Balancing Suspense and Surprise: Timely Decision Making with Endogenous Information Acquisition

Ahmed M. Alaa

Electrical Engineering Department

University of California, Los Angeles

ahmedmalaa@ucla.edu &Mihaela van der Schaar

Department of Engineering Science

University of Oxford

mihaela.vanderschaar@eng.ox.ac.uk

Abstract

We develop a Bayesian model for decision-making under time pressure with endogenous information acquisition. In our model, the decision-maker decides when to observe (costly) information by sampling an underlying continuous-time stochastic process (time series) that conveys information about the potential occurrence/non-occurrence of an adverse event which will terminate the decision-making process. In her attempt to predict the occurrence of the adverse event, the decision-maker follows a policy that determines when to acquire information from the time series (continuation), and when to stop acquiring information and make a final prediction (stopping). We show that the optimal policy has a ”rendezvous” structure, i.e. a structure in which whenever a new information sample is gathered from the time series, the optimal ”date” for acquiring the next sample becomes computable. The optimal interval between two information samples balances a trade-off between the decision maker’s ”surprise”, i.e. the drift in her posterior belief after observing new information, and ”suspense”, i.e. the probability that the adverse event occurs in the time interval between two information samples. Moreover, we characterize the continuation and stopping regions in the decision-maker’s state-space, and show that they depend not only on the decision-maker’s beliefs, but also on the ”context”, i.e. the current realization of the time series.

1 Introduction

The problem of timely risk assessment and decision-making based on a sequentially observed time series is ubiquitous, with applications in finance, medicine, cognitive science and signal processing [1-7]. A common setting that arises in all these domains is that a decision-maker, provided with sequential observations of a time series, needs to decide whether or not an adverse event (e.g. financial crisis, clinical acuity for ward patients, etc) will take place in the future. The decision-maker’s recognition of a forthcoming adverse event needs to be timely, for that a delayed decision may hinder effective intervention (e.g. delayed admission of clinically acute patients to intensive care units can lead to mortality [5]). In the context of cognitive science, this decision-making task is known as the two-alternative forced choice (2AFC) task [15]. Insightful structural solutions for the optimal Bayesian 2AFC decision-making policies have been derived in [9-16], most of which are inspired by the classical work of Wald on sequential probability ratio tests (SPRT) [8].

In this paper, we present a Bayesian decision-making model in which a decision-maker adaptively decides when to gather (costly) information from an underlying time series in order to accumulate evidence on the occurrence/non-occurrence of an adverse event. The decision-maker operates under time pressure: occurrence of the adverse event terminates the decision-making process. Our abstract model is motivated and inspired by many practical decision-making tasks such as: constructing temporal patterns for gathering sensory information in perceptual decision-making [1], scheduling lab tests for ward patients in order to predict clinical deterioration in a timely manner [3, 5], designing breast cancer screening programs for early tumor detection [7], etc.

We characterize the structure of the optimal decision-making policy that prescribes when should the decision-maker acquire new information, and when should she stop acquiring information and issue a final prediction. We show that the decision-maker’s posterior belief process, based on which policies are prescribed, is a supermartingale that reflects the decision-maker’s tendency to deny the occurrence of an adverse event in the future as she observes the survival of the time series for longer time periods. Moreover, the information acquisition policy has a ”rendezvous” structure; the optimal ”date” for acquiring the next information sample can be computed given the current sample. The optimal schedule for gathering information over time balances the information gain (surprise) obtained from acquiring new samples, and the probability of survival for the underlying stochastic process (suspense). Finally, we characterize the continuation and stopping regions in the decision-maker’s state-space and show that, unlike previous models, they depend on the time series ”context” and not just the decision-maker’s beliefs.

Related Works Mathematical models and analyses for perceptual decision-making based on sequential hypothesis testing have been developed in [9-17]. Most of these models use tools from sequential analysis developed by Wald [8] and Shiryaev [21, 22]. In [9,13,14], optimal decision-making policies for the 2AFC task were computed by modelling the decision-maker’s sensory evidence using diffusion processes [20]. These models assume an infinite time horizon for the decision-making policy, and an exogenous supply of sensory information.

The assumption of an infinite time horizon was relaxed in [10] and [15], where decision-making is assumed to be performed under the pressure of a stochastic deadline; however, these deadlines were considered to be drawn from known distributions that are independent of the hypothesis and the realized sensory evidence, and the assumption of an exogenous information supply was maintained. In practical settings, the deadlines would naturally be dependent on the realized sensory information (e.g. patients’ acuity events are correlated with their physiological information [5]), which induces more complex dynamics in the decision-making process. Context-based decision-making models were introduced in [17], but assuming an exogenous information supply and an infinite time horizon.

The notions of “suspense” and “surprise” in Bayesian decision-making have also been recently introduced in the economics literature (see [18] and the references therein). These models use measures for Bayesian surprise, originally introduced in the context of sensory neuroscience [19], in order to model the explicit preference of a decision-maker to non-instrumental information. The goal there is to design information disclosure policies that are suspense-optimal or surprise-optimal. Unlike our model, such models impose suspense (and/or surprise) as a (behavioral) preference of the decision-maker, and hence they do not emerge endogenously by virtue of rational decision making.

2 Timely Decision Making with Endogenous Information Acquisition

Time Series Model The decision-maker has access to a time-series modeled as a continuous-time stochastic process that takes values in , and is defined over the time domain , with an underlying filtered probability space . The process is naturally adapted to , and hence the filtration abstracts the information conveyed in the time series realization up to time . The decision-maker extracts information from to guide her actions over time.

We assume that is a stationary Markov process111Most of the insights distilled from our results would hold for more general dependency structures. However, we keep this assumption to simplify the exposition and maintain the tractability and interpretability of the results., with a stationary transition kernel , where is a realization of a latent Bernoulli random variable (unobservable by the decision-maker), with . The distributional properties of the paths of are determined by , since the realization of decides which Markov kernel ( or ) generates . If the realization is equal to , then an adverse event occurs almost surely at a (finite) random time , the distribution of which is dependent on the realization of the path .

The decision-maker’s ultimate goal is to sequentially observe , and infer before the adverse event happens; inference is obsolete if it is declared after . Since is latent, the decision-maker is unaware whether the adverse event will occur or not, i.e. whether her access to is temporary ( for ) or permanent ( for ). In order to model the occurrence of the adverse event; we define as an -stopping time for the process , for which we assume the following:

•

The stopping time is finite almost surely, whereas is infinite almost surely, i.e. , and .

•

The stopping time is accessible222Our analyses hold if the stopping time is totally inaccessible., with a Markovian dependency on history, i.e. , where is an injective map from to and is non-decreasing in .

Thus, unlike the stochastic deadline models in [10] and [15], the decision deadline in our model (i.e. occurrence of the adverse event) is context-dependent as it depends on the time series realization (i.e. is not independent of as in [15]). We use the notation where to denote the stopped process to which the decision-maker has access. Throughout the paper, the measures and assign probability measures to the paths and respectively, and we assume that 333The absolute continuity of with respect to means that no sample path of should be fully revealing of the realization of ..

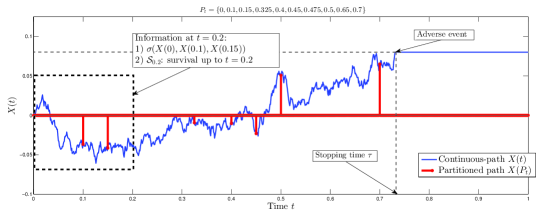

Information The decision-maker can only observe a set of (costly) samples of rather than the full continuous path. The samples observed by the decision-maker are captured by partitioning over specific time intervals: we define with , as a size- partition of over the interval , where is the total number of samples in the partition . The decision-maker observes the values that takes at the time instances in ; thus the sequence of observations is given by the process where is the Dirac measure. The space of all partitions over the interval is denoted by . We denote the probability measures for partitioned paths generated under and with a partition as and respectively.

Figure 1: An exemplary stopped sample path for , with an exemplary partition .

Since the decision-maker observes through the partition , her information at time is conveyed in the -algebra . The stopping event is observable by the decision-maker even if . We denote the -algebra generated by the stopping event as . Thus, the information that the decision-maker has at time is expressed by the filtration , and it follows that any decision-making policy needs to be -measurable.

Figure 1 depicts a Brownian path (a sample path of a Wiener process, which satisfies all the assumptions of our model)444In Figure 1, the stopping event was simulated as a totally inaccessible first jump of a Poisson process., with an exemplary partition over the time interval . The decision-maker observes the samples in sequentially, and reasons about the realization of the latent variable based on these samples and the process survival, i.e. at , the decision-maker’s information resides in the -algebra generated by the samples in , and the -algebra generated by the process’ survival .

Policies and Risks The decision-maker’s goal is to come up with a (timely) decision , that reflects her prediction for whether the actual realization is or , before the process potentially stops at the unknown time . The decision-maker follows a policy: a (continuous-time) mapping from the observations gathered up to every time instance to two types of actions:

•

A sensing action : if , then the decision-maker decides to observe a new sample from the running process at time .

•

A continuation/stopping action : if , then the decision-maker decides to stop gathering samples from , and declares a final decision (estimate) for . Whenever the decision-maker continues observing and postpones her declaration for the estimate of .

A policy is a (-measurable) mapping rule that maps the information in to an action tuple at every time instance . We assume that every single observation that the decision-maker draws from entails a fixed cost, hence the process has to be a point process under any optimal policy555Note that the cost of observing any local continuous path is infinite, hence any optimal policy must have being a point process to keep the number of observed samples finite.. We denote the space of all such policies by .

A policy generates the following random quantities as a function of the paths on the probability space :

1- A stopping time : The first time at which the decision-maker declares its estimate for , i.e. .2- A decision (estimate of ) : Given by .3- A random partition : A realization of the point process , comprising a finite set of strictly increasing -stopping times at which the decision-maker decides to sample the path .

A loss function is associated with every realization of the policy , representing the overall cost incurred when following that policy for a specific path . The loss function is given by

(1)

where is the cost of type I error (failure to anticipate the adverse event), is the cost of type II error (falsely predicting that an adverse event will occur), is the cost of the delay in declaring the estimate , is the cost incurred when the adverse event occurs before an estimate is declared (cost of missing the deadline), and is the cost of every observation sample (cost of information). The risk of each policy is defined as its expected loss

(2)

where the expectation is taken over the paths of . In the next section, we characterize the structure of the optimal policy .

3 Structure of the Optimal Policy

Since the decision-maker’s posterior belief at time , defined as , is an important statistic for designing sequential policies [10, 21-22], we start our characterization for by investigating the belief process .

3.1 The Posterior Belief Process

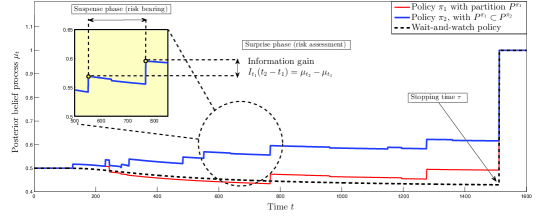

Figure 2: Depiction for exemplary belief paths of different policies under .

Recall that the decision-maker distills information from two types of observations: the realization of the partitioned time series (i.e. the information in ), and 2) the survival of the process up to time (i.e. the information in ). In the following Theorem, we study the evolution of the decision-maker’s beliefs as she integrates these pieces of information over time666All proofs are provided in the supplementary material.

Theorem 1 (Information and beliefs). Every posterior belief trajectory associated with a policy that creates a partition of is a càdlàg path given by

where is the Radon-Nikodym derivative777Since we impose the condition and fix a partition , then the Radon-Nikodym derivative exists. of the measure with respect to , and is given by the following elementary predictable process

for and for . Moreover, the path has exactly jumps at the time indexes in .

Proof: The posterior belief process is given by

(3)

where we have used the fact that in (a), and the fact that the event is -measurable in (b), and hence . Therefore, we can write the posterior belief process in the following form

Now we focus on computing . Note that using Bayes’ rule, we have that

(4)

where the existence of the Radon-Nykodim derivative follows from the fact that . Hence, we have that

Now we focus on evaluating . Using a further application of Bayes’ rule we have that

(5)

where we have used the fact that . For any partition , the likelihood ratio is an elementary predictable process that takes an initial value that is equal to the prior (when no samples are initially observed), and then takes constant values of in the interval between any two samples in the partition (only when a new sample is observed, the likelihood is updated). Hence, we have that

The process is predictable since the likelihood remains constant as long as no new samples are observed. Modulated by the survival probability, can be written as

Under usual regularity conditions on it is easy to see that will have jumps only at the time instances in the partition and at the stopping time , i.e. a total of jumps at the time indexes in .

Theorem 1 says that every belief path is right-continuous with left limits, and has jumps at the time indexes in the partition , whereas between each two jumps, the paths are predictable (i.e. they are known ahead of time once we know the magnitudes of the jumps preceding them). This means that the decision-maker obtains ”active” information by probing the time series to observe new samples (i.e. the information in ), inducing jumps that revive her beliefs, whereas the progression of time without witnessing a stopping event offers the decision-maker ”passive information” that is distilled just from the costless observation of the process’ survival. Both sources of information manifest themselves in terms of the likelihood ratio, and the survival probability in the expression of above.

In Figure 2, we plot the càdlàg belief paths for policies and where (i.e. policy observe a subset of the samples observed by ). We also plot the (predictable) belief path of a wait-and-watch policy that observes no samples. We can see that , which has more jumps of ”active information”, copes faster with the truthful belief over time. Between each two jumps, the belief process exhibits a non-increasing predictable path until fed with a new piece of information. The wait-and-watch policy has its belief drifting away from the prior towards the wrong belief since it only distills information from the process survival, which favors the hypothesis . This discussion motivates the introduction of the following key quantities.

Information gain (surprise) : The amount of drift in the decision-maker’s belief at time with respect to her belief at time , given the information available up to time , i.e. .Posterior survival function (suspense) : The probability that a process generated with survives up to time given the information observed up to time , i.e. . The function is a non-increasing function in i.e. .

That is, the information gain is the amount of “surprise” that the decision-maker experiences in response to a new information sample expressed in terms of the change in here belief, i.e. the jumps in , whereas the survival probability (suspense) is her assessment for the risk of having the adverse event taking places in the next time interval. As we will see in the next subsection, the optimal policy would balance the two quantities when scheduling the times to sense .

We conclude our analysis for the process by noting that the lack of information samples creates bias towards the belief that (e.g. see the belief path of the wait-and-watch policy in Figure 2). We formally express this behavior in the following Corollary.

Corollary 1 (Leaning towards denial). For every policy , the posterior belief process is a supermartingale with respect to , where

Proof: Recall that from Theorem 1, we know that the posterior belief process can be written as

Hence, the expected posterior belief at time given the information in the filtration can be written as

(6)

and hence can be written as

which is equivalent to

(7)

Furthermore, the term in the expression above can be expressed as

(8)

Therefore, can be written as

(9)

Now it remains to evaluate the term in order to find . We first note that

We start evaluating the above by first looking at the term . Using Bayes’ rule, we have that

(10)

where can be expanded using successive applications of Bayes’ rule as

which is equivalent to

(11)

Similarly, it is easy to see that

(12)

where again, we have used the fact that .

Now we re-formulate (10) using Bayes rule to arrive at the following

(13)

then using (11) and (12), (13) can be further reduced to

(14)

Finally, we use the expression in (14) to evaluate the term as follows

and hence the posterior belief process is a supermartingale with respect to the filtration .

Thus, unlike classical Bayesian learning models with a belief martingale [18, 21-23], the belief process in our model is a supermartingale that leans toward decreasing over time. The reason for this is that in our model, time conveys information. That is, unlike [10] and [15] where the decision deadline is hypothesis-independent and is almost surely occurring in finite time for any path, in our model the occurrence of the adverse event is itself a hypothesis, hence observing the survival of the process is informative and contributes to the evolution of the belief. The informativeness of both the acquired information samples and process survival can be disentangled using Doob decomposition, by writing as where is a martingale, capturing the information gain from the acquired samples, and is a predictable compensator process [23], capturing information extracted from the process survival.

3.2 The Optimal Policy

The optimal policy minimizes the expected risk as defined in (1) and (2) by generating the tuple of random processes in response to the paths of on in a way that ”shapes” a belief process that maximizes informativeness, maintains timeliness and controls cost. In the following, we introduce the notion of a ”rendezvous policy”, then in Theorem 2, we show that the optimal policy complies with this definition.

Rendezvous policies We say that a policy is a rendezvous policy, if the random partition constructed by the sequence of sensing actions , is a point process with predictable jumps, where for every two consecutive jumps at times and , with and , we have that is -measurable.

That is, a rendezvous policy is a policy that constructs a sensing schedule , such that every time at which the decision-maker acquires information is actually computable using the information available up to time , the previous time instance at which information was gathered. Hence, the decision-maker can decide the next ”date” in which she will gather information directly after she senses a new information sample. This structure is a natural consequence of the information structure in Theorem 1, since the belief paths between every two jumps are predictable, then they convey no ”actionable” information, i.e. if the decision-maker was to respond to a predictable belief path, say by sensing or making a stopping decision, then she should have taken that decision right before the predictable path starts, which leads her to better off by saving the delay cost . We denote the space of all rendezvous policies by . In the following Theorem, we establish that the rendezvous structure is optimal.

Theorem 2 (Rendezvous). The optimal policy is a rendezvous policy ().

Proof: Assume a discrete-time version of the problem, where the decision are made in time steps Define a value function as a map from the current history to the risk of the best policy given the history as follows:

and define the action-value function as the value function

achieved by taking actions andthen following the best policy thereafter. That is, when the decision is to continue (i.e. ), we have that

and

Based on Bellman s optimality principle [24], we know that the optimal policy has to satisfy the following in every time step, i.e.

Now let us look at the optimal partition on on the discrete time steps , and look at an arbitrary realization for . Then we pick two consecutive time indexes in , say and , with , for which , and . Since the policy is optimal, we know that

and

which is equivalent to

and

which can be further decomposed into

and

since both functions and are -measurable, then the decision-maker can compute the optimal decision sequence at time . Since this holds for an arbitrary discretization step , including an arbitrarily small step , it follows that the sensing actions construct a predictable point process under the optimal policy, which concludes the Theorem.

A direct implication of Theorem 2 is that the time variable can now be viewed as a state variable, whereas the problem is virtually solved in ”discrete-time” since the decision-maker effectively jumps from one time instance to another in a discrete manner. Hence, we alter the definition of the action from an indicator variable that indicates sensing the time series at time , to a ”rendezvous action” that takes real values, and specifies the time after which the decision-maker would sense a new sample, i.e. if then the decision-maker gathers the new sample at . This transformation restricts our policy design problem to the space of rendezvous policies , which we know from Theorem 2 that it contains the optimal policy (i.e. ).

Having established the result in Theorem 2, in the following Theorem, we characterize the optimal policy in terms of the random process using discrete-time Bellman optimality conditions [24].

Theorem 3 (The optimal policy). The optimal policy is a sequence of actions resulting in a random process with the following properties:

(Continuation and stopping)

1.

The process is a Markov sufficient statistic for the distribution of , where is the most recent sample in the partition , i.e. .

2.

The policy recommends continuation, i.e. , as long as the belief where is a time and context-dependent continuation set with the following properties: and .

(Rendezvous and decisions)

1.

Whenever and , then a rendezvous is set as follows

where .

2.

Whenever then a decision is issued, and is based on a belief threshold as follows: The stopping time is given by .

Proof: We start by proving that the optimal decision rule is Fix an optimal stopping time and an optimal partition The optimal decision rule is given by

which is equivalent to

which by smoothing can be written as

and hence we have that

Since the terms , , and are the information and delay costs, which do not depend on the choice of , we have that

which can be reduced to the following

(16)

Since is an -measurable function, we have that

(17)

which is simply minimized by setting whenever , hence we have that .

Now we resume by first defining the value and the action-value functions, and find the policy characteristics under Bellman optimality conditions.

Define a value function as a map from the current history to the risk of the best policy given the history as follows:

and define the action-value function as the value function

achieved by taking actions and then following the best policy thereafter, i.e.

Bellman optimality condition requires that at any time step , we have

Recall from the proof of Corollary 1 that the belief process follows the following dynamics

which depends only on and the most recent sample realization in the partition , which we denote as . Hence, the tuple is a Markov process since is Markovian, and the belief process follows the above Markovian dynamics, and time is deterministic. Since the survival probability depends only on , we can write the action-value function as

and consequently, the optimal actions at every time step following Bellman conditions are given by

Hence, at any time step , we only need to know the tuple in order to compute the optimal action-value function, and hence, on the path to the optimal policy, knowing only suffice to generate the random process Hence, is a Markov sufficient statistic for

Note that our proof for the optimal decision rule implies that the action-value function for stopping at time , i.e. is

whereas the continuation cost at any time step is given by finding the optimal rendezvous time . Therefore, the optimal action-value at any time step is given by

The equation above determines the stopping and continuation conditions, and using the monotonicity of the survival function in both time and the time series realizations we can show the monotonicity of the continuation set using the same arguments of Theorem 1 in [15].

The optimal rendezvous can be found by optimizing the time interval such that the cost of stopping in the next time step is minimized. Hence, we have that

(18)

where can be written as where is the information gain.

Theorem 3 establishes the structure of the optimal policy and its prescribed actions in the decision-maker’s state-space. The first part of the Theorem says that in order to generate the random tuple optimally, we only need to keep track of the realization of the process in every time instance. That is, an optimal policy maps the current belief, the current time, and the most recently observed realization of the time series to an action tuple , i.e. a decision on whether to stop and declare an estimate for or sense a new sample. Hence, the process represents the ”state” of the decision-maker, and the decision-maker’s actions can partially influence the state through the belief process, i.e. a decision on when to acquire the next sample affects the distributional properties of the posterior belief. The remaining state variables and are beyond the decision-maker’s control.

We note that unlike the previous models in [9-16], with the exception of [17], a policy in our model is context-dependent. That is, since the state is and not just the time-belief tuple , a policy can recommend different actions for the same belief and at the same time but for a different context. This is because, while captures what the decision-maker learned from the history, captures her foresightedness into the future, i.e. it can be that the belief is not decisive (e.g. ), but the context is ”risky” (i.e. is large), which means that a potential forthcoming adverse event is likely to happen in the near future, hence the decision-maker would be more eager to make a stopping decision and declare an estimate . This is manifested through the dependence of the continuation set on both time and context; the continuation set is monotonically decreasing in time due to the deadline pressure, and is also monotonically decreasing in due to the dependence of the deadline on the time series realization.

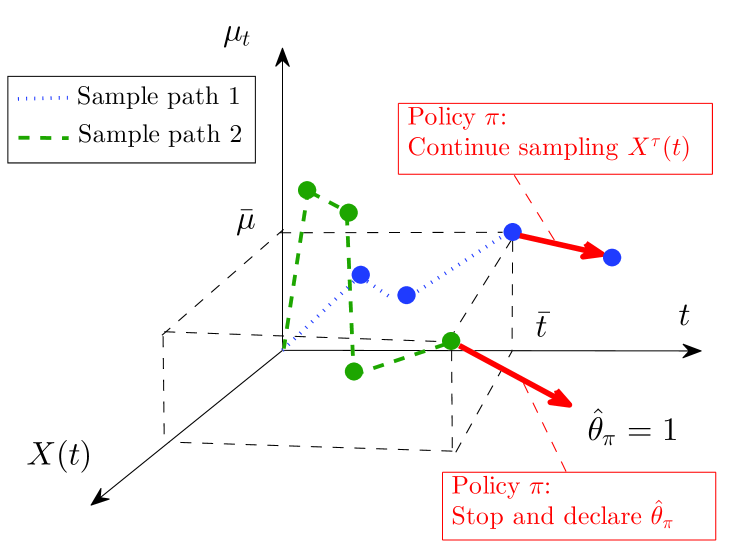

The context dependence of the optimal policy is pictorially depicted in Figure 3 where we show two exemplary trajectories for the decision-maker’s state, and the actions recommended by a policy for the same time and belief, but a different context, i.e. a stopping action recommended when is large since it corresponds to a low survival probability, whereas for the same belief and time, a continuation action can be recommended if is low since it is safer to keep observing the process for that the survival probability is high. Such a prescription specifies optimal decision-making in context-driven settings such as clinical decision-making in critical care environment [3-5], where a combination of a patient’s length of hospital stay (i.e. ), clinical risk score (i.e. ) and current physiological test measurements (i.e. ) determine the decision on whether or not a patient should be admitted to an intensive care unit.

Figure 3: Context-dependence of the decision-making policy . For the same belief and time pair (), different actions are recommended in different contexts (different sample paths).

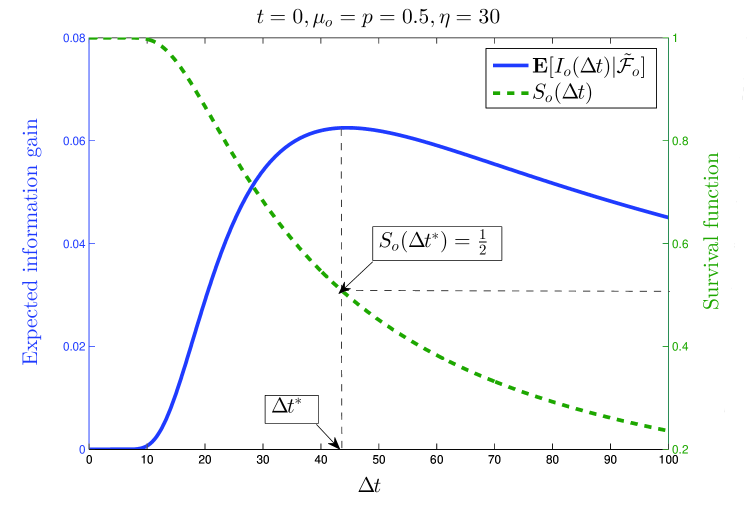

Figure 4: Surprise-suspense trade-off.

The second part of Theorem 3 says that whenever the optimal policy decides to stop gathering information and issue a conclusive decision, it imposes a threshold on the posterior belief, based on which it issues the estimate ; the threshold is , and hence weights the estimates by their respective risks. When the policy favors continuation, it issues a rendezvous action, i.e. the next time instance at which information will be gathered. This rendezvous balances surprise and suspense: the decision-maker prefers maximizing surprise in order to draw the maximum informativeness from the costly sample it will acquire; this is captured in terms of the tail distribution of the information gain . Maximizing surprise may increase suspense, i.e. the probability of process termination, which is controlled by the survival function , and hence it can be that harvesting the maximum informativeness entails a survival risk when is high. Therefore, the optimal policy selects a rendezvous that optimizes a combination of the survival risk survival, captured by the cost and the survival function , and the value of information, captured by the costs and the information gain .

To get a feel of the surprise-suspense trade-off, we assume that is a standard Brownian motion, and the prior on is , whereas the stopping time is the hitting time of a target level . When should the decision-maker set the date for the first rendezvous? In Figure 4, we plot the expected information gain from the first sample () (solid line), and the corresponding survival function (dotted line). It can be seen that the expected information gain is maximum at but with a survival probability, hence depending on the costs and , the optimal policy may favor an earlier rendezvous (i.e. ) in order to keep the survival probability within a reasonable limit and at the same time attain a reasonable level of informativeness.

4 Conclusions

We developed a model for decision-making with endogenous information acquisition under time pressure, where a decision-maker needs to issue a conclusive decision before an adverse event (potentially) takes place. We have shown that the optimal policy has a ”rendezvous” structure, i.e. the optimal policy sets a ”date” for gathering a new sample whenever the current information sample is observed. The optimal policy selects the time between two information samples such that it balances the information gain (surprise) with the survival probability (suspense). Moreover, we characterized the optimal policy’s continuation and stopping conditions, and showed that they depend on the context and not just on beliefs. Our model can help understanding the nature of optimal decision-making in settings where timely risk assessment and information gathering is essential.

5 Acknowledgements

This work was supported by the Office of Naval Research (ONR) and the NSF (Grant number: ECCS 1462245).

References

[1] Balci, F., Freestone, D., Simen, P., de Souza, L., Cohen, J. D., & Holmes, P. (2011) Optimal temporal risk assessment, Frontiers in Integrative Neuroscience, 5(56), 1-15.

[2] Banerjee, T. & Veeravalli, V. V. (2012) Data-efficient quickest change detection with on off observation control, Sequential Analysis, 31(1), 40-77.

[3] Wiens, J., Horvitz, E., & Guttag, J. V. (2012) Patient risk stratification for hospital-associated c. diff as a time-series classification task, In Advances in Neural Information Processing Systems, pp. 467-475.

[4] Schulam, P., & Saria, S. (2015) A Framework for Individualizing Predictions of Disease Trajectories by Exploiting Multi-resolution Structure, In Advances in Neural Information Processing Systems, pp. 748-756.

[5] Chalfin, D. B., Trzeciak, S., Likourezos, A., Baumann, B. M., Dellinger, R. P., & DELAY-ED study group. (2007) Impact of delayed transfer of critically ill patients from the emergency department to the intensive care unit, Critical care medicine, 35(6), pp. 1477-1483.

[6] Bortfeld, T., Ramakrishnan, J., Tsitsiklis, J. N., & Unkelbach, J. (2015) Optimization of radiation therapy fractionation schedules in the presence of tumor repopulation, INFORMS Journal on Computing, 27(4), pp. 788-803.

[7] Shapiro, S., et al., (1998) Breast cancer screening programmes in 22 countries: current policies, administration and guidelines, International journal of epidemiology, 27(5), pp. 735-742.

[8] Wald, A., Sequential analysis, Courier Corporation, 1973.

[9] Khalvati, K., & Rao, R. P. (2015) A Bayesian Framework for Modeling Confidence in Perceptual Decision Making, In Advances in neural information processing systems, pp. 2404-2412.

[10] Dayanik, S., & Angela, J. Y. (2013) Reward-Rate Maximization in Sequential Identification under a Stochastic Deadline, SIAM J. Control Optim., 51(4), pp. 2922 2948.

[11] Zhang, S., & Angela, J.Y. (2013) Forgetful Bayes and myopic planning: Human learning and decision-making in a bandit setting, In Advances in neural information processing systems, pp. 2607-2615.

[12] Shenoy, P., & Angela, J.Y. (2012) Strategic impatience in Go/NoGo versus forced-choice decision-making, In Advances in neural information processing systems, pp. 2123-2131.

[13] Drugowitsch, J., Moreno-Bote, R., & Pouget, A. (2014) Optimal decision-making with time-varying evidence reliability, In Advances in neural information processing systems, pp. 748-756.

[14] Yu, A. J., Dayan, P., & Cohen, J. D. (2009) Dynamics of attentional selection under conflict: toward a rational Bayesian account, Journal of Experimental Psychology: Human Perception and Performance, 35(3), 700.

[15] Frazier, P. & Angela, J. Y. (2007) Sequential hypothesis testing under stochastic deadlines, In Advances in Neural Information Processing Systems, pp. 465-472.

[16] Drugowitsch, J., Moreno-Bote, R., Churchland, A. K., Shadlen, M. N., & Pouget, A. (2012) The cost of accumulating evidence in perceptual decision making, The Journal of Neuroscience, 32(11), 3612-3628.

[17] Shvartsman, M., Srivastava, V., & Cohen J. D. (2015) A Theory of Decision Making Under Dynamic Context, In Advances in Neural Information Processing Systems, pp. 2476-2484. 2015.

[18] Ely, J., Frankel, A., & Kamenica, E. (2015) Suspense and surprise, Journal of Political Economy, 123(1), pp. 215-260.

[19] Itti, L., & Baldi, P. (2005) Bayesian Surprise Attracts Human Attention, In Advances in Neural Information Processing Systems, pp. 547-554.

[20] Bogacz, R., Brown, E., Moehlis, J., Holmes, P. J., & Cohen J. D. (2006) The physics of optimal decision making: A formal analysis of models of performance in two-alternative forced-choice tasks, Psychological Review, 113(4), pp. 700 765.

[21] Peskir, G., & Shiryaev, A. (2006) Optimal stopping and free-boundary problems, Birkh user Basel.

[22] Shiryaev, A. N. (2007) Optimal stopping rules (Vol. 8). Springer Science & Business Media.

[23] Shreve, Steven E. (2004) Stochastic calculus for finance II: Continuous-time models (Vol. 11), Springer Science & Business Media, 2004.

[24] Bertsekas, D. P., & Shreve, S. E. Stochastic optimal control: The discrete time case (Vol. 23), New York: Academic Press, 1978.