denoted by ) is the minimum number of balls of radius needed to cover . The entropy is the logarithm of the covering number. The -bracketing number of the set under the norm is the minimum number of -brackets under the norm needed to cover . Given two functions such that , an -bracket is the set of all functions such that . Denote the -bracketing number of by . Under the uniform norm, .

In this section, let be a centered Gaussian process on with covariance as in (7). For any , let

The space is generated by the measure of the Gaussian process with covariance function . In particular, , where the is a sequence of i.i.d.standard normal random variables, and the equality holds in distribution. For any positive integer , the -approximation number w.r.t. (e.g., Li and Linde, 1999, see also Li and Shao, 2001) is bounded above by . Under Condition 1, deduce that

| (A.1) |

There is a link between the approximating number of the centered Gaussian process with covariance and the -entropy number of the class of functions , which is denoted by . These quantities are also related to the small ball probability of under the sup norm (results hold for other norms, but will not be used here). We have the following bound on the -entropy number of .

Lemma 2

Under Condition 1, .

Proof. As previously remarked, the space is generated by the law of the Gaussian process with covariance function . For any integer , the -approximation number of , is bounded as in (A.1). In consequence, , by Proposition 4.1 in Li and Linde (1999). Then, Theorem 1.2 in Li and Linde (1999) implies that .

Lemma 3

Under Condition 1,

Proof. Functions in can be written as where . Hence, the covering number of is bounded by the product of the covering number of the sets and . The -covering number of is bounded by a constant multiple of under the supremum norm. The -covering number of is given by Lemma 2, i.e. . The lemma follows by taking logs of these quantities.

Next, link the entropy of to the entropy with bracketing of .

Lemma 4

Suppose Condition 1 holds. For the set , for any satisfying Condition 2, the -entropy with bracketing is

The same exact result holds for under Condition 2.

Proof. In the interest of conciseness, we only prove the result for

To this end, note that by Condition 2 and the triangle inequality,

By Condition 2, , and , and . By Lemma 1, . By these remarks, the previous display is bounded by

Theorem 2.7.11 in van der Vaart and Wellner (2000) says that the -bracketing number of class of functions satisfying the above Lipschitz kind of condition is bounded by the -covering number of with . Using Lemma 3, the statement of the lemma is deduced because the product of the covering numbers is the sum of the entropy numbers.

We shall also need the following.

Lemma 5

Suppose Condition 1 holds. For the set , and any satisfying Condition 2 with the addition that , the -entropy with bracketing is

If also , has -entropy with bracketing as in the above display.

Proof. The proof is the same as the one of Lemma 4. By Condition 2 and the triangle inequality, for

By Condition 2, , , and . By Lemma 1, . By these remarks, the previous display is bounded by

Theorem 2.7.11 in van der Vaart and Wellner (2000) says that the -bracketing number of class of functions satisfying the above Lipschitz kind of condition is bounded by the -covering number of with .

The last statement in the lemma is proved following step by step the proof of Lemma 4 with replaced by and by .

Lemma 6

Proof. The proof shall use the main result in Doukhan et al. (1995). Let . The elements in have finite norm because by Condition 2, and by Lemma 1. To avoid extra notation, it is worth noting that the entropy integrability condition in Doukhan et al. (1995, Theorem 1, eq. 2.10) is implied by

| (A.2) |

and with and . Then, Theorem 1 in Doukhan et al. (1995) shows that the empirical process indexed in converges weakly to the Gaussian one given in the statement of the present lemma. By Condition 3, it is sufficient to show (A.2). By Lemma 4, the integral is finite because by Condition 1.

A.1.2 Proof of Theorem 1

The proof is split into the part concerned with the constrained estimator and the one that studies the penalized estimator.

A.1.2.1 Consistency of the Constrained Estimator

At first we show Point 1 verifying the conditions of Theorem 3.2.5 van der Vaart and Wellner (2000) which we will refer to as VWTh herein. To this end, by Taylor’s Theorem in Banach spaces,

for with some and arbitrary . The variational inequality holds by definition of and the fact that . Therefore, the previous display implies that because by Condition 2. The right hand most inequality holds with equality if and only if in . This verifies the first condition in VWTh. Given that the loss function is convex and coercive and that is a closed convex set, this also shows that the population minimizer exists and is unique up to an equivalence class, as stated in the theorem. Moreover, given that , then both and are uniformly bounded by a constant multiple , hence for simplicity suppose they are bounded by . This implies the following relation

for any . Hence, for any finite real ,

To verify the second condition in VWTh, we need to find a function that grows slower than such that the r.h.s. of the above display is bounded above by . To this end, note that we are interested in the following class of functions with . This class of functions satisfies using the differentiability and the bounds implied by Condition 2. Theorem 3 in Doukhan et al. (1995) says that that for large enough , eventually (see their page 410),

Note that we have balls of size rather than and for this reason we have modified the limit in the integral. Moreover, as remarked in the proof of Lemma 6, the entropy integral in Doukhan et al. (1995) uses the bracketing number based on another norm. However, their norm is bounded by the norm used here under the restrictions we impose on the mixing coefficients via Condition 3. To compute the integral we use Lemma 4, so that the l.h.s. of the display is a constant multiple of with . The third condition in VWTh requires to find a sequence such that . Given that with , deduce that we can set . Then VWTh states that . Of course, if is finite dimensional, it is not difficult to show that . The space is finite dimensional if (7) has a finite number of terms.

We also show that a.s. which shall imply a.s. (Corollary 3.2.3 in van der Vaart and Wellner, 2000, replacing the in probability result with a.s.). This only requires the loss function to be integrable (if the loss is positive), but does not allow us to derive convergence rates. For any fixed , a.s., by the ergodic theorem, because by Condition 2. Hence, it is just sufficient to show that has finite -bracketing number under the norm (e.g., see the proof of Theorem 2.4.1 in van der Vaart and Wellner, 2000). This is the case by Lemma 4, because by Condition 1, . Hence, a.s..

To turn the convergence into uniform, note that is compact under the uniform norm and functions in are defined on a compact domain . Hence, is a subset of the space of continuous bounded function equipped with the uniform norm. In consequence, any convergent sequence in converges uniformly.

We now turn to the relation between the constrained and penalized estimator, which will also conclude the proof of Theorem 1.

A.1.2.2 The Constraint and the Lagrange Multiplier

The following lemma puts together crucial results for estimation in RKHS (Steinwart and Christmann, 2008, Theorems 5.9 and 5.17 for a proof). The cited results make use of the definition of integrable Nemitski loss of finite order (Steinwart and Christmann, 2008, Def. 2.16). However, under Condition 2, the proofs of those results still hold.

Lemma 7

Under Condition 2,

| (A.3) |

where is the canonical feature map. Moreover, if is bounded for any , then .

Lemma 8

Proof. Given that is finite and the kernel is additive, there is no loss in restricting attention to in order to reduce the notational burden. We shall need a bound for the r.h.s. of (A.3). By (7), the canonical feature map can be written as . This implies that,

By Lemma 7, (9), and the above,

In consequence of the above display, by the triangle inequality,

Given that , there is a finite such that (this proves Point 1 in the lemma). By this remark, it follows that, uniformly in , there is an such that . Hence, the maximal inequality of Theorem 3 in Doukhan et al. (1995) implies that

| (A.4) |

for some finite constant , for any , because the entropy integral (A.2) is finite in virtue of Lemma 4. Define

Given that the coefficients are summable by Condition 1, deduce from (A.4) that is a tight random sequence. Using the above display, we have shown that (A.3) is bounded by . This proves Point 2 in the lemma. For any fixed , we can choose so that in probability. By the triangle inequality and the above calculations, deduce that, in probability,

for . By tightness of , deduce that . Also, the first order condition for the sample estimator reads

| (A.5) |

for any . In consequence, . These calculations prove Point 3 in the lemma when .

The penalized objective function is increasing with . In the Lagrangian formulation of the constrained minimization, interest lies in finding the smallest value of such that the constraint is still satisfied. When equals such smallest value , we have . From Lemma 8 deduce that . Also, if is infinite dimensional, the constraint needs to be binding so that . Hence, if there is an such that . Then, we must have

But . Hence, the above display is greater or equal than

This means that cannot converge under the norm .

The statement concerning approximate minimizers will be proved in Section A.1.4.

A.1.3 Proof of Theorem 2

It is convenient to introduce additional notation and concepts that will be used in the remaining of the paper. By construction the minimizer of the population objective function is . Let be the space of uniformly bounded functions on . Let be the operator in such that , . If the objective function is Fréchet differentiable, the minimizer of the objective function in satisfies the variational inequality: for any in the tangent cone of at . This tangent cone is defined as . If is in the interior of , this tangent cone is the whole of . Hence by linearity of the operator , attention can be restricted to . When , it also holds that , for any . Then, in the following calculations, can be restricted to be in . The empirical counterpart of is the operator such that . Finally, write for the Fréchet derivative of at tangentially to , where . Then, is an operator from to . As for , the operator can be restricted to be in . These facts will be used without further notice in what follows. Most of these concepts are reviewed in van der Vaart and Wellner (2000, ch.3.3) where this same notation is used.

Deduce that is Fréchet differentiable and its derivative is the map . By the conditions of Theorem 2, , hence by the first order conditions, for any . By this remark, and basic algebra,

| (A.6) | |||||

To bound the last two terms, verify that

This follows if (i) , , , converges weakly to a Gaussian process with continuous sample paths, (ii) is compact under the uniform norm, and (iii) is consistent for in . Point (i) is satisfied by Lemma 6, which also controls the first term on the r.h.s. of (A.6). Point (ii) is satisfied by Lemma 3. Point (iii) is satisfied by Theorem 1. Hence, by continuity of the sample paths of the Gaussian process, as in probability (using Point iii), the above display holds true

To control the second term on the r.h.s. of (A.6), note that the Fréchet derivative of at is the linear operator such that , which can be shown to exist based on the remarks at the beginning of Section A.1. For any ,

| (A.7) |

using differentiability of the loss function and Taylor’s theorem in Banach spaces. By Condition 4, and the fact that is uniformly bounded, the r.h.s. is a constant multiple of . By Theorem 1 this quantity is . Given that , these calculations show that

In consequence, from (A.6) deduce that

| (A.8) | |||||

By Lemma 6, . For the moment, suppose that is the exact solution to the minimization problem, i.e. as in (10). Hence, by Lemma 8, , implying that . Finally, if , (A.8) together with the previous displays imply that in probability, where the l.h.s. has same distribution as the Gaussian process given in the statement of the theorem. It remains to show that if we use an approximate minimizer say to distinguish it here from in (10), the result still holds. The lemma in the next section shows that this is true, hence completing the proof of Theorem 2.

A.1.4 Asymptotic Minimizers

The following collects results on asymptotic minimizers. It proves the last statement in Theorem 1 and also allows us to use such minimisers in the test.

Lemma 9

Proof. At first consider the penalized estimator. To this end, follow the same steps in the proof of 5.14 in Theorem 5.9 of Steinwart and Christmann (2008). Mutatis mutandis, the argument in their second paragraph on page 174 gives

Derivation of this display requires convexity of w.r.t. , which is the case by Condition 2. By assumption, the r.h.s. is . Note that is the exact minimizer of the penalized empirical risk. Hence, eq. (5.12) in Theorem 5.9 of Steinwart and Christmann (2008) says that for any , implying that the inner product in the display is zero. By these remarks, deduce that the above display simplifies to . Deduce that so that by the triangle inequality, and Lemma 8, eventually, in probability for some .

Now, consider the constrained estimator. Conditioning on the data, by definition of , the variational inequality holds because is an element of the tangent cone of at . Conditioning on the data, by Taylor’s theorem in Banach spaces, and the fact that by Condition 2, deduce that. By the conditions of the lemma, and the previous inequality deduce that . The convergence is then turned into uniform using the same argument used in the proof of Theorem 1. Now, conditioning on the data, by Fréchet differentiability,

By Holder’s inequality, and the fact that is bounded, the r.h.s. is bounded by a constant multiple of

By Condition 2, deduce that so that, by the previous calculations, the result follows.

A.1.5 Proof of Results in Section 3.3

We use the operators , , such that for any :

| (A.9) |

To ease notation, we may write when .

The proof uses some preliminary results. In what follows, we shall assume that . This is to avoid notational complexities that could obscure the main steps in the derivations. Because of additivity, this is not restrictive as long as is bounded.

Lemma 10

Suppose that . Then, .

Proof. By construction, the linear projection satisfies and . Hence, the space is the direct sum of the set and its complement in , say . These sets are orthogonal. Note that we do not necessarily have unless the basis that spans is already linearly independent of . By Lemma 9.1 in van der Vaart and van Zanten (2008) . The norms are the ones induced by the inner products in the respective spaces. But, . Hence, we have that .

Lemma 11

Under Condition 4, if , then, in probability.

Proof. Let and be finite positive measures such that and . By Lemma 7, using the same arguments as in the proof of Lemma 8,

| (A.10) |

Taking derivatives, we bound each term in the absolute value by

By Lemma 10 and the definition of penalized estimation, independently of . Hence, . Moreover, the ’s are uniformly bounded. Therefore, the r.h.s. of the above display is bounded by a constant multiple of

The term is finite by Condition 2. By Theorem 1, we have that . Using the above display to bound (A.10), deduce that the lemma holds true if as stated in the lemma. Taking supremum w.r.t. in the above steps, deduce that the result holds uniformly in .

Lemma 12

Under Condition 4, we have that in probability for any such that in probability.

Proof. Following the same steps as in the proof of Lemma 11, deduce that

Each absolute value term on the r.h.s. is bounded in by

Define the class of functions . Given that is uniformly bounded, it can be deduced from Lemma 5 that . Hence, to complete the proof of the lemma, we can follow the same exact steps as in the proof of Lemma 8.

Lemma 13

| (A.11) |

Finally, if is a known function, the above displays hold for such that in probability.

Proof. By the triangle inequality

| (A.12) |

The first statement in the lemma follows by showing that the r.h.s. of the above is . This is the case by application of Lemmas 11 and 12.

By the established convergence in , for any , with probability going to one for any . Therefore, to prove (A.11), we can restrict attention to a bound for

From Lemma 8 and (A.5) in its proof, deduce that the above is bounded by

The first term in the product is zero so that (A.11) holds.

Finally, to show the last statement in the lemma, note that it is Lemma 11 that puts an additional constraint on . However, saying that the function is known, effectively amounts to saying that we can replace with in the definition of in (A.9). This means that so that the second term in (A.12) is exactly zero and we do not need to use Lemma 11. Therefore, is only constrained for the application of Lemma 12.

We also need to bound the distance between and , but this cannot be achieved in probability under the operator norm.

Lemma 14

Under Condition 4, we have that .

Proof. At first show that

| (A.13) |

To see this, expand the r.h.s. of (A.13), add and subtract , and verify that the r.h.s. of (A.13) is equal to

However, is the projection of onto the subspace . Hence, the middle term in the above display is zero. Then, add and subtract and rearrange to deduce that the above display is equal to

Given that and is orthogonal to elements in by definition of the projection , we have shown that (A.13) holds true. Following the proof of Corollary 5.18 in Steinwart and Christmann (2008),

because is positive and is the minimizer of the penalized population loss function (see (A.9)). Now note that the r.h.s. of the above display is bounded by using Lemma 10 and (A.9). Hence the r.h.s. of (A.13) is bounded by uniformly in , and the lemma is proved.

Lemma 15

Under Condition 4, we have that for any such that in probability.

Proof. By definition,

By Holder inequality, the absolute value of the display is bounded by

| (A.14) |

By Condition 4, , so that

using Point 2 in Theorem 1. Hence, by Lemma 14, deduce that (A.14) is bounded above by for the given choice of .

Lemma 16

Suppose that . Under Condition 4, if ,

weakly, where the r.h.s. is a mean zero Gaussian process with covariance function

for any .

Proof. Any Gaussian process - not necessarily the one in the lemma - is continuous w.r.t. the pseudo norm (Lemma 1.3.1 in Adler and Taylor, 2007). Hence, implies that in probability. By Lemma 10, deduce that . Hence, consider the Gaussian process in the lemma with . By direct calculation,

| (A.15) |

Recall the notation . Multiply and divide the r.h.s. of the display by and use Holder inequality, to deduce that (A.15) is bounded above by

using the fact that is bounded away from zero and is integrable. Hence, to check continuity of the Gaussian process at arbitrary , we only need to consider . By Theorem 2 which also holds for any , converges weakly to a Gaussian process , . Hence, converges weakly to if for any

in probability. The above display holds true if in probability as . This is the case by Lemma 14.

Furthermore we need to estimate the eigenvalues in order to compute critical values.

Lemma 17

Proof. To show Point 1, use the triangle inequality to deduce that

| (A.16) | |||||

It is sufficient to bound each term individually uniformly in .