Geometry of vectorial martingale optimal transportations and duality

Abstract.

The theory of Optimal Transport (OT) and Martingale Optimal Transport (MOT) were inspired by problems in economics and finance and have flourished over the past decades, making significant advances in theory and practice. MOT considers the problem of pricing and hedging of a financial instrument, referred to as an option, assuming its payoff depends on a single asset price. In this paper we introduce Vectorial Martingale Optimal Transport (VMOT) problem, which considers the more general and realistic situation in which the option payoff depends on multiple asset prices. We address this problem of pricing and hedging given market information – described by vectorial marginal distributions of underlying asset prices – which is an intimately relevant setup in the robust financial framework.

We establish that the VMOT problem, as an infinite-dimensional linear programming, admits an optimizer for its dual program. Such existence result of dual optimizers is significant for several reasons: the dual optimizers describe how a person who is liable for an option payoff can formulate optimal hedging portfolios, and more importantly, they can provide crucial information on the geometry of primal optimizers, i.e. the VMOTs. As an illustration, we show that multiple martingales given marginals must exhibit an extremal conditional correlation structure whenever they jointly optimize the expectation of distance-type cost functions.

Keywords: Optimal transport, Martingale, Duality, Dual attainment, Extremal correlation structure, Infinite-dimensional linear programming

MSC2010 Classification: 90Bxx, 90Cxx, 49Jxx, 49Kxx, 60Dxx, 60Gxx

1. Introduction

The theory of Optimal Transport (OT) and its probabilistic version Martingale Optimal Transport (MOT) were inspired by problems in economics and finance and have flourished over the past decades, making significant advances in theory and practice.

In this paper we introduce the vectorial Martingale Optimal Transport (VMOT) problem, which is an intimately relevant setup in view of the robust financial framework dealing with many asset prices.

To further elaborate this point, let us consider a stochastic process of e.g. company ’s stock price, where . Under the risk neutral probability we may assume is a vector-valued martingale. Now in the robust financial framework we shall not assume that the joint probability law of is known, since we are unable to determine this joint law from the market information. However, by a standard argument by Breeden and Litzenberger [9], we shall assume that the distribution of each price at each fixed maturity , i.e. , can be observed from the market.

From now on let us focus on two fixed maturity times , and denote , , , , and assume that is a (one-step, -valued) martingale: . According to the above consideration we do not assume is known, but only the -number of marginal distributions are known and fixed. This naturally leads us to consider the following VMOT problem: Let , where

Let us write , . We consider the following space of Vectorial Martingale Transportations from to

| (1.1) | ||||

Let be a (cost) function. We define the VMOT problem as

| (1.2) |

The function has a natural interpretation in finance as an exotic option whose payoff is determined by the -number of asset prices at the terminal maturity. shall be considered as a fair price of the option in the risk-neutral world governed by the law of asset prices , but since would not be observed from the financial market, we need to consider all possible laws given the marginal information . Under this information, the max / min value in (1.2) can be interpreted as the upper / lower price bound for respectively.

Note that without the martingale constraint , (1.2) would be the usual multi-marginal optimal transport problem. But (1.2) still belongs to the class of infinite-dimensional linear programming, since the martingale constraint is linear. Now unlike the optimal transport case, the problem (1.2) will be feasible (i.e. ) if only if every pair of marginals is in convex order, defined by

as shown by Strassen [54]. Thus we will always assume for all in VMOT problem. And, because we will need to calculate means and potential functions of the measures, we will make the following assumption throughout the paper (unless otherwise specified):

Assumption. All measures appearing in this paper are assumed to have finite first moments.

Our first main result investigates the extremal correlation behavior of the terminal prices conditional on , when the martingales jointly max/minimize a distance-type cost function given vectorial marginals. More precisely, we establish the following theorem.

Theorem 1.1.

Assume all are absolutely continuous with respect to Lebesgue measure, denoted as . If solves the maximization problem in (1.2) with the Euclidean distance cost , then given , the conditional distribution of lies in the set of extreme points of a convex set depending on , –almost surely.

Here we say that a random variable lies in if a.s., and a distribution lies in if has its full mass in . We shall also prove an analogous result for the minimization problem in (1.2), and we also note that Theorem 1.1 still holds for more general class of strictly convex costs . See Theorem 2.1 for more details. We further note that the statement of extremal correlation was firstly given and studied by [32] in the context of MOT and two -dimensional marginals.

Recall that the VMOT problem belongs to the class of infinite-dimensional linear programming, which implies that the problem has its dual programming problem. For the (primal) minimization problem in (1.2), its dual problem is given by

| (1.3) |

where consists of triplets and such that , , is bounded for every , and

| (1.4) |

where , . Analogous dual problem for the maximization in (1.2) is easily obtained by changing sign of to .

The dual problem also has an important interpretation in finance. Suppose a financial firm is liable for an option it has sold so that the firm has to pay at the terminal maturity . To hedge its risk, the company may consider buying European options where each payoff relies only on a single asset at a fixed time. In addition, the firm may consider holding number of shares of the asset held between the and maturity, such that its payoff at is . Notice is a function of the past prices of all assets . Thus the left hand side of (1.4) yields the overall payoff of the hedging portfolio , and the inequality (1.4) imposes that the position must subhedge the liability for all scenarios of . Now notice the dual of the maximization in (1.2) becomes an optimal superhedging problem.

Now the celebrated duality result asserts, under a mild assumption on , that the primal and dual optimal values coincide (see e.g. [27, 58])

| (1.5) | ||||

Still a natural question is whether a dual optimizer exists, that is, a “tightly” sub/superhedging portfolio can be constructed. In the past decades, researchers working in OT already realized that the existence of an optimizer to the dual problem – often called dual attainment – is the essential key for the investigation of the optimal transport plans. But due to the nature of infinite dimensionality, establishing the dual attainment turns out to be quite subtle, as can be seen e.g. by the work of Brenier [10]. Thus it is no surprise that our second main result on the dual attainment is crucial for establishing Theorem 1.1. For a measure on define its potential function . We say is irreducible if is connected and . For more information on the notion of irreducibility, see Section 3 or [7].

Theorem 1.2.

Let be irreducible pairs of marginals on . Let be a lower-semicontinuous cost such that for some continuous , . Then there exists a pointwise dual maximizer (PDM), a triplet of functions that satisfies (1.4) tightly in the following pointwise manner (but does not necessarily belong to ):

| (1.6) |

for every VMOT which solves the minimization problem in (1.2).

We analogously define a pointwise (or pathwise) dual minimizer (PDm) for which the inequality in (1.4) should be reversed and in (1.6) now solves the maximization problem in (1.2). This simply corresponds to the change of to in the theorem. We shall sometimes call Theorem 1.2 as pointwise/pathwise dual attainment (PDA) for VMOT problems.

The term pointwise indicates the fact that (1.4), (1.6) hold in a pointwise manner (i.e., the equality (1.6) is satisfied for - almost every “point” or “path” ), and that we do not impose the integrability condition, namely , , or is bounded, on the PDM. Thus, a PDM needs not be in , and moreover, may assume the value . However, it is indeed true that -a.s. and -a.s., implied by the equation (1.6). See also Remark 3.2.

A couple of pioneering works on the dual attainment for MOT problems on the line () was established by Beiglböck-Juillet [5] and Beiglböck-Nutz-Touzi [7], where they already observed that the PDA could fail if one insists the integrability condition on PDM/PDm, or if one does not impose the irreducibility on the marginals. Beiglböck-Lim-Obłój [6] established PDA without the irreducibility assumption but imposing further regularity condition on . Theorem 1.2 is a continuation of these efforts for the case , i.e., for the VMOT setup.

Further background. Let us briefly introduce the optimal transport (OT) problem, which is the prototype of MOT and VMOT problems. To begin with, let us introduce the notion of push-forward of measures. Given a measurable map and a measure on , the push-forward of by , denoted by , is a measure on satisfying

for every measurable .

Let be the projection maps given by , . For a given cost function and two Borel probability measures on , the OT problem is given by

| (1.7) |

where is the set of transport plans, or couplings, if all have given marginals and , meaning , .

Kantorovich [40, 41] proposed the general formulation of the problem (1.7) in the 1940s after Gaspard Monge’s first formulation in the 1780s [46]. Since then, many important contributions have been made on the subject, as can be seen by part through the works [1, 2, 8, 10, 11, 19, 20, 28, 31, 44, 45, 53, 55, 56, 57]. In particular, one of the central questions is when the OT plans are given by transport maps – often called Monge problem, especially when – that is, when there exists a map such that a minimizer in (1.7) is given by , where is the identity map on .

To answer, we need to understand the geometry of the OT plans. Such a characteristic structure of OT plan is encoded in its support, which exhibits the so called -cyclical monotonicity. The monotonicity is already useful, but when combined with the celebrated theorem of Rockafellar [51], we obtain the dual attainment, a cornerstone of OT: there exist two functions , called Kantorovich potentials, such that for every minimizer of the problem (1.7), we have

| (1.8) | ||||

| (1.9) |

It turns out the dual attainment is essential for understanding OT[31].

Let us view the OT maps in a slightly different angle, and for this we recall the notion of disintegration of measures. For a general measure , a disintegration of via its first marginal is

| (1.10) |

which means for any Borel sets , . The family of probabilities is called a disintegration (or kernel) of with respect to . It is known this family uniquely exists - a.e. . Perhaps probabilistic language helps to understand better. Suppose is the joint distribution of the -valued random variables , denoted as . Then , and is the conditional law of given , that is .

Now “ is given by a transport map .” is equivalent to

| (1.11) |

where is the Dirac mass at , the probability measure concentrated at . In this case one could say the solution exhibits an extremal geometry in the sense that a disintegration , which describe the solution, are as extreme as Dirac masses, the most condensed measures.

Finally, we would like to also mention some important applications of OT in economics [29, 22, 50, 18], and in statistical theory [12, 17, 52, 16].

Recently a variant of OT, referred to as martingale optimal transport (MOT), was introduced. In MOT problem, we consider the following:

| (1.12) |

where MT (Martingale Transport plans) is a subset of such that each MT satisfies , that is has its barycenter at . Notice the kernel cannot be Dirac masses unless . Nonetheless, Theorem 1.1 shows the kernel of each MOT for norm-type costs still exhibits an interesting extremal distribution.

Probabilistic description of the MOT problem is as follows: consider

| (1.13) |

over all couples of -valued random variables on some probability space such that , and , i.e. is a one-step martingale. Strassen [54] showed MT is nonempty if and only if , are in convex order .

While some pioneering works to investigate the MOT problem have been made including [4, 26, 30, 38, 39], there is a related problem, called the Skorokhod embedding problem (SEP) which has a long history in probability theory. Since Hobson [36, 37] recognised the important connection between model independent finance and asset pricing theory and SEP (see Obłój [47] for a nice overview of the SEP and Beiglböck-Cox-Huesmann [3] for a link with OT theory), much related research has been done in this context including [13, 34, 35, 49, 21] for instance.

In the early stages of development of MOT theory, most of the research focused on single asset cases. More recently there have been efforts to generalize the theory into higher dimension , especially around the theory of duality and its attainment [43, 32, 33, 24, 25, 27, 48]. Nonetheless, to the best of the author’s knowledge a complete understanding of the possibility for the dual attainment has not been achieved: the added “trading strategy” term in the dual formulation seems to drastically change the picture from the OT case, and the potential non-existence of dual optimizers makes the study of solutions to MOT much more complex in the multi-dimensional setting.

While the MOT formulation (1.12) is a natural analogue of OT, not only it has difficulty in establishing PDA, but also its assumption on the marginal information is rather unrealistic from the financial point of view. This is because MOT assumes the joint distribution of the assets and are known – the . However, in practice such information is hardly observable from the market, and this is part of the motivation for us to introduce the current VMOT formulation. Let us recall that the main difference between MOT and VMOT lies in the marginal constraint, since in VMOT only the individual laws of and – the – are assumed to be known. Thus, there are now at least three unknown couplings in the VMOT problem whose structures are of major interest: the VMOT plan , and moreover the induced couplings and .

This paper is organized as follows. In section 2 we state and prove a more detailed version of Theorem 1.1 by applying PDA. In section 3 we prove the PDA, Theorem 1.2, using a compactness result whose proof is given in an appendix. Section 4 presents further results on the structure of VMOT and optimality of induced couplings.

2. Extremal correlation of martingales – Theorem 1.1

In this section, we state and prove Theorem 2.1 which is a more precise and extended version of Theorem 1.1. We will prove it here by assuming Theorem 1.2. Let us introduce some terminology. A norm on is called strictly convex if its unit ball is strictly convex, i.e. every boundary point of is an extreme point of . Euclidean norm clearly belongs to this class. For a set , is the convex hull of , and for a convex set , is the set of extreme points of . For a measure , the support of , denoted by , is the smallest closed set on which has its full mass. For measures , there exists a unique largest measure (called the common mass of ) which is dominated by and , i.e. , , where means for every measurable . When are given by densities respectively, is given by the density . means is absolutely continuous w.r.t. the Lebesgue measure on , that is has a density function.

Theorem 2.1.

Let be pairs of probability measures on in convex order, and for all . Let where the norm is strictly convex and is differentiable on . Let be any minimizer for (1.2) where , .

-

(1)

If , then the support of coincides with the extreme points of the convex hull of itself:

-

(2)

If , we have where , meaning that the common marginal stays put under , or the minimizer does not move the mass of . Let and disintegrate as . Then

Observe is a martingale transport from to , and . Since is an identity transport, we conclude that by minimizing , we get

and moreover the latter will be the case for – a.e. .

We remark that [38], [39] studied the structure of MOT w.r.t. in the single-martingale setup, and later [5] rediscovered part of their results from a different approach. Theorem 2.1 may be viewed as a generalization of e.g. [5, Theorem 7.3, Theorem 7.4] to the multiple martingales setup, showing that the martingales given marginals are correlated in an extremal way to achieve the optimum.

Proof.

Step 1. Let us tentatively assume that are irreducible for every . This assumption will be removed in the last step. Then by Theorem 1.2 we have a PDM , that is, by denoting , and , we have

| (2.1) | ||||

| (2.2) |

Recall that in Theorem 1.2, (2.2) is attained as real-valued, yielding is finite -a.s. and finite -a.s.. In this step we shall obtain a differential identity (2.13).

To this end, recall the martingale Legendre transform of is a pair of functions defined as in [32, Definition 3.1]:

| (2.3) | ||||

| (2.4) |

In general is a convex set-valued (possibly empty, but see (2.5) below) function and we may choose a -valued function . Observe that if we define to be the convex envelope of , then is an affine tangent function to at . Now recall that is called irreducible if is connected open and . Set to be an open rectangle. Now (2.3) gives , thus

and equality holds throughout (as real-valued) - a.s.. The fact finite -a.s. then yields . With this and the fact that is Lipschitz, [32, Theorem 3.2] yields the following local regularity:

| (2.5) |

We wish to attain Lipschitz property, so we will take the Legendre transform of with respect to to obtain such property. But as is in general only locally Lipschitz, let us take the transform locally as follows: write and for , let and . Now define successively for by

| (2.6) |

Since is (globally) Lipschitz in (because is locally Lipschitz in ), (2.6) implies that is Lipschitz in , and

Let be the restriction of on , let , and let be the one-dimensional marginals of . As yields , each is differentiable -a.e.. Hence

| (2.7) |

Now because , we have

| (2.8) | ||||

| (2.9) |

We may rewrite (2.9) as

| (2.10) |

Fix at which (2.10) holds and is differentiable. Let be the subspace of spanned by the set (translation of by ). If dim then it simply means and there is nothing to prove. Thus let us assume that dim . Now [32, Lemma 4.1] showed that, if (2.8), (2.10) hold, then

| (2.11) |

where is the orthogonal projection of the -valued function on . While a proof can be found in [32], here let us give some intuition: in (2.8) the function is bounded above by , but (2.10) tells us that the function is in fact tightly bounded by for - a.e. . The facts has barycenter at and the functions and are differentiable at implies that has not much room to vary wildly near in , yielding it is forced to be differentiable at in .

Next, note that (2.8), (2.10) imply for

| (2.12) | ||||

and notice by continuity of , (2.12) holds for every . Then from (2.7), (2.11), we deduce that for any nonzero vector in , by taking -directional derivative in at , it holds that for any ,

| (2.13) |

From this identity [32] proved the theorem when the cost is given by the Euclidean norm. We will follow a similar line but as we deal with more general strictly convex norms, we shall need a more involved argument.

Step 2. We shall prove the “non-staying” property of the common mass in the case ( by irreducibility) and the “staying” property in the case for the minimization problem in (1.2).

For , (2.12) immediately implies for every at which is differentiable, thus -a.s., (which we call the non-staying property of the minimizer ) by the following reason: if , then the function must attain its maximum at by (2.12). But notice that due to the increase of the function will strictly increase as moves away from along any direction satisfying at , a contradiction. Notice we have shown that if and a PDM exists, then for , whenever exists at .

Next, the staying property for the case refers to the statement as stated in the theorem. This property was proved in e.g. [5, Theorem 7.4] for one dimensional case and then generalized in [43, Theorem 2.3] for general dimension in the MOT setup, but note that a solution of MMOT is also a solution of MOT between its own marginals and . Both [5], [43] assumed , but we note the same proof works for any strictly convex norm cost. From the staying property, the study of the geometry of is now reduced to the study of . Note that has no mass on the diagonal and must solve the VMOT problem with respect to its own one-dimensional marginals.

Step 3. By Step 2 we can assume has no mass at . Under this assumption we will show is contained in the set of extreme points of . To this end, first we will show that is contained in the boundary of , where the boundary refers to the topology of and not of . Suppose on the contrary . Then we can find a point and a subset such that is a convex combination of these, i.e.,

| (2.14) |

Then due to the linearity of , from (2.13) we deduce

| (2.15) |

Using this, we will show that

| (2.16) | the points lie on a ray emanating from . |

To see this, take , let , and let be the infinite line containing . Thanks to the strict convexity of , we will firstly show that for any , where refers to the -directional derivative w.r.t. the variable. To see this, we consider the following function on

The claim reads . Note , so

Notice , for and for since the norm is strictly convex and . Also notice is convex, hence , showing the claim in this case. Now if with and not on the same side of , then for small , so that again and . Finally if with and on the same side of , then and . With (2.15) this clearly yields (2.16). Finally, a similar argument yields (2.16) for the cost .

Now if dim , we can choose such that they are not aligned meanwhile (2.14) holds. But (2.16) then forces them to be aligned, a contradiction. If dim then since is centered at , we can choose in the opposite direction with respect to , i.e. . Also by (2.14). Then again (2.16) cannot hold, a contradiction. This yields . Now if , then again we can find such that (2.14) holds. Then by the above argument we deduce (2.16), a contradiction to the fact that , since a ray emanating from an interior point of a convex set can intersect with its boundary at one point only. Hence we get , and as the reverse inclusion is clear, we conclude . Notice this proves the theorem for , the restriction of on in Step 1. Finally, letting for the domain completes the proof of Theorem 2.1 for any irreducible pair of marginals .

Step 4. We will prove the theorem for each pair of marginals only in convex order and not necessarily irreducible. It is well known that any convex-ordered pair can be decomposed as at most countably many irreducible pairs, and the decomposition is uniquely determined by the potential functions . While more details can be found in [5], [7], we provide the statement for reader’s convenience.

[7, Proposition 2.3] For each , let be the open components of the open set in , where . Let and for , so that . Then there exists a unique decomposition such that

Moreover, any admits a unique decomposition

such that for all .

Note that must be the identity transport (i.e. is concentrated on the diagonal ) since it is a martingale and . There is no randomness in . Now for the rest of the proof we will assume to avoid notational difficulty, but one may observe the same argument works for any just with some notational challenge.

Let be a minimizer in (1.2) and let , be the unique decomposition of respectively. Then our domain is decomposed as accordingly. Now the strategy is to study the geometry of on each domain .

Let be the restriction of on . If and , then and are both irreducible and in this case we already established the theorem. On the other extreme, that is if and , then as mentioned above there is no randomness in , that is where is a coupling of and . Hence represents an identity transport, and thus the theorem obviously holds in this case.

The remaining case is and . Write for simplicity and recall that where , , and , are jointly martingales. Let and , so that is a coupling of martingales and . But since we have , thus the cost is simplified as follows:

where is the restriction of the norm on the second coordinate axis in . Hence we have and this implies is an optimizer in VMT with respect to . Now by the irreducibility of Step 3 already established the theorem for , hence the theorem also holds for as is merely an identity transport. This completes the proof of the theorem. ∎

We end this section with some examples that illustrate Theorem 2.1.

Example 2.2.

We give a maximizer for (1.2) with . As [32] observed, the inequality may be rewritten as

| (2.17) |

Fix any probability measure . Choose a family of probabilities on such that and where is the unit sphere in centered at . Now define a martingale measure by . Then is a maximizer in , where and are the one-dimensional marginals induced by . The optimality of follows from the fact that while the integration of the left hand side of (2.17) by any is a constant, the inequality (2.17) becomes an equality precisely on the set , and moreover .

Example 2.3.

We shall construct a minimizer for (1.2) with . Denote by the Lebesgue measure restricted on a set . Let , , . Recall that the projection of any element in on the “first martingale space” belongs to , that is, if then . This implies , where is the primal value of the one-dimensional MOT problem

| (2.18) |

simply because . It is well known (see e.g. [5, Theorem 7.4]) that the solution to (2.18), say , is unique and there exist functions , such that

This means that the martingale splits the mass at each in onto three points . Since the identity transport has no contribution to the cost (2.18), we see that

| (2.19) |

Now let us construct a minimizer . For each define a kernel by

Note that splits mass at toward four directions – west, east, south and north. Now let be any coupling of , and define . Then notice that , and moreover by (2.19), we have . Therefore, is a minimizer.

The next example shows the strict convexity of the norm assumption cannot be omitted in Theorem 2.1.

Example 2.4.

Strict convexity of the norm is necessary for the extremal structure of VMOT. For an example, let , , , , . Observe every leads to the same cost where (note is a singleton). Now clearly there are elements in which do not satisfy Theorem 2.1, for example one may take where is independent of and its kernel are dispersed onto .

3. Existence of dual optimizers for VMOT – Theorem 1.2

One of the most important results for the proof of Theorem 1.2 is Proposition 3.1, a compactness property of a class of convex functions.

Recall two probabilities in convex order is irreducible if is connected and ; see [7, Section 2]. In this case, is called the domain of where is the smallest interval satisfying , that is, is the union of and any endpoints of that are atoms of , and moreover, . Note that is irreducible if and only if for every and , we have

| (3.1) | where . |

In other words, is irreducible if and only if for any , every must “cut across” the point . This follows directly from the definition of potential functions and Jensen’s inequality.

For irreducible pairs with domains , let us define , and , .

Proposition 3.1.

Let be irreducible pairs of probabilities with domains . Let , . Consider the following class of functions where every satisfies the following:

-

(1)

is a real-valued convex function on ,

-

(2)

and ,

-

(3)

.

Then is locally bounded in the following sense: for each compact subset of , there exists such that on for every . Moreover, for any sequence in there exists a subsequence of and a real-valued convex function on such that for every , and the convergence is uniform on every compact subset of .

We note that the proposition for the case was proved in [7]. In this section we prove Theorem 1.2 while assuming Proposition 3.1, whose proof will then be given in an appendix. During the proof the bounding constant may vary, but observe it does not depend on .

Proof.

Step 1. The assumption for continuous , ensures as in (1.5) (for a proof, see e.g. [58]). Moreover, it is obvious that a dual optimizer exists for iff so does for . Hence by replacing with , from now on we will assume that .

As , we can find an “approximating dual maximizer” which consist of real-valued continuous functions , , and continuous bounded for every and , such that the following weak duality holds:

| (3.2) | ||||

| (3.3) |

Denote , , . By taking supremum over in (3.2), we get

| (3.4) |

Notice is a convex function on , and by definition of , we see

| (3.5) |

In this step we shall obtain local uniform boundedness of (3.8). Let be fixed. By subtracting an appropriate linear function from (3.2), that is by replacing with , with and with , we can assume

| (3.6) |

Next, observe (3.5) gives

where the second inequality is due to the convexity of and . Then by (3.3), there exists a constant such that

| (3.7) |

Let be a positive decreasing sequence tending to zero as , and write where . Then we define the compact interval for and as

Thus for example, if and , then . Let be small so that , for every . Notice . Let . Then by Proposition 3.1, there exists such that

| (3.8) |

Step 2. Let be an approximating dual maximizer. We want to show pointwise convergence of and , i.e. for -a.e. and for -a.e. as . However, in establishing the convergence we see that there is an immediate obstacle when , that is, in the duality formulation (3.2) one can always replace by for any constants satisfying and similarly replace by . This means the convergence cannot be shown for any approximating dual maximizer. In this step we will show there exists an approximating dual maximizer which satisfies the convergence.

Take an approximating dual maximizer . Observe

where the third inequality is by convexity of and . For each , let be the restriction of on then normalized to be a probability measure. Let , so that . Define

Let us fix . We claim that

To see this, recall is bounded and so by (3.8),

The constant may depend on but not on . From this and Jensen,

| (3.9) |

Next, note that as on , by taking supremum we see that

and note that obviously , so in particular

Define and observe

This implies that is bounded, and then by (3.9), is bounded. The claim is proved.

We are now ready to apply the Komlós lemma, which states that every -bounded sequence of real functions contains a subsequence such that the arithmetic means of all its subsequences converge pointwise almost everywhere. Define , and for . Observe that by repeated use of Komlós lemma, for every and , we can find a subsequence of such that

-

(1)

is a further susequence of , and

-

(2)

converges for - a.e. as ,

where . Select the diagonal sequence and again define for , , and , , and for . We finally claim that

| (3.10) |

The point is that the dependence on is now removed. To see this, as is a subsequence of for every , by Komlós lemma

| (3.11) |

In particular, both and converge for - a.e. as , hence their difference must converge for any fixed . With (3.11) this implies (3.10).

Now having an approximating dual maximizer where followed the same subsequence as did (and noting that (3.2) and (3.3) are conserved while taking convex combinations), we can repeat the same procedure for by starting from the uniform bound so that we get a further subsequence for which similar statement as in (3.10) holds for as well. Then a final application of Komlós lemma (recall ) yields an approximating dual maximizer which satisfies the claimed convergence property.

Step 3. We’ve shown there exists a sequence of functions satisfying (3.2), (3.3) for each , and admitting the limit functions such that as , for - a.e. and for - a.e. . For convenience, define and to be the set of convergence points, that is , , and

Let , . Note that , , and moreover the interior of the convex hull of is , i.e. .

In this step we will show the convergence of defined in (3.4). Fix so that . As , we can find points in , say , such that for every and . Then in view of (3.5) we see that both and are uniformly bounded in , where is a subgradient of the convex function at . Hence by taking a subsequence, we can assume that and both converge. Now define the affine function and replace with , with and with . Then we get while the convergence property of is retained. And (3.7) and Proposition 3.1 yield on .

Step 4. We will show there exists a function such that

| (3.12) |

We may define on and on so that they are defined everywhere on . For a function defined on a subset of and bounded below by an affine function, let denote the convex envelope of . Define

| (3.13) |

Then any measurable choice satisfying will satisfy (3.12). To see this, we may argue similarly as [7]. Recall

If we define , then we have

In particular by taking , we get . Next, observe that since the of convex functions is convex, we have

Then by the convergence and the definition of , we get

Since and is real-valued on , for each the convex function is real-valued thus continuous in . The subdifferential is then nonempty, convex and compact for every . Hence we can choose a measurable function satisfying . Any such choice yields (3.12) as follows:

Step 5. We will show that for any function satisfying

| (3.14) |

(we know that such a function exists by Step 4), and for any minimizer for the problem (1.2), in fact we have

| (3.15) |

In other words, every minimizer is concentrated on the contact set

whenever is chosen to satisfy (3.14). This will complete the proof.

To begin, recall -a.s., -a.s., and on where is defined as (3.4) with being its limit. For any (not necessarily an optimizer), notice that by the assumption of Theorem 1.2. Now we claim:

First, let us observe how the claim implies (3.15). Let be any minimizer for (1.2) (note that this exists by the assumption on the cost). Then and . Now we deduce

hence equality holds throughout, and this implies (3.15).

If we have pointwise convergence then the claim would have been a simple consequence of Fatou’s lemma, but we do not know such a convergence a priori. But [7] suggested a clever idea to handle this case and let us carry out a similar scheme in the current setting.

Fix any and let , . Then as in Step 2 (but instead of ), by (3.3) and (3.5) we get

From this, as , , , by Fatou’s lemma we get

This allows us to proceed

To handle the last term, let , and let be a sequence of functions satisfying . Then we compute

since = . Notice that the last integrand is nonpositive. Thus by Fatou’s lemma,

for some which is a limit point of the bounded sequence . Finally, in the last line, the inner integral equals

This proves the claim, hence the theorem. ∎

Remark 3.2.

In Step 5 we deduced , for every . Is or ? Even in one-dimension and in a fairly mild situation such as is -Lipschitz and are irreducible and compactly supported, it can happen that neither nor , as shown by examples in [7]. We may extend the notion of generalized integral of the pair introduced in [7] to the VMOT setup via (compare with [7, Definition 4.7])

| (3.16) |

For this definition to be meaningful, it is desired that the right hand side would not depend on the choice of , since this will then allow us to write the left hand side as e.g. . Although this looks fairly plausible, we shall not pursue this point further in this paper.

4. Further results on the structure of VMOT

In this section, we present two more structural results for VMOT. Recall the proof of Theorem 2.1 was based on the differential identity

where is a VMOT and is a PDM. On the other hand, the next result shall be obtained via the differential identity in variable:

Theorem 4.1.

Assume the same as in Theorem 1.2. Let be a proper subset of and assume that is absolutely continuous with respect to Lebesgue measure for every . Suppose is semiconcave in in the following sense: there exists for all such that

Assume the following twist condition: for each and where , the mapping

| (4.1) |

whenever the derivatives exist. Then there exists a family of functions for each such that for any minimizer of (1.2), is concentrated on the graph of for -a.e. .

We note that the definition of semiconcavity here is so broad that there is no regularity imposed on other than that it be real-valued and measurable.

Proof.

The same assumption as in Theorem 1.2 ensures there is a PDM. By the semiconcavity on the cost, we can assume that is concave for every for which is a PDM, that is

and for any minimizer of the primal problem (1.2),

Consider the “inverse martingale Legendre transform” (see [32])

| (4.2) |

Notice is convex and . By replacing ’s with its Legendre transform ’s with respect to the “cost” , that is, defining successively for by

we find that are convex, and

where as usual. Let us define the contact set

Let us slightly refine as follows, and define its projections:

As for all and is convex, for any VMOT .

Now we claim that for any and ,

| (4.3) | ||||

| (4.4) |

Of course exists by definition of . Also from the definition

we see that the first equality in (4.4) holds since the supremum is attained at and both and are convex. Then in turn since the supremum in (4.2) is attained at and both and are convex, the second equality holds as well.

For each define the slice set , and for define the projection of to be the collection of those ’s with . Now by (4.4) and the twist condition (4.1), we see that if and , then we must have . This implies that we can define a function such that the set is contained in the graph of for every . Finally as , we have for -a.e. , completing the proof. ∎

Remark 4.2.

In Theorem 4.1 if one could obtain a dual maximizer where all ’s and are differentiable, then the family of maps could be directly obtained by the above differential identity in ; see the next example. But instead the semiconcavity was assumed in the theorem in order to deal with more general costs.

Example 4.3.

Set and , so that we consider the covariance maximization problem of . Let be a PDM. In this case we can assume that are convex, since we can replace by the following Legendre transform (and similarly for )

So are differentiable a.e., and the differential identity in reads

which represents the function in Theorem 4.1. Interestingly, even though has no dependence on , still depends on via the “trading strategy” . This is due to the randomness of and the martingale constraint . Note that if are nonrandom, then one can take and the function becomes the monotone map. Nonetheless, observe that even if are random, the dependence of the functions on is mild; for any given marginal , their graphs are merely translations in direction.

Theorem 2.1 and Theorem 4.1 discussed the optimal structure of for VMOT . Would and also have some optimality property? To discuss, recall (2.3), (3.13) where we defined to be the convex envelope of and set . Also recall is defined by (4.2). The following theorem shows the optimality of with respect to the costs respectively from a classical duality theorem of Kellerer [42].

Theorem 4.4.

Let be a minimizer for (1.2) and let be a dual maximizer. Then satisfy the following:

| (4.5) | ||||

| (4.6) |

Proof.

Example 4.5.

In Example 2.2 and 2.3, the optimality of did not imply any constrained structure on , since could be any coupling of there. In this example we shall see that for some data (i.e. cost and marginals), may have to be constrained. As in the previous example, let and .

It is well known that the monotone coupling, which is the coupling concentrated on an increasing graph, minimizes the cost (i.e. maximizes ) among all couplings of . But in our VMOT setting, the monotone coupling may not be feasible to be since we have to satisfy but there may not exist such a . Still, may try to be as close as possible to the monotone coupling, and this in turn may affect the structure of . We explore this phenomenon with explicit examples.

Firstly, as a toy model let the marginals be those in Example 2.3: , and let be a VMOT. As maximizing is equivalent to minimizing , it is better for to stay near the diagonal . With this simple data it is feasible for to be supported on , and since , this implies must also be supported on . This uniquely determines , and any martingale measure connecting is optimal. Thus a VMOT is nonunique but are unique.

For another example, let be arbitrary but fixed. The main goal is to build a VMOT such that its first marginal is the monotone coupling of arbitrarily given marginals . To this end, set , , so that . Now since is already convex in , the first derived cost appearing in Theorem 4.4 must be the same, i.e. . This implies , thus is the tangent plane to at . In this simple case, it is easy to see what the contact set is given by:

Now choose a martingale measure which satisfies that , for which its first induced coupling is the monotone coupling of . This implies there exist Kantorovich potentials such that

| (4.9) | ||||

| (4.10) |

Let be the one-dimensional marginals of . Then the fact and (4.9), (4.10) imply that is optimal in the class . Moreover, any optimal must satisfy since (4.9), (4.10) must hold for as well.

In this example the choices were made with no specific reason, and due to this the constructed there may not fit to a prescribed marginal data . Theorem 1.2 asserts that for any cost and irreducible marginal data one can obtain a dual optimizer such that the contact set (1.6) can accommodate all VMOTs. Moreover, we have illustrated that some careful analysis of the contact set can provide information on the structure of VMOTs, as shown in Theorem 2.1, 4.1.

Lastly, motivated by this example, we address the following question: what conditions on the data and cost shall impose on the induced optimal couplings , to have some specific structures, e.g. or has to lie on “small” sets? We leave this to future research.

Appendix A Compactness of the convex potentials

We prove Proposition 3.1 which we restate for reader’s convenience.

Proposition A.1.

Let be irreducible pairs of probabilities with domains . Let , . Consider the following class of functions where every satisfies the following:

-

(1)

is a real-valued convex function on ,

-

(2)

and ,

-

(3)

.

Then is locally bounded in the following sense: for each compact subset of , there exists such that on for every . Moreover, for any sequence in there exists a subsequence of and a real-valued convex function on such that for every , and the convergence is uniform on every compact subset of .

The following class of two-way martingales will also be used often.

Definition A.2.

(1) We define to be a simple martingale measure in such that is supported at a point (say ), and is supported at two distinct points (say ). Then necessarily , and can be written as

Then we define to be the set of all such simple martingale measures.

(2) Let be the set of martingale measures in such that any satisfies for –a.e. , where .

(3) We define .

Proof of Proposition A.1.

Step 1. In this step we will prove for the simplest marginal case where and there exists such that and , that is and . For , , define the open / closed transport rays

Suppose there is and such that , and for every . First, consider the case . Then it is trivial that there is a constant such that and for all , since . By convexity of , we find on for every , proving the theorem in this most simple case.

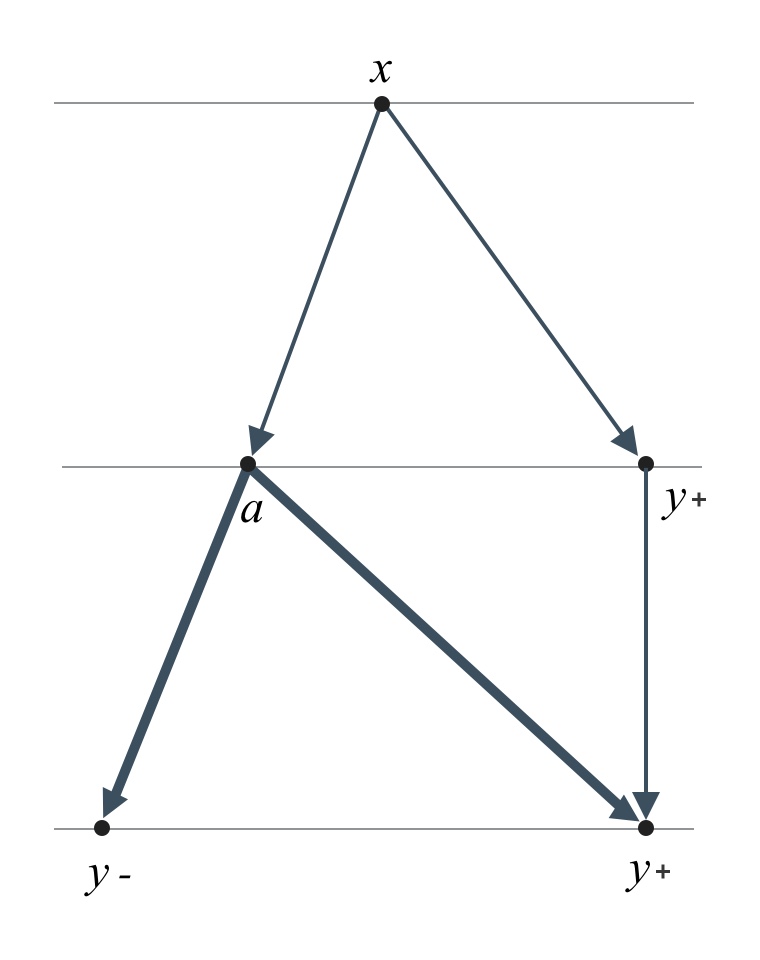

Next, consider the case that is away from , e.g. . The idea is to find probability measures where , and to find a small but positive constant (which does not depend on ) such that the martingale measure satisfies for some , i.e., for some martingale measure having marginals . If we can do so, then since is still a martingale, we infer from that we have . Then as , we are reduced to the previous case and the proposition follows. Now for this, we can simply take and . Since , clearly . Then notice we can take , implying ; see figure (1(a)).

We can describe this procedure in terms of Brownian motion and stopping time, namely, let denote a Brownian motion starting at , and define the stopping time . Then . Next, define and . Then as we have . Finally, define as the following: if then let , and if then let . We may define , but in this case simply because .

The case can be treated similarly and Step 1 is done.

Step 2. In this step we will prove for the case where are the marginals of a martingale measure of the form . Here , , and the family , is assumed to satisfy the following chain condition: if we let , , then

The chain condition immediately implies that is irreducible. As it is enough to prove this step with let us assume . Without loss of generality assume such that , and for every . Then since , by Step 1 we see that there exist such that for every

-

(1)

on , and

-

(2)

on , for any fixed .

may depend on but notice it does not depend on . Note that (1) follows from Step 1 and (2) follows from (1) and the fact that is convex. Now take small enough such that

Fix a point and take any . Let be an affine function which supports the convex function at , that is . Note that, by (1) and (2), and are bounded independently of . Let . Then , and , hence by the observation (1), (2) and the Step 1 we deduce there exists

such that for every we have on . Generalization to arbitrary is immediate through the chain condition, and this completes Step 2.

Step 3. In this step we will prove for a general irreducible pair with domain but still in dimension . In this case, it is well-known that there exists a probability measure such that is absolutely continuous with respect to Lebesgue measure, , and is irreducible with the same domain . One way to see this is the following: consider , the potential functions of . They coincide outside of while in by irreducibility. Select a convex function such that outside of while in . Then is taken to be the second derivative measure of , and by selecting sufficiently smooth one gets the desired absolute continuity.

Hence from now on we will assume without loss of generality that . Also note that we can assume since the pair is irreducible with domain and . Thus, we will assume and .

Our strategy is to reduce this situation to Step 1 and Step 2. For this, we begin by choosing a martingale measure . We can obtain such a by solving the MOT problem w.r.t. the cost [38], [39], [5]. Let , be two functions supporting , that is - a.e. .

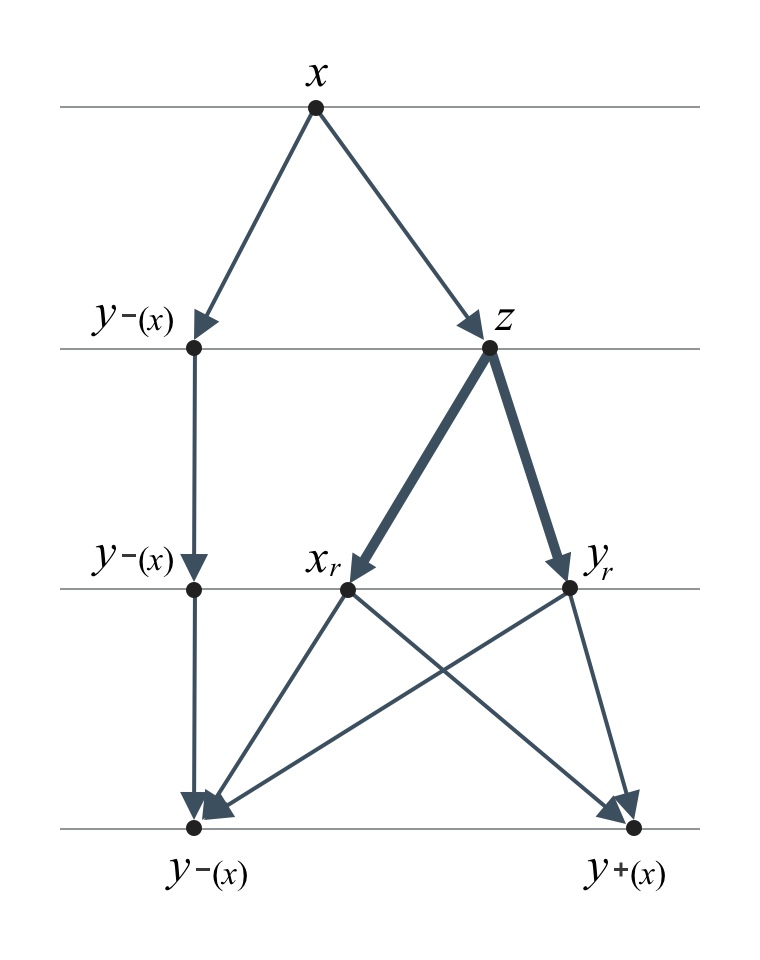

Now set such that and for any and , the restricted measure has strictly positive mass by the property of support. Pick and suppose . Fix and let be so small that . Now we claim the following: there exist positive measures satisfying , martingale measures , such that , and a positive constant such that the measure satisfies . Notice this yields as desired. See figure (1(b)).

To see this, note that the set has – positive measure since . For each , consider the martingale measure . Recall . Now we apply the same idea as in Step 1: Let and . Then define as follows: if then , and if then . Then clearly

| (A.1) |

With , satisfies

| (A.2) |

where is the joint law of and hence is a martingale measure with marginals , . Finally, set

Notice . We claim that the measure satisfies the desired property. To see this, consider the restricted measure where , . Define , . Then in view of (A.1) we have , and by (A.2) and we have for some , where is driven by the Brownian motion between times and for – a.e. .

In summary, we have shown that for any and and any sufficiently small , we can find where and martingale measures , such that , and a positive constant such that the measure satisfies . Now we make the following observation. Since , for any there exists such that , since otherwise we would have , contradicting to the irreducibility of . We choose such for each so that is an open cover of . Hence we can find a sequence such that is an open cover of , and if , , then for all , namely, the chain condition.

Now Step 2 implies that for each compact interval , there exists such that on for every , which is the content of the proposition when has no mass on the boundary of . To see this, observe that for a compact there is such that is an open cover of , so for small the shrunken covering still covers and satisfies the chain condition, hence Step 2 applies. This completes Step 3 for the case . Now the remaining case when assigns positive mass on the boundary of is simple. Write and suppose and . Recall that and is the graph of . Let . implies . Take any satisfying . Then the previous argument shows that for any and , we can find measures where , martingale measures , such that , and such that satisfies . Step 2 then yields for any , there exists such that on for every .

The case can be treated similarly, and finally note that if both and then we can conclude that

there exists such that on for every , because can be covered with finitely many appropriate intervals that we have discussed so far. The proof is therefore complete for the one-dimension case.

Step 4. In this step we will prove the local uniform bound for general . We will see how the ideas from the previous steps can be applied in the same way, but with more notational difficulty; this is why we take a different approach than [7] in establishing the local uniform bound of for in the previous steps.

Fix . As in Step 1, we begin with the most simple case where for each there is such that , , that is, and . Let , and . Note that the martingale measure has as its -dimensional marginals. Now we want to prove that there exists such that on for all , where is the convex hull of the support of . Notice that is a closed rectangle in and is the set of its vertices, consisting of points.

Suppose there is (where ) and such that , and for every . First, consider the case , where . Then just as in Step 1, it is then trivial that there is a constant such that on . Then by convexity of we get on for every , proving the proposition in this simple case. Next if , recall that in Step 1 we found such that and a constant such that the measure satisfies for some . Set , and . Then observe that implies . Since and , we are reduced to the previous case and the local uniform bound follows.

Now notice we can carry out Step 2 and 3 in this higher dimension case exactly the same way, that is, we can find a countable rectangular martingale measures (say ) which covers and satisfies the appropriate chain condition. We saw in Step 2 that the boundedness property of on each interval can propagate along such a chain, and the argument works the same way in higher dimension, simply observing that the intersecting intervals in Step 2 are now replaced by intersecting chain of rectangles. Moreover if some marginal measures assign positive mass on the boundary of , then observe that the rectangles can cover up to such boundaries so that we get the desired boundedness of all up to the boundary. This completes the proof of the local boundedness.

Step 5. It remains to prove the convergence property, and it is a direct consequence of the local bound and an application of Arzelà-Ascoli theorem, as follows: we have shown that every is uniformly bounded on any compact subset of , so with convexity of and , we deduce that the derivative of every is also uniformly bounded on any compact subset of . Hence by Arzelà-Ascoli theorem we deduce that for any sequence in and any compact set in , there exists a subsequence of that converges uniformly on . Now by increasing to and using diagonal argument, we can find a further subsequence of that converges pointwise in , and moreover, the convergence is uniform on every compact subset of .

We can deal with the convergence on the same way and let us explain in dimension to avoid notational difficulty. Suppose, for example, , , and . First of all, at the corner point the sequence is bounded, so we can choose a subsequence which converges at . Next, on any compact interval in the open line the sequence is also uniformly bounded, so by Arzelà-Ascoli theorem with diagonal selection again we can find a further subsequence which converges everywhere on . Finally, we can find a further subsequence which converges on , and hence the sequence converges everywhere on . This completes the proof of Proposition A.1. ∎

References

- [1] L. Ambrosio, B. Kirchheim, and A. Pratelli. Existence of optimal transport maps for crystalline norms. Duke Mathematical Journal. Volume 125, Number 2 (2004) 207–241.

- [2] L. Ambrosio and A. Pratelli. Existence and stability results in the theory of optimal transportation. Optimal transportation and applications. Springer Berlin Heidelberg., Volume 1813 of the series Lecture Notes in Mathematics (2003) 123–160.

- [3] M. Beiglböck, A.M.G. Cox, and M. Huesmann. Optimal transport and Skorokhod embedding. Invent. Math., 208 (2017) 327–400.

- [4] M. Beiglböck, P. Henry-Labordère, and F. Penkner. Model-independent bounds for option prices: a mass transport approach. Finance and Stochastics, 17 (2013) 477–501.

- [5] M. Beiglböck and N. Juillet. On a problem of optimal transport under marginal martingale constraints. Ann. Probab., 44(1) (2016) 42–106.

- [6] M. Beiglböck, T. Lim and J. Obłój. Dual attainment for the martingale transport problem. Bernoulli. 25 (2019), no. 3, 1640–1658.

- [7] M. Beiglböck, M. Nutz and N. Touzi. Complete duality for martingale optimal transport on the line. Ann. Probab., 45(5) (2017) 3038–3074.

- [8] S. Bianchini and F. Cavalletti. The Monge Problem for Distance Cost in Geodesic Spaces. Comm. Math. Phys., Volume 318, Issue 3 (2013) 615–673.

- [9] D.T. Breeden and R.H. Litzenberger. Prices of state-contingent claims implicit in option prices. J. Business, 51(4):621–651 (1978).

- [10] Y. Brenier. Polar factorization and monotone rearrangement of vector-valued functions. Comm. Pure Appl. Math., Volume 44, Issue 4 (1991) 375–417.

- [11] L.A. Caffarelli, M. Feldman, and R. J. McCann. Constructing optimal maps for Monge’s transport problem as a limit of strictly convex costs. J. Amer. Math. Soc., 15 (2002) 1–26.

- [12] G. Carlier, V. Chernozhukov and A. Galichon. Vector quantile regression: an optimal transport approach. The Annals of Statistics, 2016, Vol. 44, No. 3, 1165–1192.

- [13] L. Carraro, N.E. Karoui and J. Obłój. On Azéma-Yor processes, their optimal properties and the Bachelier-drawdown equation. Ann. Probab., Volume 40, Number 1 (2012) 372–400.

- [14] T. Champion and L. De Pascale. The Monge problem for strictly convex norms in . Journal of the European Mathematical Society., 12(6) (2010) 1355–1369.

- [15] T. Champion and L. De Pascale. The Monge problem in . Duke Mathematical Journal., Volume 157, Number 3 (2011) 551–572.

- [16] V. Chernozhukov, I. Fernandez-Val and A. Galichon. Quantile and Probability Curves without Crossing. Econometrica 78(3), pp. 1093–1125 (2010).

- [17] V. Chernozhukov, A. Galichon, M. Hallin, and M. Henry. Monge-Kantorovich depth, quantiles, ranks and signs. The Annals of Statistics, 2017, Vol. 45, No. 1, 223–256.

- [18] V. Chernozhukov, A. Galichon, M. Henry, and B. Pass. Identification of hedonic equilibrium and nonseperable simultaneous equations. J. Political Econ., Volume 129, Number 3 (2021).

- [19] D. Cordero-Erausquin, R. J. McCann, and M. Schmuckenschläger. A Riemannian interpolation inequality á la Borell, Brascamp and Lieb. Invent. Math., 146, (2), (2001), 219–257.

- [20] D. Cordero-Erausquin, R. J. McCann, and M. Schmuckenschläger. Prékopa-Leindler type inequalities on Riemannian manifolds, Jacobi fields, and optimal transport. Ann. Fac. Sci. Toulouse Math., 6, (15), (2006), 613–635.

- [21] A.M.G. Cox, J. Obłój and N. Touzi. The Root solution to the multi-marginal embedding problem: an optimal stopping and time-reversal approach. Probab. Theory Related Fields. 173 (2019), no. 1-2, 211–259.

- [22] C. Decker, E.H. Lieb, R.J. McCann and B.K. Stephens. Unique equilibria and substitution effects in a stochastic model of the marriage market. J. Econom. Theory 148 (2013) 778–792.

- [23] H. De March. Local structure of multi-dimensional martingale optimal transport. arXiv preprint. https://arxiv.org/abs/1805.09469

- [24] H. De March. Quasi-sure duality for multi-dimensional martingale optimal transport. arXiv preprint. https://arxiv.org/abs/1805.01757

- [25] H. De March and N. Touzi. Irreducible convex paving for decomposition of multidimensional martingale transport plans. Ann. Probab. 47 (2019), No. 3, 1726–1774.

- [26] Y. Dolinsky and H.M. Soner. Martingale optimal transport and robust hedging in continuous time. Probab. Theory Relat. Fields., 160 (2014) 391–427.

- [27] S. Eckstein, G. Guo, T. Lim, and J. Obłój. Robust Pricing and Hedging of Options on Multiple Assets and Its Numerics. SIAM J. Financial Math., 12 (2021), no. 1, 158–188.

- [28] L.C. Evans. Partial differential equations and Monge-Kantorovich mass transfer. Current Developments in Mathematics., (1997) International Press.

- [29] A. Figalli,Y-H Kim and R.J. McCann. When is multidimensional screening a convex program? J. Econom. Theory 146 (2011) 454–478.

- [30] A. Galichon, P. Henry-Labordère, and N. Touzi. A Stochastic Control Approach to No-Arbitrage Bounds Given Marginals, with an Application to Lookback Options. Annals of Applied Probability., Volume 24, Number 1 (2014) 312–336.

- [31] W. Gangbo and R.J. McCann. The geometry of optimal transportation. Acta Math., Volume 177, Issue 2 (1996) 113–161.

- [32] N. Ghoussoub, Y-H. Kim, and T. Lim. Structure of optimal martingale transport plans in general dimensions. Ann. Probab. 47(1): 109–164 (2019).

- [33] N. Ghoussoub, Y-H. Kim, and T. Lim. Optimal Brownian stopping when the source and target are radially symmetric distributions. SIAM J. Control Optim. 58 (2020), no. 5, 2765–2789.

- [34] G. Guo, X. Tan and N. Touzi. On the monotonicity principle of optimal Skorokhod embedding problem. SIAM J. Control Optim., 54-5 (2016) 2478–2489.

- [35] G. Guo, X. Tan and N. Touzi. Optimal Skorokhod embedding under finitely-many marginal constraints. SIAM J. Control Optim., 54-4 (2016) 2174–2201.

- [36] D. Hobson. Robust hedging of the lookback option. Finance and Stochastics., 2 (1998) 329–347.

- [37] D. Hobson. The Skorokhod embedding problem and model-independent bounds for option prices. In Paris-Princeton Lectures on Mathematical Finance 2010, volume 2003 of Lecture Notes in Math., Springer, Berlin (2011) 267–318.

- [38] D. Hobson and M. Klimmek. Robust price bounds for the forward starting straddle. Finance and Stochastics., Volume 19, Issue 1 (2014) 189–214.

- [39] D. Hobson and A. Neuberger. Robust bounds for forward start options. Mathematical Finance., Volume 22, Issue 1 (2012) 31–56.

- [40] L. V. Kantorovich. On the transfer of masses. Dokl. Akad. Nauk., SSSR 37 (1942) 227–229 (Russian).

- [41] L. V. Kantorovich. On a problem of Monge. Uspekhi Mat. Nauk., 3 (1948) 225–226.

- [42] H. Kellerer. Duality theorems for marginal problems. Z. Wahrsch. Verw. Gebiete., 67(4) (1984) 399–432.

- [43] T. Lim. Optimal martingale transport between radially symmetric marginals in general dimensions. Stochastic Processes and their Applications. Volume 130, Issue 4 (2020) 1897–1912.

- [44] X. N. Ma, N. S. Trudinger, and X. J. Wang. Regularity of potential functions of the optimal transportation problem. Arch. Ration. Mech. Anal., 177 (2005) no. 2, 151–183.

- [45] R. J. McCann. A convexity principle for interacting gases. Adv. Math., 128, 153–179 (1997).

- [46] G. Monge. Mémoire sur la théorie des déblais et des remblais. Histoire de l’académie Royale des Sciences de Paris (1781).

- [47] J. Obłój. The Skorokhod embedding problem and its offspring. Probability Surveys, 1 (2004) 321–392.

- [48] J. Obłój and P. Siorpaes. Structure of martingale transports in finite dimensions. arXiv preprint. https://arxiv.org/abs/1702.08433

- [49] J. Obłój and P. Spoida. An iterated Azéma-Yor type embedding for finitely many marginals. Ann. Probab., 45(4): 2210–2247 (2017).

- [50] B. Pass. Convexity and multi-dimensional screening for spaces with different dimensions. J. Econom. Theory. 147 (2012) 2399–2418.

- [51] R.T. Rockafellar. Characterization of the subdifferentials of convex functions. Pacific J. Math, 17 (1966) 497–510.

- [52] L. Rüschendorf. Construction of multivariate distributions with marginals Given. Annals of the Institute of Statistical Mathematics., 37 (1), (1985) 225–233.

- [53] F. Santambrogio. Optimal transport for applied mathematicians. Calculus of variations, PDEs, and modeling. Progress in Nonlinear Differential Equations and their Applications, 87 Birkhuser/Springer, Cham, (2015)

- [54] V. Strassen. The existence of probability measures with given marginals. Ann. Math. Statist., 36 (1965) 423-439.

- [55] N. S. Trudinger and X. J. Wang. On strict convexity and continuous differentiability of potential functions in optimal transportation. Arch. Ration. Mech. Anal., 192 (2009) no. 3, 403–418.

- [56] C. Villani. Topics in optimal transportation, Volume 58, Graduate Studies in Mathematics. American Mathematical Society, Providence, RI (2003).

- [57] C. Villani. Optimal Transport. Old and New, Vol. 338, Grundlehren der mathematischen Wissenschaften. Springer (2009).

- [58] D. Zaev. On the Monge-Kantorovich problem with additional linear constraints. Mathematical Notes., 98(5-6) (2015) 725–741.