The xyz algorithm for fast interaction search in high-dimensional data

Abstract

When performing regression on a data set with variables, it is often of interest to go beyond using main linear effects and include interactions as products between individual variables. For small-scale problems, these interactions can be computed explicitly but this leads to a computational complexity of at least if done naively. This cost can be prohibitive if is very large.

We introduce a new randomised algorithm that is able to discover interactions with high probability and under mild conditions has a runtime that is subquadratic in . We show that strong interactions can be discovered in almost linear time, whilst finding weaker interactions requires operations for depending on their strength. The underlying idea is to transform interaction search into a closest pair problem which can be solved efficiently in subquadratic time. The algorithm is called xyz and is implemented in the language R. We demonstrate its efficiency for application to genome-wide association studies, where more than interactions can be screened in under seconds with a single-core GHz CPU.

1 Introduction

Given a response vector and matrix of associated predictors , finding interactions is often of great interest as they may reveal important relationships and improve predictive power. When the number of variables is large, fitting a model involving interactions can involve serious computational challenges. The simplest form of interaction search consists of screening for pairs with high inner product between the outcome of interest and the point-wise product :

| (1) |

This search is of complexity in a naive implementation and quickly becomes infeasible for large . Of course one would typically be interested in maximising (absolute values of) correlations rather than dot products in (1), an optimisation problem that would be at least as computationally intensive.

Even more challenging is the task of fitting a linear regression model involving pairwise interactions:

| (2) |

Here is the intercept and and contain coefficients for main effects and interactions respectively, and is random noise.

In this paper, we make several contributions to the problem of searching for interactions in high-dimensional settings.

-

(a)

We first establish a form of equivalence between (1) and closest-pair problems (Shamos and Hoey, 1975; Agarwal et al., 1991). Assume for now that all predictors and outcomes are binary, so (we will later relax this assumption) and define as . Then it is straightforward to show that (1) is equivalent to

(3) for some . This connects the search for interactions to literature in computational geometry on problems of finding closest pairs of points.

-

(b)

We introduce the xyz algorithm to solve (3) based on randomly projecting each of the columns in and to a one-dimensional space. By exploiting the ability to sort the resulting points with computational cost, we achieve a run time that is always subquadratic in and can even reach a linear complexity when is much larger than the quantity of the bulk of the pairs . We show that our approach can be viewed as an example of locality sensitive hashing (Leskovec et al., 2014) optimised for our specific problem.

-

(c)

We show how any method for solving (1) can be used to fit regression models with interactions (15) by building it into an algorithm for the Lasso (Tibshirani, 1996). The use of xyz thus leads to a procedure for applying the Lasso to all main effects and interactions with computational cost that scales subquadratically in .

-

(d)

We provide implementations of both the core xyz algorithm and its extension to the Lasso in the R package xyz, which is available on github (Thanei, 2016) and CRAN.

Our work here is thus related to “closest pairs of points” algorithms in computational geometry as well as an extensive literature on modelling interactions in statistics, both of which we now review.

1.1 Related work

A common approach to avoid the quadratic cost in of searching over all pairs of variables (1) is to restrict the search space: one can first seek a small number of important main effects, and then only consider interactions involving these discovered main effects. More specifically, one could fit a main effects Lasso (Tibshirani, 1996) to the data first, add interactions between selected main effects to the matrix of predictors, and then run the Lasso once more on the augmented design matrix in order to produce the final model (see Wu et al. (2010) for example). Tree-based methods such as CART (Breiman et al., 1984) work in a similar fashion by aiming to identify an important main effect and then only considering interactions involving this discovered effect.

However it is quite possible for the signal to be such that main effects corresponding to important interactions are hard to detect. As a concrete example of this phenomenon, consider the setting where is generated randomly with all entries independent and having the uniform distribution on . Suppose the response is given by , so there is no noise. Since the distribution is the same for all , main effects regressions would find it challenging to select variables 1 and 2. Note that by reparametrising the model by adding one to each entry of for example, we obtain . The model now respects the so-called strong hierarchical principle (Bien et al., 2013) that interactions are only present when their main effects are. The hierarchical principle is useful to impose on any fitted model. However, imposing the principle on the model does not imply that the interactions will easily be found by searching for main effects first. The difficulty of the example problem is due to interaction effects masking main effects: this is a property of the signal and of course no reparametrisation can make the main effects any easier to find. Approaches that increase the set of interactions to be considered iteratively can help to tackle this sort of issue in practice (Bickel et al., 2010; Hao and Zhang, 2014; Friedman, 1991; Shah, 2016) as can those that randomise the search procedure (Breiman, 2001). However they cannot eliminate the problem of missing interactions, nor do these approaches offer guarantees of how likely it is that they discover an interaction.

As alluded to earlier, the pure interaction search problem (3) is related to close pairs of points problems, and more specifically the close bichromatic pairs problem in computational geometry (Agarwal et al., 1991). Most research in this area has focused on algorithms that lead to computationally optimal results in the number of points whilst considering the dimension to be constant. This has resulted in algorithms where the scaling of the computational complexity with is at least of order (Shamos and Hoey, 1975). Since for meaningful statistical results one would typically require , these approaches would not lead to subquadratic complexity. An exception is the so-called lightbulb algorithm (Paturi et al., 1989) which employs a similar strategy for binary data; our work here shows that this is optimal among random projection-based methods and also that it may be modified to handle continuous data and also detect interactions in high-dimensional regression settings.

In the special case where and , (3) may be seen to be equivalent to searching for large magnitude entries in the product of square matrices and . This latter problem is amenable to fast matrix multiplication algorithms, which in theory can deliver a subquadratic complexity of roughly (Williams, 2012; Davie and Stothers, 2013; Le Gall, 2012). However the constants hidden in the order notation are typically very large, and practical implementations are unavailable. The Strassen algorithm (Strassen, 1969) is the only fast matrix multiplication algorithm used regularly in practice to the best of our knowledge. With a complexity of roughly , the improvement over a brute force close pairs search is only slight.

The strategy we use is most closely related to locality sensitive hashing (LSH) (Indyk and Motwani, 1998) which encompasses a family of hashing procedures such that similar points are mapped to the same bucket with high probability. A close pair search can then be conducted by searching among pairs mapped to the same bucket. In fact, our approach for solving (3) can be thought of as an example of LSH optimised for our particular problem setting. This connection is detailed in Appendix B.

A seemingly attractive alternative to the subsampling-based LSH-strategy we employ is the method of random projections which is motivated by the theoretical guarantees offered by the Johnson–Lindenstrauss Lemma (Achlioptas, 2003). Perhaps surprisingly, we can show that using random projections instead of our subsampling-based scheme leads to a quadratic run time for interaction search (see Theorem 1 and section 5.1).

An approach that bears some similarity with our procedure is that of epiq (Arkin et al., 2014). This works by projecting the data and then searches through a lower dimensional representation for close pairs. This appears to improve upon a naive brute force empirically but there are no proven guarantees that the run time improves on the complexity of a naive search.

The Random Intersection Trees algorithm of Shah and Meinshausen (2014) searches for potentially deeper interactions in data with both and binary. In certain cases with strong interactions a complexity close to linear in is achieved; however it is not clear how to generalise the approach to continuous data or embed it within a regression procedure.

The idea of Kong et al. (2016) is to first transform the data by forming and for each predictor. Next and are tested for independence using the distance correlation test. In certain settings, this can reveal important interactions with a computational cost linear in . However, the powers of these tests depend on the distributions of the transformed variables . For example in the binary case when , each transformed variable will be a vector of 1’s and the independence tests will be unhelpful. We will see that our proposed approach works particularly well in this setting.

1.2 Organisation of the paper

In Section 2 we consider the case where both the response and the predictors are binary. We first demonstrate how (15) may be converted to a form of closest pair of points problem. We then introduce a general version of the xyz algorithm which solves this based on random projections. As we show in Section 2.1 there is a particular random projection distribution that is optimal for our purposes. This leads to our final version of the xyz algorithm which we present in Section 2.3 along with an analysis of its run time and probabilistic guarantees that it recovers important interactions. In Section 3 we extend the xyz algorithm to continuous data. These ideas are then used in Section 4 to demonstrate how the xyz algorithm can be embedded within common algorithms for high-dimensional regression (Friedman et al., 2010) allowing high-dimensional regression models with interactions to be fitted with subquadratic complexity in . Section 5 contains a variety of numerical experiments on real and simulated data that complement our theoretical results and demonstrate the effectiveness of our proposal in practice. We conclude with a brief discussion in Section 6 and all proofs are collected in the Appendix.

2 The xyz algorithm for binary data

In this section, we present a version of the xyz algorithm applicable in the special case where both and are binary, so and . We build up to the algorithm in stages, giving the final version in Section 2.2.

Define by and

| (4) |

We call the interaction strength of the pair . It is easy to see that the interaction search problem (1) can be expressed in terms of either the or the normalised squared distances. Indeed

| (5) |

Thus those pairs with large will have large, and small. This equivalence suggests that to solve (1), we can search for pairs of columns that are close in distance. At first sight, this new problem would also appear to involve a search across all pairs, and would thus incur an cost. As mentioned in the introduction, close pair searches that avoid a quadratic cost in incur typically an exponential cost in . Since would typically be much larger than , such searches would be computationally infeasible.

We can however project each of the -dimensional columns of and to a lower dimensional space and then perform a close pairs search. The Johnson–Lindenstrauss Lemma, which states roughly that one can project points into a space of dimension and faithfully preserve distances, may appear particularly relevant here. The issue is that the projected dimension suggested by the Johnson–Lindenstrauss Lemma is still too large to allow for an efficient close pairs search. The following observation however gives some encouragement: if we had so , even a one-dimensional projection will have , which implies that a perfect interaction will have zero distance in the projected space. We will later see that our approach leads to a linear run time in such a case. Importantly, we are only interested in using a projection that preserves the distances between the close pairs rather than all pairs, which makes our problem very different to the setting considered in the Johnson–Lindenstrauss Lemma.

With this in mind, consider the following general strategy. First project the columns of and to one-dimensional vectors and using a random projection : , . Next for some threshold , collect all pairs such that in the set . By first sorting and , a step requiring only computations (see for example Sedgewick (1998)), this close pairs search can be shown to be very efficient. Given this set of candidate interactions, we can check for each whether we have . The process can be repeated times with different random projections, and one would hope that given enough repetitions, any given strong interaction would be present in one of the candidate sets with high probability. This approach is summarised in Algorithm 1 which we term the general form of the xyz algorithm. A schematic overview is given in Figure 1.

There are several parameters that must be selected, and a key choice to be made is the form of the random projection . For the joint distribution of we consider the following general class of distributions, which includes both dense and sparse projections. We sample a random or deterministic number of indices from the set , , either with or without replacement. Then, given a distribution where is a class of distributions to be specified later, we form a vector with independent components each distributed according to . We then define the random projection vector by

| (6) |

Each configuration of the xyz algorithm is characterised by fixing the following parameters:

-

(i)

, a distribution for the projection vector which is determined through (6) by , a distribution for the subsample size and whether sampling is with replacement or not;

-

(ii)

, the number of projection steps;

-

(iii)

, the close pairs threshold;

-

(iv)

, the interaction strength threshold.

We will denote the collection of all possible parameter levels by . This includes the following subclasses of interest. Fix .

-

(a)

Dense projections. Let have independent components distributed according to and denote the distribution of by . This falls within our general framework above with set to and sampling without replacement. Let

-

(b)

Subsampling. Let be the set of distributions for obtained through (6) when subsampling with replacement. Let

-

(c)

Minimal subsampling. Let be the set of all parameters in such that the close pairs threshold is and takes randomly values in the set for some positive integer .

Note that we have suppressed the dependence of the classes above on the fixed distribution for notational simplicity. We define to be the set of all univariate absolutely continuous and symmetric distributions with bounded density and finite third moment. The restriction to continuous distributions in ensures that is invariant to the choice of : when , every with and the distribution for fixed yields the same algorithm. Moreover the set of close pairs in is simply the set of pairs that have for all , that is the set of pairs that are equal on the subsampled rows. We note that the symmetry and boundedness of the densities in and finiteness of the third moment are mainly technical conditions necessary for the theoretical developments in the following section. We will assume without loss of generality that the second moment is equal to . This condition places no additional restriction on since a different second moment may be absorbed into the choice of .

Minimal subsampling represents a very small subset of the much larger class of randomised algorithms outlined above. However, Theorem 1 below shows that minimal subsampling is essentially always at least as good as any algorithm from the wider class, which is perhaps surprising. A beneficial consequence of this result is that we only need to search for the optimal ways of selecting and ; the threshold is fixed at and the choice of the continuous distribution is inconsequential for minimal subsampling. The choices we give in Section 2.2 yield a subquadratic run time that approaches linear in when the interactions to be discovered are much stronger than the bulk of the remaining interactions.

a) b) c)

2.1 Optimality of minimal subsampling

In this section, we compare the run time of the algorithms in and that return strong interactions with high probability. Let be the indices of a strongest interaction pair, that is . We will consider algorithms with set to . Define the power of as

For , let

and define and analogously. Note that these classes depend on the underlying , which is considered to be fixed, and moreover that we are fixing . We consider an asymptotic regime where we have a sequence of response–predictor matrix pairs . Write for the corresponding interaction strengths, and let . Let be the probability mass function corresponding to drawing an element of uniformly at random. Note that has domain . We make the following assumptions about the sequence of interaction strength matrices .

-

(A1)

There exists such that .

-

(A2)

There exists , such that for all .

-

(A3)

There exists such that is non-increasing on .

Assumption (A1) is rather weak: typically one would expect the maximal strength interaction to be essentially unique, while (A1) requires that at most of order interactions have maximal strength. (A2) requires the maximal interaction strength to be bounded away from 0 and 1, which is the region where complexity results for the search of interactions are of interest. As mentioned earlier, if the maximal interaction strength is 1, it will always be retained in the close-pair sets , whilst if its strength is too close to 0, then it is near impossible to distinguish it from the remaining interactions. (A3) ensures a certain form of separation between maximal strength interactions and the bulk of the interactions.

To aid readability, in the following we suppress the dependence of quantities on in the notation. Given and , we may define as the expected number of computational operations performed by the algorithm corresponding to . We have the following result.

Theorem 1.

Given and , there exists such that for all we have

| (7) | ||||

| (8) |

and there exists such that

| (9) |

The theorem shows that the optimal run time is achieved when using minimal subsampling. The last point is surprising: setting , for example, will not improve the computational complexity over the brute-force approach and dense Gaussian projections hence do not reduce the complexity of the search. This is not caused by the larger computational effort involved in computing the dense projections: indeed even if these could be computed for free this result would remain. Rather the cost stems from the fact that dense projections have a much lower power for detecting true close pairs in the projected one-dimensional space.

2.2 The final version of xyz

The optimality properties of minimal subsampling presented in the previous section suggest the approach set out in Algorithm 2, which we will refer to as the xyz algorithm.

Here we are using a simplified version of the minimal subsampling proposal given in the previous section where we keep fixed rather than allowing it to be random. The reason is that the potential additional gain from allowing to be any one of two consecutive numbers with certain probabilities is minimal but necessary for Theorem 1 and so the simpler approach is preferable. We note that the uniform distribution in line 3 may be replaced with any continuous distribution to yield identical results.

To perform the equal pairs search in line 4, we sort the concatenation to determine the unique elements of . At each of these locations, we can check if there are components from both and lying there, and if so record their indices. This procedure, which is illustrated in Figure 2, gives us the set of equal pairs in the form of a union of Cartesian products. The computational cost is . This complexity is driven by the cost of sorting whilst the recording of indices is linear in . We note, however, that looping through the set of equal pairs in order to output a list of close pairs of the form would incur an additional cost of the size of , though in typical usage we would have .

Readers familiar with locality sensitive hashing (LSH) can find a short interpretation of equal pairs search as an LSH-family in the appendix. In the next section, we discuss in detail the impact of minimal subsampling on the complexity of the xyz algorithm and the discovery probability it attains.

2.3 Computational and statistical properties of xyz

We have the following upper bound on the expected number of computational operations performed by xyz (Algorithm 2) when the subsample size and number of repetitions are and :

| (10) |

The terms may be explained as follows: (i) construction of ; (ii) multiplying subsampled rows of and by ; (iii) finding the equal pairs; (iv) checking whether the interactions exceed the interaction strength threshold . Note we have omitted a constant factor from the upper bound . There is a lower bound only differing from (10) in the equal pairs search term (iii), which is instead of . It will be shown that (iv) is the dominating term and therefore the upper and lower bound are asymptotically equivalent, implying the bounds are tight.

An interaction with strength is retained in with probability . Hence it is present in the final set of interactions with probability

| (11) |

The following result demonstrates how the xyz algorithm can be used to find interactions whilst incurring only a subquadratic computational cost.

Theorem 2.

Let be the distribution function corresponding to a random draw from the set of interaction strengths . Given an interaction strength threshold , let . Define and let be defined by . We assume that . Finally given a discovery threshold let be the minimal such that . Ignoring constant factors we have

If and is bounded away from 1 we see that the dominant term in the above is

| (12) |

where . Typically we would expect to be such that as only the largest interactions would be of interest: thus we may think of as relatively small. If is such that is also larger than the bulk of the interactions, we would also expect to be small. Indeed, suppose that the proportion of interactions whose strengths are larger than is . Then . As a concrete example, if and is such that , the exponent in (12) is around 1.17, which is significantly smaller than the exponent of 2 that a brute-force approach would incur; see also the examples in Section 5. Note also that when , the exponent is 1 for all : if we are only interested in interactions whose strength is as large as possible, we have a run time that is linear in .

It is interesting to compare our results here with the run times of approaches based on fast matrix multiplication. By computing we may solve the interaction search problem (1). Naive matrix multiplication would require operations, but there are faster alternatives when . The fastest known algorithm (Williams, 2012) gives a theoretical run time of when . For xyz to achieve such a run time when for example, the target interaction strength would have to be : a somewhat moderate interaction strength. For , xyz is strictly better; we also note that fast matrix multiplication algorithms tend to be unstable or lack a known implementation and are therefore rarely used in practice. A further advantage is that the xyz algorithm has an optimal memory usage of .

We also note that whilst Theorem 2 concerns the the discovery of any single interaction with strength at least , the run time required to discover a fixed number interactions with strength at least would only differ by a multiplicative constant. If we however want a guarantee of discovering the strongest pairs the bound in Theorem 2 would no longer hold.

To minimise the run time in (12), we would like to be larger than most of the interactions in order that and hence be small, yet a smaller yields a more favourable exponent. Thus a careful choice of , on which depends, is required for xyz to enjoy good performance. In the following we show that an optimal choice of exists, and we discuss how this may be estimated based on the data.

Clearly if for some pair , we find another pair with but , we should always use rather than . It turns out that there is in fact an optimal choice of such that the parameter choice is not dominated by any others in this fashion. Define

| (13) |

where it is implicitly assumed that the minimiser is unique. This will always be the case except for peculiar values of .

Proposition 3.

Let . If has , then also with the final inequality being strict if and is a unique minimiser.

Thus there is a unique Pareto optimal . Although the definition of involves the moments of , this can be estimated by sampling from . We can then numerically optimise a plugin version of the objective to arrive at an approximately optimal .

3 Interaction search on continuous data

In the previous section we demonstrated how the xyz algorithm can be used to efficiently solve the simplest form of interaction search (1) when both and are binary. In this section we show how small modifications to the basic algorithm can allow it to do the same when is continuous, and also when is continuous. We discuss the regression setting in Section 4.

3.1 Continuous and binary

We begin by considering the setting where , but where we now allow real-valued . Without loss of generality, we will assume . The approach we take is motivated by the observation that the inner product can be interpreted as a weighted inner product of with the sign pattern of , using weights .

With this in mind, we modify xyz in the following way. We set to be . Let be i.i.d. such that . Forming the projection vector using (6), we then find the probability of being in the equal pairs set may be computed as follows.

where here is with respect to the randomness of (and, equivalently, the random indices ) with and considered fixed. The calculation above shows that the run time bound of Theorem 2 continues to hold in the setting with continuous provided we replace the interaction strengths with their continuous analogues .

As a simple example, consider the model

with and generated randomly having each entry drawn independently from each with probability . Then for a non-interacting pair , we have . For the pair we calculate an interaction strength of

Note that here that probability is over the randomness in the noise . A quick simulation gives the following table:

| 0.25 | 0.5 | 1 | 2 | 5 | ||

|---|---|---|---|---|---|---|

| 0.99 | 0.98 | 0.92 | 0.84 | 0.76 | 0.67 |

Using Theorem 2 and the above table we can estimate the computational complexity needed to discover the pair given a value of .

3.2 Continuous and continuous

The previous section demonstrated how resampling with non-uniform weights transforms a setup with continuous into one with binary response. If both and are continuous, we continue to use the previous strategy to deal with the continuous response. For the matrix with continuous predictor values we cannot use weighted resampling as the weights would depend on the interaction pair of interest. In the following we examine the effects of transformations of to a binary data matrix . To allow for randomized mappings, we define the transformations via a function as

where the transformation is always applied independently for each entry of the predictor matrix and for each subsample.

The following gives the probability of agreeing in sign with when is sampled with probability proportional to .

Proposition 4.

Given the transform and sampling an index according to , then the probability of a match is

| (14) |

Thus we may define a continuous analogue of the interaction strength based on the transform given by as

These quantities may be substituted into Theorem 2 to yield the following upper bound on expected run time when using xyz on transformed data.

Corollary 5.

Let be the distribution function corresponding to a random draw from the set of interaction strengths . Given an interaction strength threshold , let . Define and let be defined by . We assume that . Finally given a discovery threshold let be the minimal such that . Ignoring constant factors we have

The expected computational costs depends critically on the distribution of the interaction strengths . To gain a better understanding of what impact different transformations have on this distribution and subsequently on run time we will study the following simple model for :

| (15) |

where the are independent and have identical sub-exponential distributions symmetric about 0 and the rows of are i.i.d. We now introduce two practically useful choices of and study their properties in the context of model (15).

The unbiased transform

A natural choice for the transform is one that satisfies the unbiasedness requirement:

| (16) |

It turns out that this requirement uniquely defines the transform, which we refer to as the unbiased transform.

Proposition 6.

Proposition 6 shows that is a monotone function of the inner product .

We remark that if the entries of do not lie in , we may divide each entry in the th row by , and multiply by , for each . Proposition 6 will then hold for the scaled versions of and . In order to describe the performance of the unbiased transform when applied to data generated by the model (15), we define the following quantities:

We consider an asymptotic regime where may diverge as tends to infinity, though we suppress this in the notation. We introduce the following assumptions.

-

(B1)

, for and .

-

(B2)

The noise level satisfies the bound

-

(B3)

Let be such that be such that

(B1) ensures non-interactions are not too strongly correlated to the actual interaction pair . Note that (B3) allows for high-dimensional settings with .

Theorem 7.

Assume all entries of have mean zero and lie in almost surely. Further assume (B1)–(B3) hold. When and are as in Corollary 5 and the unbiased transform is used, we have

for any . Here is with respect to the randomness in and .

Though the run time above can often improve significantly on the worst-case quadratic run time, observe that unlike in the binary case, if there is no noise and , we do not necessarily have a run time close to linear in . For example, when , the interaction strength of the true interaction can be shown to equal to

Substituting this into the run time given by Theorem 2, this would result in an expected complexity of roughly ; this is still substantially smaller than a quadratic run time, but raises the question as to whether such a loss in speed is avoidable.

Additionally, if has several outlying entries, normalising the design matrix by scaling by the row-wise maximums can shrink towards . To limit the impact of this normalisation, we can first cap the entries of so their absolute value is bounded by some . Though the resulting interaction strength will not have the form given in Proposition 6, it may better discriminate between interactions of interest and noise.

Capping with is closely related to applying the sign transform, which we study next.

The sign transform

We now consider the sign transform given by ; if there are zero cases we use a coin toss to map them to . For the sign transform we have and so the interaction strength is given as:

The sign transform recovers the close to linear run time achieved in the binary case when a interaction is perfect as now if , we have . Also the sign transform is not adversely affected by the presence of outlying entries in , and for our theory we can relax the assumption that the entries of are in to here only requiring that they have a subexponential distribution. To facilitate comparison with the unbiased transform, we impose assumptions analogous to (B1)–(B3):

-

(C1)

, for and .

-

(C2)

The noise level satisfies

-

(C3)

Let be such that

Theorem 8.

Suppose that each entry of has a mean-zero subexponential distribution. Further assume (C1)–(C3). When and are as in Corollary 5 and the sign transform is used, we have

for any . Here is with respect to the randomness in and .

Both transforms yield a run time of the form . Comparing the exponents we have:

-

unbiased transform:

-

sign transform:

For bounded data and when , we have so that whereas . Hence in case of a strong signal the sign transform can give a smaller run time than the unbiased transform.

4 Application to Lasso regression

Thus far we have only considered the simple version of the interaction search problem (1) involving finding pairs of variables whose interaction has a large dot product with . In this section we show how any solution to this, and in particular the xyz algorithm, may be used to fit the Lasso (Tibshirani, 1996) to all main effects and pairwise interactions in an efficient fashion.

Given a response and a matrix of predictors , let be the matrix of interactions defined by

We will assume that and the columns of have been centred. Note that the centring of means the implicitly contains main effects terms. Let be a version of with centred columns. Consider the Lasso objective function

| (17) |

Note that since the entire design matrix in the above is column-centred, any intercept term would always be zero.

In order to avoid a cost of it is necessary to avoid explicitly computing . To describe our approach, we first review in Algorithm 3 the active set strategy employed by several of the fastest Lasso solvers such as glmnet (Friedman et al., 2010). We use the notation that for a matrix and a set of column indices , is the submatrix of formed from those columns indexed by . Similarly for a vector and component indices , is the subvector of formed from the components of indexed by .

As the sets and would be small, computation of the Lasso solution in line 3 is not too expensive. Instead line 4, which performs a check of the Karush–Kuhn–Tucker (KKT) conditions involving dot products of all interaction terms and the residuals, is the computational bottleneck: a naive approach would incur a cost of at this stage.

There is however a clear similarity between the KKT conditions check for the interactions and the simple interaction search problem (1). Indeed the computation of , the set containing all interactions that violate the KKT conditions, may be expressed in the following way:

| (18) |

Note that since is necessarily centered, there is no need to center the interactions in (18). In order to solve (18) we can use the xyz algorithm, setting in Algorithm 2 to and to each of in turn.

Precisely the same strategy of performing KKT condition checks using xyz can be used to accelerate computation for interaction modeling for a variety of variants of the Lasso such as the elastic net (Zou and Hastie, 2005) and -penalised generalised linear models. Note also that it is straightforward to use a different scaling for the penalty on the interaction coefficients in (17), which may be helpful in practice.

5 Experiments

To test the algorithm and theory developed in the previous sections, we run a sequence of experiments on real and simulated data.

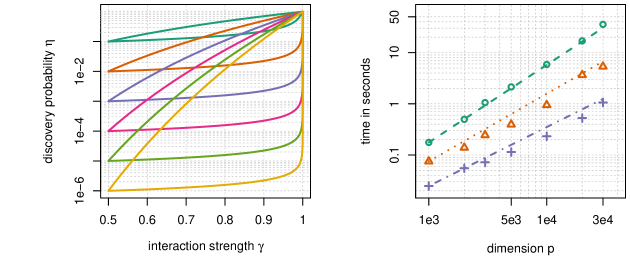

5.1 Comparison of minimal subsampling and dense projections

One of the surprising outcomes of our theoretical analysis is extent of the suboptimality of Gaussian random projections, which whilst they suffice for the conclusion of the Johnson–Lindenstrauss Lemma, are not well-suited for our purposes here (see Theorem 1). We can explicitly compute the probability of retaining an interaction of strength in for both dense Gaussian projections and minimal subsampling given an equal computational budget. We consider various values of ranging from up to and we fix . We set and select other parameters of the algorithms to ensure the average size of is equal to in the setting when all interaction strengths are equal to 0.5. Specifically we make the following choices.

-

•

: the close pairs threshold is the –quantile of the distribution of when .

-

•

: the subsample size .

We then plot the probability of discovering an interaction of strength , as a function of for different values of (Figure 3). For , is given in equation (11). For , is the –quantile of the distribution of when .

5.2 Scaling

In this experiment we test how the xyz algorithm scales on a simple test example as we increase the dimension . We generate data with each entry sampled independently uniformly from . We do this for different values of , ranging from to : this way for the largest considered there are more than million possible interactions. Then for each we construct response vectors such that only the pair is a strong interaction with an interaction strength taking values in . Through this construction, if is large enough, all the pairs except will have an interaction strength around , and very few will have one above . We thus set so that . Since the only strong interaction is , we set Each data set configuration determined by and is simulated times and we measure the time it takes xyz to find the pair . In Figure 3 we plot the average run time against the dimension with the different choices for highlighted in different colours.

Theorem 2 indicates that the run time should be of the order . We see that the experimental results here are in close agreement with this prediction.

5.3 Run on SNP data

In the next experiment we compare the performance of xyz to its closest competitors on a real data set. For each method we measure the time it takes to discover strong interactions. We consider the LURIC data set (Winkelmann et al., 2001), which contains data of patients that were hospitalised for coronary angiography. We use a preprocessed version of the data set that is made up of observations and predictors. The data set is binary. The response indicates coronary disease ( corresponding to affected and healthy) and contains Single Nucleotide Polymorphisms (SNPs) which are variations of base-pairs on DNA. The response vector is strongly unbalanced: there are affected cases () and unaffected ().

To get a contrast of the performance of xyz we compare it to epiq (Arkin et al., 2014), another method for fast high-dimensional interaction search. In order for epiq to detect interactions it needs to assume the model

| (19) |

where . It then searches for interactions by considering the test statistics

where . These are used to try to find the pair , which is assumed to be the pair for which the inner product is maximal. It is an easy calculation to show that . To maximise the inner product on the right, epiq considers pairs where is large by looking at pairs where both and are large. While the approach of epiq is somewhat related to xyz, there are no bounds available for the time it takes to find strong interactions.

We also compare both methods to a naive approach where we subsample a fixed number of interactions uniformly at random, and retain the strongest one. We refer to this as naive search.

At fixed time intervals we check for the strongest interaction found so far with all three methods. We plot the interaction strength as a function of the computational time (Figure 4). All three methods eventually discover interactions of very similar strength and it would be a hasty judgement to say whether one significantly outperforms the others. xyz nevertheless discovers the strongest interactions on average for a fixed run time compared to the other two approaches. To get a clearer picture we run two additional experiments on a slight modification of the LURIC data set. We implant artificial interactions where we set the strength to and another example with . In these two experiments xyz clearly outperforms all other methods considered (Figure 4; panels 3 and 4). Besides xyz being the fastest at interaction search, it also offers a probabilistic guarantee that there are no strong interactions left in the data. This guarantee comes out of Theorem 2. To run xyz we have to calculate the optimal subsample size (13) for use of minimal subsampling:

The sum in this optimisation can be approximated by uniformly sampling over pairs. Assume we have an interaction pair with interaction strength and say the rest of the pairs have an interaction strength of no more than . The probability that we discover this pair in one run () of the xyz algorithm is . Therefore the probability of missing this pair after runs is given by

Note that the number of possible interactions is . The whole search took seconds. Naive search offers a similar guarantee, however it is extremely weak. The probability of not discovering the pair after drawing samples (with ) is bounded by .

If we consider the run time guarantee from Theorem 2, the dominating term in the complexity of xyz in terms of is

This may be compared to the expected run time of order for naive search, which means that xyz is about times faster than naive search (when ). In the empirical comparison this factor is around .

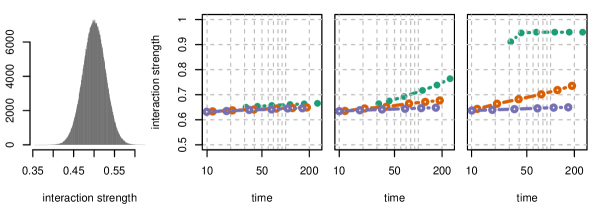

5.4 Regression on artificial data

In this section we demonstrate the capabilities of xyz in interaction search for continuous data as explained in Section 3. We simulate two different models of the form (15):

We consider three settings. For all three settings we have . We let . Each row of is generated i.i.d. as . The magnitudes of both the main and interaction effects are chosen uniformly from the interval ( main effects and interaction effects) and we set . The three settings we consider are as follows.

-

1.

, we generate a hierarchical model: and . We first sample the main effects and then pick interaction effects uniformly from the pairs of main effects.

-

2.

, we generate a strictly non-hierarchical model: and . We first sample the main effects and then pick interaction effects uniformly from all pairs excluding main effects as coordinates.

-

3.

We repeat the setting with a data set that contains strong correlations. We create a dependence structure in , by first generating a DAG with on average edges per node. Each node is sampled so that it is a linear function of its parents plus some independent centred Gaussian noise, with a variance of the variance coming from the direct parents. The resulting correlation matrix then unveils for each variable a substantial number of variables strongly correlated to (There is usually around variables with a correlation of above ). Such a correlation structure will make it easier to detect pairs of variables whose product can serve as strong predictor of , even though it has not been included in the construction of .

We run three different procedures to estimate the main and interaction effects.

-

•

Two-stage Lasso: We fit the Lasso to the data, and then run the Lasso once more on an augmented design matrix containing interactions between all selected main effects. Complexity analysis of the Least Angle Regression (LARS) algorithm (Efron et al., 2004) suggests the computational cost would be , making the procedure very efficient. However, as the results show, it struggles in situations such as that given by model 2, where a main effects regression will fail to select variables involved in strong interactions.

-

•

Lasso with all interactions: Building the full interaction matrix and computing the standard Lasso on this augmented data matrix. Analysis of the LARS algorithm would suggest the computational complexity would be in the order . Nevertheless, for small , this approach is feasible.

-

•

xyz: This is Algorithm 3; we set the parameter to be in order to target the strong interactions.

The experiment (seen in Figure 5) shows that xyz enjoys the favourable properties of both its competitors: it is as fast as the two-stage Lasso that gives an almost linear run time in , and it is about as accurate as the estimator calculated from screening all pairs (brute-force).

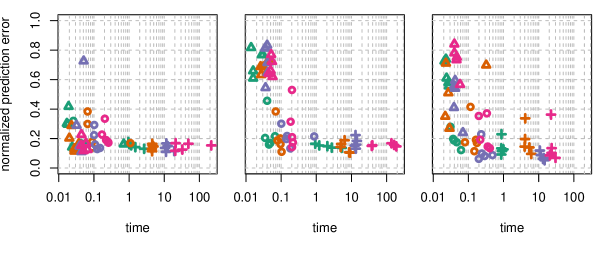

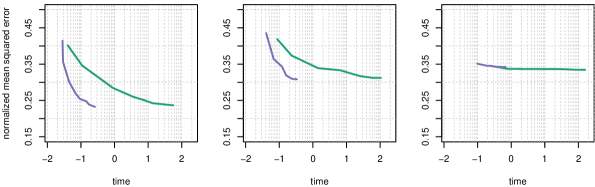

5.5 Regression on real data

Here we run xyz regression on continuous real data sets where the ground truth is unknown. On each data set we pick at random variables and run xyz and the Lasso implemented in glmnet with all interactions included. We subsample an increasing number of variables to vary the difficulty of the regression problem. For each sample we measure the run time and the normalized out of sample squared error:

Experiments are run on the following three different data sets:

-

•

Riboflavin: The Riboflavin production data set (Bühlmann et al., 2014) contains samples and predictors (gene-expressions). The response and the design are both continuous.

-

•

Kemmeren: The Kemmeren (Kemmeren and et al., 2014) data set records knockouts of genes. The data is continuous. We sample randomly from the genes not present in the subsample taken from .

-

•

Climate: The climate data set from the CNRM model from the CMIP5 model ensemble (Knutti et al., 2013) simulates the temperature of points on the northern hemisphere which is recorded in . The response simulates the temperature on a random position on the southern hemisphere. The data contains observations.

For each experiment we fix the number of runs to so the run time of xyz is . The experiments show that the xyz algorithm has a similar prediction performance to the Lasso applied to all interactions as implemented in glmnet. However xyz is around times faster for . The results of all 6 experiments can be seen in Figure 6.

6 Discussion

In this work we exploited a relationship between closest pairs of point problems and interaction search. By solving the former problem using random projections to project points down to a one-dimensional space and then sorting the resulting projected points, we were able to produce an algorithm for interaction search that enjoys a run time that is sub quadratic under mild assumptions and when used to search for very strong interactions can be almost linear. Though we have looked at interaction search in this paper, the basic engine for computing the large inner products between collections of vectors may have other interesting applications, for example in large-scale clustering problems. We hope to study such applications in future work.

Table of frequently used notation

| number of observations and number of variables | ||

| predictor matrix and response vector | ||

| th variable / column of | ||

| coefficients of main effects and interaction effects | ||

| interaction strength of the pair | ||

| distribution of projection | ||

| subsample size | ||

| projection vector | ||

| number of projections | ||

| close pairs threshold and interaction strength threshold | ||

| set of all configurations of the xyz algorithm, the elements of this set are denoted by | ||

| probability that a given interaction is present in the output of the xyz algorithm | ||

| binarized version of | ||

| predictor matrix containing all possible interaction pairs |

Appendix A

Here we include proofs that were omitted earlier.

Proof of Theorem 1

In the following, we fix the following notation for convenience:

Note that both and depend on though this is suppressed in the notation. Also define and . We will reference the parameters levels contained in as and . If then we will write for the distribution of the subsample size .

If we let denote the complexity of the search for -close pairs, similarly to (10) we have that

| (20) |

where are constants. Suppose and have . Then since searching for -close pairs is at least as computationally difficult as finding equal pairs we know that .

Similarly for we have

| (21) |

For , define

where is the set of candidate interactions when . Note that

Thus any with minimal must have as the smallest such that , whence

| (22) |

Note that does not depend on , so the above equation completely determines the optimal choice of once other parameters have been fixed. We will therefore henceforth assume that has been chosen this way so that the discovery probability of all the algorithms is at least .

The proofs of (8) and (9) are contained in Lemmas 12 and 13 respectively. The proof of (7) is more involved and proceeds by establishing a Neyman–Pearson type lemma (Lemmas 10 and 11) showing that given a constraint on the ‘size’ that is sufficiently small, minimal subsampling enjoys maximal ‘power’ . To complete the argument, we show that any sequence of algorithms with size remaining constant as cannot have a subquadratic complexity, whilst Lemma 12 attests that in contrast minimal subsampling does have subquadratic complexity under the assumptions of the theorem. Several auxiliary technical lemmas are collected in Section Technical lemmas

Our proofs Lemmas 10 and 11 make use of the following bound on a quantity related to the ratio of the size to the power of minimal subsampling.

Lemma 9.

Suppose has distribution for placing mass on and . Under the assumptions of Theorem 1,

Proof.

We have

Now the sum on the RHS is maximised over obeying constraints (A1) and (A2) in the following way. If then places all available mass on . Otherwise should be as close to constant as possible on , and zero below . In both cases it can be seen that

∎

The following Neyman–Pearson-type lemma considers only non-randomised algorithms in . In Lemma 11 we extend this result to randomised algorithms.

Lemma 10.

Let be the set of such that places mass only on a single , so the subsample size is not randomised. There exists an independent of such that for all , we have

Moreover the suprema are achieved.

Proof.

Each is parametrised by its close pairs threshold and subsample size . Given a with parameter values and we compute as follows. Note that by replacing the threshold by , we may assume that and have entries in . Thus has components in . Let be the number of non-zero components of . Then . Thus

noting that . By Lemma 14 we know there exists an such that for all the RHS is bounded below by

| (23) |

for sufficiently large. Here the constants and depend only on .

Consider . In this case, for sufficiently large we have by Lemma 14

However then for sufficiently large,

so . Note also that we must have , so . Thus by choosing sufficiently small, we can rule out and so we henceforth assume that , and that is sufficiently large such that (23) holds for all .

We have

| (24) |

Similarly we have

| (25) |

Now substituting the upper bound on implied by (24) into (25), we get

where

Now by Lemma 15, for sufficiently large and some constant we have

Thus

| (26) |

for all sufficiently large. Now given , let be such that

Consider the minimal subsampling algorithm that chooses subsample size as either or with probabilities and such that

Then we have . Now suppose has . Then in particular . We first examine the case where . Then

using Lemma 9 in the final line. Note this is non-negative for sufficiently large. When we instead have

for sufficiently large. Recall that by making sufficiently small, we can force to be arbitrarily large. Thus the result is proved. ∎

Lemma 11.

There exists an independent of such that for all , we have

Moreover the suprema are achieved.

Proof.

With a slight abuse of notation, write for the element of that fixes and . Using the notation of Lemma 10, define function by

Note that for we have

| (27) |

Now by Lemma 10 we know there exists (depending on ) such that on , is the linear interpolation of points

We claim that is concave on . Indeed, it suffices to show that the slopes of the successive linear interpolants are decreasing in this region, or equivalently that their reciprocals are increasing. We have

| (28) |

which increases as decreases, thus proving the claim.

Note also that the RHS of (28) is at most when has subsample size fixed at . Thus by Lemma 9 we see the derivatives of the linear interpolants approach infinity as they get closer to the origin. This implies the existence of an such that , where denotes the subdifferential of the function at . We may therefore invoke Lemma 16 to conclude that for with

Combining with (27) gives the result. ∎

The next lemma establishes subquadratic complexity of minimal subsampling.

Lemma 12.

Under the assumptions of Theorem 1, we have .

Proof.

Let be such that places all mass on . We have that . Thus using the inequality for , we have

Lemma 9 gives an upper bound on . Note that . Thus ignoring constant factors, we have

Taking then ensures . ∎

Lemma 13.

Let . There exists and such that for all ,

Proof.

Each is parametrised by its close pairs threshold . Given a with close pairs threshold we compute as follows. Similarly to Lemma 10 we may assume without loss of generality that and have entries in so has components in . Since as , we have

We now use Lemma 14. For sufficiently large, when the RHS is bounded below by

Here constant also depend only on . Thus

| (29) |

Similarly we have

| (30) |

Note that from (29), when we have . Thus from (21) we know there exists such that for all , we have

| (31) |

We therefore need only consider the case where and where .

Proof of Theorem 1

The proofs of (8) and (9) are contained in Lemmas 12 and 13 respectively. To show (7) we argue as follows. Given and , suppose for contradiction that there exists a sequence and such that (making the dependence on of the computational time explicit)

for all . By Lemma 12, we must have . This implies that . By Lemma 11, we know that for sufficiently large

Let be the maximiser of the LHS. In order for , it must be the case that . However we claim that minimises among all with , which gives a contradiction and completes the proof. Let be the function that linearly interpolates the points

Note that is decreasing. By considering the inverse of it is clear that is convex. With a slight abuse of notation, write for the element of such that places all mass on and . Note that

Now suppose has . Then from the above and Jensen’s inequality,

Proof of Theorem 2

Proof of Proposition 3

Let . Note that in order for it must be the case that . Therefore

| (32) | ||||

Moreover, the inequality leading to (32) is strict if is the unique minimiser and .

Technical lemmas

Lemma 14.

Let and suppose is an i.i.d. sequence with .

Then for all , there exists and such that for all and we have

Proof.

Let be the density of . Note that as , we must have , so we may assume without loss of generality that . Then by Theorem 3 of Petrov (1964) we have that for sufficiently large ,

| (33) |

Here is a constant and is the standard normal density. Now by the mean value theorem, we have

Thus from (33), for sufficiently large we have

Note that for and sufficiently large we have , whence

for , some . A similar argument yields the upper bound in the final result. ∎

Lemma 15.

Suppose . For all we have

| (34) |

Given and , there exists and such that for all we have

| (35) |

Proof.

First we show the upper bound (34). Let .

Next, by Jensen’s inequality we have . We now compute as follows.

Putting things together gives (34).

Turning now to (35), we see that the LHS equals

By Jensen’s inequality we have

But as , , which easily gives the result. ∎

Lemma 16.

Let be non-decreasing. Suppose there exists such that:

-

(i)

is concave on ;

-

(ii)

, where denotes the subdifferential of the function at .

Then if random variable has , then .

Proof.

Write Let function be defined as follows.

Note that thus defined has . We see that is convex and . Thus if , by Jensen’s inequality we have

∎

Appendix B

Connection to LSH

Minimal subsampling as considered in Algorithm 2 is closely related to the locality-sensitive hashing (LSH) framework: Define ( corresponds to the minimal subsampling projection) to be the hashing function and to be the family of such functions, from which we sample uniformly. Then is -sensitive, that is:

where . In the case of the minimal subsampling we have and . However, the typical LSH machinery cannot be applied directly to the equal pairs problem above. In our setting, we are not interested in preserving close pairs but rather the closest pairs. Theorem 1 establishes that the family leads to the maximal ratio among all linear hashing families.

Appendix C

Proof of Proposition 4

Proof.

∎

Appendix D

The unbiased transform and the sign transform

Proposition 6

Proof.

The equation

implies

This uniquely determines the unbiased transform. ∎

Lemma 17.

Consider the setup of Theorem 7. Then there exists constants such that defining

with probability at least we have:

Proof.

First we consider a capped version of :

where is to be chosen later. We may apply Hoeffding’s inequality to these bounded variables. We have to bound two terms:

Schematically the first term can be dealt with in the following way:

| (36) |

where

We deal with each term individually. Using Hoeffding’s inequality we get:

-

-

-

-

.

This gives us a bound of the interaction strength of the true interaction pair:

Similarly we can treat the interaction strength of the non interacting pairs:

-

Here we use assumption :

Hence,

For the rest we run the same bounds as before (using ). This yields the bound

The above inequality needs to hold for all at most pairs that are not interactions, so that we effectively multiply the exponential terms with . Another factor of is multiplied in for the negative sign, as the fraction also has to be bounded away from . In total we thus have:

| with probability at least |

Finally, let , then we have to set and so that the probability is bigger than . This gives:

This gives

Thus for ,

| with probability at least |

Now we extend this result to the case of unbounded errors, that is we now assume that with high probability are bounded:

Here we used the sub-exponential tail behavior of . We have . Hence we set

Thus,

with probability at least we have:

∎

Next we prove the equivalent result for the sign transform. The proof is very similar to the unbiased case:

Lemma 18.

Consider the setup of Theorem 8. Then there exists constants such that defining

with probability at least we have:

Proof.

First consider capped versions of the random variables of interest:

where and are to be chosen later. Given these capped variables we can use Hoeffding’s inequality as we now deal with bounded variables. We have to bound two terms:

We deal with each term individually. Using Hoeffding’s inequality we get:

This gives us a bound of the interaction strength of the true interaction pair:

Similarly we can treat the interaction strength of the non interacting pairs:

-

Here we use assumption . It implies

This we use for computing the expectation:

Thus the expectation is given as:

Hence,

For the rest we use the same bounds as before (using ). This yields the bound

The above inequality needs to hold for the at most pairs that are not interactions, so that we effectively multiply the exponential terms with . Another factor of is multiplied in for the negative sign, as the fraction also has to be bounded away from . In total we thus have:

| with probability at least |

Finally we have to set and so that the probability is bigger than . This gives:

This gives

Thus for

| with probability at least |

We now extend this result to the case of unbounded variables, that is we now assume that with high probability the variables and are bounded:

Here we used the sub-exponential tail behaviour of the and . There exists constants , such that and similarly for . Hence we set

Thus we have

∎

Next we prove Theorem 7:

Proof.

The proof of Theorem 8 is very similar and is thus omitted.

References

- Achlioptas [2003] D. Achlioptas. Database-friendly random projections: Johnson–lindenstrauss with binary coins. Journal of computer and System Sciences, 2003.

- Agarwal et al. [1991] P. Agarwal, H. Edelsbrunner, O. Schwarzkopf, and E. Welzl. Euclidean minimum spanning trees and bichromatic closest pairs. Discrete & Computational Geometry, 1991.

- Arkin et al. [2014] Y. Arkin, E. Rahmani, M. Kleber, R. Laaksonen, W. März, and E. Halperin. Epiq: efficient detection of snp–snp epistatic interactions for quantitative traits. Bioinformatics, 2014.

- Bickel et al. [2010] P. Bickel, Y. Ritov, and A. Tsybakov. Hierarchical selection of variables in sparse high-dimensional regression. IMS Collections, 2010.

- Bien et al. [2013] J. Bien, J. Taylor, and R. Tibshirani. A lasso for hierarchical interactions. The Annals of Statistics, 2013.

- Breiman [2001] L. Breiman. Random Forests. Machine Learning, 2001.

- Breiman et al. [1984] L. Breiman, J. Friedman, R. Olshen, and C. Stone. Classification and Regression Trees. Wadsworth, Belmont, 1984.

- Bühlmann et al. [2014] P. Bühlmann, M. Kalisch, and L. Meier. High-dimensional statistics with a view towards applications in biology. Annual Review of Statistics and Its Application, 2014.

- Davie and Stothers [2013] A. Davie and A. Stothers. Improved bound for complexity of matrix multiplication. Proceedings of the Royal Society of Edinburgh: Section A Mathematics, 2013.

- Efron et al. [2004] B. Efron, T. Hastie, I. Johnstone, and R. Tibshirani. Least Angle Regression. Annals of Statistics, 2004.

- Friedman [1991] J. Friedman. Multivariate adaptive regression splines. Annals of Statistics, 1991.

- Friedman et al. [2010] J. Friedman, T. Hastie, and R. Tibshirani. Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 2010.

- Hao and Zhang [2014] N. Hao and H. Zhang. Interaction screening for ultrahigh-dimensional data. Journal of the American Statistical Association, 2014.

- Indyk and Motwani [1998] P. Indyk and R. Motwani. Approximate nearest neighbors: towards removing the curse of dimensionality. In Proceedings of the thirtieth annual ACM symposium on Theory of computing, pages 604–613. ACM, 1998.

- Kemmeren and et al. [2014] P. Kemmeren and et al. Large-scale genetic perturbations reveal regulatory networks and an abundance of gene-specific repressors. Cell, 2014.

- Knutti et al. [2013] R. Knutti, D. Masson, and A. Gettelman. Climate model genealogy: Generation cmip5 and how we got there. Geophysical Research Letters, 2013.

- Kong et al. [2016] Y. Kong, D. Li, Y. Fan, and J. Lv. Interaction Pursuit with Feature Screening and Selection. arXiv preprint arXiv:1605.08933, 2016.

- Le Gall [2012] F. Le Gall. Faster algorithms for rectangular matrix multiplication. In Foundations of Computer Science (FOCS), 2012 IEEE 53rd Annual Symposium on. IEEE, 2012.

- Leskovec et al. [2014] J. Leskovec, A. Rajaraman, and J. Ullman. Mining of massive datasets. Cambridge University Press, 2014.

- Paturi et al. [1989] R. Paturi, S. Rajasekaran, and J. Reif. The light bulb problem. Proceedings of the second annual workshop on Computational learning theory, 1989.

- Petrov [1964] V. Petrov. On local limit theorems for sums of independent random variables. Theory of Probability & Its Applications, 1964.

- Sedgewick [1998] R. Sedgewick. Algorithms in C. Addison-Wesley, 1998.

- Shah [2016] R. Shah. Modelling interactions in high-dimensional data with backtracking. Journal of Machine Learning Research, 2016.

- Shah and Meinshausen [2014] R. Shah and N. Meinshausen. Random intersection trees. The Journal of Machine Learning Research, 2014.

- Shamos and Hoey [1975] M. Shamos and D. Hoey. Closest-point problems. In Foundations of Computer Science, 1975., 16th Annual Symposium on. IEEE, 1975.

- Strassen [1969] V. Strassen. Gaussian elimination is not optimal. Numerische Mathematik, 1969.

- Thanei [2016] G. Thanei. xyz r package, 2016. URL https://github.com/gathanei/xyz.

- Tibshirani [1996] R. Tibshirani. Regression Shrinkage and Selection via the Lasso. Journal of the Royal Statistical Society, Series B, 1996.

- Williams [2012] V. Williams. Multiplying matrices faster than coppersmith-winograd. In Proceedings of the forty-fourth annual ACM symposium on Theory of computing. ACM, 2012.

- Winkelmann et al. [2001] B. Winkelmann, W. März, B. Boehm, R. Zotz, J. Hager, P. Hellstern, and J. Senges. Rationale and design of the luric study-a resource for functional genomics, pharmacogenomics and long-term prognosis of cardiovascular disease. Pharmacogenomics, 2001.

- Wu et al. [2010] J. Wu, B. Devlin, S. Ringquist, M. Trucco, and K. Roeder. Screen and clean: a tool for identifying interactions in genome-wide association studies. Genetic Epidemiology, 2010.

- Zou and Hastie [2005] H. Zou and T. Hastie. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society, Series B, 2005.