Liquidity induced asset bubbles via flows of ELMMs

Francesca Biagini

Workgroup Financial and Insurance Mathematics, Department of Mathematics, Ludwig-Maximilians Universität, Theresienstraße 39, 80333 Munich, Germany. Emails: biagini@math.lmu.de, meyer-brandis@math.lmu.deAndrea Mazzon

Gran Sasso Science Institute, viale Francesco Crispi 7, 67100 L’Aquila, Italy. Email:

andrea.mazzon@gssi.infn.itThilo Meyer-Brandis11footnotemark: 1

Abstract

We consider a constructive model for asset price bubbles, where the market price is endogenously determined by the trading activity on the market and the fundamental price is exogenously given, as in [28]. To justify from a fundamental point of view, we embed this constructive approach in the martingale theory of bubbles, see [26] and [10], by showing the existence of a flow of equivalent martingale measures for , under which

equals the expectation of the discounted future cash flow.

As an application, we study bubble formation and evolution in a financial network.

Keywords: Bubbles, Equivalent martingale measures, Financial networks, Liquidity based model

1 Introduction

The formation of asset price bubbles has been thoroughly investigated from an economical point of view in many contributions, see Tirole [45], Allen and Gale [3], Choi and Douady [13], [14], Harrison and Kreps [22], Kaizoji [29], Earl et al. [18], DeLong, Shleifer, Summers and Waldmann [17], Scheinkman and Xiong [43], [44], Xiong [49], Abreu and Brunnermeier [1], Föllmer, Horst, and Kirman [20], Miller [35], Zhuk [50].

Different causes have been indicated as triggering factors for bubble birth, such as heterogenous beliefs between interacting agents (as in [20], [22], [43], [44], [49], [50]), a breakdown of the dynamic stability of the financial system ([13], [14]), the diffusion of new investment decision rules from a few expert investors to larger population of amateurs (see [18]), the tendency of traders to choose the same behavior as the other traders’ behavior as thoroughly as possible (see [29]), the presence of short-selling constraints (see [35]).

From the mathematical point of view, one of the main approaches is given by the martingale theory of bubbles as introduced by Cox and Hobson [16] and Loewenstein and Willard [30] and mainly developed by Jarrow, Protter et al. [23], [24], [25], [26], [27]. See Protter [41] for an overview.

In this setting a -bubble is defined as the difference between the market price of a given financial asset and its fundamental value, given by the expectation of the future cash flows under an equivalent local martingale measure .

Defined in this way, the bubble is a non-negative local martingale under , and it is strictly positive if and only if the market wealth is a strict -local martingale (for a complete analysis, see for example [10], [16], [25], [26], [30], [41]).

In a complete market (see [25]), where only one equivalent local martingale measure (ELMM) exists, only two possibilities are given: either no bubble appears at all, or a bubble is already present at the beginning. This is a strong modeling withdraw, therefore in [26] and [10] incomplete markets have been taken into consideration: the birth and the evolution of a bubble are then determined by a flow of different ELMMs that gives rise to a corresponding shifting perception of the fundamental value of the asset.

In [26] the underlying pricing measures may change only at certain stopping times, in [10] a continuous flow in the space of martingale measures is considered.

On the other hand, an alternative model is given by Jarrow, Protter and Roch in [28], where the fundamental value is exogenously given, whereas the market value is endogenously determined by the trading activity of investors, and studied through the analysis of the liquidity supply curve. For another constructive model, see also [9].

In this setting a bubble is still defined as the difference between the market value and the fundamental value , however it does not always coincide with the -bubble under a given equivalent martingale measure .

A natural question is then if it is possible to embed a constructive model, where the fundamental price is exogenous and the market price endogenous, in the martingale theory of bubbles, by determining a suitable flow of ELMMs for under which is justified from a fundamental point of view.

More precisely, given a liquidation time for the financial asset, we look for a flow of ELMMs for the market wealth such that

the fundamental value of the asset is given as the expectation of the future cash flow as in equation (3.1). Note however that we do not obtain that is also a (local) martingale under each measure of the flow, as thoroughly discussed in Remark 3.1.

Our main result is then that we can explicitly determine the form of such a flow of ELMMS in a liquidity driven model under very general assumptions, see Theorem 3.16. This require a consistent technical effort, mostly devoted to guarantee the martingale property of the chosen flows of (eventual) probability densities. In this way we are able to directly connect the impact of the underlying macro-economic factors to the shift of the resulting pricing measure, which may change over time.

As an application of our method, we consider the evolution of a bubble in a financial network and compute the generating flow of ELMMs. However, this example is also of independent interest, as it studies how the interaction of market participants in a financial network can affect asset price formation and the consequent birth of a bubble. Different studies show how contagion between investors and herding behavior may play an essential role when a bubble grows up: euphoria and exuberance can propagate among market participants, due to exchanges of ideas (see Lux [31]) or to the fact that investors may be attracted by the short period earnings of acquaintances investing in the bubbly asset, as observed by Bayer et al. in [8], where analyzing data from the housing bubble in L. A. in the 2000s the authors notice a strong contagion between neighbors.

Several contributions in the last years has been focusing on how some properties of the network, like mean degree or degree heterogeneity, can influence the contagion of failures and losses between banks during a financial crisis (see for example Acemoglu et al. [2], Allen and Gale [4], Amini et al. [5], Cont et al. [15], Gai and Kapadia [21], Newman et al. [37], Watts [46], Watts and Strogatz [47]). Some investigation has been proposed about how bubbles are generated at the microeconomic level by the interaction of market participants (see among others Lux [31], Scheinkman [43], Scheinkman and Xiong [44], Tirole [45], Zhuk [50]). However, only a few studies have been devoted to understand how the structure of a given financial network can influence the spread of contagion between investors that generates a bubble.

In [31], for example, the author models the bubble as caused by a self-organizing process of infection between traders, expressed by a system of PDEs, leading to equilibrium prices that deviate from the fundamental value. However they consider a world in which everybody is connected with everybody, so that the network structure does not enter into play.

In our special case we focus on a model for the aggregate trading volume of in dependence by some characteristics of the underlying networks of investors, such as the degree distribution.

In particular we use some modeling approach deriving from the literature on infectious processes in a population by following the so called SIS model (see Pastor-Satorras and Vespignani [38] and [39]).

We provide numerical simulations to investigate how different networks generate different contagion mechanisms and then to bubbles with different evolutions. In particular, it turns out that in more heterogenous networks (i.e. networks with a more right skewed degree distribution) contagion spread faster at the beginning so that the bubble builds up faster and bursts sooner: the nodes with high degree, which in average get infected faster, contribute with an higher weight in the more right skewed distributions.

The paper is therefore organized as follows: in Section 2 we describe the setting of the liquidity model, define the fundamental value of the asset and specify how the trading activity of investors influences the market price of the asset. In Section 3 we determine a possible flow of ELMMs satisfying (3.1) and show that the density process with is a true martingale wrt . In Section 4 we give an example showing how contagion between investors can develop the bubble in a network and compute the generating flow of ELMMs.

2 The Setting

Let be a probability space and a random time on it, representing the maturity or liquidation time of the underlying risky asset as in the setting of [26]. We assume that is endowed with a filtration satisfying the usual assumptions of completeness and right continuity.

On we have (), where , are standard -Brownian motions and is a jump process with totally inaccessible stopping time with intensity process . We assume that () are independent processes.

Following [28] we consider a financial asset whose fundamental wealth (associated to the cumulative dividend process and to the liquidation value of the asset at time ) is given by

(2.1)

with , and .

We interpret as the time of birth of a bubble for this financial asset.

The bubble follows the dynamics

(2.2)

where is the aggregate trading volume (buy market orders minus sell market orders), is the aggregate trading volume at and , are respectively a measure of illiquidity and the so called resiliency (for an economical motivation of this setting we refer to [28]). We put for a given .

We consider that satisfies the following dynamics

(2.3)

where and are progressively measurable processes that a priori can also depend on itself or on the bubble .

In [28] the aggregate trading volume is modeled as in (2.3) with and . Here we introduce the drift in order to

see the influence of the network on the size of the bubble, as we specify in Section 4.

Here the fundamental wealth process is exogenously given, while the market wealth process is endogenously determined as

At liquidation time we have : the asset is liquidated at time at the estimated firm’s value, i.e. at the fundamental value. In particular we require in the sequel that there exists an equivalent local martingale measure for only on the open interval , since around time the liquidation procedure is not subjected to market equilibrium mechanisms.

Assumption 2.1.

(i)

a.s.

(ii)

a.s. and a.s.

(iii)

and are such that there exists a unique solution of (2.3) (see for example Theorem 7 in Chapter V.3 in [40]);

(iv)

is an adapted process that satisfies the dynamics

where and are such that there exists a unique solution of (iv) according to Theorem 7 in Chapter V.3 in [40]. Moreover for every such that .

(v)

satisfies the dynamics

, with , that satisfy conditions Theorem 7 in Chapter V.3 in [40]. Furthermore , , , a.s., so that we obtain , a.s. for all .

(vi)

is bounded, i.e. a.s for all .

(vii)

is a bounded a.s. (possibly by a very large constant) -stopping time independent of such that a.s.

Notice that we assume and bounded a.s. for the sake of simplicity.

The following results still hold without these conditions by imposing some integrability conditions on . For example, it would be sufficient a.s., and a.s. for .

Remark 2.2.

Here we exclude that can depend on . However the following results also hold for the case , , , considered

in [28] to model the evolution of the bubble given by illiquidity effects.

We refer to [32] for more details in this case.

Proposition 2.3.

From the hypothesis on it follows that a.s. for all .

Proof.

Following the same argument as in [34], we have that

(2.4)

where is the local time at and the last equality follows by occupation time formula (see for example Corollary 1 in Chapter IV of [40]).

Then the integral is finite since, by the fact that a.s. for each , we have that the occupation time has compact support in . .

The bubble takes therefore the following explicit expression:

(2.5)

3 Flow of equivalent local martingale measures

Let be the space of equivalent local martingale measures for . Given , a -bubble is defined as

in the approach of [25] and [26]. In particular we have that the bubble introduced in (2.2) coincides with a -bubble if and only if

for some .

This is of course not possible in our setting. However we can find a flow such that

(3.1)

In this way the bubble described in (2.2) is the result of the shift in the pricing measure induced by the change in the macro-economic and financial conditions in the market.

Remark 3.1.

Note that (3.1) does not imply that is a martingale under . Eq. (3.1) holds -wise and in general it is not true that

for . Furthermore is an equivalent local martingale measure for only on .

We now explicitly compute a flow justifying the existence of the bubble in (2.2) from a fundamental point of view.

Let .

Then the density process of with respect to is given by

, where , , is a martingale strongly orthogonal to () and the processes , are such that for the following equality holds:

(3.2)

Since (3.2) does not involve , or , we put .

We can split (3.2) as

(3.3)

and

(3.4)

We look for a flow of the form

(3.5)

since (3.2) does not involve conditions on , and . In particular, we note that the laws of , and are invariant under this

change of measure.

If , and satisfy (3.3) and (3.4), the fundamental process under is given by

(3.6)

where denote the -standard Brownian motion given by

for .

To show the existence of the flow , we choose and so that the integrals inside the conditional expectation in (3.9) and (3.10) are zero almost surely. We show later on that a posteriori this choice ensures as well that (3.8) holds.

For , let

Notice that such is well defined since from Assumption 2.1 it holds , , a.s. for every .

With this choice we have on that

(3.11)

since by Assumption 2.1 the law of does not change under .

For define

Notice that from Assumption 2.1 and from the fact that the integral in (3.13) is bounded, we have that is finite and -measurable, and that moreover for all .

Proof.

From (3.7) and from the expressions of , and in (3.12)-(3.15) we have that

where is given in (3.13). Then from (3.6) it holds that under

where .

Thus we have

Then

Since is bounded and the first term is finite by Remark 3.2, it remains to prove

(3.16)

We have that

The first term is finite by Assumption 2.1 on and , whereas

Then (3.16) holds and we have the result.

We have therefore proved that, if we take , and as in (3.12)-(3.15), then

(3.3), (3.4) and (3.1) are satisfied.

From now on we denote for all , and for .

Note that we have not yet used the hypothesis on and of Assumption 2.1 to derive (3.5).

From now on we will need them to prove that is a true martingale for each , i.e. that each , , in (3.5) belongs to .

Remark 3.4.

By Assumption 2.1, as proved in Proposition 2.3, we exclude that the integral can explode in finite time. This is a difference with respect to [28], where the bubble bursts (i.e. ) at }.

In our model, however, the bubble can be zero, and also negative, even if the liquidity is not zero: by (2) it can be seen that this can happen when the drift of the aggregate trading volume becomes negative. In this approach, therefore, whether or not the bubble is positive depends more on the attitude of the investors than on the liquidity. In Section 4 we propose an example to show how contagion between traders in financial networks can determine the value of .

From now on, we fix .

We begin the analysis by noticing that, since ,

Let , be two positive stochastic processes such that a.s. , and let be of class 111A stochastic process is of class if, for each , is uniformly integrable.. Then is of class as well.

Proof. By Theorem 11 of Chapter I of [40] we have that a family of random variables is uniformly integrable if and only if there exists a function defined on , positive, increasing and convex, such that and

. Fix now , and call ,

and .

Since by hypothesis is uniformly integrable, there exists a function that satisfies the properties stated before. We have that

and then that

Thus

Therefore is uniformly integrable and is of class .

We have then the following

Proof. Since a local martingale is a true martingale if and only if it is of class , see Proposition 1.7 of Chapter IV of [42], we have that if is a true martingale then , being a martingale as well, is of class . Thus, by Lemma 3.5 and by (3.17), is of class , and therefore by Proposition 1.7 of Chapter IV of [42] it is a true martingale.

To prove that is a martingale we rely on some results provided by Mijatovic and Urusov [33] and by Wong and Heyde [48]. We first need some preliminaries.

Consider the state space , and a -valued diffusion on some filtered probability space, governed by the SDE

(3.18)

with , Brownian motion and deterministic functions and , that from now on we will simply denote by and , such that

(3.19)

and

(3.20)

where denotes the class of locally integrable functions on , i.e. the measurable functions that are integrable on compact subsets of .

Consider the stochastic exponential

(3.21)

with such that

(3.22)

and the auxiliary -valued diffusion governed by the SDE

(3.23)

where is a Brownian motion on some probability space .

Put and, fixing an arbitrary , define

(3.24)

(3.25)

(3.26)

(3.27)

Denote , , , , and analogously for and .

Recall that by Feller’s test for explosions exits its state space with positive probability at the boundary point if and only if

(3.28)

where .

Similarly, exits its state space with positive probability at the boundary point if and only if

(3.29)

where

Moreover, the endpoint of is said to be good if

Let the functions , , and satisfy conditions (3.19), (3.20) and (3.22), and let be a solution of the SDE (3.18).

Then the Doléans exponential given by (3.21) is a martingale for any if and only if both of the following requirements are satisfied:

(a)

condition (3.28) does not hold or conditions (3.30)-(3.31) hold;

(b)

condition (3.29) does not hold or conditions (3.32)-(3.33) hold.

We now obtain the following

Proposition 3.8.

Let be a geometric Brownian motion

(3.34)

where is a Brownian motion, and .

Then the process

is a martingale.

Proof. We show that the requirements of Theorem 3.7 hold for , with , and . Notice that , and satisfy conditions (3.19), (3.20) and (3.22) with . Then, taking for the functions (3.24)-(3.27) and first assuming , we have

(3.35)

(3.36)

(3.37)

(3.38)

with and where , , , is the incomplete Gamma function extended to all .

Notice that in (3.38) we have that

(3.39)

We obtain that:

•

in we have

thus condition (3.29) does not hold and the first requirement of (b) in Theorem 3.7 is fulfilled;

•

if we have

then condition (3.28) does not hold and the first requirement of (a) in Theorem 3.7 is fulfilled;

Therefore the second requirement of (a) in Theorem 3.7 is fulfilled.

So we have that if the requirements of Theorem 3.7 are satisfied, and thus is a martingale.

In the case , i.e. , we have that the process in (3.34) takes the form , . We can thus apply the results of Theorem 3.7 taking , , , and in (3.24)-(3.27). We have

(3.40)

where is the exponential integral function that satisfies and . Therefore and , then the first requirements of (a) and (b) of Theorem 3.7 are both satisfied and is a martingale.

Then we have immediately

To prove that Corollary 3.9 also implies that is a martingale, we extend the results of Wong and Heyde in [48].

To this purpose we consider a -progressively measurable -dimensional process of the form

(3.42)

where , is a -dimensional progressively measurable Brownian motion and are -dimensional stochastic processes independent of . Here the product between and is intended componentwise.

Define

with the convention that , and then

(3.43)

Then we have the following

Proposition 3.10.

Let be as in (3.42), and defined up to the explosion time in (3.43).

Then there also exists a -dimensional -progressively measurable process, with defined up to the explosion time with

where

such that the stochastic exponential with satisfies

Hence is a (true) martingale if and only if .

Proof. Since the proof is a long but easy extension of the result in [48], we omit it here and refer to [32].

where is the process associated to . By Corollary 3.9 and Proposition 3.10 it holds

(3.44)

We want to see that the integral of does not explode as well.

We have that

(3.45)

Define the stopping time

and notice that, since and are continuous, .

Define

If , we are done. Otherwise consider

Since for we have

it follows

for , which implies, together with (3.44), that does not explode before .

But after , up to , is

smaller than , hence on .

Repeating this argument up to , we obtain that is a martingale by Proposition 3.10.

We want now to prove that

(3.46)

with in (3.12) is a martingale as well.

We start with the following

Proposition 3.12.

Let be the bubble as in (2). Under Assumption 2.1, the Doléans exponential

is a martingale.

Proof. If we rewrite in the form (3.42), we obtain that

i.e. the process associated to in Proposition 3.10 is given by

(3.47)

We first prove that for each . We have a.s. for each by the hypothesis on and in Assumption 2.1 and by Proposition 2.3.

Thus by Theorem 2.4 of [34] and by the fact that is bounded, we obtain

(3.48)

for all , and then by the hypothesis on in Assumption 2.1, and again by Proposition 2.3, we have

By (3.48) and by Assumption 2.1 it follows that the stochastic integral in (3.47) does not explode before , so we have that for each .

We prove that this implies . By the expression of in (3.47) we have

(by the Kunita-Watanabe inequality)

(by the occupation time formula)

(3.49)

the first integral is finite because the local time has bounded support in , since does not explode before , and the second one

is finite by Assumption 2.1 and Proposition 2.3. Then the result follows by Proposition 3.10.

Let be the process associated to in Proposition 3.10, and the one associated to .

We have

and consequently, for ,

so that we can write

By Assumption 2.1 and by Proposition 2.3, with the same argument as in the proof of Proposition 3.12, we have that

Then, since by Proposition 3.12 we have , we obtain

(3.50)

Now call the process associated to in Proposition 3.10.

It holds

Then we have

where is given by

(3.51)

It follows that satisfies

and so that it takes the form

Since by Assumption 2.1 the process in (3.51) does not explode before , a.s. for each .

Thus, with the same argument as in the proof of Proposition 3.12 it can be proved that

Then by the integrability hypothesis on in (ii) of Assumption 2.1 it holds

The result then follows by Proposition 3.10 and by the fact that if is the process associated to it can easily seen that a.s. for each .

Proposition 3.14.

Consider and , with

(3.52)

and

(3.53)

where and are as in (3.15) and (3.12), and suppose that Assumption 2.1 holds.

Then and are true martingales.

The proof follows by Proposition 3.11, by Proposition 3.13 and by the following

Lemma 3.15.

Consider and , , where is a stochastic process such that the stochastic integral is well defined. Then

is a martingale if and only if is a martingale.

Proof. Theorem 4.1 in [11] states that, for a general continuous local martingale , is a martingale if and only if

where and , and . Since , this property hold for if and only of it holds for . Hence we have the result.

We are now ready to state the main result of the Section:

Theorem 3.16.

Under Assumption 2.1, defined in (3.5) belongs to for each .

Proof

The proof follows by the fact that taking and as in (3.15) and (3.12), with , , , and satisfying Assumption 2.1, then with

is a martingale with respect to time .

This follows immediately from Proposition 3.14: in (3.52) and in (3.53)

are martingales, so by Proposition 3.10 we know that and are such that the associated processes and defined in Proposition 3.10 do not explode before . Taking now , the associated process does not explode before as well, and this concludes the proof.

Remark 3.17.

Note that Theorem 3.16 also implies that , hence that our market model is arbitrage-free on .

4 Liquidity induced bubbles in a network

As an illustration of the previous results, we focus on a particular example. We note however that the results of this section are of independent interest since we provide one of the few contributions on mathematical modeling of bubbles in a network. For further results on this topic, we also refer to [7], where it is shown how bubbles can have an impact on the structure of a banking network, and to [12], where the authors describe the passage from a well-connected network with high global confidence to a poorly connected network with low global confidence, producing a boom and bust cycle. Our approach is however quite different: we consider a network of investors who may be influenced by the trading activity of their neighborhoods. Investors may place a buy market order on the bubbly asset because their neighborhoods in the network have bought the asset as well.

We model the trading contagion mechanism between agents taking place from time via the evolution dynamics of the aggregate trading volume.

Our analysis is based on some epidemiological studies, which describe how diseases spread in social networks, or how computer viruses spread from computer to computer. In particular, we focus on the SIS model, studied for example by Pastor-Satorras and Vespignani (see [38] and [39]) to analyze virus diffusion in a population.

The aggregate trading volume of an investor of degree in the network is given by the adapted stochastic process .

Put

(4.1)

We assume that

(4.2)

where is a continuous function representing the expected fraction of investors who are holding the asset (i.e. that have bought the asset and not already sold it), is the probability that an individual at the end of an edge has done a trade before or at time , is the rate of trading contagion and is the rate of selling. Furthermore and are continuous functions standing for the medium amount of asset traded per buyer and the medium amount of wealth of the investors, respectively.

Now we focus on the expression of . As stated by Pastor-Satorras and Vespignani [38], one could be tempted to impose , but this approximation can be too strong for networks with an highly inhomogeneous density, for example for networks with a power-law degree distribution.

In particular, by Bayes rule and since for any given node it holds

where is the number of nodes with degree , we have that

Therefore, as pointed out in [21] and [37], we have

(4.3)

where is the expected fraction of investors of degree that are holding the asset. Notice that, if the degree distribution is very peaked at the average degree so that we can approximate , for , then

, , and is a progressively measurable process such that

(4.8)

and . Furthermore we assume

(4.9)

Notice that from (4.7) and since a.s. for all and for all it follows and a.s. for all .

We are in the framework of Section 2, with

(4.10)

and

(4.11)

We have the following SDE for the bubble :

(4.12)

for , with explicit solution

(4.13)

Remark 4.1.

We now consider two different networks, in order to see how the characteristics of the network influence the dynamics of the expected fraction of buyers through . In the first one we have a connectivity distribution which is very peaked at the average value and decaying exponentially fast for and . Examples of this kind of networks are random graph models [19] and the small-world model of Watts and Strogatz [47]. In the second one the degree distribution is more right skewed, following for example a power law, as in the Barabási and Albert preferential attachment model [6]. From (4.6) and (4.7) we can see that the expected contagion between buyers will spread faster in the second kind of network, since the distribution puts more weight on the nodes with higher degree, resulting in a bigger value of in (4.7).

As we will notice in the next Section, the more right skewed is the degree distribution the faster the bubble will build up: this can be seen as an immediate influence of the network on

the bubble evolution.

Looking at (4.12) there are two opposite forces determining the drift: a negative contribution is given by the speed of decay , introduced in [28], whereas the term is strictly positive when the contagion effects determine the increase of the fraction of buyers.

When this last term will decay to zero or become negative, the drift will be negative as well: the bubble will revert to zero in expectation.

We conclude by showing that there exists a flow with Radon-Nykodim derivative process

(4.14)

such that

Taking , and in (3.15), (3.12) and (3.14) respectively we only need to show that that in (4.14) is in fact a martingale.

Proposition 4.2.

For each , is a -martingale.

Proof.

We show first that and in (4.10) and (4.11) satisfy Assumption 2.1.

Specifically,

by the integrability assumptions (4.9) and (4.8) on and , since .

Finally, by using Feller test it can be seen that the process does not hit the boundaries . Thus

follows by Theorem 2.4 of [34] and by the integrability assumption on .

The thesis follows by Theorem 3.16.

4.1 Numerical simulations

We now provide a numerical simulation to show how the evolution of the bubble depends on the structure of the network in our model. Specifically, we investigate how the connectivity and the degree heterogeneity of the underlying network influence the dynamics of the bubble. For this purpose, we simulate the dynamics of the bubble evolution specified in the model in (4.12),

by means of a Monte Carlo method with Euler scheme, taking for simplicity and constant.

To include the sudden burst of the bubble we change the dynamics at the moment when the bubble is not growing anymore: when the increase of the bubble stops, the market gets somehow scared, and then a sudden process of pessimistic feeling takes place, leading to the bubble burst that is commonly observed.

This has been simulated by increasing the value of and decreasing the value of in (4.12) when the bubble remains strictly below its maximum over a certain interval of time.

The illiquidity and the process are supposed to be a geometric Brownian motion, i.e. to satisfy

where and .

We compare two different cases, an Erdős-Rényi network with Poisson degree distribution

and a scale-free network with a power law distribution

(4.15)

The Erdős-Rényi network has a degree distribution which is very peaked around the mean degree , whereas the scale-free one, that is well known to better represent real world networks,

has a much larger right tale, which implies that a bigger number of nodes has a large number of neighbors.

We take two different values of in (4.15), i.e. and . obtaining therefore a more connected network (with ) and a less connected one (with ). We consider as well two Erdős-Rényi networks with and , respectively.

We simulate bubble evolution in these networks, considering the distribution up to a maximum

degree that corresponds to a network with nodes, see paragraph 3.3.2 of [36].

For each kind of network we analyze three main quantities:

•

the mean value of the maximum of the bubble;

•

the mean time at which the bubble reaches the maximum (and then it bursts);

•

the value of the bubble at a certain established time, chosen as : this is supposed to be an indicator of the speed at which the bubble

developes.

Simulating 10000 trajectories and taking , , , , , , , , , , , , and for all , we obtain the following results:

scale-free

scale-free

Erdős-Rényi

Erdős-Rényi

mean degree

max

pos max

Figure 1: Numerical results on bubble evolution in different networks.

One can notice that, as we were expecting, both the mean degree and the degree heterogeneity play a key role in the evolution of the bubble: in particular, both of them are positively correlated with

the steepness of the bubble increase during the ascending phase.

It can also be seen that in the Erdős-Rényi network, i.e. in the less right skewed one, the bubble reaches its maximum later in time: this seems to indicate that the degree heterogeneity leads

to a sooner burst of the bubble.

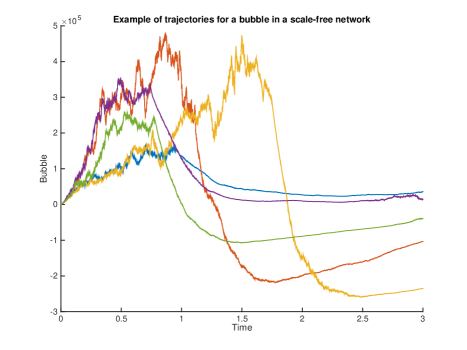

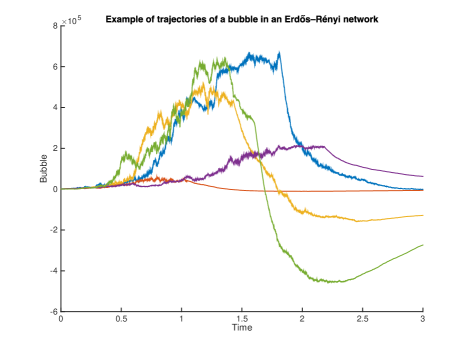

The difference in the evolution of the bubble in the two networks can also be seen in Figure 2 and Figure 3, which show five simulated trajectories of the bubble in the free-scale case and in the Erdős-Rényi case, for and respectively. Both the networks have the same mean degree .

In the scale-free network the bubble builds up faster: this is due to the fact that the distribution gives more weight with respect to the Poisson one

to the nodes with high degree, that are those that in expectation gets faster infected.

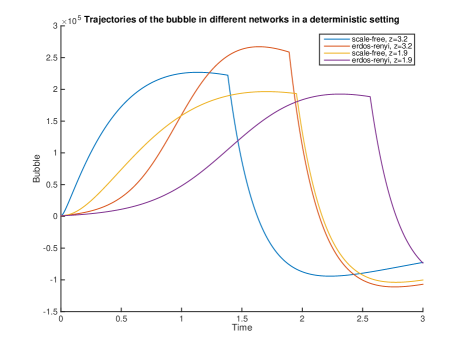

It is of interest to see the bubble behavior also in the deterministic case, i.e. when , and , see Figure 4. In the more connected and right skewed network the bubble builds up faster, and bursts faster as well. The greatest maximum is reached in the Erdős-Rényi network with , where the bubble builds up slower than in the scale-free network but it reaches a bigger value in average. As before, we see that also the connectivity

leads to a faster growth and to a sooner burst.

Abreu and Brunnermeier [2003]

D. Abreu and M.K. Brunnermeier.

Bubbles and crashes.

Econometrica, 71(1):173–204, 2003.

Acemoglu et al. [2012]

D. Acemoglu, V.M. Carvalho, A. Ozdaglar, and A. Tahbaz-Salehi.

The Network Origins of Aggregate Fluctuations.

Econometrica, 80(5):1977–2016, 2012.

Allen and Gale [2000a]

F. Allen and D. Gale.

Bubbles and crisis.

The Economic Journal, 110:236–255,

2000a.

Allen and Gale [2000b]

F. Allen and D. Gale.

Financial Contagion.

The Journal of Political Economy, 108(1):1–33, 2000b.

Amini et al. [2016]

H. Amini, R. Cont, and A. Minca.

Resilience to contagion in financial networks.

Mathematical Finance, 26(2):329–365,

2016.

Barabási and Albert [1999]

A.-L. Barabási and R. Albert.

Emergence of scaling in random networks.

Science, 286:509–512, 1999.

Battiston [2015]

P. Battiston.

Rational bubbles in closed economies.

2015.

Bayer et al. [2016]

P. Bayer, K. Mangum, and J.W. Roberts.

Speculative fever: Investor contagion in the housing bubble.

Technical report, National Bureau of Economic Research, 2016.

Biagini and Nedelcu [2015]

F. Biagini and S. Nedelcu.

The formation of financial bubbles in defaultable markets.

SIAM Journal of Financial Mathematics, 6(1):530–558, 2015.

Biagini et al. [2014]

F. Biagini, H. Föllmer, and S. Nedelcu.

Shifting martingale measures and the slow birth of a bubble.

Finance and Stochastics, 18(2):297–326,

2014.

Blei and Engelbert [2009]

S. Blei and H.-J. Engelbert.

On exponential local martingales associated with strong Markov

continuous local martingales.

Stochastic Process. Appl., 119(9):2859–2880, 2009.

Bouchard et al. [2015]

J.P. Bouchard, D. Challet, and J. da Gama Batista.

Sudden Trust Collapse in Networked Societies.

Eur Phys, 88(3):1–11, 2015.

Choi and Douady [2011a]

Y. Choi and R. Douady.

Financial Crisis and Contagion: A Dynamical Systems Approach.

2011a.

URL http://ssrn.com/abstract=1733706.

Choi and Douady [2011b]

Y. Choi and R. Douady.

Chaos and Bifurcation in 2007-08 Financial Crisis.

Management Science, 2011b.

Cont et al. [2013]

R. Cont, A. Moussa, and E.B. Santos.

Networks structure and systemic risk in banking systems.

Technical report, Handbook of Systemic Risk, Cambridge University

Press, 2013.

Cox and Hobson [2005]

A.M.G. Cox and D.G. Hobson.

Local martingales, bubbles and option prices.

Finance Stochastics, 9(4):477–492, 2005.

DeLong et al. [1990]

J.B. DeLong, A. Shleifer, L. Summers, and R. Waldmann.

Noise trader risk in financial markets.

Journal of Political Economy, 98(4):703–738, 1990.

Earl et al. [2007]

P.E. Earl, T-C Peng, and J. Potts.

Decision-rule cascades and the dynamics of speculative bubbles.

Journal of Economic Psychology, 28:351–364, 2007.

Erdős and Rényi [1960]

P. Erdős and A. Rényi.

On the evolution of random graphs.

Publication of the Mathematical Institute of the Hungarian

Academy of Science, 17-61, 1960.

Föllmer [2005]

H. Föllmer.

Equilibria in financial markets with heterogeneous agents: A

probabilistic perspective.

Journal of Mathematical Economics, 41(1-2):123–155, 2005.

Gai and Kapadia [2010]

P. Gai and S. Kapadia.

Contagion in financial networks.

Proceedings of the Royal Society, 466:2401–2423,

2010.

Harrison and Kreps [1978]

J.M. Harrison and D.M. Kreps.

Speculative investor behavior in a stock market with heterogeneous

expectations.

The Quarterly Journal of Economics, 92(2):323–336, 1978.

Jarrow and Protter [2009]

R. Jarrow and P. Protter.

Forward and futures prices with bubbles.

International Journal of Theoretical and Applied Finance,

12(7):901–924, 2009.

Jarrow and Protter [2011]

R. Jarrow and P. Protter.

Foreign currency bubbles.

Review of Derivatives Research, 14(1):67–83, 2011.

Jarrow et al. [2007]

R. Jarrow, P. Protter, and K. Shimbo.

Asset price bubbles in complete markets.

Advances in Mathematical Finance, In Honor of Dilip B.

Madan:105–130, 2007.

Jarrow et al. [2010]

R. Jarrow, P. Protter, and K. Shimbo.

Asset price bubbles in incomplete markets.

Mathematical Finance, 20(2):145–185, 2010.

Jarrow et al. [2011]

R. Jarrow, Y. Kchia, and P. Protter.

How to detect an asset bubble.

SIAM Journal on Financial Mathematics, 2:839–865,

2011.

Jarrow et al. [2012]

R. Jarrow, P. Protter, and A. Roch.

A Liquidity Based Model for Asset Price.

Quantitative Finance, 12(1):1339–1349,

2012.

Kaizoji [2000]

T. Kaizoji.

Speculative bubbles and crashes in stock markets: an

interacting-agent model of speculative activity.

Phisica A, 287:493–506, 2000.

Loewenstein and Willard [2000]

M. Loewenstein and G.A. Willard.

Rational equilibrium asset-pricing bubbles in continuous trading

models.

Journal of Economic Theory, 91(1):17–58, 2000.

Lux [1995]

T. Lux.

Herd behaviour, bubbles and crashes.

The Economic Journal, 105(431):881–896,

1995.

Mazzon [in preparation]

A. Mazzon.

Financial asset bubbles in networks.

PhD thesis, in preparation.

Mijatovic and Urusov [2012a]

A. Mijatovic and M. Urusov.

On the martingale property of certain local martingales.

Probability Theory and Related Fields, 152(1-2):1–30, 2012a.

Mijatovic and Urusov [2012b]

A. Mijatovic and M. Urusov.

Convergence of integral functionals of one-dimensional diffusions.

Electronic Communications in Probability, 17(61):1–13, 2012b.

Miller [1977]

E.M. Miller.

Risk, uncertainty, and divergence of opinion.

The Journal of Finance, 32(4):1151–1168,

1977.

Newman [2003]

M.E.J. Newman.

The structure and function of complex networks.

SIAM review, 45(2):167–256, 2003.

Newman et al. [2001]

M.E.J. Newman, S.H. Strogatz, and D.J. Watts.

Random graphs with arbitrary degree distributions and their

applications.

Physical review E, 64(2):026118, 2001.

Pastor-Satorras and

Vespignani [2001a]

R. Pastor-Satorras and A. Vespignani.

Epidemic dynamics and endemic states in complex networks.

Phys. Rev. E., 63(066117), 2001a.

Pastor-Satorras and

Vespignani [2001b]

R. Pastor-Satorras and A. Vespignani.

Epidemic spreading in scale-free networks.

Phys. Rev. Lett., 86:3200–3203, 2001b.

Protter [2005]

P. Protter.

Stochastic integration and differential equations, Second

Edition.

Springer-Verlag, Berlin, 2005.

Protter [2013]

P. Protter.

A mathematical theory of financial bubbles, volume 2081 of

Lecture Notes in Mathematics of V. Henderson and R. Sincar editors,

Paris-Princeton Lectures on Mathematical Finance.

Springer, 2013.

Revuz and Yor [1999]

D. Revuz and M. Yor.

Continuous Martingales and Brownian Motion, Third Edition.

Springer-Verlag, New York, 1999.

Scheinkman and Xiong [2003]

J. Scheinkman and W. Xiong.

Overconfidence and speculative bubbles.

Journal of political economy, 111(6):1183–1219, 2003.

Scheinkman and Xiong [2013]

J. Scheinkman and W. Xiong.

Speculation, trading and bubbles.

Economic Theory Center Research 050, Princeton University, 2013.

Tirole [1982]

J. Tirole.

On the possibility of speculation under rational expectations.

Econometrica, 53(6):1163–1182, 1982.

Watts [2002]

D. Watts.

A simple model of global cascades on random networks.

Proc. Natl Acad. Sci. USA, 99:5766–5771, 2002.

Watts and Strogatz [1998]

D.J. Watts and S.H. Strogatz.

Collective dynamics of ’small-world’ networks.

Nature, 393:440–442, 1998.

Wong and Heyde [2004]

B. Wong and C. Heyde.

On the martingale property of stochastic exponentials.

Journal of Applied Probability, 41(3):654–664, 2004.

Xiong [2012]

W. Xiong.

Bubbles, crises, and heterogeneous beliefs.

Technical report, Princeton University, Princeton, NJ, 2012.

Zhuk [2013]

S. Zhuk.

Speculative bubbles, information flow and real investment.

Information Flow and Real Investment, 2013.