A note on the Esscher transform of affine Markov processes

Abstract.

In affine models, both the martingale property of stochastic exponentials and non-explosion of affine processes can be characterized in terms of minimality of solutions to a system of generalized Riccati differential equations. We improve these characterizations for affine processes on by Mayerhofer, Muhle-Karbe and Smirnov (2011) and Keller-Ressel and Mayerhofer (2014) by showing that the characterizing minimal solution is the unique one.

1. Introduction

Affine Markov Processes constitute a fairly general class of Markov processes. They comprise, among others, the class of Lévy-processes, OU-type processes (with linear drift) driven by Lévy noise, the well known Feller diffusion [11], many celebrated interest rate models ([5], [8], [9]), stochastic volatility models in finance (Such as Bates’ [2], Heston’s [12] and Barndorff-Nielsen, & Shepard’s [1]), and models of default risk, e.g. [7]. Their extensive use in finance has motivated stochastic processes research in the last two decades. Existence Theories for general affine processes on particular state spaces have been established: We mention the one for canonical state spaces [6] and for positive semi-definite matrices [3].

Undoubtably, the class of Lévy processes [19] is the largest subclass of affine processes with a well known and well established theory. Affine processes allow differential semimartingale characteristics which are affine in the state variable. This more general dynamic behaviour complicates their analysis, and distinguishes them from the Lévy-class e.g. in the following regards:

-

(i)

A Lévy process is non-explosive, if and only if has zero potential. Affine processes, however, may explode e.g., due to increasing (along every path) jump intensities, see e.g., [6, Example 9.3 ].

-

(ii)

A Lévy process has finite exponential moment, if and only the associated Lévy-measure does [19, Theorem 25.17]. This entails, for instance, that the moment explosion is a time independent feature. In affine models, however, moment explosion may occur in finite time. For instance, the Feller diffusion [11] has non-centrally chi-square distributed marginal distributions, hence does not admit finite exponential moments of all orders. More interesting examples are provided by jump-diffusions.

-

(iii)

If is a conservative Lévy process with a.s., and for then the process

(1.1) is a true martingale (this is the so-called Esscher transform). This is not true for affine processes, in general, due to time-dependent moment explosion.

This paper deals expands on (i) and (iii)for affine processes. In this setting, the martingale property of stochastic exponentials and non-explosion of affine processes can be characterized in terms of minimality of solutions to a system of generalized Riccati differential equations. We improve the characterization of conservativeness for affine processes on by [6] and [18] by showing that minimal solutions are actually unique. In Theorem 3.1, we show that a process is conservative if and only if a related Riccati differential equation with trivial initial data does not admit non-trivial solutions. Using an exponential tilting technique we turn this result into a similar improvement of the martingale characterization of exponentially affine functionals of affine processes by [15]: For conservative affine processes starting at , the natural generalization of Lévy martingales of the form (1.1) is given by processes of the form

with an appropriately chosen . Not always such processes are either well defined for all times, nor do they always give rise to martingales. The characterization of the martingale property of is given by Theorem 4.1. Nevertheless, an Example in the final section 5 demonstrates that for a characterization of the validity of the affine transform formula and thus of moment explosion (ii) in terms of solvability of the associated generalized Riccati equations, the concept of minimal unique solutions as introduced in [15] is not redundant.

2. Setting

In this paper, is a stochastically continuous, affine Markov process with state space , see, e.g. [6]. This means, there are functions such that

| (2.1) |

for all , and . Here denotes the standard Euclidean scalar product on . Stochastic continuity of implies that are differentiable [17], [4] with functional characteristics

Furthermore, solve the generalized Riccati differential equations

| (2.2) | ||||

| (2.3) |

where and are of Lévy-Khintchine form on . In the following, we abbreviate the index sets and , and for a vector we write , where In particular111 The precise parametric conditions can be found in [6, Definition 2.6]. For the sake of simplicyt we use the minimal information necessary to derive our conclusions., for a positive semidefinite matrix , , and a Lévy measure on , we have

where is a truncation function.

Also, for , and for , the component can be written as

| (2.4) |

where , with for , . Here we use the truncation function from [6], which is a function defined in components by

and for .

Since for , we may adapt the definition of [15, Equation(5.1)]

which is the intersection of the effective domains of . For a generic affine process, we only know a-priori that . But if has non-empty interior, , then on , the functions are analytic. The last assumption will enter in section 4 only.

The partial order induced by is denoted by and is given by if and only if when and

We define a special property of a domain in :

Definition 2.1.

A set is order preserving, if for such that , we have imples .

3. Conservative Affine Processes

It can be shown that

for a real matrix , and that when , the first components of satisfy the generalized Riccati differential equation

| (3.1) |

where .

This section provides the following improvement of [18, Theorem 3.4]:

Theorem 3.1.

The following are equivalent:

-

(i)

is conservative.

-

(ii)

and the only solution of of (3.1) with is the trivial one.

The crucial point here is that we do not restrict ourselves to uniqueness only among –valued solutions of (3.1), as in [18] or in [6] (where the restriction is made to solutions being strictly negative for ).

A step to this result is the following special multivariate ODE comparison result, which is more general than [18, Proposition 3.3]:

Proposition 3.2.

Let and . If is a solution of (3.1), then , for all .

Proof.

We introduce

where . Clearly solve the generalized Riccati differential equations (2.2)–(2.3). By [10, Theorem 4.7.1] and a localizing argument, the process

is a local martingale, where is the infinitesimal generator of ; furthermore by construction we have

for each , a.s., because for any and we have

So is a positive local martingale, hence a supermartingale222For an alternative proof using the explicit semimartingale decomposition of , please consult [15, Proof of Proposition 4.6]. On the other hand, the process

is a martingale satisfying . It follows that for each , , and therefore, by taking logarithms, we obtain , for each . ∎

3.1. Proof of Theorem 3.1

In view of [6, Proposition 9.1] or [18, Theorem 3.4], only the direction (i) (ii) need to be proved. Suppose, for a contradiction, there exists a local solution on which is non-trivial. By Proposition 3.2 we have , hence there exist components of which are not identically zero on , while the last actually vanish identically zero on this interval. We introduce the index set . Without loss of generality we may assume that for , for and for . Let us choose be in , where , . Set . Knowing that for and all , we see that satisfies an autonomous differential equation

| (3.2) |

where . For each is given by

| (3.3) |

with , , for , and are positive, sigma-finite measures on which integrate

Let , where , . Since by (3.2)

we conclude that for

we have

| (3.4) |

Let us define the following Lévy measures on ,

where is a generic Borel set in whose closure is supported away from . In view of (3.4) these measures are well defined. Using the latter, we define a new system of generalized Riccati differential equations on ,

| (3.5) |

where is derived from in (3.3) by condensing into , for : For , we set

By construction, we know is a non-trivial solution of (3.5). We know that is analytic at least on the set

where . That means that is analytic in an open neighborhood of the origin. By the standard existence and uniqueness theorem of ODEs, we must have on , a mere impossibility. We have therefore proven uniqueness for solutions of the IVP (3.1) with initial data , and we are done.

4. True Exponentially Affine Martingales

Suppose be a conservative affine process on . In this section we are interested in characterizing the martingale property of discounted exponentially affine functionals of the form

for , and the linear functional , .

Let us define the extended functional characteristics , and , and the corresponding generalized Riccati differential equations

| (4.1) | ||||

| (4.2) |

For affine processes on canonical state spaces, the following is an improvement of [15, Theorem 3.1 (2)], because it is stated without using the notion of minimal solutions:

Theorem 4.1.

Proof.

By [15, Theorem 3.1 (2)] the assertion holds when the term ’unique solutions’ is replaced by ’minimal unique solution’.

Therefore, to prove the present assertion, it suffices to show that for , , , the unique minimal solutions and , of the Riccati equations (4.1)–(4.2), are actually unique.

The differential equation (4.2) for is a trivial once. Therefore it suffices to show that (4.1) yields unique solutions. By [15, Theorem 3.1 (2)], we also have that

is a -martingale on with expectation and .

Following the lines of the proof of [13, Theorem 4.14] concerning exponential tilting let us then conclude there exist measures , for each , such that is an affine process with characteristics

with real domain . Furthermore for every , , and , it holds that

In particular, we have is conservative. By Theorem 3.1, the system of generalized Riccati differential equations

| (4.3) | ||||

| (4.4) |

has a unique solution, namely the trivial one. Assume, for a contradiction, there exists a solution of (4.1) with . Define . Then is a solution of (4.3), and by assumption does not vanish identically. This contradicts Theorem 3.1.

∎

5. Non-uniqueness for Riccati differential equations

In the previous sections, we have shown that a characterizing minimal solution is actually the unique solution of a particular generalized Riccati differential equation. In general, however, we do not have uniqueness, but the affine transform formula (2.1) only holds for the unique minimal solution of the associated generalized Riccati differential equations (2.3)–(2.3) (the general theory for real exponential moments is provided in [15]).

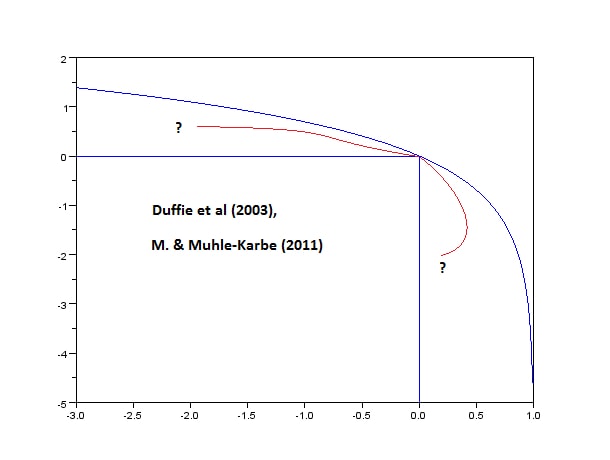

The following example of a homogeneous affine pure-jump process is used by [14] for the construction of exponentially affine strict local martingales and is inspired by Example 9.3 of Duffie et al (2003). Here the linear jump characteristic is the Lévy measure of a self-decomposable distribution. Non-uniqueness of the initial value problem below is due to the lack of regularity of the vector field at the boundary of the moment generating function.

Example 5.1.

Let , where , be an affine pure-jump process with negative linear drift

and absolutely continuous compensator

All other parameters of are zero. Since , is a special martingale with jumps of finite variation. In particular, we have the Lévy-Itô decomposition,

is homogeneous affine with characteristic exponent which satisfies for the initial value problem

| (5.1) |

It is straightforward to check that the unique solution of this equation is given by

However, for , also is a solution of (5.1).

References

- [1] O. Barndorff-Nielsen and N. Shephard, Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics, Journal of the Royal Statistical Society B, 63 (2001), pp. 167–241.

- [2] D. S. Bates, Post-’87 crash fears in the S&P 500 futures option market, Journal of Econometrics, 94 (2000), pp. 181–238.

- [3] C. Cuchiero, D. Filipović, E. Mayerhofer, and J. Teichmann, Affine processes on positive semidefinite matrices, Ann. Appl. Probab., 21 (2011), pp. 397–463.

- [4] C. Cuchiero and J. Teichmann, Path properties and regularity of affine processes on general state spaces, in Séminaire de Probabilités XLV, Springer, 2013, pp. 201–244.

- [5] Q. Dai and K. J. Singleton, Specification analysis of affine term structure models, Journal of Finance, 55 (2000), pp. 1943–1978.

- [6] D. Duffie, D. Filipovic, and W. Schachermayer, Affine processes and applications in finance, The Annals of Applied Probability, 13 (2003), pp. 984–1053.

- [7] D. Duffie and N. Garleanu, Risk and valuation of collateralized debt obligations, Financial Analyst Journal, 57 (2001), pp. 41–59.

- [8] D. Duffie and R. Kan, A yield-factor model of interest rates, Mathematical Finance, 6 (1996), pp. 379–406.

- [9] D. Duffie, J. Pan, and K. Singleton, Transform analysis and asset pricing for affine jump-diffusions, Econometrica, 68 (2000), pp. 1343–1376.

- [10] S. N. Ethier and T. G. Kurtz, Markov processes: characterization and convergence, vol. 282, John Wiley & Sons, 2009.

- [11] W. Feller, Two singular diffusion problems, Ann. of Math. (2), 54 (1951), pp. 173–182.

- [12] S. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Review of Financial Studies, 6 (1993), pp. 327–343.

- [13] M. Keller-Ressel, Affine Processes - Theory and Applications in Mathematical Finance., PhD thesis, Vienna University of Technology, 2009.

- [14] , Simple examples of pure jump strict local martingales. preprint, 2014.

- [15] M. Keller-Ressel and E. Mayerhofer, Exponential moments of affine processes, to appear in Annals of Applied Probability, (2014).

- [16] M. Keller-Ressel, E. Mayerhofer, and A. G. Smirnov, On convexity of solutions of ordinary differential equations, Journal of Mathematical Analysis and Applications, 368 (2010), pp. 247–253.

- [17] M. Keller-Ressel, W. Schachermayer, and J. Teichmann, Regularity of affine processes on general state spaces, Electron. J. Probab, 18 (2013), pp. 1–17.

- [18] E. Mayerhofer, J. Muhle-Karbe, and A. G. Smirnov, A characterization of the martingale property of exponentially affine processes, Stochastic Processes and their Applications, 121 (2011), pp. 568–582.

- [19] K.-I. Sato, Lévy Processes and Infinitely Divisible Distributions, Cambridge University Press, 1999.