PORTMANTEAU TESTS FOR ARMA MODELS WITH INFINITE VARIANCE

By J.-W. Lin AND A.I. McLeod

The University of Western Ontario

Jen-Wen Lin and A. Ian McLeod (2008).

Portmanteau Tests for ARMA Models with Infinite Variance.

Journal of Time Series Analysis, 29, 600-617

Abstract.

Autoregressive and moving-average (ARMA) models with stable Paretian

errors is one of the most studied models for time series with

infinite variance. Estimation methods for these models have been

studied by many researchers but the problem of diagnostic checking

fitted models has not been addressed. In this paper, we develop

portmanteau tests for checking randomness of a time series with

infinite variance and as a diagnostic tool for checking model

adequacy of fitted ARMA models. It is assumed that least-squares or

an asymptotically equivalent estimation method, such as Gaussian

maximum likelihood in the case of AR models, is used. And it is

assumed that the distribution of the innovations is IID stable

Paretian. It is seen via simulation that the proposed portmanteau

tests do not converge well to the corresponding limiting

distributions for practical series length so a Monte-Carlo test is

suggested. Simulation experiments show that the proposed test

procedure works effectively. Two illustrative applications to actual

data are provided to demonstrate that an incorrect conclusion may

result if the usual portmanteau test based on the finite variance

assumption is used.

Keywords. ARMA models, Infinite variance, Least squares

method, Portmanteau test, Residual autocorrelation function, Stable

Paretian distribution

1. INTRODUCTION

Time series models with stable Paretian errors have been studied by

many researchers. Adler et al. (1998) discussed many aspects of how

to apply standard Box-Jenkins techniques to stable ARMA

processes. Adler et al. (1998) concluded that, in principle, the

standard Box-Jenkins techniques do carry over to the stable setting

but a great deal of care needs to be exercised. In §2 we briefly

review the stable Paretian distribution and in §3 we develop

portmanteau tests for whiteness or randomness for an IID

series. The whiteness test is illustrated with a brief application

to exchange rate data. In §4 we develop portmanteau diagnostic

checks for residuals of an AR model fitted by least-squares

assuming the true innovations are IID stable Paretian

distributed. This is extended to the ARMA model in Appendix C. An

illustrative example shows the differences in inferences that may

result between the finite variance and infinite variance portmanteau

tests.

2. THE STABLE PARETIAN DISTRIBUTION

A stable distribution is usually defined through its characteristic function.

A random variable , or , is said to have a stable distribution

if its characteristic function has the following form:

where , is the parameter of the characteristic function,

is the index of stability, or the characteristic

exponent, satisfying , is the scale

parameter, is the skewness satisfying , is the location parameter, and

In this paper, we restrict our attention to processes generated by

application of a linear filter to an independently and identically distributed

(IID) sequence, , of random variables whose

distribution has Pareto-like tails, i.e.,

(1)

as , where

, and is a finite positive constant,

or the dispersion of the random variable .

3. PORTMANTEAU TESTS FOR RANDOMNESS OF STABLE PARETIAN TIME SERIES

In this section, we shall derive the asymptotic distributions of

portmanteau tests for checking randomness of a sequence of stable

Paretian random variables. We consider the stable analogues of

portmanteau tests of Box and Pierce (1970) as well as Peňa and

Rodriguez (2002), denoted by and , respectively. To

do so, we require some important properties of sample

autocorrelation functions (ACF) and sample partial autocorrelation

functions (PACF) of stable Paretian ARMA processes (Brockwell and

Davis, 1991, Ch. 13; Samorodnitsky and Taqqu, 1994; Adler et al.,

1998).

3.1 Asymptotic Distribution of Autocorrelation Function

Let be

an IID sequence of

stable Paretian random variables

and be the strictly

stationary process defined by

(2)

where

(3)

The stable analogue of the autocorrelation function at lag

is defined as

(4)

Eqn (4) can be estimated by

the sample autocorrelation function as follows:

(5)

for .

According to Davis and Resnick (1986), for any positive integer ,

the limiting distribution of sample autocorrelation functions is given by

(6)

where denotes convergence in distribution and

(7)

where are independent stable variables;

is positive with and the are , where

and

Under the null hypothesis that are a sequence of

IID stable Paretian random variables,

we have

and for

so

the limiting distribution of sample ACFs can be further simplified as follows:

(8)

where are given by

(9)

Note that, for ,

we may also use the mean-corrected sample autocorrelation function

at lag ,

denoted as , which is given by

(10)

Davis and Resnick (1986) indicated that

the limiting distribution of is the same as that of .

3.2 Asymptotic Distribution of Partial Autocorrelation Function

Consider an AR (p) process,

where

are a sequence of IID

stable Paretian errors,

, .

Let be a vector of

autocorrelation functions,

be the

autocorrelation matrix, and .

The Yule-Walker equations are defined as

(11)

The PACF at lag is simply

the -th element of the solution of the Yule-walker equations,

Likewise, the sample partial autocorrelation function at lag is defined as the -th element of

the sample estimate of the Yule-walker solution,

where

and are

the sample autocorrelation matrix and

the vector of sample autocorrelation functions, respectively.

It is apparent that

the sample partial autocorrelations is a function of sample autocorrelations.

Their relationship is clearly described in the Durbin-Levison algorithm.

Let be the sample PACF at lag , and

.

By the Durbin-Levison algorithm,

the vector can be expressed as a function

of , , with the -th element given by

(12)

where and are as defined above

and .

Following the proof in Monti (1994), we can derive

the asymptotic distribution of sample partial autocorrelation functions.

Under the null hypothesis that are independent,

the autocorrelation functions are all zero, and

according to Brockwell and Davis (1991, ch. 13),

Therefore,

where is a identity matrix.

By eqn. (12),

(13)

Using eqn. (8), we have

(14)

3.3 Asymptotic Distributions of and Tests

We can now derive the limiting distributions

of the and tests for checking randomness

of a sequence of stable Paretian random variables.

Under the assumption that ,

Runde (1997)

derived the limiting distribution of ,

based on the mean corrected sample autocorrelation functions.

His result is given by

(15)

where are defined in eqn. (9).

Note that if , the limiting distribution of eqn. (15)

remains the same if are replaced by .

Consider next the test of Peňa and Rodriguez (2002).

The test statistic may be given by

(16)

Following the proof of Theorem 1 in Peňa and Rodriguez (2002),

we may have the asymptotic distribution of eqn. (16) in the

following Theorem. The proof is given in Appendix A.

THEOREM 1

in eqn. (16) is asymptotically distributed as

where

are as defined in eqn. (9).

Remark 1:

It is possible to compute the

limiting distributions of

the and tests

by making use of the change variable technique and

some numerical algorithms of

calculating the probability density function

of stable random variables,

such as Mittnik et al. (1999).

This approach requires, however, intensive numerical computations.

Remark 2:

Another approach to obtaining the asymptotic distributions

of the and tests

is to simulate the aforementioned tests based on

their asymptotic distributions. For example,

is simulated as defined in Theorem 1.

This approach also requires a large scale of computation but

is much less intensive computationally than the approach

mentioned in Remark 1.

This approach will be adopted in the subsequent analysis

based on

simulations.

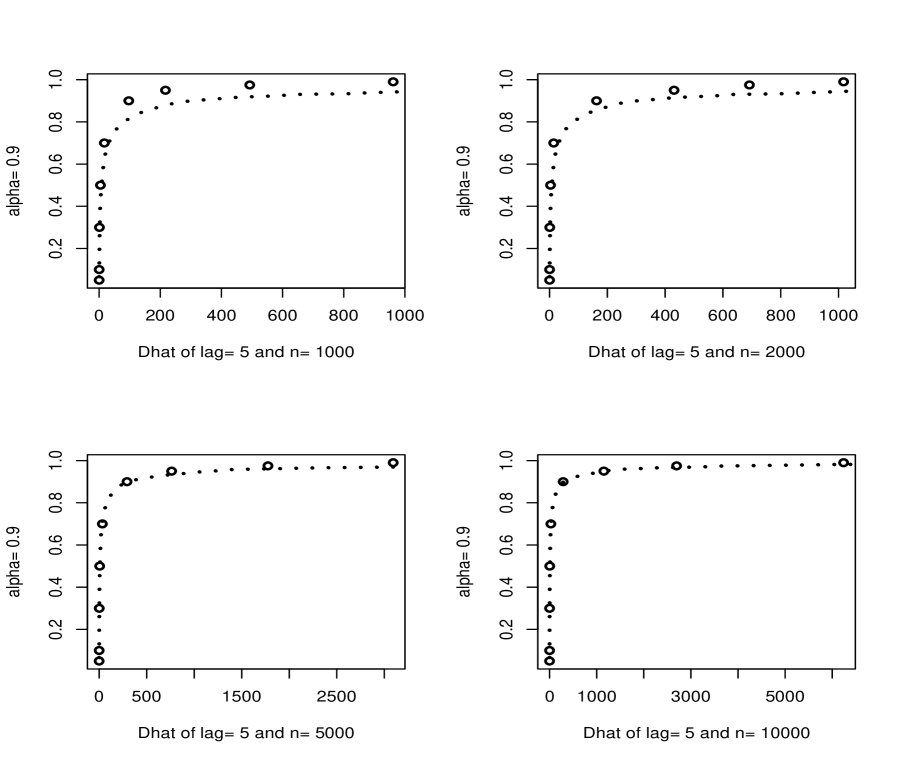

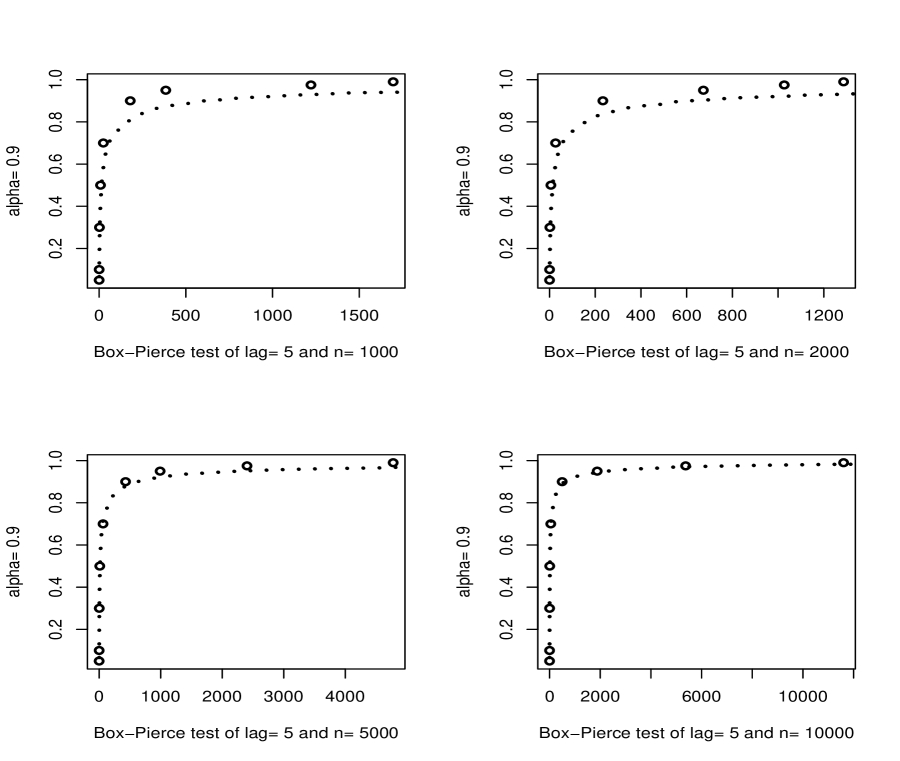

3.4 Simulation Experiments

The finite sample performance of and tests for

randomness will be investigated in this section. Based on

simulations, the 5, 10, 30, 50, 70, 90, 95, 97.5, 99

empirical quantiles of both tests with lag were calculated and

plotted against the corresponding asymptotic distributions. It is

seen in Figure 1 and Figure 2 that the empirical and asymptotic

quantiles do not agree very well unless is very large.

It is seen in Figures 1 to 2 that the speed of convergence

of both tests to the corresponding asymptotic distributions

is very slow.

A solution to this problem is to use the Monte-Carlo test or

parametric bootstrap (Appendix B).

[Figures 1 and 2 about here]

Consider the simulation experiments. IID random sequence of

with series length and ,

, , , were simulated. The empirical sizes of

both tests were calculated based on simulations and each

Monte-Carlo test was simulated based on simulations. The

results are tabulated in Table 1. It is seen that the empirical

sizes of both tests are very close to the 5% nominal level even

with .

[Table 1 about here]

3.5 Illustrative Example

Consider the daily Canada/U.S. exchange rates dated from

September 06, 1996 to September 05, 2006. The data was retrieved

from the website of the Federal Reserve Bank of St. Louis and the

returns, , were computed and tested for

randomness. The consistent estimators of McCulloch (1986) were used

to estimate and for the returns. We obtained and . It is seen that is close to zero so the series is not highly skewed. Since

is much less than , the usage of the portmanteau

tests in §3 are more reasonable than that of the ordinary

portmanteau tests in this data. The P-values for

test were determined using the asymptotic distribution

and the Monte-Carlo method in Appendix B. The results are compared

in Table 2. Note that when the finite-variance portmanteau

test suggested possible evidence of non-randomness but this is not

the case when the infinite-variance Monte Carlo test is used.

[Table 2 about here]

Remark 3: Portmanteau tests based on the

nonparametric bootstrap procedure could also be used but it would be

expected that they would be less powerful since less information is

used.

4. DIAGNOSTIC CHECK FOR MODEL ADEQUACY OF AR MODELS WITH STABLE PARETIAN ERRORS

4.1 Some Asymptotic Results

In this section, we shall derive the asymptotic

distributions of and tests

for diagnostic check in model adequacy of AR () models

with stable Paretian errors.

Consider the general AR () process as follows:

(17)

where is an IID sequence of

stable Paretian random variables, denotes the backward operator,

and .

Let denote

the estimates of autoregressive coefficients.

The residuals of the fitted model are given as follows:

(18)

and the corresponding residual autocorrelation at lag is given by

Consider the estimators of satisfying

From Appendix C, the residual autocorrelation at lag , , can be approximated by the first order Taylor expansion about

error autocorrelation functions, . Specifically, the

approximation is

(19)

where is the impulse response coefficient at lag and

is the error autocorrelation at lag .

Eqn. (19) can also be

written in matrix form, to order ,

(20)

where

(21)

By making use of eqn. (19) or eqn. (20)

as well as following the proof in Theorem 1, we may derive

the asymptotic distributions of the aforementioned portmanteau tests

for diagnostic check in AR models.

This distribution, however, is usually very complicated

and may not be traceable unless the AR

models of interest are fitted by least squares (LS).

For simplicity, we only consider the case that eqn. (17) is

estimated using least squares in the subsequent analysis.

According to 4 in Davis (1996), if the

ARMA parameters, , are estimated using

least squares , we have

converges in distribution, where denotes

the LS estimates of . Hence, in terms of our notation,

we have

.

Then, by Box and Pierce (1970),

in eqn. (18) satisfy the orthogonality conditions

and, to order ,

(22)

If we now multiply eqn. (20) on both sizes by

then using eqn. (22) we have

(23)

approximately, where is an identity matrix and

.

It was shown by Box and Pierce (1970) that

is idempotent

of rank .

Hence, the asymptotic distribution of the test

is given by

(24)

where and

are defined in eqn. (9).

Consider next the asymptotic distributions of residual partial autocorrelations.

Let be the vector of the first residual partial autocorrelations

and is the vector of error partial autocorrelations.

The Taylor expansion of

around yields

(25)

By eqn. (12) and (13), eqn. (25) becomes

(26)

Consider the Peňa-Rodriguez test as the form of

(27)

where

is the residual autocorrelation matrix.

By eqn. (26) and following

the proof in Theorem 1,

the limiting distribution of

eqn. (27) is ,

where

and

is a diagonal matrix with -th element equal to for

.

Remark 4: It is shown in Appendix C.4 that the

residuals in a fitted ARMA model are asymptotically equivalent to

those in a particular AR model. Hence the asympotic results for the

AR may be extended to the ARMA case.

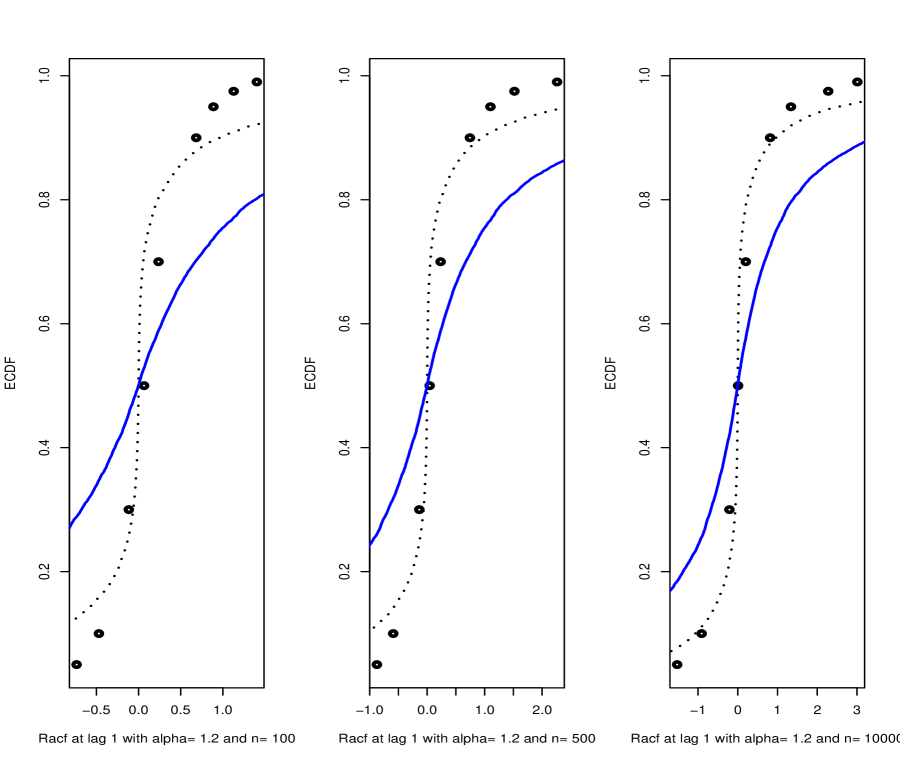

4.2 Some Size and Power Calculations

As in 3.4, the slow convergence of and tests

to their asymptotic distributions is also present at the residual

autocorrelations. The first order autoregressive process with was simulated and

AR models were fitted to the data. Then the 5, 10, 30, 50,

70, 90, 95, 97.5, 99 empirical quantiles of were

plotted against its theoretical asymptotic distribution based on

simulations. The asymptotic distribution of the error

autocorrelation at lag one, , was also plotted in Figure 3. It

is seen that empirical quantiles of get closer to its

asymptotic distribution as the series length increases. However,

this is not the case for the empirical quantiles of to

the asymptotic distribution of . Therefore, serious size

distortion may be present in this case if one uses error

autocorrelations as a diagnostic tool for checking model adequacy.

The slow convergence of residual autocorrelations to its asymptotic

distribution may cause difficulties in using portmanteau tests in

practice. Therefore, as in 3.4, we suggested using the

Monte-Carlo test to improve the effectiveness of portmanteau tests.

[Figure 3]

We now investigate the effectiveness of and tests

for diagnostic check in fitted AR models with stable Paretian

errors. The empirical sizes of and tests for a

significance test were first calculated via simulation. In

this experiment, AR models, , were

simulated, where and and AR models were fitted to

the simulated data by the Burg algorithm. The empirical size for

each test was calculated based on simulations and each

Monte Carlo test used simulations. Series length and

lags were investigated. It is seen in Table 3 that the

empirical sizes of both tests are very close to their nominal level.

[Table 3]

The empirical powers of and tests as

diagnostic tools were also investigated via simulation. Twelve

ARMA models of series length in Table 4 of

Peňa and Rodriguez (2002) were simulated and AR models

were fitted to the simulated data using the Burg algorithm. Both

tests with lags were calculated using the parametric

bootstrap procedure. The empirical powers were calculated based on

simulations and each Monte Carlo test used

simulations. It is seen in Table 4 that the empirical powers of both

tests are reasonably good for most models. Some of them are even

better than the powers listed in Peňa and Rodriguez (2002). In

addition, increasing the series length can also improve the

effectiveness of the proposed test procedure. For example, with

model 3 in Table 2, if the series length was increased to ,

the empirical powers of the test at lags were

increased significantly from 23.37%, 20.10% and 17.61% to

58.27%, 43.71% and 35.52%, respectively. Similar improvement was

also found in the test. Finally, as in Peňa and

Rodriguez (2002), our simulation experiments show that is

more powerful than as a diagnostic tool.

[Table 4]

Remark 5: It is well known that the Burg estimate of

is close to the LS estimate. The advantage of using

Burg estimate is that it is always in the stationary region and this is needed for

the Monte-Carlo test.

4.3 Illustrative Application

Tsay (2002, Ch. 2) tentatively identified an AR(3) or AR(5) model

for the monthly simple returns of CRSP value-weighted index from

January 1926 to December 1997 using the partial autocorrelation

function. Here and the usual Box-Pierce portmanteau test at

lags does not suggest model inadequacy of either model

at the 5% level. By applying our Monte-Carlo test procedure,

however, both the and tests in §4 reject both

models.

The P-values are displayed in Table 5.

The infinite variance hypothesis is plausible since the estimates

for of residuals in the fitted AR and AR models

are 1.696 and 1.635, respectively. We may conclude from this example

that using the ordinary portmanteau tests may lead to a wrong

decision if innovations have infinite variance.

[Table 5]

5. CONCLUDING REMARK

We will provide an R package implementing the portmanteau tests

described in this paper on CRAN.

APPENDIX A: PROOF OF THEOREM 1

First, by decomposing the determinant of the sample autocorrelation matrix ,

Pena and Rodriguez (2002) showed that

is a weighted function of the first partial autocorrelations.

Specifically,

(28)

Suppose that under the null hypothesis,

is asymptotic distributed as .

By applying the -method to , it follows that

is asymptotically distributed as .

From eqn. (28), we can have

(29)

Next suppose that

(30)

and apply the multivariate -method to

it follows that

(31)

From the Cramer-Wold theorem, it follows that

(32)

By eqn. (14), it follows that

(33)

Finally, from eqn. (32) and eqn. (33),

and from (30), we have the

APPENDIX B: MONTE-CARLO TEST PROCEDURE

The Monte-Carlo test procedure for diagnostic checking of AR and ARMA models

with stable Paretian errors can be summarized below. Note that, to

check randomness of a time series, we skip Step 1 and in Step 4 we

simulate data from an IID sequence of rather

than from the fitted model.

Step 1

Fit an AR model to data using least-squares or the Burg algorithm or

for ARMA, an approximate Gaussian maximum likelihood algorithm is used.

Calculate residuals and the portmanteau

test of interest , say .

Step 2

Estimate from residuals in Step 1.

The estimator given by McCulloch (1986) may be used.

Step 3

Select the number of Monte-Carlo simulations, . Typically .

Step 4

Simulate the fitted model using the estimated AR or ARMA parameters in Step 1

and in Step 2.

Obtain after estimating the parameters in the simulated series.

Step 5

Repeat Step 4 times counting the number of times that a value

of greater than or equal to that in Step 1 has been

obtained.

Step 6

The -value for the test is .

Step 7

Reject the null hypothesis if the -value is smaller than a predetermined significance level.

APPENDIX C: THE GENERALIZATION OF LINEAR EXPANSION OF RESIDUAL

AUTOCORRELATION

C.1 Introduction

Residual autocorrelations are an important tool for diagnostic checking of

autoregressive and moving average ( ARMA ) models. Their

asymptotic distributions from univariate ARMA models were first

derived by Box and Pierce (1970). McLeod (1978) refined the

derivation and extended it to the multiplicative seasonal ARMA

models. Their results were established under the assumption that

error sequences have finite variance and the parameters are

estimated using least squares, or equivalently, using maximum

likelihood estimation (MLE) for Gaussian ARMA processes. Their

result may not be valid if the parameters of interest are estimated

using other estimation methods or linear processes with infinite

variance. This section demonstrates how the linear expansion of

residual autocorrelations in Box and Pierce (1970) also holds for

other estimation methods and for AR models with stable Paretian

errors. The expansion may be used to derive the limiting

distribution of residual autocorrelations.

C.2 The Autoregressive Process

Consider an AR process as follows:

(34)

where denotes the backward operator, , and is a sequence of independent and

identical random variables with mean zero and finite variance

. For given values of parameters, we can define

(35)

and the corresponding autocorrelation function at lag as

(36)

C.3 Linear Expansion of Residual Autocorrelation

Function about Error Autocorrelation Functions

Consider approximating the residual autocorrelation

by a first order Taylor expansion about .

Let and denote and

respectively, where integer.

Consider the estimators of satisfying

(37)

We have

(38)

where

(39)

and

For LS estimates, we have that

(40)

so it is straightforward that .

Using this result, Box and Pierce (1970) showed that

to order , where

’s are the impulse response coefficients of the MA representation

of eqn. (34).

For other estimation methods, however,

may not be zero since eqn.

(40) does not hold.

To obtain a general result for , therefore,

we will calculate explicitly.

Note that can be written as follows:

(41)

By eqn. (2.15) of Box and Pierce (1970) and letting , eqn. (41)

can be expressed as follows:

(42)

where

Let denote

and approximate by replacing ’s and ’s

with ’s and ’s,

the theoretical parameters and the autocorrelations of the autoregressive process .

By the Barteltt’s formula,

as well as eqn. (37) and (42), we have

(43)

Then by making use of the recursive relation

which is satisfied by the autocorrelations of an

autoregressive process,

eqn. (2.19) of Box and Pierce (1970), or

(44)

can be simplified to yield

(45)

Note that eqn. (45) has the same form of eqn. (2.20) of

Box and Pierce (1970). Specifically, it can be seen as .

Moreover, Box and Pierce indicated that so .

Plugging this

result into eqn. (42), we have

. Consequently, eqn. (2.20) of Box and Pierce (1970)

for the linear expansion of residual autocorrelations

still holds for other estimators with order

.

Remark 6 : Many estimators of for an

AR model with Paretian stable errors have order

, such as Whittle’s, Yule-Walker and

LS estimtors. Using the result that

, and

following the proofs in this section as well as in Box and Pierce

(1970), we may obtain the linear expansion of residual

autocorrelation functions for AR models with stable Paretian

errors as in eqn. (19)

C.4 The Equality of Residuals in AR and ARIMA

Models

The result in .3 may be extended to ARIMA models using

technique in 5.1 of Box and Pierce (1970). If two time series

(a) an ARMA () process

(46)

and (b) an autoregressive series

(47)

are both generated from the same set of errors ,

where

and

If

(48)

then when the models are fitted by least squares, their residuals, and

hence also their autocorrelations, will be very nearly the same.

In this section, we consider whether the equality of residuals between

AR and ARIMA models is still valid when

the parameters are estimated by other approaches.

As in eqn. (35), define

(49)

where , and now also

(50)

where .

Using eqn. (5.12) and eqn. (5.13) of Box and Pierce (1970),

we can approximate and as follows:

(51)

and

(52)

Note that eqn. (51) and eqn. (52) can be seen as a linear regression model.

We can estimate regression coefficients, and using

any suitable method. Let denote the corresponding estimator.

Since both eqn. (51) and eqn. (52) have the same form,

their estimators should agree with each other.

For example,

least squares estimates are given by

(53)

and

(54)

Then by setting

and estimating the regression coefficients of eqn. (51) and eqn. (52), we have

(55)

Finally, by setting and

in eqn. (51) and eqn. (52),

it follows from

eqn. (55) that to order

(56)

and thus (to the same order) .

REFERENCES

Adler, R.J. Feldman, R.E. and Gallagher, C. (1998),

“Analysing Stable Time Series,”

A Practical Guide to Heavy Tails: Statistical Techniques and Applications,

Birkhuser, Boston.

Box, G.E.P. and Pierce, D.A. (1970),

“Distribution of Residual Autocorrelation in Autoregressive-Integrated Moving Average Time Series Models,”

Journal of American Statistical Association 65, 1509-1526.

Brockwell, P.J. and Davis, R.A. (1991),

Time Series: Theory and Methods,

Springer, New York.

Davis, R.A. (1996),

“Gauss-Newton and M-estimation for ARMA processes,”

Stochastic Processes and their Applications 63, 75–95.

Davis, R.A. and Resnick, S. (1986),

“Limit Theory for the Sample Covariance and Correlation Functions of Moving Averages,”

The Annals of Statistics 14, 533–558.

McCulloch, J.H. (1986), “Simple Consistent

Estimators of Stable Distribution Parameters,” Communication

in Statistics–Computation and Simulation, 15, 1109–1136.

Mittnik, S., Rachev, S.T., Doganoglu, T. and Chenyao, D. (1999),

“Maximum Likelihood Estimation of Stable Paretian Models,”

Mathematical and Computer Modelling, 29, 275–293.

Monti, A.C. (1994),

“A Proposal for Residual Autocorrelation Test in Linear Models,”

Biometrika 81, 776–780.

Peňa, D. and Rodriguez, J. (2002),

“A Powerful Portmanteau Test of Lack of Fit For Time Series,”

Journal of American Statistical Association 97, 601-610.

Runde, R. (1997),

“The Asymptotic Null Distribution of the Box-Pierce Q-Statistic for Random Variable with Infinite Variance:

An Application to German Stock Returns,”

Journal of Econometrics 78, 205-216.

Samorodnitsky, G. and Taqqu, M. (1994),

Stable-Non-Gaussian Random Processes,

Chapman-Hall, New York.

Tsay, R.S. (2002),

Analysis of Financial Time

Series, New York: Wiley.

Table I.

Empirical sizes of and

for a significance test

based on the parametric bootstrap procedure.

The empirical size for each test was

calculated based on simulations.

Each Monte Carlo test also used simulations.

Series length and lags were investigated.

Table II.

P-values for statistic using Monte-Carlo test and

-method for testing randomness of exchange-rate returns.

Monte-Carlo Test

Test

Table III.

Empirical sizes of and

for a significance test.

and tests for checking model adequacy of

AR models

fitted by the Burg algorithm.

Both tests

were implemented by the parametric bootstrap procedure.

The empirical size for each test was

calculated based on simulations.

Each Monte Carlo test also used simulations.

Series length and lags were investigated.

Table IV.

Empirical powers of and

for a significance test.

and tests for checking model adequacy of

twelve ARMA models in Table 3 of

Peňa and Rodriguez (2002)

fitted by AR using the Burg algorithm.

Both tests

were implemented based on the parametric bootstrap procedure.

The empirical power for each test was

calculated based on simulations.

Each Monte Carlo test also used simulations.

Series length and lags were investigated.

Model

1

2

3

4

5

6

7

8

9

10

11

12

Table V. An illustrated example using the monthly simple

return of CRSP value-weighted index data from Tsay (2002). The

data were fitted by an AR model and an AR model. The

entries in the first two columns are the P-values of and

in §4 based on the Monte-Carlo test; those in the

third column are the P-value of the portmanteau test of Box and

Pierce (1970) assuming a normal distribution, denoted by .

AR

AR

Figure 1:

The slow convergence of the test to its asymptotic distribution.

Random sequences of series length were simulated from .

simulations were used to

retrieve empirical percentiles of the test with .

The , , , , , , , , empirical quantiles

were plotted as black circles and

the corresponding asymptotic distribution was also plotted as the dot line.

Figure 2:

The slow convergence of the test to its asymptotic distribution.

Random sequences of series length were simulated from .

simulations were used to

retrieve empirical percentiles of the test with .

The , , , , , , , , empirical quantiles

were plotted as circles and

the corresponding asymptotic distribution was also plotted as the dot line.

Figure 3: The slow convergence of residual autocorrelation to its

asymptotic distribution. AR process, , of

series length , , were simulated respectively,

where is distributed as . The number of

simulation were used. AR models were then

fitted to simulated data and residual autocorrelation at lag one was

calculated. The , , , , , , , ,

empirical quantiles of residual autocorrelation at lag

one were plotted as circles. The corresponding asymptotic

distribution was plotted as the dot line. The asymptotic

distribution of sample autocorrelation was plotted as the real line.