Oracle-Efficient Online Learning and Auction Design

Abstract

We consider the design of computationally efficient online learning algorithms in an adversarial setting in which the learner has access to an offline optimization oracle. We present an algorithm called Generalized Follow-the-Perturbed-Leader and provide conditions under which it is oracle-efficient while achieving vanishing regret. Our results make significant progress on an open problem raised by Hazan and Koren, 2016b , who showed that oracle-efficient algorithms do not exist in general Hazan and Koren, 2016a and asked whether one can identify properties under which oracle-efficient online learning may be possible.

Our auction-design framework considers an auctioneer learning an optimal auction for a sequence of adversarially selected valuations with the goal of achieving revenue that is almost as good as the optimal auction in hindsight, among a class of auctions. We give oracle-efficient learning results for: (1) VCG auctions with bidder-specific reserves in single-parameter settings, (2) envy-free item pricing in multi-item auctions, and (3) s-level auctions of Morgenstern and Roughgarden, (2015) for single-item settings. The last result leads to an approximation of the overall optimal Myerson auction when bidders’ valuations are drawn according to a fast-mixing Markov process, extending prior work that only gave such guarantees for the i.i.d. setting.

Finally, we derive various extensions, including: (1) oracle-efficient algorithms for the contextual learning setting in which the learner has access to side information (such as bidder demographics), (2) learning with approximate oracles such as those based on Maximal-in-Range algorithms, and (3) no-regret bidding in simultaneous auctions, resolving an open problem of Daskalakis and Syrgkanis, (2016).

1 Introduction

Online learning plays a major role in the adaptive optimization of computer systems, from the design of online marketplaces (Blum and Hartline,, 2005; Balcan and Blum,, 2006; Cesa-Bianchi et al.,, 2013; Roughgarden and Wang,, 2016) to the optimization of routing schemes in communication networks (Awerbuch and Kleinberg,, 2008). The environments in these applications are constantly evolving, requiring continued adaptation of these systems. Online learning algorithms have been designed to robustly address this challenge, with performance guarantees that hold even when the environment is adversarial. However, the information-theoretically optimal learning algorithms that work with arbitrary payoff functions are computationally inefficient when the learner’s action space is exponential in the natural problem representation Freund and Schapire, (1997). For certain action spaces and environments, efficient online learning algorithms can be designed by reducing the online learning problem to an optimization problem (Kalai and Vempala,, 2005; Kakade and Kalai,, 2005; Awerbuch and Kleinberg,, 2008; Hazan and Kale,, 2012). However, these approaches do not easily extend to the complex and highly non-linear problems faced by real learning systems, such as the learning systems used in online market design. In this paper, we address the problem of efficient online learning with an exponentially large action space under arbitrary learner objectives.

This goal is not achievable without some assumptions on the problem structure. Since an online optimization problem is at least as hard as the corresponding offline optimization problem (Cesa-Bianchi et al.,, 2004; Daskalakis and Syrgkanis,, 2016), a minimal assumption is the existence of an algorithm that returns a near-optimal solution to the offline problem. We assume that our learner has access to such an offline algorithm, which we call an offline optimization oracle. This oracle, for any (weighted) history of choices by the environment, returns an action of the learner that (approximately) maximizes the learner’s reward. We seek to design oracle-efficient learners, that is, learners that run in polynomial time, with each oracle call counting .

An oracle-efficient learning algorithm can be viewed as a reduction from the online to the offline problem, providing conditions under which the online problem is not only as hard, but also as easy as the offline problem, and thereby offering computational equivalence between online and offline optimization. Apart from theoretical significance, reductions from online to offline optimization are also practically important. For example, if one has already developed and implemented a Bayesian optimization procedure which optimizes against a static stochastic environment, then our algorithm offers a black-box transformation of that procedure into an adaptive optimization algorithm with provable learning guarantees in non-stationary, non-stochastic environments. Even if the existing optimization system does not run in worst-case polynomial time, but is rather a well-performing fast heuristic, a reduction to offline optimization is capable of leveraging any expert domain knowledge that went into designing the heuristic, as well as any further improvements of the heuristic or even discovery of polynomial-time solutions.

Recent work of Hazan and Koren, 2016a shows that oracle-efficient learning in adversarial environments is not achievable in general, while leaving open the problem of identifying the properties under which oracle-efficient online learning may be possible Hazan and Koren, 2016b . We introduce a generic algorithm called Generalized Follow-the-Perturbed-Leader (Generalized FTPL) and derive sufficient conditions under which this algorithm yields oracle-efficient online learning. Our results are enabled by providing a new way of adding regularization so as to stabilize optimization algorithms in general optimization settings. The latter could be of independent interest beyond online learning. Our approach unifies and extends previous approaches to oracle-efficient learning, including the Follow-the-Perturbed Leader (FTPL) approach introduced by Kalai and Vempala, (2005) for linear objective functions, and its generalizations to submodular objective functions Hazan and Kale, (2012), adversarial contextual learning Syrgkanis et al., 2016a , and learning in simultaneous second-price auctions Daskalakis and Syrgkanis, (2016). Furthermore, our sufficient conditions are related to the notion of a universal identification set of Goldman et al., (1993) and oracle-efficient online optimization techniques of Daskalakis and Syrgkanis, (2016).

The second main contribution of our work is to introduce a new framework for the problem of adaptive auction design for revenue maximization and to demonstrate the power of Generalized FTPL through several applications in this framework. Traditional auction theory assumes that the valuations of the bidders are drawn from a population distribution which is known, thereby leading to a Bayesian optimization problem. The knowledge of the distribution by the seller is a strong assumption. Recent work in algorithmic mechanism design Cole and Roughgarden, (2014); Morgenstern and Roughgarden, (2015); Devanur et al., (2016); Roughgarden and Schrijvers, (2016) relaxes this assumption by solely assuming access to a set of samples from the distribution. In this work, we drop any distributional assumptions and introduce the adversarial learning framework of online auction design. On each round, a learner adaptively designs an auction rule for the allocation of a set of resources to a fresh set of bidders from a population.111Equivalently, the set of bidders on each round can be the same as long as they are myopic and optimize their utility separately in each round. Using our extension to contextual learning (Section 5), this approach can also be applied when the learner’s choice of auction is allowed to depend on features of the arriving set of bidders, such as demographic information. The goal of the learner is to achieve average revenue at least as large as the revenue of the best auction from some target class. Unlike the standard approach to auction design, initiated by the seminal work of Myerson, (1981), our approach is devoid of any assumptions about a prior distribution on the valuations of the bidders for the resources at sale. Instead, similar to an agnostic approach in learning theory, we incorporate prior knowledge in the form of a target class of auction schemes that we want to compete with. This is especially appropriate when the auctioneer is restricted to using a particular design of auctions with power to make only a few design choices, such as deciding the reserve prices in a second-price auction. A special case of our framework is considered in the recent work of Roughgarden and Wang, (2016). They study online learning of the class of single-item second-price auctions with bidder-specific reserves, and give an algorithm with performance that approaches a constant factor of the optimal revenue in hindsight. We go well beyond this specific setting and show that our Generalized FTPL can be used to optimize over several standard classes of auctions including VCG auctions with bidder-specific reserves and the level auctions of Morgenstern and Roughgarden, (2015), achieving low additive regret to the best auction in the class.

In the remainder of this section, we describe our main results in more detail and then discuss several extensions and applications of these results, including (1) learning with side information (i.e., contextual learning); (2) learning with constant-factor approximate oracles (e.g., using Maximal-in-Range algorithms Nisan and Ronen, (2007)); (3) regret bounds with respect to stronger benchmarks for the case in which the environment is not completely adversarial, but follows a fast-mixing Markov process.

Our work contributes to two major research agendas: the design of efficient and oracle-efficient online learning algorithms (Agarwal et al.,, 2014; Dudik et al.,, 2011; Daskalakis and Syrgkanis,, 2016; Hazan and Kale,, 2012; Hazan and Koren, 2016a, ; Kakade and Kalai,, 2005; Kalai and Vempala,, 2005; Rakhlin and Sridharan,, 2016; Syrgkanis et al., 2016b, ), and the design of auctions using machine learning tools (Cole and Roughgarden,, 2014; Devanur et al.,, 2016; Morgenstern and Roughgarden,, 2015; Kleinberg and Leighton,, 2003; Blum and Hartline,, 2005; Cesa-Bianchi et al.,, 2013). We describe related work from both areas in more detail in Appendix A.

1.1 Oracle-Efficient Learning with Generalized FTPL

We consider the following online learning problem. On each round , a learner chooses an action from a finite set , and an adversary chooses an action from a set . The learner then observes and receives a payoff , where the function is fixed and known to the learner. The goal of the learner is to obtain low expected regret with respect to the best action in hindsight, i.e., to minimize

where the expectation is over the randomness of the learner.222To simplify exposition, we assume that the adversary is oblivious, i.e., that the sequence is chosen in advance. Our results generalize to adaptive adversaries using standard techniques (Hutter and Poland,, 2005; Daskalakis and Syrgkanis,, 2016). We desire algorithms, called no-regret algorithms, for which this regret is sublinear in the time horizon .

Our algorithm takes its name from the seminal Follow-the-Perturbed-Leader (FTPL) algorithm of Kalai and Vempala, (2005). FTPL achieves low regret, , by independently perturbing the historical payoff of each of the learner’s actions and choosing on each round the action with the highest perturbed payoff. However, this approach is inefficient when the action space is exponential in the natural representation of the learning problem, because it requires creating independent random variables.333If payoffs are linear in some low-dimensional representation of then the number of variables needed is equal to this dimension. But for non-linear payoffs, variables are required. Moreover, because of the form of the perturbation, the optimization of the perturbed payoffs cannot be performed by the offline optimization oracle for the same problem. We overcome both of these challenges by, first, generalizing FTPL to work with perturbations that can be compactly represented and are thus not necessarily independent across different actions (sharing randomness), and, second, by implementing such perturbations via synthetic histories of adversary actions and thus creating offline problems of the same form as the online problem (implementing randomness).

Sharing Randomness.

Our Generalized FTPL begins by drawing a random vector of dimension , with components drawn independently from a dispersed distribution . The payoff of each of the learner’s actions is perturbed by a linear combination of these independent variables, as prescribed by a perturbation translation matrix of size , with entries in . Let denote the row of corresponding to . On each round , the algorithm outputs an action that (approximately) maximizes the perturbed historical performance. In other words, is chosen such that for all ,

for some fixed optimization accuracy . This procedure is fully described in Algorithm 1 of Section 2.

We show that Generalized FTPL is no-regret as long as is sufficiently small and the translation matrix satisfies an admissibility condition. This condition requires the rows of to be (sufficiently) distinct so that each action’s perturbation uses a different weighted combination of the -dimensional noise. To the best of our knowledge, the approach of using an arbitrary matrix to induce shared randomness among actions of the learner is novel. The formal no-regret result is in Theorem 2.5. The informal statement is the following:

Informal Theorem 1.1.

A translation matrix is -admissible if any two rows of the matrix are distinct and the minimum non-zero difference between any two values within a column is at least . Generalized FTPL with a -admissible matrix and an appropriate distribution achieves regret .

A technical challenge here is to show that the randomness induced by on the set of actions stabilizes the algorithm, i.e., the probability that is small. We use the admissibility of to guide us through the analysis of stability. In particular, we consider how each column of partitions actions of to a few subsets (at most ) based on their corresponding entries in that column. Since the matrix rows are distinct, the algorithm is stable as a whole if, for each column, the partition to which the algorithm’s chosen action belongs to remains the same between consecutive rounds with probability close to . This allows us to decompose the stability analysis of the algorithm as a whole to the analysis of stability across partitions of each column. At the column level, stability of the partition between two rounds follows by showing that a switch between partitions happens only if the perturbation corresponding to that column falls into a small sub-interval of the support of the distribution , from which it is sampled. The latter probability is small if is sufficiently dispersed. This final argument is similar in nature to the reason why perturbations lead to stability in the original FTPL algorithm of Kalai and Vempala, (2005).

Implementing Randomness.

To ensure oracle-efficient learning, we additionally need the property that the induced action-level perturbations can be simulated by a (short) synthetic history of adversary actions. This allows us to avoid working with directly, or even explicitly writing it down. This requirement is captured by our implementability condition, which states that each column of the translation matrix corresponds to a scaled version of the expected reward of the learner on some distribution of adversary actions. The formal statement is in Theorem 2.10. The informal statement is the following:

Informal Theorem 1.2.

A translation matrix is implementable if each column corresponds to a scaled version of the expected reward of the learner against some finitely supported distribution of actions of the adversary. Generalized FTPL with an implementable translation matrix can be implemented with one oracle call per round and runs in time polynomial in , , and the size of the support of the distributions implementing the translation matrix. Oracle calls count in the running time.

The use of synthetic histories in online optimization was first explored by Daskalakis and Syrgkanis Daskalakis and Syrgkanis, (2016), who sample histories of length from a fixed distribution. Our implementability property uses matrix to obtain problem-specific distributions that stabilize online optimization with shorter histories.

For some learning problems, it is easier to first construct an implementable translation matrix and argue about its admissibility; for others, it is easier to construct an admissible matrix and argue about its implementability. We pursue both strategies in various applications, demonstrating the versatility of our conditions.

Our theorems yield the following simple sufficient condition for oracle-efficient no-regret learning (see Theorems 2.5 and 2.10 for more general statements):

If there exist adversary actions such that any two actions of the learner yield different rewards on at least one of these actions, then Generalized FTPL with an appropriate translation matrix has regret and its oracle-based runtime is where is the smallest difference between distinct rewards obtainable on any one of the adversary actions.

The aforementioned results establish a reduction from online optimization to offline optimization. Recall that in the oracle-based runtime, each oracle call counts . When the offline optimization problem can be solved in polynomial time, these results imply that the online optimization problem can also be solved in (fully) polynomial time. The formal statement is in Corollary 2.11.

1.2 Main Application: Online Auction Design

In many applications of auction theory, including electronic marketplaces, a seller repeatedly sells an item or a set of items to a population of buyers, with a few arriving for each auction. In such cases, the seller can optimize his auction design in an online manner, using historical data consisting of observed bids. We consider a setting in which the seller would like to use this historical data to select an auction from a fixed target class. For example, a seller in a sponsored-search auction might be limited by practical constraints to consider only second-price auctions with bidder-specific reserves. The seller can optimize the revenue by using the historical data for each bidder to set these reserves. Similarly, a seller on eBay may be restricted to set a single reserve price for each item. Here, the seller can optimize the revenue by using historical data from auctions for similar goods to set the reserves for new items. In both cases, the goal is to leverage the historical data to pick an auction on each round in such a way that the seller’s overall revenue compares favorably with the optimal auction from the target class.

More formally, on round , a tuple of bidders arrives with a vector of bids or, equivalently, a vector of valuations (since we only consider truthful auctions), denoted . We allow these valuations to be arbitrary, e.g., chosen by an adversary. Prior to observing the bids, the auctioneer commits to an auction from a class of truthful auctions . The goal of the auctioneer is to achieve a revenue that, in hindsight, is very close to the revenue that would have been achieved by the best fixed auction in class if that auction were used on all rounds. In other words, the auctioneer aims to minimize the expected regret

where is the revenue of auction on bid profile and the expectation is over the actions of the auctioneer.

This problem can easily be cast in our oracle-efficient online learning framework. The learner’s action space is the set of target auctions , while the adversary’s action space is the set of bid or valuation vectors . The offline oracle is a revenue maximization oracle which computes an (approximately) optimal auction within the class for any given set of valuation vectors. Using the Generalized FTPL with appropriate matrices , we provide the first oracle-efficient no-regret algorithms for three commonly studied auction classes:

-

–

Vickrey-Clarkes-Groves (VCG) auctions with bidder-specific reserve prices in single-dimensional matroid settings, which are known to achieve half the revenue of the optimal auction in i.i.d. settings under some conditions Hartline and Roughgarden, (2009);

- –

- –

The crux of our approach is in designing admissible and implementable matrices. For the first two mentioned classes, VCG auctions with bidder-specific reserves and envy-free item-pricing auctions, we show how to implement an (obviously admissible) matrix , where each row corresponds, respectively, to the concatenated binary representation of bidder reserves or item prices. We show that, surprisingly, any perturbation that is a linear function of this binary representation can be simulated by a distribution of bidder valuations (see Figure 1 for an example). For the third class, level auctions, our challenge is to show that a clearly implementable matrix , with each column implemented by a single bid profile, is also admissible.

Table 1 summarizes regret bounds and runtimes of our oracle-efficient algorithms, assuming oracle calls run in time . Our algorithms perform a single oracle call per round, so oracle calls in total. Our runtimes demonstrate an efficient reduction from online to offline learning.

While, in theory, the auction classes discussed in the table do not have worst-case polynomial-time algorithms for the offline problem, in practice, the offline problems are solved by a wide range of approaches, such as integer program solvers, which run fast on typical problem instances. Our approach can turn existing offline routines into online algorithms at almost no additional cost. When one wishes to leverage provably polynomial-time algorithms, even if their outputs are sub-optimal, our framework still applies as long as the algorithms return actions whose payoffs are within a constant factor of the best payoff. We discuss this approach briefly in Section 1.3 below and then demonstrate its applicability in Section 7, where we derive a polynomial-time algorithm for online welfare maximization in multi-unit auctions.

1.3 Extensions and Additional Applications

In Sections 4–7, we present several extensions and additional applications (see Table 2 for a summary):

Markovian Adversaries and Competing with the Optimal Auction (Section 4).

Morgenstern and Roughgarden, (2015) show that level auctions can provide an arbitrarily accurate approximation to the overall optimal Myerson auction in the Bayesian single-item auction setting if the values of the bidders are drawn from independent distributions and i.i.d. over time. Therefore, if the environment in an online setting picks bidder valuations from independent distributions, standard online-to-batch reductions imply that the revenue of Generalized FTPL with the class of level auctions is close to the overall optimal (i.e., not just best-in-class) single-shot auction. We generalize this reasoning and show the same strong optimality guarantee when the valuations of bidders on each round are drawn from a fast-mixing Markov process that is independent across bidders but Markovian over rounds. For this setting, our results give an oracle-efficient algorithm with regret to the overall optimal auction, rather than just best-in-class. This is the first result on competing with the Myerson optimal auction for non-i.i.d. distributions, as all prior work Cole and Roughgarden, (2014); Morgenstern and Roughgarden, (2015); Devanur et al., (2016); Roughgarden and Schrijvers, (2016) assumes i.i.d. samples.

Contextual Learning (Section 5).

In this setting, on each round the learner observes a context before choosing an action. For example, in online auction design, the context might represent demographic information about the set of bidders. The goal of the learner is to compete with the best policy in some fixed class, where each policy is a mapping from a context to an action. We propose a contextual extension of the translation matrix . Generalized FTPL can be applied using this extended translation matrix and provides sublinear regret bounds for both the case in which there is a small “separator” of the policy class and the transductive setting in which the set of all possible contexts is known ahead of time. Our results extend and generalize the results of Syrgkanis et al., 2016a from contextual combinatorial optimization to any learning setting that admits an implementable and admissible translation matrix.

The contextual extension is particularly useful in online auction design, because it allows the learner to use any side information available about the bidders before they place their bids to guide the choice of auction. While the number of bidders might be too large to learn about them individually, the learner can utilize the side information to design a common treatment for bidders that are similar, that is, to generalize across a population.

Our performance guarantees for adaptive auction design, similar to much prior work, rely on the assumption that the bidders are either myopic or are different on each round. One criticism of this assumption is that such adaptive mechanisms might be manipulated by strategic bidders who distort their bids so as to gain in the future. The contextual learning algorithms mitigate this risk by pooling similar bidders, which reduces the probability that the exact same bidder will be overly influential in the choices of the algorithm.

Approximate Oracles and Approximate Regret (Section 6).

For some problems there might not exist a sufficiently fast (e.g., polynomial-time or FPTAS) offline oracle with small additive error as required for Generalized FTPL. To make our results more applicable in practice, we extend them to handle oracles that are only required to return an action with performance that is within a constant multiplicative factor, , of that of the optimal action in the class. We consider two examples of such oracles: Relaxation-based Approximations (Balcan and Blum,, 2006) and Maximal-in-Range (MIR) algorithms Nisan and Ronen, (2007). Our results hold in both cases with a modified version of regret, called -regret, in which the online algorithm competes with times the payoff of the optimal action in hindsight.

Additional Applications (Section 7).

Finally, we provide further applications of our work in the area of online combinatorial optimization with MIR approximate oracles, and in the area of no-regret learning for bid optimization in simultaneous second-price auctions.

-

–

In the first application, we give a polynomial-time learning algorithm for online welfare maximization in multi-unit auctions that achieves -regret, by invoking the polynomial-time MIR approximation algorithm of Dobzinski and Nisan, (2007) as an offline oracle.

-

–

In the second application, we solve an open problem raised in the recent work of Daskalakis and Syrgkanis, (2016), who offered efficient learning algorithms only for the weaker benchmark of no-envy learning, rather than no-regret learning, in simultaneous second-price auctions, and left open the question of oracle-efficient no-regret learning. We show that no-regret learning in simultaneous item auctions is efficiently achievable, assuming access to an optimal bidding oracle against a known distribution of opponents bids (equivalently, against a distribution of item prices).

| Problem Class | Regret | Section | Notes |

| Markovian, single item | 4.2 | competes with Myerson’s optimal auction | |

| contextual online auctiona | or | 5 | allows side information about bidders |

| welfare maximization, -unitb | -regret: | 7.1 | fully (oracle-free) polynomial-time algorithm |

| bidding in SiSPAs, items | 7.2 | solves an open problem Daskalakis and Syrgkanis, (2016) |

aThe two bounds are for the small separator setting and the transductive setting, respectively. Dependence on parameters other than is omitted.

bThe regime of interest in this problem is . The extended abstract Dudík et al., (2017) contained a worse bound .

2 Generalized FTPL and Oracle-Efficient Online Learning

In this section, we introduce the Generalized Follow-the-Perturbed-Leader (Generalized FTPL) algorithm and describe the conditions under which it efficiently reduces online learning to offline optimization.

As described in Section 1.1, we consider the following online learning problem. On each round , a learner chooses an action from a finite set , and an adversary chooses an action from a set , which is not necessarily finite. The learner then observes and receives a payoff , where the function is fixed and known to the learner. The goal of the learner is to obtain low expected regret with respect to the best action in hindsight, i.e., to minimize

where the expectation is over the randomness of the learner. An online algorithm is called a no-regret algorithm if its regret is sublinear in , which means that its per-round regret goes to as . To simplify exposition, we assume that the adversary is oblivious, i.e., that the sequence is chosen up front without knowledge of the learner’s realized actions. Our results generalize to adaptive adversaries using standard techniques (Hutter and Poland,, 2005; Daskalakis and Syrgkanis,, 2016).

A natural first attempt at an online learning algorithm with oracle access would be one that simply invokes the oracle on the historical data at each round and plays the best action in hindsight. In a stochastic environment in which the adversary’s actions are drawn i.i.d. from a fixed distribution, this Follow-the-Leader approach achieves a regret of . However, because the algorithm is deterministic, it performs poorly in adversarial environments Blum and Mansour, (2007).

To achieve sublinear regret, we use a common scheme, introduced by Kalai and Vempala, (2005), and optimize over a perturbed objective at each round. Indeed, our algorithm takes its name from Kalai and Vempala’s Follow-the-Perturbed-Leader (FTPL) algorithm. Unlike FTPL, we do not generate a separate independent perturbation for each action, because this creates the two problems mentioned in Section 1.1. First, FTPL for unstructured payoffs requires creating independent random variables, which is intractably large in many applications, including the auction design setting considered here. Second, FTPL yields optimization problems that require a stronger offline optimizer than assumed here. We overcome the first problem by working with perturbations that are not necessarily independent across different actions (prior instances of such an approach were only known for linear Kalai and Vempala, (2005) and submodular Hazan and Kale, (2012) minimization). We address the second problem by implementing such perturbations with synthetic historical samples of adversary actions; this idea was introduced by Daskalakis and Syrgkanis, (2016), but they did not provide a method of randomly generating such samples in general learning settings. Thus, our work unifies and extends these previous lines of research.

We create shared randomness among actions in by drawing a random vector of size , with components drawn independently from a dispersed distribution . The payoff of each of the learner’s actions is perturbed by a linear combination of these independent variables, as prescribed by a perturbation translation matrix of size , with entries in . The rows of , denoted , describe the linear combination for each action . That is, on each round , the payoff of each learner action is perturbed by , and our Generalized FTPL algorithm outputs an action that approximately maximizes . This procedure is fully described in Algorithm 1. (For non-oblivious adversaries, a fresh random vector is drawn in each round.)

In the remainder of this section, we analyze the properties of matrix that guarantee that Generalized FTPL is no-regret and that its perturbations can be efficiently transformed into synthetic history. Together these properties give rise to efficient reductions of online learning to offline optimization.

2.1 Regret Analysis

To analyze Generalized FTPL, we first bound its regret by the sum of a stability term, a perturbation term, and an error term in the following lemma. While this approach is standard (Kalai and Vempala,, 2005), we include a proof in Appendix B.1 for completeness.

Lemma 2.1 (-FTPL Lemma).

For Generalized FTPL, we have

| (1) |

where .

In this lemma, the first term measures the stability of the algorithm, i.e., how often the action changes from round to round. The second term measures the strength of the perturbation, that is, how much the perturbation amount differs between the best action and the initial action. The third term measures the aggregated approximation error in choosing that only approximately optimizes .

To bound the stability term, we require that the matrix be admissible and the distribution be dispersed in the following sense.

Definition 2.2 (-Admissible Translation Matrix).

A translation matrix is admissible if its rows are distinct. It is -admissible if it is admissible and distinct elements within each column differ by at least .

Definition 2.3 (-Dispersed Distribution).

A distribution on the real line is -dispersed if for any interval of length , the probability measure placed by on this interval is at most .

In the next lemma, we bound the stability term in Equation (1) by showing that with high probability, for all rounds , we have . At a high level, since all rows of an admissible matrix are distinct, it suffices to show that the probability that is small. We prove this for each coordinate separately, by showing that it is only possible to have when the random variable falls in a small interval, which happens with only small probability for a sufficiently dispersed distribution .444The proof of Lemma 2.4 implies a slightly tighter bound of , where is the maximum number of distinct elements in any column of . Note that -admissibility implies that .

Lemma 2.4.

Consider Generalized FTPL with a -admissible matrix with columns and a -dispersed distribution . Then,

Proof.

Fix any . The bulk of the proof establishes that, with high probability, , which by admissibility implies that and therefore .

Fix any . We first show that with high probability. Let denote the set of values that appear in the column of . By -admissibility, . For any value , let be any action that maximizes the perturbed cumulative payoff among those whose entry in the column equals :

For any , define

Note that and are independent of , as we removed the payoff perturbation corresponding to .

If , then by the -optimality of on the perturbed cumulative payoff, we have for all . Suppose . Then by the optimality of and the -optimality of ,

Rearranging, we obtain for this same that

If , then

and so where is the value of minimizing the expression on the right. Thus, in this case we have . Similarly, if , then

and so where is the value maximizing the expression on the right. In this case we have . Putting this all together, we have

The first inequality on the last line follows from the fact that and , the fact that is -dispersed, and a union bound. The final inequality follows because by -admissibility.

Since this bound does not depend on the values of for , we can remove the conditioning and bound . Taking a union bound over all , we then have that, by admissibility, , which implies the result. ∎

To bound the regret, it remains to bound the perturbation term in Equation (1). This bound is specific to the distribution . Many distribution families, including (discrete and continuous) uniform, Gaussian, Laplacian, and exponential can lead to a sublinear regret when the variance is set appropriately. Here we present a concrete regret analysis for a uniform distribution:

Theorem 2.5.

Let be a -admissible matrix with columns and let be the uniform distribution on for . Then, the regret of Generalized FTPL can be bounded as

The proof follows from Lemmas 2.1 and 2.4, by bounding the perturbation term by , then setting , and finally using the value of from the theorem, which minimizes the sum of the stability and perturbation terms, .

Throughout the paper we consider , which is the weakest setting with respect to that does not negatively impact the regret rate regardless of other problem-dependent constants such as and :

Corollary 2.6.

Let be a -admissible matrix with columns, let be the uniform distribution on for , and let . Then the regret of Generalized FTPL is .

The multiplicative weights (or exponentiated gradient) algorithms achieve the regret in this setting (Freund and Schapire,, 1997; Kivinen and Warmuth,, 1997). Our bound is generally worse, because by -admissibility, which implies that , and therefore . However, the multiplicative weights algorithms typically require running times that are polynomial in , whereas our algorithm can be exponentially faster assuming access to efficient optimization oracles. We therefore next turn our attention to the analysis of the running time of our algorithm.

2.2 Oracle-Efficient Online Learning

We now define the offline oracle and oracle-efficient online learning more formally. Our oracles are defined for real-weighted datasets, but can be easily implemented by integer-weighted oracles (see the reduction in Appendix F.2). Since many natural offline oracles are iterative optimization algorithms, which are only guaranteed to return an approximate solution in finite time, our definition assumes that the oracle takes the desired precision as an input. For ease of exposition, we assume that all numerical computations, even those involving real numbers, take time. We discuss this point in more detail in Appendix F.

Definition 2.7 (Offline Oracle).

An offline oracle Opt is any algorithm that receives as input a weighted set of adversary actions with , and a desired precision , and returns an action such that

Definition 2.8 (Oracle Efficiency).

We say that an online algorithm is oracle-efficient with per-round complexity if its per-round running time is with oracle calls counting . The notation refers to the fact that may be a function of problem-specific parameters, including .

We next define a property of a translation matrix which allows us to transform the perturbed objective into a dataset, thus achieving oracle efficiency of Generalized FTPL:

Definition 2.9.

A matrix is implementable with complexity if for each there exists a weighted dataset , with , such that

| for all : |

In this case, we say that weighted datasets , , implement with complexity .

One simple but useful example of implementability is when each column of specifies the payoffs of learner’s actions under a particular adversary action , i.e., . In this case, . Using an implementable gives rise to an oracle-efficient variant of the Generalized FTPL, provided in Algorithm 2, in which we explicitly set . Theorem 2.10 shows that the output of this algorithm is equivalent to the output of Generalized FTPL and therefore the same regret guarantees hold. Note the assumption that the perturbations are non-negative. The algorithm can be extended to negative perturbations when both and are implementable. (See Section 5 for details.)

Theorem 2.10.

Proof.

To show that the Oracle-Based FTPL procedure (Algorithm 2) implements Generalized FTPL (Algorithm 1) with , it suffices to show that at each round , for any ,

| (2) |

Note that if the above equivalence holds, then in each round, the set of actions that can return legally, i.e., actions whose payoffs are an approximation of the optimal payoff, is exactly the same as the set of actions that the offline optimization step of Algorithm 1 can legally play. Therefore, the theorem is proved if Equation (2) holds.

Let us show that Equation (2) is indeed true. For , consider any . Then, from the definition of and by implementability,

which immediately yields Equation (2).

Also, by implementability, the running time to construct the set is at most . Since there is only one oracle call per round, we get the per-round complexity of . ∎

As an immediate corollary, we obtain that the existence of a polynomial-time offline oracle implies the existence of polynomial-time online learner with regret , whenever we have access to an implementable and admissible matrix.

Corollary 2.11.

Alternative Notions of Oracles.

Throughout this paper we work with offline optimization oracles that take data with arbitrary non-negative real weights as their input. In Corollary 2.11, we then consider oracles of this form that run in polynomial time. Other notions of oracles may be natural in various applications. For instance, instead of real-weighted, one can consider integer-weighted oracles, and instead of polynomial-time, one can consider pseudo-polynomial oracles. We discuss these alternative notions in Appendix F. We show that integer-weighted oracles can be used to implement approximately optimal real-weighted oracles, so all of our results immediately extend to integer-weighted oracles. For pseudo-polynomial oracles, the running time of the algorithm depends on the pseudo-complexity of the datasets that implement (pseudo-complexity is defined in Appendix F.1). In that case, for instance, the magnitude of the weights implementing the matrix affects the final running time of the learning algorithm. In Appendix F.4 we show that the pseudo-complexities of matrices constructed in the next section are polynomial in the parameters of interest, so in those cases even pseudo-polynomial offline oracles give rise to polynomial-time no-regret algorithms.

3 Online Auction Design

In this section, we apply the general techniques developed in Section 2 to obtain oracle-efficient no-regret algorithms for several common auction classes.

Consider a mechanism-design setting in which a seller wants to allocate heterogeneous resources to a set of bidders. The allocation to a bidder is a subset of , which we represent as a vector in , and the seller has some feasibility constraints on the allocations across bidders. Each bidder has a combinatorial valuation function , where . We use to denote the vector of valuation functions across all bidders. A special case of the setting is that of multi-item auctions for heterogeneous items, where each resource is an item and the feasibility constraint simply states that no item is allocated to more than one bidder. Another special case is that of single-parameter (service-based) environments, which we describe in more detail in Section 3.1.

An auction takes as input a bid profile consisting of reported valuations for each bidder, and returns both the allocation for each bidder and the price that he is charged. In this work, we only consider truthful auctions, where each bidder maximizes his utility by reporting his true valuation, irrespective of what other bidders report. We therefore make the assumption that each bidder reports as their bid and refer to not only as the valuation profile, but also as the bid profile throughout the rest of this section. The allocation that the bidder receives is denoted and the price that he is charged is ; we allow sets to overlap across bidders, and drop the argument when it is clear from the context. We consider bidders with quasilinear utilities: the utility of bidder is . For an auction with price function , we denote by the revenue of the auction for bid profile , i.e., .

Fixing a class of truthful auctions and a set of possible valuations , we consider the problem in which on each round , a learner chooses an auction while an adversary chooses a bid profile . The learner then observes and receives revenue . The goal of the learner is to obtain low expected regret with respect to the best auction from in hindsight. That is, we would like to guarantee that

We require our online algorithm to be oracle-efficient, assuming access to an -optimal offline optimization oracle that takes as input a weighted set of bid profiles, , and returns an auction that achieves an approximately optimal revenue on , i.e., a revenue at least . Throughout the section, we assume that there exists such an oracle for , as needed in Algorithm 2.

Using the language of oracle-based online learning developed in Section 2, the learner’s action corresponds to the choice of auction, the adversary’s action corresponds to the choice of bid profile, the payoff of the learner corresponds to the revenue generated by the auction, and we assume access to an offline optimization oracle Opt. These correspondences are summarized in the following table.

| Auction Setting | Oracle-Based Learning Equivalent |

| Auctions | Learner actions |

| Bid/valuation profiles | Adversary actions |

| Revenue function | Payoff function |

For several of the auction classes we consider, such as multi-item or multi-unit auctions, the revenue of an auction on a bid profile is in range for . In order to use the results of Section 2, we implicitly re-scale all the revenue functions by dividing them by before applying Theorem 2.5. Note that, since does not change, the admissibility condition keeps the regret of the normalized problem at , according to Theorem 2.5. We then scale up to get a regret bound that is times the regret for the normalized problem, i.e., . This re-scaling does not increase the runtime, because the complexity of implementing is unchanged, only the weights appearing in sets are scaled up by a factor of , and we assume that all numerical computations take time. Refer to Appendix F for a note on numerical computations and the mild change in runtime when numerical computations do not take time.

We now derive results for three auction classes: VCG auctions with bidder-specific reserves, envy-free item-pricing auctions, and level auctions. Each auction class is formally defined in its respective subsection.

3.1 VCG with Bidder-Specific Reserves

In this section, we consider a standard class of auctions, VCG auctions with bidder-specific reserve prices, which we define more formally below and denote by . These auctions are known to approximately maximize the revenue when bidder valuations are drawn from independent (but not necessarily identical) distributions (Hartline and Roughgarden,, 2009). Recently, Roughgarden and Wang, (2016) considered online learning for this class and provided a computationally efficient algorithm whose total revenue is at least of the best revenue among auctions in , minus a term that is . We apply the techniques from Section 2 to generate an oracle-efficient online algorithm with low additive regret with respect to the optimal auction in the class , without any loss in multiplicative factors.

We go beyond single-item auctions and consider general single-parameter environments. In these environments, each bidder has one piece of private valuation for receiving a service, i.e., being included in the set of winning bidders. We allow for some combinations of bidders to be served simultaneously, and let be the family of feasible sets, i.e., sets of bidders that can be served simultaneously; with some abuse of notation we write , to mean that the set represented by the binary allocation vector is in . We assume that any bidder is allowed to be the sole bidder served, i.e., that for all , and that it is also allowed that no bidder be served, i.e., .555A more common and stronger assumption used in previous work Hartline and Roughgarden, (2009); Roughgarden and Wang, (2016) is that is a downward-closed matroid. Examples of such environments include single-item single-unit auctions (for which contains only singletons and the empty set), single-item -unit auctions (for which contains any subset of size at most ), and combinatorial auctions with single-minded bidders. In the last case, we begin with some set of original items, define the service as receiving the desired bundle of items, and let contain any subset of bidders seeking disjoint sets of items.

In a basic VCG auction, an allocation is chosen to maximize social welfare, that is, maximize , where we slightly simplify notation and use to denote the valuation of bidder for being served. Each bidder who is served is then charged the externality he imposes on others, , which can be shown to equal the minimum bid at which he would be served. Such auctions are known to be truthful. The most common example is the second-price auction for the single-item single-unit case in which the bidder with the highest bid receives the item and pays the second highest bid. VCG auctions with reserves, which maintain the property of truthfulness, are defined as follows.

Definition 3.1 (VCG auctions with bidder-specific reserves).

A VCG auction with bidder-specific reserves is specified by a vector of reserve prices for each bidder. As a first step, all bidders whose bids are below their reserves (that is, bidders for which ) are removed from the auction. If no bidders remain, no item is allocated. Otherwise, the basic VCG auction is run on the remaining bidders to determine the allocation. Each bidder who is served is charged the larger of his reserve and his VCG payment.

Fixing the set of feasible allocations, we denote by the class of all VCG auctions with bidder-specific reserves. With a slight abuse of notation we write to denote the auction with reserve prices . To apply the results from Section 2, which require a finite action set for the learner, we limit attention to the finite set of auctions consisting of those auctions in which the reserve price for each bidder is a strictly positive integer multiple of , i.e., those where for all . We will show for some common choices of that the best auction in this class yields almost as high a revenue as the best auction in .

We next show how to design a matrix for that is admissible and implementable. As a warmup, suppose we use the matrix with entries . That is, the column of corresponds to the revenue of each auction on a bid profile in which bidder has valuation and all others have valuation . By definition, is implementable with complexity using for each . Moreover, so any two rows of are different and is thus -admissible. By Theorems 2.5 and 2.10, we obtain an oracle-efficient implementation of the Generalized FTPL with regret .

To improve this regret bound and obtain a regret that is polynomial in rather than , we carefully construct another translation matrix that is implementable using a more complex dataset of adversarial actions. The translation matrix we design is quite intuitive. The row corresponding to an auction contains a binary representation of its reserve prices. In this case, proving admissibility of the matrix is simple. The challenge is to show that this simple translation matrix is implementable using a dataset of adversarial actions.

Construction of :

Let be an binary matrix, where the collection of columns contains the binary encodings of the auctions’ reserve prices for bidder . More formally, for any and a bit position , let and set to be the bit of .

In Lemma 3.3, we prove that is implementable and admissible. But first, let us illustrate the main ideas of this proof through a simple example.

| Binary encoding | |||||

| Auction | |||||

| 0 | 1 | 0 | 1 | ||

| 0 | 1 | 1 | 0 | ||

| 0 | 1 | 1 | 1 | ||

| 1 | 0 | 0 | 1 | ||

| 1 | 0 | 1 | 0 | ||

| 1 | 0 | 1 | 1 | ||

| 1 | 1 | 0 | 1 | ||

| 1 | 1 | 1 | 0 | ||

| 1 | 1 | 1 | 1 | ||

Example 3.2.

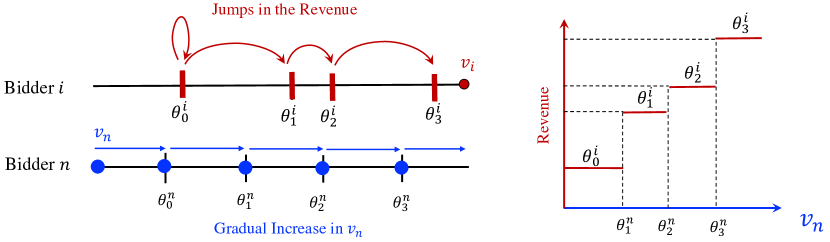

Consider for bidders and discretization levels, as demonstrated in Figure 1. As an example, we show how one can go about implementing columns and of .

Consider the first column of . It corresponds to the most significant bit of . To implement this column, we need to find a weighted set of bid profiles that generate revenues with the same differences as those between the column entries. We consider bid profiles for , with the revenue . To obtain the weights for each it is necessary (and sufficient) to match differences between entries corresponding to reserve prices with vs , and vs (denoted by in Figure 1), corresponding to the following equations:

where the left-hand sides are the differences in the revenues and the right-hand sides are the differences between the corresponding column entries. Note that the weighted set satisfies these equations and implements the first column. Similarly, for implementing the fourth column, we consider bid profiles for and equations dictated by the differences . One can verify that implements this column.

More generally, the proof of Lemma 3.3 shows that is implementable by showing that any differences in values in one column that solely depend on a single bidder’s reserve price lead to a feasible system of linear equations.

Lemma 3.3.

is -admissible and implementable with complexity .

Proof.

In the interest of readability, we drop the superscript and write for in this proof.

For any , row corresponds to the binary encoding of . Therefore, for any two different auctions , we have . Since is a binary matrix, this implies that is -admissible.

Next, we will construct the sets that implement each column . Pick and , and the associated column index . The set includes exactly the profiles in which only the bidder has non-zero valuation, denoted as for . To determine their weights , we use the definition of implementability. In particular, the weights must satisfy:

In the above equation, and encode the bit of and , respectively, so the left-hand side is independent of the reserve prices for bidders . Moreover, , so the right-hand side of the above equation is also independent of the reserve prices for bidders . Let be the bit of integer . That is, . Substituting and , the above equation can be reformulated as 666Not including the reserve 0 is a crucial technical point for the proof of implementability.

| (3) |

We recursively derive the weights , and show that they are non-negative and satisfy Equation (3). To begin, let

and for all , define

Next, we show by induction that for all . For the base case of , by definition . Now, assume that for all , . Then

Therefore all weights are non-negative. Furthermore, by rearranging the definition of , we have

where in the second equality we simply added and subtracted the term and in the last equality, we grouped together common terms.

Equation (3) is proved for a particular pair by summing the above expression for over all and canceling telescoping terms, and if , the statement holds regardless of the weights chosen.

This shows that is implementable. Note that the cardinality of each is , so is implementable with complexity . ∎

The next theorem follows immediately from Lemma 3.3, Theorems 2.5 and 2.10, and the fact that the maximum revenue is at most . Note that is bounded by the number of bidders that can be served simultaneously, which is at most .

Theorem 3.4.

Consider the online auction design problem for the class of VCG auctions with bidder-specific reserves, . Let and let be the uniform distribution as described in Theorem 2.5. Then, the Oracle-Based Generalized FTPL algorithm with and datasets that implement is oracle-efficient with per-round complexity and has regret

Now we return to the infinite class of all VCG auctions with reserve prices . We show that is a finite “cover” for this class when the family of feasible sets consists of all subsets of size at most , corresponding to single-item single-unit auctions (when ) or more general single-item -unit auctions. In such auctions, the items are allocated to the highest bids that are above their reserve, and each winner pays the larger of its reserve price and the highest bid that had cleared its respective reserve price. We assume that the ties are resolved in favor of bidders with a lower index. We prove in Appendix C.1 that for these auctions, the optimal revenue of compared with that of can decrease by at most at each round. That is,

| (4) |

Setting and using Theorem 3.4, we obtain the following result for the class of auctions .

Theorem 3.5.

Consider the online auction design problem for the class of VCG auctions with bidder-specific reserves, , in -unit auctions. Let be the uniform distribution as described in Theorem 2.5. Then, the Oracle-Based Generalized FTPL algorithm with and datasets that implement is oracle-efficient with per-round complexity and has regret

3.2 Envy-free Item Pricing

In this section, we consider envy-free item pricing Guruswami et al., (2005) in an environment with heterogeneous items with a supply of units for each item .

Definition 3.6 (Envy-free Item-Pricing Auction).

An envy-free item-pricing auction for heterogeneous items, given supply for , is defined by a vector of prices , where is the price of item . The mechanism considers bidders in order and allocates to bidder the bundle that maximizes , among all feasible bundles, i.e., bundles that can be composed from the remaining supplies. Bidder is then charged the price .

Examples of such environments include unit-demand bidders and single-minded bidders in settings such as hypergraph pricing, where bidders seek hyperedges in a hypergraph, and its variant the highway problem, where bidders seek hyperedges between sets of contiguous vertices Balcan and Blum, (2006); Guruswami et al., (2005).

We represent by the class of all such envy-free item-pricing auctions where all the prices are strictly positive multiples of , i.e., for all . Next, we discuss the construction of an implementable and admissible translation matrix . Consider a bid profile where one bidder has value for bundle and all other bidders have value for all bundles. The revenue of auction on such a bid profile is . Note the similarity to the case of VCG auctions with bidder-specific reserve prices , where bid profiles with a single non-zero valuation yielding the revenue were used to create an implementable construction for . We show that a similar construction works for .

Construction of :

Let be a binary matrix, where the collection of columns correspond to the binary encoding of the auction’s price for item . More formally, for any and , is the bit of (the integer) , where . Next, we show that is admissible and implementable. The proof of the following lemma is analogous to that of Lemma 3.3 and appears in Appendix C.2 for completeness.

Lemma 3.7.

is -admissible and implementable with complexity .

Our main theorem follows immediately from Lemma 3.7, Theorems 2.5 and 2.10, and the fact that the revenue of the mechanism at every step is at most . In general, is at most .

Theorem 3.8.

Consider the online auction design problem for the class of envy-free item-pricing auctions, . Let and let be the uniform distribution as described in Theorem 2.5. Then, the Oracle-Based Generalized FTPL algorithm with and datasets that implement is oracle-efficient with per-round complexity and has regret

Now consider the class of all envy-free item-pricing auctions where is a real number and denote this class by . We show that is a discrete “cover” for when there is an unlimited supply of all items ( for all ) and the bidders have single-minded or unit-demand valuations. In the single-minded setting, each bidder is interested in one particular bundle of items . That is, for all and otherwise. In the unit-demand setting, each bidder has valuation for item , and wishes to purchase at most one item, i.e., item . We show that in both settings, discretizing item prices cannot decrease the revenue by much (see Appendix C.3).

Lemma 3.9.

For any there is , such that for any unit-demand valuation profile with infinite supply (the digital goods setting), . Similarly, there is , such that for any single-minded valuation profile with infinite supply, .

These discretization arguments together with Theorem 3.8 yield the following result for the class of auctions (using the fact that , and setting for the unit-demand and for the single-minded setting):

Theorem 3.10.

Consider the online auction design problem for the class of envy-free item-pricing auctions, , with unit-demand bidders with infinite supply (the digital goods setting). Let be the uniform distribution as described in Theorem 2.5. Then, the Oracle-Based Generalized FTPL algorithm with and datasets that implement is oracle-efficient with per-round complexity and has regret

Similarly, for single-minded bidders with infinite supply, the Oracle-Based Generalized FTPL algorithm with and datasets that implement is oracle-efficient with per-round complexity and has regret

3.3 Level Auctions

We next consider the class of level auctions introduced by Morgenstern and Roughgarden, (2015), who show that these auctions can achieve -approximate revenue maximization if the valuations of the bidders are drawn independently (but not necessarily identically) from a distribution, thus approximating Myerson’s optimal auction Myerson, (1981). Using our tools, we derive oracle-efficient no-regret algorithms for this auction class.

The -level auctions realize a single-item single-unit allocation as follows:

Definition 3.11.

Given , an -level auction is defined by thresholds for each bidder , . For any bid profile , we let denote the largest index such that , or if . If for all , the item is not allocated. Otherwise, the item goes to the bidder with the largest index , breaking ties in favor of bidders with smaller . The winner pays the price equal to the minimum bid that he could have submitted and still won the item.

When it is clear from the context, we omit in and write just . In the remainder of the section we assume that . For , the level auctions are equivalent to the second-price auctions with reserves, so we can just appeal to the bounds from previous sections (specifically, Theorems 3.4 and 3.5 from Section 3.1).

We consider two classes of -level auctions, and , where is the set of all auctions described by Definition 3.11 with thresholds in the set and is the subset of containing the auctions in which the thresholds for each bidder are distinct.

We first consider . To construct an admissible and implementable for , we begin with a matrix that is clearly implementable, with each column implemented by a single bid profile, and then show its admissibility.

We consider the bid profiles in which the only non-zero bids are for some , and for a single bidder . Note that bidder wins the item in any such profile and pays corresponding to . We define a matrix with one column for every bid profile of this form and an additional column for the bid profile , with the entries in each row consisting of the revenue of the corresponding auction on the given bid profile. Clearly, is implementable. As for admissibility, take and the corresponding row . Note that as increases for , there is an increase in , possibly skipping the initial . As the level increases, the auction revenue attains the values , , changing exactly at those points where crosses thresholds . Since any two consecutive thresholds of are different, the thresholds of for and for can be reconstructed by analyzing the revenue of the auction and the values of at which the revenue changes. The remaining threshold is equal to the revenue of the bid profile . Since all of the parameters of the auction can be recovered from the entries in the row , this shows that any two rows of are different and is -admissible. This reasoning is summarized in the following construction and the corresponding lemma, formally proved in Appendix C.4. See Figure 2 for more intuition.

Construction of :

For and , let . Let . Let be the matrix of size with entries indexed by , such that .

Lemma 3.12.

is -admissible and implementable with complexity .

Our next theorem is an immediate consequence of Lemma 3.12, Theorems 2.5 and 2.10, and the fact that the revenue of the mechanism in each round is at most .

Theorem 3.13.

Consider the online auction design problem for the class of -level auctions. Let be the uniform distribution as described in Theorem 2.5. Then, the Oracle-Based Generalized FTPL algorithm with and datasets that implement is oracle-efficient with per-round complexity and has regret

Next, we turn our attention to the class of auctions and construct an admissible and implementable matrix for this auction class. As a warm-up, we demonstrate how the structure of differs from and argue that is not admissible for . Take such that and is some multiple of . Similarly as before, as increases there is also an increase in and the revenue . However, the thresholds of bidder are no longer required to be distinct, so can skip certain values, and as a result is not revealed for all . In addition, when the thresholds of bidder are not distinct, we have that even when strictly increases, there might be no increase in the revenue, and as a result cannot be reconstructed.

We next show how to construct an admissible matrix for . In preparation for this construction, we first define an equivalence relation among auctions which puts auctions with distinct parameters but identical outcomes in the same equivalence class. Specifically, we say that two auctions and are equivalent if for any bid profile , , i.e., they receive the same revenue on all bid profiles. Note that it is sufficient to limit our attention to a subset of auctions that includes exactly one auction from each equivalence class. The regret with respect to is the same as the regret with respect to . Also, when applying Algorithm 2, any result returned by an offline oracle for can be replaced by the equivalent without affecting the algorithm’s regret. This means that an offline oracle for can be viewed as an offline oracle for and used together with an admissible and implementable matrix for the auction class to solve the online optimization problem for the larger but equivalent auction class . In the following, we introduce an implementable and admissible construction for .

Construction of :

Let , where denotes the number of non-zero entries of a vector. Let be the matrix of size with entries indexed by , such that .

Lemma 3.14.

is -admissible and implementable with complexity for the class of auctions .

Proof.

Clearly, is implementable with complexity for the class of auctions . We show that is also admissible. Take any two auctions and in . Since these auctions are not equivalent, there is a bid profile such that . Without loss of generality, assume that . In what follows, we construct a corresponding bid profile such that . Let and be the winners in the auctions and , respectively. Let and be the bidders with second highest bucketed bids, i.e., the bidders who set prices in auctions and , respectively. We consider two cases:

If , and are not distinct, we construct the bid profile that is the same as on indices , , , and , and is 0 otherwise. Note that has at most non-zero elements, hence . Moreover, the bids of the winners and the price setters are the same in both bid profiles, so the allocations and payments of both auctions remain the same. That is,

If , and are all distinct, we construct the bid profile that is the same as on indices , , and , and is 0 otherwise (including on index ). On auction , since the bids of the winner and the price setter, and are the same in both bid profiles, the allocation and payment of both auctions remain the same, and we have . On auction , the winner’s bid remains the same and the price setter’s bid is equal or lowered, so . Hence,

Since the revenue of any auction is a multiple of and any two rows of differ in at least one entry by , we obtain that is -admissible. ∎

Our next theorem is an immediate consequence of Lemma 3.14, Theorems 2.5 and 2.10, the equality of regrets with respect to and , and the fact that the revenue of the mechanism in each round is at most . As discussed above, Algorithm 2 can use an offline oracle for in place of an offline oracle for .

Theorem 3.15.

Consider the online auction design problem for the class of -level auctions. Let be the uniform distribution as described in Theorem 2.5. Then, the Oracle-Based Generalized FTPL algorithm with and datasets that implement is oracle-efficient with per-round complexity and has regret

4 Stochastic Adversaries and Universal Benchmarks

So far our results apply to general adversaries, where the sequence of adversary actions is arbitrary, and where we can achieve the payoff that is close to the payoff of the best action in our class. For auctions, we might be interested in the comparison with an arbitrary auction rather than an auction that is in our class. In this section, we show that in certain cases this can be achieved if we impose distributional assumptions on the sequence of the adversary.

We start with the easier setting where the actions of the adversary are drawn i.i.d. across all rounds and then we analyze the slightly more complex setting where the actions of the adversary follow a fast-mixing Markov chain. For both settings we show that the average payoff of the learning algorithm is close to the optimal expected payoff, where expectation is with respect to the adversary’s distribution in the i.i.d. setting and the adversary’s stationary distribution in the Markovian setting.

In online auction design, we can combine these results with approximate optimality results of simple auctions, such as -level auctions or VCG with bidder-specific reserves, to prove universal optimality of our online learning algorithms in these distributional settings rather than only the optimality among the auctions within the class over which our algorithms are learning.

4.1 Stochastic Adversaries

I.I.D. Adversary.

When the adversary actions are drawn independently from the same unknown distribution , we can use Chernoff-Hoeffding bound to show that the average payoff of a no-regret learner converges to the best payoff one could achieve in expectation over the distribution (see Appendix D.1 for the proof):

Lemma 4.1.

Suppose that are i.i.d. draws from a distribution . Then for any no-regret learning algorithm, with probability at least ,

Markovian Adversary.

Suppose that the choice of the adversary follows a stationary and reversible Markov process based on some transition matrix with a stationary distribution . Moreover, consider the case where the set is finite. For any Markov chain, the spectral gap is defined as the difference between the first and the second largest eigenvalue of the transition matrix (the first eigenvalue always being ). We will assume that this gap is bounded away from zero. The spectral gap of a Markov chain is strongly related to its mixing time. In this work we will specifically use the following result of Paulin, (2015), which is a Bernstein concentration inequality for sums of dependent random variables sampled from a stationary Markov chain with spectral gap bounded away from zero. A Markov chain is stationary if where is the stationary distribution, and is reversible if for any , . For simplicity, we focus on stationary chains, though similar results hold for non-stationary chains (see Paulin, (2015) and references therein).

Theorem 4.2 (Paulin, (2015), Theorem 3.8).

Let be a stationary and reversible Markov chain on a state space , with stationary distribution and spectral gap . Let , then

Applying this result, we obtain the following lemma (see Appendix D.2 for the proof):

Lemma 4.3.

Suppose that the adversary actions form a stationary and reversible Markov chain with stationary distribution and spectral gap . Then for any no-regret learning algorithm, with probability at least ,

Example 4.4 (Sticky Markov Chain).

Consider a Markov chain where at each round is equal to with some probability and with the remaining probability it is drawn independently from some fixed distribution . It is clear that the stationary distribution of this chain is equal to . We can bound the spectral gap of this Markov chain by the Cheeger bound Cheeger, (1969). The Cheeger constant for a finite state, reversible Markov chain is defined, and in this case bounded, as

Moreover, by the Cheeger bound we know that . Thus we get that for such a sequence of adversary actions, with probability ,

4.2 Implications for Online Optimal Auction Design

Consider the online optimal auction design problem for a single item and bidders. Suppose that the adversary who picks the valuation profiles is Markovian and that the stationary distribution of the chain is independent across players, i.e., the stationary distribution is a product distribution . Then we know that the optimal auction for this setting is Myerson’s (optimal) auction Myerson, (1981), which translates the players’ values based on some monotone function , known as the ironed virtual value function, and then allocates the item to the bidder with the highest virtual value, charging payments so that the mechanism is dominant-strategy truthful. In this section, we use the Generalized FTPL algorithm to compete with Myerson’s optimal auction in this Markovian environment. This extends the prior work that only gave such guarantees for the i.i.d. setting.777If we know ahead of the time that the stationary distribution is symmetric across bidders, i.e., , then the optimal auction is a second-price auction with a reserve. In that case, we can appeal to Theorem 3.5 to obtain a better regret bound than those presented in this section.

A natural approach for approximating the overall optimal auction in a Markovian environment is through level auctions. As discussed in Section 3.3, Morgenstern and Roughgarden, (2015) show that level auctions with repeated thresholds and arbitrarily fine discretization approximate Myerson’s optimal auction in terms of revenue. In more detail, when distributions are bounded in , the class of auctions with achieves expected revenue of at least a factor of of the expected optimal revenue of Myerson’s auction. Since the runtime and regret of our Generalized FTPL algorithm for the class of auctions scale with the discretization level , we require to be finite. Therefore, we cannot use this characterization of Morgenstern and Roughgarden, (2015) directly. Analogously to these results, we prove and use an additive approximation guarantee for the class of discretized level auctions , showing that

| (5) |

where is the optimal revenue achievable by any dominant-strategy truthful mechanism for valuation vector distribution .

At a high level, we prove Equation (5) using a three-step approach. We first consider the discretization of the bidders’ valuations. That is, for any bid profile , we consider that denotes the bid profile where each entry of is rounded down to the nearest whole multiple of . As the first step, it is not hard to show that for any , . In the second step, we show that Myerson’s optimal auction on the discretized valuations indeed belongs to the class . That is, when represents the distribution over valuations , we have

To prove this we use a characterization of Myerson’s optimal auction on discrete (and not necessarily regular) distributions provided by Elkind, (2007). Much like level auctions, this characterization assigns a bucket number to each possible valuation of each bidder and allocates the item to the valuation with the highest bucket number. We show that one can create thresholds for each bidder to mimic this bucketing effect. Therefore, the class of auctions includes an optimal auction for the discretized valuations. In the last step, we use a result of Devanur et al., (2016) that establishes that . Putting the above ingredients together, Theorem 4.5 shows that the Genearlized FTPL algorithm for approximates Myerson’s auction for a given Markov chain. We defer the detailed proof of Theorem 4.5 to Section 4.3 after giving an example of this setting.

Theorem 4.5 (Competing with Universally Optimal Auction).

Consider the online auction design problem for a single item among bidders, where the sequence of valuation vectors is Markovian, following a stationary and reversible Markov process with a spectral gap of and with a stationary distribution which is a product distribution across bidders, meaning . Then, the Generalized FTPL algorithm for , where , guarantees the following bound with probability at least :

Example 4.6 (Valuation Shocks).

Consider the setting where valuations of players in the beginning of time are drawn from some product distribution . Then in each round with some probability the valuations of all players remain the same as in the previous round, while with some probability , there is a shock in the market and the valuations of the players are re-drawn from distribution . As we analyzed in the previous section, the spectral gap of the Markov chain defined by this problem is at least . Thus we get a regret bound which depends inversely on the quantity .

Hence, our online learning algorithm achieves revenue that is close to the optimal revenue achievable by any dominant-strategy truthful mechanism for the distribution . More importantly, it achieves this guarantee even if the valuations of the players are not drawn i.i.d. at every iteration and even if the learner does not know what the distribution is, or when the valuations of the players are going to be re-drawn, or what the rate of shocks in the markets is.

4.3 Proof of Theorem 4.5

We set out to prove that

We first show that for any and any . To start, note that the thresholds in are multiples of , so bid profiles and are bucketed identically by . Therefore, these two bid profiles have the same winner and the same payment amount (equal to the smallest bid with which the bidder still wins the item). Thus, we have that , and by Lemma 4.3, we can bound the revenue of the Generalized FTPL algorithm as

| (6) |

Next, we show that the expected revenue of the optimal auction on the rounded valuation is close to , where is the product distribution of .

Lemma 4.7.

Let be a product distribution over that are supported on multiples of . Let be the revenue of Myerson’s optimal auction on . Then,