A Stochastic Model of Optimal Debt Management and Bankruptcy

Alberto Bressan(∗), Antonio Marigonda(∗∗), Khai T. Nguyen(∗∗∗), and Michele Palladino(∗)

(*) Department of Mathematics, Penn State University

University Park, PA 16802, USA.

(**) Dipartimento di Informatica, Università di Verona, Italy

(***) Department of Mathematics, North Carolina State University, USA

Raleigh, NC 27695, USA.

A problem of optimal debt management is modeled as a

noncooperative game between a borrower and a pool of lenders,

in infinite time horizon with exponential discount.

The yearly income of the borrower is governed

by a stochastic process.

When the debt-to-income ratio reaches a given size ,

bankruptcy instantly occurs. The interest rate charged by the

risk-neutral lenders is precisely

determined in order to compensate for this possible loss

of their investment.

For a given bankruptcy threshold ,

existence and properties of optimal feedback

strategies for the borrower are studied, in a stochastic

framework as well as in a limit deterministic setting.

The paper also analyzes how the expected total cost to the borrower

changes, depending on different values of .

1 Introduction

We consider a problem of optimal debt management in infinite time horizon,

modeled as a noncooperative game between a borrower and a pool of risk-neutral lenders.

Since the debtor may go bankrupt, lenders charge a higher interest rate to offset the possible loss of part of their investment.

In the models studied in [7, 8], the borrower has a fixed income, but large values of the debt determine a bankruptcy risk.

Namely, if at a given time the debt-to-income ratio is too big, there is a positive probability that panic spreads among investors

and bankruptcy occurs within a short interval . This event is similar to a bank run.

Calling the random bankruptcy time, this means

Here the “instantaneous bankruptcy risk” is a given, nondecreasing function.

At all times , the borrower must allocate a portion of his income to service the debt, i.e.,

paying back the principal together with the running interest. Our analysis will be mainly focused on the existence and properties

of an optimal repayment strategy in feedback form.

In the alternative model proposed by Nuño and Thomas in [13], the yearly income is modeled as a stochastic process:

(1.1)

Here is an exponential growth rate, while denotes Brownian motion on a filtered probability space.

Differently from [7, 8], in [13] it is the borrower himself that chooses when to declare bankruptcy.

This decision will be taken when the debt-to-income ratio reaches a certain threshold , beyond which the burden of

servicing the debt becomes worse than the cost of bankruptcy.

At the time when bankruptcy occurs, we assume that the borrower pays a fixed price , while lenders recover a

fraction of their outstanding capital. Here is a

nondecreasing function of the debt size. For example, the borrower may hold an amount of collateral

(gold reserves, real estate) which will be proportionally divided among creditors if bankruptcy occurs. In this case,

when bankruptcy occurs each investor will receive a fraction

(1.2)

of his outstanding capital.

Aim of the present paper is to provide a detailed mathematical analysis of some models closely related to [13]. We stress that

these problems are very different from a standard problem of optimal control. Indeed, the interest rate charged by lenders is not given a priori.

Rather, it is determined by the expected evolution of the debt at all future times. Hence it depends globally on the entire feedback control

. A “solution” must be understood as a Nash equilibrium, where the strategy implemented by the borrower

represents the best reply to the strategy adopted by the lenders, and conversely.

Our main results can be summarized as follows.

•

We first assume that value at which bankruptcy occurs is a priori given, and seek an optimal feedback

control which minimizes the expected cost to the borrower.

For any value of the diffusion coefficient in (1.1), we prove that the problem admits at least one Nash equilibrium solution, in feedback form.

In the deterministic case where , the solution can be constructed by concatenating solutions of a system of two ODEs,

with terminal data given at .

•

We then study how the expected total cost

of servicing the debt together with the bankruptcy cost (exponentially discounted in time), are affected by different choices of .

Let be the salvage rate, i.e., the fraction of

outstanding capital that will be payed back to lenders if bankruptcy occurs when the debt-to-income ratio is .

If

(1.3)

then,

letting ,

the total expected cost to the borrower goes to zero.

On the other hand, if

(1.4)

then the total expected cost to the borrower remains uniformly positive as .

We remark that the assumption (1.4) is quite realistic.

For example, if (1.2) holds, then for all

large enough. We remark

that (1.4) rules out the possibility

of a Ponzi scheme, where the old debt is serviced by initiating more and more new loans. Indeed, if (1.4) holds, then

such a strategy will cause the total debt to blow up to infinity in finite time.

The remainder of the paper is organized as follows. In Section 2

we describe more carefully the model, deriving the equations

satisfied by the value function and the discounted bond price .

In Sections 3 and 4 we construct equilibrium solutions in feedback

form, in the stochastic case () and in the

deterministic case (), respectively.

Finally, Sections 5 and 6 contain an analysis of how the expected cost to the borrower

changes, depending on the bankruptcy threshold .

In the economics literature, some related models of debt and bankruptcy

can be found in [1, 3, 7, 11, 12]. A general introduction to Nash equilibria

and differential games can be found in [5, 6]. For the

basic theory of optimal control and viscosity solutions of Hamilton-Jacobi equations we refer to [4, 9].

2 A model with stochastic growth

We consider a slight variant of the model in [13]. We denote by the

total debt of a borrower (a government, or a private company)

at time .

The annual income of the borrower is assumed to be a

random process, governed by the stochastic evolution equation (1.1).

The debt is financed by issuing bonds. When an investor buys a bond of

unit nominal value, he receives a continuous stream of payments with intensity

. Here

•

is the interest rate payed on bonds, which we assume coincides with the discount rate,

•

is the rate at which the borrower pays back the principal.

If no bankruptcy occurs, the payoff for an investor will thus be

In case of bankruptcy, a lender recovers only a fraction of his outstanding capital. Here can depend on the total amount

of debt at the time on bankruptcy. To offset this possible loss, the investor buys a bond with unit nominal value at a discounted price .

As in [8, 13], at any time the value is uniquely determined by the competition of a pool of risk-neutral lenders.

We call the rate of payments that the borrower chooses to make to his creditors, at time . If this amount is not enough to

cover the running interest and pay back part of the principal, new bonds are issued, at the discounted price .

The nominal value of the outstanding debt thus evolves according to

(2.1)

The debt-to-income ratio is defined as . In view of (1.1) and (2.1), Ito’s formula [14, 15] yields the stochastic evolution equation

(2.2)

Here is the portion of the total income allocated to pay

for the debt.

Throughout the following we assume . We observe that, if ,

then the borrower’s income grows faster than the debt

(even if no payment is ever made).

In this case, with probability one the debt-to-income ratio would approach

zero as .

In this model, the borrower has two controls. At each time he can decide the portion of the total income which he allocates to repay the debt.

Moreover, he can decide at what time bankruptcy is declared.

Throughout the following, we consider a control in feedback form, so that

(2.3)

while bankruptcy is declared as soon as reaches the value .

The bankruptcy time is thus the random variable

(2.4)

At first, we let be a given upper bound to the size of the debt.

In a later section, we shall regard

as an additional control parameter, chosen by the borrower in order to minimize his expected cost.

Given an initial size of the debt,

the total expected cost to the borrower, exponentially discounted in time, is thus computed as

(2.5)

Here is a large constant, accounting for the bankruptcy cost,

while is the instantaneous cost for the borrower to implement the control .

In the following we shall assume

(A)

The cost function is twice continuously differentiable for

and satisfies

(2.6)

For example, one may take

for some .

Fix .

For a given initial debt , we define the corresponding value function as

(2.7)

Under the assumptions (A)

we have

(2.8)

Denote by

(2.9)

the Hamiltonian associated to the dynamics (2.2) and the cost function

in (2.5). Notice that, as long as , the function

is differentiable with Lipschitz continuous derivatives w.r.t. all arguments.

By a standard arguments,

the value function provides a solution to the second order ODE

(2.10)

with boundary conditions (2.8).

As soon as the function is determined, the

optimal feedback control is recovered by

By (A)

this yields

(2.11)

Assuming that lenders are risk-neutral, the discounted bond price is determined by

(2.12)

where denotes the salvage rate. In other words, if bankruptcy

occurs when the debt-to-income ratio is , then investors receive a fraction of the nominal value of their holding. Notice that

the random variable in (2.4) now

depends on the initial state , the threshold , and on the feedback control

.

By the Feynman-Kac formula, satisfies the equation

(2.13)

with boundary values

(2.14)

Combining (2.10) and (2.13),

we are thus led to the system of second order ODEs

(2.15)

with the boundary conditions

(2.16)

We close this section by collecting some useful properties of the Hamiltonian function.

Lemma 2.1.

Let the assumptions (A)

hold.

Then, for all and , the function in (2.9)

satisfies

(2.17)

(2.18)

Moreover, for every

the map is concave down and satisfies

(2.19)

(2.20)

(2.21)

Proof.

1.

Since is defined as the infimum of a family of affine functions, it is concave down.

We observe that

(2.9) implies

Taking in (2.9) we obtain the upper bound in (2.17).

By the concavity property, the map is non-increasing.

Hence (2.20) yields the upper bound in (2.18).

3.

Since for all , we have

and obtain the lower bound in (2.17). On the other hand, using the optimality condition, one computes from (2.9) that

(2.23)

where

Observe that, as , one has in (2.23).

The non-increasing property of the map yields the lower bound in (2.18).

4.

To prove (2.21) we observe that, in the first case,

there exists such that

Hence, letting we obtain

To handle the second case, we observe that, for large,

the minimum in (2.9) is attained at the unique point

where

. Hence and

MM

3 Existence of solutions

Let be given.

If a solution to the boundary value problem (2.15)-(2.16) is found,

then

the feedback control defined at (2.11) and the function

provide an equilibrium solution to the debt management problem.

In other words, for every initial value of the debt, the following holds.

(i)

Consider the stochastic dynamics (2.2),

with and .

Then for every the identity (2.12)

holds, where is the random bankruptcy time defined at (2.4) .

(ii)

Given the discounted price , for every initial data

the feedback

control is optimal for the stochastic optimization problem

To construct a solution to the system

(2.15)-(2.16),

we consider the auxiliary parabolic system

(3.2)

with boundary conditions (2.16).

Following [2], the main idea is to construct a compact, convex set of functions

which is positively invariant for the parabolic evolution problem.

A topological technique will then yield the existence of a steady state,

i.e. a solution to (2.15)-(2.16).

Theorem 3.1.

In addition to (A), assume that and

.

Then the system of second order ODEs (2.15) with boundary conditions

(2.16) admits a solution ,

such that is increasing and

is decreasing.

Proof.

1.

For any , consider the parabolic system

(3.3)

(3.4)

obtained from (3.2) by adding the terms ,

on the right hand sides. For any ,

this renders the system uniformly parabolic, also in a neighborhood of .

2.

Adopting a semigroup notation, let

be the solution of the system

(3.3)-(3.4), with initial data

(3.5)

Consider the

closed, convex set of functions

(3.6)

We claim that the above domain is positively invariant under the semigroup , namely

(3.7)

Indeed, consider the constant functions

Recalling (2.19), one easily checks that

is a supersolution and is a subsolution of the scalar

parabolic problem (3.3). Indeed

Similarly, is a supersolution and is a subsolution of the scalar parabolic problem (3.4).

This proves that, if the initial data in (3.5) take values in the box

, then for every the solution of the system

(3.3)-(3.4) will satisfy

(3.8)

for all . In turn, this implies

(3.9)

3.

Next, we prove that the monotonicity properties of and

are preserved in time.

Differentiating w.r.t.

one obtains

(3.10)

(3.11)

By (2.19), for every one has .

Hence is a subsolution of (3.10) and

is a supersolution of (3.11).

In view of (3.9), we obtain

This concludes the proof that

the set in (3.6)

is positively invariant for the system (3.3)-(3.4).

4.

Thanks to the bounds (2.17)-(2.18), we

can now apply Theorem 3 in [2] and obtain the existence of a steady state

for the system

(3.3)-(3.4).

We recall the main argument in [2]. For every the map

is a compact transformation

of the closed convex domain into itself. By Schauder’s

theorem it has a fixed point. This yields a periodic solution

of the parabolic system (3.3)-(3.4), with period .

Letting , one obtains a steady state.

5.

It now remains to derive a priori estimates on this stationary

solution, which will allow to take the limit as .

Consider any solution to

(3.12)

with increasing, decreasing, and satisfying the boundary conditions (2.16).

By the properties of derived in Lemma 2.1, we can find small enough

and such that the following implication holds:

As a consequence, if for some , then

the first equation in (3.12) implies .

We conclude that either for all , or else

attains its maximum on the subinterval .

By the intermediate value theorem, there exists a point

where

(3.13)

By (2.17), the derivative satisfies a differential inequality of the form

(3.14)

for suitable constants .

By Gronwall’s lemma, from the differential inequality (3.14) and the

estimate (3.13)

one obtains a uniform bound on , for all .

6.

Similar arguments apply to . By (2.18), the term in

(3.12) is uniformly bounded.

For every , by (3.12) shows that satisfies a linear ODE

whose coefficients remain bounded on , uniformly

w.r.t. . This yields the bound

for some constant , uniformly valid as .

To make sure that,

as , the limit satisfies the boundary value .

one needs to provide a lower bound on also in a neighborhood of , independent of . Introduce the constant

Then define

choosing so that .

We claim that the convex function

is a lower solution of the second equation in (3.12). Indeed, by

(3.12), one has

7.

Letting , we now consider a sequence

of solutions to (3.12) with

boundary conditions (2.16). Thanks to the previous estimates,

the functions are uniformly Lipschitz continuous on ,

while the functions are Lipschitz continuous

on any subinterval and satisfy

By choosing a suitable subsequence, we achieve the uniform convergence

, where are twice continuously differentiable

on the open interval , and satisfy the boundary conditions (2.16).

MM

4 The deterministic case

If , then the stochastic equation (2.2)

reduces to the deterministic control system

(4.1)

We then consider the deterministic Debt Management Problem.

(DMP)

Given an initial value of the debt,

minimize

(4.2)

subject to the dynamics

(4.1),

where the bankruptcy time is defined as in (2.4),

while

(4.3)

Since in this case the optimal feedback control and the corresponding functions

may not be smooth, a concept of equilibrium solution should be

more carefully defined.

Definition 4.1(Equilibrium solution in feedback form).

A couple of piecewise Lipschitz continuous functions and

provide an equilibrium solution to the debt management problem (DMP), with

continuous value function , if

(i)

For every ,

is the minimum cost for the optimal control problem

(4.4)

subject to

(4.5)

Moreover, every Carathéodory solution of (4.5) with is optimal.

(ii)

For every ,

there exists at least one solution of

the Cauchy problem

Notice that is the control that keeps the debt constant in time.

This value achieves the minimum in (4.9) when

This motivates the definition

(4.13)

On the other hand, if ,

then the function

is monotone increasing

and we define .

Observe that

(4.14)

We regard the first equation in (4.8) as an implicit ODE for the function . For every and , if , then this equation has no solution. On the other hand, when

the implicit ODE (4.8) can equivalently be written as

a differential inclusion (Fig. 1):

(4.15)

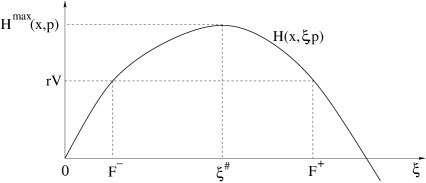

Figure 1: In the case where

, the the

Hamiltonian function has a global maximum

. For , the values

are well defined.

with the understanding that if .

Notice that is the total cost of keeping the debt constantly

equal to

(in which case there would be no bankruptcy and hence ).

Moreover,

denote by

the solution to the system of ODEs

(4.18)

with terminal conditions

(4.19)

Next, consider the point

(4.20)

and call the solution to the backward Cauchy problem

(4.21)

We will show that a feedback equilibrium solution to the

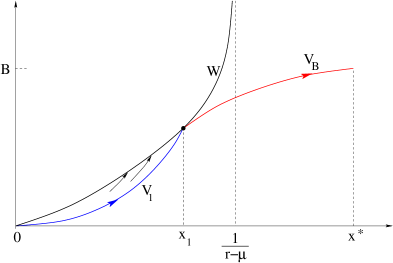

debt management problem is obtained as follows (see Fig. 2).

(4.22)

(4.23)

(4.24)

Figure 2: Constructing the equilibrium solution

in feedback form. For an initial value of the debt ,

the debt increases until it reaches , then it is held at the

constant value . If the initial debt is , the debt

keeps increasing until it reaches bankruptcy in finite time.

Theorem 4.3.

Assume that the cost function satisfies the assumptions (A), and moreover .

Then the functions in (4.22)–(4.24) are well defined, and provide an equilibrium solution to the

debt management problem, in feedback form.

Proof.

1.

The solution of (4.18)-(4.19) satisfies

the obvious bounds

We begin by proving that the function

is well defined

and strictly positive for .

To prove that

assume, on the contrary, that for some .

By the properties of the function (see Fig. 1) it

follows

(4.25)

for some constant and all , . Hence, for any solution of (4.18),

implies for all ,

providing a contradiction.

Next, observe that the functions are locally Lipschitz continuous

as long as .

Moreover, implies

Therefore, the functions are well defined on the

interval .

2.

If the construction of the functions

is already completed in step 1..

In the case where , we claim that

the function is well defined and satisfies

(4.26)

Indeed, if for some , the Lipschitz property

(4.25) again implies that for all .

This contradicts the terminal condition in (4.21).

To complete the proof of our claim (4.26),

it suffices to show that

(4.27)

This is true because

3.

In the remaining steps, we show that provide an equilibrium solution. Namely, they satisfy the properties (i)-(ii)

in Definition 4.1.

To prove (i), call the value function

for the optimal control problem (4.4)-(4.5).

For any initial value, , in both cases and ,

the feedback control in (4.24)

yields the cost . This implies

To prove the converse inequality we need to show that, for any measurable control , calling the solution to

The construction described at (4.22)–(4.24) uniquely determines a feedback equilibrium solution to the debt management problem.

In general, however, we cannot rule out the possibility that a second solution exists. Indeed, if the solution

of (4.18)-(4.19) can be prolonged backwards to the entire interval , then we could replace (4.22)-(4.23)

simply by , for all . This would yield a second solution.

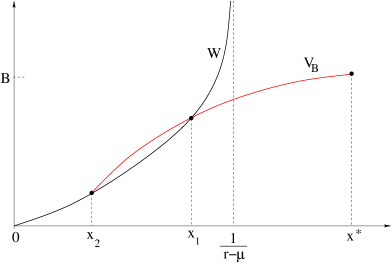

We claim that no other solutions can exist.

This is based on the fact that the graphs of and

cannot have any other intersection, in addition to and .

Indeed, assume on the contrary that for some

(see Fig. 3). Since and

, the inequalities

yield a contradiction.

Next,

let be

any equilibrium solution and define

Then

•

On the functions

provide a solution to the backward Cauchy problem (4.18)-(4.19).

•

On the function provides the value function

for the optimal control problem

subject to the dynamics (with )

and the state constraint for all .

The above implies

Since must be continuous at

the point , by the previous analysis this is possible only

if or .

Figure 3: By the monotonicity properties of the Hamiltonian function in (4.9), the graphs of and cannot have

a second intersection at a point .

5 Dependence on the bankruptcy threshold .

In this section we study the behavior of the value function

when the maximum size of the debt, at which bankruptcy is declared,

becomes very large.

For a given , we denote by ,

the solution to the system (4.18) with terminal data

(4.19).

Letting , we wish to understand whether the value function remains positive, or

approaches zero uniformly on bounded sets.

Toward this goal, we introduce the constant

Solving the above ODE with the terminal data ,

,

we obtain

(5.11)

hence

Recalling (5.4), a direct computation yields (5.8).

The upper and lower bounds for in (5.9) now

follow from (5.5) and the inequality

.

MM

Corollary 5.3.

Assume that

(5.12)

Then the value function satisfies

(5.13)

Indeed, for we have , and

(5.13) follows from the second inequality in (5.9). When , since

the map is nondecreasing, we have

Corollary 5.4.

Assume that

(5.14)

Then

(5.15)

Moreover, the followings holds.

(i)

If

(5.16)

then

(5.17)

(ii)

Assume that there exist such that

(5.18)

for all sufficiently large.

Then, for each , there exists an optimal value

such that

(5.19)

Proof.

It is clear that (5.15) is a consequence of (5.9) and (5.14). We only need to prove (i) and (ii).

For a fixed , we consider the functions of the variable alone:

for all large enough.

Hence there exists some particular value where

the function attains its

global minimum. This yields (5.19).

MM

6 Dependence on in the stochastic case

In this section we study how the value function depends on the

bankruptcy threshold , in the stochastic case

where .

Extensions of Corollaries 5.3 and 5.4,

will be proved, constructing upper and lower bounds

for the solution , of

the system (2.15)-(2.16), in the form

(6.1)

1.

We begin by constructing a suitable pair of functions .

Let be the solution to the

backward Cauchy problem

This follows from (6.9), (6.12) and Theorem 6.1.

MM

7 Concluding remarks

If we allow , then the equations

(4.8) admit the trivial solution

, , for all .

This corresponds to a Ponzi scheme, producing a debt whose size grows exponentially, without bounds. In practice, this is not realistic because there is a maximum amount of liquidity

that the market can supply. It is interesting to

understand what happens when this bankruptcy threshold

is very large.

Our analysis has shown that three cases can arise, depending on

the fraction of outstanding capital that lenders can recover.

(i)

If ,

then it is convenient to choose as large as possible.

By delaying the time of bankruptcy, the expected

cost for the borrower,

exponentially discounted in time, approaches zero.

(iii)

If and (5.16) holds then it is still

convenient to choose as large as possible. However,by delaying the time of bankruptcy, the cost to the borrower remains uniformly positive.

(iii)

If and (5.18) holds, then for every initial value

of the debt there is a choice of the bankruptcy threshold which is optimal for the borrower.

Examples corresponding to three cases (i)–(iii) are obtained

by taking

(7.1)

with , , or , respectively.

It is important to observe that the choice

of the optimal bankruptcy threshold is never “time consistent”.

Indeed, at the beginning of the game the borrower announces

that he will declare bankruptcy

when the debt reaches size . Based on this information, the lenders determine the discounted price of bonds.

However, when the time comes when ,

it is never convenient for the borrower to declare bankruptcy.

It is the creditors, or an external authority, that must enforce

termination of the game.

To see this, assume that at time when the borrower

announces that he has changed his mind, and

will declare bankruptcy only at

the later time when the debt reaches . If he chooses a control for , his discounted cost

will be

This new strategy is thus always convenient for the borrower.

On the other hand, it can be much worse for the lenders.

Indeed, consider an investor having a unit amount of outstanding capital at time . If bankruptcy is declared at time , he will recover

the amount . However, if bankruptcy is declared

at the later time , his discounted payoff will be

To appreciate the difference, consider the

deterministic case, assuming that

is the function in (7.1), with , and that

. By the analysis at the beginning of Section 5, we have

for all .

Replacing with in (5.4) we obtain that the solution to (5.3)

with terminal data

satisfies

If the investors had known in advance that bankruptcy is declared at (rather than at ),

the bonds would have fetched a smaller price.

In conclusion, if the bankruptcy threshold is chosen by the debtor,

the only Nash equilibrium can be . In this case,

the model still allows bankruptcy

to occur, when total debt approaches infinity in finite time.

References

[1] M. Aguiar and G. Gopinath,

Defaultable debt, interest rates and the current account.

J. International Economics69 (2006), 64–83.

[2]

H. Amann,

Invariant sets and existence theorems for semilinear parabolic equation and elliptic system, J. Math. Anal. Appl.65, 432–467,

1978.

[3] C. Arellano and A. Ramanarayanan,

Default and the maturity structure in sovereign

bonds. J. Political Economy120 (2102), 187–232.

[4]

M. Bardi and I. Capuzzo Dolcetta, Optimal Control and Viscosity

Solutions of Hamilton-Jacobi-Bellman Equations, Birkhäuser, 1997.

[5] T. Basar and G. J. Olsder, Dynamic Noncooperative

Game Theory, Edition, Academic Press, London 1995.

[6] A. Bressan,

Noncooperative differential games. Milan J. Math.79 (2011), 357–427.

[7]

A. Bressan and Y. Jiang,

Optimal open-loop strategies in a debt management problem,

submitted.

[8]

A. Bressan and Khai T. Nguyen,

An equilibrium model of debt and bankruptcy, ESAIM; Control, Optim. Calc. Var., to appear.

[9]

A. Bressan and B. Piccoli, Introduction to the Mathematical

Theory of Control,

AIMS Series in Applied Mathematics, Springfield Mo. 2007.

[10] M. Burke and K. Prasad,

An evolutionary model of debt.

J. Monetary Economics49 (2002) 1407-1438.

[11]

G. Calvo, Servicing the Public Debt: The Role of Expectations.

American Economic

Review78 (1988), 647–661.

[12]

J. Eaton and M. Gersovitz, Debt with potential repudiation:

Theoretical and empirical analysis. Rev. Economic Studies48 (1981), 289–309.

[13] G. Nuo and C. Thomas,

Monetary policy and sovereign debt vulnerability,

Working document n. 1517, Banco de España Publications, 2015.

[14]

B. Oksendahl, Stochastic Differential Equations: An Introduction with Applications.

Springer-Verlag, 2013.

[15]

S. E. Shreve, Stochastic calculus for finance. II.

Continuous-time models. Springer-Verlag, New York, 2004.