Structure of continuous-time ARMA process driven by semi-Levy measure

Abstract

A class of continuous-time autoregressive moving average (CARMA) process driven by simple semi-Levy measure is defined and its properties are studied.

We discuss some new insights on the structure of the semi-Levy measure which is described as periodically divisible measure.

This consideration enable us to provide statistical property of the introduced process.

We show that this process is well defined without having to assume further conditions on the measure.

We find a kernel representation of the process and present the properties of first and second moments of it.

Finally we show the efficiency of our model by implying simulated data.

AMS 2010 Subject Classification: 60E07, 60G18, 60G51.

Keywords: Continuous time ARMA; Periodic random measure; Semi-Levy process.

1 Introduction

Continuous-time models for time series exhibit both heavy-tailed and long-memory behavior. Such models are of considerable interest, specially for the modeling of financial time series. Early papers have studied the statistical analysis of continuous-time autoregressive (CAR) processes and continuous-time autoregressive moving average (CARMA) processes [8], [9], [10]. Continuous-time models have also been utilized and analyzed successfully for the modeling of irregularly spaced data.

For the first time, Brockwell [5] introduced the linear continuous-time model which is particularly advantageous for dealing with irregularly spaced data as continuous-time threshold ARMA process with . It provides the weak solution of a certain stochastic differential equation which is unique. Stramer et al. [24] investigated the existence and stability properties of these processes. Properties of linear CARMA processes driven by second order Levy processes are examined and extended to include heavier tailed series which frequently encountered in financial applications [6]. Discrete time representations for data generated by a CARMA system with mixed stock and flow data are derived by Chambers et al. [15].

Using the kernel representation of a Levy-driven CARMA process, the class of non-negative Levy-driven are extended by many authors for the non-monotone auto covariance functions. A class of fractionally integrated processes and also asymptotic properties of the CARMA processes are studied [7]. The second order Levy-driven CARMA models and some of their financial applications in particular to the modeling of stochastic volatility are discussed by Brockwell [8]. Compound Poisson process and Levy-driven stationary Ornstein Uhlenbeck (OU) process and some examples of theses models are studied in [2]. CARMA processes with a nonnegative kernel driven by a nondecreasing Levy process constituted a very general class of stationary nonnegative continuous time processes. The advantage of the nonnegativity of the increments of the driving Levy process is taken to develop a highly efficient estimation procedure for the parameters when observations are available at uniformly spaced times by Brockwell et al. [10]. They also generalized the ideas to higher order CARMA processes with nonnegative kernel. The key idea is the decomposition of the CARMA process into a sum of dependent OU processes [11].

Replacing the OU process by a Levy-driven CARMA process with non-negative kernel provides non-negative, heavy-tailed processes with a larger range of auto covariance functions [9]. It is shown that these processes are the convolution of a kernel function with a Levy-driving process. Gaussian CARMA processes are special cases in which the driving Levy process is Brownian motion. The use of more general Levy processes permits these processes with marginal distributions which may be asymmetric and heavier tailed than Gaussian. In many situations it is not appropriate to assume Gaussianity of the variables of interest, since the observed time series often exhibit features like skewness or heavy-tails which contradict the Gaussian assumption.

Jeanblanc et al. [16] give a representation of self-similar processes with independent increments as stochastic integrals with respect to background driving Levy processes.

Semi-Levy process which is a generalization of Levy process, is an additive process with periodically stationary increments. These processes have been extensively studied by Maejima and Sato [20]. Semi-Levy processes are also related to semi-selfsimilar additive processes which has independent increments and are continuous in probability with cadlag paths [19].

In this paper we introduce continuous-time ARMA process driven by second order simple semi-Levy measure which has periodically stationary increments. We show that this process is well defined without having to assume further conditions on the driving semi-Levy process. We present the expected value and covariance function of such processes and show that it is associated with a periodically divisible measure. We investigate a new integral representation of such process and discuss on basic properties of these models based on observations made at discrete times. This study has the potential to provide an approximation for every semi-Levy driven CARMA process.

This paper is organized as follows. In section 2 we present some concepts, theories and ideas regarding the semi-Levy processes, infinitely divisible, self-decomposable distribution and basic properties of them. Section 3 is devoted to the main results and introducing simple semi-Levy driven CARMA processes. For this we present the structure of the measure by a simple semi-Levy compound Poisson measure. We specialize this section to the characteristic function using the concept of periodically divisible measures. We also discuss on the solution of the stochastic differential equation driven by such semi-Levy measure in section 4. For such CARMA process we also study and obtain the first and second moments. The asymptotic behavior and stationarity of the solution are studied in this section. In section 5 we present some simulation of CARMA process driven by simple semi-Levy measure and give an example to illustrate the properties of this process.

2 Theoretical framework

In this section we study the preliminaries such as semi-Levy processes, Levy-Khintchine representation, Levy density and the concepts of infinitely divisible and self-decomposable distributions and their relations to characteristic functions which are used in this paper.

2.1 Semi-Levy processes

A general class of stochastic processes with stationary independent increments, called Levy processes are defined in [17], [1]. There are some classical applied probability models which are built on the strength of well-understood path properties of elementary Levy processes. We consider periodic independently scattered random measures, the counterparts of semi-Levy processes in stochastic processes. We provide some basic properties and examples of semi-Levy processes in this section.

A stochastic process is called an additive process if a.s., it is stochastically continuous, it has independent increments and its sample paths are right-continuous and have left-limits in . Further, if has stationary increments, it is a Levy process. In other words, a more specific definition of Levy process is as following [19].

Definition 2.1

A process defined on a probability space is said to be a Levy process if it possesses the following properties:

(i) The pathes of are -almost surely right continuous with left limits.

(ii) .

(iii) For , is equal in distribution to .

(iv) For , is independent of .

Unless otherwise stated, from now on, when talking of a Levy process, we shall always use the measure to be implicity understood as its law. It is provided a complete characterization of random variables with infinitely divisible distributions via their characteristic functions. This is the celebrated Levy-Khintchine formula [3], [4].

Theorem 2.1

The law of Levy process in terms of triplet , , is infinitely divisible if and only if there exists a triplet such that the characteristic function is given by with

where the Levy measure satisfies and the integrability condition .

As an extension of Levy process, we present the definition and some basic properties and results related of semi-Levy processes [20].

Definition 2.2

A subclass of additive processes with the property that for some and for any ,

where denotes the equality in all finite dimensional distributions is called a semi-Levy process with period .

Linear Brownian motion, compound Poisson and inverse Gaussian processes are familiar processes which are Levy as well.

Proposition 2.2

Let be an additive process and be the distribution of . If it is a semi-Levy process with period , then

for all and . If the above relation holds for all and , then is a semi-Levy process with period .

2.2 Infinity divisible and self-decomposable distributions

Let be the class of all infinitely divisible distributions on . A distribution is infinitely divisible if for each , there exists a distribution function such that is the -fold convolution of . The class of possible limit laws consists of the infinitely divisible distributions.

Remark 2.1

The random variables of a Levy process is infinitely divisible and if an infinitely divisible distribution, we can construct a Levy process from it.

An important class of random variable models for the unit time distribution as independent effects on the return may need to be scaled to be brought to comparable orders of magnitude before scaling by the square root of becomes relevant. Such considerations motivate arbitrary scaling factors and point to self-decomposable laws as candidate models.

Definition 2.3

A probability law of a random variable is said to self-decomposable just if for every constant there exists an independent random variable such that .

The class of self-decomposable distributions, denoted by has the longest history in the study of subclasses of . Let , be the characteristic function of . Then is said to be self-decomposable if for any , there exists a distribution such that

where and is also a limiting distribution of normalized partial sums of

independent random variables under infinitesimal condition, and has the stochastic integral representation with respect to a Levy

process.

Sato [22] showed that the Levy (jump) measure of a self-decomposable distribution is always absolutely continuous with respect to the Lebesgue measure and it’s density (Levy density) can be characterized by , with a so-called -function which increases on and decreases on . An infinitely divisible law is self-decomposable if the corresponding Levy density has the above form [12].

Remark 2.2

Self-decomposable laws are infinitely divisible and may be characterized nicely in terms of the Levy density.

Note that is a Levy process then is self-decomposable if and only if is self-decomposable for every . Levy’s continuity theorem enables us to show convergence of distribution through point-wise convergence of characteristic functions.

Theorem 2.3

(Levy’s continuity theorem) If for every , where and is continuous at , then converges in distribution to the random variables with characteristic function .

3 Semi-Levy driven CARMA process

If is a second-order subordinator i.e. nonnegative and nondecreasing Levy process, the semi-Levy driven CARMA process , with parameters is defined via the state space representation of the stochastic differential equation

| (3.1) |

where denotes differentiation with respect to , , and the coefficients satisfy and for . To avoid trivial complications, we shall assume that and have no common factors. Since does not exist in the usual sense, we interpret the differential equation by means of its state-space representation, consisting of the observation and state equations

| (3.2) |

and

| (3.3) |

where denotes an infinitesimal increment and

Every solution of equation satisfies the following relations for all ,

| (3.4) |

where the integral can be interpreted as the -limit of approximating Riemann-Stieltjes sums and also in the path wise sense since the paths of have bounded variation on compact intervals. From equation and the independence of the increments of one can easily verify that is Markov.

3.1 Structure of semi-Levy measure

The aim of this section is to present the structure of the simple semi-Levy measure. For this we characterize the measure in Levy-Khintchine representation to an infinitely divisible distribution. This will be done by Levy-Ito decomposition which describes the structure of a general Levy process in terms of three independent auxiliary Levy processes, each with different types of path behavior. In general case, any Levy process may be decomposed into the three independent Levy processes as Brownian motion with drift, compound Poisson process and a square integrable (pure jump) martingale with an a.s. countable number of jumps of magnitude less than 1 on each finite time interval [22], [17].

Definition 3.1

We call , a simple semi-Levy Poisson measure if there exists a partition of the positive real line as , and , where for some fixed , , and is a Poisson random measure with intensity parameter on for , where .

Such simple semi-Levy measure has the potential to approximate any semi-Levy measure. To justify that presented by the above definition is a semi-Levy measure with period , let , , , and then

So for all , have the same distribution that is the random measure has periodically stationary increments with period . Thus for , , is a semi-Levy Poisson process with parameter

| (3.5) |

where , and for .

Let be a subordinator with the following representation

| (3.6) |

where , is a simple semi-Levy Poisson process with parameter , defined by (3.5) and is an independent identically distributed sequence of random variables with probability distribution .

3.2 Representation of periodically divisible random measure

There is a strong interplay between Levy processes and infinitely divisible distributions and also between semi-Levy processes and periodically divisible (PD) of corresponding random measures. Following the definition of semi-Levy process presented by Sato [20], we introduce concept of PD random measure which provides a good platform for obtaining the results of this paper.

Definition 3.2

Random measure is called periodically divisible with period if for any fixed , random variables are independent identically distributed for all indices . So the corresponding distribution of is the same as times convolution of distribution of . Therefore

According to Proposition 2.2, we can characterize a PD random measure using its characteristic function.

Definition 3.3

A process is PD with period , if for any and we have , where , are independent identically distributed random variables which are independent of . So the corresponding characteristic functions satisfy

where .

It follows that a semi-Levy process is PD with the same period.

Lemma 3.1

Let be a semi-Levy Poisson process with parameter , defined by (3.5) and be a summation of independent identically distributed random variables which considered as independent copy of with characteristic function . The jumps are independent of . Then is called as semi-Levy compound Poisson process with characteristic function.

| (3.7) |

Sketch of proof: is a nonhomogeneous process with parameter , so is stochastically continuous in probability

as .

Thus for any , and where and we have that

Example 3.1

The semi-Levy compound Poisson process is an example of PD random measure. Let where represents the number of jumps and is a semi-Levy Poisson process with parameter . Also has the characteristic function in the form (3.7) with the assumptions of Lemma 3.1. Then we have

where and where .

Since the characteristic function of a random variable determines its distribution, we have a characterization of the distribution of the semi-Levy process by the followings.

Corollary 3.1

Lemma 3.2

If is a sequence of PD random measures with some period and , then is also PD random measure with period .

Proof: The random measure property of follows by a completely similar method to the one of [22] where such property is proved for infinite divisible distribution and so is valid for corresponding random measures. The periodicity of follows from the fact that all elements of the sequence of measures are PD with period and there is a convergence in distributions to and the period is constant. So the limit of the sequence is also PD with the same period .

Theorem 3.3

Proof: Let , be a sequence of real number, monotonic and decreasing to zero and the sequence has the following characteristic function

for all and , where is the same. The measure restricted to is finite and hence is the characteristic function of a semi-Levy random measure. We clearly have that

where is the characteristic function of defined by (3.8).

By Levy’s continuity theorem (Theorem 2.3) and Lemma 3.2, is the characteristic function of a PD measure provided that is continuous at 0.

Continuity of at 0 boils down to the continuity of the integral term. Using the properties of semi-Levy measure and monotone convergence theorem we have

4 Characterization of the solution

Our approach leads to a model which can be interpreted as a solution to the formal differential equation (3.1).

Analyzing the representation of its solution shows that it can be used to define semi-Levy driven CARMA processes.

We take a closer look at the probabilistic properties of the solution, represented in (3.4) such as second moments, Markov

property, non-stationary and limiting distributions and path behavior.

In particular, we characterize the non-stationary distribution and path behavior and give conditions for the existence of it.

In order to study the properties of in (3.4), we need to have the auxiliary results under following conditions.

Condition 1.

The is independent of for all .

Condition 2.

The eigenvalues of the matrix A are considered to have negative real parts. We remind that

the eigenvalues of a matrix A have negative real parts if and only if

| (4.9) |

If the above conditions are satisfied the solution (3.4), converges to

| (4.10) |

with the specified properties when and is the semi-Levy process.

We have restrict attention to second-order subordinator and for such process represented in (3.6) and Wald’s equation, we have

| (4.11) |

where and

| (4.12) |

where and . Since we have

In the following we find mean and second moment of , represented in (4.10), for . This is by the fact as we have a partition on positive real line, , , described more in Definition 3.1.

Let

and be a point inside some interval, say . For the simplicity we can re-consider this point as the last point of the last period interval. By this we have subinterval in each period interval. So this new notation implies that

So the expected value of for large is

For outside the range we assume that is equal to . By the fact that is semi-Levy process with periodically stationary increments and using (4.11) and (3.5) we have

where and we have . For any ,

Therefore

where is the identity matrix. So we arrive at the following lemma.

Lemma 4.1

The expected value of defined by (4.10) is periodic with period , that is . So for , the solution of the ordinary differential equation is also periodic.

Now we find the covariance function of as for and and . Let , so

Using the partition and by the fact that the increments of semi-Levy process are periodically stationary and independent, for and we have

and using the variance of as and for any ,

This is by the fact that independent increments of implies that . Therefore

So we arrive at the following lemma.

Lemma 4.2

The covariance function of defined by (4.10) is periodic with period . In the other hand

So for , and Lemma 4.1, the solution of the ordinary differential equation is weakly periodically stationary.

Remark 4.1

The eigenvalues of a matrix A, denoted by are the same as the zeroes of the autoregressive polynomial .

Proposition 4.3

If is a second-order subordinator and the eigenvalues of a matrix A have negative real parts, then the semi-Levy driven CARMA process with parameters by equations (3.2) and (4.10) is defined as

| (4.13) |

where the function is called the kernel of the CARMA process . When the Condition 1 is satisfied, then is a causal function of .

Remark 4.2

The representation (4.13) shows that if the kernel is nonnegative then, the semi-Levy driven CARMA process is nonnegative and can be used to represent nonnegative quantity process such as stochastic volatility.

5 Simulation

In this section, we verify the theoretical results concerning periodically stationary structure of the output of the CARMA model (3.2) and (3.3) by simulation.

For this, we consider a discretization of the process by imposing a partition for the whole duration of it with equally spaced points of length one. Then we generate the discretized version of the CARMA process by the following procedure which provides a discrete time periodically stationary process.

In the followings we briefly describes the simulation steps.

We present a simulation method for some discretized version of CARMA processes driven by some simple semi-Levy measure. Following Definition 3.1 we simulate some simple semi-Levy Poisson measure. Let be the period of the increments of the measure and consider period intervals as . We assume that the number of partitions in each period is fixed, say , and the subintervals form a partition of first period interval. The following period intervals are partitioned by the same number and same lengths of subintervals. Successive elements of the partitions of successive scale intervals are denoted by where their lengths admit equalities . The simple semi-Levy process , defined by (3.6), on partition has Poisson distribution with intensity parameter where for . Therefore, the simulation algorithm of is determined as follows.

-

1.

Consider some positive value as the length of the period of simple semi-Levy process , defined by (3.6), and some integer as the number of corresponding period intervals for simulation.

-

2.

Decide about the number of elements of partition in each period, say .

-

3.

Consider different positive real numbers so that and a partition of first period interval by where , and for . Elements of partitions of successive period intervals for are where .

-

4.

Let the positive real numbers be chosen as Poisson rates of occurrences, corresponding to the increments of , in (3.6), on . Also increments of on has Poisson rate of occurrence .

-

5.

Generate an independent sequence of Poisson random variables with parameter on for as .

-

6.

Create independent samples from Uniform distribution . Then sort these samples on each and denote these ordered samples by for . Finally evaluate for 111 This is by the fact that sample points of occurrence of Poisson random variables on an interval follows the order statistics of Uniform distribution.

-

7.

Let be a real number and generate independent identically distributed random variables from some probability distribution , say standard Normal distribution. Then determine by relation (3.6).

After evaluating , we produce the CARMA process in (3.2) and (3.3) by the following steps.

-

1.

Conside as some specified integer value.

-

2.

Following condition 2 and Remark 4.1 consider roots for the autoregressive polynomial with negative real parts and calculate the coefficients of as .

-

3.

Create the matrix .

-

4.

Consider some real values for the parameters , so that and have no common factors.

-

5.

Provide a discretization of in (3.3) by imposing an equally spaced partition for with some small space . Also consider initial values of such discretized vector .

-

6.

Finally, using the discretized value of provided by previous step and the values considered for parameters and relation (3.2), evaluate the corresponding discretized values of .

We simulate the process using the proposed algorithm. Hurd and Gerr [13] presented the graphical methods to verify that the simulated series are indeed PC.

Soltani and Azimmohseni [23] and Hurd and Miamee [14](Chapter 10) used the same diagnostic method to check whether the simulated data are PC with period .

In this method, for a sample of size , and a fixed , they

plotted the significant values of the sample spectral coherence

against . It has the non-zero values for , , where

Therefore, we can say something about the nature of the analyzed time series:

-

•

If in the square only the main diagonal appears, so is a stationary time series.

-

•

If there are some significant values of statistic and they seem to lie along the parallel equally spaced diagonal lines, then is likely PC-T, where is the “fundamental” line spacing. Algebraically, would be the gcd of the line spacings from the diagonal; for a sequence to be PC-T, not all lines are required to be present.

-

•

If there are some significant values of statistic but they occur in some non-regular places, then is a nonstationary time series in other than periodic sense; but note there are many hypotheses being tested, so some threshold exceedances are to be expected.

In the following, we provide one example to investigate our process.

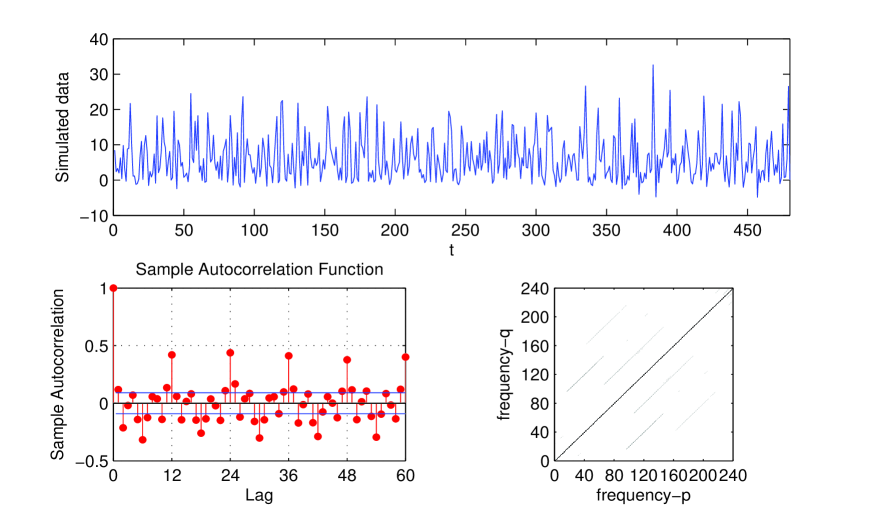

Example: We provide a simulated discretized semi-Levy driven CARMA process. For this we consider the parameters of the simple semi-Levy process as , and the length of successive subintervals of each period intervals as where corresponding rate of Poisson occurrence on these subintervals are assumed as . Also the random variables is considered to have Normal distribution with mean 3 and variance 1.

In this example we simulate a CARMA(3,2) model by assuming the roots of as , and . So the value of parameters , and are determined as and respectively. Thus, the matrix A is

By the CARMA(3.2) model in the form (3.3), we generate the values of discretized by considering some equally space partition for the duration of period intervals. Finally, we consider the values of parameters as , and and produce the CARMA process. Then we follow to verify the output of the model which provides a periodically stationary process.

In Figure 1, we see the simulated data of size with the suggested simulation algorithm (top).

The sample autocorrelation plot of this process (bottom left) and

the sample coherent statistic of data (bottom right).

The parallel lines for the sample spectral coherence confirm that

the simulated data are PC. Also, In this plot, the first significant off-diagonal is at which verifies the first significant peak at 40 and hhis shows that there is a second-order PC structure with period in the data.

References

- [1] D. Applebaum (2004) Levy Processes and Stochastic Calculus. Cambridge: Cambridge University Press.

- [2] O.E. Barndorff-Nielsen, N. Shephard (2001) Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics. J. R. Statist. Soc. B 63, 167-241.

- [3] J. Bertoin (1996) Levy Processes. Cambridge: Cambridge University Press.

- [4] J. Bertoin, F. Martinelli, Y. Peres (1999) Lectures on Probability Theory and Statistics: Ecole d’Ete de Probabilities de Saint-Flour XXVII.

- [5] P.J. Brockwell (1994) On continuous time threshold ARMA processes. J. Statist. Plann. Inference 39, 291-303.

- [6] P.J. Brockwell (2000) Heavy tailed and non-linear continuous-time ARMA models for financial time series. In Statistics and Finance: An Interface, eds W.S. Chan, W.K. Li and H. Tong, Imperial College Press, London, 3-22.

- [7] P.J. Brockwell (2004) Representations of Continuous-Time ARMA Processes. Journal of Applied Probability, Vol. 41, Stochastic Methods and Their Applications 375-382.

- [8] P.J. Brockwell (2009) Levy-driven Continuous time ARMA processes. Handbook of Financial Time Series, 457-480.

- [9] P.J. Brockwell, T. Marquardt (2005) Levy-driven and fractionally integrated ARMA processes with continuous time parameter. Statist. Sinica 15, 477-494.

- [10] P.J. Brockwell, R.A. Davis, Y. Yang (2007) Estimation for nonnegative Levy-driven Ornstein-Uhlenbeck Processes. J. Appl. Probab. Volume 44, Number 4, 977-989.

- [11] P.J. Brockwell, R.A. Davis, Y. Yang (2011) Estimation for nonnegative Levy-driven CARMA processes. J. Bus. Econ. Stat. 29 250-259.

- [12] P. Carr, H. Geman, D.B. Madan, M. Yor (2007) Self-Decomposability and option pricing. Mathematical Finance, Vol. 17, No. 1, pp. 31-57.

- [13] H.L. Hurd, N.L. Gerr (1990) Graphical methods for determining the presence of periodic correlation. Journal of Time Series Analysis 12(4): 337-350.

- [14] H.L. Hurd, A.G, Miamee (2007) Periodically Correlated Random Sequence, Spectral Theory and Practice. New York: Wiley.

- [15] M.J. Chambers, M.A. Thorntona (2011) Discrete time representation of continuous time ARMA processes. Econometric Theory, Vol 28, Issue 01, 219-238.

- [16] M. Jeanblanc, J. Pitman, M. Yor (2002) Self-similar processes with independent increments associated with Levy and Bessel processes. Stochastic Process. Appl. 100, 223-231.

- [17] A.E. Kyprianou (2006) Levy processes and infinite divisibility.

- [18] A. Makagon, A.G. Miamee, H. Salehi (1994) Continuous time periodically correlated processes: spectrum and prediction. Stoch. Proc. Appl., 49, 277-295.

- [19] M. Maejima, K. Sato (1999) Semi-selfsimilar processes. Journal of Theoritical Probability. Vol 12, No 2, 347-373.

- [20] M. Maejima, K. Sato (2003) Semi-Levy processes, semi-selfsimilar additive processes, and semi-stationary Ornstein-Uhlenbeck type processes. J. Math. Kyoto Univ. 43, 609-639.

- [21] Yu. A. Rozanov (1967) Stationary Random Processes San Francisco: Holden Day

- [22] K. Sato (1999) Levy processes and infinitely divisible distributions. Cambridge: Cambridge University Press.

- [23] AR. Soltani,M. Azimmohseni (2007) Simulation of real-valued discrete-time periodically correlated Gaussian processes with prescribed spectral density matrices. Journal of Time Series Analysis. 28(2): 225–240.

- [24] O. Stramer, R. L. Tweedie, P. J. Brockwell (1996) Existence and stability of continuous time threshold ARMA processes. Statistica Sinica 6, 715-732.