Estimation of Graphical Models through Structured Norm Minimization

Abstract

Estimation of Markov Random Field and covariance models from high-dimensional data represents a canonical problem that has received a lot of attention in the literature. A key assumption, widely employed, is that of sparsity of the underlying model. In this paper, we study the problem of estimating such models exhibiting a more intricate structure comprising simultaneously of sparse, structured sparse and dense components. Such structures naturally arise in several scientific fields, including molecular biology, finance and political science. We introduce a general framework based on a novel structured norm that enables us to estimate such complex structures from high-dimensional data. The resulting optimization problem is convex and we introduce a linearized multi-block alternating direction method of multipliers (ADMM) algorithm to solve it efficiently. We illustrate the superior performance of the proposed framework on a number of synthetic data sets generated from both random and structured networks. Further, we apply the method to a number of real data sets and discuss the results.

Keywords: Markov Random Fields, Gaussian covariance graph model, structured sparse norm, regularization, alternating direction method of multipliers (ADMM), convergence.

1 Introduction

There is a substantial body of literature on methods for estimating network structures from high-dimensional data, motivated by important biomedical and social science applications; see Barabási and Albert (1999); Liljeros et al. (2001); Robins et al. (2007); Guo et al. (2011a); Danaher et al. (2014); Friedman et al. (2008); Tan et al. (2014); Guo et al. (2015). Two powerful formalisms have been employed for this task, the Markov Random Field (MRF) model and the Gaussian covariance graph model (GCGM). The former captures statistical conditional dependence relationships amongst random variables that correspond to the network nodes, while the latter to marginal associations. Since in most applications the number of model parameters to be estimated far exceeds the available sample size, the assumption of sparsity is made and imposed through regularization. An penalty on the parameters encoding the network edges is the most common choice; see Friedman et al. (2008); Karoui (2008); Cai and Liu (2011); Xue et al. (2012), which can also be interpreted from the Bayesian perspective as using an independent double-exponential prior distribution on each edge parameter. Consequently, this approach encourages sparse uniform network structures that may not be the most suitable choice for many real world applications, which in turn have hub nodes or dense subgraphs. As argued in Barabási and Albert (1999); Liljeros et al. (2001); Newman (2001); Li et al. (2005); Fortunato (2010); Newman (2012) many networks exhibit different structures at different scales. An example includes a densely connected subgraph, also known as a community in the social networks literature. Such structures in social interaction networks may correspond to groups of people sharing common interests or being co-located (Traud et al., 2011; Newman and Girvan, 2004), while in biological systems to groups of proteins responsible for regulating or synthesizing chemical products (Guimera and Amaral, 2005; Lewis et al., 2010; see, Figure 3 for an example). Hence, in many applications, simple sparsity or alternatively, a dense structure fails to capture salient features of the true underlying mechanism that gave rise to the available data.

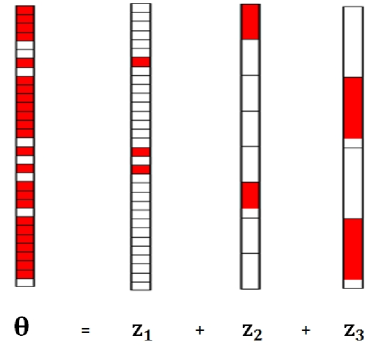

In this paper, we introduce a framework based on a novel structured sparse norm that allows us to recover such complex structures. Specifically, we consider Markov Random Field and covariance models where the parameter of interest, can be expressed as the superposition of sparse, structured sparse and dense components as follows:

| (1) |

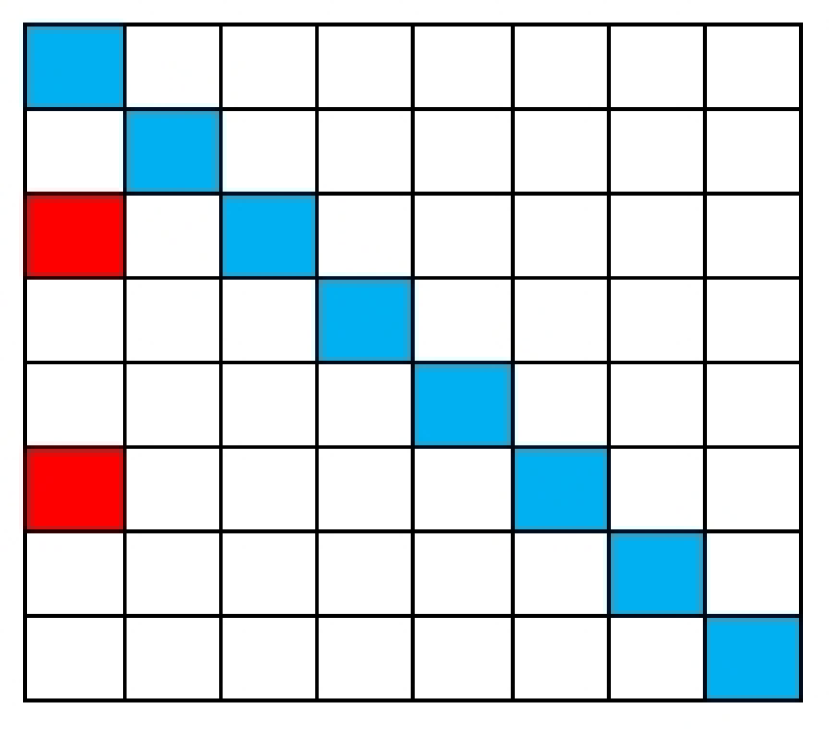

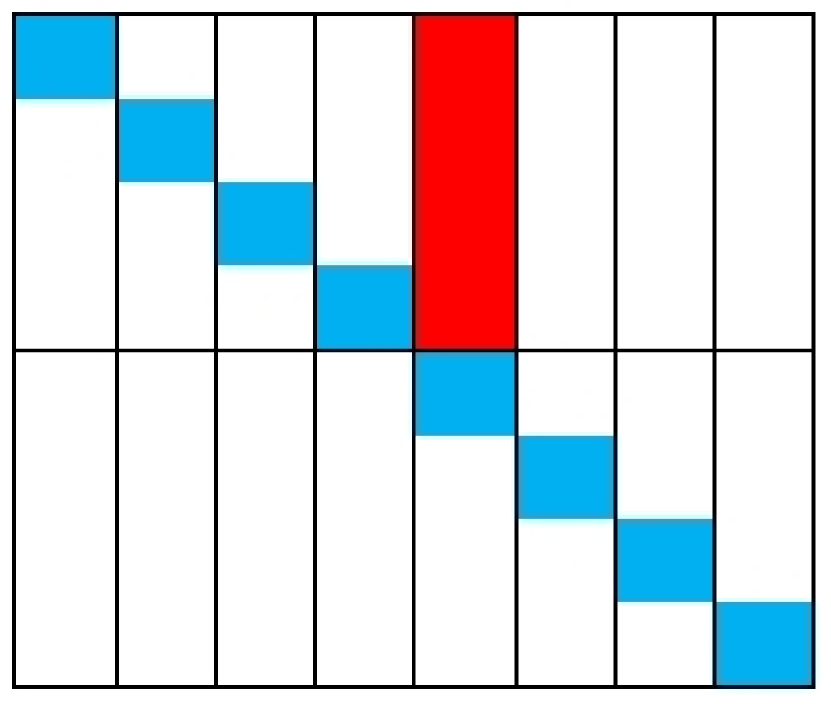

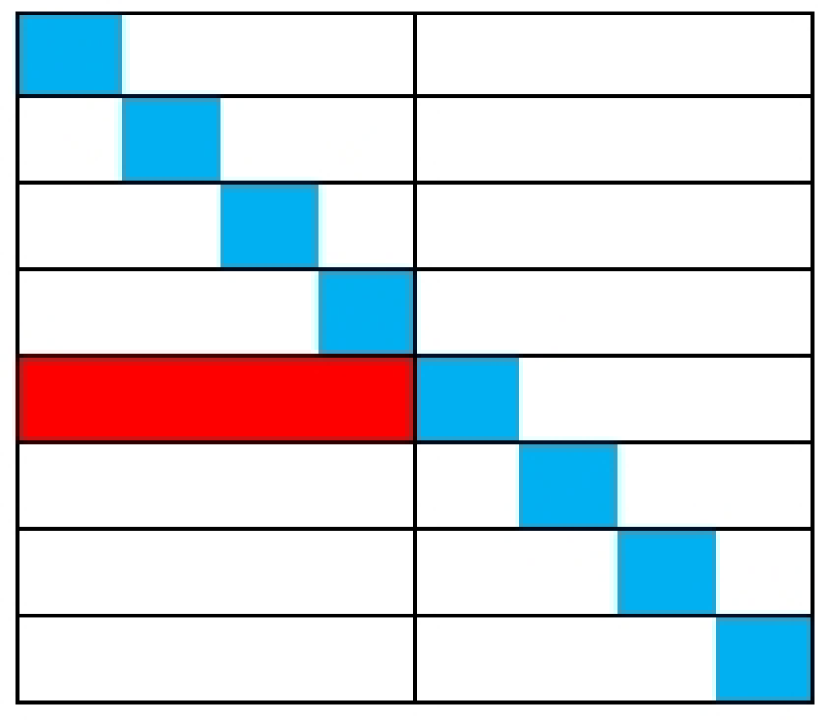

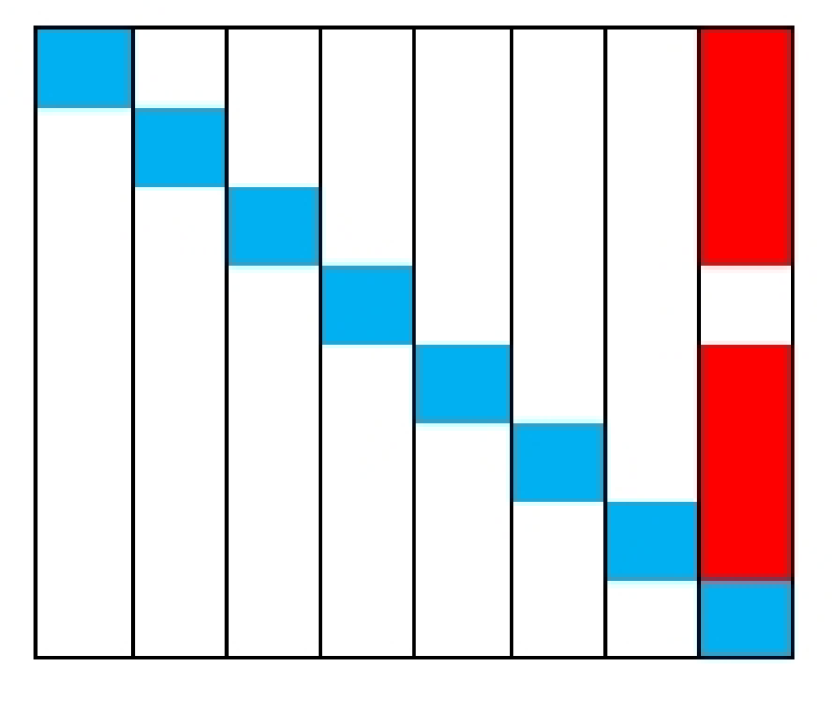

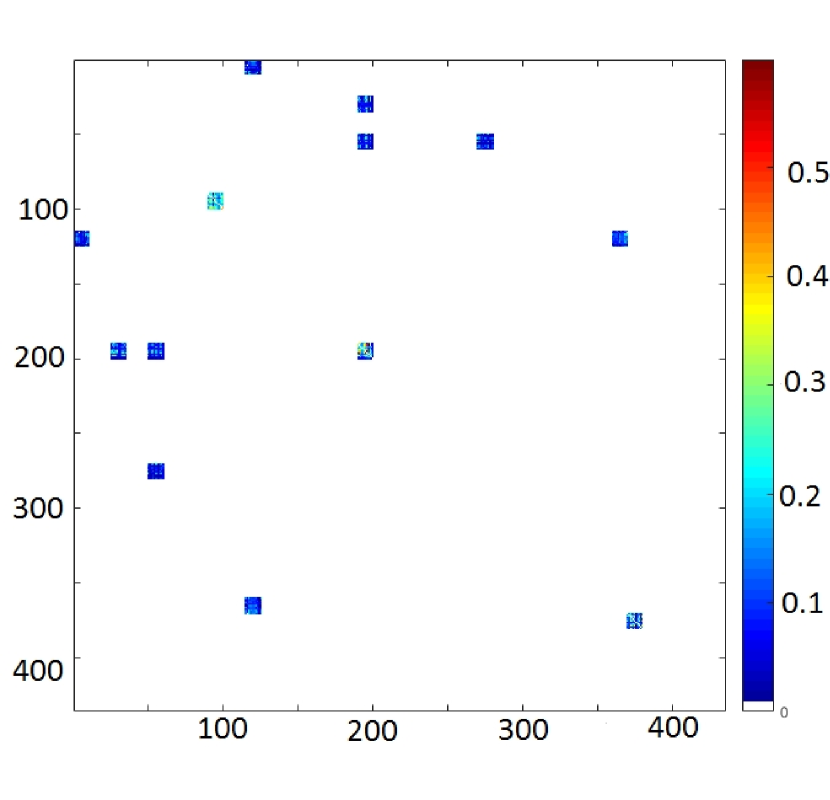

where is a sparse matrix, are the set of structured sparse matrices (see, Figure 3 for an example of such structured matrices), and is a dense matrix having possibly very many small, non-zero entries. As shown in Figure 3, the elements of represent edges between non-structured nodes, and the non-zero parts of structured matrices correspond to densely connected subgraphs (communities).

We elaborate more on the decomposition proposed above. We start by discussing on the sparse and structured sparse component and then elaborate on the dense component. Traditional sparse (lasso Tibshirani, 1996; Friedman et al., 2008) and group sparse (group lasso Yuan and Lin, 2007; Jacob et al., 2009; Obozinski et al., 2011) are tailor-made to estimate and recover sparse and structured sparse model structures, respectively. However, these methods can not accommodate different structures, unless users specify a priori the structure of interest (e.g. hub nodes and sparse components), thus severely limiting their application scope. On the other hand, the general framework introduced, is capable of estimating from high-dimensional data, groups with overlaps, hubs and dense subgraphs, with the size and location of such structures not known a priori.

Next, we discuss the role of the dense component . In many applications, the data generation mechanism may correspond to a true sparse or structured sparse structure, ”corrupted” by a dense component comprising of possible many small entries. A simple example of such a generating mechanism in linear models would have the regression coefficient being sparse with a few large entries and a more dense component having possibly many small, nonzero entries. In such instances, a pure sparse model formulation may not perform particularly well due to the presence of the dense component and may require very careful tuning to recover the sparse component of interest. This line of reasoning is also adopted in Chernozhukov et al. (2017). Note however, that the model may also be used in settings where there is a significant dense component; however, as discussed in Chernozhukov et al. (2017) recovery of the individual component is not guaranteed. Hence, in this work we adopt the viewpoint that represents a small ”perturbation” of the sparse+structured sparse structure. To achieve these goals, it leverages a new structured norm that is used as the regularization term of the corresponding objective function.

The resulting optimization problem is solved through a multi-block ADMM algorithm. A key technical innovation is the development of a linearized ADMM algorithm that avoids introducing auxiliary variables which is a common strategy in the literature. We establish the global convergence of the proposed algorithm and illustrate its efficiency through numerical experimentation. The algorithm takes advantage of the special structure of the problem formulation and thus is suitable for large instances of the problem. To the best of our knowledge, this is the first work that gives global convergence guarantees for linearized multi-block ADMM with Gauss-Seidel updates, which is of interest in its own accord.

The remainder of the paper is organized as follows: In Section 2, we present the new structured norm used as the regularization term in the objective function of the Markov Random Field, covariance graph, regression and vector auto-regression models. In Section 3, we introduce an efficient multi-block ADMM algorithm to solve the problem, and provide the convergence analysis of the algorithm. In Section 4, we illustrate the proposed framework on a number of synthetic and real data sets, while some concluding remarks are drawn in Section 5.

2 A General Framework for Learning under Structured Sparsity

We start by introducing key definitions and associated notation.

2.1 Symmetric Structured Overlap Norm

Let be an data matrix, be a symmetric matrix containing the parameters of interest of the statistical loss function . The most popular assumption used in the literature is that is sparse and can be successfully recovered from high-dimensional data by solving the following optimization problem

| (2) |

where is some set depending on the loss function; is s a non-negative regularization constant; and denotes the norm or the sum of the absolute values of the matrix elements.

To explicitly model different structures in the parameter , we introduce the following symmetric structured overlap norm (SSON):

Definition 1

(Symmetric Structured Overlap Norm). Let be a symmetric matrix containing the model parameters of interest. The symmetric structured overlap norm for a set of partitioned matrices is given by,

| (3) |

where and are nonnegative regularization constants; is the number of blocks of the partitioned matrix ; is the th block of the partitioned matrix ; is an unstructured noise matrix; denotes the norm or the sum of the absolute values of the matrix elements; and the Frobenius norm.

We note that the overlap norm defined by Mohan et al. (2012); Tan et al. (2014) encourages the recovery of matrices that can be expressed as a union of few rows and the corresponding columns (i.e. hub nodes). However, SSON represents a new symmetric and significantly more general variant of the overlap norm that promotes matrices that can be expressed as the sum of symmetric structured matrices. Moreover, unlike the previous group sparsity and the latent group lasso discussed in Yuan and Lin (2007); Jacob et al. (2009); Obozinski et al. (2011) that require users to specify structures of interest a priori, the SSON achieves a similar objective in an agnostic manner, relying only on how well such structures fit the observed data.

In many applications, such as regression models, we are interested in modeling different structures in a parameter vector . In these cases, we have the following definition as a special case of SSON:

Definition 2

Let be a vector containing the model parameters of interest. The structured overlap norm for a set of partitioned vectors is given by,

| (4) |

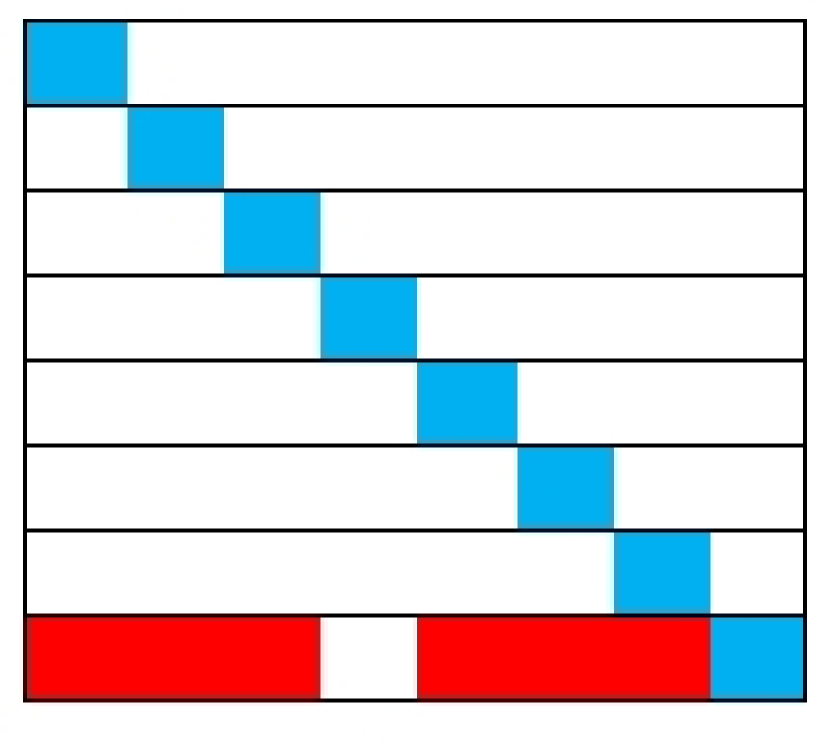

where and are nonnegative regularization constants; is the number of blocks of the partitioned vector ; is the th block of the partitioned vector (see, Figure 1); is an unstructured noise vector; denotes the norm or the sum of the absolute values of the vector elements; and the two norm.

Remark 3

In the formulation of the problem, , , and are tuning parameters corresponding to the sparse component , the structured components and the dense (noisy) component , respectively. While the nonzero components may be clustered into groups, the nonzero groups may also be sparse. The latter can be achieved by (1) when are positive constants.

Remark 4

The SSON admits the lasso (Tibshirani, 1996), the group lasso with overlaps (Jacob et al., 2009; Obozinski et al., 2011) and the ridge shrinkage (Hoerl and Kennard, 1970) methods as three extreme cases, by respectively setting , , and 111For example, with , we set when , so the problem is well-defined..

Note that SSON is rather different from the sparse group lasso, which also uses a combination of and penalization, where is the group lasso norm. The sparse group lasso penalty is , and thus the includes lasso and group lasso as extreme cases corresponding to and , respectively. However, does not split into a sparse and a group sparse part and will produce a sparse solution as long as . Hence, the sparse group lasso method can be thought of as a sparsity-based method with additional shrinkage by . The group sparsity processes data very differently from SSON and consequently has very different prediction risk behavior. The same argument illustrates the advantages of the proposed SSON penalty over the well-known elastic net penalty. The elastic net is a combination of lasso and ridge penalties (Zou and Hastie, 2005). However, the elastic net does not split into a sparse and a dense component. Our results show that SSON tends to perform no worse than, and often performs significantly better than ridge, lasso, group lasso or elastic net with penalty levels chosen by cross-validation.

Remark 5

In order to encourage different structures in the parameter matrix , we consider the Frobenius norm of blocks of partitioned matrices, which leads to recovery of dense subgraphs. Other values for the norm of such blocks are also possible; e.g. the norm.

Remark 6

The matrix is an important component of the SSON framework.

-

It enables to develop a convergent multi-block ADMM to solve the problem of estimating a structured Markov Random Field or covariance model. Note that in general, a direct extension of ADMM to multi-block convex minimization problems is not necessarily convergent even without linearization of the corresponding subproblems as shown in Chen et al. (2016).

-

From a performance standpoint, our results show that adding a ridge penalty term to the structured norm is provably effective in correctly identifying the underlying structures in the presence of noisy data (Zou and Hastie, 2005; Chernozhukov et al., 2017) (see, Figure 2 for an example of decomposition (1) in the presense of noise for covariance matrix estimation.)

Next, we discuss the use of the SSON as a regularizer for maximum likelihood estimation of the following popular statistical models: (i) members of the Markov Random Field family including the Gaussian graphical model, the Gaussian graphical model with latent variables and the binary Ising model, (ii) the Gaussian covariance graph model and (iii) the classical regression and the vector auto-regression models. For the sake of completeness, we provide a complete, but succinct description of the corresponding models and the proposed regularization.

2.2 Structured Gaussian Graphical Models

Let be a data matrix consisting of -dimensional samples from a zero mean Gaussian distribution,

In order to obtain a sparse and interpretable estimate of the precision matrix that captures conditional dependence relationships, many authors have considered the well-known graphical lasso problem (Friedman et al., 2008; Rothman et al., 2008) in the form of (2) with loss function

| (5) |

where is the empirical covariance matrix of ; is the estimate of the precision matrix ; and is the set of symmetric positive definite matrices.

As is well known, the norm penalty in (2) encourages zeros (sparsity) in the solution. However, as previously argued, many biological and social network applications exhibit more complex structures than mere sparsity. Using the proposed SSON, we define the following objective function for the problem at hand:

| (6) |

where is the model parameter matrix and the corresponding SSON defined in (1).

Formulation (2.2) allows us to obtain more accurate and compact network estimates than conventional methods whenever the network exhibits different structures. Moreover, our formulation does not require a priori knowledge of the underlying network structure (i.e. which nodes in the network form densely connected subgraphs (see, Figure 4)).

In Figure 4, the performance of our proposed approach is illustrated on two simulated data sets exhibiting different structures (sub-figures (4(c)) and (4(f))); it can be seen that the proposed SSON based graphical lasso (sub-figures (4(b)) and (4(e))) can recover the network structure much better than the popular graphical lasso based estimator (Friedman et al., 2008) (subfigures (4(a)) and (4(d))).

2.3 Structured Ising Model

Another popular graphical model, suitable for binary or categorical data, is the Ising one (Ising, 1925). It is assumed that observations are independent and identically distributed from

| (7) |

where is the partition function, which ensures that the density sums to one. Here, is a symmetric matrix that specifies the network structure: implies that the th and th variables are conditionally independent given the remaining ones.

Several papers proposing estimation procedures for this model have been published. Lee et al. (2007) considered maximizing an -penalized log-likelihood for this model. Due to the difficulty in computing the log-likelihood with the expensive partition function, several authors have considered alternative approaches. For instance, Ravikumar et al. (2011) proposed a neighborhood selection approach. The latter proposal involves solving logistic regressions separately (one for each node in the network), which leads to an estimated parameter matrix that is in general not symmetric. In contrast, several authors considered maximizing an -penalized pseudo-likelihood with a symmetric constraint on (Guo et al., 2011a, b). Under the model (7), the -pseudo-likelihood for observations takes the form

| (8) |

We propose instead to impose the SSON on in (8) in order to estimate a binary network with different structures. This leads to the following optimization problem

| (9) |

where is the model parameter matrix and the corresponding SSON defined in (1).

An interesting connection can be drawn between our technique and the Ising block model discussed in Berthet et al. (2016), which is a perturbation of the mean field approximation of the Ising model known as the Curie-Weiss model: the sites are partitioned into two blocks of equal size and the interaction between those within the same block is stronger than across blocks, to account for more order within each block. However, one can easily seen that the Ising block model is a special case of (2.3).

2.4 Structured Gaussian Covariance Graphical Models

Next, we consider estimation of a covariance matrix under the assumption that

This is of interest because the sparsity pattern of specifies the structure of the marginal independence graph (Drton and Richardson, 2002, 2008).

Let be a symmetric matrix containing the parameters of interest. Setting the loss function , Xue et al. (2012) proposed to estimate the positive definite covariance matrix, by solving

| (10) |

where is the empirical covariance matrix, , and is a small positive constant. We extend (10) to accommodate structures of the covariance graph by imposing the SSON on . This results in the following optimization problem

| (11) |

where is the model parameter matrix and the corresponding SSON defined in (1).

2.5 Structured Gaussian Graphical Models with latent variables

In many applications throughout science and engineering, it is often the case that some relevant variables are not observed. For the Gaussian Graphical model, Chandrasekaran et al. (2010) proposed a convex optimization problem to estimate it in the presence of latent variables. Let be a symmetric matrix containing the parameters of interest. Setting , their objective function is given by

| (12) |

where is the sample covariance matrix of the observed variables; and are positive constants; and the indicator function is defined as

This convex optimization problem aims to estimate an inverse covariance matrix that can be decomposed into a sparse matrix minus a low-rank matrix based on high-dimensional data.

2.6 Structured Linear Regression and Vector Auto-Regression

The proposed SSON is also applicable to structured regression problems. Although this is not the main focus on this paper, nevertheless, we include a brief discussion, especially for lag selection in vector autoregressive models that are of prime interest in the analysis of high-dimensional time series data. The canonical formulation of the regularized regression problem is given by:

| (14) |

where , , , with being the response variable and a set of -predictors that are assumed to be independently and identically distributed (i.i.d.); is a regularization parameter and is a suitable norm. Specific choices of lead to popular regularizers including the lasso -- and the group lasso.

We propose instead to impose the SSON on in (14) in order to solve structured regression problems. Problem (14) can be rewritten in the following form by introducing new variables and :

| (15) |

where ; is the model parameter vector and the corresponding structured norm defined in (2).

Problem (2.6) can equivalently be thought of as a generalization of subspace clustering (Elhamifar and Vidal, 2009). Indeed, in order to segment the data into their respective subspaces, we need to compute an affinity vector that encodes the pairwise affinities between data vectors.

An interesting application of the SSON for multivariate regression problems is on structured estimation of vector autoregression (VAR) models (Lütkepohl, 2005), a popular model for economic and financial time series data (Tsay, 2005), dynamical systems (Ljung, 1998) and more recently brain function connectivity (Valdés-Sosa et al., 2005). The model captures both temporal and cross-dependencies between stationary time series. Formally, let be a -dimensional time series set of observations that evolve over time according to a lag- model:

where are transition matrices for different lags, and independent multivariate Gaussian white noise processes. The VAR process is assumed to be stable and stationary (bounded spectral density), while the noise covariance matrix is assumed to be positive definite with bounded largest eigenvalue (Basu and Michailidis, 2015).

Given observations from a stationary VAR process, the lag- VAR can be written is given by

| (16) |

It can be seen that to estimate one can solve the following least squares problem

| (17) |

However, as the number of component time series increases, the number of parameters to be estimated grows as ; hence, structural assumptions are imposed to estimate them from limited sample size. A popular choice is the lasso (Basu and Michailidis, 2015), that leads to sparse estimates. However, it does not incorporate the notion of lag selection, which could lead to certain spurious coefficients coming from further lags in the past. To address this problem, Basu et al. (2015) proposed a thresholded lasso estimate. However, our SSON can be used for lag selection, that guarantees that more recent lags are favored over further in the past ones.

Let be a symmetric matrix containing the parameters of interest for all lages of the problem. Setting the loss function , we propose to estimate the transition matrix, by solving the following optimization problem:

| (18) |

where is the estimate of the covariance matrix and the corresponding SSON defined in (1).

3 Multi-Block ADMM for Estimating Structured Network Models

Objective functions (2.2), (2.3), (2.4), (2.5), (2.6), and (2.6) involve separable convex functions, while the constraint is simply linear, and therefore they are suitable for ADMM based algorithms. We next introduce a linearized multi-block ADMM algorithm to solve these problems and establish its global convergence properties.

The alternating direction method of multipliers (ADMM) is widely used in solving structured convex optimization problems due to its superior performance in practice; see Scheinberg et al. (2010); Boyd et al. (2011); Hong and Luo (2017); Lin et al. (2015, 2016); Sun et al. (2015); Davis and Yin (2015); Hajinezhad and Hong (2015); Hajinezhad et al. (2016). On the theoretical side, Chen et al. (2016) provided a counterexample showing that the ADMM may fail to converge when the number of blocks exceeds two. Hence, many authors reformulate the problem of estimating a Markov Random Field model to a two block ADMM algorithm by grouping the variables and introducing auxiliary variables (Ma et al., 2013; Mohan et al., 2012; Tan et al., 2014). However, in the context of large-scale optimization problems, the grouping ADMM method becomes expensive due to its high memory requirements. Moreover, despite lack of convergence guarantees under standard convexity assumptions, it has been observed by many researchers that the unmodified multi-block ADMMs with Gauss-Seidel updates often outperform all its modified versions in practice (Wang et al., 2013; Sun et al., 2015; Davis and Yin, 2015).

Next, we present a convergent multi-block ADMM with Gauss-Seidel updates to solve convex problems (2.2), (2.3), (2.4), (2.5), and (2.6). The ADMM is constructed for an augmented Lagrangian function defined by

where is the Lagrange multiplier, a penalty parameter, the loss function of interest and

| (20) |

In a typical iteration of the ADMM for solving (3), the following updates are implemented:

| (21) | |||||

| (22) | |||||

| (23) | |||||

| (24) |

where

| (25) |

To avoid introducing auxiliary variables and still solve subproblems (22) efficiently, we propose to approximate the subproblems (22) by linearizing the quadratic term of its objective function (see also Bolte et al., 2014; Lin et al., 2011; Yang and Yuan, 2013). With this linearization, the resulting approximation to (22) is then simple enough to have a closed-form solution. More specifically, letting , we define the following majorant function of at point ,

| (26) |

where is a proximal parameter, and

| (27) |

The next result establishes the sufficient decrease property of the objective function given in (22), after a proximal map step computed in (28).

Lemma 7

Proof. The proof of this Lemma follows along similar lines to the proof of Lemma 3.2 in Bolte et al. (2014).

It is well known that (28) has a closed-form solution that is given by the shrinkage operation (Boyd et al., 2011):

| (29) |

where in (3) denotes the soft-thresholds operator, applied element-wise to a matrix A (Boyd et al., 2011):

Remark 8

Note that in the case of solving problem (2.5), one needs to add another block function to the augmented Lagrangian function (3) and update . In this case, the proximal mapping of is

| (30) |

where It is easy to verify that (30) has a closed-form solution given by

where is the eigenvalue decomposition of (see, Chandrasekaran et al., 2010; Ma et al., 2013 for more details).

The discussions above suggest that the following unmodified ADMM for solving (3) gives rise to an efficient algorithm.

-

(a)

Primal variables , , , , , to the identity matrix.

-

(b)

Dual variable to the zero matrix.

-

(c)

Constants , and .

-

(d)

Nonnegative regularization constants .

Remark 9

The complexity of Algorithm 1 is of the same order as the graphical lasso (Friedman et al., 2008), the method in Tan et al. (2014) for hub node discovery and the algorithm used for estimation of sparse covariance matrices introduced by Xue et al. (2012). Indeed, one can easily see that with any set of structured matrices , the complexity of Algorithm 1 is equal to , which is the complexity of the eigen-decomposition for updating in step 2(a).

Since both the objective function and constraints of (3) become separable after using the linearization technique introduced in (26), the problem can be decomposed into smaller subproblems; the latter can be solved in a parallel and distributed manner with a small modification in Algorithm 1. Indeed, we can apply a Jacobian ADMM to solve (3) with the following updates,

| (31) |

where is defined in (28) with

| (32) |

Intuitively, the performance of the Jacobian ADMM should be worse than the Gauss-Seidel version, because the latter always uses the latest information of the primal variables in the updates. We refer to Liu et al. (2015); Lin et al. (2015) for a detailed discussion on the convergence analysis of the Jacobian ADMM and its variants. On the positive side, we obtain a parallelizable version of the multi-block ADMM algorithm.

3.1 Convergence analysis

The next result establishes the global convergence of the standard multi-block ADMM for solving SSON based statistical learning problems, by using the Kurdyka- Lojasiewicz (KL) property of the objective function in (3).

Theorem 10

Proof. A detailed exposition is given in Appendix B.

4 Experimental Results

In this section, we present numerical results for Algorithm 1 (henceforth called SSONA), on both synthetic and real data sets. The results are organized in the following three sub-sections: in Section 4.1, we present numerical results on synthetic data comparing the performance of SSONA to that of grouping variables ADMM and also for assessing the accuracy in recovering a multi-layered structure in Markov Random Field and covariance graph models that constitute the prime focus in this paper. In Section 4.2 we use the proposed SSONA for feature selection in classification problems involving two real data sets in order to calibrate SSON performance with respect to an independent validation set. Finally, in Section 4.3, we analyze using SSONA on some other interesting real data sets from the social and biological sciences.

4.1 Experimental results for the SSON algorithm on graphical models based on synthetic data

Next, we evaluate the performance of SSONA on ten synthetic graphical model problems, comprising of , 500 and 1000 variables. The underlying network structure corresponds to an Erdős-Rényi model graph, a nearest neighbor graph and a scale-free random graph, respectively. The CONTEST 111CONTEST is available at http://www.mathstat.strath.ac.uk/outreach/contest/ package is used to generate the synthetic graphs, and the UGM 222UGM is available at http://www.di.ens.fr/ mschmidt/Software/UGM.html package to implement Gibbs sampling for estimating the Ising Model. Based on the generated graph topologies, we consider the following settings for generating synthetic data sets:

-

I.

Gaussian graphical models:

For a given number of variables , we first create a symmetric matrix by using CONTEST in a MATLAB environment. Given matrix , we set equal to , where is the smallest eigenvalue of and denotes the identity matrix. We then draw i.i.d. vectors from the gasserian distribution by using the mvnrnd function in MATLAB, and then compute a sample covariance matrix of the variables. -

II.

Gaussian graphical models with latent variables:

For a given number of variables , we first create a matrix by using CONTEST as described in I. We then choose the sub-matrix as the ground truth matrix of the matrix and choseas the ground truth matrix of the low rank matrix . We then draw i.i.d. vectors from the Gaussian distribution , and compute the sample covariance matrix of the variables .

-

III.

The Binary Network:

To generate the parameter matrix , we create an adjacency matrix as in Setup I by using CONTEST. Then, each of observations is generated through Gibbs sampling. We take the first 100000 iterations as our burn-in period, and then collect observations, so that they are nearly independent.

We compare SSONA to the following competing methods:

-

•

CovSel, designed to estimate a sparse Gaussian graphical model (Friedman et al., 2008);

-

•

HGL, focusing on learning a Gaussian graphical model having hub nodes (Tan et al., 2014);

-

•

PGADM, designed to learn a Gaussian graphical model with some latent nodes (Ma et al., 2013);

-

•

Pseudo-Exact, designed to learn a binary Ising graphical model (Höfling and Tibshirani, 2009);

-

•

glasso-SF, Learning Scale Free Networks by reweighted Regularization (Liu and Ihler, 2011);

-

•

GADMM, A two block ADMM method with grouping variables.

All the algorithms have been implemented in the MATLAB R2015b environment on a PC with a 1.8 GHz processor and 6GB RAM memory. Further, all the algorithms are being terminated either when

or the number of iterations and CPU times exceed 1,000 and 10 minutes, respectively.

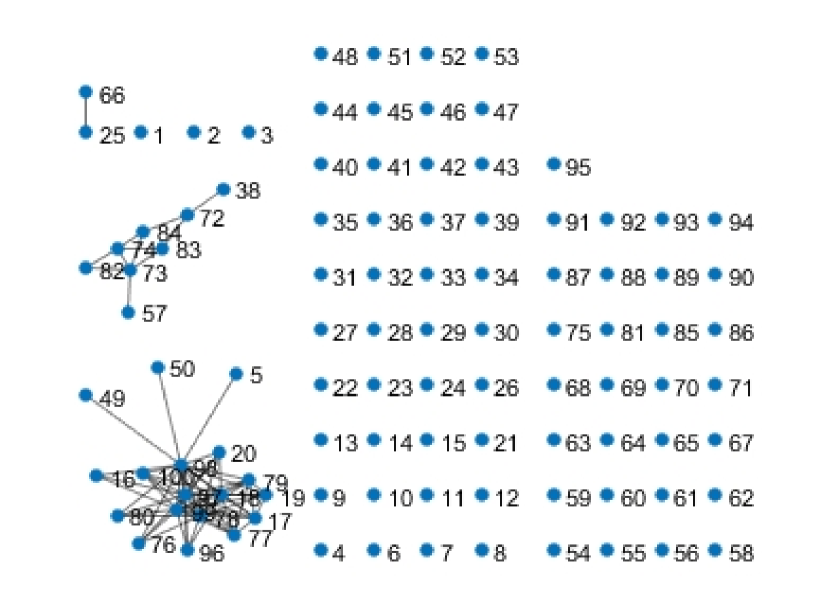

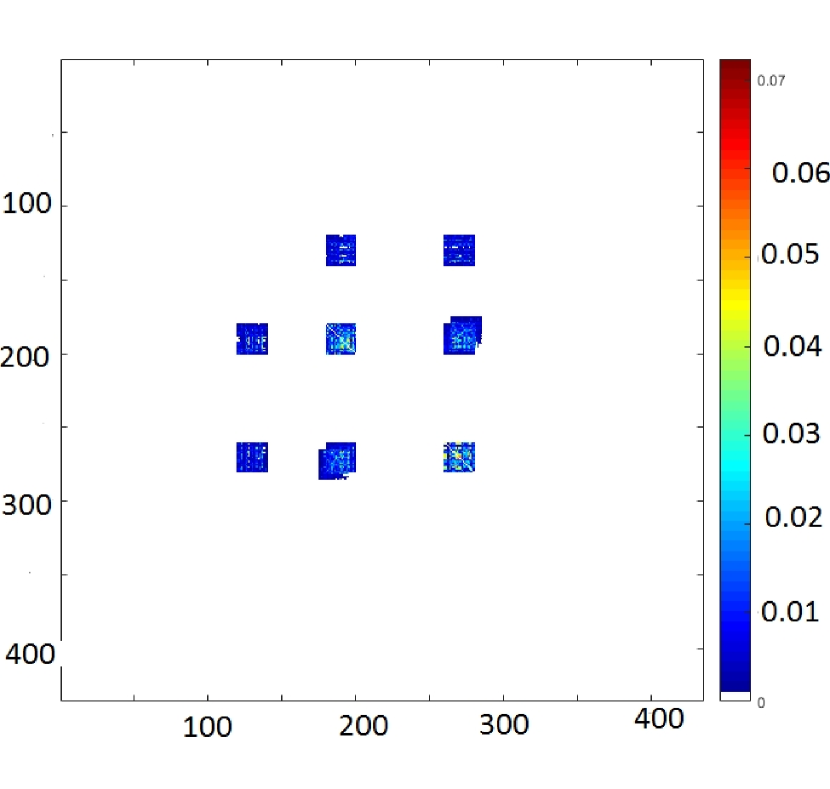

We found that in practice the computation cost for SSONA increases with the size of structured matrices. Therefore, we use a limited memory version of SSONA in our experimental results to obtain good accuracy. Block sizes in Figure 3 could be set based on a desire for interpretability of the resulting estimates. In this section, we choose four structured matrices with blocks of size

where is determined based on size of the adjacency matrix, (see, Figure 3).

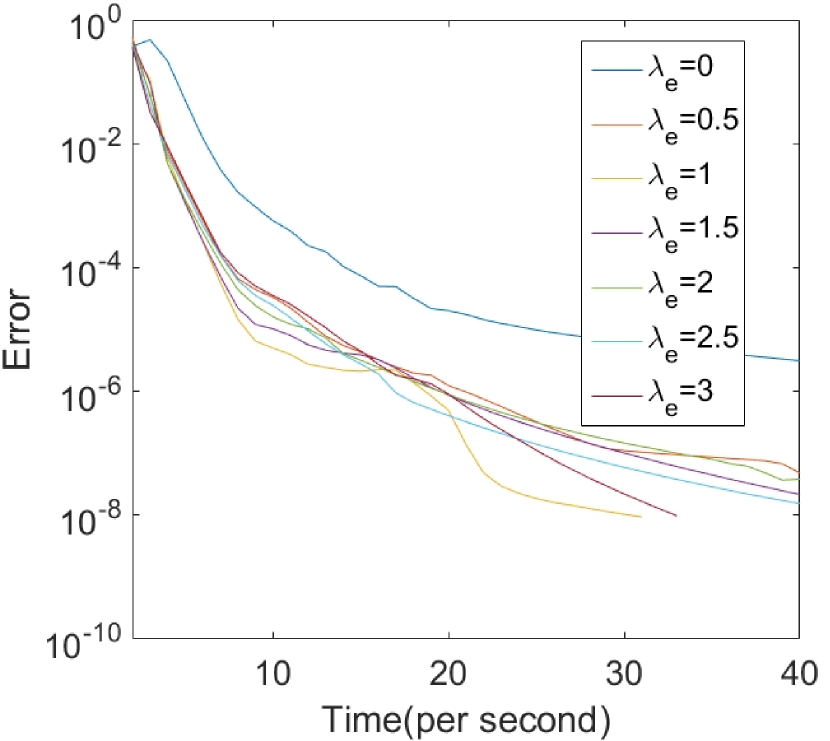

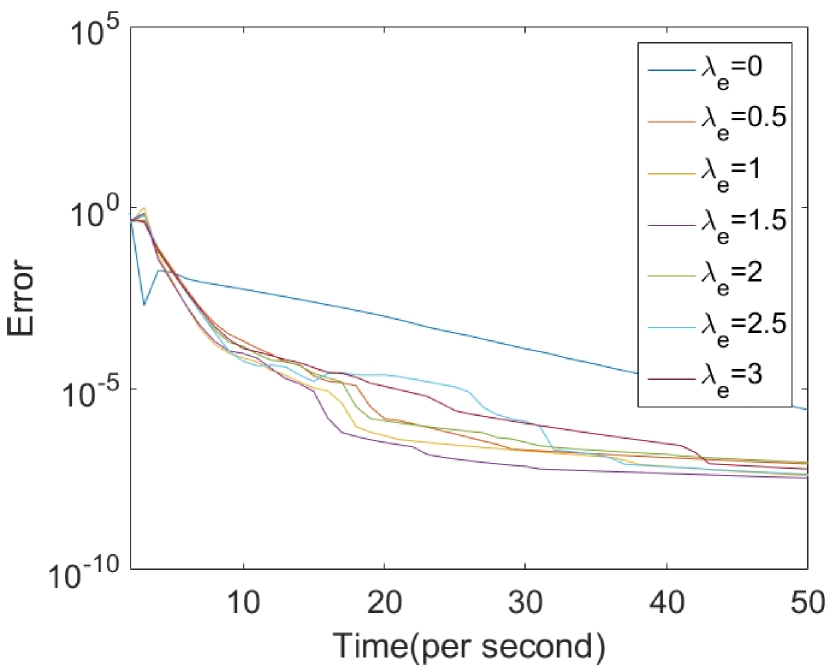

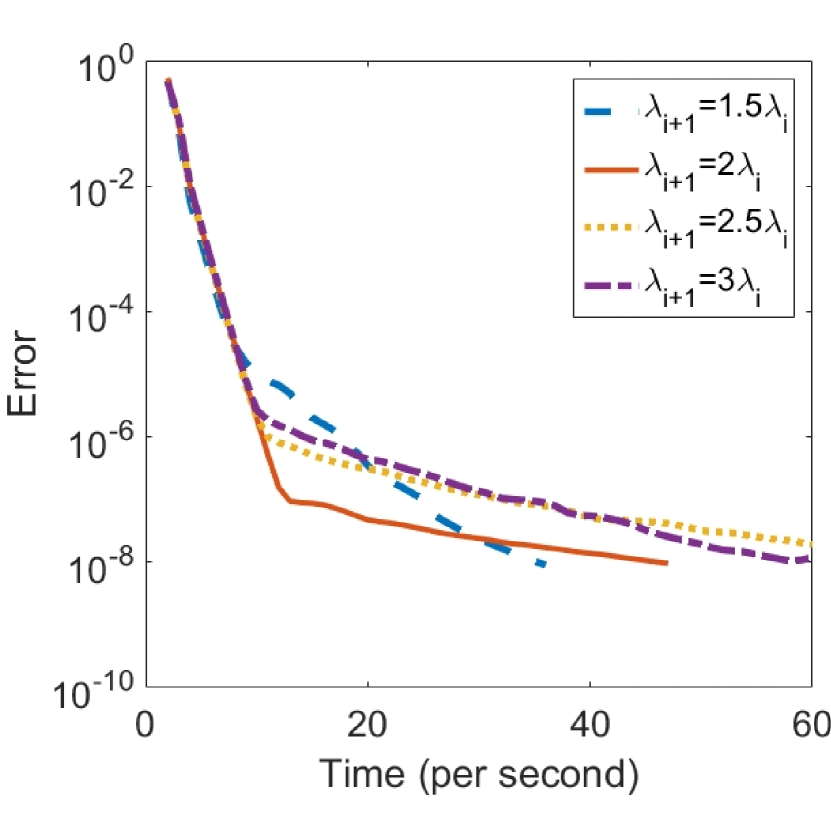

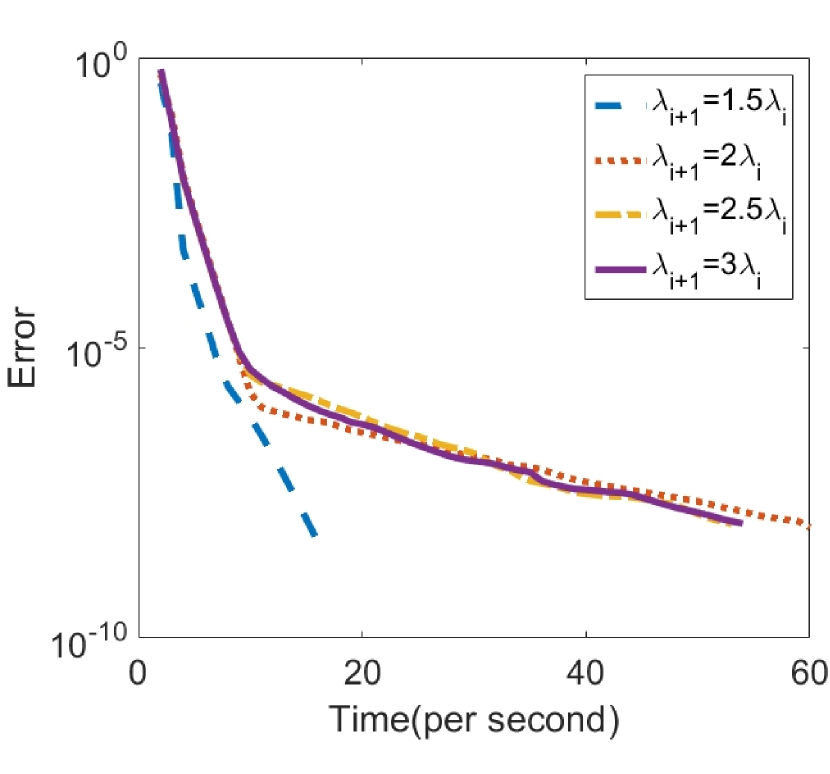

The penalty parameters and play an important rule for the convex decomposition to be successful. We learn them through numerical experimentation (see Figures 5 and 6) and set them respectively to

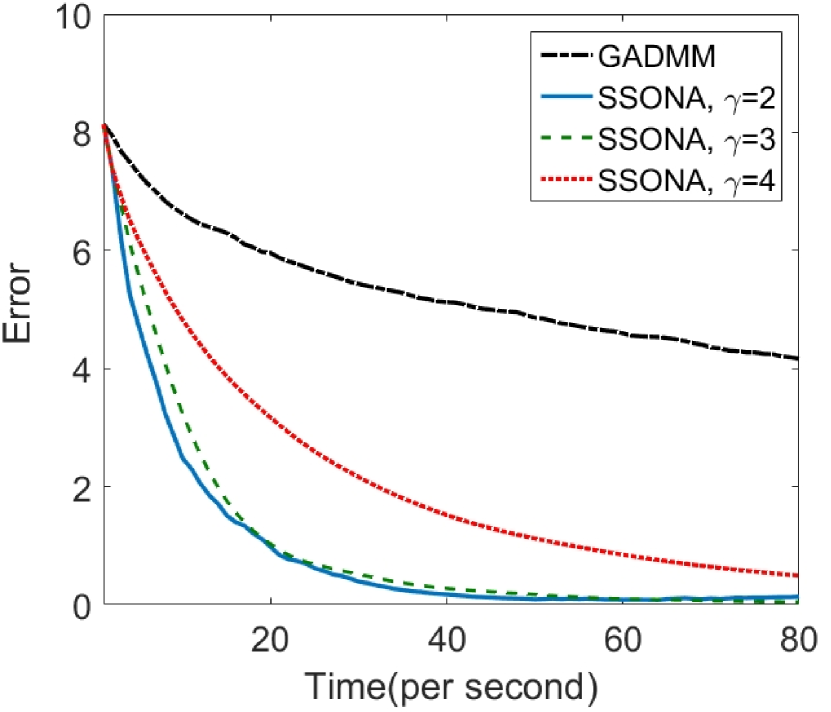

It can be seen from Figure 5 that with the addition of the ridge penalty term the algorithm clearly outperforms its unmodified counterpart in terms of CPU time for any fixed number of iterations. Indeed, when the model becomes more dense, SSONA is more effective to recover the network structure.

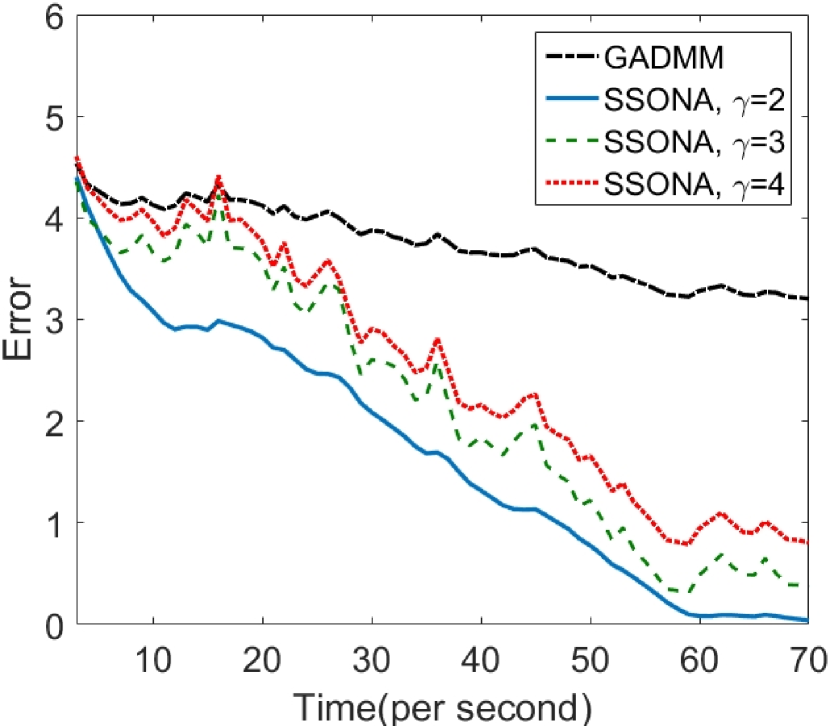

Next, we conduct experiments to assess the performance of the developed multi-block ADMM algorithm (SSONA) vis-a-vis the GADMM for solving two covariance graph estimation problems of dimension 1000 in the presence of noise. Figure 7 depicts the absolute error of the objective function for different choices of the regularization parameter of the augmented Lagrangian and that of the dense noisy component ; note that the latter is key for the convergence of the proposed algorithm.

We define the following two performance measures, as proposed in Tan et al. (2014):

-

•

Number of correctly estimated edges, :

-

•

Sum of squared errors, :

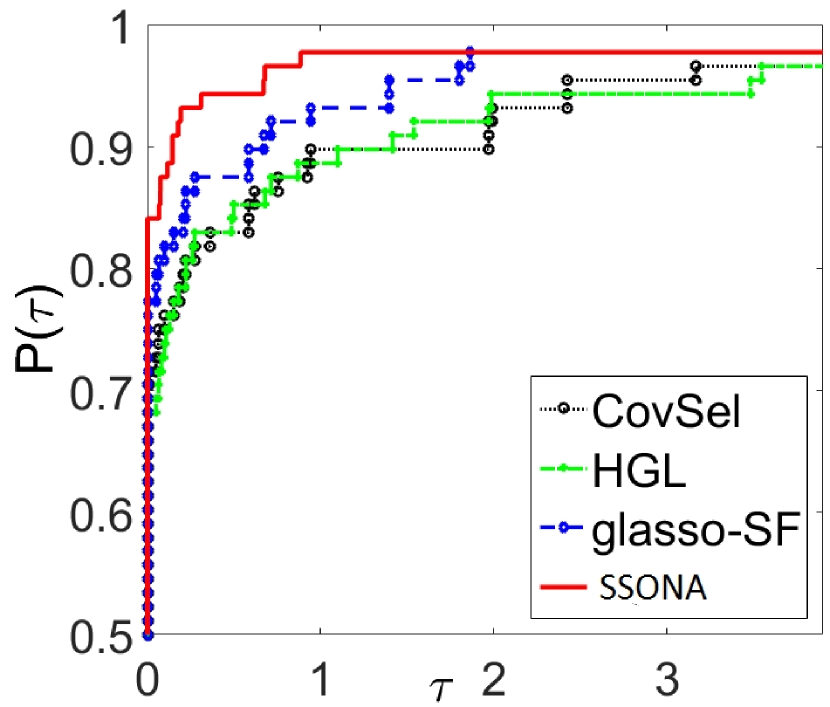

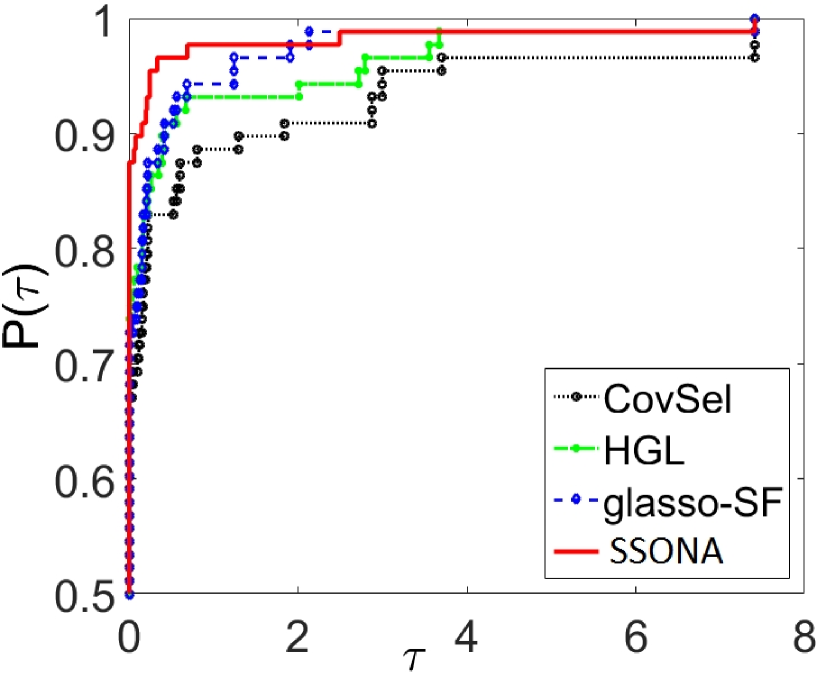

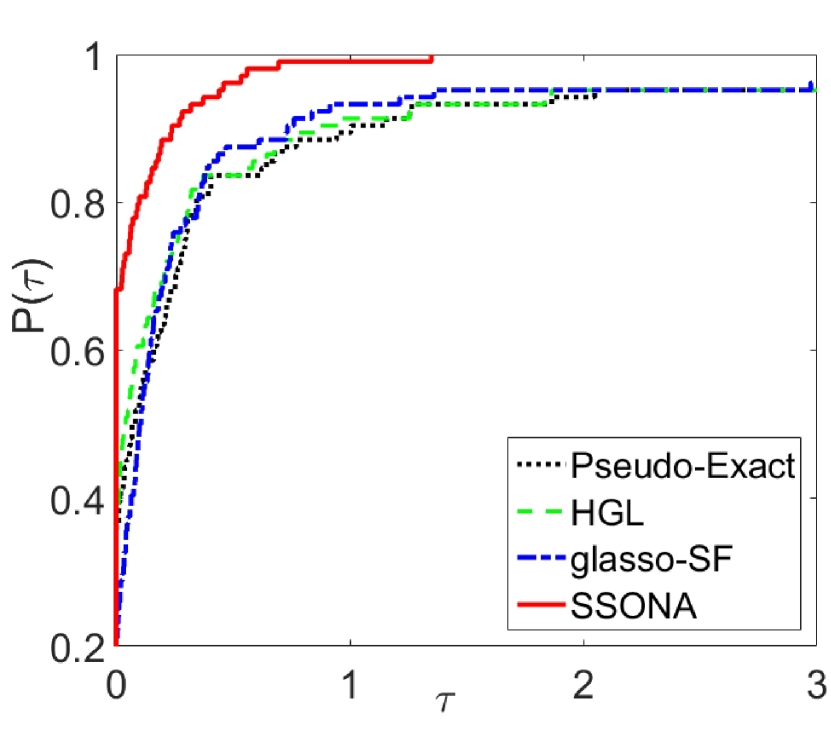

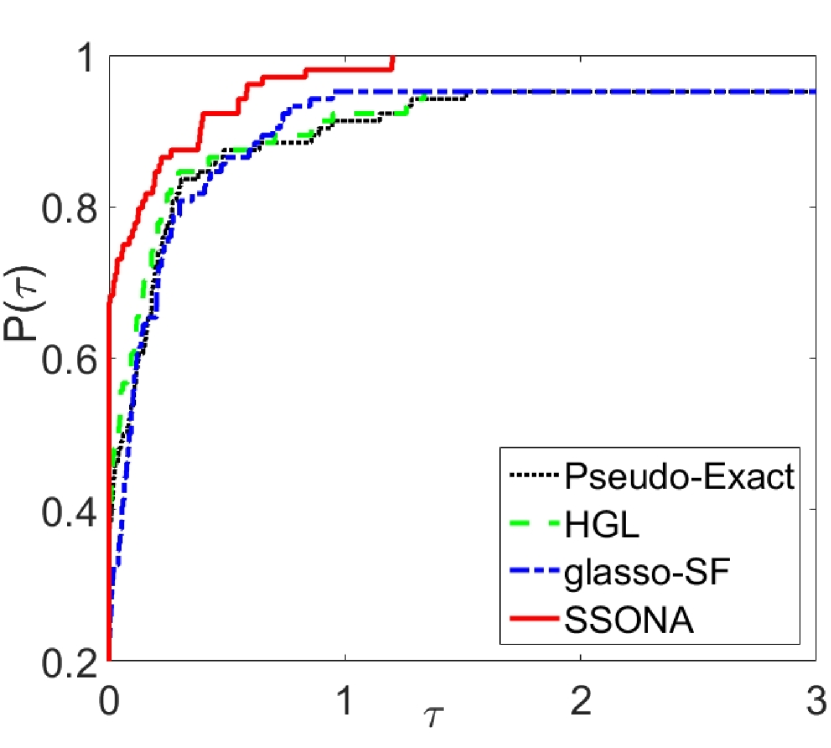

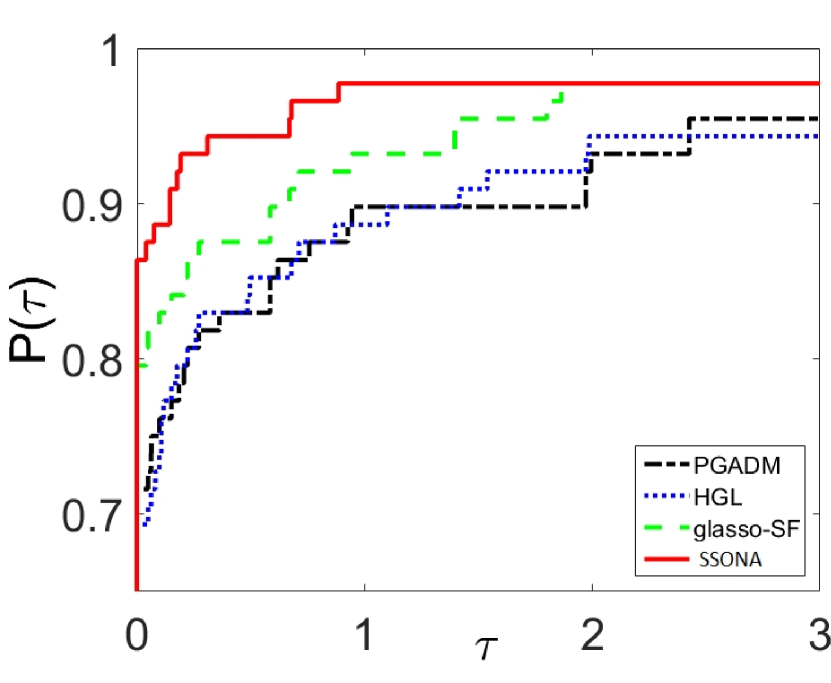

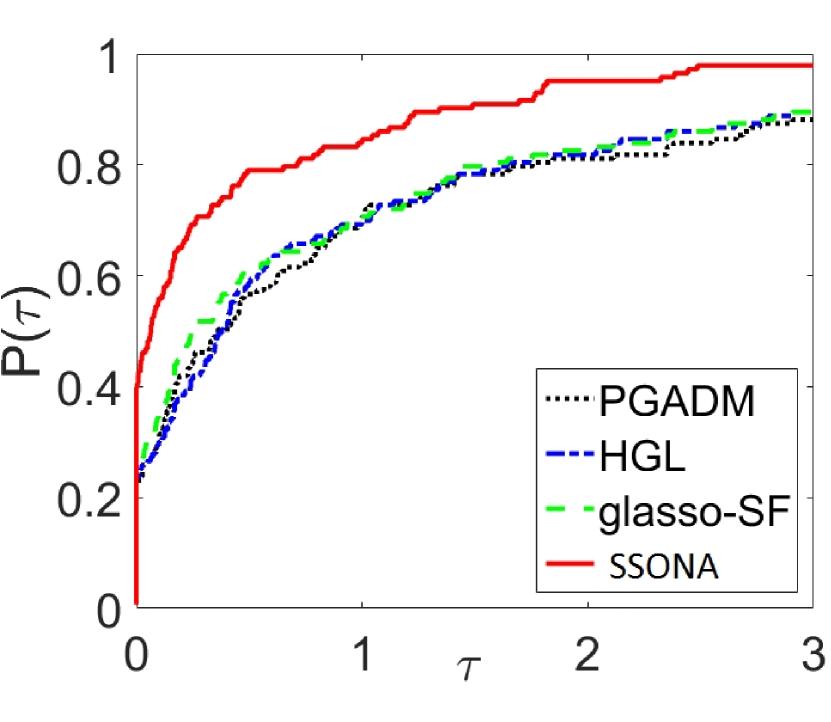

The experiment is repeated ten times and the average number of correctly estimated edges, and sum of squared errors, are considered for comparison. We have used the performance profile, as proposed in Dolan and Moré (2002), to display the efficiency of the algorithms considered, in terms of and . As stated in Dolan and Moré (2002), this profile provides a wealth of information such as solver efficiency, robustness and probability of success in compact form and eliminates the influence of a small number of problems on the evaluating process and the sensitivity of results associated with the ranking of solvers. Indeed, the performance profile plots the fraction of problem instances for which any given method is within a factor of the best solver. The horizontal axis of the figure gives the percentage of the test problems for which a method is efficient, while the vertical axis gives the percentage of the test problems that were successfully solved by each method (robustness). The performance profiles of the considered algorithms in log2 scale are depicted in Figures 8,9 and 10.

Figures 8,9 and 10 show the performance profiles of the considered algorithms for estimation of graphical models in terms of number of correctly estimated edges and sum of squared errors, respectively. The left and right panel are drawn in terms of and , respectively. The results in these figures clearly demonstrate the superior performance of the proposed method, since it solves all test problems without exhibiting any failure. Moreover, the SSONA algorithm is the best algorithm among the considered ones, as it solves more than 80 % of the test problems achieving the maximum number of correctly estimated edge and minimum value of estimation loss Further, the performance index of SSONA grows up rapidly in comparison with the other considered algorithms. The latter implies that whenever SSONA is not the best algorithm, its performance index is close to the index of the best one.

4.1.1 Experiments on structured graphical models

In this section, we present numerical results on structured graphical models to demonstrate the efficiency of SSONA. We compare the behavior of SSONA for a fixed value of with a lasso version of our algorithm. Results provided in Figures 11, 12, 13 and 14 indicate the efficiency of algorithm 1 on structured graphical models. These results also show how the structure of the network returned by the two algorithms changes with growing (note that and are kept fixed for each value of ). It can be easily seen from these figures (comparing Row I and II) that SSONA is less sensitive to the number of samples and shows a better approximation of the network structure even for small sample sizes.

4.2 Classification and clustering accuracy based on SSONA

In this section, we evaluate the efficiency of SSONA on real data sets in recovering complex structured sparsity patterns and subsequently evaluate them on a classification task. The two data sets deal with applications in cancer genomic and document classification.

4.2.1 SSONA for Gene Selection Task

Classification with a sparsity constraint has become a standard tool in applications involving Omics data, due to the large number of available features and the small number of samples. The data set under study considers gene expression profiles of lung cancer tumors. Specifically, the data222 http://www.broadinstitute.org/cgibin/cancer/publications/view/87. consist of gene expression profiles of 12,626 genes for 197 lung tissue samples, with 139 adenocarcinomas(AD), 21 squamous cell carcinomas(SQ), 20 carcinoids (COID) and 17 normal lung tissue (NL). To distinguish lung adenocarcinomas from the normal lung tissues, we consider the diagnosis of lung cancer as a binary classification problem. Let the 17 normal lung comprise the positive class and the 139 lung adenocarcinomas the negative class. Following the workflow in Monti et al. (2003), we reserve the 1000 most significant genes after a preprocessing step. In the numerical experiment, we compare group lasso (Yuan and Lin, 2007), group lasso with overlap (Obozinski et al., 2011) and SSONA according to the following two criteria: average classification accuracy and gene selection performance. The experiment is repeated ten times and the average accuracy and performance are depicted in Table 1.

| Method | Average classification accuracy | Average number of genes selected |

|---|---|---|

| Group lasso (Yuan and Lin, 2007) | 0.815(0.046) | 69.11(3.23) |

| Group lasso with overlap (Obozinski et al., 2011) | 0.834(0.035) | 57.30(2.71) |

| SSONA (4 structured matrices) | 0.807(0.028) | 61.44(2.80) |

| SSONA (6 structured matrices) | 0.839(0.022) | 56.111(2.100) |

As is shown in Table 1, SSONA achieves higher classification accuracy than the group lasso and lower classification accuracy than the latent group lasso, although the performance of all three methods is very similar and within the variability induced by the replicates. However, our SSON based lasso does not require a priori knowledge of group structures, which is a prerequisite for the other two methods. One can easily improve the the classification accuracy and gene selection performance of SSONA by adding more structured matrices.

In our experiments, SSONA selects the least number of genes and achieves the smallest standard deviation of average number of genes without any priori knowledge. Due to the different number of randomly selected genes, the average number of gene sometimes will be a non-integer.

4.2.2 SSONA for Document Classification Task

The next example involves a data set 333http://qwone.com/jason/ 20Newsgroups/ containing 1427 documents with a corpus of size 17785 words. We randomly partition the data into 999 training, 214 validation and 214 test examples, corresponding to a 70/15/15 split (Rao et al., 2016). We first train a Latent Dirichlet Allocation based topics model (Blei et al., 2003) to assign the words to 100 ”topics”. These correspond to our groups, and since a single word can be assigned to multiple topics, the groups overlap. We then train a lasso logistic model using as outcome variable indicating whether the document discusses atheism or not , together with an overlapping group lasso and a SSON based lasso model where the tuning parameters are selected based on cross validation. Table 2 shows that the variants of the SSON yield almost the same misclassification rate compared to the other two methods, while it does not require a priori knowledge of group structures.

| Method | Misclassification Rate |

|---|---|

| Group lasso (Yuan and Lin, 2007) | 0.445 |

| Group lasso with overlap (Obozinski et al., 2011) | 0.390 |

| SSONA (5 structured matrices) | 0.435 |

| SSONA (6 structured matrices) | 0.421 |

| SSONA (7 structured matrices) | 0.401 |

4.2.3 SSONA for structured subspace clustering

Our last example focuses on data clustering. The data come from multiple low-dimensional linear or affine subspaces embedded in a high-dimensional space. Our method is based on (2.4), wherein each point in a union of subspaces has a representation with respect to a dictionary formed by all other data points. In general, finding such a representation is NP hard. We apply our subspace clustering algorithm to a structured data in the presence of noise. The segmentation of the data is obtained by applying SSONA to the adjacency matrix built from the data. Our method can handle noise and missing data and is effective to detect the clusters.

Figure 15 shows that our approach significantly outperforms state-of-the-art methods.

4.3 Application to real data sets

Next, we use the SSON framework to analyze three data sets from molecular and social science domains. Although there is no known ground truth, the proposed framework recovers interesting patterns and highly interpretable structures.

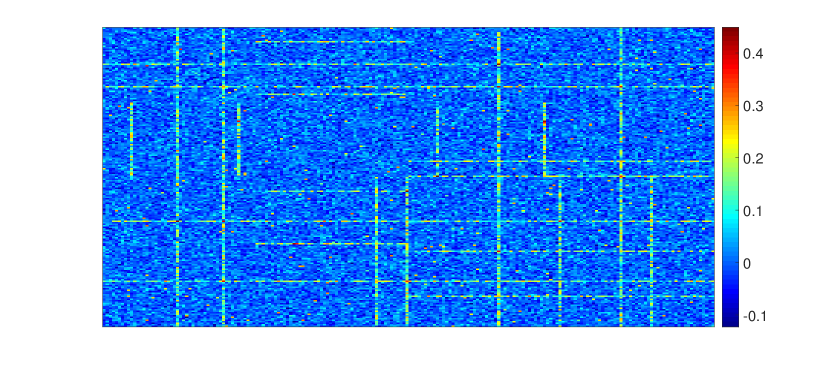

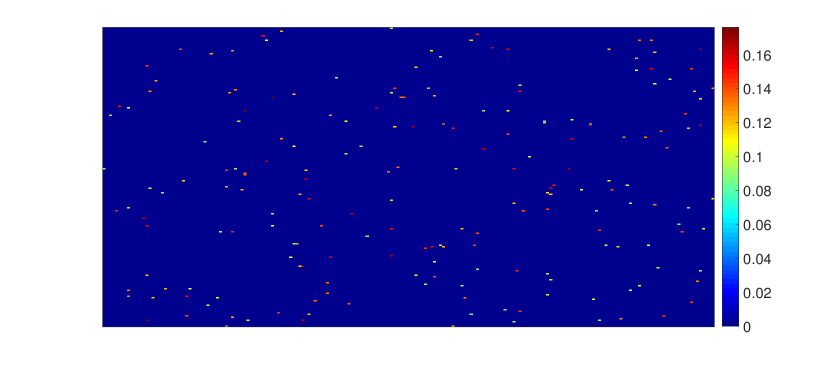

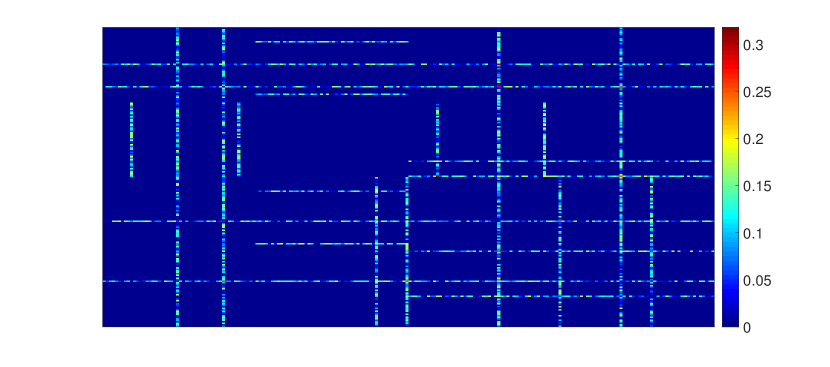

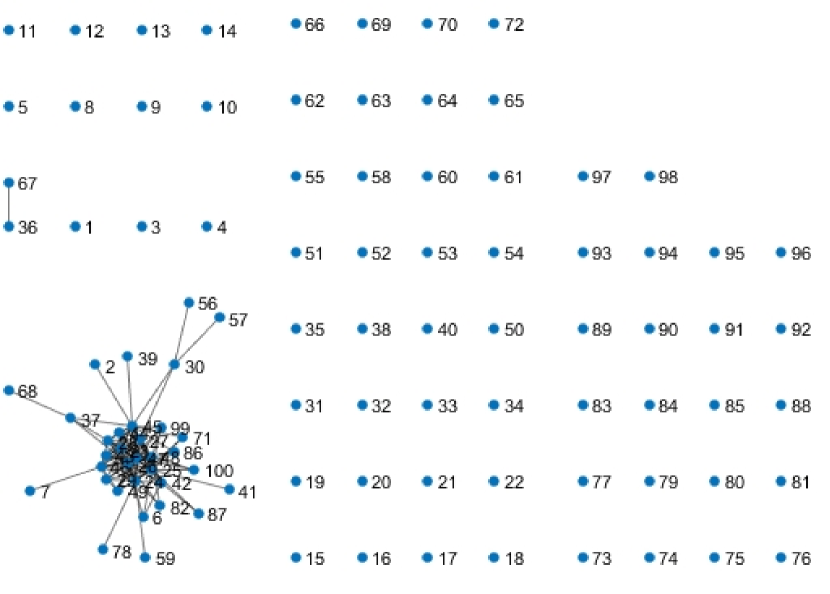

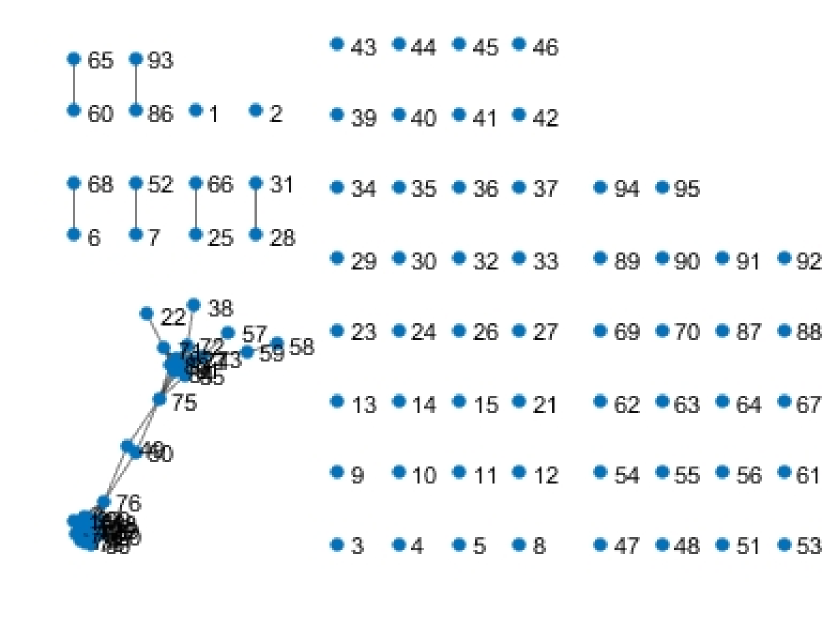

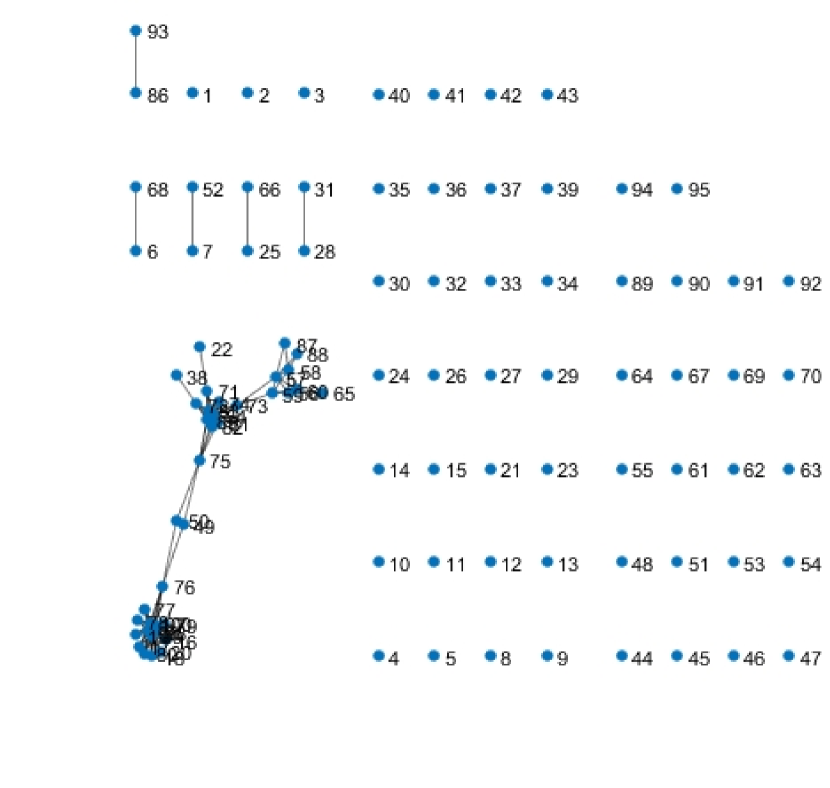

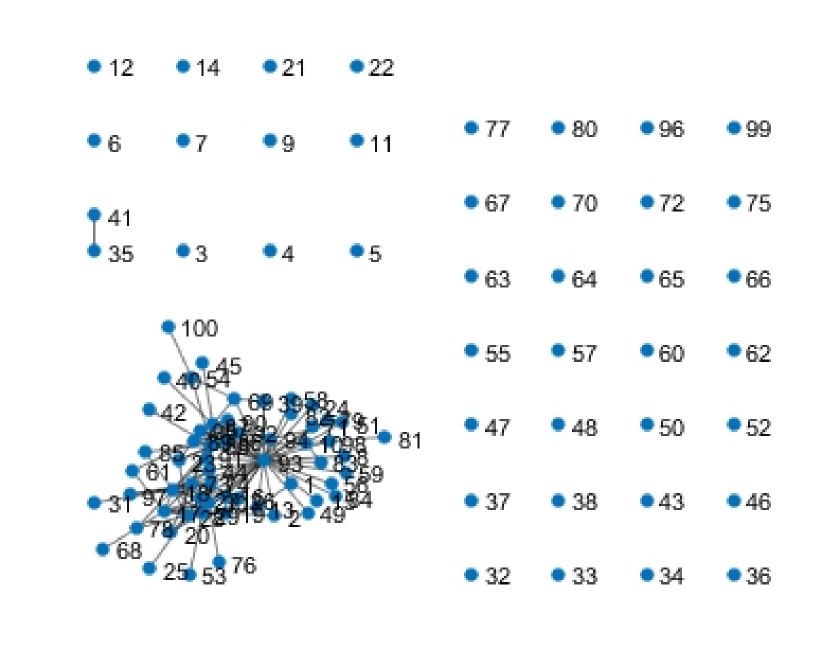

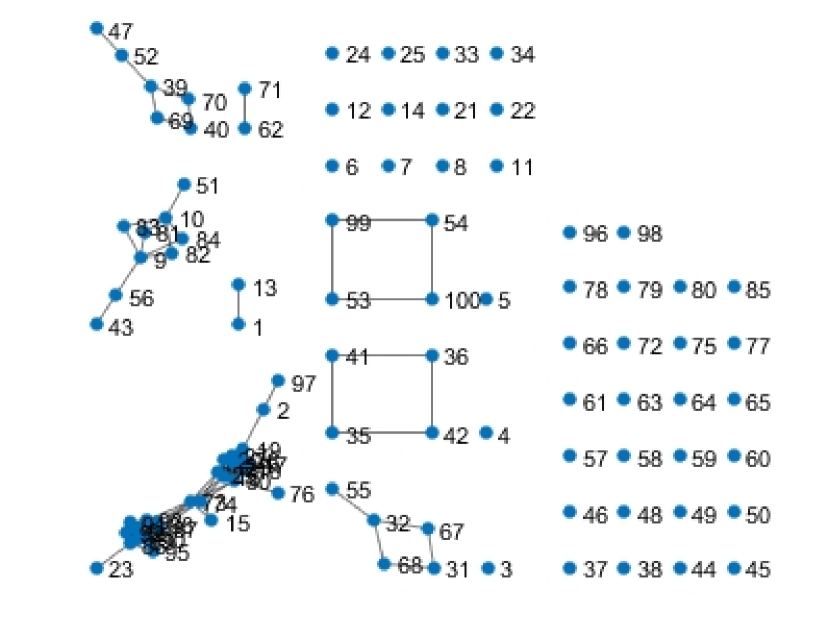

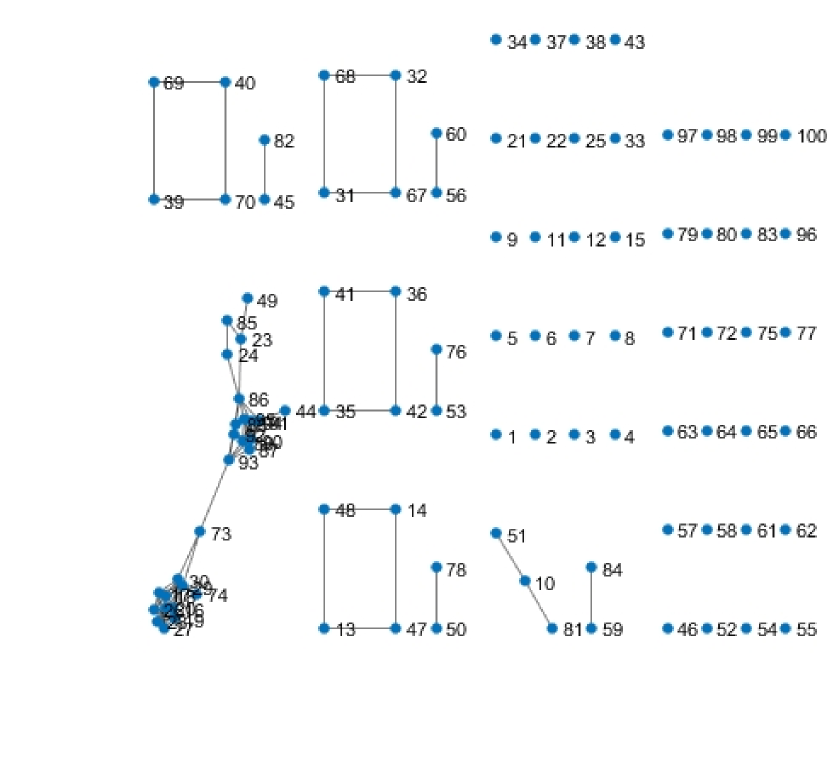

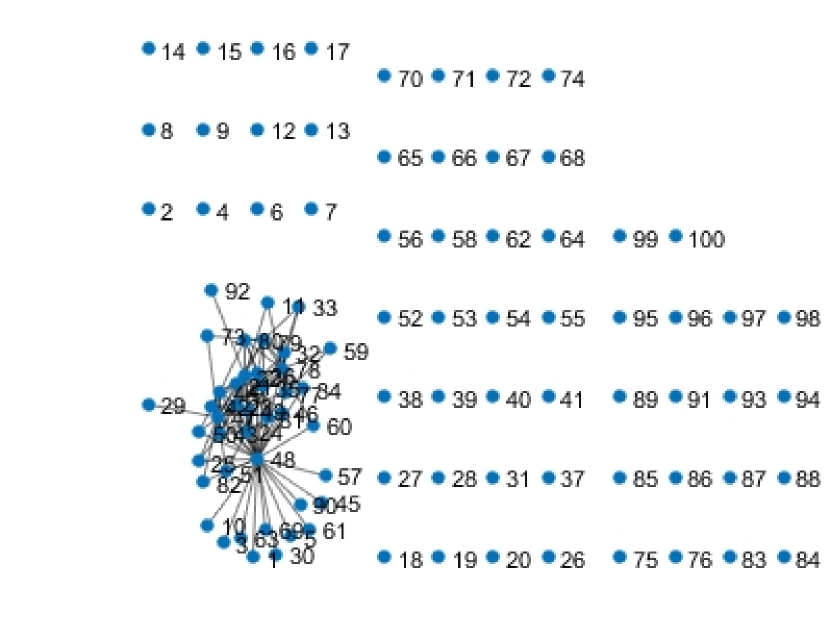

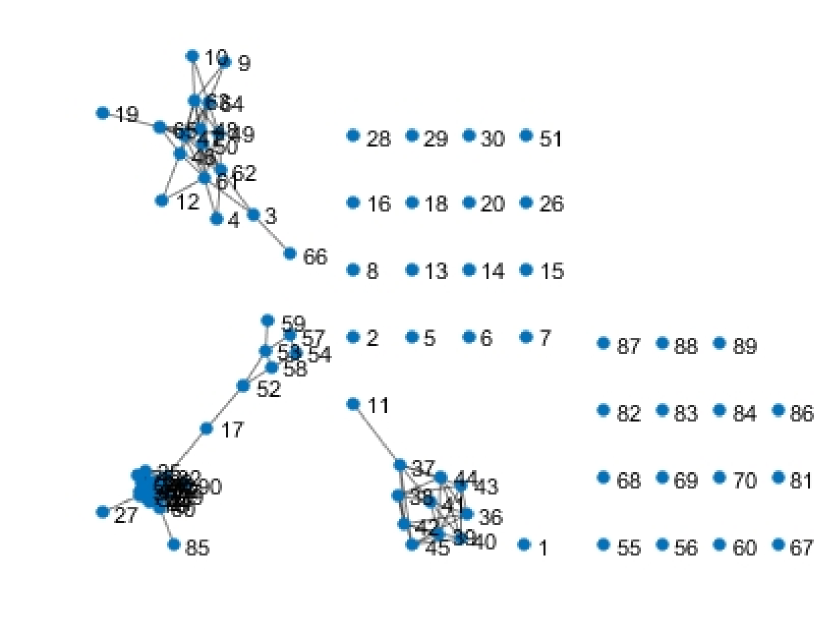

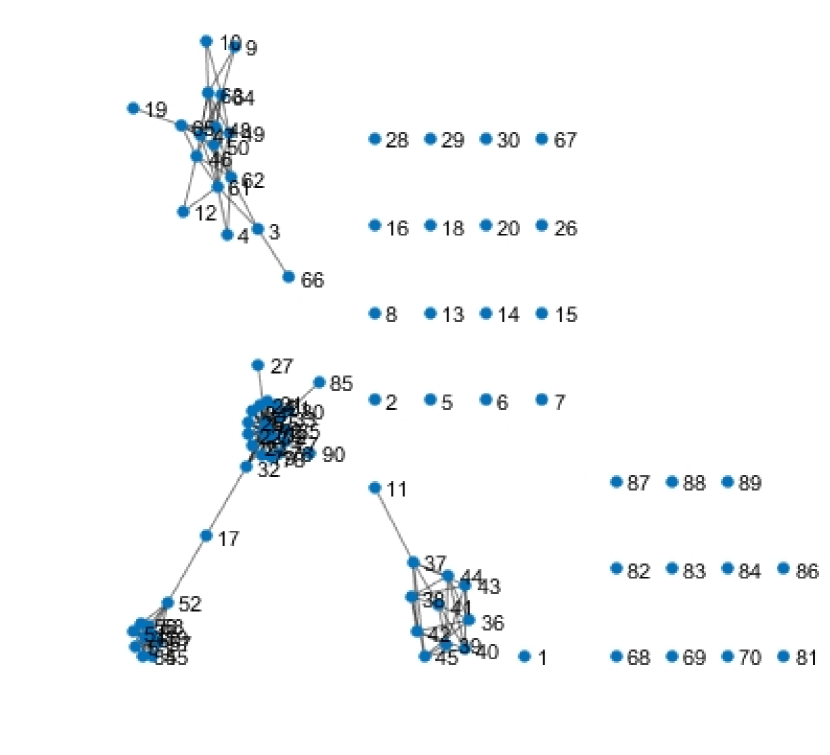

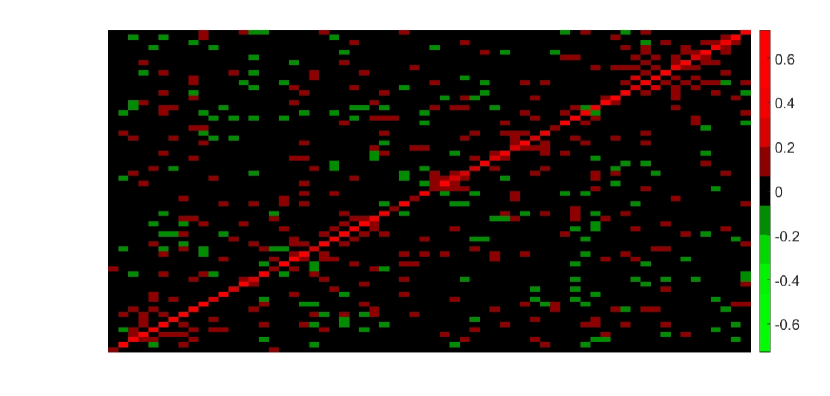

Analysis of connectivity in the financial sector.

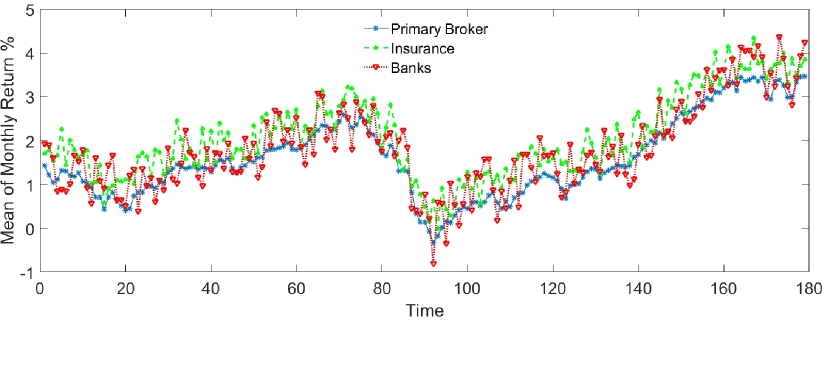

We applied the SSON methodology to analyze connectivity in the financial sector. We use monthly stock returns data from August, 2001 to July, 2016 for three financial sectors, namely banks (BA), primary broker/dealers (PB), and insurance companies (INS). The data are obtained from the University of Chicago’s Center for Research in Security Prices database (CRSP).

Our final sample covers 75 different institutions spanning a 16-year period. Figure 16 shows the mean (in %) of monthly stock returns across different sectors in each 3-year long rolling windows. As expected, the average returns are significantly lower during the financial 2007-2009 crisis period, compared to any other period in our sample. Indeed, looking across the sectors, all three sectors experienced diminished performance during the 2007-2009 crisis. Further, the almost linear ramp-up following 2009 clearly captures the recovery of financial stocks and the broader market.

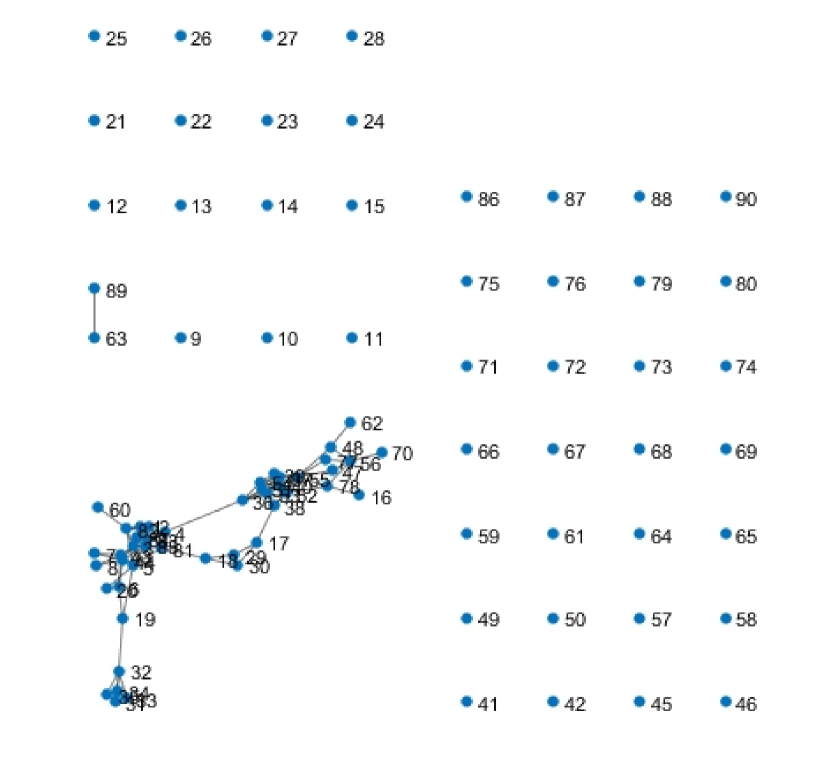

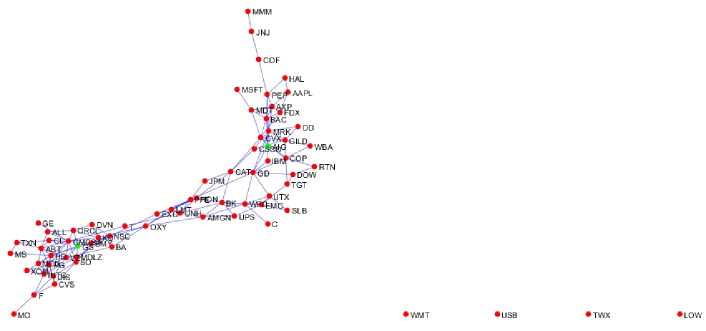

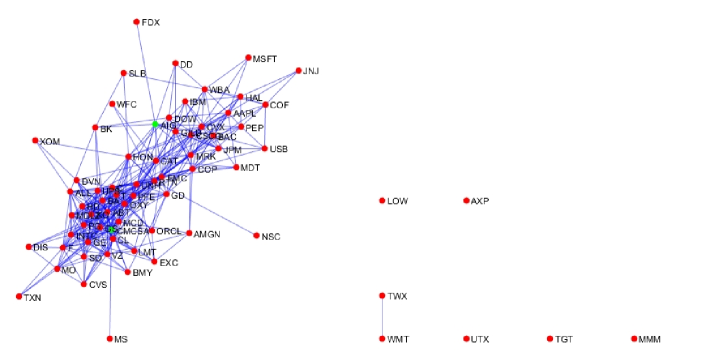

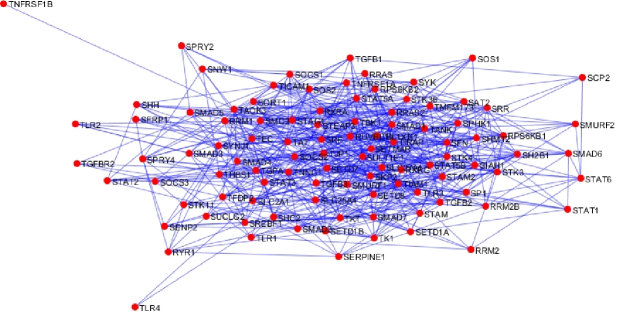

Next, we estimate a measure of network connectivity for a sample of the 71 components of the SP100 index that were present during the entire 2001-16 period under consideration. Figure 17 depicts the network estimates of the transition (lead-lag) matrices using straight lasso VAR and SSONA based VAR for the January 2007 to Oct 2009 period. It can be seen that the lasso VAR estimates produce a more highly connected network, while the SSONA ones identify two more connected components. Both methods highlight the key role played by AIG and GS (Goldman Sachs), but the SSONA based network indicates that one dense connected component is centered around the former, while the other dense connected component around the latter. In summary, both methods capture the main connectivity patterns during the crisis period, but SSONA provides a more nuanced picture.

US House voting data set.

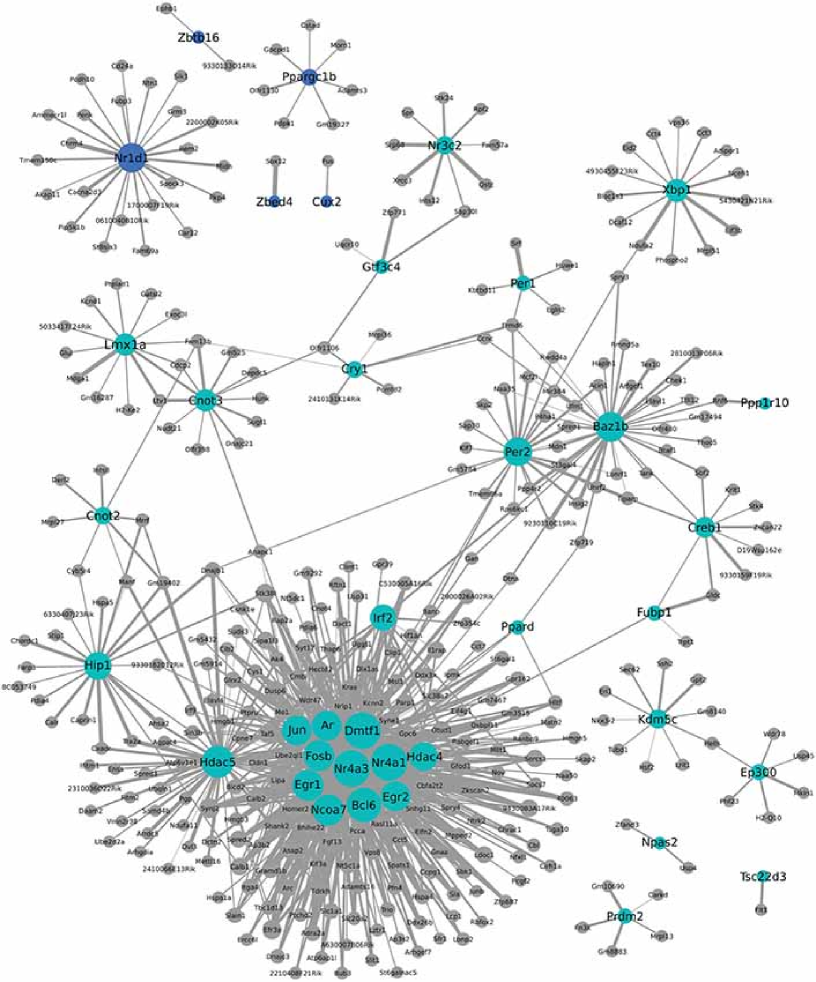

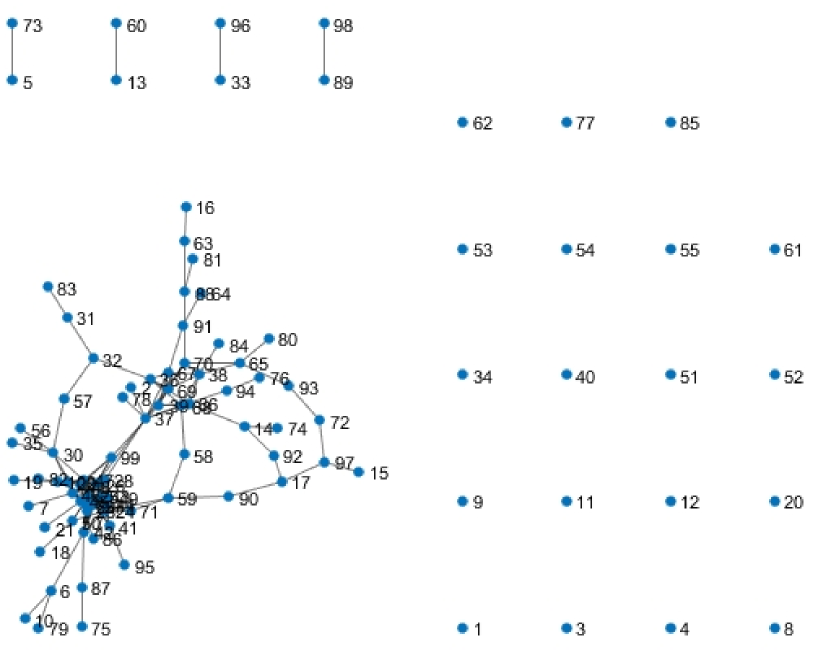

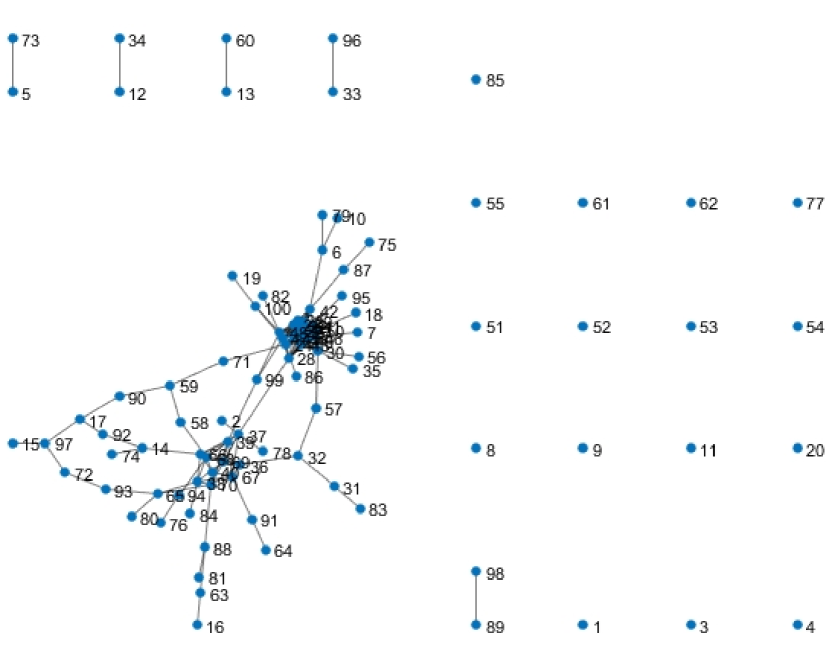

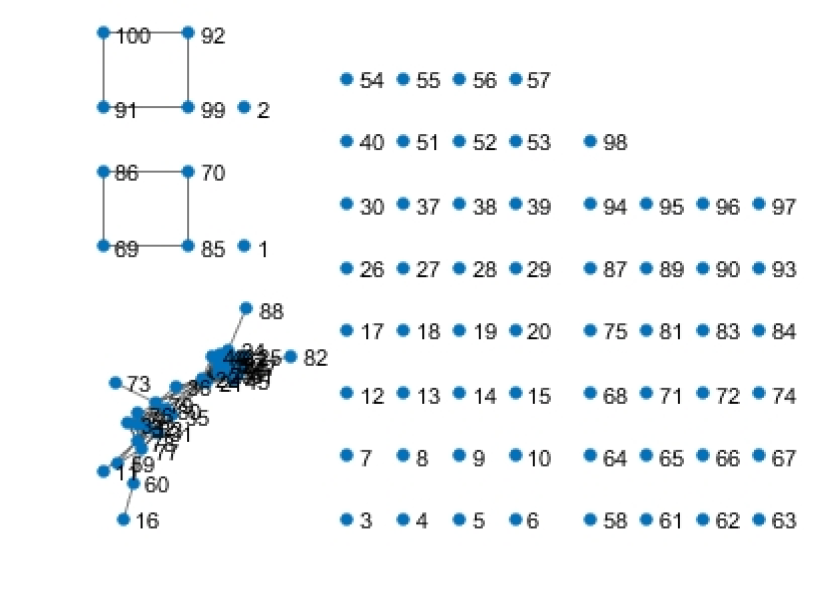

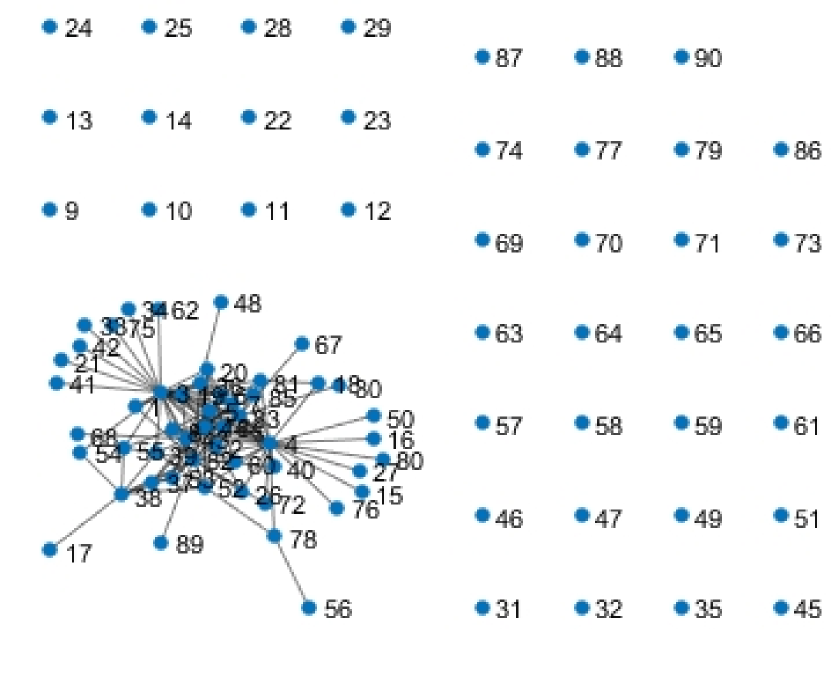

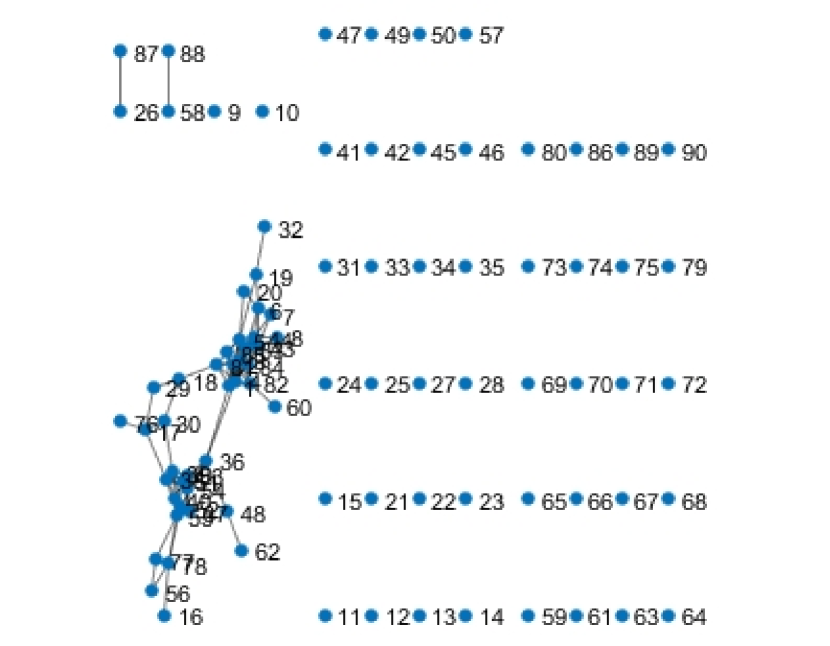

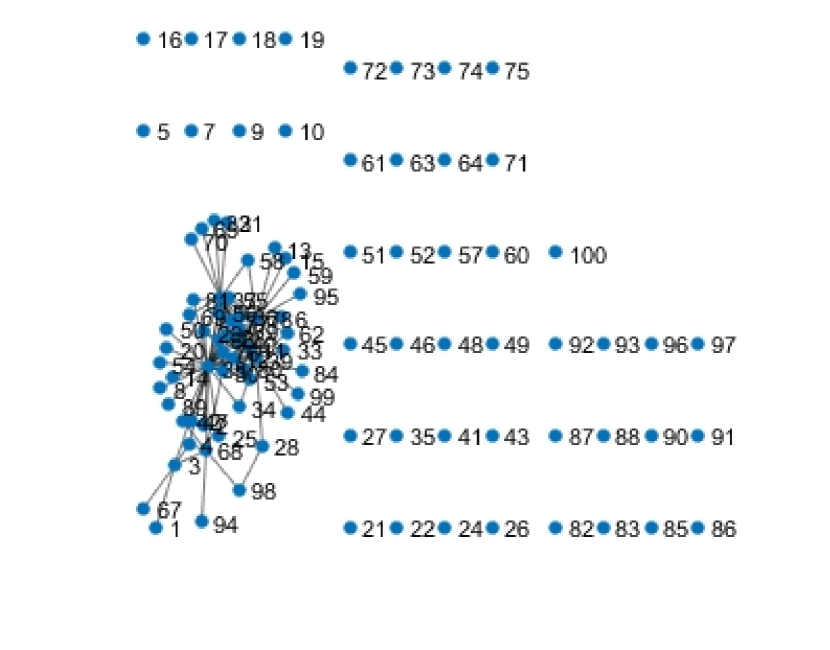

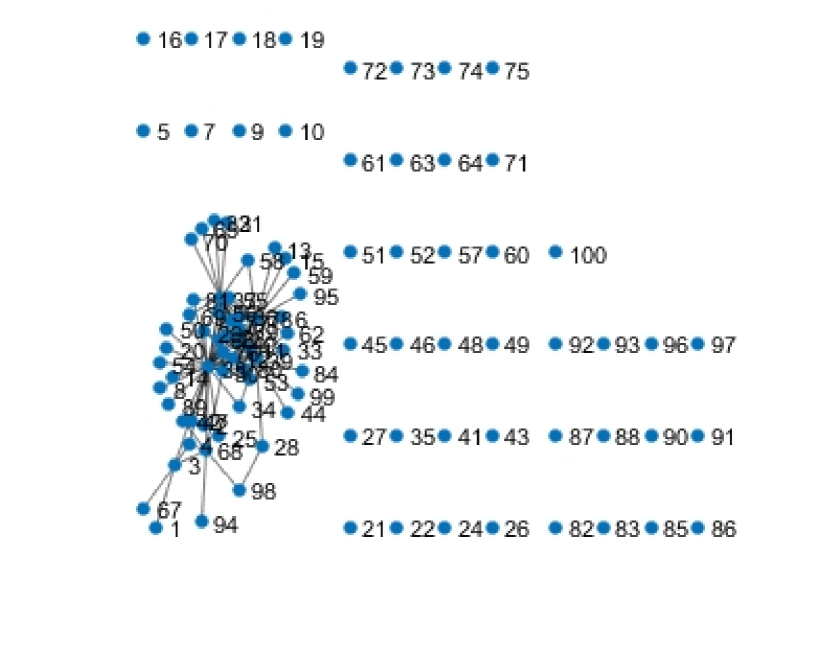

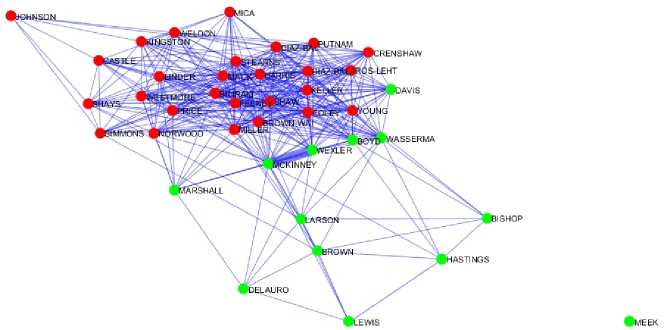

We applied SSONA to describe the relationships amongst House Representatives in the U.S. Congress during the 2005-2006 period (109th Congress). The variables correspond to the 435 representatives, and the observations to the 1210 votes that the House deliberated and voted on during that period, which include bills, resolutions, motions, debates and roll call votes. The assumption of our model is that bills are i.i.d. sample from the same underlying Ising model. The votes are recorded as ”yes” (encoded as ”1”) and ”no” (encoded as ”0”). Missing observations were replaced with the majority vote of the House member’s party on that particular vote.

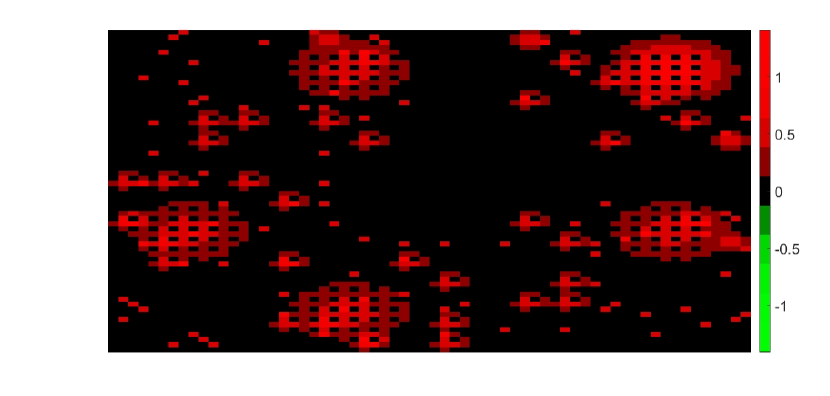

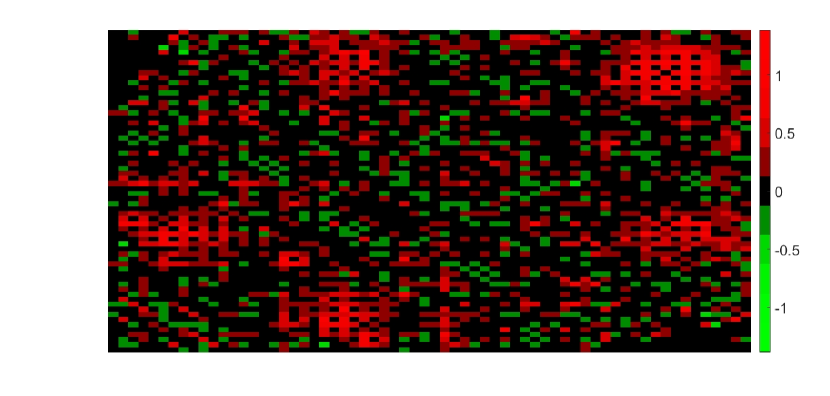

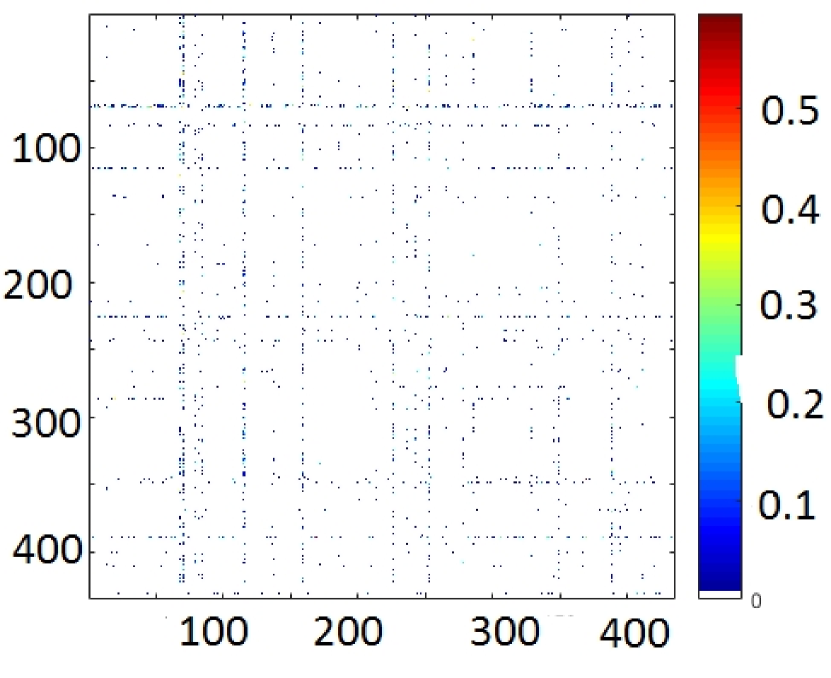

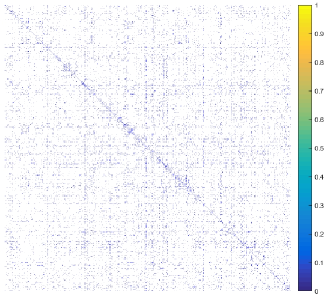

Following Guo et al. (2015), we used a bootstrap procedure with the proposed SSONA estimator to evaluate the confidence of the estimated edges. Specifically, we estimated the network for multiple bootstrap samples of the same size, and only retained the edges that appeared more that percent of the time. The goal of the analysis is to understand the type of relationships that existed among the House members in the 109th Congress. In particular, we wish to identify and interpret the presence of densely connected components, as well of sparse components. The heatmap of the adjacency matrix of the estimated network by using SSONA is depicted in Figure 18.

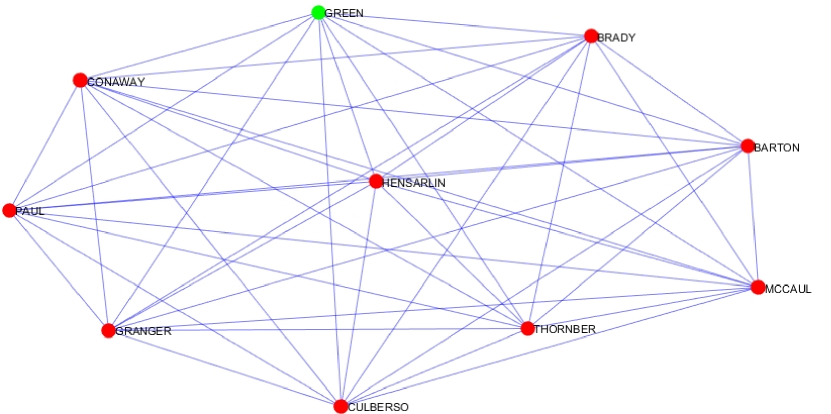

It can be easily seen that there exist densely connected components in the network, a fact that the glasso algorithm (Friedman et al., 2008) fails to recover (see, Figure 19).

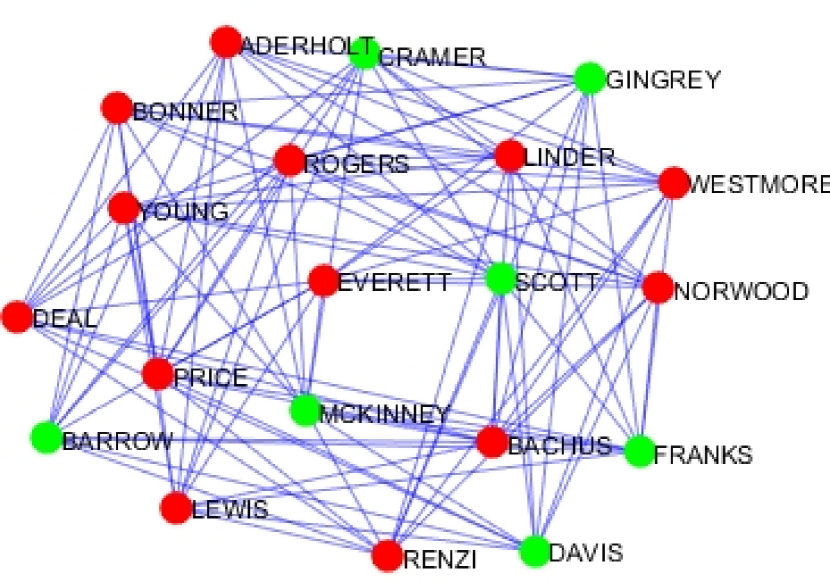

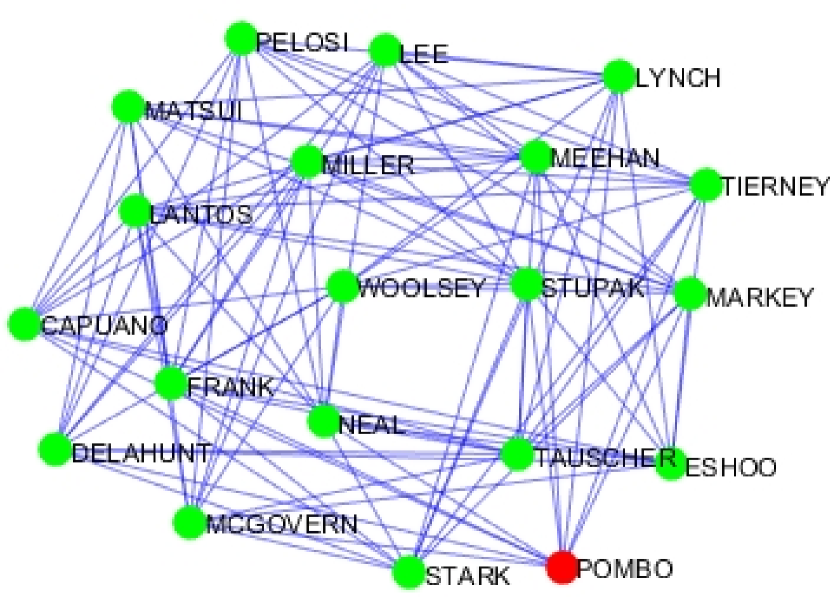

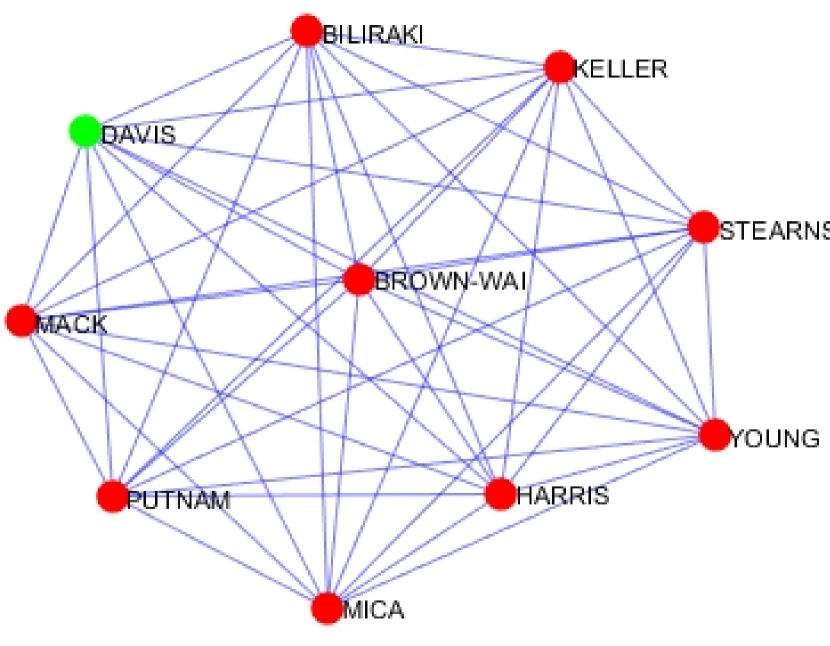

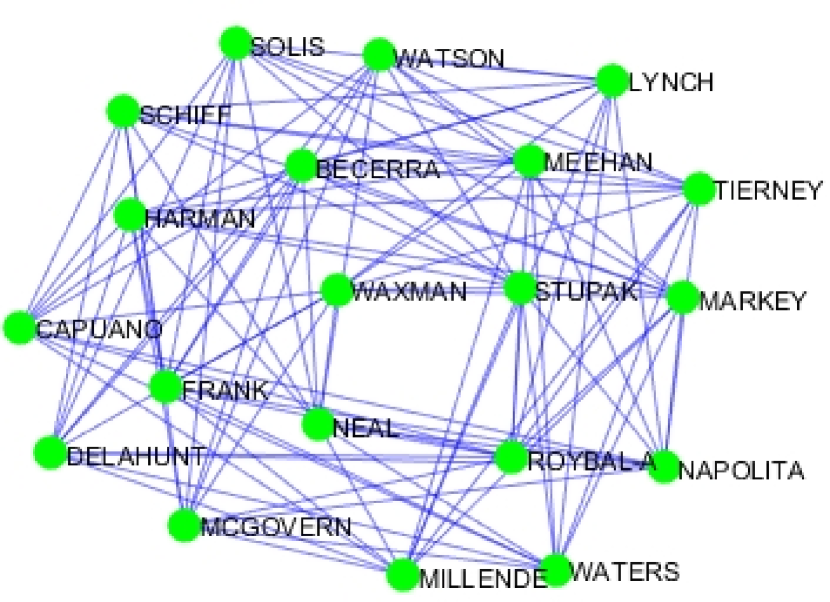

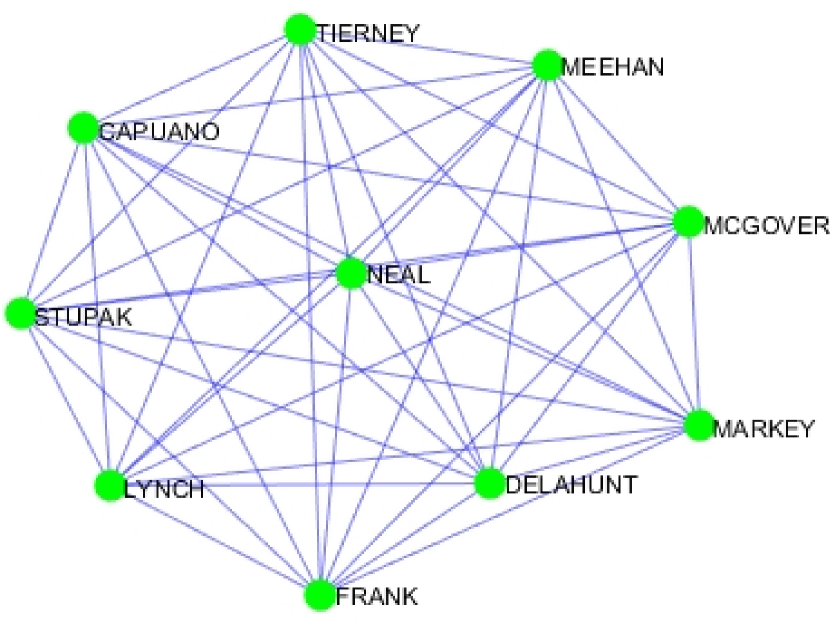

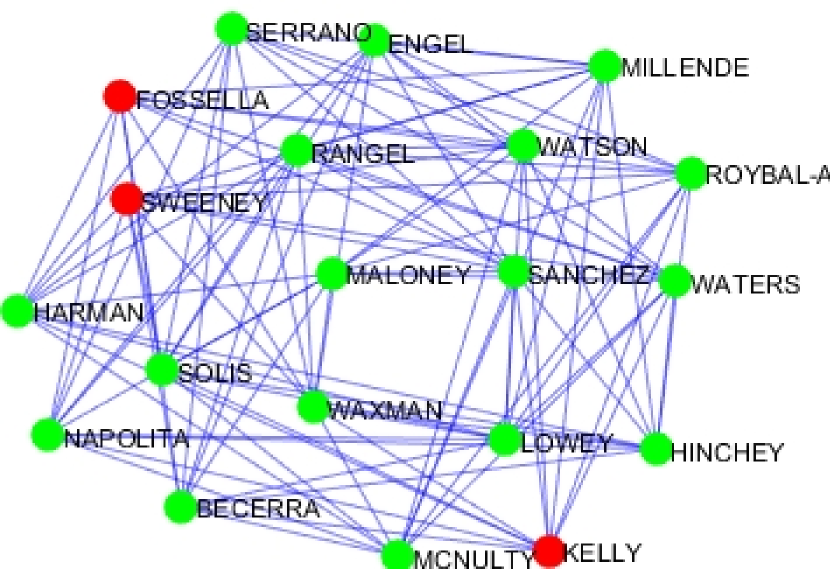

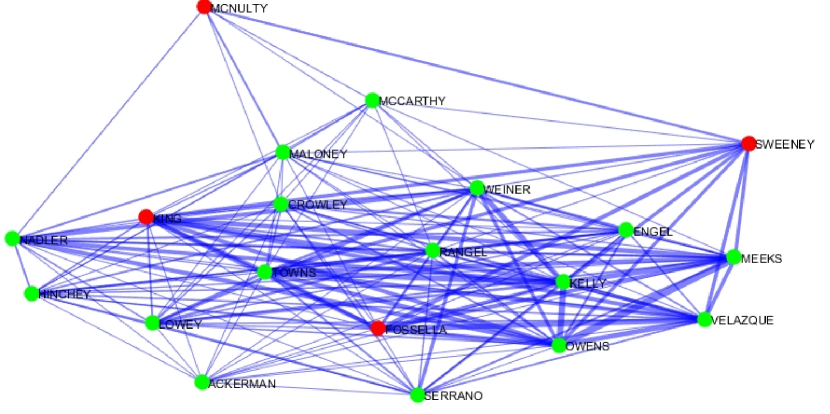

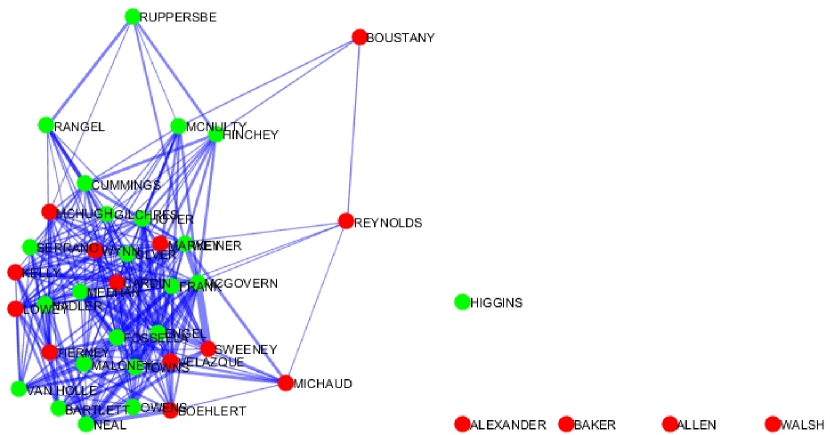

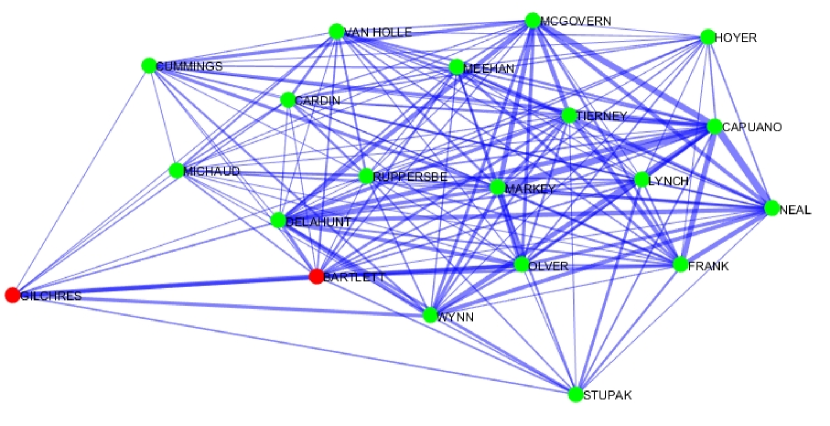

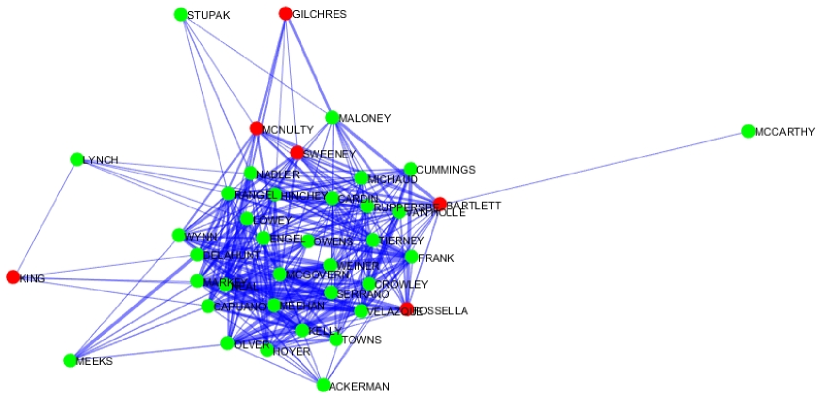

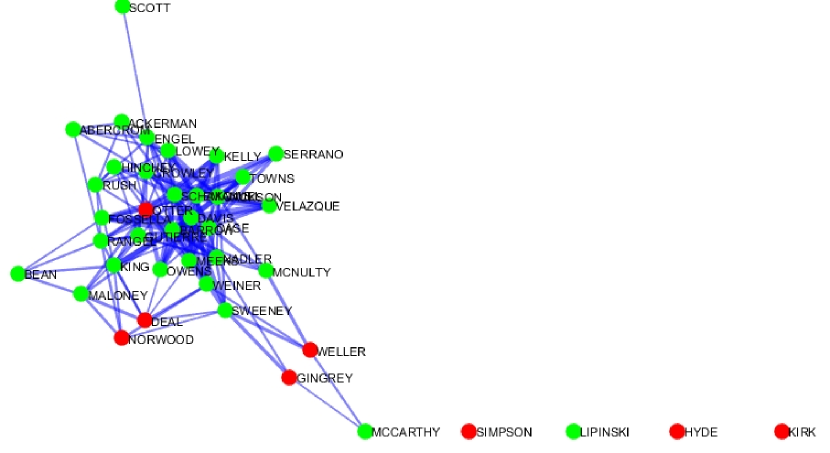

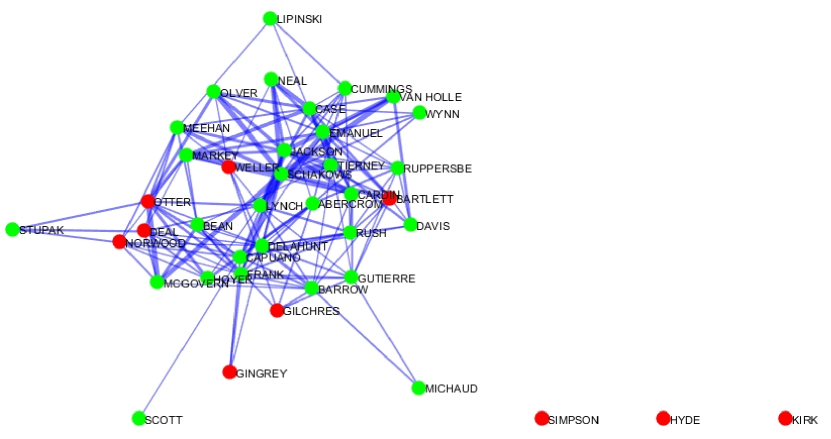

The network representation of subgraphs, with a cut-off value of 0.6, is given in Figures 20, 21 and 22. We only plot the edges associated with the subgraphs to enhance the visual reading of densely correlated areas. An interesting result of applying SSONA on this data set is the clear separation between members of the Democratic and Republican parties, as expected (see, Figures 20, 21 and 22). Moreover, voting relationships within the two parties exhibit a clustering structure, which a closer inspection of the votes and subsequent analysis showed was mainly driven by the position of the House member on the ideological/political spectrum.

Other interesting patterns emerging from the analysis is that SSONA recovers members of opposite parties as a sparse component in each subgraph (see, Figures 20, 21 and 22). For instance, Figure 21 shows that Republican members such as Simpson, Kirk and Hyde are sparsely connected in a clustered group of Democratic members. This is possibly due to the overall centrist record of Kirk and alignment of Hyde and Simpson on selected issues. Similarly, Figure 21 indicates that Democratic members Bishop, Hastings and Meek are approximately sparsely connected to a subgraph of Republican members. Bishop from Georgia has compiled a fairly conservative voting record. The same conclusion can be derived from Figure 21. Indeed, Figures 20, 21 and 22 reveals that there are strong positive associations between members of the same party and negative associations between members of opposite parties. Obviously, at the higher cutoff value the dependence structure between members of opposite parties becomes sparser.

Other patterns of interest include a strong dependence between members of two opposite parties in selected subgraphs when the members come from the same state, as is the case for New York state members Jerrold Nadler (D), Anthony D. Weiner (D), Ed Towns (D), Major Owens (D), Nydia Velázquez (D), Vito Fossella (R), Carolyn B. Maloney (D), Charles B. Rangel (D), José Serrano (D), Eliot L. Engel (D), Nita Lowey (D), Sue W. Kelly (R), John E. Sweeney (R), Michael R. McNulty (D), Maurice Hinchey (D), John M. McHugh (R), Sherwood Boehlert (R), Jim Walsh (R), Tom Reynolds (R), Brian Higgins (D) -see Figure 21. However, in this instance, there is also a cluster of positive associations between Democrats.

In summary, SSONA provides deeper insights into relationships between House members, going beyond the obvious separation into two parties, according to their voting record.

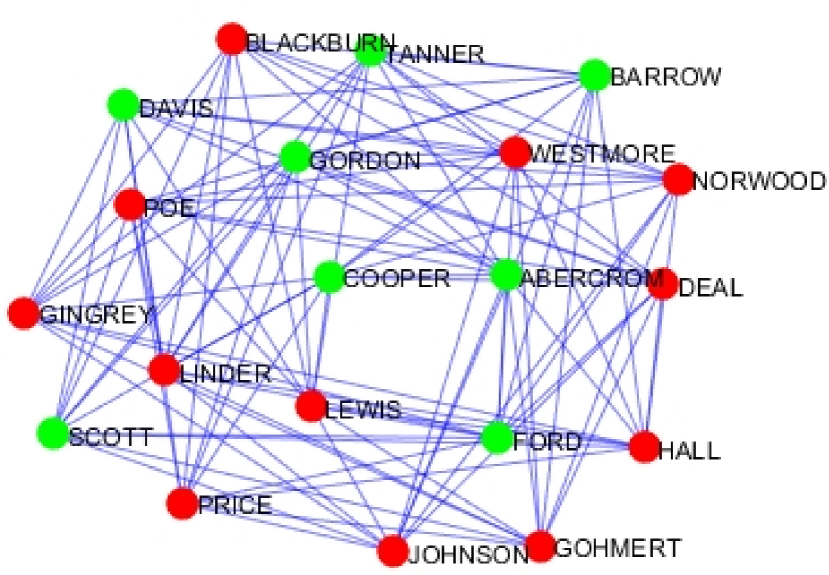

Analysis of a breast cancer data set.

We applied SSONA to a data set containing 800 gene expression measurements from large epithelial cells obtained from 255 patients with breast cancer.

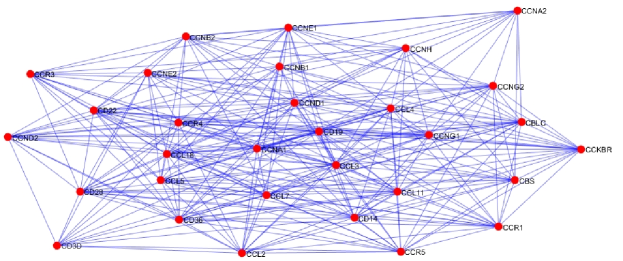

The goal is to capture regulatory interactions amongst the genes, as well as to identify genes that tend to have interactions with other genes in a group and hence act as master regulators, thus providing insights into the molecular circuitry of the disease. Figure 23 depicts the heat map of the estimated adjacency matrix for the breast cancer data set. As it is clear in Figure 23, and show that selected genes are densely connected, which is not the case when employing the the graphical lasso algorithm (see, Figure 24). Therefore, SSONA can provide an intuitive explanation of the relationships among the genes in the breast cancer data set (see, Figure 25 and 26 for two examples). These genes connectivity in the tumor samples may indicate a relationship that is common to an important subset of cancers. Many other genes belong to this network, each indicating a potentially interesting interaction in cancer biology. We omit the full list of densely connected genes in our estimated network and provide a complete list in the on-line supplementary materials available in the first author’s homepage.

5 Conclusion

In this paper, a new structured norm minimization method for solving multi-structure graphical model selection problems is proposed. Using the proposed SSON, we can efficiently and accurately recover the underlying network structure. Our method utilizes a class of sparse structured norms in order to achieve higher order accuracy in approximating the decomposition of the parameter matrix in Markov Random Field and Gaussian Covariance Graph models. We also provide a brief discussion of its application to regression and classification problems. Further, we introduce a linearized multi-block ADMM algorithm to solve the resulting optimization problem. The global convergence of the algorithm is established without any upper bound on the penalty parameter. We applied the proposed methodology to a number of real and synthetic data sets that establish its overall usefulness and superior performance to competing methods in the literature.

Acknowledgments

The authors would like to thank the Editor and three anonymous referees for many constructive comments and suggestions that improved significantly the structure and readability of the paper. This work was supported in part by NSF grants DMS-1545277, DMS-1632730, NIH grant 1R01-GM1140201A1 and by the UF Informatics Institute.

A Update for

In each iteration of Algorithm 1 the update for depends on the form of the loss function . We consider the following cases to update :

-

1.

The update for in Algorithm 1 (step 2(a)) can be obtained by minimizing

with respect to (note that the constraint in (2.2) is treated as an implicit constraint, due to the domain of definition of the function). This can be shown to have the solution

where stands for the eigen-decomposition of .

-

2.

Update for in Step 2(a) of Algorithm 1 leads to the following optimization problem

(33) We use a novel non-monotone version of the Barzilai-Borwein method (Barzilai and Borwein, 1988; Raydan, 1997; Fletcher, 2005; Ataee Tarzanagh et al., 2014) to solve (33). The details are given in Algorithm 2.

Algorithm 2 Non-monotone Barzilai Borwein Method for solving (33) Initialize The parameters:-

(a)

, , and .

-

(b)

A positive sequence satisfying .

-

(c)

Constants , , and .

Iterate Until the stopping criterion is met:-

1.

.

-

2.

Set .

-

3.

If, then

-

While , do

-

Set

-

EndWhile

-

EndIf

-

4.

Define and .

-

5.

Define

-

(a)

-

3.

To update in step 2(a), using (2.4), we have that

where such that

is the eigen-decomposition of the matrix , and and are the nonnegative and negative eigenvalues of .

B Convergence Analysis

Before establishing the main result on global convergence of the proposed ADMM algorithm, we provide the necessary definitions used in the proofs (for more details see Bolte et al. (2014)):

Definition 11

(Kurdyka- Lojasiewicz property).

The function is said to have the Kurdyka- Lojasiewicz (K-L) property at point , if there exist , and such that for all

the following inequality holds

where stands for the class of functions with the properties:

-

(i)

is continuous on ;

-

(ii)

is smooth concave on ;

-

(iii)

, .

Definition 12

(Semi-algebraic sets and functions).

-

(i)

A subset is semi-algebraic, if there exists a finite number of real polynomial functions , such that

-

(ii)

A function is called semi-algebraic, if its graph

is a semi-algebraic set in .

Definition 13

(Sub-analytic sets and functions).

-

(i)

A subset is sub-analytic, if there exists a finite number of real analytic functions , such that

-

(ii)

A function h: is called sub-analytic, if its graph

is a sub-analytic set in .

It can be easily seen that both real analytic and semi-algebraic functions are sub-analytic. In general, the sum of two sub-analytic functions is not necessarily sub-analytic. However, it is easy to show that for two sub-analytic functions, if at least one function maps bounded sets to bounded sets, then their sum is also sub-analytic (Bolte et al., 2014).

Remark 14

Each in (3) is a convex semi-algebraic function (see, example 5.3 in (Bolte et al., 2014)), while the loss function in (2.2), (2.3), (2.4), (2.5), and (2.6) is sub-analytic (even analytic). Since each function maps bounded sets to bounded sets, we can conclude that the augmented Lagrangian function

which is the summation of sub-analytic functions is itself sub-analytic. All sub-analytic functions which are continuous over their domain satisfy a K-L inequality, as well as some, but not all, convex functions (see Bolte et al., 2014 for details and a counterexample). Therefore, the augmented Lagrangian function satisfies the K-L property.

Next, we establish a series of lemmas used in the proof of Theorem 10.

Lemma 15

Let be a sequence generated by Algorithm 1, then there exists a positive constant such that

| (34) | |||||

Proof. Using the first-order optimality conditions for (21) and the convexity of , we obtain

| (35) | |||||

where the second equality follows from the fact that

| (36) | |||||

where is a Lipschitz constant of the gradient , and is a proximal parameter.

Following the same steps as (35), we have that

| (37) | |||||

and

| (38) | |||||

Let

Lemma 16

Let be a sequence generated by Algorithm 1. Then, there exists a subsequence of , such that

where

Proof. Let . Using the quadratic function , we have that

| (39) | |||||

Using (39) and the fact that each function is lower bounded, there exists , such that

| (40) | |||||

since and are all lower bounded.

Now, using Lemma 15, we have that

| (41) | |||||

Lemma 15 together with (41) shows that converges to . Note that (41) and the coerciveness of and imply that is a bounded sequence. This together with the updating formula of and (41) yield the boundedness of . Moreover, the fact that , gives the boundedness of , which implies that the entire sequence is a bounded one. Therefore, there exists a subsequence

such that as .

Now, using the fact that , and are continuous functions, we have that

Lemma 17

| (44) |

| (45) |

where

| (46) |

Now, using (41), we obtain that

| (47) |

Suppose that Algorithm 1 does not stop at a stationary point. Using Lemma 16, there exists a subsequence , such that as Using (45) and (47), we conclude that .

Proof of Theorem 10. Lemmas 16 and 17 imply that is a bounded sequence and the set of limit points of starting from is non-empty, respectively. Moreover, Lemma 5 and Remark 5 of (Bolte et al., 2014) imply that the set of limit points of starting from is compact. The remainder of the proof of this Theorem follows along similar lines to the proof of Theorem 1 in (Bolte et al., 2014), by utilizing the K-L property of the problem (3) (see, Remark 14).

References

- Ataee Tarzanagh et al. (2014) D Ataee Tarzanagh, M Reza Peyghami, and H Mesgarani. A new nonmonotone trust region method for unconstrained optimization equipped by an efficient adaptive radius. Optimization Methods and Software, 29(4):819–836, 2014.

- Barabási and Albert (1999) Albert-László Barabási and Réka Albert. Emergence of scaling in random networks. science, 286(5439):509–512, 1999.

- Barzilai and Borwein (1988) Jonathan Barzilai and Jonathan M Borwein. Two-point step size gradient methods. IMA journal of numerical analysis, 8(1):141–148, 1988.

- Basu and Michailidis (2015) Sumanta Basu and George Michailidis. Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43(4):1535–1567, 2015.

- Basu et al. (2015) Sumanta Basu, Ali Shojaie, and George Michailidis. Network granger causality with inherent grouping structure. The Journal of Machine Learning Research, 16(1):417–453, 2015.

- Berthet et al. (2016) Quentin Berthet, Philippe Rigollet, and Piyush Srivastava. Exact recovery in the Ising block model. arXiv:1612.03880, 2016.

- Blei et al. (2003) David M Blei, Andrew Y Ng, and Michael I Jordan. Latent dirichlet allocation. Journal of machine Learning research, 3(Jan):993–1022, 2003.

- Bolte et al. (2014) Jérôme Bolte, Shoham Sabach, and Marc Teboulle. Proximal alternating linearized minimization for nonconvex and nonsmooth problems. Mathematical Programming, 146(1-2):459–494, 2014.

- Boyd et al. (2011) Stephen Boyd, Neal Parikh, Eric Chu, Borja Peleato, and Jonathan Eckstein. Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine Learning, 3(1):1–122, 2011.

- Cai and Liu (2011) Tony Cai and Weidong Liu. Adaptive thresholding for sparse covariance matrix estimation. Journal of the American Statistical Association, 106(494):672–684, 2011.

- Chandrasekaran et al. (2010) Venkat Chandrasekaran, Pablo A Parrilo, and Alan S Willsky. Latent variable graphical model selection via convex optimization. In Communication, Control, and Computing (Allerton), 2010 48th Annual Allerton Conference on, pages 1610–1613. IEEE, 2010.

- Chen et al. (2016) Caihua Chen, Bingsheng He, Yinyu Ye, and Xiaoming Yuan. The direct extension of admm for multi-block convex minimization problems is not necessarily convergent. Mathematical Programming, 155(1-2):57–79, 2016.

- Chernozhukov et al. (2017) Victor Chernozhukov, Christian Hansen, and Yuan Liao. A lava attack on the recovery of sums of dense and sparse signals. The Annals of Statistics, 45(1):39–76, 2017.

- Danaher et al. (2014) Patrick Danaher, Pei Wang, and Daniela M Witten. The joint graphical lasso for inverse covariance estimation across multiple classes. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(2):373–397, 2014.

- Davis and Yin (2015) Damek Davis and Wotao Yin. A three-operator splitting scheme and its optimization applications. Set-Valued and Variational Analysis, pages 1–30, 2015.

- Dolan and Moré (2002) Elizabeth D Dolan and Jorge J Moré. Benchmarking optimization software with performance profiles. Mathematical programming, 91(2):201–213, 2002.

- Drton and Richardson (2002) Mathias Drton and Thomas S Richardson. A new algorithm for maximum likelihood estimation in gaussian graphical models for marginal independence. In Proceedings of the Nineteenth conference on Uncertainty in Artificial Intelligence, pages 184–191. Morgan Kaufmann Publishers Inc., 2002.

- Drton and Richardson (2008) Mathias Drton and Thomas S Richardson. Graphical methods for efficient likelihood inference in gaussian covariance models. Journal of Machine Learning Research, 9(May):893–914, 2008.

- Elhamifar and Vidal (2009) Ehsan Elhamifar and René Vidal. Sparse subspace clustering. In Computer Vision and Pattern Recognition, 2009. CVPR 2009. IEEE Conference on, pages 2790–2797. IEEE, 2009.

- Fletcher (2005) Roger Fletcher. On the barzilai-borwein method. Optimization and control with applications, pages 235–256, 2005.

- Fortunato (2010) Santo Fortunato. Community detection in graphs. Physics reports, 486(3):75–174, 2010.

- Friedman et al. (2008) Jerome Friedman, Trevor Hastie, and Robert Tibshirani. Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3):432–441, 2008.

- Guimera and Amaral (2005) Roger Guimera and Luis A Nunes Amaral. Functional cartography of complex metabolic networks. Nature, 433(7028):895–900, 2005.

- Guo et al. (2011a) Jian Guo, Elizaveta Levina, George Michailidis, and Ji Zhu. Joint estimation of multiple graphical models. Biometrika, 98(1):1–15, 2011a.

- Guo et al. (2011b) Jian Guo, Elizaveta Levina, George Michailidis, and Ji Zhu. Asymptotic properties of the joint neighborhood selection method for estimating categorical markov networks. arXiv preprint math.PR/0000000, 2011b.

- Guo et al. (2015) Jian Guo, Jie Cheng, Elizaveta Levina, George Michailidis, and Ji Zhu. Estimating heterogeneous graphical models for discrete data with an application to roll call voting. The Annals of Applied Statistics, 9(2):821, 2015.

- Hajinezhad and Hong (2015) Davood Hajinezhad and Mingyi Hong. Nonconvex alternating direction method of multipliers for distributed sparse principal component analysis. In Signal and Information Processing (GlobalSIP), 2015 IEEE Global Conference on, pages 255–259. IEEE, 2015.

- Hajinezhad et al. (2016) Davood Hajinezhad, Mingyi Hong, Tuo Zhao, and Zhaoran Wang. Nestt: A nonconvex primal-dual splitting method for distributed and stochastic optimization. In Advances in Neural Information Processing Systems, pages 3215–3223, 2016.

- Hoerl and Kennard (1970) Arthur E Hoerl and Robert W Kennard. Ridge regression: Biased estimation for nonorthogonal problems. Technometrics, 12(1):55–67, 1970.

- Höfling and Tibshirani (2009) Holger Höfling and Robert Tibshirani. Estimation of sparse binary pairwise markov networks using pseudo-likelihoods. Journal of Machine Learning Research, 10(Apr):883–906, 2009.

- Hong and Luo (2017) Mingyi Hong and Zhi-Quan Luo. On the linear convergence of the alternating direction method of multipliers. Mathematical Programming, 162(1-2):165–199, 2017.

- Ising (1925) Ernst Ising. Beitrag zur theorie des ferromagnetismus. Zeitschrift für Physik A Hadrons and Nuclei, 31(1):253–258, 1925.

- Jacob et al. (2009) Laurent Jacob, Guillaume Obozinski, and Jean-Philippe Vert. Group lasso with overlap and graph lasso. In Proceedings of the 26th annual international conference on machine learning, pages 433–440. ACM, 2009.

- Karoui (2008) Noureddine El Karoui. Operator norm consistent estimation of large-dimensional sparse covariance matrices. The Annals of Statistics, pages 2717–2756, 2008.

- Lee et al. (2007) Su-In Lee, Varun Ganapathi, and Daphne Koller. Efficient structure learning of Markov networks using -regularization. In Advances in neural Information processing systems, pages 817–824, 2007.

- Lewis et al. (2010) Anna CF Lewis, Charlotte M Deane, Mason A Porter, and Nick S Jones. The function of communities in protein interaction networks at multiple scales. BMC systems biology, 4(1):100, 2010.

- Li et al. (2005) Lun Li, David Alderson, John C Doyle, and Walter Willinger. Towards a theory of scale-free graphs: Definition, properties, and implications. Internet Mathematics, 2(4):431–523, 2005.

- Liljeros et al. (2001) Fredrik Liljeros, Christofer R Edling, Luis A Nunes Amaral, H Eugene Stanley, and Yvonne Åberg. The web of human sexual contacts. Nature, 411(6840):907–908, 2001.

- Lin et al. (2015) Tianyi Lin, Shiqian Ma, and Shuzhong Zhang. On the global linear convergence of the ADMM with multiblock variables. SIAM Journal on Optimization, 25(3):1478–1497, 2015.

- Lin et al. (2016) Tianyi Lin, Shiqian Ma, and Shuzhong Zhang. Iteration complexity analysis of multi-block ADMM for a family of convex minimization without strong convexity. Journal of Scientific Computing, 69(1):52–81, 2016.

- Lin et al. (2011) Zhouchen Lin, Risheng Liu, and Zhixun Su. Linearized alternating direction method with adaptive penalty for low-rank representation. In Advances in neural information processing systems, pages 612–620, 2011.

- Liu et al. (2013) Guangcan Liu, Zhouchen Lin, Shuicheng Yan, Ju Sun, Yong Yu, and Yi Ma. Robust recovery of subspace structures by low-rank representation. IEEE Transactions on Pattern Analysis and Machine Intelligence, 35(1):171–184, 2013.

- Liu and Ihler (2011) Qiang Liu and Alexander Ihler. Learning scale free networks by reweighted l1 regularization. In Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, pages 40–48, 2011.

- Liu et al. (2015) Risheng Liu, Zhouchen Lin, and Zhixun Su. Linearized alternating direction method with parallel splitting and adaptive penalty for separable convex programs in machine learning. Machine Learning, 99(2), 2015.

- Ljung (1998) Lennart Ljung. System identification. In Signal analysis and prediction, pages 163–173. Springer, 1998.

- Lütkepohl (2005) Helmut Lütkepohl. New introduction to multiple time series analysis. Springer Science & Business Media, 2005.

- Ma et al. (2013) Shiqian Ma, Lingzhou Xue, and Hui Zou. Alternating direction methods for latent variable gaussian graphical model selection. Neural computation, 25(8):2172–2198, 2013.

- Mohan et al. (2012) Karthik Mohan, Mike Chung, Seungyeop Han, Daniela Witten, Su-In Lee, and Maryam Fazel. Structured learning of Gaussian graphical models. In Advances in neural information processing systems, pages 620–628, 2012.

- Monti et al. (2003) Stefano Monti, Pablo Tamayo, Jill Mesirov, and Todd Golub. Consensus clustering: a resampling-based method for class discovery and visualization of gene expression microarray data. Machine learning, 52(1):91–118, 2003.

- Newman (2001) Mark EJ Newman. The structure of scientific collaboration networks. Proceedings of the National Academy of Sciences, 98(2):404–409, 2001.

- Newman (2012) Mark EJ Newman. Communities, modules and large-scale structure in networks. Nature Physics, 8(1):25–31, 2012.

- Newman and Girvan (2004) Mark EJ Newman and Michelle Girvan. Finding and evaluating community structure in networks. Physical review E, 69(2):026113, 2004.

- Obozinski et al. (2011) Guillaume Obozinski, Laurent Jacob, and Jean-Philippe Vert. Group lasso with overlaps: the latent group lasso approach. arXiv preprint arXiv:1110.0413, 2011.

- Rao et al. (2016) Nikhil Rao, Robert Nowak, Christopher Cox, and Timothy Rogers. Classification with the sparse group lasso. IEEE Transactions on Signal Processing, 64(2):448–463, 2016.

- Ravikumar et al. (2011) Pradeep Ravikumar, Martin J Wainwright, Garvesh Raskutti, and Bin Yu. High-dimensional covariance estimation by minimizing -penalized log-determinant divergence. Electronic Journal of Statistics, 5:935–980, 2011.

- Raydan (1997) Marcos Raydan. The Barzilai and Borwein gradient method for the large scale unconstrained minimization problem. SIAM Journal on Optimization, 7(1):26–33, 1997.

- Robins et al. (2007) Garry Robins, Pip Pattison, Yuval Kalish, and Dean Lusher. An introduction to exponential random graph models for social networks. Social networks, 29(2):173–191, 2007.

- Rothman et al. (2008) Adam J Rothman, Peter J Bickel, Elizaveta Levina, and Ji Zhu. Sparse permutation invariant covariance estimation. Electronic Journal of Statistics, 2:494–515, 2008.

- Scheinberg et al. (2010) Katya Scheinberg, Shiqian Ma, and Donald Goldfarb. Sparse inverse covariance selection via alternating linearization methods. In Advances in Neural Information Processing Systems, pages 2101–2109, 2010.

- Sun et al. (2015) Defeng Sun, Kim-Chuan Toh, and Liuqin Yang. A convergent 3-block semiproximal alternating direction method of multipliers for conic programming with 4-type constraints. SIAM journal on Optimization, 25(2):882–915, 2015.

- Tan et al. (2014) Kean Ming Tan, Palma London, Karthik Mohan, Su-In Lee, Maryam Fazel, and Daniela M Witten. Learning graphical models with hubs. Journal of Machine Learning Research, 15(1):3297–3331, 2014.

- Tibshirani (1996) Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288, 1996.

- Traud et al. (2011) Amanda L Traud, Eric D Kelsic, Peter J Mucha, and Mason A Porter. Comparing community structure to characteristics in online collegiate social networks. SIAM review, 53(3):526–543, 2011.

- Tsay (2005) Ruey S Tsay. Analysis of financial time series, volume 543. John Wiley & Sons, 2005.

- Valdés-Sosa et al. (2005) Pedro A Valdés-Sosa, Jose M Sánchez-Bornot, Agustín Lage-Castellanos, Mayrim Vega-Hernández, Jorge Bosch-Bayard, Lester Melie-García, and Erick Canales-Rodríguez. Estimating brain functional connectivity with sparse multivariate autoregression. Philosophical Transactions of the Royal Society of London B: Biological Sciences, 360(1457):969–981, 2005.

- Wang et al. (2013) Xiangfeng Wang, Mingyi Hong, Shiqian Ma, and Zhi-Quan Luo. Solving multiple-block separable convex minimization problems using two-block alternating direction method of multipliers. arXiv preprint arXiv:1308.5294, 2013.

- Xue et al. (2012) Lingzhou Xue, Shiqian Ma, and Hui Zou. Positive-definite ℓ1-penalized estimation of large covariance matrices. Journal of the American Statistical Association, 107(500):1480–1491, 2012.

- Yang and Yuan (2013) Junfeng Yang and Xiaoming Yuan. Linearized augmented Lagrangian and alternating direction methods for nuclear norm minimization. Mathematics of computation, 82(281):301–329, 2013.

- Yuan and Lin (2007) Ming Yuan and Yi Lin. Model selection and estimation in the gaussian graphical model. Biometrika, 94(1):19–35, 2007.

- Zhao et al. (2014) Changjiu Zhao, Brian Earl Eisinger, Terri M Driessen, and Stephen C Gammie. Addiction and reward-related genes show altered expression in the postpartum nucleus accumbens. Frontiers in behavioral neuroscience, 8, 2014.

- Zou and Hastie (2005) Hui Zou and Trevor Hastie. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67(2):301–320, 2005.