Pseudo-marginal Metropolis–Hastings using averages of unbiased estimators

Abstract

We consider a pseudo-marginal Metropolis–Hastings kernel that is constructed using an average of exchangeable random variables, as well as an analogous kernel that averages of these same random variables. Using an embedding technique to facilitate comparisons, we show that the asymptotic variances of ergodic averages associated with are lower bounded in terms of those associated with . We show that the bound provided is tight and disprove a conjecture that when the random variables to be averaged are independent, the asymptotic variance under is never less than times the variance under . The conjecture does, however, hold when considering continuous-time Markov chains. These results imply that if the computational cost of the algorithm is proportional to , it is often better to set . We provide intuition as to why these findings differ so markedly from recent results for pseudo-marginal kernels employing particle filter approximations. Our results are exemplified through two simulation studies; in the first the computational cost is effectively proportional to and in the second there is a considerable start-up cost at each iteration.

1 Introduction

The Metropolis–Hastings algorithm is often used to approximate expectations with respect to posterior distributions, making use of point-wise evaluations of the posterior density up to a fixed but arbitrary constant of proportionality. In cases where such evaluations are infeasible, the pseudo-marginal Metropolis–Hastings algorithm Beaumont, (2003); Andrieu and Roberts, (2009) can be used if a realisation of a non-negative, unbiased stochastic estimator of the target density, possibly up to an unknown normalisation constant, is available. These estimators can, for example, be constructed using importance sampling (Beaumont,, 2003), a particle filter or sequential Monte Carlo Andrieu et al., (2010).

A key tuning parameter of such pseudo-marginal algorithms is the number of samples or particles, which we denote by , and we are interested in the relationship between and the computational efficiency of the pseudo-marginal algorithm for approximating posterior expectations. The algorithm is a type of Markov chain Monte Carlo method: a Markov chain with stationary distribution is simulated for a finite number of steps in order to compute an appropriately normalised partial sum. This quantity then serves as an approximation of a limiting ergodic average that is almost surely equal to the expectation of interest. One natural measure of computational inefficiency, defined precisely in the sequel, is the asymptotic variance of the ergodic average of interest multiplied by the computational effort required to simulate each value of the Markov chain. Andrieu and Vihola, (2015) showed that the asymptotic variance for a pseudo-marginal algorithm is bounded below by the asymptotic variance of an idealised algorithm in which is evaluated exactly, so one can think of the relative asymptotic variance of a pseudo-marginal ergodic average as its asymptotic variance divided by the asymptotic variance of the idealised ergodic average. In some senses, this idealised algorithm is approached as and one might suppose that the relative asymptotic variance should therefore decrease to as increases. This is indeed true for estimators that arise from importance sampling (Andrieu and Vihola,, 2016), at least when the asymptotic variance is finite for some finite . An important issue, then, is whether the decrease in asymptotic variance at the expense of increased computational effort is justified in terms of computational efficiency.

In this article, we consider arbitrary pseudo-marginal algorithms where the posterior density is estimated using an average of unbiased estimators, such as with importance sampling, and we show that in all such cases the asymptotic variance when samples are used is not much smaller than the asymptotic variance when a single sample is used, divided by . Thus if the computational cost is roughly proportional to , as is often the case, there is little, if any, gain in using more than one sample. This formalises empirical observations made in Section 3.4 of an early version of Sherlock et al., (2015) (available at http://arxiv.org/abs/1309.7209v1), and generalises the main result of Bornn et al., (2016), which assumes that the pseudo-marginal kernels are positive and the estimators to be averaged are independent and take only one non-zero value. We demonstrate that our bound is tight and illustrate it through two simulation studies. In the second study, an additional fixed and large cost is associated with simulating samples, so that the computational efficiency is maximised at some . Our result also implies that asymptotic variance being infinite for implies that it is infinite for all finite . The theory also suggests that when parallel computation is feasible, it should be close to optimal to obtain one estimate on each core and then to average these. We discuss why this result differs so markedly from the particle-filter scenario, which was analyzed under significantly stronger conditions than here by Sherlock et al., (2015) and Doucet et al., (2015).

We adopt the notation ; for an integer , we set . For a probability measure on some measurable space and a -integrable test function , we define and use the notation to designate the usual Hilbert space with norm .

2 Main results

2.1 Asymptotic variance of ergodic averages and accept-reject kernels

Consider a Markov transition kernel with invariant distribution and associated Markov chain with . For any , an estimator of is the ergodic average and the asymptotic variance of the ergodic average is

All Markov kernels in this article involve accepting or rejecting a sample from a proposal kernel according to an acceptance probability . We define the marginal acceptance probability from , . The kernel is then of the form

| (1) |

2.2 Pseudo-marginal Metropolis–Hastings

Let be a probability distribution on , where denotes a dominating measure, and be a proposal kernel with density , i.e. . The -reversible Metropolis–Hastings kernel associated with is defined via (1) by taking the acceptance probability where is the Metropolis–Hastings ratio,

When pointwise relative evaluation of the density is not possible, is intractable. The pseudo-marginal Metropolis–Hastings algorithm introduces an unbiased approximation to the posterior, , where is a vector of auxiliary random variables. We will be interested in the random variable which satisfies . The pseudo-marginal algorithm simulates a Metropolis–Hastings Markov chain on the extended state space with proposal density and invariant density , i.e. proposals are accepted with the usual Metropolis–Hastings ratio, which in this case reads . Importantly, admits as its -marginal.

2.3 Pseudo-marginal algorithm using averages

Suppose that for each it is possible to generate an unbiased non-negative estimator of the target density , i.e. for any . For any integer , one may use an average of such estimators to construct the unbiased estimator . In what follows, we assume is exchangeable with joint density . This accommodates the scenario where are independent and distributed according to so . We denote the associated kernel, acceptance probability and marginal acceptance probability by , and , respectively.

Corollary of Andrieu and Vihola, (2016) shows that, for two positive integers , asymptotic variances associated with are at most those associated with for functions of the -coordinate only. Given this ordering, it is natural to ask whether the decrease in asymptotic variance is sufficient to justify the extra computational expense of . Andrieu and Vihola, (2015) show that the asymptotic variance of a pseudo-marginal algorithm ergodic average is bounded below by that of the algorithm in which is evaluated exactly; consequently, there must eventually be diminishing returns for any increase in . For functions of the -coordinate only we are interested in . A reduction in variance equivalent to that obtained by increasing from to could instead be obtained by increasing by a factor of . Since computational time is proportional to , if it is also proportional to the number of samples per iteration, , a natural way of comparing the two Markov kernels and is through their computational inefficiencies and , respectively. As shown in the sequel, these quantities are not ordered in general but Theorem 1 below shows that the quantities are. Since in many situations this can be viewed as almost ordering computational inefficiencies.

Theorem 1.

For positive integers , the pseudo-marginal kernels and satisfy

| (2) |

for any function of the -coordinate only.

Remark 1.

The inequality (8) in the proof also implies through fairly simple manipulations that the average acceptance rates satisfy .

One interesting consequence is that the class of functions with finite asymptotic variance, which is often not all of (Lee and Łatuszyński,, 2014), cannot be enlarged by increasing .

Corollary 1.

In combination with Corollary 31 of Andrieu and Vihola, (2016) we obtain that for , .

For a positive -reversible Markov kernel , for all . Consequently, Theorem 1 leads to the following generalisation of Proposition of Bornn et al., (2016).

Corollary 2.

Let be positive integers and Markov kernel be positive. For any function of the -coordinate only, .

Positivity of some random-walk-based kernels can be verified via results of Doucet et al., (2015) and Sherlock, (2016), which build upon Baxendale, (2005). Independent Metropolis–Hastings pseudo-marginal kernels are always positive, as they are themselves independent Metropolis–Hastings kernels (Andrieu and Vihola,, 2015).

2.4 Tightness of the result

The following proposition shows that the inequality in Theorem 1 cannot be improved in general, and that even if we consider averages of independent estimators the conjecture that is not true in general.

Proposition 1.

There exist pseudo-marginal kernels and such that

-

1.

With negatively correlated , .

-

2.

With independent , .

The conjectured inequality, however, does hold in continuous time. Let be an integer. We define the continuous-time Markov chain, with kernel , as the Markov chain whose transitions are identical to those of the discrete-time kernel but take place on a Poisson clock with unit rate. That is, if is the -process of a continuous-time Markov chain with transition and is the -process of the discrete-time Markov chain with kernel , then where designates a Poisson process with unit rate. For , the continuous-time asymptotic variance is defined as

Proposition 2.

For positive integers , the continuous-time chains satisfy

3 Numerical Studies

3.1 Preliminaries

We present in this Section two numerical studies. Several choices of proposal distributions are investigated and the situation when the computational time necessary to generate samples is not proportional to , due to non-negligible computational overhead, is carefully examined. Computational efficiency is measured in terms of Effective Sample Size per unit of computational time; if the computational time to generate samples in each of iterations is exactly proportional to , then we define and . Since and are intractable in general, we consistently estimate it below using realisations of the Markov chain with kernel .

3.2 Inverse Stochastic Heat Equation

We consider in this section, the problem of reconstructing the initial temperature field at time and from noisy measurements at time distributed as for some locations and independent centred Gaussian samples with variance . The temperature fields evolves according to the stochastic Heat equation

with Dirichlet boundary , and where is a space-time white noise; for the simulations, we chose and . A priori, we use a truncated Karhunen–Loève expansion to model , i.e. , where are independent. Simulations were carried out by standard forward discretization of the stochastic partial differential equations. The pseudo-marginal algorithms are started in a region of high posterior mass; we used a Crank–Nicholson proposal of the type , where is distributed according to the prior distribution, with a value of chosen such that the acceptance rate when is around . The computational efficiency is taken as the minimum computational efficiency associated with functions for . Table 1 shows approximate % confidence intervals and, as expected, the computational efficiency is maximized for .

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| CE |

3.3 Logistic regression using a latent Gaussian process

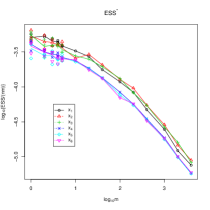

We consider a logistic regression model with fixed effects and a latent Gaussian process, following exactly the approach of Sherlock, (2016). The likelihood function is approximated by importance sampling with a data-dependent proposal distribution, similar to Filippone and Girolami, (2014) and Giorgi et al., (2015). The parameter space has dimension and the latent Gaussian process is required at observation points. Whatever the value of , at each iteration, creation of the importance sampling proposal involves a single Cholesky decomposition of an matrix; each importance sample then costs . For small values of the start-up cost dominates the cost of simulating importance samples.

The posterior mean and covariance matrix of the parameters were estimated from a trial run. For the random-walk pseudo-marginal Metropolis algorithm with , an approximately optimal scaling of was found. This scaling was then used in all runs recorded since it should also be approximately optimal for other values of Sherlock, (2016), and thus help to control the Monte Carlo variability in empirical effective sample sizes. A set of numbers of importance samples was considered. For , the pseudo-marginal algorithm was run for iterations and thinned for storage by a factor of . For larger values the run-lengths and thinning factors were respectively and (), and (), and and (). These run lengths kept the CPU time for each run between and seconds and the effective sample sizes above . Despite the large run lengths, the Monte Carlo variability was non-negligible for and so three independent runs were performed for each of these values.

Figure 1 reports the average acceptance rate, the hypothetical computational efficiencies, , and the empirical computational efficiencies, ess divided by CPU time, for all six parameters. Due to the non-negligible computational overhead, the two efficiency measures are significantly different. A pseudo-marginal independence sampler was also run and gave similar results. As the theory suggests, increasing from to samples never increases the acceptance rate by more than and the hypothetical computational efficiency is maximised at . However, due to the considerable start-up cost at each iteration, the empirical computational efficiency is maximised at around . Interestingly, it is at that the cost of creating samples approximately matches the start-up cost.

4 Averaging versus particle filtering

We have shown that if the computational cost of obtaining estimators is proportional to then it is close to optimal to choose when averaging, at least when the asymptotic variance is finite. This is very different to Sherlock et al., (2015) and Doucet et al., (2015), who found under specific assumptions that when the likelihood function of a large number of observations is estimated via a particle filter, should be chosen so that the variance of the the log-likelihood estimator is controlled: the optimal choice of is consequently typically greater than one.

This fundamental difference arises because an estimator obtained using a particle filter is not an average, but a product of dependent averages of random variables. The relative variance of an importance sampling estimator with samples is for some , whereas the relative variance of a particle filter estimate of the likelihood is of the form (Cérou et al.,, 2011),

where is is a non-negative sequence that often increases exponentially. It follows that increasing when is small can dramatically reduce the contributions of , even though by considering very large with fixed, the relative variance is .

References

- Andrieu et al., (2010) Andrieu, C., Doucet, A., and Holenstein, R. (2010). Particle Markov chain Monte Carlo methods. J. R. Statist. Soc. B, 72(3):269–342.

- Andrieu et al., (2016) Andrieu, C., Lee, A., and Vihola, M. (2016). Uniform ergodicity of the iterated conditional SMC and geometric ergodicity of particle Gibbs samplers. Bernoulli, page to appear.

- Andrieu and Roberts, (2009) Andrieu, C. and Roberts, G. O. (2009). The pseudo-marginal approach for efficient Monte Carlo computations. Ann. Statist., 37(2):697–725.

- Andrieu and Vihola, (2015) Andrieu, C. and Vihola, M. (2015). Convergence properties of pseudo-marginal markov chain monte carlo algorithms. Ann. Appl. Probab., 25(2):1030–1077.

- Andrieu and Vihola, (2016) Andrieu, C. and Vihola, M. (2016). Establishing some order amongst exact approximations of MCMCs. Ann. Appl. Probab., 26(5):2661–2696.

- Baxendale, (2005) Baxendale, P. H. (2005). Renewal theory and computable convergence rates for geometrically ergodic markov chains. Ann. Appl. Probab., 15(1B):700–738.

- Beaumont, (2003) Beaumont, M. A. (2003). Estimation of population growth or decline in genetically monitored populations. Genetics, 164:1139–1160.

- Bornn et al., (2016) Bornn, L., Pillai, N. S., Smith, A., and Woodard, D. (2016). The use of a single pseudo-sample in approximate Bayesian computation. Stat. Comput., page to appear.

- Cérou et al., (2011) Cérou, F., Del Moral, P., and Guyader, A. (2011). A nonasymptotic theorem for unnormalized Feynman–Kac particle models. Ann. Inst. H. Poincaré Probab. Statist., 47(3):629–649.

- Doucet et al., (2015) Doucet, A., Pitt, M. K., Deligiannidis, G., and Kohn, R. (2015). Efficient implementation of markov chain monte carlo when using an unbiased likelihood estimator. Biometrika, 102(2):295–313.

- Filippone and Girolami, (2014) Filippone, M. and Girolami, M. (2014). Pseudo-marginal Bayesian inference for Gaussian processes. IEEE Trans. Pattern Anal. Mach. Intell., 36(11):2214–2226.

- Giorgi et al., (2015) Giorgi, E., Sesay, S. S. S., Terlouw, D. J., and Diggle, P. J. (2015). Combining data from multiple spatially referenced prevalence surveys using generalized linear geostatistical models. J. R. Statist. Soc. A, 178(2):445–464.

- Kemeny and Snell, (1969) Kemeny, J. G. and Snell, J. L. (1969). Finite Markov Chains. Van Nostrand, Princeton.

- Lee and Łatuszyński, (2014) Lee, A. and Łatuszyński, K. (2014). Variance bounding and geometric ergodicity of markov chain monte carlo kernels for approximate bayesian computation. Biometrika, 101(3):655–671.

- Sherlock, (2016) Sherlock, C. (2016). Optimal scaling for the pseudo-marginal random walk Metropolis: insensitivity to the noise generating mechanism. Methodol. Comput. Appl. Probab., 18:869–884.

- Sherlock et al., (2015) Sherlock, C., Thiery, A., Roberts, G. O., and Rosenthal, J. S. (2015). On the efficiency of pseudo-marginal random walk Metropolis algorithms. Ann. Statist., 43(1):238–275.

Appendix

If is reversible with respect to , it can also be regarded as a self-adjoint operator on ; the Dirichlet form associated with is defined as

Proof.

(of Theorem 1) Recall Lemma of Andrieu et al., (2016): if for two -reversible Markov kernels and there exists satisfying for all , then

| (3) |

To exploit this result, we construct two -reversible Markov kernels and on the extended space such that the -marginal of the Markov chain with transition (resp. ) has the same law as the -marginal of the Markov chain with transition (resp. ). By Lemma of Andrieu et al., (2016), Theorem 1 follows once it is proved that for any it holds that

| (4) |

We define the distribution , which depends on and , through its density

| (5) |

for ; the indices in (5) and henceforth are to be understood modulo , and we have used the notation . The Metropolis–Hastings kernel proposes a move by first generating and then choosing uniformly at random in , i.e. the proposal density is

The proposed is accepted with the usual Metropolis–Hastings probability

| (6) |

The Metropolis–Hastings kernel differs from in the way is proposed. It proposes a move by first generating and then choosing such that . Since for any we have , the proposal density is

The proposed is accepted with the usual Metropolis–Hastings probability

| (7) |

From Equations (6)–(7) it follows that the -coordinates of the Markov chains with transition and equal in law, respectively, the -coordinates of the Markov chains with transitions and . To conclude the proof, we now prove inequality (4); it suffices to prove that is at most for any , i.e.

| (8) |

From (6)–(7), this is equivalent to showing that is at most

and since the two quantities inside curly brackets are at least one, the conclusion follows. ∎

Proof.

(of Proposition 1)// For 1., let , , and . Since , for any test function , , where is the Metropolis-Hasting kernel from which the pseudo-marginal kernels are derived. However, since, at stationarity, ,

Applying (3) with and again with then provides

For 2., let , , , , and . Since the Markov chains considered are finite, asymptotic variances can be calculated exactly. In particular, for and the sets and are respectively absorbing. The transition matrices for these states can be calculated respectively as

and asymptotic variances can be computed, e.g., using the expressions on p. 84 of Kemeny and Snell, (1969). With defined by and , we obtain and , so . ∎

Proof.

(of Proposition 2)

For an integer , a lag and a test function , set the lag- auto-covariance at equilibrium of the kernel . Similarly, for a lag , set the lag- auto-covariance at equilibrium in continuous time of the kernel . Since can also be expressed as , standard manipulations yield that

| (9) |

After rearranging terms and using (9), the inequality reduces to (2), proved in Theorem 1. ∎