The randomised Heston model

Abstract.

We propose a randomised version of the Heston model–a widely used stochastic volatility model in mathematical finance–assuming that the starting point of the variance process is a random variable. In such a system, we study the small-and large-time behaviours of the implied volatility, and show that the proposed randomisation generates a short-maturity smile much steeper (‘with explosion’) than in the standard Heston model, thereby palliating the deficiency of classical stochastic volatility models in short time. We precisely quantify the speed of explosion of the smile for short maturities in terms of the right tail of the initial distribution, and in particular show that an explosion rate of () for the squared implied volatility–as observed on market data–can be obtained by a suitable choice of randomisation. The proofs are based on large deviations techniques and the theory of regular variations.

Key words and phrases:

Stochastic volatility, large deviations, Heston, implied volatility, asymptotic expansion.2010 Mathematics Subject Classification:

60F10, 91G20, 91B701. Introduction

Implied volatility is one of the most important observed data in financial markets and represents the price of European options, reflecting market participants’ views. Over the past two decades, a number of (stochastic) models have been proposed in order to understand its dynamics and reproduce its features. In recent years, a lot of research has been devoted to understanding the asymptotic behaviour (large strikes [8, 9, 13], small / large maturities [24, 25, 26, 49]) of the implied volatility in a large class of models in extreme cases; these results not only provide closed-form expressions (usually unavailable) for the implied volatility, but also shed light on the role of each model parameter and, ultimately on the efficiency of each model.

Continuous stochastic volatility models driven by Brownian motion effectively fit the volatility smile (at least for indices); the widely used Heston model, for example, is able to fit the volatility surface for almost all maturities [33, Section 3], but becomes inaccurate for small maturities. The fundamental reason is that small-maturity data is much steeper (for small strikes)–the so-called ‘short-time explosion’–than the smile generated by these stochastic volatility models (a detailed account of this phenomenon can be found in the volatility bible [33, Chapters 3 and 5]). To palliate this issue, Gatheral (among others) comments that jumps should be added in the stock dynamics; the literature on the influence of the jumps is vast, and we only mention here the clear review by Tankov [49] in the case of exponential Lévy models, where the short-time implied volatility explodes at a rate of for small . To observe non-trivial convergence (or divergence), Mijatović and Tankov [47] introduced maturity-dependent strikes, and studied the behaviour of the smile in this regime.

As an alternative to jumps, a portion of the mathematical finance community has recently been advocating the use of fractional Brownian motion (with Hurst parameter ) as driver of the volatility process. Alòs, León and Vives [2] first showed that such a model is indeed capable of generating steep volatility smiles for small maturities (see also the recent work by Fukasawa [31]), and Gatheral, Jaisson and Rosenbaum [34] recently showed that financial data exhibits strong evidence that volatility is ‘rough’ (an estimate for SPX volatility actually gives ). Guennoun, Jacquier and Roome [36] investigated a fractional version of the Heston model, and proved that as tends to zero the squared implied volatility explodes at a rate . This is currently a very active research area, and the reader is invited to consult [7, 21, 22, 23, 28] for further developments. This is however not the end of the story–yet–as computational costs for simulation are a severe concern in fractional models.

We propose here a new class of models, namely standard stochastic volatility models (driven by standard Brownian motion) where the initial value of the variance is randomised, and focus our attention to the Heston version. The motivation for this approach originates from the analysis of forward-start smiles by Jacquier and Roome [39, 40], who proved that the forward implied volatility explodes at a rate of as tends to zero. A simple version of our current study is the ‘CEV-randomised Black-Scholes model’ introduced in [41], where the Black-Scholes volatility is randomised according to the distribution generated from an independent CEV process; in this work, the authors proved that this simplified model generates the desired explosion of the smile. The Black-Scholes randomised setting where the volatility has a discrete distribution corresponds to the lognormal mixture dynamics studied in [11, 12]. We push the analysis further here; our intuition behind this new type of models is that the starting point of the volatility process is actually not observed accurately, but only to some degree of uncertainty. Traders, for example, might take it as the smallest (maturity-wise) observed at-the-money implied volatility. Our initial randomisation aims at capturing this uncertainty. This approach was recently taken by Mechkov [46], considering the ergodic distribution of the CIR process as starting distribution, who argues that randomising the starting point captures potential hidden variables. One could also potentially look at this from the point of view of uncertain models, and we refer the reader to [29] for an interesting related study. The main result of our paper is to provide a precise link between the explosion rate of the implied volatility smile for short maturities and the choice of the (right tail of the) initial distribution of the variance process. The following table (a more complete version with more examples can be found in Table 1) gives an idea of the range of explosion rates that can be achieved through our procedure; for each suggested distribution of the initial variance, we indicate the asymptotic behaviour (up to a constant multiplier) of the (square of the) out-of-the-money implied volatility smile (in the first row, the function will be determined precisely later, but the absence of time-dependence is synonymous with absence of explosion).

| Name | Behaviours of () | Reference |

|---|---|---|

| Uniform | Equation 4.3 | |

| Exponential() | Theorem 4.11 | |

| -squared | Theorem 4.11 | |

| Rayleigh | Theorem 4.5 | |

| Weibull () | Theorem 4.5 |

The rest of the paper is structured as follows: we introduce the randomised Heston model in Section 2, and discuss its main properties. Section 3 is a numerical appetiser to give a flavour of the quality of such a randomisation. Section 4 is the main part of the paper, in which we prove large deviations principles for the log-price process, and translate them into short- and large-time behaviours of the implied volatility. In particular, we prove the claimed relation between the explosion rate of the small-time smile and the tail behaviour of the initial distribution. The small-time limit of the at-the-money implied volatility is, as usual in this literature, treated separately in Section 4.5. Section 5 includes a dynamic pricing framework: based on the distribution at time zero and the evolution of the variance process, we discuss how to re-price (or hedge) the option during the life of the contract. Finally, Section 6 presents examples of common initial distributions, and numerical examples. The appendix gathers some reminders on large deviations and regular variations, as well as proofs of the main theorems.

Notations: Throughout this paper, we denote the implied volatility of a European Call or Put option with strike and time to maturity . For a set in a given topological space we denote by and its interior and closure. Let , , and . For two functions and , and , we write as tends to if . If a function is defined and locally bounded on , and , define as its generalised inverse. Also define the sign function as . Finally, for a sequence satisfying a large deviations principle as tends to zero with speed and good rate function (Appendix B.1) we use the notation . If the large deviations principle holds as tends to infinity, we denote it by .

2. Model and main properties

On a filtered probability space supporting two independent Brownian motions and , we consider a market with no interest rates, and propose the following dynamics for the log-price process:

| (2.1) |

where , , and are strictly positive real numbers. Here is a continuous random variable, independent of the filtration , for which the interior of the support is of the form for some , with moment generating function , for all , and we further assume that contains at least an open neighbourhood of the origin, namely that belongs to . Then clearly all positive moments of exist. Existence and uniqueness of a solution to this stochastic system is guaranteed as soon as admits a second moment [44, Chapter 5, Theorem 2.9]. Notice that the process is not adapted to the filtration due to the lack of information on in . The process is Markovian, however, with respect to the augmented filtration .

When is a Dirac distribution (), the system (2.1) corresponds to the standard Heston model [37], and it is well known that the stock price process is a -martingale; it is trivial to check that it is still the case for (2.1). Behaviour [51], asymptotics [25, 26, 27], estimation and calibration [4, 51] of the Heston model have been treated at length in several papers, and we refer the interested reader to this literature for more details about it; we shall therefore always assume that .

Remark 2.1.

For any , the tower property for conditional expectation yields

Consider the standard Heston model (), and construct such that . Then, for any time , both random variables (in (2.1) and in the standard Heston model) have the same expectation; however, the randomisation of the initial variance increases the variance by . As time tends to infinity, it is straightforward to show that the randomisation preserves the ergodicity of the variance process, with a Gamma distribution as invariant measure, with identical mean and variance:

For any , let denote the moment generating function (mgf) of :

| (2.2) |

The tower property yields directly

| (2.3) |

where the functions and arise directly from the (affine) representation of the moment generating function of the standard Heston model, recalled in Appendix (A.1).

3. Practical appetiser and relation to model uncertainty

3.1. The bounded support case: a practical appetiser

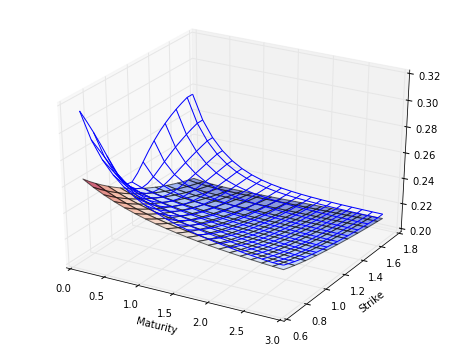

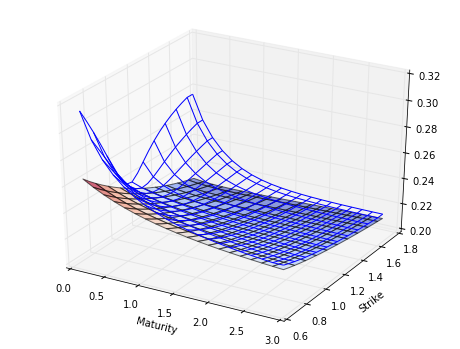

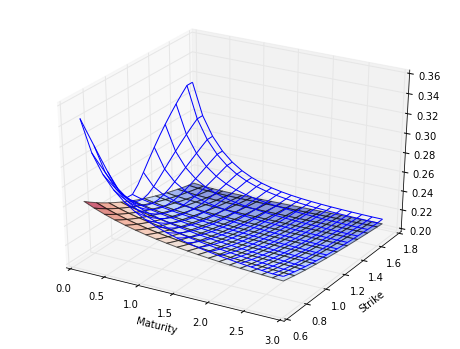

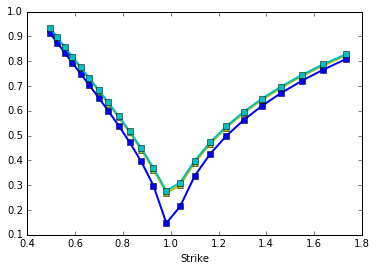

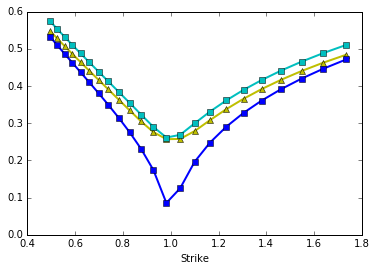

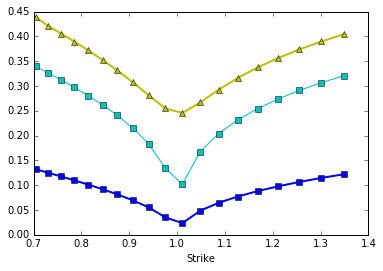

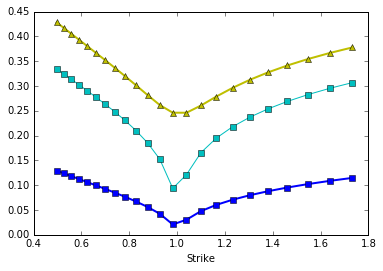

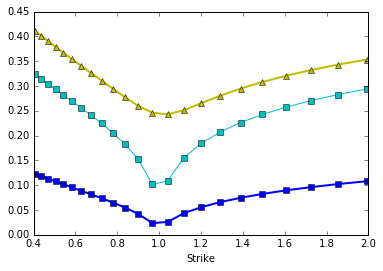

Before diving into the technical statements and proofs of asymptotic results in Section 4, let us provide a numerical hors-d’oeuvre, teasing the appetite of the reader regarding the practical relevance of the randomisation. As mentioned in the introduction, the main drawback of classical continuous-path stochastic volatility models (without randomisation and driven by standard Brownian motions), is that the small-maturity smile they generate is not steep enough to reflect the reality of the market. Graph 1 below represents a comparison of the implied volatility surface generated by the standard Heston model with

and that of the Heston model randomised by a uniform distribution with and . From the trader’s point of view, this could be understood as uncertainty on the actual value of (see also [29] for a related approach). Clearly, the randomisation steepens the smile for small maturities, while its effect fades away as maturity becomes large.

This numerical example intuitively yields the following informal conjecture:

Conjecture 3.1.

Under randomisation of the initial volatility, the smile ‘explodes’ for small maturities.

We shall provide a precise formulation–and exact statements–of this conjecture. Despite the appearances in Figure 1, the conjecture is actually false when the initial distribution has bounded support, such as in the uniform case here. However, as will be detailed in Section 6.1, greater steepness of the smile (compared to the standard Heston model) does appear for a wide range of strikes, but not in the far tails (this is quantified precisely, as well as the at-the-money curvature in the uncorrelated case, in Section 6.1). This leads us to believe that, even if ‘explosion’ does not actually occur in the bounded support case, this assumption may still be of practical relevance given the range of traded strikes.

4. Asymptotic behaviour of the randomised model

This section is the core of the paper, and relates the explosion of the implied volatility smile in small times to the tail behaviour of the randomised initial variance. Section 4.1 (Proposition 4.1) provides the short-time behaviour of the cumulant generating function (cgf) of the random sequence , and relates it to the choice of the initial distribution . This paves the way for a large deviations principle for the sequence . Section 4.2 concentrates on the case where both and are infinite: Theorem 4.5 indicates that the squared implied volatility has an explosion rate of with . The case where is covered in Section 4.3, where an explosion rate of is obtained. Section 4.4 provides the large-time asymptotic behaviour of the implied volatility in our randomised setting; in particular, the long-term similarities between standard and randomised Heston models are present in this section. Finally, Section 4.5 covers the singular case of the small-time at-the-money implied volatility.

4.1. Preliminaries

As a first step in understanding the behaviour of the implied volatility, we analyse the short-time limit of the rescaled cgf of the sequence . To do so, let be a smooth function, which can be extended at zero by continuity with . In light of (2.3), for any , we introduce the effective domain of the moment generating function of the rescaled random variable :

as well as the following sets, for any :

We now denote the pointwise limit , where

| (4.1) |

The seemingly identical notations for the function and its pointwise limit should not create any confusion in this paper. Introduce further the real numbers and and the function :

| (4.2) |

The following proposition, whose proof is postponed to Appendix D.1, summarises the limiting behaviour of as tends to zero. In view of Remark 4.2(ii) below, we shall only consider power functions of the type . It is clear that there is no loss of generality by taking , as it only acts as a space-scaling factor. We shall therefore replace the notation by to highlight the power exponent in action.

Proposition 4.1.

Let , with . As tends to zero, the following pointwise limit holds:

and is infinite elsewhere, where . Whenever (for any ), or and , the limit is infinite everywhere except at the origin.

We shall call the (pointwise) limit ‘degenerate’ whenever it is either equal to zero everywhere or zero at the origin and infinity everywhere else. In Proposition 4.1, only the last two cases are not degenerate.

Remark 4.2.

When the random initial distribution has bounded support (), Proposition 4.1 indicates that the only possible speed factor is , and a direct application of the Gärtner-Ellis theorem (Theorem B.2) implies a large deviations for the sequence ; adapting directly the methodology from [24], we obtain the small-time behaviour of the implied volatility:

Corollary 4.3.

If , then with and

| (4.3) |

Approximations, in particular around the at-the-money , of the rate function , and hence of the small-time implied volatility, can also be found in [24, Theorem 3.2], and apply here directly as well. Further, as discussed in detail in Section 6.1, higher order terms in the small-time expansion of can be obtained if the mgf of the initial randomisation is known in closed form.

4.2. The thin-tail case

In the case , Proposition 4.1 is not sufficient as several different behaviours can occur. In this case, which we naturally coin ‘thin-tail’, a more refined analysis is needed, and the following assumption shall be of uttermost importance:

Assumption 4.4 (Thin-tail).

and admits a smooth density with as tends to infinity, for some .

For notational convenience, we introduce the following two special rates of convergence , and two positive constants , :

| (4.4) |

The following theorem is the main result of this thin-tail section, and provides both a large deviations principle for the log-stock price process as well as its implications on the small-maturity behaviour of the implied volatility. Define the function by

| (4.5) |

In exponential Lévy models, the implied variance for non-zero explodes at a rate [49, Proposition 4]. Theorem 4.5 implies that in a thin-tail randomised Heston model we have a much slower explosion rate of with . In [47] the authors commented that market data suggests that implied volatility with decreasing maturity still has a reasonable range of values and does not explode significantly, which might provide empirical grounds justifying the potential value of this randomised model as an alternative to the exponential Lévy models. The theorem relies on the study of the asymptotic behaviour of the rescaled mgf of :

Lemma 4.6.

Under Assumption 4.4, the only non-degenerate speed factor is , and

| (4.6) |

Assumption 4.4 in particular implies that the function is regularly varying with index (which we denote , see also Appendix B.2 for a review of and useful results on regular variation). Without this slightly stronger assumption, however, the constant in (4.6)–essential to compute precisely the rate function governing the corresponding large deviations principle (Theorem 4.5)–would not be available. In order to prove the lemma and hence the theorem, let us first state and prove the following result:

Lemma 4.7.

If (), then at infinity, with defined as

Proof.

Proof of Lemma 4.6 and of Theorem 4.5.

By Lemma B.5, the mgf of is well-defined on . Lemmas 4.7 and C.2 imply that as tends to zero,

For the right-hand side is well defined with non-zero limit if and only if ; the case does not yield any non-degenerate behaviour, and the lemma follows.

The large deviations principle stated in Theorem 4.5 is a direct consequence of Lemma 4.6 and the Gärtner-Ellis theorem (Theorem B.2), noting that the function in (4.6) satisfies all the required conditions and admits as Fenchel-Legendre transform. The translation of this asymptotic behaviour into implied volatility follows the same lines as in [24]. ∎

4.3. The fat-tail case

If is infinite and is finite, Proposition 4.1 states that the only choice for the rescaling factor is , but the form of the limiting rescaled cumulant generating function does not yield any immediate asymptotic estimates for the probabilities. In this case, we impose the following assumption on the moment generating function of in the vicinity of the upper bound of its effective domain:

Assumption 4.8.

There exists , such that the following asymptotics hold for the cgf of as tends to from below:

| (4.7) |

and

| (4.8) |

where and .

Remark 4.9.

Example 4.10.

-

•

For the Exponential distribution with parameter , .

-

•

For the non-central -squared distribution as in Example 6.2, .

For , introduce the function as

| (4.9) |

as well as, for any the functions by and

| (4.10) |

where the functions and are defined in Lemmas D.2-D.3 respectively. Then the following behaviour, proved in Section D.2, holds for European option prices:

Theorem 4.11.

Under Assumption 4.8, European Call options with strike have the following expansion:

Moreover, the small-time implied volatility behaves as follows whenever :

where

A particular example of a randomisation satisfying Assumption 4.8 is the non-central Chi-squared distribution. This case was the central focus of [39], where the small-time behaviour of the forward smile in the Heston model was analysed. As a sanity check, our theorem 4.11 corresponds to [39, Theorem 4.1].

Corollary 4.12.

Under Assumption 4.8, for , .

Remark 4.13.

Even though the leading order in the expansion is symmetric, Theorem 4.11 explains how the asymmetry in the volatility smile is generated. In particular, the term immediately shows how the leverage effect can be produced with .

4.4. Large-time asymptotics

As observed in Figure 1, the effect of initial randomness decays when the maturity becomes large, so that the large-time behaviour of the randomised Heston model should be similar to that of the standard Heston model, which has been discussed in detail in [25, 27, 38]. In the particular example of the forward Heston model–which coincides with randomising with a non-central -squared distribution–such a large-time behaviour has been analysed in [40]. Throughout this section we assume and (this condition usually holds on equity markets, where the instantaneous correlation is negative–the so-called leverage effect), which guarantees the essential smoothness of the limiting cgf in a standard Heston as tends to infinity, and define the function on by:

| (4.11) |

where , and where the function is given in (A.1). We further denote , the convex conjugate of . Forde and Jacquier [25, Theorem 2.1] proved that and . Consider now the following assumption:

Assumption 4.14.

.

Remark 4.15.

Theorem 4.16.

Remark 4.17.

-

•

As proved in [25], the map is smooth, strictly convex, attains its minimum at the point , and .

- •

- •

Theorem 4.16 provides the large-time behaviour of the implied volatility smile with a time-dependent strike. For fixed strike, the initial randomisation has no effect, and we recover the flattening effect of the smile:

Corollary 4.18 (fixed strike).

Under Assumption 4.14,

4.5. At-the-money (ATM) case

All our small-maturity results above hold in the out-of the money case . As usual in the literature on implied volatility asymptotics, the at-the-money case exhibits a radically different behaviour, and a separate analysis is needed. We first recall in Lemma 4.19 the at-the-money asymptotics in the classical Heston model [26]. To differentiate between standard and randomised Heston models, denote by as the implied volatility in the standard Heston model with fixed initial condition .

Lemma 4.19.

[26, Corollary 4.4] In the standard Heston model with , assume that there exists such that the map is of class , then , where .

Theorem 4.20.

In a randomised Heston model, holds as time tends to zero.

Proof.

Since , then is finite. Denote by the European Call option price in the Black-Scholes model with maturity , strike and volatility , and by its price in the standard Heston model with . Using the tower property,

| (4.12) |

and Lemma 4.19 and [26, Corollary 4.5] imply that the equation holds -almost surely. Also for any , [26, Proposition 3.4] implies that

Plugging these equations back into (4.12), and equating (4.12) with , the theorem follows from

∎

Remark 4.21.

If is finite then following a similar procedure we obtain higher order terms of ,

where , , and . In the non-central chi-squared case we recover the result of [39, Theorem 4.4].

5. A dynamic pricing framework

The model proposed in this paper has so far only been studied in a static way, namely from the inception time of the (European contract), with a view towards calibration of the implied volatility surface. While providing a better fit to short-maturity options by steepening the skew, it is not obvious, however, how to use the model dynamically; in particular, it is unclear how to choose the random initial value of the volatility process during the life of the contract, should one be wishing to sell or buy the option, or for hedging purposes. Mathematically, assume that at time zero the trader chooses an initial randomisation (or classically a Dirac mass at some positive point), and suppose that, at some later time , she needs to reprice the option (with remaining maturity ). How should she choose the new initial random variable ? Since the variance process has continuous paths, a suitable choice of , consistent with the dynamics of the variance, is obviously , the solution of the SDE (2.1), after running it from time zero to time . With an initial guess at time zero, then, at time , conditional on , is distributed as , where , and is a non-central Chi-squared distribution with degrees of freedom and non-centrality parameter . From the tower property, the moment generating function of then reads

| (5.1) |

for all . Setting , we have

where . We now discuss the impact of different choices of at time zero on the distribution of and on the implied variance at time (for a remaining maturity ). We keep here the terminology introduced in Section 4 regarding the tail behaviour of .

Before diving into the detailed analysis, we argue that chosen this way should only serve as a candidate for the initial distribution at time and in practice should be recalibrated according to updated (noisy) market observations at time . Market noises explain how the distribution of can deviate from the ergodic distribution: the impact of the (instantaneous) noises can change the shape and parameterisation of the randomisation. We further comment that understanding the choice of is also useful from a model risk point of view: at time zero, it is important to understand and simulate the behaviours of model parameters at a given future time. We show in this section, in our setting, that can in fact only be fat tailed, and therefore, for consistency, one should probably start with in the class of fat-tail distributions.

5.1. The bounded-support case

In this case, ; the proof of Proposition 4.1 showed that . Combining this with (5.1), we obtain, as tends to from below,

so that, at leading order, behaves asymptotically as a fat-tail distribution as in Assumption 4.8 with . In the particular case of a uniform distribution on , as tends to from below, we obtain

Hence in a uniform randomisation environment, at future time , the shape of the distribution of depends both on and on the parameters that control the dynamics of the variance process. Moreover from Theorem 4.11, the implied variance at time , denoted by , has an explosion rate of :

5.2. The thin-tail case (Assumption 4.4)

Here again, and applying Lemma 4.7 with , we have

| (5.2) |

as tends to from below, so that a thin-tail initial randomisation generates a fat-tail distribution for at time . In light of (5.2), Assumption 4.8 does not hold, and hence is neither of Gamma or non-central Chi-squared type. A case-by-case analysis depending on the distribution of is therefore needed in order to make the term in (5.2) more precise.

Example 5.1 (Folded-Gaussian randomisation).

When , straightforward computations yield

We can obtain the small-time asymptotic expansion of the option price using an approach similar to the proof of Theorem 4.11. Specifically, only Lemma D.3 needs to be adjusted, and the rescaling factor is now ; the main contribution to the asymptotics of out-of-the-money option prices is still given in Lemma D.2. Translating this into the asymptotics of the implied variance, we obtain, for small ,

5.3. The fat-tail case

In this case, . Here we only discuss two special cases for : the Gamma distribution, and the (scaled) non-central -squared distribution.

Example 5.2 (Gamma randomisation).

If , then from (5.1), we have

Consequently is still a fat-tail distribution satisfying Assumption 4.8 with , , while the upper bound of the support of the mgf now depends on both the initial distribution and on the evolution of the process (through ). A direct application of Theorem 4.11 further suggests that, for small enough ,

Example 5.3 (Non-central randomisation).

This analysis shows that a suitable choice for , consistent with the dynamics of the variance process, can actually depend on the initial randomisation at time zero, as well as the evolution of the variance. Even though all three types of initial randomisation imply a fat-tail initial distribution at future time, the generated small remaining-maturity implied volatility smiles are very different. The folded-Gaussian (thin-tail) generates a steeper smile compared to the bounded support case; a fat-tail distribution for generate an even steeper volatility smile at , since the coefficient of the leading order is , which is strictly less than .

Remark 5.4.

All distributions discussed in Section 4 generate a fat-tail distribution for . However, should the assumptions in Section 4 break down, this may not be true any longer: Equation (5.1) suggests that the mgf of can be ill-defined whenever that of does not exist, in the case of a Cauchy distribution for example. That said, the study of the effective domain below (5.1) indicates that, in our setting, only fat-tail distributions for are possible.

6. Examples and Numerics

We now choose some common distributions supported on a subset of for the initial randomisation to illustrate the results in Section 4. We first start with the bounded support case, and provide rigorous justifications to the statements in Section 3. In Section 6.1, we consider a uniformly distributed initial variance, with finite, and provide full asymptotics of European Call prices. The remaining sections are devoted to the unbounded support case; specifically, Sections 6.2-6.4 correspond to the fat-tail case, so that Theorem 4.11 can be applied. The thin-tail environment is illustrated in Section 6.3 where the initial distribution satisfies Assumption 4.4 with .

6.1. Uniform randomisation

Assume that is uniformly distributed on with , then Corollary 4.3 provides the leading term of short-time implied volatility. However, as will be shown in Section 6.6, the true volatility smile for small is much steeper compared with the leading term, so that higher-order terms shall be considered. For any , denote by the unique solution in to the equation , with described in (4.2). From [26, Remark 2.1], existence and uniqueness of such a solution are straightforward, and holds for any non-zero . Introduce the function by

| (6.1) |

where the functions and are provided in (C.1)-(C.2). From [26, Remark 3.2], the function is well defined on . The following theorem is the main result of this section, and provides a detailed asymptotic behaviour of Call option prices as the maturity becomes small:

Theorem 6.1.

Under uniform randomisation, as decreases to zero, European Call option prices behave as

where the function was introduced in Corollary 4.3.

Remark 6.2.

- •

-

•

The asymptotics holds locally for any fixed log-strike . The numerics indicate that for small , as tends to zero, the asymptotics of option prices and volatility smile explode to infinity. This is in contrast with the standard Heston case [26, Section 5].

-

•

Since the function is strictly positive and strictly convex on and for any , the quotient on the right-hand side is well defined.

- •

Proof.

The procedure is essentially the same as the proof of Theorem 4.11. Applying Lemmas C.2 and C.4, the rescaled cgf of for each is given by (with the same notations as in (4.1))

| (6.2) |

For fixed and small enough , introduce the time-dependent probability measure by

Changing the measure, plugging (6.1) and rearranging terms yield the following expression for the Call option price with strike :

It is easy to show that for fixed , under the random variable converges weakly to a Gaussian distribution. The rest of the proof is similar to Section D.2 and we omit the details. ∎

We now explain the steepness of the volatility smile in the uncorrelated case . Using the at-the-money curvature formula for the implied volatility (in uncorrelated stochastic volatility models) proved by De Marco and Martini [17, Equation (2.9)], we can write, for any ,

| (6.3) |

where is the density of the log-price process at time . In the standard Heston model with the initial condition , such that , the small-time asymptotics of the density reads [30, Section 5.3]

with the function defined in (6.1). Applying the saddle point method similar to the proof of [26, Theorem 3.1], the small-time asymptotics of the density in a randomised setting, denoted as , has the expression

Remark 6.3.

Note the difference between the powers and in the expressions for and above. Even if, in the bounded support case, the leading-order term is not affected by the randomisation, the latter does act at higher order. We leave a precise study of this issue to further research.

The ratio then reads

It is easy to verify that and . Moreover, for any fixed ,

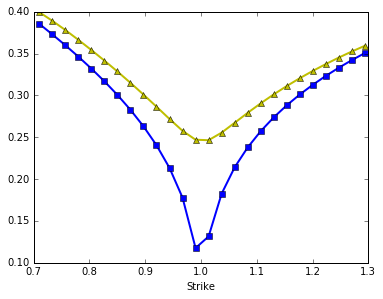

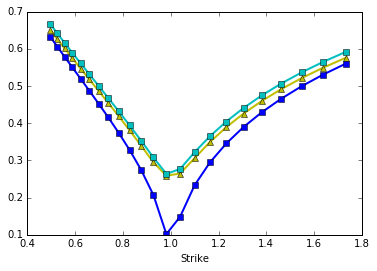

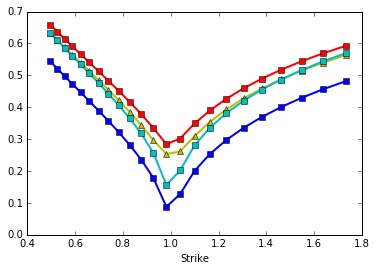

Combining these results, assume that the density at zero can be approximated by for small enough , then there exists small enough such that for all . Plugging it back to (6.3), and noticing that (Section 4.5) holds as tends to zero, then the small-time curvature in a uniformly randomised Heston is much larger compared with that of a standard Heston, implying a much steeper smile around the at-the-money. Figure 3 provides a visual help.

Finally, we mention that the tail behaviour of the implied volatility in a uniformly randomised Heston model is similar to that of the standard Heston. To see this, notice that the moment explosion property in the standard Heston setting is described in [3, Proposition 3.1]. Specifically, the explosion of the mgf of is equivalent to the explosion of the function provided in (A.1). Moreover, Equation (2.3) suggests that it is still the case in the uniform randomised setting, since is infinity. Then the similarity of the tail behaviours follows from [45] (see also [9, 13]).

6.2. Non-central -squared distribution

Assume that is non-central -squared distributed with degrees of freedom and non-centrality parameter , so that its moment generating function reads

then is infinite and . By Proposition 4.1, the only suitable scale function is , which corresponds exactly to the forward-start Heston model, the asymptotics of which have been studied thoroughly in [39]. Applying Equation D.3 and L’Hôpital’s rule with imply that, at the right endpoint , as tends to zero, the pointwise limit

can be either finite or infinite. In particular, since , the pointwise limiting rescaled cumulant generating function is not continuous at the right boundary of its effective domain. The cgf of satisfies Assumption 4.8 with , then Theorem 4.11 implies that we can recover [39, Theorem 4.1]:

6.3. Folded Gaussian distribution

Assume that , then the density of reads

which satisfies Assumption 4.4. Simple computations yield , for any , where denotes the Gaussian cumulative distribution function. Therefore, Lemma C.2 implies that for ,

If , then , and hence

The limit is therefore non-degenerate if and only if , in which case , for all , and Theorem 4.5 implies

6.4. Starting from the ergodic distribution

6.5. Other distributions

The following table (more refined version of the one in Section 1) presents some common continuous distributions for the initial variance, together with the corresponding parameters . In each case, we indicate (up to a constant multiplier) the short-time behaviour of the smile.

6.6. Numerics

We present numerical results for the implied volatility surface for three types of initial randomisation: uniform (), exponential () and folded-Gaussian (). To generate these surfaces, we apply Fast Fourier Transform (FFT) methods [14] to derive a matrix of option prices, and then compute the corresponding implied volatilities using a root-finding algorithm. The Heston parameters are given by , which corresponds to a realistic data set calibrated on the S&P options data. In view of Theorem 4.20, parameters of are chosen to satisfy , so that results of standard and randomised Heston models can be compared.

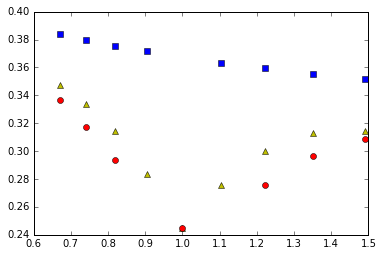

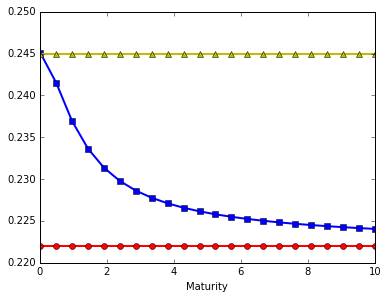

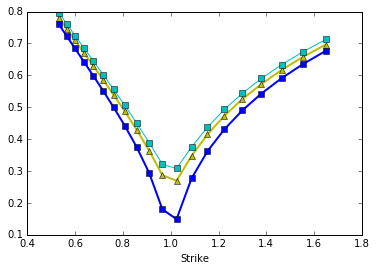

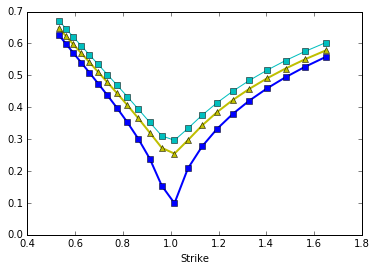

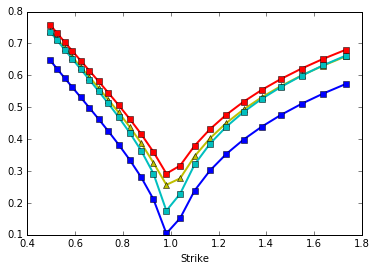

The numerics show that the randomised Heston model provides a much steeper short-time volatility smile compared with the standard Heston model, but this difference tends to fade away as maturity increases. In the uniform case, Figure 2 and (4.3) may seem contradictory at first, since the former indicates steepness and the latter excludes explosion. There is no issue here, and in fact suggests that even though there is no proper explosion, it is still possible to generate steep short-time volatility smiles in a randomised setting. In Figure 5 we test higher-order terms in a Gamma randomisation scheme while the Heston parameters remain unchanged.

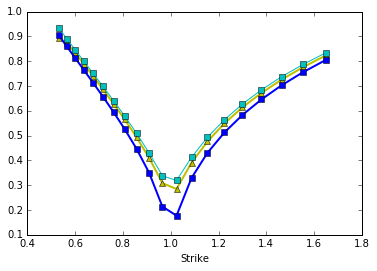

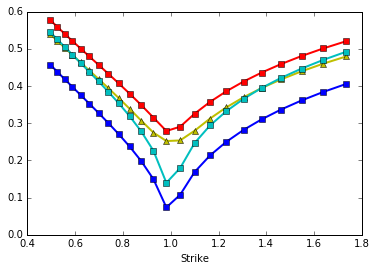

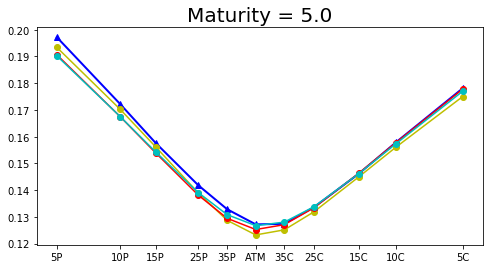

In Figure 6 we illustrate the results in Section 5. We price the option in three different randomisation schemes after one month () into the life of the contract. To compare different schemes, we again match the parameters of (at time zero) with different distributions according to Theorem 4.20. We see that the higher-order term in Theorem 4.11 is quite accurate even for relatively large time to maturity. Not surprisingly (especially in the folded-Gaussian case) the leading order is insufficient, and higher orders are needed for reliable approximations.

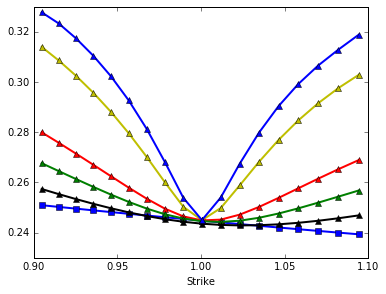

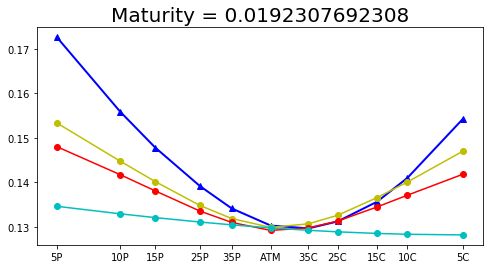

6.7. USD/JPY FX options

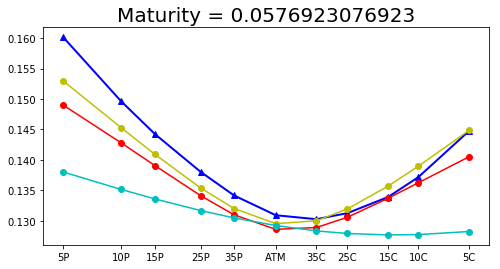

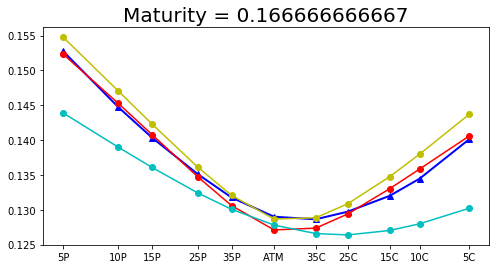

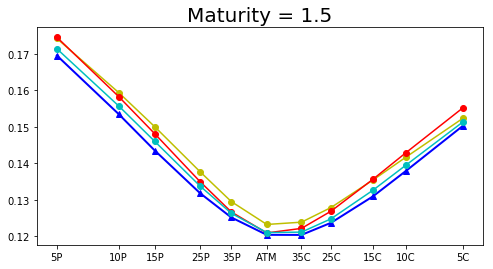

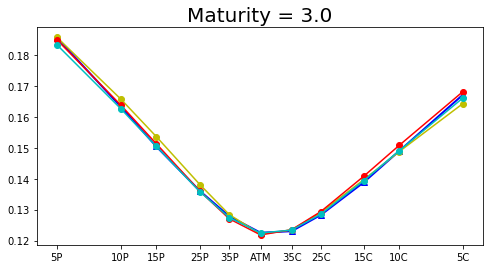

We test the calibration accuracy of the randomised Heston model using the USD/JPY FX market (ask) prices on January 20th, 2017. In the FX market the implied volatility still has the small-time explosion feature: Figure 7 shows that the volatility smile generated by a standard Heston model is too flat compared with the market data with small maturities. This finding agrees with the existing literature. For instance, in [42] the authors fixed and , and calibrated the remaining parameters in a standard Heston environment to the EUR/USD market data. They selected maturities ranging from one week to two years, then calibrated the Heston model for each fixed maturity. Even with this ‘slice-by-slice’ calibration procedure, they observed poor fit of Heston to the market data for small maturities. Unsurprisingly, they commented that time-dependent parameters, or ‘stochastic volatility plus jumps’, as appeared in [5, 6], are needed to improve the calibration accuracy. We use the same initial guess for both the standard and the randomised Heston models, then calibrate the parameter sets using the market data. The results are presented in Figure 7 and Table 2. Both randomisation schemes have substantial improvement over the standard Heston model.

| Model | Small maturities | Less than one year | Total |

|---|---|---|---|

| Standard Heston | |||

| Gamma randomisation | |||

| Uniform randomisation |

Appendix A Notations from the Heston model

In the Heston model, the log stock price satisfies the SDE (2.1), where the initial distribution is a Dirac mass at some point . As proved in [1], the moment generating function (2.2) admits the closed-form representation , for any , where

| (A.1) |

In the proof of [26, Lemma 6.1], the authors showed that the functions and have the following behaviour as tends to zero:

| (A.2) |

with , , and . The pointwise limit of the (rescaled) cumulant generating function of then reads

where and are introduced in (4.2). From [26, Section 2], the function is well defined, smooth and strictly convex on , and infinite elsewhere.

Appendix B Reminder on large deviations and Regular variations

B.1. Large deviations and the Gärtner-Ellis theorem

In this appendix, we briefly recall the main definitions and results from large deviations theory, which we need in this paper. For full details, the interested reader is advised to look at the excellent monograph by Dembo and Zeitouni [19]. Let denote a sequence of real-valued random variables. A map is said to be a good rate function if it is lower semicontinuous and if the set is compact in for each .

Definition B.1.

Let be a continuous function that tends to zero at infinity. The sequence satisfies a large deviations principle as tends to infinity with speed and rate function (in our notations, ) if for each Borel measurable set , the following inequalities hold:

Let now be the pointwise limit of the rescaled cgf of : , whenever the limit exists, and denote by its effective domain. Then is said to be essentially smooth if the interior is non-empty, is differentiable on , and for any . Finally, for any , define , the convex conjugate of function .

Theorem B.2 (Gärtner-Ellis theorem, Theorem 2.3.6 in [19]).

If the function is lower semicontinuous on and essentially smooth, and , then .

B.2. Regular variations

We recall here some notions on regular variations, following the monograph [10].

Definition B.3.

Let . A function is said to be regularly varying with index (and we write ) if , for any . When , the function is called slowly varying.

Lemma B.4 (Bingham’s Lemma, Theorem 4.12.10 in [10]).

Let be a regularly varying function with index ; then, as tends to infinity, the asymptotic equivalence holds.

Let be a random variable supported on with a smooth density . The following lemma ensures that its moment generating function has unbounded support.

Lemma B.5.

If there exists such that , then .

Proof.

Karamata’s Characterisation Theorem [10, Theorem 1.4.1] implies that for any , where the function is slowly varying, and Karamata’s Representation Theorem [10, Theorem 1.3.1] provides the following expression:

where the functions and satisfy , , and is a fixed positive number. Then there exists such that for all . Additionally, for any fixed small enough satisfying that , there exists such that , for any . Denote , then for any , and any ,

Thus there exists large enough so that , for . With ,

∎

Appendix C Preliminary computations

In view of (2.3), short-time asymptotic expansions of the functions and are necessary in order to derive the pointwise limit of the rescaled cgf of . In this appendix we provide these expansions.

C.1. Components of the mgf

We start by investigating the short-time behaviour of the function . For any , define the function by

| (C.1) | ||||

where the functions are defined below (A.2) above.

Remark C.1.

The function is well defined: to see this, we only need to check that the terms sum up to a real number, and the rest follows from [26, Remark 3.2]. The first term in (C.1) reads

which is a real number, and the sum of the remaining terms with reads (taking out the prefactor )

which is purely imaginary, so that the whole term is a real number.

The following lemma makes the effective domain of precise, and shows that it arises as the second order of the short-time expansion of a rescaled version of the function in (A.1).

Lemma C.2.

Let . As tends to zero, the map behaves as

Remark C.3.

The function defined as

| (C.2) |

is clearly real valued [26, Remark 6.2], and determines the asymptotic behaviour of the function as follows.

Lemma C.4.

The map has the following asymptotic behaviour as tends to zero:

Proof of Lemma C.2.

Obviously , so we assume from now on that . From (A.2), we have

| (C.3) |

Plugging these back into the expression of the function in (A.1), we obtain

| (C.4) |

If , is a real number and is purely imaginary, then as goes to infinity the term oscillates on the unit circle in the complex plane, thus no asymptotic can be derived.

Assume now that . Then , and Equation (C.4) yields

The form of the effective domain is straightforward from these expressions.

If without further information on higher-order terms, then . Following the same procedure as above then only the leading order can be derived, i.e.

Proof of Lemma C.4.

Assume that . Expand and to the third order,

| (C.5) |

where and . Combining these expansions with Equation (C.3) implies

| (C.6) |

If , no short-time asymptotics can be derived since tends to infinity. For the proof of the case where we refer to [26, Lemma 6.1]. Assume now that , then the following asymptotic expansions hold:

where . Consequently,

and therefore

Plugging this into (C.1), the result follows by noticing that the coefficients of and are both zero. ∎

Appendix D Proofs of the main results

D.1. Proof of Proposition 4.1

In [39, Section 6] the authors proved that whenever , and if . Throughout the proof we keep the notation , emphasising that the statement still holds for function with a general form, not only polynomials.

Case . We need to analyse the behaviour of as approaches zero. Since is strictly positive, by continuity of the mgf around the origin, converges to as tends to zero for any in , which implies that . For small , a Taylor expansion indicates that

Since is of order , then

| (D.1) |

and therefore , for all .

Case . We need to evaluate at infinity. If is finite, for sufficiently small, the term is infinite for any non-zero , hence , and is null at , and infinite elsewhere. If is infinite, then obviously . Assume first that is finite; we claim that . In fact, let be the cumulative distribution function of , then

For any small , fix , so that

since is the upper bound of the support; therefore is strictly positive, and the result follows. If , notice that is of order from Lemma C.4, and hence

When , is positive whenever . Therefore,

Case . If is finite then the pointwise limit is null on the whole real line. Assume now that is infinite and is finite. Following Remark C.3(iii), implies . For sufficiently small ,

For any fixed in , by definition there exists a positive such that is in for all less than . Then the mgf of is infinitely differentiable around the point , and the -th order derivative at this point is . Denote now , for , and . A Taylor expansion of the function around the point yields

| (D.2) |

Letting tend to zero, we finally obtain

However, the limit of depends on the explicit form of . To see this, assume that , which is guaranteed in particular when , and compute the limit when . L’Hôpital’s rule implies

| (D.3) |

D.2. Proof of Theorem 4.11

The systematic procedure is similar to the proof of [39, Theorem 3.1]. To simplify notations, write , and , whenever these quantities are well defined. We shall prove the theorem in several steps: in Lemma D.1 we show that a saddlepoint analysis is feasible; by taking the expectation under a new probability measure, the main contribution of the option price arises and its asymptotic expansion is provided in Lemma D.2; in Lemma D.3 we prove the convergence (with rescaling) of the sequence under this new measure; finally, the full asymptotics of the Call option price is obtained via inverse Fourier transform.

Lemma D.1.

Under Assumption 4.8, for any , small enough, the equation admits a unique solution such that , and the following holds as tends to zero:

where

If , then defined as the solution to satisfies .

Proof of Lemma D.1.

Assume that , the case when being analogous. Equation (2.3) implies that for any , the equation reads

| (D.4) |

The existence and uniqueness of the solution to (D.4) are guaranteed by the strict convexity of the rescaled cgf for each [43, Theorem 2.3] and (4.8), in which the denominator tends to zero as tends to the boundary of . Denote now the unique solution by . Applying Lemma C.2 and Lemma C.4 with ,

We first prove that . If , there exists a sequence and (small enough) , satisfying and for any In Section D.1 it is proved that . Also notice that for any fixed small enough the map is continuous and strictly increasing. Hence for fixed positive there are at most finitely many in the sequence such that .

Equation (D.4) implies that for fixed the limit of is infinity as tends to zero. Taking a subsequence of if necessary, assume now that , for any . Since , then for any there exists such that holds for any . Fix small enough so that , where is chosen to satisfy for any , the higher-order term in (4.8) is bounded above by one. Then for such and for any we have . The function is strictly increasing, implying

where , hence the contradiction. Therefore . Analogously we can prove that .

Case . Assume that , where . Equation (D.4) implies that , hence all the terms of order in the expansion of should be included. More specifically,

Plugging this back into (D.4) and solving at the leading order yield the desired result.

Case . In this case . Equation (D.4) now reads

| (D.5) |

Denote by as the leading order of the function . Solving (D.5) at the leading order, then from which . Higher orders in the expansion of can be derived similarly, simply by replacing the little-o term in (D.5) with precise higher-order terms provided in (4.8). We omit the details.

Finally, when , write with . As tends to zero, , , and . Plugging these into (D.4) with proves the lemma. ∎

Lemma D.2.

- (1)

-

(2)

If and , then for any , as tends to zero,

where .

Proof of Lemma D.2.

Case . Assumption 4.8 and Lemma D.1 imply

Using the expression of provided in Lemma D.1, the coefficient of the term of order is given by

Case . This case follows straightforward computations after noticing that

∎

For each and small enough, define the time-dependent measure by

Lemma D.1 implies that is finite for small . Also by definition it is obvious that , then is a well-defined probability measure for each .

Lemma D.3.

For any , let , where . Under Assumption 4.8, as tends to zero, the characteristic function of under is

where .

Remark D.4.

Remark D.5.

Intuitively, the case should be similar to the case , so that a suitable candidate for the function can be found. However, in such scenario more information on the asymptotics of and its derivative are required in order to obtain the suitable (non-constant) characteristic function. These extra assumptions turn out to be very restrictive and of little practical use, and are thus omitted.

Proof of Lemma D.3.

Assume that , with being analogous. Function can be written as

| (D.6) | ||||

Case . Lemma D.1 implies that

As a result, the lemma follows in this case from the following computations:

Case . Denote , then . Lemma D.1 implies

Consequently,

and the proof follows by noticing that and , from Lemma D.1.

∎

We finally prove the main theorem, when . The price of a European Call option with strike is

Case . The proof is identical to [39, Theorem 3.1] and is therefore omitted.

Case . The Fourier transform of the modified payoff under is

where in the second line we use the fact that . Recall that the Gamma distribution with shape and scale has density given by

| (D.7) |

Applying [35, Theorem 13.E] and Lemma D.3,

| (D.8) |

where the last line follows from Fourier inversion. Combining Lemma D.2 and (D.2), the Call price reads

Assume now that , the price of a European Put option with strike is

and the Fourier transform of the modified payoff function is

Following a similar procedure, and noticing that is a -martingale, the Put-Call parity implies

In the standard Black-Scholes model with volatility , the short-time asymptotics of the Call option price reads [26, Corollary 3.5] . Then the asymptotics of implied volatility can be derived following the systematic approach provided in [32].

D.3. Proof of Theorem 4.16

We first prove the large deviations statement, which we then translate into the large-maturity behaviour of the implied volatility. Andersen and Piterbarg [3, Proposition 3.1] analysed moment explosions in the standard Heston model, and proved that for any , the quantity always exists as long as

| (D.9) |

Moreover, the assumption implies (see [25]) that (D.9) holds for any , so that is well-defined for and any (large) in the standard Heston model. The tower property then yields

Consequently, for any large , is well-defined for , where the set is defined by

Using the expressions of functions and in (A.1), the rescaled cgf of the process reads

| (D.10) |

For any , since the quantity is strictly positive, then

| (D.11) |

Since is continuous for each , L’Hôpital’s rule implies that .

Case . Obviously , implying that . Equation (D.3) shows that

with provided in (4.11). In [25, Theorem 2.1], it is proved that the limiting function and its effective domain satisfy all the assumptions of the Gärtner-Ellis theorem (Theorem B.2), and hence the large deviations principle for the sequence follows.

Case . Equation (D.11) implies that

As a result, the essential smoothness of function is guaranteed if

Since holds for any ,

| (D.12) |

Since , Condition (D.3) holds for any . Whenever or , as functions of , the left-hand-side is strictly increasing while the right-hand-side is strictly decreasing. Therefore, (D.3) holds for any if and only if . Consequently, Assumption 4.14 ensures that , and the proof follows from the Gärtner-Ellis theorem (Theorem B.2).

We now prove the asymptotic behaviour for the implied volatility. We claim that in a randomised Heston setting the European option price has the following limiting behaviour:

The proof is covered in detail in [40, Section 5.2.2], and we therefore highlight the main ideas for completeness. From Theorem 4.16, define a time-dependent probability measure :

where is the solution to the equation . The option price is then expressed as the expectation under of a modified payoff, and can be computed by (inverse) Fourier transform with the main contribution equal to . It is also known (see [24, Corollary 2.12] for instance) that in the Black-Scholes model with volatility , the asymptotics of European option prices with strike are given by

where . Then the leading order of the large-time implied variance is obtained by solving

We omit the details of the proof which can be found in [25, 27].

References

- [1] H. Albrecher, P. Mayer, W. Schoutens and J. Tistaert. The little Heston trap. Wilmott Magazine: 83-92, January 2007.

- [2] E. Alòs, J.A. León and J. Vives. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance and Stochastics, 11(4): 571-589, 2007.

- [3] L. Andersen and V. Piterbarg. Moment explosions in stochastic volatility models Finance and Stochastics, 11(1): 29-50, 2007.

- [4] L. Andersen. Efficient simulation of the Heston stochastic volatility model. SSRN: 946405, 2007.

- [5] G. Bakshi, C. Cao and Z. Chen. Empirical performance of alternative option pricing models. Journal of Finance, 52(5): 2003-2049, 1997.

- [6] D.S. Bates. Jumps and stochastic volatility: exchange rate processes implicit in Deutsche Mark options. The Review of Financial Studies, 9(1): 69-107, 1996.

- [7] C. Bayer, P. Friz and J. Gatheral. Pricing Under Rough Volatility. Quantitative Finance, 16(6): 887-904, 2016.

- [8] S. Benaim and P. Friz. Smile asymptotics \@slowromancapii@: Models with known moment generating function. Journal of Applied Probability, 45(1): 16-32, 2008.

- [9] S. Benaim and P. Friz. Regular variation and smile asymptotics. Mathematical Finance, 19: 1-12, 2009.

- [10] N.H. Bingham, C.M. Goldie and J.L. Teugels. Regular variation. Cambridge University Press, 1989.

- [11] D. Brigo. The general mixture-diffusion SDE and its relationship with an uncertain-volatility option model with volatility-asset decorrelation. arXiv:0812.4052, 2008

- [12] D. Brigo, F. Mercurio and F. Rapisarda. Lognormal-mixture dynamics and calibration to market volatility smiles. International Journal of Theoretical and Applied Finance, 5(4): 427-446, 2002.

- [13] F. Caravenna and J. Corbetta. General smile asymptotics with bounded maturity. SIAM Fin. Math., 7(1), 720-759, 2016.

- [14] P. Carr and D. B. Madan. Option valuation using the fast Fourier transform. Journal of Computational Finance, 2: 61-73, 1999.

- [15] J. C. Cox, J. E. Ingersoll and S. A. Ross. A theory of the term structure of interest rates. Econometrica. 53(2): 385-407, 1985.

- [16] H. Cramér. Sur un nouveau théorème-limite de la théorie des probabilités. Actualités Scientifiques Industrielles, 736: 5-23, 1938.

- [17] S. De Marco and C. Martini. The term structure of implied volatility in symmetric models with applications to Heston. International Journal of Theoretical and Applied Finance, 15(4), 2012.

- [18] A. Dembo and O. Zeitouni. Large deviations via parameter dependent change of measure and an application to the lower tail of Gaussian processes. Progress in Probability, 36: 111-121. Birkhäuser, Basel, Switzerland, 1995.

- [19] A. Dembo and O. Zeitouni. Large Deviations Techniques and Applications. Springer-Verlag Berlin Heidelberg, 38, 1998.

- [20] D. Dufresne. The Integrated Square-Root Process. Research Paper 90, University of Melbourne, Melbourne, Australia, 2001.

- [21] O. El Euch and M. Rosenbaum. Perfect hedging in rough Heston models. To appear in The Annals of Applied Probability.

- [22] O. El Euch and M. Rosenbaum. The characteristic function of rough Heston models. To appear in Mathematical Finance.

- [23] O. El Euch, M. Fukasawa and M. Rosenbaum. The microstructural foundations of leverage effect and rough volatility. Finance and Stochastics, 22(2): 241-280, 2018.

- [24] M. Forde and A. Jacquier. Small-time asymptotics for implied volatility under the Heston model. IJTAF, 12(6): 861-876, 2009.

- [25] M. Forde and A. Jacquier. The large-maturity smile for the Heston model. Finance and Stochastics, 15(4): 755-780, 2011.

- [26] M. Forde, A. Jacquier and R. Lee. The small-time smile and term structure of implied volatility under the Heston model. SIAM Journal on Financial Mathematics, 3(1): 690-708, 2012.

- [27] M. Forde, A. Jacquier and A. Mijatović. Asymptotic formulae for implied volatility under the Heston model. Proceedings of the Royal Society A, 466(2124): 3593-3620, 2010.

- [28] M. Forde and H. Zhang. Asymptotics for rough stochastic volatility models. SIAM Journal Fin. Math., 8: 114-145, 2017.

- [29] J.P. Fouque and B. Ren. Approximation for option prices under uncertain volatility. SIAM Fin. Math., 5: 360-383, 2014.

- [30] P. Friz, S. Gerhold and A. Pinter. Option pricing in the moderate deviations regime. Mathematical Finance, 28(3): 962-988, 2018.

- [31] M. Fukasawa. Short-time at-the-money skew and rough fractional volatility. Quantitative Finance, 17(2): 189-198, 2017.

- [32] K. Gao and R. Lee. Asymptotics of implied volatility to arbitrary order. Finance and Stochastics, 18: 342-392, 2014.

- [33] J. Gatheral. The volatility surface: A practitioner’s guide. Wiley New York, 2006.

- [34] J. Gatheral, T. Jaisson and M. Rosenbaum. Volatility is rough. Quantitative Finance, 18(6): 933-949, 2018.

- [35] R. Goldberg. Fourier transforms. Cambridge University Press, 1965.

- [36] H. Guennoun, A. Jacquier, P. Roome and F. Shi. Asymptotic behaviour of the fractional Heston model. To appear in SIAM Journal on Financial Mathematics.

- [37] S.L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies, 6(2): 327-343, 1993.

- [38] A. Jacquier, M. Keller-Ressel and A. Mijatović. Large deviations and stochastic volatility with jumps: asymptotic implied volatility for affine models. Stochastics, 85(2): 321-345, 2013.

- [39] A. Jacquier and P. Roome. The small-maturity Heston forward smile. SIAM Financial Mathematics, 4(1): 831-856, 2013.

- [40] A. Jacquier and P. Roome. Asymptotics of forward implied volatility. SIAM Financial Mathematics, 6(1): 307-351, 2015.

- [41] A. Jacquier and P. Roome. Black-Scholes in a CEV random environment. Mathematics and Financial Economics, 12(3): 445-474, 2018.

- [42] A. Janick, T. Kluge, R. Weron and U. Wystup. FX smile in the Heston model. Springer, 2010.

- [43] B. Jorgensen. The theory of dispersion models. Chapman and Hall, 1997.

- [44] I. Karatzas and S.E. Shreve. Brownian Motion and Stochastic Calculus. Springer, 1991.

- [45] R. Lee. The moment formula for implied volatility at extreme strikes. Mathematical Finance, 14(3): 469-480, 2004.

- [46] S. Mechkov. ’Hot-start’ initialization of the Heston model. Risk, November 2016.

- [47] A. Mijatović and P. Tankov. A new look at short-term implied volatility in asset price models with jumps. Mathematical Finance, 26(1): 149-183, 2016.

- [48] D. Revuz and M. Yor. Continuous Martingales and Brownian Motion. Springer, 1999.

- [49] P. Tankov. Pricing and hedging in exponential Lévy models: Review of recent results. Paris-Princeton Lectures on Mathematical Finance: 319-359, 2010.

- [50] D. Williams. Probability with martingales. Cambridge University Press, 1991.

- [51] Zeliade Systems. Heston 2010. Zeliade Systems White Paper, http://www.zeliade.com/whitepapers/zwp-0004.pdf, 2011.