Factor Models for Matrix-Valued High-Dimensional Time Series 111 Chen’s research was supported in part by National Science Foundation grants DMS-1503409 and DMS-1209085. Corresponding author: Rong Chen, Department of Statistics, Rutgers University, Piscataway, NJ 08854, USA. Email: rongchen@stat.rutgers.edu.

Abstract

In finance, economics and many other fields, observations in a matrix form are often observed over time. For example, many economic indicators are obtained in different countries over time. Various financial characteristics of many companies are reported over time. Although it is natural to turn a matrix observation into a long vector then use standard vector time series models or factor analysis, it is often the case that the columns and rows of a matrix represent different sets of information that are closely interrelated in a very structural way. We propose a novel factor model that maintains and utilizes the matrix structure to achieve greater dimensional reduction as well as finding clearer and more interpretable factor structures. Estimation procedure and its theoretical properties are investigated and demonstrated with simulated and real examples.

1 Introduction

Time series analysis is widely used in many applications. Univariate time series, when one observes one variable through time, is well studied, with linear models (e.g. Box and Jenkins,, 1976; Brockwell and Davis,, 1991; Tsay,, 2005), nonlinear models (e.g. Engle,, 1982; Bollerslev,, 1986; Tong,, 1990), and nonparametric models (e.g. Fan and Yao,, 2003). Multivariate time series and panel time series, when one observes a vector or a panel of variables through time, is also a long studied but still active field (e.g. Tiao and Box,, 1981; Tiao and Tsay,, 1989; Engle and Kroner,, 1995; Stock and Watson,, 2004; Lütkepohl,, 2005; Tsay,, 2014, and others). Such analysis not only reveals the temporal dynamics of the time series, but also explores the relationship among a group of time series, using the available information more fully. Often, the investigation of the relationship among the time series is the objective of the study.

Matrix-valued time series, when one observes a group of variables structured in a well defined matrix form over time, has not been studied. Such a time series is encountered in many applications. For example, in economics, countries routinely report a set of economic indicators (e.g. GDP growth, unemployment rate, inflation index and others) every quarter. Table 1 depicts such a matrix-valued time series. One can concentrate on one cell in Table 1, say US Unemployment rate series and build a univariate time series model. Or one can concentrate on one column in Table 1, say, all economic indicators of US and study it as a vector time series. Similarly, if one is interested in modeling GDP growth of the group of countries, a panel time series model can be built for the first row in Table 1. However, there are certainly relationships among all variables in the table and the matrix structure is extremely important. For example, the variables in the same column (same country) would have stronger inter-relationship. Same for the variables in the same row (same indicator). Hence it is important to analyze the entire group of variables while fully preserve and utilize its matrix structure.

| US | Japan | China | ||

|---|---|---|---|---|

| GDP | ||||

| Unemployment | ||||

| Inflation | ||||

| Payout Ratio |

There are many other examples. Investors may be interested in the time series of a group of financials (e.g. asset/equity ratio, dividend per share, and revenue) for a group of companies, the import-export volume among a group of countries, pollution and environmental variables (e.g. PM2.5, ozone level, temperature, moisture, wind speed, etc) observed at a group of stations. In this article we study such a matrix-valued time series.

Matrix-valued data has been studied (e.g. Gupta and Nagar,, 2000; Kollo and von Rosen,, 2006; Werner et al.,, 2008; Leng and Tang,, 2012; Yin and Li,, 2012; Zhao and Leng,, 2014; Zhou,, 2014; Zhou and Li,, 2014). Their study mainly focuses on independent observations. The concept of matrix-valued time series was introduced by Walden and Serroukh, (2002), applied in signal and image processing. Still, the temporal dependence of the time series was not fully exploited for model building.

In this article, we focus on high-dimensional matrix-valued time series data. In cases, we may allow the dimensions of the matrix to be as large as, or even larger than the length of the observations. A well-known issue often accompanying with high-dimensional data is the curse of dimensionality. We adopt a factor model approach. Factor analysis can effectively reduce the number of parameters involved, and is a powerful statistical approach to extracting hidden driving processes, or latent factor processes, from an observed stochastic process. In the past decades, factor models for high-dimensional time series data have drawn great attention from both econometricians and statisticians (e.g. Chamberlain and Rothschild,, 1983; Forni et al.,, 2000; Bai and Ng,, 2002; Hallin and Liška,, 2007; Pan and Yao,, 2008; Lam et al.,, 2011; Fan et al.,, 2011; Lam and Yao,, 2012; Fan et al.,, 2013; Chang et al.,, 2015; Liu and Chen,, 2016).

With the above observations and motivations, in this article, we aim to develop factor models for matrix-valued time series, which fully explore the matrix structure. The rest of this article is organized as follows. In Section 2, detailed model settings are introduced and interpretations are discussed in detail. Section 3 presents an estimation procedure. The theoretical properties of the estimators are also studied. Simulation results are shown in Section 4 and two real data examples are given in Sections 5 and 6. Section 7 provides a brief summary. All proofs are in Appendix.

2 Matrix Factor Models

Let () be a matrix-valued time series, where each is a matrix of size ,

We propose the following factor model for matrix-valued time series,

| (1) |

Here, is a unobserved matrix-valued time series of common fundamental factors, is a front loading matrix, is a back loading matrix, and is a error matrix. In model (1), the common fundamental factors ’s drive all dynamics and co-movement of . and reflect the importance of common factors and their interactions.

Similar to multivariate factor models, we assume that the matrix-valued time series is driven by a few latent factors. Unlike the classical factor model, the factors ’s in model (1) are assumed to be organized in a matrix form. Correspondingly, we adopt two loading matrices and to capture the dependency between each individual time series in the matrix observations and the matrix factors. In the following we provide two interpretations of the loading matrices. We first introduce some notation. For a matrix , we use and to represent the -th row and the -th column of , respectively, and to denote the -th element of .

Interpretation I: To isolate effects, assume and , then . In this case, each column of is a linear combination of the columns of . Take the example shown in Table 1 and consider the first column of (the US economic indicators),

US

It is seen that the US GDP only depends on the first row of . Similarly, other countries’ GDP also only depends on the first row of . Hence we can view the first row of as the GDP factors. Similarly, the second row of can be considered as the unemployment factors. There is no interaction between the indicators in this setting (when ). The loading matrix reflects how each country (column of ) depends on the columns of , hence reflects column interactions, or the interactions between the countries. Because of this, we will call the column loading matrix.

Similarly, the rows of can be viewed as common factors of all rows of , and the front loading matrix as row loading matrix. Again, assume and , it follows that . Then each row of is a linear combination of the rows of . Consider the first row of ,

US Japan … China US Japan … China

It is seen that all economic movements (of each country) are driven by (row) common factors. For example, every US’s indicator depends on only the first column of . Hence the first column of can be viewed as the US factor. And the second column of can be viewed as Japan factor. The loading matrix reflects how each indicator depends on the rows of . It reflects row interactions, the interactions between the indicators within each country. Because of this, we will call the row loading matrix.

Obviously column and row interaction would be of interests and of importance. One way to introduce interaction is to assume an additive structure, by combining the column and row factor models

However, the number of factors in this model is large (). A more parsimonious model would be a direct interaction as in model (1). In this case the number of factors is only .

Interpretation II: We can view the model (1) as a two-step hierarchical model.

Step 1: For each fixed row , using data , we can find a dimensional loading matrix and dimensional factors under a standard vector factor model setting. That is,

Let be the matrix formed with rows of . Also denote as the error matrix formed with the rows of .

Step 2: Suppose each column of the assembled factor matrix obtained in Step 1 also assumes the factor structure, with a loading matrix and a dimensional factor . That is,

This step reveals the common factors that drive the co-moments in . Let be the matrix formed with the columns . And let be the error matrix formed with columns .

Step 3: Assembly: With the above two-step factor analysis and notation, assume and , we have

Hence

where . It is identical to (1).

Here we provide some additional remarks of model (1).

Remark 1: Let be the vectorization operator, i.e., converts a matrix to a vector by stacking columns of the matrix on top of each other. The classical factor analysis treats as the observations, and a factor model is in the form of

| (2) |

where is a loading matrix, of length is the latent factor, is the error term, and is the total number of factors. On the other hand, note that model (1) can be re-written as

| (3) |

Assume . Then model (3) is a special case of model (2), with a Kronecker product structured loading matrix. Hence model (1) is a restricted version of model (2), assuming a special structure for the loading spaces. The number of parameters for the loading matrix in model (2) is whereas it is for the loading matrices and in model (1). Therefore, model (1) significantly reduces the dimension of the problem.

Remark 2: Interpretation II also reveals the reduction in the number of factors comparing to using factor models for each column panel or row panel. Note that, if one ignores the interconnection between the rows and obtain individual factor models for each row, as in Step 1, the total number of factors is . These factors may have connections across rows. Step 2 exploits such correlations and uses another factor model to reduce the number of factors from to .

Remark 3: We also observed that in practice, the total number of factors used in our model may be larger than the number of factors needed in the vectorized factor model (2). This is possible since the vectorized model simultaneously exploits common driving features in all series, while the matrix factor model does it by working on the row vectors separately first (Step 1), then condensing them by the columns (Step 2). Such a two-step approach may result in redundancy (highly correlated factors) which may be further simplified. Because we are forcing the factors to assume a neat matrix structure, it is difficult to have simplifications such as having one or several elements in the factor matrix be constant zero. Since and are usually small, we will tolerate such redundancy. One extension is to assume that the factor matrix , after a certain rotation, has a block diagonal structure, resulting in a multi-term factor model

| (4) |

where is a factor matrix, and and . This will reduce the number of factors from to , with corresponding dimension reduction in the loading matrices as well. We are currently investigating the properties and estimation procedures of such a multi-term factor model.

Remark 4: As in all factor model setting, the properties or assumptions on the observed process are inferred from the assumptions on the factors and the noise processes, since the observed series are assumed to be linear combinations of the factor processes plus the noise process. Indirectly, we assume that all autocovariance matrices of lag of all series lie in a structured space, but no assumption on the contemporary covariance matrix, as we do not assume any contemporary covariance structure on the error .

Remark 5: Similar models as model (1) have been proposed and studied when conducting principal component analysis on matrix-valued data (e.g. Paatero and Tapper,, 1994; Yang et al.,, 2004; Ye,, 2005; Ding and Ye,, 2005; Zhang and Zhou,, 2005; Crainiceanu et al.,, 2011; Wang et al.,, 2016). In those studies, the matrix-valued observations are assumed to be independent, and they primarily focused on principal component analysis. To the best of our knowledge, our paper is the first one considering factor models for matrix-valued time series data.

In this article, we extend the methods described in Lam et al., (2011) and Lam and Yao, (2012) for vector-valued factor model (2) to matrix-valued factor model (1). We propose estimators for the loading spaces and the numbers of row and column factors, investigate their theoretical properties, and establish their convergence rates. Simulated and real examples are presented to illustrate the performance of the proposed estimators, to compare the asymptotics under different conditions with different factor strengths, and to explore interactions between row and column factors.

3 Estimation and Modeling Procedures

Because of the latent nature of the factors, various assumptions are imposed to ‘define’ a factor. Two common assumptions are used. One assumes that the factors must have impact on most of the series, and weak serial dependence is allowed for the idiosyncratic noise process, see Chamberlain and Rothschild, (1983); Forni et al., (2000); Bai and Ng, (2002); Hallin and Liška, (2007), among others. Another assumes that the factors should capture all dynamics of the observed process, hence the idiosyncratic noise process has no serial dependence (but may have strong cross-sectional dependence), see Pan and Yao, (2008); Lam et al., (2011); Lam and Yao, (2012); Chang et al., (2015); Liu and Chen, (2016). Here we adopt the second assumption and assume that the vectorized error is a white noise process with mean and covariance matrix , and is independent of the factor process . For ease of presentation, we will assume that the process has mean , and the observations ’s are centered and standardized through out this paper.

For the vector-valued factor model (2), it is well-known that there exists an identifiable issue among the factors and the loading matrix . Similar problem also arises in the proposed matrix-valued factor model (1). Let and be two invertible matrices of sizes and . Then the triplets and are equivalent under model (1), and hence model (1) is not identifiable. However, with a similar argument as in Lam et al., (2011) and Lam and Yao, (2012), the column spaces of the loading matrices and are uniquely determined. Hence, in the following, we will focus on the estimation of the column spaces of and , denoted by and , and referred to as row factor loading space and column factor loading space, respectively.

We can further decompose and as follows,

where is a matrix with orthonormal columns and is a non-singular matrix, for . Let denote the column space of . Then we have and . Hence, the estimation of column spaces of and is equivalent to the estimation of column spaces of and .

Write

as a transformed latent factor process. Then, model (1) can be re-expressed as

| (5) |

Equation (5) can be viewed as another formulation of the matrix-valued factor model with orthonormal loading matrices. Since and , we will perform analysis on model (1) and (5) interchangeably whenever one is more convenient than the other.

3.1 Estimation

To estimate the matrix-valued factor model (1), we follow closely the idea of Lam et al., (2011) and Lam and Yao, (2012) in estimating vector-valued factor models. The key idea is to calculate auto-cross-covariances of the time series then construct a Box-Ljung type of statistics in matrix. Under the matrix factor model and white idiosyncratic noise assumption, the space spanned by such a matrix is directly linked with the loading matrices. In what follows, we will illustrate the method to obtain an estimate of . The column space of can be estimated in a similar way using the transposes of ’s.

Let the -th column of , , , and be , , , and , respectively. Let , and be the row vectors that denote the -th row of , and , respectively. Then it follows from (1) and (5) that

| (6) |

From the zero mean assumptions of both and , we have .

Let be a positive integer. Define

| (7) | |||||

| (8) |

for . By plugging (6) into (8) and by the assumption that is white, it follows that

| (9) |

for . For a pre-determined integer , define

| (10) |

Suppose the matrix has rank (Condition 5 in Section 3.2). From (11), we can see that each column of is a linear combination of columns of , and thus the matrices and have the same column spaces, that is, . It follows that the eigen-space of is the same as . Hence, can be estimated by the space spanned by the eigenvectors of the sample version of . Assume that has distinct nonzero eigenvalues, and let be the unit eigenvector corresponding to the -th largest eigenvalue. As there are two unit eigenvectors corresponding to each eigenvalue, we use the one with positive . We can now uniquely define by

Now we construct the sample versions of these quantities and introduce the estimation procedure as follows. For any positive integer and a pre-scribed positive integer , let

| (12) | |||||

| (13) |

Then, can be estimated by , where , and are the eigenvectors of corresponding to its largest eigenvalues.

In practice, the number of row factors is usually unknown. This quantity can be estimated through a similar eigenvalue ratio estimator as described in Lam and Yao, (2012). Let be the ordered eigenvalues of . Then

For and , they can be estimated by performing the same procedure on the transposes of ’s to construct and . Once and are obtained, the estimate of can be found via a general linear regression analysis, since

Together with the orthonormal properties of both and and the properties of Kronecker product, it follows that

Let be the dynamic signal part of , that is, . Then a natural estimator of is given by,

| (14) |

Remark 6: Theoretically any can be used to estimate the loading spaces, as long as one of the is of full rank for and . Although they converge at the same rate, the estimate from the lag where the autocorrelation maximizes is most efficient. We demonstrate the impact of in the matrix factor model setting in Section 4. As the autocorrelation is often at its strongest at small time lags, a relatively small is usually adopted (Lam et al.,, 2011; Chang et al.,, 2015; Liu and Chen,, 2016). Larger strengthens the signal, but also adds more noises in the estimation of .

Remark 7: -fold cross-validation procedures can be adopted for model selection between matrix-valued factor models in (1) and vector-valued factor models in (2), and among the models with different number of factors. Specifically, we first partition the data into subsets , and fit a factor model with each of the sets. Then we use the estimated loading spaces, together with the data in to obtain the dynamic signal process for , and obtain out-of-sample residuals. Residual sum of squares (RSS) of the folds is then adopted for model comparison. Rolling-validation which uses only the data before the block for estimation can be used as well.

3.2 Theoretical Properties of the Estimator

In this section, we study the asymptotic properties of the estimators under the setting that all , and grow to infinity while and are being fixed. In the following, for any matrix , we use , , , , and to denote the rank, the spectral norm, the Frobenius norm, the smallest nonzero singular value and the -th largest singular value of . When is a square matrix, we denote by , and the trace, maximum and minimum eigenvalues of , respectively. We write when and . Define

The following regularity conditions are imposed before we derive the asymptotics of the estimators.

Condition 1. The vector-valued process is -mixing. Specifically, for some , the mixing coefficients satisfy the condition , where

and is the -field generated by .

Condition 2. Let be the -th entry of . For any , , and , we assume that , where is a positive constant, and is given in Condition 1. In addition, there exists an such that , and , where , as and go to infinity and and are fixed. For and , , .

The latent process does not have to be stationary, but needs to satisfy the mixing condition (Condition 1) and boundedness condition (Condition 2). They are weaker than stationarity. For example, when a process has a deterministic seasonal variance component or with a deterministic regime switching mechanism, it is not stationary but mixing. We do not need to assume any specific model for the latent process since we only use the eigen-analysis based on autocovariances of the observed process at nonzero lags.

Under Condition 2, may not be of full rank, which indicates that it is allowed to involve some extent of redundancy in the factors. Condition 2 also guarantees that there is no redundant row or column in , and in each row or column there is at least one factor which has serial dependence at lag . The greater dimension reduction can be achieved by a multi-term factor model in (4). We are currently investigating the properties and estimation procedures of such a multi-term factor model.

Condition 3. Each element of remains bounded as and increase to infinity.

In model (1), can be viewed as the signal part of the observation , and as the noise. The signal strength, or the strength of the factors, can be measured by the -norm of the loading matrices which are assumed to grow with the dimensions.

Condition 4. There exist constants and such that and , as and go to infinity and and are fixed.

The rates and are called the strength for row factors and the strength for column factors, respectively. They measure the relative growth rate of the amount of information carried by the observed process on the common factors as the dimensions increase, with respect to the growth rate of the amount of noise. When , the factors are strong; when , the factors are weak, which means the information contained in on the factors grows more slowly than the noises introduced as increases. For detailed discussion of factor strength, see Lam and Yao, (2012).

Condition 5. has distinct positive eigenvalues for .

As stated in Section 3, only and are uniquely determined, while and are not. However, when the eigenvalues of are distinct, we can uniquely define as , where are the unit eigenvectors of corresponding to its largest eigenvalues which make , , , and all positive, for .

The following theorems show the rate of convergence for estimators of loading spaces and the eigenvalues.

Theorem 1.

Under Conditions 1-5 and , it holds that

Concerning the impact of ’s, it is not surprising that the stronger the factors are, the more useful information the observed process carries and the faster the estimators converge. More interestingly, the strengths of row factors and column factors and determine the rates together. An increase in the strength of row factors is able to improve the estimation of the column factors loading space and vice versa.

When and are fixed, the convergence rate for estimating the loading matrices are . If the loadings are strong (), the rate is also , since the signal is as strong as the noise, and the increase in dimensions will not affect the estimation of the loading spaces. When ’s are not 0, the noise increases faster than useful information. In this case, increases in dimension will dilute the information, resulting in less efficient estimators.

Theorem 2.

With Conditions 1-5 and , the eigenvalues of which are sorted in descending order satisfy

where are eigenvalues of , for .

Theorem 2 shows that the estimators for nonzero eigenvalues of converge more slowly than those for the zero eigenvalues. It provides the theoretical support for the ratio estimator proposed in Section 3.1.

The following theorem demonstrates the theoretical properties of the estimator in (14).

Theorem 3.

If Conditions 1-5 hold, , and is bounded, we have

where .

The theorem shows that, in order to estimate the signal consistently, dimensions and must go to infinity, in order to have sufficient information on at each time point .

Since is not identifiable in model (1), another measure to quantify the accuracy of factor loading matrices estimation is the distance between and . For two orthogonal matrices and of sizes and , define

Then is a quantity between and . It is equal to if the column spaces of and are the same and if they are orthogonal.

Theorem 4.

If Conditions 1-5 hold and , we have

Theorem 4 shows that the error to estimate loading spaces is on the same order as that for the estimated ’s.

4 Simulation

In this section, we study the numerical performance of the proposed matrix-valued approach. In all simulations, the observed data ’s are simulated according to model (1),

We choose the dimensions of the latent factor process to be and . The entries of are simulated as independent processes with noise where the types and coefficients of the processes will be specified later. The entries of and are independently sampled from the uniform distribution for , respectively. The error process is a white noise process with mean and a Kronecker product covariance structure, that is, , where and are of sizes and , respectively. Both and have values on the diagonal entries and on the off-diagonal entries. For all simulations, the reported results are based on simulation runs.

We first study the performance of our proposed approach on estimating the loading spaces. In this part, the latent factors are independent AR(1) processes with the AR coefficients . We consider three pairs of combinations: , and . For each pair of and , the two dimensions are chosen to be , and . The sample size is selected as , , and . We take since it is sufficient for AR(1) model as will be shown later.

Table 2 shows the results for estimating the loading spaces and . The accuracies are measured by and using the correct and , respectively. The results show that with stronger signals and more data sample points, the approach increases the estimation accuracies. Moreover, increasing the strength of one loading matrix can improve the estimation accuracies for both loading spaces.

With the same simulated data, we compare the proposed matrix-valued approach and the vector-valued approach in Lam and Yao, (2012) through the estimation accuracy of the total loading matrix . In what follows, the subscripts mat and vec denote our approach and Lam and Yao, (2012)’s method, respectively. The loading space is computed as once we obtain estimates of and through our approach. For the vector-valued approach, we apply Lam and Yao, (2012)’s method to the observations to obtain . Table 3 presents the results for the estimation accuracies of measured by and . It shows that the matrix approach efficiently improves the estimation accuracy over the vector-valued approach.

| 0.5 | 0.5 | 20 | 20 | 5.96(0.19) | 7.12(0.03) | 5.80(0.07) | 7.09(0.01) | 5.73(0.04) | 7.08(0.01) |

|---|---|---|---|---|---|---|---|---|---|

| 20 | 50 | 5.87(0.15) | 7.07(0.02) | 5.77(0.04) | 7.05(0.01) | 5.74(0.02) | 7.04(0.01) | ||

| 50 | 50 | 6.26(0.56) | 7.05(0.01) | 5.73(0.13) | 7.04(0.00) | 5.61(0.03) | 7.03(0.00) | ||

| 0.5 | 0 | 20 | 20 | 5.36(0.41) | 5.42(2.22) | 4.27(1.13) | 1.66(1.70) | 1.52(0.75) | 0.54(0.17) |

| 20 | 50 | 5.02(0.67) | 5.15(1.61) | 1.82(0.77) | 1.32(0.60) | 0.54(0.18) | 0.53(0.17) | ||

| 50 | 50 | 3.68(0.48) | 3.44(1.23) | 1.31(0.20) | 0.65(0.19) | 0.51(0.07) | 0.28(0.08) | ||

| 0 | 0 | 20 | 20 | 0.55(0.16) | 0.44(0.10) | 0.36(0.08) | 0.31(0.06) | 0.24(0.04) | 0.22(0.04) |

| 20 | 50 | 0.25(0.06) | 0.36(0.07) | 0.16(0.03) | 0.26(0.05) | 0.10(0.02) | 0.18(0.03) | ||

| 50 | 50 | 0.13(0.02) | 0.12(0.02) | 0.09(0.01) | 0.08(0.01) | 0.06(0.01) | 0.06(0.01) | ||

| 0.5 | 0.5 | 20 | 20 | 8.75(0.17) | 8.26(0.07) | 8.24(0.18) | 8.19(0.03) | 7.62(0.17) | 8.16(0.02) |

|---|---|---|---|---|---|---|---|---|---|

| 20 | 50 | 8.72(0.10) | 8.20(0.06) | 8.40(0.09) | 8.15(0.01) | 7.92(0.16) | 8.13(0.01) | ||

| 50 | 50 | 8.51(0.14) | 8.34(0.22) | 7.62(0.14) | 8.13(0.05) | 6.81(0.06) | 8.09(0.01) | ||

| 0.5 | 0 | 20 | 20 | 6.40(0.29) | 7.19(1.13) | 5.50(0.31) | 4.66(1.45) | 4.37(0.45) | 1.64(0.72) |

| 20 | 50 | 5.64(0.24) | 6.75(1.13) | 4.75(0.35) | 2.30(0.80) | 3.37(0.45) | 0.78(0.20) | ||

| 50 | 50 | 5.07(0.10) | 4.92(0.94) | 4.46(0.29) | 1.47(0.23) | 2.73(0.46) | 0.59(0.08) | ||

| 0 | 0 | 20 | 20 | 3.64(0.23) | 0.71(0.16) | 2.77(0.16) | 0.48(0.08) | 2.07(0.13) | 0.33(0.04) |

| 20 | 50 | 2.84(0.18) | 0.44(0.07) | 2.13(0.10) | 0.30(0.05) | 1.56(0.07) | 0.21(0.03) | ||

| 50 | 50 | 1.85(0.10) | 0.18(0.02) | 1.34(0.06) | 0.12(0.01) | 0.97(0.04) | 0.09(0.01) | ||

We next demonstrate the performance of the matrix-valued approach on estimating the number of factors, and . The data are the same as the data in Table 2 with and hence the true rank pair is . Table 4 shows the relative frequencies of estimated rank pairs over simulation runs. The four pairs , , and have high appearances in all of the combinations of , and . The row for the true rank pair is highlighted. It shows that the relative frequency of correctly estimating the true rank pair improves with increasing sample size . Table 5 shows a comparison between the matrix and vector-valued approaches on estimating the total number of latent factors . The column with the true rank is highlighted. The results show that the two approaches have similar performance when the sample size is large. For smaller , the probability of the matrix-valued approach to select the rank pair is high and hence the frequency of estimating the true rank decreases.

| , | , | , | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (2,1) | 0.2 | 0.055 | 0 | 0.32 | 0.005 | 0 | 0 | 0 | 0 |

| (2,2) | 0.055 | 0.04 | 0 | 0.025 | 0.005 | 0 | 0 | 0 | 0 |

| (3,1) | 0.19 | 0.215 | 0.01 | 0.47 | 0.325 | 0.005 | 0.005 | 0 | 0 |

| (3,2) | 0.365 | 0.66 | 0.985 | 0.17 | 0.665 | 0.995 | 0.995 | 1 | 1 |

| Others | 0.19 | 0.03 | 0.005 | 0.015 | 0 | 0 | 0 | 0 | 0 |

| Others | ||||||||||||||

| vec | mat | vec | mat | vec | mat | vec | mat | vec | mat | vec | mat | |||

| 20 | 20 | 0.25 | 0.125 | 0.33 | 0.22 | 0.035 | 0.19 | 0.015 | 0.07 | 0.345 | 0.365 | 0.025 | 0.03 | |

| 0.055 | 0.02 | 0.105 | 0.06 | 0 | 0.215 | 0 | 0.045 | 0.83 | 0.66 | 0.01 | 0 | |||

| 0 | 0 | 0.005 | 0 | 0 | 0.01 | 0 | 0.005 | 0.995 | 0.985 | 0 | 0 | |||

| 20 | 50 | 0.03 | 0.015 | 0.62 | 0.32 | 0 | 0.47 | 0 | 0.025 | 0.34 | 0.17 | 0.01 | 0 | |

| 0 | 0 | 0.14 | 0.005 | 0 | 0.325 | 0 | 0.005 | 0.86 | 0.665 | 0 | 0 | |||

| 0 | 0 | 0 | 0 | 0 | 0.005 | 0 | 0 | 1 | 0.995 | 0 | 0 | |||

| 50 | 50 | 0.07 | 0 | 0 | 0 | 0 | 0.005 | 0 | 0 | 0.93 | 0.995 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | |||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | |||

We now study the effects of the lag parameter . The factors are assumed to be independent and follow the same model which is either an AR(1) or an MA(2) model. For the AR(1) model, the coefficients of all the factors are , or . For the MA(2) model, we consider the case . We take , and compare the estimation accuracies of the two loading spaces for four lag choices, . Table 6 shows the results of and . It is seen that, for the AR(1) processes, taking is sufficient. Larger in fact decreases the performance, especially for small AR coefficient cases. Note that larger increases the signal strength in the matrix , but also increases the noise level in its sample version . For an AR(1) model with small AR coefficient, the autocorrelation in higher lags is relatively small hence the additional signal strength is limited. For the MA(2) process, one must use since lag 1 autocovariance matrix is zero and does not provide any information. performs the best, since all higher lags carry no additional information, but add significant amount of noise.

| AR(1) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.9 | 20 | 20 | 0.13(0.02) | 0.10(0.02) | 0.13(0.02) | 0.10(0.02) | 0.14(0.02) | 0.10(0.02) | 0.14(0.02) | 0.11(0.02) |

| 20 | 50 | 0.05(0.01) | 0.07(0.01) | 0.05(0.01) | 0.07(0.01) | 0.05(0.01) | 0.07(0.01) | 0.06(0.01) | 0.08(0.01) | |

| 50 | 50 | 0.03(0.00) | 0.03(0.00) | 0.03(0.00) | 0.03(0.00) | 0.03(0.00) | 0.03(0.00) | 0.03(0.00) | 0.03(0.00) | |

| 0.6 | 20 | 20 | 0.36(0.07) | 0.26(0.04) | 0.41(0.08) | 0.27(0.05) | 0.47(0.10) | 0.28(0.05) | 0.53(0.12) | 0.29(0.05) |

| 20 | 50 | 0.15(0.03) | 0.19(0.02) | 0.18(0.04) | 0.20(0.03) | 0.21(0.05) | 0.21(0.03) | 0.24(0.06) | 0.21(0.03) | |

| 50 | 50 | 0.09(0.01) | 0.07(0.01) | 0.10(0.01) | 0.08(0.01) | 0.11(0.02) | 0.08(0.01) | 0.12(0.02) | 0.08(0.01) | |

| 0.3 | 20 | 20 | 1.56(0.72) | 0.57(0.13) | 2.31(0.99) | 0.60(0.16) | 2.82(1.04) | 0.63(0.18) | 3.12(1.05) | 0.67(0.18) |

| 20 | 50 | 0.64(0.21) | 0.45(0.10) | 1.14(0.49) | 0.49(0.13) | 1.66(0.68) | 0.55(0.19) | 2.13(0.82) | 0.63(0.24) | |

| 50 | 50 | 0.26(0.05) | 0.17(0.03) | 0.39(0.08) | 0.18(0.03) | 0.56(0.11) | 0.20(0.04) | 0.74(0.14) | 0.21(0.04) | |

| MA(2) | 20 | 20 | 2.60(1.11) | 0.88(0.28) | 0.48(0.12) | 0.27(0.05) | 0.59(0.15) | 0.28(0.05) | 0.68(0.17) | 0.28(0.06) |

| 20 | 50 | 2.76(1.16) | 1.13(0.56) | 0.21(0.04) | 0.21(0.03) | 0.27(0.06) | 0.22(0.04) | 0.32(0.07) | 0.22(0.04) | |

| 50 | 50 | 2.85(1.15) | 0.68(0.23) | 0.11(0.02) | 0.08(0.01) | 0.13(0.02) | 0.08(0.01) | 0.15(0.02) | 0.08(0.01) | |

Next we study the performance of recovering the signal . The latent factors are simulated in the same way as the data in Table 2. We take , , and . The recovery accuracy of , denoted by , is estimated by the average of for further normalized by , that is, . Table 7 presents the results of and for the two approaches. It shows that, when is relatively large (hence the is estimated relatively accurately), increasing improves the estimation of . For the same and relatively large , further increasing has a limited benefit in improving the estimation of . The estimation accuracies of of the proposed matrix-valued approach are better than that of the vector-valued approach, though the relative improvement decreases as increases, even the improvement of estimating is significant.

| 10 | 50 | 6.26(0.38) | 3.66(0.92) | 4.05(0.28) | 3.41(0.39) |

|---|---|---|---|---|---|

| 200 | 4.11(0.33) | 1.42(0.42) | 3.02(0.19) | 2.62(0.15) | |

| 1000 | 2.12(0.13) | 0.50(0.09) | 2.48(0.05) | 2.40(0.04) | |

| 5000 | 0.99(0.05) | 0.21(0.03) | 2.38(0.02) | 2.36(0.01) | |

| 20 | 50 | 5.65(0.39) | 2.36(1.26) | 3.07(0.27) | 1.86(0.61) |

| 200 | 3.64(0.23) | 0.71(0.16) | 1.96(0.16) | 1.11(0.05) | |

| 1000 | 1.88(0.11) | 0.29(0.04) | 1.25(0.05) | 1.02(0.01) | |

| 5000 | 0.87(0.03) | 0.13(0.01) | 1.04(0.01) | 1.00(0.00) | |

| 50 | 50 | 5.81(0.35) | 3.17(1.47) | 2.64(0.26) | 1.95(0.79) |

| 200 | 3.78(0.24) | 0.62(0.19) | 1.57(0.16) | 0.56(0.09) | |

| 1000 | 2.04(0.10) | 0.21(0.03) | 0.82(0.06) | 0.42(0.01) | |

| 5000 | 0.97(0.04) | 0.09(0.01) | 0.49(0.02) | 0.40(0.00) |

Next, we conduct a -fold cross-validation study. The data are generated in the same way as the data in Table 2 with , and . We vary the estimated number of factors and from all combinations of and . The means of the out-of-sample RSS/SST are reported in Table 8. For the matrix-valued approach, the RSS/SST decreases rapidly when and increase, before they reach the true rank pair (highlighted in the table). Then the RSS/SST value remain roughly the same with increasing estimated ranks when and . For the vector-valued approach, , hence the values in the table are the same for the same value (e.g. and are equivalent). Its performance improves quickly as increases until , the true number of factors. Then the performance remains relatively the same for .

| vec | mat | vec | mat | vec | mat | |

| 1 | 0.83 | 0.83 | 0.72 | 0.75 | 0.63 | 0.75 |

| 2 | 0.72 | 0.71 | 0.58 | 0.56 | 0.49 | 0.55 |

| 3 | 0.63 | 0.67 | 0.49 | 0.47 | 0.46 | 0.46 |

| 4 | 0.58 | 0.66 | 0.46 | 0.47 | 0.44 | 0.43 |

5 Real Example: Fama-French 10 by 10 Series

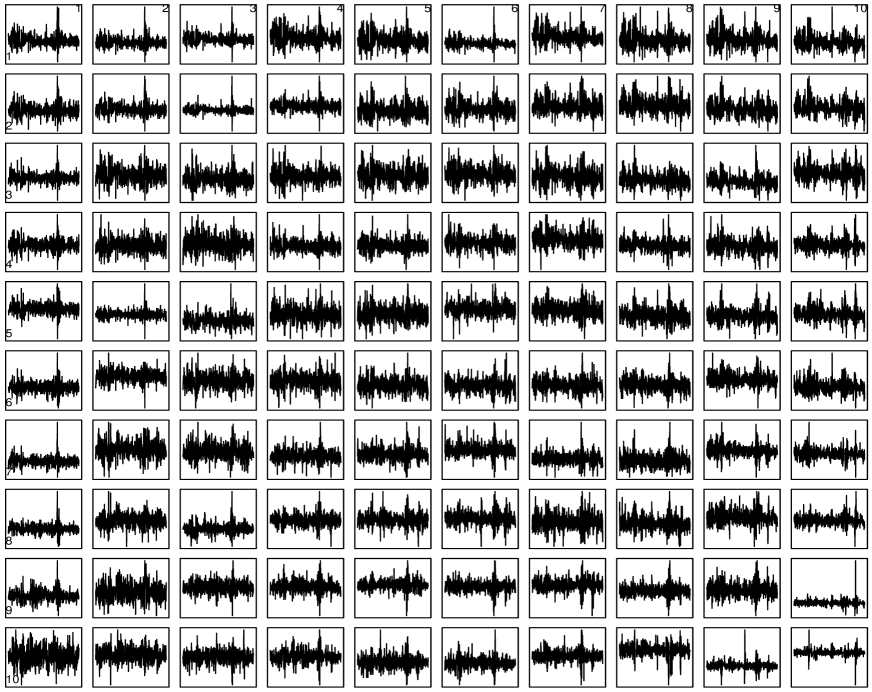

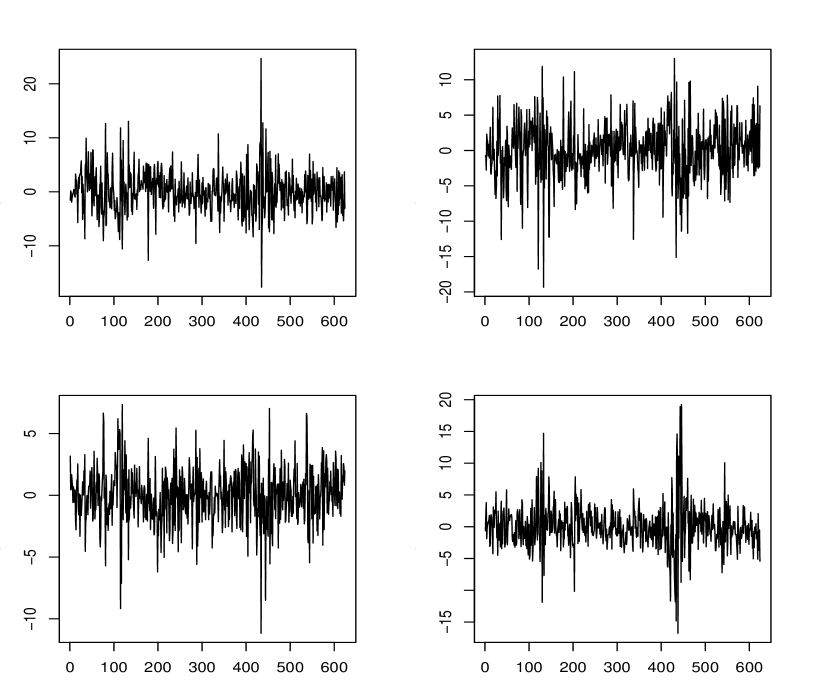

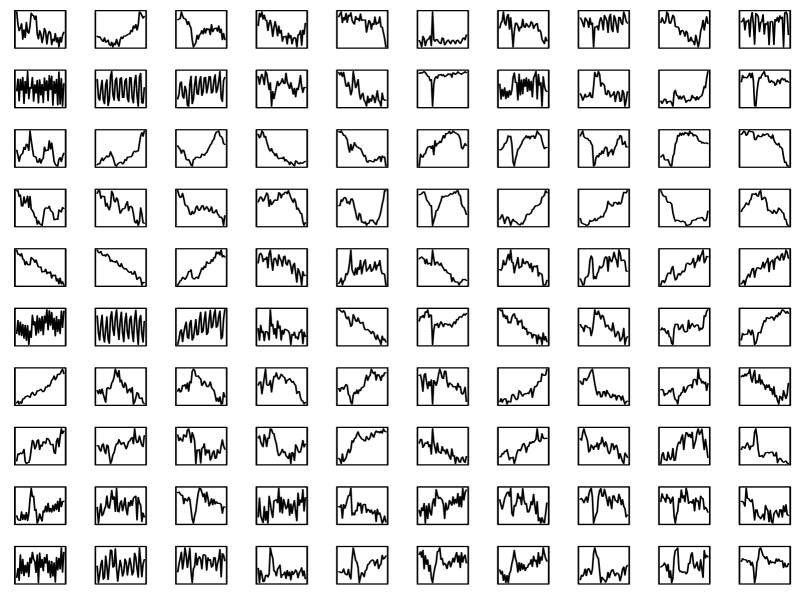

In this section we illustrate the matrix factor model using the Fama-French 10 by 10 return series. A universe of stocks is grouped into 100 portfolios, according to ten levels of market capital (size) and ten levels of book to equity ratio (BE). Their monthly returns from January 1964 to December, 2015 for total 624 months and overall 62,400 observations are used in this analysis. For more detailed information, see http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.

All the 100 series are clearly related to the overall market condition. In this analysis we simply subtract the corresponding monthly excess market return from each of the series, resulting in 100 market-adjusted return series. We chose not to fit a standard CAPM model to each of the series to remove the market effect, as it will involve estimating 100 different betas. The market return data are obtained from the same website above.

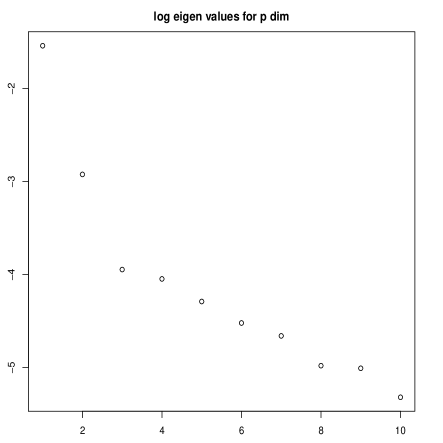

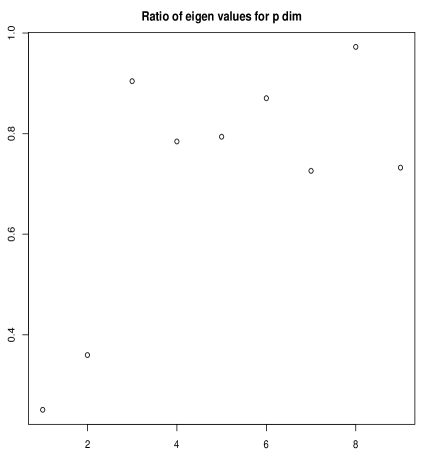

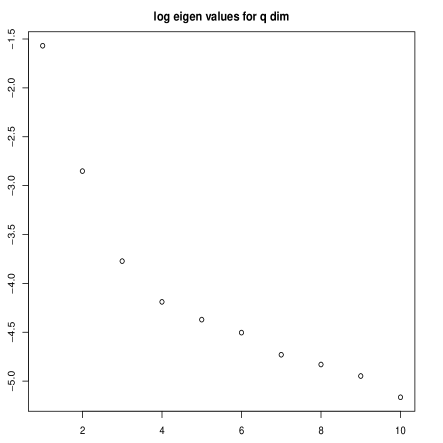

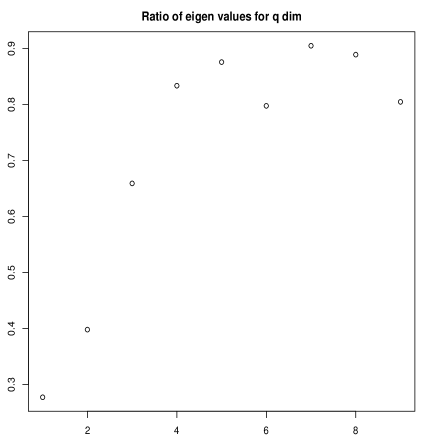

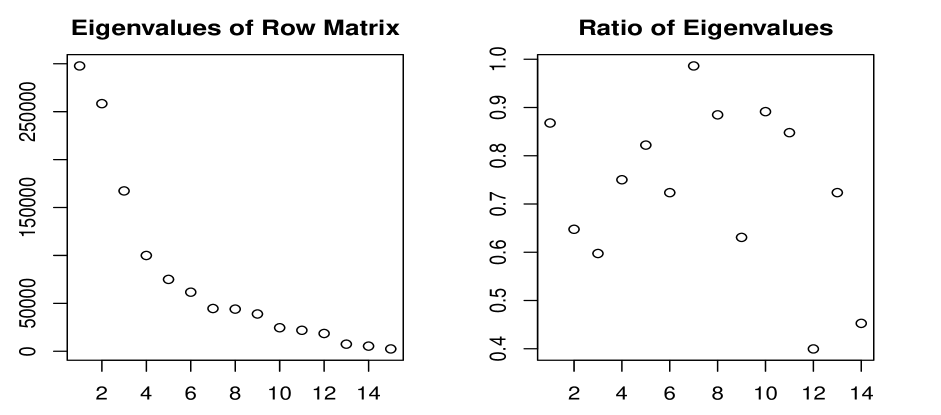

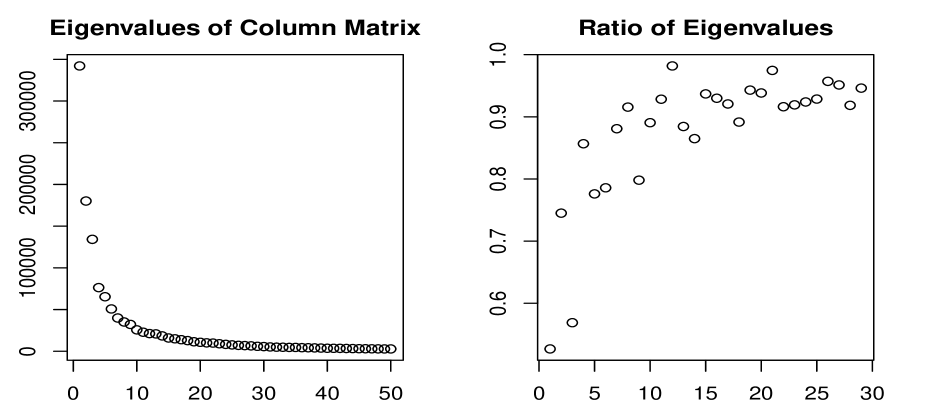

Figure 1 shows the time series plot of the 100 series (standardized), and Figures 2 and 3 show the logarithms and ratios of eigenvalues of and for the row (size) and column (BE) loading matrices. Since the series shows very small autocorrelation beyond , in this example we use . The results by using are similar. Although the eigenvalue ratio estimate presented in Section 3.1 indicates , we use here for illustration. Tables 9 and 10 show the estimated loading matrices after a varimax rotation that maximizes the variance of the squared factor loadings, scaled by 30 for a cleaner view. For size, it is seen that there are possibly two or three groups. The -st to -th smallest size portfolios load heavily (with roughly equal weights) on the first row of the factor matrix, while the -th to -th smallest size portfolios load heavily (with roughly equal weights) on the second row of the factor matrix. The largest (-th) size portfolio behaves similar to the other larger size portfolios, but with some differences. We note that the Fama-French size factor proposed in Fama and French, (1993) is constructed using the return differences of the largest 30% of the companies (combining the -th to -th size portfolio) and the smallest 30% of the companies (combining our st to rd size portfolio).

Turning to the book to equity ratio, Table 10 shows a different pattern in the column loading matrix. There seem to have three groups. The smallest -nd to -th BE portfolios load heavily on the first column of the factor matrix; the th to th BE portfolios load heavily on the second columns of the factor matrix. The smaller (st) BE portfolios load heavily on both columns of the factor matrix, with different loading coefficients.

Figure 4 shows the estimated factor matrices over time. It can be potentially used to replace the Fama-French size factor (SMB) and book to equity factor (HML) in a Fama-French factor model for asset pricing, factor trading and other usage, though further analysis is needed to assess their effectiveness. Cross-correlation study shows that there are not many significant cross-correlation of lag larger than 0 among the factors, though the factors show some strong contemporary correlation as the factor matrices are subject to rotation – in our case we performed rotation to reveal the group structure in the loading matrices. A principle component analysis of the four factor series reveals that three principle components can explain 98% of the variation in the four factors, hence there may still be some redundancy in the factors and the model may be further simplified.

| Factor | S1 | S2 | S3 | S4 | S5 | S6 | S7 | S8 | S9 | S10 |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | -13 | -14 | -13 | -13 | -10 | -5 | -2 | 1 | 6 | 7 |

| 2 | 0 | 0 | -2 | 3 | 5 | 12 | 12 | 18 | 15 | 5 |

| Factor | BE1 | BE2 | BE3 | BE4 | BE5 | BE6 | BE7 | BE8 | BE9 | BE10 |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | -21 | -14 | -11 | -9 | -4 | -1 | -1 | -4 | 1 | 3 |

| 2 | -9 | 2 | 3 | 7 | 9 | 10 | 10 | 10 | 13 | 14 |

| factor | RSS | # factors | # parameters | |

| Matrix model | (0,0) | 29,193 | 0 | 0 |

| Matrix model | (2,2) | 14,973 | 4 | 40 |

| Matrix model | (2,3) | 14,514 | 6 | 50 |

| Matrix model | (3,2) | 14,166 | 6 | 50 |

| Matrix model | (3,3) | 13,530 | 9 | 60 |

| Vector model | 3 | 16,262 | 3 | 300 |

| Vector model | 4 | 15,365 | 4 | 400 |

| Vector model | 5 | 14,565 | 5 | 500 |

| Vector model | 6 | 14,149 | 6 | 600 |

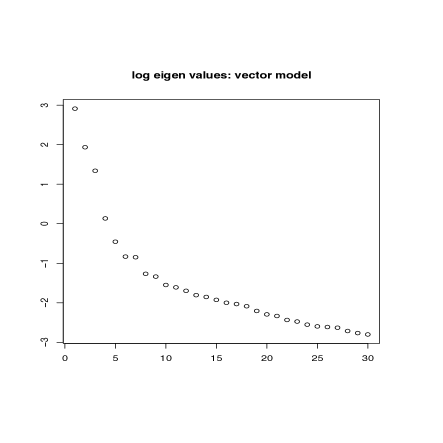

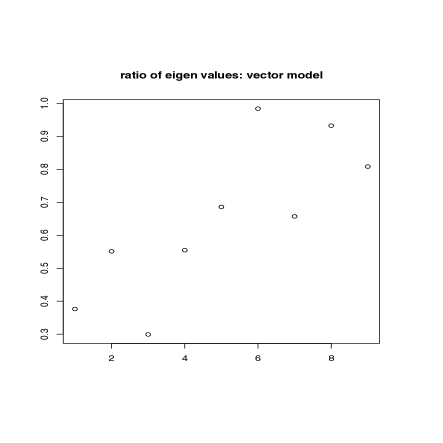

Figure 5 shows the logarithms and ratios of eigenvalues of in Lam et al., (2011) for a vectorized factor model (2). Models with various number of factors were estimated and a comparison is shown in Table 11 using a version of rolling-validation. Specifically, for each year between 1996 to 2015, we use all data available before the year to fit a matrix (or vector) factor model and estimate the corresponding loading matrices. Using these estimated loading matrices and the observed 12 months of the data in the year, we estimate the factors and the corresponding residuals. Total sum of squares of the 12 residuals of the 100 series of the 20 years are reported. The RSS corresponding to model is the total sum of squares of the observed 100 series of the 20 years being studied. It is seen that the matrix factor model with factor matrices performs better than the vectorized factor model with equal number of factors and many more parameters in the loading matrices. The matrix factor model performs similarly as the 6-factor vectorized factor model, but the number of parameters used is much smaller.

6 Real Example: Series of Company Financials

In this example we analyze the series of financial data reported by a group of 200 companies. We constructed 16 financial characteristics based on company quarterly financial reports. The list of variables and their definitions is given in Appendix 2. The period is from the first quarter of 2006 to the fourth quarter of 2015 for 10 years with total 40 observations. The total number of time series is 3,200.

Figures 6 and 7 show the eigenvalues and their ratios of and for row factors and column factors. The estimated dimensions and are both 3, though we use and for this illustration, with interesting results. Estimation is done using .

The estimated row loading matrix is rotated to maximize its variance, with potential grouping shown by the shaded areas in Table 12. It shows the loading of each financial on the five rows of the factor matrix, after proper scaling (30 times) and reordering for easy visualization. The two financials in Group 1 load almost exclusively on Row 1 of the factor matrix, with almost the same weights. The six financials in Group 2 load heavily on Row 2, again with almost the same weights. The three financials in Group 3 load on Rows 3 and 4, with somewhat different weights. Finally, the five financials in Group 4 mainly load on Row 5 of the factor matrix, with Payout.Ratio having opposite weights from the others.

The detailed grouping is shown in Table 13. Group 1 consists of asset to equity ratio and liability to equity ratio. They are two very closely related measures. Group 2 consists of six measures on earnings and returns. Group 3 consists of cash and revenue per share, and gross margin. Group 4 consists of profit growth and revenue growth comparing to the previous quarter and the same quarter last year. The Payout Ratio variable is also included in the group. Such groupings are relatively expected.

| Row Factor | F1 | F2 | F3 | F4 | F5 | F6 | F7 | F8 | F9 | F10 | F11 | F12 | F13 | F14 | F15 | F16 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 21 | 21 | -1 | -1 | -1 | -1 | -1 | 4 | -2 | 2 | 1 | 0 | 1 | 0 | 0 | -1 |

| 2 | 1 | 1 | -13 | -9 | -11 | -11 | -13 | -12 | 7 | -6 | -1 | 3 | -1 | 1 | 0 | 1 |

| 3 | 0 | 0 | 0 | -10 | 0 | -1 | 0 | -1 | -11 | 9 | -24 | -4 | -1 | 2 | -2 | 0 |

| 4 | 0 | 0 | -3 | 2 | 5 | 4 | -2 | -2 | 19 | 21 | -2 | 4 | 1 | 3 | 0 | -1 |

| 5 | 0 | 0 | -1 | 1 | 2 | 0 | -2 | -2 | -4 | 2 | 1 | 9 | -8 | -13 | -14 | -18 |

| Group 1 | AssetE.R | LiabilityE.R | ||||

|---|---|---|---|---|---|---|

| Group 2 | Earnings.R | EPS | Oper.M | Profit.Margin | ROA | ROE |

| Group 3 | Cash.PS | Gross.Margin | Revenue.PS | |||

| Group 4 | Payout.R | Profit.G.Q | Profit.G.Y | Revenue.G.Q | Revenue.G.Y |

Based on the 200 rows of the estimated columns loading matrix (corresponding to the companies), after rotation to maximize the variance, the companies are grouped into 6 groups. Table 14 shows the grouping corresponding to the industry classification index. The pattern is not as clear as the clustering of the row loading matrix but we still make some interesting discoveries. Industrial companies are mainly clustered in Groups 1 to 3; Health Care companies in Groups 2 and 3; Information Technology companies in Groups 1, 3 and 5; and Materials companies in Group 3. Looking from the other angle, we find that Group 4 mainly contains Energy companies; Group 5 mainly contains Consumer Discretionary, Financials and Information Technology companies; Group 6 mainly contains Utility companies.

Figure 8 shows the total 100 factor series in the 5 by 20 factor matrix. Interpretation of the factors is difficult. There are significant redundancy and correlation among the factors, since we have 100 factors but the time series length is only 40. Clearly the model tends to overfit. This example is for illustration purpose only, though we do find interesting features.

| group | 1 | 2 | 3 | 4 | 5 | 6 |

|---|---|---|---|---|---|---|

| Consumer Discretionary | 2 | 3 | 4 | 1 | 5 | 4 |

| Consumer Staples | 3 | 4 | 6 | 1 | 0 | 1 |

| Energy | 2 | 3 | 4 | 9 | 0 | 4 |

| Financials | 0 | 5 | 2 | 0 | 4 | 0 |

| Health Care | 0 | 5 | 17 | 0 | 1 | 2 |

| Industrials | 12 | 7 | 17 | 0 | 1 | 2 |

| Information Technology | 4 | 0 | 12 | 0 | 5 | 0 |

| Materials | 2 | 5 | 8 | 1 | 1 | 1 |

| Telecommunications Services | 0 | 2 | 1 | 0 | 0 | 0 |

| Utilities | 0 | 6 | 5 | 1 | 0 | 13 |

| factor | RSS | RSS/SST | # factors | # parameters | |

| Matrix model | (4,10) | 86,739 | 0.701 | 40 | 2,064 |

| Matrix model | (4,20) | 74,848 | 0.610 | 80 | 4,064 |

| Matrix model | (5,10) | 84.517 | 0.688 | 50 | 2,080 |

| Matrix model | (5,20) | 71,535 | 0.582 | 100 | 4,080 |

| Matrix model | (5,30) | 65,037 | 0.530 | 150 | 6,080 |

| Vector model | 3 | 79,704 | 0.650 | 3 | 9,600 |

| Vector model | 4 | 73,457 | 0.598 | 4 | 12,800 |

| Vector model | 5 | 68,428 | 0.557 | 5 | 16,000 |

| Vector model | 6 | 63,031 | 0.514 | 6 | 19,200 |

Table 15 shows a simple comparison between the matrix factor models and vectorized factor models of various size and number of factors. Since the time series is short, the table shows in-sample residual sum of squares. Again, it is seen that the matrix factor models use much fewer parameters in loading matrices to achieve similar estimation performance. The number of parameters involved is large as we are jointly modeling 3,200 time series.

7 Summary

In this paper we propose a matrix factor model for high-dimensional matrix-valued time series, along with an estimation procedure. Theoretical analysis shows the asymptotic properties of the estimators. Simulation and real examples are used to illustrate the model and finite sample properties of the estimators. The real examples show the usefulness of the model and its ability to reveal interesting features of high-dimensional time series. Significant amount of effort is needed to investigate model validation and model comparison procedures for the proposed model. Extensions to multi-term model and approaches to simply reducing factor redundancy are important research topics. Extending the model to dynamic factor model with an imposed dynamic structure on the factor matrix will be useful in terms of prediction and better understanding the dynamic nature of the matrix-valued time series.

Acknowledgments

We thank the Editors and two anonymous referees for their helpful insightful comments and suggestions, which lead to significant improvement of the paper in motivation and justification, design of simulation study and the analysis of real examples.

References

- Bai and Ng, (2002) Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica, 70(1):191–221.

- Bollerslev, (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3):307–327.

- Box and Jenkins, (1976) Box, G. and Jenkins, G. (1976). Time Series Analysis, Forecasting and Control. Holden Day: San Francisco.

- Brockwell and Davis, (1991) Brockwell, P. and Davis, R. A. (1991). Time Series: Theory and Methods. Springer.

- Chamberlain and Rothschild, (1983) Chamberlain, G. and Rothschild, M. (1983). Arbitrage, factor structure, and mean—variance analysis on large asset markets. Econometrica, 51(5):1281–1304.

- Chang et al., (2015) Chang, J., Guo, B., and Yao, Q. (2015). High dimensional stochastic regression with latent factors, endogeneity and nonlinearity. Journal of Econometrics, 189(2):297–312.

- Crainiceanu et al., (2011) Crainiceanu, C. M., Caffo, B. S., Luo, S., Zipunnikov, V. M., and Punjabi, N. M. (2011). Population Value Decomposition, a Framework for the Analysis of Image Populations. Journal of the American Statistical Association, 106(495):775–790.

- Ding and Ye, (2005) Ding, C. and Ye, J. (2005). 2-Dimensional Singular Value Decomposition for 2D Maps and Images. In Proc. SIAM Int’l Conf. Data Mining (SDM’05), pages 32–43.

- Engle, (1982) Engle, R. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflactions. Econometrika, 59:987–1007.

- Engle and Kroner, (1995) Engle, R. and Kroner, K. (1995). Multivariate simultaneous generalized arch. Econometric Theory, 11(1):122–150.

- Fama and French, (1993) Fama, E. F. and French, K. R. (1993). The cross-section of expected stock returns. Journal of Finance, 47:427–465.

- Fan et al., (2011) Fan, J., Liao, Y., and Mincheva, M. (2011). High dimensional covariance matrix estimation in approximate factor models. Annals of Statistics, 39(6):3320.

- Fan et al., (2013) Fan, J., Liao, Y., and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(4):603–680.

- Fan and Yao, (2003) Fan, J. and Yao, Q. (2003). Nonlinear Time Series: Nonparametric and Parametric Methods. Springer.

- Forni et al., (2000) Forni, M., Hallin, M., Lippi, M., and Reichlin, L. (2000). The generalized dynamic-factor model: identification and estimation. Review of Economics and Statistics, 82(4):540–554.

- Gupta and Nagar, (2000) Gupta, A. K. and Nagar, D. K. (2000). Matrix Variate Distributions. Chapman & Hall/CRC, Boca Raton, FL.

- Hallin and Liška, (2007) Hallin, M. and Liška, R. (2007). Determining the number of factors in the general dynamic factor model. Journal of the American Statistical Association, 102(478):603–617.

- Kollo and von Rosen, (2006) Kollo, T. and von Rosen, D. (2006). Advanced multivariate statistics with matrices, volume 579. Springer.

- Lam and Yao, (2012) Lam, C. and Yao, Q. (2012). Factor modeling for high-dimensional time series: inference for the number of factors. Annals of Statistics, 40(2):694–726.

- Lam et al., (2011) Lam, C., Yao, Q., and Bathia, N. (2011). Estimation of latent factors for high-dimensional time series. Biometrika, 98(4):901–918.

- Leng and Tang, (2012) Leng, C. and Tang, C. Y. (2012). Sparse matrix graphical models. Journal of the American Statistical Association, 107(499):1187–1200.

- Liu and Chen, (2016) Liu, X. and Chen, R. (2016). Regime-switching factor models for high-dimensional time series. Statistica Sinica, 26:1427–1451.

- Lütkepohl, (2005) Lütkepohl, H. (2005). New introduction to multiple time series analysis. Springer, Berlin.

- Merikoski and Kumar, (2004) Merikoski, J. K. and Kumar, R. (2004). Inequalities for spreads of matrix sums and products. Applied Mathematics E-Notes, 4:150–159.

- Paatero and Tapper, (1994) Paatero, P. and Tapper, U. (1994). Positive matrix factorization: a non-negative factor model wiht optimal utilization of errorestimates of data vaelus. Biometrika, 5(1):111–126.

- Pan and Yao, (2008) Pan, J. and Yao, Q. (2008). Modelling multiple time series via common factors. Biometrika, 95(2):365–379.

- Stock and Watson, (2004) Stock, J. and Watson, M. (2004). An empirical comparison of methods for forecasting using many predictors. Technical Report, Department of Economics, Havard University.

- Tiao and Box, (1981) Tiao, G. and Box, G. (1981). Modelling multiple time series with applications. Journal of the American Statistical Association, 76(376):802–816.

- Tiao and Tsay, (1989) Tiao, G. and Tsay, R. (1989). Model specification in multivariate time series. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 51(2):157–213.

- Tong, (1990) Tong, H. (1990). Nonlinear Time Series Analysis: A Dynamical System Approach. London: Oxford University Press.

- Tsay, (2005) Tsay, R. (2005). Analysis of Financial Time Series. New York: Wiley.

- Tsay, (2014) Tsay, R. (2014). Multivariate Time Series Analysis. New York: Wiley.

- Walden and Serroukh, (2002) Walden, A. and Serroukh, A. (2002). Wavelet analysis of matrix-valued time series. Proceedings: Mathematical, Physical and Engineering Sciences, 458(2017):157–179.

- Wang et al., (2016) Wang, D., Shen, H., and Truong, Y. (2016). Efficient dimension reduction for high-dimensional matrix-valued data. Neurocomputing, 190:25–34.

- Werner et al., (2008) Werner, K., Jansson, M., and Stoica, P. (2008). On estimation of covariance matrices with Kronecker product structure. IEEE Transactions on Signal Processing, 56(2):478–491.

- Yang et al., (2004) Yang, J., Zhang, D., Frangi, A. F., and Yang, J. (2004). Two-Dimensional PCA: A New Approach to Appearance-Based Face Representation and Recognition. IEEE Transactions on Pattern Analysis and Machine Intelligence, 26(1):131–137.

- Ye, (2005) Ye, J. (2005). Generalized Low Rank Approximations of Matrices. Machine Learning, 61(1-3):167–191.

- Yin and Li, (2012) Yin, J. and Li, H. (2012). Model selection and estimation in the matrix normal graphical model. Journal of Multivariate Analysis, 107(0):119–140.

- Zhang and Zhou, (2005) Zhang, D. and Zhou, Z. (2005). (2D)2PCA: Two-directional two-dimensional PCA for efficient face representation and recognition. Neurocomputing, 69(1):224–231.

- Zhao and Leng, (2014) Zhao, J. and Leng, C. (2014). Structured lasso for regression with matrix covariates. Statistica Sinica, 24:799–814.

- Zhou and Li, (2014) Zhou, H. and Li, L. (2014). Regularized matrix regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(2):463–483.

- Zhou, (2014) Zhou, S. (2014). Gemini: Graph estimation with matrix variate normal instances. Annals of Statistics, 42(2):532–562.

Appendix 1: Proofs

We start by defining some quantities used in the proofs. Write

The following lemma establishes the entry-wise convergence rate of the covariance matrix estimation of the vectorized latent factor process .

Lemma 1.

Let denote the -th entry of . Under Conditions 1 and 2, for any , and , it follows that

Proof.

Under Conditions 1 and 2, by Davydov’s inequality, it follows that

Here denotes a constant. ∎

Under the matrix-valued factor model (1), the can be view as the signal part and as noise. The following lemma concerns the rates of convergence for estimation of the signal, the noise, and the interaction between the two.

Lemma 2.

Under Conditions 1-4, it holds that

Proof.

Firstly, we have

Hence, by Condition 4 and Lemma 1, it follows that

Similarly, for the interaction component between signal and noise, we have

and

Lastly, for the noise term, we have

∎

With the four rates established in Lemma 2, we can now study the rate of convergence for the observed covariance matrix .

Lemma 3.

Under Conditions 1-4, it holds that

Proof.

From the definition of in (12), we can decompose into four parts as follows,

Then by Lemma 2, it follows that

∎

Lemma 4.

Under Conditions 1-4, and , it holds that

Proof.

We have

| (15) | |||||

Lemma 5.

Under Conditions 2 and 3, we have

where denotes the -th largest eigenvalue of .

Proof.

By definition, we have

Under Conditions 2-3 and by properties of Kronecker product we have

Since is a symmetric positive definite matrix, we can find a positive definite matrix , such that and . By the properties of Kronecker product, we can show that . Under Condition 2 using Theorem 9 in Merikoski and Kumar, (2004), it follows that .

Proof of Theorem 1

Proof.

By Lemmas 1-5, and Lemma 3 in Lam et al., (2011), Theorem 1 follows. ∎

Proof of Theorem 2

Proof.

The proof is quite similar to that of Theorem 1 of Lam and Yao, (2012). We denote and for the -th largest eigenvalue of and its corresponding eigenvector, respectively. The corresponding population eigenvalues are denoted by and for the matrix . Let and . We have

We can decompose by

where

For , , where by Theorem 1, and . By Lemma 4, we have and are of order and , and are of order . So .

For , define,

It can be shown that , similar to proof of Theorem 1 with Lemma 3 in Lam et al., (2011). Hence,

.

Since , for , consider the decomposition

where

By Lemma 2 and Lemma 4,

Hence .

If we use the transpose of to construct , we can obtain the asymptotic properties of the eigenvalues of estimated in a similar way. ∎

Proof of Theorem 3

Proof.

By Theorem 1, we have

The conclusion follows. ∎

Proof of Theorem 4

Proof.

We assume that is uniquely defined as , where are eigenvectors of corresponding to the largest eigenvalues , and . Then similar to proof of Theorem 3 in Liu and Chen, (2016), we can obtain the results. ∎

Appendix 2: Definitions of Financials Used

The following table shows the definition of the company financials used in the analysis. Some are directly reported by the company in their quarterly reports, and some are derived using the reported figures.

| Short Name | Variable Name | Calculation |

|---|---|---|

| Profit.M | Profit Margin | Net Income/Revenue |

| Oper.M | Operating Margin | Operating Income / Revenue |

| EPS | Diluted Earing per share | from report |

| Gross.Margin | Gross Margin | Gross Profit / Revenue |

| ROE | Return on equity | Net Income / Shareholders Equity |

| ROA | Return on assets | Net Income / Total Assets |

| Revenue.PS | Revenue Per Share | Revenue / Shares Outstanding |

| LiabilityE.R | Liability/Equity Ratio | Total Liabilities / Shareholders Equity |

| AssetE.R | Asset/Equity Ratio | Total Assets / Shareholders Equity |

| Earnings.R | Basic Earnings Power Ratio | EBIT / Total Assets |

| Payout.R | Payout Ratio | Dividend Per Share / EPS Basic |

| Cash.PS | Cash Per Share | Cash and other / Shares Outstanding |

| Revenue.G.Q | Revenue Growth over last Quarter | Revenue/ Revenue Last Quarter |

| Revenue.G.Y | Revenue Growth over same Quarter Last Year | Revenue/ Revenue Last Year |

| Profit.G.Q | Profit Growth over last Quarter | Profit / Profit Last Quarter |

| Profit.G.Y | Profit Growth over same Quarter last Year | profit / Profit Last Quarter |

In calculating profit growth ratio, an NA is recorded when profit changes from negative to positive or from positive to negative.