\nameAditya Gopalan1\emailaditya@ece.iisc.ernet.in

\nameOdalric-Ambrym Maillard2\emailodalricambrym.maillard@inria.fr

\nameMohammadi Zaki1\emailzaki@ece.iisc.ernet.in

\addr Electrical Communication Engineering,

Indian Institute of Science,

Bangalore 560012, India

\addr Inria Saclay – Île de France

Laboratoire de Recherche en Informatique

660 Claude Shannon

91190 Gif-sur-Yvette, France

Abstract

We study the task of maximizing rewards from recommending

items (actions) to users sequentially interacting with a recommender

system. Users are modeled as latent mixtures of many

representative user classes, where each class specifies a mean

reward profile across actions. Both the user features (mixture

distribution over classes) and the item features (mean reward vector per

class) are unknown a priori. The user identity is the only contextual information available to the learner while interacting. This induces a low-rank structure on the matrix of

expected rewards from recommending item to user .

The problem reduces to the well-known linear bandit when either

user- or item-side features are perfectly known. In the setting

where each user, with its stochastically sampled taste profile,

interacts only for a small number of sessions, we develop a bandit algorithm for the two-sided uncertainty. It combines the

Robust Tensor Power Method of

Anandkumar et al. (2014b) with the OFUL linear bandit algorithm of

Abbasi-Yadkori et al. (2011). We provide the first rigorous regret

analysis of this combination, showing that its regret

after user interactions is , with

the number of users. An ingredient towards this result

is a novel robustness property of OFUL, of independent interest.

Recommender systems aim to provide targeted, personalized content

recommendations to users by learning their responses over time. The

underlying goal is to be able to predict which items a user might

prefer based on preferences expressed by other related users and

items, also known as the principle of collaborative filtering.

A popular approach to model preferences expressed by users in

recommender systems is via probabilistic mixture models or latent

class models (Hofmann and Puzicha, 1999; Kleinberg and Sandler, 2004). In

such a mixture model, we have a set of items (content) that can be

recommended to users (consumers). Whenever item is recommended

to user , the system gains an expected reward of . The key

structural assumption that captures the relationship between users’

preferences is that there exists a set of latent set of representative user types or typical taste profiles. Formally, each

taste profile is a unique vector

of the expected rewards

that every item elicits under the taste profile. Each user is

assumed to sample one of the typical profiles randomly using an

individual probability distribution

; its reward distribution

across the items subsequently becomes that induced by the assumed

profile.

Our focus is to address the sequential optimization of net reward

gained by the recommender, without any prior knowledge of either

the latent user classes or users’ mixture distributions. Assuming

that users arrive to the system repeatedly following an unknown

stochastic process and re-sample their profiles over time, according

to their respective unknown mixtures across latent classes, we

seek online learning strategies that can achieve low regret

relative to the best single item that can be recommended to each

user. Note that this is qualitatively different than the task of

estimating latent classes or user mixtures in a batch fashion,

well-studied by now (Sutskever et al., 2009; Anandkumar et al., 2014a, b); the task of

simultaneously optimizing net utility in a bandit fashion in complex

expression models like these has received little or no analytical

treatment. Our work takes a step towards filling this void.

An especially challenging aspect of online learning in recommender

systems is the relatively meager number of available interactions with

a same user, which is offset to an extent by the assumption that users

can only have a limited number of taste profiles (classes). Indeed, if

one can identify the class to which a certain user belongs and

aggregate information from all other users in that class, then one can

recommend to the user the best item for the class. In practice,

classes are latent and not necessarily known in advance, and several

works

(Gentile et al., 2014; Lazaric et al., 2013; Maillard and Mannor, 2014)

study the restricted situation when each user always belongs to one

specific class (i.e., when all mixture distributions have

support size ). We go two steps further, since in many situations

(a) users cannot be assumed to belong to one class only, such as when

a user account is shared by several individuals (e.g. a smart-TV), and

(b) the duration of a user-session, that is the number of consecutive

recommendations to the same individual connected to a user-account,

cannot assumed to be long111It is also unlikely to be very

short, say, less than 3..

The key challenges that this work addresses are (1) the lack of

knowledge of “features” on both the user-side and item-side in

a linear bandit problem (in this case, both the user mixture weights

and the item class reward profiles) and (2) provable regret

minimization with very few i.e. interactions with every user

having a specific taste profile, as opposed to a large number of

interactions such as in transfer learning

(Lazaric et al., 2013).

Contributions and overview of results. We consider a setting

when users are assumed to come from arbitrary mixtures across classes

(they are not assumed to fall perfectly in one class as was the

assumption in works by

Gentile et al.(2014); Maillard and Mannor(2014)). We develop a novel

bandit algorithm (Algorithm 3) that

combines (a) the Optimization in the Face of Uncertainty Linear

bandit OFUL algorithm (Abbasi-Yadkori et al., 2011) for bandits

with known action features, and (b) a variant of the Robust Tensor

Power (RTP) algorithm (Anandkumar et al., 2014b) that uses only bandit

(partial) estimates of latent user classes with observations coming

from a mixture model. More specifically, we introduce a subroutine

(Algorithm 1) that makes use of the RTP method

to extract item-side attributes () and, contributing to its

theoretical analysis, show a recovery property

(Theorem 1). Note that the RTP method ideally

requires (unbiased) estimates of the nd and rd order moments of

actions’ rewards, but with bandit information the learner can access

only partial reward information, i.e., a single reward sample from an

action. To overcome this, we devise an importance sampling scheme

across successive time instants to build the nd and rd order

moment tensor estimates that RTP uses. For the task of issuing

recommendations, we develop an algorithm

(section 4), essentially based on OFUL,

instantiated per user, using for each the estimated latent

class vectors (obtained via the RTP subroutine) as arm

features, and uncertain parameter vector to be learned .

We carry out a rigorous analysis of the algorithm and show that it

achieves regret in rounds of

interaction (Theorem 4), provided each arriving user

interacts with the system for rounds with the same

profile. In comparison, the regret of the strategy that completely

disregards the latent mixture structure of rewards and employs a

standard bandit strategy (e.g. UCB (Auer et al., 2002)) per

user, scales as after

rounds222Roughly, each UCB

per-user plays from a pool of actions for about rounds,

thus suffering regret . , which is considerably

suboptimal in the practical case with a very large number of items but

very few representative user classes (). It is also worth

noting that the regret bound we achieve, order-wise, is what would

result from applying the OFUL or any optimal linear bandit algorithm

assuming a priori knowledge of all latent user classes

, that is . In this

sense, our result shows that one can simultaneously estimate

features on both sides of a bilinear reward model and achieve regret

performance equivalent to that of a one-sided linear model, which

is the first result of its kind to the best of our

knowledge333An earlier result of Djolonga et al. (2013)

gets regret while moreover assuming a perfect control

of the sampling process (we can’t assume this due to the user

arrivals).. Our results are presented for finite time horizons with

explicit details of the constants arising from the error analysis of

RTP, which at this point are large but possibly improvable.

En route to deriving the regret for our algorithm, we also make

a novel contribution that advances the theoretical understanding of

OFUL, and which is of independent interest. We show that in the

standard linear bandit setting, where the expected reward of an arm

linearly depends on features, OFUL yields (sub-linear)

regret even when it makes

decisions based on perturbed or inexact feature vectors

(Theorem 3), where quantifies the

distortion. This property holds whenever the perturbation error is

small enough, and we explicitly give both (a) a sufficient condition

on the size of the perturbation in terms of the set of actual

features, and (b) a bound on the (multiplicative) distortion

in the regret due to the perturbation (note that in the

ideal linear case).

2 Setup and notation

For any positive integer , denotes the set

.

At each , nature selects a user according to the

probability distribution over , independent of the past,

and is revealed to the learner. A user class is

subsequently sampled from the probability distribution

over , and (the assumed class of user ) interacts with

the learner for the next consecutive steps. Such an

interaction will often be termed a mini-session.

In each step of a mini-session, the learner plays an

action (issues a recommendation) and subsequently

receives reward , where

is a (centered) -sub-Gaussian i.i.d. random variable

independent from , representing the noise in the reward. We

let represent the vector

of the mean rewards from action in each

class. Note that

.

For convenience, we use the index notation and

introduce , where is the total number of mini-sessions,

and the total number of interactions of the learner with the

system. We denote likewise for ,

, , , and let

.

We are interested in designing an online recommendation strategy,

i.e., one that plays actions depending on past observations, achieving

low (cumulative) regret after mini-sessions,

defined as ,

where

.

In other words, we wish to compete against a strategy that plays for

every user an action yielding the highest reward in expectation under

its mixture distribution over user classes.

3 Recovering latent user classes: The

EstimateFeatures subroutine

In this section, we provide an estimation algorithm for the matrix , using the RTP method.444We consider

to describe the algorithm; is easily handled by

repeating the 3-wise sampling for

times and discarding the remaining ()

steps in the mini-session during exploration (leading to a

negligible regret overhead).

Estimation of tensors. We assume that in mini-session , when

interacting with user , the triplet is

chosen from a distribution . Letting

to

explicitly indicate the active user and action chosen at , we

form the importance-weighted estimates

for the second and third-order tensors555An alternative is the

implicit exploration method due to

Kocák et al. (2014)..

We introduce the matrices

and

with

, and the tensors

and

with

. The following

result decomposes the matrix and

tensor as weighted sums of outer products.

Lemma 1

When the user arrivals are i.i.d. according to the law ,

i.e., , it holds

that

Having shown the unbiasedness of the empirical nd and rd moment

tensors and , we next turn to showing

concentration to their respective means.

Lemma 2

Assuming that and for deterministic , for all , then

for all , with probability higher than , it holds simultaneously for all that

An immediate corollary is the following one:

Corollary 1

Provided that and for some , then on an event of probability higher than , the following hold simultaneously:

3: Compute a whitening matrix of {Take where is the diagonal matrix with the top eigenvalues of , and the matrix of corresponding eigenvectors.}

4: Form the tensor .

5: Apply the RTP algorithm (Anandkumar et al., 2014b) to , and compute its robust eigenvalues with eigenvectors . {The paper of Anandkumar et al.(2014b, Sec. 4) defines eigenvalues/eigenvectors of tensors.}

6: Compute for each , and .

7:Output: Estimate of latent classes : The matrix obtained by stacking the vectors side by side.

Reconstruction algorithm. The EstimateFeatures algorithm

(Algorithm 1) employs a whitening matrix

, of the empirical estimate of the matrix , to build

the empirical tensor . This tensor is then used to recover

the columns of the matrix via the RTP algorithm. For the sake of

completeness, we also introduce , a whitening matrix of

(i.e., ), the corresponding tensor ,

and finally the estimation error .

Reconstruction guarantee. Our next result makes use of the following proposition from

Anandkumar et al.(2014b, Theorem 5.1), restated here for completeness.

Proposition 1 (Theorem 5.1 of Anandkumar et al. (2014b))

Let , where is a

symmetric tensor with orthogonal decomposition

, where each

, is an orthonormal basis, and

is a symmetric tensor with operator norm .

Let ,

. Run the RTP algorithm

with input for iterations. Let

be the corresponding

sequence of estimated eigenvalue/eigenvector pairs returned. Then,

there exist universal constants for which the following

is true. Fix and run RTP with parameters (i.e.,

number of iterations) with , and

.

If , then with

probability at least , there exists a permutation

such that

Lemma 1 gives a decomposition of the (symmetric)

tensor , but it may be not orthogonal; standard

transformation (Anandkumar et al., 2014b, Sec. 4.3) gives an orthogonal

decomposition for the tensor666For a 3rd order tensor

and 2nd order tensor or

matrix ,

is the 3rd order

tensor defined by

.

See Anandkumar et al. (2014b) for more details on

notation and results., with a

matrix that whitens . We can thus use Proposition 1

with , , and

in order to prove the following guarantee (Theorem 1) on the

recovery error between columns of and their estimate.

We now introduce mild separability conditions on the mixture

weights and the spectrum of the 2nd moment matrix

needed for the reconstruction guarantee to hold, similar to

those assumed for Lazaric et al.(2013, Theorem 2).

Assumption 1

There exist positive constants

, , and

such that

where denotes the top eigenvalue of .

Theorem 1 (Recovery guarantee for online estimation of user classes )

Let Assumption 1 hold, and let . If the

number of mini-session satisfies

then with probability at least , there exists some

permutation such that for all , the

output of the EstimateFeatures algorithm satisfies

(1)

where .

Here, the constant (we use the ”diamond” symbol to denote it) is

with the notation .

The proof strategy follows that of Lazaric et al.(2013, Theorem

2) and is detailed in the appendix for clarity. It consists in relating, on the one hand, the

estimation errors of and of from

Corollary 1 to the condition

, and, on the other hand,

relating the reconstruction error on the columns of to the control

on the terms and

coming from

Proposition 1. We note that the bound appearing in the

condition on the number of mini-sessions is potentially large (due to

the terms , etc.). This is due to the combination of the RTP

method with the importance sampling scheme, and it remains unclear if

the bound can be significantly improved within this framework.

4 Recovering latent mixture distributions ():

robustness of the OFUL algorithm

In order to recover the weights vectors and

thus the matrix , it would be tempting to use again an instance of

the RTP method but this time to aggregate across actions, i.e., by

forming a and tensor. Unfortunately,

aggregation of elements of fails for two reasons: First, we do not

have different views across users , contrary to what we have for

actions . It is thus hopeless to be able to form an estimate of the

2nd and 3rd moment tensors as before. Second, and rather technically,

convex combinations of the need not be

positive. This prevents the application of the RTP method which

requires positive weights to work.

We thus consider a different strategy that uses an algorithm designed

for linear bandits. However since the feature matrix is unknown a

priori and can only be estimated, we need to work with perturbed

features. A first solution is to propagate the additional error

resulting from the error on the features in the standard proof of

OFUL. However, this leads to a sub-optimal regret that is no longer

scaling as with the time horizon. We overcome

this hurdle by showing in Theorem 3 a robustness

property of OFUL of independent interest, which aids us in

controlling the regret of the overall latent class algorithm

(Algorithm 3).

Consider OFUL run with perturbed (not necessarily linearly

realizable) rewards. Formally, consider a finite action set

and distinct feature vectors

.

Let

.

The expected reward when playing action at time is

denoted by , with

. Let us assume

that there exists a unique optimal action for the expected rewards

, i.e., ,

with the regret at time being

. The

key point here is that need not be linearly realizable

w.r.t. the actions’ features – we will not require that

be

.

Algorithm 2OFUL (Optimism in Face of Uncertainty for Linear

bandits) (Abbasi-Yadkori et al., 2011)

0: Arms’ features , regularization parameter , norm parameter

for all times do

1. Form the matrix

consisting of all arm features played up to time , and

. Set

.

2. Choose the action

endfor

OFUL Regret with linearly realizable rewards. The OFUL algorithm is stated for the sake of clarity as Algorithm

2. Before studying the linearly non-realizable case, we

record the well-known regret bound for it in the unperturbed

case, that is when

for some

unknown .

Theorem 2 (OFUL regret (Abbasi-Yadkori et al., 2011))

Assume that , and that for all

, ,

.

Then

with probability at least , the regret of

OFUL satisfies: ,

provided that the regularization parameter is chosen such

that .

Regret of OFUL with Perturbed Features.

We make a structural definition to present the result. Let

, where

,

is the submatrix of formed

by picking rows , and ranges over all size- subsets of

full-rank rows of . We will require for our purposes

that is not too large. For intuition

regarding , we refer to Forsgren(1996) (the

final 3 paragraphs of p. 770, Corollary 5.4 and section 7). We

remark that the condition that be small

is analogous to a -incoherence type property commonly used

in prior work (Bresler et al., 2014, Assumption A2), stating

that two distinct feature vectors and ,

, must have a minimum angle separation.

Let be arbitrary with norm

at most (it helps to think of as

an approximation of ),

,

.

We now state a robustness result for OFUL potentially of

independent interest.

Theorem 3 (OFUL robustness property)

Suppose , , ,

and .

If the deviation from linearity satisfies

(2)

then, with probability at

least for all ,

where

.

Theorem 3 essentially states that when the deviation of

the actual mean reward vector from the subspace spanned by the feature

vectors is small, the OFUL algorithm continues to enjoy a favorable

regret up to a factor . The quantity

in the result is a geometric measure of the distortion in the

arms’ actual rewards with respect to the (linear)

approximation . We control this quantity in the

next paragraph. (Note that in the perfectly linearly

realizable case , and this gives back the standard

OFUL regret up to a universal multiplicative constant.)

Applying the Robust analysis of OFUL to the Low-rank Bandit setup.

In this paragraph, we translate Theorem 3 to our Low Rank

Bandit (LRB) setting in which OFUL uses feature vectors with noisy

perturbations (estimated by, say, a Robust Tensor Power (RTP)

algorithm). Throughout this section, we fix a user

.

OFUL

LRB

Table 1: Correspondences between OFUL and Low Rank Bandit (LRB) quantities at time and for user

We can now translate Theorem 3 thanks to the correspondence with the perturbed OFUL setting: In our low-rank bandit setting, the matrix depends on the reconstruction algorithm

at mini-session . Moreover, the optimal action now depends on the user . We denote for a user the minimum gap across suboptimal actions to be .

Likewise, the error vector depends on .

Its norm appears in the condition (2)

and the definition of , and is controlled by the reconstruction error of Theorem 1. It decays with the number of mini-sessions .

We define ,

and use for ,

Using these notations, and adapting the proof of Theorem 3 to handle a variable , we can now translate

the result of the perturbed OFUL to our LRB setting:

Lemma 3

Let and . Provided that the number

of mini-sessions satisfies

, where we introduced the notation

then with probability at least ,

is small enough that for any ,

condition (2) is satisfied.

Consequently, Theorem 3 applies with

Thus, provided that the total number of mini-sessions of interaction (not necessarily corresponding to interactions with user ) is large enough,

then the OFUL algorithm run during interactions with user will achieve a controlled regret. However, we want to warn that the resulting from the RTP method, especially the second term of the max,

may be potentially large, although being a constant.

5 Putting it together: Online Recommendation

algorithm

This section details our main contributions for recommendations in the

context of mini-sessions of interactions with unknown mixtures of

latent profiles: first Algorithm 3 that

combines RTP with OFUL, and then a regret analysis in

Theorem 4.

The recommendation algorithm we propose

(Algorithm 3) uses the RTP method to

estimate the matrix and then applies OFUL to determine an

optimistic action. Importantly, it finally outputs a distribution

that mixes the optimistic action with a uniform exploration. The

mixture coefficient goes to with the number of rounds, thus

converging to playing OFUL only. It ensures that the importance

sampling weights are bounded away from in the beginning.

With Assumption 1 holding, let ,

(from

Lemma 3), and let be the first mini-session

at which

.

The regret of Algorithm 3 at time

(acting for mini-sessions of length ) using

internal instances of OFUL parameterized by

satisfies

provided that , with

,

.

Consequently, choosing and

, , say, yields the order

Discussion. (1) The regret of

Algorithm 3 scales with similar to

that of an OFUL algorithm run with perfect knowledge of the feature

matrix : . This is a non-trivial result as

is not assumed to be known a priori and is estimated by

Algorithm 3 using tensor methods.

Algorithm 3 Per-user OFUL with exploration

0: Parameters , for OFUL,

exploration rate parameters , .

1:for mini-session do

2: Get user .

3: Let

4:ifthen

5: {Carry out an ESTIMATE mini-session}

6:for step do

7: Output .

8:endfor

9: Let

(Algorithm 1) with input

{Update feature estimates using samples from

previous ESTIMATE mini-sessions}

10:else

11: {Carry out an OFUL mini-session}

12:for step do

13: Run one iteration of OFUL (Algorithm

2) with features , parameters

and , and past actions and rewards

,

, for which

and

{An instance of OFUL for each user using

current feature estimates, and observed actions and

rewards from previous OFUL mini-sessions}

14: Output action returned by OFUL

15:endfor

16:endif

17:endfor

(2)

One can also compare the result with the regret of ignoring the

mixture (low-rank) structure and simply running an instance of UCB per

user, which would scale as . This becomes highly

suboptimal when the number of actions/items is much larger than

the number of user types , demonstrating the gain from leveraging

the mixed linear structure of the problem. Note also that we do not

need a specific user to interact for a long time but for as few as

consecutive steps, contrary for instance to the transfer

method (Lazaric et al., 2013), where a large number of

consecutive interaction steps with the same user is required.

(3) It

is worthwhile to contrast the result and approach with that in

Djolonga et al.(2013) – the authors there incur

an additional regret term due to the error in approximately estimating

the low-rank matrix, which requires additional tuning ending up with a

regret of . On the other hand, we avoid this

approximation error by showing and exploiting the robustness property

of OFUL, which guarantees regret as soon as the estimated

features are within a small radius of the actual ones.

The result (and analysis) does come with a caveat that the

model-dependent term , although being independent on

the time horizon , is potentially large. With set as

in Theorem 4, it appears as an additive exponential constant term in

the regret777With additional prior knowledge of , the

dependence of the additive term can be made polynomial in

: choosing

, it holds that

.

This arises

from the RTP method, and it is currently

unclear if this term can be significantly reduced with the current

line of analysis.

Numerical evidence, however, indicates that no such large additive

constant enters into the regret (Section 5). Also,

on the bright side, note that does not need to be

known by the algorithm.

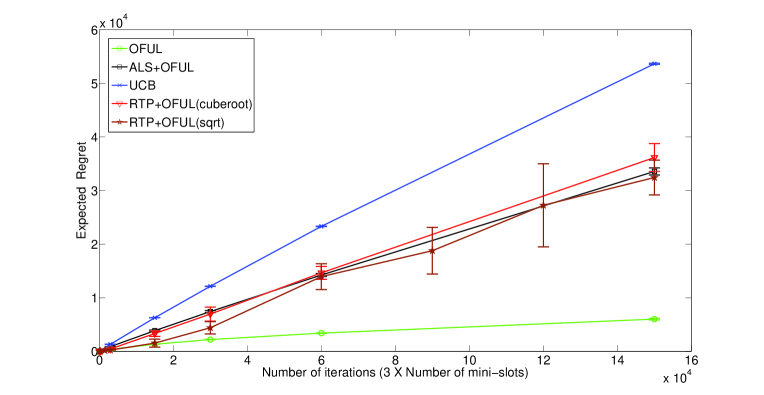

Numerical Results. The performance of the low-rank bandit

strategy (Algorithm 3) is shown in

Figure 1, simulated for users arriving uniformly at

random, user classes and actions. Both the latent class

matrix the mixture matrix are

random one-shot instantiations. The proposed algorithm (Algorithm 3), with two different

exploration rate schedules and

(’RTP+OFUL(sqrt)’ and ’RTP+OFUL(cuberoot)’ in the figure), is compared with (a) basic UCB (’UCB’ in the figure) ignoring the

linear structure of the problem (i.e., UCB per-user with

actions), (b) OFUL per-user with complete knowledge of the user

classes and always, i.e., no exploration mini-sessions, and (c) An implementation of the Alternating Least Squares estimator (Takács and Tikk, 2012; Mary et al., 2014) for the matrix along with OFUL per-user. The

proposed algorithm, with the theoretically suggested exploration

, is observed to exploit the latent structure

considerably better than simple UCB, and is not too far from the

unrealistic OFUL strategy which enjoys the luxury of latent class

information. It is also competitive with performing Alternating Least Squares, which does not come with analytically sound performance guarantees in the bandit learning setting. Also, the large additive constants in the theoretical

bounds for Algorithm 3 do not manifest here.

Figure 1: Regret of the proposed algorithm (‘RTP+OFUL’ or Algorithm

3) for two different exploration rate

schedules, compared with (a) independent UCB per-user, (b)

OFUL per-user with perfect knowledge of latent classes , and (c) Alternating Least Squares estimation for the matrix , along with OFUL per-user. Here,

users, classes, and , with

randomly generated and . Plots show the sample mean

of cumulative regret with time, with standard deviation-error

bars over sample experiments.

Related work.

The popular low-rank matrix completion problem studies the recovery

and given a small number of entries sampled at random from

with both and being tall matrices, see for instance

Jain et al.(2013) and citations therein. However, its setting is

different than ours for several reasons. It typically deals with batch

data arising from a sampling process that is not active but uniform

across entries of . Further, it requires sensing operators

having strong properties (such as the RIP property), and most

importantly, the performance metric is not regret but reconstruction

error (Frobenius or -norm).

In the linear bandit literature

(Abbasi-Yadkori et al., 2011; Rusmevichientong and Tsitsiklis, 2010; Dani et al., 2008), the key

constraining assumption is that either user side () or item side

() features are precisely and completely known a priori. In

contrast, the problem of low regret recommendation across users with

latent mixtures does not afford us the luxury of knowing either or

, and so they must be learnt “on the fly”. Another related work

in the context of bandit type schemes for latent mixture model

recommender systems is that of Bresler et al.(2014), in which,

under the very specific uniform mixture model for all users, they

exhibit strategies with good regret.

Nguyen et al.(2014) consider an alternating

minimization type scheme in linear bandit models with two-sided

uncertainty (an alternative model involving latent

“factors”). However no rigorous guarantees are given for the bandit

schemes they present; moreover, it is not known if alternating

minimization finds global minima in general. Another related work is

in the transfer learning setting from Lazaric et al.(2013):

The method combines the RTP method

(Anandkumar et al., 2014b, 2012) essentially with a

standard UCB (Auer et al., 2002), but however works in the

setting of a large number interactions with a same user, without

assuming access to “user ids”. As a result, the regret bound in

this setting scales linearly with the number of rounds. Our result in

this paper shows that with additional access to just user identifiers,

we can reduce the regret rate to be sublinear in time.

The RTP method has been used as a processing step to the EM algorithm

in crowdsourcing (Zhang et al., 2014), but only convergence

properties are considered, which is not enough to provide regret guarantees.

On the theoretical side, our contribution generalizes the setting of

clustered bandits(Maillard and Mannor, 2014; Gentile et al., 2014)

in which a hard clustering model is assumed (one user is assigned to

one class, or equivalently mixture distributions can only have support

size ). In particular, Maillard and Mannor(2014) specifically

highlight the benefit of a collaborative gain across users against

using a vanilla UCB for each user. However their setting is less

general than assuming a soft clustering of users (one user corresponds

to a mixture of classes) across various “representative” taste

profiles as we study here.

The Alternating Least-Squares (ALS) method

(Takács and Tikk, 2012; Mary et al., 2014) has been shown to yield

promising experimental results in similar settings where both and

are unknown. However, no theoretical guarantees are known for this

algorithm that may converge to a local optimum in general.

The work of Valko et al.(2014) studies

stochastic bandits with a linear model over a low-rank (graph

Laplacian) structure. However, they assume complete knowledge of the

graph and hence knowledge of the eigenvectors of the Laplacian,

converting it into a bilinear problem with only one-sided

uncertainty. This is in contrast to our setup where both,

are completely uncertain.

Perhaps the closest work to ours is that of

Djolonga et al.(2013) where the authors develop a flexible

approach for bandit problems in high dimension but with

low-dimensional reward dependence. They use a two-phase algorithm:

First a low-rank matrix completion technique (the Dantzig selector)

estimates the feature-reward map, then a Gaussian Process-UCB (GP-UCB)

bandit algorithm controls the regret, and show that if after iterations

the approximation error between the feature matrix and its estimate is

less then , the final regret is given by the sum of the regret

of GP-UCB when given perfect knowledge of the features and of

(due to the learning phase and approximation

error). This results in an overall regret scaling with .

We depart from their results in two fundamental ways: Firstly, they

have the possibility of uniformly sampling the entries (a common

assumption in low-rank matrix completion techniques). We do not have

this luxury in our setting as we do not control the process of user

arrivals, that is not constrained to be uniform. Secondly, we prove

and exploit a novel robustness property (see

Theorem 8) of the bandit subroutine we use (OFUL in

our case instead of GP-UCB), which allows us to effectively eliminate

the approximation error in their work and obtain a

regret bound (see Theorem 4).

6 Conclusion & Directions

We consider a full-blown latent class mixture model in

which users are described by unknown mixtures across unknown user

classes, more general and challenging than when

users are assumed to fall perfectly in one class

(Gentile et al., 2014; Maillard and Mannor, 2014).

We provide the first provable sublinear regret

guarantees in this setting, when both the canonical classes and user

mixture weights are completely unknown, which we believe is striking

when compared to existing work in the setting, e.g.,

alternate minimization typically gets stuck in local minima. We

currently use a combination of noisy tensor factorization and linear

bandit techniques, and control the uncertainty in the estimates

resulting from each one of these techniques. This enables us to

effectively recover the latent class

structure.

Future directions include reducing the numerical constant (e.g. using

an alternative to RTP), and studying how to combine our work with the

aggregation of user parameters suggested in

Maillard and Mannor(2014).

References

Abbasi-Yadkori et al. (2011)

Yasin Abbasi-Yadkori, David Pal, and Csaba Szepesvari.

Improved Algorithms for Linear Stochastic Bandits.

In Proc. NIPS, pages 2312–2320, 2011.

Anandkumar et al. (2012)

Animashree Anandkumar, Daniel Hsu, and Sham M Kakade.

A method of moments for mixture models and hidden markov models.

arXiv preprint arXiv:1203.0683, 2012.

Anandkumar et al. (2014a)

Animashree Anandkumar, Rong Ge, Daniel Hsu, and Sham M Kakade.

A tensor approach to learning mixed membership community models.

Journal of Machine Learning Research, 15(1):2239–2312, 2014a.

Anandkumar et al. (2014b)

Animashree Anandkumar, Rong Ge, Daniel Hsu, Sham M. Kakade, and Matus

Telgarsky.

Tensor decompositions for learning latent variable models.

J. Mach. Learn. Res., 15(1):2773–2832,

January 2014b.

Auer et al. (2002)

P. Auer, N. Cesa-Bianchi, and P. Fischer.

Finite-time analysis of the multiarmed bandit problem.

Machine Learning, 47(2):235–256, 2002.

Bresler et al. (2014)

Guy Bresler, George H Chen, and Devavrat Shah.

A latent source model for online collaborative filtering.

In Proc. NIPS 27, pages 3347–3355. Curran Associates, Inc.,

2014.

Dani et al. (2008)

Varsha Dani, Thomas P. Hayes, and Sham M. Kakade.

Stochastic Linear Optimization under Bandit Feedback.

In Proc. COLT, 2008.

Djolonga et al. (2013)

Josip Djolonga, Andreas Krause, and Volkan Cevher.

High-dimensional Gaussian process bandits.

In Proc. NIPS, pages 1025–1033, 2013.

Forsgren (1996)

Anders Forsgren.

On linear least-squares problems with diagonally dominant weight

matrices.

SIAM Journal on Matrix Analysis and Applications, 17(4):763–788, 1996.

Gentile et al. (2014)

Claudio Gentile, Shuai Li, and Giovanni Zappella.

Online clustering of bandits.

In Proc. ICML, pages 757–765, 2014.

Gheshlaghi Azar et al. (2013)

Mohammad Gheshlaghi Azar, Alessandro Lazaric, and Emma Brunskill.

Sequential transfer in multi-armed bandit with finite set of models.

In Proc. NIPS, pages 2220–2228. Curran Associates, Inc.,

2013.

Hofmann and Puzicha (1999)

Thomas Hofmann and Jan Puzicha.

Latent class models for collaborative filtering.

In IJCAI, volume 99, pages 688–693, 1999.

Jain et al. (2013)

Prateek Jain, Praneeth Netrapalli, and Sujay Sanghavi.

Low-rank matrix completion using alternating minimization.

In Proc. ACM Symposium on Theory Of computing (STOC), pages

665–674. ACM, 2013.

Kleinberg and Sandler (2004)

Jon Kleinberg and Mark Sandler.

Using mixture models for collaborative filtering.

In Proc. ACM Symposium on Theory Of Computing (STOC), pages

569–578. ACM, 2004.

Kocák et al. (2014)

Tomáš Kocák, Gergely Neu, Michal Valko, and Rémi Munos.

Efficient learning by implicit exploration in bandit problems with

side observations.

In Proc. NIPS, pages 613–621, 2014.

Lazaric et al. (2013)

Alessandro Lazaric, Emma Brunskill, et al.

Sequential transfer in multi-armed bandit with finite set of models.

In Proc. NIPS, pages 2220–2228, 2013.

Maillard and Mannor (2014)

Odalric-Ambrym Maillard and Shie Mannor.

Latent bandits.

In Proc. ICML, pages 136–144, 2014.

Mary et al. (2014)

Jérémie Mary, Romaric Gaudel, and Preux Philippe.

Bandits warm-up cold recommender systems.

arXiv preprint arXiv:1407.2806, 2014.

Nguyen et al. (2014)

Hai Thanh Nguyen, Jérémie Mary, and Philippe Preux.

Cold-start problems in recommendation systems via contextual-bandit

algorithms.

arXiv preprint, arXiv:1405.7544, 2014.

Rusmevichientong and Tsitsiklis (2010)

Paat Rusmevichientong and John N Tsitsiklis.

Linearly parameterized bandits.

Mathematics of Operations Research, 35(2):395–411, 2010.

Stewart et al. (1990)

Gilbert W Stewart, Ji-guang Sun, and Harcourt Brace Jovanovich.

Matrix perturbation theory, volume 175.

Academic press New York, 1990.

Sutskever et al. (2009)

Ilya Sutskever, Joshua B. Tenenbaum, and Ruslan R Salakhutdinov.

Modelling relational data using Bayesian clustered tensor

factorization.

In Proc. NIPS, pages 1821–1828. Curran Associates, Inc.,

2009.

Takács and Tikk (2012)

Gábor Takács and Domonkos Tikk.

Alternating least squares for personalized ranking.

In ACM Conference on Recommender systems, 2012.

Valko et al. (2014)

Michal Valko, Rémi Munos, Branislav Kveton, and Tomáš Kocák.

Spectral Bandits for Smooth Graph Functions.

In Proc. ICML, 2014.

Zhang et al. (2014)

Yuchen Zhang, Xi Chen, Dengyong Zhou, and Michael I Jordan.

Spectral methods meet EM: A provably optimal algorithm for

crowdsourcing.

In Proc. NIPS, pages 1260–1268, 2014.

Proof of Lemma 1

This result holds by construction of the estimates

and .

Note that

where holds by independence of the sample generated

by user when in the same class . Note that is the same for all interaction steps, that is , where is the class corresponding to sample .

This is the reason why we get

and not a product for instance.

Proof of Lemma 2

Since the rewards generated by each source are i.i.d., the estimate is a sum of i.i.d. random variables bounded in , re-weighted by the probability weights , which are measurable functions of the past. Assuming that there exists some

deterministic such that

, we can thus apply a version of

Azuma-Hoeffding inequality for bounded martingale difference sequence.

Let us recall that by this inequality, for a deterministic time , and being a bounded martingale difference sequence, then for all it holds

In our case, , and we deduce that

Likewise, we get that

Taking a union bound over the actions in each case, and then over the two events concludes the proof.

Proof of Corollary 1

From Lemma 2, we deduce that on an event of probability higher than , it holds simultaneously that

This indeed holds by relating the norm of the matrix (tensor) with each of the elements.

We conclude by replacing the values of and .

We prove in this section a slightly more detailed result, namely, the following:

Theorem 1.

Assume that are chosen such that .

Let

be the minimum robust eigenvalue of the tensor .

Let . Provided that

with probability higher than ,

there exists some permutation such that for all ,

where we introduced the problem-dependent constant

For general (not necessarily such that ), it holds with same probability that

where, using the notation , we have introduced the constant

Proof

The proof closely follows that of Gheshlaghi Azar et al.(2013).

First, note that by property of the rank decomposition ((Anandkumar et al., 2014b, Theorem 4.3)), it holds that

and thus .

We first decompose the following term to make appear

the terms from Proposition 1:

Note that , and are both normalized vectors.

Thus, is bounded as .

It holds for

that , and for , on the event from Corollary 1, that

(4)

The term requires a little more work. It holds that

We use the result of Lemma 5 from Gheshlaghi Azar et al.(2013) to control and .

If , then it holds

from which we deduce that

(5)

At this point, and are controlled by the perturbation method from Anandkumar et al.(2014b),

under the condition that (where is a universal constant). In this case, with probability , the RTP algorithm with well-chosen parameters achieves

In order to make the condition explicit in our setting, we use the fact that by Lemma 6 from Gheshlaghi Azar et al.(2013), if then

(6)

The condition

holds if the number of sessions is sufficiently large:

Indeed on an event of probability higher than , then

it is enough that

that is, reordering the terms, that

(7)

Now, in order to satisfy the condition , it is enough that

Let us decompose the left-hand-side term: After some simplifications using and , the previous inequality happens when

where .

Using the definition of and

then we deduce that it is enough that

that is, reordering the terms that

(8)

Combining the decomposition (B) with

(4),(5),

and using the fact that , we obtain

Now, using (6) and unfolding the last inequality, it holds with probability higher than that

which, after some cosmetic simplifications, concludes the first part of the proof of Theorem 1.

Alternatively, when

, we can always resort to the condition that in order to simplify the previous derivation. We deduce, similarly, that

where, in order to control the last term , we used the property that

Proof

Let . The

argument used to prove Theorem 2 in Yadkori et al, 2011, can be used

to show that

where is the

observed noise sequence. Let . We then have

Thus, letting and using the

above with techniques from Yadkori et al together with

, we have that

with probability at least .

Now, let be an optimal action corresponding to the

approximate parameter , and define the instantaneous

regret at time with respect to the approximate parameter

as

We now bound this approximate regret using

arguments along the lines of Yadkori et al, 2011. Consider

(9)

Noting that , the regret can be

written as

In the derivation above,

•

Steps and hold because of the following. By Lemma

4 (to follow below),

.

Since is uniquely

by hypothesis, we have, thanks to Lemma

5 (to follow below), that

, establishing . This in turn shows that the

optimal action for is uniquely at all

times , i.e.,

, which is equality .

•

Inequality holds by (9) and

holds because by definition,

and by hypothesis,

implying that .

The argument from here can be continued in the same way as in

Abbasi-Yadkori et al.(2011) to yield

This proves the theorem.

Lemma 4 (Analysis of the time-varying parameter error

)

Let be the bias in

arm ’s reward due to model error, and let be the

dimensional vector of arm reward biases. Then,

where , is the

submatrix of formed by picking rows , and

ranges over all subsets of full-rank rows of .

where represents the empirical frequency with

which action has been played up to and including

time . This allows us to equivalently interpret as

the solution of a weighted-regularized least squares

regression problem with observations (instead of

the original interpretation with observations) as follows.

Let be the diagonal matrix with the

values on the diagonal (note:

). With this, we can express as

with being a diagonal &

positive semidefinite matrix,

positive definite, and having full column rank . A

result of Forsgren(1996, Corollary 2.3) can now be

applied to yield

where ranges over all subsets of full-rank rows of ,

and is the submatrix of

formed by picking rows . Thus, . This proves the lemma.

Lemma 5 (Critical radius)

Let

. Then, the following are equivalent:

(10)

and

(11)

Proof [Proof of Lemma 5]

Assuming (11), observe that when lies in

the interior of an -ball around

, we have, for any ,

which proves one direction of the lemma. For the other direction,

note that if

for some , then by setting

, we have both

Proof [Proof of Lemma 6]

The first step is to estimate the factor in the analysis of

Perturbed OFUL. Towards this, note that the quantity

in our setting becomes

where has rank , and ranges over all

combinations of its full-rank rows. For any such subset of

linearly independent rows , we have, after denoting , that

The final term above can be bounded using Anandkumar et al.(2012, Lemma

E.4) – a version of Theorem 2.5 in Stewart et al.(1990). Assuming is invertible, and

,

then is invertible, and a resulting bound on the

norm of its inverse lets us write

Writing ( and stand for “upper” and

“lower”) with representing the subset of rows taken from the

bottom rows of (i.e., ), we have

Thus, with denoting the Frobenius norm, and using the

dominance of the Frobenius norm over the matrix -norm, with

probability at least ,

as in the proof of Lemma 7. Also, by

(14), we have that with probability at least

,

Thus,

where is the minimum gap for user across suboptimal

actions.

Provided that (1), (12) and

(15) hold, we get that with probability at least

,

for each . Also, by the definition of , the

denominator is positive, i.e.,

. Hence,

completing the proof of the result.

Lemma 9 (Bounding )

If is large enough so that (1) and

(12) hold, then

with probability at least .

Proof [Proof of Lemma 9]

Conditions (1) and (12),

together with the estimate (20), imply that for

any action ,

with probability at least .

In order to conclude the proof of Lemma 3,

we gather the conditions from Lemma 6 and Lemma 7. After some simplifications,

both conditions are satisfied as soon as

where is the instantaneous regret

of Algorithm 3 at time when the current user is .

Using the notations of Algorithm 3,

it holds that

where is an action output by

an instance of OFUL for user .

Thus, we have

(21)

For each user , the expectation in the right-hand side

above corresponds to the cumulative regret of the OFUL strategy when

interacting with user in mini-sessions through , and when

given at each mini-session the set of perturbed feature vectors

. Let count the

total number of mini-sessions from in which user is present

(note that and

). Let us denote the term

in the above explicitly using

.

We can now use the OFUL robustness guarantee – a natural technical

extension888Although Theorem 3 holds only for a

fixed perturbation and feature set , it is

not hard to see that a modification of it, with time-varying

, and being the largest

over all times , yields the same conclusion (regret

bound). We provide this extension in Theorem 5 in

Appendix E below. of Theorem 3

along with Lemma 3 – to obtain that, for a given

user sequence , with probability at

least999Although the time horizons played by each OFUL instance

per user, , are technically random and unknown to the

instance at the start, conditioning on the sequence of users

arriving at each time instant lets us use the conclusion of

Lemma 3.,

This in turn implies that

The last term on the right-hand side in is due to the fact that

with probability at most , the per-user regret

can be as large

as (the total number of time slots for which user

interacts with the system). The corresponding term in is by

using . Further bounding using the

Cauchy-Schwarz inequality

gives

Expliciting and tuning

The next step is to control the term

.

To this end, we explicit and optimize .

We write in the sequel for convenience.

If , then

Thus, this is higher than if

, that is if

. Since , we immediately get

Thus, we obtain

Using the fact that , the bound simplifies to

If, on the other hand, a bound on is not readily available

beforehand, then choosing ,

, gives, via a crude bound,

The bound above is at least provided

. Thus, we finally get that, upon setting , the total

expected regret satisfies (as an order-wise function of )

E Extension of Theorem 3: Robustness of OFUL’s

regret with time-varying features

We now control the robust regret for user ,

when OFUL is run with evolving feature matrices

with decreasing feature error

, instead of a fixed

with fixed error .

We reindex the as

and prove the following result.

Theorem 5 (OFUL robustness result, extension of

Theorem 3 for time-varying features)

Assume ,

,

, ,

and , and that for all ,

(i.e., the linearly realizable approximation with respect to the

current features has as its unique optimal action). If

(22)

then with probability

at least , for all ,

where

.

Proof

Let . The

argument used to prove Theorem 2 in Yadkori et al, 2011, shows that

where is the

observed noise sequence, and where is

the matrix built from the time varying features at time and the

action sequence thus far. Let

. We then have

Thus, letting , and using the

above with techniques from Yadkori et al together with

, we have that

with probability at least .

Now, let be an optimal action corresponding to the

approximate parameter and approximate feature , and define the instantaneous

regret at time with respect to the approximate parameter

as

We now bound this approximate regret using arguments along the lines

of Yadkori et al, 2011 as follows. Write

(23)

Noting that , the regret can be

written as

In the derivation above,

•

Steps and hold because of the following. By Lemma

10 (to follow below),

.

Since

is uniquely by hypothesis, we have, thanks to Lemma

5, that

, establishing . This in turn shows

that the optimal action for is uniquely

at all times , i.e.,

, which is precisely equality .

•

Remark. In the above, Lemma 5 is written for

generic , , so in particular applies to

each time varying , . We

also used an extended version of Lemma 4 to

the case of varying , ,

which we state and prove below as Lemma

10.

•

Inequality holds by (23) and

holds because by definition,

and by hypothesis,

implying that .

The argument from here can be continued in the same way as in

Abbasi-Yadkori et al.(2011, proof of Theorem 3) to yield

This proves the theorem.

Lemma 10 (Extension of Lemma 4 to

time-varying feature sets)

Let

be the bias in arm ’s reward due to model error, with respect

to the features , and let

. Then, we have

where ,

is the submatrix of

consisting of rows in , and ranges over

all subsets of full-rank rows of .

Proof [Proof of Lemma 10]

Let

,

thus

. We now write

where is the empirical frequency with which action

has been played up to and including time

. This allows us to equivalently interpret as the

solution of a weighted-regularized least squares

regression problem with observations (instead of

the original interpretation with observations) as follows (we

suppress the dependence of on as per the context for

clarity of notation).

Let be the diagonal matrix with the

values on the diagonal (note:

). With this, we can express as

with being a diagonal &

positive semidefinite matrix,

being positive definite, and having full column rank

. A result of Forsgren(1996, Corollary 2.3) now gives

where ranges over all subsets of full-rank rows of ,

and is the submatrix of

formed by picking rows . Thus, . This proves the lemma.

F Unregularized Least squares

In our setting where we consider finitely many arms, one way wonder

whether it is possible to remove the regularization parameter

. Following Rusmevichientong and Tsitsiklis(2010), this is

indeed possible under the assumption that the minimum eigenvalue of

is away from . Then, we first play each arm once (once for all users , not for

each of them) before running

Algorithm 3, where OFUL is used with

and with redefined to be

. This leads essentially to

similar bounds, with replaced by

, as we show below.

Let .

We receive at time , observation where and .

We make the following

Assumption 2

There exists such that

1.

2.

.

3.

.

Assumption 2.3 is satisfied for instance

when there are points in such that ,

and for . We consider the least-squares estimate

F.1 Preliminary

In case is finite, one can get the following result

In order to apply this result to the low-rank bandit problem,

we need to show that

is invertible.

In our case, this matrix is at mini-session .

Let us assume that all actions are sample at least once

in the beginning. Thus, in this case

,

where .

For convenience, let us also introduce the matrix

.

In order to show that is invertible, it us enough to show that .

Now, by the result of reconstruction of the feature matrix , we know that there exists with high probability

a permutation such that the columns are well estimated:

Thus, we study . Let be any eigenvalue of , then it holds

Thus, provided that is large enough that

we deduce that is invertible.

Using the fact that ,

This translates to the condition

that is

Thus, assuming that all actions are chosen at least once in the beginning, and that

In order to control the regret of the unregularized version of OFUL, we now

use the proof of Rusmevichientong and Tsitsiklis(2010, Theorem 4.1) combined with the fact that

to get

A straightforward adaptation of the proof of Theorem 3 then gives

Following the same steps as for Lemma 3, we finally obtain the result:

Theorem 8 (Unregularized OFUL robustness result)

Assume , for all ,

and , and that

(i.e.,

the linearly realizable approximation has as its unique

optimal action). Assume that each action has been played once. Let .

Provided that the number of mini-sessions is

large enough to satisfy

where

then with probability at least for all ,

the regret of the OFUL algorithm from decision to satisfies

where we introduced

This result enables to get the corresponding variant of Theorem 4 using an unregularized OFUL.