Model-independent pricing with insider information: a Skorokhod embedding approach

Abstract.

In this paper we consider the pricing and hedging of financial derivatives in a model-independent setting, for a trader with additional information, or beliefs, on the evolution of asset prices. In particular, we suppose that the trader wants to act in a way which is independent of any modelling assumptions, but that she observes market information in the form of the prices of vanilla call options on the asset. We also assume that both the payoff of the derivative, and the insider’s information or beliefs, which take the form of a set of impossible paths, are time-invariant. In this way we accommodate drawdown constraints, as well as information/beliefs on quadratic variation or on the levels hit by asset prices. Our setup allows us to adapt recent work of [BCH17] to prove duality results and a monotonicity principle. This enables us to determine geometric properties of the optimal models. Moreover, for specific types of information, we provide simple conditions for the existence of consistent models for the informed agent. Finally, we provide an example where our framework allows us to compute the impact of the information on the agent’s pricing bounds.

1. Introduction

It has long been recognised that information plays an extremely important role in the study of modern financial markets. This is most markedly true when two parties trading the same asset have access to different information sources, and then one can ask how the ‘insider’, who possesses additional information, should modify her behaviour to exploit her privileged position. In this paper, we aim to consider problems where the insider has a strong belief in some quantitative, or qualitative, fact about the future evolution of some asset, but is otherwise agnostic about other statistical properties determining the evolution of the asset.

A fundamental, motivating example will be the following: imagine an agent believes that the CEO of a company will act in such a way as to ensure that the share price of the company will not drop below a certain level which depends on the historical maximum of the share price, for example, because the manager is incentivised by stock options which payout provided this drawdown criteria is not breached. Then the agent may want to build this information into her valuations of e.g. derivatives written on the asset. The aim in this paper is to consider problems of this form in a model-independent framework. We claim that this is a natural framework for these problems, since the insider’s information already rules out many ‘standard’ models which would not usually satisfy such a constraint, and it is not immediately clear how the agent should choose a model which includes this information.

Problems concerning insider information have a rich literature: the first work in the mathematical finance literature is [PK96], while important subsequent work includes [BØ05, AIS98, GP98, Cam05], and this topic is still a very active area of research. Along with different information sets, agents may have different beliefs on the evolution of asset prices. This again will result in different market behaviours.

In the past few years, robust approaches to finance, where no underlying probability measure is assumed a priori, have become very popular. Only very recently, additional information and beliefs have been considered in a robust framework. In both [AL17] and [AHO16], this has been modelled by an enlargement of filtration. Closer to the approach of the current work, are the papers by [CHO16], [HO18], [BKN20], and [BZZ18], which model beliefs in a robust setting by excluding some paths from the possible evolution of the asset’s price process (see Section 1.1).

The goal of this paper is to consider the pricing and hedging problems for traders with different information and beliefs in a continuous-time, robust setting, where call prices at a fixed maturity are observed. Our analysis relies on two key assumptions. First, we only consider derivatives which are time-invariant, that is, with payoffs which are independent of the clock under which the underlying is running. These include, for example, lookback options, barrier options, corridor options, and variance options. Secondly, we assume that beliefs and insider’s additional information are time-invariant and such that they allow the insider to assume that a certain set of paths is impossible. This means specifying the set of feasible paths on which (super-)hedging arguments are required to work. Examples of beliefs we can deal with include those on quadratic variation and those on asset prices hitting (or not hitting) given barriers. As for the time-invariant information, the main example we have in mind is that of drawdown constraints, e.g. imposed by company policy, on the price process never falling below a fixed fraction of its maximum-to-date or never falling below a certain threshold once it has reached a certain level.

The assumption of time invariance allows us to translate the robust pricing problem into a constrained Skorokhod embedding problem (SEP), emulating the approach to robust finance initiated in [Hob98] (see also [Hob11]). In this way, in the first part of the paper, Sections 2 and 3, we develop a theoretical framework for our approach. We are able to extend to the current framework the analysis developed in [BCH17] for the unconstrained problem. Indeed, a simple application of the results of [BCH17] leads to a superhedging and duality result for the insider/the constrained SEP (Theorem 3.2), and to a monotonicity principle which gives a necessary condition on the optimising probability measures for the insider/the constrained SEP (Theorem 3.7). Leveraging on our duality result, we are able to provide simple necessary and sufficient conditions to exclude arbitrage for the insider in terms of solutions to the constrained SEP (Proposition 3.3). On the other hand, the monotonicity principle, that takes the form of geometric conditions on the support of the optimisers, often leads to barrier type solutions. Experience in the case without information suggests that, once the geometric structure of the support of the optimisers is understood, it is much simpler to e.g. develop numerical methods to compute the optimisers for specific examples. The main motivation for considering the problem under this assumption of time-invariance is that, as a consequence, we are able to prove the monotonicity criteria, which, as we demonstrate, in many natural examples allows us to reformulate the optimisation problems in terms of simpler, geometric criteria. This additional insight opens up a wider range of mathematical and numerical tools which may be applied to both increase understanding of the problems, and to more accurately solve the problems.

In the second part, Section 4, we illustrate that our setup allows to further investigate several concrete and financially meaningful situations gaining new insights in the insider’s behaviour in explicit situations. More precisely, we restrict ourselves to specific sets of feasible paths (cf. (4.1)). This class is quite broad, as it includes information and beliefs mentioned above on whether prices hit certain barriers, on whether the quadratic variation reaches certain levels, and on drawdown constraints. Here we are interested in three interrelated questions:

-

(1)

When does there exist arbitrage for the insider?

-

(2)

What are the worst case models for the insider?

-

(3)

Can we calculate the value of the insider’s information in specific situations?

We address the question of arbitrage in Theorem 4.1 for the specific information encoded by (4.1). Specialising to concrete examples, we show in Theorems 4.2 and 4.3 that the question of arbitrage can be reduced to simple ordering properties of particular functions. To the best of our knowledge, the present work is the first one to address the issue of arbitrage in a robust setting with additional information/beliefs.

Concerning the characterisation of worst case models we exemplify the power of the monotonicity principle in Theorem 4.4 in a concrete setup. We consider the example of variance options with drawdown constraints, and show that we are able to

-

(1)

Determine when there exists an arbitrage for the insider;

-

(2)

Characterise the class of extremal models;

-

(3)

Compute numerically the value of the insider’s information.

Specifically, in Section 4.2.1 we give a numerical example to show the impact of increasing information on the insider’s extremal model. Thereby, we can nicely illustrate the impact of increasing information; see Figure 5.

1.1. Literature

In the robust approach to mathematical finance, the usual setting consists in having some assets available for dynamic trading, and some claims which are available at time zero for static, i.e. buy-and-hold, trading. The information at the disposal of the agent is the price of assets and claims at time zero, and the evolutions of the price of assets in time. In this framework, most of the literature so far has been devoted to showing pricing-hedging duality results, that is, that the minimal cost to super-hedge pathwise a given derivative, equals its maximal price over calibrated martingale measures; see e.g. [BHP13, Acc+16, Nut14, BN15, BZ17, FH16] in discrete time, and [GHT14, DS14, DS15, BCH17, Bia+17, B+17, HO18, GTT16, Bei+17] in continuous time, among a rapidly growing literature.

The current literature on the insider problem in a robust setup is still in its infancy. In [AL17] and [AHO16] the informed agent has a richer information flow, which results in having more choices for trading strategies, and hence in cheaper robust (super-hedging) prices. In [AL17] the authors study the models under which the market is complete in a semi-static sense, and through these models they compare the robust prices of the agents with and without additional information. In [AHO16], pricing-hedging duality results are given when the additional information is disclosed either at time zero or at a given future instant in time, and it is given by specific random variables.

Mathematically, our approach is closer to [CHO16], [HO18], [BKN20], [BZZ18]. Those papers do not consider insider information, but model beliefs or prediction sets in a robust setting by specifying the set of feasible paths for the possible evolution of the asset’s price process. The main aim in these papers is the study of the pricing-hedging duality. In [CHO16] the authors work in discrete-time and study duality, showing that in some cases a gap may appear, i.e. duality may fail. In [HO18] a continuous-time setup is considered, and sufficient criteria are given so that duality holds in an asymptotic sense. In [BKN20] the authors consider a continuous-time setting and prediction sets in the space of continuous paths, and provide several duality results. Finally, in [BZZ18] the authors obtain duality and monotonicity results for a broad class of constrained optimal transport problems, under some conditions on the space of paths and on the set of admissible transports.

In the present paper we work in continuous time, so our duality results are comparable to those in [HO18],[BKN20], [BZZ18]. However, [HO18] considers derivatives with uniformly continuous payoff, so that the framework is orthogonal to the present one, where payoffs are assumed to be invariant to time change. In [BKN20] these restrictions are substantially weakened, but without the inclusion of other traded options. In [BZZ18] analyticity conditions are required on the set of admissible paths, rather than the time-invariance assumed here. Also in a similar spirit to our results in Section 4.2 is the PhD thesis of [Spo14], which considers the situation where only finitely many options are available for static trading and, for specific kinds of derivatives, describes the optimal solutions for agents having beliefs on realised variance.

To the best of our knowledge, the constrained Skorokhod embedding problem (conSEP) has not previously been systematically considered in the literature. The only papers which we are aware of, that consider related problems, are [AS11] and [AHS15], that provide conditions under which a distribution may be embedded in Brownian motion or a diffusion in bounded time, which have some connections to the results in Section 4. Also, the setting in [BZZ18] covers for example the case of robust pricing in case of bounded quadratic variation, which leads to establishing conditions for the existence of Skorokhod embeddings in bounded time.

1.2. Outline of the article

In the present paper we will work in a continuous-time setup, under the assumption that the asset’s price process evolves continuously, and all call options for a given maturity are traded at time zero in the market. We perform a time-change to formulate the pricing problem as a constrained optimal stopping problem in Wiener space and resort to Skorokhod embedding techniques. For this approach to be effective, we need to restrict our attention to the case where both the derivatives’ payoff function and the feasibility of paths are invariant to time-changes in an appropriate sense. The key concepts and definitions for this setup are introduced in Section 2. In Section 3, we show that the pricing-hedging duality and the monotonicity principle of [BCH17] can be extended in a natural way to our setting, thus allowing us to give a geometric characterisation of the support of the optimisers in the primal problem.

Then, in Section 4, we consider specific examples of feasible sets where we may apply the results of the previous sections to determine specific consequences of certain types of information possessed by the insider. We first consider the implications of information which restricts the observed paths to occur either before or after (or both) some path-dependent event. In this case, we are able to give sufficient conditions for the existence of arbitrage for the insider. Next, we consider the case where feasibility corresponds to paths which do not enter given regions of an appropriate phase-space, and determine necessary and sufficient conditions for the additional information not to introduce arbitrage possibilities. Finally, we show how the monotonicity principle can be used to derive characterising properties of the optimisers subject to a given information set. In particular, we consider the problem described at the start of the introduction, where the insider believes a certain drawdown constraint is satisfied, and wishes to understand the impact on variance derivatives. In this case, we are able to describe the properties of the resulting optimiser, and also compute numerically an upper bound on the value of the derivative in both the model without information, and the model with information. These numerical results give us a good indication of the impact of the information on the prices of other derivatives.

2. Informed robust pricing

Throughout the paper, for , we write for the space of continuous functions endowed with the topology of uniform convergence on compacts. When , we write for the subset of paths such that .

We consider a market consisting of a risk-free asset (bond), whose price is normalised to , and a risky asset (stock) which is assumed to have a continuous price evolution, though neither a reference probability nor the dynamics are specified. The assets are continuously traded on the fixed time-horizon , . Let the initial price of the stock be ; in this way we can think of the stock price process as the canonical process on . We assume we observe the prices of call options with maturity for all strikes, which corresponds to having the knowledge of the marginal distribution of at time , say , under any pricing measure by the Breeden-Litzenberger formula, [BL78]. In particular, . We assume . This condition is introduced in order to simplify the presentation, and can be relaxed (see e.g. [BCH17, Section 7]). Given a derivative with payoff function written on , the robust pricing problem is to determine

| (2.1) |

where is the set of all martingale measures on such that (by martingale measure we mean a measure under which the canonical process is a martingale). This leads to the upper price bound for the derivative related to the worst case scenario of the evolution of the risky asset. Analogously, one can consider the infimum in (2.1), that is, the lower price bound for . Mathematically the maximisation and minimisation problems are very similar, and in this article we concentrate on the former.

In practice, often not only the prices of call options with given maturity are available, but an agent may have other information or beliefs relating to the evolution of the asset price. Incorporating this information may rule out certain behaviour of the stock price , and hence certain models for , which in turn leads to potentially smaller price bounds. We model this by introducing an informed agent, also called the insider, possessing some additional information and beliefs which enables her to only consider a subset of feasible paths for (precise assumptions on will be given in (2.5)). All other paths in are deemed negligible due to the additional information held by the insider. Hence the robust pricing problem for the insider is

| (2.2) |

To give a value to the additional information, we will talk of the uninformed agent or outsider when considering an agent who does not have any other information than the call prices. Hence, the outsider’s pricing problem is the classical robust pricing problem in (2.1), which corresponds to setting in (2.2).

In the rest of this section, we recall and adapt the setup and results from [BCH17] and [Bei+17] relying on [Vov15], which will allow us to formulate and analyze (2.2) as a constrained Skorokhod embedding problem. In order to do so, we will first introduce a time-change, in Section 2.1, that is a different clock under which we want to observe the paths of . Next we will show that the pricing problem (2.2) has an equivalent formulation as an optimal stopping problem for Brownian motion on some probability space (problem (2.6)), when the derivative and the additional information are invariant with respect to this time-change. Finally, we shall pass from this weak formulation of the problem to an optimisation problem on a single probability space, the Wiener space, which will require more general stopping rules; see problem ().

2.1. Time transformation.

The key tool to translate (2.2) into a constrained Skorokhod embedding problem is the Dambis-Dubins-Schwarz Theorem. However, we need to be careful in defining the time change since we want to be able to shift pathwise inequalities from to the Wiener space and back. Moreover, the time change will be a useful tool to precisely define the options we want to consider as well as the set of feasible paths for the insider.

For and , we define the sequence of times

and we say that has quadratic variation if the sequence of functions

converges uniformly on compacts to some function in , and the limit function has the same intervals of constancy as . We denote this function by . We write for the space of all paths in possessing such a quadratic variation and such that either diverges at infinity or is bounded and has a well defined limit at infinity. These conditions are necessary in order for the map given below to be well defined. It is not hard to show that is a measurable subset of .

We define the space of stopped paths as

and equip it with the distance defined for by

which turns into a Polish space. The space is a convenient way of encoding optionality of a process in our pathwise setup, see e.g. [DM78, Theorem IV. 97]; note that optionality is equivalent to predictability, since we consider only continuous paths. More precisely, we set

where denotes the restriction of to . Then a process with is optional if and only if there is a Borel function such that .

We call the set of paths in which have a continuation in , and for we define the following new clock:

| (2.3) |

with the usual convention .

We will work with the normalising time transformation introduced by Vovk [Vov12], which is defined by given by

That is, is a version of the path run at a speed such that, for every , its pathwise quadratic variation at time is exactly . It will also be notationally useful at times to ‘forget’ the time component, and consider the function , which is equal to . Of course, the two quantities are mathematically equivalent. The normalising time transformation will be the tool that will allow us to define the class of time-invariant derivatives and the kind of time-invariant additional information which are suitable in order to develop the SEP approach to robust pricing with insider information.

Remark 2.1.

In this article, we consider payoff functions which on satisfy

| (2.4) |

for some Borel measurable . This means that the payoff function is identical for all paths which are time-transformations of each other, that is, which coincide after normalising the speed at which they run.

A key additional component in our model will be the information which is held by the insider, and which is not known to the market. We will model this by assuming that the insider knows a set of feasible paths . Thanks to Remark 2.1, we may assume without loss of generality that . As with the payoff function, we will assume that the set of feasible paths is time-invariant. More precisely, we will consider sets given by

| (2.5) |

for some measurable subset , so that . We will call the feasibility set. In this way, feasibility of a path is shifted to admissibility of the stopped path . In particular, if a path is feasible, so is any other path which is a time transformation of .

2.2. Informed robust pricing as constrained SEP

The time transformation introduced above enables us to express the robust pricing problem (2.2) as a constrained optimal stopping problem for Brownian motion.

Proposition 2.2.

The condition means that, when moving along a path of , we can stop only at times such that the stopped path lies in . This corresponds to the fact that informed agents only need to take into account the paths in the feasibility set, . The condition of uniform integrability on is - in the current setup - equivalent to being minimal, cf. [Mon72]. This means that, for any other stopping time in the same filtered probability space,

| (2.7) |

The reformulation in (2.6) shows how the maturity time , at which we know the marginal distribution of the price process, does not play any role in the pricing problem. This is a consequence of the time-invariance assumption.

Proof.

The proof of this essentially follows from [Bei+17, Section 4]: Let , be the time-change defined in (2.3), and the usual augmentation of the filtration generated by . It is easy to verify that is a stopping time with respect to the filtration . Then, the Dambis-Dubins-Schwarz theorem implies that the process is a stopped Brownian motion under in the filtration . Moreover, it is uniformly integrable and satisfies . Vice versa, let be a Brownian motion on some probability space , and be a stopping time such that is uniformly integrable with . Then, for defined by , we have that . The result follows. ∎

To be able to analyse the optimisation problem (2.6), we introduce another optimisation problem living on a single probability space, the Wiener space . To this end we consider the set

where denotes the set of probability measures on a space , and is a regular disintegration of with respect to the first coordinate . We equip with the weak topology induced by the continuous bounded functions on . Each can be uniquely characterised by the cumulative distribution function .

Definition 2.3.

We say that a measure is a randomised stopping time if the corresponding increasing process is optional, and write . For an optional process and , we define as the pushforward of under the mapping . We denote by the set of all randomised stopping times such that and .

Remark 2.4.

It is well known that any randomised stopping time can be identified with a stopping time on the extended probability space , where denotes the Borel -algebra on , and the Lebesgue measure on . One way of defining is via

As a consequence, the optional stopping theorem applies for randomised stopping times. Indeed, any process on can be lifted to a process on by setting and then the classical optional stopping theorem applies for, e.g., uniformly integrable martingales.

Considering the martingale it follows from classical results on stopping times (e.g. [Hob11, Corollary 3.3], [BCH17, Lemma 3.12], Remark 2.4) that, for with , the condition is equivalent to

| (2.8) |

which is assumed to be finite in our setup.

By [BCH17, Theorem 3.14], is non-empty and compact with respect to the topology induced by the continuous and bounded functions on . As a direct consequence we get the following result:

Corollary 2.5.

Let be closed. Then the set of feasible randomised stopping times

| (2.9) |

is convex and compact with respect to the topology induced by the continuous and bounded functions on .

We highlight here the important feature that might be empty, which can be understood as a robust arbitrage opportunity, see Proposition 3.3 and Section 4.

Proof.

Since is assumed to be closed, the function is u.s.c. Hence is a closed condition by the Portmanteau theorem. ∎

Another important property of the feasible randomised stopping times is that they are precisely the joint distributions on of pairs satisfying the constraints in (2.6). This is a straightforward extension of [BCH17, Lemma 3.11]. Putting everything together we have derived a formulation of our optimisation problem (2.2) resp. (2.6) on the Wiener space as a constrained Skorokhod embedding problem:

Proposition 2.6.

In the setting described above,

| () |

We will say that () is well posed if exists with values in for all , and is finite for one such . In particular, () is not well posed if which has a pleasing financial interpretation (cf. Proposition 3.3). The (unconstrained) Skorokhod embedding problem corresponds to the case , when all paths are feasible, hence the above supremum is taken over .

From an analytical point of view, the formulation () is extremely useful since we are now dealing with a linear optimisation problem over a convex and compact set on a single probability space. A direct consequence is the following result:

Theorem 2.7.

Proof.

We claim that without loss of generality we can assume that is bounded from above. Indeed, by the pathwise version of Doob’s inequality (see [Acc+13]),

for some martingale starting in zero. Hence condition (2.10) implies that

is bounded from above and the term is independent of by (2.8) and the assumed second moment of . Therefore, we can assume to be bounded from above.

Finally, since is compact and continuous, and by the Portmanteau Theorem the map is upper semi-continuous, we deduce the result. ∎

3. Super-replication and monotonicity principle

In this section, we show that a straightforward application of the results in [BCH17] leads to duality or superhedging results, and to a geometric characterisation of primal optimisers, that is, to the monotonicity principle for constrained Skorokhod embedding.

3.1. Duality

In this section, we first show a duality result for the problem defined in (2.6), that is for (), and then from it deduce a duality result for the original robust pricing problem defined in (2.2). The latter is the analogue of the super-replication duality in the present robust setting with additional information/beliefs. As in the classical (non-robust) case, this in turn leads to a dichotomy between existence of martingale measures and existence of arbitrage opportunities, the so-called fundamental theorem of asset pricing, which we prove at the end of this section.

A martingale is called -continuous if there exists a continuous such that . Note that a martingale which is -continuous has continuous paths, but the other implication is in general not true.

Theorem 3.1.

Let be upper semi-continuous and bounded from above in the sense of (2.10), and be closed. Set

| (3.3) |

where satisfy

| (3.4) |

Then we have

Proof.

Put

| (3.5) |

Since we assume that is upper semi-continuous and bounded from above in the sense of (2.10), it is easy to see that these properties are inherited by . Moreover, the well-posedness assumption of () for implies that () is still well-posed for and . Hence, the result follows from [BCH17, Theorem 4.2]. ∎

This duality result is already of interest in its own right. However, to identify it as a superreplication result we need to recover the hedging strategies corresponding to the martingale. For this we need some kind of pathwise martingale representation theorem. In fact Theorem 6.2 of [Vov12] can be interpreted as such. To this end, we need to introduce some more notation.

We will need the concept of simple strategy, by which we mean a process of the form

where are -stopping times such that for every one has , and are -measurable bounded functions for . For such a strategy, we can define the corresponding pathwise stochastic integral as

Then, following exactly the line of reasoning as for the proof of [Bei+17, Theorem 3.1] one can get the following result. We recall that and , and that the robust pricing problem for the insider was defined in (2.2).

Theorem 3.2.

Let be upper semi-continuous and bounded from above in the sense of (2.10), and let . Set

where and for some and all . Then we have

Theorem 3.2 is the analogue of the classical super-replication duality theorem, in the present robust insider setting. Moreover, like its classical counterpart, it additionally implies a version of the first fundamental theorem of asset pricing. In the following we will use Theorem 3.2 with different payoff functions. To stress the dependence on the cost function we will sometimes write .

Proposition 3.3.

Under the assumptions of Theorem 3.2, the following are equivalent:

-

(i)

such that ;

-

(ii)

;

-

(iii)

, simple strategies , and with such that

(3.6)

Property means that one cannot make arbitrary profits by starting with zero capital. Indeed, if (3.6) holds for some , then it does so for any .

Proof.

The equivalence between and follows from the arguments around Proposition 2.2.

: Note that implies for any derivative s.t. on , by Theorem 3.2. Pick

Suppose, for contradiction, that there exist and s.t. (3.6) is satisfied. Then,

the pair is admissible for the dual problem . However, this implies for , which gives the desired contradiction.

: By Theorem 3.2, if there is no measure such that , then for all derivatives . In particular, for

there exist and , with , such that (3.6) holds. ∎

Remark 3.4.

In this paper, we have only considered the case where the information of future call prices at a single fixed time is observed. Using similar methods to those developed in [Bei+17], it is also possible to extend Theorems 3.1 and 3.2 to the case where the call prices at times are observed, and provide a related formulation in the Brownian setup where the optimisation is over a sequence of stopping times . In this case, it is possible to consider both the cases where call price information completely fixes the distributions at the intermediate times, or it only determines the integral of particular functions, or there is a mixture of some times having full information and others lacking it. In this more general setup, it becomes possible to include a large class of options, for example, a robust approach to discretely monitored Asian options could be included.

3.2. Constrained monotonicity principle

In this section, we provide a modified version of the monotonicity principle of [BCH17] giving necessary geometric conditions on the support set of an optimiser to ().

To this end, we denote the concatenation of two paths by , i.e.

For we define the process

Definition 3.5.

A pair is called feasible stop-go pair, written , if , , the set of stopping times satisfying and a.s. is non-empty, and every such stopping time satisfies

| (3.7) |

and a.s., where both sides of (3.7) are well defined and the left hand side is finite. Here, the probability space is assumed to be rich enough to support a Brownian motion , and denotes the natural filtration generated by .

The interpretation is that on average it is better to stop a path at time with history , and to run the paths that would have carried on from from a previously stopped history (to let go), as long as this results in a feasible stopping rule. Note that since , the law of the stopped process is not changed. We remark here that – as a consequence of only considering stopping times – the definition of feasible stop-go pairs is independent of the probability space on which lives as long as it is rich enough to support the Brownian motion . In a similar manner to [BCH17, Section 5], one could introduce an even stronger notion of feasible stop-go pairs only considering one particular candidate stopping time. In this article, we do not need this generality.

For a set we denote by the set of all stopped paths which have a proper extension in :

Definition 3.6.

A set is called feasible -monotone if

A set should be viewed as a possible stopping set, i.e. a set of paths for an admissible stopping strategy in (). If such a set is feasible -monotone then there is no way of changing the stopping rule in a pathwise fashion, as in (3.7), resulting in a feasible stopping rule with higher payoff.

Theorem 3.7 (Constrained Monotonicity Principle).

4. No-arbitrage, pricing and hedging in specific information settings

Up to now we have shown that under our assumptions the robust pricing problem (2.2) can be reformulated as a constrained Skorokhod embedding problem for which we have established general results on existence, superheding, a variant of the first fundamental theorem of asset pricing, and a characterisation of optimisers.

The goal of this section is to illustrate the richness of our framework by considering some natural choices for the insider’s information set , or equivalently for the corresponding feasibility set , to show that under additional assumptions we are able to prove a variety of very explicit results in the insider’s setting.

We use the notation to denote the convex order relation between probability measures; specifically, we say that if for any convex function .

In the examples we consider, we will typically address three related questions:

- (1)

-

(2)

Assuming , can we characterise the worst case scenarios for the insider, i.e. can we characterise solutions to the constrained Skorokhod embedding problem? We provide a characterisation of the optimisers to a specific problem in Theorem 4.4.

-

(3)

Given a pair such that , and a derivative with payoff , what is the value of , and how does this differ from , the price of the uninformed agent? We answer these questions in the context of a specific example in Section 4.2.

In investigating the questions above, we will focus on the three following natural examples where the additional information/beliefs translates into stopping the Brownian motion after and/or before given stopping times. Let be stopping times such that , and are uniformly integrable, and consider the sets

| (4.1) |

These cases notably cover the examples of additional information and beliefs mentioned at the beginning of the paper, whether prices hit certain barriers, whether the quadratic variation reaches certain levels (cf. Section 4.1.1), and on drawdown constraints (cf. also Section 4.1.2).

In this situation we have the following basic result on the existence or absence of a consistent model for the insider.

Theorem 4.1.

Proof.

As a consequence of Strassen’s Theorem [Str65], a solution to the constrained problem (2.6) exists for if and only if . Similarly, in the case of , the condition is a necessary condition for the existence of a stopping time for the Brownian motion such that , but it is not sufficient unless is supported on two points due to the result of Meilijson [Mei82] and van der Vecht [Vec86].111A simple example can be constructed by considering the measures , with stopping time and . For sufficiently small, it is easily checked that , but there is no bounded stopping time embedding . Combining these two observations yields the third item. ∎

To the best of our knowledge, necessary and sufficient conditions for the existence of are unknown. We are able to provide them in specific settings (see Section 4.1), while the existence of general criteria remains an interesting open problem.

Before we proceed, we would like to remark on the specific form of the feasibility sets in (4.1). It is clear that, in general, not all information processes/feasibility sets are of the form (4.1). A full classification and analysis is beyond the scope of this paper. One of the various reasons that makes this analysis complicated is that the constraint may impose additional conditions that are not immediate from the construction of . Consider for example the case where

| (4.2) |

for some fixed , which corresponds to the drawdown constraint on the price process not dropping more than below its maximum-to-date value.

Minimality (cf. (2.7)) implies that an admissible stopping time must occur before

,

by a simple martingale argument. Hence, although there exist feasible paths in which live longer

than , any which is in must, with probability one, be bounded above by . Therefore, the set of feasible

stopped paths in this case can be replaced by . Then, from the argument above, must hold

in order to have a solution to the constrained embedding problem.

On the other hand, if the set of admissible evolutions for the asset is

which is a drawdown constraint where the constraint depends on the running average of the price process, then we are not able to replace by a ‘nice’ set as above.

Here the class of admissible stopping times is certainly bounded

above by a stopping time (), but it is easily seen that there are inadmissible paths which occur before this time.

In what follows we will consider the cases in Theorem 4.1 separately, analysing them in specific settings. In particular, in Sections 4.1.2 and 4.1.1 we present two frameworks where the additional information is of the kind in (4.1), and we are able to give necessary and sufficient conditions for the set to be non-empty, hence strengthening the result in case (1) of Theorem 4.1. In Theorem 4.4, we will exemplify the power of the monotonicity principle by showing the structure of the solutions to a Root-type optimisation problem with an Azéma-Yor-type constraint.

Moreover, in Section 4.2 we consider the additional information to be of the kind in (4.1) and, for options on variance, we determine the primal optimisers by means of our constrained monotonicity principle (Theorem 3.7), as well as the dual optimisers.

We remark that the first two cases imply results and constraints for the third case also, e.g. Theorems 4.3 and 4.2 directly imply necessary conditions for the third case. More generally, using the monotonicity principle Theorem 3.7 one can derive the corresponding versions of Root and Azéma-Yor embedding with a general time-space starting law (cf. Section 4.2 for the case of Root). Using similar arguments as in the proof of Theorem 4.3 and 4.2, with slightly more notation, one can derive the corresponding versions of these results keeping also track of the condition implying necessary and sufficient conditions for the case . We omit the details.

4.1. Information as barrier in a certain phase space.

We now consider the case where the additional information is of the kind of in (4.1) and translates in having a barrier in a certain phase space. We will see how in this situation the No-Arbitrage condition (cf. Proposition 3.3, Theorem 4.1) imposes an order between such a barrier, and the barrier characterising the unique optimal stopping for the uninformed agent in such a phase space. These results are notable since the ordering of barriers is a much weaker condition than the convex order condition, significantly strengthening the results of Theorem 4.1.

4.1.1. The Root phase space

We recall that the Root solution of the (unconstrained) Skorokhod embedding problem for the distribution is given by

where is a closed barrier, that is, implies for ; see [Roo69]. This is one of the first known solutions to SEP, and is optimal when for a strictly convex function . The Root solution is illustrated in Figure 1. To avoid trivialities, we assume that our barriers are regular (see [COT19]), that is, they are closed and is an open interval, containing the origin; any barrier which is not regular can be replaced by a regular barrier without changing the hitting time. Any regular barrier can be described by its lower semi-continuous barrier function

For the informed agent we assume that

where the stopping time is the hitting time of a regular barrier in the phase space , i.e. a Root-type barrier:

| (4.3) |

As in Theorem 4.3, we are able to determine whether is empty, and hence whether there is an arbitrage for the informed agent, through properties of the barriers.

Theorem 4.2.

Proof.

We first observe that if (4.4) holds, then we immediately have , and since , then . To show the reverse implication, suppose, for contradiction, that is non-empty and . This means that there exist pairs . Among those pairs, we consider a fixed such that there are no with , as in Figure 2.

Now consider . Denote the local time of Brownian motion in by . Since the Root embedding maximises among all stopping times which are minimal embeddings of (cf. (2.7)), simultaneously for all (e.g. by [GOR15, Theorem 3]), then in particular

On the other hand, the path stopped at cannot accumulate any more local time at after , i.e. for all , while the Root stopping rule will do so ( when ), because the barrier is assumed to be regular. Therefore,

This gives the desired contradiction, since, for any and any stopping time ,

where is the potential function associated to , i.e., . ∎

4.1.2. The Azéma-Yor phase space

We let , and define the process analogously. We start by recalling the Azéma-Yor solution of the (unconstrained) Skorokhod embedding problem (SEP). The barycenter function of a probability measure is defined by

Denote the inverse of by . The solution to the SEP by Azéma and Yor, see [AY79], is given by

This is arguably the most renowned solution to SEP, for which many properties are known, among which, that it maximises stochastically the maximum of the stopped Brownian motion. See the survey article of [Obł04] for further details. We illustrate the Azéma-Yor solution in Figure 3.

For the informed agent, we assume that

| (4.5) |

where the stopping time is the hitting time of a barrier in the phase space :

where is a Borel set induced by some increasing left-continuous Borel function via

so that and imply . Note that this gives

| (4.6) |

thus the set in (4.5) corresponds to the following set of feasible paths for the informed agent:

| (4.7) |

that is, the paths that satisfy the drawdown constraint during the period .

We now give a result which shows that, when the agent’s information is given by as in (4.7), then we can provide a simple necessary and sufficient condition for the existence of consistent models for the informed agent, cf. (1) of Theorem 4.1. If there is no ambiguity we write in the following.

Theorem 4.3.

Proof.

We first observe that if (4.8) holds, then we immediately have , and since , then .

For the reverse implication, we suppose that there exists such that , as in Figure 4.

Then we fix , and argue as follows. Define a measure

and note that, by the martingale property, . Moreover, , and for all Borel sets .

Define functions by:

and similarly for . Then are both increasing on , , and is increasing in for since . Hence we deduce that for .

Now we observe that , so . On the other hand, by the definition of the barycentre function,

It follows from that , contradicting our original assumption. ∎

Let us consider the drawdown constraint in (4.2) which corresponds to , with given as in (4.6) for . In this case Theorem 4.3 implies that must hold in order to have a feasible solution for the informed agent. This condition can of course be rephrased in terms of barycentre functions since is the inverse of the barycenter function associated to (by [AY79]). Therefore, the existence of a consistent solution for the insider is equivalent to , that is, .

Theorem 4.3 tells us when the pricing problem for the insider, cf. (2.2) or (2.6), has a feasible solution, and hence an optimiser under the conditions of Theorem 2.7, but does not tell us anything about the specific optimiser. On the other hand, the constrained monotonicity principle, Theorem 3.7, allows us to characterise the geometry of optimisers in various settings. We illustrate this in the special situation where the agent wishes to find the stopping times solving () in the case corresponding to the payoff We are interested in characterising solutions to

| (4.9) |

where

| (4.10) |

for a step function with and . We set , and note that and imply that .

We recall that in the unconstrained case, i.e. , the solution is the Root solution , the first hitting time of a barrier in space-time (see also Section 4.1.1).

In the current setup, the situation is similar:

Theorem 4.4.

Assume that and that the optimisation problem (4.9) is well posed. Then for any optimiser there exists a sequence of barriers such that

where

Moreover, for each it holds that

Proof.

To avoid too many minus signs, we redefine and for this proof we consider the minimisation variant of ().

By Theorem 2.7 we can find a minimiser, say , to the optimisation problem (4.9). By Theorem 3.7 we can pick a feasible -monotone set such that and .

We claim that

| (4.11) |

Indeed, pick with and . It holds for any by convexity of (and since we are considering minimisation instead of maximisation) that

so that (3.7) follows by two observations. First, implies the existence of at least one Brownian stopping time with such that , e.g. if then the first hitting time of Brownian motion of is such a stopping time. Second, any stopping time with necessarily satisfies , since , and the function defining is increasing.

Put and set

Pick . Then we claim that

Since the first inequality holds by construction, suppose for contradiction that . In this case, there is such that , and since it holds that . Then there exists such that and so that . However, by (4.11), this means that , which cannot be the case.

Pick such that for some . It then follows that

Then, we can conclude the existence of the barriers by the observation that conditionally on the event it holds a.s. by the strong Markov property and the fact that Brownian motion almost surely immediately returns to its starting point.

To show the final claim, note that (4.11) implies that at each the condition with implies . Just as in the first part of the proof, it then follows that there is no with and . This gives the result. ∎

Example 4.5.

Consider the case of , when . Let be given by the inverse barycentre function of , i.e. which equals

In particular, in the Root-type optimisation problem (4.9) constrained by as in (4.10), any path which reaches level will not be stopped at .

The unconstrained Root solution instead is given by the hitting time of

for some . In particular, there are paths getting arbitrary close to one but which are stopped at so that the constrained Root solution is different from the unconstrained one.

Also note that this is not related to the special case of begin atomic. Indeed, keep the same . Consider to be the uniform measure on whose inverse barycentre function is given by so that by Theorem 4.3. By the same reasoning as before, it is immediate to see that the Root solution is different from the constrained Root solution.

Remark 4.6.

Let us consider (4.9) for the case of a general increasing function yielding a corresponding set of feasible paths as in (4.10). Assume Approximate from below by step functions with corresponding sets of feasible paths and the property that . Since then , it follows that . For each , pick by Theorem 2.7 an optimiser to (the corresponding version of) (4.9), say . Since , it follows that for all

Since is compact and for all , there is a converging subsequence and any limit point must lie in Moreover, any limit point must be an optimiser by monotonicity, since

Since, by Theorem 4.4, each is given as the hitting time of barriers in space-time indexed by the running maximum, it is then plausible to conjecture that this remains true for as well. To make this argument rigorous seems to be outside the scope of this article, however we note that (4.11) still holds in the limit.

Remark 4.7.

Considering in (4.9) a maximisation problem instead of a minimisation problem, the corresponding version of (4.11) turns into

Following the line of reasoning of Theorem 4.4, one can show that the optimal stopping time will be the hitting of a sequence of inverse barriers indexed by the running maximum, i.e. the corresponding version of constrained Rost solutions. Using similar ideas one can identify the optimal solutions and worst case scenarios in various different setups.

4.2. Option pricing in the presence of insider information: Variance options

In this section, we consider the impact on the insider’s pricing bounds which come from additional information. Specifically, we suppose that the information is on the drawdown, in a similar manner to the previous discussion, for example, as in (4.10), and we look to find bounds on the prices of options on variance: that is, we consider the motivating example from the introduction, where we think of a trader who believes that the CEO of the company is attempting to satisfy a drawdown constraint, and wishes to understand the impact on pricing bounds of variance options on the same company.

To understand the structure of the derivatives, we consider an asset which follows a model of the form: , where is the discounted asset price, and a Brownian motion. The process is the volatility, and is known as the integrated variance. A variance option is then a contract which pays the holder . The most common example is the variance call, where . Note that the integrated variance process can be determined as , the quadratic variation of the logarithm of the asset price. For further details, we refer the reader to [CL10, Lee10, CW13a, CW13].

The standard method for pricing such options is to time-change the process by a time change such that is a geometric Brownian motion. With this time change, , that is, the time-scale in the transformed picture corresponds to the integrated variance process. In particular, the problem of finding a model which minimises subject to is equivalent to finding a stopping time for to minimise subject to .

We would therefore like to compare the minimal (model-independent) price of the variance option for the insider, to that for the uninformed agent. To keep things simple, we consider an option which pays the holder the square-root of the arithmetic variance, , which corresponds to choosing a time-change so that is a Brownian motion. This places us trivially in the setup of the rest of this paper.

Our problem of interest now may be posed as follows: consider an agent who has inside information on the future evolution of the asset, specifically, who knows that the price will never drop below , where is an increasing function. The agent plans to exploit this information by trading in derivatives written on the asset, and do not have strong modelling beliefs, so wish to profit from their information under any potential model. Suppose variance options with payoff are liquidly traded. To profit, they plan to sell the derivative and setup a model-independent super-hedging strategy. They want to know at what price-level they are guaranteed to make a profit. If the agent also knows the feasibility set given by (4.10), then their problem becomes to find

| (4.12) |

By Theorem 3.2, if we can identify the solution to this problem, then there exists a corresponding super-hedging strategy. However, it follows from Theorem 4.4 that the solution must be a nested sequence of barriers, which depend on the running maximum. To see how these barriers, and more specifically, the price bound, may depend on the information set, we consider the problem numerically under some additional structural examples.

4.2.1. Numerical results

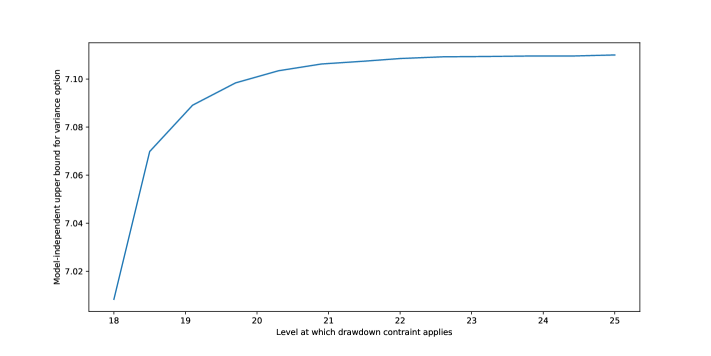

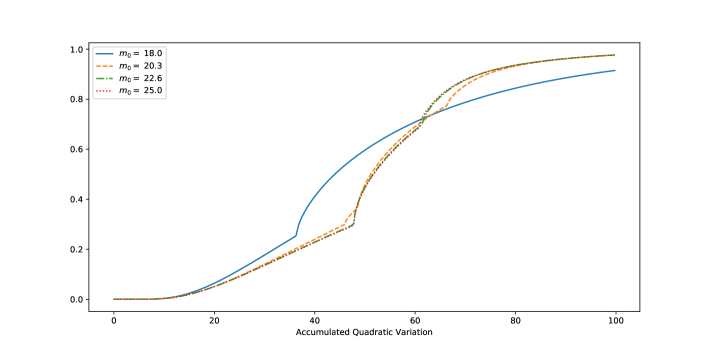

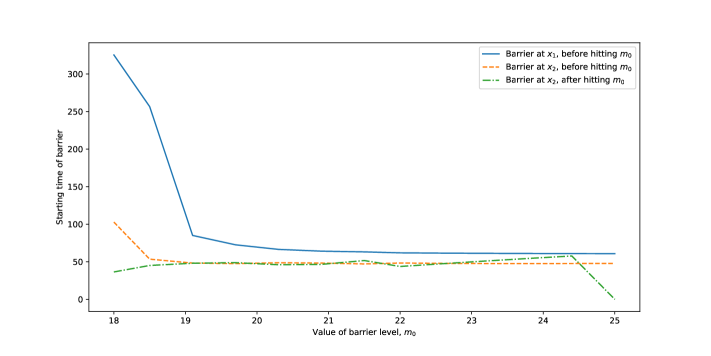

In this section we illustrate the previous example with some numerical evidence. In particular, we are interested in illustrating how the insider’s price changes as the information set changes.

Our basic setup is as follows: we suppose that the insider’s information set is determined by (4.10), where the function is of the form: , that is, there is a single step in the constraint, which comes in at the point where the maximum first exceeds the level . In the examples, we will consider the case where the information set changes by varying . Moreover, we will assume that the measure to be embedded consists of 4 atoms, at points , and we have . It follows that the main issue to be determined is the value of the barrier at the level when the level has not yet been reached, and the barrier at both before and after reaching . From Theorem 4.4, we know that the barriers at are ordered — that is, the earliest time at which we stop at before reaching , is later than the earliest time we stop at after reaching . Since the embedding constraint has two degrees of freedom (there are four atoms of mass, but two values are fixed by the requirement that the probabilities sum to one, and the requirement that the embedded mass has mean equal to ), this means that we can compute the optimal barrier by optimising over the single remaining degree of freedom.

We implement a simple numerical algorithm, inspired by the PDE characterisation of [CW13a], which finds the potential of the stopped process. By optimising over the potential functions of the measure embedded before and after reaching , we are able to compute the critical times at which the barriers must start. Here, the potential associated with a measure on is defined to be: . The numerical implementation was performed in Python222A Jupyter notebook containing the code used to produce the figures in this paper can be downloaded from https://github.com/amgc500/SEPInsider.. In Figure 5 we plot the price of the variance option as a function of . Moreover, we can see how the law of the quadratic variance in the extremal model varies as we change : this is shown in Figure 6 for several values of , as well as the values of the barrier at , before and after hitting .

Under the restriction to a small number of atomic masses, the optimal models are relatively easy to find numerically in simple examples such as these. However, Theorem 4.4 only provides necessary conditions for a given barrier to be optimal. An open, and interesting question, is whether it is possible to provide sufficient conditions, and moreover, whether a numerical scheme to compute the corresponding bounds can be implemented. Doing this appears to us to be a challenging problem, and we leave this as an open question for future work.

References

- [Acc+16] B. Acciaio, M. Beiglböck, F. Penkner and W. Schachermayer “A model-free version of the fundamental theorem of asset pricing and the super-replication theorem” In Math. Finance 26.2, 2016, pp. 233–251 DOI: 10.1111/mafi.12060

- [Acc+13] Beatrice Acciaio et al. “A trajectorial interpretation of Doob’s martingale inequalities” In The Annals of Applied Probability 23.4 Institute of Mathematical Statistics, 2013, pp. 1494–1505

- [AL17] Beatrice Acciaio and Martin Larsson “Semi-static completeness and robust pricing by informed investors” In The Annals of Applied Probability 27.4 Institute of Mathematical Statistics, 2017, pp. 2270–2304

- [AHO16] Anna Aksamit, Zhaoxu Hou and Jan Obłój “Robust framework for quantifying the value of information in pricing and hedging” arXiv:1605.02539, 2016

- [AIS98] Jürgen Amendinger, Peter Imkeller and Martin Schweizer “Additional logarithmic utility of an insider” In Stochastic Processes and their Applications 75.2, 1998, pp. 263–286 DOI: 10.1016/S0304-4149(98)00014-3

- [AS11] S. Ankirchner and P. Strack “Skorokhod embeddings in bounded time” In Stoch. Dyn. 11.2-3, 2011, pp. 215–226 DOI: 10.1142/S0219493711003255

- [AHS15] Stefan Ankirchner, David Hobson and Philipp Strack “Finite, integrable and bounded time embeddings for diffusions” In Bernoulli 21.2, 2015, pp. 1067–1088 DOI: 10.3150/14-BEJ598

- [AY79] Jacques Azéma and Marc Yor “Une solution simple au probleme de Skorokhod” In Séminaire de probabilités XIII Springer, 1979, pp. 90–115

- [BKN20] Daniel Bartl, Michael Kupper and Ariel Neufeld “Pathwise superhedging on prediction sets” In Finance and Stochastics 24.1 Springer, 2020, pp. 215–248

- [BZZ18] Erhan Bayraktar, Xin Zhang and Zhou Zhou “Transport plans with domain constraints” In Available at SSRN 3161652, 2018

- [BZ17] Erhan Bayraktar and Zhou Zhou “On arbitrage and duality under model uncertainty and portfolio constraints” In Mathematical Finance 27.4 Wiley Online Library, 2017, pp. 988–1012

- [BCH17] Mathias Beiglböck, Alexander MG Cox and Martin Huesmann “Optimal transport and Skorokhod embedding” In Inventiones mathematicae 208.2 Springer, 2017, pp. 327–400

- [Bei+17] Mathias Beiglböck et al. “Pathwise superreplication via Vovk’s outer measure” In Finance and Stochastics 21.4 Springer, 2017, pp. 1141–1166

- [BHP13] Mathias Beiglböck, Pierre Henry-Labordère and Friedrich Penkner “Model-independent bounds for option prices—a mass transport approach” In Finance and Stochastics 17.3 Springer, 2013, pp. 477–501

- [B+17] Mathias Beiglböck, Marcel Nutz and Nizar Touzi “Complete duality for martingale optimal transport on the line” In The Annals of Probability 45.5 Institute of Mathematical Statistics, 2017, pp. 3038–3074

- [BØ05] Francesca Biagini and Bernt Øksendal “A General Stochastic Calculus Approach to Insider Trading” In Applied Mathematics and Optimization 52.2, 2005, pp. 167–181 DOI: 10.1007/s00245-005-0825-2

- [Bia+17] Sara Biagini, Bruno Bouchard, Constantinos Kardaras and Marcel Nutz “Robust fundamental theorem for continuous processes” In Mathematical Finance 27.4 Wiley Online Library, 2017, pp. 963–987

- [BN15] Bruno Bouchard and Marcel Nutz “Arbitrage and duality in nondominated discrete-time models” In The Annals of Applied Probability 25.2 Institute of Mathematical Statistics, 2015, pp. 823–859

- [BL78] D. Breeden and R. Litzenberger “Prices of state-contingent claims implicit in option prices” In Journal of business 51 JSTOR, 1978, pp. 621–651

- [Cam05] L. Campi “Some results on quadratic hedging with insider trading” In Stochastics 77.4, 2005, pp. 327–348 DOI: 10.1080/17442500500183503

- [CL10] Peter Carr and Roger Lee “Hedging variance options on continuous semimartingales” In Finance and Stochastics 14.2, 2010, pp. 179–207 DOI: 10.1007/s00780-009-0110-3

- [CW13] A… Cox and J. Wang “Optimal robust bounds for variance options” arxiv:1308.4363 In ArXiv e-prints, 2013

- [CHO16] Alexander M.. Cox, Zhaoxu Hou and Jan Obłój “Robust pricing and hedging under trading restrictions and the emergence of local martingale models” In Finance Stoch. 20.3, 2016, pp. 669–704 DOI: 10.1007/s00780-016-0293-3

- [CW13a] Alexander M.. Cox and Jiajie Wang “Root’s barrier: Construction, optimality and applications to variance options” In The Annals of Applied Probability 23.3, 2013, pp. 859–894 DOI: 10.1214/12-AAP857

- [COT19] Alexander MG Cox, Jan Obłój and Nizar Touzi “The Root solution to the multi-marginal embedding problem: an optimal stopping and time-reversal approach” In Probability theory and related fields 173.1-2 Springer, 2019, pp. 211–259

- [DM78] C. Dellacherie and P.-A. Meyer “Probabilities and potential” 29, North-Holland Mathematics Studies Amsterdam: North-Holland Publishing Co., 1978, pp. viii+189

- [DS14] Yan Dolinsky and H Mete Soner “Martingale optimal transport and robust hedging in continuous time” In Probability Theory and Related Fields 160.1-2 Springer, 2014, pp. 391–427

- [DS15] Yan Dolinsky and H Mete Soner “Martingale optimal transport in the Skorokhod space” In Stochastic Processes and their Applications 125.10 Elsevier, 2015, pp. 3893–3931

- [FH16] Arash Fahim and Yu-Jui Huang “Model-independent superhedging under portfolio constraints” In Finance and Stochastics 20.1 Springer, 2016, pp. 51–81

- [GHT14] Alfred Galichon, Pierre Henry-Labordère and Nizar Touzi “A stochastic control approach to no-arbitrage bounds given marginals, with an application to Lookback options” In The Annals of Applied Probability 24.1 Institute of Mathematical Statistics, 2014, pp. 312–336

- [GOR15] Paul Gassiat, Harald Oberhauser and Gonçalo Reis “Root’s barrier, viscosity solutions of obstacle problems and reflected FBSDEs” In Stochastic Processes and their Applications 125.12, 2015, pp. 4601–4631 DOI: 10.1016/j.spa.2015.07.010

- [GP98] Axel Grorud and Monique Pontier “Insider Trading in a Continuous Time Market Model” In International Journal of Theoretical and Applied Finance 01.03, 1998, pp. 331–347 DOI: 10.1142/S0219024998000199

- [GTT16] Gaoyue Guo, Xiaolu Tan and Nizar Touzi “Optimal Skorokhod embedding under finitely many marginal constraints” In SIAM Journal on Control and Optimization 54.4 SIAM, 2016, pp. 2174–2201

- [Hob11] D. Hobson “The Skorokhod embedding problem and model-independent bounds for option prices” In Paris-Princeton Lectures on Mathematical Finance 2010 2003, Lecture Notes in Math. Springer, Berlin, 2011, pp. 267–318 DOI: 10.1007/978-3-642-14660-2˙4

- [Hob98] David G Hobson “Robust hedging of the lookback option” In Finance and Stochastics 2.4 Springer, 1998, pp. 329–347

- [HO18] Zhaoxu Hou and Jan Obłój “Robust pricing–hedging dualities in continuous time” In Finance and Stochastics 22.3 Springer, 2018, pp. 511–567

- [Kar95] Rajeeva L Karandikar “On pathwise stochastic integration” In Stochastic Processes and their applications 57.1 Elsevier Science, 1995, pp. 11–18

- [Lee10] Roger Lee “Realized Volatility Options” In Encyclopedia of Quantitative Finance John Wiley & Sons, Ltd, 2010 URL: http://onlinelibrary.wiley.com/doi/10.1002/9780470061602.eqf07040/abstract

- [Mei82] Isaac Meilijson “There exists no ultimate solution to Skorokhod’s problem” In Séminaire de Probabilités XVI 1980/81, Lecture Notes in Mathematics 920 Springer Berlin Heidelberg, 1982, pp. 392–399 DOI: 10.1007/BFb0092802

- [Mon72] Itrel Monroe “On Embedding Right Continuous Martingales in Brownian Motion” In The Annals of Mathematical Statistics 43.4, 1972, pp. 1293–1311 URL: http://www.jstor.org/stable/2239958

- [Nut14] Marcel Nutz “Superreplication under model uncertainty in discrete time” In Finance and Stochastics 18.4 Springer, 2014, pp. 791–803

- [Obł04] J. Obłój “The Skorokhod embedding problem and its offspring” In Probab. Surv. 1, 2004, pp. 321–390 DOI: 10.1214/154957804100000060

- [PK96] Igor Pikovsky and Ioannis Karatzas “Anticipative Portfolio Optimization” In Advances in Applied Probability 28.4, 1996, pp. 1095–1122 DOI: 10.2307/1428166

- [Roo69] David H Root “The existence of certain stopping times on Brownian motion” In The Annals of Mathematical Statistics 40.2 JSTOR, 1969, pp. 715–718

- [Spo14] Peter Spoida “Robust Pricing and Hedging with Beliefs about Realized Variance”, 2014

- [Str65] V. Strassen “The Existence of Probability Measures with Given Marginals” In The Annals of Mathematical Statistics 36.2, 1965, pp. 423–439 DOI: 10.2307/2238148

- [Vec86] D.. Vecht “Ultimateness and the Azéma-Yor stopping time” In Séminaire de probabilités de Strasbourg 20, 1986, pp. 375–378 URL: https://eudml.org/doc/113557

- [Vov12] Vladimir Vovk “Continuous-time trading and the emergence of probability” In Finance and Stochastics 16, 2012, pp. 561–609

- [Vov15] Vladimir Vovk “Itô Calculus without Probability in Idealized Financial Markets” In Lithuanian Mathematical Journal 55.2 Springer, 2015, pp. 270–290