Essentially high-order compact schemes with application to stochastic volatility models on non-uniform grids

Abstract

We present high-order compact schemes for a linear second-order parabolic partial differential equation (PDE) with mixed second-order derivative terms in two spatial dimensions. The schemes are applied to option pricing PDE for a family of stochastic volatility models. We use a non-uniform grid with more grid-points around the strike price. The schemes are fourth-order accurate in space and second-order accurate in time for vanishing correlation. In our numerical convergence study we achieve fourth-order accuracy also for non-zero correlation. A combination of Crank-Nicolson and BDF-4 discretisation is applied in time. Numerical examples confirm that a standard, second-order finite difference scheme is significantly outperformed.

1 Introduction

We consider the following parabolic partial differential equation for

in two spatial dimensions and time,

| (1) |

subject to suitable boundary conditions and initial condition with and with for . The functions , , , map to , and , , , and are assumed to be in and for all . We define a uniform spatial grid with step size in direction for . Setting and applying a standard, second-order central difference approximation leads to the elliptic problem

| (2) |

with , where denotes the central difference operator in direction, and if for . We call a finite difference scheme high-order compact (HOC) if its consistency error is of order for for , and it uses only points on the compact stencil, with and , to approximate the solution at .

2 Auxiliary relations for higher derivatives

Our aim is to replace the third- and fourth-order derivatives in (1) which are multiplied by second-order terms by equivalent expressions which can be approximated with second order on the compact stencil. Indeed, if we differentiate (1) (using ) once with respect to (), we obtain relations

| (3) |

where we can discretise with second order on the compact stencil using the central difference operator. Analogously, we obtain

| (4) | ||||||

where we can approximate and with second order on the compact stencil using the central difference operator. A detailed derivation can be found in [3, 5].

3 Derivation of high-order compact schemes

In general it is not possible to obtain a HOC scheme for (1), since there are four fourth-order derivatives in (1), but only three auxiliary equations for these in (2). Hence, we propose four different versions of the numerical schemes, where only one of the fourth-order derivatives in (1) is left as a second-order remainder term. Using (3) and (2) in (1) we obtain as Version 1 scheme

| (5) | ||||

as Version 2 scheme

| (6) | ||||

as Version 3 scheme

| (7) | ||||

and, finally, as Version 4 scheme

| (8) | ||||

Employing the central difference operator with for to discretise in (5)–(8) and neglecting the remaining lower-order term leads to four semi-discrete (in space) schemes. A more detailed description of this approach can be found in [3, 5]. When or these schemes are fourth-order consistent in space, otherwise second-order.

In time, we apply the implicit BDF4 method on an equidistant time grid with stepsize . The necessary starting values are obtained using a Crank-Nicolson time discretisation, where we subdivide the first timesteps with a step size to ensure the fourth-order time discretisation in terms of .

With additional information on the solution of (1) even better results are possible. If the specific combination of pre-factors in (1) and the higher derivatives in the second-order terms is sufficiently small, the second-order term dominates the computational error only for very small step-sizes . Before this error term becomes dominant one can observe a fourth-order numerical convergence. In this case we call the scheme essentially high-order compact (EHOC).

4 Application to option pricing

In this section we apply our numerical schemes to an option pricing PDE in a family of stochastic volatility models, with a generalised square root process for the variance with nonlinear drift term,

with , a correlated, two-dimensional Brownian motion, , as well as drift of the stock price , long run mean , mean reversion speed , and volatility of volatility . For one obtains the standard Heston model, for the SQRN model, see [1]. Using Itô’s lemma and standard arbitrage arguments, the option price solves

| (9) |

where and with . For a European Put with exercise price we have the final condition . The transformations , as well as [2], lead to

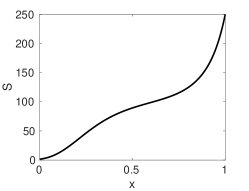

with initial condition . The function is considered to be four times differentiable and strictly monotone. It is chosen in such a way that grid points are concentrated around the exercise price in the – plane when using a uniform grid in the – plane.

Dirichlet boundary conditions are imposed at and similarly as in [2],

for all and At the boundaries and we employ the discretisation of the interior spatial domain and extrapolate the resulting ghost-points using

for . Third-order extrapolation is sufficient here to ensure overall fourth-order convergence [4].

5 Numerical experiments

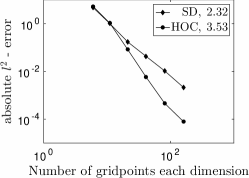

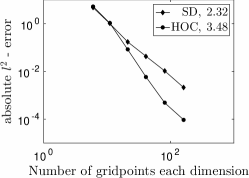

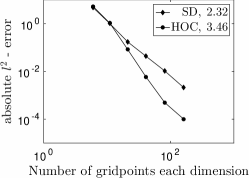

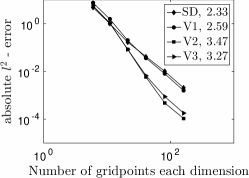

We employ the function where , and . We use , , , , , , , , , , and . Hence, . For the Crank-Nicolson method we use , for the BDF4 method . We smooth the initial condition according to [6, 3], so that the smoothed initial condition tends towards the original initial condition for . We neglect the case (Heston model), since a numerical study of that case has been performed in [2]. In the numerical convergence plots we use a reference solution on a fine grid () and report the absolute -error compared to . The numerical convergence order is computed from the slope of the linear least square fit of the points in the log-log plot.

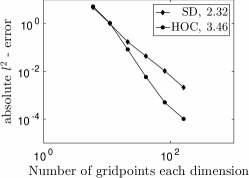

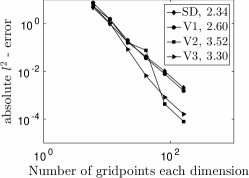

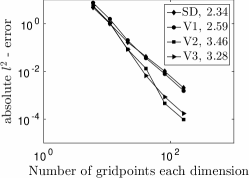

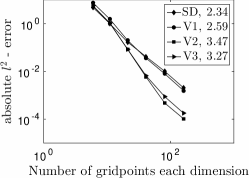

Figure 1(a) shows the transformation from to . The transformation focuses on the region around the strike price. Figures 1(b), 1(c), 1(d) and 1(e) show that the HOC schemes lead to a numerical convergence order of about , whereas the standard, second-order central difference discretisation (SD) leads to convergence orders of about , in the case of vanishing correlation. In all cases with non-vanishing correlation () we observe only slightly improved convergence for Version 1 (V1) when comparing it to the standard discretisation. Version 2 (V2) and Version 3 (V3), however, lead to similar convergence orders as the HOC scheme, even for non-vanishing correlation. Results of Version 4 are not shown as this scheme shows instable behaviour in this example.

In summary, we obtain high-order compact schemes for vanishing correlation and achieve high-order convergence also for non-vanishing correlation for the family (9) of stochastic volatility model. A standard, second-order discretisation is significantly outperformed in all cases.

Acknowledgment

BD acknowledges support by the Leverhulme Trust research project grant ‘Novel discretisations for higher-order nonlinear PDE’ (RPG-2015-69). CH was supported by the European Union in the FP7-PEOPLE-2012-ITN Program under Grant Agreement Number 304617 (FP7 Marie Curie Action, Project Multi-ITN STRIKE – Novel Methods in Computational Finance).

References

- [1] P. Christoffersen, K. Jacobs and K. Mimouni. Models for S&P500 dynamics: evidence from realized volatility, daily returns, and option prices. Rev. Financ. Stud., 23(8):3141–3189, 2010.

- [2] B. Düring, M. Fournié and C. Heuer. High-order compact finite difference schemes for option pricing in stochastic volatility models on non-uniform grids. J. Comput. Appl. Math., 271(18):247–266, 2014.

- [3] B. Düring and C. Heuer. High-order compact schemes for parabolic problems with mixed derivatives in multiple space dimensions. SIAM J. Numer. Anal., 53(5):2113–2134, 2015.

- [4] B. Gustafsson. The convergence rate for difference approximations to general mixed initial-boundary value problems. SIAM J. Numer. Anal., 18(2):179–190, 1981.

- [5] C. Heuer. High-order compact finite difference schemes for parabolic partial differential equations with mixed derivative terms and applications in computational finance. PhD thesis, University of Sussex, August 2014. http://sro.sussex.ac.uk/49800/

- [6] H.O. Kreiss, V. Thomee and O. Widlund. Smoothing of initial data and rates of convergence for parabolic difference equations. Commun. Pure Appl. Math., 23:241–259, 1970.