Elicitability and backtesting: Perspectives for banking regulation

Abstract

Conditional forecasts of risk measures play an important role in internal risk management of financial institutions as well as in regulatory capital calculations. In order to assess forecasting performance of a risk measurement procedure, risk measure forecasts are compared to the realized financial losses over a period of time and a statistical test of correctness of the procedure is conducted. This process is known as backtesting. Such traditional backtests are concerned with assessing some optimality property of a set of risk measure estimates. However, they are not suited to compare different risk estimation procedures. We investigate the proposal of comparative backtests, which are better suited for method comparisons on the basis of forecasting accuracy, but necessitate an elicitable risk measure. We argue that supplementing traditional backtests with comparative backtests will enhance the existing trading book regulatory framework for banks by providing the correct incentive for accuracy of risk measure forecasts. In addition, the comparative backtesting framework could be used by banks internally as well as by researchers to guide selection of forecasting methods. The discussion focuses on three risk measures, Value-at-Risk, expected shortfall and expectiles, and is supported by a simulation study and data analysis.

Keywords: forecasting, backtesting, elicitability, risk measurement procedure, Value-at-Risk, expected shortfall, expectiles

1 Introduction

Financial institutions rely on conditional forecasts of risk measures for the purposes of internal risk management as well as regulatory capital calculations. The two ingredients at the heart of risk measurement are the choice of a suitable risk measure and of a forecasting method, with the forecasting method being typically preceded by the choice of a model and estimation method for the (conditional) loss distribution of the underlying portfolio of risky assets. Traditionally, the choice of a risk measure was based on theoretical considerations linked to practical implications. Emmer et al. (2015) give a recent account of the pros and cons of popular risk measures with an attempt to determine the best risk measure in practice. On the other hand, Cont et al. (2010) highlight the need to consider the entire “risk measurement procedure”, which includes not just the choice of a risk measure but also how it is then estimated from the data. In particular, the notion of robustness as sensitivity to outliers is used to compare several risk measurement procedures. In the risk management context, this should also be balanced with robustness to deviations from model assumptions as well as responsiveness or sensitivity to tail events. Davis (2016) introduces a notion of consistency of risk measures and how this is relevant in the context of financial risk management.

The performance of a (trading book) risk measurement procedure can be monitored over time via a comparison of realized losses with risk measure forecasts, a process known as backtesting; see, e.g., Christoffersen (2003) and McNeil et al. (2005). Based on results of a backtest, the risk measurement procedure is deemed as adequate or not. Traditional backtests perform a statistical test for the null hypothesis:

If the null hypothesis is not rejected, the risk measurement procedure is considered as adequate. For Value-at-Risk (VaR), the Bank for International Settlements (2013, p. 103–108) has devised a three-zone approach based on a binomial test for the number of exceedances over the VaR threshold. Traditional backtests are concerned with assessing an optimality property of a set of risk measure estimates; for details see Section 2.2. They are not suited to compare different risk estimation procedures, and they may be insensitive with respect to increasing information sets; examples of this fact are provided in Holzmann and Eulert (2014); Davis (2016). Moreover, traditional backtests may not provide banks with the right incentive of developing procedures which aim for accuracy of risk measure forecasts; for an illustration, see Appendix A. In this simulation-based example, we show how optimization with respect to the test statistic of a traditional backtest may lead to unreasonable ordering of forecasting procedures.

In view of the anticipated revised standardized approach, which “should provide a credible fall-back in the event that a bank’s internal market risk model is deemed inadequate” (Bank for International Settlements, 2013, p. 5–6), Fissler et al. (2016) have recently proposed to replace traditional backtests by comparative backtests based on strictly consistent scoring functions. Comparative backtests also naturally lead to a three-zone approach, which will be described in detail in Section 2.3. Furthermore, they allow for conservative tests and are sensitive with respect to increasing information sets. Roughly, this means that a risk measurement procedure that correctly incorporates more risk factors will always be preferred over a simpler procedure that uses less information. However, comparative backtests necessitate an elicitable risk measure. Examples of elicitable risk measures are VaR and expectiles, while expected shortfall (ES) is not elicitable. However, ES turns out to be jointly elicitable with VaR, which allows for comparative backtests also for ES; for details and a literature review on elicitable risk measures, see Section 2.1.

The paper raises the point of distinguishing between traditional backtesting (current regulatory practice) and comparative backtesting. We highlight the deficiency of the former in giving financial institutions the right incentive for forecast accuracy, and argue that the existing regulatory framework can be enhanced by inclusion of comparative backtesting. On the methodological side, we show that traditional backtesting can be formalized in the form of conditional calibration tests, which provide a unifying framework for many of the existing backtests of popular risk measures. This contributes to our understanding of those often ad hoc procedures and allows us to view them as part of a bigger picture. The paper then provides a detailed investigation of the proposal of comparative backtests.

In our discussion of traditional and comparative backtests, we are focussing on the following three risk measures: VaR, a popular risk measure that is elicitable; expectiles, the only coherent and elicitable risk measures; and ES, a coherent and comonotonically additive risk measure, which is jointly elicitable together with VaR, and which is the new standard measure in banking regulation. VaR at level , denoted , of a random variable is defined as

where is the cumulative distribution function of . From the statistical perspective, is simply the -quantile of the underlying distribution. Positive values of are interpreted as losses in this manuscript, hence we are interested in for values of close to one. The Bank for International Settlements (2013, p.103–108) specifically requests values for , which we refer to as the standard Basel VaR level. ES of an integrable random variable at level is given by

The Bank for International Settlements (2014) proposes as the standard Basel ES level, as should yield a similar magnitude of risk as under the standard normal distribution. As introduced by Newey and Powell (1987), the -expectile of with finite mean is the unique solution to the equation

| (1.1) |

As shown in Bellini et al. (2014); Ziegel (2014), -expectiles are elicitable coherent risk measures for . Expectiles generalize the expectation just as quantiles generalize the median. Considering the level leads to a comparable magnitude of risk as and under the standard normal distribution; see Bellini and Bernardino (2015).

The paper is organized as follows. Section 2 contains the theoretical discussion of backtesting risk measures. In Section 2.1 we define the notion of elicitability, introduce identifiability and review characterizations of consistent scoring functions for VaR, expectiles and (VaR, ES). In Section 2.2 we define what we mean by a calibrated risk measurement procedure and describe how this concept is related to the notion of calibration of Davis (2016) and to traditional backtests in general. We move on to comparative backtests in Section 2.3, where we also explain the comparative three-zone approach. Section 2.3.1 discusses the choice of the scoring function. Section 3 contains numerical illustrations of the proposed backtesting methodologies. We first review some of the existing approaches to forecasting risk measures in Section 3.1. A simulation study is described in Section 3.2, while an application to the returns on the NASDAQ Composite index is presented in Section 3.3. Section 4 concludes the paper with a summary and a discussion of the findings, in particular, in relation to banking regulation. Appendix B contains the necessary background material for computing and estimation of expectiles, and gives a derivation of an extreme value-based estimator; some of the results here are of interest in their own right. Technical results on characterization of consistent scoring functions with positive-homogeneous score differences are delegated to Appendix C. Finally, Appendix D reports results of a simulation study, which investigates the performance of backtesting procedures in the setting where the out-of-sample size is small.

2 Backtesting of risk measures

2.1 Preliminaries

A risk measure is usually defined on some space of random variables. If is law-invariant, it can alternatively be viewed as a map from some collection of probability distributions to the real line . Law-invariance means that for two random variables and that have the same distribution, we have . All risk measures considered in this manuscript are law-invariant. Therefore, we sometimes abuse notation and write instead of , where is the distribution of . Let be a vector of risk measures.

Definition 1.

A scoring function is called strictly consistent for with respect to if

| (2.1) |

for all and all with distribution in . The scoring function is consistent if equality is allowed in (2.1). The vector of risk measures is called elicitable with respect to if there exists a strictly consistent scoring function for it.

Elicitability is useful for model selection, estimation, generalized regression, forecast ranking, and, as we will detail in this paper, allows for comparative backtesting. Elicitable functionals have already been studied in the thesis of Osband (1985), although the terminology has been coined by Lambert et al. (2008). A comprehensive literature review on elicitability can be found in Gneiting (2011), where particular emphasis is on the case . Recent advances on the case can be found in Frongillo and Kash (2015); Fissler and Ziegel (2016).

The question of elicitability of risk measures has recently received considerable attention. All available results in the case are based on the simple but powerful observation that a necessary requirement of elicitability are convex level sets in a distributional sense (Osband, 1985); see also Gneiting (2011, Theorem 6). Weber (2006) was the first to study risk measures with convex level sets. Bellini and Bignozzi (2015) used his results to study elicitability for the broad class of monetary risk measures. Under weak regularity assumptions, they show that elicitable monetary risk measures are so-called shortfall risk measures (Föllmer and Schied, 2002). For more specific classes of risk measures, such as coherent, convex or distortion risk measures, the same result can be shown without any additional regularity assumptions (Ziegel, 2014; Delbaen et al., 2016; Kou and Peng, 2014; Wang and Ziegel, 2015). While expected shortfall is itself not elicitable, Fissler and Ziegel (2016) have shown that the pair is elicitable; see also Acerbi and Szekely (2014).

The classes of (strictly) consistent scoring functions for , -expectiles and have been characterized. The following three propositions state sufficient conditions for (strict) consistency. Under mild regularity assumptions given in the cited literature and up to equivalence, these conditions are also necessary. Here, two scoring functions are called equivalent if their difference is a function of the realization only. Let denote the class of all Borel-probability distributions on , and let denote the class of all distributions with finite mean.

Proposition 1 (Thomson (1979); Saerens (2000)).

All scoring functions of the form

| (2.2) |

where is an increasing function on , are consistent for , , with respect to . The scoring functions of the above form are stricly consistent for with respect to if is stricly increasing, is integrable for all with distribution in , and all distributions in have a unique -quantile.

Proposition 2 (Gneiting (2011)).

All scoring functions of the form

| (2.3) |

where is a convex function with subgradient , are consistent for the -expectile, , with respect to . If is strictly convex, then the scoring functions of the above form are strictly consistent for the -expectile relative to the class such that is integrable for all with distribution in .

Proposition 3 (Fissler and Ziegel (2016)).

All scoring functions of the form

| (2.4) |

where is an increasing function, and is increasing and concave, are consistent for , , with respect to . If is strictly increasing and strictly concave, then the above scoring functions are strictly consistent with respect to the class of distributions which have unique -quantiles and is integrable for all with distribution in .

In risk management applications, it may be useful to allow only for strictly positive risk measure predictions. As shown in Section 2.3.1, this opens up the possibility for attractive choices of homogeneous scoring functions in the above propositions. If is assumed in (2.2) or (2.3), then, for strict consistency, we only need that or are defined on , and that they are strictly increasing or strictly convex on this domain, respectively. In the case of (2.2) this can be checked by a fairly straightforward computation. For the claim concerning (2.3), it is useful to use the decomposition of the score difference derived in the proof of Gneiting (2011, Theorem 10). Furthermore, it is sufficient to require intergrability of or for all with distribution in . If we restrict to predictions with in (2.4), only has to be defined on and has to be strictly increasing and strictly concave on this domain.

Closely connected to elicitability is the concept of identifiability. In fact, for , identifiability implies elicitability under some additional assumptions; see Steinwart et al. (2014). For , it is currently unclear whether such a general result holds; see Fissler and Ziegel (2016).

Definition 2.

The vector of risk measures is called identifiable with respect to , if there is a function such that

for all with distribution in .

Identification functions are not uniquely defined. In fact, one can multiply any identification function for a functional by a function depending only on the prediction and taking values in the space of invertible -matrices to obtain another identification function for the same functional.

for is identifiable with respect to the class of distributions with unique quantiles with identification function

| (2.5) |

the -expectile for is identifiable with respect to using the identification function

| (2.6) |

and for the level has identification function

| (2.7) |

with respect to .

2.2 Calibration and traditional backtests

We fix the following notation. Suppose that is an identifiable functional with identification function with respect to . Let be a series of negated log-returns adapted to the filtration and a sequence of predictions of , which are -measurable. Hence, the predictions are based on the information about available at time represented by the sigma-algebra . Let denote the conditional law of given the information . We assume that all conditional distributions and all unconditional distributions belong to almost surely.

Inspired by the insightful paper of Davis (2016), we give the following definition.

Definition 3.

The sequence of predictions is calibrated for on average if

it is super-calibrated for on average if component-wise, for all . The sequence of predictions is conditionally calibrated for if

it is conditionally super-calibrated for if component-wise, almost surely, for all . Sub-calibration is defined analogously.

If one knows the conditional distributions and strives for the best possible prediction of based on the information in , it is natural to use

| (2.8) |

as a predictor, which we term the optimal -conditional forecast for . For the same reason, we call the optimal unconditional forecast. Recall that we freely abuse notation in using either as a functional defined on a space of random variables or on a space of probability distributions.

Calibration characterizes optimal forecasts in the following sense. The optimal unconditional forecast is the only deterministic forecast that is calibrated for on average. However, there may be other forecasts that are calibrated for on average which are not deterministic and thus different from the optimal unconditional forecast. Likewise, the optimal conditional forecast is the only -predictable conditionally calibrated forecast for up to almost sure equivalence. It is clear that conditional calibration implies calibration on average by the tower property of conditional expectations but the converse is generally false. The notions of calibration introduced here are analogous to the notions of cross-calibration for probabilistic forecasts introduced in Strähl and Ziegel (2015).

We have introduced the notions of super- and sub-calibration as they can often be related to over- or under-estimation of the risk measure at hand. However, this depends on the specific identification function, so some care must be taken. We give details for a correct interpretation for VaR, expectiles and (VaR,ES) in Section 2.2.2.

For simplicity, we focus on one-step ahead predictions in this paper. Clearly, multi-step ahead predictions are equally important. In some instances the same theory and concepts can be transferred from the former case to the latter.

Following Fissler et al. (2016), we call any backtest that considers a null hypothesis of the type “The risk measurement procedure is correct” a traditional backtest. Traditional backtests are similar to goodness-of-fit tests, that is, they allow to demonstrate that the risk measurement procedure under consideration is making incorrect predictions, if the respective null hypothesis can be rejected. Despite the somewhat misleading terminology that a traditional backtest is passed if the null hypothesis is not rejected, this does not mean that in this case, one can be sure that the null hypothesis is correct (with a pre-specified small probability of error) as this would necessitate that we control the power of the test explicitly. This can virtually never be done as the alternative is too broad; see also Bank for International Settlements (2013, p. 103–105). As argued by Fissler et al. (2016), these issues may put the use of traditional backtest in regulatory frameworks in question. However, they may be useful for model verification just as goodness-of-fit tests have their established role in statistics.

Testing the null hypothesis

| (2.9) |

amounts to performing a traditional backtest. We describe here how tests for average calibration can be constructed but we do not implement them because the stronger notion of conditional calibration appears more adequate in a dynamic risk management context. In our data example in Section 3.3, for the more flexible models, the null hypothesis of conditional calibration cannot be rejected which indicates that testing for average calibration is superfluous. However, there may be situations where achieving average calibration is already difficult and then the following tests may be useful.

Given a series of observations and forecasts , we define . Let be a heteroscedasticity and autocorrelation consistent (HAC) estimator of the asymptotic covariance matrix (see, e.g., Andrews (1991)). Then, one can hope that is asymptotically standard normal under suitable assumptions on the identification function and the data generating process. For , sufficient mixing assumptions are detailed in Giacomini and White (2006, Theorem 4) but a multivariate generalization of this result remains to be worked out. Giacomini and White (2006, Theorem 4) show that, for , the test is consistent against the alternative for all sufficiently large, for any .

Conditional calibration is a stronger notion than average calibration, and it appears more natural in a dynamic risk management context. A traditional backtest for conditional calibration considers the null hypothesis

| (2.10) |

The requirement , almost surely, is equivalent to stating that for all -measurable -valued functions . Following Giacomini and White (2006), we consider an -predictable sequence of -matrices called test functions to construct a Wald-type test statistic:

| (2.11) |

where

is a consistent estimator of the variance of the -vector . Ideally, the parameter should be chosen such that the rows of generate . In applications, the choice of the test functions is motivated by the principle that they should represent the most important information available at time point . In our simulation study, we obtained good results with or ; for further details see Section 3.2.2. We call this type of traditional backtests conditional calibration tests. In cases where , we refer to these tests as simple conditional calibration tests. Theorem 1 in Giacomini and White (2006) says that, under the null hypothesis (2.10), as , subject to certain assumptions on the data generating process and test function sequence . This asymptotic result justifies a level test which rejects when , where denotes the quantile of the distribution. Giacomini and White (2006, Theorem 3) provide conditions such that as for multi-step ahead predictions, while Theorem 2 of Giacomini and White (2006) considers consistency of the test against global alternatives. The theorems of Giacomini and White (2006) are formulated in terms of score differences and not identification functions but their proofs solely rely on the martingale difference property of and can thus be applied in our context.

Commonly used backtests for and are closely related to conditional calibration tests for specific choices of the test functions . In fact, choosing in the case of , the conditional calibration test for is closely related to the standard backtest for based on the number of VaR exceedances (Bank for International Settlements, 2013, p.103–108). In the case of , the conditional calibration test for is related to the backtest for of McNeil and Frey (2000) based on exceedance residuals. We give further details in Examples 1, 2, and 3 below.

The notion of a calibrated risk measure (or statistic) of Davis (2016) is closely related to our notion of a calibrated sequence of predictions. Davis (2016) considers which risk measures are calibrated for which classes of models. That is, he attempts to characterize the largest class of data generating processes such that goes to zero a.s. as if is a sequence of optimal conditional forecasts for the risk measure. It turns out that for quantiles only minimal assumptions are necessary, whereas assumptions need to be stronger to work with the mean, for example. The focus of our work is more statistical. Choosing -predictable test functions encoding the available information at time point , we investigate whether and how it is possible to test in finite samples that the sequence is conditionally calibrated.

2.2.1 One-sided calibration tests

In certain situations, it may be meaningful to assess super- or sub-calibration. For example, the standard backtest for described in (Bank for International Settlements, 2013, p.103–108) is a test for conditional super-calibration. This is due to the fact that over-estimation of is not a problem as far as the regulator is concerned. Holding more capital then minimally required should always be allowed.

Suppose we wish to test the hypothesis of conditional super-calibration that component-wise, for all . That is, in the case of a -variate risk measure, we are interested in , where

For each component of the risk measure, let be an -measurable -vector of non-negative test functions. If generate then , where

We combine all of the test functions into a matrix with , which has the following structure:

Setting , the above hypothesis of conditional super-calibration can alternatively be expressed as with for all . .

From the proof of Giacomini and White (2006, Theorems 1 and 3) it follows that under given at (2.10),

| (2.12) |

where denotes the identity matrix. Hence, we can obtain an asymptotic test for with the p-value given by , . That is, is the (asymptotic) probability of obtaining a more extreme outcome than the one observed, assuming the null hypothesis is true. Let be the ordered p-values. The classical Bonferroni multiple test procedure rejects the global null hypothesis if the smallest of the p-values , where is the desired level of the (global) test. As an alternative, following Hommel (1983), we obtain a level test by rejecting the global hypothesis if for at least one we have

| (2.13) |

Hommel’s rejection rule has the advantage of allowing to detect situations with both small effects in many components and with large effects in few components. Other testing procedures in this context could also be used.

2.2.2 Examples

Example 1.

Christoffersen (1998) calls a sequence of forecasts efficient with respect to if

This requirement is the same as the one of conditional calibration of by (2.5). In fact, the dynamic quantile test of Kuester et al. (2006) (see also Christoffersen (1998); Engle and Manganelli (2004)) has similarities to a conditional calibration test. In analogy to their test, it is natural to consider test functions

for . This is also in line with the suggestion in Giacomini and White (2006), who use .

The standard backtest for specified in the Basel documents (Bank for International Settlements, 2013, p.103–108) uses the test statistic

which is the number of exceedances over the estimated , denoted , for time point . Under the null hypothesis (2.10) of conditionally calibrated -forecasts, for one-step ahead forecasts, is a binomial random variable with parameters and ; see Rosenblatt (1952); Diebold et al. (1998); Davis (2016). It is remarkable that this result holds under essentially no assumptions on or . However, when moving away from one-step ahead forecasts to multi-step ahead forecasts, things become more intricate and one has to resort to general limit theorems such as presented above for testing if has mean . This test is a test for conditional super-calibration with , because for , we obtain using (2.5)

thus, testing the null hypothesis that has mean less or equal to is equivalent to testing that has mean greater or equal to zero. This null hypothesis says that the conditional VaR predictions are at least as large as the true conditional VaR. Assuming that it is an incentive of a bank to state VaR estimates that tend to be lower than the true ones, a more prudent null hypothesis from the viewpoint of a regulator would be the opposite one-sided hypothesis that the conditional VaR predictions are at most as large as the true conditional VaR, that is, a test for conditional sub-calibration.

For one-step ahead predictions, alternatively to theory presented in this section, one can exploit the fact that the exceedance indicators , at the boundary of the null hypothesis, are independent Bernoulli random variables with success probability , which allows for an exact test rather than an asymptotic one.

Example 2.

We consider the vector of risk measures for some . Let and denote forecasts of and , respectively. Assuming , where and are -measurable and the ’s form an independent and identically distributed (i.i.d.) sequence of random variables with zero mean and variance one, for backtesting ES, McNeil and Frey (2000) introduced the following test statistic based on exceedance residuals:

| (2.14) |

It turns out that the ES backtest of McNeil and Frey (2000) is closely related to a conditional calibration test as follows. For reasonably large, we have that . Therefore, for the test statistic in (2.14), we obtain

with . Replacing by an estimate is natural when considering the test of McNeil and Frey (2000) as a conditional calibration test. The estimated volatility is then simply a part of the -measurable test function sequence that supposedly encodes the relevant information of . Of course, this test is only reasonable if is estimated as part of the forecasting model with the information at time point . The recently proposed backtests for ES of Acerbi and Szekely (2014) are in the same spirit as the test of McNeil and Frey (2000).

The backtest for ES suggested by Costanzino and Curran (2015) tests if the whole tail of the distribution beyond the -level has been estimated correctly. Strictly speaking, the test is therefore not a test for the accuracy of a sequence of point forecasts for but rather a test for the accuracy of a sequence of probabilistic forecasts for tomorrow’s loss distribution with emphasis on the left tail. Other tests in this spirit but of comparative type can be found in Gneiting and Ranjan (2011).

As ES is only identifiable jointly with VaR, one has to be careful when formulating a one-sided test for ES. Let . Then it holds for all that

This shows that, similarly to the VaR case, testing the null hypothesis of sub-calibration for the ES component is equivalent to testing that . Hence, the test of conditional sub-calibration of (VaR, ES) is a test that the conditional VaR and ES predictions are at least as large as their optimal conditional predictions. The Hommel’s procedure described in Section 2.2.1 can then be applied with p-value , where the ’s are defined in (2.12).

Example 3.

One could conceive a backtesting framework for expectiles as well, in a similar spirit to the ES backtesting procedure proposed by McNeil and Frey (2000). Assuming, as in the example above, that , where and are -measurable and the ’s are i.i.d. with zero mean and variance one, the conditional -expectile satisfies

and we see that the residuals

form an i.i.d. sequence of random variables with zero -expectile. This implies that with given at (2.6) is an i.i.d. sequence of random variables with mean zero, which can be tested using a bootstrap (as in Efron and Tibshirani (1993), Section 16.4). Here it is necessary to replace the true volatility by an estimate. This is analogous to the suggestion of McNeil and Frey (2000) for ES. Noticing that the identification function for expectiles at (2.6) is positively 1-homogeneous, we obtain that

This equality suggests that it is natural to perform a conditional calibration test for expectiles with test function and test statistic given at (2.11). This yields a valid asymptotic test under the assumptions in Giacomini and White (2006, Theorem 1). These assumptions are weaker than the model assumption .

In the case of expectiles, as in the case of VaR, a test for conditional super-calibration assesses the null-hypothesis that all conditional expectile estimates are at least as large as the true conditional expectile.

2.3 Elicitability, forecast dominance and comparative backtests

Suppose now that the functional is elicitable with respect to . Let be a series of negated log-returns adapted to the filtration as well as to the filtration . Let and be two sequences of predictions of , which are and -predictable, respectively. We assume that all conditional distributions , and all unconditional distributions belong to almost surely. We refer to the predictions as the standard procedure, while is the internal model. The two filtrations and acknowledge the fact that the internal model and the standard model may be based on different information sets. For example, one model may include more risk factors than the other, or, certain expert opinion may be used to adjust one model but not the other.

Definition 4.

Let be a consistent scoring function for with respect to . Then, -dominates (on average) if

Furthermore, conditionally -dominates if

| (2.15) |

The definition of conditional dominance is asymmetric in terms of the role of the standard procedure and the internal procedure. The standard procedure and the information it is based on are considered as a benchmark of predictive ability, which is why we condition on and not on . Any method that dominates the benchmark has superior predictive ability relative to this benchmark.

Clearly, conditional -dominance implies -dominance on average. Ehm et al. (2016, Definition 2) introduced the notion of dominance of one sequence of predictions over the other if one -dominates the other on average for all consistent scoring functions for . The notion of dominance is a strong one. That is, in the data examples of Ehm et al. (2016) it was almost never observed that one forecast dominates the other. This makes the concept difficult to employ in an applied decision making context. Furthermore, currently, a clear theoretical understanding of the notion of dominance remains elusive.

There are several reasons why the predictions should be preferred over if the former dominates the latter. Firstly, comparison of forecasts with respect to the described dominance relations is consistent with respect to increasing information sets. That is, if for all and , are the optimal conditional forecasts with repect to their filtrations as defined at (2.8), then the internal procedure dominates the standard procedure, both, conditionally and on average (Holzmann and Eulert, 2014, Theorem 1). The same is true if is -conditionally optimal and is just -predictable (Holzmann and Eulert, 2014, Corollary 2); see also Tsyplakov (2014).

Secondly, in the case , for most important functionals, including VaR and expectiles, strictly consistent scoring functions are order sensitive or accuracy rewarding in the following sense. Essentially, if or for some random variable , then

| (2.16) |

see Nau (1985); Lambert (2012) for details. Therefore, if the risk measure forecasts are always closer than to the optimal -conditional forecast, that is, or for all almost surely, then conditionally dominates . There are different proposals for notions of order sensitivity in the case ; see, for example, Lambert et al. (2008), but the situation is less clear in this case.

The condition for conditional -dominance in (2.15) can be formulated equivalently as

for all . It is tempting to work with a vector of -predictable test functions in order to test for conditional -dominance as suggested in the conditional calibration tests. However, we are interested in comparing the standard procedure to the internal procedure and reach a definite answer as to which one is to be preferred. If but for different components of the vector , no clear preference for either method can be given. Therefore, we do not pursue this approach further.

In comparative backtesting we are interested in the null hypotheses

| The internal model predicts at least as well as the standard model. | |||

| The internal model predicts at most as well as the standard model. |

The null hypothesis is analogous to the null hypothesis of a correct model and estimation procedure but now adapted to a comparative setting. As mentioned in the introduction, considering a backtest as passed if the null hypothesis cannot be rejected is anti-conservative or aggressive in nature and may therefore be problematic in regulatory practice. On the other hand, the null hypothesis is such that the comparative backtest is passed if we can reject . This means that we can explicitly control the type I error of allowing an inferior internal model over an established standard model.

We assume in the remainder of the paper that the limit

| (2.17) |

exists (while we allow it to take the values ). It is clear that -dominance on average implies . If the sequence of score differences is first-order stationary, then implies -dominance on average. Under Assumption (2.17), we can compare any two sequences of risk measure estimates with respect to their predictive performance. It is a weak assumption as it requires slightly more than that the average expected score differences are eventually of the same sign. It may be weakened at the cost of further technicalities which we have chosen to avoid. If the limit in (2.17) is non-positive, then the internal procedure is at least as good as the standard procedure, whereas the internal procedure predicts at most as well as the standard procedure if . Ordering risk measurement procedures is a compromise in the quest for conditional dominance. On the one hand, it is clearly a weaker notion than conditional dominance, but on the other hand it introduces a meaningful total order on all risk measurement procedures given a sensible choice of the scoring function ; see Section 2.3.1.

Therefore, we reformulate our comparative backtesting hypotheses as

The test statistic

for large enough, has expected value less or equal to zero under , whereas under its expectation is non-negative. Tests of or based on a suitably rescaled version of are so-called Diebold-Mariano tests; see Diebold and Mariano (1995). Under certain mixing assumptions detailed in Giacomini and White (2006, Theorem 4),

is asymptotically standard normal with an HAC estimator of the asymptotic variance, . Therefore, using the test statistic

| (2.18) |

we obtain an asymptotic level -test of if we reject the null hypothesis when , and of if we reject the null hypothesis when .

Based on the outcome of the tests of and , Fissler et al. (2016) suggest the following three-zone approach. We fix a significance level , for example, . If is rejected at level , then will not be rejected at level . Similarly, if is rejected at level , then will not be rejected at level . Therefore, we say that the internal procedure is in the red region, that is, it fails the comparative backtest if is rejected. The internal procedure is in the green region, that is, it passes the backtest, if is rejected. The internal procedure needs further investigation, that is, it falls in the yellow region, if neither , nor can be rejected. For an illustration of these decisions, see Fissler et al. (2016, Figure 1).

There is one important difference between the three-zone approach described in Bank for International Settlements (2013, p.103–108) for traditional VaR backtests and the three-zone approach of Fissler et al. (2016) described here. In the former approach, the zones arise from varying the confidence level of the hypothesis test, whereas in the latter approach the confidence level is fixed a priori, and the zones arise to separate cases where there is enough evidence to clearly decide for superiority of one procedure over the other in contrast to cases where there is no clear evidence.

2.3.1 Choice of the scoring function

Based on (2.2), (2.3) and (2.4), one has a large number of choices for strictly consistent scoring functions for VaR, expectiles and (VaR, ES). In the case of , the standard choice is to take in (2.2) leading to the classical asymmetric piecewise linear loss, see (2.19) below, also known as linlin, hinge, tick or pinball loss; see Koenker (2005) for its relevance in quantile regression. In the case of expectiles, one could argue that a natural choice is taking in (2.3), which simplifies to the squared error function for the mean (up to equivalence). This is also the scoring function suggested by Newey and Powell (1987) for expectile regression. Consistent scoring functions for (VaR, ES) have only recently been discovered; see Acerbi and Szekely (2014); Fissler and Ziegel (2016). Therefore, there is no natural classical choice for the functions , in (2.4).

A scoring function is called positive homogeneous of degree (or -homogeneous) if for all and all

Efron (1991) argues that it is a crucial property of a scoring function to be positive homogeneous in estimation problems such as regression. Patton (2011) underlines the importance of positive homogeneity of the scoring function for forecast ranking. Positive homogeneous scoring functions are also favorable because they are so-called “unit consistent”; see, for example, Acerbi and Szekely (2014). That is, if and are given in say U.S. dollars with and , then, for a positive homogeneous scoring function , the score will have unit . In particular, changing the units, from, say, U.S. dollars to million U.S. dollars, will not change the ordering of forecasts assessed by this scoring function, and will thus also leave the results of comparative backtests unchanged. Concerning the choice of the degree of homogeneity, Patton (2006) shows that in the case of volatility forecasts, requires weaker moment conditions than a larger choice of for the validity of Diebold-Mariano tests which are used in comparative backtesting. Concerning the power of Diebold-Mariano tests, Patton and Sheppard (2009) find the best overall power for volatility forecasts for the choice .

Appendix C presents results, which characterize positive homogeneous scoring functions for the risk measures that are of interest in this paper. Note that we only allow for predictions or with . As we are interested in risk measures for losses, this is not a real restriction; see also Section 3.2.

For some orders of homogeneity , there is no strictly consistent scoring function for the risk measures of interest in this paper. In particular, the attractive choice can often not be realized. However, for comparative backtesting we are not interested in absolute values of expected scores but only in differences of expected scores. Therefore, it is sufficient to have a scoring function such that the resulting score differences are homogeneous. Such homogeneous score differences of order exist for VaR, expectiles and (VaR,ES) as shown by the results in Appendix C. Examples below list scoring functions, which will be used subsequently in the simulation study and real data analysis.

Example 4.

For the comparative backtests for VaR that we investigate in Section 3.2, we consider the classical 1-homogeneous choice obtained by choosing in (2.2) leading to the scoring function

| (2.19) |

Guided by the arguments given above, we alternatively consider the 0-homogeneous score differences by choosing , which leads to the score

| (2.20) |

Example 5.

Example 6.

Acerbi and Szekely (2014) proposed a class of 2-homogeneous scoring functions for depending on a parameter . It is strictly consistent when the class of distributions is restricted to contain only distributions with

In practice, it is generally not possible to say what magnitude of is realistic to cover all possible applications. Therefore, we prefer to work with the homogeneous choices of strictly consistent scoring functions above and, more generally, of the form in Theorem C.3.

3 Numerical illustrations

3.1 Forecasting of risk measures

In this section we discuss a number of estimation procedures for producing conditional forecasts of the three risk measures discussed in this paper, namely the VaR, expectile and ES. Owing to the widespread use of VaR in the banking sector, a great number of methods exist to produce its point forecasts; see, e.g., Kuester et al. (2006) for an extensive review. In contrast, estimation and forecasting of expectiles in the risk measurement context is a relatively recent topic; see, e.g., Kuan et al. (2009). However, in many cases, similar methods as those used for VaR forecasting can be adopted for expectiles.

For illustrative purposes, we consider the following framework for forecasting of the risk measures. Suppose the series of negated log-returns can be modeled as

| (3.1) |

where is a sequence of i.i.d. random variables with zero mean and unit variance, and and are measurable with respect to the sigma algebra , representing the information about the process available up to time . In order to capture typical time dynamics of financial time series, one possibility is to assume that the conditional mean follows an ARMA process, while the condition variance evolves according to a GARCH model specification.

Let denote any of the three risk measures we consider. In the above setting, conditionally on the information up to time , the one-step ahead forecast of is

| (3.2) |

where is used to denote a generic random variable with the same distribution as the ’s. Following McNeil and Frey (2000) and Diebold et al. (2000), one can adopt a two-stage estimation procedure for the forecast . First and are estimated via the maximum likelihood procedure under a specific assumption111An alternative is to use the quasi-maximum likelihood estimation (MLE) procedure in which innovations are assumed to be standard normal. This is justified by the result in Bollerslev and Wooldridge (1992) saying that and would be consistently estimated even if the distribution of innovations is not normal, provided that the models for and are correctly specified. As pointed out in Kuester et al. (2006), the correct specification of dynamics for and may be difficult to fulfil in practice. on the distribution of the innovations in (3.1). The second stage involves estimation of , the risk measure for i.i.d. sequence , based on the sample of standardized residuals

| (3.3) |

We consider the following three approaches to handle the second stage in the forecasting procedure: fully parametric (FP), filtered historical simulation (FHS), and a semi-parametric estimation based on extreme value theory (EVT).

3.1.1 Fully parametric estimation

Under the fully parametric approach, a specific (parametric) model is assumed for the sequence of innovations . Examples of typically used probability distributions include the normal, Student’s t and a skewed t distribution (see, e.g., Fernandez and Steel (1998)). Parameters of the assumed distribution for ’s, denoted , can be estimated based on the standardized residuals in (3.3) using, for example, the maximum likelihood method. If the model for ’s coincides with the one used to estimate the filter in the first stage, then no additional estimation is required at the second stage with all model parameters coming directly from the first stage estimation. The fitted distribution is used to compute the estimate of a given risk measure. In the case of , this is given by the -quantile, , whereas a -expectile can be computed as discussed in Appendix B.1, where we give analytic expressions for expectiles of several commonly used distributions. Since we consider only continuous distributions , the ES can be computed as

where we use numerical integration to evaluate the conditional expectation.

3.1.2 Filtered historical simulation

The method employs a non-parametric estimation of the risk measures based on the standardized residuals in (3.3), which can be seen as representing a filtered time series; see, e.g., Christoffersen (2003, Chapter 5.6). In particular, we draw a sample of a large size (e.g., ) from and then take the empirical estimate of a given risk functional as the estimate for . The empirical -quantile gives the VaR estimate . The empirical -expectile is obtained using the least asymmetric weighted squares via iterative minimization of

The ES is estimated by the empirical version of the conditional expectation given that the residual exceeds the corresponding VaR estimate:

3.1.3 EVT-based semi-parametric estimation

Risk is naturally associated with extremal events, and hence risk measure estimates rely on accurate estimation of a tail of the underlying distribution. However, inference about the distributional tails is notoriously difficult as there are frequently not enough data points in the tail regions neither to give a proper justification for a parametric model nor to obtain reliable empirical estimates. Hence, unless a sufficiently long time series is available relative to the desired risk level for risk measure estimation, the two methods outlined in Sections 3.1.1 and 3.1.2 are unlikely to produce accurate forecasts. An alternative is to base estimation on asymptotic results of extreme value theory (EVT). For a detailed account, refer to, e.g., Embrechts et al. (1997).

The main premise is that, for a sufficiently high threshold , conditional excesses of random variable satisfy:

| (3.4) |

where denotes the generalized Pareto distribution with scale and shape parameter . It is common in applications to set the threshold at an upper order statistic; i.e., for some , where are the decreasing order statistics of the sample from . This leads to the following EVT-based estimates of and (see McNeil and Frey (2000)):

| (3.5) |

and

| (3.6) |

with being parameter estimates of the GP distribution fitted to excesses over . In the spirit of the above EVT-based estimators for VaR and ES, we derive an estimator for the -expectile. The details are provided in Appendix B.2.

In the discussion above we assume that threshold or equivalently , the number of upper order statistics, is given so as to ensure adequacy of the approximation in (3.4). However, in practice, an accurate choice has to be made to balance the bias-variance trade-off as a too large value of increases variability of the parameter estimates of and , while insufficiently large introduces the bias due to invalidity of (3.4). Various techniques have been proposed to assist with the choice of threshold such as graphical tools based on linearity of the mean excess function. As such methods require judgement at every time step at which conditional forecasts of risk measures are to be made, they are prohibitive for our purposes. Hence, we adopt a pragmatic approach as in McNeil and Frey (2000), and take in samples of size .

3.2 Simulation study

In practice, traditional backtesting is perhaps the most commonly used way to evaluate and subsequently choose among a number of competing forecasting procedures. While traditional backtesting is certainly suitable to capture some aspects of forecasting procedures, it does not provide information on the relative performance of different procedures with respect to the accuracy of forecasts, a seemingly natural criterion for a forecasting method. The aim of the present simulation study is to illustrate the use of the methodologies for traditional and comparative backtests discussed in the paper as well as to highlight the different messages delivered by the two types of backtests.

3.2.1 Set-up and forecasting methods

The data used for the analysis are generated from an AR(1)-GARCH(1,1) process:

| (3.7) |

where innovations form a sequence of independent random variables with a common skewed t distribution (see Example B.6) with shape parameter and skewness parameter .

Quality of a forecasting procedure is determined by various factors. In a parametric or semi-parametric set-up, potential model misspecification as well as estimation uncertainty in small samples can be detrimental for prediction. Non-parametric methods, while requiring no assumptions on the underlying model, are also subject to sampling variability and have strong limitations when dealing with extreme or tail events. The forecasting procedures we consider in the simulation study aim to cover a spectrum of models and estimation methods. We assume that the underlying process follows an AR(1)-GARCH(1,1) dynamics with innovations coming from one of the following three distributions: the normal, the Student’s t and the skewed t distribution as in Example B.6. We then consider the following estimation procedures:

-

•

fully parametric estimation (Section 3.1.1) with the methods abbreviated as ”n-FP”, ”t-FP” and ”st-FP” under the assumption of normal, t and skewed t distributed innovations, respectively;

-

•

filtered historical simulation (Section 3.1.2) with the methods abbreviated as ”n-FHS”, ”t-FHS” and ”st-FHS”;

-

•

EVT-based estimation (Section 3.1.3) with the methods abbreviated as ”n-EVT”, ”t-EVT” and ”st-EVT”.

In addition to the above-mentioned methods, we supplement results with the optimal forecasts (abbreviated as ”opt”), which uses the knowledge of the data generating process. Estimation is conducted using the moving window of size 500, and forecasts are evaluated based on the out-of-sample size of 5000 verifying observations.

3.2.2 Backtesting of risk measure forecasts

Table 1 contains an overview of the one-step ahead forecasts obtained under the procedures described in the previous section. In particular, we report the average forecasts based on the series of moving estimation windows for each of the three considered risk measures, denoted , and . The levels for VaR are chosen in accordance with typical values used for internal risk management (such as and ) as well as the standard Basel VaR level . For expectiles and ES, the levels are selected in such a way that the risk measure forecasts agree under the standard normal model.

In order to link to the previously used approaches to assess the quality of VaR forecasts (and to make comparisons between the methods), we computed the percentage of times the observations exceeded the forecasts, commonly referred to as the percentage of violations. Based on the values reported under the column ”% Viol.” in Table 1 , we observe that some of the misspecified models were actually able to hit nearly exactly the expected proportion of violations by matching the risk measure level . This is the case, for instance, for ”n-EVT” and ”t-EVT” methods at . Although large deviations from the risk measure confidence level do suggest substantial method deficiencies (as in the case of ”n-FP” and ”t-FP” methods), these values also highlight that the deviations from the level alone are unlikely to provide a good basis for differentiating the methods’ performance in terms of prediction.

Table 2 illustrates the traditional backtesting methodology presented in Section 2.2. Test statistics in (2.11) and in (2.12) are used, respectively, for two-sided and one-sided conditional calibration tests. The one-sided tests for and -expectile are tests for super-calibration with p-values given by . In the case of , we make use of the Hommel’s procedure with the adjusted p-values computed as and capped at one, where for the one-sided tests of sub-calibration; see (2.13). (The classical Bonferroni multiple test procedure resulted in qualitatively similar conclusions.) For the simple conditional calibration tests, we set . The test functions that were found to work well in this simulation study for general conditional calibration tests are

| (3.8) |

in the case of two-sided tests, and

| (3.9) |

in the case of one-sided tests. The choice of test functions is important as it affects the properties of the test. For example, we found that inclusion of the lagged values of the identification function as in Example 1 resulted in tests which rejected all of the models including the optimal forecaster for in the two-sided conditional calibration tests. A possible explanation for this phenomenon is that for a chosen test function the distribution of the test statistic becomes heavily skewed, making convergence to the asymptotic distribution slow. Another contributing factor, suggested by a referee, could be the instability of the estimate in (2.11) due to high correlation of lagged values of the identification function. As discussed in Giacomini and White (2006), the choice of the test function with too few or too many components will also have direct implications on the power of the tests.

As expected, the numerical results in Table 2 show that the backtesting decisions based on the general conditional calibration tests are more conservative in comparison to the corresponding simple conditional calibration tests, subject to a sensible choice of the test function. This is particularly visible for one-dimensional risk measures (VaR and expectiles) when performing the two-sided tests. The two-sided conditional calibration tests for these two risk measures suggest the importance of the correct specification of the likelihood used in fitting the AR(1)-GARCH(1,1) filter. The entirely parametric methods with misspecified models (here ”n-FP” and ”t-FP”) fail traditional backtests even when testing for simple conditional calibration (with the exception of ). The general conditional tests are able to pick-up the misspecified likelihoods at least in some instances; for example, when forecasting and using the (symmetric) t distribution instead of the true asymmetric underlying model, and similarly for -expectiles with and . The general conditional two-sided calibration tests also detect the differences in the second stage of risk measure forecasting when different methods are applied to filtered series of innovations. For instance, at the highest risk measure levels, the EVT-based methods tend to pass the conditional backtests in contrast to their empirical and in some cases even parametric (correctly specified) counterparts; see panels for and -expectile. This is true even under a misspecified likelihood model in the AR(1)-GARCH(1,1) filter.

We also note that the tests for one-dimensional risk measures appear to have better power properties than the tests for the two-dimensional risk measure, , although a more thorough investigation into finite sample properties of these tests would be necessary to draw more definitive conclusions. It can also be observed that the one-sided tests are less conclusive than their two-sided analogues. This is perhaps not a surprise as it may well happen that a method is not good at predicting the risk measure but gives a correct bound and thus should not be rejected by a one-sided calibration test.

| Method | % Viol. | [eq. (2.19)] | [eq. (2.20)] | [eq. (2.21)] | [eq. (2.22)] | [eq. (2.23)] | [eq. (2.24)] | |||

|---|---|---|---|---|---|---|---|---|---|---|

| n-FP | 0.440 | 9.4 | 0.7496 ( 9 ) | -0.4325 ( 7 ) | 0.440 | 1.0149 ( 9 ) | -1.0526 ( 9 ) | 0.440 | 0.6685 ( 10 ) | -0.8119 ( 9 ) |

| n-FHS | 0.406 | 10.2 | 0.7484 ( 8 ) | -0.4288 ( 9 ) | 0.542 | 1.0006 ( 7 ) | -1.3076 ( 7 ) | 0.450 | 0.6626 ( 5 ) | -0.8361 ( 4 ) |

| n-EVT | 0.406 | 10.2 | 0.7477 ( 7 ) | -0.4304 ( 8 ) | 0.553 | 1.0039 ( 8 ) | -1.3188 ( 5 ) | 0.449 | 0.6655 ( 9 ) | -0.8270 ( 8 ) |

| t-FP | 0.348 | 12.2 | 0.7527 ( 10 ) | -0.3944 ( 10 ) | 0.424 | 1.0200 ( 10 ) | -0.904 ( 10 ) | 0.421 | 0.6645 ( 7 ) | -0.8040 ( 10 ) |

| t-FHS | 0.413 | 10.0 | 0.7473 ( 6 ) | -0.4350 ( 5 ) | 0.550 | 0.9899 ( 5 ) | -1.3055 ( 8 ) | 0.456 | 0.6622 ( 4 ) | -0.8356 ( 5 ) |

| t-EVT | 0.410 | 10.3 | 0.7471 ( 5 ) | -0.4329 ( 6 ) | 0.562 | 0.9944 ( 6 ) | -1.3137 ( 6 ) | 0.457 | 0.6654 ( 8 ) | -0.8289 ( 7 ) |

| st-FP | 0.417 | 9.9 | 0.7442 ( 2 ) | -0.4391 ( 2 ) | 0.559 | 0.9865 ( 4 ) | -1.3378 ( 3 ) | 0.461 | 0.6606 ( 2 ) | -0.8460 ( 3 ) |

| st-FHS | 0.412 | 10.1 | 0.7451 ( 4 ) | -0.4387 ( 3 ) | 0.550 | 0.9808 ( 2 ) | -1.3342 ( 4 ) | 0.455 | 0.6606 ( 3 ) | -0.8488 ( 2 ) |

| st-EVT | 0.410 | 10.2 | 0.7449 ( 3 ) | -0.4363 ( 4 ) | 0.561 | 0.9844 ( 3 ) | -1.3409 ( 2 ) | 0.457 | 0.6642 ( 6 ) | -0.8350 ( 6 ) |

| opt | 0.424 | 9.5 | 0.7431 ( 1 ) | -0.4454 ( 1 ) | 0.565 | 0.9643 ( 1 ) | -1.4257 ( 1 ) | 0.467 | 0.6575 ( 1 ) | -0.8704 ( 1 ) |

| n-FP | 0.586 | 5.9 | 0.9925 ( 8 ) | -0.1055 ( 9 ) | 0.586 | 1.9845 ( 10 ) | -0.4650 ( 10 ) | 0.587 | 0.8177 ( 10 ) | -0.3975 ( 10 ) |

| n-FHS | 0.632 | 5.0 | 0.9910 ( 7 ) | -0.1123 ( 7 ) | 0.801 | 1.8718 ( 7 ) | -0.8939 ( 5 ) | 0.667 | 0.8121 ( 8 ) | -0.4261 ( 7 ) |

| n-EVT | 0.628 | 5.1 | 0.9930 ( 9 ) | -0.1080 ( 8 ) | 0.810 | 1.8756 ( 8 ) | -0.8935 ( 6 ) | 0.670 | 0.8121 ( 7 ) | -0.4259 ( 8 ) |

| t-FP | 0.518 | 7.3 | 1.0106 ( 10 ) | -0.0555 ( 10 ) | 0.631 | 1.9008 ( 9 ) | -0.6419 ( 9 ) | 0.716 | 0.8137 ( 9 ) | -0.4233 ( 9 ) |

| t-FHS | 0.631 | 5.1 | 0.9902 ( 5 ) | -0.1148 ( 5 ) | 0.822 | 1.8428 ( 5 ) | -0.8929 ( 7 ) | 0.675 | 0.8112 ( 5 ) | -0.4292 ( 5 ) |

| t-EVT | 0.630 | 5.1 | 0.9910 ( 6 ) | -0.1128 ( 6 ) | 0.826 | 1.8506 ( 6 ) | -0.8885 ( 8 ) | 0.677 | 0.8117 ( 6 ) | -0.4274 ( 6 ) |

| st-FP | 0.639 | 4.9 | 0.9858 ( 2 ) | -0.1227 ( 2 ) | 0.832 | 1.8313 ( 4 ) | -0.9156 ( 3 ) | 0.688 | 0.8096 ( 3 ) | -0.4356 ( 3 ) |

| st-FHS | 0.632 | 5.0 | 0.9887 ( 3 ) | -0.1161 ( 3 ) | 0.821 | 1.8164 ( 2 ) | -0.9174 ( 2 ) | 0.675 | 0.8096 ( 2 ) | -0.4357 ( 2 ) |

| st-EVT | 0.630 | 5.1 | 0.9890 ( 4 ) | -0.1154 ( 4 ) | 0.825 | 1.8221 ( 3 ) | -0.9153 ( 4 ) | 0.677 | 0.8100 ( 4 ) | -0.4341 ( 4 ) |

| opt | 0.649 | 4.7 | 0.9834 ( 1 ) | -0.1267 ( 1 ) | 0.837 | 1.7481 ( 1 ) | -1.0189 ( 1 ) | 0.696 | 0.8070 ( 1 ) | -0.4503 ( 1 ) |

| n-FP | 0.859 | 2.5 | 1.8649 ( 10 ) | 0.7041 ( 10 ) | 0.859 | 8.4605 ( 10 ) | 2.1097 ( 10 ) | 0.863 | 1.1638 ( 10 ) | 0.3969 ( 10 ) |

| n-FHS | 1.193 | 1.1 | 1.7398 ( 8 ) | 0.4992 ( 7 ) | 1.492 | 6.1819 ( 7 ) | 0.0652 ( 6 ) | 1.218 | 1.1268 ( 8 ) | 0.2453 ( 8 ) |

| n-EVT | 1.189 | 1.0 | 1.7115 ( 5 ) | 0.4801 ( 5 ) | 1.480 | 6.1153 ( 5 ) | 0.0651 ( 5 ) | 1.243 | 1.1240 ( 7 ) | 0.2381 ( 7 ) |

| t-FP | 0.948 | 1.8 | 1.7605 ( 9 ) | 0.5679 ( 9 ) | 1.186 | 6.0364 ( 3 ) | 0.2244 ( 9 ) | 1.781 | 1.1472 ( 9 ) | 0.2847 ( 9 ) |

| t-FHS | 1.207 | 1.1 | 1.7392 ( 7 ) | 0.5025 ( 8 ) | 1.629 | 6.7232 ( 9 ) | 0.0771 ( 8 ) | 1.246 | 1.1205 ( 5 ) | 0.2334 ( 6 ) |

| t-EVT | 1.203 | 1.0 | 1.7064 ( 4 ) | 0.4755 ( 4 ) | 1.546 | 6.1387 ( 6 ) | 0.0658 ( 7 ) | 1.266 | 1.1208 ( 6 ) | 0.2328 ( 5 ) |

| st-FP | 1.214 | 0.9 | 1.6987 ( 3 ) | 0.4734 ( 3 ) | 1.583 | 5.9688 ( 2 ) | -0.0491 ( 2 ) | 1.287 | 1.1156 ( 2 ) | 0.2195 ( 2 ) |

| st-FHS | 1.209 | 1.1 | 1.7339 ( 6 ) | 0.4991 ( 6 ) | 1.614 | 6.4895 ( 8 ) | 0.0236 ( 3 ) | 1.245 | 1.1161 ( 3 ) | 0.2221 ( 4 ) |

| st-EVT | 1.202 | 0.9 | 1.6929 ( 2 ) | 0.4651 ( 2 ) | 1.543 | 6.0779 ( 4 ) | 0.0306 ( 4 ) | 1.265 | 1.1164 ( 4 ) | 0.2215 ( 3 ) |

| opt | 1.227 | 0.9 | 1.6614 ( 1 ) | 0.4369 ( 1 ) | 1.574 | 4.9567 ( 1 ) | -0.3749 ( 1 ) | 1.297 | 1.1066 ( 1 ) | 0.1887 ( 1 ) |

| -expectile | ||||||||||||

| two-sided | one-sided | two-sided | one-sided | two-sided | one-sided | |||||||

| Method | simple | general | simple | general | simple | general | simple | general | simple | general | simple | general |

| n-FP | 0.146 | 0.018 | 0.927 | 1.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| n-FHS | 0.576 | 0.058 | 0.288 | 0.863 | 0.887 | 0.048 | 0.443 | 0.193 | 0.881 | 0.184 | 0.712 | 0.744 |

| n-EVT | 0.608 | 0.056 | 0.304 | 0.911 | 0.684 | 0.042 | 0.658 | 0.364 | 0.754 | 0.672 | 1.000 | 0.629 |

| t-FP | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.086 | 0.006 | 0.041 | 0.011 |

| t-FHS | 0.962 | 0.006 | 0.481 | 1.000 | 0.728 | 0.030 | 0.636 | 0.330 | 0.936 | 0.512 | 0.960 | 0.256 |

| t-EVT | 0.514 | 0.011 | 0.257 | 0.772 | 0.360 | 0.023 | 0.820 | 0.542 | 0.880 | 0.475 | 0.815 | 0.008 |

| st-FP | 0.740 | 0.090 | 0.630 | 1.000 | 0.429 | 0.084 | 0.786 | 0.546 | 0.569 | 0.824 | 1.000 | 0.991 |

| st-FHS | 0.851 | 0.091 | 0.425 | 1.000 | 0.708 | 0.123 | 0.646 | 0.400 | 0.909 | 0.796 | 0.956 | 0.744 |

| st-EVT | 0.674 | 0.066 | 0.337 | 1.000 | 0.377 | 0.098 | 0.812 | 0.596 | 0.935 | 0.706 | 0.851 | 0.032 |

| opt | 0.228 | 0.294 | 0.886 | 1.000 | 0.234 | 0.458 | 0.883 | 0.850 | 0.401 | 0.337 | 0.732 | 1.000 |

| n-FP | 0.006 | 0.004 | 0.003 | 0.009 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| n-FHS | 0.948 | 0.042 | 0.526 | 1.000 | 0.702 | 0.067 | 0.351 | 0.158 | 0.912 | 0.349 | 0.997 | 0.609 |

| n-EVT | 0.797 | 0.075 | 0.398 | 1.000 | 0.868 | 0.062 | 0.434 | 0.208 | 0.720 | 0.549 | 1.000 | 0.762 |

| t-FP | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 | 1.000 |

| t-FHS | 0.700 | 0.053 | 0.350 | 1.000 | 0.793 | 0.027 | 0.603 | 0.325 | 0.951 | 0.492 | 0.864 | 0.368 |

| t-EVT | 0.654 | 0.106 | 0.327 | 0.981 | 0.713 | 0.033 | 0.643 | 0.363 | 0.699 | 0.771 | 1.000 | 0.845 |

| st-FP | 0.794 | 0.261 | 0.603 | 1.000 | 0.568 | 0.066 | 0.716 | 0.467 | 0.655 | 0.898 | 0.907 | 0.249 |

| st-FHS | 0.897 | 0.111 | 0.449 | 1.000 | 0.729 | 0.073 | 0.635 | 0.393 | 0.908 | 0.690 | 0.904 | 0.875 |

| st-EVT | 0.797 | 0.180 | 0.398 | 1.000 | 0.643 | 0.077 | 0.679 | 0.435 | 0.599 | 0.968 | 1.000 | 1.000 |

| opt | 0.284 | 0.552 | 0.858 | 1.000 | 0.315 | 0.523 | 0.843 | 0.798 | 0.311 | 0.624 | 0.263 | 0.194 |

| n-FP | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| n-FHS | 0.420 | 0.007 | 0.210 | 0.630 | 0.377 | 0.045 | 0.188 | 0.100 | 0.653 | 0.231 | 0.549 | 0.538 |

| n-EVT | 1.000 | 0.186 | 0.500 | 1.000 | 0.300 | 0.080 | 0.150 | 0.085 | 0.886 | 0.226 | 0.804 | 0.577 |

| t-FP | 0.000 | 0.000 | 0.000 | 0.000 | 0.003 | 0.010 | 0.002 | 0.001 | 0.000 | 0.000 | 1.000 | 1.000 |

| t-FHS | 0.679 | 0.029 | 0.339 | 1.000 | 0.783 | 0.013 | 0.391 | 0.212 | 0.697 | 0.717 | 1.000 | 1.000 |

| t-EVT | 0.888 | 0.140 | 0.444 | 1.000 | 0.509 | 0.067 | 0.254 | 0.145 | 0.995 | 0.498 | 0.807 | 1.000 |

| st-FP | 0.454 | 0.221 | 0.773 | 1.000 | 0.601 | 0.048 | 0.301 | 0.169 | 0.695 | 0.419 | 0.597 | 0.511 |

| st-FHS | 0.584 | 0.018 | 0.292 | 0.876 | 0.826 | 0.026 | 0.413 | 0.238 | 0.843 | 0.758 | 1.000 | 1.000 |

| st-EVT | 0.554 | 0.270 | 0.723 | 1.000 | 0.552 | 0.087 | 0.276 | 0.162 | 0.962 | 0.564 | 0.868 | 1.000 |

| opt | 0.364 | 0.576 | 0.818 | 1.000 | 0.825 | 0.491 | 0.588 | 0.513 | 0.131 | 0.571 | 0.073 | 0.101 |

In addition to risk measure average forecasts, Table 1 also reports the average scores along with the corresponding method rankings using two different (consistent) scoring functions for each of the three considered risk measures. As the scoring functions we use require risk measure forecasts to be positive, we set the scores across all methods to zero in those few cases where forecasts are negative. Note that in the case of , only the forecasts for are restricted to be positive.

The method rankings based on the average scores appear to be reasonable, and suggest some more general conclusions with respect to method selection on the basis of forecasting accuracy. Similar to the results of traditional backtesting, the numerical values in Table 1 provide further support to the observation that the choice of the likelihood model in fitting the AR(1)-GARCH(1,1) filter has an appreciable influence on the accuracy of forecasts, perhaps more than previously thought in the context of using the quasi-maximum-likelihood methods. Within each likelihood model, at lower levels for risk measure, fully parametric and FHS approaches tend to demonstrate better predictive performance, whereas at higher levels EVT-based methods seem to have an advantage, in particular, in the case of VaR. When the likelihood model is misspecified in fitting the AR(1)-GARCH(1,1) filter, the non-parametric methods such as FHS and semi-parametric methods such as EVT-based estimation allow for greater flexibility to diminish the effects of model misspecification than the fully parametric approaches do. While in many cases, rankings obtained from each pair of consistent scoring functions coincide, there also exist some discrepancies. This is not a surprise in the presence of misspecified models and estimation uncertainty as already pointed out by Patton (2014). For models for which the mean score is finite, the weak law of large numbers suggests convergence of the sample average (score) to the true mean (score) as the out-of-sample size tends to infinity. However, the convergence can be fairly slow. We found that in our simulation study, the out-of-sample size of at least 1000 data points is necessary to achieve some stability in rankings. Hence, in finite sample situations, one has to be aware of the effects of sampling variability on the final rankings of the forecasting methods. Appendix D discusses results of a study where only 250 verifying observations were considered to perform backtesting. In small samples, results of both traditional and comparative backtesting may be greatly distorted by unrepresentative samples even when the underlying data generating process is stationary.

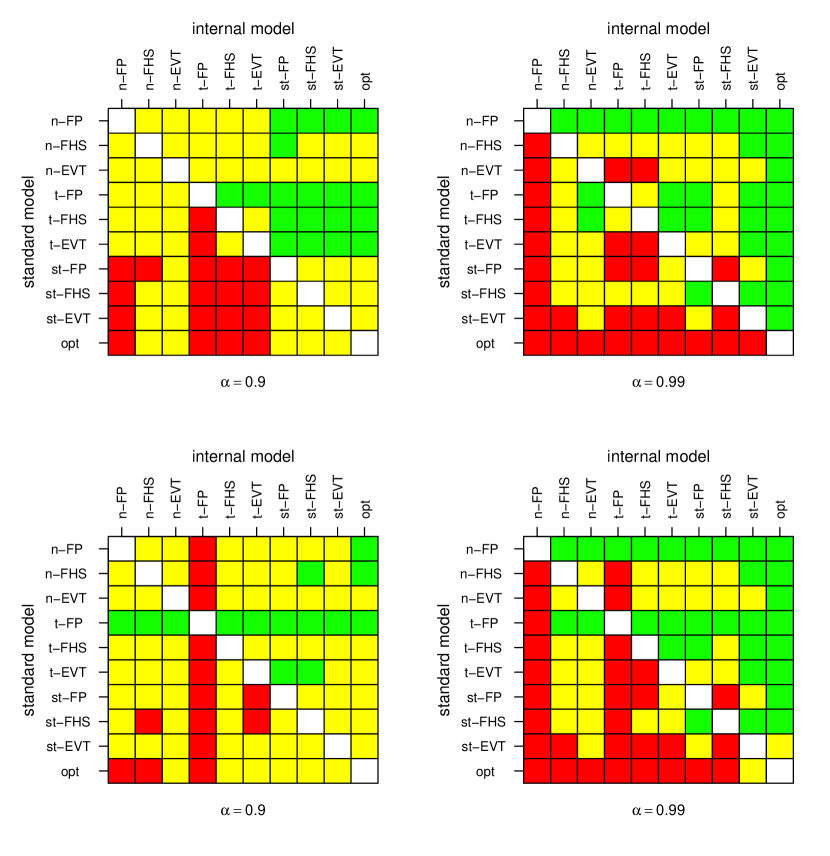

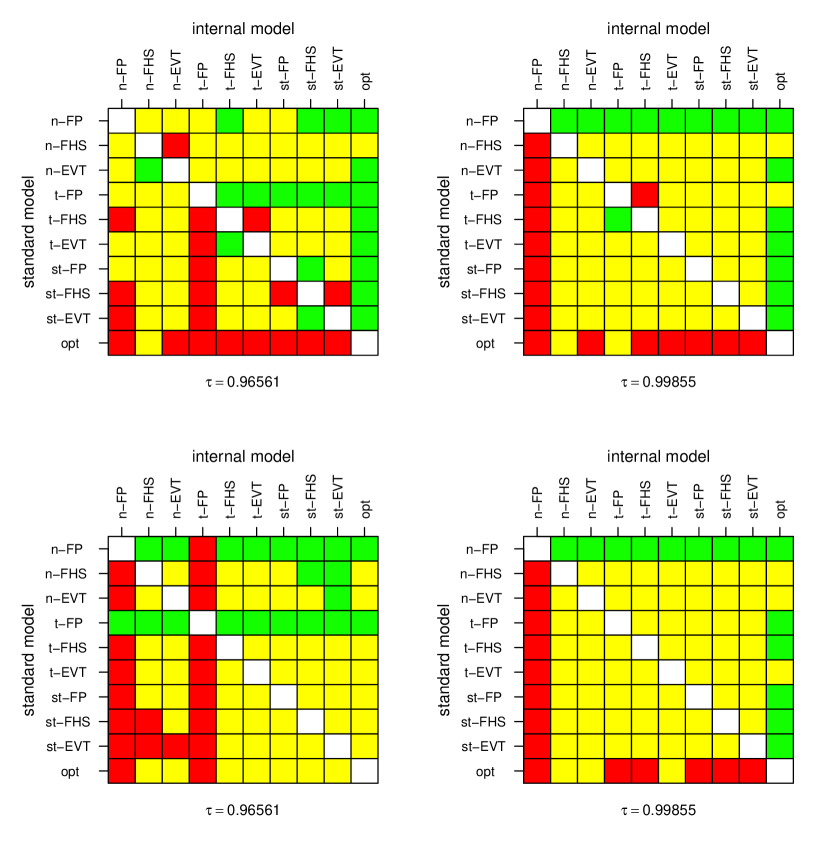

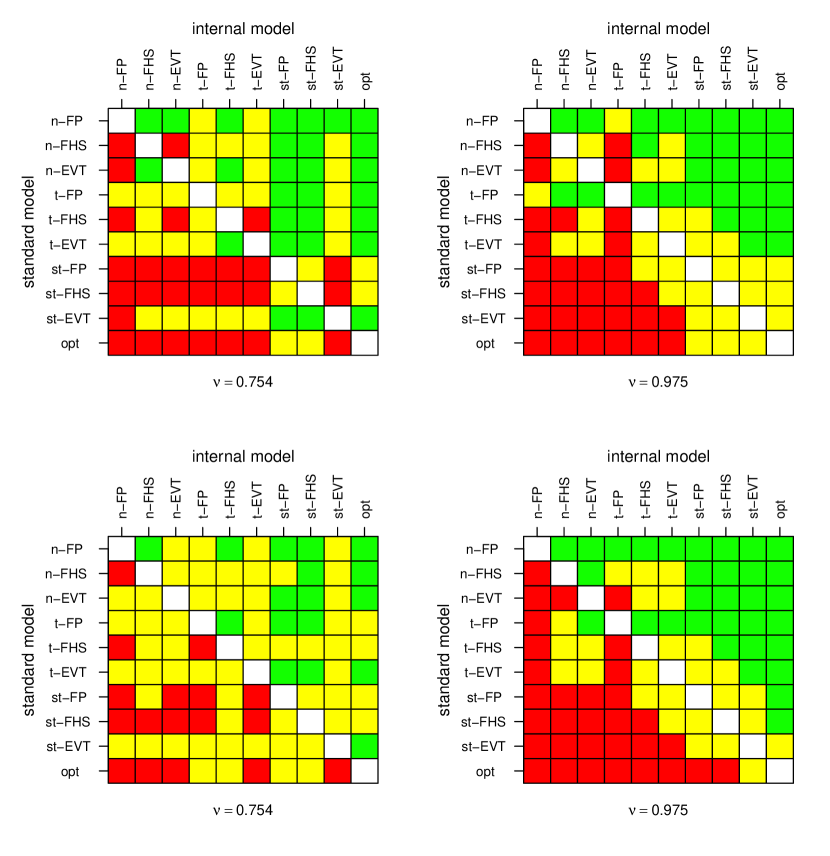

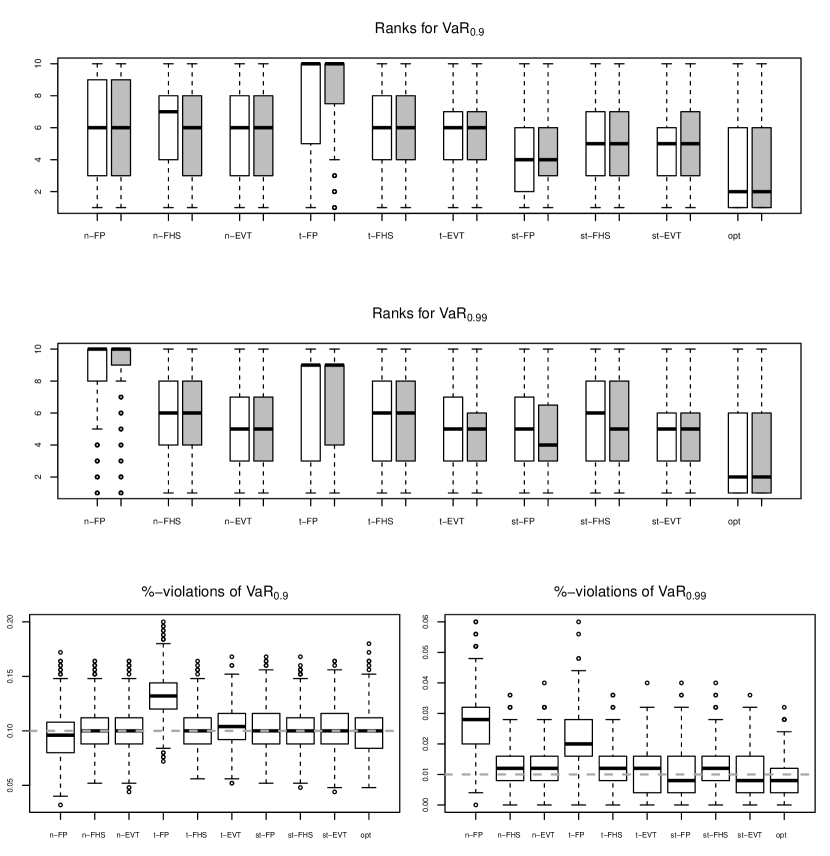

Finally, Figures 1 - 3 display the traffic light matrices for the three risk measures and two forms of consistent scoring functions for each. These plots complement the method rankings on the basis of just the average scores with the tests of predictive ability at the test level . Along the vertical axis we consider hypothetical ”standard” models with the investigated ”internal” models displayed along the horizontal axis. The red and green cells correspond to situations in which the comparative backtest is failed or passed, while yellow cells indicate cases where no conclusive evidence is available to pass or fail the comparative backtest. The rows in each figure correspond to different scoring functions used to compare the methods.

Inconclusive traffic light matrices can result if all methods are performing reasonably well, or, if the chosen scoring function has poor discrimination ability. In the case of VaR, as the discrimination ability of both chosen scoring functions seems good at level , it is likely that at several models show a reasonable predictive ability. This is in line with the largely inconclusive traditional backtests at level . At , the scoring function in (2.19) is better at identifying models with the correctly specified likelihood than the scoring function in (2.20), for which with just a few exceptions only the ”t-FP” method fails the comparative backtests as an internal method against all the other possible standard methods. At , the two scoring functions result in a good agreement with ”n-FP” being the worst forecaster (i.e., failing the comparative backtests against all the other methods), the optimal method passing comparative backtests against all other methods (the exception is ”st-EVT” under the scoring function in (2.20)).

The situation is less clear for the -expectile. At level , the ”n-FP” method fails the comparative backtest against most of the other methods under both scoring functions; the use of the scoring function in (2.22) suggests failing the ”t-FP” method as well. The ”st-EVT” method would pass the comparative backtest against the models with the normal likelihood and ”t-FP”. At level , both scoring functions do not discriminate the methods much except for flagging the optimal forecaster as better than most other methods and failing the ”n-FP” method. Expectiles have been used much less as a risk measure and it may be possible that the present methods are indeed suboptimal for expectile prediction at high levels. Again, this is in line with the results of the traditional backtests, in particular, the conditional two-sided tests.

For , the large number of conclusive comparative backtesting results indicates that we can discriminate well between methods, and, as in the case of VaR it appears less important which method to use at a lower level than at a higher level. In particular, we once again see that the methods with the correctly specified likelihood show superior predictive performance. According to the scoring function in (2.23), the ”st-EVT” method fails the comparative backtest against its parametric and non-parametric counterparts ”st-FP” and ”st-FHS” at lower levels of . No definitive conclusions with respect to these models can be drawn at .

3.3 Data analysis

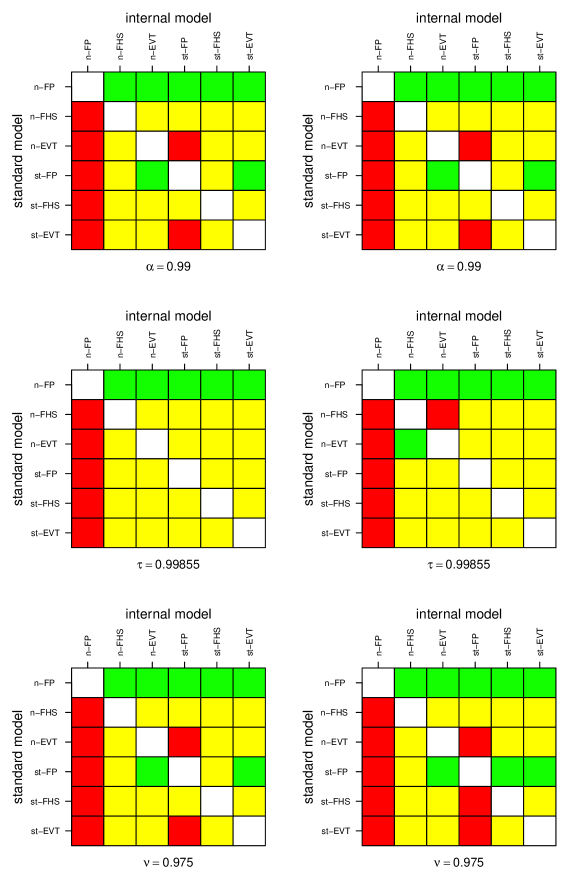

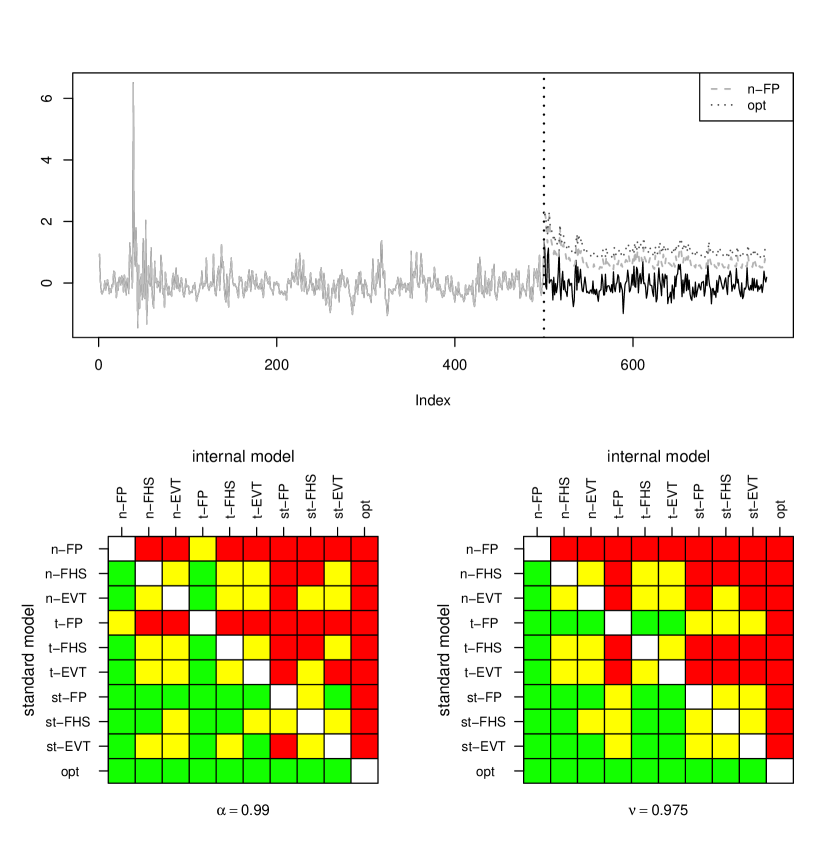

We have fitted an AR(1)-GARCH(1,1) model to the negated log-returns of the NASDAQ Composite index using a moving estimation window of 500 data points. The time series we consider is from Feb. 8, 1971 until May 18, 2016, which gives us an out-of-sample size 10,920 to perform backtesting. Table 3 summarizes results of traditional and comparative backtesting for six forecasting methods (refer to Section 3.2 for details on these methods) and, as before, for the three risk measures (VaR, expectile and the (VaR, ES) pair) at their standard Basel levels.

In the case of , the traditional backtests based on the two-sided simple conditional calibration tests are passed only under the n-EVT and st-EVT methods. So, here, the choice of the likelihood function in fitting the AR(1)-GARCH(1,1) filter seems to have a lower impact than the choice of the method at the second stage of forecasting applied to the fitted residuals. At this relatively high risk measure level, the EVT-based methods outperform their other competitors based on both the traditional backtests and the average scores. It should also be noted that the two scoring functions have lead to the same rankings of the forecasting procedures. The fully parametric methods (n-FP and st-FP) show the worst performance in terms of their predictive ability. n-FP falls into the red region against all other methods, whereas st-FP fails against the EVT methods and cannot win against the FHS methods; see the traffic light matrices in Figure 4 (top row).

On the other hand, for the 0.99855-expectile, the tests of simple conditional calibration are rejected (at 5% level) for all the methods that use the normal likelihood. Those methods that use the skewed-t likelihood also tend to rank higher; although, in terms of significance, most methods fall into the yellow region (apart from the n-FP method). The ranking of forecasts is different for the two scoring functions used. The 0-homogeneous choice at (2.22) clearly ranks the methods using the normal likelihood lower than those using the skewed-t likelihood in agreement with the results of the simple conditional calibration tests which is an argument in favour of using (2.22) rather than (2.21).

For both and 0.99855-expectile, the conditional calibration tests with the test functions as in the simulation study, lead to the failure of the corresponding traditional backtest; see Table 3 for the expectile. This may seem overly-conservative for practical purposes, and suggests either re-examining suitability of the GARCH-type filter for these data, or the use of a more appropriate test function. For , we performed the conditional calibration tests also with the test function (see Example 1) and the resulting p-values are reported in Table 3. They lead to conclusions similar to those based on the simple conditional calibration tests. This example underlines the importance of further studies on appropriate choices of test functions.

The results for with suggest better performance when a more flexible model such as the skewed-t is used to fit the AR(1)-GARCH(1,1) filter, although the use of EVT-based methods has a potential to compensate for likelihood mis-specifications. Again, fully parametric methods (n-FP and st-FP) fall into the red region in the comparative backtests against most of the other more flexible alternatives; see bottom panels in Table 3 and Figure 4. The outcomes show one interesting aspect which is not in contradiction with the theory but may be puzzling and merit further investigation in future studies: The conditional calibration test rejects all methods using a normal likelihood but the scoring functions rank the n-EVT method as the best or second best performing method. It seems that the test function used in the conditional calibration test is sensitive to the likelihood function used in fitting the AR(1)-GARCH(1,1) filter whereas the scoring functions are more sensitive to the method at the second stage giving preference to the EVT methods.

| Method | % Viol. | simple CCT | general CCT | [eq. (2.19)] | [eq. (2.20)] | |

|---|---|---|---|---|---|---|

| n-FP | 2.363 | 2.3 | 0.000 | 0.000 | 3.8497 ( 6 ) | 1.3017 ( 6 ) |

| n-FHS | 2.758 | 1.3 | 0.017 | 0.028 | 3.5842 ( 3 ) | 1.1604 ( 3 ) |

| n-EVT | 2.774 | 1.2 | 0.112 | 0.152 | 3.5675 ( 2 ) | 1.1550 ( 2 ) |

| st-FP | 2.739 | 1.3 | 0.004 | 0.012 | 3.5976 ( 5 ) | 1.1669 ( 5 ) |

| st-FHS | 2.785 | 1.2 | 0.046 | 0.108 | 3.5904 ( 4 ) | 1.1609 ( 4 ) |

| st-EVT | 2.811 | 1.1 | 0.181 | 0.290 | 3.5654 ( 1 ) | 1.1517 ( 1 ) |

| simple CCT | general CCT | [eq. (2.21)] | [eq. (2.22)] | |||

| n-FP | 2.363 | 0.000 | 0.000 | 25.9030 ( 6 ) | 0.9660 ( 6 ) | |

| n-FHS | 2.986 | 0.049 | 0.002 | 19.7333 ( 2 ) | 0.2933 ( 4 ) | |

| n-EVT | 2.966 | 0.023 | 0.001 | 19.8196 ( 5 ) | 0.3084 ( 5 ) | |

| st-FP | 3.041 | 0.163 | 0.011 | 19.8159 ( 4 ) | 0.2509 ( 1 ) | |

| st-FHS | 3.078 | 0.227 | 0.011 | 19.7533 ( 3 ) | 0.2589 ( 2 ) | |

| st-EVT | 3.037 | 0.112 | 0.006 | 19.6963 ( 1 ) | 0.2687 ( 3 ) | |

| simple CCT | general CCT | [eq. (2.23)] | [eq. (2.24)] | |||

| n-FP | 2.375 | 0.000 | 0.000 | 1.7020 ( 6 ) | 1.0492 ( 6 ) | |

| n-FHS | 2.777 | 0.022 | 0.035 | 1.6587 ( 4 ) | 0.9637 ( 4 ) | |

| n-EVT | 2.813 | 0.261 | 0.015 | 1.6560 ( 1 ) | 0.9607 ( 2 ) | |

| st-FP | 2.810 | 0.001 | 0.248 | 1.6622 ( 5 ) | 0.9691 ( 5 ) | |

| st-FHS | 2.816 | 0.139 | 0.067 | 1.6582 ( 3 ) | 0.9617 ( 3 ) | |

| st-EVT | 2.857 | 0.327 | 0.117 | 1.6563 ( 2 ) | 0.9597 ( 1 ) | |

4 Discussion