Preconditioners and Their Analyses

for Edge Element Saddle-point Systems

Arising from

Time-harmonic Maxwell Equations

Abstract

We shall propose and analyze some new preconditioners for the saddle-point systems arising from the edge element discretization of the time-harmonic Maxwell equations in three dimensions. We will first consider the saddle-point systems with vanishing wave number, for which we present an important relation between the solutions of the singular curl-curl system and the non-singular saddle-point system, then demonstrate that the saddle-point system can be efficiently solved by the Hiptmair-Xu solver. For the saddle-point systems with non-vanishing wave numbers, we will show that the PCG with a new preconditioner can apply for the non-singular system when wave numbers are small, while the methods like preconditioned MINRES may apply for some existing and new preconditioners when wave numbers are large. The spectral behaviors of the resulting preconditioned systems for the existing and new preconditioners are analyzed and compared, and numerical experiments are presented to demonstrate and compare the efficiencies of these preconditioners.

Keywords: Time-harmonic Maxwell equations, saddle-point system, preconditioners.

AMS subject cclassifications: 65F10, 65N22, 65N30

1 Introduction

In this work we shall investigate and compare some effective preconditioning solvers for the following saddle-point system:

| (1.1) |

where , , and , with . We assume that is nonsingular, so must be of full row rank. We are particularly interested in the case where is symmetric semi-positive definite, and dim, that is, is maximally rank deficient [6] [7]. The matrix is assumed to be symmetric positive definite, and is a given real number.

The saddle-point system of form (1.1) with a maximal rank deficient arises from many applications, including the numerical solution of time-harmonic Maxwell’s equations [7, 8, 17] where represents the wave number, the underdetermined norm-minimization problems and geophysical inverse problems; see more details in the recent paper [6] that was a very inspiring and innovative work and developed a class of indefinite block preconditioners for the use with the CG method, and CG may converge rapidly under certain conditions when it is applied for solving the general saddle-point system of form (1.1) with a maximal rank deficient and . It was also pointed out in [6] that the saddle-point system under the above particular setting has not received as much attention as other situations, for example, the case of a symmetric positive definite . But as it was demonstrated in [6] for the special case , when is maximally rank deficient, some nice mathematical structures may be revealed and adopted to help construct efficient solution methods. This work is initiated and motivated by [6] and will develop further in this direction, and show that new efficient numerical methods can be equally constructed for more general and difficult case .

Though most results of this work apply also to the general saddle-point system of form (1.1) with a maximal rank deficient as it was done in [6] for the case , we shall mainly focus on the saddle-point system (1.1) that arises from the edge element discretization of the following time-harmonic Maxwell equations in vacuum [17, 10, 3, 5, 11]:

| (1.2) |

where is a vector field, is the scalar multiplier, and is the given external source. is a simply connected domain in with a connected boundary , with being its outward unit normal. The wave number is given by where , and are positive frequency, permittivity and permeability of the medium, respectively. We assume that is not an interior Maxwell eigenvalue, and know the cases with appropriately small and large frequencies are physically relevant in magnetostatics, wave propagation and other applications [7]. We refer to [2, chapter 11] for a survey on this topic. The introduction of the Lagrange multiplier in (1.2) may not be absolutely necessary for the general case , for which the divergence constraint does not need to be enforced explicitly; namely it is possible to solve directly for using the first equation in (1.2) with mathematically [8], although it is still challenging to design an efficient numerical solver for this indefinite system. The saddle-point formulation (1.2) with the Lagrange multiplier is stable and well-posed [5], especially it ensures the stability and Gauss’s law when is small and may better handle the singularity of the solution at the boundary of the domain [5, 17, 3]. More importantly, the mixed form (1.2) provides some extra flexibility on the computational aspect [13] and leads to better numerical stability and more efficient numerical solvers than the single system (1.2) without Lagrange multiplier (i.e., ), as it was shown in [6] [7]. And this is also the main motivation and focus and of the current work.

After discretizing (1.2) by using the Nédélec elements of the first kind [14, 15] for the approximation of the vector field and the standard nodal elements for the multiplier , we derive the saddle-point system (1.1) of our interest. We assume that the coefficient matrix in (1.1) and its leading block are both nonsingular, which is true when the mesh size is sufficiently small [7].

Some very efficient preconditioners were proposed and analyzed recently in [6] for the special case of the saddle-point system (1.1), i.e., the wave number , and (1.1) reduces to

| (1.3) |

The following preconditioner was proposed in [6] for solving the saddle-point system (1.3):

| (1.4) |

where the matrix is the discrete Laplacian, while is a sparse matrix, whose columns span and can be formed easily using the gradients of the standard nodal bases [6]. It was proved that the preconditioned system is simply diagonal, given by

As both and are symmetric positive definite, it allows us to apply a CG-like method for the preconditioned system in a non-stardand inner product, even both and are indefinite. For the more general case , the block tridiagonal preconditioners

| (1.5) |

with double variable relaxation parameters and were studied in [7, 20, 19, 4].

In this work, we construct some new preconditioners for (1.3) and (1.1) respectively. We will first show that for the case with vanishing wave number (), instead of the aforementioned efficient solver by using the preconditioner (1.4) or (1.5) (with ), we can directly make use of the solution of the singular curl-curl system to construct a more direct and efficient solver.

As it was shown in [6] that preconditioners in (1.4) work very effectively for the special and simple case with vanishing wave number (). We shall demonstrate that similar preconditioners can be constructed also for the saddle-point linear system (1.1) with more general and difficult cases, i.e., , including high frequency waves. And we will see analytically the spectral distributions of these new preconditioners are quite similar to the ones of the existing effective preconditioners (1.5). But the new preconditioner can be applied with CG iteration under a non-standard inner product although both the coefficient matrix and the new preconditioner are indefinite for , and numerically they will perform mostly better and more stable than the existing preconditioners (1.5).

The rest of the paper is arranged as follows. We shall develop in Section 2 an important formula for computing the inverse of , based on which we propose in Subsection 3.1 some more direct and efficient solver for the saddle-point system (1.3) with vanishing wave number. Then we shall propose a new preconditioner and compare its performance with existing preconditioners for the saddle-point system (1.1) with general wave numbers, and study and compare the spectral properties of the preconditioned matrices in Subsection 3.2. Numerical experiments are presented in Section 4.

2 Computing the inverse of

We shall derive in this section some formulae for computing the inverse of the matrix in (1.1). To do so, we first recall some useful properties of the matrices , , , and , which are introduced in the Introduction.

Proposition 2.1.

We give another proof for (vi) of Proposition 2.1 in the Appendix, where the much more general cases are allowed, i.e. the cases when is non-symmetric and its (2,2) block is nonzero.

Lemma 2.2.

For the matrix in (2.2), we have the following results:

| (2.3) | |||

| (2.4) |

Proof. Using the fact that , it is easy to see from (2.2) that

The first relation in (2.3) follows readily from the fact that the (1,1) block of the following matrix

is an identity matrix. Noting that is symmetric, we know and are both symmetric. Then the two identities in (2.4) follow immediately by taking the transpose of both sides of each identity in (2.3).

Now we are ready to derive a formula for computing the inverse of the matrix in (1.1). Recall that and are invertible. We shall write the (1,1) block of the inverse as , then we have the following representation of the inverse of the saddle-point matrix .

Theorem 2.3.

The inverse of is given by

| (2.5) |

where satisfies

| (2.6) |

Proof. We write as a perturbation of in the form

| (2.7) |

then using the fact that , namely

we obtain by a direct computing that

| (2.8) |

| (2.9) |

| (2.10) |

From (2.7) we know that is the (1,1) block of so it follows from (2.4) and (2.10) that

Multiplying (2.8) by we derive

which gives

| (2.11) |

Similarly, multiplying (2.9) by we obtain

By combining this equality with the second relation in (2.10), we come to

| (2.12) |

Then we may substitute (2.12) into (2.9) to get

| (2.13) |

which proves .

Noting that we have proved , then (2.8) reduces to or , which completes the desired proof.

The following result is important to help us understand the leading block of the inverse of in (2.5).

Theorem 2.4.

The matrix is non-singular for any , and its null space is exactly the same as that of for .

Proof. By means of (ii) of Proportion 2.1, we can write for any that with and . If then . As the columns of span the null space of , there exists such that . So we see . Multiplying its both sides by we drive , hence , yielding that . Hence we have proved and also the non-singularity of the desired matrix.

Next, we consider the case with . We show the two matrices and have the same null space. First, we assume and write with and , then we see readily that , hence .

Now we assume is in the null space of . We still write , and follow the earlier proof of the non-singularity of the matrix, but with now. Then we shall deduce , which implies , hence we know .

The following result comes directly from (2.6) and Theorem 2.4. And it introduces a very crucial parameter to the expression of the leading block of the inverse of in (2.5), and it can take an arbitrary value except for .

Corollary 2.1.

For any , it holds that

| (2.14) | |||||

Corollary 2.1 can be simplified for the special case .

Corollary 2.2.

For any , we have

| (2.15) |

It is very interesting to see from above that the two matrices and are independent of the parameter , although their explicit representations in (2.14) and (2.15) look closely depending on . In conclusion, we can easily see from Theorem 2.3 and Corollary 2.1 the following formula with for computing the inverse of matrix in (1.1), which forms the basis in our construction of some new preconditioners that are discussed in the next section:

| (2.16) |

3 New preconditioners and their spectral properties

3.1 Vanishing wave number:

In this subsection we will propose a new simple solution to the saddle-point system (1.3). To do this, we can easily see from Proporsition 2.1 (vi) that , then we can rewrite the saddle-point system (1.3) as

| (3.1) | |||||

| (3.2) |

As is the discrete counterpart of the curl curl operator, so it is singular and the equation (3.1) has multiple solutions. Now we consider an arbitrary solution to (3.1). Noting that the columns of span the kernel of (see section 1), we can decompose the solution of (1.3) into for some vector . By means of (3.2) and the fact that from Proporsition 2.1, we derive from that , which yields

or

| (3.3) |

which gives another representation of the inverse and its diagonal part (see (2.1)). Here is any operator which maps any vector to a particular solution of .

We remark that if the source is divergence free in (1.2), then the Lagrange multiplier , so is the discrete in the saddle-point system (1.3). Then we get from that . In this case, the equation (3.1) reduces to . We have similar simplification in (3.3).

To find an arbitrary solution to (3.1), we may apply the CG iteration with the Hiptmair-Xu preconditioner [9], which works vey efficiently for the discrete system (3.1) arising from the discretization of the curl curl system [12]. One may also develop a preconditioner for the whole system based on the important equation (3.3).

3.2 General wave numbers:

The formula (2.16) suggests us some natural preconditioners for the saddle-point matrix in (1.1). Noting that the matrix is a dense matrix, the action of the (1,1) block of (2.16) is very expensive to compute. To overcome the difficulty, we approximate the dense matrix by the sparse matrix to get the following simplified preconditioner for the matrix :

| (3.4) |

For the simple case with vanishing wave number () and , the preconditioner (3.4) reduces to the existing one in (1.4). To ensure the nonsingularity of the matrix involved in (3.4), we can simply set the parameter so that it becomes symmetric positive definite. Moreover, this choice also ensures the nonsingularity of the matrix on the right-hand side of (3.4), as discussed below.

Theorem 3.1.

For any , the matrix on the right-hand side of (3.4) is non-singular.

Proof. It is direct to check that the preconditioned matrix is given by

Using Proposition 2.1 (i), we can further write the (1, 1) block of the above matrix as follows:

so the preconditioned matrix reads also as

| (3.5) |

We know that the leading block of in (3.5) is non-singular by Theorem 2.4, hence the desired conclusion follows.

Note that and its inverse are always symmetric positive definite for . Actually, the original matrix can be also symmetric positive definite as shown below.

Theorem 3.2.

If any and , the matrix is symmetric positive definite.

Proof. For any , we can write with and . By Proposition 2.1 we know and . Therefore,

| (3.6) |

But we have by (iii) in Proposition 2.1, and this implies

hence proves the desired result.

For and , the preconditioned matrix is self-adjoint and positive definite with respect to the inner product

| (3.7) |

So we can apply the CG iteration [1] in this special inner product for solving the preconditioned system associated with . But Theorem 3.2 does not ensure the positive definiteness of the preconditioned system for , so the CG iteration may fail theoretically. In this case, we may still apply the preconditioned MINRES with the above non-stardand inner product.

We know the convergence rates of the CG and MINRES can be reflected often by the spectrum of the preconditioned system. For this purpose, we shall now study the spectral properties of the preconditioned system . First, we present an interesting observation that the parameter does not affact the symmetric positive definiteness of the matrix .

Theorem 3.3.

For any two numbers is symmetric positive definite if and only if is symmetric positive definite.

Proof. For any suppose that is not symmetric positive definite. As this matrix is nonsingular by Theorem 2.4, hence it is not symmetric semi-positive definite. Therefore, there exists satisfying . But we can write with and . Then we can see that and from (3.6). Now for any we can easily check , hence is not symmetric positive definite.

Next we present several results about the eigenvalues of the preconditioned matrix .

Lemma 3.4.

For any , is an eigenvalue of with its algebraic multiplicity being . The rest of the eigenvalues are bounded by

| (3.8) |

Proof. The result was proved in [7, Theorem 5.1] for and . But our desired results for an arbitrary positive can be done similarly.

Theorem 3.5.

For any , is an eigenvalue of the preconditioned matrix with its algebraic multiplicity being . The rest of the eigenvalues are bounded as in (3.8).

Now we like to make some spectral comparisons between the two preconditioned systems generated by our new preconditioner and the existing block triadiagonal one in (1.5) for the saddle-point matrix . We first recall the following results from [20, Theorem 2.6].

Theorem 3.6.

For any , both and are the eigenvalues of each with its algebraic multiplicity . The rest of the eigenvalues are bounded as in (3.8).

We see from Theorems 3.5 and 3.6 that the spectra of and are quite similar, except that the latter has an extra eigenvalue , with its algebraic multiplicity being . This will be also confirmed numerically in the next section.

The block triadiagonal preconitioners reduce to symmetric if we set :

| (3.9) |

This preconditioner was analysed and applied in [7, 19] along with the MINRES iteration. We may observe from Theorems 3.5 and 3.6 that the eigenvalues of our preconditioned matrix are a little better clustered than those of as its eigenvalue is smaller than . But our new preconditioner can be applied with CG for and MINRES for . And more importantly, as we will see from our numerical experiments in next section, we can also apply the new preconditioner with CG even for and the convergence is still rather stable, while CG with preconditioner in (3.9) breaks down most of the time.

On the other hand, if we choose , the preconditioner is non-symmetric, and the methods like GMRES should be used, which are less economical than methods like CG or MINRES. Note that for we have , so is an eigenvalue of with its algebraic multiplicity being the same as for .

Now we consider the inner iterations associated with the new preconditioner . For any two vectors and , we can write

So we have to solve two linear systems associated with the discrete Laplacian and one with at each evaluation of the action of . Many fast solvers are available for solving these two symmetric and positive definite systems [13, 9]. We know from Theorem 3.5 that a small may result in a better convergence of the preconditioned Krylov subspace methods. But if is too small, the matrix would become nearly singular.

We know that the parameter depends only on the shape regularity of the mesh and the approximation order of the finite elements used, and is irrelevant to the size of the mesh [8, Theorem 4.7]. Numerically we may expect a upper bound for that ensures the positive definiteness of , and this bound should be independent of the mesh size. We shall test this numerically in the next section.

3.3 Preconditioners for more general saddle-point systems

We devote this subsection to discuss a by-product produced by our previous technique for deriving the formula (2.16) to compute the inverse , yielding an effective preconditioner for the following saddle-point matrix with an arbitrary and non-vanishing (2, 2) block :

In fact, we can easily check using Proposition 2.1 that

| (3.10) |

so is non-singular, and its inverse is given by the second matrix on the left-hand side of (3.10). Formula (3.10) is very interesting: the inverse of does not involve the inverse of matrix . Note that (3.10) holds not only for those systems arising from Maxwell equations but also for all non-singular saddle-point matrices with their block being nonzero and their leading block being maximally rank deficient; see [6] for more applications.

Motivated by (3.4), we may consider the following preconditioner:

| (3.11) |

Then we readily see a block diagonal preconditioned system:

| (3.12) |

This important relation indicates that we can always apply the CG iteration for solving the saddle-point system associated with the matrix in a special inner product as we did in section 3.2.

We can easily see that for the special case that , preconditioner reduces to

4 Numerical experiments

In this section, we present numerical experiments to demonstrate and compare the spectral distributions of the preconditioned systems of the saddle-point problem (1.1) with the existing preconditioner in (1.5) and the new one in (3.4), and the results of some Krylov subspace iterations. The edge elements of lowest order are used for the discretization of the system (1.2) in a square domain or an L-shaped domain (see Figures 1 and 2), which is partitioned using unstructured simplicial meshes generated by EasyMesh [16]. For Meshes G1 through G5, the desired side lengths of the triangles that contain one of the vertices of the domain are set to be the same. For Meshes L1 through L5, the desired side lengths of the triangles that contain the origin are one-tenth of the desired side lengths of the triangles that contain other vertices of the domain. Meshes G5 and L5 lead to linear systems of size and respectively. We use Matlab to implement all numerical iterative solvers, and the linear solvers involved in all inner iterations are achieved by preconditioned CG method (either with an incomplete Cholesky factorization as an precondtioner or with the Hiptmair-Xu solver [9]), with the stopping criterion set to be a relative -norm error of the residual less than , if not specified otherwise. The right-hand side of (1.1), denoted by , is set to be a vector with all components being ones, and the zero vector is used as the initial guess for all iterations.

We shall run respectively the CG and MINRES [18, Algorithms 1 & 2] with the new preconditioner for solving the saddle-point system (1.1), and the preconditoned MINRES with the block diagonal preconditioner , and denote these three methods by -CG, -MINRES and -MINRES respectively. In all our tests, we shall take the parameter , unless otherwise defined, and the outer iterations are terminated based on the criterion

where is the th iterate. Numbers of iteration by these solvers with different meshes and wave numbers are listed in Tables 1 and 2. With the new preconditioners, we can see that the required numbers of iteration are slightly smaller than the one by the preconditioner , which is consistent with our theoretical prediction in Section 3.2. We have also observed that the required numbers of iteration are basically independent of mesh size.

In Tables 1 and 2, we have also listed the smallest eigenvalue of the matrix

denoted by , to test its definiteness. It is easy to see by (3.5) that we can apply CG with our new preconditioner, under the special inner product defined in (3.7) if is symmetric positive definite. It is important to note that for smaller , is symmetric positive definite, thus CG can be used with the new preconditioner instead of MINRES, though the original system is indefinite. The dotted lines separate signs of : changes to negative for with Meshes G1 through G4, and for with Meshes L1 through L4. This indicates that the corresponding preconditioned matrices are no longer positive definite even under the special non-standard inner product. Thus -MINRES should be used. However, the numerical results indicate that CG still does not fail even when this violation occurs, and actually converge equally stably and fast. This shows very good stability and convergence of CG with the new preconditioner . As predicted by Theorem 3.2, one can see that the bounds shown by the dotted line is independent of the mesh size. This is an important feature in applications as it can help us determine which iterative method to use.

| 0 | 1.0 | 1.55 | 1.6 | 2 | 4 | |

| Mesh G1 | ||||||

| -CG | 5 | 6 | 11 | 11 | 11 | 25 |

| -MINRES | 5 | 6 | 11 | 11 | 11 | 25 |

| -MINRES | 6 | 9 | 14 | 13 | 13 | 30 |

| 0.4677 | 0.4677 | 0.0340 | -0.0544 | -0.8719 | -7.7031 | |

| Mesh G2 | ||||||

| -CG | 5 | 7 | 12 | 12 | 11 | 25 |

| -MINRES | 5 | 6 | 12 | 12 | 11 | 25 |

| -MINRES | 6 | 9 | 15 | 15 | 13 | 30 |

| 0.4738 | 0.4738 | 0.0360 | -0.0543 | -0.8988 | -7.9434 | |

| Mesh G3 | ||||||

| -CG | 5 | 6 | 11 | 11 | 11 | 25 |

| -MINRES | 5 | 6 | 11 | 11 | 11 | 25 |

| -MINRES | 6 | 9 | 15 | 15 | 13 | 30 |

| 0.4776 | 0.4776 | 0.0369 | -0.0536 | -0.8875 | -7.8425 | |

| Mesh G4 | ||||||

| -CG | 5 | 6 | 9 | 9 | 11 | 23 |

| -MINRES | 5 | 6 | 9 | 9 | 11 | 23 |

| -MINRES | 6 | 9 | 11 | 11 | 13 | 28 |

| 0.4769 | 0.4769 | 0.0373 | -0.0533 | -0.8823 | -7.7907 | |

| Mesh G5 | ||||||

| -CG | 5 | 6 | 9 | 9 | 11 | 23 |

| -MINRES | 5 | 6 | 9 | 9 | 11 | 21 |

| -MINRES | 6 | 8 | 11 | 11 | 13 | 28 |

| 0 | 1.0 | 1.2 | 1.25 | 2 | 4 | |

| Mesh L1 | ||||||

| -CG | 5 | 7 | 9 | 8 | 12 | 25 |

| -MINRES | 5 | 7 | 9 | 8 | 10 | 24 |

| -MINRES | 7 | 9 | 11 | 10 | 12 | 29 |

| 0.4787 | 0.2496 | 0.0039 | -0.0646 | -1.4349 | -8.3127 | |

| Mesh L2 | ||||||

| -CG | 6 | 7 | 9 | 8 | 11 | 24 |

| -MINRES | 5 | 7 | 9 | 8 | 11 | 24 |

| -MINRES | 7 | 9 | 11 | 10 | 13 | 29 |

| 0.4582 | 0.2575 | 0.0128 | -0.0556 | -1.4249 | -8.3664 | |

| Mesh L3 | ||||||

| -CG | 5 | 7 | 9 | 8 | 12 | 25 |

| -MINRES | 5 | 7 | 9 | 8 | 11 | 24 |

| -MINRES | 7 | 9 | 11 | 11 | 13 | 29 |

| 0.4758 | 0.2704 | 0.0175 | -0.0530 | -1.4580 | -8.3974 | |

| Mesh L4 | ||||||

| -CG | 5 | 7 | 8 | 8 | 10 | 24 |

| -MINRES | 5 | 7 | 8 | 8 | 10 | 24 |

| -MINRES | 6 | 9 | 11 | 11 | 13 | 29 |

| 0.4654 | 0.2753 | 0.0200 | -0.0512 | -1.4674 | -8.4450 | |

| Mesh L5 | ||||||

| -CG | 5 | 7 | 8 | 8 | 10 | 24 |

| -MINRES | 5 | 7 | 8 | 8 | 10 | 24 |

| -MINRES | 6 | 9 | 10 | 10 | 12 | 29 |

In Tables 3 and 4, we test different values of to see the influence of the inexact inner solvers on the required numbers of iteration and to compare the stabilities of the new and existing preconditioners and when they are respectively used with CG and MINRES iterations. For this, we choose a less accurate tolerance for the inner iterations associated with and . The required numbers of iteration are reported in Tables 3 and 4 when CG is used with the new and existing preconditioners and respectively. As it is expected, the results (lying on the left-hand sides of the dotted lines) indicate that should not be too small relatively to otherwise the matrix becomes nearly singular. If we ignore those results corresponding to the small values of relatively to , we may observe from Tables 3 and 4 that the difference between the required numbers of iterations for these two solvers increases with . This indicates better performance and stability of the new preconditioner than the existing one .

| 6 | 8 | 10 | 14 | 22 | ||

|---|---|---|---|---|---|---|

| 7 | 10 | 12 | 18 | 26 | ||

| 15 | 17 | 21 | 28 | 37 | ||

| 49 | 46 | 53 | 64 |

| 8 | 10 | 15 | 17 | 25 | 35 | |

|---|---|---|---|---|---|---|

| 11 | 16 | 21 | 28 | 39 | ||

| 23 | 28 | 31 | 40 | 66 | ||

| 57 | 50 | 51 | 62 | 80 |

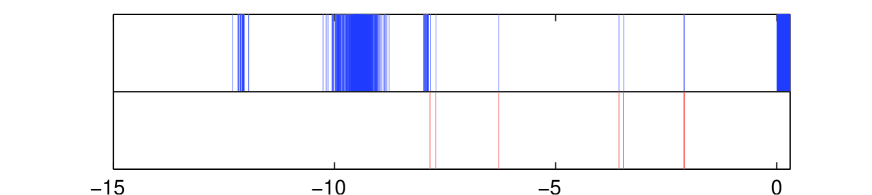

We now make some more experiments to further compare the stability of the new and existing preconditioner and . We can clearly see from Table 3 that CG can be always applied numerically with the new preconditioner and it converges very well, though it may not guarantee to converge theoretically. But this is not the case for the preconditioner . To see this, we re-run all the experiments in Table 4, but with CG iteration now instead MINRES. In each of the 24 numerical experiments, we have always experienced the case that one dividend becomes too small, which causes the break-down of the iterative process. The reasons behind are in fact very simple: we needs to divide by (with being the -th search direction) at the -th CG iteration with preconditioner , and to divide by at the -th CG iteration with the new preconditioner , due to the existence of a special inner product (3.7). Figure 3 shows the distributions of the eigenvalues smaller than of the two matrices and for , and these smaller and negative eigenvalues contribute mainly to the break-down of the iterations (most eigenvalues are larger than , but not shown in the figure). As one can see from the table, there are many more eigenvalues in the upper blue part for than in the lower red part for , which explains clearly the highly instability of CG with the preconditioner and good stability of CG with the new preconditioner . We have also observed in our experiments that a larger makes the eigenvalues distribute more stably numerically.

Next we demonstrate the distributions of the eigenvalues of the preconditioned matrices and . Figure 5 plots the eigen-distribution of the preconditioned matrix on Mesh G3 with different wave number . We can see that the lower bound of the eigenvalues for is about 0.22, and there are eigenvalues that lie between 0.22 and , while all the remaining 1773 eigenvalues stay in the range and 1, with 850 of them ( here) being 1. These results are consistent with our theoretical prediction (Theorem 3.5). For , we see negative eigenvalues, but only a few. Figure 4 shows that the eigenvalues of the preconditioned matrices and with are exactly the same for Mesh G3, with and .

Finally we test the influence of different right-hand sides on the required numbers of iteration when our new preconditioner is used. Table 5 shows this influence, where Df0g, Rf0g and RfRg represent the divergence-free and , the random and , and the random and random . As we can easily see from the table that the right-hand sides does not cause any effect on the required numbers of iterations.

| Grid | G1 | G2 | G3 | G4 | G5 |

|---|---|---|---|---|---|

| Df0g | 12 | 12 | 12 | 12 | 12 |

| Rf0g | 12 | 12 | 11 | 11 | 11 |

| RfRg | 11 | 12 | 11 | 11 | 11 |

Appendix A Appendix

In this appendix we will generalize the formula for computing the inverse of the symmetric saddle-point matrix in (2.1) to the more general case with non-symmtric generalized saddle-point matrix. For this purpose, we consider the following non-symmtric generalized saddle-point system:

| (A.1) |

where all block matrices , , and are allowed to be non-square, with . But the entire matrix is square, i.e., .

We further assume that the rank of is . Then we write as the matrix of full column rank whose columns span , and as the matrix of full row rank whose rows span the left null space of namely , and . We shall write and and the range space of by .

We are now ready to formulate the main results in this appendix.

Theorem A.1.

Assume that

| (A.2) | ||||

| (A.3) |

then the matrix is non-singular and its inverse can be represented by

| (A.4) |

where satisfies

| (A.5) | ||||

| (A.6) |

If , it holds for any such that is non-singular that

| (A.7) |

For our proof, we first introduce some notations and auxiliary results. We set and , where is the Moore-Penrose inverse of namely, is the unique solution satisfying

| (A.8) |

We borrow the following results to work out the explicit formula for the inverse in (A.4).

Theorem A.2.

Next we show that the formula (A.4) is actually the explicit form of (A.9). For this, we first present two auxiliary lemmas.

Lemma A.3.

We have

| (A.10) |

Proof. We prove only the first statement as the second follows similarly. Using the Moore-Penrose properties (A.8) it is direct to verify the symmetry of , and

which imply that . As the columns of and span , we immediately see that .

Lemma A.4.

Under the assumptions of Theorem A.1, the matrices and are non-singular.

Proof. We show only the first statement as the second follows similarly. Suppose for , then by direct computing it is easy to see so we know as is non-singular. This implies by noting that is of full row rank. Therefore we know that the square matrix is non-singular.

Using the above results we can easily derive formulas for the (1,2) and (2,1) blocks of (A.4).

Theorem A.5.

It holds that

| (A.11) |

Proof. Again we prove only the first statement. By definitions in Theorem A.2 and Lemma A.3 we know . As the matrix is of full column rank and is of full row rank, we can derive that , which ends the desired proof.

Now we go further to derive the explicit formula for computing the (1,1) block of (A.9). For this, we first show the following results.

Proposition A.6.

Let , and , then it holds that

| (A.12) | |||

| (A.13) |

Proof. The first assertion in (A.12) comes from the relations

and , which is a direct consequence of the fact that by Theorem A.5. The second assertion in (A.12) follows similarly. The relations in (A.13) can be readily verified using the facts that and , which come from Theorem A.5.

We end the proof of Theorem A.1 with the help of the following results, which can be checked directly by Proposition A.6.

Theorem A.7.

For any and , the following identities hold

References

- [1] S. F. Ashby, T. A. Manteuffel, and P. E. Saylor, A taxonomy for conjugate gradient methods, SIAM J. Numer. Anal., 27 (1990), pp. 1542–1568.

- [2] D. Boffi, F. Brezzi, and M. Fortin, Mixed Finite Element Methods and Applications, Vol. 44 of Springer Series in Computational Mathematics, Springer Berlin Heidelberg, Berlin, Heidelberg, 2013.

- [3] Z. Chen, Q. Du, and J. Zou, Finite element methods with matching and nonmatching meshes for Maxwell equations with discontinuous coefficients, SIAM J. Numer. Anal., 37 (2000), pp. 1542–1570.

- [4] G.-H. Cheng, T.-Z. Huang, and S.-Q. Shen, Block triangular preconditioners for the discretized time-harmonic Maxwell equations in mixed form, Comput. Phys. Commun., 180 (2009), pp. 192–196.

- [5] L. Demkowicz and L. Vardapetyan, Modeling of electromagnetic absorption/scattering problems using hp-adaptive finite elements, Comput. Methods Appl. Mech. Engrg., 152 (1998), pp. 103–124.

- [6] R. Estrin and C. Greif, On nonsingular saddle-point systems with a maximally rank deficient leading block, SIAM J. Matrix Anal. Appl., 36 (2015), pp. 367–384.

- [7] C. Greif and D. Schötzau, Preconditioners for the discretized time-harmonic Maxwell equations in mixed form, Numer. Lin. Algebra Appl., 14 (2007), pp. 281–297.

- [8] R. Hiptmair, Finite elements in computational electromagnetism, Acta Numerica, 11 (2002), pp. 237-339.

- [9] R. Hiptmair and J. Xu, Nodal Auxiliary Space Preconditioning in H(curl) and H(div) Spaces, SIAM J. Numer. Anal., 45 (2007), pp. 2483–2509.

- [10] P. Houston, I. Perugia, and D. Schötzau, Mixed discontinuous Galerkin approximation of the Maxwell operator: non-stabilized formulation, J. Sci. Comput., 22-23 (2005), pp. 315–346.

- [11] Q. Hu and J. Zou, Substructuring preconditioners for saddle-point problems arising from Maxwell’s equations in three dimensions, Math. Comput., 73 (2004), pp. 35–61.

- [12] T. Kolev and P. Vassilevski, Some experience with a -based auxiliary space AMG for H(curl) Problems, Report UCRL-TR-221841, LLNL, Livermore, CA, 2006.

- [13] D. Li, C. Greif, and D. Schötzau, Parallel numerical solution of the time-harmonic Maxwell equations in mixed form, Numer. Lin. Algebra Appl., 19 (2012), pp. 525–539.

- [14] P. Monk, Analysis of a finite element method for Maxwell’s equations, SIAM J. Numer. Anal., 29 (1992), pp. 714–729.

- [15] J. C. Nédélec, Mixed finite elements in , Numer. Math., 35 (1980), pp. 315–341.

- [16] B. Niceno, EasyMesh. http://web.mit.edu/easymesh_v1.4/www/easymesh.html.

- [17] I. Perugia, D. Schötzau, and P. Monk, Stabilized interior penalty methods for the time-harmonic Maxwell equations, Comput. Methods Appl. Mech. Eng., 191 (2002), pp. 4675–4697.

- [18] J. Pestana and A. J. Wathen, Combination preconditioning of saddle point systems for positive definiteness, Numer. Lin. Algebra Appl., 20 (2013), pp. 785–808.

- [19] S. L. Wu, T. Z. Huang, and C. X. Li, Modified block preconditioners for the discretized time-harmonic Maxwell equations in mixed form, J. Comput. Appl. Math., 237 (2013), pp. 419–431.

- [20] Y. Zeng and C. Li, New preconditioners with two variable relaxation parameters for the discretized time-harmonic Maxwell wquations in mixed form, Math. Comput. Probl. Eng., 2012 (2012), pp. 1–13.

- [21] Tian Y. and Takane Y., The inverse of any two-by-two nonsingular partitioned matrix and three matrix inverse completion problems, Comp. Math. Appl., 2009, 57(8), pp. 1294–1304.