Option pricing in exponential Lévy models with transaction costs.

Abstract

We present an approach for pricing European call options in presence of proportional transaction costs, when the stock price follows a general exponential Lévy process. The model is a generalization of the celebrated work of Davis, Panas and Zariphopoulou (1993), where the value of the option is defined as the utility indifference price. This approach requires the solution of two stochastic singular control problems in finite horizon, satisfying the same Hamilton-Jacobi-Bellman equation, with different terminal conditions. We introduce a general formulation for these portfolio selection problems, and then we focus on the special case in which the probability of default is ignored. We solve numerically the optimization problems using the Markov chain approximation method and show results for diffusion, Merton and Variance Gamma processes. Option prices are computed for both the writer and the buyer.

Keywords: option pricing, transaction costs, Lévy processes, indifference price, singular stochastic control, variational inequality, Markov chain approximation.

1 Introduction

The problem of pricing a European call option was first solved mathematically in the paper Black and Scholes, (1973). Even if it is quite evident that this model is too simplistic to represent the real features of the market, it is still nowadays one of the most used models to price and hedge options. The reason for its success is that it gives a closed form solution for the option price, and that the hedging strategy is easily implementable. One of the main assumptions of the Black-Scholes model is that log-returns are normally distributed. However, statistical analysis of financial data reveal that the normality assumption is not a very good approximation of reality (see for instance Cont, (2001)). Empirical log-return distributions have more mass around the origin and along the tails (heavy tails). This means that the normal distribution underestimates the probability of large log-returns, and considers them just as rare events. In the real market instead, log-returns manifest frequently high peaks, that come more and more evident when looking at short time scales. The log-returns peaks correspond to sudden large changes in the price. There is a huge literature of option pricing models that consider underlying processes with discontinuous paths. Most of these models consider the log-price dynamics following a Lévy process i.e. a stochastic process with independent and stationary increments, satisfying the additional property of stochastic continuity. Good references on the theory of Lévy processes are the books of Sato, (1999) and Applebaum, (2009). Financial applications are discussed in the book of Cont and Tankov, (2003).

Another issue of the Black-Scholes framework is that it does not consider the presence of budget constraints and market frictions such as bid/ask spread and transaction fees. In particular, in a market with transaction costs the replicating portfolio cannot be perfectly implemented. Since delta-hedging involves continuous time trading, the presence of transaction costs makes this strategy infinitely costly. Many authors attempted to include proportional transaction costs in option pricing models. In Leland, (1985), in order to avoid continuous trading, the author specifies a finite number of trading dates. He obtains a Black-Scholes-like nonlinear partial differential equation (PDE) with an adjusted volatility term that takes into account the transaction costs. However this model has several drawbacks, i.e. trading at fixed dates is not optimal and the option price diverges as the number of trading times grows. Recent developments in this direction are for instance Mocioalca, (2007), Florescu et al., (2014) and Sengupta, (2014) who consider different features of the market such as jumps, stochastic volatility and stochastic interest rate respectively.

A different approach has been introduced by Hodges and Neuberger, (1989). The authors use an alternative definition of the option price called indifference price, based on the expected utility maximization concept. An overview of these topics applied to several incomplete market models can be found in Carmona, (2009). Since a perfect replicating portfolio does not exist, there is no risk-free hedging strategy. The model has to take into account the risk profile of the writer/buyer to describe his trading preferences. Hodges and Neuberger, (1989) define the option price as the value that makes an investor indifferent between holding a portfolio with an option and holding a portfolio with this additional value, in terms of expected utility of the final wealth. The optimal hedging strategy is to keep the portfolio within a band called No Transaction region. Using numerical experiments, they verify that this strategy outperforms the one proposed in Leland, (1985). This approach has been further developed in Davis et al., (1993), where the problem is formulated rigorously as a singular stochastic optimal control problem. The authors prove that the value function of the optimization problem can be interpreted as the solution of the associated Hamilton-Jacobi-Bellman (HJB) equation in the viscosity sense. They prove also that the numerical scheme, based on the Markov chain approximation, converges to the viscosity solution. Numerical methods for this model are presented in Davis and Panas, (1994), Clewlow and Hodges, (1997) and Monoyios, (2003), Monoyios, (2004). In Whalley and Wilmott, (1997) and Barles and Soner, (1998) the problem is simplified by using asymptotic analysis for small transaction costs, in order to reduce the original variational inequality to a simpler non-linear PDE. Further developments are presented in the thesis work of Damgaard, (1998), where the author studies the robustness of the model with respect to the choice of the utility function.

In the present work, we want to develop a model for pricing options using the concept of indifference price proposed in Hodges and Neuberger, (1989) under the presence of proportional transaction costs. We consider the stock dynamics evolving as an exponential Lévy process. Portfolio models with Lévy processes and transaction costs have already appeared in the literature. For instance, in Benth et al., (2002) and Framstad et al., (1999), the authors, in order to exclude the possibility of bankruptcy, introduce strong restrictions in the set of admissible trading strategies, i.e. short-selling and borrowing money are not allowed. De Vallière et al., (2016) formulate a more general framework, where negative positions in stocks and cash are allowed, and bankruptcy is considered. They prove that the infinite horizon singular/regular control problem considered in their article, satisfies the dynamic programming principle and show that the value function is the unique continuous viscosity solution of the HJB equation.

The model we present in Section 2 is an adaptation of the model of De Vallière et al., (2016) to our finite horizon problem. Since the numerical methods for this problem are quite cumbersome, we focus on the special case of an investor with a very large credit availability i.e. we ignore the possibility of default. By assuming a risk profile described by an exponential utility function, we reduce by one the number of state variables and obtain a simpler optimization problem. In Section 3 we present the discretized version of the problem. We propose a monotone, stable and consistent numerical scheme and prove that its solution converges to the viscosity solution of the HJB equation. The discretization technique is described in the Appendix B, while the Appendix C contains the proofs of the theorems. The numerical results are presented in Section 4. Section 5 contains a summary of the outcomes, with suggestions for future improvements.

2 The model

2.1 Exponential Lévy models

Let be a Lévy process defined on the filtered probability space , where is the natural filtration. We assume that has the characteristic Lévy triplet , where , and is a positive measure on , called Lévy measure which satisfies:

| (1) |

We use the (cádlág) process to model the log-price dynamics. The stock price is therefore an exponential Lévy process such that:

| (2) |

Motivated by practical reasons, we only consider processes with finite mean and variance. The condition for a finite second moment , is directly related to the integrability conditions of the Lévy measure:

| (3) |

Considering condition (3), the dynamics of has the following Lévy-Itô decomposition:

| (4) |

where is a standard Brownian motion. The term

| (5) |

is the compensated Poisson martingale measure, where is the Poisson random measure with intensity . By applying the Itô lemma to (2) we obtain the SDE describing the evolution of the price:

| (6) |

where . We defined the drift term as:

| (7) |

2.2 Portfolio dynamics with transaction costs

In this section we follow the framework of De Vallière et al., (2016) and introduce a market model with proportional transaction costs that generalizes Davis et al., (1993). Let us consider a portfolio composed by one risk-free asset (bank account) paying a fixed interest rate and a stock . We denote by the number of shares of the stock that the investor holds. The state of the portfolio at time is and evolves following the SDE:

| (8) |

The parameters , are the proportional transaction costs when buying and selling respectively. The control process is the trading strategy that represents the cumulative number of shares respectively bought and sold up to time . The strategy is a cádlág, predictable, nondecreasing process with bounded variation, such that , i.e. we allow for an initial transaction. Under these assumptions the portfolio process is cádlág.

If at time there is an unpredictable jump in the stock price , a possible transaction should happen immediately after the jump222 The control process is assumed to be predictable, i.e. measurable with respect to the left-continuous filtration generated by . Therefore, a jump in the price and a jump in the control cannot occur simultaneously, almost surely. A deeper digression on this topic can be found in Section 2 of De Vallière et al., (2016).. If the investor at time observes a jump in the price and decides to rebalance his portfolio, he will trade at some time at the price . Under this framework, as explained in De Vallière et al., (2016), the optimal strategy cannot exist.

Definition 2.1.

The cash value function , is defined as the value in cash when the shares in the portfolio are liquidated i.e. long positions are sold and short positions are covered.

| (9) |

Definition 2.2.

For , the total wealth process is defined as:

| (10) |

We say that a portfolio is solvent at time if the portfolio’s wealth is bigger than a fixed constant , with . This constant may depend on the initial wealth and on the parameters in (8). It can be interpreted as the credit availability of the investor.

Definition 2.3.

The solvency region is defined as:

| (11) |

Since the underlying stock follows a process with jumps, it is not guaranteed that the portfolio stays solvent for all . When holding short positions, it is possible that a sudden increase in the stock price causes the total wealth to jump out of the solvency region. The same can happen with a downward jump when the investor is long in stocks and negative in cash. An immediate decrease in the stock price would make him unable to pay the debts. If the investor goes bankrupt, there are no trading strategies to save him.

Definition 2.4.

The first exit time from the solvency region is defined as:

| (12) |

Definition 2.5.

The set of admissible trading strategies is the set of all cádlág, nondecreasing, predictable, bounded variation processes such that is a solution of (8) with initial values and such that almost surely for all , and for all .

2.3 Utility maximization

Let us assume an investor builds a portfolio with cash, shares of a stock and in addition he sells or purchases a

European call option written on the same stock, with strike price and expiration date .

From now on, we introduce the superscripts , and to indicate the writer, buyer and zero-option portfolios respectively.

In the zero-option portfolio, the wealth process and the exit time correspond to (10) and (12).

Definition 2.6.

For , we define the wealth processes for the writer:

| (13) | ||||

and the buyer:

| (14) | ||||

In the case the option is exercised, , the buyer pays to the writer the strike value in cash, and the writer delivers one share to the buyer. In a market with transaction costs, the real value (in cash) of a share incorporates the transaction cost for the purchase or the sale. Therefore the buyer does not exercise when , but when .

The objective of the investor is to maximize the expected utility of the wealth at over all the admissible strategies. This expectation is conditioned on the current amount of cash and number of shares in the portfolio and on the current stock price. The exit times and for the writer and buyer portfolios, can be obtained by inserting (13) and (14) in (12). The sets of trading strategies for the three portfolios can be obtained in the same way from the Definition [2.5].

Definition 2.7.

The value function of the maximization problem for is defined as:

| (15) | ||||

where is a concave increasing utility function such that , and .

The option price for the writer (buyer), is defined as the amount of cash to add (subtract) to the bank account of the portfolio containing the option, such that the maximal expected utility of final wealth of the writer (buyer) is the same he could get with the zero-option portfolio.

Definition 2.8.

The writer price is the value such that

| (16) |

and the buyer price is the value such that

| (17) |

2.4 Hamilton-Jacobi-Bellman Equation

We present the HJB equation associated to the singular stochastic optimal control problem described before. This problem is called singular because the controls are allowed to be singular with respect to the Lebesgue measure . The derivation of the HJB equation for singular control problems can be found for instance in Fleming and Soner, (2005). We assume without proving that the value function (15) satisfies the dynamic programming principle. The HJB equation associated to (15) is the following variational inequality:

| (18) | ||||

for and . The terminal boundary conditions are given by Eq. (15) at time . Since this HJB equation is a PIDE, the non-local integral operator implies the definition of lateral conditions not only on the boundaries of the solvency region, but also beyond:

| (19) |

We refer to the arguments in De Vallière et al., (2016) to prove that the value function (15) is the unique continuous viscosity solution of (18).

2.5 Variable reduction

In the diffusion model of Davis et al., (1993), the portfolio is solvent for every (almost surely) and it is always possible to calculate the utility of the wealth at the terminal time . In the framework of De Vallière et al., (2016) the stock process can jump, and in presence of short positions the portfolio can go bankrupt at any time before the maturity .

With the intention of simplifying the maximization problem (15) and reducing the number of variables, we restrict our attention to the case of no bankruptcy. A possible idea is to consider a positive initial wealth, and define the restricted set of admissible strategies as the set of such that and for all (see Benth et al., (2002)). However, in order to implement a hedging strategy, we are interested in portfolios containing short positions as well. So, we can assume that the investor has a very large credit availability in the sense that

| (20) |

In practical terms, we ignore the possibility of default. The solvency region becomes and no lateral boundary conditions are imposed.

As in Davis et al., (1993), for , we consider the exponential utility function

| (21) |

Thanks to (20) and (21) we can remove from the state dynamics. By solving (8) we get

| (22) |

where . Using together (20), (21) and (22), and the wealth processes (10),(13),(14), we obtain for , , and :

| (23) |

where

| (24) | ||||

is our new minimization problem. The exponential term inside the expectation can be considered as a discount factor, and the second term is the terminal payoff:

-

•

No option:

(25) -

•

Writer:

(26) -

•

Buyer:

(27)

Using conditions (16), (17) together with (23), we obtain the explicit formulas for the option prices:

| (28) |

| (29) |

Since is independent on , let us write . It is convenient to pass to the log-variable , such that

| (30) |

For , the HJB Eq. (18) becomes:

| (31) | ||||

This equation is well defined for , where is the space of continuous functions with quadratic polynomial growth at infinity in , for each . Since in (24) we do not make any assumptions on the smoothness of , we will assume that it satisfies the Equation (31) in the viscosity sense. In the following, we will also assume that is continuous (this hypothesis follows the argument in Section 4 of De Vallière et al., (2016)).

3 Markov chain approximation

To solve the minimization problem (24) we use the Markov chain approximation method described in Kushner and Dupuis, (2001). The numerical technique specific for singular controls has been developed in Kushner and Martins, (1991). The portfolio dynamics (8) is approximated by a discrete state controlled Markov chain in discrete time. The method consists in creating a backward recursive dynamic programming algorithm, in order to compute the value function at time , given its value at time . Kushner and Dupuis, (2001) prove that the value function obtained through the discrete dynamic programming algorithm converges to the value function of the original problem using a “convergence in probability” argument. In Barles and Souganidis, (1991), the authors consider instead the convergence of the discrete value function to the viscosity solution of the HJB equation. Davis et al., (1993) prove the existence and uniqueness of the viscosity solution of the HJB Eq. (18) for the diffusion case, and using the method developed by Barles and Souganidis, (1991) prove that the discrete value function, obtained through the Markov chain approximation, converges to it. In this section we propose a discretization scheme and prove that it is monotone, consistent, stable, and its solution converges to the continuous viscosity solution of (31).

In this work we model the stock dynamics with a general exponential Lévy process. In practical computations, we need to specify which Lévy process we are using, and this is equivalent to select a Lévy triplet. Since every Lévy process satisfies the Markov property, we are allowed to use the Markov chain approximation approach. A possible way to construct the Markov chain is to discretize the infinitesimal generator by using an explicit finite difference method (see for instance Kushner and Dupuis, (2001) or Fleming and Soner, (2005)). This is straightforward for Lévy processes of jump-diffusion type with finite jump activity. But for Lévy processes with infinite jump activity, it is not straightforward to obtain the transition probabilities from the discretization of the generator. A common procedure is to approximate the small jumps with a Brownian motion, as explained in Cont and Voltchkova, (2005), in order to remove the singularity of the Lévy measure near the origin.

3.1 The discrete model

Thanks to the variable reduction introduced in the previous section, the optimization problem (24) only depends on two state variables. The portfolio dynamics (8) has the simpler form (using ):

| (32) |

where the SDE for the log-variable can be obtained by putting together (4) and (7). If the process has finite activity , thanks to the moment condition (3), we can define and such that the SDE of can be written as

| (33) |

If the process has infinite activity , we can approximate the “small jumps” martingale component with a Brownian motion with same variance. After fixing a truncation parameter , we can split the integrals in (32) in two domains and . The integrand on the domain , is approximated by Taylor expansion such that:

| (34) |

where we defined the new parameters:

| (35) | ||||

The process is a compensated Poisson process with finite activity and .

Now we can discretize the time and space to create a Markov chain approximation of the portfolio process (32). For , we define the discrete time step such that . We assume that the controls are constant for , and allow for a possible variation at for each . From now on, we indicate and the process immediately before the possible transaction.

Let us define the set , where is the discrete log-return step. The values can be different to capture the possible asymmetry in the jump sizes. Its dimension is . Let us define also the set , where is the discrete shares step and . Its dimension is . The discretized version of the SDE (32) is:

| (36) |

where , and . The term takes values in 333A common alternative is to consider a binomial discretization with , as in Davis et al., (1993). and satisfies and , at first order in . The term is the discrete version of the compensated Poisson jump term, and satisfies and , at first order in , with . When the continuous time jump term is , the corresponding discrete version can assume all the values in . If instead the integral has a truncation term , i.e. , we can define the subset , such that .

The Markov chain has the shape of a recombining multinomial tree, where each node has branches. The number of nodes at time is . We derive the transition probabilities by an explicit discretization of the infinitesimal generator (see Appendix B.2). Following Kushner and Dupuis, (2001), the process has to satisfy the following two conditions in order to be admissible:

-

1.

the transition probabilities have the representation:

(37) where , and , are respectively the diffusion and jump transition probabilities (see Appendix B.1).

-

2.

(local consistency) The moments of the discrete increments match those of the continuous increments, at first order in :

(38)

The process assumes values in and , are non-negative multiples of . The two increments and can occur instantaneously at time . They cannot assume values different from at the same time, and must satisfy the condition 444The values attainable by and depend on the current value of . For instance, if , then and . for all .

3.2 Discrete dynamic programming algorithm

We can formulate a discrete backward algorithm by applying the dynamic programming principle to (24) on the discrete nodes of the chain :

| (39) | ||||

The variations of are instantaneous at for each , while the process changes in the interval according to its Lévy dynamics. This feature suggests to introduce a numerical scheme based on two steps: an evolution step and a control step.

From now on we drop the superscript from . We introduce the discretization parameter and indicate the discretized value function by

. For a fixed , we adopt the common short notation .

We set the initial value for . At time , the index assumes values in

and assumes values in .

Scheme 1.

Let us define a two steps numerical scheme such that

| (40) |

where indicates all the values of not in .

such that and for each . We defined and . The coefficients satisfy and for all .

Theorem 3.1.

The computational complexity of the Algorithm [1] is

The first factor comes from the loop over all the nodes of the tree i.e. . The second factor, , comes from the loop over all the values , and the third factor, , comes from the minimum search.

For a simple diffusion process the number of branches is fixed to , but for processes with jumps it is proportional to . The standard deviation of every Lévy process satisfying (3) grows as the square root of time. Therefore the size of a space step . Let us consider for instance the integral term in Eq. (33) or (3.1). For computational reasons we have to reduce the region of integration to the bounded domain , with (see Appendix B.2). The number of branches to cover this region is .

In order to have a more accurate result, it is better to choose and consequently . In this way, the number of shares to buy or sell is more sensitive to the resolution in the log-price tree. Therefore assuming and , the total computational complexity is . For a fixed , the total complexity is reduced to .

3.3 The Merton jump-diffusion model

The first jump-diffusion model applied to finance is the Merton model, presented in Merton, (1976). In the paper, the author derives a semi-closed form solution for the price of a European call option. The Merton model describes the log-price evolution as a Lévy process with a characteristic Lévy triplet with , and Lévy measure:

| (41) |

The process can be represented as the superposition of a Brownian motion with drift and a pure jump process. The number of jumps is represented by a Poisson process with intensity . The size of the jumps is normal distributed . The dynamics of is described by the SDE (33) with . For any , the associated infinitesimal generator is:

| (42) | ||||

3.4 The Variance Gamma model

The Variance Gamma (VG) process is a pure jump Lévy process with infinite activity and no diffusion component. Applications of the VG process to financial modeling can be found for example in Madan and Seneta, (1990) and Madan et al., (1998). Consider a Brownian motion with drift and substitute the time variable with a gamma subordinator . We obtain the VG process , that depends on three parameters: is the drift of the Brownian motion, is the volatility of the Brownian motion and is the variance of the Gamma process. The VG Lévy measure is:

| (43) |

The Lévy triplet is . A VG process with an additional drift , , has the Lévy triplet . The VG SDE can be obtained directly from Eq. (32):

| (44) |

where we put , , and by (7).

However, the jump process in Eq. (44) has infinite activity, and its infinitesimal generator is not helpful for the Markov chain approximation!

We consider instead the approximated process (3.1) with .

All the parameters are obtained through the VG Lévy measure (43):

| (45) |

For any , the associated infinitesimal generator has a jump-diffusion form:

| (46) | ||||

4 Numerical results

In this section we implement the Algorithm [1] described in Section 3.2 and calculate the prices of European call options for the writer and the buyer. The prices are computed under the assumption that the stock log-price follows three different Lévy processes: a Brownian motion, a Merton jump-diffusion and a Variance Gamma, with parameters in Table 1.

| Details | Diffusion parameters | |||||||||

| 15 | 1 | 0.1 | 0.1 | 0.25 | 0.001 | |||||

| Merton parameters | ||||||||||

| 0.1 | 0.25 | 0 | 0.5 | 0.8 | 0.04 | |||||

| VG parameters | ||||||||||

| 0.1 | -0.1 | 0.2 | 0.1 | 0.05 | ||||||

| Diffusion price | Merton price | VG price | |||

|---|---|---|---|---|---|

| Closed formula | PDE | Closed formula | PIDE | Closed formula | PIDE |

| 2.2463 | 2.2463 | 3.4776 | 3.4775 | 1.9870 | 1.9871 |

For comparisons, we compute also the option prices using the standard martingale pricing theory (see Appendix A). In the Table 2 we show the at the money values obtained with the closed formula and by solving the respective PIDE. The closed formula for the diffusion process is the well known Black and Scholes, (1973) formula. To compute the Merton price we use the semi-closed formula derived in Merton, (1976), and for the VG price we used the semi-closed formula derived in Madan et al., (1998). The PIDE prices are obtained by solving the Eq. (A.2) with generators (A.3), (42) and (46) (details in Appendix A). Of course, the parameter has not been used to compute the prices in Tab. 2. We set the drift term equal to the risk free interest rate , following the common rule of the standard no-arbitrage theory. This choice is also discussed in Hodges and Neuberger, (1989),

In the following analysis, we consider the PIDE prices as our benchmarks for comparisons. In all the computations we use equal transaction costs for buying and selling, .

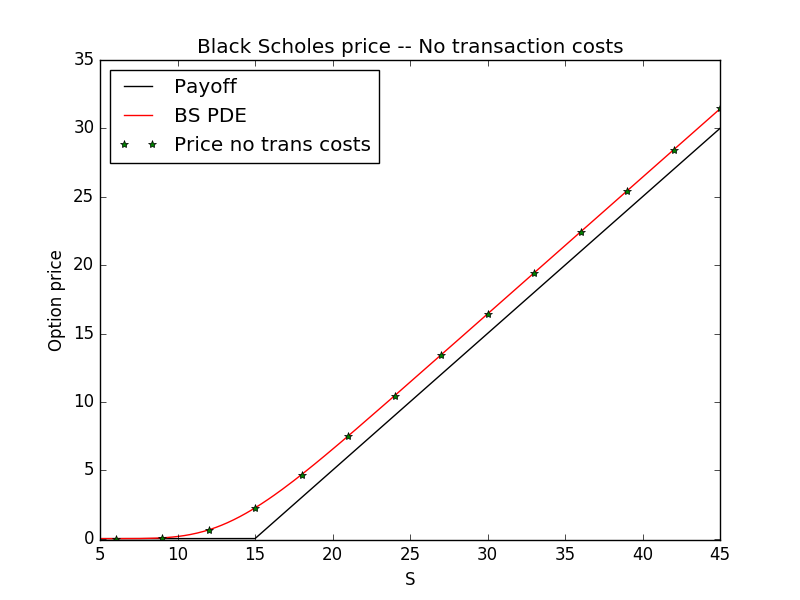

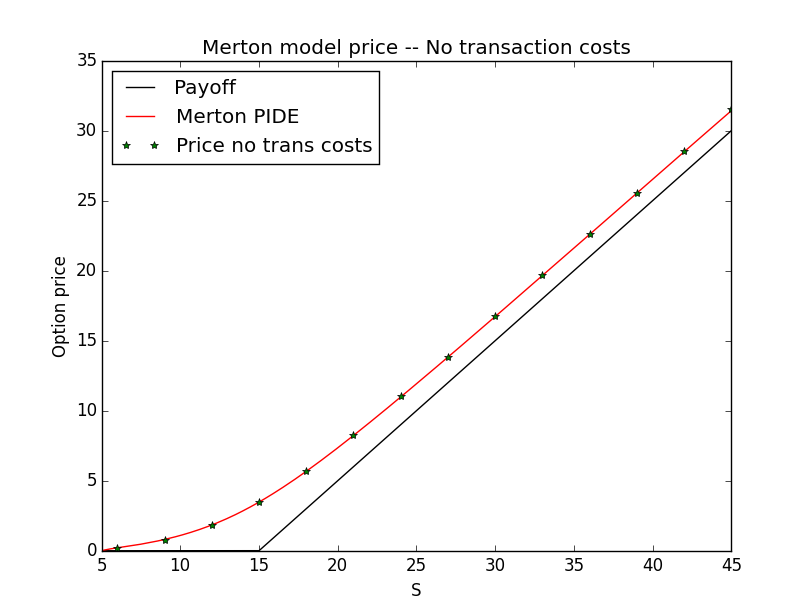

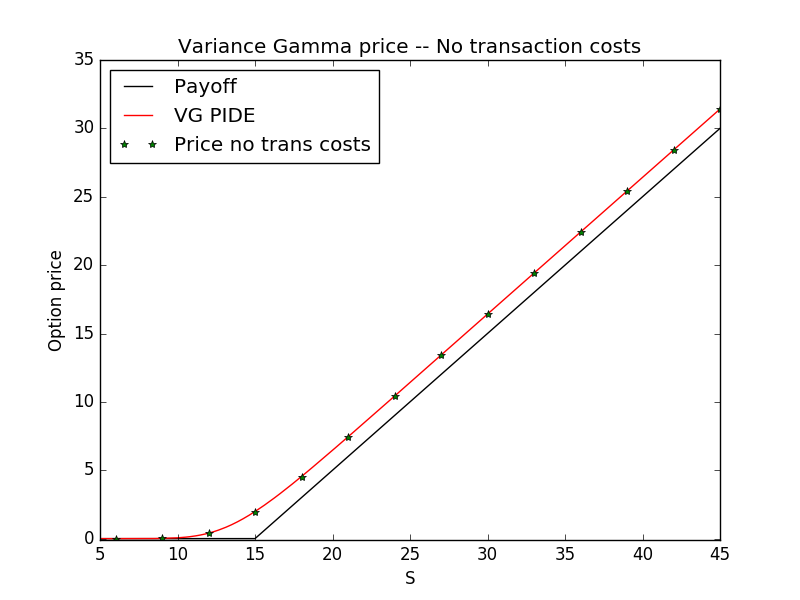

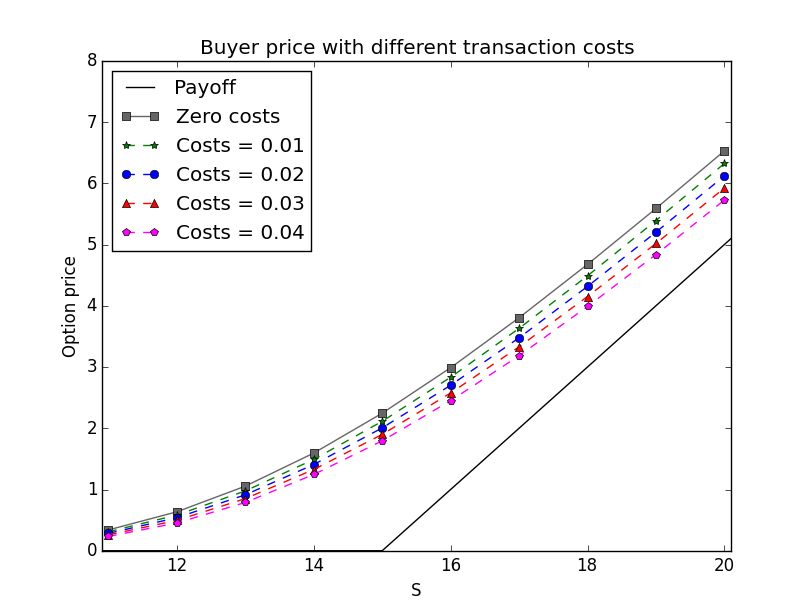

In Fig. 1 we show that the proposed model prices replicate the PIDE prices for zero transaction costs and small values of . The values of in Table 1, are chosen very small555 In chapter 5 of Grinold and Kahn, (1999) are presented some common values for the risk aversion coefficient: , and for high, medium and low level of risk aversion respectively. for this purpose. An intuitive argument to justify this choice is that for , the utility function can be approximated by a linear utility and the investor can be considered risk neutral. A rigorous argument can be found in Barles and Soner, (1998), where the authors use asymptotic analysis for small values of , and to derive a nonlinear PDE for the option price. For zero transaction costs this equation corresponds to the Black-Scholes PDE. Their argument can be extended also to PIDEs.

| Convergence table | ||||

|---|---|---|---|---|

| Execution time | ||||

| 50 | 2.241214 | 2.241764 | 2.247311 | 0.01 0.004 |

| 100 | 2.249142 | 2.249506 | 2.253159 | 0.02 0.005 |

| 200 | 2.245422 | 2.245676 | 2.248216 | 0.11 0.02 |

| 400 | 2.246784 | 2.246959 | 2.248717 | 0.85 0.04 |

| 800 | 2.246288 | 2.246271 | 2.247635 | 8.63 0.1 |

| 1600 | 2.246576 | 2.246662 | 2.247515 | 82.44 2.71 |

| 3200 | 2.246412 | 2.246471 | 2.247068 | 910.8 10.5 |

| 3500 | 2.246366 | 2.246423 | 2.246993 | 1291.3 13 |

4.1 Diffusion results

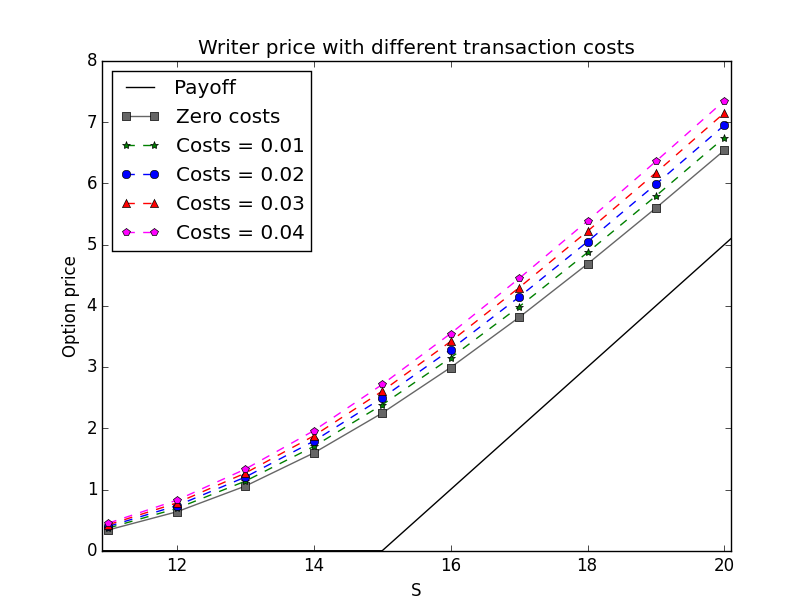

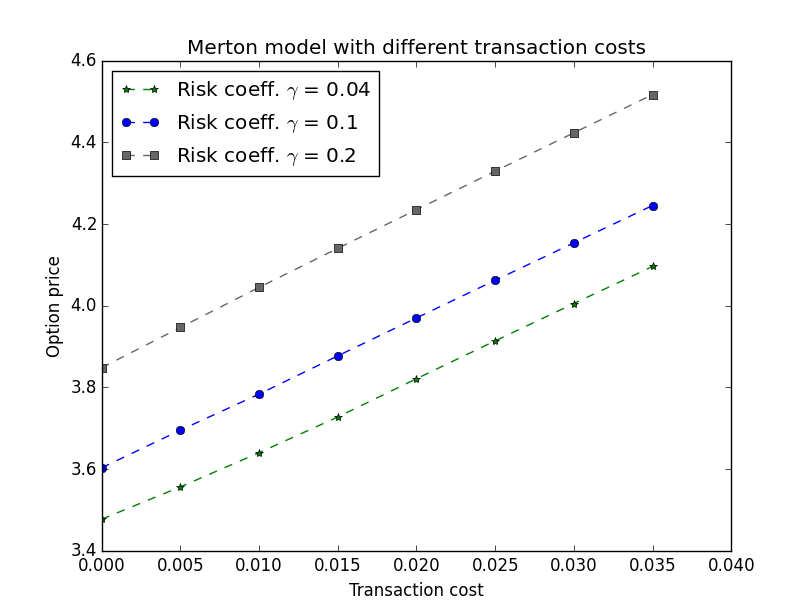

In the Figure 2 we show the diffusion writer and buyer prices with different transaction costs. We can see that a higher transaction cost corresponds to a higher writer price, while a lower transaction cost corresponds to a lower buyer price. In fact, the writer and buyer prices are respectively increasing and decreasing functions of the transaction cost, as already verified in Clewlow and Hodges, (1997). The prices in Figure 2, are calculated with time steps and . In the Table 3 we show ATM option prices for different values of , with and different risk aversion coefficients. For and the price is identical, up to the fourth decimal digit, to the original Black-Scholes price in Table 2. Using the values in Table 3 it is possible to estimate the rate of convergence. We also present the execution times, from which we can estimate the asymptotic time complexity of the algorithm. In Section (3.2) we stated that the computational complexity of the Algorithm [1] is . From the Table 3, we obtain the exponent , which is very close to the theoretical complexity value. The algorithm is written in Matlab using vectorized operations, and runs on an Intel i7 (7th Gen) with Linux.

4.2 Merton results

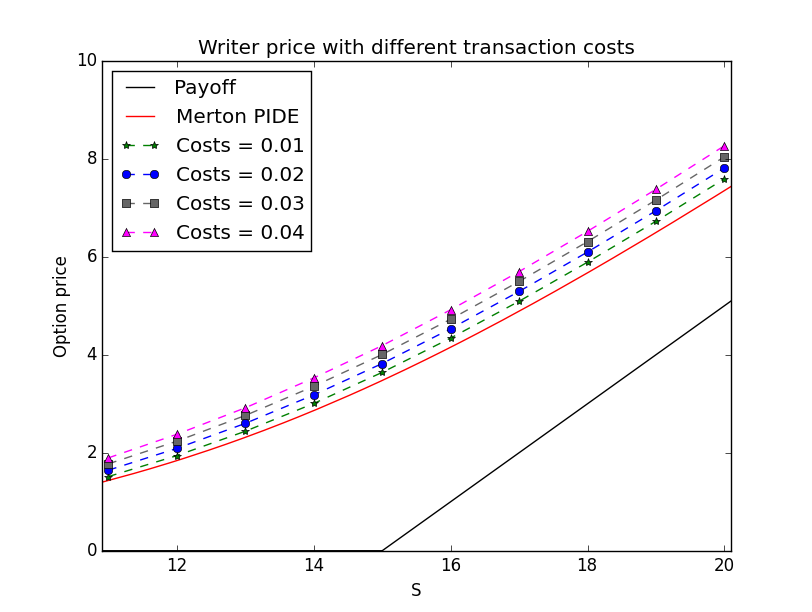

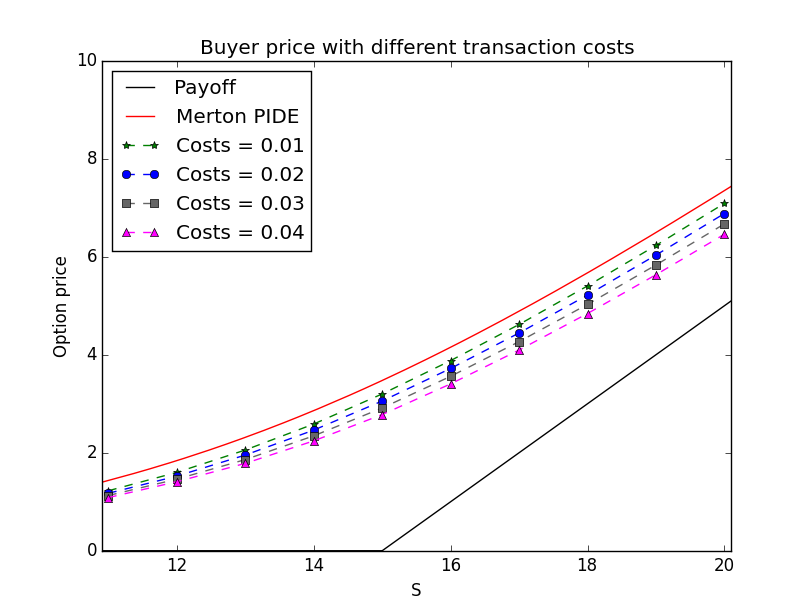

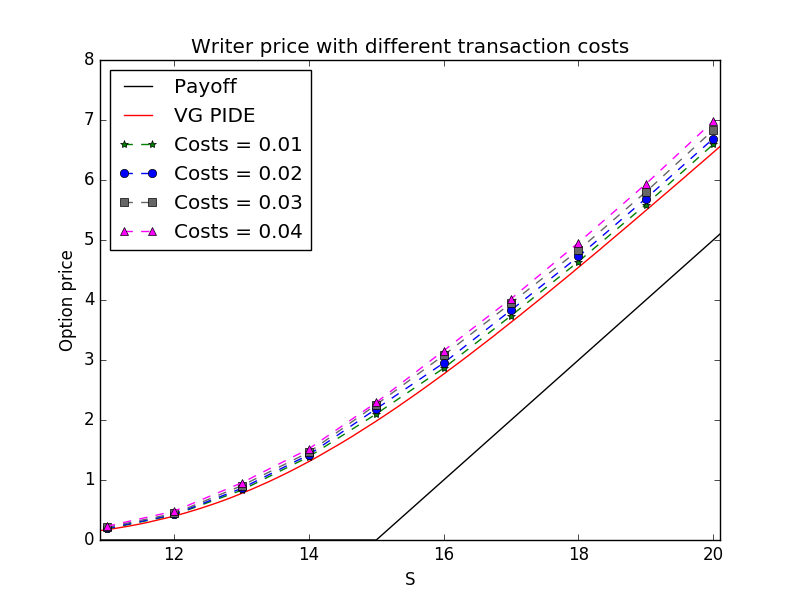

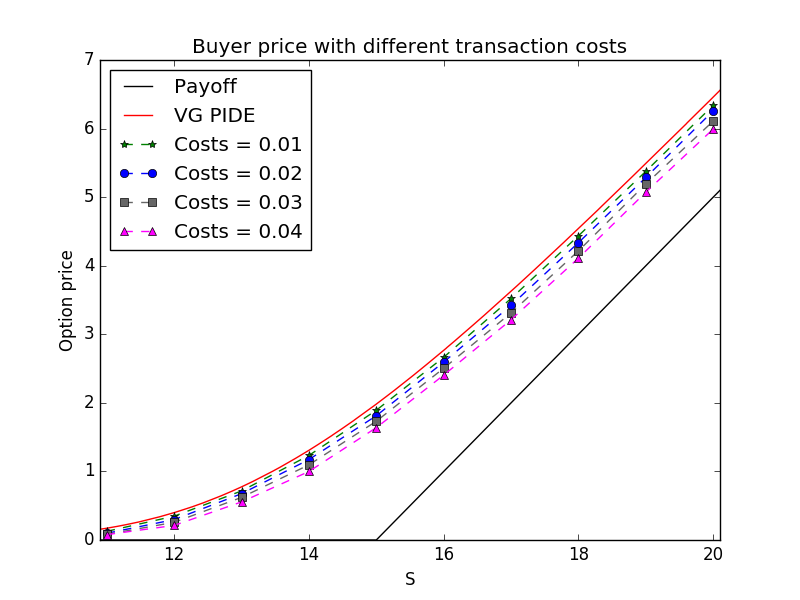

In the Figure 3 we show the writer and buyer prices for the Merton process, with parameters in Tab. 1.

An interesting feature of the multinomial tree construction for jump-diffusion processes is that .

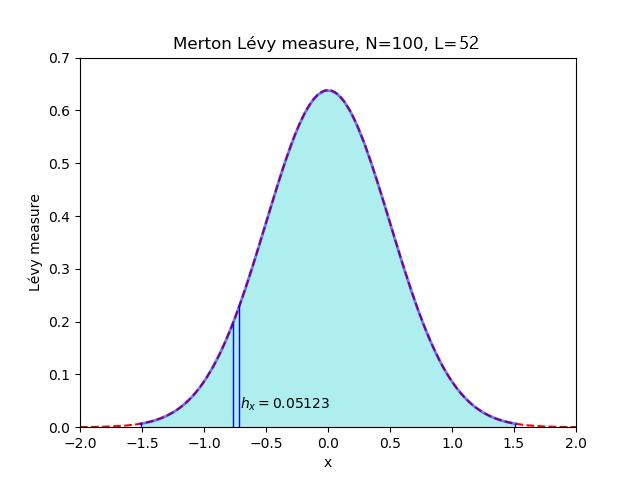

The integral domain is restricted to the bounded domain with length .

We choose the size of a space step and

with .

However, the size of the Poisson jumps does not scale with . So the number has to be chosen big enough in order

to have .

In general, for a fixed , the interval should be chosen as big as possible. In practice, the choice of the truncation depends on the shape of the Lévy measure.

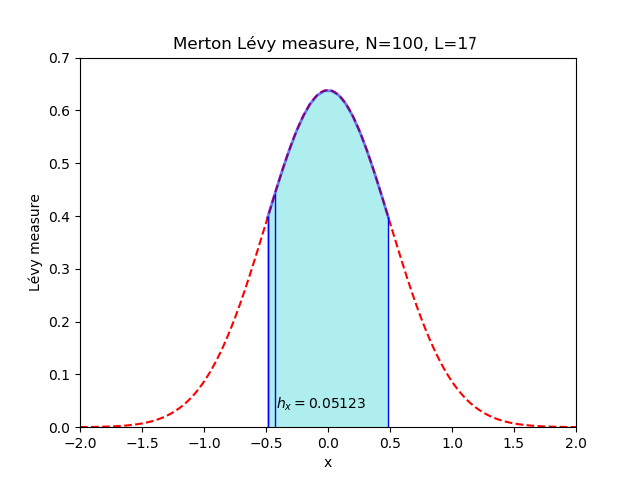

The Figures 5, 5 show two examples with and

respectively. These choices correspond to

and .

For the Merton Lévy measure (a scaled Normal distribution), a good choice is , where

is the variance of the jump component of the Merton process.

The length of the interval is thus .

It is well known that the integral over this region is about the of the total area.

Using this interval and the parameters in Tab. 1 we obtain the relation .

In the calculation of the Merton prices in Fig. 3, we used a discretization with , and ,

with a good balance between small computational time and small price error.

| Truncation error table | |||||

|---|---|---|---|---|---|

| 50 | 3.481318 | 3.481616 | 3.481617 | 3.481617 | 3.481617 |

| 100 | 3.468774 | 3.478806 | 3.479141 | 3.479146 | 3.479146 |

| 150 | 3.439090 | 3.474403 | 3.477574 | 3.477714 | 3.477742 |

| 200 | 3.399442 | 3.466338 | 3.476439 | 3.477234 | 3.477457 |

The convergence Tab. 4 shows different Merton prices for different values of and . Looking at the table from left to right, for each fixed it is possible to note how the truncation error decreases when increases.

| Convergence table | |||

|---|---|---|---|

| Price | Execution time | ||

| 50 | 61 | 3.481600 | 2.20 0.08 |

| 75 | 75 | 3.479980 | 15.15 0.07 |

| 100 | 91 | 3.479141 | 63.04 0.49 |

| 125 | 97 | 3.478254 | 148.4 1.16 |

| 150 | 105 | 3.477731 | 315.3 5.58 |

| 175 | 113 | 3.477610 | 585.7 10.57 |

| 200 | 121 | 3.477513 | 1106.0 12.2 |

In Table 5 we show several prices with increasing values of and . We choose big enough, such that the truncation error can be ignored. Given the high computational complexity of the algorithm, it is difficult to present prices with bigger values of ,. For larger values of and smaller , we expect a convergence to the Merton price in Tab. 2. The computational complexity in this case is expected to be . From the Table 5 we get the exponent equal to . This result is not so different from the theoretical value.

4.3 VG results

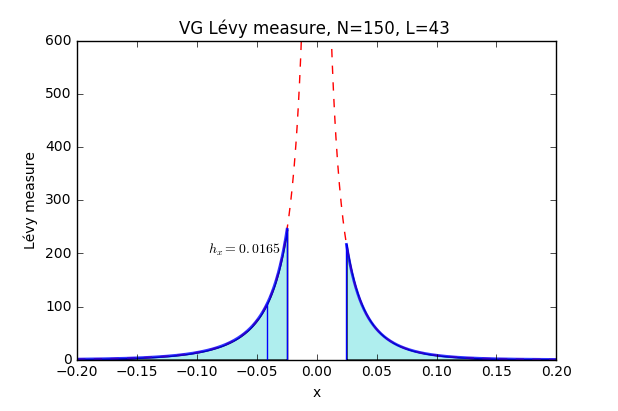

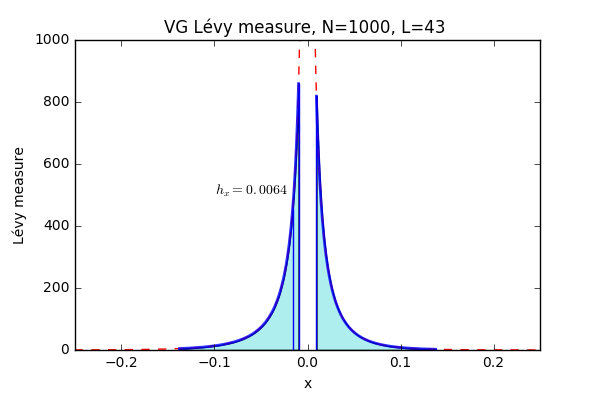

In the Figure 6 we show how the writer and buyer prices for the VG process change for several level of transaction costs (parameters in Tab. 1). In these computations we used and , such that the program can run in a reasonable amount of time. The integration region in (46) is restricted to with . The choice of and depends on the shape of the Lévy measure. In Fig. 8 and 8 we show two examples for the VG Lévy measure with , and , . The two Lévy measures are normalized, such that the integral on the region is equal to one. The area underlying the functions on is highlighted for clarity. For , we can see that in both cases it is possible to cover a very high percentage of the initial unrestricted region. We can conclude that, unlike the Merton measure, we do not need a big truncation interval. Given the space step , with and , it is enough to consider a region at least as big as the standard deviation of the unrestricted jump process666For small values of the value of is negligible. In this case it is possible to replace by the variance of the VG process . i.e. , where . Putting all together, the relation becomes , and replacing the values and we get .

| Convergence table | |||

|---|---|---|---|

| Price | Execution time | ||

| 50 | 4.73 | 1.910934 | 3.63 0.16 |

| 100 | 7.82 | 1.957806 | 26.54 0.26 |

| 150 | 10.01 | 1.982078 | 82.51 0.20 |

| 200 | 11.73 | 1.996180 | 185.2 0.81 |

| 250 | 13.14 | 2.004719 | 350.3 4.5 |

| 300 | 14.35 | 2.008536 | 654.2 7.3 |

| 350 | 15.40 | 2.009436 | 1236 12 |

In the Table 6 we present several option prices computed with different values of , but with fixed . For the VG process it is more difficult to analyze the convergence results. This is due to the approximation (3.1) introduced to replace the infinite activity jump component by a Brownian motion. All the parameters in (35) depend on , and consequently on . Within our discretization (), we have , . With the parameters under consideration, we obtain an ATM price for zero transaction costs of 1.9821, which is quite close to the PIDE price in Tab. 2.

The convergence rate of the VG PIDE is quite low and this is reflected in our algorithm. We refer to Cont and Voltchkova, (2005) for a detailed error analysis. In order to solve the PIDE (using an implicit-explicit scheme) we constructed a grid with 13000 space steps of size and 7000 time steps, and obtained the price in Tab 2, with an approximated activity . Consequently, we expect to have good convergence results in our algorithm when . All the presented prices (Figures 6) have thus a truncation error, which is adjusted by an accurate choice of the value of .

From Tab. 6 we can estimate the time complexity of this algorithm. The exponent is , indeed very close to the theoretical .

4.4 Properties of the model

| cost = 0 | cost = 0.01 | cost = 0.02 | cost = 0.03 | cost = 0.04 | |

|---|---|---|---|---|---|

| Merton | 3.4771 | 3.6400 | 3.8212 | 4.0054 | 4.1864 |

| VG | 1.9821 | 2.0921 | 2.1870 | 2.2568 | 2.3131 |

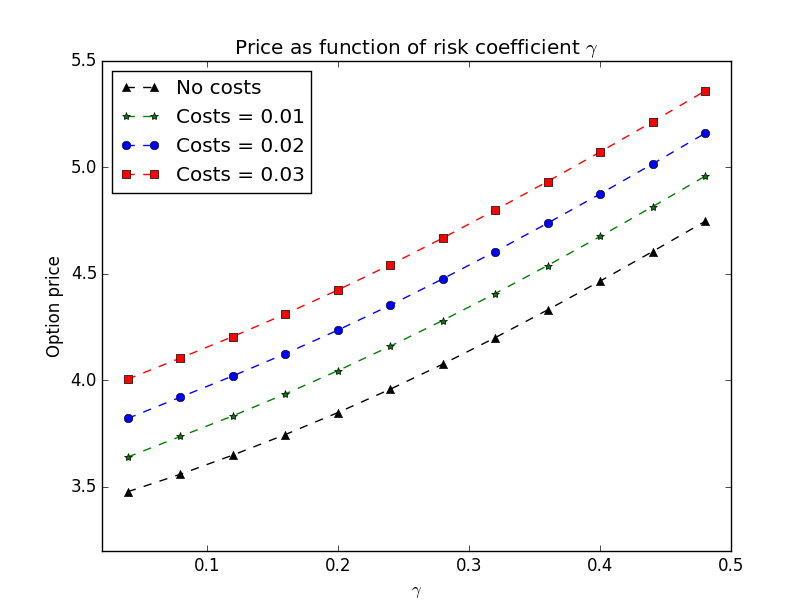

In this section we want to analyze the properties of the model and how the option price depends on the level of transaction costs , , and on the risk aversion parameter . In this numerical experiment, we use the Merton model with parameters of Tab. 1. In Tab. 7 we show the writer ATM option values for different transaction costs.

In Fig. 10 we can see better how the writer price is affected by the change of the transaction costs. The picture shows prices for different values of risk coefficient. The risk profile of the investor also plays an important role. As already shown in Hodges and Neuberger, (1989), the writer price is an increasing function of the risk aversion coefficient. Figure 10 confirms their results.

5 Conclusions

We presented a model for pricing options in presence of proportional transaction costs. This is an extension of the model first introduced by Hodges and Neuberger, (1989) and then formalized by Davis et al., (1993). The main difference between this work and the previous works in the literature is that we considered a stock dynamics that follows a general exponential Lévy process. In the present paper, we do not consider the case of bankruptcy in the numerical computations. The general Eq. (18) is a complicated equation with three state variables and a time variable, so we opted to simplify the problem by reducing the number of variables, in order to obtain the simpler HJB Eq. (31). The resulting optimization problem has been solved with the Markov chain approximation method. We proposed a monotone, stable and consistent numerical scheme and proved that its solution converges to the viscosity solution of the original HJB equation. Numerical results are obtained for diffusion, Merton jump-diffusion and Variance Gamma processes, although any Lévy process satisfying the conditions (3) can be used. The transition probabilities in the Markov chain approximation are obtained by explicit finite difference discretization of the infinitesimal generator of the process. The Brownian motion and the Merton process can be discretized directly, while the VG process needs to be approximated to remove the infinite activity jump component. Due to this approximation, the Algorithm [1] has lower performances when applied to the VG dynamics. Using numerical experiments, we confirmed some features of the model such as the relations of the price with the transaction costs and the risk aversion.

An interesting direction for future improvements, can be the development of a more efficient numerical method for solving the HJB Equation (31). There are several approaches in the literature for solving variational inequalities, such as the policy iteration method of Forsyth and Huang, 2012b , or the penalty method of Forsyth and Huang, 2012a , Wang and Li, (2014). We argue that a finite difference method based on the implicit/explicit scheme, with the possible help of the Fast-Fourier-Transform for evaluating the integral term, (as in Andersen and Andreasen, (2000) for instance) can increase the efficiency of the numerical method. Also, using a non-uniform grid as in Haentjens, (2013), can help to improve the efficiency and reduce the computational cost for both the differential and the integral part.

Acknowledgements

Our sincere thanks go to the Department of Mathematics of ISEG and CEMAPRE, University of Lisbon, http://cemapre.iseg.ulisboa.pt/. This research was supported by the European Union in the FP7-PEOPLE-2012-ITN project STRIKE - Novel Methods in Computational Finance (304617), http://www.itn-strike.eu/, and by CEMAPRE MULTI/00491, financed by FCT/MEC through Portuguese national funds. We wish also to acknowledge all the members of the STRIKE network.

Appendix A Martingale option pricing

Under a risk neutral measure , the dynamics of the stock price is described by the exponential Lévy model: where is the risk free interest rate, and is a Lévy process with Lévy triplet . Under the discounted price is a -martingale: , such that . This implies the following condition:

| (A.1) |

Let be the value of a European call option. It satisfies the following partial integro-differential equation (PIDE):

| (A.2) |

where is the infinitesimal generator of . When , if is a Brownian motion with triplet , using the condition (A.1) the infinitesimal generator is:

| (A.3) |

and the Eq. (A.2) becomes the well known Black-Scholes PDE. When is a Merton or VG process, the associated infinitesimal generators are (42) and (46) respectively, and we obtain the Merton and Variance Gamma PIDEs 777In the generator formulas, using (7) and (A.1), the parameter is replaced by .. The value of the call option is the solution of the PIDE (A.2) with the usual boundary conditions:

-

•

Payoff:

-

•

Lateral conditions:

Appendix B Properties of the Markov chain

B.1 Transition probabilities

Let us indicate the transition probabilities of by:

| (B.1) |

The number of jumps of a jump-diffusion process is Poisson distributed, i.e. , with . In a small interval , we can compute the first order approximated probabilities:

-

•

,

-

•

.

Let us consider the discrete dynamics of in Eq. (36). We assume that in a small time step the process jumps exactly once (), or does not jump at all (). The two possible mutually exclusive events are:

-

•

Diffusion. The transition probability is and . for .

-

•

Jumps. The transition probability is . The random variable takes values in (or ).

By conditioning on the values of , the total transition probability is

| (B.2) | ||||

The request of a positive probability impose a restriction on the time step size . In this section we showed that the transition probability of is a convex combination of and , as required by the property (37). We refer to Chapter 5.6 of Kushner and Dupuis, (2001) for more details.

B.2 Infinitesimal generator discretization

In this section we provide an explicit form for the transition probabilities. This can be achieved by discretizing the infinitesimal generator of the process in (32), which corresponds to the first term inside the “min” in the HJB Equation (31). In the following steps we consider only the finite activity case, but the same idea works for an infinite activity process after using the Brownian approximation. In fact, the only difference between (33) and (3.1) is the truncation in the integral.

In this section we drop the variable from , because we are interested only in the uncontrolled log-price dynamics. Let us assume for convenience that is smooth enough, the derivatives are discretized by the finite differences:

-

•

Backward approximation in time: .

-

•

Central approximation in space: .

-

•

Second order in space: .

The integral terms in (31) are truncated and restricted to the domain 888If the integral has a truncation parameter as in (46), we choose and the restricted domain becomes . . The discretization is obtained by approximating the integral by Riemann sums (see Cont and Voltchkova, (2005)):

| (B.3) |

where

| (B.4) |

We define the discrete version of , and :

| (B.5) |

The jump transition probabilities can be defined as:

| (B.6) |

The discretized equation becomes:

| (B.7) | |||

Rearranging the terms we get:

where we defined:

| (B.8) | ||||

and for . From we obtain an important restriction on the time step size: , while the condition obtained from and i.e. is easily satisfied. If we bring the term on the right hand side and use the first order Taylor approximation , we obtain:

| (B.9) | ||||

where

| (B.10) |

is the total transition probability, written in the form (37). It is straightforward to check that . Let us check that also the local consistency conditions (38) are satisfied at first order in :

We introduced , and indicate . The discrete moments match the continuous moments when and such that , and .

Appendix C Proofs of Theorems 3.1 and 3.2

Let us indicate the Eq. (31) by:

| (C.1) |

where is the integral operator and . We assume that (see Section 2.5), and following De Vallière et al., (2016) we introduce the definition of viscosity solution.

Definition C.1.

Let us prove the three properties separately.

With the square brackets, as in , we indicate all the possible values such that .

The scheme is monotone i.e. for all , it holds

Proof.

Let us write the Scheme [1] as

Since , for all , and for all , the scheme is a decreasing function of . ∎

The scheme is stable i.e. for any there exists a bounded solution , with bound independent of This is equivalent to prove that , for any and for independent on .

Proof.

The terminal conditions (25), (26), (27) are positive bounded functions in a bounded domain. Therefore we can write for all , and does not depend on . Since all the coefficients are non-negative, it follows that the scheme is sign preserving i.e. for all . We can write:

This holds for all , then . Iterating we obtain:

∎

The scheme is consistent i.e. for any smooth function

with .

Proof.

Now we look at the following cases, corresponding to each minimum value in the Scheme [1]:

1) For some , it holds

2) For some , an analogous computation leads to

3) When let us consider the expression (B.10), and expand and using (B.2) and (B.6):

Let us replace all the terms at by using the first order Taylor approximation . The two terms in can be rewritten as . Using the approximation (B.3) and (B.4) we obtain

When sending , and we obtain the desired result for all 1) 2) and 3). ∎

The proof follows closely Barles and Souganidis, (1991).

Proof.

We only prove the subsolution case, since the arguments for the supersolution are identical.

Let the strict global maximum of for some , and such that .

Then there exist sequences and such that for :

, , and is a global maximum of .

Let us define , such that when . For any it holds .

Let us consider the Scheme [1]:

where we used the monotonicity property. By sending and thanks to the consistency property, we obtain:

∎

References

- Andersen and Andreasen, (2000) Andersen, L. and Andreasen, J. (2000). Jump-diffusion processes: Volatility smile fitting and numerical methods for pricing. Rev. Derivatives Research, 4:231 – 262.

- Applebaum, (2009) Applebaum, D. (2009). Lévy Processes and Stochastic Calculus. Cambridge University Press; 2nd edition.

- Barles and Soner, (1998) Barles, G. and Soner, H. M. (1998). Option pricing with transaction costs and a nonlinear Black-Scholes equation. Finance and Stochastics, 2(4):369–397.

- Barles and Souganidis, (1991) Barles, G. and Souganidis, P. (1991). Convergence of approximation schemes for fully nonlinear second order equations. J. Asymptotic Analysis, 4:271–283.

- Benth et al., (2002) Benth, F., Karlsen, K., and Reikvam, K. (2002). Portfolio optimization in a Lévy market with intertemporal substitution and transaction costs. Stochastics and Stochastics Report, 74(3-4):517–569.

- Black and Scholes, (1973) Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities. The Journal of Political Economy, 81(3):637–654.

- Carmona, (2009) Carmona, R. (2009). Indifference Pricing. Princeton University Press.

- Clewlow and Hodges, (1997) Clewlow, L. and Hodges, S. (1997). Optimal delta hedging under transaction costs. Jornal of Economic Dynamics and Control, 21:1353–1376.

- Cont, (2001) Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2):223–236.

- Cont and Tankov, (2003) Cont, R. and Tankov, P. (2003). Financial Modelling with Jump Processes. Chapman and Hall/CRC; 1 edition.

- Cont and Voltchkova, (2005) Cont, R. and Voltchkova, E. (2005). A finite difference scheme for option pricing in jump diffusion and exponential Lévy models. SIAM Journal of numerical analysis, 43(4):1596–1626.

- Damgaard, (1998) Damgaard, A. (1998). Optimal Portfolio Choice and Utility Based Option Pricing in Markets with Transaction Costs. PhD thesis, School of Business and Economics, Odense University.

- Davis and Panas, (1994) Davis, M. H. A. and Panas, V. G. (1994). The writing price of a European contingent claim under proportional transaction costs. Computational and Applied Mathematics, 13(2):0101–8205.

- Davis et al., (1993) Davis, M. H. A., Panas, V. G., and Zariphopoulou, T. (1993). European option pricing with transaction costs. SIAM J. Control Optim., 31(2):470–493.

- De Vallière et al., (2016) De Vallière, D., Kabanov, Y., and Lépinette, E. (2016). Consumption-investment problem with transaction costs for lévy-driven price processes. Finance and Stochastics, 20(3):705–740.

- Fleming and Soner, (2005) Fleming, W. H. and Soner, M. H. (2005). Controlled Markov Processes and Viscosity Solutions. Springer; 2nd edition.

- Florescu et al., (2014) Florescu, I., Mariani, M. C., and Sengupta, I. (2014). Option pricing with transaction costs and stochastic volatility. Electronic Journal of Differential Equations, 2014(165):1–19.

- (18) Forsyth, P. and Huang, Y. (2012a). Analysis of a penalty method for pricing a guaranteed minimum withdrawal benefit (gmwb). IMA, Journal of Numerical Analysis, 32:320–351.

- (19) Forsyth, P. and Huang, Y. (2012b). Iterative methods for solution of the singular control formulation of a gmwb pricing problem. Numerische Mathematik, 122:133–167.

- Framstad et al., (1999) Framstad, N., Øksendal, B., and Sulem, A. (1999). Optimal consumption and portfolio in a jump diffusion market with proportional transaction costs. Journal of Mathematical Economics, 35:233–257.

- Grinold and Kahn, (1999) Grinold, R. C. and Kahn, R. N. (1999). Active Portfolio Management. McGraw-Hill Education; 2 edition.

- Haentjens, (2013) Haentjens, T. (2013). Efficient and stable numerical solution of the heston–cox–ingersoll–ross partial differential equation by alternating direction implicit finite difference schemes. International Journal of Computer Mathematics, 90(11):2409–2430.

- Hodges and Neuberger, (1989) Hodges, S. D. and Neuberger, A. (1989). Optimal replication of contingent claims under transaction costs. The Review of Future Markets, 8(2):222–239.

- Kushner and Dupuis, (2001) Kushner, H. and Dupuis, P. G. (2001). Numerical Methods for Stochastic Control Problems in Continuous Time. Springer; 2nd ed.

- Kushner and Martins, (1991) Kushner, H. J. and Martins, F. L. (1991). Numerical methods for stochastic singular control problems. SIAM Journal of Control and Optimization, 29(6):1443–1475.

- Leland, (1985) Leland, H. (1985). Option pricing and replication with transaction costs. The Journal of Finance, 40(5):1283–1301.

- Madan et al., (1998) Madan, D., Carr, P., and Chang, E. (1998). The Variance Gamma process and option pricing. European Finance Review, 2:79–105.

- Madan and Seneta, (1990) Madan, D. and Seneta, E. (1990). The Variance Gamma (V.G.) model for share market returns. The journal of Business, 63(4):511–524.

- Merton, (1976) Merton, R. (1976). Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics, 3:125–144.

- Mocioalca, (2007) Mocioalca, O. (2007). Jump diffusion options with transaction costs. Revue Roumaine de Mathematiques Pures et Appliquees, 52(3):349–366.

- Monoyios, (2003) Monoyios, M. (2003). Efficient option pricing with transaction costs. Journal of Computational Finance, 7:107–128.

- Monoyios, (2004) Monoyios, M. (2004). Option pricing with transaction costs using a Markov chain approximation. Jornal of Economic Dynamics and Control, 28:889–913.

- Sato, (1999) Sato, K. I. (1999). Lévy processes and infinitely divisible distributions. Cambridge University Press.

- Sengupta, (2014) Sengupta, I. (2014). Option pricing with transaction costs and stochastic interest rate. Applied Mathematical Finance, 21(5):399–416.

- Wang and Li, (2014) Wang, S. and Li, W. (2014). A numerical method for pricing european options with proportional transaction costs. Journal of Global Optimization, 60(1):59–78.

- Whalley and Wilmott, (1997) Whalley, A. E. and Wilmott, P. (1997). An asymptotic analysis of an optimal hedging model for option pricing with transaction costs. Mathematical Finance, 7(3):307–324.