1 Introduction

The concept of local risk-minimization is widely used for contingent situations in an incomplete market framework.

Local risk-minimization is closely related to an equivalent martingale measure which is well-known as

the minimal martingale measure (MMM).

For more details on

local risk-minimization, see [1] and [2].

Delta hedging, which is also a well-known hedging method and often has been used by practitioners,

is given by differentiating the option price

under a certain martingale measure with respect to the underlying asset price.

Due to the relationship between local risk-minimization and the MMM, we consider delta hedging under the MMM.

Its precise definition will be introduced in Section 2.

[2] showed explicit representations of local risk-minimizing (LRM) strategies for call options

by using Malliavin calculus for Lévy processes based

on the canonical Lévy space.

On the other hand, Carr and Madan introduced a numerical method for valuing options based on the

fast Fourier transform (FFT) in [3].

Carr and Madan’s method was used in [1] to compute LRM strategies of

call options for exponential Lévy models.

In particular, Merton models and variance gamma (VG) models were discussed

as typical examples of exponential Lévy models.

The main motivation of this paper is to investigate whether we can use delta hedging strategies as a substitute for LRM strategies,

since we can compute delta hedging strategies much easier than LRM strategies in general.

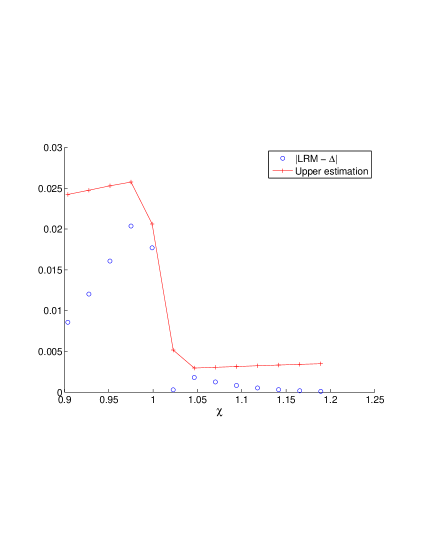

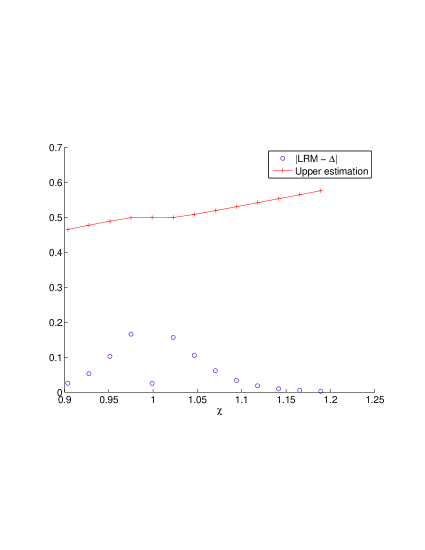

For this purpose, we analyze the difference between the two strategies both mathematically and numerically.

First, using [1], we shall obtain model-independent estimations among exponential Lévy models for the difference.

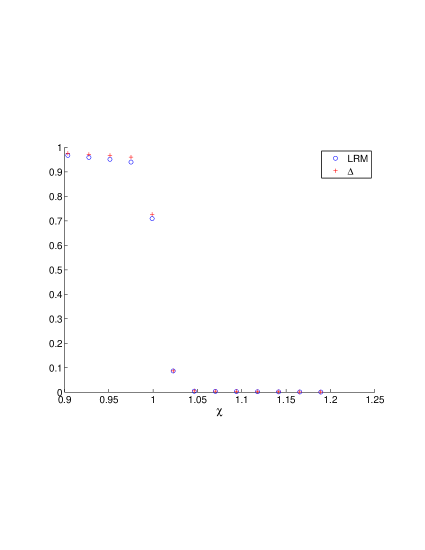

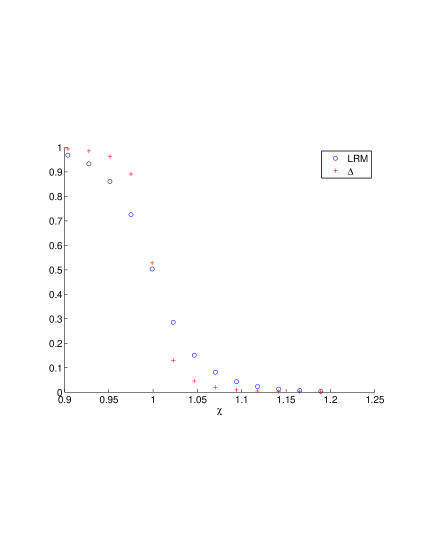

Second, in order to investigate how near the two strategies are around “at the money”,

we provide numerical experiments for two typical exponential Lévy models: Merton models and VG models.

Merton models are composed of a Brownian motion and compound Poisson jumps with normally distributed jump sizes.

VG models, which are exponential Lévy processes with infinitely many jumps in any finite time interval and no Brownian component, are

the second example.

The outline of this paper is as follows:

after giving notations and preliminaries in Section 2,

we show two model-independent estimations in Section 3.

Section 4 is devoted to numerical experiments.

Conclusions are given in Section 5.

Remark that [5] treated the same problem as ours, although all results obtained in [5] are model-dependent.

On the other hand, we obtain in this paper model-independent estimations.

In addition we shall compute numerically upper estimations of the difference between the two strategies around “at the money.”

2 Notations and preliminaries

We consider a financial market composed of one risk-free asset and

one risky asset with finite maturity .

For simplicity, we assume that market’s interest rate is zero,

that is, the price of the risk-free asset is 1 at all times.

The fluctuation of the risky asset is assumed to be given by

an exponential Lévy process on a complete probability space

, described by

|

|

|

for any , where , , ,

and .

Here is a one-dimensional standard Brownian motion

and is the compensated version of a Poisson random measure .

Denoting the Lévy measure of by ,

we have for any and

.

Now, is taken as the product of a one-dimensional

Wiener space and the canonical Lévy space for .

In addition, we take as the completed canonical

filtration for .

For more details on the canonical Lévy space, see [6] and [2].

Moreover, is also a solution of the stochastic differential

equation

|

|

|

where .

Now, defining for all ,

we have that is a Lévy process.

Our focus is to compare LRM strategies to delta hedging strategies

for call options with strike price .

Now, we give some preparations and assumptions.

Define the MMM as

an equivalent martingale measure under which any square-integrable

-martingale orthogonal to the martingale part of .

Its density is given by

|

|

|

where

and

for .

Remark that our discussion is strongly depending on the results in [1].

Thus, we need the assumptions imposed in [1] as follows:

Assumption 2.1

-

1.

, and

for .

-

2.

.

The first condition ensures

that (i) , , and

are well defined, (ii) is square integrable, and (iii)

for .

The second condition guarantees that for any .

Now we consider

|

|

|

(2.1) |

and

|

|

|

(2.2) |

Noting that (2.1) and (2.2) are functions of and , we denote them by and , respectively.

LRM strategies are given as a predictable process ,

which represents the number of units of the risky asset the investor holds

at time .

Here

its explicit representation for call options is given as follows:

Proposition 2.2 (Proposition 4.6 of [2])

For any and ,

|

|

|

(2.3) |

where .

In addition, we introduce integral representations given in [1] for and in order to see that Carr and Madan’s method is available.

The characteristic function of under is denoted by

for .

We induce an integral representation for

with firstly as follows:

|

|

|

|

|

|

|

|

|

|

|

|

where and

and .

Note that the right-hand side is independent of the choice of .

We turn next to .

Denoting , we have

|

|

|

|

|

|

|

|

Regarding , , and as functions of and ,

we have for , and

|

|

|

from (2.3).

As a result, is given as a function of ,

where is called moneyness.

Thus we denote by .

Next, we define delta hedging strategies.

Definition 2.3

For any and ,

a delta hedging strategy under for a call option with strike price is defined as

|

|

|

Remark that the above definition of delta hedging strategies

coincides with that of usual delta hedging strategies in the Black–Scholes model.

The next theorem follows from a direct calculation.

Theorem 2.4

We have

|

|

|

|

Note that is given as a function of also.

Thus we denote by .

Remark 2.5

[4] studied similar problems to this paper.

They compared some hedging errors among variance-optimal hedge, Black-Scholes hedge, and delta hedge.

3 Main results

We give two estimations of the difference as main results of this paper.

Remark that the estimations given in this section are independent of any exponential Lévy models.

Throughout this section we fix arbitrary.

We denote for short, and regard LRM and as functions of .

Let be the distribution of under , that is, for any .

First we give an estimation of , which is useful when is small.

Theorem 3.1

For any , we have the following inequality estimation:

|

|

|

(3.4) |

where

|

|

|

Hence we have as .

Proof.

We denote and by and for short.

First of all, we decompose into .

Here

|

|

|

where

|

|

|

|

|

|

Thus we have

|

|

|

|

|

|

|

|

(3.5) |

Noting that and

|

|

|

|

we obtain

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(3.6) |

In the same manner, we have

|

|

|

|

|

|

|

|

(3.7) |

|

|

|

|

(3.8) |

From (3.5), (3.6), and (3.8), we can conclude

|

|

|

|

(3.9) |

|

|

|

|

|

|

|

|

This completes the proof of Theorem 3.1.

Next we give the second estimation of for large .

Theorem 3.2

Suppose

|

|

|

(3.10) |

Then there exists a constant such that

|

|

|

(3.11) |

for any .

So that, as .

Proof.

We show (3.11) by using (3.9).

To this end we estimate and separately.

In order to estimate ,

we define a function as

|

|

|

for , which implies that

|

|

|

|

|

|

|

|

|

|

|

|

(3.12) |

where and the value of (3.12) is independent of the choice of .

Remark that the second equation of (3.12) is from (2.17) in [1].

We may choose without loss of generality.

Hence we have

|

|

|

|

|

|

|

|

|

|

|

|

Denoting for , we can see that for any .

From (3.10), we have

|

|

|

|

(3.13) |

Next we check the part.

(3.7) implies

|

|

|

|

|

|

|

|

In the same manner as the above estimation for , we estimate by using (3.12).

Replacing

with and substituting 2 for ,

we have

|

|

|

|

Hence we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(3.14) |

Noting that (3.10), and from Assumption 2.1,

we obtain

From (3.9), (3.13), and (3.14) we obtain

|

|

|

|

|

|

|

|

Remark 3.3

The condition (3.10) is not necessarily satisfied for the case of , although it holds whenever .

Thus, the proof of Proposition 2.1 in [1] includes an error.

On the other hand, [1] treated only Merton and VG models, and we can see (3.10) for both models,

because for Merton models, and Proposition 4.7 in [1] for VG models.