A note on Jump Atlas Models

Abstract.

The market weight of a stock is its capitalization (cap) divided by the total market cap. Rank these weights from top to bottom. The capital distribution curve is a plot of weights versus ranks. For the US stock market, it is linear on a double logarithmic scale, and stable with respect to time (Fernholz, 2002). This property has been captured by models with rank-dependent dynamics: Each stock’s cap logarithm is a Brownian motion with drift and diffusion coefficients depending on its current rank (Chatterjee, Pal, 2010). However, short-term stock movements have heavy tails. One can add jumps to Brownian motions to capture this. Observed time stability follows from a long-term stability result, stated and proved here. Via simulations, we find which properties of continuous models are preserved after adding jumps.

Key words and phrases:

Lévy process, capital distribution curve, competing Brownian particles, stationary distribution2010 Mathematics Subject Classification:

60J60, 60J51, 60J75, 60H10, 60K35, 91B261. Introduction

1.1. Motivation and definitions

A market model is a collection of positive real-valued continuous-time random processes : The capitalization of the th stock at time is given by . The total capitalization of the stock market is , and the market weight of the th stock at time is

| (1) |

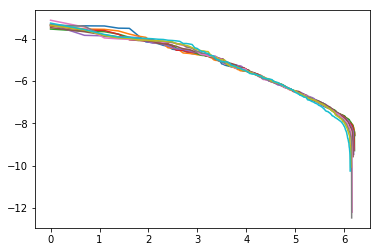

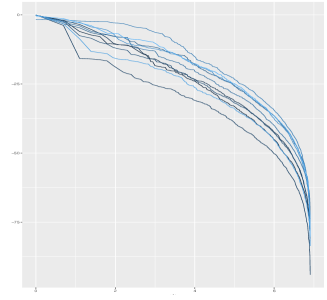

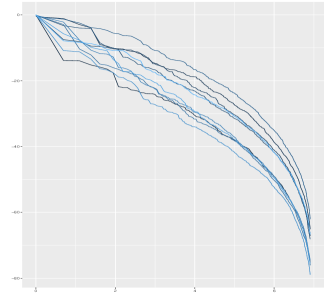

Rank these market weights from top to bottom: . [12, Chapter 5, page 95] contains the double logarithmic plot of ranked market weights , December 31, 1929–1999 (8 plots, every 10 years), stocks from the Center of Research in Securities Prices at the University of Chicago. This plot exhibits two features:

-

(A)

It is stable over time: It is almost the same for all .

-

(B)

It is close to a straight line, except at lower and upper ends.

We reproduce this (and see the same properties) in Figure 1 for the S&P 500 stocks included in this index as of May 9, 2019, in December 31, 2009–2018, using the data from the YCharts database. (The code is given on GitHub.) These observations (a) and (b) were explained by the following rank-based model in [3].

We introduce a few pieces of notation. The Dirac delta measure at point is denoted by . For a vector , its ranking permutation for the vector is defined as the unique permutation on such that:

-

•

for (this permutation is ranking the vector ).

-

•

if and , then (ties resolved in lexicographic order).

We rank from bottom to top, except market weights, ranked from top to bottom.

Definition 1.

Take continuous adapted random processes . Rank them at each time from bottom to top: for ; . If they satisfy a system of stochastic differential equations:

| (2) |

with independent Brownian motions, and constant numbers and , then is called a system of competing Brownian particles; with drift and diffusion coefficients for rank equal to and . The gap process is defined as

| (3) |

Weak existence and uniqueness in law for this system is proved in [3]. Take such a system of competing Brownian particles, and consider the following market model:

| (4) |

Definition 2.

A stationary distribution, or invariant measure, for the gap process , is any probability measure in the orthant such that implies for every . This measure is sometimes called a stationary gap distribution. The gap process is called stable if it has a unique stationary distribution , and we have:

| (5) |

We introduce the following notation. For any vector , we define two other vectors: running average , and centered vector :

| (6) |

From (6), we have the following algebraic relation:

| (7) |

Assume the average drift for the bottom-ranked particles is greater than the average drift for all particles.

| (8) |

Under this condition (8), it was proved in [3, 4] that the gap process is stable. This has the following intuition: The drift of the “cloud” composed of bottom-ranked particles is larger than the drift for all particles; therefore, the bottom-ranked particles and the top-ranked particles cannot eventually separate into two “clouds”. Multiplying the numerator and the denominator of (1) by , we see that the ranked market weights from (1) can be computed from this gap process in (3), and vice versa. Thus the vector of ranked market weights

| (9) |

has a unique stationary distribution (which is a push-forward of ), and a stability result similar to (5) holds. For the case (for some ), the distribution is a product of exponentials, [4]. The exponential distribution with rate is denoted by ; and for , this distribution takes the form

For the Atlas model (named after the ancient Atlas hero, holding the sky on his shoulders)

| (10) |

the limiting shape (as ) of the double logarithmic plot of ranked market weights from (9) is essentially a straight line, see [9]. (The precise statement is a bit more complicated.)

However, this model (2) has one disadvantage: Fluctuations of real-world stock prices are not well described by Gaussian distributions. Instead, these prices make occasional large jumpsm and fluctuations have heavy tails. This is captured by adding jump components to random processes describing the stock market dynamics. An important class of stock price models contains Lévy processes, which are generalizations of a Brownian motion: for can have some distribution other than Gaussian. In this case, the trajectories are not continuous. (A Brownian motion is the only example of a Lévy process with continuous trajectories.) Here is an example of a Lévy process.

Definition 3.

A compound Poisson process , where are independent identically distributed random variables, and is a Poisson process with rate , independent of : That is, for is distributed as a Poisson random variable with mean , and is independent of . If is the distribution of , then is called the spectral measure.

The sum of a compound Poisson process and a Brownian motion with drift and diffusion is also a Lévy process. In fact, every Lévy process with finitely many jumps on a finite time interval can be represented in this way. We say that this Lévy process is associated with triple .

Definition 4.

For every , let be a Lévy process associated with the triple , ; that is, we can express each as follows:

| (11) |

where is a Brownian motion, is a Poisson process with rate , independent of , and are i.i.d. random variables, independent of and . The processes are assumed to be independent. Modifying (2) as follows:

| (12) |

we get a system of competing Lévy particles.

In this article, we have the following goals:

- (1)

-

(2)

To find an explicit stationary distribution for the gap process, and the corresponding stationary distribution for the vector of ranked market weights (9);

-

(3)

To show that for some choice of parameters , the capital distribution curve for a large number of companies is close to the straight line.

We accomplish Goal 1 by proving a (slightly more general) result: Theorem 1.1. We accomplish Goal 3 by simulations of these particle systems. We are unable to accomplish Goal 2 in exact form: It was shown in [14] that a stationary distribution for a reflected Brownian motion with jumps in the orthant (of which the gap process is a particular case) does not have a product form. Instead, we perform numerical simulations, find empirical properties of the stationary gap distribution, and compare it to models without jumps.

Often, jumps in financial models are modeled using Lévy processes with infinitely many jumps on a finite time interval, for example -stable processes, see [11]. Such Lévy process cannot be represented as a sum of a Brownian motion and a compound Poisson process. It is important to establish results for these models. But the fluctuations of such processes do not have a second moment, and this makes modifying the proof in Section 3 quite difficult.

1.2. The main stability result

The condition (8) for a system with jumps takes the form:

| (13) | ||||

and is defined from using (6). Using (7), we can rewrite the condition (13) as

| (14) |

Each has the following meaning: For every , . This effective drift contains two terms: the actual drift in (11), and the product of , the rate of the Poisson process , with the expected value of , distributed as . Therefore, is the average drift for the bottom-ranked particles out of : The drift for the “cloud” of these particles, as they move together. Thus, plays the same role for the model (2) with jumps as the quantity for the model (12) without jumps.

Now comes the main theoretical result of this article. The proof is in Section 3.

Theorem 1.1.

Under condition (13), and an additional technical condition:

| (15) |

equivalent to for in (11), there exists a unique stationary distribution for the gap process from (3), and the stability result (5) holds. The same is true for the process (9) of ranked market weights, with another stationary distribution instead of .

Remark 1.

This statement can be extended to the case of correlated driving Brownian motions , and dependent Lévy processes . If the -dimensional Lévy process having jump measure (that is, making jumps with intensity , each jump’s displacement is distributed as the normalized measure . Indeed, our setting in Theorem 1.1 fits in this extended framework: If the jumps of the th ranked particle are governed by a finite Borel measure , , and all jumps are independent, then

| (16) |

1.3. Other results

Centering using (6) produces the centered process . This is a Markov process on the hyperplane . It is easier to prove the stability of the centered system than that of the gap process. We state this result as Theorem 1.2, proved in subsection 3.2, which we then use to deduce Theorem 1.1 in subsection 3.1. Corollary 1.3 is the law of large numbers, proved in subsection 3.3. For systems without jumps, it was proved in [4].

Theorem 1.2.

Corollary 1.3.

For any bounded measurable function ,

| (17) |

In the long run, each particle occupies each rank on average th of the time:

| (18) |

1.4. Historical review

Systems of competing Lévy particles were introduced in [29] for . Our results extend stability results [29, Theorem 1.2(a), Theorem 1.3(a)]. In [25], we studied stability of systems of two competing Lévy particles, as well as the explicit rate of exponential convergence of the gap process to its stationary distribution. Articles [1, 14, 18, 19] are devoted to stability for reflected diffusions with jumps.

For competing Brownian particles (no jumps), the stationary distribution of (3) is not known explcitily in general case. It satisfies a complicated integro-differential equation, see [4]. For , there is an explicit product-of-exponential form. Limits as of these systems are studied in [8, 30]. Applications in Stochastic Portfolio Theory are in [16, 17].

We know long-term behavior and scaling limits for infinite systems of competing Brownian particles in case for all ; see [8, 10, 24, 27, 31]. For the infinite Atlas model: , there are, in fact, infinitely many (a continuum of) stationary distributions for the gap process as in (3), and in one of them, the bottom-ranked particle behaves in the long run as the fractional Brownian motion with . We can hardly hope to get such results for infinite systems with jumps, for lack of explicit formula for stationary distributions for (3).

1.5. Simulations

As discussed earlier, we could not find the stationary gap distribution explicitly. Instead, we perform simulations of the jump Atlas model, which is a particular case of a system of competing Lévy particles. In this system, all particles move as Brownian motions, with , . In addition, the (currently) bottom-ranked particle jumps up by with intensity ; that is, , and for . This system has a stationary gap distribution by Theorem 1.1. A detailed description of simulations is given in Section 2, with code on GitHub. We answer the following questions:

-

(A)

In the stationary distribution, are gaps still exponential?

-

(B)

In the stationary distribution, are different gaps independent?

-

(C)

How do mean and variance of the gap depend on jump intensity?

-

(D)

How do mean and variance depend on jump size?

-

(E)

Is the capital distribution curve still linear on the double logarithmic plot?

The answers are: (A) No; (B) No; (C) Linear dependence (on the logarithmic scale); (D) Nonlinear dependence (on the logarithmic scale); (E) Yes.

1.6. Acknowledgements

We are grateful to the referee for help. The second author was partially supported by NSF grants DMS 1409434 and DMS 1405210. He is grateful to Ricardo Fernholz, Soumik Pal, and Mykhaylo Shkolnikov for advice and discussion.

2. Details of Simulations

2.1. Jump Atlas model

We simulate times a system of particles with time steps , up to time . We performed the following simulations:

-

(1)

and ;

-

(2)

and .

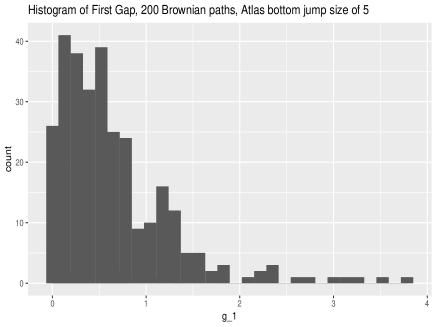

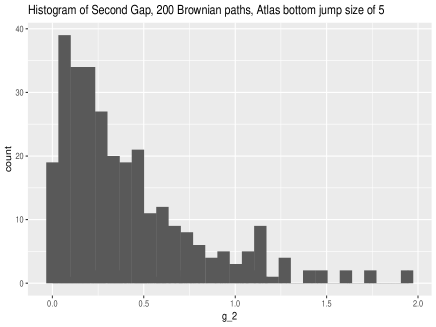

For all these 100 cases, the hypothesis that the empirical distribution is exponential, was (very much) rejected by the Kolmorogov-Smirnov test. This is in contrast with the classic Atlas model without jumps, where the stationary distribution of each gap is exponential.

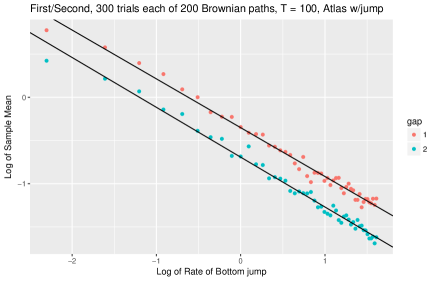

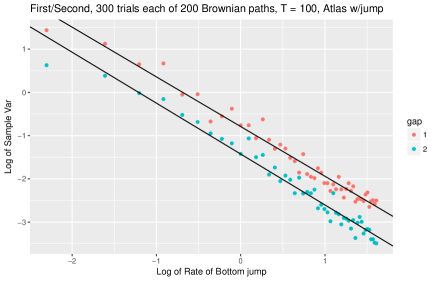

2.2. The first two gaps

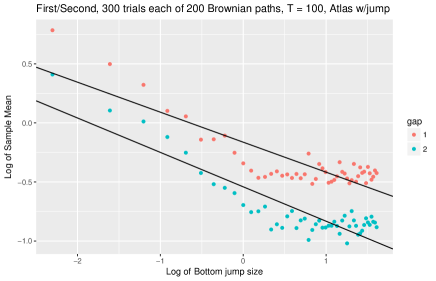

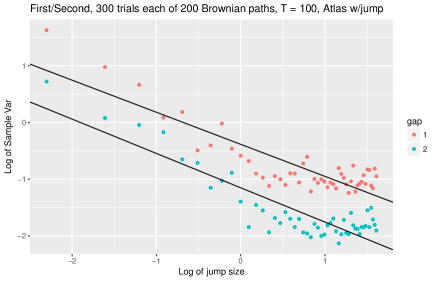

We computed empirical means and variances of the first gap and the second gap , and plotted them versus and in Figure 4 (A) and (B) in a double logarithmic plot. All plots were close to linear, with almost the same slopes for the two means, and similarly for the first two variances. We did the same for and , and plotted empirical means and variances versus in a double logarithmic plot in Figure 4 (C) and (D). These plots were not linear, but resembled functions of the type .

2.3. Comparison with classic Atlas model

Without jumps, similar linearity holds for the Atlas model from (10), if you replace by from (10), [4]. The th gap with has mean and variance . Therefore,

That is, the double logarithmic plot of mean vs has a linear shape with slope and intercept . For the variance vs , this double logarithmic plot has a similar linear shape, but with slope and intercept . In this respect, the intensity in this jump Atlas model behaves similarly to the drift in the classic Atlas model, but the jump size behaves differently.

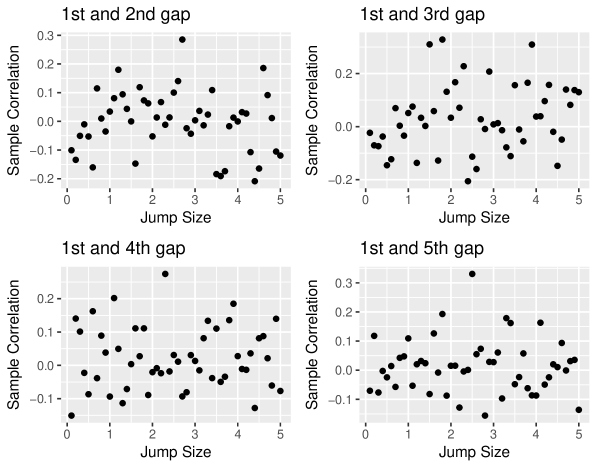

2.4. Correlations

We computed Pearson correlation coefficients between the first gap and the next 4 gaps. They are plotted in Figure 3 vs jump size . Although the variables are not normal, we still use Pearson correlation coefficient for the -test, since the sample is large, and thus the -variable (for a large degree of freedom) is close to normal. For the sample size 300, Pearson coefficient corresponding to is . We see that many points (much more than 5% of the total quantity) are above this level, but not many are below . Thus we can rule out the hypothesis that the first and the second gaps are independent. Instead, there is evidence that they are positively correlated. This is in contrast with the case of no jumps, when the stationary distribution has independent components.

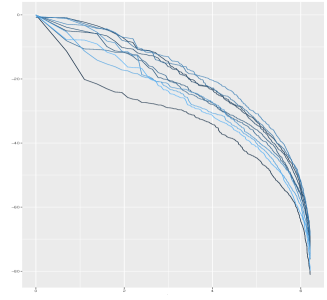

2.5. Capital distribution curve

Recall that in real-world stock markets and in the classic Atlas model, the capital distribution curve is linear in the double logarithmic scale. Now we simulate a jump Atlas model, modified slightly by allowing the bottom-ranked particle to have a continuous linear drift as well as jumps. Each graph displays simulations of the capital distribution curve, with the number of stocks, time steps , time horizon . For the bottom-ranked particle, we denote its continuous drift by , its jump size by , and jump intensity , see Figure 5. All other particles are driftless Brownian motions. All diffusion coefficients .

3. Proofs

We introduce some notation: For a vector and a permutation on , we denote , . The dot product of and in is denoted by . The Euclidean norm of is defined as . We denote the transition kernel for the centered process by .

3.1. Derivation of Theorem 1.1 from Theorem 1.2

3.2. Proof of Theorem 1.2

The key ingredient is the function

| (19) |

which satisfies the following statement for some constants and all :

| (20) |

We shall show (20), and then complete the proof of Theorem 1.2. The generator consists of the continuous part and the jump part . That is,

| (21) | ||||

where for , we define as follows:

and is the push-forward to the measure with respect to the mapping

| (22) |

Therefore, we can rewrite the integral in the right-hand side of from (21) as

| (23) |

Now, plug in from (19) into (21). In [3, Appendix, Proof of (2.18)] (with notation slightly different than here), the expression is already calculated: It is the coefficient attached to in [3, Appendix, Proof of (2.18), (A.13)]. In our notation, we have:

| (24) |

We can rewrite (24) as

| (25) |

Consider the expression inside of the integral in (23) for from (19). The function is infinitely differentiable on , and

| (26) |

Therefore, we have:

| (27) |

We can write the following Taylor decomposition for all :

| (28) |

The error term is given by the following expression for some :

| (29) |

| (30) |

Letting and in (28),

| (31) |

From (30) and the observation that , we have

| (32) |

Combine (15), (30), (31), (32), and apply Lebesgue dominated convergence theorem to infer

| (33) |

Rewrite the expression inside the integral in (33) as follows:

Integrating with respect to , we obtain:

| (34) |

| (35) |

As calculated in [3, p.2302, (2.17)], via summation by parts,

| (36) |

Similarly, we can rewrite the sum in (35) as

| (37) |

Now we combine (25), (33), (35), (36), (37) with the observation that . Letting , we have:

| (38) |

Note that and as for . As in [3, p.2302], we have:

| (39) | ||||

From (38) and (39), we can prove (20), which is the main step of this proof of (5). We complete this proof as follows. Denote by the Lebesgue measure on . The centered system forms a Feller continuous strong Markov process, because is a Feller continuous strong Markov process, by [28, Theorem 2.4, Theorem 5.3, Example 1]; and is a continuous function of . Next, is a -process in the terminology of [21, Subsection 3.2]: That is, there exists a nonzero function ( is the Borel -algebra over ), lower semicontinuous in the first argument and a measure in the second argument; and for a probability measure on ,

| (40) |

Let be the transition kernel of a (centered) system of competing Brownian particles with the same drifts and diffusions , but without any jumps. Then

| (41) |

Indeed, we treat as , with an orthogonal coordinate system. The drift coefficients are bounded, and the covariance matrix field is uniformly elliptic: There exists a such that , , . Under such conditions, the transition kernel has a Lebesgue density which satisfies a parabolic PDE with maximum principle; thus this density is strictly positive on the whole space. This completes the proof of 41.

Since is the jump intensity of the multidimensional process , we conclude that with probability the system of competing Lévy particles does not jump until time , and behaves as a system of competing Brownian particles. Thus

| (42) |

It follows from (41) and (42) that

| (43) |

The rest of the proof can be split in several small steps. The definition of a petite set is taken from [21, Subsection 4.1]: There exists a nontrivial measure on and a probability measure on such that for all , with defined in (40).

-

(A)

The discrete-time Markov chain is irreducible with respect to Lebesgue measure: For every subset with , there is a positive probability that starting from any , the Markov chain will eventually visit . We took this definition from [20, Section 4.2]. This follows from (43), take or any positive integer.

-

(B)

We claim that all compact subsets of are petite for the discrete-time Markov chain . By [20, Proposition 6.2.8(b)], this property is true for a discrete-time Markov chain which is Feller continuous (transition kernel maps bounded continuous functions to bounded continuous functions), if it has positivity property (43) for subset of positive -measure, with support of having non-empty interior. This is indeed applicable here, since is the Lebesgue measure and therefore trivially has a non-empty interior.

- (C)

Combine these statements (A), (B), (C), and finish the proof of (5).

3.3. Proof of Corollary 1.3

Let us show (17). From (20) by [22, Theorem 4.2] it follows that the process is positive Harris recurrent: It has a unique (up to multiplication by a constant) invariant measure, and this measure is finite; it is equal to . Applying [20, Theorem 17.1.7] (stated and proved for discrete-time Markov chains, but similarly shown for continuous-time Markov processes), we get (17).

The limit (18) follows from (17) in the same way as [3, (2.22)] follows from [3, (2.19)]: Indeed, the limit exists by (17). But in this system of particles, their dynamics depends only on their current ranks. Apply any fixed permutation to the particle indices. Then the permuted system is still governed by the same law as the original system. Therefore, the limit in the right-hand side of (17) must be the same for all permutations . The sum of these limits is ; therefore, each of these limits is equal to . There are permutations on which map to . Therefore, the right-hand side of (18) is the sum of terms, each of which is equal to ; the result is .

4. Conclusion

We established long-term stability results for systems of competing Brownian particles with jumps, which we named competing Lévy particles. However, we cannot find an explicit formula for stationary gap distribution, and the corresponding distribution for ranked market weights. Instead, we studied the properties of this stationary gap distribution via Monte Carlo simulations. Gaps are not independent and exponential. However, capital distribution curves are still approximately linear in the log-log scale, which captures the property of the real world markets. In the log-log scale, mean and variance of the first and second gaps depend linearly on the jump intensity, but not on the jump size. Such linearity holds for the classic Atlas model (with drift of the bottom particle instead of jump intensity).

Possible future research:

-

(A)

Find how the th margin of the stationary distribution depends on .

-

(B)

Simulate more general models of competing Lévy particles, instead of the jump Atlas model, and replicate the research above in this more general setting.

-

(C)

Find or estmate exponential rate of convergence to the stationary distribution as .

-

(D)

Extend to competing Lévy particles with infinitely many jumps on finite time interval.

References

- [1] Rami Atar, Amarjit Budhiraja (2002). Stability Properties of Constrained Jump-Diffusion Processes. Electr. J. Probab. 7 (22), 1–31.

- [2] Rami Atar, Amarjit Budhiraja, Paul Dupuis (2001). On Positive Recurrence of Constrained Diffusion Processes. Ann. Probab. 29 (2), 979–1000.

- [3] Adrian D. Banner, E. Robert Fernholz, Ioannis Karatzas (2005) Atlas Models of Equity Markets. Ann. Appl. Probab. 15 (4), 2996–2330.

- [4] Adrian D. Banner, E. Robert Fernholz, Tomoyuki Ichiba, Ioannis Karatzas, Vassilios Papathanakos (2011). Hybrid Atlas Models. Ann. Appl. Probab. 21 (2), 609–644.

- [5] Richard F. Bass (1979). Adding and Subtracting Jumps from Markov Processes. Trans. Amer. Math. Soc. 255, 363–376.

- [6] Richard F. Bass, Etienne Pardoux (1987). Uniqueness for Diffusions with Piecewise Constant Coefficients. Probab. Th. Rel. Fields 76 (4), 557–572.

- [7] Amarjit Budhiraja, Chihoon Lee (2007). Long Time Asymptotics for Constrained Diffusions in Polyhedral Domains. Stoch. Proc. Appl. 117 (8), 1014–1036.

- [8] Manuel Cabezas, Amir Dembo, Andrey Sarantsev, Vladas Sidoravicius (2019). Brownian Particles with Rank-Dependent Drifts: Out-of-Equilibrium Behavior. To appear in Comm. Pure Appl. Math. Available at arXiv:1708.01918.

- [9] Sourav Chatterjee, Soumik Pal (2010). A Phase Transition Behavior for Brownian Motions Interacting Through Their Ranks. Probab. Th. Rel. Fields 147 (1), 123–159.

- [10] Amir Dembo, Li-Cheng Tsai (2017). Equilibrium Fluctuation for the Atlas Model. Ann. Probab. 45 (6B), 4529–4560.

- [11] Rama Cont, Peter Tankov (2004). Financial Modelling with Jump Processes. Chapman & Hall.

- [12] E. Robert Fernholz (2002). Stochastic Portfolio Theory. Applications of Mathematics 48. Springer.

- [13] E. Robert Fernholz, Ioannis Karatzas (2009). Stochastic Portfolio Theory: An Overview. Handbook of Numerical Analysis: Mathematical Modeling and Numerical Methods in Finance, 89–168.

- [14] Fabrice M. Guillemin, Ravi R. Mazumdar, Francisco J. Piera (2008). On Product-Form Stationary Distributions for Reflected Diffusions with Jumps in the Positive Orthant. Adv. Appl. Probab. 37 (1), 212–228.

- [15] Tomoyuki Ichiba, Ioannis Karatzas, Mykhaylo Shkolnikov (2013). Strong Solutions of Stochastic Equations with Rank-Based Coefficients. Probab. Th. Rel. Fields 156 (1-2), 229-248.

- [16] Benjamin Jourdain, Julien Reygner (2015). Capital Distribution and Portfolio Performance in the Mean-Field Atlas Model. Ann. Finance 11 (2), 151-198.

- [17] Ioannis Karatzas, Andrey Sarantsev (2016). Diverse Market Models of Competing Brownian Particles with Splits and Mergers. Ann. Appl. Probab. 26 (3), 1329-1361.

- [18] Offer Kella, Ward Whitt (1996). Stability and Structural Properties of Stochastic Storage Networks. J. Appl. Probab. 33 (4), 1169–1180.

- [19] Ravi R. Mazumdar, Francisco J. Piera (2008). Comparison Results for Reflected Jump-Diffusions in the Orthant with Variable Reflection Directions and Stability Applications. Electr. J. Probab. 13 (61), 1886–1908.

- [20] Sean P. Meyn, Richard L. Tweedie (2009). Markov Chains and Stochastic Stability. Cambridge University Press.

- [21] Sean P. Meyn, Richard L. Tweedie (1993). Stability of Markovian Processes II: Continuous-Time Processes and Sampled Chains. Adv. Appl. Probab. 25 (3), 487–517.

- [22] Sean P. Meyn, Richard L. Tweedie (1993). Stability of Markovian Processes III: Foster-Lyapunov Criteria for Continuous-Time Processes. Adv. Appl. Probab. 25 (3), 518–548.

- [23] Soumik Pal, Jim Pitman (2008). One-Dimensional Brownian Particle Systems with Rank-Dependent Drifts. Ann. Appl. Probab. 18 (6), 2179–2207.

- [24] Andrey Sarantsev (2016). Infinite Systems of Competing Brownian Particles. Ann. Inst. H. Poincaré 53 (4), 2279–2315.

- [25] Andrey Sarantsev (2016). Explicit Rates of Exponential Convergence for Reflected Jump-Diffusions on the Half-Line. ALEA Lat. Am. J. Probab. Math. Stat. 13 (2), 1069–1093.

- [26] Andrey Sarantsev (2017). Reflected Brownian Motion in a Convex Polyhedral Cone: Tail Estimates for the Stationary Distribution. J. Th. Probab. 30 (3), 1200–1223.

- [27] Andrey Sarantsev, Li-Cheng Tsai (2017). Stationary Gap Distributions for Infinite Systems of Competing Brownian Particles. Electr. J. Probab. 22 (56), 1–20.

- [28] Stanley A. Sawyer (1970). A Formula for Semigroups, with an Application to Branching Diffusion Processes. Trans. Amer. Math. Soc. 152 (1), 1–38.

- [29] Mykhaylo Shkolnikov (2011). Competing Particle Systems Evolving by Interacting Lévy Processes. Ann. Appl. Probab. 21 (5), 1911–1932.

- [30] Mykhaylo Shkolnikov (2012). Large Systems of Diffusions Interacting Through Their Ranks. Stoch. Proc. Appl. 122 (4), 1730-1747.

- [31] Li-Cheng Tsai (2018). Stationary Distributions of the Atlas Model. Electr. Comm. Probab. 23 (10), 1–10.