Convergence of the Euler-Maruyama method for multidimensional SDEs with discontinuous drift and degenerate diffusion coefficient

Abstract

We prove strong convergence of order for arbitrarily small of the Euler-Maruyama method for multidimensional

stochastic differential equations (SDEs) with discontinuous drift and degenerate diffusion coefficient.

The proof is based on estimating the difference between the Euler-Maruyama scheme and another numerical method, which is constructed by applying the Euler-Maruyama scheme to a transformation of the SDE we aim to solve.

Keywords: stochastic differential equations, discontinuous drift, degenerate diffusion, Euler-Maruyama method, strong convergence rate

Mathematics Subject Classification (2010): 60H10, 65C30, 65C20 (Primary), 65L20 (Secondary)

1 Introduction

We consider time-homogeneous stochastic differential equations (SDEs) of the form

| (1) |

where is the initial value, is the drift and is the diffusion coefficient.

The Euler-Maruyama approximation with step-size of the solution to (1) is given by

| (2) |

with for , . In particular, for , we have

For Lipschitz, Itô [9] proved existence and uniqueness of the solution of (1).

In this case the Euler-Maruyama method (2) converges with strong order to the true solution,

see [12, Theorem 10.2.2]. Higher order algorithms exist, but require stronger conditions on the coefficients.

In applications, frequently SDEs with less regular coefficients appear.

For example in stochastic control theory, whenever the optimal control is of bang-bang type, meaning that the strategy is of the form for a measurable set , the drift of the controlled dynamical system is discontinuous.

Furthermore, there are models which involve only noisy observations of a signal that

has to be filtered. After applying filtering theory the diffusion coefficient

typically is degenerate in the sense that , for some .

This motivates the study of SDEs with these kind of irregularities in the coefficients.

If is bounded and measurable, and is bounded, Lipschitz, and uniformly non-degenerate, i.e. if there exists a constant such that for all and all it holds that , Zvonkin [30] and Veretennikov [26, 27] prove existence and uniqueness of a solution. Veretennikov [28] extends these results by allowing a part of the diffusion to be degenerate.

In [17] existence and uniqueness of a solution for the case where the drift is

discontinuous at a hyperplane, or a special hypersurface and where the diffusion coefficient is degenerate is proven,

and in [24] it is shown how these results extend to the non-homogeneous case.

Currently, research on numerical methods for SDEs with irregular coefficients is highly active. Hutzenthaler et al. [8] introduce the tamed Euler-Maruyama scheme and prove strong order convergence for SDEs with continuously differentiable and polynomially growing drift that satisfy a one-sided Lipschitz condition. Sabanis [23] proves strong convergence of the tamed Euler-Maruyama scheme from a different perspective and also considers the case of locally Lipschitz diffusion coefficient. Gyöngy [4] proves almost sure convergence of the Euler-Maruyama scheme for the case where the drift satisfies a monotonicity condition.

Halidias and Kloeden [7] show that the Euler-Maruyama scheme converges strongly for SDEs with a discontinuous monotone drift coefficient. Kohatsu-Higa et al. [13] show weak convergence with rates smaller than 1 of a method where they first regularize the discontinuous drift and then apply the Euler-Maruyama scheme. Étoré and Martinez [1, 2] introduce an exact simulation algorithm for one-dimensional SDEs with a drift coefficient which is discontinuous in one point, but differentiable everywhere else. For one-dimensional SDEs with piecewise Lipschitz drift and possibly degenerate diffusion coefficient, in [14] an existence and uniqueness result is proven, and a numerical method, which is based on applying the Euler-Maruyama scheme to a transformation of (1), is presented. This method converges with strong order . In [15] a (non-trivial) extension of the method is introduced, which converges with strong order also in the multidimensional case. The paper also contains an existence and uniqueness result for the multidimensional setting under more general conditions than, e.g., the ones stated in [17].

The method introduced in [15] is the first numerical method that is proven to converge with positive strong rate for multidimensional SDEs with discontinuous drift and degenerate diffusion coefficient. It requires application of a transformation and its numerical inverse in each step, which makes the method rather slow in practice. Furthermore, the method requires specific inputs about the geometry of the discontinuity of the drift to calculate this transformation. This is a drawback, if, e.g., the method shall be applied for solving control problems, since the control is usually not explicitly known. So a method is preferred that can deal with the discontinuities in the drift automatically.

First results in this direction are contained in a series of papers by Ngo and Taguchi. In [22] they show convergence of order up to of the Euler-Maruyama method for multidimensional SDEs with discontinuous bounded drift that satisfies a one-sided Lipschitz condition and with Hölder continuous, bounded, and uniformly non-degenerate diffusion coefficient. In [20] they extend this result to cases where the drift is not necessarily one-sided Lipschitz for one-dimensional SDEs, and in [21] they extend the result for one-dimensional SDEs by allowing for discontinuities also in the diffusion coefficient. For many applications, their results fail to be applicable, since they only hold for one-dimensional SDEs and their method of proof relies on uniform non-degeneracy of the diffusion coefficient.

Contrasting the above, there are several delimiting results which

state that even equations with infinitely often differentiable coefficients

cannot always be solved approximately in finite time, even if the

Euler-Maruyama method converges,

cf. Hairer et al. [6], Jentzen et al. [10], Müller-Gronbach and Yaroslavtseva [19], Yaroslavtseva [29].

However, there is still a big gap between the assumptions on the coefficients

under which convergence with strong convergence rate has been proven and the

properties of the coefficients of the equation presented in

[6].

In this paper we prove strong convergence of order for arbitrarily small of the Euler-Maruyama method for multidimensional SDEs with discontinuous drift satisfying a piecewise Lipschitz condition and with a degenerate diffusion coefficient. Note that we do not impose a one-sided Lipschitz condition on the drift. So even for SDEs with non-degenerate diffusion coefficient, which do not have a one-sided Lipschitz drift, this result is novel.

Our convergence proof is based on estimating the difference between the Euler-Maruyama scheme and the scheme presented in [15]. Close to the set of discontinuities of the drift, we have no tight estimate of this difference, so we need to study the occupation time of an Itô process with degenerate diffusion coefficient there. Away from the set of discontinuities, it is essential to estimate the probability that during one step the distance between the interpolation of the Euler-Maruyama method and the previous Euler-Maruyama step becomes greater than some threshold.

This paper’s result is the first one that gives strong convergence and also a strong convergence rate of a fully explicit scheme for multidimensional SDEs with discontinuous drift and degenerate diffusion coefficient, and the first one for multidimensional SDEs with discontinuous drift that does not satisfy a one-sided Lipschitz condition.

2 Preliminaries

In this section we first state the assumptions on the coefficients of SDE (1), under which the result of this paper is proven, then we study the occupation time of an Itô process close to a hypersurface, and finally we recall the transformation from [15], which is also essential for our proof.

2.1 Definitions and assumptions

We want to prove strong convergence of the Euler-Maruyama method for SDEs with discontinuous drift coefficient. Instead of the usual requirement of Lipschitz continuity we only assume that the drift is a piecewise Lipschitz function on the .

Definition 2.1 ([15, Definitions 3.1 and 3.2]).

Let .

-

1.

For a continuous curve , let denote its length,

The intrinsic metric on is given by

where , if there is no continuous curve from to .

-

2.

Let be a function. We say that is intrinsic Lipschitz, if it is Lipschitz w.r.t. the intrinsic metric on , i.e. if there exists a constant such that

The prototypical examples for intrinsic Lipschitz function are given, like in the one-dimensional case, by differentiable functions with bounded derivative.

Lemma 2.2 ([15, Lemma 3.8]).

Let be open and let be a differentiable function with . Then is intrinsic Lipschitz with Lipschitz constant .

Definition 2.3 ([15, Definition 3.4]).

A function is piecewise Lipschitz, if there exists a hypersurface with finitely many connected components and with the property, that the restriction is intrinsic Lipschitz. We call an exceptional set for , and we call

the piecewise Lipschitz constant of .

In this paper will be a fixed -hypersurface, and we will only consider piecewise Lipschitz functions with exceptional set . In the following, denotes the piecewise Lipschitz constant of a function , if is piecewise Lipschitz, and it denotes the Lipschitz constant, if is Lipschitz.

We define the distance between a point and the hypersurface by , and for every we define .

Recall that, since , for every there exists an open environment of and a continuously differentiable function such that for every the vector has length 1 and is orthogonal to the tangent space of in . On a given connected open subset of the local unit normal vector is unique up to a factor .

We recall a definition from differential geometry.

Definition 2.4.

Let be any set.

-

1.

An environment is said to have the unique closest point property, if for every with there is a unique with . Therefore, we can define a mapping assigning to each the point in closest to .

-

2.

is said to be of positive reach, if there exists such that has the unique closest point property. The reach of is the supremum over all such if such an exists, and 0 otherwise.

Now, we give assumptions which are sufficient for the results in [15] to hold and which we need to prove the main result here.

Assumption 2.1.

We assume the following for the coefficients of (1):

-

1.

and are bounded;

-

2.

the diffusion coefficient is Lipschitz;

-

3.

the drift coefficient is a piecewise Lipschitz function . Its exceptional set is a -hypersurface of positive reach and every unit normal vector of has bounded second and third derivative;

-

4.

non-parallelity condition: there exists a constant such that for all ;

-

5.

the function defined by

(3) is and all derivatives up to order three are bounded.

Theorem 2.5 ([15, Theorem 3.21]).

Remark on Assumption 2.1:

-

1.

For existence and uniqueness of a solution to (1), in [15, Theorem 3.21] instead of Assumption 2.1.1 only boundedness in an -environment of is needed. However, for the proof of our convergence result we require global boundedness. Note that other results in the literature on numerical methods for SDEs with discontinuous drift also rely on boundedness of the coefficients, cf. [20, 21, 22].

-

2.

Assumption 2.1.2 is a technical condition; the focus in this paper is on other types of irregularities in the coefficients. There are results in the literature, where the authors deal with a non-globally Lipschitz diffusion coefficient, see, e.g., [5], but in contributions where only Hölder continuity is required for , usually uniform non-degeneracy is assumed.

- 3.

-

4.

Assumption 2.1.4 means that the diffusion coefficient must have a component orthogonal to in all . This condition is significantly weaker than uniform non-degeneracy, and it is essential: in [17] we give a counterexample for the case where the non-parallelity condition does not hold. Then, even existence of a solution is not guaranteed.

-

5.

Assumption 2.1.5 is a technical condition, which is required for our transformation method to work. Boundedness of and is needed for proving the local invertibility of our transform. Existence and boundedness of and is required for the multidimensional version of Itô’s formula to hold for the transform, see [15].

Moreover, it has been shown in [15, Proposition 3.13] that is a well-defined function on , i.e. it does not depend on the choice of the normal vector and, in particular, on its sign.

Example 2.6.

Suppose is the finite and disjoint union of orientable compact -manifolds. Then is of positive reach by the lemma in [3], and each connected component of separates the into two open connected components by the Jordan-Brouwer separation theorem, see [18].

Thus is the union of finitely many disjoint open connected subsets of ; we can write .

Suppose there exist bounded and Lipschitz -functions such that , and suppose that is bounded, Lipschitz, and with for every .

Then it is readily checked that and satisfy Assumption 2.1.

2.2 Occupation time close to a hypersurface

In this section we study the occupation time of an Itô process close to a -hypersurface. In the proof of our main theorem, the Euler-Maruyama approximation in equation (2) will play the role of that Itô process.

Theorem 2.7.

Let be a -hypersurface of positive reach and let be such that the closure of has the unique closest point property. Let further be an -valued Itô process

with progressively measurable processes , , where is -valued and is -valued. Let the coefficients be such that

-

1.

there exists a constant such that for almost all it holds that

-

2.

there exists a constant such that for almost all it holds that

Then there exists a constant such that for all ,

For the proof we will construct a one-dimensional Itô process with the property that is close to , if and only if is close to . For the construction of we decompose the path of into pieces close to and pieces farther away. These pieces are then mapped to by using a signed distance of from and pasted together in a continuous way.

A signed distance to is locally given by , where is a local unit normal vector.

Lemma 2.8.

For all it holds that .

Proof.

Fix and consider the function defined by . By definition of the projection map , has a minimum in , such that . Hence from , we get . This implies , since is a scalar multiple of .

Using that for an , we compute

| (4) |

For with small we get

such that the directional derivative of in direction in is 1. From this and from (2.2) it follows that . This also holds for by the continuity of . ∎

The following lemma states that for any continuous curve in there is a continuous path of unit normal vectors, such that to every point of we can assign a signed distance in a continuous way.

Lemma 2.9.

Let be a continuous function. Then there exists such that

-

1.

is continuous;

-

2.

for all ;

-

3.

is orthogonal to in the point for all .

Proof.

For we denote the tangent space to in by . Let

The set is nonempty and its elements are bounded by . Let . There exists an open and connected subset such that , and a unit normal vector .

Since is open and is continuous, there exists such that . By the definition of there exists and continuous, with and for all .

Since is unique up to a factor , the mapping either coincides with or on . Without loss of generality we may assume that the former is the case. Thus we can extend continuously to by defining for all .

Now, if was strictly smaller than , then we could use the same mapping to extend continuously beyond , contradicting the definition of . ∎

We will need the following estimate on the local time of a one-dimensional Itô process.

Lemma 2.10.

Let be an Itô process with bounded and progressively measurable coefficients .

Then .

The claim is a special case of [20, Lemma 3.2]. We give a proof for the convenience of the reader.

Proof.

From the Meyer-Tanaka formula [11, Section 3.7, Eq. (7.9)] we have

Using the inequality we get

and, using Itô’s -isometry,

The claim now follows by applying the Cauchy-Schwarz-inequality and taking the supremum over all . ∎

We are ready to prove the result of this section.

Proof of Theorem 2.7.

Let . Define a mapping by

Note that and , so that .

Next we decompose the path of : let . In particular we have , if . For , define

By Lemma 2.9 there exist continuous , with and for all . Without loss of generality can be chosen such that . We construct a one-dimensional process as follows:

where without loss of generality the are chosen such that

| (5) |

Note that by construction both sides of (5) can only take the values .

We have thus constructed a continuous -valued process with the property that the occupation time of in an environment of is the same as the occupation time of in an environment of , i.e. , iff for all .

To show that is an Itô process, we want to use Itô’s formula. For this we recognize that , depending on its proximity to , is either constant or locally of the form for a suitable choice of the unit normal vector. Denote . The function is locally a signed distance to and . This can be seen by following the proof of [3, Theorem 1]. Hence, we may apply Itô’s formula to get

By Lemma 2.8 we have , and hence

Since and are bounded by construction, , is bounded (c.f. the remark on Assumption 2.1.3), and by Assumption 1 of the theorem, the coefficients of are uniformly bounded. Therefore , with bounded and progressively measurable .

Let . For all , we have . Thus by Assumption 2 of the theorem,

By the occupation time formula [11, Chapter 3, 7.1 Theorem] for one-dimensional continuous semimartingales, we get

∎

2.3 The transformation

The proof of convergence is based on a transformation that removes the discontinuity from the drift and makes the drift Lipschitz while preserving the Lipschitz property of the diffusion coefficient.

A suitable transform is presented in [15]. We recall it here.

Define ,

where is smaller than the reach of , see Assumption 2.1.3, is the function defined in Assumption 2.1.5, and

with positive constant and

If is chosen sufficiently small, see [15, Lemma 3.18], is invertible by [15, Theorem 3.14].

Furthermore, Itô’s formula holds for and by [15, Theorem 3.19].

By [16, Lemma 4], is bounded and piecewise Lipschitz with exceptional set .

Hence, [15, Lemma 3.6], [15, Lemma 3.8], and [15, Lemma 3.11] assure that is Lipschitz.

3 Main result

We are ready to formulate the main result.

Theorem 3.1.

In preparation of the proof of the main result, we prove two lemmas.

Lemma 3.2.

Proof.

For all and all , define

| (7) |

Lemma 3.3.

Proof.

where we applied Doob’s submartingal inequality, and in the last step used that . ∎

Now, we are ready to prove our main result.

Proof of Theorem 3.1.

Since is Lipschitz by the proof of [15, Theorem 3.20],

| (8) |

with as in (6). Let be the Euler-Maruyama approximation of . It holds that

| (9) |

For estimating the first term in (9), recall that by [15, Theorem 3.20], the transformed SDE (6) has Lipschitz coefficients. Since the Euler-Maruyama method converges with strong order for SDEs with Lipschitz coefficients (see [12, Theorem 10.2.2]), there exists a constant such that for sufficiently small ,

| (10) |

We now turn to the second term in (9), i.e. we estimate the difference between applied to the Euler-Maruyama approximation of and the Euler-Maruyama approximation of . Denote, for all ,

With we have by Itô’s formula,

so that

Applying the Cauchy-Schwarz inequality to the Lebesgue integrals and the -dimensional Burkholder-Davis-Gundy inequality [8, Lemma 3.7] to the Itô integrals, we obtain

| (11) |

For estimating in (11), we will use that

With this and the definition of in (7), we get

By Lemma 3.3, , and by Theorem 2.7, , for suitable constants . In order to minimize the bound on , we choose such that is minimized for sufficiently small, yielding for arbitrarily small . Hence, with , , , we get

Thus, with and for arbitrarily small fixed , it holds that for sufficiently small

| (12) |

4 Examples

We ran simulations for several examples – ones of theoretical interest as well as an example coming from applications.

When studying stochastic dynamical systems which include a noisy signal, then filtering this signal leads to a higher dimensional system with a degenerate diffusion coefficient. Stochastic control problems often lead to an optimal control policy which makes the drift of the system discontinuous. Examples are models with incomplete market information in mathematical finance where the rate with which cashflows are paid from a firm value process change systematically when the asset-liability ratio passes a certain threshold which then triggers a rating change.

The class of equations studied here appears frequently in several areas of applied mathematics and the natural sciences.

Step-function

In the first example the drift is the step function , and . It can easily be checked that these coefficients satisfy Assumption 2.1. In particular, note that the non-parallelity condition is trivially satisfied, since is uniformly non-degenerate. Since does not satisfy a one-sided Lipschitz condition, our result is the first one that gives a strong convergence rate of the Euler-Maruyama method for this example.

Discontinuity along the unit circle

Dividend maximization under incomplete information

In insurance mathematics, a well-studied problem is the maximization of the expected discounted future dividend payments until the time of ruin of an insurance company, a value which serves as a risk measure. In [25] the problem is studied in a setup that allows for incomplete information about the market. This leads to a joint filtering and stochastic optimal control problem, and after solving the filtering problem, the driving dynamics are high dimensional and have a degenerate diffusion coefficient. This issue is described in more detail in [25]. Solving the stochastic optimal control problem in dimensions higher than three with the usual technique (solving an associated partial differential equation) becomes practically infeasible. Therefore, one has to resort to simulation. The SDE that has to be simulated has the coefficients

where are known constants.

The arguments are elements of the simplex ,

and the corresponding processes stay within this simplex almost surely, see [25].

The function determines the hypersurface along which the drift is discontinuous: .

In our simulations we choose and affine linear, but note that we need not restrict ourselves

to affine linear .

We need to check Assumption 2.1: Since , are bounded, and all first order derivatives of the entries of are bounded. Hence, is Lipschitz. is piecewise Lipschitz, and since is affine linear, . Whether the non-parallelity condition holds depends on the choice of the parameters, but for ours the condition is satisfied. Assumption 2.1.5 can easily be checked. Note that the coefficients can be extended to the whole of in a way that they still satisfy our assumptions.

Error estimate

The -error is estimated by

where is the numerical approximation of with step size , is an estimator of the mean value using paths, and is a normalizing constant so that .

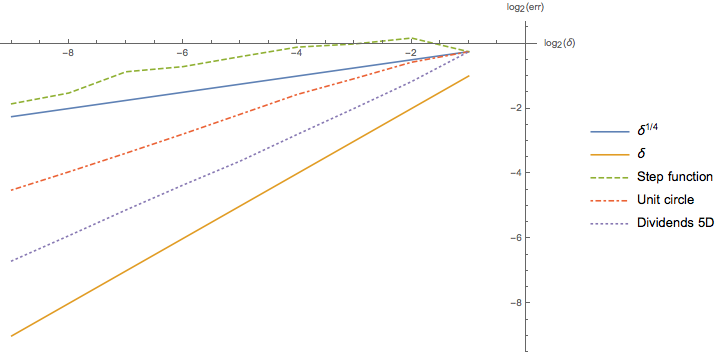

Figure 1 shows of the estimated -error of the Euler-Maruyama approximation of plotted over for the examples presented above.

We observe that the theoretical convergence rate is approximately obtained for the example of a step-function and that the other examples converge at a faster rate.

In particular, for the examples with degenerate diffusion coefficient, the convergence rate is not worse than for the other example.

Even for the step-function example, for sufficiently small step-size the convergence rate seems to be higher than the theoretical one.

Hence, it will be an interesting topic for future research to prove sharpness, or find a sharp bound.

Even though the proven rate for the Euler-Maruyama method is lower than for the transformation-based method from [15], the calculations are usually faster in practice using the first method, since the simulation of a single path is faster. Table 1 confirms this claim: we observe that computation times are higher by up to two orders of magnitude for the transformation method, while the estimated error is of comparable size.

| computation time | estimated error | |||

| EM | GM | EM | GM | |

| Step function | 10.84 | 86.92 | 0.1324 | 0.3362 |

| Unit circle | 14.39 | 5267.37 | 0.0195 | 0.0323 |

| Dividends 5D | 45.52 | 7398.97 | 0.0026 | 0.0032 |

For completeness, we remark that one can construct examples, where the transformation method is much faster while giving a smaller error. For example, start with prescribing the transform and set and . This leads to and . Hence, if we use the transformation method with the same , then and the transformation method gives the estimate , which is the exact solution.

Conclusion

In this paper we have for the first time proven strong convergence and also a positive strong convergence rate for an explicit method (the Euler-Maruyama method) for multidimensional SDEs with discontinuous drift that has a degenerate diffusion coefficient, or with a discontinuous drift that does not satisfy a one-sided Lipschitz condition, or both. The Euler-Maruyama method has the advantage that it does not need the exact form of the set of discontinuities of the drift as an input, and that in practice, computation of one path is fast in comparison to the second method in the literature that can deal with this class of SDEs. Our numerical experiments suggest that in addition to these advantages, it even seems that the Euler-Maruyama method converges at a higher than the theoretically obtained rate for many examples and it will be a topic of future research to prove sharpness, or find a sharp bound.

Acknowledgements

The authors thank Andreas Neuenkirch and Lukasz Szpruch for fruitful discussions that helped to improve the estimate in Lemma 3.3 and hence the obtained convergence rate and Thomas Müller-Gronbach for pointing out an inaccuracy in the definition of .

G. Leobacher is supported by the Austrian Science Fund (FWF): Project F5508-N26, which is part of the Special Research Program “Quasi-Monte Carlo Methods: Theory and Applications”. A part of this paper was written while G. Leobacher was member of the Department of Financial Mathematics and Applied Number Theory, Johannes Kepler University Linz, 4040 Linz, Austria.

M. Szölgyenyi is supported by the Vienna Science and Technology Fund (WWTF): Project MA14-031. Furthermore, M. Szölgyenyi is grateful for the AXA Research Grant “Numerical Methods for Stochastic Differential Equations with Irregular Coefficients with Applications in Risk Theory and Mathematical Finance”.

References

- Étoré and Martinez [2013] P. Étoré and M. Martinez. Exact Simulation for Solutions of One-Dimensional Stochastic Differential Equations Involving a Local Time at Zero of the Unknown Process. Monte Carlo Methods and Applications, 19(1):41–71, 2013.

- Étoré and Martinez [2014] P. Étoré and M. Martinez. Exact Simulation for Solutions of One-Dimensional Stochastic Differential Equations with Discontinuous Drift. ESAIM: Probability and Statistics, 18:686–702, 2014.

- Foote [1984] R. L. Foote. Regularity of the Distance Function. Proceedings of the American Mathematical Society, 92(1):153–155, 1984.

- Gyöngy [1998] I. Gyöngy. A Note on Euler’s Approximation. Potential Analysis, 8:205–216, 1998.

- Gyöngy and Rásonyi [2011] I. Gyöngy and M. Rásonyi. A Note on Euler’s Approximation for SDEs with Hölder Continuous Diffusion Coefficients. Stochastic Processes and their Applications, 121(10):2189–2200, 2011.

- Hairer et al. [2015] M. Hairer, M. Hutzenthaler, and A. Jentzen. Loss of Regularity for Kolmogorov Equations. The Annals of Probability, 43(2):468–527, 2015.

- Halidias and Kloeden [2008] N. Halidias and P. E. Kloeden. A Note on the Euler–Maruyama Scheme for Stochastic Differential Equations with a Discontinuous Monotone Drift Coefficient. BIT Numerical Mathematics, 48(1):51–59, 2008.

- Hutzenthaler et al. [2012] M. Hutzenthaler, A. Jentzen, and P. E. Kloeden. Strong Convergence of an Explicit Numerical Method for SDEs with Nonglobally Lipschitz Continuous Coefficients. The Annals of Applied Probability, 22(4):1611–1641, 2012.

- Itô [1951] K. Itô. On Stochastic Differential Equations. Memoirs of the American Mathematical Society, 4:1–57, 1951.

- Jentzen et al. [2016] A. Jentzen, T. Müller-Gronbach, and L. Yaroslavtseva. On Stochastic Differential Equations with Arbitrary Slow Convergence Rates for Strong Approximation. Communications in Mathematical Sciences, 14(6):1477–1500, 2016.

- Karatzas and Shreve [1991] I. Karatzas and S. E. Shreve. Brownian Motion and Stochastic Calculus. Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- Kloeden and Platen [1992] P. E. Kloeden and E. Platen. Numerical Solutions of Stochastic Differential Equations. Stochastic Modelling and Applied Probability. Springer Verlag, Berlin-Heidelberg, 1992.

- Kohatsu-Higa et al. [2013] A. Kohatsu-Higa, A. Lejay, and K. Yasuda. Weak Approximation Errors for Stochastic Differential Equations with Non-Regular Drift. 2013. Preprint, Inria, hal-00840211.

- Leobacher and Szölgyenyi [2016] G. Leobacher and M. Szölgyenyi. A Numerical Method for SDEs with Discontinuous Drift. BIT Numerical Mathematics, 56(1):151–162, 2016.

- Leobacher and Szölgyenyi [2017] G. Leobacher and M. Szölgyenyi. A Strong Order 1/2 Method for Multidimensional SDEs with Discontinuous Drift. The Annals of Applied Probability, 27(4):2383–2418, 2017.

- Leobacher and Szölgyenyi [2018] G. Leobacher and M. Szölgyenyi. Correction note for: A strong order 1/2 method for multidimensional SDEs with discontinuous drift. 2018.

- Leobacher et al. [2015] G. Leobacher, M. Szölgyenyi, and S. Thonhauser. On the Existence of Solutions of a Class of SDEs with Discontinuous Drift and Singular Diffusion. Electronic Communications in Probability, 20(6):1–14, 2015.

- Lima [1988] Elon L. Lima. The Jordan-Brouwer Separation Theorem for Smooth Hypersurfaces. The American Mathematical Monthly, 95(1):39–42, 1988.

- Müller-Gronbach and Yaroslavtseva [2016] T. Müller-Gronbach and L. Yaroslavtseva. On Hard Quadrature Problems for Marginal Distributions of SDEs with Bounded Smooth Coefficients. 2016. arXiv:1603.08686.

- Ngo and Taguchi [2016a] H. L. Ngo and D. Taguchi. On the Euler-Maruyama Approximation for One-Dimensional Stochastic Differential Equations with Irregular Coefficients. 2016a. arXiv:1509.06532.

- Ngo and Taguchi [2016b] H. L. Ngo and D. Taguchi. Strong Convergence for the Euler-Maruyama Approximation of Stochastic Differential Equations with Discontinuous Coefficients. 2016b. arXiv:1604.01174.

- Ngo and Taguchi [2016c] H. L. Ngo and D. Taguchi. Strong Rate of Convergence for the Euler-Maruyama Approximation of Stochastic Differential Equations with Irregular Coefficients. Mathematics of Computation, 85(300):1793–1819, 2016c.

- Sabanis [2013] S. Sabanis. A Note on Tamed Euler Approximations. Electronic Communications in Probability, 18(47):1–10, 2013.

- Shardin and Szölgyenyi [2016] A. A. Shardin and M. Szölgyenyi. Optimal Control of an Energy Storage Facility Under a Changing Economic Environment and Partial Information. International Journal of Theoretical and Applied Finance, 19(4):1–27, 2016.

- Szölgyenyi [2016] M. Szölgyenyi. Dividend Maximization in a Hidden Markov Switching Model. Statistics & Risk Modeling, 32(3-4):143–158, 2016.

- Veretennikov [1981] A. YU. Veretennikov. On Strong Solutions and Explicit Formulas for Solutions of Stochastic Integral Equations. Mathematics of the USSR Sbornik, 39(3):387–403, 1981.

- Veretennikov [1982] A. YU. Veretennikov. On the Criteria for Existence of a Strong Solution of a Stochastic Equation. Theory of Probability and its Applications, 27(3), 1982.

- Veretennikov [1984] A. YU. Veretennikov. On Stochastic Equations with Degenerate Diffusion with Respect to Some of the Variables. Mathematics of the USSR Izvestiya, 22(1):173–180, 1984.

- Yaroslavtseva [2016] L. Yaroslavtseva. On Non-Polynomial Lower Error Bounds for Adaptive Strong Approximation of SDEs. 2016. arXiv:1609.08073.

- Zvonkin [1974] A. K. Zvonkin. A Transformation of the Phase Space of a Diffusion Process that Removes the Drift. Mathematics of the USSR Sbornik, 22(129):129–149, 1974.

G. Leobacher

Institute for Mathematics and Scientific Computing, University of Graz, Heinrichstraße 36, 8010 Graz, Austria

gunther.leobacher@uni-graz.at

M. Szölgyenyi 🖂

Institute of Statistics and Mathematics, Vienna University of Economics and Business, Welthandelsplatz 1, 1020 Vienna, Austria

michaela.szoelgyenyi@wu.ac.at