Julien Guyon

, Romain Menegaux

Bloomberg L.P., Quantitative Research

and Marcel Nutz

Columbia University, Departments of Statistics and Mathematics

Abstract.

We derive sharp bounds for the prices of VIX futures using the full information of S&P 500 smiles. To that end, we formulate the model-free sub/superreplication of the VIX by trading in the S&P 500 and its vanilla options as well as the forward-starting log-contracts. A dual problem of minimizing/maximizing certain risk-neutral expectations is introduced and shown to yield the same value.

The classical bounds for VIX futures given the smiles only use a calendar spread of log-contracts on the S&P 500. We analyze for which smiles the classical bounds are sharp and how they can be improved when they are not. In particular, we introduce a family of functionally generated portfolios which often improves the classical bounds while still being tractable; more precisely, determined by a single concave/convex function on the line. Numerical experiments on market data and SABR smiles show that the classical lower bound can be improved dramatically, whereas the upper bound is often close to optimal.

In this article, we derive sharp bounds for the prices of VIX futures by using the full information of S&P 500 smiles at two maturities. The VIX (short for volatility index) is published by the Chicago Board Options Exchange (CBOE) and used as an indicator of short-term options-implied volatility. By definition, the VIX is the implied volatility of the 30-day variance swap on the S&P 500; see [9]. Equivalently, using the well-known link between realized variance and log-contracts [21], the VIX at date is the implied volatility of a log-contract that delivers at , where days and is the S&P 500 at date :

we are assuming zero interest rates, repos, and dividends for simplicity. The log-contract can itself be replicated at using call and put options on the S&P 500 with maturity .

The VIX index cannot be traded, but VIX futures can: the VIX future expiring at is an instrument that pays at . While can be replicated, its square root cannot; instead, sub/superreplication in the S&P 500 and its options leads to model-free lower/upper bounds on the price of the VIX future.

The classical sub/superreplication argument is based on the fact that one can replicate any affine function of at using cash and log-contracts with maturities and . Thus, one searches for the sub/superreplication of the square root function by an affine function that gives the maximum/minimum portfolio price. Since the square root is a concave function, it is below all its tangent lines, and the classical superreplication boils down to selecting the line that gives the minimum portfolio price. This argument shows that, in the absence of

arbitrage, the price of the VIX future at time cannot exceed the implied volatility

of the forward-starting log-contract on the index,

starting at the VIX future’s expiry and maturing at ,

Subreplicating the VIX future using the same instruments corresponds to subreplicating the square root by an affine function. This yields zero as a lower bound for the future’s price, which is clearly a poor estimate.

These classical bounds are suboptimal in the sense that they only use the prices of log-contracts. Our aim is, instead, to extract the full information contained in the S&P 500 smiles at and , by also including all vanilla options at these maturities as (static) hedging instruments, as well as trading (dynamically, i.e., at ) in the S&P 500 itself and the forward-starting log contract. Moreover, we allow the deltas at to depend on the information available, that is, the S&P 500 and the VIX index at .

The first part of the paper analyzes this problem for general smiles. We formulate the sub/superreplication as a linear programming (LP) problem and define absence of arbitrage in this setting. The latter leads to the existence of risk-neutral joint distributions for which constitute the domain of an optimization problem dual to sub/superreplication (Theorem 3.4). The first two marginals and are given by the market smiles at and , whereas the distribution of merely satisfies a certain constraint. The dual problem is thus reminiscent of a (constrained) martingale optimal transport problem, but falls outside the transport framework because the third marginal is not prescribed. This necessitates a novel argument for our duality theorem which establishes the absence of a duality gap (Theorem 4.1), i.e., primal and dual problem have the same value. This theorem holds, more generally, for an option payoff rather than just the VIX. As a last abstract contribution, we characterize those smiles for which the classical bounds for the VIX future are optimal (Theorems 5.1 and 5.2). The lower bound is optimal if and only if , which never happens in practice. The characterization for the upper bound is more subtle, it states that a convex-order condition in two dimensions holds, or equivalently that a model with constant forward volatility is contained in the dual domain.

While our theoretical bounds are sharper than the classical ones, the corresponding hedging portfolios can only be found numerically, and the numerical problem is far from trivial. Aiming for a balance between flexibility and tractability, we introduce a family of functionally generated portfolios that are determined by a one-dimensional convex/concave function and a constant (Definition 6.3). The space of one-dimensional convex functions is easy to search numerically, and the generated portfolios are guaranteed to satisfy the sub/superhedging conditions at all values of the underlying, by our construction. We show that the lower price bound obtained by functionally generated portfolios improves the classical one as soon as (Proposition 6.4) and here the generating function can be chosen explicitly of an inverse “hockey stick” form.

In the second part of the paper, we study specific families of smiles and corresponding portfolios. The case where is a Bernoulli distribution gives rise to a “complete market” where the VIX future can be replicated. While the classical upper bound is not sharp unless has a very particular form, we show how functionally generated portfolios lead to the sharp bound as given by the unique risk-neutral expectation (Section 7). When is a general distribution with compact support, we present various sufficient conditions for the classical upper bound to be suboptimal (Section 8). Finally, we discuss a family of examples for which the classical upper bound is already sharp (Section 9).

The third part of the paper presents numerical experiments using smiles from market data as well as smiles generated by a SABR model. We compare the classical bounds, the bounds obtained from functionally generated portfolios, and the bounds computed by an LP solver that correspond to the theoretical, optimal bounds modulo discretization error. For the generating functions, we use piecewise linear maps and a cut square root; the latter yields the best approximation in our experiments. The results suggest that the classical lower bound can be improved dramatically by functionally generated portfolios; the bound from the LP solver is only slightly better. On the other hand, the classical upper bound is already surprisingly sharp for typical smiles.

Turning to the existing literature on volatility derivatives, the most closely related work is due to De Marco and Henry-Labordère [12] who investigate bounds for VIX options, i.e., calls and puts on the VIX, given the smile of the S&P 500 and the VIX future as liquidly tradable instruments. Thus, compared to [12], we take a step back by investigating bounds for the VIX future itself, given the smile of the S&P 500. The sub/superreplication problem in [12] leads to a linear program with a dual akin to (constrained) martingale optimal transport. The numerical results show that, for typical market smiles, the optimal upper bound on VIX options is equal to an analytical (a priori suboptimal) bound that the authors derive. For a further discussion of numerical solutions to sub/superreplication problems, we also refer to [16], and to [2, 15] for background on martingale optimal transport. While [12] and the present paper consider derivatives on options-implied volatility, previous literature has studied derivatives on realized volatility. Using power payoffs, Carr and Lee [6] show that, if the returns and the volatility of an asset are driven by independent Brownian motions, the asset smile at a given maturity determines the distribution of the realized variance at , hence allowing perfect replication of derivatives on realized variance. Using business-time hedging, Dupire [13] derives a lower bound for a call on realized variance at a given maturity , given the asset smile at . Carr and Lee [7] extend Dupire’s idea to tackle the cases of puts on realized variance as well as forward-starting calls and puts on realized variance. More recently, Cox and Wang [10] have derived the optimal portfolio subreplicating convex functions of realized variance. While these works assume that the underlying has continuous paths, Kahalé [20] considers the model-free hedging of discretely monitored variance swaps based on squared logarithmic returns in a setting where the underlying may have jumps, and thus perfect hedging is not possible despite dynamic trading in the underlying. The optimal subhedging price and a corresponding hedge are obtained. This analysis has been extended by Hobson and Klimmek [17] who consider both sub- and superhedging; moreover, they study a variety of variance swap contracts and dynamic trading can be constrained to discrete rebalancing dates in their setting. The authors link this problem to Perkins’ solution of the Skorokhod embedding problem and derive optimal price bounds and hedging strategies.

The remainder of the article is structured as follows. Section 2 describes the primal problems of sub/superreplication and recalls the classical bounds on VIX futures, while absence of arbitrage and existence of risk-neutral measures are characterized in Section 3. In Section 4 we formulate the dual problem of maximizing over risk-neutral expectations and prove the absence of a duality gap. Next, we characterize in Section 5 the market smiles for which the classical bounds on VIX futures are already sharp.

In Section 6 we introduce the functionally generated portfolios and show that they essentially always improve the classical lower bound. The subsequent sections study examples where the classical upper bound is not optimal, when the smile is a two-point distribution (Section 7) or more generally a distribution with compact support (Section 8). On the other hand, Section 9 provides smiles for which the classical upper bound is optimal. Finally, numerical experiments using SABR and market smiles are presented in Section 10.

2. Primal problem and classical bounds

2.1. Setting and notation

For simplicity, we assume zero interest rates, repos, and dividends. Moreover, we take as given the full market smiles of the S&P 500 index at two maturities and

days, that is, the continuum of all call prices for strikes . For each maturity , , absence of static arbitrage (or butterfly arbitrage) is equivalent to the existence of a risk-neutral measure such that the price of any vanilla option written on is the expectation of the payoff under , and we shall refer to as a smile as well. (The notation refers to the second derivative measure of the convex function .)

In particular, the price of at time 0 must be the initial value of the S&P 500. Therefore, throughout the article, denotes the identity on and

, are probability measures on with mean .

Absence of dynamic (calendar) arbitrages will be discussed in Section 3.

We call forward-starting log-contract (FSLC for short) the financial derivative that pays

at , where days. We recall that, by definition of the VIX (substituting the strip of out-the-money

options by the log-contract for simplicity), the price at

of the FSLC is , the square of the VIX at . For the log-contracts to have finite prices, the following is in force throughout the paper.

Assumption 2.1.

The given marginals satisfy

For convenience, we set

Moreover, we denote by

(2.1)

the price at time 0 of the FSLC. As we will recall in Section 3, absence

of dynamic arbitrage implies that and are in convex

order. Then, , and if

and only if , as is strictly convex.

2.2. The primal problem

We consider a market with two trading dates ( and ) where the financial instruments are the S&P 500 (tradable at and ), the vanilla options on it with maturities and (tradable at ), and the FSLC (tradable at ). Note that we consider only static positions in vanilla options, but we allow dynamic trading, that is, trading at , in the S&P 500 and the FSLC. We are interested in deriving the optimal lower and upper bounds on the price of the VIX future expiring at , given these instruments.

Similarly as in De Marco and Henry-Labordère [12], the model-independent

no-arbitrage upper bound for the VIX future is the smallest price at time 0 of a superreplicating portfolio,

(2.2)

where is the set of integrable superreplicating portfolios,

i.e., the set of all measurable functions with , that satisfy the superreplication constraint

(2.3)

This linear program is known as the primal problem; stands for “primal” and stands for the value of

the VIX at the future date . At time , delta-hedging in

the S&P 500 and in the FSLC is allowed.

The respective deltas, and ,

may depend on the values and of the S&P 500 and the

VIX at . Since the price at

of the FSLC is , the delta strategies are costless, and the price of the portfolio is . Similarly, the lower bound on the VIX future is the largest price of a subreplicating portfolio,

(2.4)

where is the set of integrable subreplicating portfolios, defined like but with the opposite inequality

(2.5)

We shall see in Remark 4.9 that the portfolios could also be required to be continuous, without changing the values of and .

Remark 2.2.

CBOE [9] actually uses a finite number of out-the-money options to approximate the log profile. If this trapezoidal approximation were known at time , our analysis would apply to the real VIX formula by simply substituting the approximation for the log profile in the constraints (2.3) and (2.5). However, the list of out-the-money options used in the official VIX formula depends on the locations of zero bid quotes and hence varies over time, so the approximation used for computing the official VIX at time is only known at . Maturity interpolation is another practical concern if no options with maturity are quoted. Then CBOE considers the two closest quoted maturities and straddling and interpolates linearly the corresponding variance swap variances. Sub/superreplication then requires trading options with maturities and . Instead, our idealized setting corresponds to interpolating the and smiles and trading only in the synthetic options.

Remark 2.3.

An analogous linear program can be studied if the payoffs and are replaced by general payoffs and , where denotes the price at of . In particular, bounds for options written on the price at of forward-starting calls or puts can be found using the same approach.

2.3. The classical bounds for VIX futures

Suppose for the moment that as defined in (2.1) is nonnegative, as will be the case in the absence of arbitrage. Then,

it is well known that

(2.6)

Indeed, if , the portfolio given by

(2.7)

has price and belongs to because

This corresponds to the superreplication

of a straight line () by a tangent parabola (), or, equivalently, to the superreplication of the square root () by its tangent line at . If , one can simply replace

by an arbitrarily small in (2.7), showing that . Similarly, canceling the dependency of the left-hand side of the subreplication constraint (2.5)

on yields

Thus, the classical lower bound is trivial. In the following sections, we shall investigate how to obtain bounds sharper than the interval .

3. Arbitrages and martingale measures

In this section, we define (dynamic) arbitrage and relate its absence to the existence of certain risk-neutral measures.

A model-free arbitrage is usually defined as a strategy that has a negative price at time 0 and generates a nonnegative payoff at the final horizon . We shall distinguish two types of arbitrages.

An -arbitrage is an arbitrage that only trades in the S&P 500 and its vanilla options. More precisely, let be the set of measurable functions with , such that

then an -arbitrage is an element of such that .

An -arbitrage, on the other hand, also trades in the FSLC at . Let be the set of measurable functions with , , such that

then an -arbitrage is an element of such that .

Since any such element can be scaled, we observe that there is an -arbitrage in the market if and only if

and the analogue with holds for -arbitrages.

Clearly, absence of -arbitrage implies absence of -arbitrage, and we shall see in Theorem 3.4 that they are in fact equivalent. Before that, let us introduce the risk-neutral measures that are dual to the portfolios.

Definition 3.1.

We denote by the set of all martingale laws on with marginals

and , i.e., probability measures such that

For ,

(3.1)

is the price at of the FSLC under , and we denote by

the subset of all such that is -a.s. constant. In this case, necessarily -a.s.

Next, we define a set of measures on the extended space , where the last coordinate will accommodate the VIX at . With a mild abuse of notation, we write for the identity on this space.

Definition 3.2.

Let be the set of all the probability

measures on such

that

(3.2)

Note that for all , we have

(3.3)

More precisely, extending the definition (3.1) of to , we have

(3.4)

that is, projecting the VIX squared onto functions of always yields . Moreover, Jensen’s inequality implies

(3.5)

To relate the spaces and , we introduce the following notation. For , let be the projection of onto the first two coordinates, i.e.,

(3.6)

and let be the projection onto the third coordinate. Thus, and under . Conversely, let , then we denote by

the law of under . Recalling (3.5),

is the unique probability

distribution on such that and -a.s. The following is an immediate consequence of the tower property.

Lemma 3.3.

(i)

If , then .

(ii)

If , then .

While elements of are interpreted as general joint models for the S&P and the VIX, the second part of the lemma shows that elements of can be seen as special models of a “local volatility” type where the VIX is a function of . Finally, elements of are even more particular models where this function is constant; they are of “Black–Scholes” type as far as the forward volatility is concerned.

We can now formulate the main result of this section, stating that absence of arbitrage is equivalent to the existence of risk-neutral measures. More precisely, absence of -arbitrages and -arbitrages turns out to be equivalent, meaning that the possibility of trading the FSLC at does not add any restriction in our model-free setting. Hence, we will simply speak of absence of arbitrage in later sections.

Theorem 3.4.

The following assertions are equivalent:

(i)

The market is free of -arbitrage,

(ii)

the market is free of -arbitrage,

(iii)

,

(iv)

,

(v)

and are in convex order, i.e., for any convex function .

Proof.

We show (ii) (i) (v) (iii) (iv) (ii); the first implication is obvious. To see that (i) (v), assume that there exists a convex function such that . By convexity,

for all , where denotes the right derivative of . As a consequence, the portfolio

is an -arbitrage. The implication (v) (iii) is Strassen’s theorem [24] and (iii) (iv) is a direct consequence of Lemma 3.3(ii). Finally, let us prove that (iv) (ii). Let and let . Using (3.2), the price of this portfolio at time 0 is

and as consequence, the market is free of -arbitrage.

∎

Remark 3.5.

Since and are probabilities on the real line with the same mean, they are in convex order

if and only if for all , i.e., calls with maturity are cheaper than calls with maturity . See, e.g., [14, Theorem 2.58] for a proof.

4. Duality

In this section, we introduce the dual problems to sub/superreplicating the VIX and prove the absence of a duality gap as well as the existence of an extremal model. We let

(4.1)

These dual problems are of a non-standard type. Indeed, while maximizing (or minimizing) over is the “martingale optimal transport” problem (see, e.g, [2, 4, 15]), the optimization over is quite different since one marginal (the law of the third component ) is not prescribed. The marginal is merely required to satisfy (3.2) and in particular, (4.1) is not a constrained Monge–Kantorovich transport problem.

Formally, the dual problem (4.1) arises by permuting the inf and sup operators (written here for the superreplication problem) as shown below, where denotes the set of nonnegative measures on and acts as the set of Lagrange multipliers associated with the superreplication constraint:

The second equality stems from the fact that (a) if then the term is nonnegative for all , hence the term is equal to , and (b) otherwise the term can be made as large and negative as desired by picking and letting tend to , where are such that constraint (2.3) is violated, so the term is equal to . The fourth equality uses that (a) if then for all unconstrained the curly bracket term is equal to , and (b) otherwise the curly bracket term can be made as large and negative as desired by picking a convenient or or or depending on which of the four conditions (3.2) defining is not satisfied, so the infimum term is equal to .

It is well known that such a formal duality may fail for infinite dimensional linear programming problems. Next, we shall establish rigorously the absence of a duality gap for general options ; this does not cause additional work compared to the VIX future.

We extend the definition of the dual problem to

and similarly extend and by writing instead of on the right-hand side of (2.3).

Theorem 4.1.

Let be upper semicontinuous and satisfy

(4.2)

for some constant . Then

Moreover, if and only if , and in that case the supremum is attained.

Choosing , this shows in particular that there is no duality gap for the superreplication of VIX futures, and that a worst-case model exists. The analogue for the subreplication follows by considering .

In view of Theorem 3.4, we also obtain yet another characterization for the absence of arbitrage.

Corollary 4.2.

The following assertions are equivalent:

(i)

The market is arbitrage-free,

(ii)

,

(iii)

.

Several duality results related to ours where previously obtained in [2, 3, 4, 12], among others. In our setting, the fact the one marginal of the measures in is not prescribed, combined with the non-compactness of the state space, necessitates a novel technique of proof.

4.1. Proof of the duality theorem

In the rest of this section, we report the proof of Theorem 4.1 in several steps; the strategy is to reduce our duality to a tailor-made auxiliary duality via the Minimax Theorem. Apart from having no duality gap, the auxiliary duality needs to satisfy two requirements: its constraints should be less restrictive than the ones of the original problem, and they need to be strong enough to imply the continuity and compactness properties needed for the application of the Minimax Theorem.

The growth condition (4.2) immediately implies that if and only if is empty. Thus, we may focus on the case , and then (4.2) implies that is finite.

4.1.1. Superhedge for a superlinearly growing function of

The main aim of this step is to find a superlinearly growing function of which can be superhedged at a finite price. This will be crucial to prepare the ground for the Minimax Theorem later on.

Lemma 4.3.

There exists a function of superlinear growth such that and . Moreover, can be chosen convex, strictly increasing, and to satisfy .

Proof.

The existence of follows from (the proof of) the de la Vallée–Poussin theorem [11, Theorem II.22] and Assumption 2.1.

∎

Lemma 4.4.

There exists a continuous, increasing function with and such that setting , we have

(4.3)

for all .

Proof.

Let ; then the desired inequality (4.3) is equivalent to

for all . Let for and extend this function to by setting for . Then,

by the convexity and symmetry of . Thus, it is sufficient to find such that

(4.4)

Indeed, define

(4.5)

Then is nonnegative and concave, and for all . This inequality is trivial for , so that

In particular, choosing and , we see that (4.4) is satisfied.

It follows from (4.5) that is increasing, implies that , and the superlinear growth of yields that .

∎

4.1.2. An auxiliary duality

Let be a measurable space and let be the set of all probability measures on . It is well known that infinite-dimensional linear programming duality fails in general, and often topological conditions are used to obtain a positive result. The following lemma holds in the space of measurable functions without any topology; instead, it is based on two features: finite-dimensional Lagrange multipliers and the no-arbitrage type condition (4.6). Thus, it is in the spirit of the robust duality results provided in [5] for equality constraints and in [1] for inequality constraints. We use the notation .

Lemma 4.5.

Let be measurable and such that for all ,

(4.6)

Moreover, let

(4.7)

For any measurable function , we have

and the infimum is attained if it is finite.

Proof.

This is a special case of the one-step duality result in [1, Theorem 4.3]. Indeed, let be the set of all probability measures on ; then (4.6) is the robust no-arbitrage condition of [1, 5]. Moreover, if we see as the increment of a stock price vector over a single period, then is precisely the set of supermartingale measures for . The lemma then follows from [1, Theorem 4.3] once we note that a set which is -null for all is necessarily empty since includes the Dirac measures at all points of .

∎

Remark 4.6.

Condition (4.6) is necessary for the validity of Lemma 4.5. Indeed, let and . We consider the butterfly and put payoffs

which are bounded continuous functions on . Then, and hence . However, the infimum equals one because for any whereas . In particular, there is a duality gap.

We shall apply the lemma as follows. Let and let be its Borel -field. Moreover, let be the function introduced in Lemma 4.3 and let

where and is the price of the right-hand side in (4.3) as implied by and ,

Let . Since the functions all have strictly negative values at the point , the no-arbitrage condition (4.6) holds.

We define as in (4.7). Moreover, let be the cone consisting of all functions of the form for some . Lemma 4.5 yields the following.

Corollary 4.7.

Let be measurable. Then

4.1.3. Proof of duality for VIX options

We shall apply Corollary 4.7 in combination with the Minimax Theorem. For that, we need the following facts.

Lemma 4.8.

The set is weakly compact. Moreover, if is as in Theorem 4.1, then is weakly upper semicontinuous on .

Proof.

To see that is closed, let converge weakly to . Let and note that is continuous and bounded from below. Hence, is bounded and for . In view of , it follows that and then monotone convergence yields , i.e., .

The tightness of follows from

and

(4.8)

indeed, the above is bounded by for all . Thus, compactness holds by Prokhorov’s theorem.

Given , the semicontinuity of implies the semicontinuity of , by the Portmanteau theorem. To see that is semicontinuous as well, we pass to the limit using the growth condition on , the superlinear and superquadratic growth of and , respectively, and (4.8).

∎

We have now prepared all the tools for the proof of the main result.

We first show that the supremum is attained. Indeed, note that is a closed subset because the defining conditions (3.2) are determined by bounded continuous test functions. Thus, it is weakly compact by Lemma 4.8 which also shows that is weakly upper semicontinuous and thus attains its supremum on .

Next, we turn to the duality. Let us write for the set of all functions of the form

where and are measurable. Note that is a linear space. Moreover, we let (resp. ) be the subspace consisting of those functions whose coefficients are continuous (resp. continuous and bounded). By the definition of the primal problem, we then have

Using Lemma 4.4 and in particular the definition of , we see that for every there exists such that . Together with the fact that is a linear space, that yields the first equality in

where the last step used Corollary 4.7 applied to the function with a fixed ; note that is upper semicontinuous and satisfies (4.2). Hence, by Lemma 4.8, the linear mapping is weakly upper semicontinuous on the weakly compact set . On the other hand, is linear on for fixed . In particular, is “concave-convexlike” in the sense of [23] and it follows via the Minimax Theorem in the form of [23, Theorem 4.2] that

By linearity of , we have if , and since for , we conclude that

As a consequence, .

It remains to prove the converse inequality. Let and ; thus

Taking expectations on both sides yields

and as and were arbitrary, it follows that . This completes the proof that .

∎

Remark 4.9.

One consequence of the above proof is that , i.e., the value of the primal problem does not change if we require the functions to be continuous.

4.2. Local volatility property of the superreplication price

The following result shows that the superreplication bound for the VIX future can be computed on the dual side by merely maximizing over models of “local volatility” type, i.e., models of the form for some , with the notation introduced above Lemma 3.3.

This property greatly simplifies the computation of ; it is particular to superreplication of the VIX because it is based on the concavity of the square root.

Proposition 4.10.

We have

Proof.

We have by Lemma 3.3 and the second equality holds by the definition of . To see the converse inequality, let and consider ; cf. (3.6) for the notation. Then, using (3.4) and the concavity of the square root,

As was arbitrary, the result follows.

∎

5. Characterization of market smiles for which the classical bounds are optimal

In this section, we characterize the market smiles for which the classical upper bound and the classical lower bound from Section 2.3 are already optimal.

Let us first consider the subreplication problem; here our result shows that the classical bound is never sharp in practice.

Theorem 5.1.

We have if and only if .

Proof.

Assume that , thus and the infimum defining is attained (Theorem 4.1). Hence, there exists such that . Since -a.s., this means that -a.s. and thus by (3.3), whence . Conversely, if , let be the law of under . Then and , so that .

∎

Next, we consider the superreplication problem where the characterization turns out to be nondegenerate. We recall that two distributions on are said to be in convex order if

for any convex function .

Theorem 5.2.

The following assertions are equivalent:

(i)

,

(ii)

there exists such that -a.s.,

(iii)

,

(iv)

and are in convex order,

(iv’)

and are in convex order.

Proof.

(i) (ii)

By Theorem 4.1, the supremum defining is attained, so there exists

such that .

Thus, by (3.3), which by the strict convexity of the square implies -a.s.

(ii) (iii) Let be

such that -a.s. By Lemma 3.3(i), the projection of onto the first two coordinates belongs to , and

As a consequence, and in particular

(iii) (iv) (iv’) Let us define and as well as

Then, is precisely the set of probability measures

on such that

By Strassen’s theorem [24], this set is nonempty if and only if and are in convex order, which yields the equivalence of (iii) and (iv), and then also of (iv’) due to .

(iii) (i)

Let and recall the definition of above Lemma 3.3. Since and

-a.s., we have . Conversely, by (2.6).

∎

The necessary and sufficient conditions in Theorem 5.2 are not straightforward to check given the marginals. While the convex ordering of two measures on can be verified by computing the one-parameter family of call option prices, cf. Remark 3.5, no simple family of test functions exists in two or more dimensions. See also Johansen [18, 19] and Scarsini [22] for more precise (negative) results.

Thus, we are interested in simpler criteria, at the expense of not being sharp. The following is a condition that involves only call and put prices, and we shall give more conditions in the context of the examples in Sections 8 and 9.

Proposition 5.3.

Denote by and the prices at time 0 of the call and put options with maturity and strike . Let

where

If there exists such that ,

then .

Proof.

By Theorem 5.2, a necessary condition for

is that and

are in convex order. Since ,

this is equivalent to

where denotes the

price of the out-the-money option, i.e., if

and otherwise. Since , we have and

Therefore, the necessary condition for can be stated as for all .

If this condition is not met, then since by (2.6).

∎

6. A family of functionally generated portfolios

In this section, we introduce a new family of portfolios that sub/superreplicate the VIX. Their main merits are their simple functional form and that their sub/superreplication property is guaranteed by construction for all values of the underlying—in contrast to numerical solutions of the linear programming problems.

While these portfolios are not optimal in general, i.e., their prices do not attain and , they often improve the classical bounds from Section 2.3, in particular the lower bound. In specific examples, they even turn out to be optimal, as we shall see in the subsequent sections.

Our portfolios are based on concave/convex payoffs of both the S&P 500 and its logarithm. Let us start with superreplicating portfolios. For a convex function

and , we denote by

the smallest function

such that for all and .

Moreover, we denote by the right

derivative of with respect to its -th argument.

As mentioned in Section 5, the space of convex functions in two dimensions is still intractable. Thus, we specialize further to the form

(6.2)

where is a (one-dimensional) convex function and . (Adding a constant in front of does not increase the generality.)

Definition 6.3.

Let be convex (concave) and . The portfolio defined by Proposition 6.1 (Proposition 6.2) based on is called the superreplicating (subreplicating) portfolio generated by and .

We call these portfolios functionally generated because they are determined by a single real function and a constant. As convex functions on are well approximated by linear combinations of call payoffs, is is easy to search numerically over a representative subset of this class. Of course, any functionally generated portfolio is superreplicating as a special case of Proposition 6.1, and the analogue holds for subreplication using concave functions.

The classical superreplication portfolio (2.7) corresponds to the particular

case where ; that is, is a linear function and , so that does not depend on the first variable . Indeed, in this case, we have

, , and .

For to be finite, one must choose ,

in which case .

Minimizing

Our portfolios are more general in that we consider a convex function of rather than a linear function of . We remark that it is meaningless to consider functions of the first variable alone:

for to be finite, must depend

on the second variable and in fact be unbounded.

Let and be the sets of all convex functions on and , respectively.

The two families of superreplicating portfolios considered above correspond to the price bounds

(6.3)

which satisfy

the expectation of a non-integrable function is read as in the above formulas.

For the analogous definitions in the subreplication problem, exchanging convex/concave as well as inf/sup, we have .

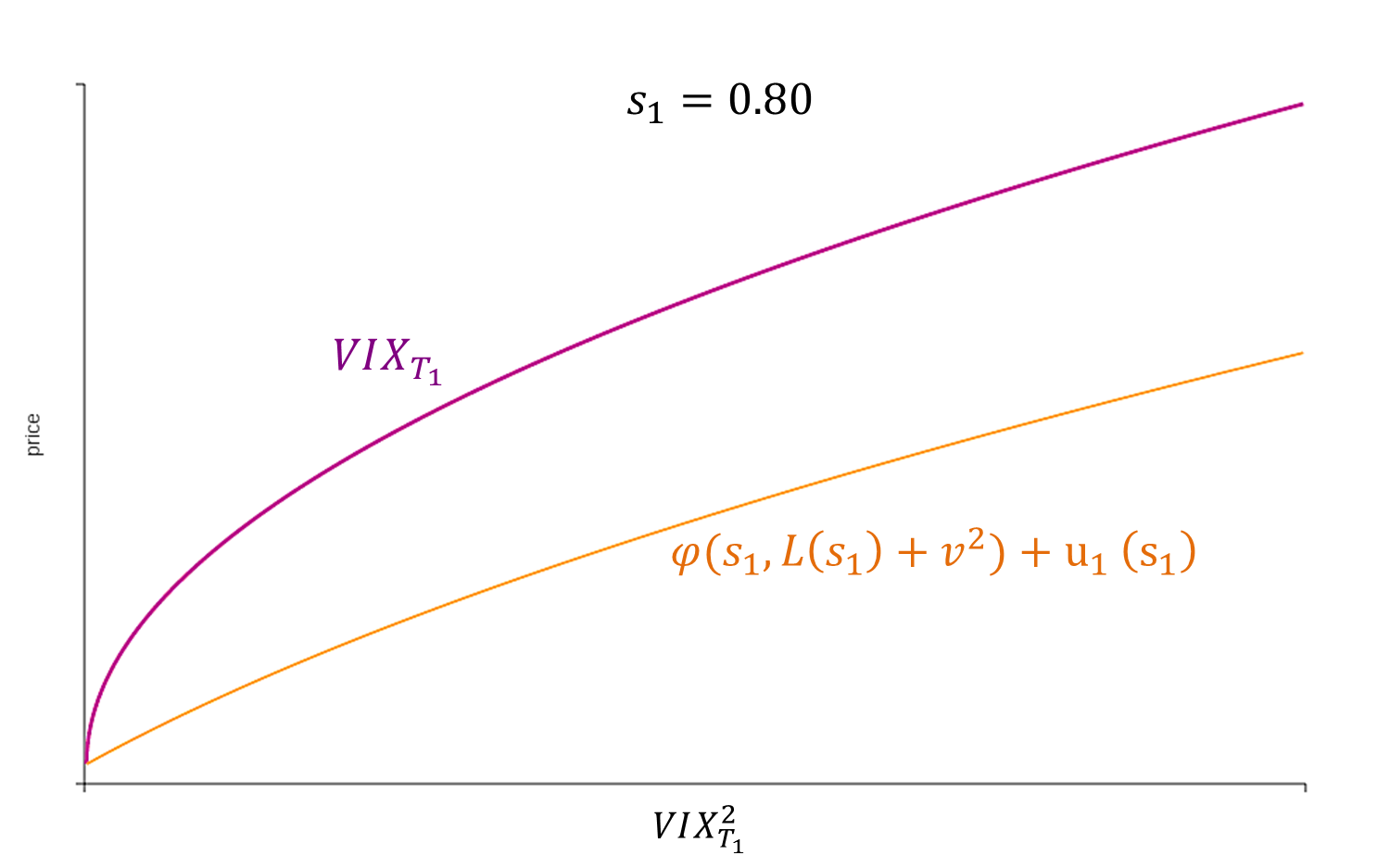

The following result shows that functionally generated portfolios improve the classical subreplication bound in all relevant cases. While we already know from the abstract result in Theorem 5.1 that when , we now construct an explicit, functionally generated subreplicating portfolio that has strictly positive price.

Proposition 6.4.

Let be in convex order.

Then there exists a functionally generated subreplicating portfolio with strictly positive price.

More precisely, it is generated by the concave function and a constant , where and . The values of the constants depend on and can be found explicitly as indicated in the proof.

Proof.

We consider the concave function defined by

where and . Moreover, let . Then, denoting

(6.4)

we have

Since

the infimum of over can only be attained for or , whence

Figure 1. Graph of for

As , the function is bounded from below on (see Figure 1). For , the minimum of is strictly negative,

The function then has two distinct zeros and we observe that as and as .

Let . Then and hence

Next, we show that there exist parameters such that

(6.5)

Since are in convex order and is strictly convex,

and this value is independent of . Let . In view of Assumption 2.1, choosing small enough guarantees that and then choosing also small enough yields , for . As a result, we have

which proves our claim (6.5).

With this choice of and , we have

Optimizing over the parameter leads us to the choice . Summarizing, the portfolio

with deltas as in Proposition 6.2, is subreplicating at price

∎

Remark 6.5.

In many important cases it is straightforward to find satisfying (6.5). Indeed, suppose that have continuous densities . Then, is suffices to choose such that . Or, if (and hence ) is concentrated on a compact interval , then we can choose such that .

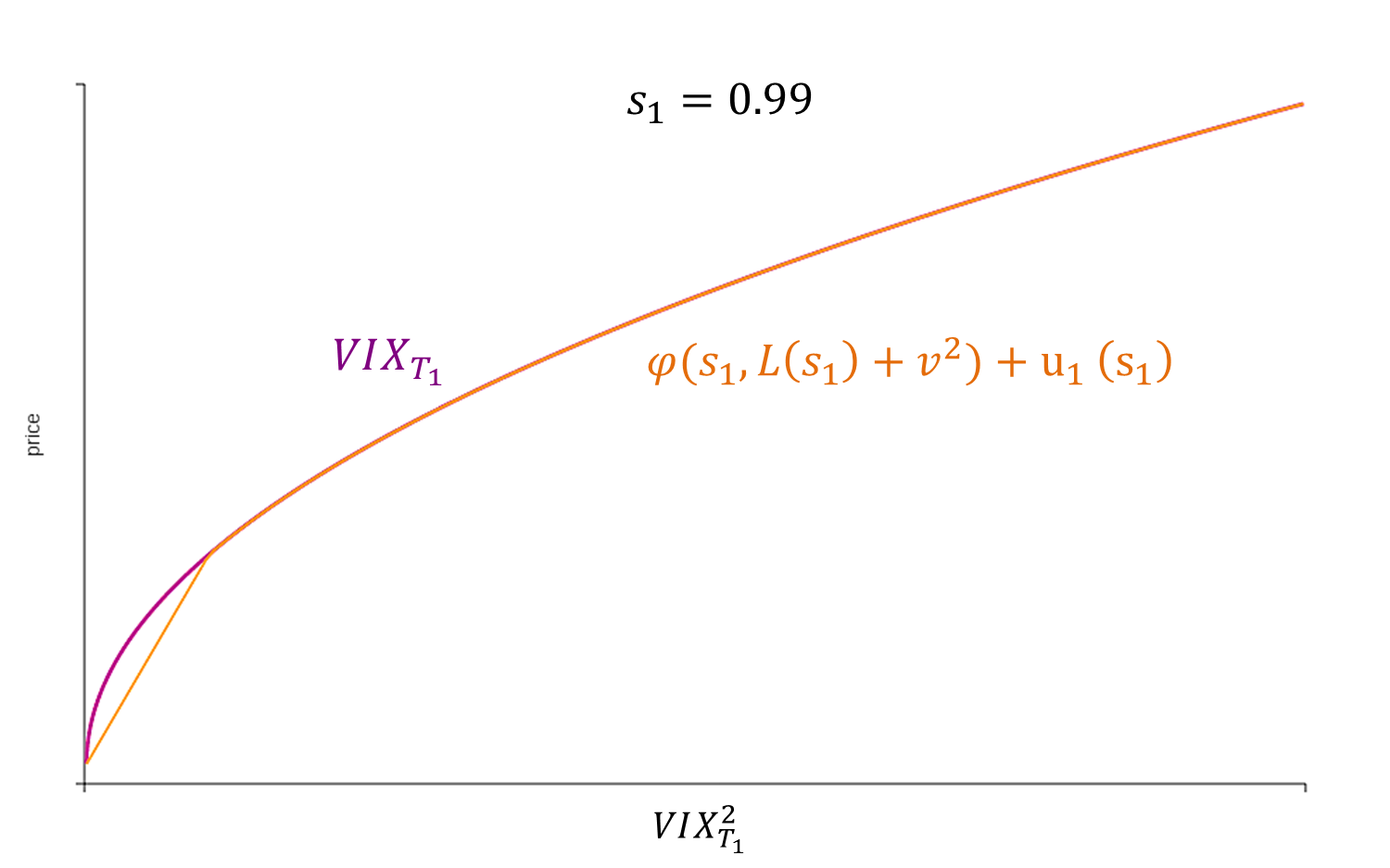

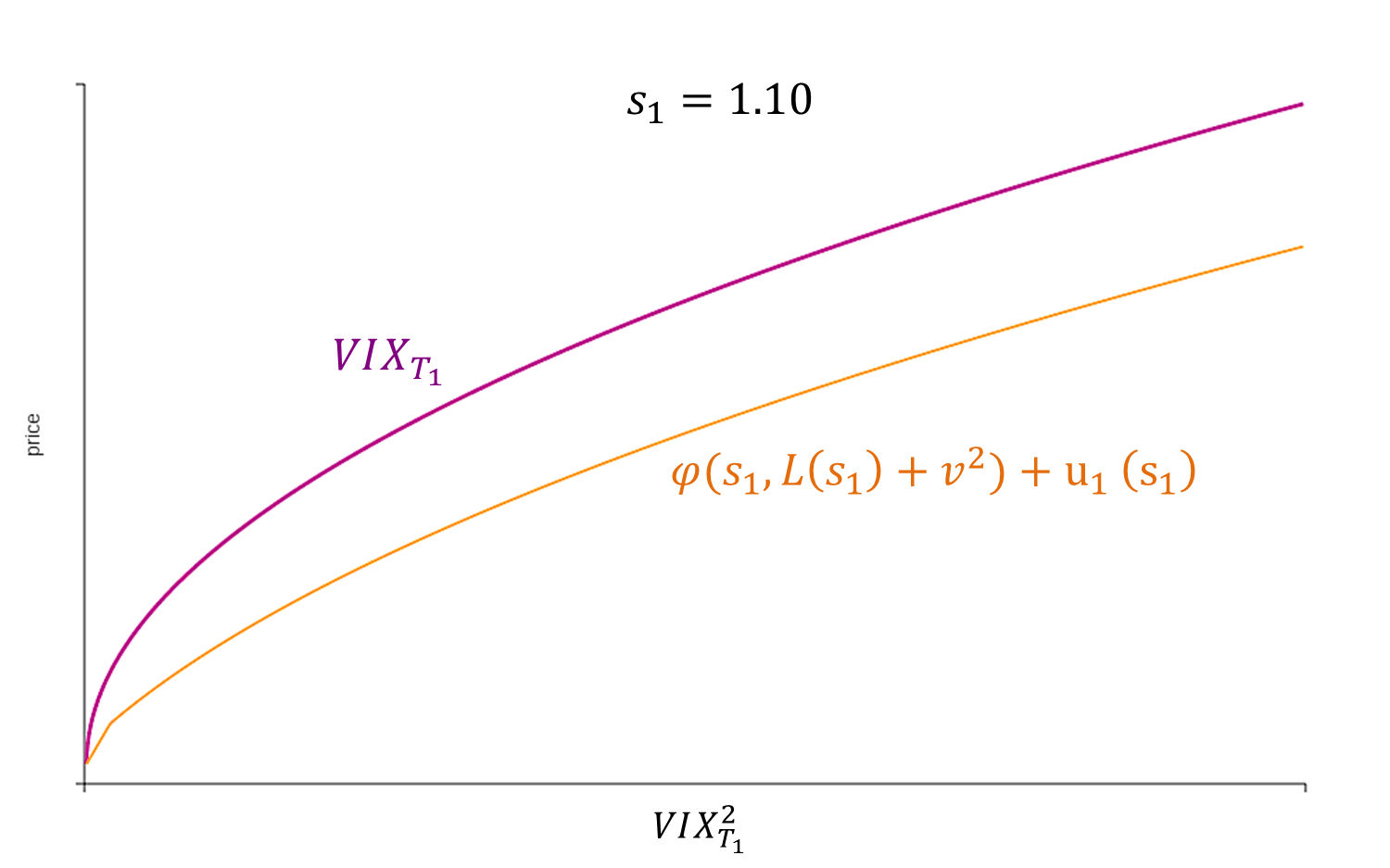

7. The case where is a Bernoulli distribution

In this section, we study in detail an example where the

classical upper bound is typically not optimal, i.e.,

. We will explicitly compute the

optimal bound and derive (-)optimal superreplicating portfolios within the functionally generated class. In all of this section, is a Bernoulli distribution,

(7.1)

Thus,

can only take the two values and these are the only free parameters—the fact that has mean determines the value of .

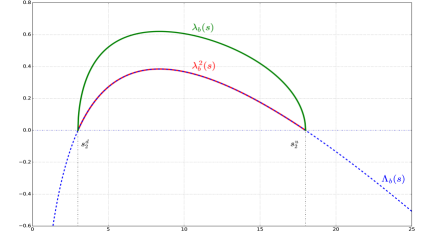

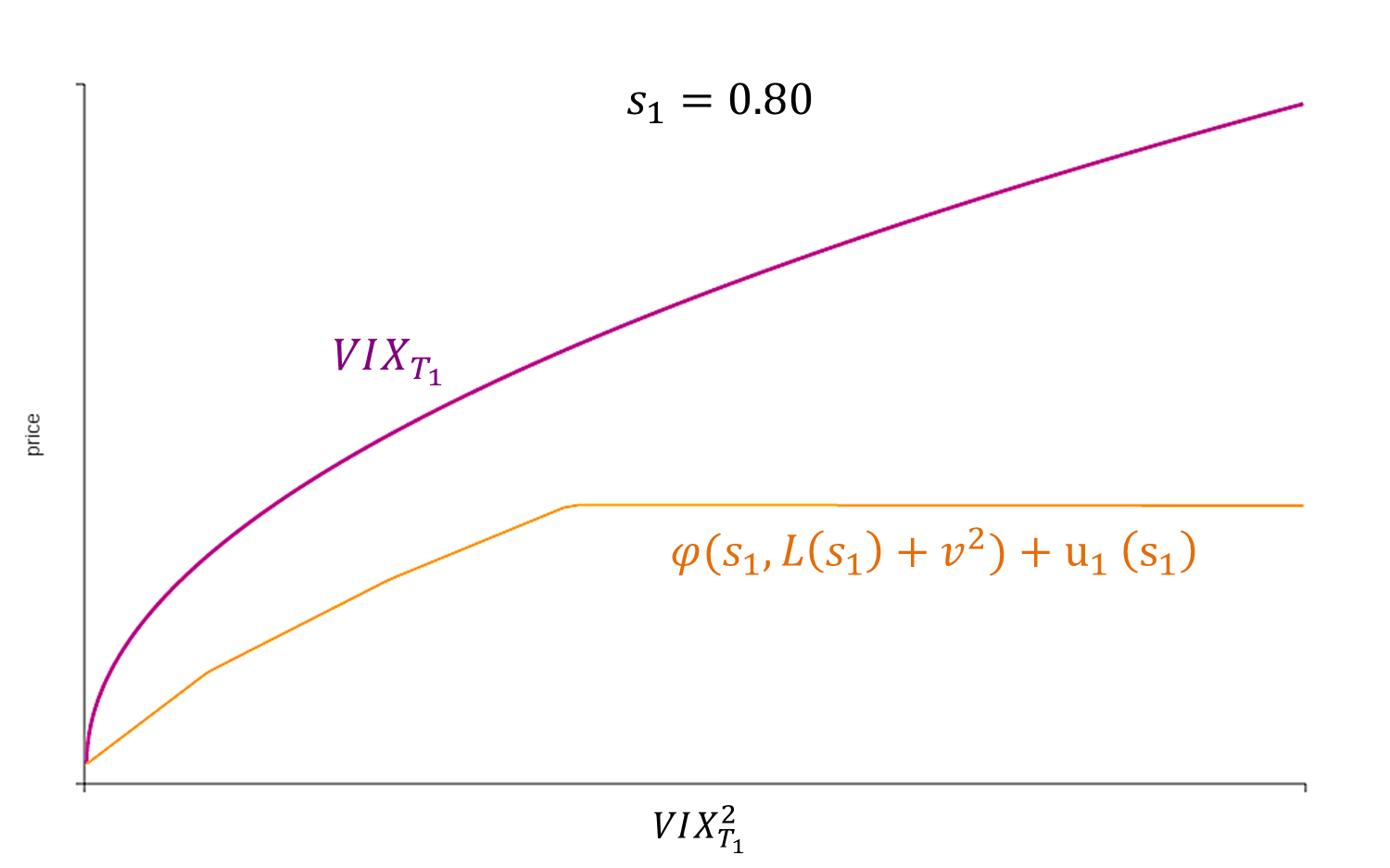

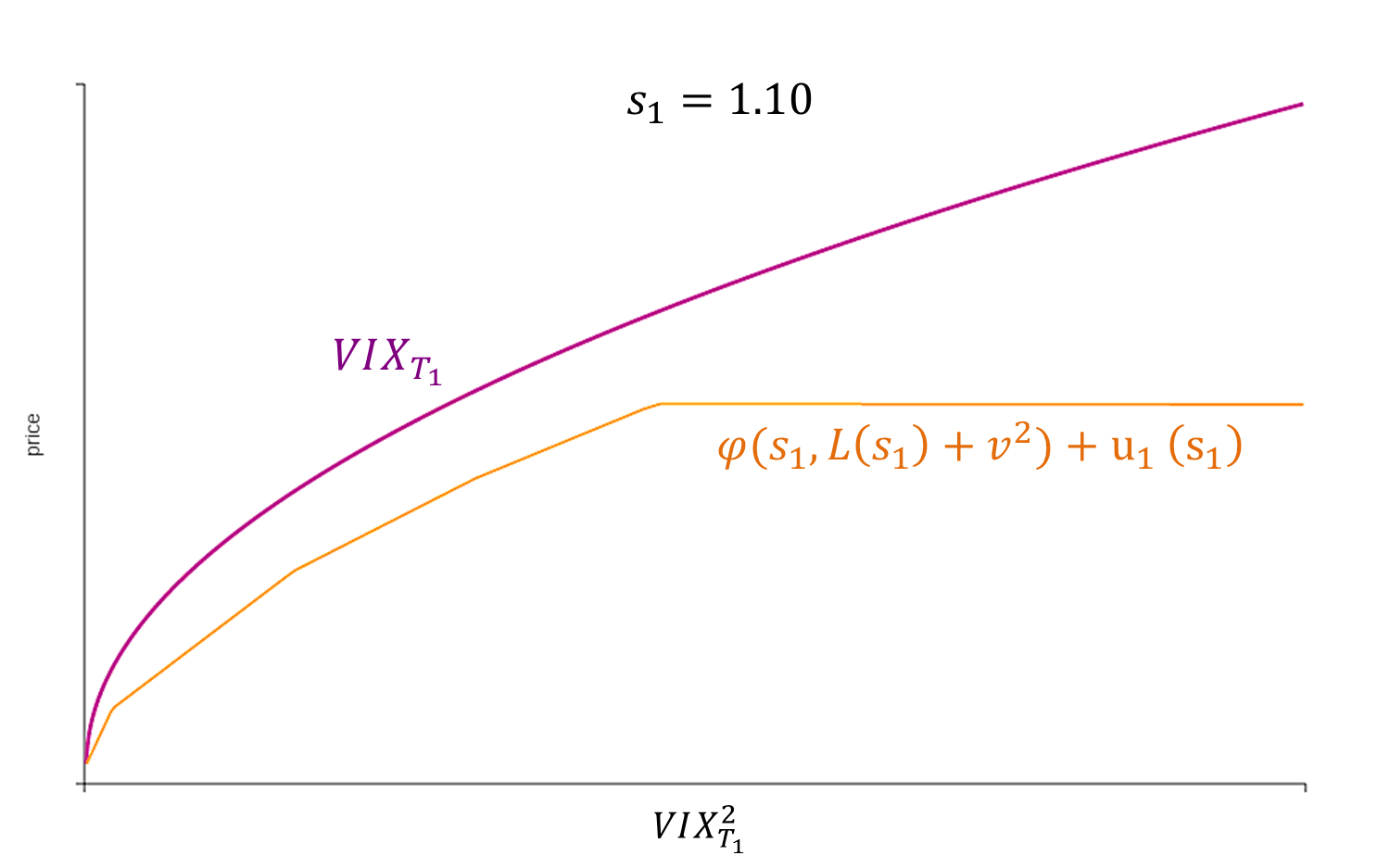

In our first result, we show that in the absence of arbitrage, the sets and both have a unique element. As a consequence, and this number can be computed explicitly as the expectation under the unique risk-neutral measure. Some notation is needed to state this result. We define the functions

which will represent the unique martingale transition probabilities.

Moreover, an important role will be played by the function

(7.2)

Note that the function depends only on the two values , . When , is the risk-neutral price of the FSLC in the one-step binomial model (hence the subscript ), given the price of the S&P 500 index at time . In particular, in this model, one can replicate the log-contract payoff at by holding units of cash at and units of the index over , where is the delta of the log-contract in the one-step binomial model:

(7.3)

(7.4)

We observe that . Moreover, from (7.3), the function is strictly concave. As a consequence, for all

, and for all

. We denote by the square root of on the interval ,

For any , the equation is equivalent to the equation which has exactly two solutions that we denote by

(7.5)

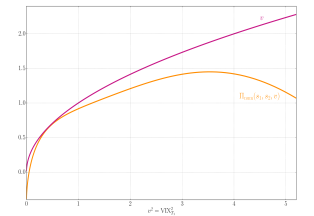

For convenience, we write for the unique solution of . Figure 2 shows the graphs of and .

Figure 2. and its square-root,

Theorem 7.1.

Let be the Bernoulli distribution (7.1). Then, there is no arbitrage, or equivalently , if and only if . In this case, has a unique element

, given by

(7.6)

and has a unique element

, given by

In particular, -a.s. Moreover,

(i)

if is the Bernoulli distribution that takes values in for some , then and ,

(ii)

if is a different distribution, then and .

Proof.

We first characterize the absence of arbitrage. Let . Then, and are in convex order and in particular .

Since , we have

That is, the transition probabilities satisfy and , and as a consequence, is uniquely determined and given by (7.6).

Conversely, assume that and let

be the probability measure on defined by (7.6). We readily verify that and in particular . The latter is equivalent to the absence of arbitrage; cf. Theorem 3.4.

Next, suppose that and let be its element. We have ; cf. Lemma 3.3(ii).

Let ; we prove that .

The martingale condition

implies that

hence the transition probabilities

do not depend on , and since the first marginal of both

and is , the projection of onto the first two

coordinates is equal to . Moreover, -a.s.,

Therefore, -a.s., showing that is the unique element of .

(i) By the definition of , we have if and only if is -a.s. constant. Due to the strict concavity of , this happens only if is atomic with at most two atoms. If is a Dirac mass, since it has mean , it can only be (which we consider a special case of the Bernoulli distribution). If has two atoms at then we must have , i.e., , and . As a consequence, there exists such that and . We recall from Theorem 5.2 that implies .

(ii) If we are not in the case (i), then , so Theorem 5.2 implies that . Moreover,

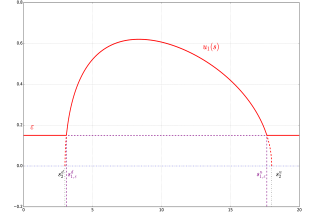

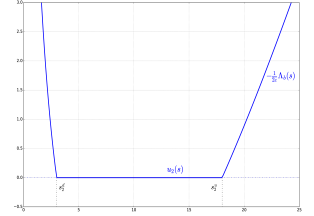

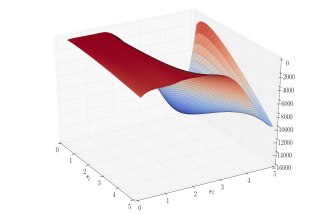

Next, we derive an explicit superreplicating portfolio with -optimal price. It turns out that such a portfolio can be chosen of the functionally generated form (6.1), (6.2). To that end, we first observe that is of the form as defined in (6.4),

Let , , and , i.e., are the two values such that . Note that and define

Using this function as a generator as in Proposition 6.1, we have

Notice that on the support of , so that the payoff is free at time 0. Moreover, one can obtain the wealth at for zero initial cost; cf. the proof of Proposition 6.1.

We now complete the portfolio using the procedure detailed in Proposition 6.1: as

we have

If , then and the above supremum is attained for and .

If , then ,

therefore the supremum is attained for and . As a consequence, the portfolio defined by

(7.9)

is superreplicating by Proposition 6.1, since .

The payoffs and are plotted in Figure 3. Both and are continuous functions, with and .

Figure 3. Profiles of an -optimal superreplicating portfolio when is Bernoulli

Proposition 7.2.

Let be the Bernoulli distribution (7.1) and . For , the portfolio defined in (7.9) is superreplicating and has price . Moreover, if , then for all small enough .

Proof.

The superreplication property has already been argued. By definition, -almost everywhere and as a consequence,

using the formula from Theorem 7.1. If and is such that , then we have in the above and thus .

∎

8. The case where has compact support

In this section, we focus on the case where has compact support in . We denote

(8.1)

We assume throughout this section that the market is arbitrage-free, i.e., that and are in convex order. This implies that , in particular,

satisfy .

Continuing the discussion from the preceding section, we seek sufficient conditions on the market smiles and under which , and corresponding portfolios.

Following Theorem 5.2, three strategies can be used to prove that . We can (i) find a superreplication portfolio whose price is strictly smaller than , (ii) show that and are not in convex order, or (iii) verify that .

The following result uses all three strategies. We recall from Section 7 the function defined in (7.2), its root for as well as and the solutions from (7.5).

Proposition 8.1.

Assume (8.1) and absence of arbitrage. Each of the following implies :

(i)

,

(ii)

, which holds in particular if and ,

(iii)

for .

Proof.

(i) Let be such that . Exactly as in Section 7, the portfolio defined in (7.9) superreplicates the VIX, and its price is bounded from above by . This proves that .

(ii) Let . As is decreasing, this means that the support of is not included in the convex hull of the support of , so these distributions are not in convex order, and then the same holds for and . By Theorem 5.2, we conclude that . If , then due to the strict convexity of , which yields the second claim.

(iii) Since and are in convex order, . For any and for -almost all ,

where denotes the set of all probability measures such that and . Indeed, the inequality follows directly from the definition (3.1) of and the fact that ; moreover, since is convex, the supremum is attained when is the Bernoulli distribution that takes values in and has mean , whence the equality. As a consequence,

hence and the set is well defined. Let , then for -a.e. . As a consequence, if , there exists no such that -a.s., that is, . By Theorem 5.2, this implies .

∎

9. Smiles for which the classical upper bound is optimal

In this section, we show how to construct examples of arbitrage-free smiles such that the classical upper bound is optimal, i.e., . We recall from Theorem 5.2 that this is equivalent to of Definition 3.1 being nonempty. Going backward, let , that is, and the price of the FSLC at is constant and equal to . Disintegrating into its first marginal and a transition kernel , these two conditions can be stated as

Conversely, if is a stochastic kernel with these two properties, then . In brief, constructing an element of boils down to determining such a kernel.

One instance, similar to Example 4.14 in [12], is the following conditional Bernoulli model. Given and measurable functions such that , let

(9.1)

Then, satisfies the two conditions if and only if, -a.s.,

, i.e.,

and ,

i.e.,

The latter can be rewritten as

and for , is a decreasing continuous function on such that and . Therefore, if is given and , then there exists a unique such that the above conditions are satisfied. Now, (9.1) defines a kernel . If is any distribution on with mean , we can set and define to be the second marginal of . Then, we have constructed smiles together with an element , thus .

A similar reasoning can be applied to three-point or -point models instead of Bernoulli.

10. Numerical results

10.1. LP solver

When we numerically solve the primal problems (2.2) and (2.4), we discretize the payoffs and using a finite basis of out-the-money (OTM) calls and puts, cash , an initial delta , as well as the log-contract (so that the LP solver can exactly recover the classical superreplicating portfolio). Moreover, we decompose the deltas and over a polynomial basis, with respective orders and :

Numerically, we can only check the super/subreplication constraints (2.3) and (2.5) on a large but finite grid of values of . Therefore our numerical upper bound is

(10.1)

where

(with ) and is the set of variables such that

Here, denotes the OTM vanilla payoff, i.e.,

denotes the market price of the OTM vanilla payoff ,

and denotes the price of the variance swap of

maturity , i.e., of the payoff .

Similarly, our numerical lower bound reads

(10.2)

where is the set of variables such that for all , . Note that if we could check the constraints everywhere, and not only on the finite grid , we would have and , which means that and would be acceptable upper and lower bounds. Thus it is important to use a large enough grid .

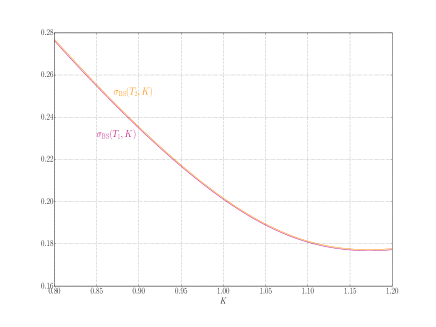

To solve the problems (10.1) and (10.2), we have used the software package MOSEK, with , , and a grid of constraints made of 130 values of , 130 values of (unevenly distributed from 0.01 to 5, and including the strikes of the OTM calls and puts) and 100 values of (unevenly distributed from to ). Let us first consider the case where the smiles and are those of a SABR model

(10.3)

with , , , , and months. The corresponding smiles and densities are reported in Figure 4. The implied volatility of the FSLC is . The LP solver yields , together with the classical superreplicating portfolio (2.7), so the classical upper bound seems to be optimal. For the lower bound, we get , which is much larger than the classical lower bound (zero), and the corresponding portfolio is reported in Figure 5.

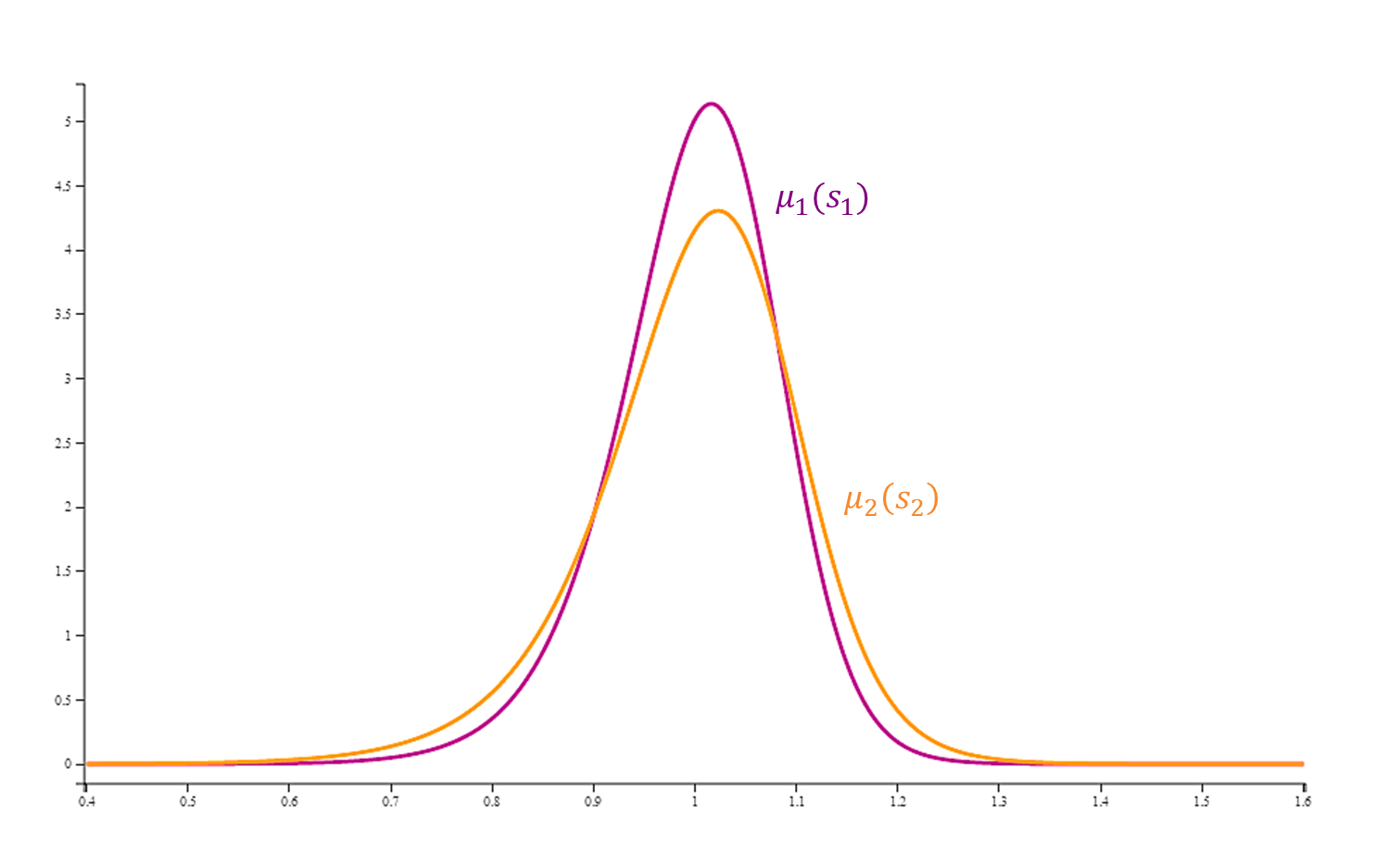

Figure 4. Smiles (left) and densities (right) of the SABR model (10.3) at maturities months and days; , , , and

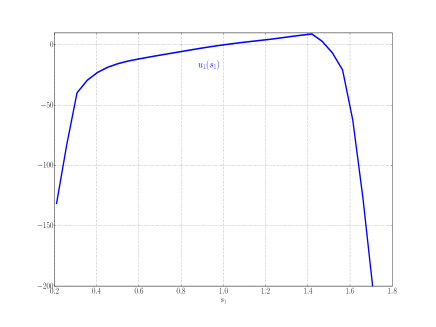

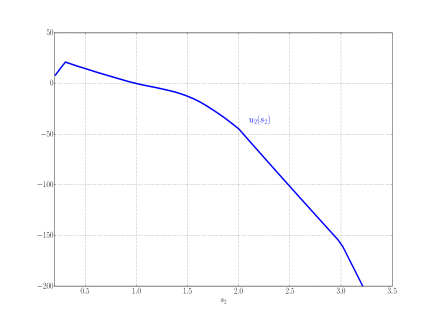

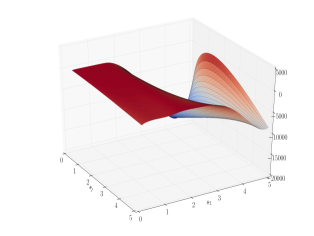

Figure 5. Numerical optimal subreplicating portfolio (top left), (top right), (bottom left), (bottom right) when and are the SABR risk-neutral measures of Figure 4, using polynomials , of degree 4

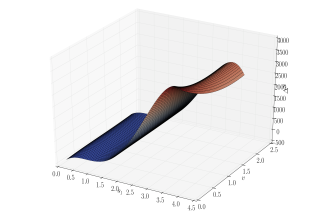

In Figure 6 we check the subreplication constraints . Note that, since the grid is finite, subreplication is not guaranteed everywhere. For instance, Figure 7 shows that at the very high value , the subreplication constraint is not satisfied for some . This is because is not a value of in the grid ; its nearest neighbors in this grid are and .

Figure 6. Left: and as a function of , for and . Right: as a function of for . This quantity is always negative. We used the SABR risk-neutral measures of Figure 4.Figure 7. as a function of for . This quantity is not always negative (maximum value: 26). We used the SABR risk-neutral measures of Figure 4.

10.2. Optimization over functionally generated subreplicating portfolios

We recall from (6.3) that ,

where is the bound obtained from functionally generated portfolios,

10.2.1. Piecewise linear profiles

Here we consider concave functions on that are piecewise linear. We start with a partition of and look at the concave, piecewise linear functions defined on with kinks at the points and a nonpositive right slope. These can be parametrized in the following way:

We then extend the domain of definition of these functions to by linear extrapolation. Finally, we consider the homothetic transforms of the , i.e., ; these form a subset of .

The associated optimization problem satisfies , where

By concavity of the square root, the above infimum is reached either at the kinks of or for :

The results we obtained for market and SABR risk-neutral densities all have fit the VIX very closely for one value of (the tip of ), then slip to the left, as shown in Figure 8. Lower bounds are reported in Table 1.

Figure 8. Subreplication with a piecewise linear profile

10.2.2. Cut square root

To obtain an even closer fit to the VIX, we consider the concave function

for positive . The corresponding is then

which leads to the optimization problem

Out of the concave functions we tested, this cut square root yielded the best results, that is, the highest lower bound for the price of the VIX future, as can be seen in Table 1. The LP solver of Section 10.1 gave a better lower bound for both the SABR smiles ( versus ) and the market smiles as of May 5, 2016 (8.4% versus 7.8%), but the portfolio it yields is not guaranteed to subreplicate everywhere, as the subreplication constraint is only verified for a finite grid. By contrast, the functionally generated portfolios are subreplicating everywhere, by construction.

Figure 9. Subreplication with a cut square root profile

We would like to thank Bruno Dupire for fruitful discussions, as well as Lorenzo Bergomi, Stefano De Marco, Pierre Henry-Labordère, the Associate Editor, and two anonymous referees for their helpful comments on a preliminary version of this article. The research of M. Nutz is supported in part by an Alfred P. Sloan Fellowship and NSF Grant DMS-1512900.

References

[1]

Bayraktar, E., Zhao, Z.: On arbitrage and duality under model uncertainty and portfolio

constraints, to appear in Math. Finance, 2014.

[2]Beiglböck, M., Henry-Labordère, P., Penkner, F.:

Model-independent bounds for option prices: A mass-transport

approach, Finance Stoch., 17(3):477–501, 2013.

[3]

Beiglböck, M., Juillet, N.:

On a problem of optimal transport under marginal martingale

constraints, Ann. Probab., 44(1):42–106, 2016.

[4]Beiglböck, M., Nutz, M., Touzi, N.: Complete duality for martingale optimal transport on the line,

to appear in Ann. Probab., 2016.

[5]

Bouchard, B., Nutz, M.:

Arbitrage and duality in nondominated discrete-time models,

Ann. Appl. Probab., 25(2):823–859, 2015.

[6]Carr, P., Lee, R.: Robust replication of volatility derivatives, preprint, 2009.

[7]Carr, P., Lee, R.: Hedging variance options on continuous semimartingales, Finance Stoch., 14(2):179–207, 2010.

[8]Carr, P., Madan D.: Towards a theory of volatility trading,

Reprinted in Option Pricing, Interest Rates, and Risk Management, Musiela, Jouini, Cvitanic, University Press, 417–427, 1998.

[9]The CBOE volatility index - VIX, www.cboe.com/micro/vix/vixwhite.pdf

(accessed on August 3, 2016).

[10]Cox, A., Wang, J.: Root’s barrier: Construction, optimality and applications to variance options, Ann. Appl. Probab., 23(3):859–894, 2013.

[11]

Dellacherie, C., Meyer, P.-A.:

Probabilities and Potential A, North Holland, Amsterdam, 1978.

[12]De Marco, S., Henry-Labordère, P.: Linking

vanillas and VIX options: A constrained martingale optimal transport

problem, SIAM J. Financial Math., 6(1):1171–-1194, 2015.

[13]Dupire, B.: Model free results on volatility derivatives, SAMSI,

Research Triangle Park, 2006.

[14]

Föllmer, H., Schied, A.:

Stochastic Finance: An Introduction in Discrete Time.

W. de Gruyter, Berlin, 3rd edition, 2011.

[15]Galichon, A., Henry-Labordère, P., Touzi, N.: A

stochastic control approach to no-arbitrage bounds given marginals,

with an application to Lookback options, Ann. Appl. Probab.,

24(1):312–336, 2014.