Multivariate MixedTS distribution

Abstract

The multivariate version of the Mixed Tempered Stable is proposed. It is a generalization of the Normal Variance Mean Mixtures. Characteristics of this new distribution and its capacity in fitting tails and capturing dependence structure between components are investigated. We discuss a random number generating procedure and introduce an estimation methodology based on the minimization of a distance between empirical and theoretical characteristic functions. Asymptotic tail behavior of the univariate Mixed Tempered Stable is exploited in the estimation procedure in order to obtain a better model fitting. Advantages of the multivariate Mixed Tempered Stable distribution are discussed and illustrated via simulation study.

Keywords: MixedTS distribution, MixedTS Tails, MixedTS Lévy process, Multivariate MixedTS.

1 Introduction

The Mixed Tempered Stable (MixedTS from now on) distribution has been introduced in Rroji and

Mercuri (2015) and used for portfolio selection in Hitaj

et al. (2015) and for option pricing in Mercuri and

Rroji (2016). It is a generalization of the Normal Variance Mean Mixtures (see Barndorff-Nielsen et al., 1982) since the structure is similar but its definition generates a dependence of higher moments on the parameters of the standardized Classical Tempered Stable (see Küchler and

Tappe, 2013; Kim

et al., 2008) that replaces the Normal distribution.

Recently different multivariate distributions have been introduced in literature for modeling the joint dynamics of financial time series. For instance, Kaishev (2013) considers the LG distribution defined as a linear combination of independent Gammas for the construction of a multivariate model whose properties are investigated based on its relation with multivariate splines. Another model is based on the multivariate Normal Tempered Stable distribution, defined in Bianchi

et al. (2016) as a Normal Mean Variance Mixture with a univariate Tempered Stable distributed mixing random variable that is shown to capture the main stylized facts of multivariate financial time series of equity returns.

In this paper, we present the multivariate MixedTS distribution and discuss its main features.

The dependence structure in the multivariate MixedTS is controlled by the components of the mixing random vector. A similar approach has been used in Semeraro (2008) for the construction of a multivariate Variance Gamma distribution starting from the idea that the components in the mixing random vector are Gamma distributed. However, as observed in Hitaj and

Mercuri (2013a, b), Semeraro’s model seems to be too restrictive for describing the joint distribution of asset returns. In particular, the sign of the skewness of the marginal distributions determines the sign of the covariance. This means, for instance, if two marginals of a multivariate Variance Gamma have negative skewness, their correlation can never be negative. The additional parameters in the multivariate MixedTS introduce more flexibility in the dependence structure and overcome these limits. Indeed, we compute higher moments for the multivariate MixedTS and show how the tempering parameters break off the bond between skewness and covariance signs.

We discuss a simulation method and propose an estimation procedure for the multivariate MixedTS. In particular the structure of univariate and multivariate MixedTS allows us to generate trajectories of the process using algorithms that already exist in literature on the simulation of the Tempered Stable distribution (see Kim

et al. (2008)).

The proposed estimation procedure is based on the minimization of a distance between empirical and theoretical characteristic functions. As explained for instance in Yu (2004), in absence of an analytical density function, estimation based on the characteristic function is a good alternative to the maximum likelihood approach.

An estimation procedure can be based on the determination of a discrete grid for the transform variable and on the Generalized Method of Moments (GMM) as for instance in Feuerverger and

McDunnough (1981). The main advantage of this approach is the possibility of obtaining the standard error for estimators whose efficiency increases as the grid grows finer. However, the covariance matrix of moment conditions becomes singular when the number of points in the grid exceeds the sample size. The GMM objective function explodes thus the efficient GMM estimators can not be computed. To overcome this problem Carrasco and

Florens (2000) developed an alternative approach, called Continuum GMM

(henceforth CGMM), that uses the whole continuum of moment conditions associated to the difference between theoretical and empirical characteristic functions.

Starting from the general structure of the CGMM approach, we propose a constrained estimation procedure that involves the whole continuum of moment conditions. Results on asymptotic tail behavior of marginals are used as constraints in order to improve fitting on tails. An analytical distribution that captures the dependence of extreme events is helpful in many areas such as in portfolio risk management, in reinsurance or in modeling catastrophe risk related to climate change. The proposed estimation procedure is illustrated via numerical analysis on simulated data from a bivariate and trivariate MixedTS distributions. We estimate parameters on bootstrapped samples and investigate their empirical distribution.

The paper is structured as follows. In Section 2 we give a brief review of the univariate MixedTS, study its asymptotic tail behavior and discuss the MixedTS Lévy process. The definition and main features of the multivariate MixedTS distribution are given in Section 3. In Section 4 we explain the estimation procedure and present some numerical results. Section 5 draws some conclusions.

2 Univariate Mixed Tempered Stable

Let us recall the definition of a univariate Mixed Tempered Stable distribution.

Definition 1.

A random variable is Mixed Tempered Stable distributed if:

| (1) |

where parameters , and conditioned on the positive r.v. , follows a standardized Classical Tempered Stable distribution with parameters i.e.:

| (2) |

or equivalently

| (3) |

where and (see Kim et al., 2008, for more details on CTS).

For this distribution it is possible to obtain the first four moments which are reported in the following proposition.

Proposition 2.

The first four moments of the MixedTS have an analytic expression since:

| (4) |

where and are the third and fourth central moments respectively.

We observe that and depend on the mixing random variable and on the tempering parameters and . Indeed, we are able to obtain an asymmetric distribution even if we fix . It is worth to note that parameters and may have an economic interpretation. In particular, can be thought as the risk free rate and as the risk premium of the unit variance process . In the Normal Variance Mean Mixtures is not possible to have negatively skewed distribution with . From an economic point of view, it is not possible to have a positive risk premium for unit variance for negatively skewed distributions. This is a drawback of the Normal Variance Mean Mixture model since negative skewness is frequently observed in financial time series.

The mixture representation becomes very transparent for cumulant

generating functions. Let

| (5) |

and

| (6) |

where is the cumulant generating function of a random variable . Then we have

| (7) |

As shown in Rroji and Mercuri (2015), if , we get some well-known distributions used for modeling financial returns as special cases. For instance if the Variance Gamma introduced in Madan and Seneta (1990) is obtained. Fixing and letting go to infinity leads to the Standardized Classical Tempered Stable Kim et al. (2008). Choosing:

and computing the limit for we obtain the Geometric Stable distribution (see Kozubowski et al. (1997)).

2.1 Fundamental strip and moment explosion

Laplace transform theory tells us that given a random variable the set of where:

is a strip, which is called the fundamental strip of . Depending on the tails of the strip can be the entire set of complex numbers , a left or right half-plane, a proper strip of finite width or degenerate to the imaginary axis if both tails are heavy. From here on we neglect the case since the MixedTS becomes a Normal Variance Mean Mixture and we refer to Barndorff-Nielsen et al. (1982) for the fundamental strip and tail behavior in this special case. When , with cumulant generating function in (6) has fundamental strip .

Theorem 3.

Suppose now has fundamental strip for some . A concrete example would be . Then we have:

-

1.

If then has fundamental strip .

-

2.

If then has fundamental strip , where is the unique real solution to .

-

3.

If then has fundamental strip , where is the unique real solution to .

-

4.

If then has fundamental strip where are the two real solutions of .

Proof.

First of all we prove point 1 where has fundamental strip . Any point can be written as:

We start from

Since is a convex function, we have:

Collecting terms with and we get:

| (9) |

If the right hand side in (9) is less than .

To prove the second point, it is enough to observe that

is a convex continuous function. Moreover, the condition implies that:

As observed in Giaquinta and

Modica (2003), a convex continuous function in the compact interval , and has a unique zero . In our case, this result ensures that is the unique real solution of the equation Following the same steps in point 1 we get the result in point 2.

Point 3 is the same of point 2.

Point 4. It is sufficient to observe that is a continuous convex function such that . For any

, there exists a neighborhood of zero such that . Continuity and convexity ensure the existence of two zeros . The remaining part of the proof arises from the same steps in point 1.

∎

2.2 Tail Behavior of a Mixed Tempered Stable distribution

In order to study the tail behavior of a , that denotes a MixedTS distribution with Gamma mixing r.v., we need first to recall the structure of its moment generating function where without loss of generality we require .

If , the moment generating function is defined as:

| (10) |

We recall some useful results on the study of asymptotic tail behavior given in Benaim and Friz (2008). Given the moment generating function of a r.v. with cumulative distribution function defined as:

we consider and defined respectively as:

| (11) |

and

| (12) |

where . Criterion I in Benaim and Friz (2008) for asymptotic study of tails states:

Proposition 4.

-

1.

If for some , for some , as then

-

2.

If for some , for some , as then

We remark that stands for regularly varying functions of order , i.e. set of slowly varying functions and the derivative of order of the moment generating function .

Before studying the tail behavior of the , let us study first the tail behavior of a . The fundamental strip is and the moment generating function is:

| (13) |

We consider separately two cases:

-

1.

,

-

2.

.

Considering the right tail of a CTS we have and the converges to constant as .

CTS case - 1: Under the assumption that , we apply criterion 1 in Benaim and

Friz (2008) checking that the first derivative of satisfies for some , as .

The first derivative of in (13) is:

Evaluating at point and computing the limit for , we obtain:

where the term is a constant. Therefore we have shown that the first order derivative of satisfies criterion 1 in Benaim and

Friz (2008) when .

CTS case - 2 Let us consider now the right tail behavior for where both and converge to some constants as . We compute the second order derivative of the and show that criterion 1 in Benaim and Friz (2008) is verified for .

We evaluate at point and for we obtain the following result:

Now we study the right tail behavior of the . From Theorem 3 we have that can be or , therefore in order to study the behavior of the moment generating function in (10) we consider separately two cases:

case 1: covers case 1 and 3 in Theorem 3. The moment generating function of the , defined in (10), at the critical point is finite. We compute the first order derivative of and verify if criterion 1 in Benaim and Friz (2008) is satisfied. We consider separately the two cases and .

-

•

Observe that since the term is a positive constant, we can conclude that the moment generating function of the , in case of and , satisfies criterion 1 in Benaim and Friz (2008) for .

-

•

and . In this particular case both the moment generating function of the and and its first derivative are constants, therefore we compute the second derivative of the m.g.f. of the .

Since , we have that the following limit converges to a positive constant as :

The term is a positive constant term in case 1 and 3 of Theorem 3 and the same holds for the positive constant term . Now we study the asymptotic behavior of as

Combining these results together we conclude that the moment generating function of the in case of and satisfies criterion 1 in Benaim and Friz (2008) for i.e.:

case - 2 At this point we are left with the case when which covers cases 2 and 4 in Theorem 3. We recall that the m.g.f of the at point is:

| (14) |

Multiplying and dividing by in (14) we have:

Substituting with we obtain:

| (15) |

We can show that is a slowly varying function that implies is a regularly varying function.

Let us study the following limit:

| (16) |

When we have , is a slowly varying function, since applying de l’Hôpital theorem to (16) we get:

| (17) |

Concluding we can say that in case the criterion one in Benaim and Friz (2008) is satisfied for .

The study of the left tail behavior follows the same steps as above.

Remark 5.

In the CTS distribution and influence both higher moments and tail behavior. The singularities in Theorem 3 are helpful in describing the asymptotic behavior of the MixedTS tails based on the result:

| (18) |

From point 1 in Theorem 3 we get for the MixedTS the same asymptotic tail behavior as in the CTS, i.e. exponentially decaying, while in the other points of Theorem 3 the ’s satisfy the additional condition . Singularities in point 2 and 3 describe respectively right and left asymptotic tail behavior. In point 4 asymptotic of both tails are deduced. The scale parameter of the mixing r.v. allows us to have more flexibility in capturing tails once skewness and kurtosis, which depend on and , are computed. Consider for example point 2 where that implies, for fixed , from where we deduce that a higher weight is given to the right tail of the MixedTS than in the CTS case.

We conclude this section by investigating numerically the implications of Proposition 4. Results on the behavior of tails can be used for the identification of and in (11) and in (12). Indeed, for , we have:

| (19) |

while, for , we obtain:

| (20) |

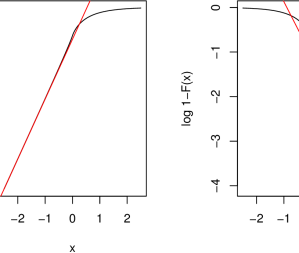

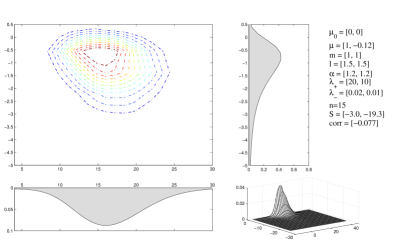

Figure 1 refers to the behavior of and of for the MixedTS- with parameters , , , and .

Considering relations in (19) and in (20), we estimate and as the slope of two linear regressions following four steps: Given a sample composed by observations, we determine the empirical cumulative distribution function . Then we determine and as the empirical quantiles at level and , i.e.:

and

The set [, , ,] refers to the sorted values from the smallest to the largest .

We introduce the sets and defined as:

We use the elements in the set to estimate as the slope of the linear regression:

while the elements in the set are used for the estimation of the coefficient as the slope of the following regression:

where is an error term. In Figure 2 we show the behavior of the estimated and for varying if true values are and . This result is useful in estimation of a MixedTS- since it can be used as a constraint in the optimization routine when we require the empirical and to be equal to the corresponding counterpart.

2.3 MixedTS Lévy process

Suppose is an infinitely divisible distribution on with cumulant function .

Then there is a convolution semigroup of probability measures on

and a Lévy process such that for and .

In Rroji and

Mercuri (2015) it is shown that the distribution is infinitely divisible. According to the general theory, see for example Prop.3.1, p.69 in Cont and

Tankov (2004), there exists a Lévy process such that . We have

| (22) |

thus if is with mixing distribution , then is with mixing distribution . In the case is with mixing distribution then is with mixing distribution , since implies .

Definition 6.

A Lévy process such that is called the Lévy process.

The Lévy process is first of all a Lévy process, thus it starts at zero and has independent and stationary increments, and we have for

| (23) |

For example with gamma mixing

| (24) |

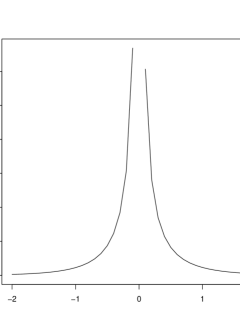

We conclude this section by showing how to determine the Lévy measure from a numerical point of view.

The Lévy-Khintchine formula says

| (25) |

where is the indicator function, is the Lévy density. Differentiating twice yields:

| (26) |

Choosing , the integral in (26) becomes:

| (27) |

Therefore is the bilateral transform of with . The Lévy density is determined using the Bromwhich inversion integral (see Boas, 2006, for details). In Figure 3, we have the Lévy density of the with fixed parameters , , , and

3 Multivariate Mixed Tempered Stable

In this section we define the multivariate MixedTS distribution, analyze its characteristics in the particular case the mixing r.v. is multivariate Gamma distributed.

3.1 Definition and properties

Definition 7.

A random vector follows a multivariate MixedTS distribution if the component has the following form:

| (28) |

where is the component of a random vector , defined as:

| (29) |

and are infinitely indivisible defined on with and mutually independent; and

| (30) |

It is worth to notice that in Definition 7 it is possible to consider a finer sigma field generated from the sequence of r.v.’s . Let us define as:

| (31) |

and require the distribution of to be a Standardized Classical Tempered Stable:

| (32) |

Notice that this condition is the generalization of (30) since the following implications hold:

The sigma field is also suitable in order to define the dependence

structure between components since we impose independence among ’s.

We remark that if , and for each :

we have that is sum of two Gamma’s with the same scale parameter. Applying the summation property, we have that guarantees infinite divisibility, necessary for definition of multivariate MixedTS-.

Remark 8.

The multivariate MixedTS definition in (28) using matrix notation reads:

| (33) |

where , such that , is a random vector with positive elements, is a random matrix positive defined, such that and is a standardized Classical Tempered Stable random vector.

The characteristic function of the multivariate MixedTS has a closed form formula as reported in the following proposition (for the derivation see Appendix B).

Proposition 9.

The characteristic function of the multivariate MixedTS is:

|

|

(34) |

where the

is the characteristic exponent of a standardized Classical Tempered Stable r.v.

defined as:

Proposition 10.

Consider a random vector where the distribution of each component is for . The formulas for the moments are:

-

•

Mean of the general element:

(35) -

•

Variance of the element:

(36) -

•

Covariance between the and elements:

(37) -

•

Third central moment of the component:

(38) -

•

Fourth central moment of the element:

(39)

See Appendix A for details on moment derivation. From (37) and (38) is evident that the multivariate overcomes the limits of the multivariate Variance Gamma distribution in capturing the dependence structure between components (see Hitaj and Mercuri (2013a)). Indeed, the relation that exists between the sign of the skewness of two marginals and the sign of their covariance in the multivariate Variance Gamma, is broken up by the tempering parameters in the multivariate .

In particular the following result determines the existence of upper and lower bounds for the covariance depending on the tempering parameters. Here we consider the cases that the Semeraro model is not able to capture.

Theorem 11.

Let and be two components of a multivariate MixedTS-, the following results hold:

-

1

where is defined in (36) and if , and

-

2

and if and

-

3

and if or

Proof.

Let us first discuss the case where both components have positive skewness. In this case the lower bound of the covariance exists if the following problem admits a solution:

| (40) |

The signs of skewness depend on the signs of the following quantities:

The feasible region of the minimization problem in (40) depends on the difference between tempering parameters. We observe that the cubic function is strictly increasing and satisfies the following limits:

Therefore exists only one such that The sign of is determined by the following implications:

The feasible region can be written as:

and the lower bound is while the upper bound is In this case the lower bound is negative when

or

Now we consider the case when both skewnesses are negative. Following a similar procedure the feasible region becomes:

The and the upper bound is . The upper bound is negative when

or

The last case refers to the context when the skewnesses have different signs and following the same procedure as above we have and ∎

3.2 Simulation scheme

The structure of the univariate / multivariate MixedTS distribution allows us to exploit the procedures (algorithms) for the estimation of the Tempered Stable proposed in literature for instance in Kim et al. (2008). The steps that we follow for the simulation of a multivariate MixedTS with components are listed below.

-

1.

Simulate independent random variables and for .

-

2.

Compute for .

-

3.

Simulate .

-

4.

Compute .

-

5.

Repeat the steps from to .

The multivariate MixedTS inherits from its univariate version a similar level of flexibility. For instance, choosing all for we obtain the multivariate Variance Gamma introduced in Semeraro (2008) as a special case. As observed in Hitaj and

Mercuri (2013a), the Semeraro’s model is not able to capture some situations often observed in financial time series. We recall that Semeraro’s model has the same structure as in (28) but instead of each we have where are independent Standard Normals. This structure limits the capacity of the multivariate Variance Gamma distribution in capturing different dependence structures between components of a random vector, as the sign of skewness is determined by the sign of and the covariance between components has the same form as in (37). In particular this distribution is not able to reproduce negatively correlated components with marginal negative (or positive) skewness or positively correlated components with different signs on the marginal skewness. The multivariate overcomes these limits as the sign of marginal skewness depends on and on the tempering parameters.

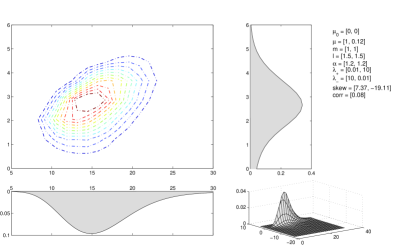

In Figures 4 and 5 we report the level curves of joint densities of bivariate and the corresponding marginal densities. In the Figure 4 we consider the case where the marginal distributions have opposed signs for skewness ( and ) and positive correlation. In the Figure 5 the components are negatively correlated with marginal negative skew distributions ( and ). These cases can not be reproduced using the Semeraro model.

4 Estimation procedure

In this section we introduce an estimation procedure of the multivariate MixedTS based on the distance between the empirical and theoretical characteristic functions . Constraints on tail behavior are considered in order to improve the fitting on tails. Before formulating the problem mathematically let us first define the following two quantities: a weighting function given by:

and the error term computed on the empirical characteristic function computed on a sample of size and the theoretical characteristic function , defined as:

The minimization problem reads:

| (41) |

where is the inner product between

vectors and ; is the set of the MixedTS parameters.

,

determine the left tail

behavior of the empirical and theoretical marginal distribution while

,

refer respectively to the

empirical and theoretical marginal right tail. For the quantities

,

,

,

we refer to Section

2.2.

The integral in (41) is evaluated using Monte Carlo simulation since can

be seen as a multivariate Standard Normal random variable. We observe that the objective function in (41) is bounded since the and the error term is bounded.

In the constrained problem (41) we introduce a dynamic penalty to the objective function. Let us first introduce the following two vectors:

The considered penalty function is defined as:

The optimization problem in (41) becomes the following unconstrained optimization:

| (42) |

A standard approach used when working with dynamic penalty function is to solve a sequence of unconstrained minimization problems:

| (43) |

where the penality coefficient at each iteration increases, i.e. (see Eiben and Smith, 2003, for more details). The algorithm stops when , for a fixed small . In this paper we choose a different method where at each iteration of the Nelder and Mead (1965) algorithm the penalty in (42) is updated according to:

In this way instead of solving a sequence of problems defined in (43) we have only one problem to solve.

4.1 Numerical Example

In the previous Section we introduced a methodology for the estimation of a multivariate MixedTS distribution based on the minimization problem in (42). The integral in the objective function is computed through Monte Carlo simulation based on the following approximation:

| (44) |

where with

are extracted from a multivariate Standard Normal and refers to the

numbers of points used in the evaluation of integral.

We investigate the behavior of the estimators for implementing the following steps:

-

1.

We generate a sample of size from a bivariate and a trivariate MixedTS distributions.

-

2.

Using a boostrap technique with replacement we draw samples of size .

-

3.

For each boostrapped sample we estimate the parameters by solving problem (42).

- 4.

| true | est | median | sd | I quart | III quart | |

|---|---|---|---|---|---|---|

| 0.0000 | 0.0213 | 0.0042 | 0.0285 | -0.0175 | 0.0266 | |

| 0.0000 | -0.0057 | 0.0089 | 0.0214 | -0.0061 | 0.0225 | |

| 1.0000 | 1.0608 | 1.0617 | 0.2278 | 0.9876 | 1.2024 | |

| 1.5000 | 1.3968 | 1.4312 | 0.1988 | 1.2682 | 1.5173 | |

| 1.2000 | 1.2390 | 1.2829 | 0.2387 | 1.1505 | 1.4599 | |

| 1.0000 | 1.0955 | 1.1601 | 0.3139 | 1.0277 | 1.3648 | |

| 1.0000 | 1.1865 | 1.1889 | 0.3210 | 1.0180 | 1.4203 | |

| 0.0000 | 0.0049 | 0.0000 | 0.0316 | -0.0267 | 0.0288 | |

| 0.0000 | 0.0084 | -0.0052 | 0.0260 | -0.0249 | 0.0152 | |

| 1.0000 | 1.0588 | 1.0000 | 0.1599 | 0.9287 | 1.0881 | |

| 1.5000 | 1.4028 | 1.4604 | 0.1644 | 1.3526 | 1.5412 | |

| 0.8000 | 0.8059 | 1.0422 | 0.1896 | 0.9022 | 1.1949 | |

| 1.0000 | 1.1884 | 1.0064 | 0.3171 | 0.8367 | 1.2124 | |

| 1.0000 | 1.1774 | 0.9770 | 0.2698 | 0.8436 | 1.1393 | |

| 0.5000 | 0.5146 | 0.5884 | 0.2546 | 0.4295 | 0.7542 |

| true | est | median | sd | I quart | III quart | |

|---|---|---|---|---|---|---|

| 0.0 | -0.0109 | -0.0003 | 0.0148 | -0.0276 | 0.0231 | |

| 0.0 | 0.009 | 0.0037 | 0.0124 | -0.0195 | 0.0227 | |

| 1.0 | 0.874 | 1.0079 | 0.0920 | 0.9149 | 1.1898 | |

| 1.5 | 1.589 | 1.4728 | 0.0973 | 1.2910 | 1.6037 | |

| 1.2 | 1.293 | 1.2082 | 0.1220 | 1.0204 | 1.4252 | |

| 1.0 | 1.137 | 1.1434 | 0.1621 | 0.9317 | 1.4400 | |

| 1.0 | 1.036 | 1.1609 | 0.1709 | 0.9106 | 1.4735 | |

| 0.0 | -0.030 | 0.0030 | 0.0164 | -0.0260 | 0.0297 | |

| 0.0 | 0.0038 | 0.0059 | 0.0123 | -0.0149 | 0.0261 | |

| 1.0 | 1.1012 | 0.9989 | 0.0795 | 0.8709 | 1.1389 | |

| 1.5 | 1.3658 | 1.4504 | 0.1045 | 1.2822 | 1.6287 | |

| 0.8 | 0.9922 | 0.8842 | 0.0793 | 0.7857 | 1.0449 | |

| 1.0 | 1.2896 | 1.0929 | 0.1385 | 0.8728 | 1.3232 | |

| 1.0 | 0.9882 | 1.0910 | 0.1405 | 0.8613 | 1.3337 | |

| 0.0 | -0.0170 | 0.0009 | 0.0185 | -0.0310 | 0.0293 | |

| 0.0 | 0.0145 | 0.0005 | 0.0157 | -0.0252 | 0.0278 | |

| 1.0 | 1.0590 | 1.0122 | 0.0915 | 0.8903 | 1.1881 | |

| 1.5 | 1.4448 | 1.4924 | 0.0994 | 1.3272 | 1.6502 | |

| 1.8 | 1.8683 | 1.8181 | 0.1163 | 1.5877 | 1.9538 | |

| 1.0 | 1.2061 | 1.2104 | 0.1876 | 0.9789 | 1.5956 | |

| 1.0 | 1.1152 | 1.2462 | 0.1877 | 1.0229 | 1.6222 | |

| 0.5 | 0.5177 | 0.5414 | 0.1168415 | 0.3591 | 0.7435 |

5 Conclusion

We introduced a new infinitely divisible distribution called multivariate MixedTS. This new distribution is a generalization of the Normal Variance Mean Mixtures. The flexibility of the multivariate MixedTS distribution is emphasized by means of a direct comparison with the multivariate Variance Gamma, which is a competing model that presents some limits. The multivariate Variance Gamma distribution is not able to capture the dependence structure between components of a random vector, which is important if we work with financial markets data. We showed that using the multivariate distribution these limits are overcome, which is due to the presence of the tempering parameters. Taking into account the structure of the new distribution we propose a simulation procedure which exploits the existence of algorithms in literature for the simulation of the Tempered Stable distribution. We also propose an estimation procedure, based on the minimization of a distance between the empirical and theoretical characteristic functions. Results on asymptotic tail behavior of marginals are used as constraints, in the optimization problem, in order to improve tail fitting. Capturing the dependence of extreme events is helpful in many areas such as in portfolio risk management, in reinsurance or in modeling catastrophe risk related to climate change. The proposed estimation procedure is illustrated through a numerical analysis on simulated data from a bivariate MixedTS. We estimate parameters on bootstrapped samples and investigate their empirical distribution. Finally, some remarks on possible future research starting from this paper are listed below. One can study the multivariate MixedTS considering other mixing distributions, rather than Gamma. Empirical investigation on the ability of the proposed distribution in fitting the data in different fields would also be of interest. Another important issue would be the study of the efficiency of the estimators resulting from the proposed estimation methodology.

References

- Barndorff-Nielsen et al. (1982) Barndorff-Nielsen, O., J. Kent, and M. Sørensen (1982). Normal variance-mean mixtures and z distributions. International Statistical Review, 145–159.

- Benaim and Friz (2008) Benaim, S. and P. Friz (2008). Smile asymptotics II: models with known MGF. J. Appl. Probab 45, 16–32.

- Bianchi et al. (2016) Bianchi, M. L., G. L. Tassinari, and F. J. Fabozzi (2016). Riding with the four horsemen and the multivariate normal tempered stable model. International Journal of Theoretical and Applied Finance 19(04), 1650027.

- Boas (2006) Boas, M. L. (2006). Mathematical methods in the physical sciences; 3rd ed. Hoboken, NJ: Wiley.

- Carrasco and Florens (2000) Carrasco, M. and J.-P. Florens (2000). Generalization of GMM to a continuum of moment conditions. Econometric Theory 16(06), 797–834.

- Cont and Tankov (2004) Cont, R. and P. Tankov (2004). Financial modelling with jump processes. Chapman & Hall/CRC, Boca Raton, FL.

- Eiben and Smith (2003) Eiben, A. E. and J. E. Smith (2003). Introduction to evolutionary computing, Volume 53. Springer.

- Feuerverger and McDunnough (1981) Feuerverger, A. and P. McDunnough (1981). On the efficiency of empirical characteristic function procedures. Journal of the Royal Statistical Society. Series B (Methodological), 20–27.

- Giaquinta and Modica (2003) Giaquinta, M. and G. Modica (2003). Mathematical Analysis: Functions of One Variable. Number v. 1 in Mathematical analysis. Birkhäuser Boston.

- Hitaj and Mercuri (2013a) Hitaj, A. and L. Mercuri (2013a). Hedge fund portfolio allocation with higher moments and mvg models. Advances in Financial Risk Management: Corporates, Intermediaries and Portfolios, 331–346.

- Hitaj and Mercuri (2013b) Hitaj, A. and L. Mercuri (2013b). Portfolio allocation using multivariate variance gamma models. Financial markets and portfolio management 27(1), 65–99.

- Hitaj et al. (2015) Hitaj, A., L. Mercuri, and E. Rroji (2015). Portfolio selection with independent component analysis. Finance Research Letters. To appear.

- Kaishev (2013) Kaishev, V. K. (2013). Lévy processes induced by dirichlet (b-) splines: Modeling multivariate asset price dynamics. Mathematical Finance 23(2), 217–247.

- Kim et al. (2008) Kim, Y. S., S. T. Rachev, M. L. Bianchi, and F. Fabozzi (2008). Financial market models with Lévy processes and time-varying volatility. Journal of Banking & Finance 32(7), 1363–1378.

- Kozubowski et al. (1997) Kozubowski, T. J., K. Podgórski, and G. Samorodnitsky (1997). Tails of Lévy measure of geometric stable random variables.

- Küchler and Tappe (2013) Küchler, U. and S. Tappe (2013). Tempered stable distributions and processes. Stochastic Processes and their Applications 123, 4256–4293.

- Madan and Seneta (1990) Madan, D. and E. Seneta (1990). The variance gamma (V.G.) model for share market returns. Journal of Business 63, 511–524.

- Mercuri and Rroji (2016) Mercuri, L. and E. Rroji (2016). Option pricing in an exponential mixedts lévy process. Annals of Operations Research, 1–22.

- Nelder and Mead (1965) Nelder, J. A. and R. Mead (1965). A simplex method for function minimization. Computer Journal 7, 308–313.

- Rroji and Mercuri (2015) Rroji, E. and L. Mercuri (2015). Mixed Tempered Stable distribution. Quantitative Finance 15, 1559–1569.

- Semeraro (2008) Semeraro, P. (2008). A multivariate variance gamma model for financial applications. International Journal of Theoretical and Applied Finance 11(01), 1–18.

- Yu (2004) Yu, J. (2004). Empirical characteristic function estimation and its applications. Econometric Reviews 23(2), 93–123.

Appendix A Derivation of higher order moments

For the general element of the random vector , the mean is obtained as:

From the tower property applied to the conditional expected value we get:

Observe that is a standardized Tempered Stable, from where we have:

and since

First we consider the diagonal elements of the variance-covariance Matrix. For the component of the random vector we have:

Applying the binomial formula we rewrite as:

The linearity property of the expected value allows the identification of three terms:

We observe that the first term is related to the variance of the component of the mixing random vector . Using the tower property, the second term becomes the expected value of while the last expected value is zero.

The covariance between the and elements of the random vector is obtained as:

Notice that the first term is related to the covariance between the component of the mixing random vector . The last equality comes from the condition:

Applying the tower property, we have:

We recall that the random variables and are independent for and therefore:

Finally we compute the covariance :

We now compute the term of the skewness-coskewness matrix:

Using the Newton formula we obtain:

where using the tower property and the mean of a standardized Tempered Stable we get:

while

The quantity is the third moment of the MixedTS and can be computed as:

Therefore:

We derive the formula for the central comoments . The first terms is the fourth central moment of the univariate MixedTS distribution:

Using the binomial formula we have:

Using the conditional Tempered Stable assumption we have:

Appendix B Derivation of the multivariate MixedTS characteristic function

Let be a multivariate MixedTS, its characteristic function is:

| (45) |

Substituting in 45 the components defined in (28) we have:

| (46) |

Applying freezing property for the expected value and considering the conditional expected value with respect to the field defined as :

| (47) |

Using the condition in (32) and measurable with respect to the field we obtain:

| (48) |

Since and indicating with the characteristic exponent of the Standardized Classical Tempered Stable, we obtain:

| (49) |

Recalling that as in (29) and using and for the logarithm of the m.g.f. of and , we obtain the result in (34)