Inventory growth cycles with debt-financed investment

Abstract

We propose a continuous-time stock-flow consistent model for inventory dynamics in an economy with firms, banks, and households. On the supply side, firms decide on production based on adaptive expectations for sales demand and a desired level of inventories. On the demand side, investment is determined as a function of utilization and profitability and can be financed by debt, whereas consumption is independently determined as a function of income and wealth. Prices adjust sluggishly to both changes in labour costs and inventory. Disequilibrium between expected sales and demand is absorbed by unplanned changes in inventory. This results in a five-dimensional dynamical system for wage share, employment rate, private debt ratio, expected sales, and capacity utilization. We analyze two limiting cases: the long-run dynamics provides a version of the Keen model with effective demand and varying inventories, whereas the short-run dynamics gives rise to behaviour that we interpret as Kitchin cycles.

keywords:

macroeconomic dynamics , business cycles , inventories , disequilibrium analysisJEL:

C61, E12, E20, E321 Introduction

Inventory fluctuations have been known for a long time to be a major component of the business cycle [1]. According to [2], even though investment in inventory accounts for a very small fraction of output (about 1 percent in the U.S.), changes in inventory investment account for a disproportionately large fraction of changes in output over the cycle (about 60 percent on average for seven postwar recessions in the U.S.). Nevertheless, inventory dynamics has received relatively little attention in the theoretical literature. A review of earlier models is provided in [3], where it is observed that, whereas “the prevailing micro theory viewed inventories as a stabilizing factor”, the data shows that output is more volatile than final sales (namely output less inventory investment), suggesting a destabilizing role for inventories in macroeconomics. The landscape has not changed significantly since then, with a few recent papers focussed on incorporating inventories in fully micro founded general equilibrium models [17, 18]. As remarked in these papers, explaining inventories in a frictionless general equilibrium model is as challenging as explaining money, forcing this type of analysis to rely on frictions, such as delivery costs and stockout-avoidance motives, akin to the attempts to incorporate a financial sector into DSGE models. In this paper, we follow an alternative approach based on disequilibrium models where sluggish adjustment, adaptive expectations, and sectoral averages replace market clearing, rational expectations, and representative agents [7].

Our starting point is the growth cycles model proposed in [6] along the lines originally formulated in [13]: investment in inventory adjusts to a desired inventory-to-expected-sales ratio, whereas expected sales themselves adapt taking into account fluctuating demand. As shown in [6], the interplay between the long-run growth trend and short-run adjustment of inventory stock and expected sales determine the stability of the model. Whereas sufficiently sluggish adjustments promote stability, the model exhibits dynamic instability if the adjustment speeds exceed certain thresholds. Moreover, a flexible inventory adjustment speed can lead to persistent cyclical behaviour. The model in [6] is described by means of a two-dimensional dynamical system with normalized expected sales and inventory levels (or equivalently, capacity utilization) as state variables and therefore necessarily neglects several other macroeconomic dynamic feedback channels. In particular, the model takes the wage share of the economy as constant, so that endogenous cycles arising from distributional conflict à la Goodwin [8] are not considered. Moreover, in the absence of an explicit financial sector, there is no role in the model for the kind of Minskyan instability [14] arising from debt-financed investment.

In this paper, we present in Section 2 a unified model with both inventory and labour market dynamics, as well as allowing for financial considerations to play a role in investment decision through profits net of debt servicing. The resulting dynamics leads to the five-dimensional system derived in Section 3, with the traditional wage share and employment rate variables of the Goodwin model [8] augmented by the debt ratio of firms as in the Keen model [11], in addition to the expected sales and capacity utilization variables of the Franke model [6] mentioned above. Global analysis of such high-dimensional nonlinear system is beyond the scope of current techniques, and even local analysis of the interior equilibrium proves to be laborious and not very illuminating. In the remainder of the paper we opt instead to investigate two well defined limiting cases.

In Section 4 we consider the type of long-run dynamics that arises when firms have no planned investment in inventory and make no adjustments for short term fluctuations in inventory and expected sales. The resulting model is thus four-dimensional, as the ratio of expected sales to output is now constant. Further simplification is achieved by specifying the long-run growth rate of expected sales. When this is chosen to be a constant as in [6], we find that the labour market part of the model only achieves equilibrium for a particular initial condition for employment. Alternatively, choosing the long-run growth rate of expected sales to be the same as the instantaneous growth rate of capital leads to a three-dimensional model for wage share, employment rate, and debt ratio, with a constant capital utilization. The non-monetary version of this model is very similar to the original Keen model, but now with a non-trivial effective demand and fluctuating inventories. As in the Keen model, an equilibrium with infinite debt ratio is also possible but highly problematic in this model, because it leads to infinitely negative inventory levels. When the model is cast in nominal terms, we find that the equilibrium with explosive debt is no longer possible, essentially because the positive wealth effect in the consumption function raises demand and consequently the inflation rate. On the other hand, in addition to a deflationary state first observed in [10], a new type of debt crisis corresponding to vanishing wage share and employment rate but with a finite debt ratio arises as a possible stable equilibrium.

In Section 5 we turn our attention to the opposite limiting case, namely a no-growth regime where the only drivers of expected sales and inventory investment are short-run fluctuations in demand. Further ignoring the wealth effect in the consumption function allows us to focus exclusively on a reduced two-dimensional describing the relationship between demand and expected sales. This fascinating system undergoes a bifurcation from a locally stable equilibrium in which demand equals expected sales to an unstable limit cycle. We find that the higher the adjustment speeds of inventory and expected sales, the harder it is to achieve stability. On the other hand, stability is enhanced when prices react faster to mismatch between demand and expected sales. The interplay between supply, demand, and prices is even more involved when we consider an alternative model in which prices adjust indirectly through the mismatch between actual and desired inventory levels, rather then directly through changes in inventory. In this case, the increased information lags give rise to stable limit cycles that strongly resemble the Kitchin cycles first reported in [12].

2 The General Model

2.1 Accounting structure

We consider a three-sector closed economy consisting of firms, banks, and households. The firm sector produces one homogeneous good used both for consumption and investment.

Capital and utilization

Denote the total stock of capital in the economy in real terms by and assume that it determines potential output according to the relationship

| (1) |

where is a constant capital-to-output ratio. The actual output produced by firms is assumed to consist of expected sales plus planned inventory changes , that is,

| (2) |

and in turn determines capacity utilization as

| (3) |

Finally, capital is assumed to change according to

| (4) |

where denotes capital investment in real terms and is a depreciation rate expressed as a function of capital utilization .

Effective demand and inventories

Denote total real consumption by banks and households by , which together with capital investment determine total sales demand

| (5) |

also in real terms. The difference between output and demand determines actual changes in the level of inventory held by firms. In other words,

| (6) |

where denotes the stock of inventories and denotes investment in inventory, which consists of both planned and unplanned changes in inventory, denoted by and respectively. Substituting (2) into (6), we see that unplanned changes in inventory are given by

| (7) |

and therefore accommodate any surprises in actual sales compared to expected sales. Finally, total real investment in the economy is given by , that is, it consists of changes in inventory, both planned and unplanned, plus capital investment.

Labor cost and employment

Let the nominal wage bill be denoted by , the total workforce by and the number of employed workers by . We then define the productivity per worker , the employment rate and the nominal wage rate as

| (8) |

whereas the unit cost of production, defined as the wage bill divided by quantity produced, is given by

| (9) |

We will assume throughout that productivity and workforce grow exogenously according to the dynamics

| (10) |

Nominal quantities

Denoting the unit price level for the homogenous good by , it is clear that the portion of the nominal output consisting of sales should be given by . Accounting for inventory changes is less straightforward, as there can be many alternative definitions of the cost of inventory. We follow [7] and value inventory changes at cost , as this is what is incurred by the acquisitions department of a firm (represented by the term under the capital account in Table 1) in order to purchase unsold goods from the production department (represented by a revenue in the current account).

We therefore find that nominal output is given by 111This corresponds to equations (8.24) and (8.25) in [7].

| (11) |

In other words, nominal output consists of nominal sales plus change in value of inventory minus an inventory value adjustment term . It is important to emphasize that even though total output in real terms satisfies according to (6), nominal output is given by . In other words, the relationship is true if and only if either or .

Financial Balances

Further denoting household deposits by and loans to firms by , we arrive at the balance sheet, transactions, and flow of funds described in Table 1 for this economy. Notice that we are assuming, for simplicity, that households do not borrow from banks and firms do not keep positive deposits, preferring to use any balances to repay their loans instead.

| Households | Firms | Banks | Sum | ||

| Balance Sheet | |||||

| Capital stock | |||||

| Inventory | |||||

| Deposits | 0 | ||||

| Loans | 0 | ||||

| Sum (net worth) | |||||

| Transactions | current | capital | |||

| Consumption | 0 | ||||

| Capital Investment | 0 | ||||

| Change in Inventory | 0 | ||||

| Accounting memo [GDP] | [] | ||||

| Wages | 0 | ||||

| Depreciation | 0 | ||||

| Interest on deposits | 0 | ||||

| Interest on loans | 0 | ||||

| Profits | 0 | ||||

| Financial Balances | 0 | 0 | |||

| Flow of Funds | |||||

| Change in Capital Stock | |||||

| Change in Inventory | |||||

| Change in Deposits | 0 | ||||

| Change in Loans | 0 | ||||

| Column sum | |||||

| Change in net worth | |||||

It follows from Table 1 that the net profit for firms, after paying wages, interest on debt, and accounting for depreciation (i.e consumption of fixed capital) is given by

Observe that, even though changes in inventory add to profits, sales constitute the only way for firms to have positive gross profits (i.e before interest and depreciation) since

It is also assumed in Table 1 that all profits are reinvested, that is, . The financial balances row on Table 1 corresponds to the following ex post accounting identity between total nominal savings and investment in the economy:

| (12) |

In particular for the firm sector we have

| (13) |

where denotes the pre-depreciation profit.

Intensive variables

To obtain a steady state in a growing economy, we normalize real variables by dividing them by total output , namely

| (14) |

and nominal variables by dividing them by (even though this is not equal to nominal output according to the remark following (11)), that is

| (15) |

We use and as proxies for the actual wage share and debt ratio , which case can readily be obtained by dividing the expressions above by

| (16) |

2.2 Behavioural Rules

We now specify the behavioural rules for firms, banks, and households. Namely, for given values of the state variables, firms decide the level of capital investment , planned changes in inventory , and expected sales , whereas banks and households decide the level of consumption and . This in turn determines capital by (4), output by (2), utilization by (3), sales demand by (5), and unplanned changes in inventory by (7). Consequently, since productivity and workforce growth are exogenous, the level of output in turn gives the number of employed workers and the employment rate by (8). Further specification of the dynamics for the nominal wage rate and prices then completes a model.

Firms

We start by assuming that firms forecast the long-run growth rate of the economy to be a function of utilization and (pre-depreciation) expected profitability defined as

| (17) |

where denotes the expected nominal output. Inserting (14) and (15) and into (17), we find that the expected profitability can be expressed as

| (18) |

In addition to taking into account the long-run growth rate , firms adjust their short-term expectations based to the observed level of demand. This leads to the following dynamics for expected demand:

| (19) |

for a constant , representing the speed of short-term adjustments to observed demand. We assume further that firms aim to maintain inventories at a desired level

| (20) |

for a fixed proportion . While this means that the long-term growth rate of desired inventory level should also be , we assume again that firms adjust their short-term expectations based on the observed level of inventory. This leads to the following expression for planned changes in inventory:

| (21) |

for a constant , representing the speed of short-term adjustments to observed inventory.

To complete the specification of firm behavior, we assume that investment is given by

| (22) |

for a function capturing explicitly the effects of both capacity utilization and expected profits. Based on (4), this leads to the following dynamics for capital,

| (23) |

Banks and Households

We assume that total consumption is given by

| (24) |

for a function of the wage and debt ratios and . This includes, for example, the usual case where nominal consumption of households and banks is assumed to be given by constant fractions of income and wealth, namely,

| (25) | ||||

| (26) |

Under the additional simplifying assumption that and , we have

| (27) |

with and . Alternatively, we can follow [16] and assume that and , that is, banks have zero net worth and charge zero intermediation costs (and therefore have no consumption), in which case (27) holds with and . In either case, we see that (27) is an example of (24) with

| (28) |

for non-negative constants and . We then find that nominal demand is given by

| (29) |

from which we obtain the auxiliary variable

| (30) |

Price and wage dynamics

For the price dynamics we assume that the long-run equilibrium price is given by a constant markup times unit labor cost , whereas observe prices converge to this through a lagged adjustment with speed . A second component with adjustment speed is added to that dynamics to take into account short-term considerations regarding unplanned changes in inventory volumes:

| (31) |

We assume that the wage rate follows

| (32) |

for a constant . The assumption states that workers bargain for wages based on the current state of the labour market, but also take into account the observed inflation rates. The constant represents the degree of money illusion, with corresponding to the case where workers fully incorporate inflation in their bargaining.

3 The main dynamical system

Combining (20) and (21), we see that output is given by

| (33) |

so that the inventory-to-output ratio is given by

| (34) |

Differentiating (33) and using (19) and (6), we obtain the following dynamics for output

| (35) |

The dynamics for the wage share follows from (32) and (31):

| (36) |

where the inflation rate is defined in (31). For the employment rate , we use (35) and (10) to obtain

| (37) |

For the debt ratio , using the expression for debt change in (13), we find that

| (38) |

Similarly, for the expected sales ratio , we use (19) to obtain

| (39) |

Finally, for the capacity utilization , using (23) we find

| (40) |

Since is expressed in (30) as a function of and and is given in (18) as a function of , we see that the model can be completely characterized by the state variables satisfying the following system of ordinary differential equations:

| (41) |

To obtain an interior equilibrium point , observe that the second equation in (41) requires that

| (42) |

which when inserted in the forth equation leads to and

| (43) |

at equilibrium. Using this and (42) in (35) therefore gives

| (44) |

Inserting (44) into (34) implies that , so that the equilibrium level of inventory is the desired level . Substituting into (31) leads to an equilibrium inflation of the form

| (45) |

that is, without any inventory effects. Using the third equation in (41) we see that the debt ratio at equilibrium satisfies

| (46) |

Moving to the last equation in (41), we obtain that the investment function at equilibrium satisfies

| (47) |

which can be inserted in (30) to yield the equilibrium capacity utilization as the solution to

| (48) |

We can then obtain the values of by solving (46)-(47) with defined from (18). Finally, returning to the first equation in (41) we find the equilibrium employment rate by solving

| (49) |

We therefore see that existence and uniqueness of the interior equilibrium depends on properties of the functions and , which need to be asserted in specific realizations of the model.

To summarize, an interior equilibrium of (41) is characterized by a constant growth rate of output equal to , constant capacity utilization, expected sales equal to demand, and the level of inventory equal to a constant proportion of expected sale. The present model is nevertheless highly complex. It needs the specification of at least fourteen parameters in addition to three behavioural functions. The exploration of other possible equilibrium points is considerably involved, and any local stability analysis will reveal to be a cumbersome and non-intuitive exercise.

In order to build intuition about the system, we follow the strategy of considering the lower-dimensional subsystems that arise in some limiting cases for the model parameters and behavioural functions. We start with a few special cases corresponding to known models in the literature.

3.1 The Goodwin model

The simplest special case of (41) consists of the model proposed in [8]. The original Goodwin model is formulated in real terms, which we can easily reproduce by setting , meaning that the rate of inflation is zero, and setting . It also makes no reference to inventories, thereby implicitly assuming that output equals demand. We can recover this from the general model of the previous section by assuming that , meaning that there is no desired inventory level () or planned investment in inventory (), and that , meaning that firms have perfect forecast of demand and set at all times. In addition, Goodwin adopts a constant capital-to-output ratio, which we can recover by setting . Finally, although not explicitly mentioned in [8], we adopt a constant depreciation rate for the Goodwin model.

The only explicit assumption of the Goodwin model regarding the behaviour of firms is that investment is equal to profits, which in the present setting corresponds to

since in (18). The model is also silent about banks, but it follows from (13) and the investment rule above (recalling that ) that at all times, so we assume for simplicity that . Alternatively we could adopt an arbitrary constant level of debt , observing that, in a growing economy, .

Regarding households, the assumption in [8] is that all wages are consumed, namely in the notation of (25). For consistency, we set , even though this is not relevant when .

3.2 The Franke model

As mentioned in Section 1, our proposed dynamics for inventories follows closely the Metzlerian model formalized in [6]. The Franke model is also formulated in real terms, so we maintain the choice of and from the previous section, and normalizes all variables by dividing them by instead of , resulting in the intensive variables

Crucially, the model in [6] implicitly assumes a constant wage share (see, for example, footnote 9 on page 246), so that the first equation in (41) is simply . The second equation in (41) then decouples from the rest of the system and simply provides the employment rate along the solution path, in particular leading to a constant employment rate at equilibrium. As with the Goodwin model, the Franke model is also silent about banks, implicitly assuming that firms can raise the necessary funds for investment through retained profits and savings from households, which we reproduce here by setting in (41).

The behaviour of firms, on the other hand, is almost identical to the one adopted here, with our equations (19), (20), and (21) corresponding directly to equations (7), (2), and (3) in [6], respectively, provided we take

| (53) |

as the long-run growth rate of expected sales. For the investment function, we recover the assumption in [6] by setting

| (54) |

for an increasing function . Regarding effective demand, instead of modelling consumption and investment separately, the assumption in [6] is that demand in excess of output is given directly in terms of utilization, which we can reproduce in our model by setting

| (55) |

for a decreasing function . With these choices, it is a simple exercise to verify that the fourth and fifth equations in (41) are equivalent to equations (9)-(10) for and in [6], with equilibrium values given by

| (56) |

It is shown in [6] that this equilibrium is locally asymptotically stable provided the speed of adjustment of inventories is sufficiently small. For above a certain threshold, however, local stability can only be asserted when the speed of adjustment of expected sales is sufficiently small. The main innovation in [6] consists of adopting a variable speed of adjustment and investigate its effects on the stability of the equilibrium. It is then shown that even in the unstable case, namely when both and are large enough so that the equilibrium is locally repelling, global stability can be achieved provided decreases fast enough away from the equilibrium. As stated in [6], the equilibrium is “locally repelling, but it is attractive in the outer regions of the state space”, giving rise to periodic orbits.

3.3 The original Keen model

The model proposed in [11] is based on the same assumptions of the Goodwin model regarding the price-wage dynamics ( and ), desired inventory level (), expected sales ( and ), constant capital-to-output ratio with full utilization (), and constant depreciation rate (). The innovation in the model is that investment is now given by

| (57) |

where we used the fact that in (18). Moreover, the identity implies that

| (58) |

that is, in (24). In other words, in the absence of either price or quantity adjustments, total consumption plays the role of an accommodating variable in the model.

Since (19) is degenerate in the limit case , we again use instead of (33) to obtain the growth rate of the economy as

| (59) |

With these parameter choices, the system (41) reduces to

| (60) |

where . It is then easy to see that (46), (47) and (49) reduce to

| (61) |

from where we obtain the interior equilibrium point found in [9], which is shown to be locally stable provided the investment function is sufficiently increasing at equilibrium, but does not exceed the amount of net profits by too much.

3.4 Monetary Keen model

As shown in [10], it is relatively straightforward to incorporate the price-wage dynamics in (31)-(32) in the original Keen model. Adopting all the parameter choices and functional forms of the previous section (including ) with the exception of arbitrary constants and , we find that (41) reduces to the three-dimensional system

| (63) |

where and . Solving (46), (47) and (49) for this system gives an interior equilibrium analogous to that of the original Keen model. Apart from it, [10] showed that the system (63) also admits the equilibrium , as well as a new class equilibria of the form or where

| (64) |

is a wage share satisfying (deflation) and is a finite debt ratio obtained as the solution of a non-linear equation. The stability of all three types of equilibrium is analyzed in detail in [10], with the overall conclusion that “money emphasizes the stable nature of asymptotic states of the economy, both desirable and undesirable.”

4 Long-run dynamics

As mentioned in Section 2.2, the core dynamics for expected sales and inventories in the model consists of the interplay between long-run expectations and short-run fluctuations characterized by equations (19)-(21). It is therefore instructive to investigate the properties of the sub-models that arise when each of these effects is considered separately. We start with case where short-run fluctuations are ignored by firms, namely when . In addition, we assume that there are no planned changes in inventories, namely that , so that and any discrepancy between supply and demand is absorbed by unplanned inventory changes .

Observe that, in this case, the growth rate of the economy is given by

| (65) |

as there is no feedback channel from the demand on either expected sales or planned inventories , and consequently no impact of demand on output , which is therefore solely determined by the expected long-run growth rate of the economy. Consequently, the fourth equation in (41) is identically zero, which is consistent with the fact that , and the system reduces to

| (66) |

where and . Notice also that the inventory-to-output ratio can no longer be determined by (34) (since ), but should instead be found from the auxiliary equation

| (67) |

The interior equilibrium for (66) is obtained from (46)-(49) with . In particular, since , this equilibrium implies that according to (67), which is consistent with (44) and with . This is the analogue of the good equilibrium for the original Keen model, corresponding to a finite debt ratio and non-zero wage share and employment rate.

Observe that in the special case , that is, a constant long-run growth rate for expected sales corresponding to the model proposed in [6], we find that the employment rate in (66) is constant, as should be expected in a model where the output growth rate is identical to the sum of population and productivity growth rates. But this immediately implies that the interior equilibrium in (46)-(49) can only be achieved for the initial condition , with any smaller initial employment rate leading to and any bigger one leading to . We therefore do not pursue this special case further.

Alternatively, the special case

| (68) |

is conceptually much closer to the original Keen model in [11], in that expected sales (and therefore output) grow at the same rate as capital. In this case, capacity utilization is given by a constant , as the fourth equation in (66) vanishes and the model reduces to a three-dimensional system for , which we now consider in its real and monetary versions.

4.1 Real version

Consider first the model in real terms, that is to say, with the wage-price parameters set to and as in the original Goodwin and Keen models. We then obtain that the system (66), with given by (68), reduces to

| (69) |

where as before, and we have adopted a consumption function of the form . We regard this as the closest model to the original Keen model in (60), but with a non-trivial effective demand of the form

| (70) |

and fluctuating inventory levels given by

| (71) |

The system (69) also admits a bad equilibrium of the form . Nevertheless, for (or any other consumption function that includes a positive wealth effect), this equilibrium implies that and consequently , which is not economically meaningful. For this reason, in the next section we investigate a monetary version of the model where inflation becomes infinite as in accordance with the price dynamics (31) with . Interestingly, the system (69) also admits a bad equilibrium of the form , which was not possible in the original Keen model. Nevertheless, it is easy to see that this equilibrium is unstable provided

| (72) |

a condition that is likely to be satisfied in practice.

4.2 Monetary version

Using (31)-(32) as the price-wage dynamics leads to the following monetary version of the model of the previous section

| (73) |

where and

| (74) |

As before, we regard this as the closest model to the monetary Keen model in (63), but with a non-trivial effective demand given by (70) and fluctuating inventory levels given by (71).

In what follows, we denote and for convenience. Let be the Jacobian matrix of (73), given by

| (75) |

with

| (76) | ||||

| (77) | ||||

| (78) | ||||

| (79) |

Under technical conditions similar to those found in [9, 5, 10] we shall establish that the model (73) exhibits three meaningful types of equilibrium points, analogous to those described in [10]. The first one is a good equilibrium, corresponding to a desirable situation with finite debt and positive wages and employment. The second one is a debt crisis equilibrium corresponding to a finite level of debt and vanishing wages and employment. The third one is a deflationary state that can either accept credit explosion or not, which appears with the introduction of price dynamics. A fourth situation corresponding to the trivial equilibrium is theoretically possible, but always unstable and therefore irrelevant in the present context. The following results rely on a standard equilibrium analysis with Hartman-Grobman theorem and can be skipped at first reading.

We start by assuming that for all and satisfies

| (80) |

We assume further that

| (81) |

Trivial equilibrium

Steady growth equilibrium

Following [9], we call the equilibrium with finite debt and positive wages and employment rate the good equilibrium for (73). We can see from the second equation in (73) that this is characterized by

| (82) |

which can be uniquely solved for because of condition (80). This corresponds to a steady state where the growth rate equals , the natural growth rate of the economy. Accordingly, is a root of the following quadratic equation:

| (83) |

where

Provided , there is at least one real solution to (83) given by

| (84) |

It is rather difficult to get information out of this expression, and one shall study the above value numerically.

We shall impose , in order to ensure that . Given , we obtain

| (85) |

which, on account of (81), always exists provided . At the point , the Jacobian (75) becomes

| (86) |

Computing the characteristic polynomial for the matrix (86) and applying the Routh-Hurwitz criterion provides a necessary and sufficient condition for all the roots of a cubic polynomial to have negative real part, which in turn ensure local stability for this equilibrium point. They boil down to the following two fairly non-intuitive conditions, which need to be checked numerically:

| (87) | ||||

| (88) |

At equilibrium, we find that demand equals

| (89) |

When , this equilibrium is not economically meaningful, since in this case (67) leads to vanishing inventories in finite time and the model ceases to make sense. Accordingly, this restricts the constant capacity utilization to the range

| (90) |

in which case the relative inventory level converges to the equilibrium value

| (91) |

with the Keen model of [11] corresponding to structurally unstable special case with and .

Debt crisis

As described in [9], a key feature of the original Keen model [11] is that it admits an equilibrium of the form , that is to say, corresponding to unbounded growth in the debt ratio at the same time that the wage share and employment rate decrease to zero. The analysis in [9] was done using a change the variable and observing that becomes an equilibrium point for the transformed system.

In the present case, we see that this change of variable turns the third equation in (73) into

Using the price dynamics (31), with demand given by the (30) and consumption of the form we find that the term in the expression above becomes

from which we deduce that does not lead to in the transformed system. Observe that a similar problem arises with the term originating from the first equation in (73) whenever . More generally, we conclude that the system (73) does not exhibit an equilibrium characterized by provided the consumption function has a wealth effect that grows at least linearly in .

On the other hand, system (73) admits a different type of debt crisis corresponding to no economic activity and a finite debt ratio, namely, an equilibrium of the form where satisfies

| (92) |

with

| (93) |

Deflationary equilibria

Another undesired type of equilibrium, similar to the new one found in [10], appears in the monetary version of the long-run dynamics and corresponds to a very specific situation when decreasing real wages, due to low employment rate, are compensated by deflation in the economy. Similar to Section 3.4, these equilibria are of the form where and are solutions to the nonlinear equations

| (95) | ||||

| (96) |

where

| (97) |

Observe that (81) implies that , confirming that this equilibrium corresponds to a deflationary economy.

The Jacobian matrix (75) at this point, becomes

| (98) |

Inverting the order of and thus provide a lower triangular matrix, from which we can immediately obtain the three eigenvalues. Assuming , the conditions for local stability of then read

| (99) |

all of which must be checked numerically. In other words, local stability of the deflationary equilibrium cannot be ruled out a priori either.

5 Short-run dynamics

5.1 Supply-demand tâtonnement

In contrast with Section 4, we now consider what happens when only short-run effects are taking into account. For this, suppose that , so that the long-run equilibrium corresponds to an economy with zero growth. In this case, expected sales and investment in planned inventory should be driven solely by short-run fluctuations in demand, and we accordingly set

| (100) |

Inserting this into (31), (34), and (35), we see that the inventory ratio and instantaneous growth rate of the economy become

| (101) |

Similarly, because the long-run equilibrium level for capital is constant, investment is only necessary in order to replace depreciated capital, so that we can set

| (102) |

The system (41) then becomes

| (103) |

To proceed with the analysis further, we now consider the type of short business cycles first reported in [12], which are attributed to the response of firms to changes in inventory, but with lags in information. Accordingly, we focus exclusively on the fluctuations generated by the adjustment terms related to the parameters and set and , thereby ignoring both the labour cost push in (31) and the effect of employment in the wage bargaining equation (32). This leads to

| (104) |

Assuming further that for and that

| (105) |

we find that , so that the growth rate of is the same as the one of . We then obtain that (103) decouples into a two-dimensional system for the variables and of the form

| (106) |

and an auxiliary system for that can be solved after have been determined.

This is a situation with constant level of capital, and investment answering to running costs and depreciation only. The productivity and the population size are assumed to be constant. Firms adjust their expectations by replicating the demand with relaxation parameter . Inventories aim at being a fraction of that expected demand, with relaxation parameter . Prices move only to accommodate inventories, via the parameter . Wages respond to inflation though the parameter and the aggregate real purchasing power is affected by . We are thus in a strictly short-run supply-demand tâtonement mechanism.

5.2 Phase plan analysis

It is easy to see that is invariant by (106), which induces that is also invariant. Nothing, however, bounds either these two variables or the auxiliary function from above. Consequently, great care shall be taken in the interpretation of the model dynamics, since it allows for , or without any direct feedback.

We rewrite the system (106) into the following form

| (107) |

where and

The above inequalities hold for any positive parameters configuration. The isocline is given by the lines and , and it easily follows that on and on .

On the other hand, the isocline is given by the following two functions of :

with The polynomial itself has two real roots given by

It is easy to see that , since , and that , since . Moreover, on the interval we have that , so that the curves are not defined and . Alternatively, on , we have that for and for .

Notice that or imply for all . This actually provides limit cases and . In addition, we can show that

which is greater than one provided . In that case, we find that . On the other hand, for large values of , we have that

| (108) |

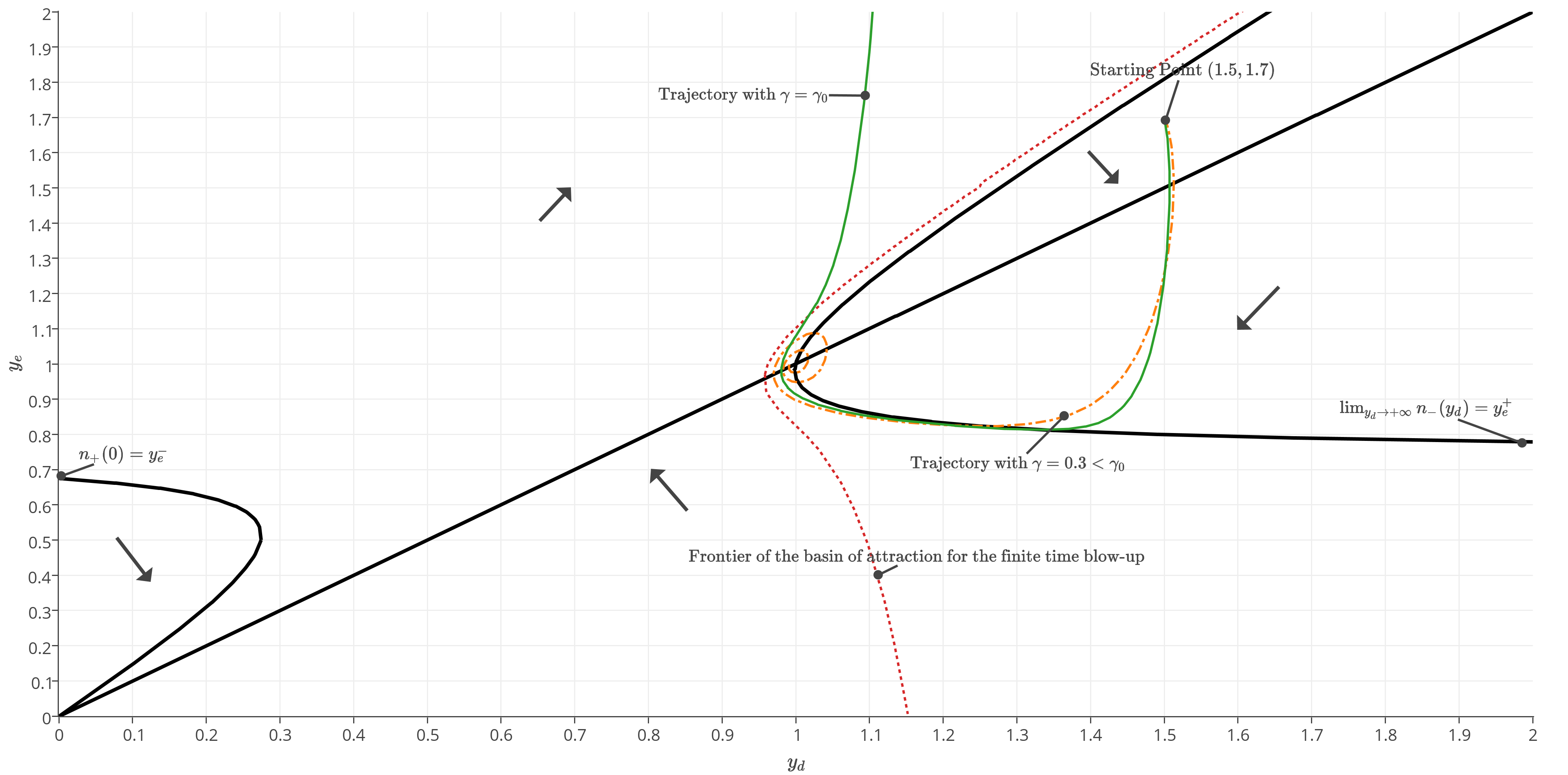

so that . This is summed up by black thick lines and arrows giving the directional quadrants of the system in each area on Figure 1.

5.3 Equilibrium points

Three equilibria are possible for (107). The first equilibrium corresponds to the interior equilibrium (44) in the general model with . At this equilibrium, expected sales equals output and equals demand: the tâtonnement is successful. Moreover, the equilibrium inflation rate and the growth rate are both zero, and are constant, and inventory provides a constant buffer between production and sales.

The Jacobian matrix of (107) is

At the first equilibrium, it simplifies into

which yields the characteristic equation:

All parameters being positive, and , the real part of the two roots is negative if and only if (Routh-Hurwitz criterion)

| (109) |

This equilibrium is thus locally attractive if (109) holds. When , the roots of the characteristic equations are purely imaginary and the system undergoes an Andronov-Hopf bifurcation. The first Lyapunov exponent at the bifurcation value is positive, so that the bifurcation is sub-critical: the limit cycle is unstable (this is confirmed by simulations). When , in full generality, the equilibrium point is locally repelling.

The second equilibrium is given by and means the collapse of the market, with all variables dwindling to zero. At this point the Jacobian matrix is

and we see that this equilibrium is unstable for and fails to be asymptotically stable, even if , since the kernel of the Jacobian is of dimension one.

If the system does not converge toward nor , there exists a singular attractive state for (106) characterized by a finite-time blow-up towards . By writing the system under the form , we obtain the dynamics

| (110) |

We are interested in the finite-time blow-up for both and toward , since is super-linearly increasing in , according to (108). We are able to express (110) as a second order non-linear differential equation:

| (111) |

and the local behavior defined by . In that case, factorizing by allows to approximate (111) around that point by

This is a generalized Emdem-Fowler equation [15], whose solution is of the form

reaching zero in finite time for any parameters . This situation translates into a singular behaviour: when expectations and demand are very high, inventories must decrease to answer expected sales, and prices are pushed down to control unplanned inventories. However this stimulates the aggregate demand, which in turns boost the expectations. The growth rate of shrinks and the situation gets worse.

5.4 Price adjustment and information lag: another view

In the present case, assumption (31) takes on a major role about firms speed of price adjustment, where it is assumed that they take into account direct unplanned inventory investment. This has a significant impact on the stability of a supply-demand equilibrium.

Consider an alternative assumption to (31) with prices adjusting with the difference between desired and observed inventory levels:

| (112) |

which, along with previous assumptions, provides the inflation rate . Computations provide an alternative short-run business cycles system of the form

| (113) |

that we compare with (106). The slight difference with the latter concerns the first equation, for which the isocline is given by instead of . Equilibrium points are interestingly the same, i.e., a supply-demand equilibrium , a market collapse , and a finite-time blow-up toward . The impact on stability is however much more involved. The Jacobian for the first equilibrium is given by

| (114) |

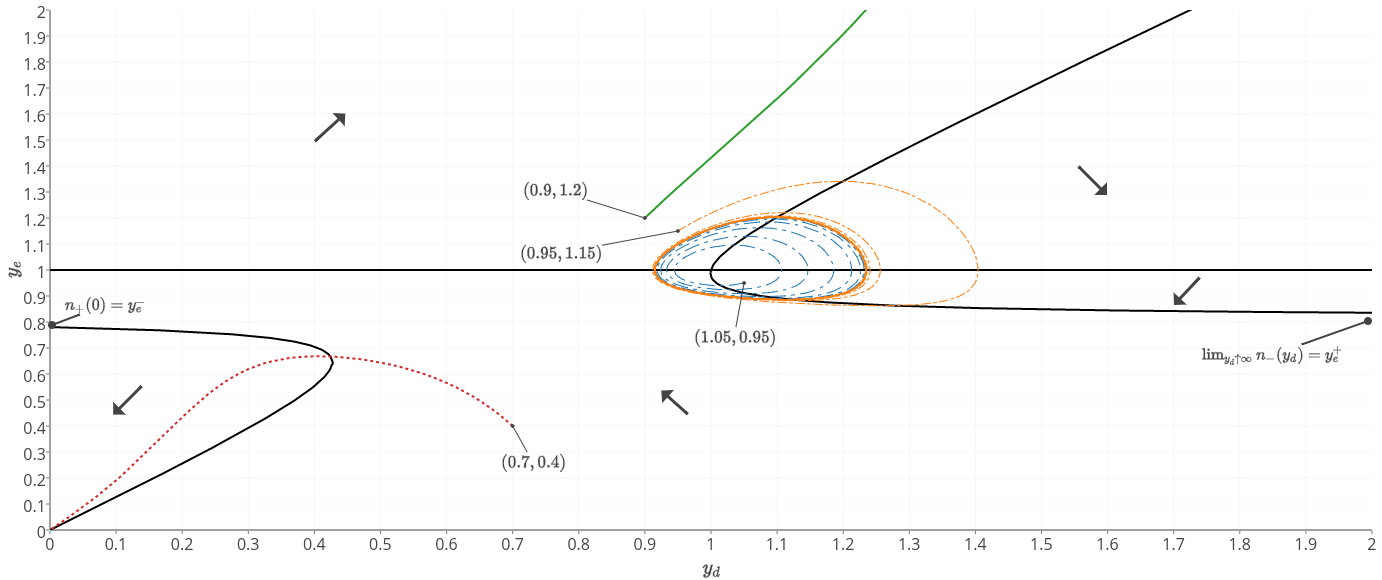

Since all entries of the matrix above are positive, both root of the characteristic equation are positive. This equilibrium point is thus locally repelling. We observe on Figure 2 that points starting in the close neighborhood of converge to a semi-stable limit cycle. Trajectories starting in the external neighborhood of that limit cycle converge also numerically to that limit cycle, so that the latter is locally stable. These assertions are supported by the two trajectories starting respectively at and on Figure 2. This seems to correspond strongly to a Kitchin cycle [12], where lag in information and decision adjustment (through parameters , and ) affect prices, output, demand, inventory and employment in a periodic manner. This cycle is locally stable, that is, it attracts a whole region including it.

At the bad equilibrium the Jacobian equals

| (115) |

where the two eigenvalues are negative if and only if . Therefore, this point can be locally attractive, as the trajectory starting at shows on Figure 2. Here, the low level of inventories pushes prices up, and pulls demand down, in a spiral dynamics toward a complete shut-down of economical activities: employment and utilization dwindle to zero, and the market shuts down.

The finite-time blow-up is similar to the previous case. See for example the trajectory starting at on Figure 2.

6 Conclusions

In the present article, we have presented a general, albeit complex, stock-flow consistent model for inventory dynamics in a closed monetary economy. The model relies heavily on adapted behaviour of firms regarding expected sales and desired inventory levels. To gain insight, we analyze the model in two specific limiting versions: a long-run dynamics ignoring the effect of instantaneous fluctuations in demand and a short-run one solely driven by these fluctuations.

The long-run dynamics gives rise to a version of the Keen model [11] where demand is not necessarily equal to output. This sheds light on the question of whether the rich set of trajectories obtained in [11] and related models of debt-financed investment were an artefact of a strictly supply-driven model with no role for Keynesian effect demand. As the above analysis shows, one can relax the constraints of the Keen model by allowing an independently specified consumption function and still obtain broadly the same conclusions. The main difference is that the debt crisis, previously characterized by an explosive debt ratio, gets replaced by an equally bad equilibrium with a finite debt ratio but collapsing economy with vanishing wage share and employment rates. In both cases, Minskyan instability arising from financial charges lead to the collapse of profits and an induced debt crisis.

The short-run dynamics reveals inventory cycles related to nominal rigidity of demand. For given speeds of expectations adjustment and inventory stocks, a high degree of nominal illusion is necessary to ensure local stability. Yet, this situation can show divergence as the model does not include long-run feedback channels. A second dimension, illustrated by the difference in behavior in Sections 5.3 and 5.4, is the type of information on inventory used for price adjustment. By replacing unplanned inventory investment with mismatch in desired inventory levels as the factor determining price adjustments, we create a lag in information that gives rise a stable limit cycle which we interpret as a Kitchin cycle. Nevertheless, this does not get rid of the divergent path, still possible if the situation is too far from the interior equilibrium. In addition, we have the possibility of a market failure where demand and supply meet at zero, for a condition that appears repeatedly in this section provided . In other words inventories must adjust faster than expectations to avoid this type of crash.

In its closing sentences, [18] asserts that “general-equilibrium analysis of the business cycle with inventories is still in its infant stage.” This is also true for disequilibrium analysis of the business cycle in the burgeoning recent literature on stock-flow consistent models [4], where inventories have received comparatively less attention than their more glamorous financial counterparts - cash balances, government deficits and the like. We hope this paper will help bring the analysis of inventory dynamics to a more diverse adolescence.

Acknowledgements

We are grateful to the participants of the Applied Stock-Flow Consistent Macro-modelling Summer School (Kingston University, August 1-8, 2016) where this work was presented. Partial financial support for this work was provided to MRG by the Institute for New Economic Thinking (Grant INO13-00011) and the Natural Sciences and Engineering Research Council of Canada (Discovery Grants) and to ANH by the Chair Energy and Prosperity, Energy Transition Financing and Evaluations.

References

- [1] M. Abramovitz, Inventories and Business Cycles, with Special Reference to Manufacturer’s Inventories, National Bureau of Economic Research, 1950.

- [2] A. S. Blinder, Retail inventory behavior and business fluctuations, Brookings Papers on Economic Activity, (1981), pp. 443–520.

- [3] A. S. Blinder and L. J. Maccini, Taking stock: A critical assessment of recent research on inventories, Journal of Economic Perspectives, 5 (1991), pp. 73–96.

- [4] E. Caverzasi and A. Godin, Stock-flow consistent modeling through the ages, Economics Working Paper Archive 745, Levy Economics Institute, Jan. 2013.

- [5] B. Costa Lima, M. Grasselli, X.-S. Wang, and J. Wu, Destabilizing a stable crisis: Employment persistence and government intervention in macroeconomics, Structural Change and Economic Dynamics, 30 (2014), pp. 30 – 51.

- [6] R. Franke, A Metzlerian model of inventory growth cycles, Structural Change and Economic Dynamics, 7 (1996), pp. 243 – 262.

- [7] W. Godley and M. Lavoie, Monetary economics : an integrated approach to credit, money, income, production and wealth, Palgrave Macmillan, Basingstoke, 2007.

- [8] R. M. Goodwin, A growth cycle, in Socialism, Capitalism and Economic Growth, C. H. Feinstein, ed., London, 1967, Cambridge University Press, pp. 54–58.

- [9] M. R. Grasselli and B. Costa Lima, An analysis of the Keen model for credit expansion, asset price bubbles and financial fragility, Mathematics and Financial Economics, 6 (2012), pp. 191–210.

- [10] M. R. Grasselli and A. Nguyen Huu, Inflation and speculation in a dynamic macroeconomic model, Journal of Risk and Financial Management, 8 (2015), p. 285.

- [11] S. Keen, Finance and economic breakdown: Modeling Minsky’s “Financial Instability Hypothesis”, Journal of Post Keynesian Economics, 17 (1995), pp. 607–635.

- [12] J. Kitchin, Cycles and trends in economic factors, The Review of Economics and Statistics, (1923), pp. 10–16.

- [13] L. A. Metzler, The nature and stability of inventory cycles, The Review of Economics and Statistics, 23 (1941), pp. 113–129.

- [14] H. P. Minsky, Can ‘it’ happen again ?, M E Sharpe, Armonk, NY, 1982.

- [15] A. D. Polyanin and V. F. Zaitsev, Handbook of exact solutions for ordinary differential equations, Boca Raton: CRC Press,— c1995, 1 (1995).

- [16] S. Ryoo, The paradox of debt and Minsky’s financial instability hypothesis, Metroeconomica, 64 (2013), pp. 1–24.

- [17] P. Wang, Y. Wen, and Z. Xu, What inventories tell us about aggregate fluctuations—A tractable approach to (S,s) policies, Journal of Economic Dynamics and Control, 44 (2014), pp. 196 – 217.

- [18] Y. Wen, Input and output inventory dynamics, American Economic Journal: Macroeconomics, 3 (2011), pp. 181–212.