Functional Laws for Trimmed Lévy Processes

Abstract

Two different ways of trimming the sample path of a stochastic process in : global (“trim as you go”) trimming and record time (“lookback”) trimming are analysed to find conditions for the corresponding operators to be continuous with respect to the (strong) -topology. A key condition is that there should be no ties among the largest ordered jumps of the limit process. As an application of the theory, via the continuous mapping theorem we prove limit theorems for trimmed Lévy processes, using the functional convergence of the underlying process to a stable process. The results are applied to a reinsurance ruin time problem.

Keywords: functional laws; Skorokhod -topology; trimming càdlàg functions; trimmed Lévy processes; reinsurance risk processes.

2010 Mathematics Subject Classification: 60G51; 60G52; 60G55

1 Introduction

By “trimming” a process we mean identifying “large” jumps of the process, in some sense, and deleting them from it.

The term has its origins in the statistical practice of identifying “outliers” in a sample of i.i.d. random variables, then removing them from a statistic of interest, typically, the sample sum, which can be considered as a stochastic process in discrete time.

More recently, the techniques have been transferred to processes such as extremal processes and Lévy processes indexed by a

continuous time parameter,

where asymptotic properties of the trimmed process have been worked out in a number of interesting cases.

The asymptotic studied may be large time (), as in the statistical situation, or, for continuous time processes, small time (). The small time case extends our understanding of local properties of the process and can have direct application as for example in

Maller and Fan [8] and Maller and Schmidli [10]; the large time case has the statistical applications alluded to, such as the robustness of statistics, and insurance modelling, etc., as we discuss later.

This area of research can be regarded as combining studies on properties of extremes of the jumps of a process with those of the process itself; the former, a version of extreme value theory; the latter relating, for example, to domains of attraction of the process. A combination of the two fields enriches both, and the trimming idea is a natural way of approaching this.

Research in a similar direction has been carried on by Silvestrov and Teugels [11]; see also their references.

In the present paper we extend some earlier work of the present authors to consider various ways of trimming the sample path of a stochastic process in the space

of càdlàg functions. The initial set-up is very general. We begin in Section 2 by establishing continuity properties (in the Skorokhod (strong) -topology) of operators which remove extremes.

There are a number of intuitively reasonable ways of defining such operators. Not all of them behave in the same way, and Section 2 is devoted to teasing out the differences between them. We take a dynamic sample path approach which brings into focus some interesting and distinctive features not previously apparent. Proofs for Section 2 are in Section 4.

An application of the ideas to the functional convergence of a Lévy process in the domain of attraction of a stable law is then given. Statements for these are in Section 3, and proofs of them are in Section 5. Continuity properties of certain extremal operators are closely related to the occurrence or otherwise of tied (equal) values in the large jumps of the limiting process and consequently we need to analyse these too. A final Section 6 develops a motivating application to a reinsurance ruin time problem.

2 Extremal Operators on Skorokhod Space

Let be the space of all càdlàg functions: endowed with the Skorokhod (strong) -topology. Denote the sup norm by , so that , where for each , is the value of at time . Convergence in the -topology is characterised as follows. Let be the set of all continuous and strictly increasing functions with and . Denote by the identity map. Let . Then in if there exists a sequence such that

Intuitively, -convergence requires “matching jumps” at “matching points” after a deformation of time. We refer to Chapter VI in Jacod and Shiryaev [6] and Section 12 in Billingsley [1] for more information on the Skorokhod space. For other topologies on we refer to Skorokhod [12] and Whitt [14].

We proceed by setting out some basic methods of trimming extremes.

2.1 Global (Pointwise) Trimmers (“Trim As You Go”)

Let with jump process . Set . Define the following extremal operators mapping into :

(i) ;

(ii) ;

(iii) ; and

(iv) .

Here (i) is the running supremum process of , and (ii) is the running supremum process for . In (iii), represents the magnitude of largest (positive) jump of up till time , and represents the largest magnitude of the negative jumps of up till time ; while in (iv), represents the magnitude of largest jump in modulus of up till time .

With these operators we can define what we call global, or pointwise, trimming operators. Let , . Take and define iteratively

(v) the extremal positive (negative) trimming operators

(vi) the extremal positive (negative) jump operators

(vii) the trimming operators (for )

(viii) the extremal modulus trimming operators

(ix) and the extremal modulus jump operators

Here (v) is with the largest jumps of up till time subtracted, and is similar with the negative jumps of largest magnitude subtracted. In (vii), has the positive and negative jumps of largest magnitudes subtracted, while (viii), has the largest jumps in modulus of up till time removed from . In (vi) and (ix), and are the largest values in magnitude for positive (negative), or in modulus, jumps of the corresponding processes.

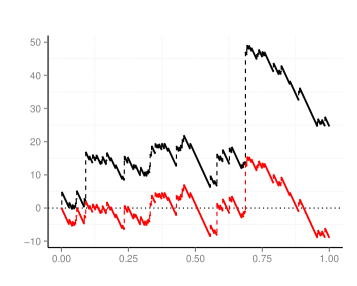

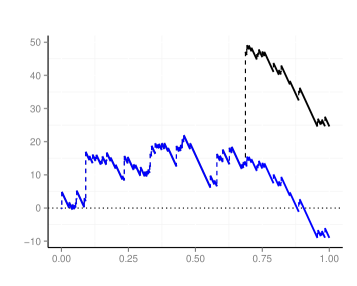

We call the operators in (v), (vii), (viii), “Trim As You Go” operators because at each point in time, the designated number of largest positive (negative) jumps up to that point are removed from the process. See Figure 1 in Section 2.3 for an illustration with a schematic insurance risk process.

To analyse the convergence of these operators in , we need the following considerations. We say that an operator is -continuous at if implies . We say that is -continuous at if implies , as . In general, being -continuous at does not imply that is -continuous at . However, this is true if in addition is -compatible, by which we mean for all , . The operator is called jointly -continuous at if for any sequence converging to in the -topology, there exists in , such that, simultaneously as , , and . The following simple proposition summarises.

Proposition 2.1.

Let be -compatible and take . Suppose is -continuous at . Then is jointly -continuous at .

Proof of Proposition 2.1: Assume is -compatible and -continuous at . Since , , i.e., , together with being -continuous at , implies , i.e., , proving the proposition.

Proposition 2.2.

Each of the operators defined in (i)–(ix) is

-

(a)

-Lipschitz, hence continuous in norm;

-

(b)

-compatible; and, consequently, by Proposition 2.1, jointly -continuous.

Proof of Proposition 2.2: (a) For example, we prove (iii). When ,

| (1) | |||||

| (3) |

using the triangle inequality .

(b) We prove this for (iv), for example. Let , , and . Then

Remark 2.1.

We refer to Section IV.2 in Jacod and Shiryaev [6] for other continuity properties of common mappings in the Skorokhod topology.

2.2 Signed Modulus Trimmers

In Section 3 we will consider a Lévy process which is to be trimmed. Before this, in the present subsection, we want to draw attention to an issue that arises with modulus trimming when considered pathwise. There may be one or more jumps equal in magnitude to the largest of , for . We refer to these as “tied” values (for the modulus, with a similar concept for the positive and negative jumps).

Buchmann, Fan and Maller [2] (hereafter, “BFM”) define a “modulus trimmed Lévy process” as follows. Denote the largest modulus jump of up to time , i.e., the jump corresponding to the largest of , , by . When there is no tie for , the sign of is uniquely determined. When there is a tie, the procedure in BFM is to nominate a jump chosen at random among the almost surely (a.s.) finite number of tied values according to a discrete uniform distribution on the collection of ties. While appropriate in the context of BFM, this definition is problematic when we consider the sample path of the process on . To see why, take a simple example. Suppose for some the largest modulus jump up till time is tied at values with opposite signs, say:

while for all . For each , if we were to choose from with equal probability to be trimmed from , the sample path of the resulting trimmed process would not be in .

Thus, we need to design a way to define signed modulus trimming on the sample path of so as to stay within . One way to do this is as follows (we now revert to the general setup). For , define the last modulus record time process on as

| (4) |

Then the signed largest modulus jump up till time is , and the signed largest trimmer can be defined as . More generally, interpret , let , and, for , set

Now is not in general globally -continuous, that is, it is not -continuous at all . Take for example and . Then , but

However, is continuous when there is no change of signs of ties in the limit. This is shown in Theorem 2.1, which uses the following notation. For each , collect the times of occurrence of the largest values, and the times of occurrence of values having largest modulus, into sets and , thus:

| (5) |

and

| (6) |

We use the convention that when is continuous on , then . Recall that a càdlàg function has only finitely many jumps with magnitude bounded away from 0, so and are finite sets (we include in this the possibility that one or other of them may be empty) for functions . Collect the sign changing largest modulus jumps contained in into the set

Note that implies . Conversely, implies or .

In the next theorem, we show that when there is no sign change among ties of large modulus jumps in and its trimmed versions for all , is jointly -continuous at . The next theorem is proved in Section 4.

Theorem 2.1.

is jointly -continuous at if . Consequently, is jointly -continuous at if for all , when .

2.3 Record Times Trimmers (“Lookback Trimming”)

On the function space , we can extend the idea of trimming by including a random location where trimming starts and hence define a second kind of trimming. For define the first (positive) record time in by

| (7) |

for , and similarly we could define the first (negative) record time. Likewise,

| (8) |

gives the first modulus record time. The corresponding record time trimmers are

| (9) |

Expanding, can be written for as

Thus, is trimmed at time if the record occurs before , otherwise not. Figure 1 gives an illustration of the two trimming types for a compound Poisson risk process as used in insurance risk modelling (cf. Section 6).

Set . For , define the order record times trimmers as

| (10) |

and, for , replace each , in (10) by and .

While the record trimming functionals are -compatible, they are not however of the type described in Section 2.1. In fact they are not globally -continuous.

Example 2.1.

[ is not globally norm or -continuous.]

(i) is not -continuous. To see this, let . For set . Observe that . In particular, as . However,

and

Thus, is -compatible, but not -continuous in .

(ii) also is not -continuous. To see this, take with . Then , hence for , once ,

Consequently, we have , but not .

Recall the definitions of and in (5) and (6). Our main result of this section is that the record time trimmer is jointly -continuous at if and only if does not admit ties. The next theorem is proved in Section 4.

Theorem 2.2.

Let and .

(i) If then is jointly -continuous at . Consequently, if

for all , then is jointly -continuous at .

(ii) If is -continuous at then .

The same holds true with replaced by and replaced by .

3 Functional Laws for Lévy Processes

A number of interesting processes can be derived by applying the operators in Section 2 to Lévy processes. In the present section , , will be a real valued càdlàg Lévy process with canonical triplet . The positive, negative and two-sided tails of the Lévy measure are, for ,

The jump process of is , the positive jumps are , and the magnitudes of the negative jumps are . The processes and , when present, are non-negative independent processes. For any integers , let be the largest positive jump, and let be the largest jump in , i.e., the negative of the smallest jump. These kinds of ordered jumps are carefully defined in BFM, allowing for the possibility of tied values. (Recall the discussion in Subsection 2.2.) We can similarly define and for the ordered jumps in .

Throughout, for small time convergence () we assume when dealing with modulus trimming and or (or both when appropriate) when dealing with one-sided trimming. In particular, these ensure there are infinitely many jumps , or , a.s., in any bounded interval of time.

As demonstrated in Section 2, the largest modulus trimming as defined in BFM is not natural for the functional setting, so here we adopt a modified definition. Write to denote the largest jump in modulus up to time , taking the sign of the latest largest modulus jump. Then define the trimmed Lévy processes

| (11) |

which we call the asymmetrically trimmed and modulus trimmed processes, respectively. With the convention , taking or in asymmetrical trimming gives one-sided trimmed processes and .

In this section we apply a functional law for Lévy processes attracted to a non-normal stable law to get two theorems for trimmed Lévy processes. is said to be in a non-normal domain of attraction at small (large) times if there exist non-stochastic functions and such that

| (12) |

where is an a.s. finite, non-degenerate, non-normal111When is , a standard normal random variable, the large jumps are asymptotically negligible with respect to and (14) and (15) remain true with and a standard Brownian motion; see Fan [4]. random variable. Then (12) implies that the two-sided tail of is regularly varying (at 0 or , as appropriate), with index . The limit rv has the distribution of , where is a stable() Lévy process. The canonical triplet for will be taken as , where has tail function , , for some .

In the small time case, conditions on the Lévy measure for (12) to hold can be deduced from Theorem 2.2 of Maller and Mason [9], whose result can also be used to show that (12) can be extended to convergence in ; that is,

| (13) |

weakly as with respect to the -topology. Large time () convergence in (13) also follows from (12) as is well known.

Assuming the convergence in (13), we can prove a variety of interesting functional limit theorems for by applying the operators in Section 2. We list some examples in Theorem 3.1 and prove them in Section 5.

Theorem 3.1 considers (i) lookback trimming, (ii) two-sided (or one-sided, with or taken as 0) trimming, and (iii) signed modulus trimming defined as in Subsection 2.2. To specify the lookback trimming in this situation, recall the definition of the record time trimming functionals in (9) and (10). Using them, we define, for , lookback trimmed paths of order , based on positive jumps, being processes on , indexed by , as

and, for

Theorem 3.1.

Assume is in the domain of attraction of a stable law at (or ) with nonstochastic centering and norming functions , , so that (12) and (13) hold. In the following, convergences are with respect to the -topology in .

(i) Suppose and . Then, for the same and ,

| (14) |

(ii) Assume and . Then, for the same and ,

| (15) |

(iii) Suppose only and . Then, for the same and ,

| (16) |

Remark 3.1.

(i) BFM and also Maller and Mason [9] include convergence of the quadratic variation of in their expositions. Using these as basic convergences (i.e., together with (12) and (13)) would lead to functional convergences of the jointly trimmed process together with its trimmed quadratic variation process, and we could then consider self-normalised versions. But we omit the details of these.

(ii) Fan [3] proved the converses in (ii) and (iii) of Theorem 3.1 for ,

i.e., if the convergence in (15) or (16) holds for a fixed , then

is in the domain of attraction of a stable law with index at small times.

We conclude this section by mentioning that the same methods can be used to get functional convergence for jumps of an extremal process together with trimmed versions. Again, we omit further details.

4 Proofs for Section 2

For the proof of Theorem 2.1 we need a preliminary lemma. Let denote the set of accumulation points of a sequence as . Recall that and , the last and first modulus record time processes, are defined in (4) and (8); , the first positive record time process, is defined in (7).

Lemma 4.1.

Take and suppose with . Then for each ,

(i) if , then and ;

(ii) if , then .

(iii) If and , then for all sufficiently large , for each .

Proof of Lemma 4.1: (ii) We consider the case only; can be argued similarly. Take and let with . Then there are such that for . This also means .

Fix a time and assume . Recall that is a finite set. Let with . Observe that and, thus, since , . For (ii) it thus suffices to show that .

To see this, note that there exist and such that for all , (because and is finite), and, also,

| (17) |

To explain (17): the quantity

is with all positive jumps equal in magnitude to the largest jump up till time subtracted. Applying the operator to this produces the largest of the remaining jumps, hence the second largest jump, in magnitude, of , up till time . This is strictly smaller than the magnitude of the largest jump, which is . So indeed there is a such that (17) holds.

Let be the limit along a subsequence . Contrary to the hypothesis, suppose and, thus, for all sufficiently large . For those , also being larger than , observe that

Here the second equality holds because implies for any , for large , and thus subtracting any such jumps from does not affect the value of . Using (1) again now gives

where the last inequality holds by (17). This contradiction gives , completing the proof that .

(iii) For this, suppose again and, in addition, . We can take and (17) now takes the form

for some and all . Suppose that for some . Then we must have , as otherwise

This contradiction proves the result.

Proof of Theorem 2.1: Assume . We first show that is -compatible. Let and recall from Proposition 2.2 that is -compatible. Since

and

we have . Thus

Then is -compatible, because

It remains to show that is -continuous at . Suppose . If , then , hence is trivially -continuous. Alternatively, suppose . Then

The first term on the RHS tends to and the second term on the RHS does not exceed

| (18) |

By Lemma 4.1, for each . If , then the second term on the RHS of (4) tends to . Suppose where . Then . But since for all , we also have for all . Thus . This completes the proof.

Proof of Theorem 2.2: Again we only consider the case of .

(i) Let in and . Then there exists a sequence such that . If then and , so

Alternatively, if , then by Lemma 4.1 there is an such that for all and, for those , we also have

As , the right hand-side converges uniformly (in the supremum norm) to , which shows that is jointly -continuous at . For , recall the definition of in (10). Since is -continuous at and is assumed -continuous at , then the composition is -continuous at . An analogous argument holds for .

(ii) Contrary to the hypothesis, assume that for some . Noting that and we introduce

As , we have and, in particular, . Observe that and , . Hence, for all ,

Finally, let be such that . Then . As is continuous at ,

and, thus,

To summarise, we showed that , but not , contradicting the -continuity of at .

5 Proof of Theorem 3.1

Let be the jumps of a Lévy process having Lévy measure , with ordered jumps and , as specified in Section 3. In what follows we will assume throughout, so there are always infinitely many positive and negative jumps of , a.s., in any interval of time.

Let be an i.i.d. sequence of exponentially distributed random variables with common parameter and let with . Write

for the right-continuous inverse of the right tail (with similar notations for the left tail and the two sided tail ). The following distributional equivalence can be deduced from Lemma 1.1 of BFM:

| (19) |

We refer to BFM for more background information on the properties of the extremal processes and the trimmed Lévy processes.

Proof of Theorem 3.1, Part (i) We give proofs just for ; is very similar. Recall the definition of in (13) and assume the convergence of to a stable process as in (13). The process has Lévy measure which is diffuse (continuous at each ).

For each the jump of at is

| (20) |

Hence, for each , and we can write

We want to apply the continuous mapping theorem and deduce the convergence in (14) from this. By Theorem 2.2, to apply the continuous mapping theorem it is enough to verify that there are no ties a.s. among the first largest positive jumps in the limit process . Let . We wish to show that . Denote by the th largest jump of up to time . Note that

Since is diffuse, we have for all . Thus, by (19) (with and replaced by and ),

So we can apply Theorem 2.2 as forecast and complete the proof.

Proof of Theorem 3.1, Part (ii) We first prove (15) and consider only the trimming operator ( is treated analogously.) By (20) we can write, for each and ,

Since is globally -continuous on by Proposition 2.2, we can apply the continuous mapping theorem to get that

in , as or . This completes the proof of (15).

Proof of Theorem 3.1, Part (iii) Again by (20), we have

Recall from Theorem 2.1 that is -continuous on , where

Thus, in order to apply the continuous mapping theorem, we need to show that . Note that , where

Hence, it is enough to show that , or, equivalently,

| (21) |

where denotes the th largest modulus jump of up till time .

To simplify notation, during the remainder of this proof, write for the modulus jumps , and for their ordered values in the intervals or , write or , , . We aim to show

| (22) |

from which (21) will follow immediately.

We consider first the case . Define a sequence of random times by

| (23) |

Since a.s., we have and a.s. On , we have , hence on the event ,

This implies that

Define , where denotes a point mass at . is a Poisson random measure on with intensity . Let

be the number of points which satisfy with . Then, recalling that , event has probability

| (24) | |||||

| (25) | |||||

| (27) | |||||

| (29) | |||||

| (30) |

In the second equality we used the compensation formula, and in the third we used a version of (19) appropriate to the . The last expression in (24) is 0 because is diffuse, so for all . This means, with probability , there are no tied values among the largest jumps in for all . (Note that this is ostensibly a much stronger statement than requiring there be no tied values among the largest jumps up until a fixed time .)

Next we consider . It is enough to show that . We restrict ourselves to the event , which we have proved has probability 1. On this event, there are no ties for the largest value among . Recall the definition of the sequence in (23). The largest jump remains constant on the interval . We aim to subdivide the interval so that the second largest jump up till time , which is strictly less than , is constant within that subinterval. First we consider the case when . Define for each ,

Note that as . Next define a further sequence in such that and for

Then we can decompose

| (31) |

When and , we have , hence

When and , , we have , hence

So the events on the RHS of (31) are subsets of

| (32) |

The probability of the event on the RHS of (5) can be computed in a similar way as in (24) to be 0. Hence, reverting to the original notation, we have

For , we can proceed iteratively with similar arguments to arrive at (22) hence (21). This completes the proof of (16).

6 Applications to Reinsurance

Many examples can be generated from the convergences in (14), (15) and (16) using the continuous mapping theorem. Here we mention one which is of particular interest in reinsurance. The idea is that the largest claim up to a specified time incurred by an insurance company (the “cedant”) is referred to a higher level insurer (the “reinsurer”). See Fan et al. [5] for details and references to the applications literature. This is known as the largest claim reinsurance (LCR) treaty: having set a fixed follow-up time , we delete from the process the largest claim occurring up to and including that time. We refer to Ladoucette and Teugels [7] and Teugels [13] for more detailed expositions.

The LCR procedure can be made prospective by implementing it as a forward looking dynamic procedure in real time, from the cedant’s point of view. Designate as time zero the time at which the reinsurance is taken out. The first claim arriving after time is referred to the reinsurer and not debited to the cedant. Subsequent claims smaller than the initial claim are paid by the cedant until a claim larger than the first (the previous largest) arrives. The difference between these two claims is referred to the reinsurer and not debited to the cedant. The process continues in this way so that at time , the accumulated amount referred to the reinsurer equals the largest claim up till that time. This procedure has the same effect as applying the “trim as you go” operator to the risk process. (It is also possible to apply “lookback” trimming to a reinsurance model in a natural way.)

A primary quantity of interest is the ruin time, at which the process describing the claims incoming to the company reaches a high level, . After reinsurance of the highest claims, the process is reduced to , with ruin time . Supposing is Lévy with heavy tailed canonical measure, , not uncommon assumptions in the modern insurance literature, we assume (12) with no centering necessary, and from the continuous mapping theorem immediately deduce an asymptotic distribution for as , and hence for , for high levels. Specifically, if (15) holds with and , then

where .

Acknowledgement We are grateful to Prof. Jean Jacod whose suggestion to YFI at the Building Bridges conference in Braunschweig 2013 started us on this pathwise analysis. Buchmann and Maller’s research was partially funded by ARC Grants DP1092502 and DP160104737. Yuguang Ipsen was formerly at the Australian Research Council Centre of Excellence for Mathematical and Statistical Frontiers, School of Mathematics and Statistics, University of Melbourne. She acknowledges support from the Australian Research Council. We are grateful also to two referees whose careful readings resulted in significant improvements to the paper.

References

- [1] Billingsley, P. (1999). Convergence of Probability Measures, 2nd edition. John Wiley & Sons, Inc.

- [2] Buchmann, B., Fan, Y. and Maller, R. A. (2016). Distributional representations and dominance of a Lévy process over its maximal jump processes. Bernoulli 22, 2325–2371.

- [3] Fan, Y. (2015). Convergence of trimmed Lévy process to trimmed stable random variables at small times. Stochastic Process. Appl. 125, 3691–3724.

- [4] Fan, Y. (2015). Tightness and convergence of trimmed Lévy processes to normality at small times. Journal of Theoretical Probability. DOI:10.1007/s10959–015–0658–0.

- [5] Fan, Y., Griffin, P., Maller, R., Szimayer, A. and Wang, T. (2017). The effects of largest claims and excess of loss reinsurance on a company’s ruin time and valuation. Risks 5, 3.

- [6] Jacod, J. and Shiryaev, A. N. (2003). Limit Theorems for Stochastic Processes. Springer-Verlag.

- [7] Ladoucette, S. A. and Teugels, J. L. (2006). Reinsurance of large claims. J. Comput. Appl. Math. 186, 163–190.

- [8] Maller, R. A. and Fan, Y. (2015). Thin and thick strip passage times for Lévy flights and Lévy processes. http://arxiv.org/abs/1504.06400.

- [9] Maller, R. A. and Mason, D. M. (2010). Small-time compactness and convergence behavior of deterministically and self-normalised Lévy processes. Trans. Amer. Math. Soc. 362, 2205–2248.

- [10] Maller, R. A. and Schmidli, P. (forthcoming). Small time almost sure behaviour of extremal processes. Advances in Applied Probability.

- [11] Silvestrov, D. S. and Teugels, J. L. (2004). Limit theorems for mixed max-sum processes with renewal stopping. Annals of Applied Probability 14, 1838–1868.

- [12] Skorokhod, A. V. (1956). Limit theorems for stochastic processes. Theory Probab. Appl. 1, 261–290.

- [13] Teugels, J. L. (2003). Reinsurance actuarial aspects. EURANDOM Report 2003-006, Technical University of Eindhoven, The Netherlands..

- [14] Whitt, W. (2002). Stochastic-process Limits, an Introduction to Stochastic-process Limits and their Application to Queues. Springer-Verlag.