Michael Minyi Zhang

michael_zhang@utexas.eduHenry Lam

henry.lam@columbia.eduLizhen Lin

lizhen.lin@nd.eduThe University of Texas at Austin, Austin, TX 78712, USA.

Columbia University, New York, NY 10027, USA.

University of Notre Dame, Notre Dame, IN 46556, USA.

Abstract

Effective and accurate model selection is an important problem in modern data analysis. One of the major challenges is the computational burden required to handle large data sets that cannot be stored or processed on one machine. Another challenge one may encounter is the presence of outliers and contaminations that damage the inference quality. The parallel “divide and conquer” model selection strategy divides the observations of the full data set into roughly equal subsets and perform inference and model selection independently on each subset. After local subset inference, this method aggregates the posterior model probabilities or other model/variable selection criteria to obtain a final model by using the notion of geometric median. This approach leads to improved concentration in finding the “correct” model and model parameters and also is provably robust to outliers and data contamination.

††journal: Computational Statistics & Data Analysis

1 INTRODUCTION

In many data modeling scenarios, many plausible models are available to fit to the data, each of which may result in drastically different predictions and conclusions. Being able to select the right model for inference is a crucial task. As our main example, we consider model selection for a normal linear model:

(1)

where is an dimensional response vector, is an dimensional design matrix and is a dimensional vector of regression parameters. Here the candidate models to be selected could refer to the sets of significant variables. In a Bayesian setting, we have a natural probabilistic evaluation of models through posterior model probabilities. Depending on the objectives of the data analysis, we may be interested in assessing the belief on which is the “best” model or obtaining predictions with minimum error.

Existing procedures to accomplish the aforementioned goals, however, will perform poorly under the presence of outliers and contaminations. In addition, Markov chain Monte Carlo (MCMC) algorithms for these methods do not scale to big data situations. The goal of this paper is to investigate a “divide-and-conquer” method that integrates with existing Bayesian model selection techniques, in a way that is robust to outliers and, moreover, allows us to perform Bayesian model selection in parallel.

Our “divide-and-conquer” strategy is based on the ideas for robust inference using the notion of the geometric median [1], especially the median posterior in the Bayesian context [2, 3]. Previous work in this area has focused on the performance in parametric inference.

Our contribution in this paper is to demonstrate the effectiveness of these ideas in selecting the correct class of models on top of the parameters. In particular, we show that the model aggregated across different subsets (the “divide”) has improved concentration to the true model class compared to the one using the full data set. This concentration is in terms of the posterior model probabilities to the point mass assigned to the true model. The result also holds jointly with the concentration of the parameter estimates, and under the presence of outliers and hence demonstrates robustness. We carry out extensive numerical studies on simulation data and a real data example to demonstrate the performance of our proposed approach.

2 BAYESIAN MODEL SELECTION

In Bayesian model selection, we define the prior model probability for each of the model () under consideration. For model , we additionally have parameters with prior , which leads to a likelihood . Thus, the posterior model probability for model , , is proportional to

However, as noted in [4], choosing the model with the highest posterior model probability is not always the best option nor should one neglect the risk of model uncertainty. Instead of resorting to a single model for predicted values (or some quantity of interest in general), [5] proposes to average over the model uncertainty with Bayesian model averaging (BMA) to obtain a posterior mean and variance of at a covariate level :

We will focus on BMA in our theoretical developments in this paper. Our numerical experiments, however, will show that our divide-and-conquer strategy is also effective in applying on other model selection methods.

The first alternative to BMA is the median probability model, which can be shown to be optimal if we must choose one model for prediction [4]. In this approach, we define the posterior inclusion probability of each predictor () as the sum of posterior model probabilities of the models that include predictor , namely . The median probability model is the model that includes the predictors if .

Second, using the maximum value of the likelihood for each model , where is the maximum likelihood estimate of , we can perform penalized model selection through the Akaike information criterion (AIC) [6] or the Bayesian information criterion (BIC) [7] by selecting the model with the lowest information criterion:

The final model selection technique we will consider is stochastic variable selection through the spike and slab model [8], which allows for variable shrinkage under high-dimensional models.

For the purposes of this paper, we will use the rescaled spike and slab model [9]. To perform posterior inference in this model, we first define where is the unbiased estimate of under the full model and let be some small number. The model is defined to be the following mixture model:

3 DIVIDE-AND-CONQUER AND ROBUST BAYESIAN MODEL SELECTION

In our robust model selection strategy, we divide observations into subsets of roughly equal sample size. Then inference, model selection and prediction is performed for the linear model independently across subsets using the existing Bayesian model selection procedures, which are then combined to form a final model or a combined prediction value.

Given linear model (1), we first define the following priors on a normal likelihood with response variable and -dimensional predictor . The observations are divided into subsets with observations within each subset. One has,

To compensate for the data division, we raise the likelihood of the divided data to the -th power and adjust the normalizing constant accordingly so that the likelihood for is:

The intuition and motivation for raising the subset likelihood to -th power is to adjust the potentially inflated variance of the subset posterior distribution.

Exploiting conjugacy, we obtain the full conditionals for data subset :

Let , then integrating out the parameters gives us the following marginal distribution :

For distributed AIC and BIC model evaluation, we raise the likelihood term of the AIC and BIC formula to the power of :

In applying our procedure with the spike and slab prior, we derived the full Gibbs sampler for our procedure. For posterior inference in the spike and slab model, let , we can perform Gibbs sampling by drawing from the following posteriors:

Once inference is built on each subset, the key step is to aggregate the subset models (or estimates) together into a final model (or estimate). To aggregate our results, we collect the number of subset models or estimates and find the geometric median between these elements. The geometric median for a set of elements valued on a Hilbert space , is defined as

(2)

where is the norm associated with the inner product in [3]. The solution can generally be effectively approximated using the Weiszfeld algorithm [10].

For instance, in the case of aggregating the posterior model probabilities across subsets of data, the geometric median operates on the space of posterior distributions and the geometric median posterior model probability, , is defined as:

(3)

where is the posterior model probabilities for subset , and denotes the space of distributions on support points. The metric here can be taken as the Euclidean metric, or an integral probability metric (IPM) defined as for some class of functions [11, 12].

For the model selection techniques discussed earlier (AIC, BIC, and the median model selection), we can choose a final model in two ways: One, we can select the best model locally on each subset, use it for prediction, and then aggregate the results (estimate combination). Or two, we can take the median of the model selection criteria and choose that particular model on each subset and then aggregate the results to get a final model (model combination).

However, in Bayesian model averaging and spike and slab modeling we do not choose a final model. We can still perform model or estimate combination by aggregating the posterior model probabilities. We consider both model and estimate combinations in our experiments and show that they yield similar results in our experimental settings.

fordo

Raise likelihood to -th power

Compute inference for for

Draw predictive values from predictive posterior for

Calculate posterior model probabilities

Calculate geometric median of posterior model probabilities over the subsets using (3).

Approximate geometric medians of posterior parameter probabilities or predictive values given individual models over the subsets using (2).

Obtain BMA estimate:

Algorithm 1Algorithm for robust model selection in the case of BMA.

4 IMPROVED CONCENTRATION AND ROBUSTNESS

In this section we provide theoretical justification on the robustness in the divide-and-conquer strategy. In particular, we focus on BMA. Additionally, we show that the aggregated model class from our strategy concentrates faster, in terms of posterior model probabilities, to the correct class compared to using the whole data set at once. This concentration result can be joint with parameter estimation, and also applies in a way that exhibits robustness against outliers. Note that we do not raise the subset likelihood to -th power in our current theoretical analysis, but the results can be generalized by imposing slightly stronger entropy conditions on the model.

Let be the domain of , our set of model indices and parameters. Let be the true data generating parameter, and let be a generic data point. Let be the true conditional density of given , and be the true density of the covariates . We denote . Let be the distribution defined by and is the true distribution . For convenience, we denote where is the expectation under . We denote as the true probability measure taken on the data of size and . Lastly, we denote as the -packing number of a set of probability measures under the metric , which is the maximal number of points in such that the distance between any pair is at least . We implicitly assume here that is separable. The following Theorem 1 follows from a modification of Theorem 2.1 in [13]:

Theorem 1

Assume that there is a sequence such that and as , a constant , and a set so that

1.

2.

3.

where and is the Hellinger distance. Then we have

(4)

for any and sufficiently large such that and , where is a universal constant.

The proof of Theorem 1 is in the Appendix. As noted by [13], the important assumptions are Assumptions 1 and 3. Essentially, Assumption 1 constrains the size of the parameter domain to be not too big, whereas Assumption 3 ensures sufficient mass of the prior on a neighborhood of the true parameter. The concentration result (4) states that the posterior distribution of is close to the true with high probability, where the closeness is measured in terms of the Hellinger distance between the likelihoods. Note that the RHS of (4) consists of three terms. The dominant term is the power-law decay in . The other two exponential decay terms result from technical arguments in the existence of tests that sufficiently distinguish between distributions [14, 15].

Next we describe the concentration behavior of BMA. We focus on the situations where all the candidate models are non-nested, i.e. only one model contains distributions that are arbitrarily close to the truth. Without loss of generality, we let be the true model.

Theorem 2 (BMA of Non-Nested Models)

Suppose the assumptions in Theorem 1 hold. Also assume that, for sufficiently small , for any . Let be the same universal constant arising in Theorem 1. We have

1.

For any given ,

(5)

for sufficiently large .

2.

For any given ,

(6)

for sufficiently large , where is the Euclidean distance, and is the point mass on .

Note that the assumption for any and sufficiently small is a manifestation of the non-nested model situation, asserting that only one model is “correct”. Result 1 is a concentration on the posterior probability of picking the correct model to be close to 1.

Result 2 translates this in terms of the Euclidean distance between the model posterior probability and the point mass on the correct model. Result 3 is an alternative using the Hellinger distance.

Note that the concentration bound for Hellinger distance (7) is inferior to that for Euclidean distance (6) for small since instead of shows up in the RHS of (7). This is because in our proof, the function that appears in (14) has derivative which is at , and thus no linearization is available when is close to 0.

Theorem 2 can be modified to handle the case where multiple models contain the truth. In particular, the expression inside the probability in (5) becomes

where is the collection of all such that contains the true model. In (6) and (7), the use of is replaced by an existence of some probability vector (dependent on ) supported on the indices in . In other words, one now allows comparing with an arbitrary allocation of probability masses to all true models in the concentration bound. These modifications can be seen by following the arguments in the proof of Theorem 2. Specifically, (9) would be modified as

Then (10) would imply a modified version of (11), namely

giving the claimed modification for (5). Then, following (12), we could find a probability vector to make all terms vanish except one, which is in turn bounded by . This gives the claimed modifications for (6) and (7).

The following result states how a divide-and-conquer strategy can improve the concentration rate of the posterior model probabilities towards the correct model:

Theorem 3 (Concentration Improvement)

Suppose the assumptions in Theorem 2 hold. Let , and

.

For sufficiently large , letting be constants such that and , we have:

1.

, the geometric median under of , satisfies

(16)

where , and .

2.

Let be the number of model classes, then:

(17)

3.

Suppose in addition that, for any such that for , we have

(18)

where , with being a characteristic kernel defined on the space and is the corresponding reproducing kernel Hilbert space (RKHS), and and are constants. Moreover, assume that there is a universal constant such that for all , and we choose such that . Then

where is defined as , is a sufficiently large constant, is the geometric median of under the -norm, and is the delta measure at the true parameter.

The significance of Theorem 3 is the improvement of the concentration from power-law decay in Theorem 2 to exponential decay, as the number of subsets grows. Such type of results is known in the case of parameter estimation (e.g., [2, 3]). Theorem 3 generalizes to the case of model selection.

Results 1 and 2 describe the exponential concentration for the model posteriors to the correct model, while Result 3 states the joint concentration in both the model posterior and the parameter posterior given the correct model, when one adopts a second layer of divide-and-conquer on the parameter posterior conditional on each individual candidate model. Result 3 in particular combines with the parameter concentration result in [3].

Note that we have taken a hybrid viewpoint here that we assume a “correct” model and parameters in a frequentist sense. Under this view, a posterior probability more concentrated towards the truth is more desirable. This constitutes our main claim that the divide-and-conquer strategy is attractive. This view has been used in existing work like [2, 3].

Finally, the following theorem highlights that the concentration improvement still holds even if the data are contaminated to a certain extent:

Theorem 4 (Robustness to Outliers)

Using the notation in Theorem 3, but assume instead that, for where ,

Theorem 4 stipulates that when a small number of subsets are contaminated by arbitrary nature, the geometric median approach still retains the same exponential concentration.

The proofs of both theorems rely on a key theorem on geometric median in [1], restated in the Appendix. We focus on Theorem 3, as the proof for Theorem 4 is a straightforward modification in light of Theorem 5.

Proof of 3.

Under the additional assumptions, we can invoke Corollary 3.5 in [3] to obtain that

The result follows from applying a union bound and together with (17).

\qed

5 SIMULATIONS AND DATA ANALYSIS

For the BMA, AIC, BIC and median probability model tests, we generate data from a model , where is a matrix and is a dimensional vector with true predictors. We assess the aforementioned model selection techniques with four tests, over trials for the contamination and magnitude tests and over trials for the coverage test on and subsets for the magnitude and coverage tests and and subsets for the contamination tests with 1,000 iterations on each MCMC chain and a burn-in period of the initial iterations.

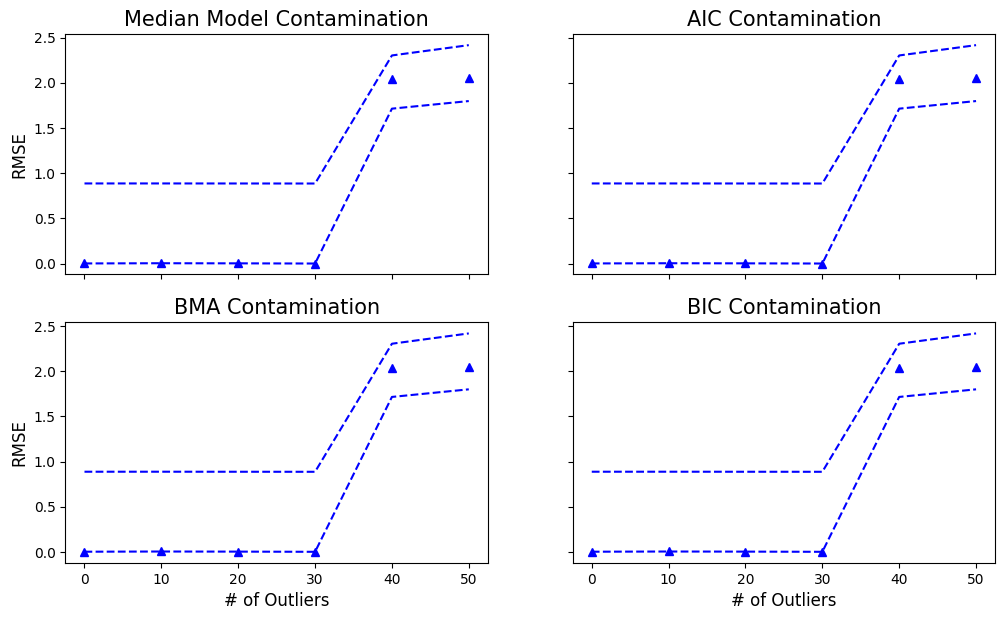

The first test is the contamination test which examines the root mean square error (RMSE) of held-out test data of size against the number of outliers present (as many as in our experiments) in the training data, . We generate outliers by taking the maximum of the absolute value of the data and add a given magnitude value. Each outlier has a relative magnitude of 10,000 meaning that we find the largest output, such that , so that the value of the outlier is . For the contamination test, we expect to see superior performance with regards to RMSE of the subset median posterior as long as the number of outliers per subset does not exceed . Figure 1 demonstrates the robustness of our technique to the number of outliers when we divide the data into subsets. We can see that the empirical distribution of the RMSE over trials for subsets (green dashed line) falls dramatically below that of the RMSE distribution of subset for each model selection technique when outliers are present except in the case when outliers are present for Bayesian model averaging which approaches the point where the theoretical guarantees of our method are violated.

Figure 1: Contamination test.

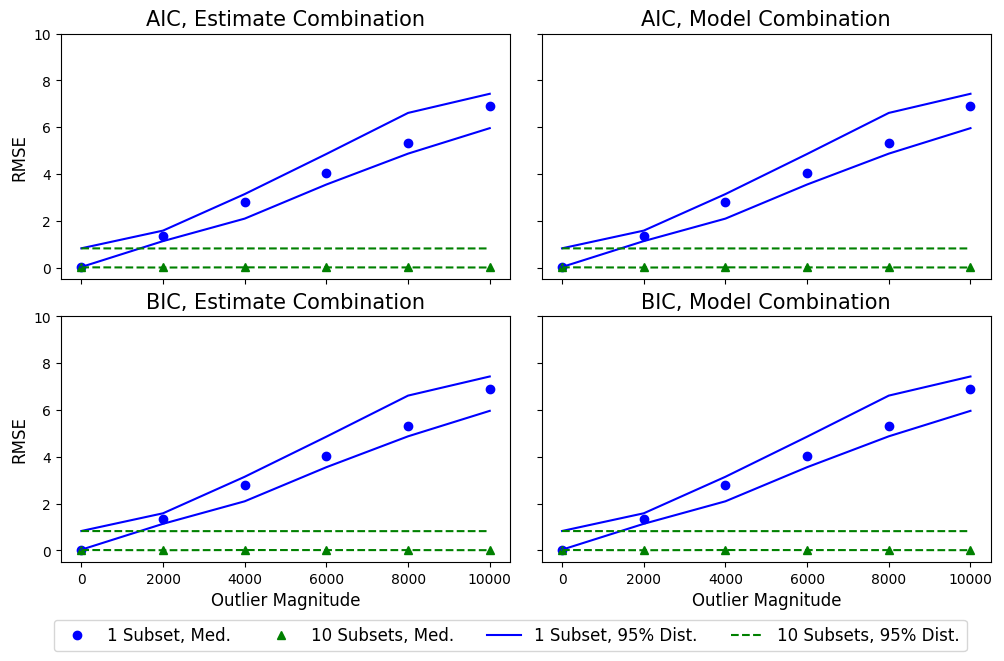

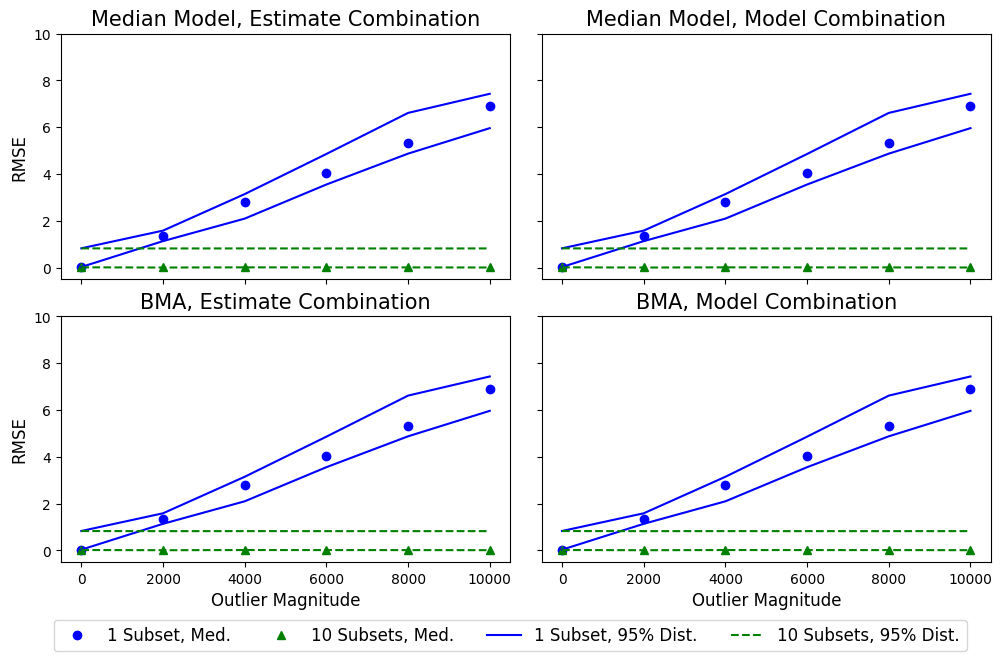

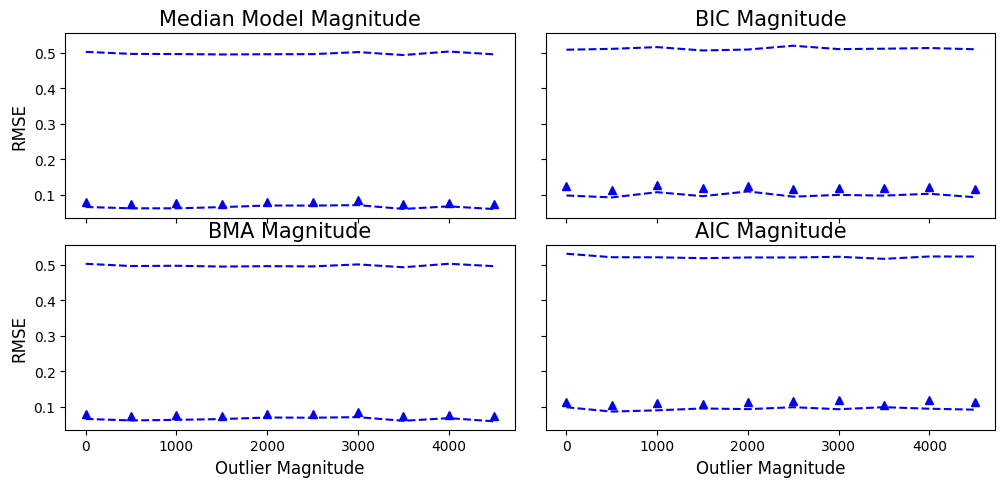

The second test assesses the RMSE of the held-out test data of size against the increasing relative magnitude of one outlier present in the training data. We expect to see nearly constant RMSE on the subset run as the relative magnitude of a single outlier increases, thus the procedure is robust. We can see in Figure 2 that the RMSE of distributed variants of the model selection techniques are lower than the single processor variants as the number of outliers increases. In the magnitude test, we can categorically observe that subset RMSE is invariant to the relative magnitude of one outlier present in the data whereas the RMSE grows rapidly on one subset.

Figure 2: Magnitude of outlier test.

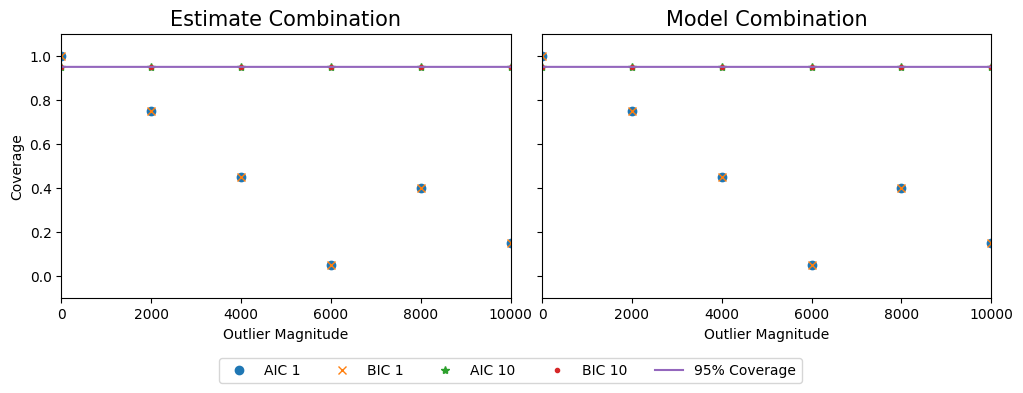

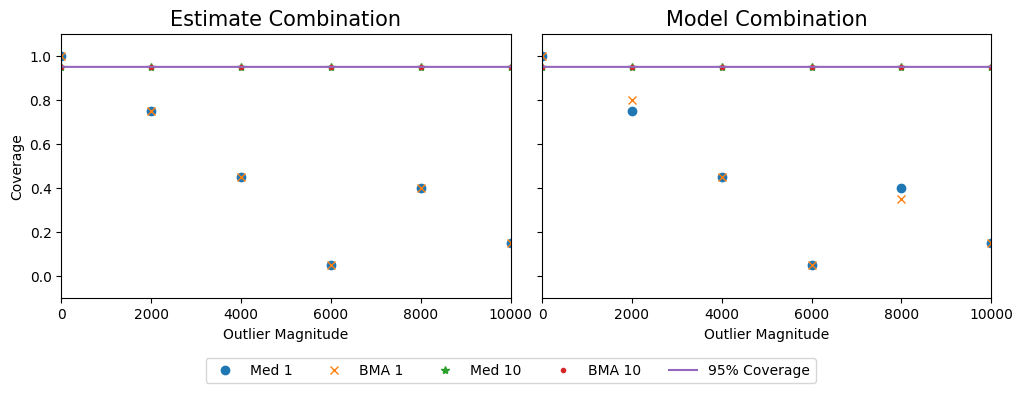

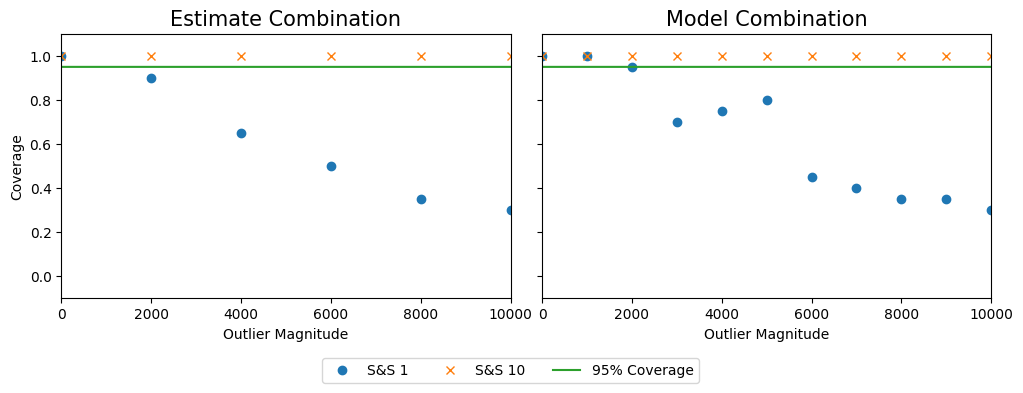

The next test assesses the frequentist posterior coverage of the true held-out predictive value of size , , against the increasing relative magnitude of one outlier in the training data. To calculate coverage we generate independent MCMC chains at each level of outlier magnitude and calculate the proportions of chains which include the true predictive value within the and percentiles of the posterior predictive draws. For the coverage test we see that the empirical coverage of a single predictive value for the distributed subsets is, on average, regardless of the magnitude of the outlier as opposed to the empirical coverage for the single subset. In the subset case, we can see that the empirical coverage degrades almost to zero as the magnitude of the outlier grows. (see Figure 3).

Figure 3: Testing empirical coverage of predictive value.

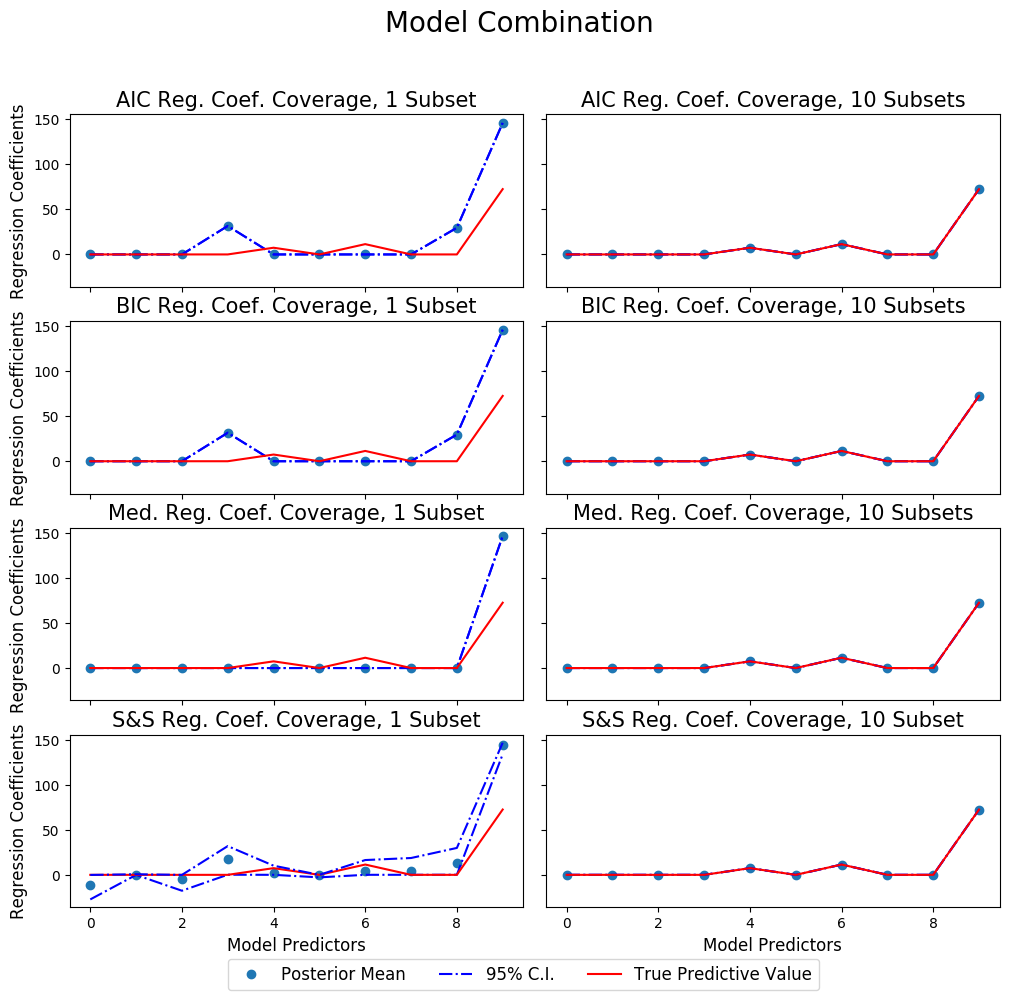

Our last evaluation is the coverage of the regression coefficients and the ability for our model selection techniques to choose the correct model under the distributed setting with a single outlier of magnitude 10,000. We compare the posterior credible interval of the regression coefficients for and subsets. Note that we do not include nested models in our evaluations or models larger than the true model (i.e models with more than covariates included). Furthermore, we perform this evaluation under two settings: One, where we combine the optimal local model seleceted on each subset (“Model Combination”) or if we combine the subposterior estimates and select the optimal model globally (“Estimate Combination”) As seen in Figure 4, the parallel technique is able to select the correct model subset test, the outlier leads to the incorrect model being selected. Additionally, Figure 5 demonstrates that model and estimate combination yield similar results with the regression coefficient coverage test.

Figure 4: Posterior regression parameter coverage test results, estimate combination.Figure 5: Posterior regression parameter coverage test results, model combination.

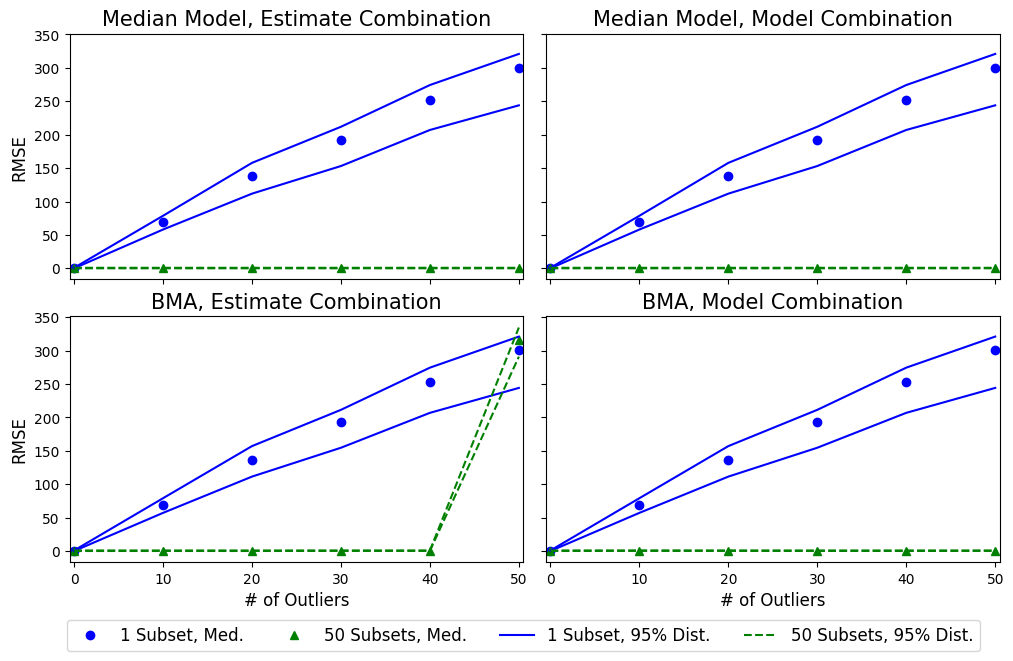

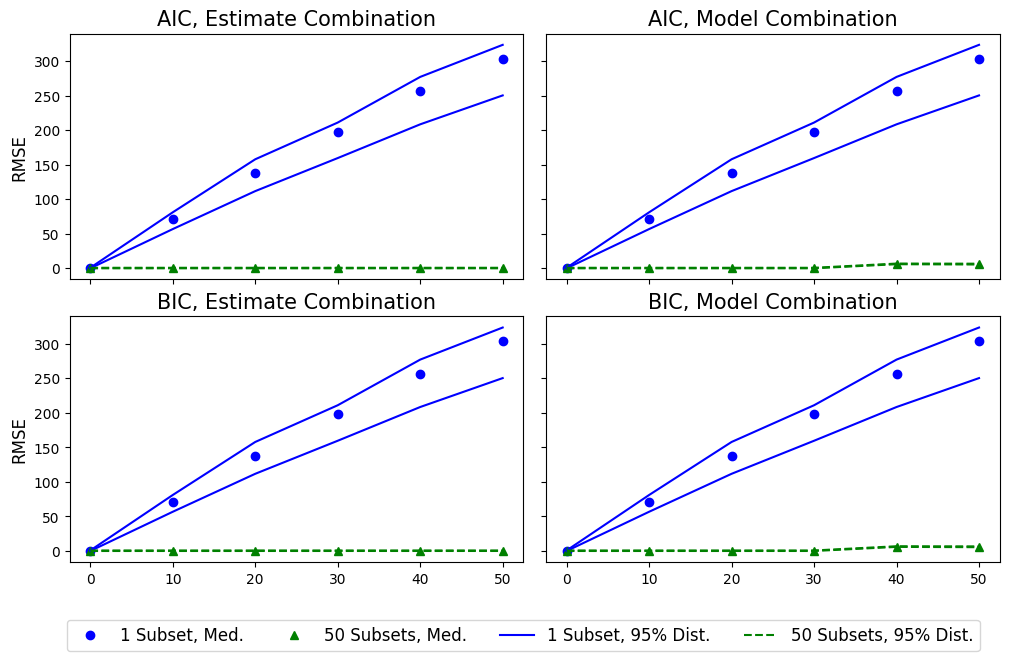

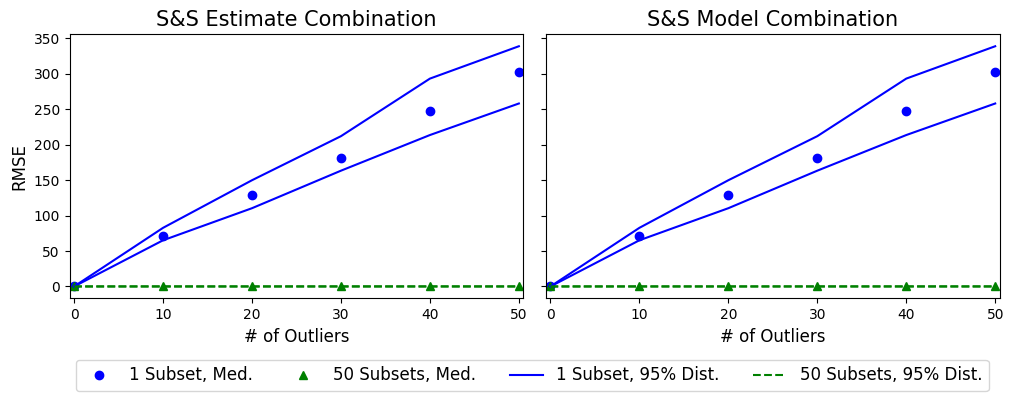

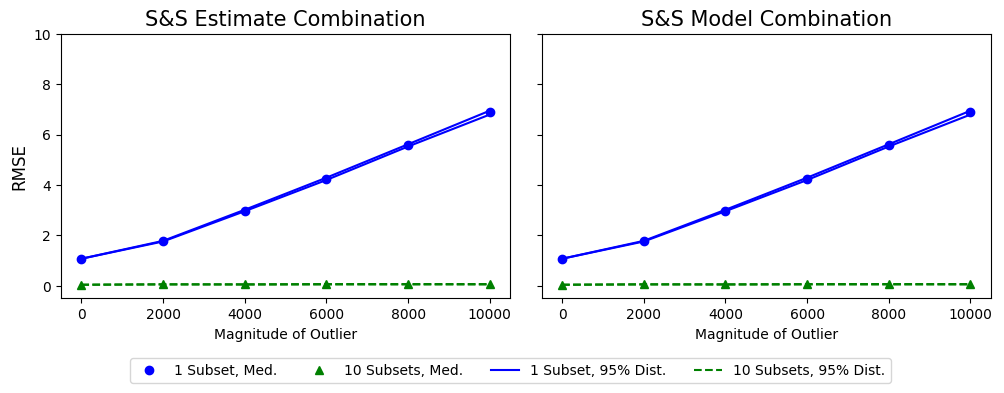

Also, we would like to see if the results still hold between model and estimate combination for the other simulation studies performed. Figs. 6, 7, and 8 show that there is little difference in how we combine the information for model selection in each of the tests evaluated.

Figure 6: Contamination test

Figure 7: Coverage test.

Figure 8: Magnitude test.

Furthermore, we wish to evaluate our method a large synthetic dataset with the same synthetic generating process as above, but with one million observations divided over 50 processors. Here, we examine the behavior of our method when we increase the magnitude of one outlier in the dataset and when we increase the number of outliers with fixed magnitude. In Figure 9, we can see that our performance is robust when the number of outliers per subset fulfills Theorem 4. When the number of outliers reaches 40 and 50, we see start to see a noticeable degradation of our method’s predictive ability. However, this degradation is still small relative to what we might observe in the case where we do not divide the data into subsets.

Additionally, we would like to see the computational gain of dividing the data for this situation in terms of CPU time for running the model selection and inference procedure. For one subset the average computation time is 91,829.15 seconds with a standard error of seconds. For ten subsets, the average computation time is 10,301.60 seconds with a standard error of seconds. And for fifty subsets, the average computation time is 29,49.74 seconds with a standard error of seconds which signifies that we obtain critical computational performance when dividing our method across multiple processors.

Figure 9: Synthetic big data results.

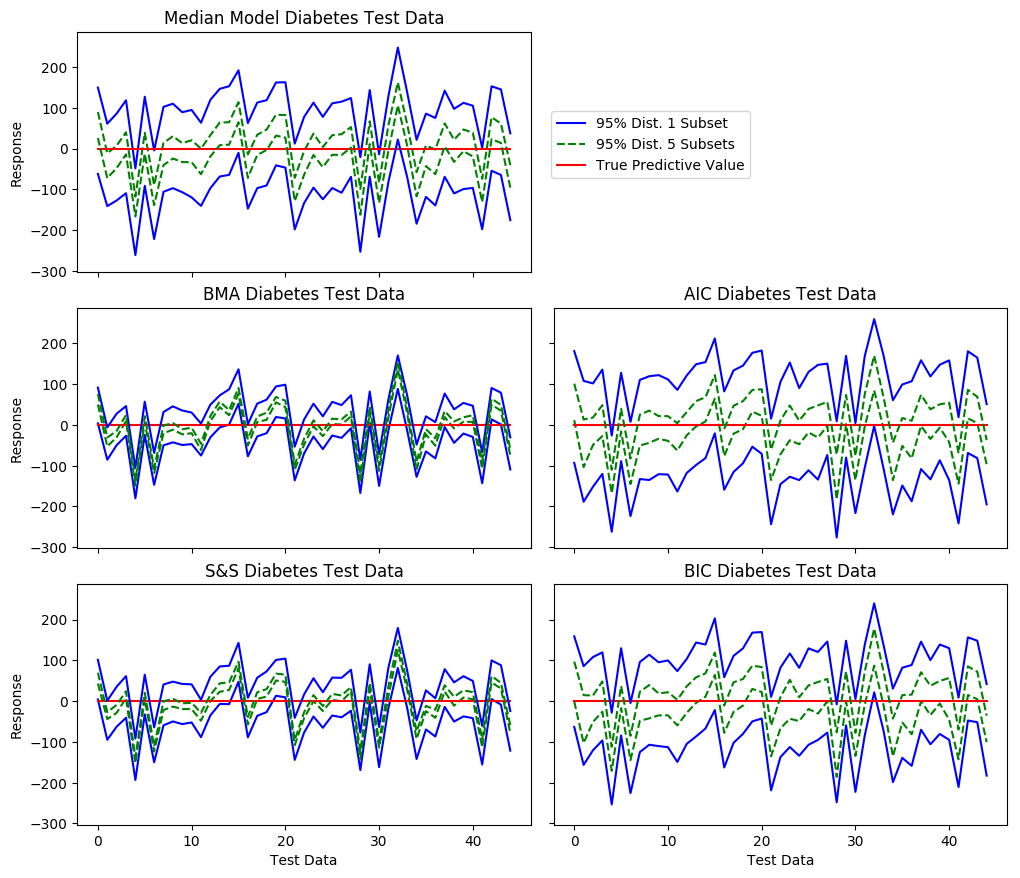

Lastly, we evaluate our parallel model selection method on the diabetes data set used in [16]. The diabetes data consists of a dimension design matrix scaled with unit norm and zero mean and a single response vector. We held out observations for test evaluation and plotted the posterior credible intervals for the predictive values centered at zero after subtracting the true predictive value. We can see in Fig. 10 that, after dividing the data across 5 subsets, we can attain a tighter credible interval over the true value for each model selection technique.

Figure 10: Diabetes test data results.

6 CONCLUSION

While a substantial body of work exists for fast and scalable Bayesian inference methods, few research methods are available on robust and scalable model selection.

We have studied in this paper a divide-and-conquer strategy that contributes to filling this gap. This strategy operates by taking the geometric median of posterior model probabilities or other selection criteria that extends previous results focusing on parametric inference. We show theoretically how the strategy, particularly in the setting of BMA, can be robust to outliers and, moreover, exhibits faster concentration to the true model in terms of posterior model probabilities. The concentration result also applies to the joint setting of model selection and parameter estimation. We illustrate with both simulation data and a real data example how a variety of our strategy leads to more robust inference compared to standard approach that does not divide data into subsets. The strategy we present is simple to execute and is foreseen to have good practical value.

Consider a Hilbert space and . Let be a collection of independent random -valued elements. Let be constants such that and . Suppose that there exists such that for all , where ,

Let be the geometric median of . Then

where , and

ACKNOWLEDGMENTS

The contribution of Lizhen Lin was funded by NSF grants IIS 1663870, CAREER DMS 1654579. The contribution of Henry Lam was funded by NSF grants CMMI-1542020, CMMI-1523453 and CAREER CMMI-1653339. The contribution of Michael Zhang was funded by NSF grant 1447721.

REFERENCES

References

[1]

S. Minsker, Geometric median and robust estimation in Banach spaces,

Bernoulli 21 (4) (2015) 2308–2335.

[2]

X. Wang, P. Peng, D. B. Dunson, Median selection subset aggregation for

parallel inference, in: Advances in Neural Information Processing Systems,

2014, pp. 2195–2203.

[3]

S. Minsker, S. Srivastava, L. Lin, D. B. Dunson, Scalable and robust Bayesian

inference via the median posterior, in: Proceedings of the 31st International

Conference on Machine Learning (ICML-14), 2014, pp. 1656–1664.

[4]

M. M. Barbieri, J. O. Berger, Optimal predictive model selection, Annals of

Statistics (2004) 870–897.

[5]

J. A. Hoeting, D. Madigan, A. E. Raftery, C. T. Volinsky, Bayesian model

averaging: a tutorial, Statistical science (1999) 382–401.

[6]

H. Akaike, A new look at the statistical model identification, IEEE

Transactions on Automatic Control 19 (6) (1974) 716–723.

[7]

G. Schwarz, Estimating the dimension of a model, The Annals of Statistics 6 (2)

(1978) 461–464.

[8]

E. I. George, R. E. McCulloch, Variable selection via Gibbs sampling, Journal

of the American Statistical Association 88 (423) (1993) 881–889.

[9]

H. Ishwaran, J. S. Rao, Spike and slab variable selection: Frequentist and

Bayesian strategies, Annals of Statistics (2005) 730–773.

[10]

E. Weiszfeld, Sur le point pour lequel la somme des distances de points

donnes est minimum, Tohoku Mathematical Journal 43 (1937) 355–386.

[11]

B. K. Sriperumbudur, A. Gretton, K. Fukumizu, B. Schölkopf, G. R. G.

Lanckriet, Hilbert space embeddings and metrics on probability measures, The

Journal of Machine Learning Research 11 (2010) 1517–1561.

[12]

B. K. Sriperumbudur, K. Fukumizu, A. Gretton, B. Schölkopf, G. R. G.

Lanckriet, et al., On the empirical estimation of integral probability

metrics, Electronic Journal of Statistics 6 (2012) 1550–1599.

[14]

L. Birgé, Approximation dans les espaces métriques et théorie de

l’estimation, Zeitschrift für Wahrscheinlichkeitstheorie und verwandte

Gebiete 65 (2) (1983) 181–237.

[15]

L. Le Cam, Asymptotic Methods in Statistical Decision Theory, Springer Science

& Business Media, 2012.

[16]

B. Efron, T. Hastie, I. Johnstone, R. Tibshirani, et al., Least angle

regression, The Annals of statistics 32 (2) (2004) 407–499.