ALEA020150000

Distributional properties and parameters estimation of GSB Process: An approach based on characteristic functions

Abstract.

A general type of a Split-BREAK process with Gaussian innovations (henceforth, Gaussian Split-BREAK or GSB process) is considered. The basic stochastic properties of the model are studied and its characteristic function derived. A procedure to estimate the parameter of the GSB model based on the Empirical Characteristic Function (ECF) is proposed. Our simulations suggest that the proposed method performs well compared to a Method of Moment procedure used as benchmark. The empirical use of the GSB model is illustrated with an application to the time series of total values of shares traded at Belgrade Stock Exchange.

Key words and phrases:

GSB process, STOPBREAK process, Noise Indicator, Split–MA process, Empirical characteristic function estimation.2010 Mathematics Subject Classification:

62M10, 91B84, 65D30.1. Introduction

The so-called STOchastic Permanent BREAKing (STOPBREAK) process, firstly introduced by Engle and Smith (1999), was successfully used in modeling time series with “large shocks”, which have permanent, emphatic fluctuations in their dynamics. After this initial contribution, the STOPBREAK notion has been considered by several authors. For instance, in Diebold (2001) or Gonzalo and Martinez (2006) some modifications of the STOPBREAK process were discussed, while Huang and Fok (2001) and Kapetanios and Tzavalis (2010) investigated applications of the processes of this type. Finally, some new extensions in modeling structural breaks and “large shocks” in empirical time series dynamics can be found, for instance, in Dendramis et al. (2014, 2015) or Hassler et al. (2014). In those papers, different empirical applications of STOPBREAK-based models were investigated: economic stability of the oil market, relationships between daily closing market indexes of different countries, etc.

Stojanović et al. (2011, 2014, 2015) proposed an extension of the STOPBREAK process, where the so-called noise threshold indicator was set. The model obtained in this way, named the Split-BREAK process, represents a generalization of the basic STOPBREAK process, but also includes, in some special cases, other well-known time series models (see the following Section). In this paper, the Gaussian distribution of the innovations of Split–BREAK process is assumed, and this process was named the Gaussian Split-BREAK GSB process. A brief theoretical background, i.e., a definition and the basic stochastic properties of the process, are given in Section 2. The main results of the paper are presented in the sections to follow. In Section 3, we pay a special attention to the series of increments, named the Split–MA process. First of all, a general explicit expression of an arbitrary order characteristic functions (CFs) of this process is given. Based on this, we investigate some distributional properties of the Split-MA process. In Section 4, we consider an estimation procedure of the Split-MA process parameters, using the Empirical Characteristic Functions ECF technique. In the same section, we also study the asymptotic properties of these estimators. The numerical simulations of the ECF estimators are considered in Section 5. An application of the GSB process and the ECF estimation procedure in modeling the dynamics of the total values of shares trading on Belgrade Stock Exchange are described in Section 6. Finally, some conclusions are presented in Section 7.

2. GSB process. Definition and main properties

To begin with, we define a general form of the GSB process, as well as its basic stochastic properties.

Definition 2.1.

Let , with be a time series of random variables on some probability space . Let be a filtration and denote by a sequence of independent identical distributed (i.i.d.) Gaussian random variables, adapted to the filtration . We say that series obeys a Gaussian Split-BREAK process, if and only if it satisfies

| (2.1) |

where

| (2.2) |

is the Noise Indicator of the (previous) realizations of , , , , and is a back–shift operator.

Notice that, according to (2.2),

i.e. the sequence is a martingale difference, as in the basic STOPBREAK model. Moreover, the values of the series determine the amount of participation of the previous elements of innovations in the series . The level of realizations of the innovations which will be statistically significant to be included in (2.2) was determined with the parameter . In that way, the GSB process varies between the well known linear stochastic models (see, for more details Stojanović et al., 2014, 2015). In the dependence of and we have, for instance, the following processes:

Subsequently, we suppose that and when the model (2.1) has the form

| (2.3) |

where and satisfy the non–triviality condition . Thus, the representation (2.3) can be considered as a specific non-linear ARMA model with the “temporary” components , which imply the specific structure of the GSB process. It was proven in Stojanović et al. (2014) that the necessary and sufficient conditions of strong stationarity of the series are that the zeros of the polynomial satisfy the conditions , , i.e., that inequality holds. In this case, the mean of the GSB series is , and its covariance function satisfies recurrence relation

where

On the other hand, similarly to the basic STOPBREAK process, the equality (2.3) enables the additive decomposition where

is a sequence of random variables, called as the martingale means. In this way, the series represents a generalization of an analogue series in Engle and Smith (1999). It can be easily shown that satisfies the same stationarity conditions as the series . Moreover, regardless to stationary of the series and , it follows

| (2.4) |

and based on that, we have . In a similar way, the variance of GSB process can be obtained. According to the equality

| (2.5) |

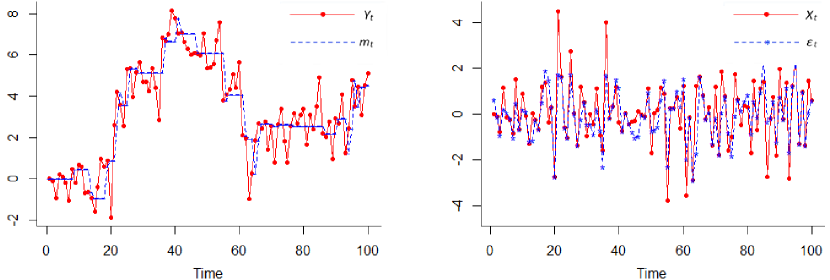

the conditional variance of is constant and equal to the variance of , and the variances of and satisfy the relation . Note that the equalities (2.4) and (2.5) can explain the stochastic behavior of the series . Namely, the sequence is predictable, and it represents a stability component of the process . On the other hand, realizations of the innovations represent the random fluctuations around the values (see Figure 2.1, left).

We next describe the stochastic structure of another time series, the so–called increments , . According to (2.3), this series can be written as

| (2.6) |

Therefore, has the multi-regime structure, depending on the realizations of indicators . If all squared innovations are sufficiently large (i.e. greater than ), an increment will be equal to . On the other hand, squared innovations, which do not exceed the critical value , produce a “part of” MA representation of the series (Figure 2.1, right). Due to this, is named the Gaussian Split-MA model of order p, or simply the Split-MA model.

Note that is a stationary process, with the mean and the covariance

| (2.7) |

In Stojanović et al. (2014) it was shown that the process is invertible if and only if the zeros , , of the polynomial meet the condition , , i.e., the inequality holds. Then,

| (2.8) |

where

| (2.9) |

Stojanović et al. (2014) proved that the representation is almost surely unique, as well as that the sum on the right side converges with the probability one and in the mean–square.

According to the aforementioned facts, the conditions of invertibility of increments are weaker than the stationary conditions of the series and . This is particularly interesting in the case of the so–called integrated standardized time series, where Further, we take into consideration time series of this type, for the following reasons:

(i) In this case, the series and are non–stationary processes, with the non–zero mean. These properties are typical in dynamics of the time series with “large shocks”, as well as in their practical applications.

(ii) If the parameter takes a non–trivial values, i.e., , the series will be stationary and invertible. Then, the whole estimation procedure of unknown parameters, as we see further, will be based just on its realizations.

(iii) Finally, the assumption is fully in line with the definition of basic STOPBREAK process in Engle and Smith (1999), where .

Figure 2.1 illustrates the dynamics of the kind of time series defined above, in the case of the simplest, the GSB(1) and Split-MA(1) processes, where the model’s parameters are .

3. Distributional properties of Split–MA process

In this section, we consider some distributional properties of increments . For this purpose, we define the parameter vector . Note that the critical value can be easily obtained as , where is the cumulative distribution function (CDF) of distributed random variable. We now introduce the following definition:

Definition 3.1.

Let and , , be the overlapping blocks of the process . The –dimensional CF of the random vector is

| (3.1) |

The following statement gives an explicit expression of the CF of Split–MA process.

Theorem 3.2.

Let be the Split-MA(p) process defined by . Then, CF of the order of the random process is given by

| (3.2) | |||||

where and , , .

Proof.

According to the definition of the Split–MA process, as well as the CF (3.1), it is valid that , where

and, for an arbitrary , we denote . As the random variables and are independent, it follows that , and , . Thus, is a series of uncorrelated random variables, with the CF

| (3.3) |

where and are the CDFs of the random variables and , respectively. As appropriate CFs of these random variables are and , a substitution in (3.3) gives

| (3.4) |

According to this, it is obvious that , and the CF can be rewritten in the form

The last equality and Eq.(3.4) imply Eq.(3.2), i.e., complete the proof of this theorem. ∎

Remark 3.3.

According to the previous theorem, the first two orders CFs of are

| (3.5) | |||||

respectively, where .

The CFs in Eqs.(3.5)–(3.3) can be used to study the stochastic properties of the series and for parameters estimation. Note that the first order CF (3.5) and Levy’s convergence theorem immediately imply:

Corollary 3.4.

The CDF of the random variables , is

where denotes the convolution operator and , , are the CDFs of the random variables with the Gaussian distribution .

Moreover, the following proposition gives a recurrence relation for moments of the Split–MA process.

Theorem 3.5.

For an arbitrary , the Split–MA processs has the finite -th moment

where ,

and is a sequence of algebraic polynomials defined by the generating function

Proof.

Let us denote , where , . According to Leibniz’s formula, the -th derivative of the CF can be written as

Since and , , we conclude that and . Furthermore, one can easily prove that

for each On the other hand, for the derivatives of even orders we have

i.e.,

| (3.7) |

where we set and . Using the induction method, it can be proven that

Then, substituting in (3.7) and using that , the statement of this theorem follows immediately. ∎

Remark 3.6.

According to Theorem 3.5, we can simply obtain the kurtosis

It is obvious that the equality holds if and only if

| (3.8) |

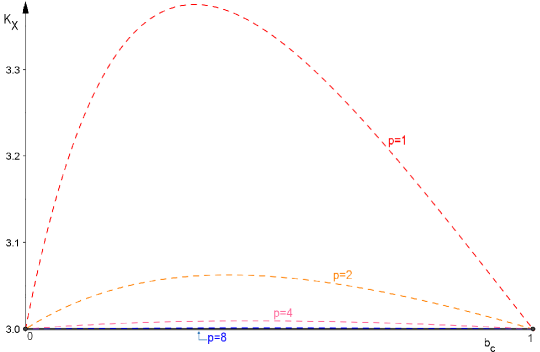

In the first case, the Split–MA model is reduced (almost surely) to the linear MA model, while the other two cases give the Gaussian innovations . Thus, (3.8) represents the necessary and sufficient conditions for the process to have a Gaussian distribution. In general, for the non–trivial values and under previously assumed condition , it will be . Then, the random variables have a non–Gaussian distribution “peaked” at . However, the higher order Split–MA processes approximately have the Gaussian distribution, under condition

Typical situation of this kind can be seen in Figure 3.2, where the kurtosis of the Split–MA processes, as the functions of , and with equidistant coefficients , , are shown. In this case, after some simple computations, we find that

In a more precise manner, the following statement provides some sufficient conditions for the asymptotic normality of the Split–MA process of infinite order.

Theorem 3.7.

Let , , be the Split–MA process, with and for the infinite number of . If for any the condition

holds, then the random variables have the Gaussian distribution , where .

Proof.

Similarly to the proof of Theorem 3.2, denote , . Hence, the equalities and hold. According to

it follows Therefore, the sum converges almost surely, i.e., the process is well defined.

Further on, for an arbitrary , denote , , and . We then have

i.e. Lyapunov’s condition holds. Thus, , , and according to this, it is easy to obtain the statement of this theorem. ∎

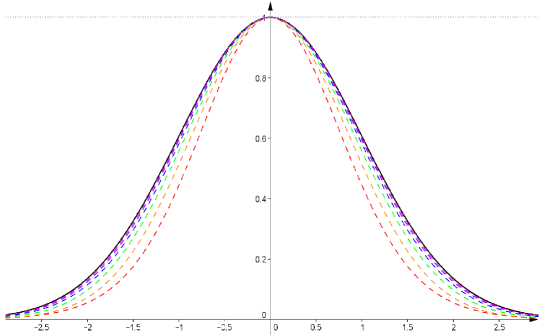

The previous theorem shows that probability distributions of the large–order Split–MA processes, with “small variation” of coefficients , can be approximated with a Gaussian distribution. The CF of the standard Gaussian distribution is shown in Figure 3.3, and compared to the CFs of Split–MA processes with the equidistant coefficients , where , and . In this case, it is obvious that , and therefore, a normal approximation of distributions of the Split–MA series of larger order is valid. On the other hand, it is clear that the Split–MA models with a “small” order have a pronounced “peaked” distribution, that significantly differs from the Gaussian one. Therefore, in addition to the general model, we will further investigate, in more details, an estimation procedure of the simplest Split–MA process, when .

4. Estimations of parameters by the ECF method

Parameters estimation procedure of the standard STOPBREAK model, introduced by Engle and Smith Engle and Smith (1999), was mainly based on the quasi–maximum likelihood (QML) method. In case of the Split–BREAK model, it can be proven that the likelihood function is unbounded at the origin, and it disables the usage of the QML, as well as some closely related methods, based on the maximum likelihood approach. For these reasons, Stojanović et al. (2011, 2015) have used some distributional independent estimation methods, that were based on two typical non–parametric procedures: methods of moments and Gauss–Newton’s regression for non-linear functions. However, the main problem in realization of these procedures is non-observability of the Split–MA process , for .

Here we describe the new parameters estimation procedure for this process, based on the Empirical Characteristic Function (ECF) method. In the time series analysis, this method was described for the first time in Feuerverger (1990), as well as in Knight and Satchell (1996, 1997). After that, several authors (cf. Singleton, 2001; Knight et al., 2002; Knight and Yu, 2002) described implementation of the ECF method in econometric analysis and finance. On the other hand, several other new theoretical extensions of the CF–based estimators can be found, for instance in Balakrishnan et al. (2013) and Kotchoni (2012, 2014). Here we apply a similar procedure as in parameters estimation of the so–called Split–SV model, described in Milovanović et al. (2014) and Stojanović et al. (2016).

The main aim of the ECF method is to minimize “the distance” between the theoretical CF and the appropriate ECF of some stochastic model. In case of the Split–MA process we denote as a realization of the series of length . Then the appropriate -dimensional ECF of the random sample is

and the objective function is

| (4.1) |

where is the CF of order , defined by Eq. (3.1), and is a some weight function. The estimates based on the ECF method are thus obtained by a minimization of the objective function (4.1) with respect to the parameter . More precisely, they represent the solutions of the minimization equation

| (4.2) |

where is the parameter space of the non–trivial, stationary and invertibile Split–MA process. One of the important problems here is the choice of block size . We refer to Knight and Yu (2002), where the optimal values of were discussed in order to achieve asymptotic efficiency of the ECF estimators for some linear Gaussian time series. Similarly to them, we investigate the strong consistency and asymptotic normality (AN) of the ECF estimates of Split–MA model’s parameters, under certain necessary conditions.

Theorem 4.1.

Let be the true value of the parameter , and for an arbitrary , let be solutions of the equation . In addition, let us suppose that the following regularity conditions are fulfilled:

-

(i)

There exists the set , where is chosen sufficiently large so that for all ;

-

(ii)

is a regular matrix;

-

(iii)

is a non-zero matrix, uniformly bounded by the strictly positive, -integrable function .

Then, is strictly consistent and asymptotically normal estimator for , for any .

Proof.

In order to prove the consistency of , we check the sufficient consistency conditions of extremum estimators (see, for instance Newey and McFadden, 1994). Note that, under assumption (i), the set is a compact, and . As the series is ergodic and is an unbiased estimator of , the strong law of large numbers gives , and hence , when .

Further, if we define the function

then, according to Eq.(3.2), it is obvious that is continuous on . Using the same deliberation as in case of the standard MA processes (see, for instance Yu, 2004), it is easy to see that, under assumption , the equality holds only if . Thus, has an unique minima at the true parameter value, and in the same way as in Knight and Yu (2002), it can be proven that

Hence, , , i.e., uniformly converges almost surely to . Consequently, according to Theorem 2.1 in Newey and McFadden (1994), , when i.e., the estimator is strictly consistent.

In order to show the AN, note that the function has continuous partial derivatives up to the second order, for any component of the vector . Thus, the Taylor expansion of at gives

For a sufficiently large , we substitute by , under assumption (ii) and the fact that . Then we have

According to the mentioned properties of the function , it can be differentiated under the integral sign, e.g.,

| (4.3) |

and

| (4.4) | |||||

| (4.5) |

where

Under assumption (iii), the inequalities hold, and consequently

| (4.6) |

Now, we write the gradient of as

where It can then be shown (see, for instance Yu, 2004) that the finite non–zero limit

exists if the series , , has the finite and non–zero sum. In case of the Split-MA model, according to Eq.(2.7), we have

According to this, it is obvious that for the non–trivial values , the inequalities hold for each . By applying the central limit theorem for stationary processes, we obtain

and this convergence and Eqs.(4.5)–(4.6) imply

This completes the proof of the Theorem. ∎

Remark 4.2.

The assumption (i) of the previous theorem ensures the compactness of the parameters set, and it is necessary to provide the strong consistency of the ECF estimates of Split–MA model’s parameters. On the other hand, assumptions (ii) and (iii) enable that regular random matrices converge almost surely to the non-zero finite matrix , when . In this way, these two assumptions are necessary for AN of the ECF estimates. Note that all these assumptions are weaker than the general regularity conditions of ECF estimators (see, for instance Knight and Yu, 2002). Hence, they can be satisfied in most applications of the GSB process.

Remark 4.3.

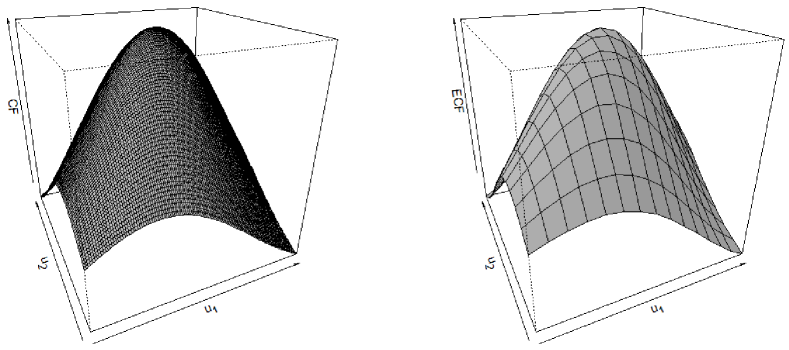

According to the proof of the previous theorem, continuous function , providing that , attains the unique minimum at . This is the so-called identification condition, which holds if the order of the CF of Split–MA model is at least equal to the number of its parameters. As we mentioned before, we consider the simplest model of the Split–MA process, when and . Hence, we use the CF of order , i.e., the ECF procedure based on two–dimensional random vector . Note that, in this case, the objective function represents a double integral with respect to the weight function . Therefore, as we will see later on, it can be numerically approximated by using some cubature formulas. In addition, we give an explicit expression of the two–dimensional CF of in Eq.(3.3). As it can be seen, this function takes only real values, and the following real–valued function

may be used as its empirical estimate. Figure 4.4 illustrates the graphs of two–dimensional CF , as well as the appropriate ECF , when and .

5. Numerical simulations of the ECF estimates

5.1. Simulating the Split–MA process

In the first part of this Section, we present the pseudo algorithm intended to simulate the Split–MA(1) model, as well as to compute its initial parameters’ estimates. It is based on 1 000 independent Monte Carlo replications of our model, i.e., the 1 000 independent realizations of the series

where and . We consider two different simple sizes, (large sample) and (small sample). This is primarily to show that convergence

implies that the procedure of parameters estimation of the Split–MA(1) model can be applied in the case of short time series (see Stojanović et al., 2011, pp. 57). Naturally, the number of observations () implies the different values of the appropriate estimation errors, which will be also investigated.

In the first estimation step, we have computed the estimates obtained by the method of moments. The autocorrelation function of the Split-MA(1) process is given by

| (5.1) |

and as the estimates of we used the statistic where is the empirical first correlation of . Note that the inequalities hold if and only if . After that, according to Eq.(2.7), the estimate of the can be computed as , where is the empirical variance of . Finally, by solving the equation with respect to , we obtain the estimate of the critical value , where is the CDF of distributed random variable. Using some well-known facts about the continuity of the stochastic convergences (cf. Serfling, 1980, pp. 24,118), the strong consistency and asymptotic normality of the mentioned estimates can be proven (see, for more details Stojanović et al., 2011). In the following part, we describe in detail the ECF procedure for parameters estimation of the Split–MA model, and we also compare its efficiency with the estimates obtained by the method of moment.

5.2. Computing the ECF–based estimator

As we mentioned above, the ECF estimation procedure of the parameters of Split–MA(1) process is based on the minimization of the following double integral

| (5.2) |

with respect to the weight function . In our investigation, some typical exponential weight functions are considered. These functions put more weights around the origin, which is in accordance with the fact that CF in this point contains the most of information about the probability distribution of estimated model. On the other hand, exponential weights have a numerical advantage, because the integral in (5.2) can be numerically approximated by using some -point cubature formula

| (5.3) |

where are the cubature nodes and are the corresponding weight coefficients.

A particular problem here is a choice of the weight function . For this purpose, we consider the weight functions , where . For all of these weights we use a product cubature formula based on the one-dimensional Gauss-Radau formula (cf. Mastroianni and Milovanović, 2008, pp. 329–330 or Milovanović, 2015) with respect to an exponential weight on . Namely, introducing the polar coordinates and , the integral in (5.3) is reduced to

| (5.4) |

where is given by

| (5.5) |

The integral (5.5) can be approximated by the composite trapezoidal rule in points , , as

Using the nodes after certain transformations, can be represented in the form

In this way, we obtain the cubature formula

where are weights of the one–dimensional -point Gauss–Radau formula

On the other hand, the nodes are zeros of the polynomial orthogonal on with respect to the exponential weight function . In our calculations we use with nodes (, ). The numerical construction of the Gauss-Radau formulas can be done by the Mathematica package ‘‘OrthogonalPolynomials’’, for an arbitrary number of points (see, for more details Cvetković and Milovanović, 2004; Milovanović and Cvetković, 2012).

After numerical construction of cubature rules, the objective function (5.2) is minimized by a Nelder-Mead method, and the estimation procedure is realized by the original authors’ codes written in statistical programming language “R”. The estimates obtained by the method of moments were used as the initial estimated values, and the performance of these and ECF estimates was examined in case of the simplest, Split-MA model. For a true value of the parameter it was chosen the vector , where .

5.3. Simulations Results

We apply the ECF method, with the initial values that were obtained by the previously described method of moments estimation procedure. In this way, we compute the ECF estimates of parameters of the Split–MA model. Their summarized values, i.e. the true parameter values (TRUE), averages of estimated parameters (MEAN), together with their minimums (MIN), maximums (MAX), bias (BIAS) and the corresponding root mean squared errors (RMSE), are set in rows of the Tables 5.1 and 5.2. In the first (numerical) column of both Tables there are the estimated values of the initial estimates, obtained by the method of moments. The following three columns contain the estimated parameters’ values obtained by the ECF procedures, with respect to the weights , . As it can be seen, in comparison to initial estimates, the ECF estimates have a smaller estimation errors. Also, the averages of the ECF estimates of the all estimated parameters are close to their true values.

| Parameters | Initial | ECF estimates/weights | |||

|---|---|---|---|---|---|

| estimates | |||||

| TRUE | 0.6827 | 0.6827 | 0.6827 | 0.6827 | |

| MIN | 0.2661 | 0.4093 | 0.3999 | 0.5131 | |

| MEAN | 0.6781 | 0.6867 | 0.6865 | 0.6859 | |

| MAX | 0.9962 | 0.9065 | 0.9967 | 0.8959 | |

| BIAS | -4.55E-03 | 4.04E-03 | 3.81E-03 | 3.23E-03 | |

| RMSE | 0.1452 | 0.0731 | 0.0888 | 0.0641 | |

| TRUE | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| MIN | 0.3957 | 0.6078 | 0.5696 | 0.5711 | |

| MEAN | 1.0477 | 1.0256 | 1.0282 | 1.0226 | |

| MAX | 1.9911 | 1.5952 | 1.6843 | 1.6893 | |

| BIAS | 4.77E-02 | 2.56-02 | 2.82E-02 | 2.26E-02 | |

| RMSE | 0.2880 | 0.1464 | 0.2291 | 0.1740 | |

| TRUE | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| MIN | 0.6534 | 0.7822 | 0.7641 | 0.8292 | |

| MEAN | 0.9880 | 0.9984 | 0.9963 | 0.9984 | |

| MAX | 1.5151 | 1.2311 | 1.2974 | 1.2128 | |

| BIAS | -1.20E-02 | -1.60E-03 | -3.70E-03 | -1.63E-03 | |

| RMSE | 0.1482 | 0.0680 | 0.0851 | 0.0597 | |

| Sample size: | |||||

| Weights: | , | ||||

| Parameters | Initial | ECF estimates/weights | |||

|---|---|---|---|---|---|

| estimates | |||||

| TRUE | 0.6827 | 0.6827 | 0.6827 | 0.6827 | |

| MIN | 0.5212 | 0.5773 | 0.5494 | 0.5442 | |

| MEAN | 0.6851 | 0.6833 | 0.6841 | 0.6830 | |

| MAX | 0.8686 | 0.8169 | 0.8304 | 0.8028 | |

| BIAS | 2.44E-03 | 6.39E-04 | 1.42E-03 | 2.64E-04 | |

| RMSE | 0.0532 | 0.0406 | 0.0520 | 0.0417 | |

| TRUE | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| MIN | 0.5859 | 0.6532 | 0.7176 | 0.6876 | |

| MEAN | 1.0190 | 1.0117 | 1.0125 | 0.9916 | |

| MAX | 1.5952 | 1.4944 | 1.4601 | 1.4736 | |

| BIAS | 1.90E-02 | 1.17E-02 | 1.25E-02 | -7.42E-03 | |

| RMSE | 0.1886 | 0.1527 | 0.1329 | 0.0847 | |

| TRUE | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| MIN | 0.8375 | 0.8883 | 0.8436 | 0.8836 | |

| MEAN | 1.0012 | 0.9992 | 0.9988 | 0.9996 | |

| MAX | 1.1730 | 1.1131 | 1.1518 | 1.1194 | |

| BIAS | 1.21E-03 | -7.91E-04 | -1.20E-03 | -4.04E-04 | |

| RMSE | 0..0507 | 0.0374 | 0.0489 | 0.0380 | |

| Sample size: | |||||

| Weights: | , | ||||

What follows is an empirical investigation of the asymptotic properties (strong consistency and asymptotic normality) of the parameters’ estimators of our model, which were formally proved in Theorem 4.1. One should remark that in our simulation study, for all of the observed weights, the ECF estimates have a more prominent stability, compared to the appropriate initial estimates. This can be easily seen according to their estimated errors, as well as in Figures 5.5 and 5.6: the initial estimates (panels above), and the ECF estimates with the weights , (panels bellow).

Furthermore, we have obtained some testing results concerning the AN of initial and ECF estimates of our model, which is expected according to Theorem 4.1. For this purpose, we have used Anderson-Darling and Cramer-von Mises tests of normality, which test statistics (labeled as and , respectively), as well as the corresponding –values, are computed by using the appropriate procedures from the R-package “nortest”, authorized by Gross (2013). Additionally, we have used the composite Jarque-Bera (JB) test of normality, with specified number of the Monte-Carlo replications, realized in R-package “normtest” (Gavrilov and Pusev, 2014). These values are shown in Tables 6.5 and 6.6, where one can see that the AN is mostly confirmed for the ECF estimates of parameters and . On the other hand, it varies to a some degree in the case of parameter , as a consequence of the multi–stage estimation procedure of this model’s parameters. Certain confirmations of these facts are also given in the histograms of their empirical distribution, presented in Figures 5.5 and 5.6.

| Parameters | Statistics | Initial | ECF estimates/weights | ||

| estimates | |||||

| 0.8398∗ | 0.6280 | 0.3471 | 0.4576 | ||

| (–value) | (0.0305) | (0.1016) | (0.4794) | (0.2642) | |

| 0.1266∗ | 0.1043 | 0.0822 | 0.0698 | ||

| (–value) | (0.0488) | (0.0980) | (0.1937) | (0.2807) | |

| 7.7128∗ | 5.1060 | 3.6464 | 2.0886 | ||

| (–value) | (0.029) | (0.073) | (0.142) | (0.326) | |

| 2.1285∗∗ | 0.8923∗ | 1.2947∗∗ | 0.8813∗ | ||

| (–value) | (2.07E-05) | (0.0226) | (2.31E-03) | (0.0246) | |

| 0.3517∗∗ | 0.1179 | 0.1722∗ | 0.1640∗ | ||

| (–value) | (8.71E-05) | (0.0639) | (0.0122) | (0.0156) | |

| 22.670∗∗ | 7.6551∗ | 13.350∗∗ | 7.0815∗ | ||

| (–value) | (0.002) | (0.021) | (0.003) | (0.036) | |

| 1.5831∗∗ | 0.3479 | 0.4613 | 0.5573 | ||

| (–value) | (1.02E-04) | (0.4774) | (0.2587) | (0.1199) | |

| 0.2587∗∗ | 0.0396 | 0.0668 | 0.0623 | ||

| (–value) | (1.02E-04) | (0.6898) | (0.3080) | (0.3523) | |

| 19.085∗∗ | 0.6704 | 2.1195 | 0.3181 | ||

| (–value) | (2.E-03) | (0.6860) | (0.310) | (0.836) | |

| Parameters | Statistics | Initial | ECF estimates/weights | ||

| estimates | |||||

| 0.5039 | 0.3845 | 0.6432 | 0.3802 | ||

| (–value) | (0.2037) | (0.3943) | (0.0932) | (0.4025) | |

| 0.0513 | 0.0664 | 0.1138 | 0.0593 | ||

| (–value) | (0.4924) | (0.3118) | (0.0727) | (0.3857) | |

| 7.6025∗ | 0.5500 | 2.7498 | 1.5539 | ||

| (–value) | (0.031) | (0.732) | (0.248) | (0.462) | |

| 0.9288∗ | 0.6048 | 1.0144∗ | 0.7144 | ||

| (–value) | (0.0184) | (0.1159) | (0.0115) | (0.0622) | |

| 0.1517∗ | 0.0898 | 0.1644∗ | 0.1269∗ | ||

| (–value) | (0.0226) | (0.1546) | (0.0154) | (0.0483) | |

| 6.6989∗ | 2.1136 | 6.1157∗ | 4.3429 | ||

| (–value) | (0.042) | (0.334) | (0.048) | (0.103) | |

| 0.3375 | 0.3491 | 0.6819 | 0.3312 | ||

| (–value) | (0.5039) | (0.4745) | (0.0748) | (0.5122) | |

| 0.0555 | 0.0548 | 0.0934 | 0.0410 | ||

| (–value) | (0.4332) | (0.4430) | (0.1384) | (0.6630) | |

| 2.1136 | 1.8737 | 3.1342 | 1.3905 | ||

| (–value) | (0.337) | (0.377) | (0.194) | (0.488) | |

6. Application of the model

In this section, we describe a practical application of the GSB process of order in modelling dynamics of some financial series. For this purpose, we first observed the dynamics of the total values of trading 15 Serbian shares with the highest liquidity, integrated within the so–called BELEX15 financial index (Series A). This index was defined and methodologically processed at the end of September 2005. All its changes until the end of 2014 have been observed here, as the “large” time series with a total of data. On the other hand, the total values of trading by the Minimum Price (MP) method on the Belgrade Stock Exchange (Series B) were also observed. It was chosen as an example of short time series with a total of (only) data.

For both empirical data series (A and B), as a basic financial series we observed the realization of the log–volumes

where are the share prices (in Serbian dinars) and are the volumes of trading, i.e., the number of shares which were traded on a certain day. In this way, the days of trading are used as successive data set , and the estimates of the parameters were obtained from a realization of Split–MA(1) process , where . Estimated parameters’ values from both series, along with the appropriate values of objective function , are shown in the Tables 6.5 and 6.6.

| Parameters | Initial | ECF estimates/weights | ||

|---|---|---|---|---|

| estimates | ||||

| -0.3973 | – | – | – | |

| 0.6591 | 0.5912 | 0.4632 | 0.5366 | |

| 0.5866 | 0.6842 | 0.3815 | 0.5376 | |

| 0.6467 | 0.3752 | 0.4381 | 0.4645 | |

| 1.16E-5 | 1.62E-6 | 1.58E-6 | 8.68E-7 | |

For the initial values of parameters we took the estimates obtained by the method of moments, as in the previous simulations. After that, we obtained the ECF estimates of parameters for the previously described weights , . Note that estimates of the first correlation of both series satisfy the inequality . Thus, according to (5.1), the estimates of the parameter , shown in the next row of both tables, meet (the non-triviality) condition . Also, the estimated values of parameters in the case of “small” Series B are more stable, but they have slightly higher values of estimated errors.

| Parameters | Initial | ECF estimates/weights | ||

|---|---|---|---|---|

| estimates | ||||

| -0.4771 | – | – | – | |

| 0.9123 | 0.8984 | 0.9071 | 0.9258 | |

| 6.7633 | 6.0235 | 6.4595 | 7.5623 | |

| 2.3195 | 2.2468 | 2.2876 | 2.3716 | |

| 2.65E-5 | 4.21E-6 | 4.21E-6 | 2.35E-6 | |

In Figure 6.7 the empirical PDFs of both data series were compared with the PDFs obtained by fitting with the initial estimates, as well as with the ECF estimates of the Split–MA(1) process. As it can be easily seen, in both cases the ECF estimates provide better match to the empirical PDF. Note that the fitted PDF of the Series A (graph on the left) was estimated using the ECF procedure with a usual Gauss-Hermitian cubature, i.e., with the weight function when . On the other hand, in the case of the Series B (graph on the right) cubature with the weight function when was used.

Finally, we explore the possibility of fitting the realizations of series and , as well as to compare them with the empirical series and . For this purpose, we apply the following iterative equations

| (6.1) |

where is the estimate of the critical value , obtained by using the previous ECF procedure, with cubature weight parameter (Series A), and (Series B). On the other hand, we use and as initial values of the iterative procedure (6.1), where is the empirical mean of the series .

A correlation between the log–volumes and the martingale means can also be seen in Figure 6.8 (graph on the left). Obviously, the high correlation of the Series A implies greater fluctuations in the dynamics of martingale means series. In that way, it points to the empathic presence of the “large shocks” in dynamics of the log–volumes. On the other hand, it is obvious that Series B has a slightly more prominent stability and a smaller presence of the emphatic fluctuations in its dynamics. In the same Figure (graphs on the right) graphs of the realizations of the Split–MA(1) process and the innovations are shown.

7. Conclusion

In recent years, various modifications of the STOPBREAK process have been successfully applied to describe dynamics of time series with emphatic and permanent fluctuations. The previous statistical analysis confirms and justifies such a possibility in the case of the GSB process, where the Gaussian distribution for the innovations is assumed. In this paper, the GSB process has been used as a stochastic model in order to describe the behavior of the market capitalizations on the Serbian stock market. However, with certain modifications, this process can also be applied for estimation of similar time series (financial or any other).

Acknowledgements

The authors would like to thank Belgrade Stock Exchange for the consignment of datasets and the constructive information regarding them. Authors are also very grateful to an anonymous referee for pointing out several mistakes in a preliminary version, together with valuable suggestions and comments that have allowed us to improve the paper.

References

- Balakrishnan et al. (2013) N. Balakrishnan, M. R. Brito and A. J. Quiroz. On the goodness-of-fit procedure for normality based on the empirical characteristic function for ranked set sampling data. Metrika 76, 161–177 (2013).

- Cvetković and Milovanović (2004) A. S. Cvetković and G. V. Milovanović. The Mathematica Package “OrthogonalPolynomials”. Facta Univ. Ser. Math. Inform. 19, 17–36 (2004).

- Dendramis et al. (2014) Y. Dendramis, G. Kapetanios and E. Tzavalis. Level shifts in stock returns driven by large shocks. J. Empir. Finance 29, 41–51 (2014).

- Dendramis et al. (2015) Y. Dendramis, G. Kapetanios and E. Tzavalis. Shifts in volatility driven by large stock market shocks. J. Econom. Dynam. Control 55, 130–147 (2015).

- Diebold (2001) F. X. Diebold. Long memory and regime switching. J. Economet. 105 (1), 131–159 (2001).

- Engle and Smith (1999) R. F. Engle and A. D. Smith. Stochastic Permanent Breaks. Rev. Econ. Stat. 81, 553–574 (1999).

- Feuerverger (1990) A. Feuerverger. An efficiency result for the empirical characteristic function in stationary time-series models. Canadian Journal of Statistics 18, 155–161 (1990).

- Gavrilov and Pusev (2014) I. Gavrilov, R. Pusev. Tests for Normality. R package version 1.1, http://CRAN.R-project.org/package=normtest (2014).

- Gonzáles (2004) A. González. A smooth permanent surge process. SSE/EFI Working Paper Series in Economics and Finance 572, Stockholm.

- Gonzalo and Martinez (2006) J. Gonzalo and O. Martinez. Large shocks vs. small shocks (Or does size matter? May be so). J. Econometrics 135, 311–347 (2006).

- Gross (2013) L. Gross. Tests for Normality. R package version 1.0-2, http://CRAN.R-project.org/package=nortest (2013).

- Hassler et al. (2014) U. Hassler, P. M. M. Rodrigues and A. Rubia. Persistence in the banking industry: Fractional integration and breaks in memory. J. Empir. Finance 29, 95–112 (2014).

- Huang and Fok (2001) B. -N. Huang and R. C. W. Fok. Stock market integration-an application of the stochastic permanent breaks model. Appl. Econom. Lett. 8 (11), 725–729 (2001).

- Kapetanios and Tzavalis (2010) G. Kapetanios and E. Tzavalis. Modeling structural breaks in economic relationships using large shocks. J. Econom. Dynam. Control 34 (3), 417–436 (2010).

- Knight and Satchell (1996) J. L. Knight and S. E. Satchell. Estimation of stationary stochastic processes via the empirical characteristic function. Manuscript, University of Western Ontario (1996).

- Knight and Satchell (1997) J. L. Knight and S. E. Satchell. The cumulant generating function estimation method. Econom. Theory 13, 170–184.

- Knight et al. (2002) J. L. Knight, S. E. Satchell and J. Yu. Estimation of the stochastic volatility model by te empirical characteristic function method. Aust. N. Z. J. Stat. 44 (3), 319–335 (2002).

- Knight and Yu (2002) J. L. Knight and J. Yu. Empirical characteristic function in time series estimation. Econom. Theory 18, 691–721 (2002).

- Kotchoni (2012) R. Kotchoni. Applications of the characteristic function-based continuum GMM in finance. Comput. Statist. Data Anal. 56, 3599–3622 (2012).

- Kotchoni (2014) R. Kotchoni. The indirect continuous-GMM estimation. Comput. Statist. Data Anal. 76, 464–488 (2014).

- Mastroianni and Milovanović (2008) G. Mastroianni and G. V. Milovanović. Interpolation Processes – Basic Theory and Applications, Springer Monographs in Mathematics, Springer–Verlag, Berlin–Heidelberg (2008).

- Milovanović (2015) G. V. Milovanović. Construction and applications of Gaussian quadratures with nonclassical and exotic weight function. Stud. Univ. Babeş¸–Bolyai Math. 60, 211–233 (2015).

- Milovanović and Cvetković (2012) G. V. Milovanović and A. S. Cvetković. Special classes of orthogonal polynomials and corresponding quadratures of Gaussian type. Math. Balkanica 26, 169–184 (2012).

- Milovanović et al. (2014) G. V. Milovanović, B. Č. Popović and V. S. Stojanović. An application of the ECF method and numerical integration in estimation of the stochastic volatility models. Facta Univ. Ser. Math. Inform. 29 (3), 295–311 (2014).

- Newey and McFadden (1994) W. K. Newey and D. McFadden. Large sample estimation and hypothesis testing: in Handbook of Econometrics. Vol. 4. Amsterdam: North-Holland (1994).

- Serfling (1980) R. Serfling. Approximation Theorems of Mathematical Statistics, John Wiley & Sons, Inc. (1980).

- Singleton (2001) K. Singleton. Estimation of affine pricing models using the empirical characteristic function. J. Econometrics 102, 111–141 (2001).

- Stojanović et al. (2011) V. Stojanović, B. Popović and P. Popović. The Split-BREAK model. Braz. J. Probab. Stat. 25 (1), 44–63 (2011).

- Stojanović et al. (2014) V. Stojanović, B. Popović and P. Popović. Stochastic analysis of GSB process. Publ. Inst. Math.(Beograd)(N.S.) 95 (109), 149–-159 (2014).

- Stojanović et al. (2015) V. Stojanović, B. Popović and P. Popović. Model of General Split-BREAK process. REVSTAT 13 (2), 145–-168 (2015).

- Stojanović et al. (2016) V. S. Stojanović, B. Č. Popović and G. V. Milovanović. The Split-SV model. Comput. Statist. Data Anal. 100, 560–581 (2016).

- Yu (2004) J. Yu. Empirical Characteristic Function Estimation and Its Applications, Econometric Rev. 23 (2), 93–123 (2004).