New results on the asymptotic and finite sample properties of the MaCML approach to multinomial probit model estimation

Abstract

In this paper the properties of the maximum approximate composite marginal likelihood (MaCML) approach to the estimation of multinomial probit models (MNP) proposed by Chandra Bhat and coworkers is investigated in finite samples as well as with respect to asymptotic properties. Using a small illustration example it is proven that the approach does not necessarily lead to consistent estimators for four different types of approximation of the Gaussian cumulative distribution function (including the Solow-Joe approach proposed by Bhat). It is shown that the bias of parameter estimates can be substantial (while typically it is small) and the bias in the corresponding implied probabilities is small but non-negligible. Furthermore in finite sample it is demonstrated by simulation that between two versions of the Solow-Joe method and two versions of the Mendell-Elston approximation no method dominates the others in terms of accuracy and numerical speed. Moreover the system to be estimated, the ordering of the components in the approximation method and even the tolerance used for stopping the numerical optimization routine all have an influence on the relative performance of the procedures corresponding to the various approximation methods. Jointly the paper thus points towards eminent research needs in order to decide on the method to use for a particular estimation problem at hand.

- AIC

- Akaike Information Criterion

- APB

- Average Percentage Bias

- ASC

- Alternative Specific Constant

- BIC

- Bayesian Information Criterion

- bME

- bivariate Mendell-Elston

- CCL

- Composite Conditional Likelihood

- CDF

- Cumulative Distribution Function

- CEF

- Conditional Expectation Function

- CL

- Composite Likelihood

- CLAIC

- Composite Likelihood Akaike Information Criterion

- CLBIC

- Composite Likelihood Bayesian Information Criterion

- CML

- composite marginal likelihood

- c.p.

- ceteris paribus

- DCM

- Discrete Choice Models

- DGP

- Data Generating Process

- DM

- Decision Maker

- GHK

- Geweke-Hajivassiliou-Keane

- IC

- Information Criteria

- iid

- independent, identically distributed

- KLD

- Kullback-Leibler Divergence

- LLN

- Law of Large Numbers

- MaCML

- maximum approximate composite marginal likelihood

- MAE

- mean absolute error

- MC

- Monte Carlo

- MCMC

- Markov Chain Monte Carlo

- ME

- Mendell-Elston

- ML

- maximum likelihood

- MNP

- multinomial probit

- MSE

- mean squared error

- MSL

- maximum simulated likelihood

- MVNCDF

- multivariate normal cumulative distribution function

- OLS

- Ordinary Least Squares

- PQD

- Positive Quadrant Dependence

- RMSE

- root mean squared error

- RUM

- random utility model

- RV

- Random Variable

- SEM

- Structural Equation Models

- SJ

- Solow-Joe

- SLLN

- Strong Law of Large Numbers

- ULLN

- Uniform Law of Large Numbers

- WLLN

- Weak Law of Large Numbers

- WTP

- Willingness to Pay

KEYWORDS: Multinomial probit, Discrete choice model, MACML estimation approach, Estimation method, Monte Carlo experiment

1 Introduction

Discrete choice models are routinely used for modeling mode choice, destination choice, choice of travel time, route choice, vehicle purchase decision, activity choice and many other areas. They are used for example for the evaluation of new mode options, the design of pricing schemes for public transport, the adoption of new vehicle technologies, the impact of the provision of travel time information as well as in the simulation of transportation systems. Discrete choice models have been used in cross sectional data sets based on revealed preferences as well as panel data sets combining revealed and stated preference data.

Most commonly discrete choice models are formulated using the random utility model (RUM) paradigm with the two basic models being the multinomial logit (MNL) and the multinomial probit (MNP) model. While the MNL models suffers from the IIA assumption that led to the formulation of ’generalized extreme value’ (GEV) models (see for example Train; 2009) the MNP model family offers better modeling flexibility at the expense of higher computational costs.

A major reason for the high computational costs is that the probit likelihood by definition involves a multivariate normal cumulative distribution function (MVNCDF) which is analytically intractable and hence it is necessary to rely on approximation methods in order to evaluate the likelihood. For standard quadrature methods the relationship between the dimension of the integral and the computational complexity is of exponential order which renders those methods too time consuming for all but the smallest choice sets.

Therefore, the integral is usually approximated by Monte Carlo (MC) simulations, which are in comparison less accurate. When combined with maximum likelihood estimation those methods are known as maximum simulated likelihood (MSL) approach. The most widely used method is the algorithm by Geweke-Hajivassiliou-Keane (GHK) (see Train; 2009, p. 115). The assessment of integrals by simulation is computationally efficient because the computational complexity of the simulation is an approximately linear function of the dimension of the integral (see Hajivassliliou; 2000, p. 88f). Like MC methods in general MSL is justified asymptotically, which induces the need to rely on many simulation runs and, nevertheless, leads to biased estimates whenever the number of MC replications is finite and (see Train; 2009, p. 250ff).

In this regard, several authors have suggested that analytic approximations might have the potential to offer a faster way to estimate MNP models. In fact, the use of analytic approximations – namely the Clark approximation – to estimate MNP models predated the introduction of MSL (Daganzo et al.; 1977). However, with the advent of MSL this approximation was deemed to be too imprecise and, therefore, its importance vanished (Horowitz et al.; 1982). In general analytic approximations of the MVNCDF are known to be less accurate than quadrature and simulation methods (Joe; 1995) but they share neither the infeasibility of quadrature methods nor the long computation times of MSL.

Utilizing an analytic approximation Bhat (2011) recently introduced the maximum approximate composite marginal likelihood (MaCML) approach for simulation-free estimation of MNP models combining the Solow-Joe (SJ)-approximation for the MVNCDF and composite marginal likelihood (CML) estimation with the specific aim to speed up the estimation of complex MNP models.

In a first simulation study MaCML is reported to be up to 350 times faster than MSL estimation while the accuracy of parameter recovery was at least at par with the latter (Bhat and Sidhartan; 2011). A later simulation study revealed that the difference in computation times shrinks once MSL estimation is also performed within the CML framework but that there is still a reasonable performance gain which is then fully attributable to the analytic approximation (Cherchi et al.; 2016). Furthermore, (Cherchi et al.; 2016) report that MaCML is faster and more accurate than several competing estimation procedures including two GHK variants as well as Bayesian Markov Chain Monte Carlo (MCMC) estimation.

Despite those first results and the effort undertaken by Bhat (2011) to provide theoretical justification for this specific combination of methods, there are some open questions that warrant further investigation: Firstly, we are not aware of any results addressing the consistency of the estimator. The consistency of CML methods is rather well understood (see Varin et al.; 2011) but it is unclear how the MVNCDF approximation interferes with estimation.

As the choice probabilities enter the log-likelihood in a nonlinear manner it is not clear that unbiased estimation of the probabilities leads to unbiased maximum (composite) likelihood estimators.

Secondly, a recent contribution by Connors et al. (2014) notes that (Bhat; 2011) does not discuss the merits of alternative analytic approximations of the MVNCDF. They provide evidence that the Mendell-Elston (ME)-approximation is superior to the SJ-approximation with regard to accuracy and computation time. Those results were generated for a large set of different MVNCDFs and the approximations were judged by the ability to replicate the MVNCDF-probability from known parameters Connors et al. (2014). Furthermore, (Trinh and Genz; 2015) have recently presented an improved variant of the ME-approximation. Those results raise the question whether a combination of the ME-approximation with CML estimation is better suited to estimate MNP models than the current MaCML approach.

Note in this respect that it is common practice (see Horowitz et al. (1982) and Kamakura (1989)) to differentiate between (a) prediction accuracy, that is the predictive performance of the approximation with known parameters as assessed for example by (Connors et al.; 2014), and (b) estimation accuracy for the parameters themselves.

It is important to acknowledge that those two accuracy types are related but distinct concepts. This becomes even more important for some applications of MNP models e.g. value of travel time or willingness to pay analysis where transformations of the parameter estimates (such as quotients of coefficients) and not the probabilities are the result primary of concern (see Calfee et al.; 2001).

The papers (Bhat and Sidhartan; 2011) and (Cherchi et al.; 2016) assess the estimation accuracy of the SJ-approximation for various (simulated) data sets and (Kamakura; 1989) does the same for the ME-approximation,222(Kamakura; 1989) compares the estimation and prediction accuracy of the ME-approximation with the Clark- and separate split approximation, see (Langdon; 1984). It has been shown repeatedly that those approximations are inferior (in terms of both accuracy concepts) to the ME (see Kamakura (1989), Rosa (2003)) and, therefore, those approximation are not part of our comparison. but there is no published comparison regarding the estimation accuracy of the SJ- and ME-approximations in the context of MNP model estimation.

The main contributions of this paper can be summarized as follows: First, we investigate the asymptotic bias of various MaCML estimators using different approximations to the MVNCDF in a simple example showing that the MaCML approach does not deliver consistent estimators. By differentiation between predictive and estimation accuracy we demonstrate that the bias in estimated parameters can be sizeable while the bias in predicting choice probabilities in the example is small albeit not negligible. Second, we compare the bias for different data generating processes in an attempt to identify situations where one of the approximations works better than the others. Third, we assess the finite sample estimation accuracy of all methods using a cross-sectional MNP model taken from (Bhat and Sidhartan; 2011). These results are of particular importance because they shed light on the typical computation time of each estimator. It will be shown that there is no clear cut winner in those comparisons.

The outline of the paper is as follows: In section 2 the model used for demonstration purposes is introduced. Section 3 describes the various approximation concepts used and surveys the literature on properties of the various concepts. Section 4 then presents and discusses our findings and section 5 concludes the paper.

2 The multinomial probit model

In this paper for illustration purposes we will use the following simple MNP model based on the random utility function with an Alternative Specific Constant (ASC) as the only explanatory variable, that is

where at total of decisions between alternatives are observed.

The vector is assumed to be independently identically (i.i.d) normally distributed with mean vector of zero and variance matrix assumed to be known. Therefore, we only need to fix in order to ensure that the model is identified. Thus only three ASCs constitute parameters to be estimated.

Denote the difference between the utility induced by choosing the -th and the -th alternative by and define the dimensional differencing matrix obtained from inserting a column of entries equaling as the -th column of the dimensional identity matrix. Then the probability that individual chooses alternative is defined as (defining as the vector composed of all s)

| (1) |

where denotes the distribution function of a three-dimensional normal Random Variable (RV).

Note that the choice probabilities in this situation are a function of and therefore the scaled log-likelihood under the assumption of independent choices can be written as

| (2) |

where denotes the indicator function and the number of individuals choosing alternative .

The resulting maximum likelihood estimator is defined as . Under the assumption of independent observations this scaled log-likelihood converges to a non-stochastic limiting function by the Weak Law of Large Numbers (WLLN),

| (3) |

Under the assumption that and is compact this result immediately extends to uniform convergence (as in this case ) and therefore, subject to identification, to the consistency of the maximum likelihood estimator (see for example Ferguson; 1996, p. 114). If in the likelihood the probability is replaced by a continuous approximation it follows along the same lines that

| (4) |

Again the corresponding maximizers converge to the maximizer of the limiting function . This allows the investigation of the asymptotic bias by examining the function for different approximation approaches.

3 Methods for the approximation of choice-probabilities

This section provides a total of four approximation methods for the MVNCDF . As for diagonal transformation matrices it follows that we will in the following without restriction of generality assume that the coordinates have been scaled such that is a correlation matrix.

All approximation methods are based on the SJ and the ME approach. The presentation is short and focused on the MNP model introduced in section 2. For a more general discussion of the SJ-approximation the reader is referred to (Joe; 1995). (Mendell and Elston; 1974) as well as (Kamakura; 1989) provide further information regarding the ME-approximation.

3.1 Solow-Joe approximation

In the Solow-Joe approximation (Solow; 1990; Joe; 1995) used by (Bhat; 2011) the multivariate normal distribution is factorized into a product of conditional distributions, which are in turn approximated by linear projections (see Joe; 1995, p. 958).333This is the first of two different approximations proposed by (Joe; 1995). The second approximation, sometimes labeled as the second-order approximation, is in theory more precise but its computation is more costly due to the appearance of tri- and quadvariate MVNCDFs. (Sidharthan; 2012) compared the influence both approximations have on parameter estimation and advises (except for rare special cases) against the use of the second-order approximation (see Sidharthan; 2012, p. 134ff). For a three dimensional case of calculating the MVNCDF for where are standard normally distributed we obtain (using ):

| (5) | ||||

Here the approximation replaces the conditional expectation by the linear projection

| (6) |

where Q is a matrix whose s entry is where and q is a row vector with entries: , where . Note that for (with denoting the correlation between and ),

and

Therefore, the covariance matrix in (6) is of the following form,

| (7) |

The approximation error of the SJ approximation arises because in general .

From the standpoint of application, there are three issues that warrant further discussion. Firstly, it should be clear that the ordering of the components in equation (5) is arbitrary because the factorization would be equally valid for any permutation of the components. The major contribution of (Joe; 1995) over the older paper by (Solow; 1990) is the suggestion to tackle this problem by computing the average over all possible factorizations. For larger choice sets this total enumeration is infeasible and (Joe; 1995) suggests to take the average of to randomly selected permutations (see Joe; 1995, p. 958). However, (Bhat; 2011) proposes that for the purpose of MaCML estimation it is sufficient to use only one randomly drawn permutation per estimation step (see Bhat; 2011, p. 926f). In the respective simulations the performance improvement for utilizing two instead of one permutation is reported to be only marginal (see Bhat and Sidhartan; 2011). (Connors et al.; 2014) assess the influence of the number of reorderings on the prediction accuracy of the SJ-approximation and conclude that averaging over 10 permutations provides a good compromise between computation time and accuracy (see Connors et al.; 2014, p. 127f).

Secondly, the linear projection (6) involves the inverse of the matrix Q and, therefore, the approximation is only compute-able when Q is non-singular. Numerically Q is almost singular if or is large or and . Therefore numerical implementation needs to regularize in these situations.

Thirdly, the approximation might yield values smaller that zero or larger than one which is problematic for calculating the log-likelihood which contains the term

The linear projection in the second term is not bounded between zero and one. That positivity is not ensured proves to be particularly problematic because in this case it is impossible to compute the approximation. This problem is discussed neither in (Joe; 1995) nor (Bhat; 2011). However, (Bhat and Sidhartan; 2011) briefly discusses the issue and state that it happens mainly during gradient based optimization. Their solution for this problem, which they describe as relatively rare, is to compute the approximation based on a different permutation until the result is positive. Likewise, the averaging suggested by Joe should ease this problem.

Finally typically does not pose large problems as in this case still is defined and the risk that the whole likelihood becomes larger than one usually is small. In any case this does not interfere with the maximization of the likelihood.

3.2 Mendell-Elston approximation

The basic idea of the ME approximation as introduced by Mendell and Elston (1974) is to approximate the truncated normal by a normal distribution with matching moments. For reasons of uniformity of presentation we will base the following exposition on the same factorization as SJ (see (5)),

| (8) | ||||

| (9) | ||||

Therefore, in order to apply the approximation it is necessary to know all the conditional moments that show up in (9). (Kamakura; 1989) utilizes the ME approximation for MNP model estimation and provides an algorithm for the calculation of the moments of a truncated normal (see Kamakura; 1989, p. 256). Using our notation an algorithm can be defined for the general case of as follows: For and we start with and . Then the algorithm for ME is given by

| (10) | ||||

where and with . Furthermore, note that denotes the short-form of . In combining the recursive algorithm with (9) we denote the general ME-approximation as,

| (11) | ||||

Again, the ordering of the components in the factorization in (8) is arbitrarily chosen from the possible permutations of the components. However, because of the very nature of the ME-approximation it is possible to tackle this problem without brute-force averaging. The idea is to pick the factorization, whose factors are closest to the normal distribution. In this regard, (Langdon; 1984) derived the first four moments of factors resulting from different factorizations of a three alternative probit model. The skewness and kurtosis of those factors were closest to the normal distribution whenever the terms were sorted with the standard deviation of the utility differences in ascending order.

With his recursive algorithm in mind (Kamakura; 1989) presents a slightly modified procedure. The first term is still the one with the minimum standard deviation but all subsequent ones are chosen to have the minimal amongst the remaining integration limits. The simulations by (Connors et al.; 2014) reveal that instead of only focusing on the standard deviations the optimal factorization (in terms of approximation accuracy) uses a decreasing order of the upper integration limits.

3.3 Bivariate Mendell Elston approximation

Recently, Trinh and Genz (2015) presented an improved version of the ME-approximation. The major contribution is the use of bivariate normal distributions within the ME-approximation and the development of formulas for the corresponding moments whose derivation is largely based on prior results from (Muthen; 1990). Furthermore, their algorithm utilizes several pre-processing steps routinely used in conjunction with quadrature methods (e.g. handling the covariance matrix in its Cholesky factorized form). However, their approximation is still based on the general idea of ME and basically results in the replacement of the univariate with bivariate normal distributions in (11). We will abbreviate this special variant of ME as bivariate Mendell-Elston (bME).

In the simulations that accompany their theoretical work (Trinh and Genz; 2015) confirm the aforementioned results of (Connors et al.; 2014) and show that reordering leads to considerable gains with regard to the predictive accuracy. Furthermore, they illustrate that

for their bivariate ME-approximation it is possible to perform the

reordering based on the results from the univariate ME, which provides

substantial benefits regarding computation time.

3.4 Comparison of MVNCDF approximations: literature review

In this section we briefly review the literature on comparisons between the SJ- and ME-approximation with regard computation time and predictive accuracy. From the previous paragraphs we know that both approximations rely on the availability of a method to compute one dimensional MVNCDFs. For the computation of the SJ and the bME approximation additional two dimensional MVNCDF-integrals need to be solved, which is computationally more burdensome.444A comparison of the computational burden of evaluating the one dimensional Gaussian cdf versus a bivariate MVNCDF in MATLAB led to roughly a factor 15. Furthermore, the computational costs of the two strategies to improve the approximation accuracy by averaging over different permutations of the components vary by a large margin. (Joe; 1995) proposes that averaging over all alternative is the optimal strategy for the SJ-approximation, however, this strategy has fixed computational costs of . Optimal reordering strategies for the ME-approximations boil down to a sorting operation with worst case costs of .

Those preliminary observations are reflected in the empirical findings regarding the comparison of computation times. (Joe; 1995) states (without providing detailed quantitative evidence) that the ME-approximation is faster than the all-permutations SJ-approximation. He attributes this to the computational burden imposed on the SJ-approximation by the need to evaluate MVNCDF-integrals of dimension higher than one (see Joe; 1995, p. 960).

(Connors et al.; 2014) compare the computation times of an optimally ordered ME-approximation and a SJ-approximation with 10 reorderings in a broad set of possible covariance configurations. Depending on the dimension of the MVNCDF the SJ-approximation is on average 12 to 63 times slower than the ME-approximation (see Connors et al.; 2014, p. 130).555It is worth noting that the simulations by (Connors et al.; 2014) reveal that as expected both approximations are faster than the GHK-algorithm and quadrature methods. (Trinh and Genz; 2015) confirm parts of this finding for the univariate and bivariate ME-approximation, which are shown to be at least 10 times faster than Monte Carlo evaluation of the integral. Similar results are reported by (Rosa; 2003), who evaluates the approximations in the context of Probit-Based Stochastic User Equilibrium models and states that the mean computation time for the SJ-approximation is up to 100 times larger than the respective value of the ME-approximation. Furthermore, the standard deviation of the computation time is higher for the SJ-approximation (see Rosa; 2003, p. 181). (Rosa; 2003) utilizes averaging over all permutations whenever the integral dimension is smaller than 10 and 1000 permutations for larger integrals. Finally, (Trinh and Genz; 2015) compare the computation times of SJ and their bivariate ME-approximation for one specific five-dimensional MVNCDF and find that their algorithm is 16 times faster than a SJ-approximation with averaging over all permutations.

The results regarding the prediction accuracy are not as clear-cut as the result regarding computation time. On the one hand the results by (Joe; 1995) suggest that the approximations are comparable. Furthermore, (Trinh and Genz; 2015) also present simulations were the SJ-approximation with all permutations is superior to the univariate as well as the bivariate ME-approximation.

On the other hand the results of (Connors et al.; 2014) and (Rosa; 2003) suggest that the SJ-approximation is inferior with regard to almost any performance metric. (Rosa; 2003) reports that the average percentage error is always larger for the SJ-approximation when compared to the ME-approximation (see Rosa; 2003, p. 178ff). The average percentage error of the ME-approximation is found to be up to 20 times lower than the error of the SJ-approximation. However, (Rosa; 2003) illustrates that it is possible to narrow down the spread by excluding cases with small true probabilities from the simulations. This is in line with (Trinh and Genz; 2015), who find that the predictive accuracy of both ME-approximations is lower for smaller true probabilities.

(Connors et al.; 2014) provide a broad range of simulation settings. However, the setup differs slightly from (Rosa; 2003) and (Joe; 1995) because the accuracy/error calculations are done for the logarithm of the probabilities. For the simulation setting of (Connors et al.; 2014) the ME-approximation seems to outperform the SJ-approximation for every number of choice alternative regardless of the performance measure reported.

It is worth noting that the results of (Connors et al.; 2014) might be influenced by the method used to generate the covariance matrices. The relationship between a correlation (R) and a covariance matrix () is,

| (12) |

where is a diagonal matrix of the same dimension as R, whose entries are the standard deviations . The covariance matrices in (Connors et al.; 2014) are computed as , where is the identity matrix and is a scalar and as well as the correlation matrix R are generated at random. When compared to equation (12) it is clear that by construction the methodology of (Connors et al.; 2014) typically produces covariance matrices with small correlations for sizeable .

However, the ME-approximation works particularly well for MVNCDF with small correlations (see Rice et al. (1979, p. 455f) and Trinh and Genz (2015, p. 995)) and, therefore, this method might benefit from the experimental methodology.

In summing up this section we conclude that the literature indicates that the ME-approximation is supposedly superior to the SJ-approximation with regard to computation time as well as prediction accuracy. It is worth noting that most comparisons considered the SJ-approximation with averaging over all permutations, while (Bhat; 2011) suggests to use only one permutation for MaCML estimation. Furthermore, we outlined that the appearance of small true probabilities as well as the correlation structure might influence the performance of the approximations and we will devote special care to those cases in the following simulations.

4 Main findings

In this section the properties of estimators obtained by maximizing the approximated composite marginal likelihood are discussed. Here estimation is performed using observations of sample size where accounts for all explained and explanatory variables. In the motivating example .

The scaled logarithm of the composite likelihood666Note that (standard) maximum likelihood estimation is included in the CML framework as one special case. is denoted as where denotes the parameter vector to be estimated. For the model in section 2 thus . Then the CML approach obtains the estimator

Under well known appropriate regularity conditions we obtain almost surely both pointwise and uniformly in where the limiting criterion function is continuous in and uniquely maximized at the true parameter vector .

The MaCML approach defines the pseudo CML by replacing the MVNCDF by the approximation . Here in this paper. Consequently the MaCML estimator is defined as

Again almost surely uniformly in combination with continuity of the limiting criterion function leads to convergence of to , the maximizer of over (assuming uniqueness of the maximizer). It follows that the asymptotic bias is given by and hence can be investigated based solely on .

Therefore in this section, first we investigate the properties of (section 4.1) followed by results for the finite-sample case in section 4.2. All calculations are done in MATLAB R2015b,777Some of our functions are derived from (Genz; 2015) as well as from the R and GAUSS code of (Bhat and Sidhartan; 2011). whose mvncdf function is used to compute the ’true probabilities’. This function is stated to provide an accuracy of for integrals of dimension smaller than four and for integrals of higher dimension.

4.1 Large-Sample Properties of MaCML estimators

In this section we assess the consistency of MaCML estimation with four different approximations,

-

1.

SJ as an average over all permutations (SJ-A),

-

2.

SJ with one random permutation (SJ-1),

-

3.

semi-optimally ordered, univariate ME (ME),

- 4.

The bME variant we use combines bME with a univariate reordering in order to speed up computations: For ME we apply a reordering scheme where we reorder the ASCs in descending order. Even though the ASCs are a prominent part of the upper integration limits of the ME approximations (see (10) and remember that ) this is not the optimal reordering suggested by (Connors et al.; 2014). Most notably we do not reassess and potentially alter the reordering after each component of the approximation (see (11)) is computed. However, preliminary tests have shown that the optimal reordering scheme, which reorders after each component is computed, leads to discontinuities in the limiting likelihood function . Clearly discontinuities pose severe threats for the typically applied gradient methods for numerical function optimization.

In order to apply SJ-1 in the context of the limiting distribution, which is the expected value of the scaled likelihood, we compute the mean of all possible log likelihood values resulting from the single ordering approximations. In comparison to SJ-A this mean value is an outer mean (averaging the logarithms of the approximated probabilities), while in the case of SJ-A the mean is computed as an inner mean (first averaging, then taking logarithms) of the approximated probabilities.

We simulate limiting (pseudo-)likelihoods for 8.000 different models of the type introduced in section 2. The ASCs as well as the standard deviations are drawn from uniform distributions and , respectively. We iterate through different bounds (, )888Values of larger than 2 lead to an extensive share of models with at least one very small true probability (e.g. for K=1, L=4 we observed that 96 percent of the models have at least one true probability smaller than 0.001). and simulate 1000 instances for each combination.

The correlation matrices are generated by the Vine-based method of (Lewandowski et al.; 2009) which is designed to uniformly generate correlation matrices from the space of positive definite correlation matrices (see Lewandowski et al.; 2009). In order to simulate matrices with small correlations it is possible to depart from the uniform sampling and instead sample with probability proportional to , where scales the penalty for the appearance of large correlations. The respective covariance matrices are calculated using (12).

We search the maximum of each limiting (pseudo-)likelihood using an optimization algorithm, which is constrained to [-2L,2L] for each parameter and initialized at the true values in order to speed up the calculations. As this setup essentially imposes an additional condition of local identifiability around the true value the results presented below are best-case estimates of the asymptotic bias.

We report the errors as measured by a) the root mean squared error (RMSE), and b) the mean absolute error (MAE), , where denotes a transformation of the estimator and the true parameter vector used in the -th Monte Carlo replication. The mapping hereby corresponds either to the difference in a particular coordinate , the maximum over all coordinates or the maximal deviation in the corresponding probabilities .

The first column of Table 1 shows the average asymptotic estimation error of the approximations with regard to the estimated parameters. The first and by far most important observation is that even for a simple model all approximations yield inconsistent estimators. For reasons already discussed both SJ variants and bME are comparable accuracy-wise, while the univariate ME approximation has the worst accuracy. Note, that the better performance of approximations that utilize a bivariate MVNCDF is expected because the computation of each true probability involves only the evaluation of a three dimensional MVNCDF (see (1)).

|

| 0 | 0.001 | 0.01 | 0.05 | ||

| max. RMSE | SJ-A | 0.196 | 0.049 | 0.029 | 0.023 |

| SJ-1 | 0.194 | 0.040 | 0.027 | 0.023 | |

| ME | 0.331 | 0.103 | 0.091 | 0.082 | |

| bME | 0.140 | 0.158 | 0.138 | 0.113 | |

| max. MAE | SJ-A | 0.058 | 0.021 | 0.018 | 0.015 |

| SJ-1 | 0.057 | 0.021 | 0.017 | 0.015 | |

| ME | 0.143 | 0.069 | 0.064 | 0.061 | |

| bME | 0.063 | 0.086 | 0.082 | 0.074 | |

| number of obs. | 8000 | 5218 | 4041 | 2384 |

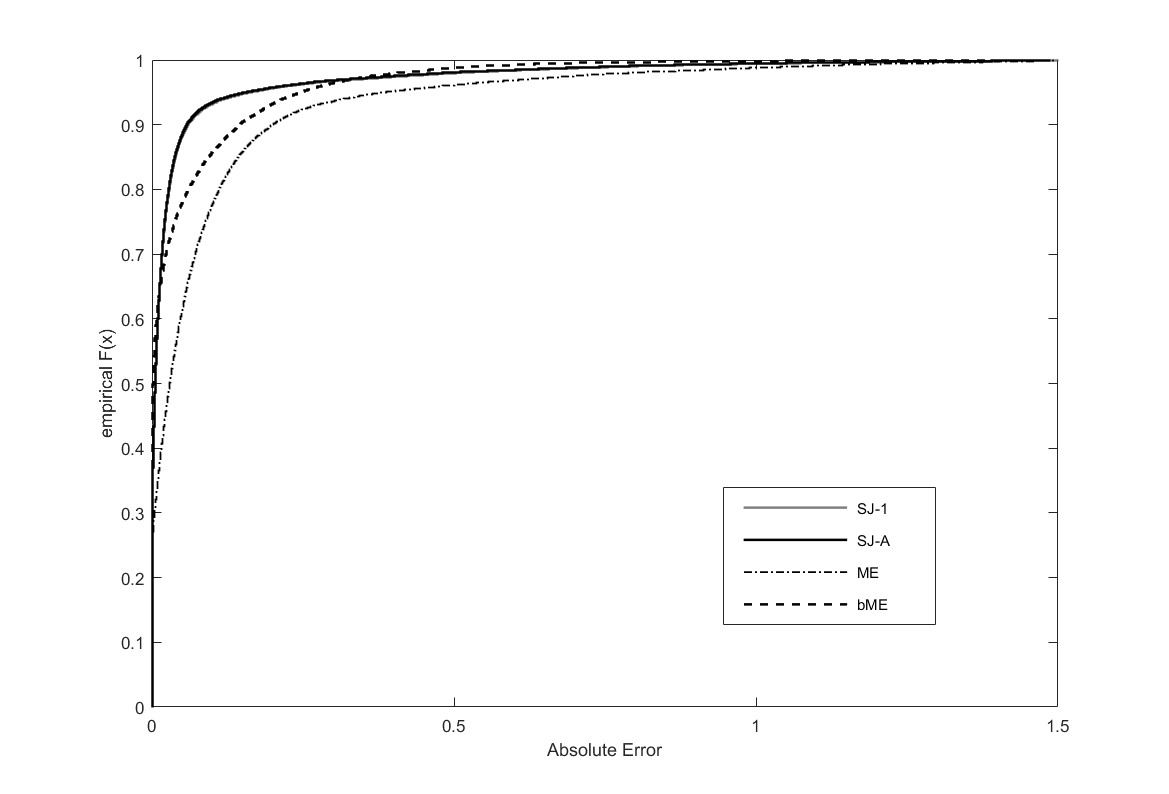

Furthermore, the SJ variants show a large difference between MAE and RMSE, which hints to the fact that the SJ might produce a higher share of large errors, especially when compared to the values for bME which have a smaller difference. Figure 1, which depicts the empirical distribution functions of the maximum absolute error for the 8.000 models of the base case, provides further evidence in this regard. As is clearly visible from the intersecting empirical cumulative density functions that neither bME nor the SJ variants (whose graphs are practically indistinguishable) are uniform best. However, we conclude from the figure that ME is dominated by the three other approximations with respect to the estimation accuracy measured by MAE. Additionally, it is clearly visible that both SJ variants and bME have extremely small asymptotic errors for about 70 percent of the simulation instances, while this share for ME is only 30 percent. Therefore, even though the MaCML estimators are inconsistent, we can conclude that at least for the simple model considered here the asymptotic error is often very small.

In order to assess the effect that the occurrence of small true probabilities has on the estimation Table 1 includes results for subsets of the simulation. Those subsets contain only models whose smallest true probability is larger than the respective thresholds. The discussion from section 3.4 suggests that the performance of the approximations should improve with rising thresholds. We are able to observe this effect for all approximations. However, while the accuracy of bME also improves the change is far less substantial and, therefore, both SJ variants outperform bME for all but the base case.

For several applications not the coefficients but the predicted probabilities at the estimated coefficients, which we will from now on call estimated probabilities, are of primary concern. Because the mapping from parameter estimates to probabilities is non-linear the errors in estimated probabilities need to be assessed separately from the estimation error of the parameters. Table 2 shows that those errors are substantially smaller than the errors in the estimated parameter. This might be mainly an effect of the tail regions of MVNCDF being insensitive to changes in the parameters. It is, however, noteworthy that there are mixed results for the performance gains resulting from the exclusion of small probabilities. While both SJ variants and ME show small improvements the accuracy of bME decreases notably. When interpreting those results, it is important to keep in mind that the MaCML approach is pitched for situations where MSL is infeasible (see Bhat and Sidhartan; 2011) because of large choice sets. With a large number of alternatives in a choice set the chance is high that some have a choice probability which is small.

| 0 | 0.001 | 0.01 | 0.05 | ||

| max. RMSE | SJ-A | 0.004 | 0.003 | 0.003 | 0.003 |

| SJ-1 | 0.004 | 0.003 | 0.003 | 0.003 | |

| ME | 0.015 | 0.014 | 0.014 | 0.013 | |

| bME | 0.013 | 0.016 | 0.017 | 0.020 | |

| max. MAE | SJ-A | 0.002 | 0.002 | 0.002 | 0.002 |

| SJ-1 | 0.002 | 0.002 | 0.002 | 0.002 | |

| ME | 0.012 | 0.011 | 0.010 | 0.010 | |

| bME | 0.007 | 0.010 | 0.012 | 0.015 | |

| number of obs. | 8000 | 5218 | 4041 | 2384 |

Furthermore we have investigated the interrelation between the magnitude of correlation and estimation accuracy. The setup is similar to the simulations used in the preceding paragraph but for every we only draw 4.000 true models (500 for each combination of and ). As described in the introduction to this section increased values of lead to fading correlations. The results are shown in table 3. The first column denotes the case of uniform sampling , which was used for the previous simulations. Reading from left to right, it is clearly visible that as the correlations get weaker (for increasing ) MAE and RMSE are declining. This observation, which applies to all approximations is not surprising because a MVNCDF without correlations is just the product of its marginal distribution functions.

| 1 | 5 | 50 | 100 | ||

|---|---|---|---|---|---|

| max. RMSE | SJ-A | 0.165 | 0.134 | 0.113 | 0.117 |

| SJ | 0.171 | 0.132 | 0.116 | 0.115 | |

| ME | 0.270 | 0.240 | 0.228 | 0.227 | |

| bME | 0.131 | 0.115 | 0.104 | 0.103 | |

| max. MAE | SJ-A | 0.049 | 0.036 | 0.029 | 0.029 |

| SJ | 0.049 | 0.036 | 0.029 | 0.028 | |

| ME | 0.126 | 0.105 | 0.097 | 0.096 | |

| bME | 0.060 | 0.055 | 0.048 | 0.048 |

To sum up the large-sample results indicate that the SJ variants and bME are at par with regard to the parameter estimation error. SJ is superior for situations without small probabilities and for estimated probabilities. Furthermore, this section showed that with regard to the limiting estimation error ME is inferior to the other three approximation in almost any setting. The performance of all approximations is improved almost equally as correlations get weaker.

4.2 Finite-Sample Properties of MaCML estimators

We assess the finite sample properties of MaCML estimation with three different approximations,

The reordering strategies match those from the large-sample simulation but in this section we apply MaCML estimation to a model selected from the literature (see Bhat and Sidhartan (2011) as well as Cherchi et al. (2016)). The model is a cross-sectional mixed multinomial probit model with five alternatives. Those alternatives are explained by five explanatory variables (drawn from independent standard normal distributions) and their respective parameters are assumed to be an instance of a multivariate normal distribution with mean and covariance matrix,

The error terms are assumed to be normally distributed with a mean of zero and a diagonal covariance matrix whose entries are 0.5. We generated 20 data sets of size 5000 by drawing values of the vector and the error term from their respective distribution. Based on those values we calculated the utility and the chosen alternative is the one with the highest utility.

Our aim is to estimate the linear (b) as well as the covariance parameters. The covariance parameters are estimated using the corresponding Cholesky decomposition (). In order to find the optimum of the likelihood function we rely on the BFGS-algorithm provided by MATLABs fminunc function. To ensure competitive computation times we have derived the respective analytic gradients for all pseudo-likelihoods but other than that relied on the default options. Following (Bhat and Sidhartan; 2011) we initialize the optimizer at the true values and use one random permutation per observation for the SJ approximation, which stays the same during the optimization. We report the mean estimate over all 20 data sets as well as the estimation errors in form of the mean MAE over all 20 data sets for each respective parameter. Note that the MAE is calculated as the mean of the respective absolute errors for each data set and is not equivalent to the absolute difference between the mean estimate and the true value.999We do not consider the Average Percentage Bias (APB) reported in (Bhat and Sidhartan; 2011), due to its known shortcomings. For reasons of comparability we calculated the APB as described in (Bhat and Sidhartan; 2011): For the SJ approximation our simulations resulted in an APB of 3.9%, while (Bhat and Sidhartan; 2011) report an APB of 5.5 % for the same experimental setting.

| Parameter | true value | SJ-1 | ME | bME | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| mean | MAE | SD MAE | mean | MAE | SD MAE | mean | MAE | SD MAE | ||

| linear parameters | ||||||||||

| 1.50 | 1.53 | 0.12 | (0.112) | 1.47 | 0.04 | (0.095) | 1.47 | 0.04 | (0.067) | |

| -1.00 | -1.02 | 0.09 | (0.045) | -0.99 | 0.03 | (0.069) | -0.98 | 0.03 | (0.043) | |

| 2.00 | 2.04 | 0.18 | (0.052) | 1.97 | 0.04 | (0.066) | 1.95 | 0.05 | (0.042) | |

| 1.00 | 1.01 | 0.09 | (0.048) | 0.96 | 0.04 | (0.039) | 0.97 | 0.03 | (0.046) | |

| -2.00 | -2.03 | 0.18 | (0.105) | -1.96 | 0.05 | (0.080) | -1.95 | 0.06 | (0.077) | |

| covariance parameters (Cholesky factors) | ||||||||||

| 1.00 | 1.03 | 0.10 | (0.053) | 1.05 | 0.06 | (0.059) | 1.03 | 0.04 | (0.045) | |

| -0.50 | -0.52 | 0.07 | (0.044) | -0.51 | 0.06 | (0.054) | -0.52 | 0.06 | (0.058) | |

| 0.25 | 0.26 | 0.05 | (0.081) | 0.14 | 0.11 | (0.078) | 0.31 | 0.07 | (0.073) | |

| 0.75 | 0.75 | 0.09 | (0.138) | 0.75 | 0.08 | (0.127) | 0.73 | 0.06 | (0.059) | |

| 0.00 | 0.00 | 0.07 | (0.056) | 0.16 | 0.16 | (0.107) | -0.07 | 0.08 | (0.041) | |

| 0.87 | 0.90 | 0.09 | (0.046) | 0.97 | 0.11 | (0.062) | 0.87 | 0.04 | (0.036) | |

| 0.43 | 0.41 | 0.08 | (0.053) | 0.45 | 0.05 | (0.075) | 0.38 | 0.08 | (0.044) | |

| -0.14 | -0.18 | 0.09 | (0.069) | -0.18 | 0.08 | (0.044) | -0.18 | 0.08 | (0.045) | |

| 0.00 | -0.02 | 0.09 | (0.049) | -0.01 | 0.08 | (0.063) | -0.01 | 0.08 | (0.052) | |

| 0.87 | 0.86 | 0.11 | (0.053) | 0.85 | 0.06 | (0.071) | 0.86 | 0.06 | (0.046) | |

| 0.24 | 0.27 | 0.08 | (0.071) | 0.30 | 0.10 | (0.076) | 0.25 | 0.07 | (0.029) | |

| 0.00 | 0.01 | 0.09 | (0.047) | 0.19 | 0.20 | (0.058) | -0.06 | 0.10 | (0.049) | |

| 0.60 | 0.59 | 0.08 | (0.044) | 0.65 | 0.09 | (0.029) | 0.59 | 0.06 | (0.054) | |

| 0.00 | -0.01 | 0.10 | (0.124) | -0.06 | 0.09 | (0.057) | 0.01 | 0.08 | (0.060) | |

| 1.00 | 0.98 | 0.11 | (0.047) | 0.91 | 0.10 | (0.042) | 0.98 | 0.05 | (0.048) | |

| Mean MAE and mean SD across parameters | 0.097 (0.067) | 0.081 (0.067) | 0.061 (0.051) | |||||||

| Mean time and SD in minutes | 6.01 (1.65) | 3.80 (0.90) | 13.68 (4.78) | |||||||

The results in Table 4 show that the findings from the last section do only partially carry over to the finite sample case. The bME approximation shows the smallest MAE with ME and SJ in the second and third place. The major difference between bME and ME is in the ability to recover the covariance parameters. Both, ME and bME are slightly superior in recovering the linear parameters when compared to SJ. The SJ estimation results showed a greater variability when compared to ME and bME. The varying ability to recover the linear parameters is clearly indicated by the large MAE, especially when compared to the good mean estimate. However, there were, as expected because the estimation was initialized at the true parameter values, no results suspicious of non-convergence.

The results regarding the computation time are of course only informative with respect to the relative difference between the approximations and in this regard they are in line with the previous discussion. Especially bME is dramatically slower than ME and SJ. This has several reasons: First of all this approximation is based on multiple bivariate MVNCDFs whose evaluation accounts for most of the computational burden. Second, this leads to – in terms of computing time – more costly calculations for the analytic gradient. Third, in order to ensure semi-optimal reordering a full univariate ME approximation needs to be computed within the bME-algorithm. On the other hand SJ is slower than ME because of the need to evaluate bivariate MVNCDFs and their corresponding gradients.

Table 5 provides information on the accuracy of estimates of quotients of the coefficients such as the value of time in mode choice models. It can be seen that the values for ME and bME only slightly decreases while the performance of SJ-1 now is comparable to the one achieved using ME. This indicates that the SJ-1 approach shows a larger tendency to converge to various points on the line . Preliminary experiments with random initialization show that this behavior features very prominently in these cases.

| Parameter | true value | SJ-1 | ME | bME | |||

|---|---|---|---|---|---|---|---|

| mean | MAE | mean | MAE | mean | MAE | ||

| linear parameters | |||||||

| -0.67 | -0.67 | 0.03 | -0.68 | 0.03 | -0.67 | 0.02 | |

| 1.33 | 1.34 | 0.04 | 1.34 | 0.04 | 1.33 | 0.04 | |

| 0.67 | 0.66 | 0.02 | 0.66 | 0.02 | 0.66 | 0.02 | |

| -1.33 | -1.33 | 0.03 | -1.34 | 0.04 | -1.33 | 0.04 | |

| Mean MAE | 0.024 | 0.024 | 0.024 | ||||

It is worth noting that by design the starting values of the optimization are not varied101010The same is true for (Bhat and Sidhartan; 2011) and (Cherchi et al.; 2016), who all focus on parameter recovery starting from the true values. but like MNP models in general the convergence of an optimizer to a global optimum is not assured for MaCML estimation and, therefore, finite-sample results are sensitive to initial values. An investigation of this point is left for further research.

| Tolerance | 0.5 | 0.5 | 0.5 | |

|---|---|---|---|---|

| SJ-1 | mean MAE | 0.064 | 0.097 | 0.098 |

| SAD | - | 0.422 | 0.014 | |

| comp. time | 2.25 | 7.17 | 9.60 | |

| ME | MAE | 0.087 | 0.088 | 0.088 |

| SAD | - | 0.022 | 0.000 | |

| comp. time | 5.49 | 6.20 | 6.17 | |

| bME | MAE | 0.062 | 0.063 | 0.063 |

| SAD | - | 0.020 | 0.000 | |

| comp. time | 14.49 | 22.10 | 21.81 |

In comparing our results with (Bhat and Sidhartan; 2011) we noticed that (Bhat and Sidhartan; 2011) utilize a custom gradient tolerance of in order to assess whether the calculated gradient is numerically zero. The lower the gradient tolerance the faster the optimizer terminates once it reaches a point close to the optimum or for that matter any ’flat region’ of the pseudo-likelihood. The results in Table 6, which we have generated by simulating 10 data sets of size 5000 for every gradient tolerance, show that lowering the gradient tolerance for our example not only leads to different MAEs but also influences the computation times. The main profiteer from a lower gradient tolerance is the SJ approximation, while the results of ME and bME remain remarkably stable. This hints to the fact that estimation performance might be improved by fine-tuning the optimization.

5 Conclusions

In this paper we have surveyed several analytic approximations for the MVNCDF with regard to their feasibility in MNP model estimation. Using a simple cross sectional model we compared four approximations from the literature (SJ-1, SJ-A and ME as well as bME) focusing on estimation rather than prediction accuracy.

Our main results given in section 4.1 show that even for the simple model considered in this paper the MaCML-estimator is inconsistent for all approximations considered. The degree of asymptotic bias changes with the specific data generating process but is often very small. We have identified that true

models with at least one small probability as well as strong correlation structures have an adverse effect

on estimation accuracy. Furthermore, our simulations show that the parameter estimates are asymptotically more biased than the probability estimates. This is important to keep in mind if the MaCML-estimates

are used to calculate the value of travel time or equivalent quantities involving one or more parameters.

In general the large-sample results show that SJ and bME are almost head-to-head with SJ

being superior in special cases while we find that the ME approximation championed by (Connors et al.; 2014) is

dominated by those approximations with respect to asymptotic absolute bias in our setup.

Still, all approximations

lead to inconsistent estimators. While the asymptotic bias is small for the example considered there is no guarantee that this is also true for more complicated models. The results in this paper provide hints on the directions where the search for ’bad’ situations continues.

On the other hand it might be possible to derive explicit bounds for the bias as a function of bounds

for the approximation error (see e.g. the work of Langdon (1984) on the trivariate ME approximation). Such a bound would be very helpful as it might allow to identify cases where a large

bias is to be expected and to obtain an (estimated) bound on the magnitude on the bias. This is left

for future research.

The results from our finite sample testing, albeit limited to just one selected model with limited number of replications, show that bME and ME perform slightly better than SJ with only one permutation, which is the default MaCML configuration. This is contrary to the large sample results where the opposite ordering has been found. Our finite sample results also shed some light on the typical runtime of MaCML estimation. The computation of bME is an order of magnitude slower than both alternatives and hence probably not the preferred option.

Secondly, estimation utilizing SJ in the example was slower than ME-based MaCML estimation due to the evaluation of bivariate MVNCDFs and its gradients. This is especially important in considering internal averaging, which is in theory beneficial to SJs performance but adds to the costs from a computational standpoint. Jointly the result indicate that the choice of the appropriate approximation to be used is not straightforward and more research is needed.

The investigation of the approximations demonstrated that the topic of ordering of the components for the numerical optimization is a very sensitive one as it has a large impact on the results both in terms of accuracy and in terms of computation time. From our results for the limiting pseudo-likelihood for SJ it is demonstrated in line with the literature that already using only one random permutation delivers similar results to averaging over all combinations. However, it is important to use the same ordering for the whole optimization. For ME an optimal ordering might be beneficial but again it is of importance that only one ordering is used because otherwise discontinuities in the criterion function might cause problems for the numerical optimization. As the optimal ordering depends on the parameter values in this case it is unclear how the ordering should be done. Again this is left for future research.

Finally the discussion in section 4.2 suggests that it is warranted to assess the optimization of MaCML pseudo-likelihoods more broadly by moving beyond parameter recovery which induces the need to find viable initial estimators. In this respect it is currently totally unknown what the consequences of different initialization routines on the properties of the MaCML estimators are. Preliminary tests suggest that the SJ approach might be more heavily affected than the ME approximations to this issue. Again detailed investigations are left for future research.

Acknowledgments

This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors. The authors would like to thank Daniel Rodenburger for pointing the authors to the idea of unifying the presentation of the ME and SJ approximation as well as for carrying out some preliminary simulations.

References

- (1)

- Bhat (2011) Bhat, C. R. (2011). The maximum composite marginal likelihood (macml) estimation of multinomial probit-based unordered response choice models, Transportation Research Part B 45(7): 923–939.

- Bhat and Sidhartan (2011) Bhat, C. R. and Sidhartan, R. (2011). A simulation evaluation of the maximum approximate composite marginal likelihood (macml) estimator for mixed multinomial probit models, Transportation Research Part B 45(7): 940–953.

- Calfee et al. (2001) Calfee, J., Winston, C. and Stempski, R. (2001). Econometric issues in estimating consumer preferences from stated preference data: A case study of the value of automobile travel time, The Review of Economics and Statistics 83(4): 699–707.

- Cherchi et al. (2016) Cherchi, E., Dubey, S., Daziano, R. A., Pinjari, A. R. and Bhat, C. R. (2016). Simulation evaluation of emerging estimation techniques for multinomial probit models, TRB 95th Annual Meeting Compendium of Papers .

- Connors et al. (2014) Connors, R., Hess, S. and Daly, A. (2014). Analytic approximation for computing probit choice probabilities, Transportmetrica 10(2): 119–139.

- Daganzo et al. (1977) Daganzo, C. F., Bouthelier, F. and Sheffi, Y. (1977). Multinomial probit and qualitative choice: A computational efficent algorithm, Transportation Science 11(4): 338–358.

- Ferguson (1996) Ferguson, T. (1996). A Course in Large Sample Theory, Chapman & Hall/CRC, Boca Raton.

- Genz (2015) Genz, A. (2015). MVNXPB, a MATLAB/Octave function for the approximation of multivariate Normal probabilities., www.math.wsu.edu/faculty/genz/software/matlab/.

- Hajivassliliou (2000) Hajivassliliou, V. A. (2000). Practical issues in maximum simulated likelihood, in R. Mariano, T. Schuermann and M. J. Weeks (eds), Simulation-based Inference in Econometrics, Cambridge University Press, Cambridge, chapter 3, pp. 71–99.

- Horowitz et al. (1982) Horowitz, J. L., Sparmann, J. M. and Daganzo, C. F. (1982). An investigation of the accuracy of the clark approximation for the multinomial probit model, Transportation Science 16(3): 382–401.

- Joe (1995) Joe, H. (1995). Approximations to multivariate normal rectangle probabilities based on conditional expectations, Journal of the American Statistical Association 90(431): 957–964.

- Kamakura (1989) Kamakura, W. A. (1989). The estimation of multinomial probit models: A new calibration algorithm, Transportation Science 23(4): 253–265.

- Langdon (1984) Langdon, M. G. (1984). Improved algorithms for estimating choice probabilities in the multinomial probit model, Transportation Science 18(3): 267–299.

- Lewandowski et al. (2009) Lewandowski, D., Kurowicka, D. and Joe, H. (2009). Generating random correlation matrices based on vines and extended onion method, Journal of Multivariate Analysis 100(9): 1989–2001.

- Mendell and Elston (1974) Mendell, N. and Elston, R. (1974). Multifactorial qualitative traits: Genetic analysis and prediction of recurrence risks, Biometrics 30: 41–57.

- Muthen (1990) Muthen, B. (1990). Moments of the censored and truncated bivariate normal distribtion, British Journal of Mathematical and Statistical Psychology 43: 131–143.

- Rice et al. (1979) Rice, J., Reich, T. and Cloninger, C. (1979). An approximation to the multivariate normal integral: Its application to multifactorial qualitative traits, Biometrics 35: 451–459.

- Rosa (2003) Rosa, A. (2003). Probit Based Methods in Traffic Assignment and Discrete Choice Modelling, Phd-Thesis, Napier University.

- Sidharthan (2012) Sidharthan, R. (2012). On the Estimation and Application of Flexible Unordered Spatial Discrete Choice Models, Phd-Thesis, The University of Texas at Austin.

- Solow (1990) Solow, A. R. (1990). A method for approximating multivariate normal orthant probabilities, Journal of Statistical Computation and Simulation 37: 225–229.

- Train (2009) Train, K. E. (2009). Discrete Choice Methods with Simulation, 2 edn, Cambridge University Press, Cambridge.

- Trinh and Genz (2015) Trinh, G. and Genz, A. (2015). Bivariate conditioning approximations for multivariate normal probabilities, Statistics and Computing 25(5): 989–996.

- Varin et al. (2011) Varin, C., Reid, N. and Firth, D. (2011). An overview of composite likelihood methods, Statistica Sinica 21: 5–42.