Optimal Risk-Averse Timing of an Asset Sale:

Trending vs Mean-Reverting Price Dynamics

Abstract

This paper studies the optimal risk-averse timing to sell a risky asset. The investor’s risk preference is described by the exponential, power, or log utility. Two stochastic models are considered for the asset price – the geometric Brownian motion and exponential Ornstein-Uhlenbeck models – to account for, respectively, the trending and mean-reverting price dynamics. In all cases, we derive the optimal thresholds and certainty equivalents to sell the asset, and compare them across models and utilities, with emphasis on their dependence on asset price, risk aversion, and quantity. We find that the timing option may render the investor’s value function and certainty equivalent non-concave in price. Numerical results are provided to illustrate the investor’s strategies and the premium associated with optimally timing to sell.

Keywords: asset sale, risk aversion, certainty equivalent, optimal stopping, variational inequality

JEL Classification: C41, G11, G12

Mathematics Subject Classification (2010): 60G40, 62L15, 91G10, 91G80

1 Introduction

We consider a risk-averse investor who seeks to sell an asset by selecting a timing strategy that maximizes the expected utility resulting from the sale. At any point in time, the investor can either decide to sell immediately, or wait for a potentially better opportunity in the future. Naturally, the investor’s decision to sell should depend on the investor’s risk aversion and the price evolution of the risky asset. To better understand their effects, we model the investor’s risk preference by the exponential, power, or log utility. In addition, we consider two contrasting models for the asset price – the geometric Brownian motion (GBM) and exponential Ornstein-Uhlenbeck (XOU) models – to account for, respectively, the trending and mean-reverting price dynamics. The choice of multiple utilities and stochastic models allow for a comprehensive comparison analysis of all six possible settings.

We analyze a number of optimal stopping problems faced by the investor under different models and utilities. The investor’s value functions and the corresponding optimal timing strategies are solved analytically. In particular, we identify the scenarios where the optimal strategies are trivial. These arise in the GBM model with exponential and power utilities, but not with log utility or under the XOU model with any utility. The non-trivial optimal timing strategies are shown to be of threshold type. The optimal threshold represents the critical price at which the investor is willing to sell the asset and forgo future sale opportunities. In most cases, the optimal threshold is determined from an implicit equation, though under the GBM model with log utility the optimal threshold is explicit. Moreover, intuitively the investor’s optimal timing strategy should depend, not only on risk aversion and price dynamics, but also the quantity of assets to be sold simultaneously. In general, we find that the dependence is neither linear nor explicit. Nevertheless, under the GBM model with log utility, the optimal price to sell is inversely proportional to quantity so that the sale will always result in the same total revenue regardless of quantity. In contrast, under the XOU model with power utility, the optimal threshold is independent of quantity, and thus the total revenue scales linearly with quantity.

While all utility functions considered herein are concave, the timing option to sell may render the investor’s value functions and certainty equivalents non-concave in price under different models. For instance, under the GBM model with log utility the value function can be convex in the continuation (waiting) region and concave when the value function coincides with the utility function for sufficiently high asset price. Under the XOU model, we observe that the value functions are in general neither concave nor convex in price. If the time of asset sale is pre-determined and fixed, then the value functions are always concave. Therefore, the phenomenon of non-concavity arises due to the timing option to sell. Mathematically, the reason lies in the fact that the value functions are constructed using convex functions that are the general solutions to the PDE associated with the underlying GBM or XOU process.

To better understand the investor’s perceived value of the risky asset with the timing option to sell, we analyze the certainty equivalent associated with each utility maximization problem. With analytic formulas, we illustrate the properties of the certainty equivalents. In all cases, the certainty equivalent dominates the current asset price, and the difference indicates the premium of the timing option. The gap typically widens as the underlying price increases before eventually diminishing to zero for sufficiently high price. As a consequence, the certainty equivalents are in general neither concave nor convex in price. If the optimal strategy is trivial, the certainty equivalent is simply a linear function of asset price.

In the literature, Henderson (2007) considers a risk-averse manager with a negative exponential utility who seeks to optimally time the investment in a project while trading in a correlated asset as a partial hedge. Under the GBM model, the manager’s optimal timing strategy is to either invest according to a finite threshold or postpone indefinitely. In comparison, the investor in our exponential utility case under the GBM model may either sell immediately or at a finite threshold, but will never find it optimal to wait indefinitely. Evans et al. (2008) also study a mixed stochastic control/optimal stopping problem with the objective of determining the optimal time to sell a non-traded asset where the investor has a power utility. In our paper, we show that the optimal timing with power utility is either to sell immediately or wait indefinitely under the GBM model, but the threshold-type strategy is optimal under the XOU model.

Our study focuses on the GBM and XOU models for the asset price. A related paper by Leung et al. (2015) analyzes optimal stopping and switching problems under the XOU model. Their results are applicable to our case with power utility under the same model. Other mean-reverting price models, such as the OU model (see e.g. Ekström et al. (2011)) and Cox-Ingersoll-Ross (CIR) model (see e.g. Ewald and Wang (2010); Leung et al. (2014)), have been used to analyze various optimal timing problems. The recent work by Ekström and Vaicenavicius (2016) investigates the optimal timing to sell an asset when its price process follows a GBM-like process with a random drift. All these studies do not incorporate risk aversion.

Alternative risk criteria can also be used to study the asset sale timing problem. Inspired by prospect theory, Henderson (2012) considers an S-shape (piecewise power) utility function of gain/loss relative to the initial price. Under the GBM model, the investor may find it optimal to sell at a loss. Pedersen and Peskir (2016) solves for the optimal selling strategy under the mean-variance risk criterion. Instead of maximizing expected utility, one can also incorporate alternative risk penalties to the optimal timing problems. Leung and Shirai (2015) study this problem under both GBM and XOU models with shortfall and quadratic penalties. Other than asset sale, the problem of optimal time to sell and/or buy derivatives by a risk-averse investor has been studied by Henderson and Hobson (2011); Leung and Ludkovski (2012), among others.

A natural extension for future research is to continue to investigate the asset sale timing under other underlying dynamics, such as models with jumps, stochastic volatility, and/or regime switching. Another major direction is to incorporate model ambiguity to the associated optimal stopping problems; see Riedel (2009); Cheng and Riedel (2013). In addition to the trading of risky assets, it is also of interest to incorporate utility and partial hedging in the optimal liquidation of derivatives.

We organize the rest of the paper in the following manner. In Section 2, the asset sale problems are formulated for different utilities and price dynamics. In Section 3, we present the solutions of the problems and discuss the optimal selling strategies. We analyze the certainty equivalents in Section 4. All proofs are included in Section 5.

2 Problem Overview

We consider a risk-averse asset holder (investor) with a subjective probability measure . For our optimal asset sale problems, we will study two models for the risky asset price, namely, the geometric Brownian motion (GBM) model and the exponential Ornstein-Uhlenbeck (XOU) model. First, the GBM price process satisfies

with constant parameters and , where is a standard Brownian motion under . Under the second model, the XOU price process is defined by

| (2.1) |

where the log-price is an OU process with constant parameters , .

The investor’s risk preference is modeled by three utility functions:

-

(1)

Exponential utility

with the risk aversion parameter ;

-

(2)

Log utility

-

(3)

Power utility

where , with the risk aversion parameter . In particular, when , the power utility is linear, corresponding to zero risk aversion.

Denote by the filtration generated by the Brownian motion , and the set of all -stopping times. The investor seeks to maximize the expected discounted utility from asset sale by selecting the optimal stopping time. Denote by the quantity of the risky asset to be sold. For simplicity, we limit our analysis to simultaneous liquidation of all units. The investor will receive the utility value of or , , under the GBM and XOU model respectively, when all units are sold at time .

Therefore, the investor solves the optimal stopping problems under two different price dynamics:

| (2.2) | |||

| (2.3) |

for , where is the constant subjective discount rate. We have used the shorthand notations: and . By the standard theory of optimal stopping (see e.g. Chapter 1 of Peskir and Shiryaev (2006) and Chapter 10 of Øksendal (2003)), the optimal stopping times are of the form

| (2.4) | ||||

| (2.5) |

In this paper, we analytically derive the value functions and show they satisfy their associated variational inequalities. Under the GBM model, for any fixed , the value functions , for , satisfy the variational inequalities

| (2.6) |

for , where is the infinitesimal generator of defined by

| (2.7) |

Likewise, under the XOU model the value functions , , solve the variational inequalities

| (2.8) |

for , where

| (2.9) |

is the infinitesimal generator of the OU process (see (2.1)). For optimal stopping problems driven by an XOU process, we find it more convenient to work with the log-price

To better understand the value of the risky asset under optimal liquidation, we study the certainty equivalent associated with each utility maximization problem. The certainty equivalent is defined as the guaranteed cash amount that generates the same utility as the maximal expected utility from optimally timing to sell the risky asset. Precisely, we define

| (2.10) | |||||

| (2.11) |

for , under the GBM and XOU models respectively. Certainty equivalent gives us a common (cash) unit to compare the values of timing to sell under different utilities, dynamics, and quantities.

Moreover, the certainty equivalent can shed light on the investor’s optimal strategy. Indeed, applying (2.10) and (2.11) to (2.4) and (2.5) respectively, we obtain an alternative expression for the optimal stopping time under each model:

| (2.12) | ||||

| (2.13) |

In other words, it is optimal for the investor to sell when the certainty equivalent is equals to the total cash amount of or , under the GBM or XOU model respectively, received from the sale.

3 Optimal Timing Strategies

In this section, we present the analytical results and discuss the value functions and optimal selling strategies under the GBM and XOU models. The methods of solution and detailed proofs are presented in Section 5.

3.1 The GBM Model

To prepare for our results for the GBM model, we first consider an increasing general solution to the ODE:

| (3.1) |

with defined in (2.7). This solution is with

| (3.2) |

By inspection, we see that when , and when

Theorem 3.1

Consider the optimal asset sale problem (2.2) under the GBM model with exponential utility.

-

(i)

If then it is optimal to sell immediately, and the value function is .

-

(ii)

If then the value function is given by

where the optimal threshold is uniquely determined by the equation

(3.3) The optimal time to sell is

Under the GBM model with exponential utility, the optimal selling strategy can be either trivial or non-trivial. When the subjective discount rate equals or exceeds the drift of the GBM process, it is optimal to sell immediately. This is intuitive as the asset net discounting tends to lose value. On the other hand, when , the investor should sell when the unit price exceeds a finite threshold. At the optimal sale time , the investor receives the cash amount from the sale of units of In other words, is the per-unit price received upon sale, but according to (3.3) it varies depending on the quantity and risk aversion parameter .

Theorem 3.2

Consider the optimal stopping problem (2.2) under the GBM model with log utility. The value function is given by

where is the unique optimal threshold. The optimal time to sell is

With log utility, the optimal strategy is to sell as soon as the unit price of the risky asset, , enters the upper interval . Note that the optimal threshold is inversely proportional to quantity, so the total cash amount received upon sale, , remains the same regardless of quantity. In other words, the log-utility investor is not financially better off by holding more units of . Under exponential utility, the optimal selling price is implicitly defined by (3.3) in Theorem 3.1 and must be evaluated numerically. In contrast, the optimal threshold under log utility is fully explicit.

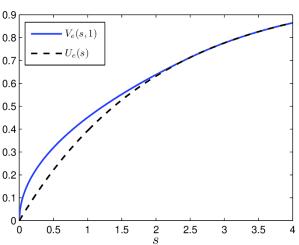

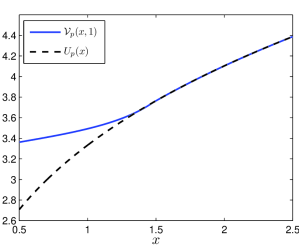

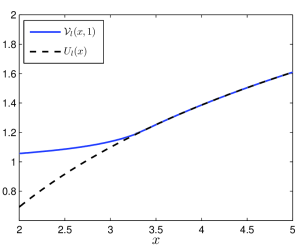

Turning to the value functions, a natural question is whether they preserve the concavity of the utilities. Indeed, if the investor sells at a pre-determined fixed time , then the expected utility is concave in for any concave utility function . From Theorem 3.1, we see that is concave in for all On the other hand, is concave in when , but it is neither convex nor concave in when . In other words, the timing option to sell gives rise to the possibility of non-concave value function. In Figure 1, we plot the value functions associated with the exponential and log utilities when the investor is holding a single unit of the asset. The value functions dominate the utility functions, and coincide smoothly at the optimal selling thresholds. In Figure 1(b), the value function under log utility is shown to have two possible shapes. For , i.e. , the value function is convex when is lower than , and concave for . In the other scenario, , i.e. , the value function is concave.

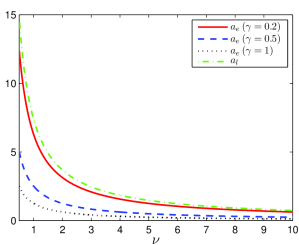

Figure 2 illustrates the effect of quantity on optimal selling thresholds and under exponential and log utilities respectively. The optimal strategy under power utility is trivial and thus omitted from the figure. The optimal threshold is decreasing in for each fixed risk aversion and . Moreover, for any fixed quantity, a higher lowers the optimal selling price. The quantity effectively scales up the risk aversion to the value instead of . Increase in either of these parameters results in higher risk aversion, inducing the investor to sell at a lower price. In comparison, the log-utility optimal threshold is explicit and inversely proportional to , as seen in the figure.

We conclude this section with a discussion on the optimal liquidation strategy under power utility. First, observe that for any the power process is also a GBM satisfying

with new parameters

Then, the process is a submartingale (resp. supermartingale) if (resp. ). As a result, the optimal timing to sell is trivial, as we summarize next.

Theorem 3.3

Consider the optimal asset sale problem (2.2) under the GBM model with power utility.

-

(i)

If , then it is optimal to sell immediately, and the value function .

-

(ii)

If , then it is optimal to wait indefinitely, and the value function .

3.2 The XOU Model

In this section, we discuss the optimal asset sale problems under the XOU model. As is well known (see p.542 of Borodin and Salminen (2002) and Prop. 2.1 of Alili et al. (2005)), the classical solutions of the ODE

| (3.4) |

for , are

| (3.5) | |||

| (3.6) |

Alternatively, the functions and can be expressed as

where is the parabolic cylinder function or Weber function (see Erdélyi et al. (1953)). Direct differentiation yields that , , , and . Hence, both and are strictly positive and convex, and they are, respectively, strictly increasing and decreasing. In particular, the function plays a central role in the solution of the optimal asset sale problems under the XOU model.

Theorem 3.4

Under an XOU model with exponential utility, the optimal asset sale problem admits the solution

| (3.7) |

with the constant

The critical log-price level satisfies

| (3.8) |

The optimal time to sell is

According to Theorem 3.4, the investor should sell all units as soon as the asset price reaches or above. The optimal price level depends on both the investor’s risk aversion and quantity, but it stays the same as long as the product remains unchanged.

Theorem 3.5

Under an XOU model with log utility, the optimal asset sale problem admits the solution

| (3.9) |

with the coefficient

| (3.10) |

The finite critical log-price level is uniquely determined from the equation

| (3.11) |

The optimal time to sell is

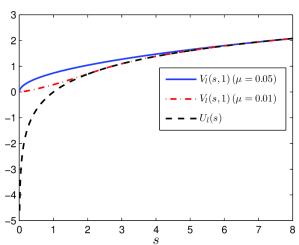

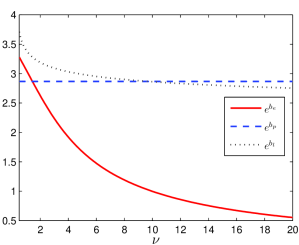

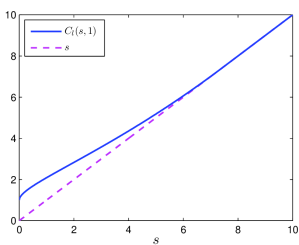

In Figure 3(d), we see that the optimal unit selling price is decreasing in but when multiplied by the quantity , the total cash amount received from the sale increases.

For the case of power utility, we observe that is again an XOU process, satisfying

| (3.12) |

with the new parameters , and . In particular, both the original long-run mean and volatility parameter have been scaled by a factor of , while the speed of mean reversion remains unchanged. Therefore, the value function admits the separable form:

| (3.13) |

where

| (3.14) |

Hence, without loss of generality, the optimal timing to sell can be determined from the optimal stopping problem in (3.14), and the corresponding value function can be recovered from (3.13).

Theorem 3.6

Under the XOU model with power utility, the solution to the optimal asset sale problem is given by

where

The critical log-price threshold satisfies the equation

| (3.15) |

where . The optimal asset sale timing is

The investor should sell all units the first time the asset price reaches the level According to (3.15), the optimal price level is independent of quantity , as we can see in Figure 3(d).

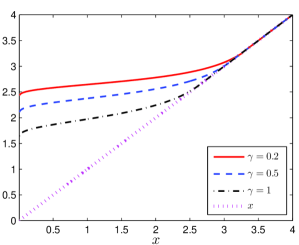

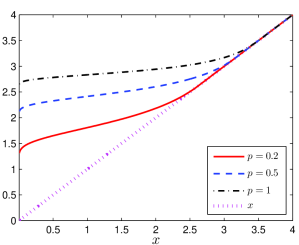

Under the XOU model, the value functions are not necessarily concave in due to the convex nature of and the timing option to sell. Let’s inspect the value functions in Figure 3. In each of these three cases, the value function is initially convex before smooth-pasting on the concave utility.

In Table 1, we summarize the results from Sections 3.1 and 3.2 and list the optimal thresholds for all the cases we have discussed. All thresholds, except , are implicitly determined by the equations referenced in the table. The asset price model plays a crucial role in the structure of the optimal strategy. Under the GBM model with exponential utility, immediate liquidation may be optimal in one scenario regardless of the current asset price. On the contrary, with the same utility under the XOU model, immediate liquidation is never optimal and the investor should wait till the asset price rises to level With power utility, the GBM model implies a trivial optimal strategy, whereas the XOU model results in a threshold-type strategy. Lastly, even though both GBM and XOU price processes lead to non-trivial strategies for log utility, the optimal threshold is explicit while must be computed numerically.

4 Certainty Equivalents

Having derived the value functions analytically, we now state as corollaries the certainty equivalents and , defined respectively in (2.10) and (2.11) under the GBM and XOU models. Furthermore, to quantify the value gained from waiting to sell the asset compared to immediate liquidation, we define the optimal liquidation premium under each model:

| (4.1) | ||||

| (4.2) |

for . We will examine the dependence of this premium on the asset price and quantity.

Corollary 4.1

Under the GBM model, the certainty equivalents under different utilities are given as follows:

-

(1)

Exponential utility:

-

(2)

Log utility:

-

(3)

Power utility:

With exponential and log utilities, the certainty equivalents dominate – the value from immediate sale, and they coincide when the asset price exceeds the corresponding optimal selling thresholds. With power utility, the investor either sells immediately or waits indefinitely, corresponding to the certainty equivalents of value and , respectively.

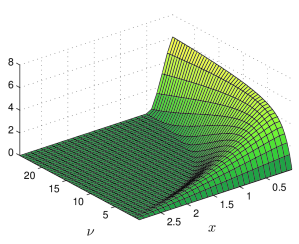

The impact of on is both direct in its certainty equivalent’s expression, but also indirect in the derivation of . As a result, the relationship between and is rather intricate. In comparison, the explicit formula for the optimal threshold under log utility facilitates our analysis on the behavior of the certainty equivalent . Fix any price , is convex in when . Consequently, the liquidation premium is maximized at However, when then is concave on the price interval and convex on This implies that there exists an optimal quantity that maximizes the liquidation premium. This is useful when the investor can also choose the initial position in .

Next, we state the certainty equivalents under the XOU model.

Corollary 4.2

Under the XOU model, the certainty equivalents under different utilities are given as follows:

-

(1)

Exponential utility:

-

(2)

Log utility:

-

(3)

Power utility:

(4.3)

For all three utilities, the certainty equivalents are equal to the immediate sale value, , when the asset price is in the exercise region, where all units are sold. In addition, we emphasize that both and are dependent on which can be observed from (3.8) and (3.11). In contrast, the optimal log-price threshold under power utility is independent of . Consequently, if we consider any fixed in the continuation region then the certainty equivalent is linear and strictly increasing in This is interesting since under exponential and log utilities, increasing quantity has the effect of making the investor more risk-averse. In other words, as long as quantity is large enough, the investor will liquidate everything immediately even if the current price appears unattractive.

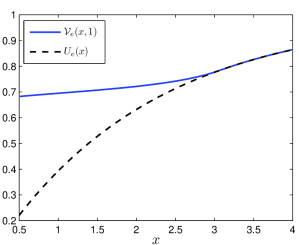

Let us now examine the certainty equivalents’ dependence on the asset price. Under the GBM model, we plot the certainty equivalents, and against prices, respectively, in Figures 4(a) and 4(b), with a single unit of asset held. The optimal selling strategy for power utility is trivial, and thus, not presented. From Section 3.1, we know that for sufficiently large it is optimal to sell and thus the certainty equivalents will eventually coincide with and be linear. Notice that in both Figures 4(a) and 4(b), the certainty equivalents are concave for small and subsequently convex for large . In general, the certainty equivalents are neither concave nor convex functions of asset price, especially since the value functions and are not necessarily concave.

In Figure 4(a), we have also shown for different values of risk aversion level . As the investor becomes more risk-averse, it becomes optimal to sell the asset earlier. This is reflected by the certainty equivalent’s convergence to the linear price line at a lower price. Moreover, a less risk-averse certainty equivalent dominates a more risk-averse one at all prices. Similar effects of risk aversion is also seen in Figure 4(c) for exponential utility and Figure 4(d) for power utility under the XOU model.

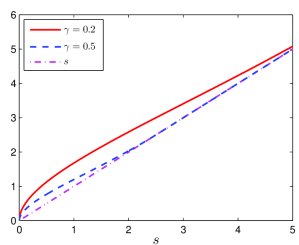

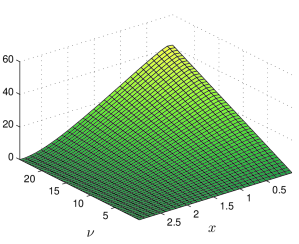

Figures 5(a) and 5(b), respectively, illustrate the liquidation premia for exponential and power utilities under the XOU model. The liquidation premium for power utility is linear in for any fixed value of , but the exponential utility liquidation premium is nonlinear. In general, the liquidation premium vanishes when is sufficiently high when the asset price is in the exercise region. As we can see from Figures 5(a) and 5(b) and Figures 4(a)-(d), the optimal liquidation premium tends to be large and may increase when the asset price is very low. This suggests that there is a high value of waiting to sell the asset later if the current price is low. As the asset price rises, the premium shrinks to zero. The investor finds no value in waiting any longer, resulting in an immediate sale.

5 Methods of Solution and Proofs

In this section, we present the detailed proofs for our analytical results in Section 3, from Theorems 3.1 - 3.2 for the GBM model to Theorems 3.4 - 3.6 for the XOU model. Our method of solution is to first construct candidate solutions using the classical solutions to ODEs (3.1) and (3.4), corresponding to the GBM and XOU models respectively, and then verify that the candidate solutions indeed satisfy the associated variational inequalities (2.6) and (2.8).

5.1 GBM Model

Proof of Theorem 3.1

(Exponential Utility). To prove that the value functions in Theorem 3.1 satisfy the variational inequality in (2.6), we consider the two cases, and , separately.

When , it is optimal to sell immediately. To see this, for any fixed we verify that satisfies (2.6). Since for all we only need to check that the inequality

| (5.1) |

holds for all . First, we observe that the sign of the LHS of (5.1) depends solely on

| (5.2) |

The first and order second derivatives are, respectively,

from which we observe that is strictly concave on . Furthermore, and the fact imply that has a global maximum. Since (resp. ) if (resp. ), the maximum of is non-positive if . As a result, is non-positive for all which yields inequality (5.1), as desired.

For an arbitrary , we can view together as the risk aversion parameter for the exponential utility, and equivalently consider the asset sale problem with and risk aversion without loss of generality. When , we consider a candidate solution of the form , where is a constant to be determined. Recall that is less than when and hence is an increasing concave function. We solve for the optimal threshold and coefficient from the value-matching and smooth-pasting conditions

| (5.3) | ||||

This leads to the following equation satisfied by the optimal threshold :

| (5.4) |

We now show that there exists a unique and positive root to (5.4). Our approach involves establishing a relationship between (5.4) and To this end, first observe that the exponential utility has the following properties:

| (5.5) |

where

and is a decreasing and convex solution to (3.1). In addition, we have

| (5.6) |

The limits in (5.5) and condition (5.6) together imply that the function admits the following analytic representation:

| (5.7) |

where

and

We refer the reader to Section 2 of Zervos et al. (2013) and Chapter 2 of Borodin and Salminen (2002) for details on the representation.

Next, dividing by and differentiating in , we have

| (5.8) |

The crucial step is to recognize that finding the root to the derivative in (5.8) is equivalent to solving (5.4). Furthermore, appealing to (5.7), the LHS of (5.8) becomes

where

Since both and are strictly positive for , we conclude that (5.4) is equivalent to the equation By differentiating, we obtain . Since for all , the sign of depends solely on , and thus on defined in (5.2). The function is strictly concave on Since , the maximum of is strictly positive. This implies that there exists a unique positive such that Consequently, we have

| (5.9) |

This together with the fact that , lead us to conclude that there exists a unique such that if and only if . The latter holds due to the facts:

| (5.10) |

Therefore, we conclude that there exists a unique finite root to equation (5.4). Furthermore, by the nature of we have

| (5.11) |

Finally, from (5.3) we deduce that

Proof of Theorem 3.2

(Log Utility). For any fixed follows a GBM process with the same drift and volatility parameters as In other words, we can reduce the problem to that of selling a single unit of a risky asset whose price process is with initial value Therefore, we construct a candidate solution of the form , where is a positive constant. The value-matching and smooth-pasting conditions are

| (5.12) | ||||

| (5.13) |

These equations can be solved explicitly to give a unique solution and consequently the coefficient The optimal aggregate selling price translates into the optimal unit selling price

Next, we show that given in Theorem 3.2 indeed satisfies the variational inequality

where is the infinitesimal generator of the GBM process This is equivalent to showing that in (3.2) satisfies the variational inequality (2.6). First, on we have Next, observe that the function

has a unique root at such that

On we have To show that we need to prove that or equivalently,

| (5.14) |

This follows directly from the definition of in (3.2).

5.2 XOU Model

Proof of Theorem 3.4

(Exponential Utility). Recall that the functions and (see (3.5) and (3.6)) are respectively increasing and decreasing. Since the exponential utility is strictly increasing, we postulate that the solution to the variational inequality (2.8) is of the form , where is a positive coefficient to be determined. By grouping with , the problem of selling units of the risky asset can be reduced to that of selling a single unit. The value-matching and smooth-pasting conditions are

| (5.16) | ||||

| (5.17) |

Using (5.16), we have Combining (5.16) and (5.17), we obtain (3.8) for .

Next, we want to establish that

| (5.18) |

First, using (2.9) we compute

Then, for any

where we have used the fact that conditioned on has a folded normal distrbution. Furthermore, since this bound is time-independent and finite, we deduce that (5.18) is indeed true. We follow the arguments in Section 2 of Zervos et al. (2013) to obtain the representation

| (5.19) |

where

| (5.20) |

and

To see the connection between (5.2) and (3.8), we divide both sides of (5.2) by and differentiate with respect to , and get the derivative

| (5.21) | ||||

| (5.22) |

where

| (5.23) |

By comparing (3.8) to the numerator on the RHS of (5.21), and given that in (5.22) is strictly positive, we see that the equation satisfied by in (3.8) is equivalent to Therefore, our goal is to show that has a unique and finite root.

Differentiating (5.23) with respect to yields

Furthermore, observe that the sign of depends solely on We proceed to show that has a unique root. To facilitate computation, we define a new function

Since is obtained through dividing and multiplying by strictly positive terms, any root of must also be a root of and vice-versa.

To find the root of , we solve

| (5.24) |

The RHS of (5.24) is a strictly increasing linear function. As for the LHS, we observe that

Hence, in order for to have a unique root, it suffices to show that the LHS of (5.24) is strictly decreasing. Given that , , and is strictly increasing, it remains to show that the function is strictly increasing for all . The quotient rule gives

The numerator goes to as goes to and goes to as goes to Moreover, the derivative of is which is strictly positive. This proves that the function is indeed strictly increasing and as a result, has a unique root, denoted by . Finally, observe that

| (5.25) |

Combining (5.25) with , we now see that a unique root, , such that , exists if and only if . To examine this limit, we apply the definition of to get

| (5.26) | ||||

| (5.27) |

Since is strictly decreasing in , (5.26) and (5.27) hold if and only if . This shows, as desired, that there exists a unique and finite such that

Moreover, by (5.25), we see that

| (5.28) |

Proof of Theorem 3.5

(Log Utility). Since where is an OU process, the optimal asset sale problem can be viewed as that under an OU process with a linear utility and a transaction cost (resp. reward) of value if (resp. ) (see Leung and Li (2015)).

The functions and given in (3.5) and (3.6) are respectively strictly increasing and decreasing functions. For any given is also a strictly increasing function. This prompts us to postulate a solution to the variational inequality (2.8) of the form where is a constant to be determined. Consequently, the optimal log-price thershold is determined from the following value-matching and smooth-pasting conditions:

| (5.29) |

Combining these equations leads to (3.10) and (3.11). Straightforward computation yields

which is a strictly decreasing linear function with a unique root For any ,

which implies that

With this, we follow the arguments in Section 2 of Zervos et al. (2013) to obtain the representation

| (5.30) |

where and are as defined in (5.20). We relate (5.30) to (3.11) by first dividing both sides of (5.30) by and differentiating with respect to This yields

| (5.31) | ||||

where

Comparing (3.11) and the RHS of (5.31), along with the facts that and , we see that solving equation (3.11) for the log-price threshold is equivalent to solving

Direct differentiation yields that

| (5.32) |

The fact that implies that there exists a unique such that if and only if . By the definition of , we have

| (5.33) |

Given that is strictly decreasing in we conclude that in order for (5.33) to hold, we must have . This means that there exists a unique and finite such that . Moreover, given (5.32), we have

| (5.34) |

Furthermore, since both and are strictly positive, must also be positive.

Lastly, we need to check that the following variational inequality holds for any fixed :

| (5.35) |

To begin, on the interval we have Next, on the region , we have

since the function is increasing on due to (5.33) and (5.34). Also, we note that

The latter inequality is true due to (5.32) and (5.34). defined in Theorem 3.5 is therefore the optimal solution to the optimal asset sale problem under log utility.

Proof of Theorem 3.6

(Power Utility). Since the powered XOU process, , is still an XOU process, the asset sale problem is an optimal stopping problem driven an XOU process, which has been solved by the authors’ prior work; see Theorem 3.1.1 of Leung et al. (2015). Therefore, we omit the proof.

References

- Alili et al. (2005) Alili, L., Patie, P., and Pedersen, J. (2005). Representations of the first hitting time density of an Ornstein-Uhlenbeck process. Stochastic Models, 21(4):967–980.

- Borodin and Salminen (2002) Borodin, A. and Salminen, P. (2002). Handbook of Brownian Motion: Facts and Formulae. Birkhauser, 2nd edition.

- Cheng and Riedel (2013) Cheng, X. and Riedel, F. (2013). Optimal stopping under ambiguity in continuous time. Mathematics and Financial Economics, 7(1):29–68.

- Ekström et al. (2011) Ekström, E., Lindberg, C., and Tysk, J. (2011). Optimal liquidation of a pairs trade. In Nunno, G. D. and Øksendal, B., editors, Advanced Mathematical Methods for Finance, chapter 9, pages 247–255. Springer-Verlag.

- Ekström and Vaicenavicius (2016) Ekström, E. and Vaicenavicius, J. (2016). Optimal liquidation of an asset under drift uncertainty. Working Paper.

- Erdélyi et al. (1953) Erdélyi, A., Magnus, W., Oberhettinger, F., and Tricomi, F. G. (1953). Higher Transcendental Functions, volume 2. McGraw-Hill.

- Evans et al. (2008) Evans, J., Henderson, V., and Hobson, D. (2008). Optimal timing for an indivisible asset sale. Mathematical Finance, 18(4):545–567.

- Ewald and Wang (2010) Ewald, C.-O. and Wang, W.-K. (2010). Irreversible investment with Cox-Ingersoll-Ross type mean reversion. Mathematical Social Sciences, 59(3):314–318.

- Henderson (2007) Henderson, V. (2007). Valuing the option to invest in an incomplete market. Mathematics and Financial Economics, 1(2):103–128.

- Henderson (2012) Henderson, V. (2012). Prospect theory, liquidation, and the disposition effect. Management Science, 58(2):445–460.

- Henderson and Hobson (2011) Henderson, V. and Hobson, D. (2011). Optimal liquidation of derivative portfolios. Mathematical Finance, 21(3):365–382.

- Leung and Li (2015) Leung, T. and Li, X. (2015). Optimal mean reversion trading with transaction costs and stop-loss exit. International Journal of Theoretical & Applied Finance, 18(3):15500.

- Leung et al. (2014) Leung, T., Li, X., and Wang, Z. (2014). Optimal starting–stopping and switching of a CIR process with fixed costs. Risk and Decision Analysis, 5(2):149–161.

- Leung et al. (2015) Leung, T., Li, X., and Wang, Z. (2015). Optimal multiple trading times under the exponential OU model with transaction costs. Stochastic Models, 31(4):554–587.

- Leung and Ludkovski (2012) Leung, T. and Ludkovski, M. (2012). Accounting for risk aversion in derivatives purchase timing. Mathematics & Financial Economics, 6(4):363–386.

- Leung and Shirai (2015) Leung, T. and Shirai, Y. (2015). Optimal derivative liquidation timing under path-dependent risk penalties. Journal of Financial Engineering, 2(1):1550004.

- Øksendal (2003) Øksendal, B. (2003). Stochastic Differential Equations: an Introduction with Applications. Springer.

- Pedersen and Peskir (2016) Pedersen, J. L. and Peskir, G. (2016). Optimal mean-variance selling strategies. Mathematics and Financial Economics, 10(2):203–220.

- Peskir and Shiryaev (2006) Peskir, G. and Shiryaev, A. N. (2006). Optimal Stopping and Free-boundary problems. Birkhauser-Verlag, Lectures in Mathematics, ETH Zurich.

- Riedel (2009) Riedel, F. (2009). Optimal stopping with multiple priors. Econometrica, 77(3):857–908.

- Zervos et al. (2013) Zervos, M., Johnson, T., and Alazemi, F. (2013). Buy-low and sell-high investment strategies. Mathematical Finance, 23(3):560–578.