Non-Gaussian analytic option pricing: a closed formula for the Lévy-stable model

Abstract

We establish an explicit pricing formula for the class of Lévy-stable models with maximal negative asymmetry (Log-Lévy model with finite moments and stability parameter ) in the form of rapidly converging series. The series is obtained with help of Mellin transform and the residue theory in . The resulting formula enables the straightforward evaluation of an European option with arbitrary accuracy without the use of numerical techniques. The formula can be used by any practitioner, even if not familiar with the underlying mathematical techniques. We test the efficiency of the formula, and compare it with numerical methods.

Key words— European option, -stable distribution, Lévy process, Mellin transform, Multidimensional complex analysis

I. Introduction

Black-Scholes (BS) model [3] is the well established option pricing model which opened the way to the development of theory derivative pricing, and remains a fundamental tool in the construction of hedging policies. It is a Gaussian model – the underlying price dynamics is described by a geometric Brownian motion. Nice feature of the BS model is that the solution is analytically solvable, i.e., the price of an European option under this model can be written out explicitly via a formula involving only elementary functions.

Black-Scholes theory, however, does not describe well extreme events, such as dramatic price drops, which appear more often than predicted by Gaussian models [23, 15]. As a result, many generalizations of BS models that incorporate extreme events have been introduced.

Particularly interesting are models based on -stable (or also called Lévy) distributions. These distributions possess polynomial decays of the tails which makes large jumps much more probable. The first signs of heavy tails in financial modeling have been discussed in seminal works of Mandelbrot and Fama in 1960s [18, 7]. The Lévy distributions decay as , where is called stability parameter. For financial applications, it is typical to assume , because the sample paths are a.s. continuous; for most financial applications, – see [6] and references therein. When , we recover the ordinary Gaussian distribution.

However, in general, price (or log-price) driven by a Lévy distribution does not possess finite moments , resulting in potentially infinite option values (see [5] and references therein). To cope with this divergence, Carr and Wu introduced, a model featuring a Lévy-driven underlying price [5], with a so-called condition of maximal negative asymmetry (or skewness) on the Levy process that ensures the option price to remain finite. Following Carr and Wu, we will refer to this model as the FMLS (Finite Moment Log Stable) or simply the Lévy-stable model.

Existing option pricing methods under Lévy stable model include Monte-Carlo related simulations [25], which converge with a very good degree of precision (although structurally possessing a statistical error), and numerical evaluation of integrals (Mellin-Barnes integrals in [16], integrals on the Lévy density in [12]). However, unlike to Black-Scholes model, no simple closed formula existed to evaluate the option price directly. The purpose of this paper is to establish such a formula for the Lévy-stable model; it will be achieved under the form of the rapidly convergent series , whose terms are very simple and straightforward to compute. The calculation of the series is based on techniques known from complex analysis, particularly Mellin-Barnes integral representation and residue theory in .

The paper is organized as follows: in the next section we briefly recall some facts and notations about Lévy-stable option pricing. In section 3, we establish a Mellin-Barnes integral representation for the call price in . In section 4, we compute this integral by means of residue summation, and prove the pricing formula (38). In section 5, we demonstrate the efficiency of this formula and we check it by comparing to results obtained via numerical tools. For the readers’ convenience, we also add an appendix with finer details of Mellin transform in and , and some tools from fractional analysis that turn out to be useful for stable option pricing.

II. Lévy stable option pricing

In this section, we briefly recall the definition and main properties of -stable distributions and corresponding Lévy process. We focus on the application to financial modeling, particularly to Finite moment log-stable processes.

The log-stable, (or log-Lévy model), is a non-Gaussian model into which the underlying price is assumed to be described by the stochastic differential equation

| (1) |

where is the Lévy process. The probability distribution of the Lévy process is the -stable distribution which is typically defined through the Fourier transform as

| (2) |

where for and . Parameter is the stability parameter which controls decay of the tails, and asymmetry parameter that influences the asymmetry of the distribution. For we obtain symmetric distribution, for we have the distribution with maximal asymmetry. Sometimes, it is convenient to introduce the four-parameter class of stable distributions involving also location and scale parameters. This can be done straightforwardly .

Stable distributions have heavy-tails, in other words they decay polynomially as when , except in two cases [27]:

-

, reduces to the Gaussian distribution (regardless of ) and the Lévy process becomes ordinary Brownian diffusion;

-

, possesses one heavy-tail (positive or negative, depending on the sign of ) and another tail with exponential decay for . For the support of the distribution is even confined to the positive/negative half-axis.

In the case , the process defined by Eq. (1) has all moments finite. The finiteness of the moments is the result of the fact that the (two-sided) Laplace transform of exists only for and is equal to

| (3) |

The process with has been used in connection to option pricing in [5] and is called Finite Moment Log Stable (FMLS) process. In this case, the solution for the SDE (1) is:

| (4) |

The parameter comes from the Esscher transform . The normalization is connected to the existence of an equivalent risk-neutral measure, which has the martingale property [9]. As a result, can be calculated as

| (5) |

The integral converges only for FMLS process, i.e. in the case only of maximal negative asymmetry case [5] (compare with Eq. (3)) and reads

| (6) |

where we have introduced the normalization, so that becomes distribution variance of Gaussian distribution (Black-Scholes model – see Appendix B for more details).

The price of an European call option can be generally expressed as

| (7) |

where , is the maturity time. The boundary condition is for European call option defined as , where is the strike price of the call option. For the FMLS model, the call price (7) can be expressed as the convolution of a modified payoff and a Green function [16]:

| (8) |

where the Green function can be expressed under the form of a Mellin-Barnes integral, that is, an integral over a vertical line in (see Eq. (78) in Appendix, where the reader will find more details and references about Mellin-Barnes integrals and their link to fractional diffusions): for any ,

| (9) |

Let us mention that the asymmetry of the Lévy distribution can be equivalently described by the parameter that is confined to the so-called Feller-Takayasu diamond [10]

| (10) |

Parameter is uniquely determined by and . For example, for , the value corresponds to the case when and conversely, corresponds to . In all cases corresponds to . For more details about stable distributions, see e.g., Refs. [27, 22, 14].

III. Mellin-Barnes representation for the stable call price

We now derive an expression for the price (8) under the form on an integral of some complex differential 2-form. Let then , , , ; we will also assume that (Lévy-Pareto case) and that (Carr-Wu maximal negative asymmetry hypothesis).Let us define . We can rewrite the modified payoff as

| (11) |

so that the option price can be conveniently rewritten as

| (12) |

Let us now show how to rewrite the option price (12) with help of Mellin-Barnes integral representations.

Lemma 1.

Assume that ; then for any the following holds:

| (13) |

Now, introduce

| (14) |

so that we can write:

| (15) |

Proposition 1.

The following Mellin-Barnes representations in and hold:

(i) -integral:

| (16) | ||||

and this double integral converges into the polyhedra

(ii) -integral:

| (17) |

and this integral converges into the half-plane

Proof.

We start by (ii): integrating over the Green parameter in the -integral in the definition (14) results in:

| (18) |

Then we use the Gamma functional relation:

| (19) |

and this yields the desired result (17).

To prove (ii), we start by introducing a supplementary Mellin-Barnes representation for the exponential term (see eq. (52) in Appendix):

| (20) |

where the integral converges for , or, equivalently said, . Plugging this into the -integral in the definition (14) gives birth to a Beta integral [1]:

| (21) |

Simplifying by in the incoming double integral yields the representation (17) ∎

IV. Residue summation and closed pricing formula

I. integral

Proposition 2.

The integral can be expressed as the sum of the following absolutely convergent series:

| (22) |

Proof.

The characteristic quantity associated to the Mellin-Barnes representation (22), is, by definition (see [19, 20] or Appendix) is

| (23) |

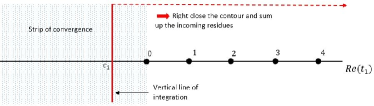

as soon as . Therefore, the integral over the vertical line can be right closed, thus corresponding to minus the sum of the residues associated to poles in the right half-plane (see fig. 1). Because of the singular behavior of the Gamma function around its negative arguments (50) these residues are induced by the -term and equal

| (24) |

∎

II. integral

Proposition 3.

The integral can be expressed as the sum of the following absolutely convergent double series:

| (25) |

Proof.

Let us introduce the notations

| (26) |

and the complex differential 2-form

| (27) |

so that (16) can be written under the standard form of a Mellin-Barnes integral in :

| (28) |

The characteristic vector associated to is (see [19, 20] and Appendix of this paper) :

| (29) |

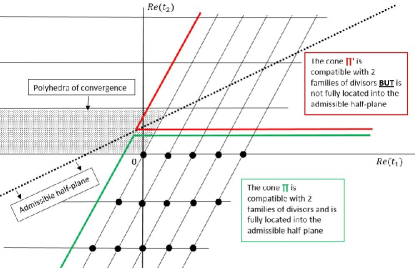

and therefore the half-plane of convergence one must considers:

| (30) |

is the one located under the line (see fig. 2):

| (31) |

Because , the cone defined by

| (32) |

is included in ; moreover it is compatible with the two families of divisors

| (33) |

induced by the and functions respectively. To compute the residues associated to every element of the singular set , we change the variables:

| (34) |

so that in this new configuration reads

| (35) |

With this new variables, the divisors and are induced by the and functions, and intersect at every point of the type , . From the singular behavior of the Gamma function (50) around a singularity, we can write:

| (36) |

Taking the residues and simplifying:

| (37) |

Summing in the whole cone yields the series (25) ∎

III. Closed pricing formula

Theorem 1.

Let , let and . For any and under maximal asymmetry hypothesis, the European call price is equal to:

| (38) |

Proof.

In the case of Black-Scholes, i.e. , the pricing formula (38) can be rewritten as:

| (39) |

where in this case . We recover the formula obtained in [2] for the Black-Scholes call. In particular, if we suppose that the asset is "at-the-money forward", that is:

| (40) |

then by definition and we are left with:

| (41) |

Series (41) is a power series of the market volatility which starts for :

| (42) |

Recalling , we have:

| (43) |

which is the Brenner-Subrahmanyam approximation [4] for the call price. Series (41) is also derived in appendix directly from Taylor expanding the Black-Scholes formula, which turns out to be easy in the ATM-froward case. The interested reader can compare the two equivalent representations (41) and (89).

V. Numerical applications

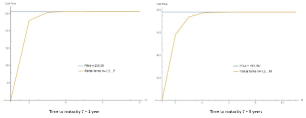

Let us demonstrate the results obtained in the previous section in the real estimation of option pricing. First, we demonstrate that the double-series (38) converges quickly after very few terms. Tab. 1 provides an example of the series convergence of an option with parameters . The convergence is a little bit slower when grows, but remains very efficient, see for instance Table 2. In Fig 3 we compute the partial terms of the series (38) as a series of , that is, the sum of vertical columns in tables 1 and 2, for a time to maturity being 1 or 5 years. We observe that, in both cases, the convergence is fast.

| =1Y | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| 0 | 395.167 | 49.052 | 4.962 | 0.431 | 0.033 | 0.002 | 0.000 |

| 1 | -190.223 | -32.268 | -4.005 | -0.405 | -0.035 | -0.003 | -0.000 |

| 2 | 23.829 | 7.767 | 1.317 | 0.164 | 0.017 | 0.001 | 0.000 |

| 3 | 1.430 | -0.649 | -0.211 | -0.036 | -0.004 | -0.000 | -0.000 |

| 4 | -0.246 | -0.029 | 0.013 | 0.001 | 0.000 | 0.000 | 0.000 |

| 5 | -0.046 | 0.004 | 0.000 | -0.000 | -0.000 | -0.000 | -0.000 |

| 6 | 0.001 | 0.000 | -0.000 | -0.000 | 0.000 | 0.000 | 0.000 |

| 7 | 0.001 | -0.000 | -0.000 | 0.000 | 0.000 | -0.000 | -0.000 |

| 8 | 0.000 | -0.000 | 0.000 | 0.000 | -0.000 | -0.000 | 0.000 |

| Call | 229.914 | 253.790 | 255.866 | 256.024 | 256.035 | 256.035 | 256.035 |

| =5Y | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 978.516 | 313.038 | 81.607 | 18.274 | 3.626 | 0.651 | 0.108 | 0.016 | 0.002 | 0.000 |

| 1 | -454.606 | -198.750 | -63.582 | -16.576 | -3.712 | -0.736 | -0.132 | -0.022 | -0.003 | -0.000 |

| 2 | 54.963 | 46.168 | 20.184 | 6.457 | 1.683 | 0.377 | 0.075 | 0.013 | 0.002 | 0.000 |

| 3 | 3.183 | -3.721 | -3.1258 | -1.367 | -0.438 | -0.114 | -0.026 | -0.005 | -0.001 | -0.000 |

| 4 | -0.529 | -0.162 | 0.189 | 0.158 | 0.069 | 0.022 | 0.006 | 0.001 | 0.000 | 0.000 |

| 5 | -0.096 | 0.021 | 0.007 | -0.008 | -0.006 | -0.003 | -0.001 | 0.000 | 0.000 | 0.000 |

| 6 | 0.003 | 0.003 | -0.001 | -0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| 7 | 0.002 | -0.000 | -0.000 | 0.000 | 0.000 | -0.000 | -0.000 | -0.000 | -0.000 | -0.000 |

| 8 | -0.000 | -0.000 | 0.000 | -0.000 | -0.000 | 0.000 | 0.000 | -0.000 | -0.000 | -0.000 |

| Call | 581.436 | 738.034 | 773.313 | 780.252 | 781.475 | 781.672 | 781.702 | 781.706 | 781.706 | 781.706 |

Additionally, we compare the prices obtained for various Lévy parameter and market configurations (in and out of the money), via different techniques. Let us assume an option with market parameters . We compare in and out of the money option prices via three different techniques:

-

•

Series formula (38) obtained in this paper. Only the first terms of the double series are taken into account (, ), demonstrating its quickness of convergence;

-

•

Gil-Pelaez numerical estimation. The results obtained by a numerical evaluation of the Gil-Pelaez type: the price of an European call option with spot , strike and maturity is:

Using Gil-Pelaez (see for instance [21]) and denoting one finds

(44) (45) Finally, rearranging the equation of the call price, we get

(46) The characteristic function in the Lévy-stable model with maximal assymetry is [5]:

(47) where ; the integrals in (46) can be carried out easily with a code in R or C++. In the following array, we show that our analytic results are completely confirmed by this evaluation for any .

-

•

Discretization of calculated by Mellin-Barnes integral used in (8). One calculates the probability distribution by the Mellin-Barnes integral for a grid of functions, and replace the integral for option pricing (8) by a discrete sum over this grid. Of course the price is as more precise as the grid is dense. In the following array, we observe that the result of this technique fits very well with the analytic results for ; this techniques becomes less precise when : this is because the probability distribution function decays less fast, and thus the grid should be extended to become more accurate.

| Out of the money (S=3800) | ||||||

| Analytic result (38) | 284.52 | 268.52 | 256.04 | 246.60 | 239.83 | 235.52 |

| Gil-Pelaez | 284.52 | 268.52 | 256.04 | 246.59 | 239.83 | 235.51 |

| Discretization | 292.74 | 272.17 | 257.63 | 247.45 | 240.20 | 235.74 |

| In the money (S=4200) | ||||||

| Analytic result (38) | 547.67 | 523.25 | 502.53 | 485.07 | 470.56 | 458.79 |

| Gil-Pelaez | 547.67 | 523.25 | 502.53 | 485.07 | 470.56 | 458.79 |

| Discretization | 557.47 | 527.39 | 504.59 | 486.05 | 470.98 | 459.10 |

VI. Conclusion and perspectives

In this paper, we have shown that the formula for an European call option driven by the Finite moment log-stable process can be obtained in the form of rapidly convergent double series (38).

The formula provides a new and efficient analytic tool in the non-Gaussian derivative pricing – it provides the market practitioner with a simple tool that can be easily used without any deeper knowledge of advanced mathematical techniques.The series terms are straightforward to evaluate by simple functions - the only "transcendence" being carried by the particular values of the Gamma function.It can also be easily used to imply the volatility from market observations.

The convergence of the series is fast enough to ensure excellent levels of precision only with summing the first few terms of the series. Moreover, as there is no need to use a numerical estimation techniques.

Moreover, the residue technique can be successfully applied to a much wider class of models. First, one would like to relax the maximal asymmetry hypothesis , which may not be precise enough for less liquid markets; in this case, the Lévy propagator (8) is known to diverge, but the Mellin-Barnes integral representation provide us with a natural regularization tool, and the residues summation will remain finite in this case. Second, one can extend the fractional differential equation (71) to a space-time fractional diffusion. The resulting Green function is obtained as a superposition of stable distributions. In both cases, the residue summation technique will give a finite result. The computation will be detailed in future works.

Acknowledgements

We wish to thank Raphael Douady and Zari Rachev for their interest in this work and their valuable suggestions. J. K. was supported by the Austrian Science Fund, grant No. I 3073-N32 and the Czech Science Foundation, grant No. 17-33812L.

Appendix A APPENDIX: Mellin transforms and residues

We briefly present here some of the concepts used in the paper. The theory of the one-dimensional Mellin transform is explained in full detail in [8]. An introduction to multidimensional complex analysis can be found in the classic textbook [11], and applications to the specific case of Mellin-Barnes integrals is developed in [19, 20].

I. One-dimensional Mellin transforms

1. The Mellin transform of a locally continuous function defined on is the function defined by

| (48) |

The region of convergence into which the integral (48) converges is often called the fundamental strip of the transform, and sometimes denoted .

2. The Mellin transform of the exponential function is, by definition, the Euler Gamma function:

| (49) |

with strip of convergence . Outside of this strip, it can be analytically continued, expect at every negative integer where it admits the singular behavior

| (50) |

3. The inversion of the Mellin transform is performed via an integral along any vertical line in the strip of convergence:

| (51) |

and notably for the exponential function one gets the so-called Cahen-Mellin integral:

| (52) |

4. When is a ratio of products of Gamma functions of linear arguments:

| (53) |

then one speaks of a Mellin-Barnes integral, whose characteristic quantity is defined to be

| (54) |

governs the behavior of when and thus the possibility of computing (51) by summing the residues of the analytic continuation of right or left of the convergence strip:

| (55) |

For instance, in the case of the Cahen-Mellin integral one has and therefore:

| (56) |

as expected from the usual Taylor series of the exponential function.

II. Multidimensional Mellin transforms

1. Let the , , be vectors in ,and the , be complex numbers. Let and in and "." represent the euclidean scalar product. We speak of a Mellin-Barnes integral in when one deals with an integral of the type

| (57) |

where is a complex differential 2-form who reads

| (58) |

The singular sets induced by the singularities of the Gamma functions

| (59) |

are called the divisors of . The characteristic vector of is defined to be

| (60) |

and the admissible half-plane:

| (61) |

2. Let the in , the be linear aplications and be a subset of of the type

| (62) |

A cone in is a cartesian product

| (63) |

where and are of the type (62). Its faces are

| (64) |

and its distinguished boundary, or vertex is

| (65) |

3. Let . We group the divisors of the complex differential form into two sub-families

| (66) |

We say that a cone is compatible with the divisors family if:

-

-

Its distinguished boundary is ;

-

-

Every divisor and intersect at most one of his faces:

(67)

Appendix B Fractional diffusion equation and log-stable processes

Under the Carr-Wu maximal negative hypothesis , or equivalently, , it is known that the probability distributions of the log-returns (i.e., the Green functions, or fundamental solutions associated to the the option price (7)) satisfy the equation (see [16, 15] and references therein):

| (70) |

which is a particular case of the generic space-fractional diffusion

| (71) |

Here, the space fractional derivatives is a Riesz-Feller derivatives, a two-parameter operator defined by its action on the Fourier space (see [10, 17] for more details on fractional analysis):

| (72) |

It is a consequence of definition (72) that Green functions associated to space fractional diffusions can be written under the form

| (73) |

These functions have been extensively studied [17]; they can conveniently be expressed as Mellin-Barnes integrals. Introducing

| (74) |

then for any the following representation holds:

| (75) |

The Green function (75) extends to negative arguments via the symmetry property:

| (76) |

In the Finite Moment Log-Stable model, where the maximal negative asymmetry hypothesis holds, one notes that

| (77) |

and therefore we may denote the corresponding Green function by:

| (78) |

where is the Heaviside step function. In particular, when (Gaussian, i.e. Black-Scholes case), and:

| (79) |

Using the Legendre duplication formula [1] and performing a change of variables shows that (79) can be written under the form

| (80) |

Using the inversion formula (52), we get:

| (81) |

Recalling that, in the Gaussian case, and , then the Green function in the convolution (8) becomes

| (82) |

which is the well-known heat kernel. It is the fundamental solution of the one-dimensional diffusion (heat) equation

| (83) |

which is the particular case of the fractional diffusion (70) for , and a reduction of the Black-Scholes PDE after a suitable change of variables [26], whose solution is given by the Black-Scholes formula:

| (84) |

where and is the normal distribution function. A particular case occurs when the asset is "at-the-money forward", that is when

| (85) |

because, then, and the Black-Scholes formula (84) reduces to

| (86) |

In this case, it is easy to Taylor expand the normal distribution functions [1], with the result:

| (87) |

and therefore the price goes as:

| (88) |

which is the approximation obtained by Brenner and Subrahmanyam in [4]. Last, one can note that, using the particular values for the Gamma function at half integers [1], one can rewrite the series (87) as

| (89) |

References

- [1] Abramowitz, M. and Stegun, I., Handbook of mathematical functions, 1972, Dover Publications

- [2] Aguilar, J.-Ph., A series representation for the Black-Scholes formula, 2017, arXiv:1710.01141

- [3] Black, F. and Scholes, M., The pricing of options and corporates liabilities, 1973, Journal of political economy 81 p.637

- [4] Brenner, M. and Subrahmanyam, M.G., A simple approach to option valuation and hedging in the Black-Scholes model, 1994, Financial Analysts Journal, 25-28

- [5] Carr, P., Wu, L., The finite moment log-stable process and option pricing, 2003, Journal of Finance, 38, 34–105

- [6] Cont, R., Potters, M. and Bouchaud, J.P., Scaling in financial data: stable laws and beyond, 1997, Scale invariance and beyond, Dubrulle, Granette, Sornette eds., Springer

- [7] Fama, E. F., The behavior of stock market prices, Journal of Business, 1965, 38, 34–105

- [8] Flajolet, P., Gourdon, X. and Dumas, P., Mellin transform and asymptotics: Harmonic sums, Theoretical Computer Science, 1995, 144, 1–2, 3-58

- [9] Gerber, H., Hans, U. and Shiu, E., Option pricing by Esscher transforms, 1993, Institut de sciences actuarielles (HEC)

- [10] Gorenflo, R. and Mainardi, F., Parametric subordination in fractional diffusion processes, 2012, Fractional dynamics: recent advances, World Scientific Publishing

- [11] Griffiths, P. and Harris, J., Principles of Algebraic Geometry, 1978, Wiley & sons

- [12] Hurst, S.R., Platen, E., Rachev, S., Option pricing for a logstable asset price model, 1998, Mathematical and computer modeling, 29, pp. 105–119

- [13] Kleinert, H., Option pricing from path integral for non-Gaussian fluctuations. Natural martingale and application to truncated Lévy distributions, 2002, Physica A, 312, 1–2, 217–242

- [14] Kleinert, H., Path integrals in quantum mechanics, statistics, polymer physics and financial markets, 2009, World Scientific

- [15] Kleinert, H., Quantum field theory of black-swan events, Foundation of Physics, 2013, 1, available online at http://klnrt.de/409 (accessed 16 oct. 2017)

- [16] Kleinert, H., Korbel, J., Option pricing beyond Black-Scholes based on double-fractional diffusion, Physica A, 2016, 449, 200–214

- [17] Mainardi, F., Pagnini, G. and Saxena, R., Fox H-functions in fractional diffusions, Journal of computational and applied mathematics, 2005, 178, 321-331

- [18] Mandelbrot, B., The variation of certain speculative prices, Journal of Business, 1963, 36, 394–419

- [19] Passare, M.,Tsikh, A. and Zhdanov, O., A multidimensional Jordan residue lemma with an application to Mellin-Barnes integrals, 1994, Aspects of Math., E26, 233-241

- [20] Passare, M.,Tsikh, A. and Zhdanov, Multiple Mellin-Barnes intgrals as periods of Calabi-Yau manifolds, 1997, Theor. Math. Phys., 109, 1544-1555

- [21] Rouah, F., The Heston Model and its Extensions in Matlab and C#,2013, John Wiley & Sons

- [22] Ken-Iti Sato, Lévy Processes and Infinitely Divisible Distributions, 1999, Cambridge Studies in Advanced Mathematics, Cambridge University Press

- [23] Taleb, N. N., The Black Swan: The Impact of the Highly Improbable Fragility, 2010, Random House Publishing Group

- [24] Tankov, P., Financial Modelling with Jump Processes, 2003, Chapman & Hall/CRC Financial Mathematics Series, Taylor & Francis

- [25] Tankov, P. and Poirot, J., Monte-Carlo option pricing for tempered stable (CGMY) process, 2006, Asia Pacific Financial Markets, 13

- [26] Wilmott, P., Paul Wilmott on Quantitative Finance, Wiley & Sons, 2006

- [27] Zolotarev, V. M., One-dimensional Stable Distributions, 1986, Translations of mathematical monographs, American Mathematical Society