Root consistent estimation of the marginal density in some time series models

Abstract

In this paper, we consider the problem of estimating the marginal density in some nonlinear autoregressive time series models for which the conditional mean and variance have a parametric specification. Under some regularity conditions, we show that a kernel type estimate based on the residuals can be root consistent even if the noise density is unknown. Our results, which are shown to be valid for classical time series models such as ARMA or GARCH processes, extend substantially the existing results obtained for some homoscedatic time series models. Asymptotic expansion of our estimator is obtained by combining some martingale type arguments and a coupling method for time series which is of independent interest. We also study the uniform convergence of our estimator on compact intervals.

1 Introduction

Estimating the marginal density of a stationary time series has been extensively studied in the literature. Kernel density estimation is probably one of the most popular methods used for this problem and the properties of the so-called Parzen-Rosenblatt estimator have been investigated under various mixing type conditions. See for instance Robinson (1983), Ango Nze and Doukhan (1998),Doukhan and Louhichi (2001) or Roussas (2000). See also the monograph of Bosq (1998) for kernel density estimation for strong mixing sequences and Dedecker et al. (2007) for numerous weak dependence conditions ensuring consistency properties of this estimator.

However, when additional structure is assumed for the stochastic process of interest, kernel density estimation can be used more cleverly for getting sharper rates of convergence, in particular consistency. This atypical rate of convergence in nonparametric density estimation has been first noticed for the estimation of the density of some functionals of independent random variables. See Frees (1994), Schick and Wefelmeyer (2004b) and Gin and Mason (2007). In time series, existing contributions exploits the representation of the marginal density as a convolution product between the innovation density and the marginal density of a predictable process. Such an approach has been used by Saaevedra and Cao (1999), Schick and Wefelmeyer (2007) and Schick and Wefelmeyer (2004a) for estimating the marginal density of invertible moving average processes. In the last contribution, sharper results are obtained for possibly infinite moving averages processes. More recently, Kim et al. (2015) obtained some results for nonlinear and homoscedastic autoregressive processes of order for which the conditional mean has a parametric specification. Another recent contribution has been made by Delaigle et al. (2015) who constructed a consistent estimator of the density of the log-volatility for a GARCH process. Note however that the purpose of this latter contribution is not the estimation of the marginal distribution and the volatility process is not directly observed. Moreover, the approach used seems specific to the autoregressive equation followed by the GARCH.

In the literature, consistent estimation of the marginal density in conditionally heteroscedastic time series models has not been considered. Moreover, even in the homoscedastic case, a general approach has not been studied for getting this convergence rate. In this paper, we consider the problem of estimating the marginal density with the rate of convergence in some autoregressive time series models, conditionally homoscedastic or heteroscedastic. We will restrict our study to short memory models with a location-scale formulation

where the conditional mean and volatility depends smoothly on a finite-dimensional parameter . With respect to the existing results, our approach covers lots of cases, from the ARMA processes with independent and identically distributed innovations to ARMA processes with a GARCH noise. Let us also mention that our contribution gives an answer to a question addressed in Zhao (2010), a paper in which an estimator similar to our was suggested for density estimation in autoregressive time series models. However, apart from some classical smoothness conditions, the root- consistency of our estimator is only guaranteed under the square integrability, with respect to the noise distribution, of the conditional density of the marginal given the noise component . This condition is not always satisfied and has to be checked for the model under study. In this paper, we show in particular that ARMA processes with GARCH errors satisfy in general this integrability condition. A similar integrability condition has been observed by Müller (2012) for estimating the marginal density in some homoscedastic regression models. See also Schick and Wefelmeyer (2009) who showed that estimating a convolution of some powers of independent random variables can lead to a slower rate of convergence when this conditions fails to hold.

The paper is organized as follows. In Section , we define our estimator and give its asymptotic properties. In Section , we check the assumptions of our Theorems for some standard examples of time series models. We also compare our assumptions with that used in the aforementioned references. Section is devoted to a comparison by simulation of our estimator with the standard Parzen-Rosenblatt estimator. Proofs of our results are postponed to the last section of the paper.

2 Marginal density estimation of a time series

2.1 Model and marginal density estimator

We first introduce the general model used in the sequel. Let be a sequence of i.i.d square integrable random variables. If denotes a Borel subset of , we consider two measurable functions . We assume that for a , is a stationary process such that

| (1) |

Note that the two functions and will be more precisely defined almost everywhere, where denotes the Lebesgue measure on and the probability distribution of . We also assume that , i.e

for a suitable measurable function defined almost everywhere. We also set

The realizations of all the past values are not available. Then we assume that there exist measurable functions such that (resp. ) is an approximation of (resp. ). Then we use the notations

Our estimator is based on the representation of the marginal density of the stationary process as a smooth functional of the noise density . More precisely, setting and denoting by denotes the conditional density of given , we have for ,

f_X(v)=E[f(v—X_t^-)]=E[1σi(θ0)f_ε(v-mi(θ0)σi(θ0))]. Imagine first that a sample is available. Then the vector of innovations is also observed. The noise density can be estimated by the classical Parzen-Rosenblatt kernel estimator. If be a probability density with compact support , which will be assumed to be continuously differentiable in the sequel, we set

Then, using the expression (2.1), we define the following unfeasible estimator

with for . In practice, the parameter has to be estimated and only the vector is observed. Let us introduce additional notations. For , we set . We call the process the residual process. We also denote by and the truncated versions of and respectively, e.g . Then, if denotes an estimator of , the feasible estimator of is defined by

Note that are the residuals obtained after the estimation step. In the homosecedastic case, i.e there exists such that for all , our estimator is simply defined by

| (2) |

Note that the estimation of the variance is unnecessary in the homoscedastic case. Estimator of type (2) already appears in the literature but using a convolution approach. See for instance Schick and Wefelmeyer (2007) for linear processes, Müller (2012) for homoscedastic regression models and Kim et al. (2015) for some non linear conditionally homoscedastic time series. In this case, the kernel is a convolution product of type and the estimator (2) is obtained as a convolution product of two kernel estimators: the Parzen-Rosenblatt estimator, with kernel , of the density of and that of with the same kernel. In this paper, we will consider an arbitrary continuously differentiable kernel and the homoscedastic case as a special case of the conditionally heteroscedastic case, by setting in this case the two quantities and to in all our statements.

2.2 Assumptions and asymptotic behavior of the marginal density estimate

We now give our assumptions for deriving the asymptotic behavior of the unfeasible estimator and the feasible estimator . In the sequel, we will denote by a norm on whatever the value of the integer . We will still denote by the corresponding operator norm. For a family of matrices and a family of real numbers, we set and , where . Finally, since for , and are measurable functions of , we define some coupling versions of these two quantities. For an integer , we denote by a copy of and we denote by and the two random variables defined as and but for which is replaced with

One can note that has the same distribution than . The interest of such coupling method will be explained in Section . The following assumptions will be needed.

- A1

-

The parameter where is a compact set of .

- A2

-

The volatility is bounded away from zero, i.e there exists such that a.s. We also assume a.s. Moreover, there exists and such that

and

- A3

-

The two applications and are a.s two times differentiable over . Moreover, there exists such that the following random variables are integrable.

where for a function , and denote the two first derivatives of .

- A4

-

There exists an estimator of such that .

- A5

-

The noise density is bounded and the two first derivatives , are bounded.

- A6

-

Let a compact interval of the real line. For all , we assume that the ratio has a density denoted by and we set for ,

We assume that the application is jointly measurable and also that there exists such that for all ,

- A7

-

The envelope function defined by satisfies for some . Moreover, there exist some constants such that

where denotes the bracketing numbers of the family .

Notes

-

1.

Different constants and can be found for the three bounds given assumptions A2. However, we can alway take the minimal value of the exponents , the maximal value of the constant and the maximal value of the constants . So there is no loss of generality in assuming the same constants for the three bounds.

-

2.

Assumption imposes a restriction on the dependence structure of the time series models. These conditions, which are usually referred as short-memory properties, are satisfied for the standard ARMA or GARCH processes. Roughly speaking, this weak dependence condition means that a perturbation of initial conditions in the data generating process is forgotten exponentially fast. This type of dependence condition is also used by Zhao (2010) or Kim et al. (2015).

Discussion of the assumption A6.

Our results require some regularity conditions for the family of functions . The integrability condition assumed on is necessary for root consistency, as shown in Theorem 1 stated below. One can also rely this function to the conditional density of . Indeed, if is a measurable function, we have, setting for simplicity of notations and ,

This shows that can be seen as a version of the conditional density of given that . In what follows, we discuss alternative expressions for the function as well as some sufficient conditions ensuring the square integrability of required in A3.

-

1.

For the homoscedastic model, the volatility equals to a constant . Then if has a density denoted by , we have . In this case, estimation of parameter will be unnecessary.

-

2.

For a pure heteroscedastic model, i.e the conditional mean reduced to a constant , assumption A3 can hold only if . For , one can show that for , . In this case, we have for ,

Then if for instance is bounded, the integrability condition given in A3 is guaranteed as soon as , which is not a strong restriction.

-

3.

In the location-scale case with a non degenerate conditional mean, we assume that the distribution of the couple has a density denoted by . Then if , the distribution of the couple has a density given by

We deduce that

(3) Using Jensen inequality and a change of variables, one can show that

(4) Then the integrability condition given in A3 follows if is bounded and if

is finite.

Discussion of the assumption A3.

Assumption A3 imposes some moment restrictions and smoothness conditions. In the pure heteroscedastic case, we only have to check integrability of

In the homoscedastic case, these conditions reduce to the integrability of

These moment restrictions are explained by the technique used for the proof of Theorem given below and which consists in studying the derivative of with respect to , the estimator of . For a general heteroscedastic time series model, other conditions could be possible, the single requirement is to get the conclusions of the lemmas 6, 7, 8. We now give the asymptotic behavior of our estimates. We first start with the unfeasible estimator .

Theorem 1.

Assume that there exists such and .

-

1.

Assume that assumptions A2, A5 and A6 hold true. Then for all , we have

(5) In particular, for all , we have

-

2.

If in addition assumption A7 holds true, the approximation (5) is uniform in . In particular

Note.

The proof of Theorem relies on the decomposition of a statistic for which the degenerate part is shown to be negligible under our bandwidth conditions. The bandwidth condition is a bias condition, the bias of our estimator has to decrease faster than the rate . However, our estimator will be first approximated by a U-statistic involving dependent random variables in order to facilitate the study of its asymptotic behavior. In the next result, we compare the asymptotic behavior of the feasible estimator with that of the unfeasible one. For , we denote by the density of . We also set

In the sequel will denote the partial derivative with respect to of the function . By convention, we represent by a column vector. Moreover, will denote the transpose of a matrix .

Theorem 2.

Assume that there exists such that and and that assumptions A1-A6 hold true. Then we have

Note.

For the comparison of the two estimators and , we do not use statistics arguments. We wanted to avoid additional regularity conditions on the function and its local approximation when , these conditions being difficult to check for practical examples. For the proof of Theorem , we first show that the effect of truncations of is negligible. Then, we use dependent approximations of these quantities. Finally, we study a Taylor expansion of order and control the local approximation of the derivatives using martingale tools and integration with respect to the residual process . Then regularity conditions concern exclusively the densities of this residual process. One can note that the range of bandwidths allowed in Theorem is reduced with respect to Theorem . In the next result, we provide the asymptotic distribution of the feasible estimator of . To this end, it is necessary to use a particular representation of the estimator . Similar representations are used in Zhao (2010) or Kim et al. (2015).

- A8

-

There exists a square integrable process taking values in , the space of real matrices of size and a measurable function such that , and are square integrable, (where and ) and

For stating our next result, we define for and ,

Corollary 1.

Under the assumptions A1-A6 and A8, the process converges in the sense of finite dimensional distributions towards a centered Gaussian process such that for ,

Moreover if assumption A7 also holds, the convergence occurs in .

Notes

-

1.

In the homoscedastic case, one can check that the covariance structure of the Gaussian process is the same as in Theorem of Kim et al. (2015). Thus, our result can be seen as an extension of the result obtained in their paper, allowing an arbitrary number of lags in the conditional mean and also conditional heteroscedasticity.

- 2.

3 Examples

In this section, we explain how to check the assumptions for some classical time series models.

3.1 Conditionally homoscedastic times series

Let us assume that

We remind that where denotes the density of . In this case, assumption holds true for instance if is bounded. Moreover, assumption is satisfied if is Lipschitz and . Indeed, the latter condition entails that the measure of assumption has a finite mass and in this case, the polynomial decay of the bracketing number is classical. See van der Vaart (1998), Example . For homoscedastic and autoregressive time series with one lag, Kim et al. (2015) obtained a root consistent estimation of the marginal density by using a representation of the density of as a convolution product. In that paper, similar regularity assumptions are used for the noise distribution. These authors use bandwidth conditions similar to ours (see Theorem of their paper). Their moment conditions for and its derivative are less restrictive than ours but at the same time more regularity conditions on the density of have to be checked for their non linear models. See Assumption and Assumption of that paper for a precise statement of their regularity conditions. One advantage of our approach is to present a unified approach for homoscedastic and heteroscedastic time series and for which the dynamic can depend on an arbitrary and possibly infinite number of lags.

The case of ARMA processes.

Let us now consider the case of ARMA processes, i.e there exist two integers and such that

As usual, we assume that for , the roots of the two polynomials and are outside the unit disc. Then defining

and , we have

where denotes the companion matrix associated to and

Then we have

| (6) |

Moreover can be defined by setting to in (6). Now we explain how to check assumptions . Assumption will be checked directly for ARMA-GARCH processes.

-

•

Assumption holds if . Indeed, using the well-known infinite moving-average representation

we have . Then assumption A3 holds true using (6) (the order of the derivative can be arbitrary in this example).

-

•

Now assumptions follows from the fact that is bounded and Lipschitz. Indeed, using the infinite moving average representation, we have . If we assume, without loss of generality, that and also for simplicity, we have

where denotes the probability distribution of the random variable . Hence the boundedness and Lipschitz property of follows from assumption .

-

•

Finally, assumptions hold true using for instance conditional maximum likelihood estimators. See Brockwell and Davis (1991), Chapter , for some asymptotic results for different inference methods of ARMA parameters.

Let us now compare our results with that of Schick and Wefelmeyer (2007). The results obtained by these authors are very general for applications to linear processes which contain ARMA processes as a special case. Their results are shaper than ours because they obtained uniform convergence of their convolution estimate on the real line whereas we consider uniformity only on compact intervals. However, our results applies if has a moment of order , whereas Schick and Wefelmeyer (2007) use a moment of order (see assumption F of the paper). Moreover, the kernels used in Schick and Wefelmeyer (2007) cannot be nonnegative (see the assumption applied with an order for the kernel) and then the estimator of the density can take negative values. This excludes some classical kernels often used by the practitioners.

3.2 Pure GARCH models

In this subsection, we consider the process

with , . We set . Moreover let

Then is (up to parameter ) a GARCH process. We set

There exist a sequence of i.i.d random matrices of size and a sequence of random vectors of dimension such that

| (7) |

We defer the reader to Francq and Zakoïan (2010), p., for a precise expression of as well as the definition of the Lyapunov exponent of the sequence . The following assumptions will be needed.

- G1

-

and for all , .

- G2

-

We have and for and .

In the sequel, we denote by a generic positive constant. Under the assumption G1, there exist and an integer such that and . Using the representation

and the fact that , we get

Then, we have also . Now we check the assumptions A2, A3, A4 and A8, A5 and A6.

-

1.

We first check A2. Setting for ,

we have the recursive equations with

Then is the companion matrix associated to . Since , the spectral radius of is less than and there exists a positive integer such that and then if is small enough, using the continuity of . In particular, we have the expansion

Then, using the fact that the sequence is bounded and , we deduce that

This shows that for some . The proof of

is similar, using the expansion of and the fact that .

-

2.

The assumption A3 follows from the fact that the random variables and have moments of any order if is sufficiently small (see the proof Theorem in Francq and Zakoïan (2010), part for the main arguments used for showing these properties).

-

3.

For checking A4 and A8, one can use the Gaussian QML estimator. When all the GARCH coefficients are assumed to be positive, the representation A8 holds for the corresponding estimator (see Francq and Zakoïan (2010), p. ). Note that the representation A8 requires the assumptions G1 and G2.

-

4.

Finally we check the assumptions A5 or A6. First, we note that assumption A5 does not hold when . In this case, the ratio is degenerate and does not have a density. For estimating , one can use the classical kernel estimate, the approach proposed in this paper has no interest because the convergence rate will be similar. In the sequel, we assume that . Using Lemma 2 and the representation of GARCH processes as an ARCH process, one can see that is sufficient for A5. Moreover, using the additional assumptions and is bounded for , assumption A6 also holds if or . Note that the moment condition is satisfied under the classical condition which implies .

Notes

-

1.

If we assume that in the model, one can use the logarithm to get

One can apply our results for estimating directly the density of . Setting and , one can show that the density of satisfies the assumption A5 if we additionally assume that is bounded. Moreover, we have where denotes the density of . Then one can show that assumption A6 is satisfied if , which is a classical condition found in practice in using GARCH models. Moreover, it is also possible to show that assumption A7 is satisfied under the additional condition: is bounded. The proof is omitted since one can use Lemma 2 (3.) as well as some arguments used in the proof of Lemma 2. All the other assumptions are automatically satisfied it G1 and G2 hold true. Note that the root consistent estimation of the density of is studied in Delaigle et al. (2015), for a GARCH process. Here we consider the estimation of the density of which is a different problem but this convergence rate also holds. Note also that we consider a more general GARCH model in this work.

-

2.

One can prove similar results for pure ARCH processes (i.e in the GARCH model), assuming . However assumption A6 (resp. assumption A7) requires (resp. ). See Lemma 2 for details. Let us show that assumption A6 is not satisfied in the case . In the case , we have . Then if is the marginal density of the process, we have

Let us assume that , is positive and (the last condition holds true when ). Then we have when . However, one can check that for any . Indeed, we have

which is finite (the integrability holds around the singularity , is bounded outside a neighborhood of and ). We recover a phenomenon described by Schick and Wefelmeyer (2009) when Frees estimator is applied for estimating the density of a sum of powers of two independent random variables. In general, a slower convergence rate is obtained when square integrability of the density fails. See Schick and Wefelmeyer (2009), Theorem , where the rate is obtained in the estimation of the density of a sum of squares .

-

3.

When some parameters of the GARCH process are equal to zero, assumption A3 is not always guaranteed unless assuming . In this case assumption A3 is automatic.

3.3 ARMA processes with GARCH noises

In this subsection, we consider the model

We define for , As for ARMA processes, we define

In addition to assumption G1 for the Garch parameters , we consider the following classical assumption which guarantees causality and invertibility of the ARMA part.

- AG1

-

The roots of the two polynomials and defined by

are outside the unit disc.

- AG2

-

We have .

Note the if is small enough, the assumption AG1 will be also valid for all . Assumption AG2 is restrictive but we do not find a way to avoid this moment condition for checking assumption A3. This restriction is due to the technique used for the proof of Theorem , with a control of the derivative of our estimator with respect to when is close to . Note that, under the assumptions AG1-AG2, we have . We now check the assumptions , except A5 and A7 which we were able to check only in the pure GARCH case.

-

1.

For the assumption A2, one can use the following expansions for . If

we have

where , and are the companion matrices associated to , and respectively and

Then assumption A2 follows from the fact that if is small enough, there exists three positive integers such that for . The proof uses the same arguments as in the pure GARCH case and is omitted.

-

2.

The assumption A3 holds true if we assume . In this case, using the expansions

and the equation for to show that on can show that , and have a moment of order . Moreover, one can show that , and have a moment of order . This is sufficient for checking A3.

-

3.

Assumptions A4 and A8 hold true if we consider the Gaussian quasi maximum likelihood. See the proof of Theorem in Francq and Zakoïan (2010). Note that the expansion given in A8 requires that lies in the interior of and that .

-

4.

Assumption A6 is a consequence of Lemma 3. Indeed, if is bounded, the conditional density of is bounded. Since the couple can be expressed as

for some summable sequences of coefficients and , Lemma 3 guarantees that the density of this couple can be bounded as follows: for a positive constant . Then one can conclude using inequality (4) and assumption AG2 which entails the condition .

4 Simulation study

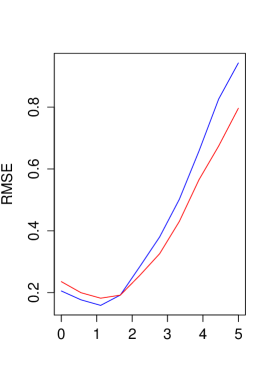

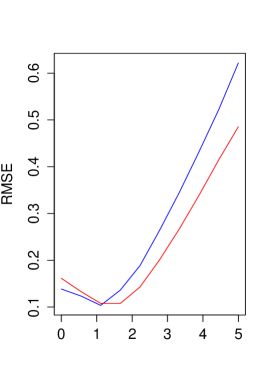

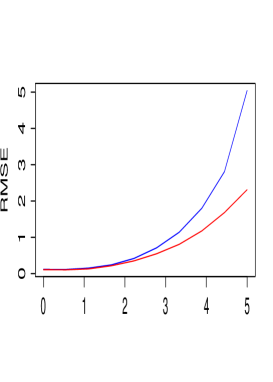

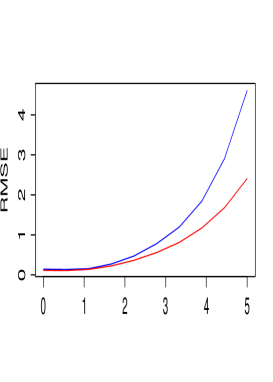

In this section, we compare by simulation the mean square error of our estimator with that of the classical kernel density estimate. Our estimator is implemented using the quadratic kernel. The standard kernel density estimate is computed using the function Density of the software R. Bandwidth selection for our estimator is beyond the scope of this paper. However, we use the simple approach proposed in Kim et al. (2015) which consists in multiplying the bandwidth selected for the kernel density estimate by a factor where is compatible with our theoretical results. For a bandwidth with the optimal rate, we then keep the constant and simply modify the rate. In our simulations, we found that the exponent provides good results. In the sequel, we consider three simulation setups.

-

1.

In the first setup, we consider the conditionally homoscedastic case, with the AR process such that is i.i.d with (the Student distribution with degrees of freedom).

-

2.

In the second setup, we consider the pure ARCH case with a GARCH process such that . The noise component still follows a distribution.

-

3.

In the last setup, we consider an AR process with a GARCH noise,

We assume that follows a standard Gaussian. One can show that the moment condition required for applying our results is not satisfied in this example.

Note that GARCH parameters are chosen so that the expectation of the square equals to and lag coefficients have typical values encountered in practice. The marginal density is evaluated at points equally spaced, starting from to . The true density is approximated by

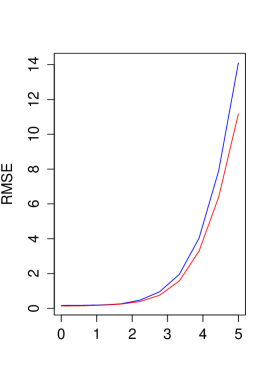

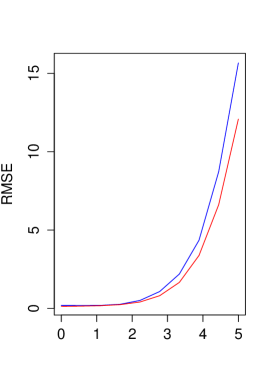

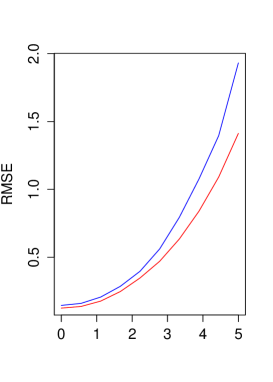

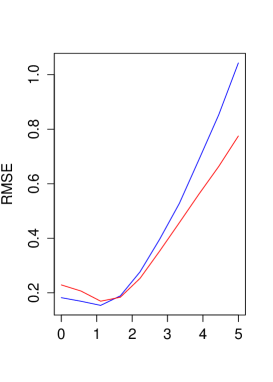

The RMSE of the estimator is normalized by the value of the density: . This RMSE is approximated by its empirical counterpart using samples. GARCH parameters are estimated using the function garchFit of the package fGarch. The R code is available on request from the author. In Figure 1, 2 and 3, the blue curve represents the normalized RMSE for kernel density estimation and the red curve that for our method. Whatever the original bandwidth selection, our estimator performs better even if the sample size is small for estimating accurately GARCH processes. A notable exception is the second setup when is in a neighborhood of . In this case, the standard method performs better. This is not surprising because of the singularity at point , a point for which our method is almost equivalent to the standard one and our bandwidth parameter does not have the optimal convergence rate. This problem is less perceptible for the larger sample size . A general finding is the notable superiority of our method for estimating the tails, which have an important rule in financial time series. For practical applications, adequation tests based on the marginal density as proposed in Kim et al. (2015) can also be adapted to GARCH processes, using our results. This problem will not be studied is the present paper.

5 Proofs of the results

In the subsequent proofs, will denote a generic constant that can change from line to line. Moreover, if is a random variable, we set . For deriving our results, we first introduce a coupling method which will be very useful. The goal of this coupling method is to construct dependent random sequences which approximate some weakly dependent random sequences. Then, we show that our initial estimator is asymptotically equivalent to an estimator involving an dependent random sequence, provided that grows with a polynomial rate.

5.1 From dependence to dependence via coupling

Let be a measurable application taking values to an arbitrary measurable space . If , we set

where is a family of i.i.d random variables independent from and such that for all , has the same distribution than . In this case, the sequence is dependent. This means that for all , the two algebra and are independent. We call this new sequence a dependent approximation of . Note that has the same distribution than . Note that the two processes and are of this form, if denotes the set of real-valued functions defined on the set . We will denote by and their corresponding dependent approximations. These coupling versions of the conditional mean/variance of the process will be central in our proofs. One can note that and their derivatives with respect to have the same distribution than the original quantities.

5.2 A martingale decomposition

The control of the derivative of our estimator will be done using appropriated martingale differences. In this subsection, we set for ,

Let and . Here denotes the integer part of the ratio and is an integer . for , we set . For each , we define two filtrations. We set for ,

Now if is a random variable measurable with respect to , we set

and

Then for each , and are two martingales differences. Moreover, if denotes integration with respect to the distribution of , we have

| (8) |

The following lemma will be needed in the sequel for controlling triangular arrays of martingale differences.

Lemma 1.

Assume that for a , . Let be a sequence of finite sets such that for some . For each , let be a martingale difference. We assume that

and that

with , . Then we get the conclusion:

Proof of Lemma 1.

Let such that . We set . For simplicity of notations, we suppress the dependence in of our quantities. Then we set

We first show that

| (9) |

To this end, we use the bound

If , we have

Using the expression of and the assumptions of the lemma, the latest probability is . Moreover

This show (9). To end the proof we have to show that

| (10) |

We will prove (10) using the exponential inequality of Freedman for martingales (see Freedman (1975)). Let . First we choose such that

Using the fact that

we get

Then (10) follows from our conditions on . The proof of Lemma 1 is now complete.

5.3 Proof of Theorem

For simplicity of notations, we drop the parameter and simply write for instance instead of . Let and sufficiently small such that and . We denote by the integer part of and by the integer part of the ratio . Then we set and

Note that the cardinal of the set satisfies . We set

Note first that

| (11) |

Indeed, using Lemma 5, we have

Moreover, there exists a constant such that

Hence (11) follows. In the sequel, we study the behavior of the estimator .

5.3.1 Bias part

We remind that . Since is bounded, there exists such that for all ,

| (12) |

From (12), we deduce that

Using the condition , we get

5.3.2 The variance part

We first focus on

We set for ,

For this part we set

and

Using the independence properties, observe that

From the first writing of , we have for ,

Moreover, for , we have, using dependence,

Moreover, we have

Then we get,

| (13) |

Note that . Moreover, it is easily seen that

This means that converges pointwise to in probability. Note that is a random function taking values in , the space of real-valued and continuous functions defined on the compact interval . From (13) and the Kolmogorov-Chentsov tightness criterion in (see for instance Kallenberg (1997), Corollary ), we deduce that

Using the same type of arguments, one can also show that

where

Moreover, since is , we have (see also the control of the biais)

Now we are going to show that

| (14) |

The proof is divided into two parts. In the first part, we show that

| (15) |

We have

Using (12), the condition and the fact that , we get (15). To show (14), it remains to show that

| (16) |

where .

-

1.

To show (16) when is the singleton , we use Jensen inequality and the fact that the translations are continuous in . More precisely, we have

-

2.

To show (16) when is a compact interval not reduced to one point, we proceed in two parts.

-

(a)

We first show that

(17) To this end, we will use Lemma in van der Vaart (1998). We set

For the family of functions, we consider the envelope function defined by

where is defined in assumption . For bounding the bracketing numbers of this family, we first observe that if is an bracketing in , then (i.e ) entails that

Moreover, one can show that

Then, we have

and the bracketing numbers of the family are of polynomial decay. Next we show that

(18) To show (18), we consider for a given , some brackets that cover . For each integer , we consider an element . Then, for , if , we set , with

Then, if , we have and

Since for each , we have , we conclude that

Since is arbitrary, we conclude (18). Moreover, setting, for , , we have

Here . Then, from (18), one can choose such that and . Hence, from Lemma in van der Vaart (1998), we deduce that

and hence (17).

- (b)

-

(a)

5.4 End of the proof of Theorem

Collecting the results of the two previous subsections, we have shown that

uniformly on and with a uniform convergence on for the partial sum involving if assumption holds true. Then it is straightforward to show that one can replace and by in this asymptotic expansion. Indeed, we have

and for the uniform convergence over , one can use the bounds

Using the same arguments, can be replaced with . Finally, using the arguments given in the proof of Lemma 5, we have

The proof of the tightness of will be studied in detail in the proof of Corollary .

5.5 Proof of Theorem

Using Lemma 4 and our bandwidth conditions, we have

where is defined as but the quantities and being replaced with and respectively. This shows that possible truncations of the conditional mean/variance only using is asymptotically negligible for our estimator. Now, for , we recall that and denote the dependent approximations of and respectively. Then setting , we define

and

In the rest of the proof, we fix a real number such that and we denote by the integer part of . Using Lemma 5, we have

We will also suppress some terms in the estimator in order to get stochastic independence between the two couples of random functions and involved in the U-statistic. To this end we set for , and ,

Using the condition , we have

5.5.1 Outline of the proof

The goal of the proof is to show that

| (19) |

and in a second step that

| (20) |

In the proof of Theorem , we have already shown that

Note that from assumption A4, assertion (19) will hold if for all and integers such that , we have

where is a short notation for . We will show the following sufficient condition

Then the two assertions (19) and (20) (and then Theorem ) will follow if we show that

| (21) |

| (22) |

and

| (23) |

where the function is defined before the statement of Theorem . Assertion (21) will be studied using martingale properties (see the subsection 5.2). In the rest of the proof, we prove the assertions (21), (22) and (23). Note that we have the following expression.

5.5.2 Proof of assertion (21)

We set

Let a sequence of positive real numbers such that . We take for instance . Let a family of points in such that for , there exists such that . The set can be chosen such that . Using Lemma 8 (3), we first notice that

To show (21), it remains to prove that

But this is a consequence of Lemma 1 applied coordinatewise to , using the martingale decomposition (8). The assumptions used in Lemma 1 can checked using Lemma 8.

5.5.3 Proof of assertion (22)

5.5.4 Proof of assertion (23)

We set

Using Lemma 6 and Lemma 7, it is easily seen that for ,

To end the proof of assertion (23), it remains to show that for ,

| (25) |

Note that . To show (25), we first notice that for . Then, since , it is easily seen that

Now, we set for and ,

Then assertion (23) will follow if we show that

| (26) |

We have using the dependence,

Moreover, using the fact that and that is bounded, we get for each . Now, (26) will follow if we show that . But this is a consequence of the following bounds. First, there exists such that

For , we set and . Then . Then, using assumption A5, we have

In the previous bounds, the real number does not depends on . Then (26) follows and the proof of assertion (23) is now complete. This ends the proof of Theorem .

5.6 Proof of Corollary

From Theorem , Theorem and assumption A8, we have

The first part of the corollary concerns the convergence of the finite dimensional distributions. Note also that the previous convergence is uniform if assumption A7 holds true. Convergence of finite dimensional distributions is straightforward using a central lime theorem for weakly dependent time series. For instance, the central limit theorem given in Zhao (2010), Theorem , applies in our case. For the uniform convergence, it remains to show the tightness of the empirical process . Since we assumed A7, it is only necessary to study the tightness in , the space of real-valued and continuous function defined on , of

To this end, we use the Kolmogorov-Chentsov criterion (see for instance Kallenberg (1997), Corollary ). If satisfy , we have from Jensen inequality,

Then the tightness will follow if we show that

| (27) |

Note that

Moreover, for , and , we have

Then using assumption A2 and assumption A5, we deduce that there exist such that for all ,

where is defined in assumption A2. The proof of the last inequality uses the same arguments than the proof of Lemma 7. This control of covariances immediately implies (27). The tightness criterion of Kolmogorov-Chentsov applies. The proof of Corollary is now complete.

5.7 Checking the regularity assumptions on densities

Density regularities of ARCH processes

Here, we assume that is a stationnary ARCH process defined by

We assume here that and that is bounded. We set . We denote by the probability density of the conditional variance and for , which is well defined for . We also set and for a compact interval which does not contain , .

Lemma 2.

-

1.

Assume that . Then is bounded. Moreover, if , then for all , we have .

-

2.

Assume that . Then there exists a constant such that for , we have

-

3.

In addition to the previous point, assume that there exists such that and that is bounded. Then there exists a real number such that . Moreover there exists some constants such that

Proof of Lemma 2.

Before proving the lemma, we first derive an expression for involving conditional distributions. We will use for the notation , we set We set and

The measure will denote the probability distribution of . Moreover, we set

and

If is a bounded and measurable function, we have

Then we deduce that for ,

| (28) |

-

1.

The fact that is bounded is a consequence of the expression (28), using the fact that and then are bounded. Moreover, we have

This bound gives the result.

-

2.

We use the expression (28). Using some basic computations, it is easily seen that for real numbers ,

for some constant . Setting now for ,

we have for ,

We deduce that for ,

Moreover, it is easily seen that has a density such that

where . Then, it can be shown that

This proves the second point of this lemma.

-

3.

We first show that under our assumptions,

(29) We first observe that

Then we deduce that the function defined by

satisfies . Using the expression (28), condition and the decomposition , we get the bound

This shows (29). For simplicity, we now assume that (the case is identical). First, we show that there exists such that . We have Since is compact and is bounded from below, there exists such that when . We choose such that . We get

This shows that . Finally, we consider the bracketing numbers of the family . Let be such that . Let . We have

Since we have

where the second integrability condition follows from the assumption on and (29), the bound given for easily follows (see van der Vaart (1998), Example , for and a probability measure, but the arguments are similar in our case). This completes the proof of the lemma.

A result for ARMA-GARCH processes

Lemma 3.

Assume that and are two summable sequences of real numbers such that for and for and there exists an integer such that . Let be a stationary process of real random variables such that and such that the conditional distribution of has a bounded density. Then the density of the couple satisfies for a positive constant .

Proof of Lemma 3.

We set and we denote by the conditional density of given that for . We consider two cases.

-

1.

We first assume that . We set

and with . We also set

We also denote by the rotation of such that where . For simplicity of notations, we only use one sign ”integral” and do not precise the boundaries for integration in the next computations. Then if denotes the probability distribution of , we have

Since is bounded, it is easily seen that for a positive constant .

-

2.

We next consider the case . We set

and . For simplicity of notations, we assume that (otherwise, as in the previous point, a change of variables is needed in the computations given below). Denoting by , the probability distribution of , we have

Then we get

We deduce that there exists such that .

5.8 Auxiliary Lemmas

This subsection presents two auxiliary Lemma which assert that under our assumptions, truncated versions and of and have no effect in the asymptotic expansion of our estimator. Moreover, and can be replaced with their dependent approximations, provided grows at an arbitrary small power of . We first observe that if the kernel is Lipschitz continuous and bounded, we have for any ,

In particular, is Hölder continuous with exponent . This fact will be used in the two following lemmas. In what follows, we set for and ,

Here and . We also set

Lemma 4.

Assume that there exists such that . Then we have .

Proof of Lemma 4

Since , it is enough to prove that

where is defined in assumption A2. Let be a positive real number such that . Using assumption A2, we have

One can choose for instance . Moreover, setting , we have

Using assumption A2 and the Cauchy-Schwarz inequality, we deduce that

Lemma 5.

Assume that with and that . Then if

We have .

Proof of Lemma 5

Since , it is enough to prove that

where is defined in assumption A2.

-

•

As in the proof of Lemma 4, we use assumption A2 to get

-

•

Using the previous point, we have also for ,

Using assumption A2, we get

Using the two previous points and assumption A2, we get

Then the result follows from the conditions , and .

5.9 Residual process regularity and an auxiliary lemma

In this subsection, we provide auxiliary lemmas which give regularity properties of the density of the residual process as well as some moment conditions for its dependent approximation. Then we will state Lemma 8 which will be required for the proof of Theorem . For , the density of will be denoted by . We have the expression

| (30) |

The following lemma is given without proof. The assertions given below are mainly a consequence of the Lebesgue theorem for the derivative of an integral depending on a parameter.

Lemma 6.

Assume that assumptions A3 and A5 hold true.

-

1.

We have . For , the function has a derivative such that . Moreover, there exists a number not depending on such that

-

2.

For each , the function is two times differentiable. Moreover, there exists a number not depending on such that

and

-

3.

There exist two constants and such that

-

4.

If a function continuously differentiable and with a compact support. Then, for , we have

The next lemma is given without proof because it results from simple computations.

Lemma 7.

Assume that assumption A3 holds true. We set and . Note that .

-

1.

We have , , , and .

-

2.

We have , and .

-

3.

Let be a positive number. There exists a positive real number such that

and

Now we state a lemma which will be useful for studying the uniform convergence of some sums of martingale differences. We set where is the integer part of . Moreover, we set

Lemma 8.

Assume that assumptions A3and A5 hold true.

-

1.

We set . Then we have

-

2.

We have

-

3.

Let be a positive number. We have

Proof of Lemma 8.

We only prove the result for the conditionally heteroscedastic case, the homoscedastic uses similar arguments and is simpler.

-

1.

It is only necessary to prove that

We recall that

We define

Then . Moreover

Then we get

The result follows from assumption A3 and Lemma 7.

-

2.

Since

we have, using the compact support of the kernel , and the equality ,

Then we conclude that

From the assumption A3, we have and . Then the result follows from the point of Lemma 7.

-

3.

If and are such that and , some basic computations lead to the inequality

Then the result follows from assumption A3 and Lemma 7.

References

- Ango Nze and Doukhan (1998) P. Ango Nze and P. Doukhan. Functional estimation for time series: Uniform convergence properties. J. Statist. Plann. Inference, 68:5–29, 1998.

- Bosq (1998) D. Bosq. Nonparametric Statistics for Stochastic Processes. Estimation and Prediction, volume 110. Lecture Notes in Statistics. Springer, 1998.

- Brockwell and Davis (1991) P. J. Brockwell and R.A. Davis. Time Series: Theory and Methods. Second Edition. Springer Series in Statistics, 1991.

- Dedecker et al. (2007) J. Dedecker, P. Doukhan, J.-R. Leon, S. Louhichi, and C. Prieur. Weak dependence, with examples and some applications. Springer Berlin, 2007.

- Delaigle et al. (2015) A. Delaigle, A. Meister, and J. Rombouts. Root-t consistent density estimation in garch models. Journal of Econometrics, page http://dx.doi.org/10.1016/j.jeconom.2015.10.009, 2015.

- Doukhan and Louhichi (2001) P. Doukhan and S. Louhichi. Functional estimation of a density under a new weak dependence condition. Scand. J. Statist., 28:325–341, 2001.

- Francq and Zakoïan (2010) C. Francq and J-M. Zakoïan. GARCH models: structure, statistical inference and financial applications. Wiley, 2010.

- Freedman (1975) D.A. Freedman. On tail probabilities for martingales. Ann. Probab., 3:100–118, 1975.

- Frees (1994) E.W. Frees. Estimating densities of functions of observations. J. Amer. Statist. Assoc., 89:517–525, 1994.

- Gin and Mason (2007) E. Gin and D.M. Mason. On local u-statistic processes and the estimation of densities of functions of several sample variables. Ann. Statist., 35:1105–1145, 2007.

- Kallenberg (1997) O. Kallenberg. Foundations of Modern Probability. Springer, 1997.

- Kim et al. (2015) K.H Kim, T. Zhang, and W.B. Wu. Parametric specification test for nonlinear autoregressive models. Econometric Theory, 31:1078–1101, 2015.

- Müller (2012) U. U. Müller. Estimating the density of a possibly missing response variable in nonlinear regression. Journal of Statistical Planning and Inference, 142:1198–1214, 2012.

- Robinson (1983) P.M. Robinson. Nonparametric estimators for time series. J. Time Ser. Anal., 4:185–207, 1983.

- Roussas (2000) G.G. Roussas. Asymptotic normality of the kernel estimate of a probability density function under association. Statist. Probab. Lett., 50:1–12, 2000.

- Saaevedra and Cao (1999) A. Saaevedra and R. Cao. Rate of convergence of a convolution-type estimator of the marginal density of an ma(1) process. Stochastic Process. Appl., 80:129–155, 1999.

- Schick and Wefelmeyer (2004a) A. Schick and W. Wefelmeyer. Root consistent and optimal density estimators for moving average processes. Scand. J. Statist., 31:63–78, 2004a.

- Schick and Wefelmeyer (2004b) A. Schick and W. Wefelmeyer. Root n consistent density estimators for sums of independent random variables. J. Nonparametr. Statist., 16:925–935, 2004b.

- Schick and Wefelmeyer (2007) A. Schick and W. Wefelmeyer. Uniformly root consistent density estimators for weakly dependent invertible linear processes. Ann. Statist., 35:815–843, 2007.

- Schick and Wefelmeyer (2009) A. Schick and W. Wefelmeyer. Convergence rates of density estimators for sums of powers of observations. Metrika, 69:249–264, 2009.

- van der Vaart (1998) A.W. van der Vaart. Asymptotic Statistics. Cambridge University Press, 1998.

- Zhao (2010) Z. Zhao. Density estimation for nonlinear parametric models with conditional heteroscedasticity. Journal of Econometrics, 155:71–82, 2010.