ampmtime

Estimation of heterogeneous individual treatment effects with endogenous treatments

Abstract.

This paper estimates individual treatment effects in a triangular model with binary–valued endogenous treatments. Following the identification strategy established in Vuong and Xu (forthcoming), we propose a two–stage estimation approach. First, we estimate the counterfactual outcome and hence the individual treatment effect (ITE) for every observational unit in the sample. Second, we estimate the density of individual treatment effects in the population. Our estimation method does not suffer from the ill–posed inverse problem associated with inverting a non–linear functional. Asymptotic properties of the proposed method are established. We study its finite sample properties in Monte Carlo experiments. We also illustrate our approach with an empirical application assessing the effects of 401(k) retirement programs on personal savings. Our results show that there exists a small but statistically significant proportion of individuals who experience negative effects, although the majority of ITEs is positive.

Keywords: Nonseparable triangular models, binary endogenous variable, counterfactual mapping, individual treatment effects, 401(k) retirement programs

1. Introduction

Nonseparable triangular models have been studied extensively in the recent econometric literature, thereby allowing researchers to understand the nature of instrumental variables in the presence of endogeneity. See e.g. Chesher (2003, 2005) and Imbens and Newey (2009). One appealing feature of nonseparable models is that the non-additive error in the causal relationship implies that the ceteris paribus effects of covariates on the outcome variable “vary across individuals that, measured by covariates, are identical,” Chesher (2003). Such heterogeneous causal effects are referred as “individual treatment effects”(ITE) in the literature. See e.g. Rubin (1974), Heckman, Smith, and Clements (1997) and Heckman and Vytlacil (2005).

Estimating ITE and its distribution is crucial for evaluating a social program, especially in view of the political issues associated with it (see Heckman, Smith, and Clements, 1997). From an individual’s perspective, however, her ITE is more helpful for evaluating her treatment participation decision than an average effect. While the “average person” may benefit from a particular treatment, some individuals may experience little benefit or even some loss from participating, in which case alternative treatment options may be preferred. Indeed, while the individual treatment effects of 401(k) retirement programs on personal savings are mostly positive in our sample, our empirical analysis indicates that there are individuals who experience negative benefits from participating to 401(k) retirement programs.

In this paper, we consider a triangular model with a binary endogenous regressor. Because of the self–selection issue, individuals who are treated are different from those who choose not to be treated. We address this issue with a binary valued instrumental variable (see e.g. Imbens and Angrist, 1994). Limited variations of instrumental variables have been emphasized in the recent treatment effect literature. Moreover, natural experiments (e.g. Angrist and Evans, 1998; Post, Van den Assem, Baltussen, and Thaler, 2008) and eligibility for treatment participation (e.g. Angrist, 1990; Abadie, 2003) provide commonly used binary–valued instrumental variables.

The distribution of heterogeneous treatment effects has also been studied using quantiles. For instance, Abadie, Angrist, and Imbens (2002) and Froelich and Melly (2013) estimate the quantile treatment effects (QTE) for the complier group, a subpopulation defined by Imbens and Angrist (1994) under binary–valued instruments. For the population QTE, Chernozhukov and Hansen (2004) propose a GMM–type approach in a linear quantile specification. Subsequently, Chernozhukov and Hansen (2006, 2008) generalize Chernozhukov and Hansen (2004)’s estimation procedure by using quantile regression methods. In a fully nonparametric setting, Horowitz and Lee (2007) and Gagliardini and Scaillet (2012) modify Chernozhukov and Hansen (2004)’s moment conditions using the Tikhonov regularization to deal with the ill–posed inverse problem for deriving asymptotic properties of their estimators.

Our approach is novel and simple to implement. Instead of solving the moment conditions in Chernozhukov and Hansen (2005), we use the quantile invariance condition to match the realized outcome with its counterfactual outcome for every observational unit in the sample through a so-called counterfactual mapping. Specifically, our approach recovers the ITE for every individual in the sample and does not suffer from the ill–posed inverse problem associated with inverting a non–linear functional. In particular, we show that the ITEs are estimated uniformly at the parametric rate. Given the recovered ITEs, we estimate the density by kernel methods and establish its asymptotic properties. Though it might be possible to obtain a density estimate from QTE estimates, this would involve a more complicated two–stage procedure and a delicate trimming scheme (see e.g. Marmer and Shneyerov, 2012).

We apply our approach to study the effects of 401(k) retirement programs on personal savings. Introduced in the early 1980s, the 401(k) retirement programs aim to increase savings for retirement. Endogeneity arises as individuals with a higher preference for savings are more likely to participate and also have higher savings than those with lower preferences (see, e.g., Poterba, Venti, and Wise, 1996). Following e.g. Abadie (2003) and Chernozhukov and Hansen (2004), we use 401(k) eligibility as an instrumental variable for 401(k) participation. We estimate the ITEs for every individual in the sample as well as its density. Our results show that there exists a small but statistically significant proportion (about 8.77%) of individuals who experience negative effects, although the majority of ITEs is positive. It has been argued in the literature (see e.g. Engen, Gale, and Scholz, 1996) that some individuals could suffer from the program due to the Crowding Out Effect. We offer a complementary explanation as individuals with negative ITEs are more likely to be younger, single, from smaller and lower income families but with higher family net financial assets than the rest of the sample.

The structure of the paper is organized as follows. In Section 2, we introduce the triangular model and discuss its identification and estimation. Section 3 provides Monte Carlo experiments to illustrate the performance of our proposed estimator. Section 4 derives its asymptotic properties. Section 5 applies our estimation method to assess the effects of 401(k) retirement programs on personal savings. Proofs of our results are collected in the Appendix.

2. Model, Identification and Estimation

2.1. The triangular model

Following Chesher (2005), we consider a nonseparable triangular model with an outcome equation and a selection equation:

| (1) | ||||

| (2) |

Here is the outcome variable, is an endogenous dummy that indicates the treatment status, is a vector of observed covariates (not necessary exogenous) and is a binary instrumental variable for , i.e., . The two latent random variables and are scalar valued disturbances. Moreover, the function and are unknown structural relationships. In particular, is continuous and strictly increasing in .

The key feature in the above triangular model is the nonseparability of in the error term . With a nonseparable , the ceteris paribus effects on the outcome variable from covariates “vary across individuals that, measured by covariates, are identical,” Chesher (2003). In the treatment effect literature, such heterogeneous causal effects are referred as “individual treatment effects”(ITE), i.e.,

See e.g. Rubin (1974) and Heckman, Smith, and Clements (1997). After controlling for , the ITE is still a random object since it depends on the latent variable . Our interest is to recover the ITE for each individual from her observables , and to estimate the probability density function of ITE in the population. In particular, a decision-maker can use the former to evaluate an individual’s participation choice, while the latter characterizes the distribution of treatment effects, which has been central in the program evaluation literature (see e.g. Heckman, Smith, and Clements, 1997).

We now provide two examples to illustrate the nonseparability of the structural relationship .

Example 2.1 (Additive error with generalized heteroscedasticity): Let

where is a real-valued function, is a positive function that captures the heteroscedasticity in the disturbance, and has zero mean and unit variance, unconditionally. This model is a generalization of a nonparametric regression model with heteroskedastic errors studied by e.g. Andrews (1991). The difference is that the heteroscedasticity term depends on the endogenous binary variable . In particular, when is a constant, the above specification becomes an additive nonparametric regression with some endogenous regressor as studied by e.g. Newey and Powell (2003) and Darolles, Fan, Florens, and Renault (2011).

Example 2.2 (Semiparametric transformation model): Consider

where and is an unknown monotone function. See Horowitz (1996) when is exogenous. A parametric example of the monotone function is the Box–Cox transformation when is positive:

where is a model parameter. Such a transformation is useful when the dependent variable has a limited support. Indeed, the transformed dependent variable can have an unlimited support thereby ensuring a linear model specification with its usual assumptions. Various extensions of the Box–Cox transformation have been developed in the literature (see e.g. Sakia, 1992), where monotonicity is a common feature in all these transformations. Recently, Chiappori, Komunjer, and Kristensen (2015) have studied the case where some variables such as is endogenous.

2.2. Identification

Vuong and Xu (forthcoming) establish identification of the triangular model (1)-(2) in a constructive way and show that it only requires binary variations of the instrumental variable . Given the monotonicity of , the ITE can be written as a function of the observables :

| (3) |

where for are defined as the counterfactual mappings that depend on covariates and the value of , namely,111The function denotes the inverse of . Hereafter, for a generic random variable with distribution , we denote its support by , defined as the closure of the open set .

By definition, are monotone functions mapping onto , where , and we have .

To obtain the ITE for an individual with , it suffices to identify the counterfactual mapping , where . Let be the propensity score function. For expositional simplicity, suppose and for all . W.l.o.g., throughout we assume . Moreover, for any and , let

| (4) |

Imbens and Rubin (1997) show that is the conditional distribution function of given the complier group, namely, . Let be the support of . It is straightforward to see that . Next, we present the identification of established in Vuong and Xu (forthcoming).

Theorem 1.

(Vuong and Xu, forthcoming) In the triangular model (1)-(2), suppose (i) is continuous and strictly increasing in ; (ii) is conditionally independent of given , i.e., with for all ; (iii) conditional on , the joint c.d.f. is continuous; (iv) for and . Then, , and the counterfactual mapping is identified by

where is continuous on and strictly increasing on for , and .

In Theorem 1, condition (i) – (iii) are standard in the triangular model literature. The support condition (iv) requires that, conditional on , the subpopulation , i.e., the complier group introduced in Imbens and Angrist (1994), contains the same information on individual treatment effects as the whole population. It is weak as it is satisfied as soon as has a rectangular support given . See Vuong and Xu (forthcoming). It is testable since is identified by (4). When (iv) fails to hold, the counterfactual mappings are partially identified on intervals. It is worth pointing our that (iv) is needed for identification of ITE even if one assumes the error term was observed in the data.

2.3. Estimation

We now develop nonparametric estimators of the counterfactual mappings for and the probability density function of ITE. On one hand, can be used to construct the ITE for any individual in the population from her observables . On the other hand, the probability density function is a convenient way to characterize the distribution of the ITE when the ITE is continuously distributed.222Under Condition (i)–(iii), the ITE can have a mass point when has slope one in some intervals contained in its support, i.e., on some . Then, conditional on , ITEs take the same value for all . Hence, ITE has a mass point at . Such a case, however, can be detected given the identification of . Our estimation approach is fully nonparametric. To present the basic ideas, we assume that the covariates are discrete random variables with a finite support. Our analysis can be extended using e.g. the kernel method to the case where are continuous at the cost of exposition.

Let be an i.i.d. sample generated from the underlying structure of the triangular model. Our proposed estimation procedure takes two steps: First, for a given value of , we estimate the counterfactual mapping by a simple estimator that minimizes a convex population objective function. In the second step, we construct a pseudo sample of the counterfactual outcomes for all individuals in the sample and then nonparametrically estimate the density function using the kernel method. We introduce some notation. Fix . For simplicity, we suppress the dependence on in the following discussion. For each and , let

where .

For , let

be the population objective function. Such an objective function is motivated by the quantile regression method in Koenker and Bassett (1978). To see this, note that the quantile invariant condition in Chernozhukov and Hansen (2005) implies that for satisfying (equivalently, ), we have

| (5) |

In the next lemma, we show that (5) is indeed the first–order condition of the population objective function , which is continuously differentiable and weakly convex on . We also show that is strictly convex on and minimized uniquely on at whenever . A similar argument also holds for the population objective function .

Lemma 1.

Suppose the conditions in Theorem 1 hold. Then, for and , the function is continuously differentiable and weakly convex in where . Moreover, if , then is strictly convex in , and uniquely minimized on at .

Lemma 1 provides a basis for our nonparametric estimation of the counterfactual mappings and . It is worth pointing out that each minimization is a one–dimensional optimization problem.

We are now ready to define our estimator. For expositional simplicity, let be a compact interval . For , and , let and

Moreover, let

where . For simplicity, we assume the support is known. See e.g. Guerre, Perrigne, and Vuong (2000) for nonparametric estimation of the support if it is unknown.

Given the sample , we can construct the counterfactual outcome for every individual in the sample from her observables . Namely,

Thus, we can estimate the ITE by (3), i.e., for ,

| (6) |

In particular, we can construct a pseudo sample from the observed sample .

It is worth pointing out that the first–stage estimation is computationally simple and does not suffer from an ill–posed inverse problem (see e.g. Horowitz and Lee, 2007). In particular, to solve the one–dimensional optimization problem for each individual’s counterfactual outcome, the practitioner can use a grid search algorithm that is simple but highly robust. As is shown below, the first–stage estimation bias uniformly converges to zero at the parametric rate of , given that all the covariates are discrete variables.333If contains continuous random variables, then we need to smooth over as otherwise there may not be enough observations for which .

Next, we follow Guerre, Perrigne, and Vuong (2000) to estimate the density function by the kernel method. To clarify ideas, let be a subinterval of the ITE’s support. Then, we define the density estimator:

where is a bandwidth and is a kernel with a compact support. Because the kernel estimator suffers from boundary issues, then we restrict the estimation of to the inner subset .

3. Monte Carlo Experiments

To illustrate the finite sample performance of the proposed estimator, we conduct a Monte Carlo study. For simplicity, we do not include other covariates in the specification. Following the conditions in Theorem 1, the data generating process is given by

where for ,444We also consider other functional forms for , e.g., and . The results are qualitatively similar. and conforms to a joint distribution with uniform marginal distributions on and Gaussian copula with correlation coefficient .555A copula is a multivariate probability distribution of random variables, each of which is marginally uniformly distributed on . The Gaussian copula is constructed from a multivariate normal distribution. See e.g. Nelsen (2007). Because is continuous and strictly increasing in , Condition (i) in Theorem 1 is satisfied. We set and and , respectively. The value of determines the size of the compliers group, i.e., . Hence, the larger , the more “effective” the instrumental variable . In our setting, is distributed on with mean and median 1.125 in the population. Moreover, we set where is independent of . Conditions (ii)–(iv) in Theorem 1 are satisfied. In particular, condition (iv) holds since has a rectangular support as noted in Vuong and Xu (forthcoming).

Table 1 reports the finite sample performance of our ITE estimates in terms of the Root Mean Squared Error (RMSE). Specifically, for each size we draw to obtain a sample of size . We then compute the true ITE by and its estimate by (6) for each individual . To obtain the RMSE for each such individual’s ITE, we draw another 200 samples from for . These are used to repeatedly estimate the ITEs for the individuals in the original sample by where is the estimate of using the –th new drawn sample. Thus, we obtain the RMSE of by . For comparison, we also provide the RMSE of the LATE over the 200 replications/samples within curly brackets as proposed by Imbens and Angrist (1994).666For our Monte Carlo setting, the LATE reduces to for , respectively. Moreover, the LATE is estimated by for a given sample, where and are the sample means of and given , respectively, for . In particular, unlike ITE and its estimate, LATE and its estimate do not vary across individuals by definition. By comparing their RMSEs from Table 1, a surprising result is that estimating treatment effects at individual level (i.e. ITE) is not more difficult than to estimate treatment effects at aggregated level (e.g. LATE) for every sample size. As sample size increases, both the bias and standard error decrease at the expected –rate. The estimation error (i.e. its size and standard deviation) depends on the sample size and the compliers group’s proportion . Specifically in the different designs, the finite sample performance of the ITE estimator depends on the value of . For example, the performance of our estimator under is similar to that under . This observation is consistent with our asymptotic properties established in the next section.

| Sample size | ||||

|---|---|---|---|---|

| Ave. RMSE | 1.2918 | 0.6076 | 0.4071 | |

| 1,000 | Std. RMSE | (0.5279) | (0.2912) | (0.2231) |

| LATE RMSE | {1.0448} | {0.5159} | {0.3619} | |

| Ave. RMSE | 0.9343 | 0.4381 | 0.2670 | |

| 2,000 | Std. RMSE | (0.4289) | (0.2122) | (0.1511) |

| LATE RMSE | {0.6639} | {0.3759} | {0.2532} | |

| Ave. RMSE | 0.6059 | 0.3245 | 0.18313 | |

| 4,000 | Std. RMSE | (0.2839) | (0.1455) | (0.0985) |

| LATE RMSE | {0.5057} | {0.2220} | {0.1790} |

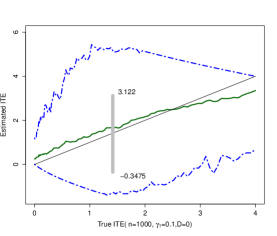

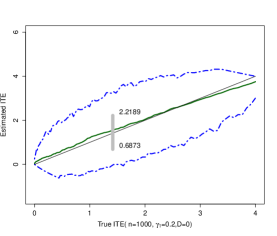

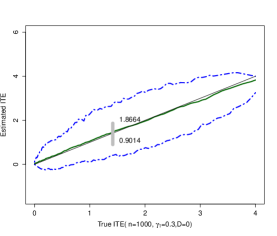

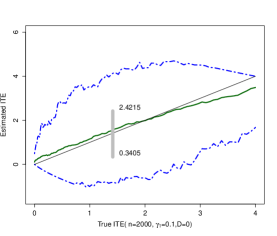

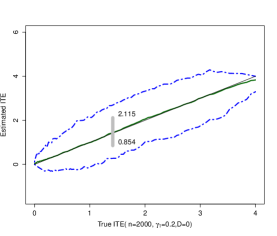

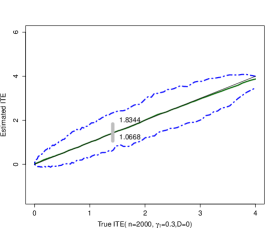

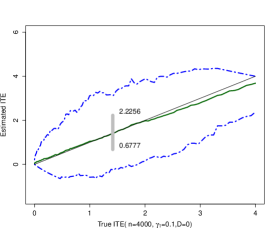

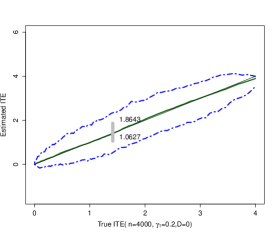

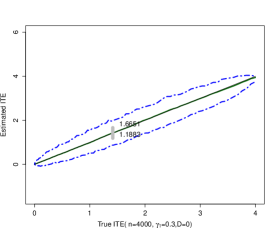

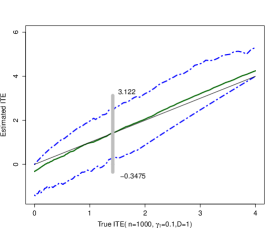

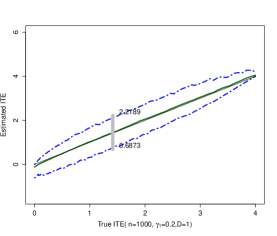

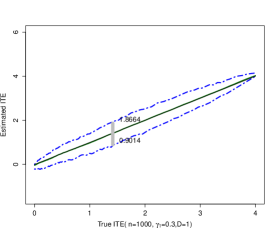

Figures 1 and 2 illustrate the performance of the ITE estimates for the individuals with and , respectively. In particular, we plot the ITE estimates versus the true ITE. The green solid line is the mean and the dotted lines give the confidence interval computed from the 200 repetitions. The grey solid line is the 45–degree diagonal. The ITE estimates for the group behave better than the estimates for . This observation is also consistent with our asymptotic results in the next section: The performance of of an individual with depends on the density function of , evaluated at her quantile in the distribution, conditional on the compliers group (and as well). In our setting, the conditional density of given the compliers group is larger uniformly at all quantiles than that of , which leads to a more accurate estimator for the group . For comparison, we also plot the true value of LATE with the 90% confidence interval of its estimate in grey color columns. Overall, estimates of ITE and LATE behave similarly. Note that for any individual in the group , our estimator of the ITE behaves better than LATE.

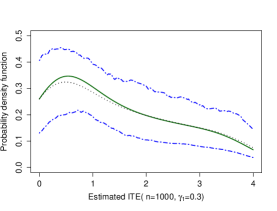

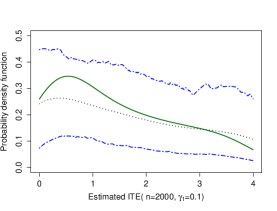

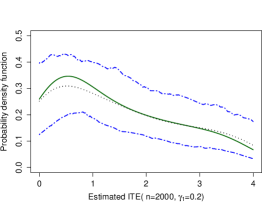

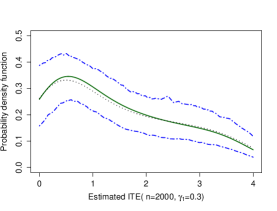

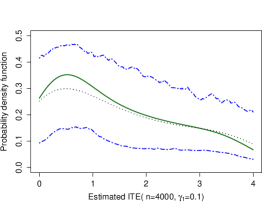

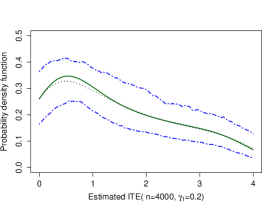

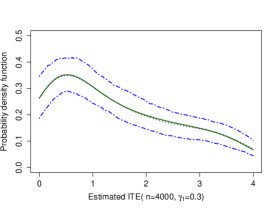

For the density estimator, we choose the bandwidth and the pdf of the standard normal as the kernel function. Figure 3 shows the performance of our density estimator . The black dotted line is the true density of the ITE and the green one is the average of our density estimates over the 200 repetitions. We also provide the and percentiles of estimated densities using blue dotted lines, which gives the (pointwise) 90% confidence band. Figure 3 shows again the importance of the size of the complier group through .

4. Asymptotic Properties

We now establish the asymptotic properties of our proposed nonparametric estimators. We first show the uniform –consistency of the counterfactual mapping estimator , and we give its limiting distribution. We then establish the asymptotic properties of our density estimator taking into account the first-step estimation of .

For estimation, we strengthen Conditions (i) and (iii) in Theorem 1, respectively, to

Condition (i)’: is continuously differentiable and strictly increasing in .

Condition (iii)’: The conditional distribution of given is absolutely continuous with respect to Lebesgue measure. Moreover, the conditional density function is continuous for all .

Under Conditions (i)’, (ii) and (iii)’, the conditional distribution is absolutely continuous with respect to Lebesgue measure and its density is also continuous. Therefore, the complier distribution defined by (4) is also absolutely continuous with respect to Lebesgue measure for . Let be its density.

To simplify the exposition, we introduce the following assumption.

Assumption 1: For every , (i) , where and are finite, and (ii) . Moreover, (iii) is a vector of discrete random variables with a finite support.

When has an unbounded support, we can always apply a known strictly increasing bounded continuous transformation to to satisfy Assumption 1-(i). Assumption 1-(ii) requires that the density be bounded away from zero on its support. It can be relaxed at the cost of technical complications due to e.g. some trimming. As indicated earlier, Assumption 1-(iii) can be relaxed to allowed for continuous variables in by introducing some smoothing methods such as kernel ones.

The next theorem establishes the uniform consistency of the counterfactual mapping estimator on its full support. It also gives its –asymptotic distribution. For and , let be the scale–adjusted complier density and be the probability rank of in the distribution of given . Under the monotonicity of and the definition of , we have

where .

Theorem 2.

Suppose the conditions in Theorem 1, Conditions (i)’, (iii)’ and Assumption 1 hold. Then, for and , we have

Moreover, the empirical process converges in distribution to a zero–mean Gaussian process with covariance kernel

The uniform convergence of includes the boundaries, which is due to Assumption 1-(ii). Moreover, letting in gives the asymptotic variance of as follows:

As approaches its boundaries, the asymptotic variance decreases to zero. Therefore, we obtain a more accurate estimate of the counterfactual outcome when it is closer to the boundary points. We also note that the asymptotic variance of is inversely proportional to , but is independent of the magnitude of ITE.

Theorem 2 is important for several reasons. First, given an arbitrary triplet , we can provide a –consistent estimate of the counterfactual outcome whenever and . Its standard error is given by

where and are sample frequencies, and

| (7) |

in which is a kernel density estimator and are sample frequencies. Equation (7) follows from differentiating (4). Second, given the uniform –consistency of , it follows that also uniformly converges to at the –rate.

Next, we turn to the asymptotic properties of our density estimator .

Assumption 2: (i) On some interval of , the density function admits up to –th continuous bounded derivatives with . Moreover, . (ii) The kernel is a symmetric -th order kernel with support and twice continuously bounded derivatives.777A -th order kernel is a function integrating to one and satisfying if and if . (iii) The bandwidth .

The first part of Assumption 2-(i) is a high level condition requiring that the random variable has a smooth density function conditional on . It is satisfied if for and the density of given are–th continuously differentiable. The second part of Assumption 2-(i) is standard for kernel estimation. Assumptions (ii) and (iii) relate to the choice of the kernel function and bandwidth , respectively. In particular, following Guerre, Perrigne, and Vuong (2000), the bandwidth in (iii) leads to oversmoothing relative to the optimal bandwidth, i.e., (see Stone, 1982).

Given Assumption 2 and the uniform convergence of to at the –rate, we show in the Appendix that the first–step estimation error is asymptotically negligible in . Thus, we obtain the following result.

Theorem 3.

Suppose the conditions in Theorem 2 and Assumption 2 hold. Then,

5. Individual Effects of 401(k) Programs

In this section we apply our estimation method to study the effects of 401(k) retirement programs on personal savings. The 401(k) retirement programs were introduced in the early 1980s to increase savings for retirement. Since then, they became increasingly popular in the US. It has been argued in the literature that participants might self–select into the programs non-randomly (see, e.g., Poterba, Venti, and Wise, 1996). People with a higher preference for savings are more likely to participate and have higher savings than those with lower preferences.

Following e.g. Abadie (2003) and Chernozhukov and Hansen (2004), we use 401(k) eligibility as an instrumental variable for 401(k) participation. This is because 401 (k) plans are provided by employers. Hence, only workers in firms that offer such programs are eligible so that the monotonicity in (2) is satisfied.888Imbens and Angrist (1994) define monotonicity as: for all , where is the potential treatment status at . In our application, is 401(k) eligibility and . Therefore, a.s., i.e., Imbens and Angrist (1994)’s monotonicity condition holds. Moreover, Vytlacil (2002) show that such a condition is observationally equivalent to the functional monotonicity in (2).

5.1. Data

The dataset consists of 9,275 observations from the Survey of Income and Program Participation (SIPP) of 1991 as in Abadie (2003). The observational units are household reference persons aged 25-64 and spouse if present. The included households are those with at least one member employed, with Family Income in the k – k interval. Eligibility for 401(k) outside the interval is rare as noted by Poterba, Venti, and Wise (1996).

| Entire sample | By 401(k) participation | By 401(k) eligibility | |||

| Participants | Non-participants | Eligibles | Non-eligibles | ||

| Treatment | |||||

| 401(k) Participation | 0.0000 | ||||

| (0.4472) | (0.4564) | (0.0000) | |||

| Instrument | |||||

| 401(k) Eligibility | 0.3921 | 1.0000 | 0.1601 | ||

| (0.4883) | (0.0000) | (0.3668) | |||

| Outcome variable | |||||

| FNFA | 19.0717 | 38.4730 | 11.6672 | 30.5351 | 11.6768 |

| (in thousand $) | (63.9638) | (79.2711) | (55.2892) | (75.0190) | (54.4202) |

| Covariates: | |||||

| Family income | 39.2546 | 49.8151 | 35.2243 | 47.2978 | 34.0661 |

| (in thousand $) | (24.0900) | (26.814.2) | (21.6492) | (25.6200) | (21.5106) |

| Age | 41.0802 | 41.5133 | 40.9149 | 41.4845 | 40.8194 |

| (10.2995) | (9.6517) | (10.5323) | (9.6052) | (10.7163) | |

| Married | 0.6286 | 0.6956 | 0.6030 | 0.6772 | 0.5972 |

| (0.4832) | (0.4603) | (0.4893) | (0.4676) | (0.4905) | |

| Family size | 2.8851 | 2.9204 | 2.8716 | 2.9079 | 2.8703 |

| (1.5258) | (1.4681) | (1.5472) | (1.4770) | (1.5565) | |

Table 2 presents the summary statistics of the full sample as well as by eligibility and participation status. The dependent variable is the Family Net Financial Assets (FNFA), the treatment variable is the participation in 401(k), and the instrumental variable is the eligibility for 401(k). About in the sample participate in the program and are eligible for it. Other covariates include family income, age, marital status and family size. Similar to Chernozhukov and Hansen (2004), age and income are grouped into categorical variables 0, 1, 2 and 3 by using the 1st, 2nd and 3rd quartiles.

| Family income | Age | Married | Family size | ||||

|---|---|---|---|---|---|---|---|

| By percentile | <0.25 | 2.29 | 4.29 | By value | 0 | 12.83 | |

| (18.83) | (21.08) | (50.55) | |||||

| 0.25–0.5 | 7.68 | 14.49 | 1 | 22.76 | 13.59 | ||

| (29.16) | (62.78) | (70.45) | (47.59) | ||||

| 0.5–0.75 | 16.63 | 21.43 | 2 | 29.11 | |||

| (53.15) | (67.33) | (82.70) | |||||

| >0.75 | 49.76 | 36.86 | 3 | 19.17 | |||

| (104.87) | (87.31) | (66.86) | |||||

| 4 | 17.53 | ||||||

| (56.83) | |||||||

| >4 | 12.51 | ||||||

| (52.46) |

Table 3 provides the mean and standard error (in parentheses) of the outcome variable FNFA by percentiles sorted according to covariates. Clearly, FNFA is monotone increasing in family income and age. According to family size, FNFA is maximized at family size 2 and decreases with family size when it is larger than 2. Moreover, married households have higher FNFA than unmarried ones on average.

In Table 5, we provide OLS and 2SLS estimates as a benchmark for comparison with our ITE estimates. Our results replicate the estimates in Abadie (2003). The OLS estimates in column (1) show a significantly positive association between participation in 401(k) and net financial assets given covariates. Furthermore, the 2SLS estimates in column (3) confirms the positive, but attenuated treatment effects after controlling for endogeneity of participation. It turns out that FNFA increases rapidly with family income and age, and is lower for married couples and larger families.

| OLS | 2SLS | |||

|---|---|---|---|---|

| First stage | Second stage | |||

| Participation in 401(k) | 13.5271 | 9.4188 | ||

| (1.8103) | (2.1521) | |||

| Constant | 10.0421 | 0.0567 | 9.0076 | |

| (10.9142) | (0.0464) | (10.9559) | ||

| Family income (in thousand $) | 0.9769 | 0.0013 | 0.9972 | |

| (0.0833) | (0.0001) | (0.0838) | ||

| Age | -2.3100 | -0.0048 | -2.2386 | |

| (0.6177) | (0.0023) | (0.6201) | ||

| Age squared | 0.0387 | 0.0001 | 0.0379 | |

| (0.0077) | (0.0000) | (0.0077) | ||

| Married | -8.3695 | -0.0005 | -8.3559 | |

| (1.8299) | (0.0079) | (1.8290) | ||

| Family size | -0.7856 | 0.0006 | -0.8190 | |

| (0.4108) | (0.0024) | (0.4104) | ||

| Eligibility for 401(k) | 0.6883 | |||

| (0.0080) | ||||

Note: The dependent variable is family net financial assets (in thousand $). Family income and age enter into the regression as continuous variables. The sample includes 9,275 observations from the SIPP of 1991. The observational units are household reference persons aged -, and spouse if present, with Family Income in the $k-k interval. Heteroscedasticity robust standard errors are given in parentheses.

5.2. ITE Estimates

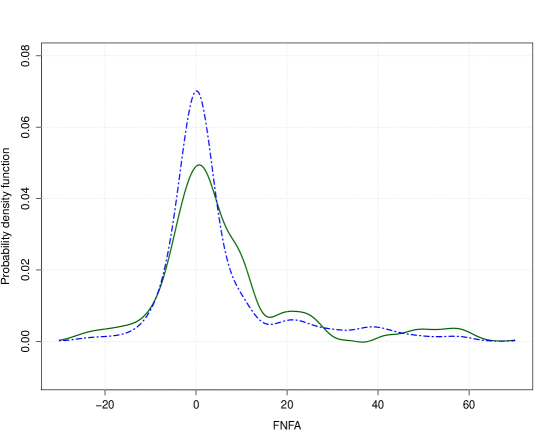

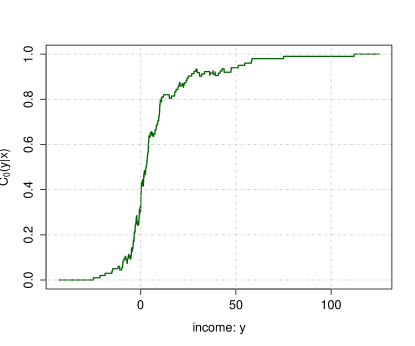

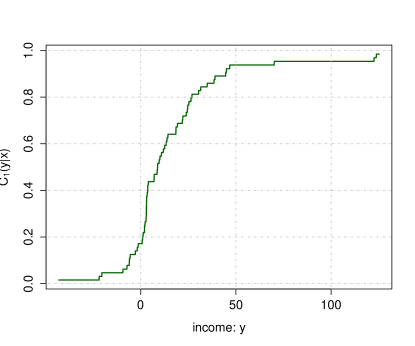

To begin with, we first check the support condition for identification, i.e. Condition (iv) in Theorem 1. Because those who are not eligible for 401(k) (i.e. ) cannot participate in the program, then by (4) and . It follows that for all . Hence, to check Condition (iv), it suffices to verify the support condition for . To do so, we estimate the density function by (7) and the density function directly from the data.

Fix the subgroup of individuals whose income is between the 25% and 50% percentile, age between 40 and 48 years old, and family size smaller than 3.999We repeat this for other values of covariates. The results are qualitatively similar. Figure 4 plots the density estimate using the green solid line, and the density estimate using the blue dotted line. From Figure 4, the two distributions roughly share the same support.

Moreover, as shown in Vuong and Xu (forthcoming), the main restrictions imposed by our model require that defined by (4) should be monotone increasing for and all . We plot estimates of and in Figure 5 for the subgroup of Figure 4. Both of them are increasing functions globally.

Table 6 reports summary statistics of the ITE estimates in our sample. From Table 6, the ITE has a mean of $k and median of $k, indicating a long right tail of the ITE distribution. The mean of ITE is larger than the average treatment effects (ATE) of OLS and 2SLS, which are $13.53k and $9.42k, respectively, while the median of ITE turns out to be smaller than these two ATEs. The differences reflect the distortion due to the linear specification used in OLS and 2SLS, as well as the selection bias.

| Min | Max | Mean | Std. | . | ||

|---|---|---|---|---|---|---|

| -918 | 1,533 | 22.45 | 102.77 | 3.10 | 8.83 | 20.90 |

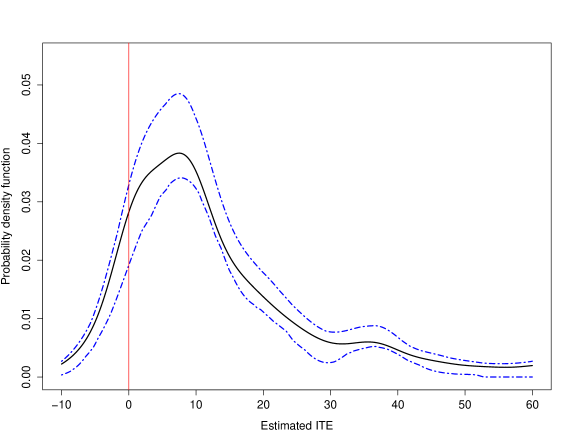

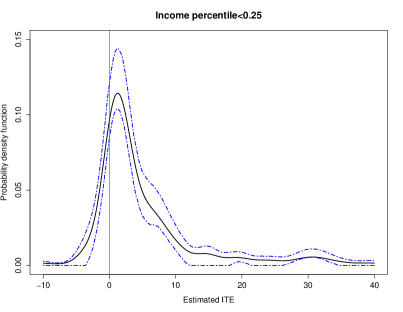

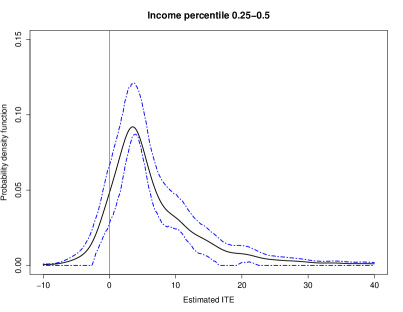

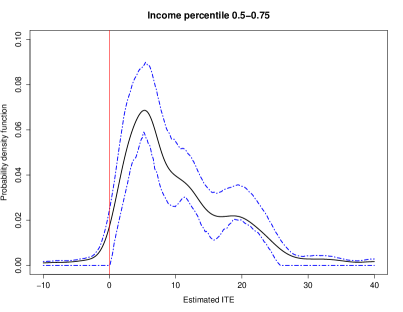

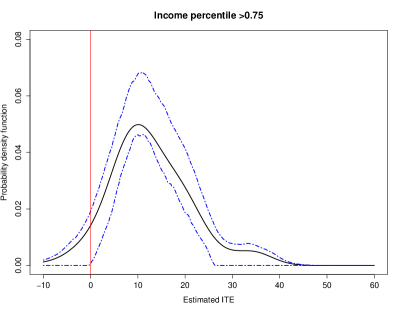

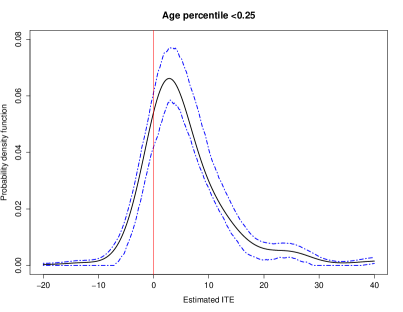

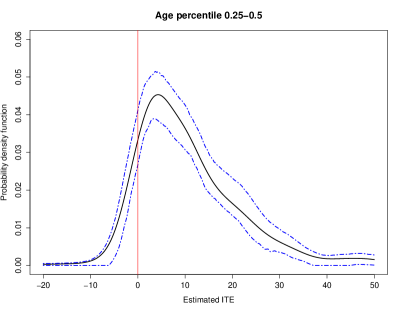

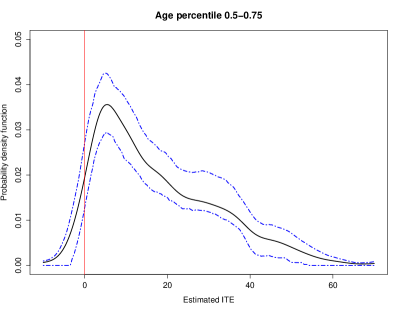

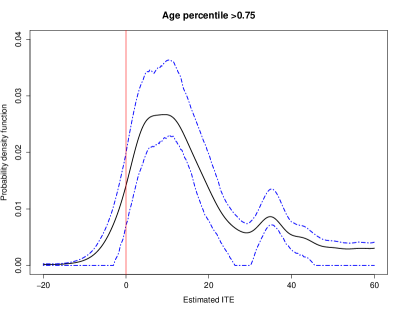

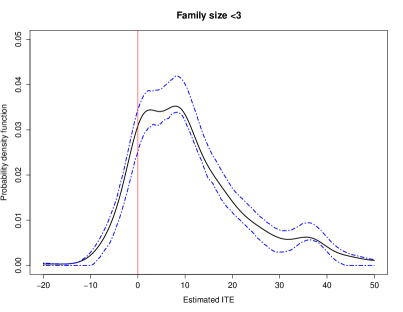

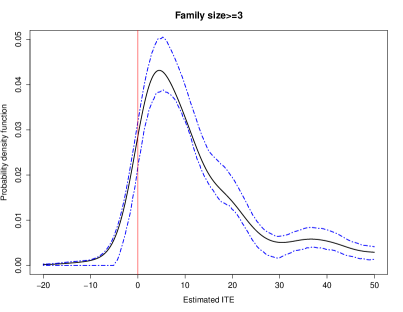

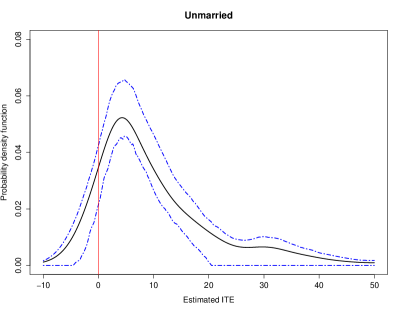

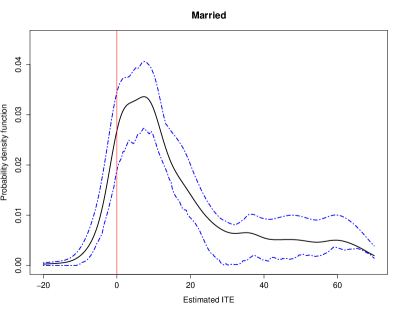

Figure 6 provides the ITE density estimates for the full sample along with pointwise bootstrap confidence intervals. The participation effects of 401(k) on net financial assets are distributed on the interval [-$10k, $60k], with a mode around $4k. As the bootstrap confidence intervals indicate, the ITE density is quite well-estimated. Figures 7, 8, 9 and 10 plot the ITE density estimates conditional on income, age, family size and family status, separately. In particular, the ITE density given income shifts to the right with a slight increase in variance as income increases, revealing that ITEs for individuals with high income is larger though more heterogeneous than for those whose income are low. Thus, the benefits from participating to 401(k) retirement programs on personal savings increase as Family Income increases. Though not as pronounced, the same trend is found when conditioning on age, family size and family status.

A striking feature of Figures 6, 7, 8, 9 and 10 is that there exists a small but statistically significant proportion (about 8.77% in the full sample) of individuals who experience negative effects, although the majority of ITEs is positive.101010For such an empirical evidence, one could investigate it alternatively by using the (conditional) quantile treatment effects for the complier group (see e.g. Abadie, Angrist, and Imbens, 2002; Froelich and Melly, 2013) at low quantiles. We thank Isaiah Andrews for this point. This is especially the case for young individuals (age percentile below 0.25) where such a proportion is 15.93%. Such a finding is new. In particular, Table 7 provides the summary statistics of the subgroup with negative ITEs, compared with the subgroup with positive ITE and the entire sample. Individuals with negative ITEs are more likely to be younger, single, and from smaller families with lower family income. A puzzling feature is that the subgroup with negative ITEs has a larger FNFA than the rest of the sample, though the large standard error (113.92) indicates a large heterogeneity among this group. Our conjecture is that the majority of this group use their savings to invest aggressively in their own businesses or in financial markets.

| Negative ITE | Positive ITE | Entire sample | |

|---|---|---|---|

| Participation in 401(k) | 0.2534 | 0.2784 | 0.2762 |

| (0.4352) | (0.4482) | (0.4472) | |

| FNFA (in thousand $) | 21.9558 | 18.7946 | 19.0717 |

| (113.9247) | (56.9039) | (63.9638) | |

| Family income | 30.5890 | 40.0872 | 39.2546 |

| (in thousand $) | (16.8846) | (24.5117) | (24.0900) |

| Age | 34.8327 | 41.6805 | 41.0802 |

| (9.2949) | (10.1917) | (10.2995) | |

| Married | 0.5572 | 0.6354 | 0.6286 |

| (0.4970) | (0.4813) | (0.4832) | |

| Family size | 2.6421 | 2.9084 | 2.8851 |

| (1.4826) | (1.5280) | (1.5258) | |

| Number | 813 | 8,462 | 9,275 |

Figure 11 uses a classification tree to summarize the benefits and losses of participation decisions for all individuals in the sample: Among those who are eligible, 5.67% of them participate in 401(k) but have negative ITEs, while 27.52% do not participate but would benefit from the 401(k) program. There are also 90.55% of non-eligible individuals who would benefit from the program if they participate. In monetary terms, the 401(k) program provides an average increase of $29.62k in FNFA to the 2,356 participants with positive ITEs and an average decrease of $19.42k in FNFA to the 206 participants with negative ITEs. That is a net increase of $65.7939 million in total in FNFA for the 401(k) program based on our sample of 9,275 households.

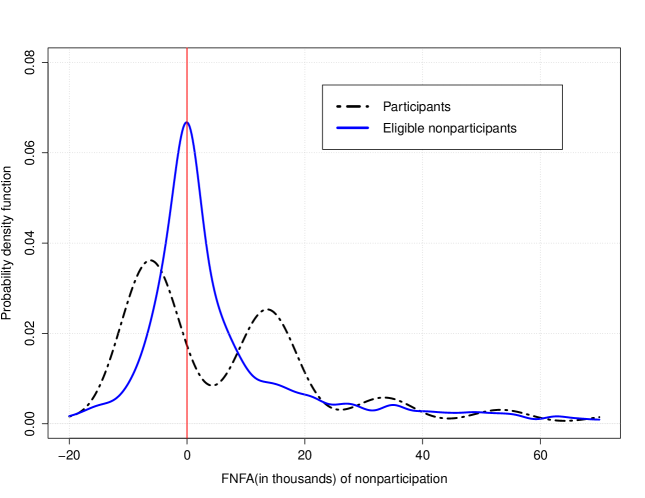

From Figure 11, about 93.12% of those who are eligible but do not participate in 401(k) programs have positive ITEs. How should one interpret this empirical evidence? Do these eligible nonparticipants have low preference for savings, or low ability for managing their financial assets? Our ITE estimates show that the average ITE for the group of eligible nonparticipating households is $40.36k, which is significantly larger than $25.68k, the average ITE of the participating group. This evidence suggests an adverse selection issue: Households who benefit more are less likely to participate. To shed some light on this second puzzling finding, Figure 12 provides density estimates of the potential outcome for not participating to the 401(k) program for the participating group as well as the group of eligible nonparticipants. An interesting feature is that the distribution of participants’ counterfactual FNFA (i.e., their savings without participating to 401(k) programs) are bimodal: Without participating to 401(k) programs, those participants would either do quite well or extremely poorly on their savings. In contrast, for the group of eligible but not participating households, the FNFA conforms to a unimodal distribution.

Finally, we can consider the following counterfactuals: Given that we recover the ITE for each individual, we can entertain a situation in which each eligible individual chooses his/her best option regarding participation. The 401(k) program would lead to a total increase of $116.4681 million in FNFA coming from the 2,356 eligible households with positive ITEs and the 1,001 eligible households with positive ITEs who did not participate. In addition, if the 401(k) program was available to all households, under the same scenario where each household is perfectly informed and make the correct decision, the 401(k) program will gain an additional $120.8375 million in FNFA due to those 5,105 non-eligible households with positive ITEs. This would lead to the maximum gain of $237.3056 million in FNFA for the 401(k) program from the 9,275 households in our sample.

References

- (1)

- Abadie (2003) Abadie, A. (2003): “Semiparametric instrumental variable estimation of treatment response models,” The Journal of Econometrics, 113(2), 231–263.

- Abadie, Angrist, and Imbens (2002) Abadie, A., J. Angrist, and G. Imbens (2002): “Instrumental variables estimates of the effect of subsidized training on the quantiles of trainee earnings,” Econometrica, 70(1), 91–117.

- Andrews (1991) Andrews, D. W. (1991): “Asymptotic normality of series estimators for nonparametric and semiparametric regression models,” Econometrica, pp. 307–345.

- Angrist, Chernozhukov, and Fernández-Val (2006) Angrist, J., V. Chernozhukov, and I. Fernández-Val (2006): “Quantile regression under misspecification, with an application to the US wage structure,” Econometrica, 74(2), 539–563.

- Angrist (1990) Angrist, J. D. (1990): “Lifetime earnings and the Vietnam era draft lottery: evidence from social security administrative records,” The American Economic Review, pp. 313–336.

- Angrist and Evans (1998) Angrist, J. D., and W. N. Evans (1998): “Children and their parents’ labor supply: evidence from exogenous variation in family size,” The American Economic Review, 88(3), 450–477.

- Chernozhukov and Hansen (2004) Chernozhukov, V., and C. Hansen (2004): “The Effects of 401(K) Participation on the Wealth Distribution: An Instrumental Quantile Regression Analysis,” The Review of Economics and Statistics, 86(3), 735–751.

- Chernozhukov and Hansen (2005) (2005): “An IV model of quantile treatment effects,” Econometrica, 73(1), 245–261.

- Chernozhukov and Hansen (2006) (2006): “Instrumental quantile regression inference for structural and treatment effect models,” Journal of Econometrics, 132, 491–525.

- Chernozhukov and Hansen (2008) (2008): “Instrumental variable quantile regression: A robust inference approach,” Journal of Econometrics, 142(1), 379–398.

- Chesher (2003) Chesher, A. (2003): “Identification in nonseparable models,” Econometrica, 71(5), 1405–1441.

- Chesher (2005) (2005): “Nonparametric identification under discrete variation,” Econometrica, 73(5), 1525–1550.

- Chiappori, Komunjer, and Kristensen (2015) Chiappori, P.-A., I. Komunjer, and D. Kristensen (2015): “Nonparametric identification and estimation of transformation models,” Journal of Econometrics, 188(1), 22–39.

- Darolles, Fan, Florens, and Renault (2011) Darolles, S., Y. Fan, J.-P. Florens, and E. Renault (2011): “Nonparametric instrumental regression,” Econometrica, 79(5), 1541–1565.

- Engen, Gale, and Scholz (1996) Engen, E. M., W. G. Gale, and J. K. Scholz (1996): “The illusory effects of saving incentives on saving,” The Journal of Economic Perspectives, 10(4), 113–138.

- Froelich and Melly (2013) Froelich, M., and B. Melly (2013): “Unconditional quantile treatment effects under endogeneity,” Journal of Business & Economic Statistics, 31(3), 346–357.

- Gagliardini and Scaillet (2012) Gagliardini, P., and O. Scaillet (2012): “Nonparametric instrumental variable estimation of structural quantile effects,” Econometrica, 80(4), 1533–1562.

- Guerre, Perrigne, and Vuong (2000) Guerre, E., I. Perrigne, and Q. Vuong (2000): “Optimal Nonparametric Estimation of First-Price Auctions,” Econometrica, 68(3), 525–574.

- Heckman, Smith, and Clements (1997) Heckman, J. J., J. Smith, and N. Clements (1997): “Making the most out of programme evaluations and social experiments: Accounting for heterogeneity in programme impacts,” The Review of Economic Studies, 64(4), 487–535.

- Heckman and Vytlacil (2005) Heckman, J. J., and E. Vytlacil (2005): “Structural equations, treatment effects, and econometric policy evaluation1,” Econometrica, 73(3), 669–738.

- Horowitz (1996) Horowitz, J. L. (1996): “Semiparametric estimation of a regression model with an unknown transformation of the dependent variable,” Econometrica, pp. 103–137.

- Horowitz and Lee (2007) Horowitz, J. L., and S. Lee (2007): “Nonparametric instrumental variables estimation of a quantile regression model,” Econometrica, 75(4), 1191–1208.

- Imbens and Angrist (1994) Imbens, G. W., and J. D. Angrist (1994): “Identification and estimation of local average treatment effects,” Econometrica, 62(2), 467–475.

- Imbens and Newey (2009) Imbens, G. W., and W. K. Newey (2009): “Identification and estimation of triangular simultaneous equations models without additivity,” Econometrica, 77(5), 1481–1512.

- Imbens and Rubin (1997) Imbens, G. W., and D. B. Rubin (1997): “Estimating outcome distributions for compliers in instrumental variables models,” The Review of Economic Studies, 64(4), 555–574.

- Koenker and Bassett (1978) Koenker, R., and G. Bassett (1978): “Regression quantiles,” Econometrica, pp. 33–50.

- Koenker and Xiao (2002) Koenker, R., and Z. Xiao (2002): “Inference on the quantile regression process,” Econometrica, 70(4), 1583–1612.

- Marmer and Shneyerov (2012) Marmer, V., and A. Shneyerov (2012): “Quantile-based nonparametric inference for first-price auctions,” Journal of Econometrics, 167(2), 345–357.

- Nelsen (2007) Nelsen, R. B. (2007): An introduction to copulas. Springer Science & Business Media.

- Newey and Powell (2003) Newey, W. K., and J. L. Powell (2003): “Instrumental Variable Estimation of Nonparametric Models,” Econometrica, 71(5), 1565–1778.

- Post, Van den Assem, Baltussen, and Thaler (2008) Post, T., M. J. Van den Assem, G. Baltussen, and R. H. Thaler (2008): “Deal or no deal? decision making under risk in a large-payoff game show,” The American Economic Review, pp. 38–71.

- Poterba, Venti, and Wise (1996) Poterba, J. M., S. F. Venti, and D. A. Wise (1996): “How Retirement Saving Programs Increase Saving,” The Journal of Economic Perspectives, 10(4), 91–112.

- Rubin (1974) Rubin, D. B. (1974): “Estimating causal effects of treatments in randomized and nonrandomized studies.,” Journal of Educational Psychology, 66(5), 688.

- Sakia (1992) Sakia, R. (1992): “The Box-Cox transformation technique: a review,” The statistician, pp. 169–178.

- Stone (1982) Stone, C. J. (1982): “Optimal global rates of convergence for nonparametric regression,” The Annals of Statistics, pp. 1040–1053.

- Van Der Vaart and Wellner (1996) Van Der Vaart, A. W., and J. A. Wellner (1996): Weak Convergence. Springer.

- Vuong and Xu (forthcoming) Vuong, Q., and H. Xu (forthcoming): “Counterfactual mapping and individual treatment effects in nonseparable models with discrete endogeneity,” Quantitative Economics.

- Vytlacil (2002) Vytlacil, E. (2002): “Independence, monotonicity, and latent index models: An equivalence result,” Econometrica, 70(1), 331–341.

Appendix A Proofs

A.1. Proof of Lemma 1

Proof.

First, we differentiate with respect to . Noting that for a continuous distribution , we obtain

Moreover, we have

It follows that

where the last step comes from the definition of in (4). Fix . Note that is weakly increasing on and strictly increasing on by Theorem 1. Moreover, because ,111111When such a rank of is unknown, we can modify the objective function by . The additional term changes the sign of based on the relative rank of while its scale does not matter for the optimization of . then has a weakly and strictly increasing derivative on and , respectively. Therefore, is weakly and strictly convex on and , respectively, for arbitrary . Furthermore, if , we have if and only if by Theorem 1. Thus, uniquely solves the first–order condition whenever . A similar argument also applies to the population objective function . ∎

A.2. Proof of Theorem 2

Proof.

Fix . All the following argument is conditional on . For simplicity, we suppress the dependence on , e.g., we use for , omit the term in the estimation, and in the conditional probability . Moreover, we only show the results for . The proof for the case can be derived similarly.

First, we show uniform consistency. By Angrist, Chernozhukov, and Fernández-Val (2006), it suffices to show that for any compact set . By the law of large number, we have pointwise convergence, i.e., . Then, it suffices to show the stochastic equicontinuity of the empirical process , which directly follows the general argument in Koenker and Xiao (2002). Next, we establish the limiting distribution of the process.

Taking the directional derivative, we have

where the remainder term is bounded by

By the computational properties of linear programming in Koenker and Bassett (1978, Theorem 3.3), we have uniformly in . We can derive a similar expression for . Note that and as minimizes . Hence, we have

uniformly in .

Following the convention, we introduce some notation from the empirical process literature: For and a generic function , let and . Hence, the above condition can be rewritten as

uniformly in . It follows that

| (8) |

Because , then by Taylor expansion,

Thus,

where the last term is uniform in due to the uniform convergence of to .

Let . Therefore, (8) implies

Note that which does not depend on . Hence,

Moreover, the derivative of is the derivative of . Thus, using (4) and the definition of , a Taylor expansion gives

where is between and . Note that uniformly in . It follows that

Because is Donsker, by the empirical process theorem (see e.g. Van Der Vaart and Wellner, 1996), we have the equicontinuity of the function class . Hence, uniformly in ,

which converges to a zero-mean Gaussian process. Thus, we obtain

| (9) |

where the right–hand side converges to a zero-mean Gaussian process. Therefore, converges in distribution to a zero-mean Gaussian process.

Its covariance kernel for is obtained as

where the second and third equalities use the definition of , and the fourth equality uses . The expression for given in the theorem follows upon noting that

A.3. Proof of Theorem 3

Proof.

We have , where

is the infeasible kernel estimator of . From standard kernel estimation, we have

since leads to oversmoothing. Thus, it suffices to show that the same uniform convergence rate holds for . We actually show that

so that the first step estimation error is negligible given our choice of bandwidth.

From a second-order Taylor expansion we have

where is between and . Since from Theorem 3, we have

where the summation is a nonparametric estimator of . Therefore,

which is an . Furthermore, because is bounded, we have

which is also an provided . Therefore, the first-step estimation error is negligible. ∎