Crises and Physical Phases of a Bipartite Market Model

Abstract

We analyze the linear response of a market network to shocks based on the bipartite market model we introduced in dehmamy2014classical , which we claimed to be able to identify the time-line of the 2009-2011 Eurozone crisis correctly. We show that this model has three distinct phases that can broadly be categorized as “stable” and “unstable”. Based on the interpretation of our behavioral parameters, the stable phase describes periods where investors and traders have confidence in the market (e.g. predict that the market rebounds from a loss). We show that the unstable phase happens when there is a lack of confidence and seems to describe “boom-bust” periods in which changes in prices are exponential. We analytically derive these phases and where the phase transition happens using a mean field approximation of the model. We show that the condition for stability is with being the inverse of the “price elasticity” and the “income elasticity of demand”, which measures how rash the investors make decisions. We also show that in the mean-field limit this model reduces to a Langevin model bouchaud1998langevin for price returns. Thus we provide analytical support for the power of the model in classifying the stability of markets where it’s applicable.

I Inroduction

Economical and financial systems are attractive to physicists because of their highly dynamic and complex structure which is generally much more challenging as a complex system than systems exhibiting a high degree of symmetry studied in traditional physics. The goal of this paper is to derive analytical results regarding the physics and phases of a model we developed for quantifying the linear response in a bipartite, dynamical network. While our discussion will exclusively concern a largely simplified financial network and its mean-field behavior, a similar methodology based on an “effective theory” approach could be employed in analyzing the response of many other dynamical bipartite networks. Especially networks pertaining to resources and agents using resources, such as power grids and some special food webs, might benefit from a similar type of modeling.

The global financial crisis that followed which started around 2007 made it clear to us how limited our understanding of the dynamics of financial markets are. In recent years, economists seem to have acknowledgement the fact that we cannot predict the real world dynamics with idealized assumptions and we need to account for complex relations of different players in an economical system. Scholars have started consider the network of such interactions and how they may affect business cycles, cause cascades, or contagion. Gale2 ; acemoglu2012network . Our goal here is to make a first attempt at quantitatively modeling the continuous dynamics of a market system in the simplest form and to lowest order. In an earlier paper we introduced a bipartite network model for investment markets in which investors traded assets in a fashion similar to common stock markets dehmamy2014classical . The assumption of the market being a bipartite network is, of course, a major simplification. In reality, there undoubtedly exist many strong financial interactions among investors and even among assets. In our paper dehmamy2014classical the major investors were banks or other major financial institutions. It should be noted that interbank lending network is a very complex and important, multiplex network and much research has been dedicated to it (see furfine2003interbank ; upper2011 ; bargigli2016interbank ; farboodi2014intermediation and references therein).

Our simplified bipartite model, which has “assets” as one layer and “investors” on the other side, ignoring all intra-layer connections, was constructed in order to assess the first order response dynamics of a market to any change. In this model neither money nor number of shares is conserved, as investors are assumed to trade with entities both inside and outside the network – though such conservation laws can be imposed if needed. The weighted connections indicate the amount of investments. The details of the model and the phenomenological derivation for it are explained in the dehmamy2014classical . The goal of this paper is to derive analytical results about the stability conditions for such market dynamics.

There are many different models for financial networks Haldane ; allen2000financial ; Kok ; kok2 ; kok3 each assessing a different aspects of connectivity which use familiar assumptions about dynamics in of prices based on existing economic models. Our model, on the other hand, is at its core what we call an “effective theory” in physics. It attempts to model the dynamics of a market by making minimal assumptions about details and assuming system-wide parameters. It only uses the microscopic behavior of agents as input. The demonstration of the genericity of our model is the subject of another forthcoming paper lagrangian .

Perhaps the closest model to ours in the context bipartite model of investment networks was introduced by Caccioli et al. caccioli2014stability . As will become clear in the derivations below, our model in fact also reduces to a Langevin equation’s model for price-dynamics in a stock market introduced by Bouchaud bouchaud1998langevin . There the authors argue that the price dynamics near the onset of a crisis is simlar to a damped harmonic oscillator plus non-linear terms that become relevant after the phase transition to an unstable phase. Our model has such non-linear naturally from the start and no extra assumption is needed. In another forthcoming paper we will discuss the application of our model in stock markets in detail.

Our model relies on 2 behavioral parameters, one for supply/demand and one for investor decisions. Over time-scales where the behavioral parameters are not changing much, we are arguing that the large scale dynamics of the market can modeled and simulated. It is in this regime that our model may provide cucial insight into stability of a market and serve as a tool for regulators.

II Model and Notation

We will refer the model as the Group-Impulse Portfolio-Sharing Investment (GIPSI) model henceforth. In essence the GIPSI model summarizes how investors and their brokers may behave on average in a market, if they are aware of the market news.

Investors

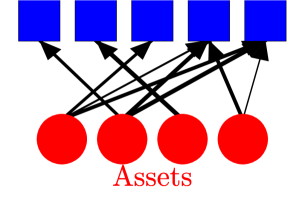

We will approximate the investiment market as a bipartite network as shown in Fig. 1. On one side we have the “Assets,” which are what is traded, and on the other we have the “Investors” that own the assets. The “assets” are labeled using Greek indices . To each asset we assign a “price,” at time . The “investors” are labeled using Roman indices . Each investor has an “equity” , a time , i.e. their net worth. Each investor has a portfolio, meaning differing amounts of holdings in each of the asset types. The amount of asset that investor holds is denoted by , which is essentially an entry of the weighted adjacency matrix of the bipartite network.

We assume that there is a group-impulse in the decision-making, the so-called “herding effect” devenow1996rational ; bikhchandani2000herd where all agents will have the same level of panic or calmness in a situation. They will adjust their portfolio by looking at the gains or losses they incurred recently. So one of the equations is a generalization of a simple portfolio adjustment protocol

We argue that, if the assumption Their level of panic is reflected in the so-called “Income elasticity of demand”, which we will denote as . This assumption has been critisized by some scholars as being unrealistic based on other empirical evidence about “fire sales” shleifer2011fire , claiming that the leverage (i.e. ratio of investments to equity) . Our justification for this assumption is based on a mean field assumption. We believe that most of these institutions will be leveraged to close to the maximum amout allowed by regulations, thus having similar leverage. Aside from that, if the assumption of herding holds for response to a rapid change, using the same factor makes sense for at least the mean field behavior of the system.

The supply and demand equation for the prices has a similar structure

where would be what is usually called “price elasticity” in economics. There is also a third equation which is related to how trading, i.e. changes the equity of an investor, which turns out to be dehmamy2014classical . A crucial point for having a more realistic model for such systems is the fact that there is a response time associated with each of these equations. describing how each of the variables , and evolve over time. A key feature of our model is that the weights of links are time-dependent, and this introduces dynamics into our network.

For brevity, we define . The equations of the GIPSI model may be written as

| (1) | ||||

| (2) | ||||

| (3) |

where has the meaning of external force. where is the time-scale in which investors respond to a change in their net worth, and is the time-scale of market’s response.

The importance of this model as a lowest order approximation of linear response in a market system is the subject of a separate paper in preparation lagrangian ; dehmamy2016graduate . But just to motivate the use of this model, we only note that the lowest order effective Lagrangian model (in the spirit of Landau-Ginzburg models) for the response of a market defined by the dynamical variables and plus dissipation yields equations with the structure of (1)-(3).

| symbol | denotes |

|---|---|

| Holdings of investor in asset at time | |

| Normalized price of asset at time () | |

| Equity of bank at time . | |

| Inverse price elasticity | |

| Income elasticity of demand (rashness) |

III Confidence in the market in terms of based on market response

The simple strategies devised above are expected to describe the linear response of the market in the mean-field approximation. The sign of may be considered an indicator for confidence in the market: positive means in response to a loss (i.e. ) the investor sells assets (i.e. ). This can be interpreted as the investor fearing more losses and therefore reducing their holdings. By the same token negative may signal confidence in the market as it indicates a willingness to buy more shares when the investor has lost money.

Note that the GIPSI model Eq. (1)–(3) are response euation, i.e. they yield no dynamics of there is no change in the variables . To assess the behavaior of this system we will introduce an initial shock to the system. We do this by assuming a delta function change in equity for some investor , meaning that at agent either gained or lost money from outside the market and it’s decision to trade in the market triggers the response of the market 111It turns out that the qualitative behavior of the final state after a shock to the system is only weakly sensitive to the value of the response times . The response times only need to be nonzero. As we will show analytically below, the phase of the system is determined by the two behavioral couplings and . The plots shown below are for ..

For the empirical analysis we will use the same Eurozone crisi data we used in the original paper dehmamy2014classical which consists of sovereign bonds of five European countries, namely Greece Italy, Ireland, Portugal and Spain (GIIPS), as assets and the network of major banks and financial institutions who purchased and traded these bonds. Many smaller players and the European Central Bank (ECB) that also participated in the trades are not in this data and their existence justifies the non-conservation of the total amount of holdings in the network. They are also partly responsible for dissipation in the dynamics. The data is given in the appendix of dehmamy2014classical .

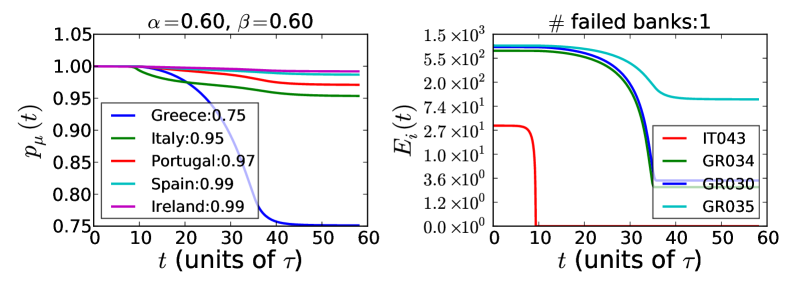

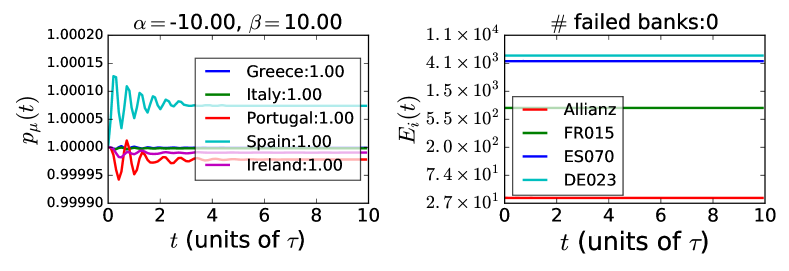

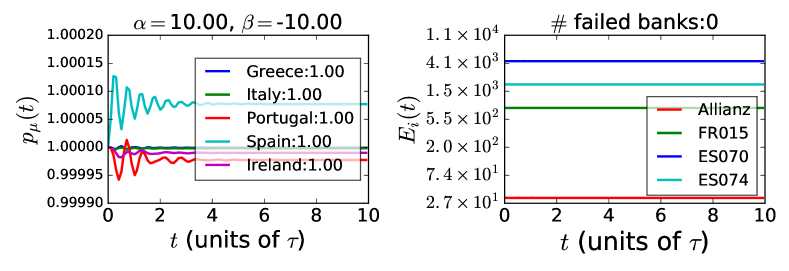

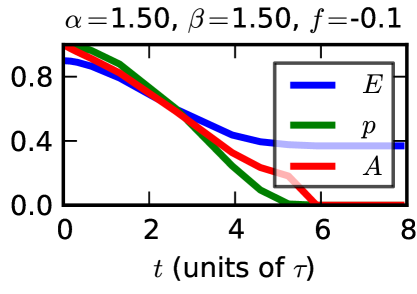

Fig. 2 shows 4 examples of choices for and and the response of the prices and equities of banks to a shock to a random bank in the system 222It turns out that, similar to a system in the thermodynamic limit, the details of which bank is shocked through doesn’t matter in the final state of the systemdehmamy2014classical .. As we will show below, all these choices fall in the “stable” regime, though the losses incurred from a negative shock (i.e. ) are much larger in magnitude when and have the same sign than when they have opposite signs. The upper left plot in Fig. 2 is for and . This is what one normally expects from this system: means if a bank incurs a loss, they try to make up for it by making money from selling assets; means if there is selling pressure (more supply than demand) the prices will go down. There are, however, cases where the opposite happens. Negative values for and are possible in the real world and are known as “contrarian” behavior. For example, a contrarian investor is someone who invest more in asset when they actually lose money on asset . This happens a lot when there is confidence in the market and investors believe the price will rebound. The market may also sometimes behave in a contrarian fashion, when there is an anticipation of good news that overcomes the selling pressure, or when other investors outside our Eurozone GIIPS network (such as smaller investors or the ECB) are actually exerting a buying pressure.

As is seen in Fig. 2 this results in price slightly oscillating around its original value. This trust mechanism plays an important role in the stability of the market. It requires that one side (either investor or the prices) behaves in a contrarian fashion and the other side behaves normally.

IV Phases and Confidence

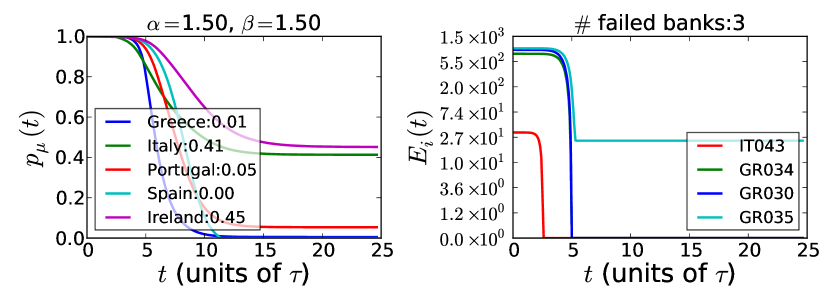

As we see the behavior of prices and equities in the case where the product is positive and negative differ qualitatively. When negative shocks () cause a noticeable drop in prices and some equities333All of are positive quantities and we do not allow them to go negative., whereas when there is only oscillation and the final values of and are very close to their original values.

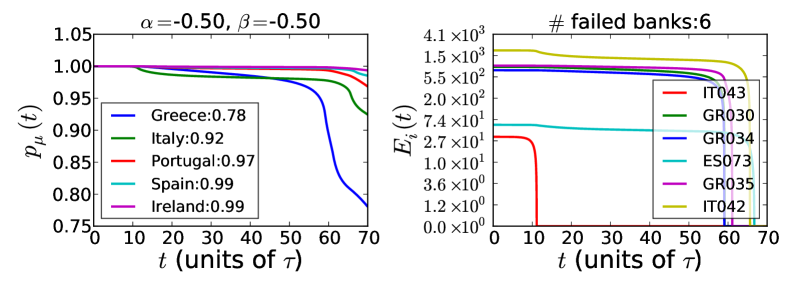

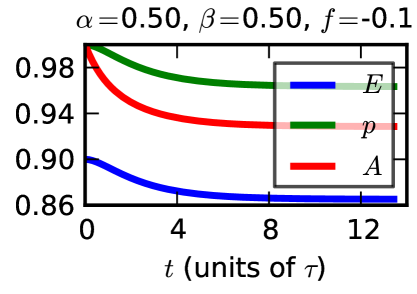

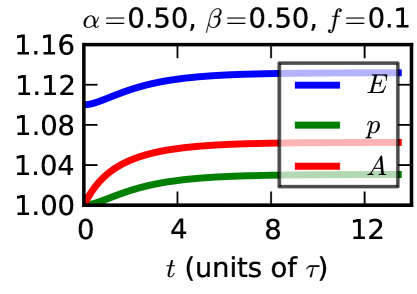

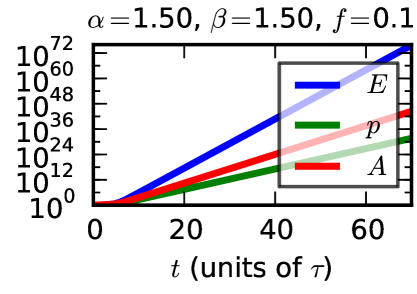

There is, however, another qualitatively different regime which is not shown in Fig. 2. This happens when and is shown in Fig. 3. In fact, this qualitative difference becomes much clearer when we show the effect of a positive shock to the system in Fig. 4. There we see that when after a positive shock eventually stops growing and reaches a new equilibrium, whereas when all three variables grow exponentially, indefinitely. In other word an economic “bubble” forms. So if it lasts for a long time either forms a bubble or results in a crash.

This leads to the following conclusions:

-

1.

When no investor goes bankrupt, but also the amount of money lost or generated during the trading is negligible. This makes these regimes (where either the investors or the market is contrarian, but not both) good for preventing failures, but they are very undesirable for profit making.

-

2.

When the system does not show oscillation but eventually settles into new equilibrium states not far from the original situation. Negative shocks may cause bankruptcy of some investors, depending on how their assets compares to their equity initially.

-

3.

When , negative shocks cause exponential drops in assets and equities. If persists there will be a crisis. Positive shocks may form bubbles and periods of exponential growth.

IV.1 The full phase diagram

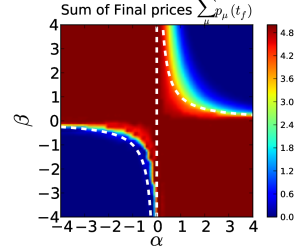

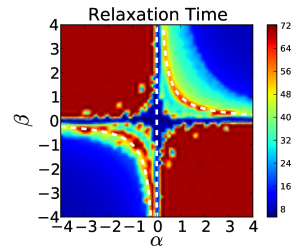

Fig. 5 shows an example of the average final prices and relaxation time for the system for various values of and . It seems the system has two prominent phases: One in which a new equilibrium is reached without a significant depreciation in all of the GIIPS holdings (upper left and lower right quadrants), and one where all GIIPS holdings become worthless (above dashed line in the upper right quadrant and all of lower left quadrant). In both the first and the third quadrants in the transition region the relaxation time becomes very large, which means that the forces driving the dynamics become very weak. Both the smoothness and the relaxation time growth seem to be signalling the existence of a second order phase transition. The phase transition seems to be described well by:

Now we do a systematic numerical analysis of different phases of this phenomenological model. We identify to phases and what appears to be a second order phase transition between them. We then modify the equations (1)–(3) and analytically derive the condition for the phase transition. The GIIPS data is very heterogeneous, in the sense that for each of these European countries there are generally less than a handful of investors who hold more than half of the total sovereign debt of that country. If we make a mean field assumption and break the network apart, assuming there is one major investor for each asset , we can treat that as a 1 investor 1 asset system and try to derive the phases in that case. As we show below, the 1 by 1 system, despite not having the richness of the networked system in terms of the details of the final state, nevertheless exhibits the same phases. In addition we are able to analytically derive the phase transitions.

V Analytical derivation of the mean-field phase space

In the mean-field approach described above, we are dealing with a 1 investor by 1 asset system with a single and . We can combine Eqs. (1)–(3) in a 1 by 1 system by taking another derivative from (2). This way we can eliminate most occurrences of and an find an equation for (see Appendix A) which has some non-linear terms in it.

Defining the “return” as the fundamental variable, the nonlinearities are roughly of type . In short, the equations are

| (4) | ||||

| (5) |

As we show in Appendix A none of the nonlinearities on the r.h.s. can be large in the stable phase where . We also show there that becomes its value plus other nonlinear terms that cannot be large when and For a small shock we may safely use . Thus for a time-scale where and is not changing much we are essentially dealing with a damped harmonic oscillator. Notice that equation (5) is almost identical to what Bouchaud proposes in bouchaud1998langevin to explain the 1987 crash.

Although depends on and , we can use an approximate exponential ansatz . The solutions to are:

Thus we get three regimes:

-

1.

When there will be oscillatory solutions. This happens when For this is just the condition we observed for oscillations in our simulations.

-

2.

When , i.e. we have decaying solutions but both . Therefore the changes won’t be large and eventually the sytems settles in new equilibrium.

-

3.

When , i.e. we will have two real solutions for with opposite signs. The presence of the positive root signals an instability because this solution diverges.

Thus we have proven the existence of the three phases we had observed earlier and dervied the transition conditions analytically. It is easy to prove that in the unstable phase both exponents appear in the solution: The return is

Since at the initial conditions dictated we have and therefore both solutions appear with equal strength. It follows that whenever one of the solutions ( in our case) is positive the solution diverges. When a bubble forms and grows exponentially and when , because our variables are non-negative, the price just crashes to zero. This proves that the sufficient condition for stability is . Also note that the nonlinear terms are all proportional to and therefore at

and so the solution is exact at . The details of the derivations as well as the nonlinear terms are given in Appendix A.

In Appendix B we provide another, direct proof for the phase transition being at using exponential ansatz for all three variables

We then show that near the phase transition the exponents in show that the near the phase exponents for all three need to be the same. Moreover, as can be seen in the right figure in Fig. 5 near the phase transition the time-scale of the system’s evolution is very long compared to other time-scales in the system and thus much longer than in (5), meaning

This leads to a massive simplification of the equations and yields

as the phase transition point, which for infinitesimal shocks recovers .

VI Conclusion

We have shown that the GIPSI model dehmamy2014classical for response dynamics of a bipartite investment market exhibits three phases: two stable phases, one of which is oscillatory the other logistic-like; one unstable phase with indefinite exponential decay or growth depending on the initial perturbation. The unstable phase can exist in real world, though it must be short-lived. It can describe “boom-bust” periods: crisis periods (as was shown in dehmamy2014classical ) or periods of rapid growth, so-called “bubbles”. We also derive these phases analytically from a mean-field version of the model. The mean-field equations become almost identical to the Langevin equations proposed by Bouchaud bouchaud1998langevin which could well describe behavior of markets near crashes. The non-linear terms required for the transition in Bouchaud’s model exist naturally in the GIPSI model and nothing new needs to be added by hand.

VII acknowledgments

We thank the European Commission FET Open Project “FOC” 255987 and “FOC-INCO” 297149, NSF (Grant SES-1452061), ONR (Grant N00014-09-1-0380, Grant N00014-12-1-0548),DTRA (Grant HDTRA-1-10-1-0014, Grant HDTRA-1-09-1-0035), NSF (Grant CMMI 1125290), the European MULTIPLEX and LINC projects for financial support. We also thank Stefano Battiston for useful discussions and providing us with part of the data. The authors also wish to thank Matthias Randant and others for helpful comments and discussions, and especially Fotios Siokis for sharing important points about the data and the Eurozone crisis. S.V.B. thanks the Dr. Bernard W. Gamson Computational Science Center at Yeshiva College for support.

References

- [1] Daron Acemoglu, Vasco M Carvalho, Asuman Ozdaglar, and Alireza Tahbaz-Salehi. The network origins of aggregate fluctuations. Econometrica, 80(5):1977–2016, 2012.

- [2] F. Allen, , and D. (2007). Gale. Systemic risk and regulation. in the risks of financial institutions. (pp. 341-376). University of Chicago Press.

- [3] Franklin Allen and Douglas Gale. Financial contagion. Journal of political economy, 108(1):1–33, 2000.

- [4] Leonardo Bargigli, Giovanni di Iasio, Luigi Infante, Fabrizio Lillo, and Federico Pierobon. Interbank markets and multiplex networks: centrality measures and statistical null models. In Interconnected Networks, pages 179–194. Springer, 2016.

- [5] Sushil Bikhchandani and Sunil Sharma. Herd behavior in financial markets. IMF Economic Review, 47(3):279–310, 2000.

- [6] J-P Bouchaud and Rama Cont. A Langevin approach to stock market fluctuations and crashes. The European Physical Journal B-Condensed Matter and Complex Systems, 6(4):543–550, 1998.

- [7] Fabio Caccioli, Munik Shrestha, Cristopher Moore, and J Doyne Farmer. Stability analysis of financial contagion due to overlapping portfolios. Journal of Banking & Finance, 46:233–245, 2014.

- [8] Nima Dehmamy. Effective lagrangian model of bipartite market response. in preperation, 2016.

- [9] Nima Dehmamy. First Principles and Effective Theory Approaches to Dynamics of Complex Networks. PhD thesis, Boston University, PhD Dissertation, 2016.

- [10] Nima Dehmamy, Sergey V Buldyrev, Shlomo Havlin, H Eugene Stanley, and Irena Vodenska. Classical mechanics of economic networks. arXiv preprint arXiv:1410.0104, 2014.

- [11] Andrea Devenow and Ivo Welch. Rational herding in financial economics. European Economic Review, 40(3):603–615, 1996.

- [12] Maryam Farboodi. Intermediation and voluntary exposure to counterparty risk. Available at SSRN 2535900, 2014.

- [13] Craig Furfine. Interbank exposures: Quantifying the risk of contagion. Journal of Money, Credit, and Banking, 35(1):111–128, 2003.

- [14] G. Hał aj, , and C. Kok. Assessing interbank contagion using simulated networks. Computational Management Science: 1-30., 2013.

- [15] G. Hał laj, , and C. Kok. Modeling emergence of the interbank networks. European Central Bank Working Paper, forthcoming, 2013.

- [16] A. G. Haldane and R. M. May. Systemic risk in banking ecosystems. Nature 469, 351-355, 2011.

- [17] M. Montagna, , and C. Kok. Multi-layered interbank model for assessing systemic risk. No. 1873. Kiel Working Paper, 2013.

- [18] Andrei Shleifer and Robert Vishny. Fire sales in finance and macroeconomics. The Journal of Economic Perspectives, 25(1):29–48, 2011.

- [19] Christian Upper. Simulation methods to assess the danger of contagion in interbank markets. Journal of Financial Stability, 7(3):111–125, 2011.

Appendix A Analytical results from the 1 Investor vs 1 Asset system

Here we present the analytical solution to the 1 by 1 model and derive the curve where the phase transition is happening in figure 5. At any time the equations for a 1 by 1 system become

| (6) | ||||

| (7) |

Below we will try to find the condition for a phase transition in the solutions to these equations.

We can try to eliminate and . We first need to find the expression for first. Taking another derivative from the second equation yields

| (8) |

combining this with the first equation results in:

| (9) | |||

| (10) |

where the nonlinear term is again quadratic in (thus a generalized form of the Fisher equation) and looks like

| (11) | ||||

| (12) |

Below we will also show that in the stable regime the non-linearity in the frequency, namely the term, is of the order and thus remains small if we show that at small times the behavior of in the stable regime is oscillating around zero.

This time the dynamics is richer and we have a damped oscillator with a driving force coupled to and nonlinearities of type . Taking the return as the fundamental variable, the nonlinearities are roughly of type . In short, the equations are

| (13) | ||||

| (14) | ||||

| (15) |

Although depends on and , we can use an approximate time dependent exponential ansatz . The solutions to are:

When and there will be oscillatory solutions. For example when , which only happens for negative we have such oscillatory solutions. This is consistent with the simulations which showed the oscillatory behavior was in the quadrants. For the stability, however we care about the real solutions.

When , which happens when , we will have two real solutions with opposite signs. The presence of the positive root signals an instability because the solution diverges. For a delta function shock of magnitude at we found that:

Having initially scaled to , the condition for existence of the positive root becomes:

This dependence on the shock magnitude is normal, as a strong enough kick can kick a particle out of a local minimum. The shock can be arbitrarily small and therefore the absolute condition for stability is as we anticipated

| (16) |

Now the question is, which solution does the system pick when it is shocked. The return is

Since at the initial conditions dictated we have

And therefore both solutions appear with equal strength. It follows that whenever one of the solutions ( in our case) is positive the solution diverges. When a bubble forms and grows exponentially and when , because our variables are non-negative, the price just crashes to zero. This proves that the sufficient condition for stability is . Also note that the nonlinear terms are all proportional to and therefore at

and so the solution is exact at .

A.1 Validity of perturbation theory near the phase transition

For the above solution to be valid we must confirm that the corrections are small. We must find a small parameter that exists in the neglected terms which allows perturbative solutions to be viable. We had two sets of nonlinearities: (1) ; (2) .

A.1.1 the non-linearity

First let us examine the nonlinear terms in . Note that the instability happens when the larger root becomes positive. Thus near the transition we have

| (17) | ||||

| (18) | ||||

| (19) |

And so being close to the phase transition means . The consequence of this is that for we get (using the found above)

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) | ||||

| (25) |

A.1.2 The non-linearity

We wish to examine if the assumption that in the stable regime remain small is a consistent assumption, thus making perturbative expansion valid. Any term above non-linear in is thus higher order in this approximation. We wish to find the part of that is linear in the first time derivative. In the stable regime changes are slow and thus a short time after the shock we can expand the variables in Taylor series near . Again, we will rescale the variables at to . Using the (3) we get

| (27) | ||||

| (28) | ||||

| (29) |

Thus the assumption of smallness of the derivatives is consistent and we may use perturbation theory and safely discard the non-linear terms in finding the stability conditions. This way the stability condition is just having a positive in (16). One can also check the stability by explicitly using the exponential ansatz found above as is given in what follows.

Appendix B Proof for using properties of the phase transition

Since we have coupled second order equations, the solutions may be estimated using an exponential ansatz as follows. Equations (1) and (2) are second order and therefore will naturally have two solutions for and . Also, since , will also have two modes. Therefore the exponential ansatz must have at least two exponents. Thus for each of the three variables we have:

In principle the exponents can be time-dependent, but we will first try and see f there are asymptotically exponential solutions. Thus we assume that they vary slowly with time. By choosing the units of to be such that at , and the shocked equity is , the boundary conditions that we had become:

and:

| (30) | ||||

| (31) | ||||

| (32) |

At the phase transition we expect the greater exponents, which we take to be , to become small relative to other time-scales in the problem, i.e. , and change sign from negative (which would result in exponential decay) to positive (which results in divergence of ). This means that close to the phase transition:

From the initial conditions, this results in:

| (33) | ||||

| (34) | ||||

| (35) |

For we have a little more details.

Which for small shocks reduces to:

Now back to the equations (1)-(3). First let us reexamine the third equation (3). The effect of a delta function shock is the above and . Since and we can neglect . The last equation becomes:

| (36) | ||||

| (37) | ||||

| (38) | ||||

| (39) |

For arbitrary this relation can only hold if . Thus we define:

Let us also get an estimate for , the smaller exponent in . We will go very close to the transition line where . From Eq. (1) we have:

With an exponential ansatz the left hand side is:

The greater root is and the smaller root is . Even away from the transition line we approximately have:

Thus we can approximate the expression for to:

This way Eq. (3) becomes

| (41) |

Eq. (1) becomes

| (42) |

Which again only holds if . Thus

Again, note that the condition for being close to the transition point was:

Discarding higher than linear order terms in and looking at times yields:

| (43) |

Performing the same procedure on Eq. (2) results in (since )

| (44) | ||||

| (45) | ||||

| (46) |

And so, the condition for the phase transition becomes:

Now, taking the shock to zero results in a phase transition at:

| (47) |