1 Introduction

Calibrating martingales to given option prices is a central topic of mathematical finance,

and it is thus a natural question which sets of option prices admit such a fit, and which do not.

Note that we are not interested in approximate model calibration, but in the consistency

of option prices,

meaning arbitrage-free models that fit the given prices exactly.

Put differently, we want to detect arbitrage in given prices.

We do not consider continuous call price surfaces, but restrict to the

(practically more relevant) case of finitely many strikes and maturities.

Therefore, consider a financial asset with finitely many European call options written on it.

In a frictionless setting, the consistency problem is well understood:

Carr and Madan [4] assume that interest rates, dividends and bid-ask spreads are zero,

and derive necessary and sufficient conditions for the existence of arbitrage free models.

Essentially, the given call prices must not admit calendar or butterfly arbitrage.

Davis and Hobson [6] include interest rates and dividends and give similar results.

They also describe explicit arbitrage strategies, whenever arbitrage exists.

Concurrent related work has been done by Buehler [2].

Going beyond existence, Carr and Cousot [3] present practically appealing explicit constructions

of calibrated martingales.

More recently,

Tavin [18] considers options on multiple assets and studies the existence of arbitrage strategies in this setting. Spoida [16] gives conditions for the consistency of a set of prices

that contains not only vanillas, but also digital barrier options. See [11]

for many related references.

As with virtually any result in mathematical finance, robustness with respect to market frictions

is an important issue in assessing the practical appeal of these findings. Somewhat surprisingly,

not much seems to be known about the consistency problem in this direction, the single exception being a paper

by Cousot [5]. He allows positive bid-ask spreads on the options, but not on the underlying,

and finds conditions on the prices that determine the existence of an arbitrage-free

model explaining them.

The novelty of our paper is that we allow a bid-ask spread on the underlying.

Without any further

assumptions on the size of this spread, it turns out that there is no connection between

the quoted price of the underlying and those of the calls: Any strategy trying to

exploit unreasonable prices can be made impossible by a sufficiently large bid-ask spread

on the underlying (see Example 2.3 and Proposition 4.1).

In this respect, the problem

is not robust w.r.t. the introduction of a spread on the underlying. However,

an arbitrarily large spread seems questionable, given that spreads are usually tight

for liquid underlyings. We thus enunciate

that the appropriate question is not “when are the given prices consistent”,

but rather “how large a bid-ask spread on the underlying is needed to explain them?”

Therefore, we put a bound on the spread of the discounted prices, and want to determine the

values of that lead to a model explaining the given prices.

We then refer to the call prices as -consistent (with the absence of arbitrage).

To define the payoff of the call options, we use an arbitrary reference price

process that evolves within the bid-ask spread. We show (Proposition 2.5)

that the consistency problem does not change dramatically if this reference process

is the arithmetic average of the bid and ask prices of the underlying.

Recall that the main technical tool used in the papers [4, 5, 6] mentioned above

to construct arbitrage-free models

is Strassen’s theorem [17], or modifications thereof.

In the financial context, this theorem shows the existence of martingale models for

option prices that increase with maturity.

The latter property breaks down if a spread on the underlying is allowed.

We will therefore employ some results from our recent companion paper [9],

which deals with variants of Strassen’s theorem and approximating sequences

of measures by peacocks (processes increasing w.r.t. the convex order).

We assume discrete trading times and finite probability spaces throughout;

no gain in tractability or realism is to be expected by not doing so.

In the case of a single maturity, we obtain simple explicit conditions

that are equivalent to -consistency (Theorem 3.1).

The multi-period problem, on the other hand, seems to be

challenging. We provide two partial results: necessary (but presumably not sufficient) explicit

conditions for -consistency (Theorem 5.3), and sufficient semi-explicit conditions (Theorem 4.3). Here, by “semi-explicit” we mean the following: Our consistency definition

requires the existence of two sequences of measures, which are not “too far apart”,

and one of which is a peacock. They correspond to a consistent price system resp. to a reference price

that defines the option payoffs. Our result does not say anything about the existence

of the reference price process, but contains explicit conditions for the existence of the peacock.

The structure of the paper is as follows.

In Section 2 we describe our setting and give a precise formulation of our problem.

Also, the significance of peacocks and approximating sequences of measures is explained.

Then, in Section 3 we present

necessary and sufficient conditions for the existence of arbitrage

free models with bounded bid-ask spreads for a single maturity.

Our main results on the multi-period problem are contained in Section 4.

There, we invoke the main result from [9].

Necessary (but more explicit) conditions for multiple maturities are found in Section 5.

Section 6 concludes.

2 The consistency problem under bid-ask spreads

Our time index set will be , where ,

and means today.

By a slight abuse of terminology, we will call the integers in

“maturities” and not “indices of maturities”. We write

for the set of positive times in .

Whenever we talk about “the given prices” or similarly,

we mean the following data:

|

|

|

(2.1) |

|

|

|

(2.2) |

|

corresponding call option bid and ask prices (at time zero) |

|

|

|

|

(2.3) |

|

|

|

(2.4) |

We write for the time zero price of a zero-coupon bond maturing at ,

and for the discounted strikes. The symbol denotes

a call option with maturity and strike .

In the presence of a bid-ask spread on the underlying,

it is not obvious how to define the payoff of an option; this issue seems to have been

somewhat neglected in the transaction costs literature. Indeed, suppose that an agent

holds a call option with strike , and that at maturity bid and ask are resp. . Then, the agent might wish to exercise the option to obtain a security

for instead of ,

or he may forfeit the option on the grounds that spending

would earn him a position whose liquidation value is only . The exercise decision

cannot be nailed down without making further assumptions.

In practice, the quoted ticker price of the underlying is the last price at which an actual transaction

has occurred. This price then triggers cash-settled options. However, this approach

is not feasible in our setup, which does not include an order book.

In the literature on option pricing under transaction costs,

it is usually assumed that the bid and ask of the underlying are constant multiples

of a mid-price (often assumed to be geometric Brownian motion). This mid-price

is then used as trigger to decide whether an option should be exercised, followed by

physical delivery [1, 7, 19]. The assumption that such a constant-proportion

mid-price triggers exercise

seems to be rather ad-hoc, though.

To deal with this problem in a parsimonious way, we assume that call options are cash-settled,

using a reference price process . This process

evolves within the bid-ask spread. It is not a traded asset by itself, but just

serves to fix the call option payoff for strike and maturity .

This payoff is immediately transferred to the bank account without any costs.

Definition 2.1.

A model consists of a finite probability space with a discrete

filtration and three adapted stochastic processes

, , and , satisfying

|

|

|

(2.5) |

Clearly, and denote the bid resp. ask price

of the underlying at time .

Note that, in our terminology, the initial bid and ask are part of the given

prices (see (2.4)), and thus the processes in Definition 2.1 are indexed

by and not by .

As for the reference price process , we

do not insist on a specific definition (such as, e.g., ), but allow

any adapted process inside the bid-ask spread.

We now give a definition for consistency of option prices, allowing for

(arbitrarily large) bid-ask

spreads on both the underlying and the options.

Definition 2.2.

The prices (2.1)–(2.4) are consistent with the absence of arbitrage,

if there is a model (in the sense of Definition 2.1) such that

-

•

,

-

•

There is a process such that for

and such that is a

-martingale

w.r.t. the filtration .

The pair is called a consistent price system.

The process is also called a shadow price.

According to Kabanov and Stricker [13] (see also [14]),

these requirements yield an arbitrage free model comprising

bid and ask price processes for the underlying and each call option. Indeed, for the call

with maturity and strike , one may take

as bid price process (and similarly for the ask price), and

as

the process in the second part of Definition 2.2.

We recommend Section 1 of Schachermayer’s recent book [15] as an accessible

introduction to the FTAP under proportional transaction costs.

As mentioned in the introduction, if consistency is defined according to Definition 2.2,

then there is no interplay between the current prices of the underlying and the options,

which seems to make little sense. As an illustration,

the following two-period example shows how frictionless arbitrage strategies may fail in the presence

of a sufficiently large spread;

a general result is given in Proposition 4.1 below.

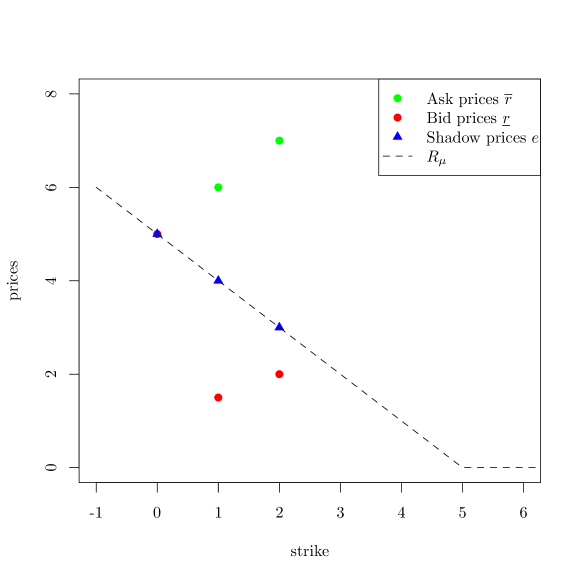

Example 2.3.

Let be arbitrary. We set and assume

|

|

|

Thus is “too expensive”, and without frictions,

buying would be an arbitrage opportunity (upon selling one unit of stock if expires in the money).

In particular, the first condition from Corollary 4.2 in [6] and equation (5) in [5]

are violated: they both state that is necessary for the absence of arbitrage strategies.

But with spreads we can choose as large as we want and still the above prices would be consistent with no-arbitrage.

Indeed, we can define a deterministic model as follows:

|

|

|

Note that

|

|

|

This model is free of arbitrage (see Proposition 4.1 below).

In particular, consider the portfolio : the short call finishes in the money with payoff .

This cannot be compensated by going short in the stock, because its bid price stays at 2.

The payoff at time of this strategy, with shorting the stock at time , is

|

|

|

Our focus will thus be on a stronger notion of consistency, where the discounted spread

on the underlying is bounded. Hence, our goal becomes to determine how large a spread

is needed to explain given option prices.

Definition 2.4.

Let . Then the prices (2.1)–(2.4) are

-consistent with the absence of arbitrage, or simply -consistent,

if they are consistent (Definition 2.2) and the following conditions hold,

|

|

|

|

(2.6) |

|

|

|

|

(2.7) |

The bound (2.7) is an additional mild assumption on the reference

price , made for tractability, and makes sense given

the actual size of market prices and spreads (recall that ).

With the same justification, in our main results on -consistency we will assume that all

discounted strikes are larger than .

If and the bid and ask prices in (2.3)

and (2.4) agree, then we recover the frictionless

consistency definition from [6].

As mentioned above, we do not insist on any specific definition of the reference price .

However, it is not hard to show that choosing yields

almost the same notion of -consistency.

Proposition 2.5.

Let and assume that we are interested in arbitrage free models where,

in addition to the requirements of Definition 2.4,

we have that

|

|

|

(2.8) |

Let us then call the prices (2.1)-(2.4) arithmetically

-consistent.

For , the prices are arithmetically -consistent if and only

if they are -consistent.

Proof.

First, assume that there exists an arithmetically -consistent model with corresponding stochastic processes .

We define new bid and ask prices and .

Then (2.8) implies that .

Therefore, the model consisting of is -consistent.

Conversely, assume that the given prices are -consistent.

Then there exist processes and

on a probability space such that a.s.

We then simply set and , and have thus constructed an arithmetically -consistent model.

∎

Note that the statement of Proposition 2.5

does not hold for consistency (instead of -consistency), nor does it

hold if we replace (2.8) with

|

|

|

where and .

The process does not have to be a martingale,

as is not traded on the market.

The option prices give us some information about the marginals of the process , though.

On the other hand, the process

has to be a martingale, but we have no information about its marginals,

except that .

This implies

|

|

|

(2.9) |

where denotes the infinity Wasserstein distance, and

the law of a random variable. The distance is defined on ,

the set of probability measures on with finite mean, by

|

|

|

The infimum is taken over all probability spaces

and random pairs with marginals .

See [9] for some references on .

For

and random variables and , the condition

is equivalent

to the existence of a probability space with random variables

such that a.s. (This is another result due

to Strassen, see Proposition 4.6 below.)

Definition 2.6.

Let be two measures in . Then we say that is smaller in convex order than , in symbols , if for every convex function we have that , as long as both integrals are well-defined.

A family of measures in is called a peacock, if for all in (see Definition 1.3 in [12]).

For and we define

|

|

|

(2.10) |

the call function of .

The mean of a measure will be denoted by .

These notions are useful for constructing models for -consistent prices,

as made explicit by the following lemma. As is evident from its proof,

the sequence consists of the marginals of a (discounted) reference price,

whereas gives the marginals of a martingale within the bid-ask spread.

The proof uses a coupling result from our companion paper (Lemma 9.1 in [9]).

Lemma 2.7.

For the prices (2.1)–(2.4)

are -consistent with the absence of arbitrage,

if and only if and there are sequences of finitely supported measures

and in such that:

-

for all and , and for ,

-

is a peacock and its mean satisfies , and

-

for all .

Proof.

Let and be as above.

Recall that Strassen’s theorem (Theorem 8 in [17]) asserts that any peacock

is the sequence of marginals of a martingale.

Therefore, there is a finite filtered probability space

with a martingale such that is the law of for .

From (iii), and the remark before Definition 2.6, it follows that there is a

probability space with processes and such that

and for .

As in the the proof of Theorem 9.2 in [9], it is easy to see that the finite support

condition implies that there is a finite probability space with these properties.

The sufficiency statement now easily follows from Lemma 9.1 in [9]. Indeed, that lemma yields

a finite filtered probability space with adapted processes

and satisfying

-

•

is a martingale,

-

•

and for

-

•

for

It then suffices to define

|

|

|

to obtain an arbitrage free model. Note that the second assertion in (ii) ensures that

holds for and not just .

Conversely, assume now that the given prices are -consistent. For ,

define as the law of and as the law of .

It is then very easy to see that the stated conditions are satisfied. As for the finite support condition,

note that the probability space in Definition 2.1 is finite.

∎

To prepare for the central notions of model-independent and weak arbitrage,

we now define semi-static trading strategies in the bank account, the underlying asset,

and the call options. Here, semi-static means that the position in the call

options is fixed at time zero. The definition is model-independent; as soon

as a model (in the sense of Definition 2.1) is chosen, the number of

risky shares in the -the trading period, e.g., becomes

|

|

|

(2.11) |

Definition 2.8.

-

A semi-static portfolio, or semi-static trading strategy, is a triple

|

|

|

where , are Borel measurable

for , analogously for ,

and for .

Here, denotes the investment in the bank account,

denotes the number of stocks held in the period from to ,

and is the number of options with maturity and strike which the investor buys at time zero.

-

A semi-static portfolio is called self-financing, if

|

|

|

holds for and ,

, where

|

|

|

(2.12) |

-

For prices (2.1)–(2.4), the initial portfolio value

of a semi-static portfolio is given by

|

|

|

This is the cost of setting up the portfolio .

-

The liquidation value at time is defined as

|

|

|

Having defined semi-static portfolios, we can now formulate two useful notions of arbitrage.

Definition 2.9.

Let .

The prices (2.1)–(2.4) admit

model-independent arbitrage with respect to spread-bound , if we can form a

self-financing semi-static portfolio

in the bank account, the underlying asset and the options, such that the initial

portfolio value is negative

and the following holds: For all real numbers ,

, that satisfy

|

|

|

|

|

|

|

|

|

|

|

|

(cf. (2.5), (2.6), and (2.7)),

we have .

Definition 2.10.

Let .

The prices (2.1)–(2.4) admit

a weak arbitrage opportunity with respect to spread-bound

if there is no model-independent arbitrage strategy (with respect to spread-bound ),

but for any model satisfying (2.6) and (2.7),

there is a semi-static portfolio such that the initial portfolio value is non-positive,

|

|

|

and

|

|

|

Most of the time we will fix and write only model-independent arbitrage, meaning model-independent arbitrage with respect to spread-bound , and similarly for weak arbitrage.

The notion of weak (i.e., model-dependent) arbitrage was first used in [6], where the authors give examples to highlight the distinction between

weak arbitrage and model-independent arbitrage. The crucial difference is that a weak arbitrage

opportunity may depend on the null sets of the model. E.g., suppose that we would like to use two different

arbitrage strategies according to whether a certain call will expire

in the money with positive probability or not.

Such portfolios could serve to exhibit weak arbitrage (Definition 2.10),

but will not show model-independent arbitrage (Definition 2.9).

4 Multiple maturities: equivalent conditions for consistency

and -consistency

As mentioned in the introduction, our main goal is to find the least bound on the underlying’s

bid-ask spread that enables us to reproduce given option prices.

The following result clarifies the situation if no such bound is imposed

(see also Example 2.3). In our wording, we first seek conditions for

consistency (Definition 2.2) and not -consistency

(Definition 2.4).

Recall the notation used in, and explained before, Theorem 3.1, where is allowed in

(3.1)-(3.4), inducing a dependence of these conditions

on and . In the following proposition, on the other hand, we require

, and therefore the current bid and ask prices

of the underlying are irrelevant when checking consistency of option prices.

Thus, the notion of -consistency seems to make

more sense than consistency.

Proposition 4.1.

The prices (2.1)–(2.4)

are consistent with the absence of arbitrage (see Definition 2.2)

if and only if,

for all , the conditions (3.1)–(3.4) from Theorem 3.1 hold for .

Proof.

By mimicking the proof of the first part of Theorem 3.1 for we see that the conditions are necessary.

Now fix and assume that the conditions hold.

Exactly as in the sufficiency proof of Theorem 3.1, we can construct such that

.

The linear interpolation of the points can

then be extended to a call function of a measure (see the final part of the sufficiency proof of Theorem 3.1).

We define random variables such that the law of is given by .

Then we have that

|

|

|

Furthermore, we pick and set

(Dirac delta) for all .

Clearly, is a peacock, and we set , which implies .

Finally, we define and , and have thus constructed an arbitrage free model.

∎

To prepare for our main result on -consistency in the multi-period model,

we now recall the main result of [9], which gives a criterion

for the existence of the peacock from Lemma 2.7.

Recall also the notation introduced before Definition 2.6.

According to Proposition 3.2 in [9],

for , a measure , and ,

the set

|

|

|

has a smallest and a largest element, and their respective call functions can

be expressed explicitly by the call function of (see (2.10)) as follows:

|

|

|

|

|

|

|

|

where denotes the convex hull.

The main theorem of [9] gives an equivalent condition for the existence of a peacock

within -distance of a given sequence of measures.

Theorem 4.2 (Theorem 3.5 in [9]).

Let and be a sequence in such that

|

|

|

is not empty. Then there exists a peacock

such that

|

|

|

(4.1) |

if and only if for some

and for all , ,

we have

|

|

|

(4.2) |

Here,

depends on and .

In this case it is possible to choose .

We can now give a partial solution to the multi-period -consistency problem.

The existence of the measures from Lemma 2.7 (the marginals

of ) has to be assumed, but the existence of the peacock can be

replaced by fairly explicit conditions, using Theorem 4.2.

Theorem 4.3.

For the prices (2.1)–(2.4)

are -consistent with the absence of arbitrage,

if and only if and there is a sequence of

finitely supported measures in such that:

-

for all and , and for ,

-

There is

|

|

|

such that for all and

|

|

|

where is as in Theorem 4.2 and

for .

Proof.

Immediate from Lemma 2.7 and Theorem 4.2.

∎

As we allow an arbitrary reference price process in Definitions 2.1

and 2.2, our notion of consistency is fairly weak. It can be weakened further

by requiring that the bound (2.6) holds only with a certain probability

instead of almost surely. However, according to the following theorem,

we can always find such a model as soon as the prices are consistent.

Theorem 4.4.

Let and .

For given prices (2.1)–(2.4) the following are equivalent:

-

(i)

The prices satisfy Definition 2.4 (-consistency), but

with (2.6) replaced by the weaker condition

|

|

|

-

(ii)

The prices are consistent with the absence of arbitrage.

For the proof of Theorem 4.4 we employ a result from [9]

on the modified Prokhorov distance.

Definition 4.5.

For and two probability measures on ,

we define the modified Prokhorov distance as

|

|

|

(To define the standard Prokhorov distance, replace by in the right-hand side.)

Note that

A well known result, which was first proved by Strassen, and was then extended by Dudley [8, 17], explains the connection of to minimal distance couplings.

Proposition 4.6.

Given measures on , , and , there exists a probability space with random variables and such that

|

|

|

(4.3) |

if and only if

|

|

|

(4.4) |

The following result shows that, unlike for , there always exists

an approximating peacock w.r.t. for . This explains

why the very weak condition of consistency is sufficent to imply (i)

in Theorem 4.4.

Theorem 4.7 (Theorem 8.3 in [9]).

Let be a sequence in , , and . Then, for all there exists a peacock with mean such that

|

|

|

Proof of Theorem 4.4.

(i) implies (ii) by definition.

To show the other implication,

we define probability measures as in

the proof of Proposition 4.1,

such that for

and .

Now we pick . Then by, Theorem 4.7,

there exists a peacock with mean

such that for all .

We can now use Proposition 4.6 and proceed as in the proof

of Lemma 2.7 to conclude that there exist stochastic processes

and whose marginal distributions

are given by resp. , such that is a martingale and such that

|

|

|

The coupling lemma we use (Lemma 9.1 in [9]) was formulated in [9]

for the special case , but the proof trivially extends to .

We then simply put

|

|

|

5 Multiple maturities: necessary conditions for -consistency

The main result of the preceding section (Theorem 4.3) gives semi-explicit

equivalent conditions for -consistency. The goal of the present section

is to provide explicit necessary conditions.

For a single maturity, the -consistency conditions (Theorem 3.1)

are a generalization of the frictionless conditions in [5, 6].

They guarantee that for each maturity the option prices

can be associated to a measure , such that

(cf. Lemma 2.7).

In this section we state necessary conditions for multiple periods.

Our conditions (see Definition 5.1 and Theorem 5.3)

are fairly involved, and we thus expect that it might not be

easy to obtain tractable equivalent conditions. In the case where there is only a spread on the options, but not

on the underlying, it suffices to compare prices with only three or two different maturities

(see equations (4), (5) and (6) in [5] and Corollary 4.2 in [6])

to obtain suitable consistency conditions. These conditions ensure that the family of measures is a peacock.

If we consider a bid-ask spread on the underlying and

want to check for -consistency according to

Definition 2.4 (), it turns out that

we need conditions that involve all maturities simultaneously (this will become clear

by condition (4.2) below).

We thus introduce calendar vertical baskets (CVB), portfolios which consist of various long and short positions in the call options.

We first give a definition of CVBs.

Then, in Lemma 5.2 we will study a certain trading strategy involving a short position in a CVB.

This strategy will then serve as a base for the conditions in Theorem 5.3,

which is the main result of this section.

Note that our definition of a CVB depends on :

the contract defined in Definition 5.1 only provides necessary conditions in markets

where the bid-ask spread is bounded by .

Definition 5.1.

Fix and and assume that vectors

, , and

are given, such that

-

(i)

for all ,

-

(ii)

and for all ,

-

(iii)

and for all ,

-

(iv)

and either or for all .

Then we define a calendar vertical basket with these parameters as the contract

|

|

|

(5.1) |

The market ask resp. bid-price of are given by

|

|

|

|

|

|

|

|

(5.2) |

We will refer to as the maturity of the CVB.

Lemma 5.2.

Fix .

For all parameters as in Definition 5.1,

there is a self-financing semi-static portfolio whose initial value is given by ,

such that for all models satisfying (2.6) and (2.7)

and for all

one of the following conditions holds:

-

and , or

-

and .

In particular, all corresponding cash-flows are non-negative.

The arguments of are of course the

same as in (2.11), and are omitted for brevity.

In the proof of Lemma 5.2, we define the functions inductively.

As we are defining a model-independent strategy, we could also use the deterministic dummy

variables (2.12)

from Definition 2.8 as arguments. It seems more natural to write

,

though. We just have to keep in mind that

have to be constructed as functions of

, without using the

distribution of these random vectors.

Moreover, note that later on in Theorem 5.3 we will only need the case where , therefore we excluded the case .

Proof of Lemma 5.2.

Assume that we buy the contract

|

|

|

(5.3) |

thus we are getting an initial payment of .

We have to keep in mind that if for some , then the

corresponding expression in (5.3) denotes a long position in the underlying, and if

for some , then the expression in (5.3) denotes a short position in the underlying

plus an additional deposit of in the bank account at time 0

(see the beginning of Section 3).

To ease notation, we will write instead of and instead of .

We will show inductively that after we have traded at time we can end up in one of two scenarios:

either the investor holds a non-negative amount of bank units (i.e., ), we will call this scenario A,

or we have one short position in the underlying (i.e., ) and ;

we will refer to this as scenario B.

Note that scenarios A and B are not disjoint, but this will not be a problem.

We will first deal with the case where and afterwards with the case .

We start with and first assume that .

If expires out of the money, then we do not trade at time 1 and obtain ,

so we are in scenario A.

Otherwise we sell one unit of the underlying, and thus

|

|

|

yielding scenario B. Recall from Section 2 that .

If then .

We do not close the short position in this case and

we get that , so we also get to scenario B.

For the induction step we split the proof into two parts.

In part A we will assume that after trading time we are in scenario A,

and in part B we will assume that at the end of period we are in scenario B.

Part A:

We will show that after we have traded at time

we can end up either in situation A or B.

First we assume that , and so both expressions in (5.3) with maturity denote options (and not the underlying).

Under these assumptions satisfies

|

|

|

Clearly, if or if both options expire out of the money, then ,

and we are in situation A.

So suppose that and that . This also implies that .

If this is the case, we go short one unit of the underlying, and can be bounded from below as follows,

|

|

|

|

|

|

|

|

This corresponds to situation B.

Next assume that and . Then we have that .

After trading time we end up in scenario B,

|

|

|

|

We proceed with the case that and .

As , we can close the long position in the underlying and end up in scenario A at the end of time ,

|

|

|

The case where is easily handled, because the long and the short position simply cancel out.

We are done with part A.

Part B:

Assume that after we have traded at time we are in scenario B, and thus

First we will consider the case where .

If at time the option with strike expires in the money, we do not close the short position and have

|

|

|

|

|

|

|

|

|

|

|

|

which means that we end up in scenario B.

Now we distinguish two cases according to and ,

and always assume that expires out of the money.

If , then we also have that and that .

We close the short position to end up in scenario A,

|

|

|

|

|

|

|

|

If on the other hand and , we do not trade at time to stay in scenario B,

|

|

|

|

|

|

|

|

We proceed with the case where and .

As before, we have , and we can close one short position to stay in scenario B,

|

|

|

|

|

|

|

|

|

|

|

|

If and , then we distinguish two cases:

either expires out of the money, in which case we cancel out the long and short position in the underlying and have

|

|

|

which corresponds to scenario A. Or, expires in the money.

Then we sell one unit of the underlying and hence we end up in scenario B,

|

|

|

|

|

|

|

|

|

|

|

|

In the last inequality we have used that ,

and that .

The case where is again easy to handle, because the long and the short position cancel out

and we are in scenario B at the end of the -st period.

Thus after we have traded at time we are either in scenario A or scenario B, which proves the assertion if .

The proof for is similar.

We will first show that after trading at time 1 we can either be in scenario A or scenario B, and the statement of the proposition then follows

by induction exactly as in the case .

First we assume that . Then, if the option expires out of the money, we are in scenario A;

otherwise we go short in the underlying and have

|

|

|

|

which corresponds to scenario B.

If , then we also have that , and hence we are in scenario B.

∎

According to Lemma 5.2, there is a semi-static, self-financing trading strategy for the buyer of the contract ,

such that only depends on (the investor might have some surplus in the bank account).

In the following we will use this strategy and only write resp.

instead of resp. .

In the case where and we will say that the calendar vertical basket expires out of the money; otherwise we will say that it expires in the money.

The next theorem states necessary conditions for the absence of arbitrage in markets with spread-bound .

Theorem 5.3.

Let , such that and and , , .

Fix prices as at the beginning of Section 2, with

for all .

Then, for all calendar vertical baskets with maturity and parameters and ,

the following conditions are necessary for -consistency,

-

(i)

|

|

|

(5.4) |

-

(ii)

|

|

|

(5.5) |

-

(iii)

|

|

|

|

(5.6) |

-

(iv)

|

|

|

(5.7) |

Proof.

We will assume that and that . The other cases can be dealt with similarly.

In all four cases – we will assume that until time we followed the trading strategy described in

Lemma 5.2.

If (5.4) fails, then we set

|

|

|

and buy , making an initial profit.

If the calendar vertical basket expires out of the money, then we have model-independent arbitrage.

Otherwise we have a short position in the underlying at time . In order to close the short position, we buy units of the underlying at time ,

and we buy units of the underlying at time .

The liquidation value of this strategy at time is then non-negative,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Next, assume that (5.5) fails. Then buying the contract

|

|

|

earns an initial profit.

If expires out of the money, then we leave the portfolio as it is. Otherwise we immediately enter a short position and close it

at time . The liquidation value is then non-negative,

|

|

|

|

|

|

|

|

If (5.6) fails, then we buy the contract for negative cost.

Again we can focus on the case where expires in the money.

We sell one unit of the underlying at time and close the short position at time .

The liquidation value of this strategy at time is non-negative,

|

|

|

We will show that there cannot exist an -consistent model, if (5.7) fails.

In every model where the probability that expires in the money is zero,

we could simply sell and follow the trading strategy from

Lemma 5.2, realizing (model-dependent) arbitrage.

On the other hand, if expires in the money with positive probability, then we can use the same strategy as

in the proof of . At time the liquidation value of the portfolio is positive with positive probability.

∎

Note that, if then has the same payoff as . Keeping this in mind,

it is easy to verify that the conditions from Theorem 5.3 are a generalization of equations (4), (5) and (6) in [5].

It remains open whether (5.4), (5.5), (5.6) and (5.7) are also sufficient for the existence of an -consistent model.

Conjecture 5.4.

Given the conditions stated in Theorem 5.3 the given prices are -consistent with the absence of arbitrage if and only if

(5.4), (5.5), (5.6), and (5.7) hold.

There is weak arbitrage whenever (5.4), (5.5), and (5.6) hold but (5.7) fails.

Theorem 5.3 can be used to find arbitrage opportunities associated with given market prices.

However, it might not be clear how to find parameters that satisfy the conditions

of Definition 5.1. For the reader’s convenience, we finish this section with an algorithm

which can be used to create CVBs given the prices at the beginning of Section 2.

It is not hard to see that it yields all possible parameter configurations.

Once a particular CVB is chosen, its bid price can be obtained via (5.2).

-

(i)

Pick and and set .

-

(ii)

Given , ,

and

first pick .

-

(iii)

Choose distinguishing the following cases:

-

•

if set ;

-

•

if set ;

-

•

if pick ;

-

•

if pick ;

-

(iv)

Set and pick

such that either or .

-

(v)

Appendix A Proof of Theorem 3.1: -consistency

We first show that the conditions are necessary.

Throughout the proof we will denote the option by to ease notation.

Suppose that are such that (3.1) does not hold.

We buy a butterfly spread, which is the contract

|

|

|

and get an initial payment. Its payoff at maturity is positive if expires in the interval and zero otherwise, and so we have model-independent arbitrage.

If (3.1) fails for we buy the contract

|

|

|

and make an initial profit.

Note that denotes the underlying.

At maturity the liquidation value of the contract is given by

|

|

|

which is always non-negative.

Suppose that (3.2) fails for . Then we buy a call spread and invest in the bank account.

This earns an initial profit, and at maturity the cashflow generated by the options is at least , which means that we have arbitrage.

Now we consider the case where . Note that in this case (3.2) is equivalent to

|

|

|

If this fails we buy , sell one unit of the underlying, and invest in the bank account.

Again we earn an initial profit, and at maturity we close the short position and have thus constructed an arbitrage strategy.

If (3.3) fails for , then we buy the call spread and get an initial payment. Its payoff at maturity is always non-negative.

If (3.3) fails for , then we sell and buy one unit of the stock, which also yields model-independent arbitrage.

We show that we cannot find an arbitrage-free model for the given prices, if (3.4) fails.

Later, in Appendix B, we will show that there is a weak arbitrage opportunity in this case

(which entails, according to Definition 2.10, that there is no model-independent arbitrage).

In any model where we could sell . As this option is never exercised, this yields arbitrage.

If on the other hand and , then we buy the call spread at zero cost.

At maturity the probability that the options generate a positive cashflow is positive.

If , then we buy the contract instead, and at maturity the liquidation value of the portfolio

is given by , which is positive with positive probability.

This completes the proof of necessity.

Now we show that the conditions in Theorem 3.1 are sufficient for

-consistency, using Lemma 2.7.

We first argue that we may w.l.o.g. assume that .

Indeed, we could choose

|

|

|

and set . Then all conditions from Theorem 3.1 would still hold,

if we included an additional option with strike and bid and ask price equal to zero.

So from now on we assume that .

We will first show that, for , we can find such that the linear interpolation of the points

, is convex, decreasing,

and such that the right derivative of satisfies . Then we will extend to a call function, and its associated measure will be the law of .

The sequence can then be interpreted as

shadow prices of the options with strikes

Before we start we will introduce some notation.

For we denote the line connecting and by , i.e.,

|

|

|

If is known for some , then we denote the line connecting and

by , i.e.,

|

|

|

The linear interpolation of and will be denoted by ,

|

|

|

We will refer to the slopes of these lines as and respectively.

First we will construct . In order to get all desired properties – this will become clear towards the end of the proof

– has to satisfy

|

|

|

(A.1) |

and

|

|

|

(A.2) |

We will argue that we can pick such an by showing that

|

|

|

(A.3) |

Using (3.2) twice we can immediately see that (A.3) holds for ,

|

|

|

If on the other hand we rewrite the right hand side of (A.3) to , where .

Then from (3.1) we get that

|

|

|

and as the inequality follows.

The above reasoning shows that existence of an such that (A.1) and (A.2) hold.

Next we want to construct for given . It has to satisfy the requirements

|

|

|

(A.4) |

and

|

|

|

(A.5) |

Again we will argue that we can pick such an by considering the corresponding inequalities. First note that the inequality

|

|

|

follows directly from (A.1). Next we want to prove that

|

|

|

(A.6) |

Therefore observe that

|

|

|

If (A.6) follows from (3.1), because . For

we may simply use the fact that and hence we get that

. For we may use to get

|

|

|

where the last inequality follows from the fact that and that

|

|

|

In the last step we used that .

Now suppose we have already constructed . Then for we have that

|

|

|

(A.7) |

and

|

|

|

(A.8) |

Note that for we need an appropriate and in order for (A.7) to hold.

For instance, we can set

and .

We want to show that we can choose such that (A.7) and (A.8) hold for .

First, the inequality

|

|

|

is equivalent to

|

|

|

which is again equivalent to

|

|

|

and holds by (A.8).

The inequality

|

|

|

can be shown using the same arguments as before:

first we note that and then we distinguish between , and .

We have now constructed a finite sequence .

Observe that for all the bounds on from above, namely (A.1) and (A.2) for ,

(A.4) and (A.5) for and (A.7) and (A.8) for , ensure that .

Denote by the linear interpolation of the points . Then is convex,

which is easily seen from

|

|

|

Furthermore, by (A.4)

|

|

|

Finally, is strictly decreasing on which is most easily seen from .

Therefore can be extended to a call function as follows (see Proposition 2.3

in [9]),

|

|

|

Let be the associated measure. Then .

If we define a measure by setting for Borel sets .

The set is defined as . Then .

Similarly, if we define for Borel sets ,

and if then we simply set .

Furthermore for we have that , therefore has support .

Clearly, by definition of , we have that .

Hence, by Lemma 2.7 the prices are -consistent with the absence of arbitrage.